Crypto World

SOL price prediction as Solana RWA Tokenization value breaks $1.66B record

Solana price is catching its breath after a ferocious multi‑month rally, slipping back toward the mid‑$80s as traders reassess how much upside is left in one of this cycle’s most aggressive beta plays. The pullback is sharp, but it is not disorderly; it looks like a market that simply ran too far, too fast.

Summary

- Solana price slips toward the mid-$80s after an aggressive multi-month run, with YCharts showing a near 56% drawdown from a year ago.

- Polymarket contracts still price meaningful odds of SOL above $160 and even new all-time highs by end-2026, highlighting a wide distribution of outcomes.

- Bitcoin and Ethereum prices frame Solana inside a broader macro risk-on tape, with high Solana volumes keeping liquidity conditions supportive.

Solana price cools, prediction markets stay bold

As of early U.S. trading, Solana (SOL) changes hands around $86.07, down 4.4% on the session, after trading near $90.03 24 hours ago. Perplexity Finance data show a 24‑hour range between roughly $84.41 and $86.57, with spot market cap hovering near $48.55B and volumes around $57.32M. YCharts puts Solana’s daily reference price at $85.94 for February 16, down from $88.16 yesterday and dramatically below roughly $194.43 a year ago, a drawdown of about 55.8%.

Despite that drawdown, prediction markets have not written Solana off. A Polymarket market asking whether Solana will hit a fresh all‑time high by December 31, 2026, prices that probability near 16%, while a separate contract on “What price will Solana hit in 2026?” shows traders assigning roughly 32% odds to SOL trading above $160 before year‑end 2026. In that market, downside brackets such as “↓ 60” and “↓ 40” still command substantial probability, underscoring that “the path to new highs is anything but linear.”

Macro risk lens and wider crypto tape

This recalibration comes as digital assets continue to trade as the purest expression of macro risk appetite. Bitcoin (BTC) is hovering around $68,000–$69,000, with 24‑hour highs just above $69,000 and lows near $68,150, on roughly $37.8B in trading volume across major BTC/USD venues. Ethereum (ETH) changes hands close to $1,970–$1,975, after printing a 24‑hour high near $2,095.87 and a low around $1,933.97, with market cap near $237B. Solana (SOL) itself trades in the mid‑$80s, with Metamask data putting spot near $85.43 and 24‑hour volumes approaching $9.75B, a sign that “high 24h volume… improves liquidity and reduces slippage for traders.

Solana RWA tokenization efforts intensify

Solana’s RWA tokenization value smashing the 1.66 billion dollar mark reinforces the chain’s narrative as real financial infrastructure, not just a speculative L1, and that matters for SOL’s future pricing power. As more real-world assets settle and trade on Solana, fee revenue, demand for blockspace, and (crucially) the incentive to hold SOL for staking and governance all scale with it, giving fundamentals a chance to catch up with and eventually justify higher valuations in the next risk-on phase.

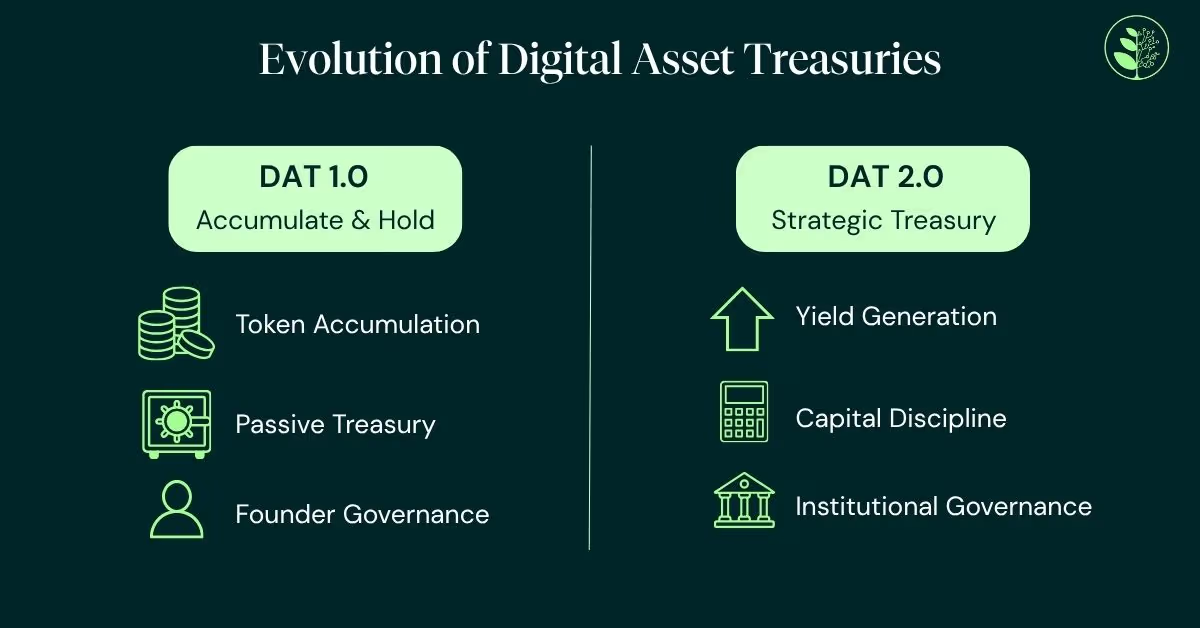

The era of buying bitcoin and calling it a treasury strategy is over.

