Crypto World

Ripple builds a $3.5B empire as XRP sinks toward the $1 mark

In the last week of June, XRP printed its weakest price since late 2024, briefly touching $1.01 before stabilizing in the $1.05 to $1.13 range where it has traded through early July. The token is down more than 25% for the year and roughly 65% below the $3.65 cycle high it set in July 2025. On the same June days that the chart broke down, tokenized real-world assets on the XRP Ledger crossed $3.5 billion, more than triple the level at which they started the year, spot XRP exchange-traded funds extended a net inflow streak that would reach eight consecutive weeks, and Ripple stood weeks away from full European authorization under MiCA.

Summary

- Ripple has delivered record institutional growth in 2026, but XRP remains more than 25% lower this year and near multi-year lows.

- The article examines both sides of the debate: whether Ripple’s expanding infrastructure will eventually lift XRP or whether the company and token have permanently diverged.

- Upcoming CLARITY Act votes, ETF flows, XRPL upgrades, and institutional adoption could determine whether the gap between Ripple and XRP finally closes.

That is the whole story in one paragraph, and it is genuinely strange. By any operational measure, the 12 months behind Ripple are the most productive in the company’s history: a settled SEC case, launched ETFs, a $1.25 billion prime brokerage acquisition, membership in the clearing infrastructure of American equities, a stablecoin with $18 billion in quarterly transfer volume, and regulatory licenses stacking up on three continents.

By the only measure most holders care about, the same 12 months are the worst since the 2022 bear market. The gap between what Ripple built and what XRP is worth has never been wider, and how that gap closes, upward through the price or downward through the narrative, is now the central question hanging over the fourth largest ecosystem in crypto.

This feature lays out both sides honestly: the case that the infrastructure eventually drags the token up, and the case that the token and the company have simply decoupled, with the price telling the truer story.

The year Ripple built: an inventory

It helps to see the accumulation in one place, because no single item explains the disconnect. The pattern does.

Legal closure came first. The SEC’s enforcement case against Ripple, filed in December 2020, formally concluded in 2025 with a financial settlement, ending the overhang that had defined the token’s American existence for half a decade and building on the 2023 court finding that programmatic exchange sales of XRP were not securities transactions.

Then distribution. Spot XRP ETFs launched in November 2025 across 5 providers and have accumulated roughly $1.49 billion in cumulative net inflows since. May 2026 was the strongest month of the year with $118 million, including a record $60.5 million week.

The streak ran 8 consecutive weeks into July, as crypto.news reported, before showing its first daily pauses, and assets under management sit near $1.05 billion, about 1.5% of the token’s market capitalization, led by Bitwise at $331 million, Canary at $265 million, and Franklin at $262 million.

Then market plumbing. Ripple closed its acquisition of prime broker Hidden Road in October 2025 and rebranded it Ripple Prime. On March 2, 2026, Ripple Prime joined the participant directory of the National Securities Clearing Corporation, placing an XRP-linked institution inside the DTCC complex that clears the bulk of American equity trading and safeguards roughly $100 trillion in assets. DTCC has since named Ripple Prime to the working group of more than 50 firms shaping its tokenization service for Russell 1000 stocks, ETFs, and Treasuries, scheduled for October 2026.

Then the ledger itself. XRPL tokenized assets grew from $991 million on January 1 to $3.5 billion by midsummer. In early May, JPMorgan, Mastercard, Ondo Finance, and Ripple completed the first cross-border tokenized US Treasury redemption on the XRPL, settling in under 5 seconds. Daily transactions hit 3 million on March 15, roughly three times mid-2025 averages.

A protocol amendment from XRPL version 3.1.0 that would enable fixed-term lending through Single Asset Vaults is under validator vote, and support has been climbing toward the 80% supermajority it needs, a governance process crypto.news has tracked as it approaches the threshold.

Then the stablecoin. RLUSD reached a $1.72 billion market capitalization in under a year, moved more than $18 billion in the first quarter alone, and Ripple hedged the strategy in July by joining Open USD, the consortium dollar token backed by Visa, Mastercard, Stripe, BlackRock, and more than 140 other companies.

Then the licenses. A full Electronic Money Institution approval from Luxembourg in February, UK Financial Conduct Authority permissions in January, and the full MiCA Crypto-Asset Service Provider license on July 6 that opened all 30 countries of the European Economic Area, arriving days after the transition deadline locked unlicensed competitors out of the bloc.

Any one of these, delivered into the 2024 market, would have produced a rally measured in double digits. Delivered into 2026, the entire list produced a chart that goes down and to the right.

The year XRP traded: an autopsy

The price ledger is shorter and harsher. XRP closed 2025 near $1.90 after the July peak at $3.65, rallied to about $2.40 in the new year, then spent 2026 in decline: a sharp February selloff that prompted Standard Chartered to cut its year-end target from $8 to $2.80, a spring of lower highs between $1.28 and $1.50, a June that opened near $1.30 and closed near $1.04, and a July that has been a daily fight to defend the $1 line.

The token trades below every major moving average, with the 20-day near $1.11, the 50-day near $1.20, and the 200-day near $1.52. Relative strength readings in the low 30s mark the deepest oversold territory of the cycle.

Two facts about the decline matter for interpreting it. First, it was market-wide. Bitcoin fell from above $100,000 to below $62,000, briefly touching $58,000. Ethereum, Solana, and BNB fell comparably or worse; total crypto market capitalization shed $2.3 trillion over 8 weeks, and digital assets posted a third consecutive losing quarter, the longest streak since 2022, as institutional capital rotated toward AI equities. Everything outside Bitcoin and Ethereum lost roughly 23% in 6 months. XRP’s beta to that drawdown was high, as it always is, because the token falls harder than Bitcoin when sentiment turns.

Second, and more uncomfortable for the bull case, none of the good news interrupted it. The full MiCA license produced a 3% weekly decline around the preliminary approval and indifference at the final one. The DTCC milestone passed without a candle. The Treasury redemption pilot with JPMorgan, arguably the most institutionally significant event in XRPL history, is invisible on the chart.

The one catalyst the market visibly responds to is legislative: the token jumped 4.5% within an hour of the CLARITY Act clearing committee on May 14, and it sagged when the July 4 signing target slipped, price action crypto.news examined as the delay sank in. The market has, in effect, told everyone what it is waiting for, and it is not another license.

What the forecasters did with the same facts

The professional forecasting record around XRP in 2026 is itself evidence of the disconnect, because analysts looking at identical data have produced the widest dispersion of targets for any large-cap asset.

Standard Chartered entered the year at $8 for 2026 and cut to $2.80 in February after the selloff, a 65% downgrade in a single revision, while explicitly leaving its 2030 target untouched at $28. The bank’s stated logic was that regulatory clarity, institutional involvement, and new investment products justify higher long-term valuations, but near-term price action would remain correlated with the broad crypto market. That is the lag thesis and the beta thesis coexisting in one research note.

Bitwise carries a $4.94 year-end forecast. JPMorgan’s contribution is conditional rather than directional: $4 to $8.4 billion of first-year ETF inflows if the CLARITY Act passes, with no comparable estimate under failure. Algorithmic models cluster far lower, in the $1.70 to $2 band, essentially extrapolating the chart. The professional consensus for year-end sits above $2, which would require a 77% rally from current levels in under 6 months, a move the asset has produced before but only during regime changes in sentiment.

Forecast dispersion this wide is unusual for an asset of this size, and it maps precisely onto the two readings of the disconnect. Analysts weighting the infrastructure see multiples of the current price; models weighting the tape see the current price as fair. When the same inputs produce a $1.70 answer and a $28 answer depending on the discount rate applied to institutional adoption, the market is not confused. It is unpriced, waiting on the one variable, classification, that neither the company nor the chart can supply.

The bear reading: the token and the company are different assets

The uncomfortable thesis deserves its full strength. Ripple’s success and XRP’s value are linked by a mechanism, and the mechanism is thin.

Ripple the company earns revenue from payments, custody, prime brokerage, and stablecoin float. Almost none of that revenue requires the XRP price to be anything in particular. The company’s own announcements make the point unintentionally: the MiCA license release mentions XRP essentially once, in the boilerplate.

Ripple Payments has moved more than $100 billion across 60-plus markets, but most of that volume settles in fiat or RLUSD, and where it does route through the XRP Ledger, the burned fee per transaction is a fraction of a cent. 3 million daily transactions at those rates destroys token supply at a pace measured in rounding errors. The stablecoin strategy, on this reading, actively competes with the bridge-asset story that once justified the token: every corridor that settles in RLUSD is a corridor that does not need XRP volatility risk.

