Crypto World

Qualcomm (QCOM) Stock Rockets 15% After Meta Partnership and Aggressive Data Center Goals

Key Takeaways

- Qualcomm increased its fiscal 2029 non-smartphone revenue forecast to approximately $40 billion from $22 billion

- The chip manufacturer established a data center revenue objective exceeding $15 billion by fiscal 2029

- Meta Platforms committed to a multi-year partnership utilizing Qualcomm’s Dragonfly C1000 server chip

- Automotive segment generated record $1.3 billion in Q2 FY2026, representing 38% growth year-over-year

- QCOM shares surged up to 15% following the announcement before moderating

During Wednesday’s investor presentation, Qualcomm unveiled an aggressive expansion strategy that sent Wall Street into a frenzy. The semiconductor company nearly doubled its fiscal 2029 revenue projection for non-smartphone segments, elevating the target to approximately $40 billion from the previous $22 billion goal announced in 2024. The stock rallied as much as 15% during trading.

The previous $22 billion projection was already considered ambitious for a corporation still predominantly associated with mobile phone processors. The revised figure signals that Qualcomm is making a substantial wager on markets outside traditional handsets.

The cornerstone of this transformation is the data center sector. Qualcomm introduced the Dragonfly C1000, a server chip featuring over 250 proprietary cores. Additionally, the company launched a portfolio of AI acceleration products specifically engineered for inference workloads rather than training applications. Leadership is pursuing more than $15 billion in data center revenue by fiscal 2029, starting from essentially zero currently.

To put this in perspective, Qualcomm generated $10.6 billion in total revenue during fiscal Q2 2026. Mobile chip sales accounted for approximately $6 billion of that figure. Data center contributions remain negligible at present.

The most significant announcement wasn’t technical specifications — it was customer validation. Meta Platforms committed to a multi-year, multi-generation agreement to deploy Qualcomm’s new processor across its data center infrastructure, with production scheduled to commence in the second half of 2028. Securing Meta as a launch partner lends substantial credibility to the data center initiative.

Meta Agreement Validates Data Center Strategy

Qualcomm’s innovative High Bandwidth Compute (HBC) architecture employs vertical chip stacking instead of traditional horizontal layouts, positioning memory and processing units in closer proximity. The manufacturer claims this configuration enhances data transfer rates and power efficiency.

The initial generation of this architecture is slated to debut in data center deployments next year, with widespread commercial availability anticipated in 2028. Qualcomm is simultaneously engaging with mobile device, personal computer, and automotive manufacturers about future integration of this technology into their products.

Executive Vice President Durga Malladi stated directly: “What starts in data centers is not going to end there.”

The AI250 accelerator, built on the HBC framework, won’t enter commercial sampling until mid-2027. Meta’s CPU manufacturing doesn’t begin until late 2028. These remain forward-looking milestones rather than realized revenue.

Automotive Segment Delivers Current Results

While the data center narrative focuses on 2028 and beyond, the automotive division is generating results today. Qualcomm reported record automotive revenue of $1.3 billion in fiscal Q2 2026, reflecting 38% year-over-year expansion. The company projects $10 billion in annual automotive revenue by fiscal 2029, supported by a design-win backlog the company estimates at approximately $65 billion.

This trajectory provides tangible evidence for the broader diversification thesis. The automotive business demonstrates the strategy can succeed beyond smartphones in at least one significant market.

From a valuation perspective, the stock trades at roughly 17 times non-GAAP earnings. That multiple sits well below broader market averages and significantly trails valuations assigned to leading AI semiconductor companies — indicating the market continues to view Qualcomm primarily through the lens of its smartphone chip business.

QCOM finished Thursday at $189.39, declining 7.57% for the session, retreating from Wednesday’s investor day-driven rally.

Three altcoins enter the weekend within reach of record highs (ATH), led by WhiteBIT Coin, which trades about 12% below its peak. Hyperliquid and Tron complete a list picked on one rule, proximity to all-time highs.

The selection follows the same criteria as previous weekend editions. The gaps are wider this time, so each chart needs a stronger trigger. The table below maps the key levels.

Altcoin

Price

ATH

Below ATH

Key Resistance

Key Support

WhiteBIT Coin (WBT)

$56.52

$64.11

~12%

$58.00

$55.93 (0.618 Fib)

Hyperliquid (HYPE)

$58.26

$76.70

~24%

$63.66 (0.236 Fib)

$55.41 (0.382 Fib)

Tron (TRX)

$0.331

$0.4313

~23%

$0.3359 (0.382 Fib)

$0.3101 (0.618 Fib)

WBT Holds the Golden Pocket Below $58

WhiteBIT Coin (WBT) trades near $56.62, down about 0.5% on the day. The price sits roughly 12% below its record of $64.11 from December 2025.

The coin broke down from an ascending parallel channel earlier this year. The lower band of that channel was confirmed as resistance on July 6.

Since then, the price has moved sideways below resistance at $58. However, it still holds above the golden pocket, the 0.618 Fibonacci retracement near $55.93.

If sellers push lower, the 0.5 Fibonacci level near $53.31 marks the next support, followed by the 0.382 level near $50.69. WBT also featured previously and trades almost flat a week later.

Meanwhile, volume keeps contracting, which suggests accumulation. A strong catalyst and expanding volume could still send the price to a record, even this weekend.

HYPE Corrects 24% From Its June Record

Hyperliquid (HYPE) trades near $58.26, down about 1.7% on the day. The token sits 24% below its all-time high of $76.70, reached on June 16.