By early 2026, more than 200 publicly listed companies hold digital assets on their balance sheets, collectively managing over $115 billion (DLA Piper, October 2025). The total market capitalization of these companies reached approximately $150 billion by September 2025 – a nearly fourfold increase from the year before. Yet several of these companies now trade at discounts to the value of the assets they hold. The market is sending a clear signal: accumulation alone is no longer enough.

Investors want to see capital discipline and economic return. Management teams have responded with share repurchase programs and transparency metrics such as “BTC per share,” designed to show the value a treasury adds beyond the token price (AMINA Bank Research, 2026). The shift from passive accumulation to active yield generation – from “DAT 1.0” to “DAT 2.0”—is now the defining theme of the sector.

Three broad models are emerging. Each carries a different risk – return profile and places distinct demands on governance, technical capability and infrastructure.

Infrastructure participation and staking

The most protocol-native approach involves staking tokens to support network consensus and earning rewards in return. For bitcoin-focused treasuries, this increasingly extends to the Lightning Network and other native infrastructure that generates routing and liquidity-based fees. Staking requires careful analysis of the technical security and smart contract risks.

The numbers have grown quickly. Bitmine Immersion Technologies reported over 3 million staked ETH by early 2026, with total holdings of $9.9 billion and annualized staking revenue of approximately $172 million (SEC Filing, March 2026). Its proprietary validator network marginally outperformed the Composite Ethereum Staking Rate, demonstrating the edge that institutional-grade infrastructure can deliver even in a protocol-level yield environment.

SharpLink Gaming deployed $200 million in ETH into restaking infrastructure via EigenCloud, targeting higher yields by securing applications ranging from AI workloads to identity verification (SEC Filing, 2025). Restaking – where already-staked ETH is used to secure additional services, with careful governance.

Active trading and market-driven income

A second set of strategies leverages market structure – funding-rate arbitrage, basis trading and options premiums. These can be effective and often market-neutral, but they demand trading expertise, robust risk controls and round-the-clock monitoring. The governance implications are significant: this approach effectively converts a treasury function into a trading operation. Like any trading function, it can be difficult to find skilled staff required to monitor complex positions and correlation risks.

One prominent Japanese listed company illustrates both the potential and the complexity. Holding over 35,000 BTC by the end of 2025, it generated the equivalent of approximately $55 million in bitcoin income revenue through option-based strategies, with operating profit growth exceeding 1,600% year-on-year. Yet the same company recorded a substantial net loss due to non-cash mark-to-market revaluations under local accounting standards (TradingView; Kavout, 2026). For investors, this disconnect between operational cash flow and reported earnings makes evaluation materially harder – and underscores why governance and transparency matter as much as headline returns.

Galaxy Digital offers a contrasting hybrid model, combining its own digital asset treasury with institutional services including collateralized lending, strategic advisory, and infrastructure. In Q3 2025, Galaxy posted a record adjusted gross profit of over $730 million (Mint Ventures Research, 2025). Notably, the firm has diversified its yield sources beyond pure crypto by repurposing its Helios mining facility as an AI compute campus secured by long-term contracts – a signal that the most resilient treasuries may be those that derive income from multiple, uncorrelated sources.

Credit deployment and net interest margin

A third route treats digital assets as productive balance-sheet capital. The model involves borrowing against crypto holdings on a non-recourse basis, receiving stablecoin liquidity, and deploying it into higher-yielding private credit. It preserves long-term exposure to the underlying asset while generating recurring interest income from short-duration, real-economy lending. In particular, this strategy demands expertise in yield, credit risk and fixed income.

The mechanics draw directly from traditional banking: liquidity management, underwriting, governance and controlled leverage. Under this type of model, a company acquires bitcoin, borrows against those holdings on a non-recourse basis—meaning the downside is limited to the collateral—and deploys the proceeds into diversified private credit portfolios supporting real-economy lending. If bitcoin appreciates, the company retains the upside after repaying the loan, combining potential capital gains with recurring interest income.

For credit deployment models to work credibly, they need to be grounded in operational financial infrastructure rather than built from scratch. The approach is most effective when it extends from an existing platform with real lending relationships and established client accounts. In our view at Greenage, this is also an area where governance and due diligence frameworks are particularly important, given that capital is being deployed into third-party credit opportunities that must be assessed on a counterparty-by-counterparty basis.

The success of this model is also tied to the maturation of stablecoins as institutional infrastructure. By 2026, stablecoins underpin cross-border payments, real-time settlement and T+0 clearing (same-day settlement) for enterprises (Foley & Lardner, January 2026). Coinbase Institutional projects total stablecoin market capitalization could reach $1.2 trillion by 2028 (Coinbase Institutional, August 2025). For credit deployment strategies, stablecoins provide a sound medium for capital deployment in lending markets.

The new measure of maturity

Recent market conditions have reinforced a simple truth: price appreciation alone is not a treasury strategy. The growing range of yield solutions reflects a sector learning from its own history—sustainable income generation makes digital assets more productive components of a corporate balance sheet.

No single model is definitive. The most effective treasuries will blend approaches depending on risk appetite, operational capability and governance structure. But the direction of travel is clear. Passive holding is no longer sufficient to justify digital assets’ place on the balance sheet. Yield is becoming the central measure of treasury maturity –and the core factor in how the market values companies with digital asset exposure.

The winners in this next phase will not be the largest holders. They will be the most disciplined operators.

Important Notice:

This article has been prepared by Greengage & Co. Limited for informational and thought leadership purposes only. It is intended solely for use by businesses, professional counterparties and institutional market participants and is not directed at retail consumers. It does not constitute financial advice, investment advice, a financial promotion, or a recommendation or inducement to buy, sell, or hold any asset, security, or financial instrument.