Supply mechanics deepen the skepticism, and they deserve their own accounting. Ripple releases up to 1 billion XRP from escrow every month under a schedule set in 2017, relocking the majority into new escrow contracts while a smaller portion enters circulation through sales and ecosystem distributions. The market has watched this metronome for years, and its psychological weight exceeds its mechanical weight: even in months when net new supply is modest, the release event itself gives traders a recurring reason to expect selling, and expectations of supply function like supply. Set the monthly release against the demand side and the imbalance is stark. The entire ETF complex has absorbed roughly $1.49 billion over 8 months, an average of around $6 million of daily buying, in a token that trades north of $1.4 billion in daily volume.

Institutional flows at that scale can support a floor; they cannot fight a distribution schedule and a bear market simultaneously. The bear case does not need Ripple to fail. It needs only for the demand mechanisms to keep growing slower than the supply mechanisms, which is a fair description of every month of 2026 so far.

There is also the exchange migration to consider from the skeptical side. Tokens leaving exchanges for ETF custody are commonly read as bullish scarcity, but a share of that movement is simply the same speculative holders changing wrappers, retail selling spot that funds buy into trusts, with no net new demand created. The flow data cannot distinguish conviction from repackaging, which is why the bears discount it. The comparison Brad Garlinghouse himself invited when he attacked Michael Saylor’s leverage model cuts both ways, as crypto.news observed: both Strategy and Ripple sit atop enormous token treasuries whose value depends on a market they are simultaneously supplying.

On this view, the 2026 chart is not a mispricing. It is the market correctly concluding that owning XRP is not owning Ripple, that the institutional build-out accrues to Ripple’s private shareholders, and that the token’s fair value is whatever speculative demand plus modest utility demand will bear in a risk-off tape. The disconnect is not a gap waiting to close. It is the honest spread between an equity story and a token story that were never the same story.

The bull reading: infrastructure is demand with a lag

The counterargument does not deny any of that. It argues the causality has a delay measured in years, and that 2026 is the trough of the lag, not the verdict.

Start with the demand channels that did not exist 18 months ago. ETFs holding $1.05 billion sound small against a $69 billion market cap until you note the direction and the constraint: 8 straight weeks of net inflows through the worst quarter since 2022, from a buyer base that is still legally capped. Pension funds, sovereign wealth funds, and most insurance portfolios cannot allocate to an unclassified asset at all.

That is precisely the constraint the CLARITY Act removes by making XRP a digital commodity under CFTC oversight, and it is why JPMorgan and Standard Chartered independently project $4 to $8.4 billion in first-year inflows under passage, a 5- to 8-fold expansion of the current ETF base. The bill’s merged draft is due the week of July 13, with floor action targeted a week later. The single largest catalyst in the token’s history has a date range attached to it.

Second, the utility story is finally measurable instead of theoretical. Tokenized assets tripling to $3.5 billion, a functioning institutional redemption pilot with the largest bank in America, a lending protocol approaching validator approval, and RLUSD volume in the tens of billions are all activity that lives on the ledger whose native asset is XRP.

The fee-burn mechanism is tiny per transaction, but the investment case was never fee burn; it is that reserve requirements, liquidity provisioning, and settlement paths on a busy institutional ledger create structural demand for the asset that denominates it. Japan already offers the proof of concept, where SBI’s remittance corridors made the country the one place XRP is used at scale in production, a story crypto.news has documented, and Europe post-MiCA is the first market since Japan where Ripple holds the full regulatory stack to attempt a repeat.

Third, the on-chain footprint of conviction is visible even at the lows. Whale accumulation ran through the spring, with roughly 450 million XRP moving through Binance in a 10-day stretch in March, wallet creation hit a 3-month high near 5,000 per day in late June, and large-holder balances rose while retail sentiment collapsed. Someone with size is treating $1 as a level to buy, and the historical pattern in this asset is that accumulation phases at multi-month lows precede the violent repricings the token is famous for. July, for what it is worth, is historically XRP’s strongest month, averaging around 10% gains, though seasonality in a fear-gripped market deserves limited weight.

The bull synthesis: the company spent 2026 building the pipes, the law that fills them sits 3 weeks from a vote, and the price is a coiled spring compressed by macro conditions that have nothing to do with Ripple. Standard Chartered, even after cutting its 2026 target to $2.80, left its 2030 target at $28, which is the lag thesis expressed as a forecast.

The map of the battlefield at $1

For traders, the disconnect compresses into a few price zones that both camps agree on even while disagreeing about everything else.

Support is a dense band between $1.00 and $1.06, where a thick concentration of historical buying has absorbed every test since late June, including seven separate probes of the $1.04 to $1.06 area. Beneath it, the map goes dark: a decisive daily close below $1 opens territory the token has not traded since 2024, with the next meaningful demand zone estimated between $0.80 and $0.90. The bounce attempts of early July have built a sequence of higher lows above $1.03, and the immediate breakout zone sits at $1.056 to $1.066, where a surge of volume, at one point 1,400% above the hourly average, marked the strongest buying of the month.

Resistance begins where the moving averages live. The 20-day average near $1.11 and the descending channel midline have capped every rally attempt; above that, $1.18 to $1.20 is the zone that separates a technical bounce from a trend change, since it contains the 50-day average and the highs of the last failed breakout. A move through $1.20 would be the first structural repair of the year. The level that matters for the larger argument is further up: analysts broadly treat $1.65 as the line above which the downtrend that began at $3.65 would formally be broken.

The holder structure beneath those levels is where the two theses interact most directly. Exchange balances have been falling as tokens migrate to ETF custodians and cold storage, whale addresses have grown through the decline, and the retail cohort, measured by funding rates and sentiment indexes reading extreme fear, is maximally absent.

That configuration, shrinking liquid supply against a depressed price, is the classic setup for violent moves in both directions: thin order books amplify whatever catalyst arrives. A CLARITY passage into this structure would meet little overhead supply until the mid-$1.20s. A failure into this structure would find equally little bid support below $1. The market has arranged itself for an outsized reaction to a binary event, which is rational, because that is exactly what the calendar is offering.

What would actually settle the argument

Disconnects resolve through evidence, and four specific markers will decide which reading was right.

The CLARITY floor vote before the August 7 recess is the binary. Passage activates the constrained buyer base and converts the classification question from risk to fact; failure removes the identified catalyst and hands the bear thesis another year of confirmation. Nothing else on this list matters as much.

XRPL settlement disclosures are the slow variable. Europe will produce client announcements through the fall; the tell is whether named institutions settle on the ledger or through RLUSD and fiat rails that bypass the token. Every disclosure is a data point for exactly the mechanism the two camps dispute.

ETF flow behavior around the $1 level tests the institutional bid. The first net outflow day arrived on June 30 as the quarter closed. If inflows resume through a flat tape, the allocation story survives the drawdown. If outflows follow the price down, the ETF base was momentum money wearing an institutional costume.

The lending amendment vote tests whether the ledger’s institutional roadmap ships. Validator support has been grinding toward the 80% threshold; activation would open uncollateralized fixed-term credit through Single Asset Vaults, the first XRPL primitive aimed squarely at the institutional DeFi demand the bull case requires.

One more marker sits outside the token entirely: Ripple’s own capital decisions. The company has explored an initial public offering intermittently, and hints have circulated that XRP holders might somehow participate in a listing. Nothing concrete has emerged, and nothing should be assumed, but the scenario clarifies the stakes of the disconnect better than any chart.

If Ripple lists, the market will finally price the company and the token side by side, in public, every trading day. Either the equity valuation validates the institutional story and drags attention back to the ledger that underpins it, or investors will buy the company and continue ignoring the token, at which point the decoupling thesis stops being a thesis and becomes a quote on two screens. The company has every incentive to make the token matter before that comparison goes live.

For holders, the practical takeaway is about position sizing against a calendar, not about conviction in either narrative. The next 26 days contain the merged CLARITY draft, a possible floor vote, the July escrow release, continuing ETF flow data, and the validator vote on the lending amendment. That is an unusual density of resolution for a single month. The disconnect between Ripple’s year and XRP’s year has been stable precisely because nothing forced the two stories to reconcile. The Senate schedule is about to force it.

The widest gap in crypto right now is not between any two tokens. It is between a company having its best year and a token having its worst, wearing the same three letters. Markets close gaps like this one eventually, and they are indifferent about the direction. 26 days of Senate calendar will supply the first, and probably decisive, piece of the answer.

