Crypto World

Private credit firms prepare for bank run-type panic by gating investor withdrawals

Private credit giant Apollo Global Management capped withdrawals on Monday. As a group, retail investors were able to take out just 45% of the money they’d originally asked to withdraw.

Escalating a well-publicized crisis in private equity and credit, Apollo is the sixth major asset manager this year to tell investors they need to slow down their withdrawal requests.

Apollo Debt Solutions, a non-publicly traded credit company with a net asset value of about $15 billion, received redemption requests exceeding 11% of its outstanding shares in the first quarter.

The fund enforced a 5% quarterly cap and returned roughly $730 million of the more than $1.5 billion in requests it received. Redeeming investors received less than half of the full disbursements they requested.

Private credit peers Blackstone and Blue Owl have also been restructuring their withdrawal policies under pressure. Apollo held its 5% withdrawal limit.

Apollo joins Blackstone, BlackRock, Blue Owl Capital, Morgan Stanley, and Cliffwater in gating investor withdrawals this quarter.

The industry sold these funds to individuals as a path to “democratization” of institutional-grade yields.

In fact, private equity (PE) and private credit companies merely democratized purchases by regular people who often didn’t understand that PE managers can choose the valuations of their assets with far less oversight and regulatory obligations than public fund managers.

Because the valuations of these assets occur privately, there’s no real-time price-seeking mechanism to determine the proper valuation of these assets.

As such, PE managers typically mark-up their assets consistently, quarter after quarter, until they suddenly plunge in value during a crisis or liquidity crunch, such as the current Iran war or AI-induced layoffs.

Because it’s impossible to sell out of these credit and equity instruments on secondary exchanges, investors may only request redemptions quarterly.

However, funds typically cap total withdrawals at 5% of their net asset value per quarter. If more people want out than the cap allows, everyone gets a haircut on their redemption request.

The problem, therefore, is structural. The underlying loans are illiquid and artificially marked-up. The quarterly redemption window created an illusion of liquidity for a small number of withdrawal requests that doesn’t match the immense size of the assets.

This is seen particularly during any type of bank run-type scenario where withdrawal requests arrive en masse.

About 80% of traditional private credit investors are institutions, according to JP Morgan, yet many retail investors have joined them in recent years.

Main Street investors, who piled in chasing yields of 8% to 10%, have far less patience.

PE giant Blue Owl, for example, drew roughly 40% of its over $300 billion in assets from individuals, according to Fortune.

Blackstone’s Private Credit Fund recorded a record 7.9% redemption request totaling nearly $4 billion. Blackstone actually raised its quarterly cap to 7% and injected $400 million of its own capital to help calm some of that panic.

Equally alarming, BlackRock’s $26 billion HPS Corporate Lending Fund received $1.2 billion in withdrawal requests, or 9.3% of assets, and paid out $620 million.

Morgan Stanley’s North Haven Private Income Fund received requests for over 10% of shares and capped payouts at 5%.

Cliffwater’s $33 billion flagship fund saw the worst of it. Investors demanded 14% of shares back. The firm slashed that in half to a 7% limit.

Blue Owl nearly went off the deep end. In February, the firm permanently halted quarterly redemptions from its retail-focused Blue Owl Capital Corp II.

Read more: Tether: Ten years, 100,000,000,000 USDT, and still no audit

The wave of redemptions has many causes, not least of which is a sudden realization that PE managers have broad discretion to mark-to-market values of assets with little to no secondary market transactions forcing them to properly or conservatively value those holdings.

Moreover, there are fears that AI will trigger sudden job losses this year, creating a bank run-type scenario by fixed income investors.

The escalating war in Iran is also not helping.

Private credit funds loaded up on loans to mid-sized software firms during the boom years, as well, which are now at risk due to AI. Justifiably, investors now question how good those loans are.

The private credit default rate reached 5.8% through January 2026, according to Fitch. That’s the highest since the index launched.

UBS has warned that severe AI disruption could push defaults to 13%.

Wall Street spent years pitching private credit as a better way to optimize yield. Now investors are feeling the pinch of illiquidity and mark-to-market valuations.

You can always check in, but you can’t always check out.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Key takeaways:

-

Investors dumped gold and bonds for cash as war-driven oil spikes and inflation forced a defensive market stance.

-

Rising yields and a 20% rate hike chance signal a tight outlook, leaving Bitcoin vulnerable amid soaring US debt.

Bitcoin (BTC) retested the $67,500 support level on Monday, a move that coincided with gold prices suffering their sharpest correction in over 50 years. Fears of a prolonged war in Iran and the inflationary impact of oil prices holding above $85 pushed investors to cut risk.