Digital assets are subject to significant price volatility and regulatory change. Past performance is not indicative of future results. All investments carry risk, including the potential loss of capital. Forward-looking statements and market projections referenced herein are sourced from third-party research and do not represent the views or predictions of Greengage & Co. Limited.

Greengage & Co. Limited is not authorized or regulated by the Financial Conduct Authority for investment business. Greengage acts solely as an introducer to independent third-party service providers and does not arrange investments, provide lending, custody, or investment management services.

Readers should seek independent professional advice before making any investment decision.

Prediction markets are pushing into Asia’s largest economies even as local gambling laws impose strict limits on traditional betting activities. The region’s combination of scale, active retail participation, and limited local alternatives creates a compelling case for prediction markets to grow, though regulatory risk remains a defining factor.

That dynamic mirrors a broader pattern in crypto where technology often outpaces licensing and oversight. Polymarket, one of the fastest-growing platforms, is already recording weekly volumes above $1 billion and has added Chinese-language support. New entrants like PredicXion are betting that region-focused events will help unlock adoption in markets where localization matters just as much as the product itself.

Yet Asia’s landscape is fragmented and legally intricate, with access, language, and regulation not always aligning with the sector’s global ambitions. As platforms push forward, the legal framework—rather than technology—could ultimately shape how quickly prediction markets scale in the region.

Key takeaways

- Asia’s largest economies show robust demand for prediction markets, but India’s heavy taxation on undisclosed gains and China’s outright ban on crypto activities create a complex regulatory backdrop.

- Japan and South Korea—two leading crypto markets in Asia—maintain strict gambling rules, which narrows access yet leaves room for localized efforts and experimentation.

- Polymarket remains a reference point for the model, with weekly volume surpassing $1 billion and expansion into Chinese-language support, while regional players like PredicXion emphasize Asia-centric events.

- Regulatory classification—whether these platforms are treated as gambling, information markets, or financial instruments—will largely determine their future in Asia and beyond.

Asia’s market pull and regulatory headwinds

GDP scale matters in the appeal of prediction markets. In 2024, major Asian economies such as China, India, Japan, and South Korea ranked among the world’s top five by gross domestic product, underscoring why the region is a focal point for growth in data-driven prediction tools. While India and China do not have explicit frameworks addressing blockchain-based prediction markets, both maintain restrictive environments for crypto. India imposes heavy taxation on gains, while China enforces an outright ban on several crypto activities, including trading and mining.

South Korea’s example is particularly instructive: it is one of the world’s largest economies by GDP, and its won (KRW) consistently features among the most active fiat currencies in crypto markets. Kaiko’s data highlight the KRW’s prominence in on-chain trading activity, a reminder that local currency liquidity can play a pivotal role in any regional expansion of prediction markets.

From a market perspective, Korea is often cited as a fertile ground for retail crypto adoption. Yet the local market’s gambling laws create a nuanced environment for prediction-market operators. Heechang Kang, co-founder of research firm Four Pillars, told Cointelegraph that while the Korean market could offer significant opportunities, platforms must address audiences beyond Western-focused themes to achieve broader traction.

The regulatory lens: gambling vs information markets

The regulatory question is at the heart of Asia’s prediction-market push. In several markets, authorities classify activities tied to wagering on uncertain outcomes as gambling, a category that is tightly controlled or prohibited outside state-run frameworks. Andy Cheung, founder and CEO of PredicXion, stresses that this creates a “significant concern” for operators operating in jurisdictions where gambling rules are opaque or stringent.

Despite these realities, some analysts argue that prediction markets are not simply gambling. Jaewon Kim, a researcher at Four Pillars, has framed the distinction around output: gambling is a closed loop of bets against a house, while prediction markets aggregate collective expectations about real-world events. Kim noted that during the 2024 U.S. presidential election, prediction markets gained traction and, in some cases, proved more accurate than polls or expert forecasts, underscoring the informational value they can offer beyond pure wagering.

China’s strict online policy complicates access, with many users turning to VPNs to reach platforms like Polymarket. However, this circumvents controls rather than resolves the legal risk, and authorities’ stance on whether prediction-market-like activity falls under gambling or a distinct information-market category remains unsettled. In Korea and Japan, regulators have yet to issue clear guidance specific to blockchain-based prediction markets, but both countries maintain rigorous gambling restrictions that can constrain user participation and operator growth.

Localized platforms, regional focus, and the path forward

Against this backdrop, Asian-anchored platforms are emphasizing localization as a core strategy. PredicXion is attempting to tailor markets toward events familiar to Asian retail audiences, seeking to avoid directly traversing heavily restricted markets where possible. Cheung notes that in several jurisdictions, operators must navigate a maze where wagering on uncertain outcomes is often treated as gambling, potentially limiting the range of acceptable products and geographies.

Polymarket’s approach illustrates the regional tension between global platforms and local realities. The platform has returned to activity levels comparable to those seen during the U.S. presidential election, a signal of resilience in a market where regulatory clarity remains uneven. Its expansion into Chinese-language support aims to widen accessibility, while its presence in Asia continues to test how far a global model can travel when local rules push back.

At the same time, the industry’s argument that prediction markets offer value beyond wagering hinges on their ability to aggregate real-world expectations. Jaewon Kim’s assessment points to an informational utility that could align with regulated financial-like instruments if policymakers converge on a workable classification. The question for investors and builders is whether regulators will carve out a distinct lane for prediction markets as information markets or keep them tethered to gambling frameworks with narrow licensing pathways.

In practice, the next steps will be defined by regulatory decisions across Asia’s largest economies. Platforms that can demonstrate responsible governance, transparent operation, and robust consumer protections may find a path forward even as others retreat to clearer, more tightly controlled markets.

