Crypto World

Saylor’s Bitcoin Flywheel Is Now Spinning in Reverse

Strategy turned a software company into the largest corporate Bitcoin holder on earth by exploiting a simple loop: trade above your Bitcoin’s value, issue stock, buy more Bitcoin, repeat. In June 2026, Bitcoin broke below $60,000, the stock fell under its own Bitcoin value, and the loop began running the other way. Here is how the machine works, why it reverses, and whether Saylor is actually trapped.

Summary

- Strategy’s mNAV fell to roughly 0.80, meaning its stock trades below the value of the Bitcoin it holds, which disables the premium-funded loop the company used to grow.

- The same reflexive flywheel that compounded gains on the way up now compounds pressure on the way down: at a discount, issuing equity destroys Bitcoin per share, and issuing preferred stock turns expensive, choking both funding taps at once.

- Annual dividend obligations across its preferred stack quadrupled to about $1.2 billion while cash reserves fell roughly 38%, collapsing dividend coverage from more than seven years to around 14 months.

- STRC, the key funding instrument, trades near $82 against a $100 par value, and a tiny 32-Bitcoin sale to fund a dividend broke Strategy’s long-standing never-sell narrative.

- Analysts are split between a “trap” thesis and a “strained but not broken” view, and the outcome hinges almost entirely on Bitcoin’s price, with a roughly $1 billion debt maturity in 2027 as the key deadline.

For five years, Michael Saylor ran one of the most effective financial machines in modern markets, a self-reinforcing loop that converted a mid-sized software company into the largest corporate holder of Bitcoin on earth, with more than 847,000 coins on its balance sheet.

The machine had a simple engine at its center: as long as Strategy’s stock traded at a premium to the value of the Bitcoin it held, the company could issue new shares or preferred stock above that value, use the cash to buy more Bitcoin, and increase the amount of Bitcoin backing each existing share, which justified the premium and let the loop run again. It was elegant, it was relentless, and for a long time, it worked spectacularly, turning Strategy into a Bitcoin proxy that often rose faster than Bitcoin itself.

In late June 2026, that engine threw itself into reverse. Bitcoin crashed below $60,000, Strategy’s stock fell beneath the value of its own Bitcoin, and the loop that had compounded gains on the way up began compounding pressure on the way down.

This piece explains how the flywheel works, why a falling price flips it into a doom loop, and whether Saylor is genuinely trapped or merely strained.

The reason this matters far beyond one company is that Strategy is the template. Hundreds of imitators built Bitcoin and crypto treasury companies on the same premium-driven logic, and the entire category has never faced a real test of what happens when the premium evaporates, and the price of the underlying asset sits below cost.

Strategy is now running that experiment in public, with its stock at a multi-year low, a stack of preferred shares trading below their face value, a dividend bill that has quadrupled in six months, and analysts openly debating whether the company can keep funding itself without selling the Bitcoin on which its entire identity is built, never selling.

The mechanics are intricate, but the core story is one of reflexivity, a feedback loop that amplifies whatever direction the market is already moving, and the lesson it is teaching is that a flywheel is only a flywheel while the premium holds.

The machine that made Strategy the biggest Bitcoin holder on earth

To understand why Strategy is in trouble, you first have to understand why it worked so well, because the same mechanism does both. The key number is something analysts call mNAV, shorthand for the ratio between the company’s market value and the net asset value of the Bitcoin it holds.

When mNAV is above one, the stock trades at a premium: investors are paying more for a share of Strategy than the Bitcoin behind that share is worth. That premium is the fuel for the entire engine. When the stock trades above the value of its Bitcoin, Strategy can issue new shares into the market, raise cash at that elevated price, spend the cash on more Bitcoin, and end up with more Bitcoin per share than it started with, even after the new shares dilute the count. Existing shareholders come out ahead, the higher Bitcoin-per-share figure justifies the premium, and the company can do it all again.

This is the flywheel, and for years it spun in Strategy’s favor with remarkable force. Every time Bitcoin rose, the premium tended to widen, which let Strategy raise more capital on better terms, which bought more Bitcoin, which lifted Bitcoin-per-share and the stock alongside it.

The company layered on a second source of fuel, a series of preferred stock instruments that let it raise money without diluting common shareholders directly, expanding the machine’s capacity. By accumulating relentlessly through this loop, Strategy built a position of more than 847,000 Bitcoin, acquired at an average price of roughly $76,000 per coin, and turned itself into the way many investors chose to hold leveraged exposure to Bitcoin through a regular brokerage account.

Saylor made perpetual accumulation the company’s whole identity, and the premium-funded flywheel was the mechanism that made the accumulation possible. The crucial thing to notice, the thing that explains everything that followed, is that the entire machine depends on that premium. Take away the premium, and the engine does not just slow down. It runs backward.

The week the premium died

That is precisely what happened in the final week of June 2026, and the speed of it caught even seasoned observers off guard. Bitcoin, which had been grinding lower for weeks beneath all of its major moving averages, broke hard, falling to around $59,000 in its worst single-day drop in months, a decline of roughly 5% that triggered a cascade of forced liquidations across crypto derivatives markets, with about $1.1 billion of leveraged positions wiped out in a single day. Strategy fell with it, as it almost always does, but it fell further.

The stock dropped more than 10% to around $92, then slid the next session again, breaking below $100 for the first time since early 2024 and hitting a two-and-a-half-year low. From its peak, the stock had lost roughly 81% of its value, erasing on the order of $150 billion in market capitalization.

The number that mattered most, though, was not the stock price or even the Bitcoin price. It was the mNAV, which fell to approximately 0.8. Strategy was now trading at a discount to its own Bitcoin: the market valued the company at less than the coins on its balance sheet were worth.

For a company whose entire model rests on trading at a premium, crossing below 1 is not a cosmetic change but a structural one, because it disables the engine. And it disabled both halves of that engine at once. With the common stock below the value of its Bitcoin, issuing new shares would destroy Bitcoin-per-share rather than build it.

With the preferred shares trading well below their face value, raising money through new preferred issuance had become punishingly expensive. Both capital taps, the two ways Strategy funds itself, were constrained at the same moment, and the company found itself holding more than 847,000 Bitcoin bought at an average price far above the current one, sitting on an estimated $10.6 billion in unrealized losses, with every coin it purchased in 2024, 2025, and 2026 underwater. The premium that powered the flywheel was gone, and without it, the machine had nothing to run on.

Why a discount breaks the flywheel

It is worth being precise about why crossing below an mNAV of one is so damaging, because the reversal is not merely the absence of the previous tailwind; it is an active headwind. Run the flywheel logic backward, and the problem becomes clear.

At a premium, issuing stock to buy Bitcoin increases Bitcoin-per-share, which helps shareholders. At a discount, the same action does the opposite: if the company issues shares below the value of its Bitcoin and uses the proceeds to buy more, each existing share ends up backed by less Bitcoin than before, not more, because the new shares were sold for less than the Bitcoin they represent.

The accretive loop becomes a dilutive one. The single most important tool Strategy used to grow now actively harms the shareholders it is meant to serve, which means the company effectively cannot use it. The equity engine does not just idle at a discount; it goes into reverse if switched on.

The preferred-stock engine suffers a parallel breakdown. Strategy’s preferred instruments were designed to raise money efficiently, but that efficiency depended on those instruments trading at or above their face value. When they slip well below face value, the company can only issue new ones by effectively promising a much higher yield, which makes the funding expensive and, past a point, impractical. So the second tap tightens just as the first one closes.

The result is a company that, at the very moment its Bitcoin is underwater, and its cash needs are rising, has lost the two mechanisms it relied on to raise money. This is the essence of reflexivity, the property that makes the model so powerful in both directions.

On the way up, a rising price widens the premium, which eases funding, which buys more Bitcoin, which lifts the price further. On the way down, a falling price kills the premium, which chokes funding, which raises the specter of selling Bitcoin to cover obligations, which threatens to push the price down further still. The machine is built to amplify, and amplification is wonderful until the direction changes.

STRC: the funding engine that stalled

Nowhere is the stall more visible than in the preferred instrument Strategy nicknamed Stretch, which trades under the ticker STRC and has become the clearest barometer of the company’s stress.

STRC is a perpetual preferred stock, meaning it has no maturity date, with a variable dividend rate that the company resets monthly with the explicit goal of keeping the security trading near its $100 face value.

Strategy launched it in mid-2025 through an offering that raised roughly $2.5 billion, marketing it to income-seeking investors as something close to a high-yield savings account, a stable instrument paying a generous dividend, recently around 11.5%, distributed in cash twice a month.

As a fundraising engine, STRC was meant to let Strategy raise money to buy Bitcoin without diluting common shareholders, and it worked beautifully while it traded at or above face value.