The chart looks the most neutral of the three. The price has trended lower since the record. It now heads toward the 0.382 Fibonacci retracement at $55.41, a standard correction target.

In the coming weeks, that level converges with a long-term ascending trendline. Buyers have already confirmed the line twice since February.

If the correction deepens, the next support zone sits slightly above the golden pocket, the 0.618 Fibonacci level at $42.07. Recent unstaking of $291 million by Multicoin and Paradigm added pressure below $60.

Volume keeps contracting, which signals accumulation and no decisive move from either side. The RSI reads about 40, still neutral but pointing down.

TRX Coils Inside a Triangle That Targets $0.3611

Tron (TRX) trades near $0.331, up about 1.4% on the day. The price sits 12% below its late-May high of $0.3775 and roughly 23% below the record of $0.4313.

The daily chart looks the most bullish of the three. An ascending trendline has supported the price since February and has been confirmed four times.

The price now trades between the 0.382 Fibonacci retracement at $0.3359 and the golden pocket at $0.3101. The flat resistance and rising lows form an ascending triangle, a bullish formation.

The pattern indicates a target of $0.3611, just above the 0.236 Fibonacci level at $0.3518. A confirmed breakout would reopen the longer path to the record.

Volume keeps decreasing, which points to accumulation below resistance. The RSI reads 58 and keeps rising, though it stays in the neutral zone.

Altcoins ATH: What to Watch This Weekend

Each setup now hinges on one level. WBT must reclaim $58, HYPE has to defend $55.41, and TRX needs to break $0.3359.

A move through those levels would strengthen each thesis and could point toward record territory. Failure would hand the initiative back to sellers heading into next week.

Broader conditions still matter, as Bitcoin works through its own late-cycle phase. A weekend risk-on move would give all three altcoins the push they need.

To read the latest cryptocurrency market analysis from BeInCrypto, click here.

The post 3 Altcoins That Could Reach New All-Time Highs This Weekend appeared first on BeInCrypto.

Ethereum remains under pressure on the higher timeframes despite showing signs of stabilization over the past several weeks. The daily structure continues to trade below key moving averages, while the 4-hour chart shows buyers attempting to build a higher low above a key support area. On-chain data also continues to provide a constructive backdrop as exchange balances keep declining.

Ethereum Price Analysis: The Daily Chart

The daily chart shows ETH trading around $1.86K after recovering from the June sell-off that briefly pushed the price into the major demand zone around $1.5K. Although that support area successfully halted the decline, the broader trend has yet to shift decisively in favor of the bulls.

The asset sits just above the higher trendline of the long-term descending channel after the recent breakout. However, both the 100-day and 200-day moving averages are still overhead, indicating that sellers still control the higher timeframe structure. The recent test of the 100-day moving average around $2k has been rejected, which leaves ETH trapped beneath several technical barriers.

The first resistance sits around the $2K supply zone, where the key moving averages also converge. A stronger resistance zone is located roughly around $2.4K, which capped the previous recovery attempt in April. Reclaiming these levels would be required to suggest that the broader downtrend is losing momentum.

ETH/USDT 4-Hour Chart

The lower timeframe presents a more constructive picture. Since the early July rebound, ETH has been printing higher highs and higher lows while respecting a rising trendline (white) that continues to support the advance.

Yet, following the rejection from the higher boundary of the ascending channel (yellow), the asset has pulled back toward the white trendline, where buyers have so far stepped in. These trendlines form a short-term rising wedge, and as long as price remains above the lower bound and the $1.75K support zone, the short-term bullish structure remains intact.

The next objective for buyers is another test of the recent highs around $1.9K to $1.95K. A decisive breakout above that region and the channel could open the path toward the daily supply zone at $2K.

On the other hand, a breakdown below the white ascending trendline would weaken the short-term structure and increase the probability of a deeper retracement toward $1.75K, with $1.7K and $1.6k serving as the next notable support levels.

On-Chain Analysis

The Exchange Supply Ratio continues to trend lower, reaching fresh lows despite Ethereum’s prolonged corrective phase. This metric measures the proportion of ETH held on centralized exchanges, and a declining reading generally indicates that coins are leaving exchanges and moving into private wallets or long-term storage.

The persistent decline suggests that sell-side liquidity available on exchanges continues to shrink. Historically, sustained exchange outflows have often reflected improving investor conviction and reduced immediate selling pressure.

Although this alone does not guarantee an upside reversal, the on-chain backdrop appears considerably healthier than the current price structure. If demand begins to strengthen while exchange balances remain depressed, the reduced available supply could provide additional support for a broader recovery once ETH overcomes its key technical resistance levels.

The post Ethereum Price Prediction: Where Is ETH Headed After the $1,950 Rejection? appeared first on CryptoPotato.

A trader holding USDT can now move from Bitcoin into gold, oil or a product linked to SpaceX without opening a brokerage account. The balance, interface and trading hours may look familiar. What the trader owns can change with every click.

That difference matters as major centralized exchanges like MEXC expand beyond crypto. The exchange now offers commodities, equity futures, pre-IPO products, and access to US-listed shares. Its strategy reflects a wider race among exchanges and fintech apps to become the place where users trade almost anything.

The market is growing quickly. Tokenized stocks reached a record market value of about $2.3 billion in July, up from $329 million a year earlier.