As Asia weighs these choices, observers should watch regulatory statements and licensing developments in India, China, Korea, and Japan—along with evolving cross-border approaches to information markets. The outcome will shape not just where prediction markets can operate, but how they are structured, marketed, and perceived by everyday users seeking to gauge the pulse of real-world events.

Crypto World

Ripple Joins SWIFT’s Certified Partner Program, Gaining Access to a $150 Trillion Network

TLDR:

- Ripple Treasury is officially listed in SWIFT’s Certified Partner Program and confirmed on both directories.

- Banks using Ripple Treasury can now access SWIFT’s Alliance Lite2 messaging network directly.

- Ripple’s platform supports SWIFT, EBICS, SFTP, APIs, combining legacy and blockchain rails in one.

- Rather than replacing SWIFT, Ripple positions itself as the bridge between old and new finance.

Ripple has officially joined SWIFT’s Certified Partner Program, marking a notable shift in how the blockchain payments company positions itself within the global financial system.

Rather than replacing SWIFT, Ripple Treasury now operates as a certified partner inside the network. This move gives banks access to both legacy and blockchain payment rails through a single platform.

The development has drawn renewed attention to Ripple’s long-term strategy in the institutional payments space.

Ripple Treasury Gains Direct Access to SWIFT’s Messaging Network

Banks using Ripple Treasury can now connect to SWIFT’s Alliance Lite2 messaging network directly. They no longer need separate SWIFT infrastructure to access the network. This is confirmed on both Ripple’s partner page and SWIFT’s official partner directory.

Through this integration, users also get access to SWIFTRef data inside the platform. This covers IBAN lookups and ABA routing lookups built into payment workflows. These tools are standard requirements for institutions processing cross-border transactions daily.

Ripple Treasury supports multiple connectivity options alongside SWIFT. These include EBICS, SFTP, APIs, and alternative networks. Together, they give financial institutions a flexible, consolidated payments infrastructure under one platform.

One Platform Now Bridges Legacy Banking and Blockchain Rails

The integration positions Ripple as a bridge between traditional finance and blockchain-based payments. Banks no longer face a binary choice between old and new systems. Both options are now available through a single interface.

SWIFT processes approximately $150 trillion in transactions annually. Ripple now sits within that network while also developing its own blockchain payment alternative. This dual positioning is a calculated move in a competitive institutional market.

For banks, the practical outcome is reduced operational complexity. Connecting to two separate systems traditionally required significant infrastructure investment. With Ripple Treasury’s SWIFT certification, that barrier is considerably lower.

The development represents a maturation in how blockchain companies approach institutional adoption. Instead of positioning purely as a disruptor, Ripple has taken a complementary route.

That strategy may prove more effective in driving real-world adoption among regulated financial institutions.

Chainlink has released 17.875 million LINK tokens valued at approximately $165 million in its scheduled quarterly unlock, according to on-chain data.

Of the newly unlocked supply, 14.875 million LINK, worth about $125 million, was transferred directly to the Binance cryptocurrency exchange. Market analysts note that such heavy inflows into exchanges typically signal anticipated sell-side activity.

Whale Interest in LINK Rises Despite Bearish Price

Blockchain analyst EmberCN explained that Chainlink moved the remaining 4.125 million tokens, valued at roughly $40.1 million, to a multi-signature wallet that distributes staking rewards.

While this incentivizes network participants, it creates a circular economic challenge. Chainlink inflates its supply to pay stakers, diluting the underlying value those same stakers are attempting to capture.

This structural inflation is taking a toll on the token’s market performance. Data from BeInCrypto shows a nominal 0.83% gain to $8.67 over the past 24 hours.

However, LINK has declined 7% over the past month and plunged 60% over the previous six months.

Despite the bearish price action, blockchain analytics firm Santiment reports a 25% increase in the number of whale wallets holding 1 million or more LINK over the past year. The total number of these large-tier addresses has grown from 100 to 125.

Santiment interpreted this accumulation as smart money quietly positioning for a market reversal, saying:

“This may not seem like it has much correlation with price while Bitcoin and all of crypto has remained in a bear cycle… But when markets flip positive once again, look for assets that whales have quietly been flocking to.”

This is unsurprising, considering Chainlink is widely considered an essential infrastructure for the crypto industry.

Over the past year, it has established pilots with global entities like Swift, Mastercard, and J.P. Morgan for tokenized assets and cross-chain functionality.

Ultimately, Chainlink appears to be winning the race to build enterprise blockchain infrastructure, but its retail and institutional investors are losing the battle against structural dilution.

Until the broader market sees a material reduction in quarterly exchange distributions or a direct mechanism linking institutional utilization to public token demand, the asset’s valuation faces a difficult recovery.

The post Massive Chainlink Token Unlock Sparks Sell-Off Fears appeared first on BeInCrypto.

A Nevada judge has extended a court-ordered halt on Kalshi’s ability to offer event-based contracts to residents in the state, ruling that the products fall under unlicensed gambling as defined by Nevada law. In a Friday hearing in Carson City, Judge Jason Woodbury granted a preliminary injunction sought by the Nevada Gaming Control Board, barring Kalshi from letting Nevadans place bets on outcomes ranging from sports to elections and entertainment without a gaming license, according to Reuters.

The injunction builds on a temporary restraining order issued on March 20, which will stay in place through April 17 while the court considers longer-term restrictions. Kalshi, which operates from New York, contends that its contracts are financial derivatives—specifically swaps—that should be overseen exclusively by the Commodity Futures Trading Commission (CFTC).

