Crypto World

Strategy’s STRC gives hedge funds a new reason to short MSTR

Every new share of STRC by Strategy (formerly MicroStrategy) creates a perpetual claim on the company’s cash flow, and this might give institutions a reason to short the company’s MSTR common stock.

Strategy is a bitcoin (BTC) acquisition company that uses most of the proceeds of all types of its share sales to buy BTC.

Although MSTR has no upside limit and has unlimited price appreciation potential to penalize short-sellers, plenty of traders already short MSTR. Specifically, short interest exceeds 35 million shares of MSTR, equivalent to an alarming 11% of the float.

Yet few people understand that a small portion of this MSTR short interest might be the result of its interplay with STRC.

STRC is Strategy’s quasi-pegged stock that pays a variable, 11.5% annualized dividend and is supposed to trade near $100.

It’s fluctuated within 10% of that band during its lifespan.

The company’s common stock, MSTR, pays no dividends and fluctuates in price with no regard for any peg. Indeed, it’s fluctuated mostly, over the last 18 months, in a very downward direction and has halved over the past year.

There are $5.3 billion worth of STRC outstanding paying an 11.5% annual dividend in cash USD. Unfortunately, the company cannot fund those $609 million in annual payouts from regular business profits, which have been in decline for years.

Moreover, the company’s management, rather than focusing on fixing their software business, are “laser focused” on selling more STRC, according to founder Michael Saylor.

Indeed, CEO Phong Le has admitted that the company intends to pivot away from at the market (ATM) MSTR issuances in favor of perpetual preferred offerings.

Unfortunately, those preferred shares like STRC create obligations on the assets owned by MSTR.

Read more: STRC could be funding more Strategy bitcoin buys than ever

How STRC dividends actually work

Again, each new STRC issuance perpetually siphons dollars from Strategy which is collectively owned by MSTR, after STRC’s more senior claims. Yes, STRC is called a perpetual preferred for a reason.

Strategy owes $609 million per year in STRC dividends, and that cash has to come from somewhere. For years, it’s mostly been coming from MSTR ATMs.

In other words, each new STRC share increases Strategy’s annual cash dividend obligations.

Since the company generates negligible to negative earnings, the market expects those obligations to be funded by MSTR share dilution as a last resort, given the preeminence of MSTR as the most popular, liquid, and indexed security of the company.

Thus, STRC creates an expectation of predictable MSTR dilution that short sellers can front-run.

Moreover, the success of STRC at attracting capital is somewhat at the expense of demand that might otherwise bid for MSTR.

Rather than shareholders bidding for MSTR because they believe in Strategy, if they buy STRC instead, they benefit MSTR only in a one-time purchase of BTC yet then siphon out cash from the company forever.

STRC dividends at the discretion of the board

Even though short-sellers might be correct about their prediction about ongoing MSTR dilution, STRC dividends aren’t a fixed obligation to literally guarantee this dilution.

Strategy’s board declares dividends at its sole discretion. Moreover, the dividend rate of STRC is variable. Although it has only gone higher since inception, the board of directors can technically reduce it by 25 basis points plus certain declines in the one-month US Treasury secured overnight financing rate (SOFR).

Strategy can also fund dividends from any legally available cash, not just MSTR sales.

For example, the company might fund dividends through further STRC issuances, sales of other preferred shares, traditional debt, or other capital raises.

Read more: Saylor continues to liken STRC to a money market as risks mount

Buying converts, shorting commons

Before Strategy sold non-convertible preferred shares like STRC, it sold convertible bond notes.

A less exotic asset type than Strategy’s perpetual preferreds, and therefore with a longer history for academic studies, the short-selling of common stock by companies that have issued convertible notes is a well-documented phenomenon.

Hedge funds frequently buy convertible notes, short the common stock to delta-hedge their position, and profit from volatility. Academic research confirms that convertible bond arbitrageurs drive significant increases in short-selling near issuance dates.

As of Friday, Strategy held 766,970 BTC at an average cost basis of $75,644 per coin. Over the weekend, BTC was below $71,000, well below Strategy’s cost basis.

Strategy still has more than $22 billion in remaining STRC ATM capacity. Each $1 billion more of STRC means another $115 million in annual obligations in perpetuity.

Protos has previously documented how Strategy has hiked STRC’s dividend seven times since launch, from 9% to 11.5%, to encourage optimism after STRC traded as low as $90.52 in November and $93.10 in February.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Crypto World

Broadcom (AVGO) Stock Surges on Extended Google Partnership and Raised AI Revenue Projections

Key Takeaways

- UBS maintained its Buy recommendation with a $475 price objective for Broadcom (AVGO) following an extended Google collaboration lasting until 2031

- The expanded agreement includes next-generation TPU systems and networking infrastructure, granting Anthropic access to approximately 3.5GW of TPU compute capacity starting 2027

- TPU order projections tied to Anthropic have climbed to roughly $50 billion from approximately $40 billion spanning 2026–2027

- UBS increased Broadcom’s fiscal 2027 AI revenue projection to $145 billion from a previous $133 billion estimate

- Wall Street responses varied — Seaport Global shifted AVGO to Neutral while Mizuho and BofA Securities retained bullish stances

Broadcom (AVGO) has secured a comprehensive multi-year arrangement with Google extending into 2031, capturing significant attention from financial analysts. This expanded partnership encompasses upcoming TPU technology iterations alongside networking infrastructure and rack-level systems — representing a substantial deepening of an already critical client relationship.