US Treasuries also faced a sell-off during this period, suggesting that traders aggressively built cash positions. Yields on the US 5-year Treasury jumped to 4.10%, marking a nine-month high as traders demanded better returns. With the S&P 500 hitting its lowest point in over six months on Monday, evidence suggested a broad rush to liquidity.

Cash is king amid economic uncertainty, while Bitcoin risks further downside

Investors appeared to be raising cash either to cover recent losses or to brace for further price drops across risk markets.

The ongoing war in Iran pushed oil prices past $90, creating inflationary pressure. The Wall Street Journal reported that the US planned to deploy roughly 3,000 troops to the Middle East to counter Iran’s influence over the Strait of Hormuz. Part of the decline in gold prices was likely linked to fading expectations for US monetary policy easing in the near term.

Bond market futures showed that the implied probability of the Federal Open Market Committee (FOMC) hiking interest rates by July surged to 20.5%, up from 0% just one week prior. Investors anticipated a cooling job market as high interest rates continued to reduce corporate expansion incentives.

Tech stocks fall, inflation hurts consumers

US legislators debated an additional $200 billion in funding to support the war in Iran, according to The Washington Post. Kevin Hassett, director of the US National Economic Council, stated that $12 billion had already been spent. Lawmakers did not authorize the war, and Congress showed growing unease with the military strategy, according to AP.

Meanwhile, the US national debt soared past $39 trillion, which further pushed consumers toward a cost-of-living crisis. Fear of excessive speculative investment in the artificial intelligence sector emerged after Reuters reported that ChatGPT maker OpenAI offered private-equity firms a guaranteed minimum return of 17.5% while the company remained largely unprofitable.

Some of the world’s largest tech companies faced losses of 10% or more over the past six weeks, including Google (GOOG US), Meta (META US), and IBM (IBM US). Thus, regardless of the sharp correction in gold prices, traders increasingly feared recession risks or a surge in inflation above the 4% fixed income returns.

Related: Bitcoin holders shift from panic to cash-buffer discipline as volatility deepens

The combination of declining stock prices and persistent inflationary pressure explained why investors aggressively sought the safety of cash positions.

Regardless of favorable Bitcoin onchain metrics, broader macroeconomic conditions remained unfavorable for sustainable bullish momentum. The decline in gold prices while investors offloaded US Treasuries served as a sign of risk aversion. The odds of a $66,000 retest remain a serious threat, at least until inflation and war expenses hold US monetary policy tight for a longer period.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

Circle stock fell 19% after the latest Senate draft of the Clarity Act included restrictions on stablecoin yield.

Crypto markets dipped slightly on Tuesday as geopolitical uncertainty persisted and investors considered the implications of the U.S. Senate’s revised draft of the crypto market structure bill, or Clarity Act.

Bitcoin (BTC) is trading at around $70,000, down less than 1% over the past 24 hours. ETH and SOL fell 0.6% to $2,135 and $90, respectively. Meanwhile, Ripple (XRP) slipped 3%.

Total crypto market capitalization is down 0.2% to $2.48 trillion, according to Coingecko.

Bitcoin surged above $71,000 on Monday after President Donald Trump announced a five-day postponement of planned strikes on Iran’s power infrastructure, citing what he called productive talks with Tehran. However, Iran’s Fars news agency denied that any talks had taken place.

Clarity Act Draft Rattles Stablecoin Stocks

Circle stock plunged 19%, and Coinbase dropped 8% after details emerged from the latest draft of the Clarity Act, which would restrict stablecoin yield offerings. The revised language, crafted by Senators Angela Alsobrooks and Thom Tillis, would ban yield payments for simply holding a stablecoin while permitting narrowly defined activity-based rewards tied to transactions or platform usage.

Crypto industry insiders got their first look at the revised text during a closed-door review on Capitol Hill on Monday, according to Coindesk.

Big Movers

Nearly all of the Top 100 digital assets posted minor losses over the last 24 hours.

Today’s top gainers are Bittensor (TAO) and World Liberty Financial (WLFI), which surged 10%.

Monero (XMR) and Polkadot (DOT) are the biggest losers, down 5% and 4%, respectively.

Around 79,000 leveraged traders were liquidated for $153 million in the past 24 hours, according to CoinGlass. Bitcoin accounted for $46 million, while ETH made up $33 million.

Bitcoin exchange-traded funds (ETFs) recorded inflows of $163.5 million on Tuesday, snapping a three-day losing streak, according to SoSoValue.

The Crypto Fear & Greed Index sits at 11, indicating ‘Extreme Fear’, and has spent the bulk of March below 20, a prolonged stretch of pessimism not seen since the depths of the 2022 bear market.

Active, actively managed crypto exchange-traded products are emerging as the next frontier for institutional exposure, as the market moves beyond passive price-tracking funds. 21shares, a leading issuer in the space, argues that the asset class’s nascency makes it particularly amenable to portfolio-level management.