Key takeaways

- Nevada extends a ban on Kalshi’s event-based contracts, blocking trading in the state without a gaming license.

- The judge frames Kalshi’s contracts as functionally indistinguishable from traditional sports betting, effectively classifying them as gambling under state law.

- Kalshi argues the products are CFTC-regulated swaps, setting up a clash between state gaming authorities and federal market regulators.

- The CFTC has signaled it will defend its regulatory remit over prediction markets in court against state challenges.

- Regulatory pressure is broadening, with Utah moving to block Kalshi and similar platforms, underscoring a shifting legal landscape for prediction markets in the U.S.

Nevada’s ruling and Kalshi’s legal position

During the hearing, Judge Woodbury described Kalshi’s contracts as essentially mirroring the mechanics of licensed sports betting. He stated that, no matter how one frames the product, placing a wager on a game outcome via Kalshi is “indistinguishable” from traditional gaming activity and thus requires a Nevada gaming license. Reuters characterized the judge’s comments as a strong alignment with the board’s position that Kalshi’s offerings violate state gaming statutes.

The court’s decision reinforces a broader pattern of state regulators scrutinizing prediction markets, with Nevada’s action marking the first time a state has obtained a court-enforceable ban on Kalshi. Kalshi has argued that its contracts are swaps—financial instruments that should fall under federal oversight by the CFTC rather than state gaming commissions. The dispute illustrates a central tension in U.S. financial-regulatory policy: whether prediction markets should be treated as gambling, derivative trading, or something in between subject to multiple layers of regulation.

Regulatory backdrop: CFTC’s stance and the broader market implications

At the federal level, the CFTC has maintained that it has jurisdiction over prediction markets and has signaled it is prepared to defend that authority in court against state challenges. In a recent industry appearance, CFTC Chair Rostin Behn emphasized the potential value of prediction markets as “truth machines”—markets where financial incentives are aligned to reveal more reliable signals about future events than traditional polling. The department’s posture suggests a willingness to push back against state-level attempts to curb or reinterpret the scope of what constitutes a regulated market in this space.

The Nevada decision comes against a backdrop of growing state action targeting prediction-market-style bets. In nearby Utah, lawmakers advanced legislation aimed at classifying proposition-style bets on in-game events as gambling, effectively blocking Kalshi and similar platforms in the state. While Utah’s move is separate from Nevada’s court action, it signals a broader regulatory trend that could constrain operators seeking to offer event-based contracts across multiple jurisdictions.

What this means for traders, investors, and builders

For participants who once considered Kalshi’s offerings as a way to hedge uncertainty around events, the Nevada ruling highlights the volatility of a regulatory landscape that remains unsettled at the state level. The outcome could influence where Kalshi and other prediction-market platforms search for licenses, or whether they pivot to offer alternative products that fit within existing regulatory frameworks. Investors and developers alike should monitor both state actions and federal court challenges, as a ripple effect could shape pathway approvals, compliance costs, and the speed at which new markets might emerge in regulated environments.

From a market-structure perspective, the clash underscores a growing complexity for platforms that rely on real-money participation tied to outcome-based events. If regulators ultimately converge on a uniform approach—whether to treat such markets as gambling, as regulated derivatives, or under a hybrid framework—the regulatory timeline and required safeguards will determine how quickly participants can access these products in major markets.

What to watch next

The Nevada case remains open as the court continues to consider longer-term restrictions beyond the current injunction. Key questions include whether Kalshi can secure the necessary gaming licenses in Nevada, how the company will position its product as it navigates state-by-state licensing regimes, and how federal authorities will respond to continued state-level challenges. In parallel, lawmakers in other states may push forward with legislation that redefines the legal boundaries of prediction markets, potentially accelerating a more unified approach—or further fragmenting access across the United States.

Readers should stay tuned for court updates, as well as any statements from the CFTC or Kalshi on the evolving regulatory posture. The next phase will likely clarify whether prediction markets survive within a patchwork of state licenses and whether federal guidance or court rulings will ultimately steer the sector’s regulatory trajectory.

A Nevada court has moved to keep Kalshi out of the state’s event-contract market while the legal fight continues.

Summary

- Nevada judge backed regulators and said Kalshi’s event contracts are no different from sports betting.

- The ruling extends Kalshi’s Nevada ban while the court reviews longer-term restrictions through April 17.

- The case deepens the clash between state gambling laws and federal oversight claims over prediction markets.

The ruling came after the Nevada Gaming Control Board asked the court to block the company from offering contracts tied to sports, elections, and entertainment outcomes.

The case adds to a wider debate over whether prediction market contracts fall under federal derivatives law or state gambling rules. Kalshi has said its products are financial contracts, while Nevada regulators have argued that the offerings match gambling activity under state law.

Judge Jason Woodbury said he would grant a preliminary injunction against Kalshi at a hearing in Carson City. According to Reuters, the order prevents the company from allowing Nevada residents to trade event contracts without a gaming license.

The move extends a temporary restraining order issued on March 20. That order will stay in effect through April 17 while the court completes the next steps in the case.

Kalshi had argued that its contracts are “swaps” and fall under the oversight of the Commodity Futures Trading Commission. The company has maintained that federal law gives the CFTC authority over these products.

The judge did not accept that position. Reuters reported that Woodbury said buying a contract tied to a game result is the same as placing a wager through a sportsbook. He said, “No matter how you slice it, that conduct is indistinguishable.”

State regulators score early court win

The ruling marks the first time a state has secured a court-enforced ban that is currently active against Kalshi. That gives Nevada an early legal win as more states question prediction markets tied to sports and similar events.