In June 2026, STRC broke down. It fell to record lows near the low 80s, roughly 17% below its face value, and that gap is what signals the engine has stalled. The loop only works above par: when STRC trades above $100, Strategy can issue new shares and funnel the proceeds into Bitcoin cheaply. Below par, that mechanism breaks, because issuing new preferred stock at a discount means accepting a far higher effective cost of capital.

The decline also drew a pointed accusation from longtime Bitcoin critic Peter Schiff, who argued that Saylor had marketed STRC to risk-averse retirees by assuring them the volatility had been stripped out, and that with the instrument now well below what many paid for it, erasing close to two years of dividends in price terms, the company had made material misrepresentations. Strategy’s defenders counter that the dividend rate resets precisely to pull the price back toward par over time, and that the decline reflects the market demanding a higher yield in a stressed environment rather than a fundamental break.

Either way, the practical reality is the same: the instrument designed to be Strategy’s smooth, reliable funding engine is sputtering, and a sputtering STRC means the company has lost its least dilutive way to raise cash at the worst possible time.

The dividend bill nobody is talking about enough

While the headlines fixate on the Bitcoin price and the stock, the more immediate pressure on Strategy is something quieter and arguably more dangerous: a cash squeeze created by its own dividend obligations. As Strategy issued more and more preferred stock to fund its Bitcoin buying, it accumulated a growing stack of instruments, STRC alongside others trading under tickers like STRK, STRF, STRD, and STRE, each carrying a dividend that must be paid in cash.

The combined annual obligation across all of them has ballooned from roughly $300 million at the start of 2026 to approximately $1.2 billion by June, a near fourfold increase in under six months. That is $1.2 billion a year the company must pay out, regardless of what Bitcoin does, regardless of whether its stock trades at a premium or a discount.

Against that rising bill, the company’s cash cushion has shrunk. Strategy’s dollar reserves fell by about 38% over the first half of 2026, partly because it spent roughly $1.5 billion in May buying back convertible notes, draining the very buffer that supports the dividends. The result is a metric that has deteriorated alarmingly: dividend coverage, a measure of how long the cash reserve could keep funding the payouts, collapsed from more than seven years to around 14 months.

One prominent analytics firm calculated that Strategy would need to rebuild its reserves to roughly $2.8 billion to restore a comfortable two years of coverage, and urged the company to halt Bitcoin purchases entirely until it does.

The squeeze is structural and self-inflicted: the more preferred stock Strategy issued to buy Bitcoin, the larger its perpetual cash obligations grew, and those obligations do not pause when Bitcoin falls. Crucially, the dividends are cumulative, meaning any payment Strategy skips still has to be made up later, so the company cannot simply switch them off to conserve cash without damaging its standing with the investors it depends on.

This is the real near-term pressure point. It is not that Bitcoin is down; it is that the bills come due in dollars, the dollar reserve is shrinking, and the usual ways of refilling it have stopped working.

The 32-Bitcoin sale that said everything

The moment that crystallized the market’s anxiety was almost comically small in scale. In late May and early June 2026, Strategy sold 32 Bitcoin, worth around $2.5 million, to help fund a distribution on its preferred stock.

Against a holding of more than 847,000 coins, 32 Bitcoin is a rounding error, a fraction of a fraction of the stack. And yet the disclosure sent a shock through the market, with Strategy’s shares falling more than 9% in a single session and Bitcoin itself sliding on the news. The reaction was wildly out of proportion to the size of the sale, which is exactly what made it significant.

The reason a negligible sale moved the market so much is that it broke a narrative. For years, Saylor’s defining promise was that Strategy buys Bitcoin and never sells it, that the company is a one-way accumulation vehicle whose conviction is absolute. The 32-coin sale, however tiny, was the first time in roughly 4 years that Strategy had sold any Bitcoin at all, and it was sold not opportunistically but to cover a cash obligation.

The company framed it as a demonstration of strength, proof that it could meet its dividend commitments through asset sales if needed. The market read it the opposite way: as the first visible crack in the never-sell promise, and as confirmation that the dividend machine had grown large enough to force sales of the asset it was built to accumulate.

A treasury company that has to sell its treasury to pay its bills has crossed a psychological line, and the size of the sale is almost beside the point. What investors saw was the principle giving way, and the principle was the whole story. Once the market accepts that Strategy will sell Bitcoin to meet obligations, the only remaining question is how much and how often, and that question hangs over everything.

Is Saylor actually trapped?

This brings us to the word that has attached itself to Saylor’s situation: trapped.

The trap thesis, laid out by several analysts, runs like this. Strategy cannot effectively buy, because at a discount, raising money to purchase Bitcoin destroys shareholder value rather than creating it. It cannot easily sell, because dumping Bitcoin would crystallize billions in losses and, given Strategy’s size, would likely push the Bitcoin price down further, deepening the very problem it is trying to solve and harming the asset that underpins the entire structure. And it cannot comfortably stand still, because the dividend obligations keep coming due in cash, the reserve keeps shrinking, and the preferred shares keep signaling stress.

One veteran portfolio manager assigned rough odds to the outcomes, putting his base case at a 70% chance that Strategy keeps selling small amounts of stock at unfavorable, non-accretive levels, slowly grinding the mNAV down toward an even steeper discount, with a smaller chance that Saylor sells several billion dollars of Bitcoin outright to buy time. In this reading, every available move makes some part of the structure worse, which is what a trap means.

The case against the trap framing deserves equal weight, because the situation, while genuinely strained, is not the same as imminent collapse, and several analysts argue exactly that. Forced selling is not actually required right now. Strategy is not contractually obligated to sell Bitcoin to defend its preferred shares; it can raise the dividend rate, issue shares even at unattractive levels, or use other tools to signal it can keep paying, and it has been doing so. It still holds an enormous, unencumbered Bitcoin position and retains real flexibility.

One prominent equity analyst reiterated a buy rating with a price target far above the current level, describing the preferred-stock decline as a market-driven reset of the yield investors require instead of a structural breakdown, a sign of a model strained but not broken.

Saylor himself points out that, despite the brutal drawdown, the stock remains a multiple of where it traded when he began buying Bitcoin in 2020, and that the company’s long-term objective is to maximize Bitcoin per share over the years, not to defend any particular monthly price. And the entire predicament reverses if Bitcoin simply recovers: a rising price would restore the premium, reopen the funding taps, and turn the flywheel forward again.

The honest assessment is that Strategy is under real, compounding pressure with a narrowing set of good options, which is a serious condition, but it is not yet insolvency, and conflating strain with doom is its own kind of error.

The 2027 wall and the price that has to hold

If you want to know what the market is really watching for, look past the daily price swings to a specific date and a specific number. Strategy carries debt, and one analyst has flagged roughly $1 billion of it maturing in September 2027.

To repay that obligation without selling Bitcoin, the reasoning goes, Strategy’s stock would need to trade above roughly $183, a level that corresponds to a Bitcoin price somewhere around $91,500 at an mNAV of one.

With the stock near or below $100 and Bitcoin around $60,000, the company sits far below that threshold, which is why the 2027 maturity has become a focal point. It is not an immediate crisis, since the date is more than a year out and Strategy has tools and time, but it functions as a deadline against which all the other pressures are measured. The runway is real, but it is not unlimited.

This frames the two scenarios cleanly. In the recovery scenario, Bitcoin climbs back over the months ahead, Strategy’s stock returns to a premium, the funding engine reopens, the preferred shares drift back toward par, and the dividend coverage rebuilds, at which point the trap dissolves, and the flywheel resumes spinning forward, exactly as it has after previous Bitcoin downturns.

Saylor’s entire bet is that this is what happens, that Bitcoin’s long-term trajectory rescues the structure as it always has before, and that conviction through the drawdown is the price of the eventual recovery.

In the adverse scenario, Bitcoin stays low or falls further, the discount persists, STRC remains below par, the cash reserve keeps shrinking against the $1.2 billion dividend bill, and Strategy is forced into steady, value-destroying sales of stock or, eventually, Bitcoin, grinding the structure down toward the 2027 wall in a weakened state.

The truth is that no one knows which path unfolds, because it depends overwhelmingly on the one variable Saylor cannot control, the price of Bitcoin. What can be said is that the model has lost its margin for error. For years, the flywheel gave Strategy the luxury of never having to be right about timing. Now, for the first time, timing matters, and the company is waiting on a price recovery it can only hope for.

What it means beyond Strategy

Step back from the single company and the larger significance comes into focus, because Strategy is not an isolated case but the original of a type. Its success spawned a wave of imitators, more than 200 Bitcoin and crypto treasury companies built on the identical premium-driven logic, each raising capital against a market premium to its holdings and buying more of the underlying asset, each implicitly assuming the premium would persist.

None of these companies had truly been tested by a sustained environment in which the underlying asset trades below their cost and the premium turns into a discount, because that environment had not arrived at scale.

