Crypto World

Ripple IPO and XRP holders: what you would get

Brad Garlinghouse said one word, “maybe,” and the XRP community heard a promise. Asked whether holders could get a piece of Ripple if it goes public, he nodded toward a “special arrangement.” This is what was actually said, what holders could realistically receive, and the downside almost nobody is talking about.

Summary

- Ripple chief executive Brad Garlinghouse said that “if and when” Ripple goes public, the company might do “something special” for XRP holders, then immediately added it was “not in the immediate term.”

- That hedged “maybe” was offered in response to a direct question, not volunteered as a plan, and he declined to commit to any mechanism such as a token buyback.

- Ripple and XRP are legally and financially separate assets: holding XRP grants no shares, no dividends, and no claim on Ripple’s corporate profits, and no bridge between the two currently exists.

- The mechanisms holders imagine, preferential IPO share access, long-term holding rewards, or tokenized Ripple equity, are all unannounced and face serious securities-law hurdles given XRP’s legal history.

- The overlooked risk is that a Ripple IPO could actually pressure XRP, by drawing institutional capital toward Ripple stock and pushing the company to monetize its escrow holdings to satisfy public-market investors.

One word from Ripple’s chief executive set the XRP community alight, and that word was “maybe.” Speaking on the “Crypto In America” podcast with journalist Eleanor Terrett, Brad Garlinghouse was asked the question XRP holders have wanted answered for years: if Ripple ever goes public, could the people who hold XRP get a piece of it. He did not say no. He gestured first at the indirect benefits Ripple already provides, then, pressed on whether the company would do something specific for holders in an initial public offering, he said, “Maybe, but that is not in the immediate term.”

That was the entire substance of it, a hedged possibility wrapped in a qualification, offered in answer to a direct question rather than announced as a plan. And yet within hours it had been clipped, shared, and reshaped across XRP social media into something close to a corporate commitment, with community members urging one another to “hold accordingly.” The gap between what Garlinghouse actually said and what the community heard is the real story here, because the difference between a hinted-at maybe and a planned reward is the difference between a reasonable hope and a misplaced expectation.

The reason the remark landed so hard is the situation it landed into. XRP holders have spent 2026 watching Ripple collect exactly the kind of institutional wins the community long predicted, settlements with JPMorgan, stablecoin launches with major partners, a steady drumbeat of bank deals, while the token itself has stayed pinned near a dollar and change, beneath every major moving average. That combination, corporate triumph paired with token stagnation, breeds a particular hunger: the sense that the wins are real but are somehow not reaching holders, and that some missing mechanism could finally connect the two. Into that hunger dropped Garlinghouse’s nod, and it did what a catalyst does in a starved market.

This piece separates the hope from the reality. It covers exactly what was said and the precise wording that matters, the crucial distinction between Ripple the company and XRP the token, the mechanisms a holder benefit could theoretically take and why each is harder than it sounds, why Ripple may not even go public soon, the indirect benefit Ripple genuinely does provide, and the downside almost nobody is discussing: that an IPO could actually work against XRP. The goal is the real picture, neither dismissing the possibility nor inflating it into the certainty the hype implied.

What Garlinghouse actually said

Precision matters here, because the entire community reaction rests on a few carefully chosen words, and those words were more conditional than the excitement suggested. Garlinghouse did not volunteer the remark; he was asked directly whether XRP holders could share in Ripple’s success if the company eventually launched an initial public offering. His first instinct was to point to the indirect benefit Ripple already provides, saying he hopes XRP holders feel they benefit from Ripple’s existence through the work the company does to grow the XRP ecosystem. Only when pressed on whether Ripple would do something specific for holders in an IPO scenario did he offer the line that ignited everything: “Maybe, but that is not in the immediate term.”

When pushed further on concrete mechanisms, including a possible token buyback, he declined to commit to any of them, pointing back instead to what Ripple already does for the ecosystem. So the full extent of the supposed promise is a “maybe,” qualified as not near-term, given in response to a direct question rather than offered as a plan, with no program described, no mechanism named, and no action committed to. The community heard “Ripple will do something special for holders.” What Garlinghouse actually said was closer to “maybe someday, if we go public, which is not happening soon.”

Those are not the same statement, and stacking the two conditionals reveals how far the exciting headline sits from anything concrete: a possible benefit, attached to a possible IPO, that he himself describes as not a priority. It is worth adding that days earlier, at an industry conference, Garlinghouse had been cooler still on the idea of going public at all, emphasizing that staying private gives Ripple flexibility. Read in that context, the podcast remark was a hint, not a plan and certainly not a promise. Any honest assessment of what holders would actually get has to begin from that fact rather than from the amplified version that spread online.

Ripple is not XRP: the distinction that decides everything

To understand why this question is so charged, and so easily misunderstood, you have to grasp a distinction that still confuses many people: Ripple and XRP are legally and financially separate assets, and owning one does not mean owning the other. Ripple is a private technology company that builds payment and liquidity products, some of which use the XRP Ledger. XRP is a cryptocurrency, the native asset of the XRP Ledger, which is a decentralized, open-source blockchain that Ripple does not control. Holding XRP gives you ownership of that token and nothing else.

It confers no shares in Ripple, no dividends, no voting rights, and no claim whatsoever on Ripple’s corporate profits or assets. The two are different things with different value drivers, and the price of one does not automatically move the other. That distinction is why the company-versus-token gap keeps resurfacing across Ripple’s 2026 story. Ripple can win institutional business, launch products, and deepen its corporate value without automatically delivering a direct benefit to XRP holders.

This separation is the foundation of the entire holder-payout question, because it means there is no existing structure, no dividend, no buyback mechanism, no holder-equity bridge, that currently connects Ripple’s corporate fortunes to the people who hold XRP. Any such benefit would require a deliberate corporate decision: Ripple choosing to extend something to holders of a token that is legally distinct from its stock. That is precisely what makes Garlinghouse’s “maybe” notable, because it gestures at the possibility of Ripple voluntarily building a connection that does not exist and is not required to exist. The community’s hope is that Ripple might someday decide to construct that bridge.

The reality is that no bridge exists today, none is planned, and the entire question is whether Ripple might ever choose to build one. Everything that follows, every imagined mechanism and every obstacle, flows from this single fact: a Ripple IPO would, by default, do nothing for XRP holders, because the token and the company are separate. Only an affirmative, deliberate choice by Ripple could change that. Until such a choice is announced, a holder payout remains speculation, not entitlement.

The mechanisms holders imagine

Once the “maybe” spread, the community began filling in the blank with specific mechanisms, and it is worth laying them out, because they define the range of what “something special” could plausibly mean. The most discussed idea is preferential access to IPO shares, an arrangement in which verified long-term XRP holders, or users staking on the XRP Ledger, would be granted priority subscription rights to buy into a Ripple offering at favorable terms before the general public. This is the version that most directly answers the community’s wish, because it would let XRP holders transition, at least partly, into Ripple shareholders. It would turn token loyalty into an equity stake.

A second imagined mechanism is a long-term holding reward, a community-based structure that would give some benefit to holders who have kept XRP for a defined period, rewarding loyalty without necessarily handing over equity. A third, more technically ambitious idea is tokenized Ripple equity: a blockchain-based representation of Ripple stock made available to eligible token holders, which would use the very tokenization technology the industry is racing to build in order to bridge the gap between Ripple shares and XRP. Some in the community have also floated the notion of an “equity-token-bound” proof of entitlement, a digital claim linking XRP holding to some future right in Ripple. Each of these would, in its own way, construct the bridge between Ripple equity and XRP holders that currently does not exist.

The crucial thing to hold in mind is that all of them remain imagined, not announced. Garlinghouse named none of them; he declined, in fact, to endorse any specific structure when asked. They represent the community’s wish list of what “something special” might be, not a menu Ripple has offered. The distance between a fan’s plausible idea and a company’s actual program is considerable, especially when the imagined benefit touches securities law, global compliance, investor eligibility, and the legal separation between Ripple equity and XRP.

Why each mechanism is harder than it sounds

The reason Garlinghouse spoke in hints instead of specifics is almost certainly that nearly every concrete version of a holder benefit collides with serious obstacles, and understanding those obstacles is essential to a realistic view. The largest is securities law, and it is a particularly sharp problem for XRP of all tokens. Linking a cryptocurrency’s holding to equity benefits raises exactly the kind of securities-law questions that defined Ripple’s long and costly legal battle, the years-long fight over whether XRP sales amounted to unregistered securities transactions. Building a formal bridge that rewards XRP holders with equity or equity-like rights risks recreating the very entanglement between the token and the company that Ripple spent years and enormous legal resources trying to separate.

The company would have to navigate that terrain with extreme care, because a poorly designed holder-benefit program could reintroduce the argument that XRP is a security tied to Ripple’s enterprise, which is the last thing Ripple wants. That is why the catalyst that matters more than the IPO is still statutory clarity from the CLARITY Act, not an undefined corporate reward. Federal clarity can strengthen XRP’s status without blurring the line between the token and Ripple equity. A holder-equity program, by contrast, could blur that line if designed carelessly.

