Crypto World

Tesla Stock Drops Despite Q2 Production Beat as Concerns Deepen

TLDR

- Tesla exceeded Wall Street expectations by producing 451758 vehicles during the second quarter.

- Tesla shares declined after the production update as investors remained concerned about profitability.

- Investors shifted their attention from production growth to vehicle margins and overall financial performance.

- Elon Musk’s long-term strategy around robotaxis, artificial intelligence, and autonomous driving remains central to Tesla’s valuation.

- The upcoming earnings report is expected to provide clearer insight into Tesla’s margins, cash flow, and future growth outlook.

Tesla (TSLA)reported stronger-than-expected second-quarter production, yet its shares declined after the update. The mixed reaction highlighted persistent concerns about profitability despite improving vehicle output. Investors now await the company’s earnings report for clearer evidence of financial strength.

Strong Production Eases Demand Concerns

Tesla produced 451,758 vehicles during the second quarter, beating most Wall Street expectations. The result suggested customer demand remained stronger than many analysts anticipated. The production update also eased concerns after a weaker first quarter.

The stronger figure supported the view that Tesla regained production momentum during the quarter. However, the market quickly shifted attention beyond headline production numbers. Investors focused on whether higher output would improve financial performance.

Production growth alone did not convince the market about Tesla’s long-term outlook. Instead, investors questioned whether discounts reduced profitability across vehicle sales. That concern limited enthusiasm despite the better-than-expected production result.

Tesla Stock Falls Despite Production Surprise

Tesla shares fell after the production announcement despite the positive surprise. The market reaction showed investors wanted stronger evidence than higher vehicle production. Many analysts believe revenue quality remains more important than delivery volume.

The company can deliver more vehicles while generating weaker profits through aggressive price reductions. That possibility remains a major concern for shareholders. Strong production therefore failed to remove questions about operating margins.

Tesla continues to trade at a premium compared with traditional automakers. That valuation creates higher expectations for earnings growth and future expansion. Investors therefore expect exceptional financial performance rather than ordinary automotive results.

Future Growth Remains the Central Focus

Chief Executive Officer Elon Musk continues to promote autonomous driving, robotaxis, artificial intelligence, energy storage, and humanoid robots. Those businesses remain central to the long-term investment case for Tesla. Supporters believe those technologies justify the company’s premium valuation.

Bullish investors argue the latest production figures prove Tesla recovered from earlier weakness. They believe the first quarter represented a temporary slowdown instead of lasting demand problems. The stronger production data strengthened that argument.

Bearish investors maintain Tesla must prove those vehicles generated healthy profits. They expect upcoming earnings to reveal margin trends and cash flow performance. Management commentary on pricing, robotaxis, and autonomous driving could also influence future sentiment.

The upcoming earnings report now represents the next major catalyst for Tesla shares. Investors expect updates on gross margins, operating income, and free cash flow. Those results will determine whether Tesla can support its premium valuation after the stronger quarter.

Every dollar Robinhood Chain earns, a tenth goes to a DAO treasury controlled by strangers. The arrangement has been covered a dozen times as good news for Arbitrum’s token.

Summary

- Robinhood Chain runs on Arbitrum’s Orbit stack, and under the Arbitrum Expansion Program every Orbit chain settling outside Arbitrum One routes 10% of net protocol revenue back to the Arbitrum ecosystem.

- The split is fixed: 8% to the Arbitrum DAO treasury, controlled by ARB tokenholders, and 2% to the Arbitrum Developer Guild.

- The figures are now real, no longer theoretical. Robinhood Chain has passed $2 million in cumulative revenue since its July 1 launch, with roughly $200,000 flowing to Arbitrum, and Arbitrum reported the network earning over $800,000 in a single seven-day stretch, annualizing near $42 million.

- The payment is calculated on net revenue after operating costs, applies to sequencer profits, and may extend to MEV capture if the chain adopts Arbitrum’s Timeboost mechanism.

- Every version of this story published so far has been written for ARB holders. The unexamined half is what the arrangement costs the brokerage, and why a company with a $2.2 billion war chest chose to pay it.

Nobody has asked the other question: what a licensed brokerage that spent a decade removing intermediaries bought by becoming a tenant.