In an exclusive conversation, Duncan Moir, president of 21shares, outlined a strategy that blends bottom-up research on individual assets with quantitative and discretionary top-down risk controls to steer portfolios. The firm has been expanding its portfolio-management and trading ranks to support more sophisticated products, he said, reflecting a broader shift in the crypto ETP space toward active strategies.

We’ve had to hire and build out the team with people who have different trading and portfolio management expertise, but now we have a solid team and we think we’ll be able to deliver strong actively managed products.

Industry data underscore the trend: active exchange-traded products worldwide held nearly $1.8 trillion in assets by the end of 2025, according to data compiled by Morningstar and Goldman Sachs Asset Management.

Moir also pointed to the strategic role of FalconX, which acquired 21shares in October, as a force-multiplier for product development, particularly as the firm pursues more complex offerings.

Regional demand for crypto ETPs and ETFs remains uneven. In the United States, investor interest remains skewed toward the largest-cap crypto assets, while in Europe institutions are showing appetite for newer assets and the application layer beyond base-layer tokens. This divergence reflects a mature European investor base already holding BTC and ETH and looking to broaden crypto allocations with yield-oriented or theme-driven products.

In this environment, 21shares has rolled out Europe-listed ETP linked to Strategy’s preferred stock (STRC), offering exposure to a Bitcoin-focused capital strategy with a high-yield profile. The product has attracted strong early interest across regions as investors seek straightforward exposure to yield via traditional brokers.

Crypto ETPs evolve beyond passive exposure

As the crypto ETP and ETF market matures, issuers are moving beyond simple price tracking, with more complex structures emerging across the US and Europe.

One area gaining traction is staking, a process that allows investors to earn yield by locking up crypto assets to help secure blockchain networks. In October, Grayscale introduced staking across its ETPs, making its Ether funds among the first US-listed spot crypto ETFs to offer staking rewards while extending the feature to its Solana trust pending ETP approval.

In March, asset manager BlackRock launched a Nasdaq-listed Ethereum product that incorporates staking, combining spot Ether exposure with yield generation. The fund recorded $15.5 million in trading volume on its first day.

As new exchange-traded products come to market, Moir said 21shares evaluates potential launches based on three factors: internal research, client demand, and broader market trends, with its research team identifying early opportunities and institutional feedback helping gauge interest. This triad helps determine whether a niche, single-asset product or a broader thematic offering best fits conviction and demand.

Among examples of the approach in practice is 21shares’ Bitcoin-and-gold ETP. Cross-listed in London and live for several years, Moir notes that the product has delivered some of the strongest risk-adjusted returns among European ETPs, illustrating the appeal of balanced exposure across flagship crypto and traditional stores of value.

From a portfolio perspective, the combination “just makes total sense,” he added, citing diversification benefits across Bitcoin and gold.

What’s next for crypto ETPs and investors

The evolving landscape suggests investors can expect more nuanced structures, including yields and staking rewards embedded in traditional brokerage-accessible formats. The FalconX deal accelerates product development by providing deeper execution capabilities and liquidity to support a broader range of strategies. As institutions in Europe deepen their crypto allocations and U.S. issuers explore tiered yield and application-layer exposures, the market will likely see a steady cadence of launches that blend traditional finance rails with crypto’s distinct yields and risk profiles.

Looking ahead, the conversation centers on how regulators will shape access to staking-based products, how quickly large-cap and next-generation assets receive broad market validation, and how issuers balance risk controls with the demand for yield-driven strategies. For investors, the key watchpoints are whether new products deliver clear, repeatable performance across cycles, and how cross-border listings and collaborations—such as 21shares’ integration with FalconX—affect liquidity, pricing, and transparency in the evolving crypto ETP ecosystem.

Readers should watch regulatory clarity in major markets and the pace of institutional adoption as 21shares and peers press forward with more sophisticated, yield-focused offerings that aim to turn crypto exposure into scalable, traditionally accessible investment strategies.

Key Takeaways

- Micron shares declined approximately 15% across four consecutive trading sessions following exceptional Q2 fiscal 2026 results

- Quarterly revenue reached $23.86 billion, representing nearly a 200% surge from the prior year’s $8.05 billion

- According to CEO Sanjay Mehrotra, current production capacity meets only 50% to 66% of major customer demand

- Competitor SK Hynix announced plans for an $8 billion EUV equipment investment and potential $10 billion U.S. stock listing — intensifying competitive dynamics

- Leading Wall Street firms including Bank of America, Morgan Stanley, and JPMorgan elevated their price projections following the earnings announcement

Micron delivered exceptional quarterly results last week. Wall Street’s reaction? A double-digit decline.