Now it has, and Strategy, as the largest and most leveraged example, is the stress test the entire category is watching. What breaks or holds at Strategy tells every imitator something about the durability of the model they copied.

The deeper lesson is about the nature of reflexivity itself, and it is a lesson that applies to far more than Bitcoin treasuries. A reflexive machine, one whose inputs feed its outputs feed its inputs, is a wealth-compounding marvel while the cycle runs in your favor and a value-destroying trap when it runs against you, and the same features that make it powerful in one direction make it dangerous in the other.

Strategy’s flywheel did not change; the direction did, and that was enough to convert the most admired financial engine in crypto into a structure that analysts now describe with words like pickle and trap. Whether Saylor escapes depends on Bitcoin, and Bitcoin has rescued him before, which is why writing the company off would be as foolish as assuming it is invincible.

The honest watch list is short and specific: whether the mNAV climbs back above one, whether STRC reclaims its par value, whether the dividend coverage stabilizes, whether the company sells more Bitcoin, and above all, whether Bitcoin’s price recovers in time. Until those questions resolve, the machine that built the largest corporate Bitcoin position on earth is spinning in reverse, and everyone who copied it is watching to see how far backward it goes.

Frequently Asked Questions

What is mNAV and why does it matter for Strategy?

mNAV is the ratio between Strategy’s market value and the net asset value of the Bitcoin it holds. Above 1, the stock trades at a premium to its Bitcoin, which lets the company issue shares above that value, buy more Bitcoin, and increase Bitcoin per share, the loop that powered its growth. In June 2026, mNAV fell to about 0.8, meaning the stock trades at a discount to its own Bitcoin. That breaks the engine, because issuing shares at a discount destroys Bitcoin per share instead of building it, disabling Strategy’s main way of funding itself.

Why is Strategy’s flywheel now working against it?

Because the model is reflexive, amplifying whatever direction the market is moving. At a premium, a rising Bitcoin price widens the premium, eases funding, and buys more Bitcoin, lifting the stock further. At a discount, a falling price kills the premium, chokes funding, and raises the prospect of selling Bitcoin to cover obligations, which can push the price down further. The same mechanism that compounded gains on the way up now compounds pressure on the way down. Both of Strategy’s funding taps, common equity and preferred stock, are constrained at once because the stock trades below its Bitcoin value.

What is STRC and why is its price important?

STRC, nicknamed Stretch, is Strategy’s perpetual preferred stock, with a variable dividend reset monthly to keep it trading near its one-hundred-dollar face value. It was a key fundraising engine: when it trades above face value, Strategy can issue more and buy Bitcoin cheaply without diluting common shareholders. In June 2026, it fell to record lows near the low eighties, well below par, which breaks that mechanism, because issuing new preferred at a discount means a much higher cost of capital. Its slide is the clearest market signal that Strategy’s smoothest funding source has stalled.

Is Michael Saylor being forced to sell Bitcoin?

Not in a forced, contractual sense, at least not yet. Strategy did sell thirty-two Bitcoin in mid-2026 to fund a dividend, its first sale in about four years, which alarmed the market as a symbolic break from its never-sell stance. But the company is not required to sell to defend its preferred shares; it can raise the dividend rate, issue shares, or use other tools, and it retains a large, unencumbered Bitcoin position. The risk is that persistent stress leads to steady, value-destroying sales over time. Analysts consider a near-term forced liquidation unlikely, while disagreeing on how much pressure builds from here.

Why did selling just 32 Bitcoin matter so much?

Because it broke a narrative instead of a balance sheet. 32 Bitcoin is a rounding error against Strategy’s 847,000-coin stack, but it was the first sale in roughly four years and was made to cover a cash obligation, not to take profit. Saylor’s defining promise was that Strategy buys and never sells, so any sale, however small, signaled that the dividend machine had grown large enough to force sales of the asset it exists to accumulate. Once the market saw the never-sell principle give way, the only remaining questions were how much and how often, which is why a tiny sale moved the stock sharply.

Could Strategy recover, or is the model broken?

It could recover, and the outcome depends overwhelmingly on Bitcoin’s price, which Saylor cannot control. If Bitcoin climbs back, the premium returns, the funding taps reopen, the preferred shares drift toward par, and the flywheel resumes spinning forward, as it has after past downturns. If Bitcoin stays low, the discount persists, the cash squeeze from a $1.2 billion dividend bill worsens, and the company faces steady, value-destroying sales heading toward a roughly $1 billion debt maturity in 2027. Some analysts call the model strained but not broken; others see a trap. The honest answer is that the margin for error is gone, and timing now matters.

This article is information, not investment advice. It describes a fast-moving and contested situation, and prices, holdings, dividend obligations, and analyst views change quickly. Figures reflect reporting available as of June 25, 2026. Cryptocurrency and equities are volatile, and nothing here is a recommendation to buy or sell any asset. Verify current data from primary sources and consider your own circumstances before making any decision.

Crypto World

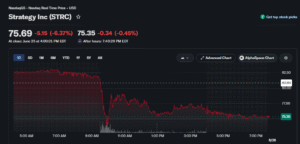

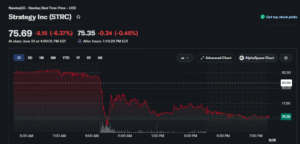

Rosen Law Firm Investigates MicroStrategy Over Michael Saylor’s Alleged Misleading Claims on STRC

TLDR:

- Rosen Law Firm has launched a securities investigation into MicroStrategy over alleged misleading STRC claims by Michael Saylor.

- STRC preferred stock has dropped over 22% from its $100 par value, trading as low as the low $80s in June 2026.

- Strategy’s annualized STRC dividend rate has climbed to 11.50%, adding tens of millions in additional annual payout obligations.

- Strategy sold 32 BTC in late May 2026 to cover dividends, marking its first disclosed net Bitcoin disposal in years.

Rosen Law Firm has opened a formal investigation into MicroStrategy, now rebranded as Strategy Inc., over potential securities claims tied to STRC preferred stock.

The probe follows allegations that co-founder Michael Saylor made misleading promises of guaranteed returns to investors.

STRC has since dropped over 25% from its $100 par value. Shareholders holding MSTR common stock and preferred securities: STRF, STRC, STRK, and STRD are covered under the investigation.

Rosen Law Firm Targets Saylor’s Alleged Misleading Promises to STRC Investors

Rosen Law Firm is preparing a class action to recover losses for affected Strategy investors. The investigation centers on whether Saylor’s public statements on STRC constituted materially misleading business information.

Investors who purchased Strategy securities may be entitled to compensation through a contingency fee arrangement, with no out-of-pocket costs required.

The firm directed affected investors to take immediate action. “To join the prospective class action, go to rosenlegal.com/cases/strategy-inc/join or call Phillip Kim, Esq. toll-free at 866-767-3653 or email case@rosenlegal.com for information on the class action,” the firm stated in its announcement.

Rosen Law Firm has a documented track record in securities class action litigation. The firm ranked No. 1 by ISS Securities Class Action Services for the number of settlements in 2017 and has remained in the top four each year since 2013. It has recovered hundreds of millions of dollars for investors globally, securing over $438 million in 2019 alone.

The investigation comes as MSTR common shares have fallen to a 28-month low in June 2026. Losses on MSTR have far exceeded Bitcoin’s own drawdown over the same period.

This widening gap has drawn fresh scrutiny toward the company’s leveraged Bitcoin acquisition model and Saylor’s public representations to investors.

STRC Preferred Stock Collapse Raises Questions on Strategy’s Sustainability

STRC has traded as low as the low $75s in recent sessions, down more than 25% from its $100 par value target. The preferred stock was originally structured to provide stable, low-cost funding for Bitcoin purchases. That structure has since deteriorated under sustained market pressure throughout June 2026.

Source: YahooFinance

The firm underlined the importance of selecting experienced legal counsel for affected investors. “We encourage investors to select qualified counsel with a track record of success in leadership roles,” Rosen Law Firm noted, adding that many firms issuing similar notices lack comparable experience or meaningful peer recognition.

Under STRC’s contractual terms, when the stock falls below the $95 threshold, the dividend rate increases by 0.5% increments.

The annualized rate currently sits at 11.50%, with effective yields climbing higher due to the discounted trading price. Additional annual payout obligations are now estimated in the tens of millions of dollars.

Strategy’s cash cushion supporting these dividends has narrowed sharply from multi-year coverage to roughly 14 months in some analyst estimates.

The company also sold 32 BTC in late May 2026 to help cover dividend payments: the first disclosed net Bitcoin disposal in years.

Unrealized paper losses on Strategy’s Bitcoin holdings are reported to exceed $10 billion, as questions around capital sustainability and the company’s broader Bitcoin development narrative continue to grow.

Sharplink, the Ethereum treasury company, has made its first Ether purchase in eight months as ETH slid to the lowest level seen this year. The move highlights how corporate balance-sheet strategies can continue even when broader market momentum weakens.