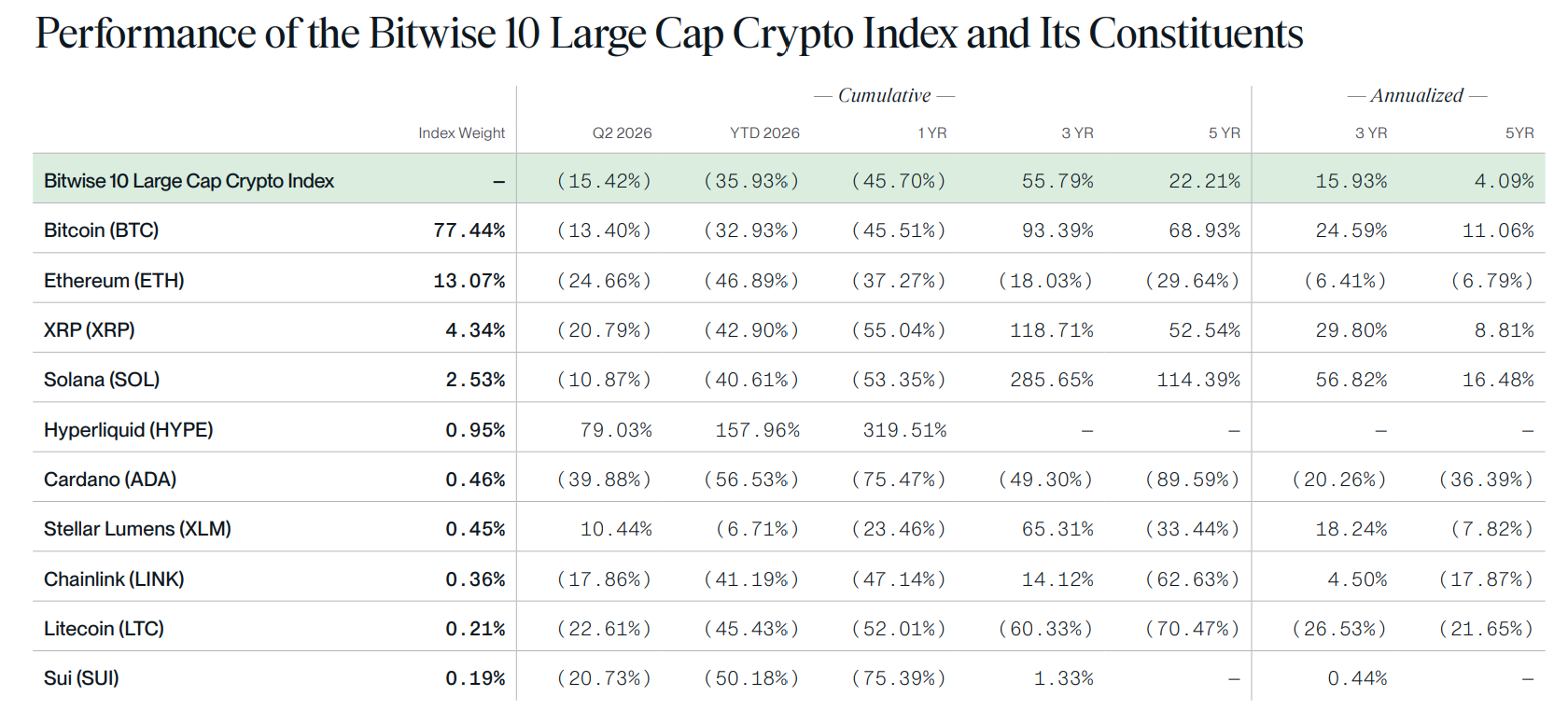

Stablecoin volume hit a record $1.79 trillion in June, even as the tokens’ total supply shrank. The split captures a market pricing crypto for a downturn while its usage keeps climbing.

A Bitwise report, Visa’s on-chain data, and new ownership figures point the same way. Stablecoin transfers and prediction markets hit records even as the Bitwise 10 Large Cap Crypto Index fell 15.4%.

Prices Fell, But the Plumbing Kept Growing

The second quarter was crypto’s third straight losing quarter, the longest run since 2022. Spot Bitcoin (BTC) exchange-traded funds posted their worst quarter of outflows. On-chain activity and trading volume slipped.

Yet the Bitwise report argues the market has it backwards. Crypto is being priced for a bear market, it says, even though the industry is roughly twice its 2022 size. Deeper liquidity and more institutions now sit on-chain.

The gap shows up in the fundamentals. Measured against the 2022 low, Ethereum (ETH) transaction activity is up about 13 times. Value locked in decentralized finance has climbed more than 60%, and stablecoin assets have roughly doubled.

Prices still lagged. The flagship crypto index fund lost ground, with eight of its 10 holdings in the red.

That divide has reopened the question of whether the market has already found the bear market bottom.

Stablecoin Volume and Derivatives Led the Quarter

Stablecoins settled about 2.3 times Visa’s payment volume over the past year, Bitwise said. In June, transfers reached the $1.79 trillion record, according to Visa Onchain Analytics. Rising institutional stablecoin volume kept settlement near all-time highs.

A shrinking stablecoin supply once signaled trouble. Terra’s 2022 collapse erased tens of billions and froze the market. This time supply eased while transfers set a record, a very different backdrop.

USD Coin (USDC) handled about two-thirds of that volume. Regulated dollars are taking share as institutions lean in.

Trading told a similar story. June spot volume across major exchanges fell roughly 5% from May, while derivatives volume rose about 4%. Active traders stayed engaged even as casual buyers stepped back.

Tokenized Assets and Prediction Markets Set Records

Tokenized real-world assets climbed 50.3% this year to $32.89 billion, the report said. Prediction market volume hit a record $43.2 billion in the quarter, close to 18 times its level a year earlier.

Crypto equities held up too. The Bitwise Crypto Innovators 30 Index rose 30.6%. Apps such as Hyperliquid, PancakeSwap, and Aave each earned close to $900 million in revenue over the past year.

Advisers increasingly favor stablecoins and tokenization over direct Bitcoin bets. Individuals still hold about two-thirds of Bitcoin supply.

However, institutions and funds bought roughly 829,000 BTC in 2025, while retail wallets shed about 696,000, according to River.

Bitwise framed the split between price and progress as the setup for the next cycle.

“That foundation won’t stop the winter, but it determines what grows in the spring,” Matt Hougan wrote.

The next few quarters will test whether usage pulls prices up or weak prices sap momentum. For now, the data shows an industry still growing while its market value waits to catch up.

The post Crypto Bear Market? These Reports Say the Industry Has Never Been Stronger appeared first on BeInCrypto.

Jito has proposed a governance overhaul that would direct 100% of the DAO’s JTX revenue share toward open-market JTO buybacks and permanent token burns through at least Q4 2027.

Summary

- Jito has proposed using DAO revenue for JTO buybacks and permanent token burns through Q4 2027.

- JIP-38 would place most protocol revenue under DAO control, with JTO holders governing allocations.

- JTO rose as much as 8% after the governance proposal was unveiled, according to crypto.news.

According to a governance proposal published by Jito on July 13, the protocol has introduced JIP-38, which would formally classify Jito as a token-centric network where nearly all major network revenue flows to the decentralized autonomous organization and remains under the control of JTO token holders.

The proposal triggered an immediate market reaction, with Jito (JTO) climbing as much as 8% shortly after its release, according to data from crypto.news.

Revenue would be redirected to JTO holders

Under JIP-38, Jito proposes using the DAO’s entire share of JTX revenue to buy JTO tokens on the open market before permanently removing those tokens from circulation. According to the proposal, this arrangement would remain in place for at least one year, extending through the fourth quarter of 2027.

One exception remains in the framework. The proposal states that 20% of JTX platform fees would continue to be reinvested into JTX development rather than being allocated to buybacks and burns. Jito said the remaining major revenue streams would continue flowing through the DAO under governance controlled by JTO holders.

To carry out the program, the proposal calls for buybacks to be executed automatically through a Rev Splitter mechanism overseen by the project’s Dev Council. Alongside the automation process, Jito plans to update its governance documentation so the protocol’s operating model formally recognizes the token-centric structure.

According to JIP-38, existing revenue allocation commitments would be completed before a comprehensive review of protocol fee streams takes place in Q4 2027.

During that review, governance participants would evaluate the performance of token buybacks, ecosystem incentives, and other capital allocation methods before JTO holders vote on the network’s next long-term revenue framework.

Governance changes extend beyond token burns

Beyond the buyback program, JIP-38 outlines several operational changes intended to support the new revenue structure. According to the proposal, the Rev Splitter would become progressively more automated while governance records would be updated to match the revised economic model.

Jito also stated in the proposal that the framework is designed so value generated across the network accrues to the JTO token instead of external corporate entities. Any future changes to revenue allocation after Q4 2027 would require approval through governance voting by JTO holders.

The proposal arrives as Jito continues expanding its presence across the Solana ecosystem. Earlier this year, as previously reported by crypto.news, 21Shares launched the 21Shares Jito Staked SOL ETP (JSOL) on Euronext Amsterdam and Euronext Paris.

The issuer said the product provides regulated exchange-traded exposure to Solana through JitoSOL while embedding staking rewards, allowing investors to access the asset through traditional brokers and banks without managing wallets or staking infrastructure.

Institutional support for the protocol has also grown over the past year. As previously reported by crypto.news, Andreessen Horowitz’s (a16z) crypto division invested $50 million in Jito to help expand the Solana staking protocol’s ecosystem.