Kraken says its xStocks products have generated more than $25 billion in cumulative transaction volume. Robinhood has also expanded its stock-token business, while Coinbase is developing its own tokenized equity offering.

The central question is whether exchanges can make traditional markets easier to access without blurring what users are actually buying.

The SpaceX Test

MEXC saw the appetite directly through its SPACEX(PRE) Launchpad. Across two rounds, the exchange says almost 80,000 users submitted close to $200 million in subscriptions.

For Vugar Usi, MEXC’s CEO, the response showed that crypto traders are looking beyond digital assets.

“Users do not necessarily want separate platforms for separate asset classes,” Usi told BeInCrypto. “They want one place where they can move between crypto, equities, precious metals and other opportunities with lower friction.”

Yet SPACEX(PRE) also shows why that convenience requires clearer explanations. Despite being traded through a spot-style interface, the product does not represent direct SpaceX ownership.

MEXC describes it as a Mirror Credits product that tracks the company’s value. Holders receive no voting rights, dividends, or direct shareholder claim.

The exchange also offers equity futures, which let users speculate on stock prices with USDT and leverage. Again, traders do not own the underlying shares.

Its RealStocks service has a different structure. Launched in June, it gives eligible users access to US-listed equities through a securities brokerage partner. MEXC says these purchases represent actual shares and include dividends where applicable.

These distinctions can disappear when every product sits inside one app.

One Interface, Different Rights

US regulators have already identified several tokenization models. A token may represent an indirect interest in shares held by a custodian. It may also be a synthetic contract that tracks a stock without carrying any ownership rights.

In a January statement, the US Securities and Exchange Commission warned that third-party tokenized products can expose investors to risks they would not face when holding the underlying security, including the possible failure of the token issuer.

The label “tokenized stock” therefore tells users very little on its own. They need to know who holds the underlying asset, whether the product can be redeemed, and what happens if the issuer or exchange fails. Voting rights, dividends and transfer restrictions also vary.

Usi acknowledged that wider availability raises the platform’s responsibility.

“Wider access does not mean every product should be presented in the same way to every user,” he said. “For more complex products, platforms need clearer risk disclosures, appropriate user terms and educational content that explains how the product works, including potential losses and market-specific risks.”

Trust Becomes Harder to Measure

Moving into equities and commodities also expands an exchange’s compliance burden. Securities rules differ across jurisdictions, so a platform may retain a single interface while offering a different product catalogue in each country.

MEXC appointed Robert MacDonald as chief compliance officer in July. The company says it is expanding its compliance team and adding automated screening, while retaining human review for most fraud decisions.

It has also committed to expanding its Guardian Fund from $100 million to $500 million over two years and has added 1,000 BTC. These figures remain company-reported. A protection fund does not explain when users qualify for compensation or replace independent verification of liabilities.

Usi argued that users should examine regular Proof of Reserves disclosures, external security assessments and how platforms respond to incidents.

“But no single fund, audit or data point is enough,” he said. “Users should look for consistency.”

Crypto exchanges are getting closer to becoming global investment platforms. Demand is already visible. Their harder task is making each product as easy to understand as it is to trade.

The post Crypto Exchanges Want to Be Your Broker. The Fine Print Matters appeared first on BeInCrypto.

India’s Internet Freedom Foundation (IFF) has publicly challenged a government order requiring GitHub to remove access to multiple repositories connected to Jack Dorsey’s decentralized messaging app, BitChat—arguing the action bypasses safeguards built into India’s more formal website-blocking process.

The dispute escalated shortly after India’s cybercrime agency instructed GitHub to disable access to three BitChat repositories within a matter of hours, warning that the decentralized messaging system could be used to circumvent internet shutdowns, evade lawful surveillance, and support unlawful activity. IFF says the order is unconstitutional and should be withdrawn.

Key takeaways

- IFF condemns a GitHub takedown order over BitChat, saying it exceeds government authority under India’s Information Technology Act.

- The foundation argues the notice should have followed India’s formal website-blocking procedure, which includes procedural protections.

- IFF disputes the rationale for removal, noting the repositories were not accused of containing specific unlawful content.

- The underlying controversy centers on BitChat’s decentralized architecture, designed to function without internet connectivity by routing messages over Bluetooth between nearby devices.

IFF challenges the legal route used for the GitHub takedown

In a statement posted on X, IFF said the government’s order was issued under Section 79(3)(b) of India’s Information Technology Act, rather than through the established process for website blocking. According to IFF, that distinction matters because the standard approach is tied to formal procedures and safeguards.

The foundation’s core claim is that the government used an enforcement mechanism that allows rapid platform action without the protections that accompany the country’s website-blocking framework. IFF urged authorities to withdraw the notice and to publish all takedown orders made under the same provision, suggesting a broader transparency and accountability issue beyond the BitChat case.

What the cybercrime order alleged—and what IFF contests

IFF’s criticism comes a day after India’s cybercrime agency directed GitHub to disable access to three BitChat repositories within three hours. The agency’s stated concern was that BitChat—by virtue of being decentralized—could help users communicate even during internet disruptions, potentially undermining shutdowns and lawful monitoring.

IFF pushed back on that justification on two fronts. First, it argued that the order did not identify any specific unlawful material inside the repositories. Second, IFF said the reasoning effectively treated BitChat’s design choices—especially its ability to relay messages without internet access—as sufficient grounds for removal on their own.

In IFF’s view, that approach risks expanding enforcement beyond content-based restrictions and into architecture-based suppression—an issue that tends to carry significant implications for developers and open-source ecosystems.