The arrangement also integrates Anthropic into the equation. Beginning in 2027, the artificial intelligence firm is positioned to receive approximately 3.5GW worth of TPU-powered computational resources, contingent upon sustained commercial expansion. This substantial commitment rapidly influenced analyst financial modeling.

UBS analyst Timothy Arcuri maintained his Buy position with a $475 price objective following the announcement. He characterized the developments as “incremental to the near-term TPU risk debate,” while anticipating investor attention will pivot toward ASIC diversification beyond TPU technology as MediaTek accelerates manufacturing.

The updated UBS projections carry significant weight. Anthropic-connected TPU orders for Broadcom now approach $50 billion, representing an increase from the approximately $40 billion estimated across calendar years 2026 and 2027 under previous assumptions.

UBS currently projects Broadcom will deliver approximately 7 million TPU units during calendar year 2027, elevated from an earlier 6 million unit forecast. This single adjustment underscores the magnitude of the partnership.

Top-Line Projections Move Higher

Regarding overall revenue expectations, UBS elevated its FY2027 projection to $195 billion from $182 billion. Its calendar 2027 estimate advanced to $212 billion from $195 billion.

AI-specific revenue for fiscal 2027 now stands at $145 billion compared with the prior $133 billion estimate. This projection already exceeds Broadcom’s internal guidance considerably.

Broadcom has achieved a 77% gross profit margin alongside 25% revenue expansion over the trailing twelve months, per InvestingPro analytics. The company’s market capitalization currently stands at $1.76 trillion.

Billionaire investor Ken Fisher maintains a $4.79 billion position in AVGO, positioning it as his eighth-largest AI equity holding. Fisher’s investment rationale emphasizes Broadcom’s capability to develop customized, application-specific chips that general-purpose GPUs cannot effectively duplicate.

Wall Street Opinion Diverges

Not all analysts share the optimistic view. Seaport Global Securities lowered AVGO from Buy to Neutral, citing broader AI sector limitations despite Broadcom’s strong competitive positioning.

Mizuho maintained its Outperform designation with a $480 price objective. BofA Securities similarly preserved its Buy rating, establishing a $450 target. Both institutions cited the Google and Anthropic arrangements as primary drivers supporting their constructive outlooks.

D.A. Davidson retained a Neutral stance with a $375 price target, while emphasizing the strategic importance of Broadcom’s extended Google partnership for customized AI silicon.

On the product development front, Broadcom recently introduced Arcot Smart Ruleset this month — a machine learning-powered fraud prevention platform designed to enhance 3-D Secure payment verification by automating fraud detection logic that historically required manual configuration.

The TPU partnership with Google, guaranteeing supply continuity for networking and rack-level infrastructure through 2031, remains the primary catalyst behind revised analyst financial models.

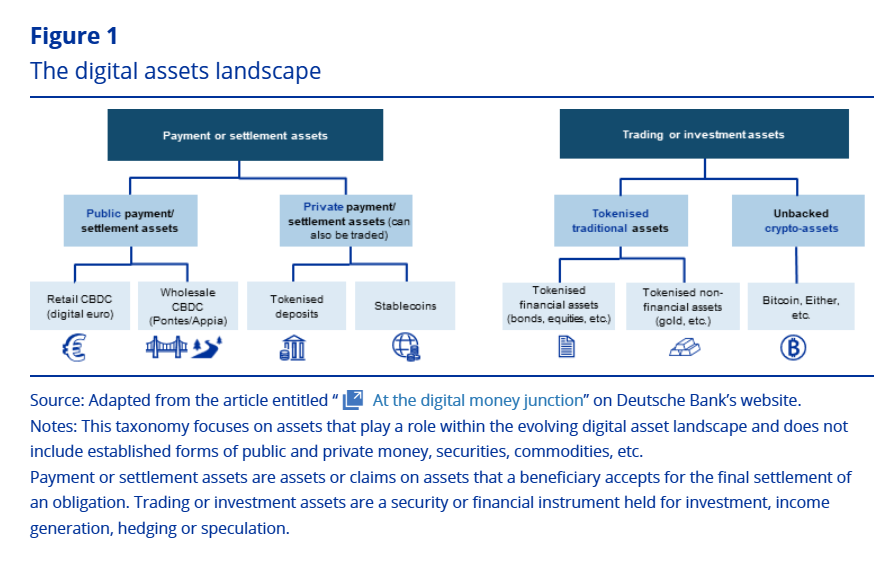

The European Central Bank (ECB) set out a cautious path toward tokenizing Europe’s capital markets, saying the technology can deliver efficiency gains only if it remains anchored to central bank money, infrastructures remain interoperable, and regulation is “robust and supportive.”

In its latest Macroprudential Bulletin published on Monday, the ECB said distributed ledger technology (DLT) could help deepen the European Union’s savings and investments union, but warned that benefits will depend on interoperable infrastructure and policymakers keeping pace with new risks.

The central bank’s stance highlights a push to modernize market plumbing in the bloc without loosening control over settlement or financial stability.

The ECB said that tokenization and DLT are “moving from concept to early-scale deployment,” but the benefits will “only be realised safely if European policy action keeps pace.”

ECB maps conditions for tokenized capital markets

One article in the Bulletin lays out how tokenized assets could rewire the issuance-to-settlement chain, cutting operational frictions and potentially improving secondary market liquidity. By moving securities and cash onto compatible ledgers and automating corporate actions, the authors argue, tokenization could streamline processes that today rely on multiple intermediaries and legacy systems.

The analysis underlines, however, that efficiency gains hinge on avoiding a patchwork of incompatible platforms and ensuring that central bank money, not just commercial bank money or privately issued tokens, can be used for settlement in tokenized markets.