The investment included an allocation of JTO tokens to the venture firm, adding another high-profile backer as the protocol seeks approval for its latest governance proposal.

Strategy has raised $466.7 million through fresh MSTR stock sales while leaving its Bitcoin holdings unchanged at 843,775 BTC for the week ending July 12.

Summary

- Strategy raises $466.7 million through MSTR stock sales.

- Company keeps Bitcoin holdings unchanged at 843,775 BTC.

- Standard Chartered maintains $100,000 Bitcoin target despite treasury concerns.

According to a Form 8-K filed with the U.S. Securities and Exchange Commission (SEC), Michael Saylor-led Strategy sold 4,818,781 Class A MSTR shares between July 6 and July 12 through its at-the-market (ATM) program, generating approximately $466.7 million in net proceeds. Despite the capital raise, the company reported that it did not purchase or sell any Bitcoin during the reporting period.

The filing showed Strategy continued to hold 843,775 BTC, acquired for about $63.69 billion at an average purchase price of $75,476 per Bitcoin, excluding fees and expenses. Following the latest issuance, the company still has roughly $23.79 billion available under its MSTR ATM stock program.

Strategy keeps Bitcoin holdings unchanged after recent sale

Fresh SEC disclosures also showed Strategy held approximately $3 billion in U.S. dollar reserves as of July 12. According to the filing, the cash is intended to cover preferred stock dividends and interest payments on the company’s debt. The reported balance also includes expected proceeds from ATM share sales that had not settled by the reporting date.

The company further disclosed that it did not repurchase any shares under its existing buyback programs during the same week.

The latest filing follows Strategy’s $216 million Bitcoin sale disclosed the previous week, only the second BTC sale in the company’s history. At the time, the company said the proceeds would be used to fund dividends tied to its STRC preferred stock and other digital credit securities. After that transaction, Strategy’s Bitcoin balance fell to 843,775 BTC, where it has remained through the latest reporting period.

Earlier reports also noted that Strategy has authorization to sell up to $1.25 billion worth of Bitcoin under its BTC Monetization Program, a development that has drawn close attention from market participants even though the company has not announced additional BTC sales.

Standard Chartered says treasury uncertainty drove recent weakness

Attention around Strategy’s Bitcoin plans increased after Executive Chairman Michael Saylor posted the company’s familiar Bitcoin acquisition chart on July 12 with the message, “Orange dots tell only part of the story.” As crypto.news reported earlier, the post did not confirm whether Strategy had bought, sold, or held Bitcoin during the latest reporting week.

Crypto.news also noted that Strategy’s public Bitcoin tracker continued to show 843,775 BTC, matching the latest SEC filing. The company typically reports treasury activity through regulatory filings, meaning social media posts do not establish whether a transaction has occurred or indicate its direction.

The latest disclosure comes as Bitcoin has climbed back above $64,000 after Standard Chartered reaffirmed its $100,000 price target for the end of 2026. In a research note, the bank said recent weakness in Bitcoin was driven largely by uncertainty surrounding Strategy’s evolving treasury approach rather than by any deterioration in Bitcoin’s underlying fundamentals.

Standard Chartered added that the recent pullback should not be interpreted as a change to its long-term bullish outlook for the cryptocurrency.

Reed Smith, the global law firm with more than 30 offices across North America, Europe and Asia, has introduced an automated compliance platform aimed at helping crypto firms prepare for the European Union’s Markets in Crypto-Assets (MiCA) regime as oversight intensifies. The tool, called “Aquarius,” is designed to streamline parts of the MiCA workload while keeping legal review integrated into the process.

Reed Smith says Aquarius can automate tasks such as crypto-asset classification, regulatory white paper generation, due diligence workflows and environmental, social and governance (ESG) disclosures. The firm also plans to extend the platform to other compliance environments beyond the EU, including the United Kingdom, the United Arab Emirates, Hong Kong and Singapore.

Key takeaways

- Reed Smith’s Aquarius platform targets MiCA implementation by automating classification, documentation, due diligence and ESG disclosures.

- The rollout comes as the EU moves deeper into full MiCA enforcement following the end of the July 1 transition period.

- Even with harmonized rules, authorization and ongoing supervision—especially for custodians—remain operationally demanding.

- Policymakers are also discussing possible changes to MiCA’s stablecoin framework, including rules for non-euro-denominated issuers.

Aquarius aims to reduce compliance friction as MiCA matures

MiCA is intended to create a consistent licensing and rulebook for digital asset service providers across the EU’s 27 member states, covering areas such as consumer protection and operational requirements. Reed Smith’s stated goal with Aquarius is to make entry into the European market—or expansion within it—more manageable by combining automated workflows with legal expertise.

The timing is notable. Earlier this month, the EU’s MiCA transition period ended on July 1, after which firms could no longer rely on temporary national exemptions tied to countries that had previously adopted longer grandfathering arrangements. For companies that had planned compliance in phases, the end of that window effectively tightened the deadline pressure and increased the urgency to demonstrate readiness under the full framework.

For operators, this matters because MiCA compliance is not a one-time checkbox. Firms must be able to show they meet licensing criteria and operational expectations, and they must be prepared for ongoing regulatory attention as supervisory activities ramp up.

MiCA authorization is only the start for custodians

Even though MiCA harmonizes the regulatory landscape, authorization still appears challenging for many service providers. Last week, the European Securities and Markets Authority (ESMA) launched a supervisory review of authorized crypto-asset service providers. According to earlier reporting referenced in the source material, ESMA’s focus includes how custodians safeguard client assets and how they manage operational risks.

That emphasis aligns with industry concerns around the practical burden of compliance. Sebastien Dessimoz, co-founder and managing partner of Taurus (a digital asset infrastructure provider), is cited as saying that a MiCA license is “only the beginning” for custodians. He points to continued scrutiny over cybersecurity, governance and the ability to protect client assets—issues that do not end at the moment a firm receives authorization.

In other words, compliance strategy increasingly becomes a continual operational process: firms must maintain controls, demonstrate effectiveness over time and ensure that risk management keeps pace with both technology and regulatory expectations.

Potential stablecoin rule revisions add uncertainty for issuers

Beyond licensing, the regulatory picture may be shifting for specific segments of the market. Reports suggest that EU policymakers are considering revisions to MiCA’s stablecoin framework, particularly rules governing the issuance of stablecoins that are not denominated in euros.

As cited in the source material, Euronews attributes part of the impetus for the discussions to the United States’ GENIUS Act, which created a federal framework for payment stablecoins. While the details of any EU changes were not specified in the source excerpt, the implication for market participants is clear: stablecoin issuers may need to plan for evolving requirements, especially where cross-border regulatory influence could reshape how issuers are classified and supervised.

For companies preparing documentation, disclosures or product roadmaps, this type of policy uncertainty can materially affect timelines and internal sign-offs—particularly if compliance artifacts must be updated to reflect shifting interpretations or amended standards.

Why automated compliance tools are gaining attention

Reed Smith positions Aquarius as a way to combine standardized processes with legal oversight, targeting repetitive and documentation-heavy steps that can slow down onboarding and expansion. If implemented effectively, automation could help reduce time-to-readiness by making it easier for firms to assemble core compliance outputs—such as classification materials, regulatory white paper drafts, and due diligence documentation—before legal teams finalize and validate them.

At the same time, automation does not eliminate the underlying regulatory obligations. The ESMA supervisory review referenced in the source underscores that regulators are looking beyond initial submissions to real-world custody practices, operational controls and risk management behavior.

Readers should watch how platforms like Aquarius are used in practice: whether firms treat automation as a way to build defensible compliance packages and then continuously monitor operations, or whether they simply accelerate paperwork without improving the controls supervisors expect.

As MiCA supervision expands and stablecoin-specific discussions continue, the next phase of compliance will likely be defined by two tracks: ongoing custody and operational scrutiny from regulators, and potential adjustments to stablecoin rules that could ripple into disclosures and product structures. Firms should monitor both developments while validating that their compliance systems can adapt quickly as requirements evolve.

Google Gemini AI just framed Bitcoin current price position as a coiled spring rather than a broken asset. The model predicts $120,000 to $150,000 by the end of 2026, treating the current $64,000 level as the exact setup that precedes a major liquidity break.

The bull case is built on 3 compounding forces rather than a single catalyst. Bitcoin sits near $64,000 today, and the model opens by describing the setup as coiled for a major liquidity break, which is a specific framing that implies the move will be fast and sharp rather than gradual once it begins.

Compounding spot ETF inflows are the first force, with institutional demand continuing to absorb supply at a pace that steadily reduces what is available on the open market.

Expanding corporate treasury adoption is the second force, with more companies following the Strategy playbook and treating Bitcoin as a core balance sheet reserve rather than a speculative bet.