Utah has also moved against the sector. Lawmakers there passed a bill last month that classifies proposition-style bets on in-game events as gambling and seeks to block such products from platforms including Kalshi and Polymarket.

The dispute also comes as the CFTC continues to defend its role in prediction markets. CFTC Chairman Michael Selig said last month that the agency is ready to fight in court to protect its jurisdiction from states and other regulators.

Selig also described prediction markets as “truth machines” during an industry conference. He said markets where users risk money on outcomes can offer a clearer signal about future events than opinion polls, setting up a sharper clash between federal oversight claims and state gaming laws.

Anthropic confirmed it will block Claude subscription access for third-party AI agent tools, including OpenClaw, effective April 5 at 12 pm PT.

The policy shift forces thousands of developers who built autonomous workflows on flat-rate Claude plans to either pay API token rates or migrate to competing models.

Why Anthropic Cut OpenClaw From Claude Subscriptions

Boris Cherny, Anthropic’s Head of Claude Code, announced the restriction, indicating that subscriptions were never designed for the heavy usage patterns generated by third-party agentic tools.

“Capacity is a resource we manage thoughtfully, and we are prioritizing our customers using our products and API,” he said.

The economic mismatch had been growing for months. Agentic loops in OpenClaw can consume millions of tokens in a single session.

A single afternoon of automated debugging could burn through enough tokens to cost upwards of $1,000 at standard API rates, Skypage making $200 flat-rate subscriptions deeply unprofitable for Anthropic.

Anthropic offered subscribers a one-time credit equal to their monthly plan cost, discounted usage bundles, and full refunds for those who cancel.

Developer Backlash and Migration Signals

The response has been quick, with some users already canceling their subscriptions. The general sentiment is that the decision is an admission that Anthropic cannot compete with open-source agents.

“No thanks. Subscription canceled. New models have already been configured,” wrote one user.

Developer Alex Finn called it a “massive mistake” and predicted local models would match Opus 4.6 performance within six months.

He outlined a hybrid setup using Claude Opus as orchestrator with Gemma 4 and Qwen 3.5 for execution, costing roughly $200 monthly.

Others criticize Anthropic for gaslighting users, arguing that the company initially blamed usage patterns before admitting it was prioritizing its own products.

Users want published token budgets for each subscription tier and advance notice of future policy changes.

A Dual Strategy Takes Shape

The timing reveals a broader Anthropic play as the company expands its Microsoft 365 connector to all Claude plans, including Free.

The integration connects Claude with Outlook, SharePoint, OneDrive, and Teams, Microsoft positioning it directly against Microsoft Copilot’s $30-per-user monthly pricing.

OpenClaw creator Peter Steinberger recently joined OpenAI, VentureBeat, adding competitive tension to the decision.

Anthropic has been building Claude Cowork as an alternative to third-party agent tools, and this restriction steers users toward that product.

Whether the cost of lost developer trust outweighs the infrastructure savings remains the open question heading into Q2 2026.

The post AI Fallout Begins as Claude Creators Cut Off Their Most Powerful Users appeared first on BeInCrypto.

If the closing bell has long been a business model, then 24/7 trading is an attempt to break it. As the NYSE, Nasdaq, CME and Cboe race to introduce round-the-clock trading, the question is who stands to gain and who could lose.

The answer is quite simple, Mati Greenspan, CEO and founder of Quantum Economics, told CoinDesk: “The biggest losers in 24/7 stock trading won’t be traders: they’ll benefit massively. It’ll be the middlemen who’ve long made money when traders can’t trade.”

Greenspan, also a market analyst, alleged that when markets reopen after what he called a big event, “a handful of firms decide the first tradable price. Oftentimes, they will explicitly use a price that triggers stop losses for their clients, closing them out at a loss and making a profit for the broker who is essentially trading against the client.”

When Greenspan was asked whether brokers coordinate around pricing during market closures, he was blunt in his claim: “Yes, manipulation outright.”

“They basically get to control prices, often with hours to strategize,” he said. “Often hunting stops losses. When big news happens on weekends, the house tends to take liberties with pricing at the opening bell.”

His comments come as several major U.S. exchanges are looking to offer around-the-clock trading services. The NYSE said it is seeking SEC approval for 24/7 trading. Nasdaq announced similar plans in December. CME plans to roll out 24-hour crypto futures in 2026, pending approval, and Cboe recently expanded U.S. index options to 24/5 trading.

‘Plausible deniability’

While Greenspan’s comments could be seen as accusatory, it’s not hard to see why such practices could be prominent in the after-hours market. When the usual trading hours come to a close, at 4 p.m. ET, the thin liquidity can make prices easier to influence.

“After the 4 p.m. closing bell, you simply don’t have the same liquidity,” said Joe Dente, a floor broker at the New York Stock Exchange. “People have gone home and the liquidity is not there, so you’re going to see larger spreads.”

Wider spreads and thinner order books, he said, create an environment where price movements can be exaggerated compared with the regular session.

Academic research also supports the view that extended trading sessions are structurally different from core market hours. A widely cited joint UC Berkeley–University of Rochester study found that after-hours price discovery is “much less efficient,” citing lower volume and thinner liquidity that limit the speed at which information is incorporated into prices.

When asked whether manipulation already occurs during those periods, Dente said it is “possible,” but he also pointed out that “the event of 24-hour trading is going to leave things open to manipulation,” referring to conditions already seen in after-hours markets

Greenspan, meanwhile, noted that these alleged manipulation practices are “not exactly above board, so they [brokers who might be taking part in such actions] tend to maintain plausible deniability.”