There is a particular irony in a company whose entire founding pitch was the removal of intermediaries acquiring one. Robinhood spent a decade telling retail investors that the layers between them and the market were extractive, that commissions were a tax on participation, and that the right architecture was fewer parties taking a cut. On July 1 it launched its own blockchain, the most complete expression of that philosophy available: a settlement layer it controls, sequencing it operates, and fee revenue it collects. And under the terms of the technology stack it chose, a tenth of what that chain nets goes to somebody else. Specifically, 8% goes to a treasury controlled by holders of a governance token, and 2% funds a developer guild, both under an arrangement called the Arbitrum Expansion Program. The mechanism has been reported repeatedly since Offchain Labs disclosed it, always from one direction: what it means for ARB, why the token rallied, how a governance asset acquired a revenue claim. This piece asks the question those pieces did not. What did Robinhood buy, what is it paying, and does the arithmetic work.

What the arrangement actually is

The mechanics are specific enough to matter, and they have been reported loosely in several places.

The Arbitrum Expansion Program applies to any Layer 2 or Layer 3 chain built with Arbitrum’s Orbit toolkit that settles outside Arbitrum One or Arbitrum Nova. Those chains route 10% of net protocol revenue back to the Arbitrum ecosystem. Of that 10%, eight percentage points flow to the Arbitrum DAO treasury, which ARB tokenholders control through governance, and two percentage points fund the Arbitrum Developer Guild, which supports tooling, grants, and protocol work.

Three details in that description carry weight and are frequently dropped.Net, not gross. The calculation runs on revenue remaining after network operating costs, which ties the payment to a chain’s actual profitability instead of raw transaction throughput. That is materially friendlier to an operator than a gross fee would be, and it means a chain running at thin margins pays little regardless of volume.

Sequencer profits are the base. The revenue subject to sharing comes from the entity that orders and processes transactions, which on Robinhood Chain is Robinhood. That is the same revenue line this publication has examined as the core economics of any Layer 2, and it is precisely the line the chain exists to capture.

MEV may be included. If the chain adopts Timeboost, Arbitrum’s mechanism for capturing maximal extractable value from transaction ordering, those revenues could fall under the sharing arrangement as well. Whether Robinhood adopts it is a live question with real dollars attached, since ordering advantages on a chain hosting tokenized equities are worth considerably more than on a memecoin venue.

For contrast, Arbitrum One sends 100% of its own fees to the Arbitrum treasury. The Orbit arrangement is the lighter one, which is the point: it is the price of using the stack without settling on the flagship chain.

The numbers, now that they exist

For the first three weeks this was an abstraction. It is not anymore.

Robinhood Chain has passed $2 million in cumulative revenue since its July 1 launch, with approximately $200,000 routed to the Arbitrum ecosystem under the program. That is a clean 10%, and it is the first hard confirmation that the mechanism operates as described, not as an aspiration in a governance document.

Around that sit the throughput figures that produced it. The chain processed roughly 4 million transactions in its first week. Uniswap alone recorded $500 million in 24-hour volume on it. A single day in early July cleared $568 million. Within about two weeks the chain was clearing more than $800 million in daily decentralized exchange volume, briefly exceeding Ethereum’s, with roughly $3.9 billion across a week. Arbitrum reported the network earning over $800,000 in revenue across seven days, which annualizes near $42 million. Deposits crossed $600 million this week, rising 50% in seven days.

Now the distortion that every honest reading has to apply. The chain is running a 90-day gas subsidy, expiring around October, which means users are not paying the fees a mature chain would charge and the revenue figures are suppressed accordingly. Our audit of the chain’s first month documented how thoroughly that subsidy inflates activity metrics; it works in the opposite direction on revenue. The $42 million annualized figure is therefore both a real number and a floor, and the interesting reading comes after the subsidy lapses, when volumes and revenues both reprice. For broader context, crypto.news has also explained the subsidy distorting these numbers.

At current run rates, Arbitrum’s share is roughly $4 million a year. Against Robinhood’s quarterly revenue near $1.27 billion, that is a rounding error. Against the chain’s own economics, it is a tenth of everything.

What Robinhood bought

The arrangement only looks strange if you assume the alternative was free. It was not, and the alternatives are worth setting out because the choice reveals the strategy.