How BitChat is designed to work without the internet

BitChat is described as a decentralized messaging app that routes encrypted messages between nearby devices using Bluetooth rather than relying on internet connectivity or centralized servers. This design is intended to keep communication possible when conventional networking is unavailable.

IFF pointed to that same feature as the subject of the government’s concern, arguing that the decentralized model—particularly its offline and proximity-based capability—was cited as justification rather than any identifiable illegal content.

This is not a purely theoretical distinction. If a messaging platform is removed primarily because it can operate during outages, the line between lawful restrictions on content and broader restrictions on tools that enable communication during shutdowns becomes a central policy question.

BitChat’s adoption surge during outages and unrest

BitChat’s visibility has grown alongside periods of unrest and connectivity failures. Cointelegraph previously reported on the app’s July 2025 launch, describing a decentralized approach that can support local messaging when normal internet routes are disrupted. Since then, BitChat has reportedly gained traction in multiple countries during moments of high disruption.

According to earlier reporting cited by the article, adoption increased during events including protests, natural disasters, and internet shutdowns across places such as Madagascar, Nepal, Uganda, Jamaica, and Iran. The pattern—more installs when connectivity is disrupted—helps explain why a case involving GitHub repositories can quickly become a flashpoint for broader debates over censorship, shutdown circumvention, and the role of open-source development during emergencies.

For investors and builders in the crypto-adjacent decentralization ecosystem, the case also underscores a recurring theme: software that is designed for resilience and offline functionality can attract regulatory attention even when it is not directly tied to specific illegal content.

Authorities have yet to clarify how they will apply Section 79(3)(b) in cases involving open-source code with offline or decentralized capabilities, and IFF’s demand to publish all takedown orders under that provision suggests further legal and procedural scrutiny ahead. Readers should watch whether GitHub complies permanently, whether the repositories are restored, and whether any court or regulatory process follows to test IFF’s constitutional arguments.

Among others abandoning the treasury approach include Sequans Communications (SQNS), which sold 1,025 BTC before disposing of nearly 80% of its remaining holdings to repay convertible debt. It has ruled out further purchases and plans to monetize its remaining 658 BTC.

Nakamoto (NAKA), whose shares have fallen 99% since its May 2025 SPAC deal, sold around 284 BTC to raise $20 million for working capital following its acquisitions of BTC Inc. and UTXO Management. It sold roughly 40 BTC received through its derivatives program, according to VanEck’s Sigel. Almost 70% of its remaining 5,342 BTC were pledged against a Kraken loan maturing in December, creating what Sigel described as a potential binary event.

It’s not only specialist treasury companies that are reducing their holdings of the largest cryptocurrency. Crypto miners including Bitdeer and MARA Holdings are selling bitcoin to repurchase or repay debt and repurpose their energy-supply deals and computing resources to power AI data centers.

Other sellers include Empery Digital, which has reportedly sold almost half its bitcoin to finance buybacks and debt repayment, and Strategy, which has sold about 3,620 BTC in recent weeks and authorized additional sales to support its U.S. dollar reserves.

Strategy, which started the investment trend, remains the largest publicly listed holder of bitcoin, with more than 840,000 BTC. CEO Michael Sayler remains bullish.

The Council of the European Union has sanctioned Justin Sun-owned HTX and Huobi Global S.A in a move that it hopes will “further cripple Russia’s economy and war machine.”

HTX and Huobi are now officially on the EU’s “list of credit and financial institutions and entities providing crypto-assets services or payment services established outside of the Union that are significantly frustrating the purpose of the prohibitions in this Decision, Decision 2014/145/CFSP, Regulation (EU) No 833/2014 and Regulation (EU) No 269/2014.”

One of the payment networks being targeted is the A7 Network, which is behind the A7A5 stablecoin.

Read more: UK sanctions HTX for alleged Russian sanctions violations

The sanctions targeting HTX follow the United Kingdom Foreign, Commonwealth, and Development Office sanctions against Huobi Global S.A., which claimed that it was providing financial services to Russia, including interacting with the A7 Network.

At the time, HTX tried to claim that “the listed entity Huobi Global S. A. is distinct from the online HTX exchange.”

However, a Protos review determined that Huobi Global S.A. was the owner of the HTX trademark in the United States and had described itself in court filings as the firm that “owns and operates HTX.”

Furthermore, these European Union sanctions explicitly list HTX alongside Huobi Global SA.

HTX moves its reserves and wallets

Following this, HTX disclosed that it had moved over $1 billion worth of its reserves to an undisclosed custodian.

HTX says on its proof of reserves page that in order to verify these quantities, we should “please directly contact the third-party custodians.”

However, HTX hasn’t responded to requests from Protos for the identity of that custodian.

More recently, blockchain intelligence firm TRM Labs has claimed that HTX has been rapidly churning through wallets.

This means that other cryptocurrency entities that want to prevent transactions from the sanctioned HTX are struggling as their list of HTX-related addresses ends up out of date.

Ari Redbord, global head of policy at TRM Labs, described the behavior as “HTX changing its wallets every few hours to stay a step ahead of screening built on static lists.”

HTX told The Block that these practices “reflect routine, security-driven platform operations common across the industry.” It adds that it “categorically rejects any characterization implying otherwise.”

These additional sanctions are likely to complicate HTX’s business.

Protos reached out to HTX for comment, but it didn’t respond before publication.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

A US police union representing more than 382,000 members has reversed its position and endorsed the latest CLARITY Act after lawmakers added language addressing its concerns about cryptocurrency investigations.