Following the release of Q2 fiscal 2026 earnings on Wednesday, Micron shares have experienced consecutive daily losses spanning four trading sessions. The negative price action has left many observers perplexed, particularly considering the impressive financial metrics.

Quarterly revenue totaled $23.86 billion — representing approximately a threefold increase from the $8.05 billion Micron generated during the comparable quarter last year. Management also projected gross margin percentages hovering around 80% for the upcoming quarter.

Despite the recent downturn, Micron shares have surged more than 300% over the trailing twelve months. The memory chip manufacturer stands as the sole technology company among America’s top 10 market leaders posting year-to-date gains, while Oracle and Microsoft have both retreated over 20%.

Citi’s semiconductor analyst Atif Malik attributed the selloff primarily to investor profit-taking. “Higher FY27 capex and peak gross margin concerns (81% > Nvidia’s 75%) likely induced some profit taking after a strong stock run into the print,” he noted.

Production Capacity Lags Behind Customer Requirements

CEO Sanjay Mehrotra spoke openly about current supply constraints during an interview with CNBC’s Squawk on the Street on Thursday.

“Memory today is very tight supply and supply cannot be brought up that easily,” he explained. Major clients are presently obtaining only “50% to two-thirds of their requirements.”

This supply squeeze stems directly from artificial intelligence demand. Micron, SK Hynix, and Samsung collectively dominate the high-bandwidth memory segment that powers AI processors from manufacturers such as Nvidia and AMD.

The explosion in AI infrastructure investments has elevated memory pricing while keeping availability constrained. Mehrotra indicated the company’s robust financial performance directly mirrors these market dynamics.

Major financial institutions including Bank of America, Morgan Stanley, and JPMorgan raised their valuation targets for Micron following the quarterly disclosure, suggesting analysts remain optimistic about longer-term prospects despite near-term share price weakness.

South Korean Rival Escalates Competition

Compounding investor concerns this week, SK Hynix unveiled two significant strategic initiatives that unsettled Micron shareholders.

The Seoul-based chipmaker submitted regulatory documentation on Tuesday revealing intentions to acquire approximately $8 billion worth of extreme ultraviolet (EUV) lithography systems from ASML through the end of 2027 — representing a substantial commitment to advanced manufacturing capabilities.

Simultaneously, Korea Economic Daily published reports indicating SK Hynix is evaluating a potential U.S. stock exchange listing that could generate up to $10 billion in capital. U.S. investors presently face restricted access to SK Hynix equity, with most exposure limited to over-the-counter trading or exchange-traded funds such as the iShares MSCI South Korea ETF.

A domestic U.S. listing could fundamentally alter investment flows within the memory semiconductor sector. SK Hynix currently commands a forward price-to-earnings multiple of approximately 4.8 times, compared to Micron’s 5.3 times valuation, based on FactSet data.

During Tuesday’s midday trading session, Micron shares declined an additional 2.4%, prolonging the post-earnings retreat to four consecutive sessions.

Morgan Stanley will let clients trade tokenized versions of U.S. stocks and ETFs on its internal ATS from late 2026, tying into SEC pilots at DTCC and Nasdaq for on‑chain settlement.

Summary

- Morgan Stanley plans to enable tokenized issuance and settlement for selected blue‑chip U.S. stocks and ETFs on its alternative trading system in H2 2026, running alongside traditional shares.

- The move rides a tokenized stock market that has grown to about $800m in value and $1.8b in monthly volume, with roughly 50,000 monthly active and 130,000 total holding addresses.

- It fits a broader U.S. shift: the SEC has given DTCC’s DTC a three‑year window to custody tokenized securities and approved a Nasdaq pilot for tokenized stock settlement without changing trading rules.

Morgan Stanley plans to switch on tokenized stock trading for institutional clients on its internal alternative trading system in the second half of 2026, a significant escalation of Wall Street’s push to bring traditional equities onto blockchain rails. Amy Oldenburg, the bank’s head of digital assets strategy, told a panel at the Digital Asset Summit in New York on Tuesday that the ATS — which currently handles listed stocks, ETFs and American depositary receipts — will allow certain securities to be issued and settled in tokenized form alongside their conventional counterparts. “This is not FOMO,” Oldenburg said in separate comments reported by AOL, describing the rollout as “a very managed and stepped journey” tied to a broader modernization of Morgan Stanley’s trading and settlement infrastructure.