Beyond securities law, the practical obstacles multiply. A preferential-share program would require verifying who is a genuine long-term holder, drawing cutoff lines that would inevitably be seen as arbitrary or unfair, and managing the identity and compliance machinery to do it at scale across a global, pseudonymous holder base. A holding-reward structure raises questions of how to fund it and how to avoid favoring large holders over small ones. Tokenized equity would face the full weight of securities regulation governing who can own and trade company stock, plus the technical and legal work of making a regulated equity instrument function on a blockchain.

Each mechanism, in other words, is not just a matter of Ripple deciding to be generous; it is a tangle of legal exposure, fairness problems, and operational complexity, any one of which could sink it. This is why the most dramatic interpretations of “special arrangement” are also the least likely. A sober reading has to weight the modest possibilities, a governance gesture, a symbolic recognition, or simply Ripple structuring its business so more value flows through XRP over time, far more heavily than the windfall the community imagined.

Why Ripple may not even go public soon

The entire holder-benefit scenario is downstream of a prior question that often gets lost in the excitement: will Ripple even go public at all, and if so, when. On this, Garlinghouse has been consistent and notably unenthusiastic. He has repeatedly described an IPO as not a priority, and his reasoning is grounded in the current state of the public markets for crypto companies. He has pointed to the underwhelming performance of crypto-related public listings, citing peers whose post-listing stock has struggled, and noted reports that at least one major exchange had delayed its own listing plans.

His view, in short, is that the public markets have not treated Ripple’s peers well, and that there is little reason to rush into that environment. He has also made a positive case for staying private, arguing that it preserves flexibility, including, he joked, the freedom to speak openly without lawyers drafting every word. This is not the posture of a company on the verge of ringing the opening bell. It means the holder-benefit question is built on a foundation that is itself uncertain: a possible reward contingent on an IPO that the chief executive describes as neither planned nor imminent.

That is the sense in which the whole thing is a maybe attached to a maybe. For an XRP holder weighing what they might receive, this is the most important practical point, because even the most generous imaginable holder benefit is irrelevant unless and until Ripple actually decides to go public. By Garlinghouse’s own account, that decision is not on the calendar. The community’s hope therefore rests on two sequential uncertainties: first that Ripple goes public, and second that, having done so, it chooses to extend something to holders it is under no obligation to help.

Either link breaking is enough to make the whole scenario evaporate. That is why the IPO hint should not be treated like a near-term catalyst, even if it tells holders something about how Ripple thinks about its community. The comment matters as a signal of openness, but it does not change the current legal structure, the current IPO timeline, or the current token economics. XRP holders should separate those categories carefully.

The indirect benefit Ripple already provides

Set against the speculation is Garlinghouse’s actual, stated position, which deserves a fair hearing because it is not a trivial argument: that XRP holders already benefit from Ripple’s existence, indirectly but intentionally. The foundation of this argument is a simple fact: Ripple is the largest single holder of XRP. That gives the company a stronger economic incentive than anyone else to increase the token’s value and adoption, because Ripple profits when XRP rises, just as holders do. Its incentives are genuinely aligned with holders, even without any formal program linking the two.

Every commercial partnership Ripple pursues, every payment corridor it opens, every institutional deal it closes, and every regulatory battle it fights is evaluated, at least in part, through the lens of how it drives XRP utility and liquidity. Garlinghouse’s framing is that this alignment is the real benefit, that Ripple’s entire strategy is built around making XRP the most useful, liquid, and trusted digital asset in payments and settlement, and that by growing the ecosystem it makes what holders own more valuable, even without a dividend or an equity link. That is where XRP’s actual utility remains central to the long-term case. The token’s real thesis has to rest on usage, liquidity, and settlement demand, not on implied ownership of Ripple.

Garlinghouse has pointed to concrete examples of this posture, including Ripple’s backing of XRP treasury companies such as Evernorth, which is working to build a large XRP treasury business with Ripple’s support, an effort Garlinghouse frames as helping XRP holders, the XRP community, and Ripple shareholders at the same time. This argument has genuine merit and should not be dismissed as spin. The company’s commercial work plausibly does increase XRP’s utility and demand over time, which is a real, if diffuse, benefit to anyone holding the token. The counterpoint, and the reason the “maybe” resonated, is that many in the community find this indirect alignment insufficient.

They want a concrete share of Ripple’s corporate success, not an incentive structure that may or may not translate into token-price appreciation. That dissatisfaction is precisely the nerve Garlinghouse’s remark touched. His indirect-benefit argument is, in effect, his answer to it: you already benefit, just not in the direct way you want. Whether that answer satisfies holders depends on whether Ripple’s wins eventually become visible in XRP demand rather than simply in Ripple’s corporate valuation.

The downside nobody mentions: an IPO could hurt XRP

Here is the part of the story that the bullish excitement almost entirely skips: a Ripple IPO is not unambiguously good for XRP, and there is a credible case that it could actively work against the token, at least in the near term. The first channel is competition for capital. Today, an institution that wants exposure to Ripple’s success has essentially one liquid way to get it: buy XRP, the token associated with the company’s ecosystem. If Ripple goes public, that changes.

Suddenly there is a direct way to own a piece of Ripple itself, a regulated equity that offers what a token cannot: potential dividends, audited financial transparency, ownership of the company’s actual assets and cash flows, and the compliance comfort of a listed stock. Faced with that choice, institutional capital that might have flowed into XRP as a proxy for Ripple could instead flow into Ripple stock, siphoning off the very institutional demand the XRP bull case depends on. The IPO, in this reading, would give the market a cleaner instrument for the Ripple thesis, and XRP could lose its role as the default vehicle for it. That is the uncomfortable side of where XRP trades while holders wait: the market wants direct token demand, not merely a story about Ripple’s corporate success.

The second channel is selling pressure from Ripple itself. As a private company, Ripple has long been criticized for selling XRP from its large escrow holdings, a persistent source of new supply. After an IPO, that pressure could intensify instead of ease, because a public company answers to Wall Street’s quarterly demands for cash flow and profitability. To satisfy those demands and bolster its financial reports, Ripple’s board could face strong incentives to monetize tens of billions of XRP from its escrow accounts in a more systematic and aggressive way, creating an invisible, long-term overhang on the token’s price.

None of this is certain, and a well-managed IPO could be handled in ways that limit these effects, but the point is that the community’s framing of an IPO as pure upside for holders is incomplete. The honest version acknowledges that going public is a double-edged sword for XRP. It could, in the bullish case, come bundled with a “special arrangement” that rewards holders, or it could, in the bearish case, drain attention and capital away from the token while increasing the supply pressure on it. Holders hoping for the first should at least weigh the second.

What it means for holders today

So what should an XRP holder actually take from all of this, standing in the present with the token trading near a dollar and the “special arrangement” still nothing more than a hedged remark? The disciplined answer is to give the IPO hint the weight it actually carries, which is to say very little, and to keep attention on the catalysts that truly move XRP. A possible IPO reward is a weak basis for any decision, because it is a maybe attached to a maybe: an unplanned, undefined benefit contingent on an IPO that Ripple does not prioritize. It is better regarded as a distant possible upside not to be counted on than as a catalyst to position around.

The things that will actually determine XRP’s path are observable and concrete: whether the CLARITY Act passes and writes XRP’s commodity status into federal law, whether spot ETF flows compound or trickle, whether the network’s settlement usage grows enough to translate into real token demand against the escrow supply, and where Bitcoin drags the broader market. Those are the signals worth watching, and the IPO hint is not among them. This does not mean the remark is meaningless. It reveals something real about Ripple’s posture toward its community, a willingness to at least entertain the idea of connecting corporate success to holders, which is more than many companies would offer.

But revealing a posture is not the same as making a commitment, and the most useful thing a holder can do is to enjoy the signal for what it shows about Ripple’s attitude while declining to build any expectation on top of it. The community heard a promise. What Garlinghouse offered was a maybe, and in investing the difference is everything. An XRP holder is better served by evaluating the token on its actual merits, its use in payments, its regulatory position, its adoption, and its supply dynamics, than by speculating about an IPO reward that exists only as a hedged possibility.

That possibility is attached to an IPO that may never come, and that could, in some scenarios, hurt the token as much as help it. The hope is understandable. The discipline is to keep it in proportion. If Ripple ever announces a real program, holders can judge the terms then; until then, the “special arrangement” is a signal, not a strategy.

Frequently asked questions

Did Ripple promise XRP holders a payout from its IPO?

No. Ripple chief executive Brad Garlinghouse said that “if and when” Ripple goes public, the company might do “something special” for XRP holders, then immediately added that it was “not in the immediate term.” That was a hedged “maybe” offered in response to a direct question, not a plan, a program, or a commitment, and he declined to endorse any specific mechanism such as a token buyback. The community amplified the remark into something close to a promise, but no payout has been announced, no mechanism has been described, and the comment was explicitly conditional on an IPO that Garlinghouse describes as not a priority.