The third force is a favorable macroeconomic shift toward global rate cuts, which loosens liquidity conditions and pushes capital toward higher returning assets as cash yields decline.

Together these 3 forces are described as institutionalizing Bitcoin as a core macroeconomic asset, which continues to dry up liquid supply and sets the stage for a supply shock rally over the next 18 months.

The model does not pin everything on a single legislative event or exact timing window, instead treating the structural forces already in motion as sufficient to push price toward that $120,000 to $150,000 target by year end.

The bear case is the starkest downside scenario in any Bitcoin prediction covered in this series. If persistent regulatory friction or a broader global recession triggers aggressive risk off liquidation across traditional markets, the model sees a structural breakdown toward $40,000 to $45,000.

That bear case is notably more severe than the $55,000 to $60,000 floors named in most other predictions in this series, reflecting how seriously Gemini treats the tail risk of a genuine macro shock rather than just a crypto specific pullback.

Bitcoin Price Prediction: BTC Quietly Builds A Base While The Market Waits For The Next Liquidity Break

The daily chart shows Bitcoin at $64,135 after a recovery off the June lows near $58,000 that has been building steadily over the past 2 weeks.

Price has pushed back above $64,000 on this candle, which is the highest close since late May and represents a series of higher lows forming since the June bottom.

That pattern of higher lows combined with relatively consistent green sessions is the most encouraging technical development this chart has shown in months. Resistance sits first at $68,000, the level that capped multiple push attempts throughout May and June, with a much heavier ceiling near $80,000 where the most extended rally of 2026 ultimately stalled.

The $40,000 to $45,000 bear case floor sits well below current price but is not so remote that it can be dismissed, given how far Bitcoin has already fallen from its October highs near $127,000.

Support holds at $59,000, the most recent cycle low that was tested and held in late June. The broader structure still shows lower highs stretching all the way back to October, meaning the dominant downtrend has not reversed on any technical basis yet.

Momentum on the daily candles looks constructive and improving, with the past week delivering some of the cleaner green closes seen anywhere on this chart since the April rally attempt.

The supply shock framing Gemini uses fits what the chart is showing in one important way, price is not breaking down despite sustained selling pressure over many months, which suggests a floor may genuinely be forming. A clean break and hold above $68,000 would be the first real signal that the coiled spring Gemini is describing has finally started to release.

Here is What Gemini AI Predicts About LiquidChain

Most people will only see this rotation in hindsight. The smart money has already moved.

Large caps are not failing. They are out of room. Bitcoin, Ethereum, and XRP keep pressing against the same ceilings with nothing breaking through. Every macro tailwind has a new arrival date. Every institutional wave lands next quarter. Sitting in assets where the upside depends entirely on someone else’s decision is not a strategy. It is a waiting room.

Capital that has survived enough cycles knows one thing. It moves before the destination becomes obvious.

Early-stage infrastructure plays by completely different rules. A small market cap means that a modest rotation can produce dramatic price movement. The returns live in the gap between what something is genuinely worth and what the market has assigned it so far. That gap exists only while the project remains undiscovered. Once found, it closes permanently.

Multi-chain fragmentation is bleeding DeFi every single day. Bitcoin, Ethereum, and Solana exist as completely isolated systems. No native bridge between them. Every user crossing those boundaries absorbs the cost directly in fees, slippage, and failed transactions. Every single crossing. Every single time.

Gemini AI predicts LiquidChain fixes that entirely. All 3 networks within a single execution layer. One deployment reaches everything. Zero cross-chain tax on any interaction.

The presale is at $0.01454 with just over $890,000 raised. The market has not found this yet. That is exactly the point.

Execution is unproven. Adoption is unknown. Established assets offer a predictable ride toward a ceiling everyone can already see. LiquidChain is an entry point that disappears the moment the market looks up.

The post Google Gemini AI Predicts Shocking Bitcoin Price by End of 2026 appeared first on Cryptonews.

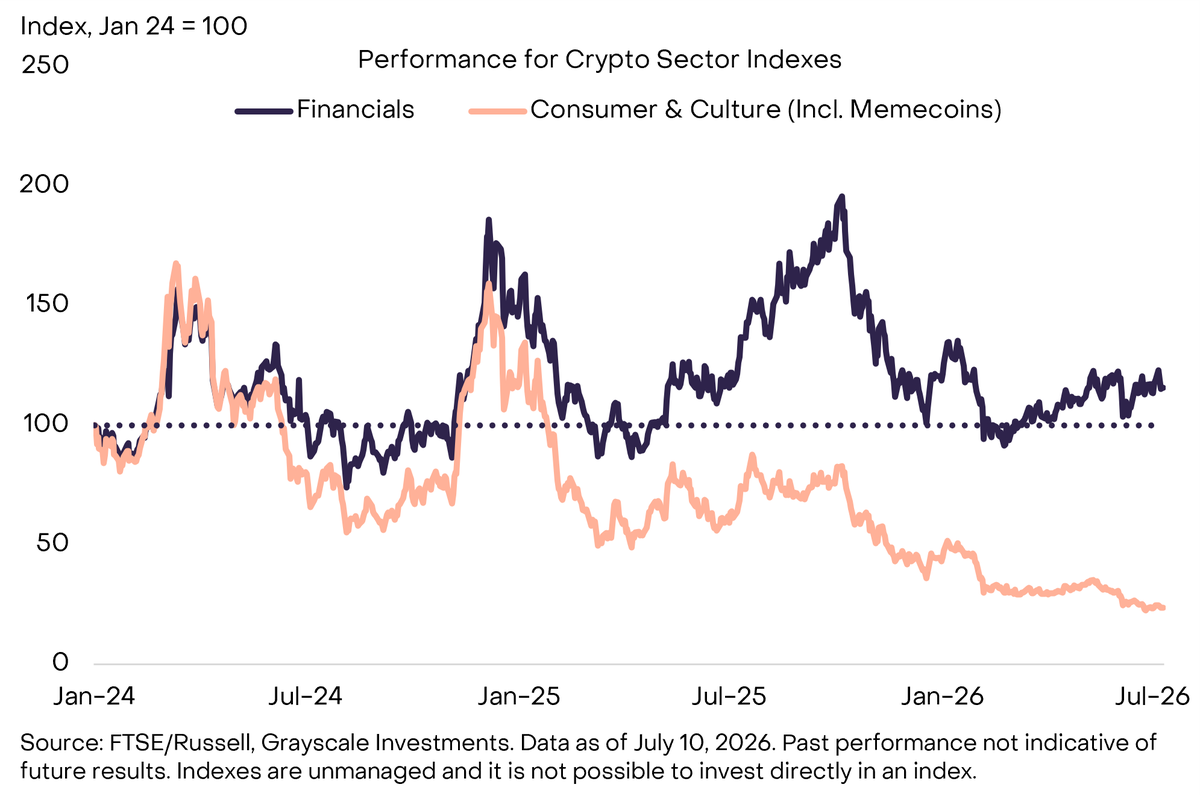

Grayscale says the crypto market is increasingly rewarding tokens with real fundamentals, and financial protocols led by Hyperliquid (HYPE) are pulling far ahead of meme coins.

The asset manager attributes the divide to a crypto bear market and rising institutional adoption. Both forces are separating revenue-generating projects from speculative tokens with little underlying value.

Why the Crypto Market Rewards Fundamentals Now

Grayscale built its case with its Crypto Sectors framework, a set of indexes developed with FTSE Russell. The system sorts more than 150 protocols by function and is reassessed each quarter. Grayscale’s recent research groups tokens by what they do, not the story around them.

Follow us on X to get the latest news as it happens

The Financials Crypto Sector covers protocols that deliver financial transactions and services on-chain. Their fundamentals track the adoption of stablecoins, tokenized assets, and other blockchain use cases.

Stablecoin settlement volume recently hit fresh records, reinforcing that demand. The gap widens in a downturn, when tokens without revenue fall hardest.

Hyperliquid Pulls Ahead as Memecoins Fade

Since the start of 2024, the Financials Crypto Sector has gained roughly 15%, while the Consumer and Culture Crypto Sector has fallen about 75%. That leaves financial tokens ahead of their consumer peers by about 90 percentage points.

By contrast, the lagging sector is dominated by meme coins like Dogecoin (DOGE), the 2013 original, which Grayscale says now make up around 85% of its market value.

Grayscale singles out Hyperliquid as the standout. The on-chain exchange routes trading fees into an assistance fund that buys back HYPE, tying the token’s value to actual platform usage.

Hyperliquid’s HYPE token has climbed from an all-time low near $3.81 in late 2024 to a June 2026 peak of $76.70. It traded near $63 on Monday, up about 29% on the year, and ranks 10th by market value.

“Crypto markets are rewarding tokens with strong fundamentals. These include Hyperliquid and other leading financial applications of blockchains,” Grayscale noted.