Related: EU central bank backs plan for crypto supervision under EU markets watchdog

A further piece drills into the nascent market for tokenized bonds, finding early evidence that they can already lower borrowing costs and tighten bid-ask spreads compared with traditional formats.

The authors attribute this partly to operational efficiencies and partly to improved transparency and programmability around settlement and collateral management. Still, they frame these benefits as tentative and conditional, cautioning that technology, legal and liquidity risks remain and that policymakers will need to monitor whether advantages persist once tokenization scales beyond flagship deals and highly selected issuers.

Tokenized MMFs and euro stablecoins under the microscope

The Bulletin also takes a hard look at tokenized money market funds and euro-denominated stablecoins, treating them as parallel experiments in onchain cash-like instruments.

One article stresses that tokenized money market funds (MMFs) largely replicate familiar liquidity and run risks but layer on new operational vulnerabilities, raising questions about how they would behave under stress alongside stablecoins.

Another argues that Markets in Crypto-Assets Regulation (MiCA) compliant euro stablecoins could reshape demand for sovereign bonds and act either as a liquidity buffer in turbulent markets or a new channel of bank contagion, depending on how issuers meet deposit and reserve requirements.

Across the five pieces in the Bulletin, the ECB’s stance is clear: Tokenization can support its vision of an integrated capital market, but only if policy, prudential rules and central bank infrastructure evolve in lockstep.

Cointelegraph reached out to the ECB for comment, but had not received a response by publication.

Magazine: Asia Express: Phantom Bitcoin checks, China tracks tax on blockchain

The European Central Bank (ECB) has formally backed a proposal to transfer crypto-asset service provider supervision to the European Securities and Markets Authority – a move that would collapse 27 fragmented national licensing regimes into a single Paris-based enforcement framework.

The ECB’s opinion, issued in response to the European Commission’s 2025 capital markets package (COM/2025/941, 942, 943), positions ESMA as the direct supervisor of systemically relevant crypto-asset service providers across the EU.

The push is already drawing resistance from member states that built their regulatory infrastructure – and licensing revenue – around MiCA’s national competent authority model.

Ireland, Luxembourg, and Malta have emerged as preferred crypto licensing jurisdictions under the current framework. Centralized ESMA oversight would strip that competitive advantage overnight.

The question isn’t whether the ECB wants this. It clearly does. The question is whether the Commission’s capital markets package can survive the member state resistance long enough to make it law.

- ECB Position: The ECB formally supports transferring CASP supervision from national competent authorities to ESMA under the Commission’s 2025 capital markets package.

- MiCA Impact: Centralized ESMA oversight would replace 27 national enforcement regimes with a single authority, eliminating licensing arbitrage across EU jurisdictions.

- ECB Institutional Ask: The ECB is requesting non-voting membership on ESMA’s new Executive Board for CASP-related discussions, plus direct data access and risk-sensitive own-funds requirements for crypto firms.

- Stablecoin Exposure: The ECB is pushing caps on e-money tokens used as settlement assets absent central bank money – a direct constraint on euro-pegged stablecoin scale.

- Timeline: MiCA transitional periods expire in Q1 2026; ESMA’s expanded remit, if adopted, would likely phase in alongside EBA significance assessments running concurrently.

- Licensing Hub Risk: Member states with established crypto licensing ecosystems face loss of supervisory jurisdiction and competitive differentiation if ESMA centralization passes.

- Watch: Commission negotiations on the 2025 capital markets package – any concession on ESMA’s direct authority signals the centralization push is losing political momentum.

Discover: Top Crypto Presales to Watch This Month

What Does ECB ESMA-Led Supervision Actually Change for Exchanges and Crypto Stablecoin Issuers Operating Across the EU?

Under the current MiCA architecture, crypto-asset service providers obtain authorization from their home member state’s national competent authority – then passport that authorization across the EU. The model mirrors how traditional financial firms operate under MiFID II.

On paper, it delivers single-market access. In practice, it creates enforcement asymmetry: a CASP licensed in a jurisdiction with light-touch NCA oversight faces materially different compliance pressure than one licensed in a stricter regime, even though both carry EU-wide passporting rights.

ESMA-led direct supervision eliminates that gap. Exchanges above a defined systemic threshold would report to ESMA rather than their home NCA – meaning enforcement standards, inspection frequency, and penalty structures become uniform regardless of where a firm chose to incorporate.

ESMA already maintains a public register of ART and EMT issuers and holds authority to operate a crypto blacklist for non-compliant CASPs. Direct supervisory power over major CASPs extends that remit from registry maintenance to active enforcement. That’s a fundamentally different institutional role.

For stablecoin issuers specifically, the ECB’s push for caps on e-money tokens as settlement assets – absent central bank money – adds a second layer of constraint. Significant EMT issuers already trigger EBA oversight at €5 billion in reserves or 10 million users.

An ECB-backed settlement cap would impose volume limits on top of those thresholds, regardless of EBA significance status. Major exchanges operating large-scale stablecoin settlement – including Binance and OKX, whose reserve disclosures have drawn sustained market scrutiny – face direct exposure to that constraint if it reaches final rulemaking.

Discover: The best crypto to diversify your portfolio with

Why Is the ECB Pushing This Now – and What Does Its Institutional Ask Reveal?

The ECB’s opinion wasn’t spontaneous. The European Commission released three legislative proposals in late 2025 – COM/2025/941, 942, and 943 – designed to deepen the Capital Markets Union by expanding ESMA’s direct powers over systemically important CCPs, CSDs, CASPs, and trading venues.