Does holding XRP give me any ownership of Ripple?

No. Ripple and XRP are legally and financially separate assets. Ripple is a private technology company that builds payment and liquidity products, some of which use the XRP Ledger. XRP is the native cryptocurrency of the XRP Ledger, a decentralized blockchain that Ripple does not control. Holding XRP grants no shares in Ripple, no dividends, no voting rights, and no claim on the company’s profits or assets.

What could a “special arrangement” actually look like?

The mechanisms the community imagines include preferential access to Ripple IPO shares for verified long-term XRP holders, long-term holding rewards for those who keep XRP for a defined period, and tokenized Ripple equity made available to eligible holders. All of these are unannounced and remain speculation instead of anything Ripple has offered. Each also faces serious obstacles, especially securities law, because linking token holding to equity benefits raises exactly the questions Ripple fought during its long legal battle over XRP. More modest possibilities, such as a governance gesture or simply structuring the business so more value flows through XRP, are more realistic than a direct equity windfall.

Is Ripple actually going to have an IPO?

It is uncertain, and Garlinghouse has repeatedly described going public as not a priority. He has cited the weak post-listing performance of crypto-company peers and reports of a major exchange delaying its own plans, and he has argued that staying private preserves flexibility. This matters because the entire holder-benefit question is downstream of an IPO happening at all. Even the most generous imaginable reward is irrelevant unless Ripple first decides to go public and then chooses to extend something to holders.

Could a Ripple IPO actually be bad for XRP?

It could, and this is the part the bullish framing tends to skip. An IPO would give institutions a direct way to own Ripple through regulated stock that offers dividends, financial transparency, and ownership of company assets, potentially drawing capital that might otherwise have flowed into XRP as a proxy for Ripple. Separately, as a public company answerable to quarterly earnings expectations, Ripple could face stronger incentives to monetize its large XRP escrow holdings more aggressively, adding long-term selling pressure on the token. Going public is therefore a double-edged sword for XRP, with credible downside as well as the hoped-for upside, and holders should weigh both.

What should XRP holders actually focus on?

On the observable catalysts that truly move the token instead of the IPO hint. Those include whether the CLARITY Act passes and codifies XRP’s commodity status, whether spot XRP ETF flows compound or stall, whether the network’s settlement usage grows into real token demand against the escrow supply, and the direction of Bitcoin and the broader market. The “special arrangement” remark is best treated as a small signal about Ripple’s posture toward its community, given minimal weight in any actual view of XRP’s prospects. Evaluating XRP on its real merits, utility, regulatory position, adoption, and supply, is far sounder than positioning around a hedged maybe.

This article is information, not investment advice. Prices, corporate plans, and statements reflect reporting available as of June 28, 2026, and can change quickly. Brad Garlinghouse’s comments were conditional and did not constitute a commitment or a program. Nothing here is a recommendation to buy or sell XRP or any security. Verify current details from primary sources and consider your own circumstances before making any decision.

MicroStrategy’s $64 billion Bitcoin (BTC) bet has become a stress test for everyone who funded it. BTC now trades below $60,000, and the renamed company, Strategy, sits at a discount to its own holdings.

The question dividing investors is no longer whether Strategy gets liquidated tomorrow. It is who absorbs the losses while the company keeps its coins and keeps paying to hold them.

How the Bitcoin Flywheel was Built

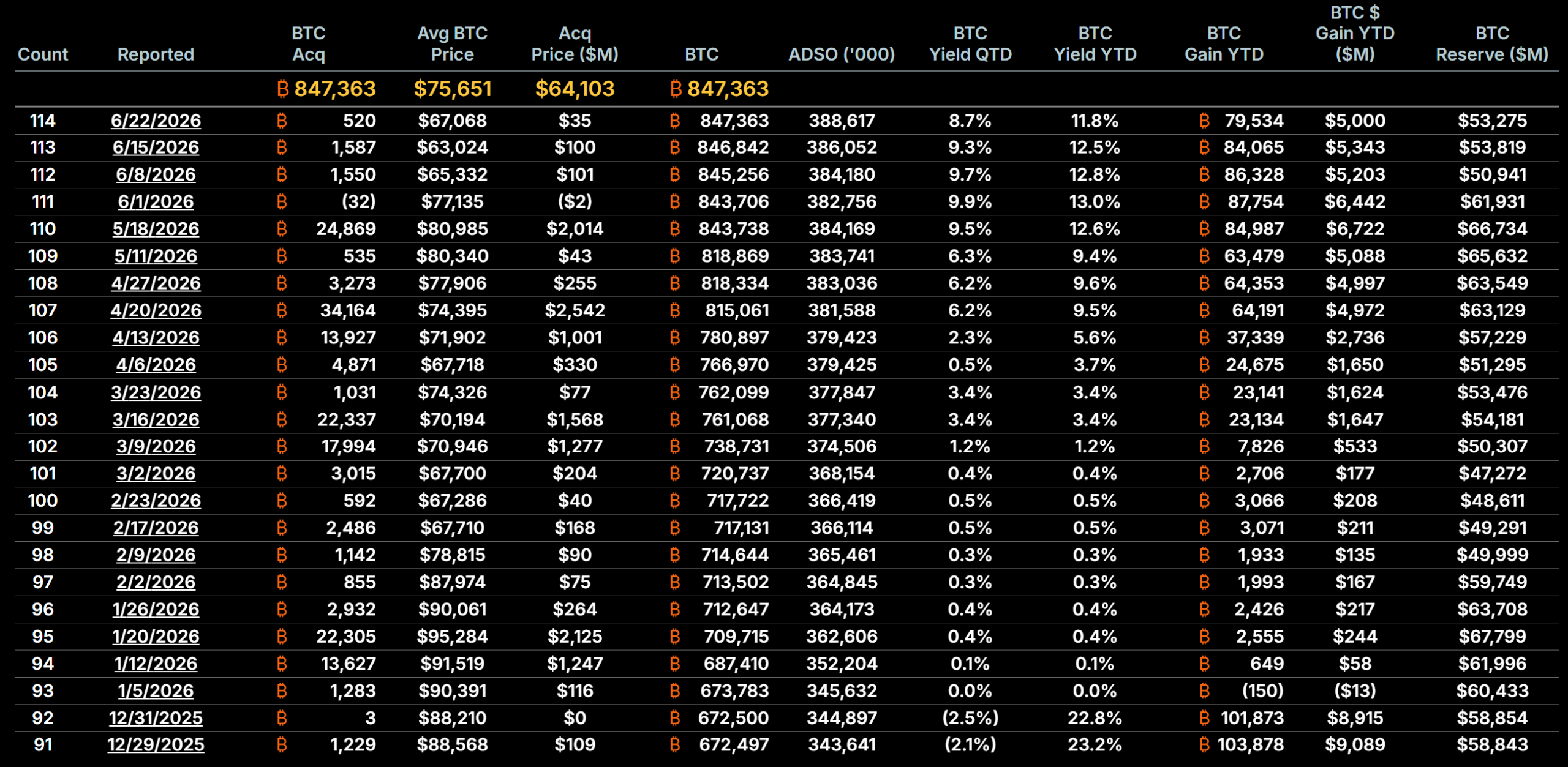

By June 22, Strategy held 847,363 BTC bought for $64.1 billion, an average of $75,651 each. That is the largest corporate Bitcoin position anywhere.

The model runs like a flywheel. The company sells stock and debt, buys more Bitcoin, and its shares climb when BTC rises. However, falling prices spin the machine in reverse.

BTC has fallen below $60,000 this week, its lowest level since 2024. The stock has slid with it, dropping under the value of the Bitcoin on its books.

A new accounting standard made the pain visible. Since 2025, FASB rule ASU 2023-08 forces firms to mark Bitcoin to fair value each quarter. As a result, Strategy booked a $14.46 billion unrealized loss in early 2026. That produced a $12.54 billion net loss, or $38.25 for every diluted share.

Follow us on X to get the latest news as it happens

Who Actually Pays for MicroStrategy’s Bitcoin Bet

The bill does not fall on Strategy alone. As the flywheel slows, the cost spreads to five groups, in rough order of exposure.

- Common shareholders

They stand first in line. When the stock trades below the value of its Bitcoin, the company still raises cash by selling new shares. Each sale buys less Bitcoin than it hands away.

“If we decide to sell $1 billion of MSTR stock and buy $1 billion of Bitcoin… when you do it at 1.0x MNAV… it is dilutive. It is a minus 48 basis point yield. It costs the shareholders $310 million,” Michael Saylor, Executive Chairman, Strategy, said during Q1 2026 earnings call.

Existing owners are left holding a smaller claim on the same coins, and that dilution is how the strategy gets funded.

- Investors in other treasury companies

The copycats have fared worse than the original. Their shares once traded far above the Bitcoin they held, lifted by hype.

As that premium faded, many Bitcoin treasury company stocks fell much harder than Bitcoin itself, leaving late buyers deep underwater.