Build independently. A brokerage could commission a chain from scratch, own 100% of sequencer revenue, and pay nothing to anyone. The cost is time, engineering risk, and security. Rolling your own settlement layer means auditing it, defending it, and answering for it when something breaks, which for a regulated financial institution holding customer assets is not a theoretical exposure. It also means no ecosystem: no existing tooling, no bridges, no wallets that already work.

Use an existing chain. Deploy on Arbitrum One or Base or anywhere else, pay ordinary fees, capture nothing. This is what Robinhood actually did first, launching tokenized stock offerings on Arbitrum in 2025 before committing to its own chain, and the limitation is obvious: you are a tenant with no landlord’s economics and no control over the roadmap, the fee schedule, or who else gets to build next door.

Take the Orbit path. Get a chain you brand, control, and sequence, with Offchain Labs providing technical support, inheriting the Arbitrum ecosystem’s tooling and security assumptions, at the price of a tenth of net revenue. The launch specifications suggest what that bought: 100-millisecond block times, EVM compatibility, ETH as the gas asset instead of a new token nobody asked for, and a chain live and processing millions of transactions within a week of announcement.

Read that way, the 10% is a build-versus-buy decision resolved in favour of speed, and for a public company with a stock to defend and a crypto revenue line that fell 47% year over year in the first quarter, speed was plausibly worth more than margin. Our earnings analysis covered why the timing mattered so much.

The uncomfortable version of the same read is that Robinhood, having concluded that owning the rails is where the value sits, does not actually own them. It leases them, with favourable terms, from a decentralized organization whose token holders vote on what to do with the proceeds.

The tenant problem

That last sentence is not a rhetorical flourish. It describes a governance relationship that no traditional financial infrastructure arrangement resembles, and it has consequences nobody has priced.

The 8% going to the Arbitrum DAO treasury is controlled by ARB tokenholders through governance votes. Those holders decide how the money is deployed. They also, through the same governance process, hold influence over the direction of the technology stack Robinhood’s chain depends on. A licensed brokerage supervised by federal regulators is now a revenue contributor to, and a dependent of, an entity whose decision-making runs through token voting by anonymous participants.

For most crypto-native businesses that is unremarkable. For a public company that files with the SEC, answers to a board, and holds customer assets under regulatory obligation, it is a novel counterparty structure. The questions it raises are practical, not philosophical: what happens if governance votes to change the fee arrangement, what recourse exists if the stack’s roadmap diverges from the tenant’s needs, and how a regulated institution documents dependency on a DAO in its risk disclosures.

There is also a competitive dimension. The Orbit program applies universally, meaning any competitor can take the same path on the same terms. The arrangement Robinhood entered is not exclusive and confers no advantage over the next brokerage to build a chain, which limits how much of a moat the whole exercise creates. What it does create is a template, and the rest of the industry has noticed: our coverage of the tokenized-equity race documented Nasdaq building blockchain share issuance with Kraken’s parent and ICE working with OKX, none of which requires anyone to build from scratch.

Does the arithmetic work

Set aside the framing and ask the commercial question, because the answer determines whether any of this matters.

Roughly $42 million annualized in chain revenue, before the subsidy expires, against $4 million to Arbitrum. Against a company whose quarterly revenue runs near $1.27 billion, the chain contributes something in the low single-digit percentage range of annual revenue at current run rates, and the Arbitrum payment is immaterial to the parent by any measure.

Which means the fee share is not the story financially. It is the story structurally, because it clarifies what the chain actually is. Robinhood did not build a chain to earn sequencer fees; the numbers are too small relative to its brokerage business for that to be the motivation. It built one to control the settlement layer for tokenized equities, to avoid depending on a competitor’s infrastructure as that market develops, and to own the venue where its own products trade. Sequencer revenue is a byproduct, and 10% of a byproduct is a reasonable price for the option.

The test comes when the byproduct stops being small. If tokenized equities scale the way the DTCC’s entry into the same market suggests they might, and if Robinhood Chain hosts a meaningful share of that activity, the sequencer line grows and the 10% grows with it. A tenth of a rounding error is nothing. A tenth of a business is a negotiation, and the Arbitrum Expansion Program’s terms were set by the party that wrote them.

The precedent this sets

Strip out the two companies and the arrangement describes something the industry has been moving toward without naming: infrastructure providers taking a percentage of businesses they do not operate.