According to on-chain data tracked by Arkham, a wallet associated with Sharplink received 5,000 ETH on Thursday via crypto prime brokerage FalconX. Arkham data places the transaction at roughly $7.85 million. FalconX was last recorded supplying Sharplink with ETH on Oct. 26, when the company bought $78.3 million worth of Ether.

Key takeaways

- Sharplink bought 5,000 ETH on Thursday, marking its first Ether acquisition in about eight months.

- The purchase comes as Ether fell to $1,537—its lowest price level reported for 2026.

- Arkham’s on-chain records show FalconX was also the execution partner on Sharplink’s previous reported ETH buy on Oct. 26.

- Sharplink’s Ether strategy is tied to a multi-factor thesis that includes US stablecoin/crypto regulatory progress and continued real-world asset tokenization.

- The company is also expected to be added to the Russell 2000 and Russell 3000 indexes, a development investors may watch for potential capital-market spillovers.

A corporate buy at ETH’s 2026 low

Ether’s decline to $1,537 on Thursday provides the immediate backdrop for Sharplink’s latest treasury action. While the broader market reaction is typically measured by price and volatility, the company’s decision points to a different lens: steady accumulation even during softer conditions.

Bitrue Research Institute’s Andri Fauzan Adziima characterized the behavior as evidence of ongoing corporate conviction. “I’m seeing genuine corporate accumulation conviction holding strong amid subdued price action,” Adziima told Cointelegraph.

In other words, the purchase aligns with a pattern that treasury operators often follow—building positions when liquidity is available and valuations are comparatively depressed—rather than waiting for a market uptrend to begin. Traders may therefore interpret Thursday’s on-chain activity as a signal that Sharplink sees more than just short-term price pressure in its Ether holdings.

What Sharplink has previously pointed to

The latest buy also fits with remarks made by Sharplink CEO Joseph Chalom earlier this year. In May, he outlined three catalysts he believed could support Ether’s outlook.

First, Chalom pointed to the US CLARITY Act. Second, he connected potential upside to a renewed appetite for market risk, which he said would depend on easing geopolitical tensions and a cooling of the “artificial intelligence investment thesis.” Third, he emphasized continued expansion in real-world asset (RWA) tokenization.

That regulatory and tokenization framework remains a central uncertainty. While the Senate has not yet voted on its version of the CLARITY Act, the House Financial Services Committee said it plans to hold a hearing on July 17.

The political and market assumptions around these catalysts are also moving targets. The article notes that the US and Iran are working toward a final peace agreement to end months of conflict. Separately, tokenized real-world assets have reportedly reached a distributed asset value of $31.55 billion, approaching what the source describes as the highest level seen this year.

Sharplink’s Ether position and rivals’ momentum

Sharplink’s latest transaction comes as it continues to build a sizable Ether balance. Founded in 2019 as an affiliate marketing service provider for sports betting and gambling industries, the company pivoted to become an Ethereum treasury business in June 2025. Consensys co-founder and CEO Joe Lubin was named chairman at that time.

At its peak, Sharplink was described as the largest publicly traded corporate holder of ETH, though it later lost that top position to Bitmine in August—just two months after Bitmine launched its own Ether buying strategy.

The company now holds 876,285 ETH and ETH equivalents accumulated through a combination of active purchases and staking rewards, the source reports. Bitmine, by comparison, is reported to hold 5.67 million ETH after acquiring an additional 52,203 ETH last week.

Bitmine chairman Tom Lee added context around the broader timing of accumulation, saying the company “continue[s] to maintain a steady pace of accumulation throughout 2026” and that it believes “we are in the early stages of crypto spring.”

Corporate treasury strategy meets public-market access

Beyond the on-chain buy, Sharplink is approaching a different milestone: its expected inclusion in the Russell 2000 and Russell 3000 indexes on Monday. Index additions are often viewed as meaningful because many passive and active funds—including exchange-traded funds—tend to rebalance holdings around such changes.

In May, Chalom said joining the Russell indexes would broaden Sharplink’s shareholder base and strengthen access to capital markets. For investors, the combination of a continuing treasury accumulation plan and wider index-driven visibility could matter, particularly for those tracking how crypto-linked equities integrate into mainstream portfolios.

Looking ahead, readers should watch whether Sharplink’s renewed buying pace persists beyond this single reported transaction—especially as US regulatory timelines around the CLARITY Act and shifting macro conditions influence risk appetite. The next on-chain confirmations and how the market responds to index inclusion may offer additional clues about whether this “accumulation conviction” translates into a sustained corporate bid for Ether.

Stablecoin infrastructure company StablecoinX has completed its merger with TLGY Acquisition Corp, a publicly traded special purpose acquisition company, allowing it to begin trading on Nasdaq on Friday.

StablecoinX is the first public stablecoin infrastructure company focused on supporting the Ethena ecosystem through decentralized verifier nodes and software infrastructure, and will trade under the symbol “USDE,” according to a statement on Thursday.

“We believe Ethena has emerged as one of the most important platforms powering the next generation of digital dollars,” said Edward Chen, CEO and Chairman of StablecoinX.

The Nasdaq debut is a big bet that stablecoins are becoming the plumbing of global finance, and comes despite a broader crypto bear market and Ethena’s relatively small 1.4% market share of the stablecoin market compared with those offered by its competitors, such as Tether and Circle.

Ethena’s USDe is a yield-bearing synthetic dollar-pegged stablecoin. Unlike USDt (USDT) or USDC (USDC), which are backed by actual dollars, USDe (USDE) maintains its $1 peg through a derivatives strategy.

It is backed by crypto collateral in Bitcoin and Ether and short futures positions on those same assets, enabling the long and short positions to cancel out the price volatility, helping to keep its value at approximately $1.

Ethena’s delta-neutral strategy works well in normal markets but is vulnerable during periods when futures funding rates go negative.

USDe supply falls

While stablecoin circulation has grown in recent years, USDe market capitalization has declined by 70% since its peak in October to around $4.5 billion today, ranking it sixth among stablecoins.

USDe supply has fallen since the bull market peak. Source: CoinGecko

StablecoinX’s treasury also holds approximately 3 billion Ethena governance tokens (ENA), or around 20% of the total supply, valued at approximately $275 million. The company announced a $360 million capital raise to purchase ENA on Sunday.

However, the asset is currently trading at $0.08, down 94% from its April 2024 all-time high.

Related: Yield-bearing stablecoins surge as Washington fights over yield

The company has three business lines: a decentralized verifier node (DVN) serving as a cross-chain message verifier for the Ethena ecosystem, a middleware software stack called “Stablecoin Harness” and distribution services, which are currently in development.

The company says the three businesses reinforce one another, though the broader crypto bear market presents a challenging backdrop for its Nasdaq debut.

Crypto SPACs and crypto treasuries have had a tough time this year as the broader market has tanked 52%, with $2.3 trillion leaving the space since October and crypto falling out of favor among investors.

Pre-merger TLGY fell 6.93% on Thursday on OTC markets to end the day trading at $9.40, according to Google Finance data.

Magazine: AI is banking the unbanked in Africa… faster than crypto

More than half of UK wealth advisors say most of their clients’ crypto holdings sit outside their oversight. A new CoinShares survey blames firm policy, not investor appetite or advisor knowledge.

The poll of 261 wealth professionals across France, Germany, Italy, Switzerland and the UK found 52% of British advisors report a management gap above 50%. Across Europe, one in four faces the same blind spot.

Firm Policy Drives the Crypto Blind Spot

The survey defines the management gap as the share of a client’s digital asset exposure that an advisor cannot see. Holdings on personal exchanges or self-custody wallets fall outside the advisory relationship.

The report ties the gap to one factor. Some 61% of advisors work at firms that restrict digital assets or give no internal guidance. In those firms, active recommendation drops to 1%, against 48% at firms with clear support.

The gap moves the other way, from 4% at supportive firms to 34% at restrictive ones. CoinShares put the unmanaged exposure 8.5 times wider in blocked firms, the basis for its wrong-way risk warning.

The knowledge gap tracks the same line. More than three-quarters of advisors who call themselves under-informed work at blocked firms. That suggests training follows firm policy rather than the reverse.

The pattern is sharpest in the UK, which posts the widest gap even as domestic crypto regulation reforms advance.

“This is not a knowledge problem. It is not a demand problem. It is a firm-policy problem becoming a wrong-way risk,” Jean-Marie Mognetti, CoinShares co-founder and CEO said in the report.

Follow us on X to get the latest news as it happens

Advisors Want Access, Not Training

Asked what would raise their confidence, advisors pointed to structural change. Regulatory recognition of digital assets as a mainstream asset class ranked first at 45%. Access to exchange-traded products (ETPs) followed at 43%.