The plan positions Morgan Stanley to sit directly in the middle of the fast-growing tokenized stocks segment, where on-chain representations of U.S. equities have reached roughly $800 million in market value and about $1.8 billion in monthly trading volume as of December 2025, according to ChainCatcher’s market research. That same research notes around 50,000 monthly active addresses and 130,000 total holding addresses in tokenized equities, a sign that usage is moving beyond niche experiments and into regular portfolio construction for offshore and crypto-native investors. For Morgan Stanley’s ATS, the initial phase will likely focus on tokenized blue-chip U.S. stocks and ETFs, with Oldenburg previously signaling interest in connecting the bank’s wealth clients and advisory channels to a broader lineup of digital securities over time.

Morgan Stanley’s move lands in a regulatory environment that has turned sharply more accommodating to tokenized securities. In late 2025, the U.S. Securities and Exchange Commission granted a no-action letter to the Depository Trust & Clearing Corporation (DTCC), allowing its Depository Trust Company unit to custody and recognize tokenized stocks, bonds and other real-world assets on selected blockchains for a three-year period. This effectively gave DTCC permission to run tokenization services at scale and paved the way for mainstream broker-dealers and banks to plug into on-chain settlement without abandoning the existing market structure.

More recently, the SEC approved a pilot for Nasdaq to support tokenized stock trading, letting participants choose tokenized settlement while keeping the same order book, priority rules and shareholder rights as traditional equities. ChainCatcher notes that the Nasdaq pilot is designed to “explore the feasibility of on-chain settlement without changing the trading structure,” a model that closely mirrors Morgan Stanley’s plan to add tokenized legs into an existing ATS rather than create a separate crypto-only exchange. In parallel, Morgan Stanley has filed for spot Bitcoin and Solana ETFs, is preparing a native Bitcoin custody and trading platform, and, according to RootData and CryptoRank, is developing a digital wallet to support tokenized assets — suggesting that tokenized stocks are one pillar in a broader multi-asset digital securities roadmap.

Quick Overview

- AeroVironment introduced the Locust X3 directed-energy laser platform for countering unmanned aerial threats

- Shares declined 2.3% during midday trading session following the announcement

- The weapon system delivers 20kW to over 35kW of laser power and features multi-platform deployment capability

- Operating costs are significantly reduced compared to conventional interceptors due to elimination of ammunition requirements

- Company financials reveal robust 17.3% three-year revenue expansion but challenged profitability margins

AeroVironment (AVAV) revealed its newest anti-drone technology Tuesday, though investors responded with lukewarm enthusiasm.

The defense contractor introduced the Locust X3, a directed-energy weapon platform engineered to identify, track, and neutralize small-to-medium unmanned aircraft systems and select ground-level targets. Share prices retreated 2.3% by midday in New York trading, even as the S&P 500 remained relatively unchanged.

The Locust X3 employs laser technology delivering between approximately 20 kilowatts and exceeding 35 kilowatts of power. Integrated software handles autonomous detection, tracking, and engagement operations.

Deployment flexibility spans ground-based vehicles, stationary installations, and naval vessels, providing versatility across diverse operational theaters. AeroVironment emphasizes the platform’s modular architecture, enabling future upgrades and seamless integration with current defense infrastructure.

Economics represent a crucial advantage. Traditional interceptor systems demand physical ammunition replenishment, while this laser platform enables unlimited engagements without reload constraints. This capability becomes particularly valuable when confronting large formations of inexpensive hostile drones.

Foundation in Military Collaboration

AeroVironment indicated the Locust X3 leverages experience from previous U.S. Army program deployments. The architecture also supports Department of Defense objectives for unified cross-platform compatibility.

Shares traded at a price-to-book multiple of 2.3, approaching the lower boundary of its five-year range. Wall Street analysts maintain a consensus price target of $315.62. The Relative Strength Index (RSI) registered 39.89, approaching oversold conditions.

Profitability Challenges Despite Revenue Growth

The company has achieved 17.3% compound annual revenue growth across the trailing three-year period, demonstrating strong top-line momentum. Profitability metrics present a contrasting narrative—operating margin stands at -5.9% with net margin at -13.93%.

Balance sheet strength appears solid, featuring a current ratio of 5.51 and minimal leverage with a debt-to-equity ratio of 0.19. Return on equity, however, reflects negative performance at -7.55%.

Institutional investors control 65.49% of outstanding shares, indicating substantial confidence from large asset managers. Insider ownership measures 2.47%.

Volatility considerations include a beta coefficient of 2.03, categorizing the stock as high-volatility. The Piotroski F-Score of 3 suggests potential operational challenges.

Insider activity showed 10 selling transactions during the previous three-month period, a metric warranting attention.

The Beneish M-Score of -0.83 indicates some financial reporting concerns. Meanwhile, the Altman Z-Score of 5.61 signals strong balance sheet stability and low bankruptcy risk.

The Locust X3 represents [[LINK_START_3]]AeroVironment[[LINK_END_3]]’s continued expansion into counter-unmanned systems and directed-energy capabilities, market segments experiencing heightened defense spending interest.