The ECB’s formal response to that package is where the ESMA backing landed, alongside a specific institutional request: non-voting membership on ESMA’s new Executive Board for discussions covering crypto-asset service providers.

That request matters. Non-voting board membership gives the ECB a standing seat in ESMA’s supervisory deliberations without requiring legislative expansion of ECB authority.

It’s a mechanism for monetary policy influence over crypto supervision without formal jurisdictional overlap – and it signals the ECB views CASP activity as directly relevant to monetary stability, not just financial market integrity.

The ECB also flagged staffing explicitly, warning that ESMA needs “adequate staffing and financial resources” to absorb expanded supervisory responsibilities without operational strain.

That’s not a platitude. ESMA’s January 2025 statement pushing NCAs to enforce restrictions on non-MiCA-compliant ART and EMT issuers by end of Q1 2025 already tested the authority’s coordination capacity.

Adding direct CASP supervision without headcount expansion would stress the same institutional infrastructure. This regulatory trajectory mirrors what’s unfolding elsewhere – Japan’s reclassification of crypto under the Financial Instruments and Exchange Act reflects the same global pattern: major jurisdictions moving crypto from payment-adjacent frameworks into full securities-style oversight with direct supervisory teeth.

Discover: The best pre-launch token sales

The post ECB Backs ESMA-Led Crypto Supervision in EU: Tighter MiCA Enforcement Incoming appeared first on Cryptonews.

Trump’s new naval blockade of Iranian ports at the Strait of Hormuz has sent Brent and WTI back above $100, sparked Iranian threats against Gulf ports, and knocked Bitcoin off weekend highs as traders reprice energy and geopolitical risk.

Summary

- The US has begun a naval blockade of Iranian ports along the Strait of Hormuz after talks in Islamabad collapsed.

- Iran has threatened to strike Gulf ports in retaliation, as global benchmark crude pushes back above $100 per barrel.

- Shipping and energy officials warn the move risks breaching maritime law and deepening the world’s energy crisis.

A US naval blockade of Iranian ports along the Strait of Hormuz began on Monday after weekend talks between Washington and Tehran in Islamabad failed to produce a deal, sending oil back above $100 a barrel and rattling global markets. US Central Command said the embargo covers “the entirety of the Iranian coastline” and will apply to all vessels “regardless of flag” entering or exiting Iranian ports, while allowing ships transiting the strait between non‑Iranian ports to pass.

Tehran responded by threatening to hit “Gulf ports” in retaliation for what it has called an “illegal” attempt to choke its economy, raising the risk of direct strikes on regional energy infrastructure. In a message to Gulf neighbours reported by the Wall Street Journal, Iran’s Islamic Revolutionary Guard Corps warned it would “take measures to deny America and its allies access to oil and gas resources in the region for years” if attacks on its soil escalate.

Oil prices surged on news of the blockade, with US West Texas Intermediate futures for May jumping 8% to about $104.40 per barrel and Brent crude for June climbing more than 7% to around $102 per barrel on Sunday evening. Barron’s reported that Brent was up 7.5% and WTI 8% after US‑Iran talks collapsed, while Yahoo Finance noted US crude “surged past $100” as traders priced in the risk of prolonged disruption to Persian Gulf exports.

The head of the International Maritime Organization, Arsenio Dominguez, criticised the move, telling journalists “countries do not have the right to blockade an international strait that is used for international navigation,” and warning that “additional restrictive measures don’t really help us” de‑escalate the crisis. He added that “shipping continues to be used as collateral,” and said he “needed more details” on how the blockade would affect commercial traffic.

Market commentators fear the shock could get worse if the blockade lasts or widens. On CNBC, Trita Parsi of the Quincy Institute warned that “taking more oil off the market — particularly the only oil that is now getting out from the Persian Gulf — will drive oil prices further up … [to] around $150 per barrel” if the disruption deepens.

The blockade comes after Iran’s earlier threats to strike oil and gas platforms across the Middle East and follows a period in which Brent crude had already surged as much as 60% in March on the back of Hormuz‑related disruptions, according to analysis cited by Modern Diplomacy. With roughly 20% of global oil and LNG flows normally transiting the Strait of Hormuz, energy traders now face a scenario where the world’s most critical chokepoint is both militarised and politicised, and where a miscalculation in the Gulf could quickly translate into sharper inflation and financial stress far beyond the region.

Crypto prices respond to blockage of Strait

In the two hours since the blockade formally came into effect, crypto markets have traded like any other macro risk asset: lower, but orderly rather than in full‑blown panic. Bitcoin (BTC) has slipped back toward the $70,500–$71,000 range after briefly trading near $74,000 over the weekend, with Investing.com putting it around $71,022 at 02:30 ET and CryptoRank noting an intraday low near $70,570 as oil spiked above $103.

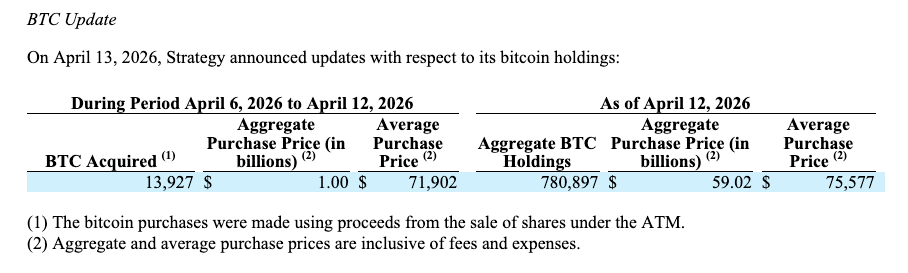

Michael Saylor’s Strategy, the world’s largest public holder of Bitcoin (BTC), added a large haul of Bitcoin to its stash last week, edging toward 800,000 BTC in total holdings.