Summary

- The National Fraternal Order of Police has reversed course and endorsed the latest CLARITY Act.

- The union says revised provisions preserve law enforcement powers to investigate crimes involving digital assets.

- Senate delays and election-year disputes have pushed Polymarket’s 2026 passage odds down to 33%.

According to former Fox Business reporter Eleanor Terrett, the National Fraternal Order of Police now supports the bill after reviewing provisions tied to the Blockchain Regulatory Certainty Act. The union believes the language protects the ability of police and prosecutors to pursue crimes involving digital assets.

In a July 24 letter to Senate Banking Committee Chairman Tim Scott and ranking member Elizabeth Warren, FOP National President Patrick Yoes backed the latest version of H.R. 3633, formally known as the Digital Asset Market Clarity Act.

Yoes wrote that revised Section 10604, which amends the BRCA, does not restrict law enforcement agencies or prosecutors from addressing illegal conduct involving cryptocurrencies. According to the letter, the clarification directly answers concerns the union raised during earlier negotiations over the legislation.

Terrett, however, reported that the BRCA provisions remained unchanged in the latest bill released Wednesday. She noted that it was unclear which changes the FOP was referring to when it announced its support.

The apparent inconsistency leaves open whether the union assessed language added at an earlier stage, received separate assurances from lawmakers, or interpreted an existing provision differently. Neither the FOP letter nor Terrett’s report identified a specific newly amended passage beyond Section 10604.

Revised provisions preserve crypto enforcement powers

Explaining its reversal, the FOP cited several sections that it believes will help federal, state and local agencies investigate financial crimes involving digital assets. The union said investigators need clear authority and practical tools as they confront fraud, organized crime and illicit finance conducted through crypto networks.

Among those provisions, the legislation would create safeguards addressing fraud linked to digital asset kiosks. According to the FOP, the measure also applies anti-money laundering and sanctions compliance duties across parts of the crypto industry.

The letter pointed to rules intended to help investigators act before suspected criminal funds leave their reach. Those provisions would protect digital asset companies and stablecoin issuers from liability when they voluntarily delay suspicious transactions or respond to a law enforcement request.

Given how quickly cryptocurrencies can cross jurisdictions, the FOP argued that temporary transaction holds could give investigators time to prevent losses, recover stolen assets and disrupt illegal activity. The union presented those protections as an important tool for cases in which funds might otherwise disappear before officers can intervene.

Bank Secrecy Act provisions also contributed to the union’s support. According to the letter, the revised bill updates the treatment of digital assets under rules governing monetary instruments, helping existing reporting and enforcement requirements apply more clearly to crypto activity.

Other sections direct government agencies to share information and coordinate their responses to illicit finance risks. The FOP added that the bill would strengthen international cooperation on anti-money laundering enforcement and sanctions involving digital assets.

Under Title IX, the legislation would establish a grant program for state and local digital asset enforcement work. The FOP said it would also create a national security and law enforcement training program, form a digital asset cyber innovation center and introduce measures designed to protect older consumers from deception.

Addressing protections for software developers, the union said the bill would not prevent authorities from investigating crimes, prosecuting offenders or applying existing criminal laws. Its letter specifically cited 18 U.S.C. § 1960, a federal statute covering certain unlicensed money-transmitting activity.

The FOP also pointed to language preserving liability for people who knowingly transfer funds tied to criminal offenses or promote unlawful activity. According to the union, this distinction gives responsible developers legal certainty without shielding individuals who intentionally assist illegal transactions.

Senate delay pushes CLARITY Act beyond the August recess

The endorsement has arrived as the CLARITY Act faces a shrinking congressional timetable. As crypto.news reported earlier on July 24, Senate Majority Leader John Thune does not expect the Senate to approve the market structure legislation before lawmakers leave Washington for the August recess.

Thune’s position removes a deadline that crypto industry supporters had treated as important for completing the bill in 2026. Following the development, Polymarket traders lowered the probability of the legislation becoming law this year to 33%.

Attention has therefore moved to the session after the November midterm elections. During that period, lawmakers will return to government funding measures, defense legislation and other unfinished bills that will also compete for limited Senate floor time.

According to Wintermute head of policy and advocacy Ron Hammond, the CLARITY Act still has enough bipartisan backing to pass but has become trapped in election-year disputes. Hammond attributed the immediate obstacle to political messaging rather than a shortage of votes in the Senate.

With Democrats preparing to campaign against President Donald Trump and alleged corruption, Hammond expects some lawmakers to avoid backing a major cryptocurrency bill before the election. His assessment suggests the FOP endorsement may resolve one law enforcement dispute without removing the political barriers delaying a Senate vote.

In its letter, the FOP described the latest provisions as a meaningful effort to provide stronger investigative tools, clearer compliance paths and better coordination between agencies. The union said its initial concerns had been satisfactorily addressed and offered to work with lawmakers to secure passage of the amended bill.

Leading economist Peter Schiff has warned that rising oil prices could drive July CPI numbers higher after a drop in the June CPI, which was largely due to oil declining by 30%.

Oil prices have risen sharply after renewed US-Iran hostilities, Houthi attacks on Saudi-linked tankers, and fresh oil supply concerns.