“If that’s not already a bubble burst, how would that bubble burst?” Tom Lee, Chairman of BitMine, said while many treasury stocks traded below net asset value.

- Passive and index fund investors

This group never chose the bet. MSCI has proposed removing companies whose digital assets exceed half their total assets from its global indexes.

“Feedback from the consultation confirmed institutional investor concern that some DATCOs exhibit characteristics similar to investment funds, which are not eligible for inclusion in the MSCI Indexes,” MSCI said in its official announcement earlier this year.

Strategy clears that bar with ease. An exclusion would force index funds and pension trusts to sell automatically, whatever the price, just to keep tracking the benchmark.

- Convertible bondholders and preferred shareholders

These investors lent on the assumption that MicroStrategy could always refinance. If Bitcoin stays depressed into 2027, that assumption breaks.

“Proceeds from the bitcoin sales are expected to be used to fund distributions on preferred stock,” Strategy indicated in the June 1 Form 8-K.

Bondholders can demand cash, and preferred holders still expect dividends, both drawing on a reserve of just $1.4 billion.

- MicroStrategy itself

The company is the backstop of last resort. On its first quarter 2026 earnings call, Michael Saylor again framed Strategy as a net buyer that never sells.

“We will probably sell some Bitcoin to fund a dividend just to inoculate the market, just to send the message that we did it.”

Yet if financing freezes while debt and dividends come due, keeping that vow could become impossible.

“We will sell Bitcoin when it is advantageous to the company. We are not going to sit back and just say we will never sell the Bitcoin,” Strategy co-CEO Phong Le added.

The Real Test Arrives in 2027

MicroStrategy faces no margin call today. Its main debt is unsecured, so a falling price alone cannot trigger a forced sale. The threat is a date, not a level.

Holders of a $1.01 billion convertible note can demand repayment on September 15, 2027. If the shares sit below the conversion price, that claim becomes a cash bill the company must cover.

Strategy has neared this edge before. A 2022 Silvergate loan backed by Bitcoin carried a margin call near $21,000 before the firm repaid it. Moving to unsecured notes and preferred stock removed the automatic trigger, but not the obligation.

Some peers have already blinked. This month one Nasdaq company sold Bitcoin to repay debt, and its shares jumped. Analysts have also questioned Strategy’s exit liquidity if it is ever forced to sell at scale.

For now, no forced sale looms. The pressure has simply moved from a price trigger to a calendar. The number that matters is no longer $60,000, but the September 2027 repayment date.

The post Who Actually Pays When MicroStrategy’s $64 Billion Bitcoin Bet Goes Wrong? appeared first on BeInCrypto.

TLDR:

- Hyper Foundation committed about $10 million to support USDH migration across affected ecosystem projects.

- Eligible builders must complete migration or orderly shutdown activities before the end of July deadline.

- USDH holders can swap tokens for USDC through supported HyperCore and HyperEVM migration pathways.

- Grant allocations depend on deployment costs or affected USDH total value locked across supported protocols.

Hyper Foundation has introduced a grant program worth approximately $10 million to support projects affected by the USDH sunset. The initiative targets builders migrating away from the stablecoin or winding down USDH-dependent services before the end of July.

Eligible teams have already been contacted as the network moves through an organized transition process. The funding aims to reduce migration costs while helping maintain continuity across the Hyper ecosystem.

Hyper Foundation Unveils $10M USDH Migration Grant Program

Hyper Foundation said the grants will support builders whose products relied on USDH before its retirement. According to the foundation, eligible recipients include HIP-1 spot deployers, HIP-3 perpetual deployers, HyperEVM protocols, dedicated USDH: USDC bridge operators, and Native Markets.

The grants fall into two categories. Migration grants support teams replacing USDH with USDC, while wind-down grants assist projects ending USDH-related operations. The foundation noted that wind-down grants remain smaller than equivalent migration awards.

According to Hyper Foundation, every recipient has committed to completing migration or orderly shutdown activities before the end of July. The program seeks to minimize disruption while encouraging structured transitions across supported applications.

Grant calculations also differ between ecosystem participants. HIP-1 and HIP-3 recipients receive allocations based on auction deployment costs, while HyperEVM protocol grants depend on the amount of USDH total value locked affected by the sunset.

USDH Holders Receive Migration Options as Ecosystem Shifts to USDC

Hyper Foundation also outlined the migration process for users holding USDH. The organization encouraged users to follow instructions directly from the protocols where their assets remain deployed.

Users can exchange USDH for USDC through the HyperCore spot order book. The foundation also confirmed that HyperEVM users can swap USDH for USDC at a one-to-one ratio through Across without paying transaction fees.

Wu Blockchain highlighted the announcement shortly after the grant program became public. The report noted that the funding package covers both migration expenses and wind-down costs for affected ecosystem participants.

Hyper Foundation also acknowledged the contribution of builders, users, and Native Markets throughout the USDH rollout. The organization credited community participation and direct coordination with helping the migration process progress smoothly during the transition period.

Bitcoin is set up for a tense July after June delivered the token’s weakest monthly performance since mid-2022. BTC is down roughly 18.5% for the month and has struggled to defend the $60,000 psychological level.

Analysts are split between two forces: downside pressure tied to Bitcoin’s technical weakness, and a potential “liquidity magnet” effect that has historically coincided with sharper rebounds. Traders watching July closely will likely focus on whether BTC can reclaim key long-term indicators before any mean-reversion bounce plays out.

Key takeaways

- June’s drawdown puts pressure on Bitcoin’s ability to hold support near $60,000, with further weakness possible if longer-term trend levels fail.

- Liquidation data referenced by analyst Fleh points to a large short-liquidation concentration near $67,600, which could act as a magnet on a rebound.

- CoinGlass data cited in the coverage suggests Bitcoin has historically posted an average gain of about 7.6% in July, after a weak June.

- Seasonality in midterm-election years has been stronger for BTC, with an average July return of roughly 10.3% in those years.

- Another technical risk factor is Bitcoin trading below its 200-week simple moving average region near $62,445, a condition that preceded deeper weakness in 2022.

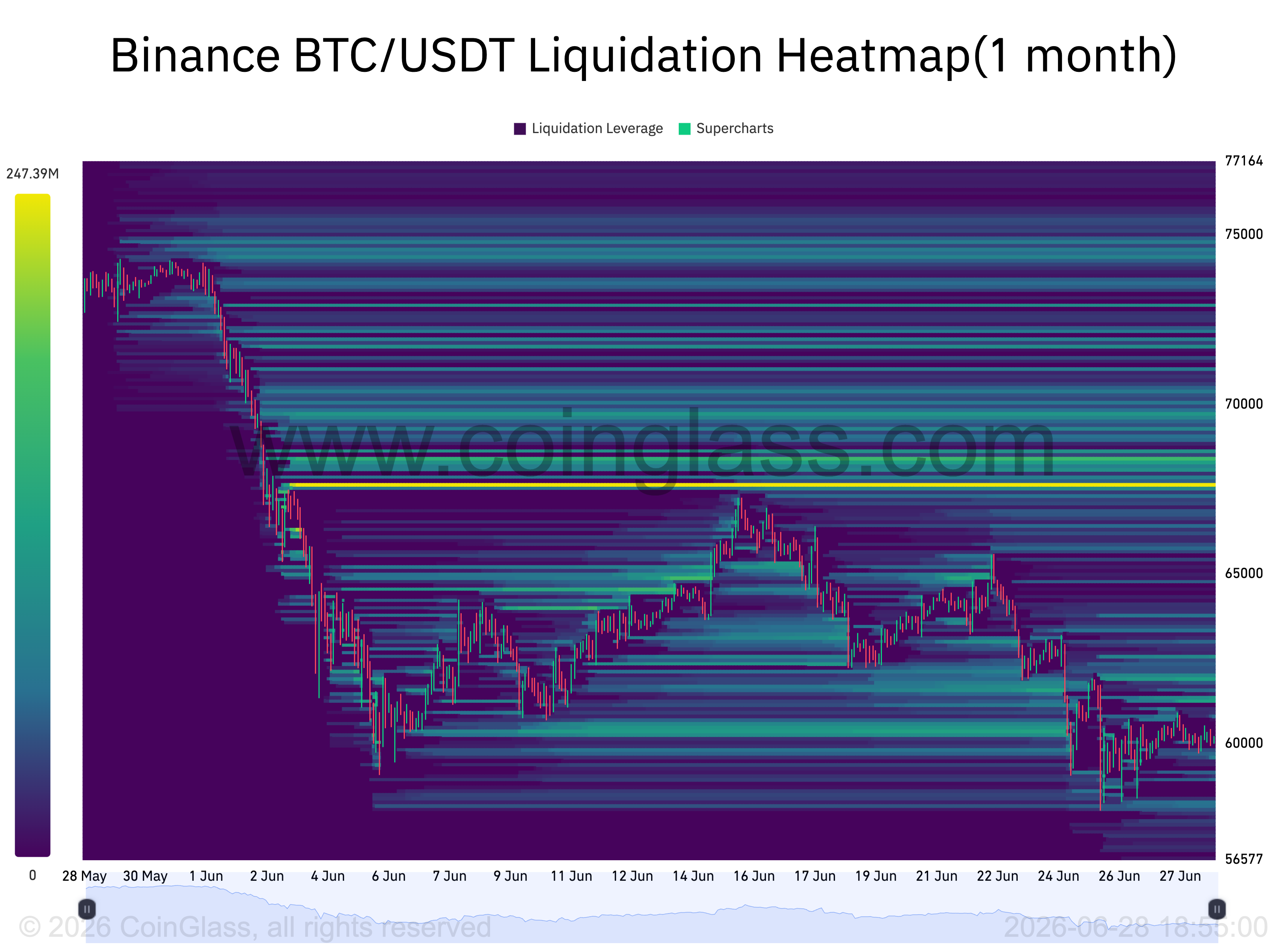

Liquidity heatmap points to a potential “magnet zone”

One of the more constructive arguments for July comes from liquidation positioning. In a post shared by analyst Fleh, the trader highlighted Binance BTC/USDT liquidation heatmap levels indicating heavy short-liquidation liquidity above current price.