CoinShares commissioned the survey through Citywire. The firm is itself a Nasdaq-listed issuer of crypto ETPs, the access advisors ranked second.

Client-facing educational tools ranked last at 9%. The split suggests the barrier is institutional, since neither recognition nor product access is something an advisor can deliver alone. A broader EU crypto rules review is now testing how the framework performs.

Regulation Could Close the Gap

Britain’s stance has shifted fast. The Financial Conduct Authority banned retail sales of crypto exchange-traded notes in January 2021. It reopened retail crypto ETN access in October 2025. The regulator has since proposed letting authorized funds hold up to 10% in those products.

On the continent, the Markets in Crypto-Assets (MiCA) transition ends on July 1. The shift creates a single European crypto market for regulated products. France’s financial regulator, the AMF, has opened a review of which assets qualify for UCITS funds. Digital assets still make up a sliver of Europe’s roughly €15 trillion regulated retail fund market.

Italy offers a counterpoint. Its advisor-led retail model records the lowest gap in the survey at 12%. With the MiCA July deadline approaching, engagement is converting demand into managed exposure there.

For wealth firms, the cost of waiting is rising. An estimated £1 trillion ($1.3 trillion) will pass to the UK’s next generation within a decade. Advisors who cannot see a client’s crypto risk losing the account as it changes hands.

Up to 8% already report rising client interest alongside an unmanaged majority, a sign clients are not waiting. The coming year of rule changes may decide who keeps that wealth in view.

The post About 50% of UK Wealth Advisors Cannot See Most of Their Clients’ Crypto Holdings appeared first on BeInCrypto.

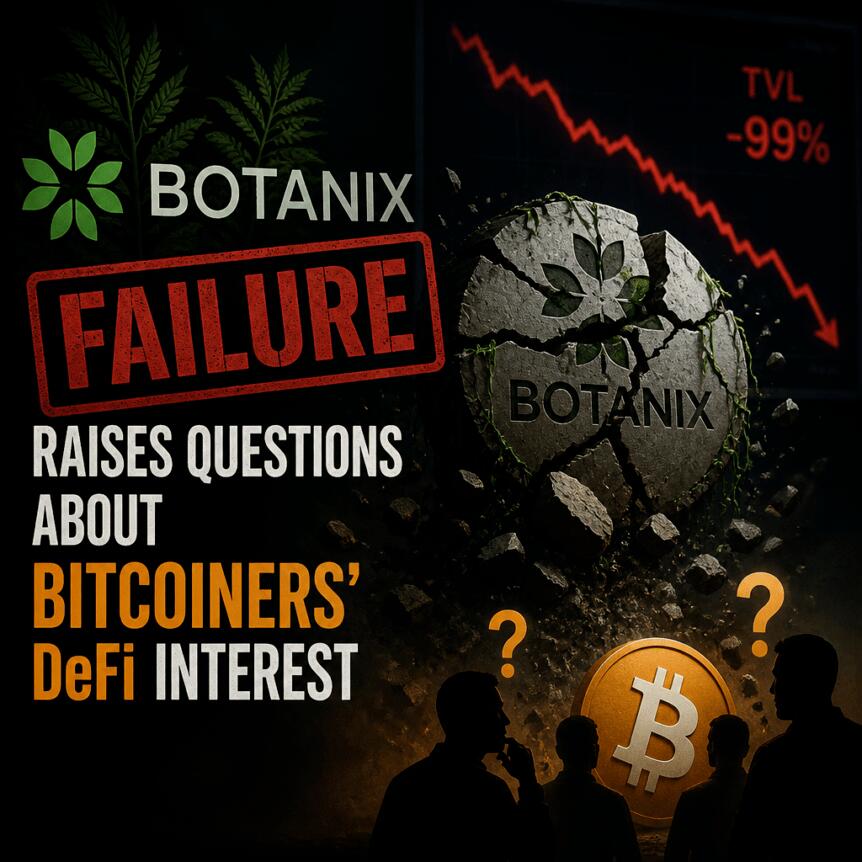

Bitcoin DeFi is struggling to move beyond the promise stage, and the shutdown of Botanix earlier this month has become a new stress test for the idea of “programmable Bitcoin.” The closure—after nearly four years of work and about a year of mainnet uptime—raises a hard question for builders: if a well-funded, technically ambitious Bitcoin scaling project with live applications and competitive yields can’t sustain usage, is decentralized finance actually in Bitcoin’s roadmap in the way advocates expected?

Data from DefiLlama suggests the scale remains small. Total value locked (TVL) across Bitcoin DeFi protocols is about $4.12 billion, a figure that’s tiny relative to Bitcoin’s roughly $1.2 trillion market capitalization and far smaller than the value managed through spot Bitcoin exchange-traded funds, corporate treasuries, and custodial accounts. As Bitwise’s Andre Dragosch put it in comments to Cointelegraph, Bitcoin’s strength as “pristine collateral” has outpaced the plausibility of Bitcoin as a standalone DeFi execution layer.

Key takeaways

- Botanix shut down citing insufficient demand for the network’s yield and activity to cover ongoing infrastructure costs.

- Bitcoin DeFi TVL remains comparatively small, with DefiLlama placing it at about $4.12 billion across protocols.

- Wrapped BTC on large, liquid Ethereum-compatible venues continues to outcompete Bitcoin-aligned execution chains on practical convenience and liquidity.

- Some builders argue the issue is structural—Bitcoin’s user base behaves more like reserve-asset holders than active DeFi traders.

- Other teams say the opportunity is real but depends on trust, institutional-grade risk frameworks, and Bitcoin-anchored designs rather than direct EVM cloning.

Botanix’s shutdown spotlights a demand problem

Botanix announced it was winding down without pointing to a hack or regulatory shock. Instead, the project attributed the decision to demand. According to the shutdown description, the chain “worked” technically: around 25 million transactions, roughly 200,000 wallets, and tens of millions of dollars in bridged funds. Yet those metrics did not translate into the fee volume needed to sustain the business.

The project’s co-founders pointed to a pattern familiar across parts of BTCFi: users often come for yield and treat BTC primarily as store-of-value collateral, then adopt passive strategies. When borrowing, trading, and frequent fund movements don’t happen at a scale large enough to generate consistent protocol fees, even solid technical execution can fail to reach economic viability.

As Botanix’s design reflects broader BTCFi infrastructure, users had to bridge Bitcoin into a tokenized representation on an Ethereum Virtual Machine (EVM)-based environment before accessing DeFi functionality. That additional bridge step—and the smart contract assumptions that come with it—remains a recurring friction point for Bitcoiners, even when a team argues its security model is more Bitcoin-aligned than typical wrapped BTC approaches.

Botanix co-founder Willem Schroé told Cointelegraph that he would not have changed the core architecture. In his view, the “best rates” the project offered were not enough to defeat the default utility of wrapped BTC on Ethereum. He attributed this outcome to Ethereum’s extensive infrastructure, entrenched liquidity, and longer-established “Lindy effect,” along with practical differences in user experience and regulatory comfort.

Why “native” Bitcoin DeFi hasn’t become mainstream

More broadly, Botanix’s experience reinforced a conclusion echoed by researchers: Bitcoin is still primarily treated as a reserve asset rather than a platform for programmable financial products. For many existing DeFi patterns—lending, leveraged exposure, and yield—wrapped BTC on established EVM ecosystems is described as “genuinely sufficient” for user needs.

That sufficiency matters because BTCFi alternatives frequently ask users to accept additional complexity: bridge risk, custody assumptions during tokenization, and the unfamiliarity of a smaller application ecosystem. When the liquidity, integrations, and trading venues are already available through wrapped BTC on major networks, users have less incentive to migrate to a dedicated Bitcoin-aligned execution layer.

The broader BTCFi landscape also appears to concentrate around venues that have “own the user relationship,” leaving independent infrastructure to row upstream against convenience and branding. In the same vein, activity consolidation on liquid venues can make it harder for smaller Bitcoin-specific projects to bootstrap the kind of fee-generating usage they need.

Quantitatively, the gap between hype and usage remains stark. A May 2026 analysis cited by Cointelegraph, based on a GoMining survey of 730 Bitcoin holders, reported that 77% had never used a BTCFi platform and only 3% had integrated BTCFi into their overall Bitcoin strategy. Even with the caveat that the sample consisted of engaged Bitcoin holders who opted into the survey, the results suggest BTCFi is still closer to a niche behavior than a mass-market routine.

Justin d’Anethan of Arctic Digital added that liquidity and yields on EVM or Solana Virtual Machine (SVM) native solutions often remain better than those offered by Bitcoin-specific approaches. He also described the real-world alternatives many clients use when they want to “put their Bitcoin to work,” including centralized desks and exchanges lending out BTC, basis-style structures, and institutional credit pools.

Are “standalone” Bitcoin DeFi layers the wrong target?