Some fund managers make the same case. Tushar Jain, chief investment officer of Multicoin Capital, says leading protocols should be judged like companies. His firm holds HYPE and sees Hyperliquid leading in on-chain derivatives.

“Solana is a business. Hyperliquid is a business. They are meant to go and generate cash flow, and that is the primary thing that gives those tokens value…” Jain said in a recent interview.

Other revenue-focused projects have leaned into the same shift, including a recent revenue-funded token burn. Whether that lead holds may hinge on consumer tokens building real income. For now, Grayscale’s data suggests fundamentals, not speculation, are setting the market’s winners apart.

The post Grayscale Says the Crypto Market Is Rewarding a Different Kind of Token appeared first on BeInCrypto.

Coinbase Ventures maintained its lead among crypto-focused venture capital investors in the first half of 2026, completing the most funding deals in CryptoRank’s dataset. The Coinbase exchange’s corporate VC arm recorded 30 deals from January through June, edging out Animoca Brands (19), a16z (18), and Tether (15), according to CryptoRank’s funding analytics.

While top investors kept showing up, the wider market remains under pressure. Total funding for crypto companies dropped to $1.4 billion in June, down from $3.8 billion in April—an indication that deal activity is still more fragile than headline counts alone suggest. Even so, July brought a modest rebound, with $456 million raised across 12 funding rounds so far.

Key takeaways

- Coinbase Ventures led deal counts in H1 2026 with 30 investments, followed by Animoca Brands (19), a16z (18), and Tether (15), per CryptoRank.

- Funding volumes remain depressed: June totals fell to $1.4 billion (down from $3.8 billion in April), alongside fewer rounds (61 in June vs. 89 in May).

- DeFi, payments, and AI dominate VC interest over the past year, collectively accounting for hundreds of fundraising rounds.

- Investor participation narrowed: unique investors fell to 242 in June from 452 in October 2025.

- Geography is uneven: US-based VCs led in capital deployed over six months, while a large share of funds came from undisclosed locations.

Coinbase Ventures stays on top as deal volume softens

Across the first half of 2026, the most active crypto-focused investors by number of deals were concentrated among a handful of firms. Coinbase Ventures’ 30 transactions placed it above Animoca Brands, a16z, and Tether in CryptoRank’s tally.

Looking beyond H1, CryptoRank data shows that Coinbase Ventures also remained highly active over the previous 12 months, completing 75 deals—more than any other listed contender. Animoca Brands followed with 40 deals, YZi Labs (formerly Binance Labs) with 39, GSR with 31, and a16z with 30.

Those sustained activity levels stand in contrast to softer market conditions. Crypto VC fundraising fell to $1.4 billion in June, down 63% from $3.8 billion in April. Deal counts declined as well: June saw 61 fundraising rounds, compared with 89 in May.

Still, the pattern is not uniformly downward. CryptoRank data indicates a slight recovery relative to earlier in the year: April’s totals included a two-year low of $698 million across 71 fundraising rounds, and June—while weaker than May—did not repeat that extreme low.

Where the capital goes: DeFi, payments, and AI lead

Crypto VC interest over the past year skewed heavily toward three categories: decentralized finance, payments, and AI-linked crypto initiatives. According to CryptoRank, DeFi protocols accounted for 216 fundraising rounds, payments startups logged 131 rounds, and AI-crypto companies raised through 128 rounds.

Infrastructure also remained a consistent focus. CryptoRank reports 110 funding rounds for infrastructure providers during the same period, while all other sectors recorded fewer than 100 rounds.

For investors and founders, this distribution matters because it suggests VC capital is still flowing toward applications and rails rather than exclusively chasing speculative narratives. Even during a period of reduced fundraising totals, the categories attracting the most rounds tend to have clearer product pathways—whether that’s enabling on-chain finance, improving transaction and settlement use cases, or integrating AI capabilities into crypto systems.

Shifts inside the portfolio: Coinbase Ventures’ thematic exposure

Coinbase Ventures’ participation over the last six months shows a thematic pattern aligned with broader market preferences, though with a degree of specificity. CryptoRank data indicates Coinbase Ventures took part in:

- Seven investment rounds linked to payment protocols

- Four rounds supporting DeFi projects

- Three rounds tied to infrastructure and real-world asset tokenization

That mix reflects a VC approach that emphasizes core crypto primitives and monetizable use cases. At the same time, the relatively small number of rounds in each subcategory (for Coinbase Ventures’ own activity) highlights that even top investors are not scaling uniformly—rather, they are selecting fewer bets while still covering key themes.

Fewer participants, different geography, and what to watch next

Even as deal counts remained steady for certain lead investors, the broader ecosystem saw reduced participation. CryptoRank shows the number of unique investors in June fell to 242 from 452 unique investors in October 2025. That contraction suggests a more selective capital environment: fewer players are deploying money, even if some large funds continue to originate deals.

Geography provides another lens on how VC behavior is concentrating. Over the past six months, US-based VCs contributed $5.8 billion, while Australia-based VCs deployed $3.6 billion. CryptoRank also reports that more than $11.6 billion was invested from undisclosed locations, underscoring how opaque parts of the fundraising landscape remain.

With July activity already showing $456 million raised across 12 funding rounds so far, the immediate question for market participants is whether this qualifies as a durable rebound or merely a short-term uptick. CryptoRank’s June-to-July movement suggests conditions can improve after declines, but the drop in unique investors—and the still-low June fundraising level versus April—signals that conviction and breadth in the VC market may take longer to fully return.

Sam Altman, ChatGPT AI, just put a clean number on SpaceX’s stock price prediction, treating the post-IPO pullback as the entry point rather than a warning sign. The model predicts $225 by year-end 2026, implying roughly 55% upside from where shares sit today, with $250 or more possible if growth accelerates.

The bull case anchors everything to a revenue figure that most investors have not fully processed yet. SpaceX generated $18.7 billion in revenue in 2025, with Starlink contributing approximately 60% of that total, meaning the satellite internet business alone produces more annual revenue than most mid-cap tech companies.

That combination of broadband, aerospace, defense, and AI infrastructure exposure in a single ticker is genuinely rare and is exactly what the model points to when justifying a premium valuation.

Starlink’s subscriber base keeps expanding with recurring revenue that grows more predictable each quarter. SpaceX maintains an unmatched launch cadence that no competitor has come close to matching. Starship continues making progress toward full reusability, and emerging AI infrastructure opportunities tied to satellite connectivity and compute at the edge are adding an entirely new growth layer on top of the existing business.

Together, those factors support renewed momentum after what the model frames as a natural post IPO pullback rather than a fundamental problem with the business.

The bear case names 3 specific risks rather than vague downside concerns. Major Starship delays would undercut the reusability thesis that justifies much of the long-term valuation premium. Continued pressure from AI infrastructure spending on profitability could squeeze margins faster than revenue growth can offset.

And investors rejecting a valuation that remains exceptionally high relative to current sales is the simplest and most immediate risk, since SpaceX went public at a valuation that already priced in years of future growth. Under that scenario, the model sees shares drifting toward $110 to $120 instead.

SpaceX Price Prediction: SpaceX Grinds Toward Its Post IPO Floor With A $225 Target Sitting Far Overhead

The 3-hour chart shows SpaceX at $145.35 after a sharp decline from IPO-week highs near $219, set in mid-June.

That entire move from the IPO spike down to current levels has taken less than a month, which is the kind of violent post IPO repricing that happens when early momentum buyers take profits and retail enthusiasm collides with the reality of a stock priced for perfection.

Price has been grinding lower in a series of lower highs since that June 17 peak, with each bounce attempt setting a new lower high before rolling back over again.

The most recent sessions from July 8 through 10 have been particularly weak, with the stock losing ground steadily and now trading near its lowest level since the IPO opened.

Resistance sits first near $155, the level that capped the most recent bounce attempt in early July, with a heavier ceiling near $173, where the post-peak consolidation zone lived for several days before breaking down. Support holds near $145, the current test zone, and the lowest level this stock has traded since going public.

Below that, no clear technical floor exists on this chart since the IPO history is too short to establish meaningful prior support. The overall pattern here is a classic post IPO distribution, with the stock spending every day since the initial spike working off excess early enthusiasm rather than building any kind of base.

Momentum looks weak and still pointed lower on the 3-hour candles, with sellers maintaining control throughout the most recent trading sessions. For the $225 bull case to become technically relevant, SpaceX first needs to stop making lower highs, reclaim $160, and hold it through a stretch of earnings-driven news flow that confirms the Starlink revenue trajectory the model is relying on.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

LiquidChain Is Catching the Attention of SpaceX holders: ChatGPT AI Predicts It’s the Next 100x

The rotation is already happening. Most people will only see it in hindsight.

Large-cap crypto is not failing. It is capped. Bitcoin, Ethereum, and XRP have been pressing against the same resistance bands for weeks. The macro tailwinds keep getting delayed.