This is where the line between actual manipulation and proof that such practises occur starts to blur.

A widely cited SSRN study on opening price manipulation shows how brokers can influence prices during the pre-open auction by submitting and canceling large orders, temporarily pushing stocks away from their fundamental value before broader liquidity returns.

The research found that such manipulation can create distorted opening prices that are later corrected once the full market begins trading, leaving investors who bought at the inflated price with losses. Because these distortions occur before normal trading volume returns, the resulting price moves can appear indistinguishable from ordinary market volatility.

Still another broker, familiar with overnight trading practices and who asked not to be named because they were not authorized to speak publicly, said thin overnight liquidity can occasionally make it easier for coordinated strategies to influence prices in less widely traded stocks.

And this is not just anecdotal evidence.

In late 2025, the SEC settled charges over a multi-year spoofing scheme involving deceptive orders used to move prices in thinly traded securities. Regulators also fined Velox Clearing $1.3 million for failing to detect “layering” and “spoofing” in volatile stocks.

Meanwhile, the U.S. Financial Industry Regulatory Authority (FINRA), in its 2026 Annual Regulatory Oversight Report, cited firms for “failing to maintain reasonably designed supervisory systems and controls, including with respect to the identification and reporting of potentially manipulative activity conducted in after-hours trading.”

A win for retail?

Whether it’s hard to point out how widespread these accusations are, one thing is for sure: if trading goes 24/7, traders will be the ultimate winners, particularly retail traders.

In today’s electronic markets, traders who respond fastest to market news have a structural advantage.

“There’s always an edge for whoever has the fastest computers and the best program writers,” said Dente, noting that algorithms can react to news and orders “in a nanosecond.” For individual investors, he added, keeping up with that speed is difficult. “How does the human person keep up with that?”

And reacting to these events becomes even harder for smaller investors when the market is closed, leaving those retail or smaller traders at a massive disadvantage.

Pranav Ramesh, head of quantitative research for options at Nasdaq and co-founder of Leadpoet, said thin markets can amplify those risks.

“Broker coordination may often show up as industry-wide alignment around routing and execution practices, especially where a large share of retail flow ends up with a small number of wholesalers,” he said. “Outside regular hours, scrutiny can be harder because the market is thinner and there are fewer straightforward reference points for investors to benchmark execution quality,” Ramesh said in his personal capacity.

Sources familiar with broker routing and liquidity practices told CoinDesk that price-setting power in thin sessions is real, particularly when major news breaks while markets are closed. According to those sources, coordination around routing, spreads and execution practices during extended gaps has historically been easier precisely because retail traders cannot participate.

This is precisely what around-the-clock trading will solve for traders, according to Greenspan, who said 24/7 markets would blunt fintech firms’ advantage by removing the weekend vacuum entirely.

The recent Middle East conflict has been a perfect example of how this can open up more trading opportunities when markets remain closed. Decentralized exchange, Hyperliquid, which trades on blockchain 24/7, has seen growing interest from traders betting on traditional financial assets, including oil and gold, during the weekend, when traditional exchanges are closed.

It has become so popular that weekly derivatives trading volume on the platform topped $50 billion, while it generated $1.6 million in revenue over 24 hours, outpacing the entire Bitcoin blockchain’s revenue. The platform has also recently added an S&P 500 perpetual contract.

Needless to say, major exchanges will also likely benefit from trading fees if they open for 24/7 trading.

Whether round-the-clock trading ultimately weakens brokers’ influence on price setting remains to be seen. What is clear is that exchanges and investors stand to gain from markets that never close.

“Traders can react in real time without being at the mercy of the middlemen — the brokers,” said Greenspan.

Read more: Bitcoin’s weekend selloff may be over with CME’s 24/7 crypto trading move

A Nevada judge has reportedly extended a ban preventing Kalshi from offering event-based contracts in the state, ruling that the products constitute unlicensed gambling under state law.

Judge Jason Woodbury said at a hearing in Carson City on Friday that he will grant a preliminary injunction requested by the Nevada Gaming Control Board, barring the company from allowing residents to trade on outcomes such as sports, elections and entertainment events without a gaming license, according to Reuters.

The decision extends a temporary restraining order issued on March 20, which will remain in effect through April 17 while the court finalizes longer-term restrictions.

Kalshi, based in New York, has argued that its contracts are financial derivatives, specifically “swaps,” that fall under the exclusive oversight of the Commodity Futures Trading Commission (CFTC).

Related: Appeals court denies Kalshi request to block Nevada enforcement action

Judge says Kalshi contracts mirror sports betting

Woodbury rejected Kalshi’s argument, claiming that there is a direct comparison between traditional sports betting and Kalshi’s platform, according to Reuters. He said that placing a wager through a licensed sportsbook and buying a contract tied to a game outcome are functionally the same, per the report.

“No matter how you slice it, that conduct is indistinguishable,” the judge reportedly said, adding that such activity qualifies as gaming under Nevada law and cannot be offered without proper licensing.

The case marks the first time a state has secured a court-enforced ban currently in effect against the company.

Last month, Utah lawmakers also passed a bill targeting Kalshi and Polymarket that classifies proposition-style bets on in-game events as gambling, aiming to block such offerings in the state.

Related: Kalshi CEO fires back against Arizona criminal charges as ‘total overstep’

CFTC vows court fight over prediction market oversight

The CFTC has asserted authority over prediction markets, with Chairman Michael Selig warning that the agency is prepared to defend its jurisdiction in court against any challenges from states or other regulators.

Speaking at an industry conference last month, Selig said prediction markets can act as “truth machines,” arguing that when participants put money behind their views, these markets can produce more transparent and reliable signals about future events than traditional opinion polling.