The largest cluster referenced sits around $67,645. The charting data shown in the report cites approximately $247.39 million in liquidation leverage and roughly $2.26 billion in cumulative short liquidation leverage in that area, according to CoinGlass heatmap figures.

In markets, large concentration zones like this are sometimes described as “magnet zones.” The logic is straightforward: if price rises toward areas where leveraged short positions are concentrated, those shorts can be forced to exit through liquidation. Closing shorts generally requires buying Bitcoin back, which can amplify upward momentum and increase the odds of a sharper move than spot flows alone would suggest.

Fleh’s outlook, as quoted in the original coverage, is that BTC may bottom near $60,000 “for now,” targeting a rally toward $75,000 before any further downside risk materializes.

Seasonality and historical July performance

Beyond liquidation dynamics, the bullish case is also supported by historical calendar behavior—though this is not a guarantee. According to CoinGlass data highlighted by analyst CGT_Trader, Bitcoin has delivered an average gain of about 7.6% in July. The same dataset shows June has been weaker on average, with an average June return around -1.40%.

The key practical takeaway for traders is that July has often started with a rebound after a soft June. The report notes that even in bear-market years, July has still produced positive performance—for example, BTC gained 20.96% in July 2018 and 16.8% in July 2022.

More recent examples cited include a 2.95% rise in July 2024 and an 8.13% gain in July 2025, which the authors frame as further evidence that the seasonal pattern can persist through different regimes.

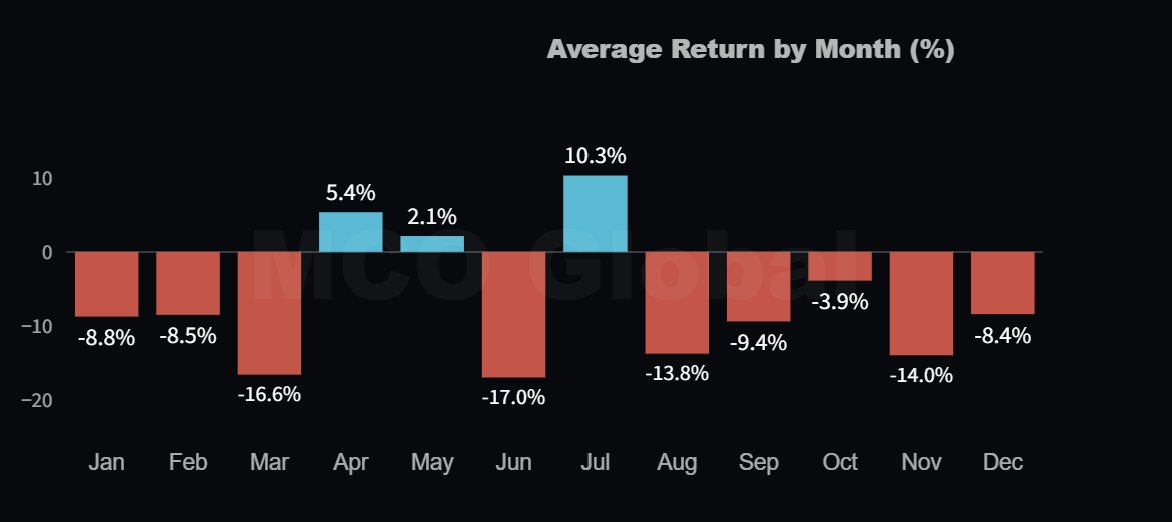

A separate midterm-election-year seasonality view referenced in the coverage shows Bitcoin averaging a 10.3% gain in July during those years—its strongest monthly return in that subset. That statistic contrasts with an average June loss of about 17% in midterm-election years, strengthening the “post-sell-off bounce” narrative.

Using the report’s current-price assumption near $60,000, a 7.6% average July gain implies a move toward roughly $64,500. The stronger 10.3% midterm-year average suggests a potential stretch toward about $66,100. If Bitcoin repeats the more dramatic bear-market rebounds seen in 2022 and 2018, the upside range suggested in the coverage lands between $70,000 and $72,500. A more aggressive “2020-style” July rally would be consistent with Fleh’s $75,000 target.

Technical pressure: risk grows if BTC can’t reclaim long-term support

While the upside thesis leans on liquidity and seasonal mean reversion, the downside case remains anchored in Bitcoin’s longer-term technical picture. The original analysis notes that BTC is still trading below its 200-week simple moving average, with that long-term reference around $62,445.

That matters because losing long-term moving-average support often increases the odds that rallies fail and price remains heavy until a deeper correction runs its course. The report draws a parallel to 2022: it states that a similar loss of long-term moving-average support preceded additional weakness before Bitcoin eventually formed a bottom.

In the coverage, this backdrop is described as a “bear flag breakdown,” with the expectation that unless BTC quickly reclaims the 200-day SMA area, downside risk in July could extend toward $55,000. The same article links to earlier coverage about capitulation risk near $50,000, underscoring that the technical narrative for this cycle has included concerns about sustained liquidation-driven selling pressure.

For investors, the practical distinction is timing. A liquidity-magnet rebound near $67,600 would require BTC to first stabilize around the $60,000 region and begin reclaiming higher levels. If instead price continues to slip below the long-term moving-average zones highlighted in the analysis, the short-term liquidation “magnet” argument could be delayed or invalidated by renewed downside momentum.

What to watch next in July

Heading into the month, the most important signals are whether BTC can hold near $60,000 and whether it reclaims the long-term moving-average region cited near $62,445. If it does, the $67,600 liquidity cluster could become a focal point for short-liquidation-driven buying; if it doesn’t, the reported $55,000 risk scenario may gain credibility and further weaken the odds of a quick mean-reversion bounce.

TLDR:

- Bitcoin approaches a rare weekly death cross as traders monitor long-term market direction closely.

- Strategy’s mNAV has dropped below 1.0 for the first time during this market cycle.

- Michael Saylor hinted at more Bitcoin discussions despite growing valuation concerns.

- Technical signals and institutional buying remain key factors shaping Bitcoin sentiment.

Bitcoin could soon print a rare weekly death cross as bearish technical signals return to the market. At the same time, Michael Saylor has hinted that Strategy may continue accumulating Bitcoin despite growing pressure on its valuation.

The two developments have reignited discussion around Bitcoin’s price outlook and institutional demand. Investors are now watching technical charts alongside corporate buying activity for the next major market signal.

Bitcoin Weekly Death Cross Raises Fresh BTC Price Concerns

Crypto Rover shared that Bitcoin is approaching a weekly death cross, a technical pattern that appears when the long-term moving average falls below the shorter trend. The account noted that the previous weekly death cross preceded another 28% decline in Bitcoin’s price.

The same post highlighted Bitcoin’s historical four-year market cycle. According to Crypto Rover, another extended correction could align with the later stages of the current cycle if previous patterns repeat.

The signal has attracted attention because weekly chart formations appear far less often than daily indicators. Traders typically monitor them for broader market direction rather than short-term volatility.

Despite the technical setup, the pattern alone does not determine future price action. Market participants continue weighing macroeconomic conditions, liquidity, and institutional demand alongside historical chart behavior.

Michael Saylor Hints at More Bitcoin Buying Despite Strategy Valuation Pressure

While bearish technical signals circulated, Michael Saylor posted that more charts would be needed, a familiar response that often precedes fresh Bitcoin discussions. His comment followed renewed debate surrounding Strategy’s ability to continue funding Bitcoin purchases.

Wise Advice pointed to Strategy’s market value relative to its Bitcoin holdings. The account noted that the company’s modified net asset value, or mNAV, has fallen below 1.0 for the first time during the current market cycle.

According to the same discussion, Strategy previously suggested that issuing new equity below roughly 1.22 times mNAV could reduce shareholder value. That threshold has prompted questions about whether additional equity-funded Bitcoin purchases remain practical under current market conditions.