Peter Schiff Flags Inflation Concerns Ahead Of Fed Meeting

Schiff’s warning comes amid renewed US-Iran tensions and supply chain concerns after Iran imposed a blockade on the Strait of Hormuz and the Bab el-Mandeb Strait. The economist noted that June CPI numbers were lower due to a substantial drop in crude prices. However, the recent increase in prices could undermine June’s progress and drive inflation higher in July.

Schiff stated in a post on X,

“Investors celebrated the June CPI, as a 30% fall in the price of oil led to a larger-than-expected decline. But so far in July, the price of oil is already up 30%, back above $90 per barrel.”

Schiff said that if prices went back above $100, it would mark a 43% increase from recent lows, and would adversely impact July CPI numbers. Brent crossed the $100 mark hours after the warning of Houthi-led attacks on Saudi oil tankers.

“If the price hits $100 by month-end, that will be a 43% rise. July CPI could be a doozy.”

Schiff argued that June’s lower CPI numbers were due to lower oil prices, and higher prices in July could completely reverse progress and drive inflation higher.

“No, it’s just that the only reason June CPI fell so much was the 30% drop in oil. That will likely be completely reversed by an even bigger rise in the price of oil in July.”

Oil Prices Could Push July Inflation Numbers Higher

US Bureau of Labor Statistics data showed a 0.4% decline in headline CPI, as against the expected 0.1% decline. Meanwhile, annual inflation fell from 4.2% to 3.5%, below the expected 3.8%. The decline was primarily attributed to declining energy prices.

US Bureau of Labor Statistics data show the energy index declined 5.7% in June, its largest decline since April 2020, when gasoline prices fell by nearly 10%. Meanwhile, Core CPI remained unchanged, but was 2.6% higher than last year.

However, energy prices are 15.7% higher than last year, while gasoline prices are up 26.7% over the same period. This could push household expenses even higher if oil prices remain high for the rest of the month.

Renewed Geopolitical Headwinds

Oil prices have spiked after another flare-up in the Middle East following an attack on Saudi oil tankers. Iran has also blockaded the Bab el-Mandeb Strait through the Houthis, a route Saudi exporters rely heavily on since the restrictions in the Strait of Hormuz. Reuters has reported a drastic decline in Iranian oil exports, which fell from 2 million barrels per day to nearly zero during the ongoing conflict. Goldman Sachs analysts also issued a dire warning, telling Reuters Brent could cross $120 if the ongoing disruptions continue.

Diplomatic efforts have also stalled, with US Secretary of State Marco Rubio accusing Iran of being unwilling to negotiate while maintaining Washington remained committed to negotiations. US and Iranian military activity also increases the risk of damaging crucial oil infrastructure.

Fed Meeting Takes Center Stage

Focus now shifts to the Federal Open Market Committee (FOMC) meeting, scheduled for July 28 and 29. Rising oil prices could influence the Federal Reserve’s decision on interest rates. Policymakers believe one report is not sufficient to establish a downward trend.

Governor Chris Waller had said after the June report that the Fed needed to see several months of softer data before it could establish that inflation was moving towards its 2% target. Analysts expect the Fed to maintain its target range at 3.50%-3.75%.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

Senate Democrats are mounting a fresh push to rewrite the CLARITY Act’s ethics provisions after dismissing the White House-backed proposal unveiled by GOP senators, according to Politico.

Senator Ruben Gallego blasted the latest draft and said that the proposal Republicans sent back was “not a serious effort” despite months of bipartisan negotiations.

Dispute Deepens in Senate

At the center of the dispute is how to prevent President Donald Trump from profiting from digital assets. Democrats insist they cannot support ethics rules that are enforceable only by the Department of Justice. Negotiations involving Gallego, Senators Cynthia Lummis and Bernie Moreno, and the White House ultimately collapsed over whether state attorneys general should also have authority to enforce the provisions.

In an interview on Thursday, Gallego said,

“I can’t imagine that that’s a serious effort – after all the work that we’ve done with our Republican colleagues, that they would take the months and months of work and somehow interpret that and turn around and think what they offered was even remotely close.”

Gallego added that he is now working with Senator Thom Tillis and other unnamed Republicans on a counterproposal, while insisting, “We are still in this fight.”

Lummis defended the proposal while Tillis said the White House-approved language was “good,” but acknowledged that further changes may be necessary to secure the 60 votes needed to advance the legislation. Tillis added that another round of discussions with the White House is expected to determine whether additional revisions would be “acceptable” to the president.

The disagreement has also put the bill’s timeline in doubt. Senate Majority Leader John Thune said that he no longer expects the Senate to pass either the CLARITY Act before lawmakers leave for the August recess.

Hopes that the CLARITY Act could provide the US crypto industry with long-awaited regulatory clarity have been one of the factors supporting bullish expectations for the market this year. However, prediction market odds of the bill’s passage declined amid disagreements over ethics provisions and other issues that have slowed negotiations.

Middle Ground

Coinbase CEO Brian Armstrong recently warned that parts of the company’s business could move overseas if the US fails to pass clear crypto legislation. While Coinbase wants to keep most of its operations in the country, the exec said regulatory clarity is needed to prevent capital, businesses and users from shifting offshore.

Amid the ongoing standoff, crypto commentator Crypto Sensei recently proposed a compromise to break the deadlock. In a recent post on X, he suggested keeping the DOJ as the primary enforcer while imposing statutory deadlines for investigations, creating an independent ethics review body to oversee DOJ decisions, and allowing state attorneys general to intervene only under limited conditions if the DOJ fails to act.

He also called for annual disclosures detailing ethics complaints, investigations, and enforcement actions for greater transparency.