Magazine: Bitcoin may take 7 years to upgrade to post-quantum — BIP-360 co-author

Crypto World

Hyperliquid Burns 49,000+ HYPE Tokens in a Single Day, Confirming Net Deflationary Status

TLDR:

- HyperCore burned 49,360.33 HYPE at ~$35.09 on April 2, pushing the protocol into net deflationary territory.

- Even with 26,665 HYPE distributed to stakers and validators, net circulation still dropped by 17,075 tokens.

- Hyperliquid’s annual deflation rate stands at ~6.15M HYPE, contrasting sharply with Solana’s 25.19M SOL inflation.

- The HIP-3 flywheel ties protocol revenue directly to buybacks, creating self-sustaining and organic supply reduction.

Hyperliquid recorded a net removal of 17,075 HYPE tokens from circulation on April 2, 2026. HyperCore repurchased and permanently burned 49,360.33 HYPE at an average price of approximately $35.09.

Alongside this, HyperEVM gas fees contributed an additional 146.43 HYPE to the burn total. Even after distributing 26,665 HYPE as staking and validator rewards, the protocol remained firmly in net deflationary territory for the day.

Buyback Mechanism Drives Daily Deflationary Pressure

The April 2 activity placed Hyperliquid’s annualized deflation rate at roughly 6.15 million HYPE per year. On a monthly basis, that translates to approximately 512,262 HYPE removed from circulation.

These figures reflect a consistent pattern emerging from HyperCore’s revenue-backed buyback program. The numbers stand in sharp contrast to Solana, which inflates by around 25.19 million SOL annually through staking and validator rewards.

HyperCore’s buyback model operates on a price-sensitive basis, which makes it naturally self-adjusting. When HYPE prices rise, fewer tokens are repurchased with the same revenue.

Conversely, when prices fall, the same revenue buys and burns more tokens. This mechanism creates a built-in buffer against extreme supply pressure at different points in the market cycle.

The burn also accounts for a worst-case assumption regarding team token unlocks. Hyperliquid Labs is allocated 173,000 HYPE per month in vesting, equal to about 5,766 HYPE per day.

Even if this entire allocation were sold into the market, the protocol would still achieve net deflation under the current numbers. That assumption was already factored into the 17,075 HYPE net removal figure.

This structure sets Hyperliquid apart from many protocols that rely on token emissions to incentivize participation.

Here, buybacks are funded by actual trading revenue from HyperCore, not newly minted supply. That distinction matters when evaluating the long-term sustainability of the deflationary model.

HIP-3 Adoption Strengthens the Protocol’s Revenue Flywheel

Greater adoption of HIP-3 is central to sustaining and potentially accelerating this deflationary trend. As more users trade through the protocol, activity increases and so does revenue.

Higher revenue, in turn, supports larger buybacks and more burns. The cycle reinforces itself without depending on external capital injections.

This flywheel effect ties protocol growth directly to supply reduction. Each new participant adds to the trading volume that funds the next round of buybacks.

Over time, this creates persistent and organic buy pressure on HYPE. The pressure comes from protocol economics, not from speculative demand or marketing cycles.

Trading activity on HyperCore feeds directly into the buyback pool used for burns. The April 2 figures show that this model is already producing measurable results at current price levels.

As HIP-3 usage grows, the mechanism is designed to scale accordingly. The connection between adoption and deflation is direct and quantifiable.

Validators and stakers received 26,665 HYPE in rewards during the same period. That distribution ensures continued network participation while the broader supply still contracts.

The balance between rewarding contributors and reducing circulating supply appears to be working as intended on April 2.

JerryRigEverything Disassembles LG’s Rollable Phone and Unrolls the Secrets From a Lost Prototype

These tips changed my life #PersonalFinance #financialliteracy #EduTok #finance

Cambridge men defeat Oxford to extend era of dominance

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

These tips changed my life #PersonalFinance #financialliteracy #EduTok #finance

![BITCOIN IS ABOUT TO DROP !!! [Bear Flag Confirmed]](https://wordupnews.com/wp-content/uploads/2026/04/1775318607_maxresdefault-80x80.jpg)

BITCOIN IS ABOUT TO DROP !!! [Bear Flag Confirmed]

Say This Prayer When You Need Financial Breakthrough #jesus #prayer #christianyoutube #holyspirit

-

NewsBeat2 days ago

NewsBeat2 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business2 days ago

Business2 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion22 hours ago

Fashion22 hours agoWeekend Open Thread: Spanx – Corporette.com

-

Entertainment5 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World3 days ago

Crypto World3 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech6 days ago

Tech6 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World4 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Entertainment7 days ago

Entertainment7 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Tech6 days ago

Tech6 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Sports4 days ago

Sports4 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech4 days ago

Tech4 days agoEE TV is using AI to help you find something to watch

-

Business3 days ago

Business3 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Fashion7 days ago

Fashion7 days agoAmazon Sundays: Soft Spring Layers

-

Tech6 days ago

Tech6 days agoElon Musk’s last co-founder reportedly leaves xAI

-

Fashion5 days ago

Fashion5 days agoThe Best Spring Trends of 2026

-

Tech4 days ago

Tech4 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech5 days ago

Tech5 days agoApple will hide your email address from apps and websites, but not cops

-

Politics5 days ago

Politics5 days agoShould Trump Be Scared Strait?

-

Crypto World5 days ago

Crypto World5 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech5 days ago

Tech5 days agoFlipsnack and the shift toward motion-first business content with living visuals

You must be logged in to post a comment Login