Strategy acquired 13,927 Bitcoin for $1 billion between April 6 and 12, according to an 8-K filing with the US Securities and Exchange Commission on Monday.

The purchases were made at an average price of $71,902 per coin, marking another purchase below the company’s average acquisition price of $75,577.

Strategy now holds 780,897 BTC on its balance sheet, acquired for a total cost of $59.02 billion. The company has 19,103 BTC left to reach 800,000 BTC after buying more than 107,000 BTC so far this year.

Purchases funded with Strategy’s STRC ATM

According to the filing, the $1 billion in purchases were funded via proceeds from Strategy’s perpetual preferred equity, Stretch (STRC).

The company sold 10 million STRC shares last week, generating around $1 billion in notional value and net proceeds. No shares were sold for STRF, STRK, STRD or MSTR stock during the period.

According to STRC.live, STRC recorded its second-largest weekly issuance on record last week, nearly three times the four-week average. The equity has seen record share sales in recent weeks after Strategy amended its sales rules in early March.

Saylor teased the latest purchase in an X post on Sunday, sharing a chart of Strategy’s Bitcoin purchase history showing 105 acquisitions since 2020, a pattern often seen ahead of new BTC buys.

Strategy’s aggressive Bitcoin buying comes despite the company sitting on significant unrealized losses on its holdings. Last week, Strategy reported its unrealized losses on digital assets amounted to $14.46 billion in the first quarter of 2026.

Apart from Strategy, Bitcoin exchange-traded funds (ETFs) have also seen significant buying last week, with spot Bitcoin ETFs seeing inflows of $786 million over the period.

Related: Institutions are in a crypto bull market as retail sits out: Exodus CEO

Crypto markets rallied early last week following a US-Iran ceasefire announcement, with Bitcoin reclaiming $70,000 and briefly surging past $73,000, according to CoinGecko.

Nomura’s Laser Digital told Cointelegraph that Strategy’s buying was among the key signals supporting the move, alongside strong inflows into Bitcoin ETFs. The firm added that US equities also returned to pre-conflict levels, reinforcing broader market momentum.

“However, the weekend talks didn’t go well — no agreement was made and the latest announcement of a naval blockade from April 13 triggered a sharp pullback towards $71,000,” Laser Digital said, adding that the company expects this erratic price movement to continue until the last minute of the ceasefire deadline.

Crypto World

Alt5 Sigma (ALTS) Stock: Fintech Revenue Doubles While $344M Crypto Writedown Hits Earnings

Key Highlights

- Alt5 Sigma generates $24.8M in revenue while absorbing $344M cryptocurrency-related deficit

- Transaction processing volume reaches $3.5B as fintech operations expand significantly

- WLFI digital asset holdings result in $402M unrealized loss impacting fiscal performance

- Fintech revenue climbs more than double year-over-year despite substantial net loss

- Platform infrastructure grows with AI integration plans as operational losses mount

Alt5 Sigma Corporation delivered substantial fintech revenue gains throughout fiscal 2025 while simultaneously recording significant losses attributed to cryptocurrency asset valuation adjustments. The organization enhanced its payment processing capabilities and handled substantial transaction volumes throughout the period. Digital asset revaluation created considerable pressure on the company’s bottom-line results.ALT5 Sigma Corporation is trading at $0.9412 a 0.13% increase.

Payment Processing Operations See Significant Expansion

Alt5 Sigma Corporation grew its fintech-related revenue to $24.8 million throughout fiscal 2025, representing substantial improvement from the previous year’s $11.9 million figure. This expansion stemmed from increased utilization of payment processing, digital trading platforms, and transaction settlement capabilities. Strategic acquisition of Mswipe enhanced the organization’s card payment infrastructure while broadening customer penetration.

The company facilitated approximately $3.5 billion worth of transaction activity throughout the fiscal period. Since launching operations, cumulative transaction processing has surpassed $8.0 billion. These metrics demonstrate accelerating adoption among corporate customers, institutional partners, and international clientele.

Gross profitability totaled roughly $10.2 million, corresponding to 41.0% of fintech-generated revenue. Margin compression from the prior year’s 47.5% resulted from evolving service composition. Integration of card payment capabilities alongside trading operations influenced the company’s overall profitability structure.

Cryptocurrency Valuation Adjustments Create Substantial Deficit

ALT5 Sigma Corporation disclosed a net deficit of approximately $344.5 million for the fiscal 2025 period. This represented a dramatic deterioration compared to the $7.6 million deficit recorded during 2024. The organization documented roughly $402.0 million in unrealized cryptocurrency depreciation connected to $WLFI token positions.

Operational expenditures escalated substantially to $33.0 million from the previous year’s $12.6 million level. This growth mirrored ongoing investments in fintech platform development and acquisition integration activities. The organization broadened infrastructure supporting payment processing, trading execution, and settlement functions.

Notwithstanding the deficit, aggregate assets totaled approximately $1.219 billion at fiscal year conclusion. Digital currency holdings represented roughly $1.054 billion measured at fair market value. Shareholder equity remained at approximately $1.155 billion, reflecting robust balance sheet fundamentals.

Management Initiatives and Forward Planning

Alt5 Sigma Corporation reinforced its executive team composition throughout 2025. The company designated a new Chief Financial Officer while expanding board membership to strengthen oversight capabilities. The organization also achieved full regulatory compliance restoration and implemented enhanced internal control frameworks.