Even so, Saylor’s brief response has kept attention on Strategy’s long-standing Bitcoin accumulation strategy.

Investors now await any official filings or announcements that could clarify whether another Bitcoin purchase is approaching while the company navigates changing market dynamics.

Crypto World

Ethereum Price Analysis: The Crucial Daily RSI Divergence That Could Save ETH From New Lows

Ethereum remains under pressure across higher timeframes, but the latest price action is showing early signs that bearish momentum may be losing strength. While the broader trend remains decisively bearish, the recent movements suggest that sellers may be approaching exhaustion after weeks of sustained downside.

Ethereum Price Analysis: The Daily Chart

ETH’s recent rejection from the $1.72K-$1.78K supply zone triggered another leg lower, pushing it back into the critical $1.46K-$1.53K demand region. This zone has acted as support multiple times throughout June and continues to attract buyers whenever the price approaches it.

The most notable development on the daily timeframe is the emerging bullish divergence on the RSI. While the asset has continued making lower lows during June, the RSI has been forming higher lows near oversold territory. This divergence suggests that downside momentum is weakening despite ETH remaining near cycle lows.

Although a bullish divergence alone does not guarantee a reversal, it often appears during the latter stages of bearish trends and can serve as an early warning that sellers are losing control. As long as ETH holds above the $1.46K-$1.53K support area, the divergence remains valid, increasing the probability of a relief rally.

However, confirmation would require a break above the nearest resistance zones, particularly the $1.72K-$1.78K supply area. Until then, the broader trend remains bearish despite the improving momentum profile.

ETH/USDT 4-Hour Chart

On the 4-hour timeframe, Ethereum has spent the past several sessions consolidating above the lower demand zone after the sharp sell-off from resistance.

A descending trendline has capped every recovery attempt since the June 22 rejection. However, the asset is now compressing directly beneath that trendline, while volatility continues to contract. This setup creates the possibility of a short-term breakout if buyers can push through trendline resistance.

A successful breakout would likely target the $1.72K-$1.78K supply zone, which served as the origin of the latest decline. Such a move would align well with the bullish RSI divergence visible on the daily chart and could provide the first meaningful recovery rally in several weeks.

On the downside, the $1.52K area remains the key level to monitor. Losing this support would invalidate the short-term bullish scenario and shift focus back toward deeper downside continuation within the broader downtrend.

For now, Ethereum appears trapped between support and descending resistance, with the next directional move likely determined by whichever side breaks first.

Sentiment Analysis

The liquidation heatmap reveals an interesting shift in liquidity positioning.

While liquidity remains concentrated above the current price, particularly between roughly $1.68K and $1.80K, Ethereum is currently trading beneath these large clusters. Markets often gravitate toward areas with substantial leveraged positioning, making those overhead liquidity pools attractive short-term targets.

This creates a scenario where ETH could stage an upside liquidity sweep before any larger directional move develops. A breakout above the 4-hour descending trendline would increase the probability of price moving into these overhead liquidity pockets, triggering short liquidations and fueling a squeeze toward the $1.7K-$1.8K region.

At the same time, the heatmap also shows notable liquidity beneath the market around the lower support region, meaning both sides of the range remain vulnerable to liquidation-driven volatility.

Combined with the bullish daily RSI divergence and the compression beneath 4-hour trendline resistance, the current setup suggests Ethereum may first attempt an upside liquidity grab before the market determines whether a more sustainable recovery can develop. The reaction around the $1.72K-$1.80K liquidity cluster will likely provide important clues regarding Ethereum’s next major trend.

The post Ethereum Price Analysis: The Crucial Daily RSI Divergence That Could Save ETH From New Lows appeared first on CryptoPotato.

The world’s highest IQ record holder just declared that the XRP Supercycle is only beginning, while three bullish signals hit the chart at the same time. The token trades near $1.05 as the narrative quickly gains momentum.

The combination of high-profile sentiment and technical alignment is reshaping how traders frame the next XRP cycle.

Why the Highest IQ Holder Sees an XRP Supercycle Starting

A supercycle is a multi-year market phase in which an asset moves through extended upside expansion rather than a typical shorter rally. The XRP narrative just got a major sentiment boost from YoungHoon Kim, holder of the verified world record for the highest IQ at 276.

Kim publicly declared on X that the XRP Supercycle is only just beginning. His statement immediately spread across crypto communities, framing the current phase as the very early innings.

Furthermore, the message landed at a moment when both technical and on-chain indicators are aligning for the Ripple token.

Follow us on X to get the latest news as it happens.

Such declarations always generate excitement among holders. However, the framing matters because it aligns with structured cycle perspectives shared by serious technical analysts. As a result, the supercycle conversation has expanded beyond pure sentiment and into long-term, data-driven market modeling for XRP.

Technical analyst ChartNerdTA recently highlighted relevant historical cycle data. XRP’s moves from one periodic cycle high to the next have averaged three to five years over the past decade-plus.

Furthermore, this remains one of the cleanest cycle structures in the entire crypto sector.

The data points toward a specific possibility. If a cycle bottom forms during 2026, the next major XRP top could realistically land between 2028 and 2030.

The current market context supports the broader bullish thesis. XRP’s market capitalization remains above $65 billion with 24-hour trading volume still active, according to CoinGecko data.

Institutional interest stays strong, supported by ongoing spot ETF inflows and Ripple’s expanding cross-border payments business across multiple international corridors.

The 3 Bullish Signals Now Lighting Up XRP

A bullish signal is a technical or on-chain indicator that suggests buying pressure may begin to outweigh selling momentum in the short term. XRP has just triggered three of them at once, reinforcing the broader narrative pushed by the highest-IQ holder this week.

The first signal comes from the Tom DeMark Sequential indicator on the daily chart. The setup printed a fresh “9” buy signal, as flagged by analyst Ali Charts. Furthermore, the reading often signals exhaustion in downtrends and tends to precede short-term relief rallies lasting 1 to 4 candles.

The second signal is a Morning Star Doji candlestick pattern. The formation took shape across the past three sessions near the $1.02 to $1.07 support zone. As a result, the structure now reinforces the case for a localized bottom in the short-term XRP price action.

The third signal comes from on-chain activity. Daily active addresses jumped from around 23,000 on June 14 to nearly 39,500 in recent days. Moreover, the surge points to genuine network engagement rather than speculative positioning alone, driving short-term price recovery.

Together, the three signals form a rare alignment. Technical reversal patterns are now meeting concrete on-chain growth at a defended support zone. However, confirmation will require sustained buying volume and a clean break above immediate resistance toward the $1.30 level.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

The wider question remains open. A confirmed near-term move would mark the first technical validation. However, if the supercycle thesis from the highest IQ holder holds, the real story lies years ahead.

Either way, the current setup combines technical, on-chain, and narrative forces in a way XRP has rarely seen before.

The post Highest IQ Holder Backs an XRP Supercycle as 3 Bullish Signals Hit at Once appeared first on BeInCrypto.

TLDR:

- Forbes estimates CZ’s fortune at $110B, placing the Binance founder ahead of Bill Gates in the latest rankings.

- Binance ownership remains the largest contributor to CZ’s wealth despite past regulatory settlements and leadership changes.

- Forbes says Bill Gates’ continued philanthropy has reduced his personal fortune while keeping him among top billionaires.

- CZ noted crypto wealth changes rapidly because private company valuations and digital asset prices fluctuate daily.

Changpeng Zhao, widely known as CZ, has moved ahead of Bill Gates on the latest Forbes billionaire rankings. The shift reflects the growing value of Binance alongside rising digital asset markets.

CZ’s estimated fortune now stands at $110 billion, placing him above the Microsoft co-founder in Forbes’ published list. The milestone also highlights how crypto infrastructure has become a significant source of global wealth.

CZ Tops Bill Gates as Binance Valuation Lifts Net Worth

Forbes estimates CZ’s net worth at $110 billion. Bill Gates follows with an estimated $108 billion. The updated rankings place CZ at No. 17 globally, while Gates ranks No. 19.

The largest contributor to CZ’s fortune remains his ownership stake in Binance. Forbes estimates that he still controls roughly 90% of the world’s largest cryptocurrency exchange.

The value of that stake has increased alongside stronger activity across digital asset markets. CZ also holds substantial personal cryptocurrency investments.

Previous public statements indicate that most of his personal assets remain invested in crypto, including Bitcoin and Binance Coin. Forbes factors those holdings into its overall wealth calculations.

CZ acknowledged the published ranking after its release but noted that billionaire estimates can change rapidly. He pointed to crypto market volatility, saying real-time valuations often differ from published figures because private company values and digital assets fluctuate continuously.

Binance Recovery Strengthened CZ’s Position

Binance remained the world’s largest cryptocurrency exchange despite major regulatory challenges over the past several years.

After stepping down as chief executive following a U.S. settlement in 2023, CZ retained his reported ownership stake in the company.

According to Forbes, Binance’s business recovered as trading activity stabilized and the exchange maintained a leading share of global crypto trading volume. That recovery significantly increased the estimated value of CZ’s equity.