The post Dem Senator Slams GOP’s CLARITY Ethics Proposal as ‘Not a Serious Effort’: Report appeared first on CryptoPotato.

Crypto markets showed renewed signs of life this week as institutional investors fueled the longest streak of inflows into US spot Bitcoin exchange-traded funds (ETFs) since April and crypto-linked stocks rallied on optimism over US regulation. But the more intriguing story may be unfolding outside crypto: AI’s grip on speculative capital is beginning to loosen.

After dominating markets for nearly two years, the AI trade is becoming more selective as investors distinguish between companies with sustainable earnings and those riding the hype cycle. The Philadelphia Semiconductor Index, or SOX, recently slipped into a technical bear market after falling 20% from its recent high, although it remains well above year-ago levels.

Some analysts believe the shift could mark the beginning of a broader rotation back into digital assets. While it’s too early to call a lasting trend, improving regulatory clarity, a recovery in ETF demand, and easing enthusiasm for AI are creating a more constructive backdrop for crypto than investors have seen in months.

Bitcoin ETFs post six-day inflow streak as market sentiment improves

US spot Bitcoin ETFs extended their inflow streak to six consecutive trading days, attracting $203.1 million in fresh capital as institutional demand showed tentative signs of recovery.

The latest inflows brought the six-day total to roughly $930 million, marking the funds’ longest winning streak since April as Bitcoin briefly climbed above $67,000. The renewed demand coincided with improving market sentiment, with the Crypto Fear & Greed Index recovering from “extreme fear” to “fear.”

Since launching in January 2024, US spot Bitcoin ETFs have attracted $51.8 billion in cumulative net inflows and now hold $80.9 billion in net assets, although they remain down $4.84 billion on a year-to-date net flow basis. Analysts said Bitcoin needs to hold above the $65,000-$65,500 range to strengthen the case for a sustained bullish breakout.

Crypto rally gains momentum as AI trade shows signs of cooling

The rally in Bitcoin and broader digital asset markets coincided with progress on US crypto legislation and a cooling AI trade, fueling expectations that capital may be rotating back into crypto.

The broader crypto market rallied alongside crypto-related stocks, with Coinbase, American Bitcoin and Cipher Digital posting double-digit percentage gains. Sentiment brightened after US Treasury Secretary Scott Bessent said lawmakers were at the “1-yard line” on the CLARITY Act, legislation that would establish a regulatory framework for digital assets.

Analysts also pointed to fading momentum in AI equities as another potential catalyst. FRNT Financial CEO Stephane Ouellette said that slowing enthusiasm for AI stocks and growing confidence in the interest-rate outlook could support a breakout in Bitcoin. The SOX Index, a benchmark for AI chipmakers, had recently fallen more than 20% from its recent high after concerns over elevated valuations and AI infrastructure spending.

AI infrastructure deals drive rally in Bitcoin mining stocks

Bitcoin mining stocks surged after Hut 8 and IREN unveiled multibillion-dollar AI infrastructure agreements, reinforcing the sector’s lucrative shift toward data centers and cloud computing as digital asset markets continued to struggle.

Hut 8, IREN, Cipher Digital, CleanSpark and MARA Holdings each gained after Hut 8 announced a 15-year, $9.8 billion lease for its AI data center campus and IREN disclosed $2.8 billion in cloud services contracts with AI developers. The deals underscore how miners are diversifying beyond Bitcoin production as mining economics become more challenging, with IREN now projecting more than $4 billion in annual recurring AI cloud revenue by the end of 2026.

While investors have rewarded the AI pivot, analysts say it also raises new questions around execution and funding. Blocksbridge Consulting estimates the sector will require roughly $50 billion in additional capital to achieve its AI ambitions, even as insider stock sales have drawn increased scrutiny.