Andre Dragosch argued to Cointelegraph that Botanix’s failure points to a structural mismatch between where Bitcoiners allocate capital and what standalone Bitcoin DeFi execution layers require. In his framing, capital seeking yield has largely shifted toward wrapped BTC products on mature, liquid venues rather than bridging into bespoke federations.

For Dragosch, the key isn’t just that people haven’t “discovered” Bitcoin-native DeFi, but that the base-layer culture and design incentives of Bitcoin—slow, conservative, and aligned with store-of-value narratives—don’t naturally produce the kind of user demand that bespoke execution layers depend on.

That view implies a central tension: Bitcoin’s “reserve collateral” role may be driving the next wave of institutional adoption, while “onchain execution” is a separate goal requiring a different user base and different economic incentives. The next phase of adoption, Dragosch suggested, may run through institutions and balance sheets more than through new Bitcoin DeFi execution stacks.

Builders still see room—trust and Bitcoin-anchored design matter

Not everyone agrees that the problem is a lack of demand for Bitcoin-backed lending and yield, but there is a shared theme around trust and infrastructure readiness.

Diego Gutierrez Zaldivar, CEO of RootstockLabs—an EVM-compatible, Bitcoin-secured sidechain—disputed the idea that there is no demand for Bitcoin-linked DeFi services. He told Cointelegraph that the constraint is trust: institutions require operational, legal, and risk management frameworks that go beyond simply deploying smart contracts.

Zaldivar also claimed that more than 40% of Bitcoin DeFi activity runs through Rootstock, pointing to use cases such as real-world asset settlements and institutional vaults. He further said that flows involving hundreds or even thousands of BTC deposits have started to appear—something he said was rare only two or three years ago.

Meanwhile, Chainway Labs co-founder Orkun Mahir Kılıç, associated with Citrea, criticized the premise of cloning EVM DeFi primitives onto Bitcoin as a dead end. He argued Botanix’s outcome reflects a verdict on that approach rather than on Bitcoin DeFi itself. In his view, while “more secure” doesn’t automatically change user behavior, the security guarantee can be decisive for institutions and large holders who need trust-minimized transactions without a custodian to fail.

For other users, he suggested, the differentiator is not abstract security—it’s the presence of applications that genuinely aren’t available elsewhere.

As Bitcoin DeFi continues to test whether its economic model can survive outside Ethereum’s deepest liquidity, the key things to watch next are whether Bitcoin-anchored projects can sustain fee-generating usage without relying on passive collateral behavior, and whether institutional flows grow in ways that reduce the dependency on bridging and trusted intermediaries.

Kraken and Maple have teamed up to launch an onchain “warehouse financing” facility designed to support crypto-backed loans with a structure borrowed from traditional credit markets. The partnership aims to help Kraken expand its institutional lending operation while limiting the amount of balance-sheet capital it needs to deploy for each loan issuance.

In a Thursday announcement, the firms said the facility will fund Kraken’s OTC lending business using a bankruptcy-remote special purpose vehicle (SPV) and USDC-denominated financing. Maple is providing senior financing, while Kraken retains a stake in the transactions.

Key takeaways

- Kraken and Maple are applying a traditional warehouse/credit structure to crypto-backed lending, using a bankruptcy-remote SPV.

- Maple will supply senior financing for the loans, while Kraken will keep exposure through a retained stake.

- The facility is intended to allow collateral and loan performance tracking onchain, including Bitcoin and Ether-backed loans.

- Kraken affiliates are expected to originate, sell, and service loans, with third-party SPV administration by Zaria.

- The partners did not disclose the facility’s size or financing terms.

How the “onchain warehouse” structure works

Warehouse financing is a familiar concept in traditional markets: lenders provide capital that can support a stream of loans, while loan assets are packaged and managed in ways that can isolate risk. In this case, Kraken’s OTC lending is planned to be financed via an SPV intended to be “bankruptcy-remote,” meaning the loan collateral is structured so the borrower cannot simply file for bankruptcy to disrupt repayments and asset separation.

According to the announcement, Maple’s senior financing will be routed through the SPV, while Kraken will retain a stake. The SPV is also designed to support onchain transparency—Maple said the setup gives institutional lenders senior, overcollateralized exposure backed by Bitcoin and Ether, with collateral and loan performance tracked onchain.

That distinction matters for institutional participants who need predictable legal and operational processes in addition to technical visibility. Compared with many earlier crypto lending designs—often based on more direct counterparty structures—this approach borrows from established credit securitization mechanics to separate roles: originators, holders of collateral, financiers, and administrators.

Roles of Kraken Financial, Zaria, and Maple

The facility’s operational flow is split among several entities. Kraken affiliates will originate, sell, and service the loans while retaining a position in the transaction, according to the announcement.

Kraken Financial, described as a Wyoming-chartered Special Purpose Depository Institution, will hold the underlying collateral. Independent SPV administrator Zaria will oversee administration of the facility, while Maple provides senior financing through the SPV structure.

Kraken and Maple did not disclose the facility’s total size or any financial terms, leaving investors without key details such as leverage, pricing, or the expected scope of loan volumes. Those missing datapoints will likely be important for market participants assessing how “warehouse” capacity translates into real lending throughput.

Tokenized credit keeps pulling in institutional capital

The launch arrives as tokenized credit continues to broaden beyond early experiments. According to RWA.xyz data cited in the announcement, tokenized credit has grown to more than $6.2 billion in distributed value—up from roughly $1.87 billion a year ago. The same source is used to frame Maple as the largest platform in the sector, with approximately $1.4 billion in tokenized credit assets.

This matters because scaling tokenized lending depends on two linked developments: more institutional comfort with credit risk (including seniority and collateralization) and more infrastructure for tracking and managing loan performance. By tying credit exposure to onchain accounting while keeping the legal architecture anchored in an SPV, the partnership is positioning institutional lenders to evaluate risk with more real-time transparency than in purely offchain structures.

The firms’ move also fits into a broader post-2022 pattern in crypto finance, where lending businesses rebuilt after high-profile collapses. Failures involving Celsius and BlockFi, among others, accelerated scrutiny across counterparties, collateral practices, and liquidity management—pressuring the market to adopt more conservative structures and clearer risk segregation.

Broader lending momentum—and why it still isn’t uniform

Interest in tokenized credit has also been reinforced by mainstream finance research. Earlier coverage noted that in May, analysts at Bernstein suggested tokenized credit could be a large expansion vector for blockchain-based lending, estimating a potential addressable market of up to $4 trillion as tokenized credit expands beyond niche use cases into areas such as mortgages, auto loans, and small-business lending.

At the same time, not all lending is progressing evenly. While institutional-grade, collateralized products are gaining traction, parts of decentralized finance have faced setbacks. Earlier this month, lending protocol Radiant Capital said it would wind down after failing to recover from a $50 million exploit in 2024, citing an inability to replace lost funds or secure new capital. That contrast underlines a key tension in the sector: onchain lending is advancing where it can align incentives and reduce fragility, but many DeFi lending models still struggle when they encounter capital replacement and risk-control challenges.

In May, Kraken and Maple’s ecosystem context also included other moves toward tokenized lending capacity—such as Ripple securing a $200 million credit facility from Neuberger Berman to expand its institutional prime brokerage lending business. That financing was described as intended to support margin lending and other credit products for hedge funds, trading firms, and institutional clients. Together with the Kraken-Maple facility, these developments point to a recurring theme: regulated institutions and established asset managers are exploring credit lines and onchain settlement where they can better manage risk.

Going forward, the most important things to watch are whether the partnership reports concrete deployment figures—such as loan volume, onboarding pace, default or liquidation behavior, and how efficiently onchain tracking maps to real-world servicing—and whether other lenders adopt similar SPV-style architectures for crypto-backed credit. With the facility’s size and terms not yet disclosed, market participants will likely look for early operational signals to judge how quickly “onchain warehouse financing” can move from structure to sustained lending scale.

Ether treasury company Sharplink has bought Ether for the first time in eight months as the token sank to its lowest price this year on Thursday.

On-chain data from Arkham shows a wallet associated with Sharplink received 5,000 Ether (ETH), worth $7.85 million, from crypto prime brokerage FalconX on Thursday. The last time it received Ether from FalconX was on Oct. 26, when it bought $78.3 million worth of ETH.

The purchase comes as Ether hit $1,537 on Thursday, its lowest price in 2026. The latest purchase could suggest a revival of the company’s active Ether accumulation strategy.

“I’m seeing genuine corporate accumulation conviction holding strong amid subdued price action,” Andri Fauzan Adziima, the research lead at Bitrue Research Institute, told Cointelegraph.

Sharplink CEO Joseph Chalom told Cointelegraph in May that he saw three catalysts that could spur growth in the price of Ether.