Posts shared by DeFiTracer on X highlighted the updated Forbes rankings, describing CZ as the richest individual in the cryptocurrency industry. The discussion quickly spread across the crypto community as investors compared traditional technology fortunes with wealth created through digital asset infrastructure.

The rankings also reflect Bill Gates’ long-term philanthropic strategy. Forbes notes that Gates has continued transferring substantial assets to charitable causes through the Gates Foundation, reducing his personal fortune over time while remaining among the world’s wealthiest individuals.

The latest billionaire list illustrates how ownership of crypto infrastructure can rival wealth generated through traditional technology companies.

While token prices influence personal fortunes, Binance’s business valuation remains the largest driver behind CZ’s estimated net worth, according to Forbes. The figures also serve as a reminder that billionaire rankings change frequently as private company values and cryptocurrency markets continue to move.

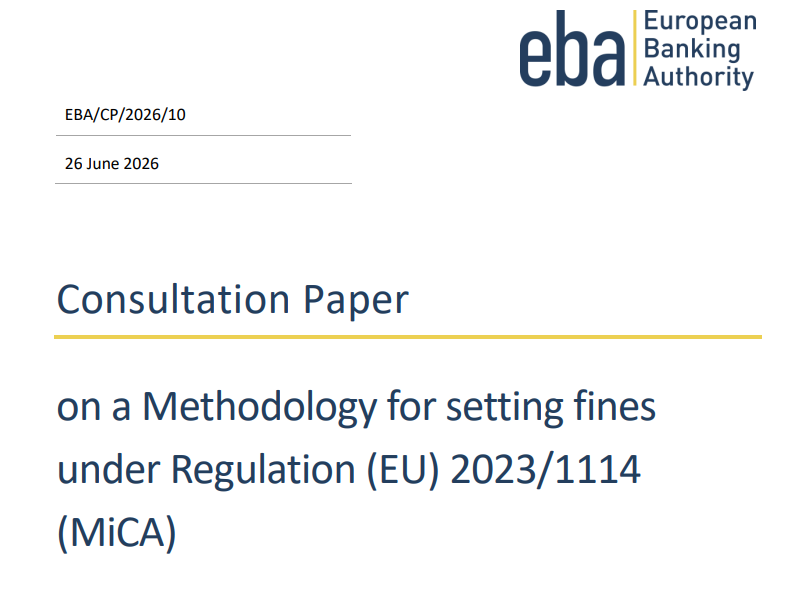

The European Banking Authority (EBA) has published a consultation paper outlining how it plans to calculate fines for crypto asset issuers that breach the EU’s Markets in Crypto-Assets (MiCA) framework. The proposal—released June 26—signals that regulators intend to move from rulemaking to consistent, standardized enforcement for “significant” token issuers.

Under the draft methodology, the EBA would apply a structured two-step process: it would first establish a baseline severity for an infringement and then adjust the result based on aggravating or mitigating factors. The framework is designed to cover significant asset-referenced tokens (ARTs) and significant e-money tokens (EMTs), with penalty caps intended to be large enough to deter major market players.

Key takeaways

- The EBA’s June 26 consultation sets out a standardized method for determining MiCA-related fines for issuers of “significant” ARTs and EMTs.

- Fines could reach statutory ceilings of up to 12.5% of annual turnover for significant ART issuers and up to 10% for significant EMT issuers, or up to two times the profits from the violation.

- The EBA’s enforcement “teeth” arrive as MiCA licensing requirements take effect on July 1, ending a transitional period for many firms.

- Crypto firms that miss licensing deadlines face operational constraints—and potentially the very types of conduct targeted by the EBA’s fine methodology.

- Executives have a consultation window until September 28 to comment on the EBA’s approach, but the July 1 compliance deadline leaves little time for adjustments in practice.

A penalty playbook for MiCA breaches

MiCA is the EU’s landmark digital asset regulation, built to bring order to the market by requiring token issuers and crypto service providers to meet bank-like compliance expectations—covering issues such as consumer protections and capital reserves—to access the bloc’s single market.

In its consultation paper, the EBA focuses on enforcement for significant tokens as defined under MiCA. The document proposes a consistent approach to fines rather than leaving penalty levels to ad hoc determinations. According to the EBA, the methodology begins by evaluating the baseline seriousness of an infraction and then accounts for behavior-specific circumstances, such as factors that would increase or reduce culpability.

The proposed ceilings are explicitly framed as punitive. The consultation states that final penalties could be set up to statutory maximums of 12.5% of annual turnover for issuers of significant ARTs and 10% for issuers of significant EMTs. The paper also references a cap of two times the profits generated by the violation, a design intended to prevent companies from treating enforcement risk as a cost of doing business.

EBA’s consultation paper (June 26) lays out the framework in more detail, including the procedural steps the authority would use when calculating penalties.

MiCA licensing deadline turns the calendar into a compliance cliff

The fine methodology arrives at a moment when the industry is already facing a hard operational deadline. By July 1, crypto companies must have obtained formal licenses from national regulators to legally offer services across the EU and to market stablecoins within the 27-nation bloc. The deadline ends the transitional period that allowed some operators to continue functioning under less stringent local rules.

The EBA’s penalty methodology is therefore more than a theoretical enforcement blueprint. Companies that fail to secure regulatory authorization by July 1 could be forced to halt or narrow certain activities. The timing also raises the risk of triggering conduct that falls under the types of non-compliance the EBA’s framework is meant to penalize.

Earlier coverage from Cointelegraph also highlighted that the July 1 deadline would constrain firms unable to complete MiCA authorization processes in time. In practical terms, that means executives and compliance teams may be operating under uncertainty while regulatory paperwork catches up—right as the EBA is preparing to standardize what happens when rules are broken.

Binance’s EU restrictions underscore the operational impact

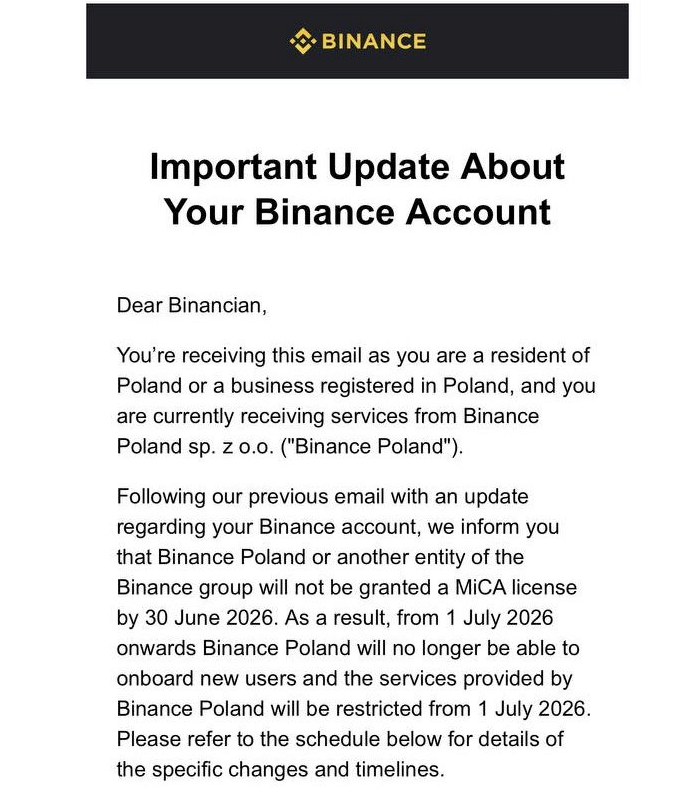

One of the clearest real-world signals comes from Binance. According to Cointelegraph, the exchange notified European Union users that it would restrict access to some services after it failed to secure MiCA authorization from a member state ahead of the July 1 deadline. The reported reason was that Binance withdrew its MiCA license application in Greece.

As users shared notices on social media, Binance indicated that it would stop onboarding new EU users and limit certain services for EU-based accounts effective July 1. The notices also stated that withdrawals would remain available after that date, aligning with regulatory expectations that customers should be able to exit their positions even when trading or onboarding restrictions apply.

The timing matters for market participants because it suggests a likely pattern: without authorization, major venues may shift from growth mode to risk containment. For users, that translates into fewer options for new entry, while for institutions and market makers it can affect liquidity planning and compliance coverage across jurisdictions.

Cointelegraph reported that Binance saw substantial daily net outflows around the announcement, citing DefiLlama data. The exchange’s subsequent outflow figures over the following two days were also reported by Cointelegraph, reflecting how quickly liquidity can move when regulatory access changes.

EU enforcement in focus as the US relies more on action-by-action

Beyond the specific penalty mechanism, the EBA consultation highlights a broader enforcement posture. By publishing a clear fining methodology just as MiCA licensing takes effect, EU authorities appear to be emphasizing predictability and deterrence—leaving less room for interpretation that enforcement might be gradual or forgiving.