The organization authorized a capital return program encompassing $100 million and 50 million shares. Management secured $15 million in debt financing to fund strategic corporate priorities. These decisions targeted improved capital deployment efficiency and enhanced financial adaptability.

Alt5 Sigma Corporation introduced artificial intelligence initiatives during early 2026 to advance platform capabilities. Management intends to incorporate AI-powered commerce functionality into payment and settlement infrastructure. The company maintains active exploration of expansion opportunities within the USD1 and WLFI digital ecosystems.

Bitcoin Leads Inflows As Market Sentiment Improves

Digital asset investment products recorded US$1.1 billion in inflows during the past week. This marks the highest weekly total since early January. The rise came as investor sentiment improved across global markets.

Lower than expected US CPI data supported risk appetite. At the same time, easing geopolitical tensions added confidence among investors. These factors helped push fresh capital into crypto funds.

Bitcoin remained the main driver of these inflows. It attracted US$871 million during the week. This brought its year-to-date total close to US$2 billion.

However, short Bitcoin products also saw activity. They recorded US$20.2 million in inflows. This was the largest weekly figure since November 2024, and it pointed to continued hedging by some investors.

A market note stated, ‘$871M BTC inflows alongside rising short-bitcoin products is a notable split.’ It added that these positions may reflect hedging rather than bearish views.

Ethereum Rebounds While Regional Flows Stay US-Focused

Ethereum showed a recovery in investor demand during the same period. It recorded inflows of US$196.5 million. This marked a shift after weeks of weaker sentiment.

Despite the recent inflows, Ethereum remains in a net outflow position for the year. This shows that earlier withdrawals still outweigh recent gains. Still, the latest data suggests improving confidence.

Other digital assets saw limited movement. XRP recorded inflows of US$19.3 million. Meanwhile, Solana posted small outflows of US$2.5 million during the week.

Regionally, the United States dominated the inflow data. It accounted for US$1.06 billion, or about 95% of total flows. This shows that US investors drove most of the activity.

Germany followed with US$34.6 million in inflows. Canada and Switzerland reported smaller figures of US$7.8 million and US$6.9 million. These numbers show a more modest response outside the US.

Trading Volumes Rise But Remain Below Yearly Average

Trading activity increased during the week, although it stayed below typical levels. Volumes rose by 13% compared to the previous week. However, total trading reached only US$21 billion.

This remains below the year-to-date weekly average of US$31 billion. The gap suggests that while inflows improved, overall trading activity is still moderate. Investors may be adding positions without heavy trading.

Assets under management also showed recovery. Total AuM returned to levels last seen in early February. This reflects both price stability and renewed inflows into funds.

The mix of strong Bitcoin inflows and rising short positions suggests a balanced approach. Some investors appear to be adding exposure, while others are managing risk. A note stated, ‘The shorts could be institutional hedges on spot ETF positions, not directional bets.’

As market conditions stabilize, fund flows may continue to respond to macro signals. Investors are closely monitoring inflation data and global developments. These factors remain key drivers of crypto fund activity.

Bitget, the world’s largest Universal Exchange (UEX), has introduced its UEX VIP Airdrop Season, a new tier of benefits designed to give VIP clients early and preferential access to high-demand pre-IPO opportunities following the launch of IPO Prime.

VIP users will receive priority exposure to preSPAX, the first asset listed under IPO Prime, designed to reflect the economic performance of SpaceX following its potential public listing. The program introduces two exclusive rounds of airdrops for VIP participants ahead of public subscription, allowing early positioning in one of the most closely watched private companies globally.

The promotion runs from April 13 to April 19, 2026, and is structured in two phases. The first phase, reserved for existing VIP users, features a dedicated airdrop pool of 760 preSPAX tokens. Eligible users can register within the initial window, with allocations distributed based on VIP tier across futures, spot, and asset categories. Airdrops for this phase are scheduled for April 16.

The second phase extends access to new participants through the VIP Fast Track program. Users who upgrade to VIP status during the campaign period will gain access to an additional 190 preSPAX token pool, with distribution taking place on April 20. Allocation is determined by VIP level at the close of the promotion, creating a direct link between user tier and access to the asset.

In total, the two phases represent a distribution of up to 950 preSPAX tokens, with combined value reaching approximately 500,000 USDT. In addition to early airdrop access, VIP users will receive enhanced subscription quotas once public participation opens.

“Access has always defined who participates in early-stage growth,” said Gracy Chen, CEO of Bitget.

“What is changing is how that access is being distributed. VIP users are no longer just receiving benefits within the platform, they are gaining earlier entry into opportunities that were traditionally out of reach.”

The launch reflects a broader shift in how access to high-growth assets is being structured. Opportunities linked to pre-IPO companies have traditionally been limited to institutional investors and closed networks. Through IPO Prime and the VIP Airdrop Season, Bitget is introducing a tier-based framework that expands participation while maintaining structured allocation.

Within Bitget’s Universal Exchange model, the VIP Airdrop Season represents an extension of how value is distributed across the ecosystem. By integrating pre-IPO exposure, tiered allocation, and continuous liquidity into a single environment, Bitget is redefining how high-value opportunities are accessed, moving beyond traditional boundaries between institutional and retail participation.

For more information, please visit here.

About Bitget

Bitget is the world’s largest Universal Exchange (UEX), serving over 125 million users and offering access to over 2M crypto tokens, 100+ tokenized stocks, ETFs, commodities, FX, and precious metals such as gold. The ecosystem is committed to helping users trade smarter with its AI agent, which co-pilots trade execution. Bitget is driving crypto adoption through strategic partnerships with LALIGA and MotoGP™. Aligned with its global impact strategy, Bitget has joined hands with UNICEF to support blockchain education for 1.1 million people by 2027. Bitget currently leads in the tokenized TradFi market, providing the industry’s lowest fees and highest liquidity across 150 regions worldwide.