AeroVironment maintains a market capitalization near $9.96 billion.

Key Takeaways

- Microsoft has secured a lease for a 700-megawatt data center facility in Abilene, Texas, initially planned for Oracle and OpenAI

- The facility is located adjacent to the Stargate campus, Oracle and OpenAI’s premier AI infrastructure project

- The agreement was finalized with developer Crusoe following Oracle and OpenAI’s decision to abandon their plans for the location

- A Reuters source confirmed that OpenAI’s current agreements with Oracle remain unchanged

- Oracle previously disputed media reports suggesting capacity delays at the Abilene location, labeling them as false

Microsoft has secured access to a substantial Texas data center facility that was originally intended for Oracle and OpenAI, based on a Bloomberg News report released Tuesday.

The facility, located in Abilene, Texas, boasts approximately 700 megawatts of power capacity. Its location is particularly notable — positioned immediately adjacent to the Stargate campus, which represents Oracle and OpenAI’s primary artificial intelligence infrastructure initiative.

The lease arrangement was negotiated with Crusoe, the development company responsible for the Abilene facility. Both Oracle and OpenAI had previously abandoned discussions to utilize the location before Microsoft entered negotiations.

When contacted by Reuters, a Microsoft representative stated the company had no information to share. Neither Oracle nor Crusoe provided responses to comment requests.

Earlier in the month, Bloomberg reported that Oracle and OpenAI had cancelled expansion plans at the Abilene location. The negotiations allegedly stalled because of financial challenges and evolving requirements from OpenAI.

Oracle rejected that narrative, asserting that reports about delayed capacity at Abilene were not accurate.

Oracle Partnership with OpenAI Remains Intact

A source with direct knowledge of the matter informed Reuters that OpenAI’s current contractual arrangements with Oracle are still active — indicating this transaction doesn’t dissolve their overarching collaboration.

This is a nuanced yet significant point. Microsoft’s acquisition of the Abilene facility doesn’t automatically indicate deterioration in the Oracle-OpenAI relationship, at least based on this information.

MSFT shares declined 2.69% during trading. Oracle (ORCL) dropped 4.42%.

The Competition for AI Infrastructure Space

Technology corporations have been rapidly expanding data center infrastructure to accommodate artificial intelligence applications. Microsoft’s Copilot platform and OpenAI’s ChatGPT both require massive computational power.

A 700-megawatt installation represents a significant capacity addition. For context, this level of power can support dozens of thousands of AI processors operating at maximum capacity.

Microsoft has emerged as one of the most aggressive investors in AI infrastructure development, having invested billions in OpenAI alongside its own internal expansion efforts.

Acquiring a location that was initially developed for rival organizations is uncommon, though understandable considering the current scarcity of available data center capacity.

Crusoe, the development firm, focuses on environmentally sustainable computing infrastructure. The company did not provide a response to Reuters’ inquiry.

The Abilene transaction has not received official confirmation from any involved parties. All information stems from Bloomberg’s reporting, which cited anonymous sources.

Oracle’s Stargate campus continues to operate next to the location Microsoft is preparing to occupy — establishing Abilene as a significant hub of AI infrastructure in West Texas.

As of Tuesday afternoon, Microsoft, Oracle, and OpenAI had all declined to release official statements regarding the development.

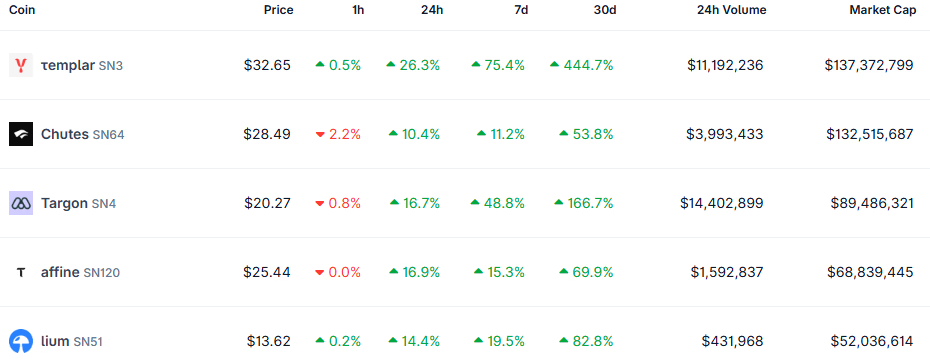

Bittensor subnet tokens’ cumulative valuation has climbed to $1.5 billion as nearly every token in the ecosystem posts double- or triple-digit 30-day gains.