The first was the passage of the CLARITY Act in the US, while the second was a return to market risk appetite, which will depend on an easing in geopolitical tension and cooling of the artificial intelligence investment thesis. Chalom’s third catalyst was the continued growth of real-world asset tokenization.

The Senate is yet to vote on its version of the CLARITY Act, and the House Financial Services Committee said it would hold a hearing on the bill on July 17. The US and Iran are working toward a final peace agreement to end months of conflict and tokenized real-world assets have now reached a distributed asset value of $31.55 billion, close to its highest level this year.

Sharplink now holds 876,285 ETH

Sharplink was founded in 2019 as an affiliate marketing service provider to the sports betting and gambling industries, but pivoted to become an Ethereum treasury company in June 2025, with Consensys co-founder and CEO Joe Lubin named as chairman.

It became the largest publicly traded corporate holder of ETH, but lost the title to Bitmine in August, just two months after Bitmine launched its own Ether buying strategy.

Related: Bitmine, Sharplink and Joe Lubin back Ethereum R&D nonprofit

The company now holds 876,285 ETH and ETH equivalents, which it has accumulated over time through active ETH purchases and staking rewards. Its competitor, Bitmine, holds 5.67 million ETH after acquiring another 52,203 ETH last week.

Source: Sharplink

“We continue to maintain a steady pace of accumulation throughout 2026. We believe we are in the early stages of crypto spring,” Bitmine chairman Tom Lee said.

Sharplink added to the Russell indexes

The purchase also comes just days before Sharplink is expected to join the Russell 2000 and Russell 3000 indexes on Monday.

Inclusion in the indexes is widely viewed as positive because many active and passive funds, including exchange-traded funds, typically buy stocks from them.

Chalom in May said that joining the Russell indexes would broaden the company’s shareholder base and strengthen its access to capital markets.

Magazine: Guide to the top and emerging global crypto hubs: Mid-2026

Story Protocol, a layer-1 blockchain built around intellectual property licensing, is pivoting to artificial intelligence as it rebrands as the DATA Foundation.

The company said Thursday that it will focus on building “essential infrastructure for training AI,” which it called “the most valuable and least solved category of IP.”

“Frontier AI labs have hit a multi-billion-dollar data bottleneck, where the internet has been effectively exhausted for scraping,” the company said. “The remaining supply is either expensive and bespoke or legally undocumented, leaving labs without a way to source data at scale, prove its provenance, or guarantee its quality.”

Story is the latest crypto project to turn to AI as funding and hype for the technology accelerate. Multiple crypto miners have also shifted to running the high-performance computers needed for AI, giving a major boost to their revenue in a crypto bear market.

The company said it is also launching an on-chain registry for AI training data provenance and licensing, called Trace, and is integrating with Kled, a company that provides licensable data sets for AI training.

Story president and product chief Andrea Muttoni will become CEO of the DATA Foundation, and Kled founder Avi Patel will join as chief data officer and adviser.

Andrea Muttoni speaking at a conference in Italy in 2024. Source: YouTube

Muttoni said that a year ago, Story had “set out to build the IP layer for the internet,” but the companies behind the “most valuable music, games, and brands guard their most valuable IPs jealously, and the open nature of permissionless licensing clashed with the very control the companies want to keep.”

He added that Story found an AI data-processing project it incubated, called Poseidon, had shown “immediate traction” with major AI firms and raised a $15 million seed round in July 2025.

Muttoni said that as AI companies “effectively run out of internet to scrape,” those that can supply them with “clean, verified, licensed data at scale are going to become some of the most valuable businesses ever built.”

He added that Poseidon will be “the processing layer of the protocol,” while Trace, the on-chain registry, will allow AI companies to verify entire data sets and allow contributors to enforce their terms.

Muttoni said that Kled, which pays people for tasks such as taking videos of their surroundings or capturing ambient audio to train AI, will also become the “flagship app” on DATA.

Related: Crypto Biz: Is AI the exit strategy for miners?

“The most important IP of this era is the data you can’t scrape: how a surgeon’s hands move, how a robot grips, how people speak, drive, and work in the real world,” said Story founder Seung-yoon Lee, who will serve as an adviser to DATA.

“DATA is where that conviction goes next: an end-to-end network that proves real-world data’s origin, licenses it, and pays the people who made it,” he added.

Story’s pivot comes as other major crypto platforms are retooling for AI.

Forbes reported Monday that Web3 gaming powerhouse Immutable is pivoting from gaming to launch an AI marketing platform aimed at game publishers.

Crypto exchange Coinbase announced earlier this month that it is launching a tool that will allow consumer AI models to connect with a user’s exchange account and make trades or execute strategies as it seeks to expand beyond being a platform to buy and sell crypto.

Magazine: AI is banking the unbanked in Africa… faster than crypto

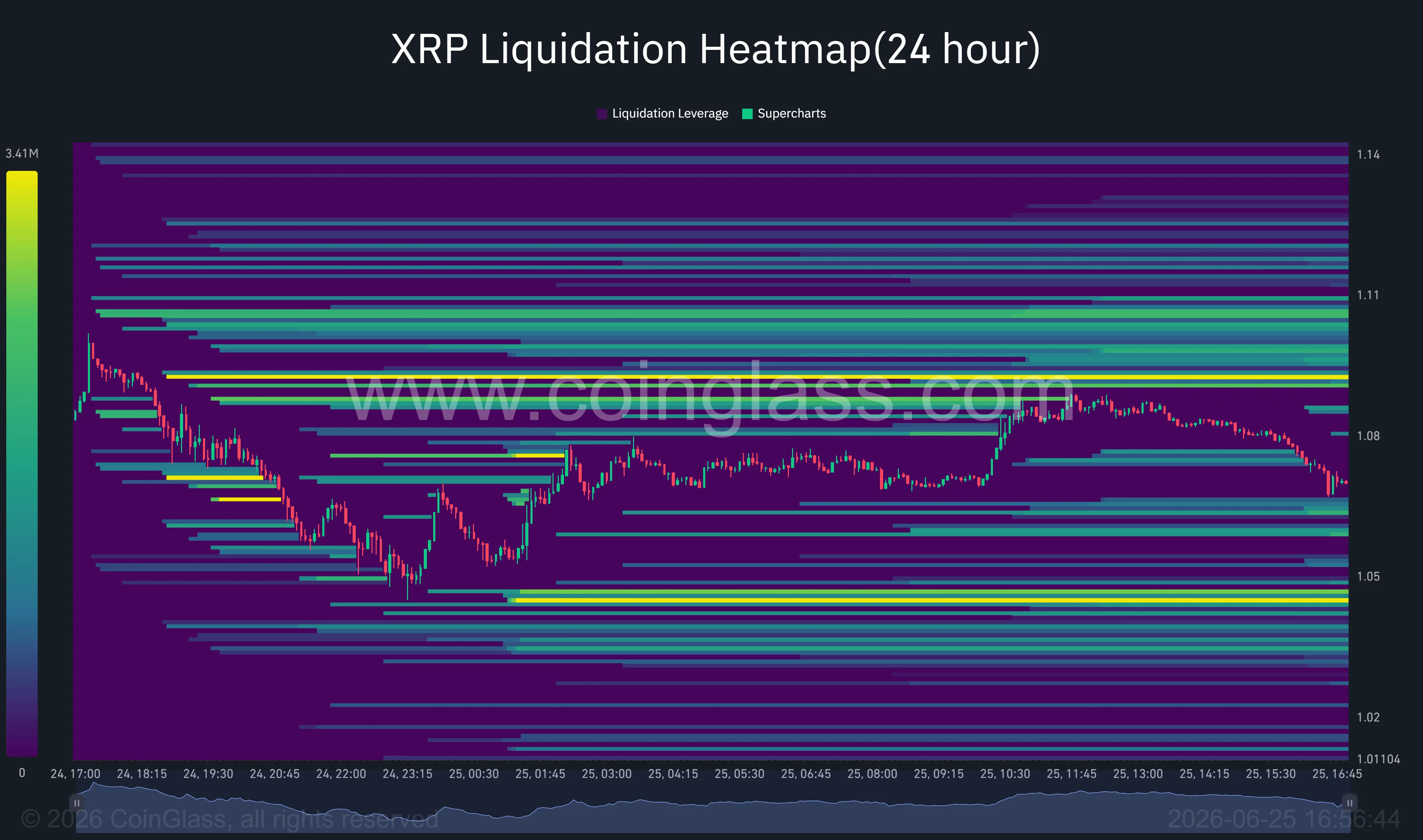

XRP has dropped through the $1.07 support area as traders brace for another leg lower amid mounting bearish pressure.

Summary

- XRP has fallen below the key $1.07 support level, increasing the risk of a deeper correction.

- Bearish chart patterns, liquidation clusters, and weak momentum continue to favor sellers.

- Regulatory uncertainty and macroeconomic headwinds have added pressure to the token’s near-term outlook.