The TEM AI Infrastructure Growth Index. Source: The Energy Mag

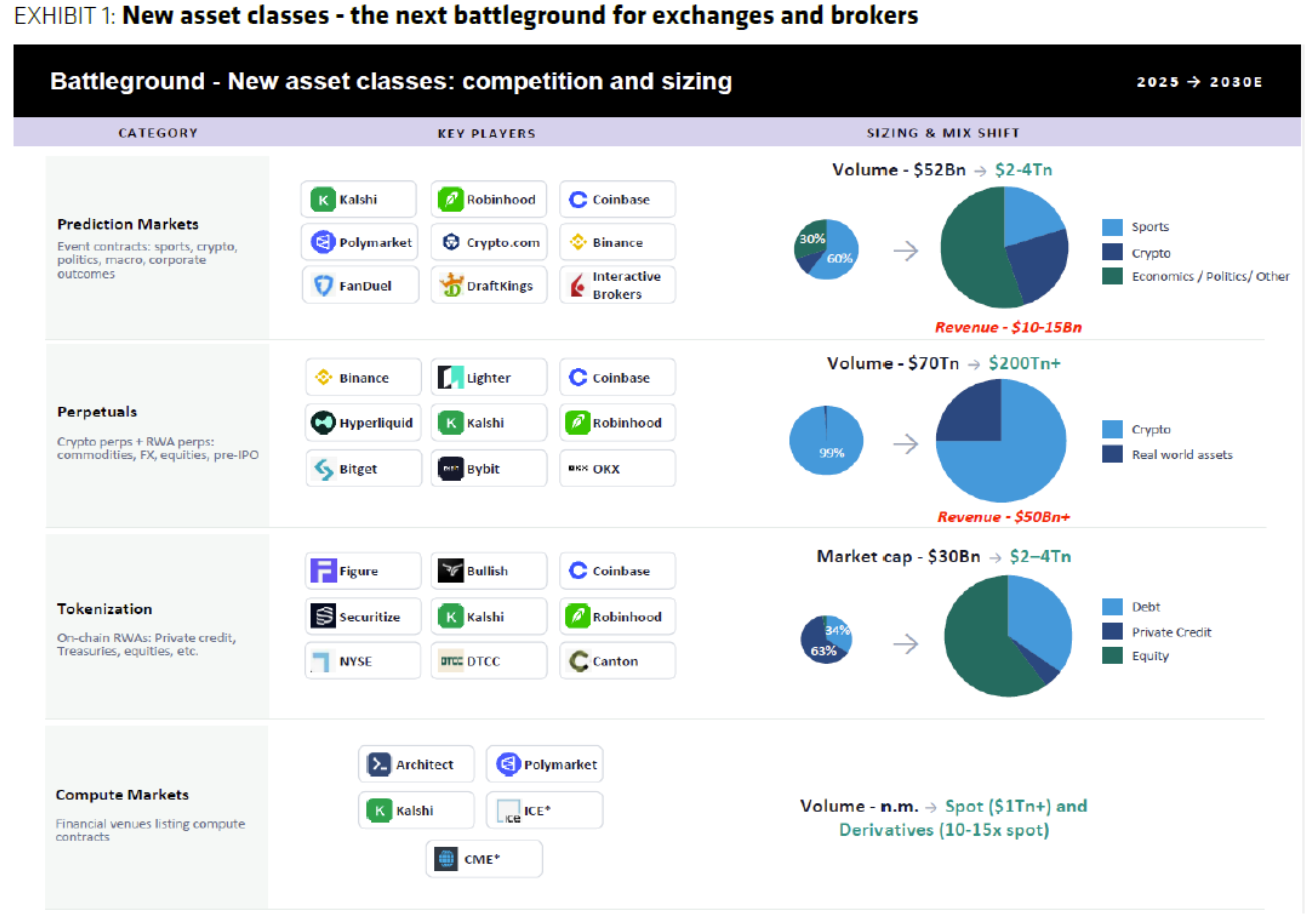

Bernstein sees tokenization, prediction markets driving Robinhood’s next growth phase

Bernstein raised its price target on Robinhood, arguing the brokerage’s long-term growth will be fueled by tokenized assets and prediction markets rather than traditional crypto trading.

The investment firm increased its price target on Robinhood shares to $160 from $130 while maintaining an Outperform rating. Analysts forecast prediction markets will become the company’s fastest-growing business, generating $1.7 billion in revenue by 2028. Bernstein also identified tokenized equities as a major growth opportunity, citing Robinhood’s Arbitrum-based layer-2 network as key infrastructure for bringing real-world assets onchain.

The bullish outlook comes as Wall Street accelerates its tokenization push, with companies such as Broadridge, Alpaca, Securitize and Cantor Fitzgerald expanding blockchain-based securities infrastructure.

Bernstein identified prediction markets, perpetual futures and tokenized equities as key competitive battlegrounds for Robinhood. Source: Bernstein

Crypto Biz is your weekly pulse on the business behind blockchain and crypto, delivered directly to your inbox every Thursday.

GMP using ‘existing resources’ to guard No 10 North as ‘talks underway over long-term security funding’

VGLT: Avoiding Long-Duration Treasuries At Present Despite Higher Yields (NASDAQ:VGLT)

3 Altcoins That Could Reach New All-Time Highs This Weekend

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread – Corporette.com

-

Politics6 days ago

Politics6 days agoThe House | The City of London can help the new chancellor deliver growth in every postcode

-

Crypto World6 days ago

Crypto World6 days agoRipple Payments Joins MiCA With 14 Firms, Does It Mean Anything For XRP?

-

Politics5 days ago

Politics5 days agoDemocrats look to World Cup watch parties to register thousands of voters

-

Crypto World7 days ago

Crypto World7 days agoRipple wins EU-wide access as ESMA adds it to MiCA register

-

Crypto World3 days ago

Crypto World3 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

Tech4 days ago

Tech4 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

NewsBeat4 days ago

NewsBeat4 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Tech4 days ago

Tech4 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

News Videos5 days ago

News Videos5 days agoBig Money Is Entering XRP

-

Business3 days ago

Business3 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Crypto World6 days ago

Crypto World6 days agoKaspersky exposes OkoBot’s 20-module crypto wallet attack

-

Business7 days ago

Business7 days agoAirlines warn Sunshine Protection Act could disrupt flight scheduling

-

Entertainment3 days ago

Entertainment3 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

NewsBeat7 days ago

NewsBeat7 days agoDurham County Council to send out electoral registration emails

-

Crypto World7 days ago

Crypto World7 days agoMiCA Licensing Faces Delays as ESMA Adds 14 CASPs to Register

-

Crypto World2 days ago

Crypto World2 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

NewsBeat4 days ago

NewsBeat4 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Crypto World6 days ago

Crypto World6 days agoChip Stocks Enter Bear Market After Moonshot Ai Unveils Kimi K3 Model

-

Tech4 days ago

Tech4 days agoWatch Flock Safety CEO Garrett Langley discuss the future of surveillance at TechCrunch Disrupt 2026

You must be logged in to post a comment Login