The institutional inflows keep getting pushed to next quarter. Holding assets where the upside depends on catalysts you cannot control is not a strategy. It is waiting.

A capital that has navigated enough cycles does not wait at resistance. It moves before the destination becomes obvious.

Early-stage infrastructure plays operate on different math entirely. A small enough market cap means a modest rotation produces dramatic price movement. The asymmetry exists because the market has not priced in what is being built yet. That gap between current valuation and what the project is actually worth is where the returns come from.

Multi-chain fragmentation costs DeFi real money every single day. Bitcoin, Ethereum, and Solana run completely isolated liquidity systems with no native way to connect them. Every user moving value between ecosystems absorbs that cost directly in fees, slippage, and failed transactions.

LiquidChain collapses all 3 networks into a single execution layer. One deployment. Full ecosystem access. No cross-chain tax on every interaction.

The market has not found this yet. That is the entire point.

The presale is at $0.01454 with just over $820,000 raised. Ground floor is not a marketing phrase here. It is a description of where this actually sits in its lifecycle.

Execution is unproven. Adoption is unknown. Those risks are real and worth naming directly. Established assets offer a smoother ride toward a ceiling that is already visible. This offers an earlier seat at a table that has not been set yet.

Explore the LiquidChain Presale

The post Sam Altman ChatGPT AI Predicts Insane SpaceX Stock Price by End of 2026 appeared first on Cryptonews.

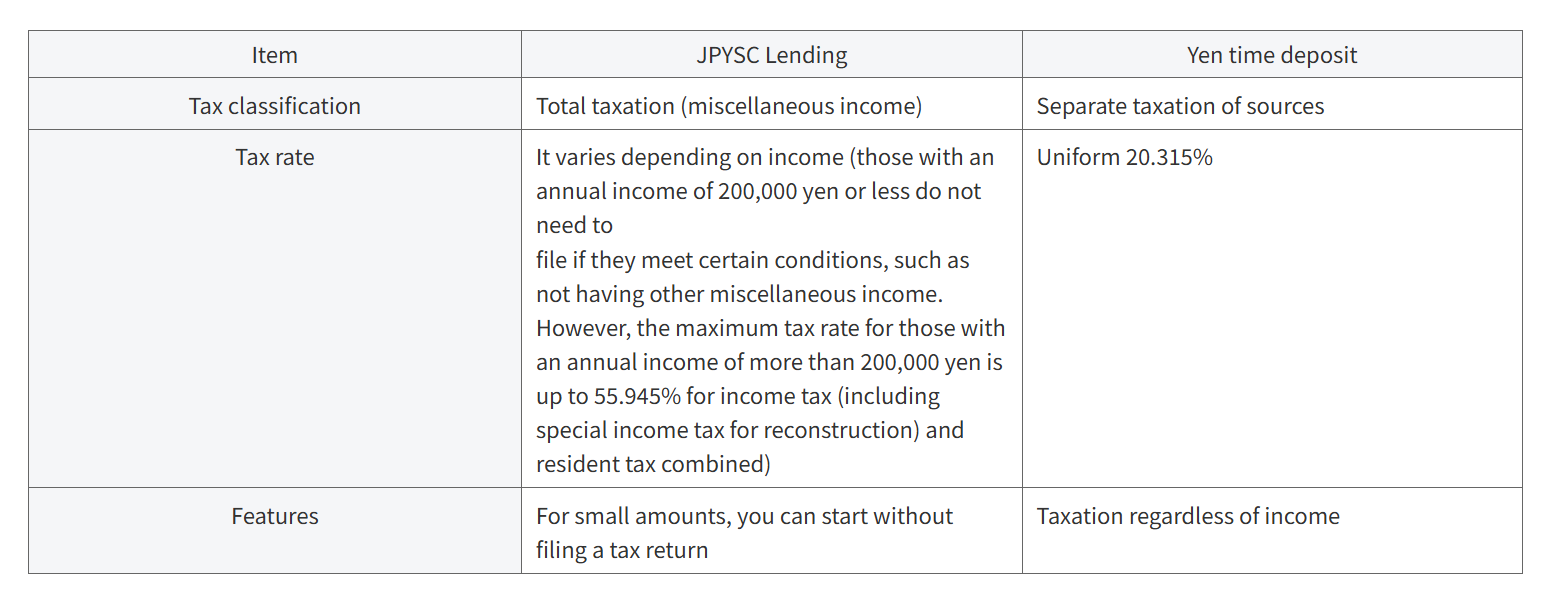

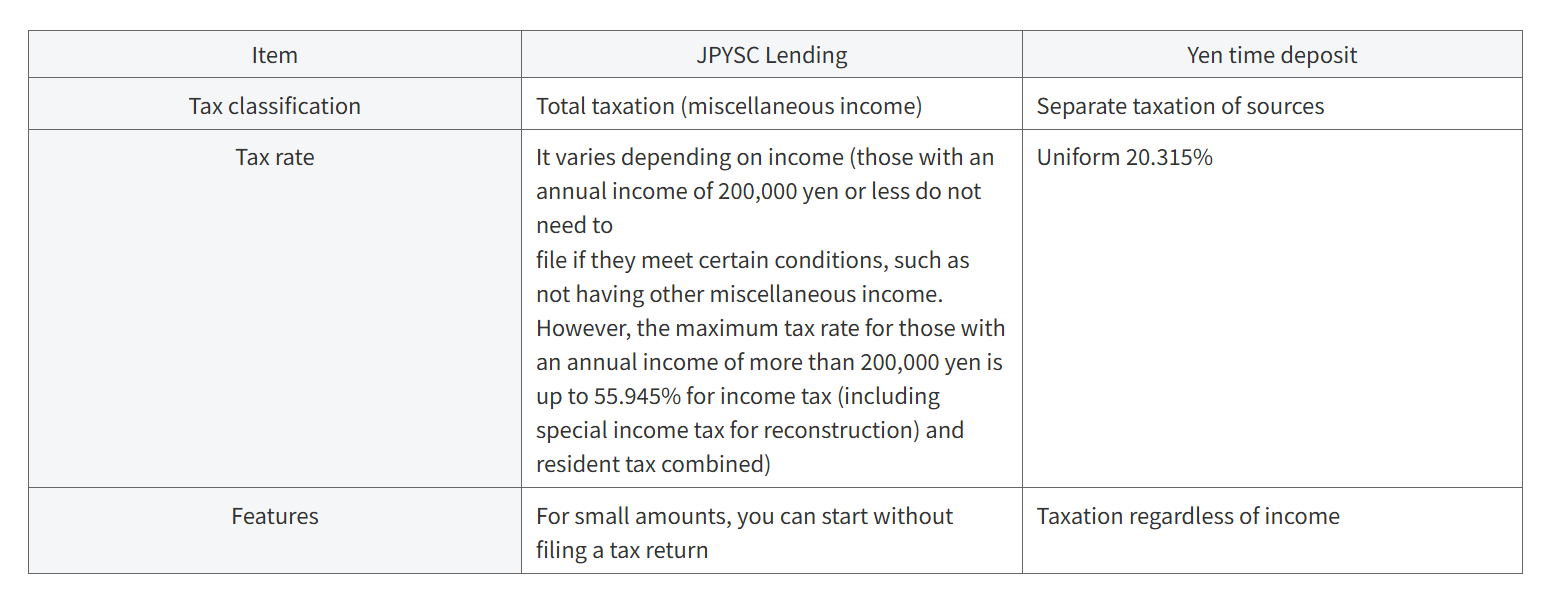

Tokyo-based SBI VC Trade will begin accepting applications Thursday for a Japanese yen-denominated stablecoin lending service offering an initial annualized rate of 3% on JPYSC lent for 12 weeks.

Customers will lend JPYSC to the SBI Holdings subsidiary from Thursday and receive the tokens back with a lending fee at maturity, the company said in a Monday press release. At the advertised rate, the gross return over the 12-week term would be about 0.69%, before tax.

The company said the product pays more than the 0.325% to 1% annual rate SBI cited for ordinary yen deposits. Still, it is not a bank deposit, is not covered by deposit insurance and generally cannot be canceled early.

JPYSC lent to SBI VC Trade will also fall outside statutory asset segregation requirements, meaning customers could lose some or all of their tokens if the company goes bankrupt, according to the release.

The launch gives JPYSC a new use case just weeks after SBI introduced the trust-structured yen stablecoin on June 24, with regulated stablecoins evolving from payments to yield-bearing instruments in Japan. SBI VC Trade previously launched stablecoin lending services in Japan in March for Circle’s dollar-denominated USDC (USDC) stablecoin.

SBI claimed this was the first service to allow Japanese customers to lend their yen-denominated stablecoins in exchange for passive yield.