According to data from crypto.news, XRP (XRP) price has fallen about 8% over the past week, extending losses after breaking below the $1.085 support area that had contained the price for several sessions.

The breakdown has left the token trading near $1.07 and shifted short-term sentiment firmly in favor of sellers as traders contend with regulatory uncertainty, weak on-chain activity, and a cautious macro backdrop.

Technical breakdown exposes lower support levels

The daily chart shows XRP slipping beneath the Murrey Math 3/8 support level at $1.0742, a zone that had acted as the lower boundary of its recent trading range. Price is now approaching the next major Murrey support near $0.9766, while the 14-day RSI sits around 33, leaving momentum close to oversold territory but without any confirmed bullish divergence.

On the four-hour chart, XRP continues to trade inside a descending channel after rejecting the upper trendline during its latest recovery attempt. Supertrend remains bearish with resistance near $1.115, while the Aroon indicator favors sellers, with Aroon Down above 70 and Aroon Up at zero, suggesting the prevailing downtrend remains intact.

Unless buyers reclaim the $1.11-$1.12 region, rallies may continue to attract selling pressure.

CoinGlass liquidation data shows the largest concentration of leveraged short liquidations around $1.09, while another significant liquidity cluster sits near $1.045 below the current price. Those zones could become near-term magnets as leveraged traders are forced out of positions.

Meanwhile, the absence of equally large liquidation pockets immediately above current levels suggests buyers have limited fuel for a sustained squeeze unless fresh demand enters the market.

Commenting on the market structure, well-followed analyst Altcoin Sherpa argued that XRP continues to weaken across multiple timeframes.

“Honestly doesn’t look great on the lower time frames (or any time frame) and I think this probably keeps grinding lower. Wouldn’t be surprised to see this go to like $0.75.”

Sherpa’s view aligns with the high-volume profile shown on his chart, where the next major demand zone sits well below current prices.

Macro risks and regulatory uncertainty continue to weigh on sentiment

Beyond the charts, traders are also watching an approaching July 1 regulatory deadline under California’s Digital Asset Financial Assets Law. Ripple has not yet appeared on the state’s public registry of confirmed applicants, prompting concerns that administrative delays could affect regional operations involving its RLUSD stablecoin and payment services. Although the issue is limited to California, uncertainty has added another layer of caution to XRP trading.

On-chain activity has offered little encouragement. Exchange inflows increased as large holders moved tokens onto trading platforms, suggesting some whales preferred reducing exposure rather than accumulating in weakness.

At the same time, XRP Ledger activity has remained subdued following the conclusion of Ripple’s long-running SEC case, leaving the market without a fresh catalyst to attract meaningful retail participation.

Global macro conditions have added further pressure. Rising geopolitical tensions in the Middle East have pushed energy prices higher and revived concerns that inflation could remain elevated. These developments have reduced expectations for Federal Reserve rate cuts and encouraged investors to rotate away from higher-risk assets, including cryptocurrencies.

As Bitcoin has struggled to regain momentum under those conditions, XRP and other large-cap altcoins have experienced sharper percentage declines as leverage unwinds across the market.

The bearish outlook would begin to weaken if XRP reclaims the $1.085-$1.11 resistance band and breaks above the descending channel, potentially forcing short sellers to cover positions clustered near $1.09.

Failure to defend the $1.045 liquidity zone, however, could expose the psychologically important $1.00 level, while a decisive break below that support would strengthen the case for a deeper decline toward the $0.97 Murrey support and potentially the $0.75 area highlighted by Altcoin Sherpa.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Blockchain technology has transformed the way digital assets are created, transferred, and managed. While early blockchain networks operated largely in isolation, the industry’s rapid growth has created a new challenge: enabling seamless communication between multiple blockchain ecosystems. As decentralized technologies continue to mature, the next stage of blockchain evolution is no longer about building individual networks—it’s about connecting them.

Blockchain connectivity is becoming the foundation for a more unified digital economy where assets, data, applications, and users can move freely across different chains without friction. This shift is opening new possibilities for scalability, efficiency, and innovation that were previously impossible.

Why Connectivity Matters

The blockchain ecosystem has expanded into hundreds of independent networks, each designed with different priorities. Some prioritize speed, others emphasize security, privacy, decentralization, or specialized applications. While this diversity fuels innovation, it also fragments liquidity, users, and applications.

Without reliable connectivity, users often face:

- Complicated asset transfers

- Multiple wallet management

- Fragmented liquidity

- Duplicate infrastructure

- Poor user experience

The next generation of blockchain infrastructure aims to eliminate these barriers by making different networks work together as a cohesive ecosystem.

Beyond Simple Asset Transfers

Early interoperability solutions focused primarily on transferring tokens between blockchains. While valuable, future connectivity extends far beyond moving digital assets.

Modern blockchain communication enables:

- Cross-chain smart contract execution

- Shared liquidity across ecosystems

- Unified decentralized applications

- Secure messaging between blockchains

- Cross-network governance

- Identity portability

- Data synchronization

Instead of isolated chains competing for users, networks can now collaborate while maintaining their own unique strengths.

The Rise of Cross-Chain Applications

The next wave of decentralized applications is increasingly becoming chain-agnostic.

Rather than forcing users to choose a single blockchain, future applications can leverage the advantages of multiple networks simultaneously.

For example, an application could:

- Execute transactions on one chain for lower costs

- Store important data on another device for greater security

- Access liquidity from several ecosystems

- Verify identities across multiple networks

- Utilize specialized services from different blockchain infrastructures

This flexibility allows developers to optimize performance without compromising user experience.

Smarter Infrastructure

Artificial intelligence, automation, and programmable infrastructure are beginning to complement blockchain connectivity.

Smart routing systems can automatically determine:

- The fastest network

- The lowest transaction costs

- The most secure execution path

- Optimal liquidity sources

- Efficient settlement routes

Rather than requiring users to manually select networks, future infrastructure can make these decisions automatically in the background.

Security Remains the Priority

Greater connectivity also increases responsibility.

Every connection between blockchains creates additional security considerations. As a result, the industry continues investing heavily in:

- Cryptographic verification

- Decentralized validation

- Multi-layer security models

- Formal smart contract verification

- Continuous monitoring systems

- Trust-minimized communication protocols

Strong security practices ensure that greater interoperability does not come at the expense of decentralization or user protection.

Improved User Experience

One of the biggest transformations may be invisible to users.

Future blockchain applications are expected to hide much of the underlying complexity.

Instead of asking users to:

- Switch networks

- Bridge assets manually

- Understand multiple token standards

- Manage numerous wallets

Applications can perform these processes automatically.

Users simply interact with services while the underlying infrastructure coordinates activity across multiple blockchains behind the scenes.

Supporting Global Digital Economies

As digital finance, tokenized assets, gaming, supply chains, and digital identity continue expanding, seamless blockchain connectivity becomes increasingly essential.

Connected blockchain infrastructure can support:

- Global payments

- Tokenized real-world assets

- Cross-border commerce

- Enterprise data sharing

- Digital identity systems

- Autonomous machine-to-machine transactions

- Decentralized financial infrastructure

The ability to securely exchange information across networks creates opportunities for entirely new digital business models.

The Road Ahead

The future of blockchain is unlikely to be dominated by a single network. Instead, it is shaping up to become an interconnected ecosystem where specialized blockchains collaborate rather than compete.

Connectivity enables developers to build more capable applications, businesses to operate more efficiently, and users to enjoy smoother digital experiences. As interoperability technologies continue advancing, blockchain infrastructure will increasingly resemble the internet itself—a network of networks working together to deliver seamless global access.

Conclusion

The next stage of blockchain connectivity represents a major milestone in the industry’s evolution. Rather than existing as isolated ecosystems, blockchains are becoming interconnected platforms capable of securely exchanging assets, data, and functionality across diverse networks.

As this infrastructure matures, users may no longer need to think about which blockchain they are using. Instead, they will simply access decentralized services that work seamlessly across an increasingly connected digital landscape. This evolution has the potential to unlock greater innovation, broader adoption, and a more efficient decentralized future for everyone.

REQUEST AN ARTICLE

Advance Financial Accounting (AFA)2026 #exampreparation #importantquestions with answers#2ndsembcom

GTA 6 marks the death of physical video games – we only have ourselves to blame

Why is Samsung Electronics stock plunging today?

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Blockchain.com files with SEC for U.S. IPO

Weekend Open Thread: Miami – Corporette.com

Advance Financial Accounting (AFA)2026 #exampreparation #importantquestions with answers#2ndsembcom

![Trump Shocking News [Crypto Reacts]](https://wordupnews.com/wp-content/uploads/2026/06/1782448392_maxresdefault-80x80.jpg)

Trump Shocking News [Crypto Reacts]

EV VS Petrol cars #financeshorts #moneytips #stockmarket #finance #evcharging #viralvideo #shorts

-