This contrasts with a more enforcement-driven approach often associated with the United States, where regulatory outcomes can depend heavily on case-by-case actions. In the EU’s model, the framework aims to define the penalty logic upfront, providing firms with a clearer sense of the regulatory “cost of non-compliance” if they operate without the required authorizations or breach MiCA obligations.

The EBA also set a consultation period that runs until September 28, giving industry participants time to lobby for changes to the fine methodology. Still, the practical reality is that companies must operate compliantly well before the EBA’s final guideline is locked in—meaning the July 1 deadline will test compliance systems first, and only then will firms try to influence the methodology through formal feedback.

As the consultation deadline approaches, market participants should watch whether national regulators align quickly on implementation details and how quickly firms adapt their compliance programs ahead of and after July 1—because the EBA’s penalty framework will likely shape boardroom decisions long before any final rules are formally adopted.

Bitcoin (BTC) is heading for its worst monthly loss since mid-2022, with BTC down roughly 18.5% in June as price struggles to hold the psychological $60,000 support level.

BTC/USD monthly chart. Source: TradingView

Will Bitcoin’s downside momentum extend in July, or is BTC preparing for a recovery?

Key takeaways:

- Bitcoin’s liquidity map shows a major short-liquidation “magnet zone” near $67,600.

- BTC has historically gained 7.6% on average in July, while midterm-year seasonality points to an even stronger 10.3% average return.

Bitcoin may hit $75,000 in July

July may become a “bullish month for Bitcoin,” according to analyst Fleh, who predicted BTC price to rally toward $75,000 next month.

The bullish thesis is based on Bitcoin’s Binance BTC/USDT liquidation heatmap, which shows a large concentration of short liquidation levels sitting above the current price.

On the monthly chart, the strongest visible liquidity cluster sits near $67,645, where the chart shows around $247.39 million in liquidation leverage and roughly $2.26 billion in cumulative short liquidation leverage.

Binance BTC/USDT liquidation heatmap (1 month). Source: CoinGlass

For beginners, such clusters are often called “magnet zones.” When many leveraged positions are concentrated around the same price area, the market can move toward that zone because liquidations create forced buying or selling pressure.

In this case, significant liquidity sits above Bitcoin’s current price near $60,000.

If BTC rebounds and pushes toward $67,600, short sellers may be forced to close their positions. Since closing shorts requires buying Bitcoin back, that can add fresh upside pressure and fuel a short squeeze.

“I think $BTC bottoms here at 60k for now, targeting 75k to the upside before any chance of lower,” Fleh said in a Saturday post.

BTC rises 7.6% on average in July

Bitcoin’s historical monthly returns also support Fleh’s bullish July outlook.

BTC has returned a 7.6% gain on average in July, making it one of its stronger months after a typically weaker June, which shows an average return of -1.40%, according to CoinGlass data highlighted by analyst CGT_Trader.

Bitcoin monthly returns tracking the July performance in since 2013. Source: CoinGlass/CGT_Trader

The trend has appeared even during bear market years.

For instance, Bitcoin rose 20.96% in July 2018 and 16.8% in July 2022. More recently, BTC gained 2.95% in July 2024 and 8.13% in July 2025, strengthening the case for another green month ahead.

A separate midterm-year seasonality chart also shows that- Bitcoin has averaged a 10.3% gain during the month, its strongest monthly return in such years.

Bitcoin performance by month during US mid-term election years. Source: More Crypto Online

That compares with an average 17% loss in June, pointing to the possibility of a post-sell-off mean-reversion bounce.

Based on Bitcoin’s current price near $60,000, its historical July average return of 7.6% projects a move toward roughly $64,500, while the stronger midterm-year average of 10.3% points to about $66,100.

A repeat of Bitcoin’s bear-market July rebounds from 2022 and 2018 would put BTC between $70,000 and $72,500, while a 2020-style July rally would bring Fleh’s $75,000 target within reach.

BTC’s dip below the 200-week SMA may extend slide

Bitcoin’s ongoing drop below its 200-week simple moving average (200-day SMA, the blue line) near $62,445 raises the risk of further downside in July.

BTC/USD weekly chart. Source: TradingView

A similar loss of long-term moving-average support preceded deeper weakness during the 2022 bear market, when BTC continued lower before forming a bottom.

Related: Bitcoin faces fresh capitulation risk as 50K BTC moved at a loss

Bitcoin’s bear flag breakdown raises the odds of a price decline toward $55,000 in July unless BTC quickly reclaims the 200-day SMA.

BTC/USD daily chart. Source: TradingView

The European Banking Authority on Friday unveiled a sweeping framework to penalize cryptocurrency issuers that violate the European Union’s digital-asset laws, signaling a tougher enforcement stance as the trade bloc finalizes its historic regulatory architecture.

The consultation paper published June 26 establishes a standardized playbook for hitting non-compliant issuers of what the EBA considers “significant” tokens with potentially multimillion-euro penalties. Under the proposal, the Paris-based watchdog will deploy a strict two-step process to determine fines, assessing the baseline severity of an infraction before factoring in aggravating or mitigating behavior.

The move represents the sharpening of teeth for the EU’s landmark Markets in Crypto-Assets (MiCA) regulation. Introduced to bring order to a historically freewheeling sector, MiCA is the world’s first comprehensive regulatory regime for digital assets, forcing token issuers and crypto service providers to operate with bank-like compliance, consumer protections and capital reserves if they want access to the single European market.

The stakes for non-compliance are explicitly designed to be punitive. According to the EBA’s consultation paper, final penalties could reach statutory ceilings of 12.5% of annual turnover for issuers of significant asset-referenced tokens and 10% for significant e-money tokens, or two times the profits generated by the violation, caps meant to deter even the largest global digital-asset operators.

Cover screenshot of European Banking Authority’s 14-page consultation paper.

Source: EBA

The roll-out of the penalty framework comes at a critical juncture for Europe’s digital asset industry, landing just days ahead of a crucial July 1 deadline. By the start of next month, cryptocurrency firms must have secured formal licenses from national regulators to legally offer their services or market stablecoins within the 27-nation bloc, ending a transitional grace period that allowed many operators to function under looser local rules.

Related: Binance faces EU service limits next week as MiCA rules take effect

Firms that fail to secure their regulatory passports by July 1 face the prospect of being forced to halt operations entirely or risk triggering the exact infractions, such as unauthorized public disclosures or organizational failures, that the EBA’s new framework is built to penalize.

Binance pushes “pause” on EU operations after license fail

The world’s biggest exchange operator, Binance, last week notified European Union users that access to key services will be restricted after the exchange failed to secure MiCA authorization from a member state before the July 1 deadline after it withdrew its MiCA license application in Greece.

Those restrictions include halting the onboarding of new EU users and limiting certain services for EU-based accounts effective July 1, according to exchange notices shared by users on social media.

Notice sent by Binance to customers in Poland. Source: IT_Tech_PL

The notices said users will still be able to withdraw their assets after that date, stating that “all digital assets are still available for withdrawal,” in line with applicable regulatory requirements.

Binance recorded $1.96 billion in daily net outflows on Wednesday, following its withdrawal announcement, according to DefiLlama data viewed by Cointelegraph on Sunday. The exchange then saw another $2.52 billion and $1.46 billion in net outflows over the following two days.

EU move shows sharp contrast with US enforcement approach

The timing underscores the European Union’s broader strategy to position itself as the dominant global standard-setter for digital finance, contrasting sharply with the regulation-by-enforcement approach seen in the United States. By laying out clear financial penalties right as the licensing mandate takes effect, authorities in Brussels are telling the market that the era of leniency is officially over.

The industry now has a three-month consultation window ending September 28 to lobby for changes to the EBA’s penalty methodology. However, with the July 1 licensing cliff edge just days away, executives will have to navigate an unforgiving compliance environment long before the final fining guidelines are formalized under law.

XRP Valuation NEW MATH!

Reality star ‘scarred for life’ after being mauled by XL Bully

‘Our broken system creates broken kids’

-

Sports5 days ago

Sports5 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech6 days ago

Tech6 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics2 days ago

Politics2 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics3 days ago

Politics3 days agoPotential 2028er World Cup attendee leaderboard

-

Business2 days ago

Business2 days agoAsia stock markets slide as tech shares slump

-

Tech3 days ago

Tech3 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World5 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business5 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World2 days ago

Crypto World2 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports2 days ago

Sports2 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World2 days ago

Crypto World2 days agoRTX holders must register wallets before token distribution begins

-

Crypto World2 days ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World1 day ago

Crypto World1 day agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Sports3 days ago

Sports3 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Crypto World2 days ago

The DATA Foundation Launches to Tackle AI’s Multi-Billion Dollar Training Data Bottleneck

-

Crypto World3 days ago

Crypto World3 days agoStrategy (MSTR) has a 10-month cash runway for dividends, but retail investors are losing faith

-

Crypto World3 days ago

Crypto World3 days ago21Shares Cuts 2026 Crypto Forecasts as Institutional Demand Rises

You must be logged in to post a comment Login