By offering yields “exceeding” the typical annual rate for yen deposits, SBI anticipates an expansion among yen-denominated stablecoin holders and said the service will be “core” for realizing the future of onchain finance.

JPYSC lending service features. Source: sbivc.co.jp

Solana partnership widens onchain ambitions

SBI is separately building the infrastructure it hopes will eventually move JPYSC beyond its own platform and into a broader market for tokenized assets and cross-border settlement.

SBI Holdings announced a strategic partnership with the Switzerland-based Solana Foundation on Monday, aiming to build a Japanese onchain financial market.

As part of the partnership, the Solana Foundation will join SBI R3 Japan, which will be renamed SBI Solana Global and issue a new growth strategy focused on the yen-backed stablecoin.

The initiative aims to position Japan as a leading hub for onchain finance, while expanding stablecoins and tokenized real-world asset usage across Asia. It also includes building more infrastructure for institutional onchain financial services, cross-border payments and payment infrastructure for AI agents.

Related: Metaplanet explores Bitcoin-backed digital credit with JPYC in Japan

Japanese PM reaffirms support for crypto and Web3 startups: report

The stablecoin lending service’s launch follows positive regulatory signals for Japanese Web3 startups and cryptocurrency companies.

The Japanese government plans to strengthen support for crypto and Web3 startups, Japanese Prime Minister Sanae Takaichi reportedly said during a video address at the WebX 2026 conference.

Some of the promised measures include increased funding from government-backed funds and easing of regulatory requirements.

In May 2025, Takaichi introduced the “Startup Total Power Package,” which outlined policies tied to increased governmental funding to accelerate startups. The package builds on the “Five-Year Startup Development Plan” formulated in 2022, which aims to increase investments in startups to 10 trillion yen by the fiscal year 2027.

In April 2026, the Japanese government amended the Financial Instruments and Exchange Act to classify crypto assets as financial instruments, moving digital assets out of the experimental payments category into the same league as its stock market.

Magazine: Dubai tops Asian crypto hubs, Taiwan passes crypto laws: Asia Express

U.S. President Donald Trump has urged senators to move quickly on the Digital Asset Market Clarity (CLARITY) Act, framing the push as a tribute to the late Senator Lindsey Graham, who died over the weekend. The timing matters: the Senate is expected to be in session for only about four more weeks before a month-long August state work period, leaving a narrow window for any major legislation to clear.

Trump’s appeal, posted Monday on Truth Social, highlights Graham’s long-running support for the bill and calls on lawmakers to pass CLARITY “in honor of” the South Carolina senator. Graham, 71, served in the Senate since 2003. Following his death—and reports that another Republican senator, Mitch McConnell, is hospitalized—Republicans’ effective majority has narrowed to 51-47, raising the odds that the bill will need additional Democratic backing to reach the 60 votes typically required in the Senate.

Key takeaways

- Trump urged the Senate to pass the CLARITY Act, citing Lindsey Graham’s support before his death.

- The Senate’s working balance is tighter than before: Republicans are reported at 51-47, making bipartisan support more likely.

- CLARITY is expected to shift regulatory enforcement authority for parts of the digital-asset market from the SEC toward the CFTC.

- Many Senate Democrats have indicated they oppose the bill without additional ethics safeguards related to potential conflicts of interest.

- With only a few weeks left in the current session before August recess, lawmakers have limited time to resolve outstanding objections.

Trump ties CLARITY push to Graham’s legacy

In a Monday Truth Social post, Trump said Graham had been “a big supporter” of the CLARITY Act and called on senators to advance the legislation. The president also referenced the senator’s death, effectively urging legislators to treat the bill’s progress as a commemorative step.

Graham’s record with the CLARITY Act appears less direct than Trump’s framing suggests. In the current Congress, Graham is reported to have not served on the Senate banking committee or the agriculture committee, and he did not cast any votes advancing CLARITY. Cointelegraph previously reported that he did not appear to make public statements specifically supporting CLARITY during the current session. Still, he voted in favor of the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act in 2025, indicating he has supported certain crypto-related legislative efforts in recent years.

What CLARITY would change for crypto regulation

The central policy bet behind CLARITY is a reallocation of regulatory oversight. The bill is expected to move much of the authority for enforcing digital-asset regulation from the U.S. Securities and Exchange Commission (SEC) to the Commodity Futures Trading Commission (CFTC). For market participants, that shift matters because it would likely change which regulator leads on enforcement posture, interpretations of market structure, and how compliance expectations are set.

However, the legislative path is not just about jurisdiction—it’s also about trust and process. Senate Democrats have previously signaled they are unlikely to support the legislation without provisions aimed at addressing possible conflicts of interest involving lawmakers and the crypto industry. Some lawmakers have pointed to Trump’s ties to digital asset-related projects, including his memecoin activity, as well as the family’s World Liberty Financial company, as part of the rationale for demanding ethics-related changes before they back the bill.

Earlier coverage from Cointelegraph noted that this ethics and conflict-of-interest debate is part of why the bill could face resistance on the Senate floor.

https://cointelegraph.com/news/ethics-democrats-market-structure-clarity-bill-markup

Senate math tightens as leadership and votes are tested

In practical terms, CLARITY’s chances depend on the ability to assemble enough votes quickly. With Graham’s death—and with Mitch McConnell reported hospitalized—Republicans’ current majority has been reduced to 51-47. That arithmetical squeeze increases the likelihood that Democratic support will be necessary to hit the 60-vote threshold.

Cointelegraph reports that it sought comment from the offices of Senators Tim Scott, Kirsten Gillibrand, and Angela Alsobrooks regarding Trump’s remarks but did not receive an immediate response.

Support from within the Republican ranks appears at least partially energized by Trump’s message. Senator Cynthia Lummis, in a Monday post on X, said she supported Trump’s comment and described Graham as “passionate about ensuring that American leadership stayed at the forefront of everything – including digital assets.” Cointelegraph also contacted Lummis’ office to request clarification about Graham’s position on digital assets, but received no immediate reply.

The clock is running before August recess

Even if sentiment shifts, lawmakers still face a calendar constraint. The Senate has around four weeks left in session before a month-long state work period in August. That limited schedule creates pressure to resolve both the political and procedural issues surrounding CLARITY—particularly the ethics concerns that have been signaled by Senate Democrats.

What remains uncertain is whether the bill can be moved fast enough to secure the additional votes required, and whether any amendments or guarantees on conflicts-of-interest questions can satisfy enough skeptics to reach the needed margin. Investors and builders watching U.S. crypto regulation will likely focus on whether the debate turns from jurisdiction alone to the specific standards Democrats demand—since that is where the most durable resistance appears to be forming.

For now, the key question is whether Trump’s public push—and the loss of a major backer—changes the Senate’s willingness to compromise on ethics provisions, or whether the vote count still stalls despite the political momentum. With the legislative window shrinking, the next developments from the Senate floor and committee actions will be the most important indicators of whether CLARITY is headed to passage or remains stuck in partisan friction.

Darlington’s Northern Lights choir celebrates summer concert

Conor McGregor Says He’s ‘Beyond Dark’ After Suspected Torn ACL Ends UFC 329 Comeback in 69 Seconds

Crypto Bear Market? These Reports Say the Industry Has Never Been Stronger

-

News Videos7 days ago

News Videos7 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Fashion5 days ago

Fashion5 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Tech7 days ago

Tech7 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Sports4 days ago

Sports4 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports6 days ago

Sports6 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Tech6 days ago

Tech6 days agoAnthropic brings Claude Cowork to mobile and web as usage data shows most users aren’t coding

-

Sports4 days ago

Sports4 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Sports6 days ago

We have punished the disrespect

-

Crypto World7 days ago

Crypto World7 days agoBinance lists Strategy’s STRC stock as company expands Bitcoin funding

-

Tech4 days ago

Tech4 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Tech7 days ago

Tech7 days ago9 Best Keyboards (2025), Tested and Reviewed

-

Business7 days ago

Business7 days agoEnbridge: AI Tailwind Priced In (Rating Downgrade)

-

Crypto World6 days ago

Crypto World6 days agoClaude AI Created Something Anthropic Never Designed

-

News Videos7 days ago

News Videos7 days ago“What’s going on?!” Carl Froch discusses Floyd Mayweather Jr financial issues

-

Crypto World6 days ago

Crypto World6 days agoNasdaq arthritis company holding Moshe Hogeg crypto hits all-time low

-

Entertainment7 days ago

Entertainment7 days agoTaylen Biggs Reveals The Celebrity She Dreams Of Interviewing

-

Crypto World7 days ago

Crypto World7 days agoMicrosoft Cuts 4,800 Jobs as Xbox Loses 3,200 Roles in Reset

-

News Videos5 days ago

News Videos5 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

Tech6 days ago

Tech6 days agoKeychron is stepping outside keyboards with a $349 Thunderbolt 5 dock aimed at power users

You must be logged in to post a comment Login