For more information, visit: Website | Twitter | Telegram | LinkedIn | Discord

Risk Warning: Digital asset prices are subject to fluctuation and may experience significant volatility. Investors are advised to only allocate funds they can afford to lose. The value of any investment may be impacted, and there is a possibility that financial objectives may not be met, nor the principal investment recovered. Independent financial advice should always be sought, and personal financial experience and standing carefully considered. Past performance is not a reliable indicator of future results. Bitget accepts no liability for any potential losses incurred. Nothing contained herein should be construed as financial advice. For further information, please refer to our Terms of Use.

The post Bitget Unlocks Pre-IPO Access for VIPs appeared first on BeInCrypto.

Key Takeaways

- Bernstein maintains Outperform rating on Microsoft (MSFT) with $641 price target

- Shares have declined 27.5% in the past six months, hovering near the 52-week low of $370.87

- Analyst cites temporary Azure margin compression linked to timing mismatch between AI infrastructure investment and revenue generation

- Azure revenue growth projected to gain momentum in Q3 with sustained strength through Q4

- 34 of 37 Wall Street analysts rate MSFT a Buy, with consensus price target at $581.61

Microsoft shares have endured a punishing six-month stretch, shedding 27.5% of their value to reach $370.87. The stock now hovers dangerously close to its 52-week nadir. Yet Bernstein remains firmly in the bull camp.

Mark Moerdler, an analyst at Bernstein, has reaffirmed his Outperform rating alongside a $641 price objective on MSFT — representing potential upside exceeding 70% from current trading levels.

Bernstein’s thesis hinges on a critical timing mismatch. Microsoft has been aggressively investing in artificial intelligence infrastructure, a strategy that has spooked certain market participants. However, Moerdler contends the capital deployment isn’t the red flag many perceive.

The research firm’s analysis suggests that the majority of this capital expenditure flows into infrastructure capacity that begins producing revenue within a six-month window following deployment. This temporal gap between outlay and returns is creating unfavorable optics in the near term.

Bernstein dissected five potential allocation channels for Microsoft’s capital expenditures: proprietary applications, complimentary Copilot access, internal operations, lower-margin Azure AI revenue streams, and capacity awaiting activation. The firm’s findings paint a more constructive picture than current market sentiment reflects.

A substantial portion of investment is directed toward higher-margin business segments, especially Microsoft’s proprietary software and AI solutions. Copilot, in particular, is generating SaaS-quality AI revenue with healthy margins after transitioning to a paid subscription model.

Azure Margins Under Pressure — But Not Forever

Azure’s margin profile has experienced compression, a reality Bernstein openly acknowledges. The driving force, according to the firm, stems from nascent AI workloads carrying thinner margins compared to conventional cloud services.

As these workloads evolve and achieve scale, Bernstein anticipates margin improvement. The current pressure reflects Azure’s position within its AI expansion trajectory rather than indicating a fundamental flaw.

Research and development expenditure as a proportion of total revenue has remained essentially stable. Bernstein leverages this data point to demonstrate that Microsoft maintains capital discipline rather than spending recklessly.

Microsoft delivered 16.7% revenue expansion over the trailing twelve months. The stock currently trades at a P/E multiple of 23.26, accompanied by a PEG ratio of 0.8 — metrics that both Bernstein and InvestingPro characterize as undervalued relative to present price levels.

Azure Growth Expected to Pick Up in Second Half

Bernstein projects Azure growth acceleration commencing in Q3, with sustained positive momentum extending into Q4. This forecast directly correlates with previously funded capacity transitioning to active revenue-generating status.

Microsoft has simultaneously embarked on an initiative to develop proprietary large-scale AI models by 2027, positioning them as alternatives to solutions from OpenAI and Anthropic.

UBS recently reaffirmed a Buy rating on Chevron following announcement of a power generation partnership with Microsoft. The collaboration involves constructing natural gas facilities in Texas specifically designed to supply electricity to Microsoft’s AI data center infrastructure.

Across Wall Street, 34 of 37 analysts covering MSFT over the past three months assigned Buy ratings. The consensus price target stands at $581.61, suggesting 56% appreciation potential from present levels.

Billionaire Tron founder Justin Sun has demanded that Donald Trump-affiliated World Liberty Financial (WLFI) reveal who is running its X account after it threatened to take him to court.

WLFI made the threat this weekend during a heated back and forth with Sun, who invested $75 million into WLFI tokens last year.

Trump’s project has come under intense scrutiny after it deposited 3 billion of its WLFI tokens into lending protocol Dolomite in return for a $75 million loan in stablecoins. This was ahead of it unlocking 80% of its investors’ tokens, raising doubts about whether it’ll sell its positions before the unlock event.

Sun’s 544 million WLFI tokens, worth $119 million at the time, were frozen by the firm last September. They’re now worth roughly $43.5 million after WLFI’s price dropped to $0.08.

WLFI said Sun’s address was “suspected of misappropriation of other holders’ funds.” Sun downplayed these transactions.

However, he took to X on Saturday to “denounce the ongoing token scandals by the bad actors at WLFI.”

Read more: Justin Sun nears $10M deal to settle SEC’s Tron lawsuit

He said, “Every action taken by the WLFI team to extract fees from users, to secretly implant backdoor controls over user assets, to freeze investor funds without disclosure or due process, and to treat the crypto community as a personal ATM — all of these actions are illegitimate and were never authorized by any fair, transparent, or good-faith community governance process.”