Decentralized artificial intelligence (AI) protocol Bittensor’s native TAO token has rallied roughly 90% over the past month from around $180 at the start of March to above $332 as of March 24, and the momentum is spilling over into its subnet token ecosystem.

According to CoinGecko data, the Bittensor Subnets category is up 30% over the past 24 hours to a combined market capitalization of $1.47 billion, with trading volume topping $118 million. Of the subnet tokens tracked on the platform, a significant number have posted triple-digit percentage gains over the past month.

What Are Subnets?

Subnets are specialized mini-networks within the Bittensor ecosystem, each dedicated to a specific AI task, ranging from language model training and decentralized compute to sports prediction and cybersecurity. Miners within each subnet compete to produce high-quality AI outputs, while validators evaluate performance and allocate TAO rewards accordingly.

Since the launch of dynamic TAO (dTAO) in February 2025, each subnet operates as its own automated market maker with a natively assigned token. The valuation of each subnet token is determined by the amount of TAO staked into that subnet’s reserves, creating a direct economic link between TAO’s price and subnet token performance. The subnet ecosystem first crossed $500 million in April 2025, and by July 2025, the cumulative subnet market cap had neared $1 billion as TAO treasury companies like xTAO and Synaptogenix emerged.

The relationship is reflexive: as TAO appreciates, each subnet’s TAO reserve becomes more valuable, inflating subnet token prices, which, in turn, attract more stakers and attention to the ecosystem.

Subnet Standouts

The TAO rally accelerated on March 20 after Nvidia CEO Jensen Huang and investor Chamath Palihapitiya endorsed Bittensor’s decentralized AI training model on the All-In Podcast.

That enthusiasm has cascaded into subnet tokens. τemplar (SN3) — the subnet behind the Covenant-72B model that triggered the Nvidia-fueled rally — is now the top subnet token with a $137 million market cap after rallying 444% over the past month.

Other notable 30-day performers include OMEGA Labs (SN24) at 440%, Level 114 (SN114) at 280%, BitQuant (SN15) at 230%, Nova (SN68) at 218%, and Grail (SN81) at 211%.

Even the more established subnet tokens with larger market caps have posted strong monthly returns. Chutes (SN64), which has a $132 million market cap, is up 54% over 30 days. Targon (SN4) has gained 166%, Ridges AI (SN62) is up 85%, and Hippius (SN75) has risen 115%.

The primary catalyst for the broader rally was the reveal of Covenant-72B, a large language model trained permissionlessly across Bittensor’s Subnet 3 by over 70 contributors using commodity internet hardware. The model was trained on 1.1 trillion tokens and achieved a 67.1 MMLU score, confirmed in a March 2026 arXiv paper, putting it in a competitive range with Meta’s Llama 2 70B.

The Nvidia CEO endorsed both proprietary and open-source AI models as complementary during the podcast appearance, framing foundational AI technology as benefiting from decentralized innovation.

Beta Play on Decentralized AI

The outsized returns in subnet tokens relative to TAO itself reflect a dynamic familiar to crypto markets: smaller-cap ecosystem tokens tend to act as leveraged bets on their parent protocol. With TAO’s market cap sitting at roughly $3 billion and individual subnet tokens ranging from $1 million to $110 million, the tokens offer significantly higher volatility in both directions.

Looking ahead, the Bittensor network plans to expand its active subnet capacity from 128 to 256 later this year, which could bring a fresh wave of new subnet token launches and further broaden the category.

Before the first TAO halving in December 2025, subnets had already reached a cumulative $1.28 billion market cap, with Yuma, a subsidiary of Digital Currency Group, contributing to 14 different subnets. A potential regulatory decision on converting the Grayscale TAO Trust into a spot ETF could also provide additional institutional access by late 2026.

For now, the surge in subnet tokens signals that market participants are betting the decentralized AI narrative has staying power, and that Bittensor’s expanding network of specialized AI subnets will be at its center.

Arbitrum Sepolia, the primary testnet for the leading Ethereum Layer-2, has stopped block production. The network suffered a critical consensus failure at block 204606366, causing a chain split between node operators using different CPU architectures.

Developers relying on the testnet for pre-deployment validation are currently stalled as Offchain Labs engineers deploy emergency fixes.

- Consensus Failure: The chain halted at block 204606366, triggering a major outage that disrupted the network from 6:44 AM to 9:02 PM.

- Hardware Split: The breakdown was caused by a rare execution deviation where ARM and x86 processors produced conflicting block results.

- Operator Action: Node runners must currently restart with safety verification flags disabled or migrate entirely to x86 hardware to sync.

Why Did the Arbitrum Sepolia Nodes Split?

The outage is technical, specific, and severe. At block 204606366, the Arbitrum Sepolia sequencer produced a batch that processed differently depending on the validating node’s hardware. Nodes running on ARM architecture calculated a different state root than those on x86 chips, effectively splitting the network’s brain. This deviation forced a halt to block production, as the chain could not reach consensus on a valid path forward.