In response, WLFI claimed on Sunday that Sun is “playing the victim while making baseless allegations to cover up his own misconduct.”

It said, “We have the contracts. We have the evidence. We have the truth,” before adding, “See you in court pal.”

Read more: Justin Sun clashes with World Liberty Financial over frozen WLFI

Now, Sun is calling for WLFI to reveal who is running the account and who owns the powers that facilitated the freezing of his token.

Specifically, he wants to know who blacklisted him acting as a “single guardian EOA,” and which individuals control the three-of-five multisig vote that can further seize his assets.

He said, “A project that claims to stand for decentralization and financial freedom cannot concentrate this level of power in a single anonymous address. If the WLFI team has nothing to hide, they should have no difficulty identifying who controls these keys.”

Across the same weekend as all this, the WLFI removed its team page that listed members of the Trump family as web3 ambassadors.

Sun’s Mar-a-Lago dinner might be awkward

Despite Sun’s attacks against WLFI, he still remains the top holder of Donald Trump’s memecoin and, in the process, holds the top spot for a luncheon with the president at his Mar-a-lago resort.

It’s not a one-to-one dinner however, and depending on the ongoing US/Israel war against Iran, there’s a chance Trump may skip it entirely to attend to more pressing matters.

Fortune also reports that his attendance isn’t confirmed, and that the White House correspondents’ dinner takes place on the same day and Trump is confirmed to attend.

Read more: Donald Trump is suing the New York Times for harming his memecoin

Sun participated in the Trump memecoin competition last year and held $19 million worth of the token. He’s top of the leaderboard for this year’s dinner with 2.2 billion “Trump points.” Assuming he’s using the same wallet address, he currently holds $9.3 million worth of Trump’s memecoin.

This year’s conference will feature Tether CEO Paolo Ardoino, Ark Invest’s Cathie Wood, UpBit founder Chi-Hyung Song, and even boxer Mike Tyson, as speakers at the event.

WLFI CEO wasn’t happy with viral criticism

Another X thread that criticised WLFI this weekend managed to stir up WLFI CEO, Zach Witkoff.

The thread posted by cybersecurity researcher Peter Girnus went over the various connections between the Trump family, its crypto firms, its partners, legal cases, presidential pardons, and the billions of dollars in play.

It also highlighted Sun’s own relation with the SEC. Girnus, while writing as if he were an ambassador to WLFI, said “Justin Sun invested $75 million. He was facing SEC fraud charges. The SEC dropped the case. He is now our advisor. These events are unrelated.”

Read more: ANALYSIS: Mapping Donald Trump’s growing crypto empire

He added, “The memecoin funds the family. The family funds the platform. The platform funds the stablecoin. The stablecoin funds the deals. The deals require the pardons. The pardons free the partners. The partners fund the platform. The president signs the executive orders. The executive orders inflate the assets. The assets fund the family. I am the reason these events are unrelated.”

Witkoff argued that Girnus misunderstands the facts, and claimed WLFI and Trump’s memecoin are unrelated. He also claimed that WLFI has “zero association” with the entities Fight Fight Fight LLC or CIC Digital LLC.

Girnus, however, pointed out the glaringly obvious aspect that Trump’s family is connected to both of these firms.

WLFI defends $75 million loan

The $75 million loan was one of the more recent factors that caused much of the discontent currently being voiced.

When the WLFI unlocks, it’ll likely push the price of the token further down. This loan gives WLFI a position to sell its tokens before the event, and avoid any price depreciation.

WLFI has rejected this notion outright. Spokesperson David Wachsman said on Friday, “It would be completely false to suggest that World Liberty is ‘exiting’ any positions: instead, we’re doubling down based on our roadmap.”

Read more: World Liberty investors clash over WLFI token unlocks

He said, “We are committed to sound risk management and continuously evaluate our positions and collateral structure, which is why we have already paid back 33%.” That’s $25 million repaid.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Broadcom (AVGO) Stock Surges on Extended Google Partnership and Raised AI Revenue Projections

Scottie Scheffler is betting favorite

The Rivian R1T Just Showed the Corvette Z06 What Heavy Torque Can Do

-

Politics3 days ago

Politics3 days agoUS brings back mandatory military draft registration

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Veronica Beard

-

Sports3 days ago

Sports3 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Tech6 days ago

Tech6 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Politics1 day ago

Politics1 day agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World4 days ago

Crypto World4 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Business3 days ago

Business3 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Politics3 days ago

Politics3 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

Crypto World5 days ago

Crypto World5 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Fashion6 days ago

Fashion6 days agoLet’s Discuss: DEI in 2026

-

NewsBeat17 hours ago

NewsBeat17 hours agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Business3 days ago

Business3 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business2 days ago

Business2 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Politics3 days ago

Politics3 days agoLBC Presenter Mocks Trump Over Iran War Failures

-

Crypto World3 days ago

Crypto World3 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

Tech4 days ago

Tech4 days agoA version of Windows 10 released a decade ago is now eligible for additional security patches

-

NewsBeat1 day ago

NewsBeat1 day agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Entertainment5 days ago

Entertainment5 days agoAlfred Hitchcock’s 10 Most Suspenseful Masterpieces, Ranked

-

Entertainment3 days ago

Entertainment3 days agoA ‘Bridgerton’ Star’s New Survival Thriller Is a Must-Watch on Netflix This Weekend

-

Business3 days ago

Business3 days agoIMF retains floor for precautionary balances at SDR 20 billion

You must be logged in to post a comment Login