Offchain Labs identified the issue as a major outage. While mainnet operations remain unaffected, this incident highlights the fragility of heterogeneous hardware environments in decentralized networks. To resume syncing, node operators on version 3.8.0 must restart with the flag --node.feed.input.verify.dangerous.accept-missing, a command that explicitly bypasses standard input verification protocols. This is a stopgap, not a solution.

Testnets are designed to break so mainnets do not, but reliability on Arbitrum Sepolia has become a recurring friction point. Since the deprecation of the Goerli testnet in March 2024, Sepolia has served as the critical staging ground for dApps before they launch on the main Ethereum Layer-2 network. Frequent downtime here translates directly to delayed mainnet deployments and stalled audit timelines.

DeFi Exploits over the past year… — Emperor Osmo

1/ Moby Trade/Arbitrum (Jan 2025) $2.5M

Leaked private key. $1.5M recovered by whitehat.

2/ Hyperliquid bridge (Mar 2025) $17M

Smart contract exploit.

3/ UPCX (Apr 2025) $70M

Compromised private key. Token crashed 70%.

4/ GMX V1 (May 2025)…

(@Flowslikeosmo) March 22, 2026

(@Flowslikeosmo) March 22, 2026

This is not an isolated event. The network faced similar stability challenges in August. While other protocols execute smooth, planned infrastructure updates—such as the recent Tellor Palmito testnet upgrade—Arbitrum’s unexpected halts force developers into reactive maintenance.

For institutional players building on Arbitrum, the requirement to swap hardware architectures mid-development to maintain a sync is a red flag for infrastructure maturity. The ecosystem needs stability, not just throughput.

What to Watch: The Path to Resolution

Offchain Labs has not yet released a permanent patch for the ARM/x86 deviation. At press time, the recommended fix requires manual intervention from every node operator. The team has announced plans for a new Nitro version update and a fresh database snapshot to resolve the compatibility issues fully.

Traders and developers should monitor the official status page for the release of the new snapshot. Until a verified patch confirms cross-architecture consistency, the testnet remains in a fragile state. If the fix lags, deployment schedules across the Arbitrum Orbit ecosystem will slide.

Discover: The best new crypto in the world

The post Arbitrum Sepolia Testnet Halts Block Production in Partial Outage appeared first on Cryptonews.

Crypto World

BMO launches tokenized cash and deposits on CME’s 24/7 settlement network: Bank of Montreal

Bank of Montreal enables clients to convert dollars into tokenized cash on CME and Google Cloud’s Universal Ledger for round-the-clock margin, collateral and B2B payments.

Bank of Montreal announced it will allow clients to convert dollars into tokenized cash and deposits on CME and Google Cloud’s Universal Ledger infrastructure, enabling 24/7 settlement for margin, collateral and business-to-business payments. The move integrates one of North America’s largest banks by assets into the CME’s continuous settlement rails, expanding institutional access to tokenized financial services beyond traditional trading hours.

The Universal Ledger platform, operated jointly by CME and Google Cloud, supports real-time asset movement and settlement outside conventional market windows. BMO’s integration represents a major adoption milestone for institutional tokenization infrastructure, allowing the bank’s client base direct access to around-the-clock digital asset settlement capabilities.

Sources: BMO

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Apple May Give Siri a Big AI Overhaul in iOS 27

‘US troops gather in Gulf’ and ‘Strictly No Baftas’

Multibillion-dollar bailout for major aluminium maker

-

Crypto World4 days ago

Crypto World4 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics4 days ago

Politics4 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Crypto World3 days ago

Crypto World3 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

News Videos6 days ago

News Videos6 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World3 days ago

Crypto World3 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Politics7 days ago

Politics7 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Tech5 days ago

Tech5 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Crypto World6 days ago

Crypto World6 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

Sports2 days ago

Sports2 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

NewsBeat6 days ago

NewsBeat6 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

News Videos6 days ago

News Videos6 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

Politics5 days ago

Politics5 days agoGender equality discussions at UN face pushbacks and US resistance

-

Business2 days ago

Business2 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Business6 days ago

Business6 days agoWho Was Alex Pretti? 5 Key Facts About the ICU Nurse Killed by Federal Agents in Minneapolis

-

Sports1 day ago

Sports1 day agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Tech2 days ago

Tech2 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Sports4 days ago

Sports4 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

-

Tech7 days ago

Tech7 days agoSubnautica 2 might finally be entering early access in May

-

Sports6 days ago

Vikings Free Agency Enters Phase 2 with Key Questions

You must be logged in to post a comment Login