Arbitrum’s position under this model is closer to a franchise operator than a blockchain. It supplies the technology, the tooling, the security assumptions, and the developer support, and it collects a percentage of what franchisees earn across an expanding set of chains it did not build. Offchain Labs has been explicit that this is the strategy, framing enterprise adoption as the revenue thesis and noting that the flagship chain’s economics are separate. The model compounds with adoption in a way that grants and one-time licensing never do.

That has an obvious appeal for anyone holding the governance token, and it has a less obvious implication for everyone building on the stack. A percentage arrangement set at launch, when the tenant is small and the terms are generous, is an arrangement that becomes expensive precisely when the tenant succeeds. Ten percent of nothing costs nothing. Ten percent of a settlement layer hosting a meaningful share of tokenized equities is a real line item, and it is collected by a party whose consent the tenant needed at the start and whose terms the tenant did not write.

The comparison from outside crypto is the app store. Developers accepted a percentage when the platform was small and the alternative was no distribution, and spent the following decade in litigation and regulatory complaint about the rate. Nothing about the Arbitrum arrangement is coercive in that way, since alternatives genuinely exist and the terms are public. But the structural shape is familiar, and the history of platform percentages is that they are renegotiated by the largest tenants, eventually, loudly.

Robinhood is now among the largest tenants on this particular platform. Whether it ever behaves like one is a question for the quarter after the subsidy expires, when the numbers stop being small enough to ignore.

What to watch

The revenue line after October. The 90-day gas subsidy expires around then, and the first unsubsidized quarter is the only honest read on what the chain actually earns. Both volumes and revenues reprice, in opposite directions, and the net is unknown.

Whether Timeboost gets adopted. MEV capture on a chain hosting tokenized equities is worth real money, and adopting Arbitrum’s mechanism would likely bring those revenues under the sharing arrangement. The decision is a direct read on how Robinhood values ordering revenue against the cost of sharing it.

Disclosure in the filings. Whether the chain’s economics, including the Arbitrum arrangement, appear in Robinhood’s regulatory filings as a described dependency or a risk factor, and in what language. A public company documenting a revenue-sharing obligation to a DAO would be a first worth reading closely.

Whether the terms hold. The Expansion Program’s rates are set by Arbitrum governance. Any proposal to change them, in either direction, would test how much leverage a large Orbit tenant actually has, and Robinhood is now among the largest.

Competing chains on the same terms. Every brokerage that follows takes the same deal. If the tokenized-equity market fragments across several Orbit chains, the interesting question stops being what Robinhood pays and becomes what Arbitrum collects from an entire category it does not operate.

A final note on why the framing in the existing coverage matters more than it looks. Every account of this arrangement published so far was written for holders of a governance token, which meant the operative question was always whether the revenue share is large enough to justify a rally. That is a legitimate question and it produced accurate reporting. It also produced a blind spot, because a revenue share has two sides and only one of them was ever examined.

The side nobody covered is the one with the public company, the regulatory filings, the customer assets, and the board. Robinhood’s chain is now a material piece of its strategic story, its stock trades on the strength of that story, and the chain’s economics include a permanent obligation to an entity that no securities analyst covering the stock has any reason to have heard of. That gap between how crypto covers a deal and how equity markets would cover the same deal is where most of the useful analysis in this sector currently sits, and it is worth reading every ecosystem announcement with the question of who else is party to it. The same platform-ownership pattern is also visible in the same playbook in prediction markets, where distribution, licensing, and customer ownership intersect.

Frequently asked questions

What is the Arbitrum Expansion Program?

An arrangement under which any Layer 2 or Layer 3 chain built with Arbitrum’s Orbit technology stack, and settling outside Arbitrum One or Nova, routes 10% of its net protocol revenue back to the Arbitrum ecosystem. Of that, 8% goes to the Arbitrum DAO treasury controlled by ARB tokenholders, and 2% funds the Arbitrum Developer Guild.

How much has Robinhood Chain actually paid?

Roughly $200,000, against more than $2 million in cumulative chain revenue since the July 1 launch, which confirms the 10% rate operating in practice. Arbitrum separately reported the network earning over $800,000 in a single seven-day period, annualizing near $42 million, though those figures are suppressed by an ongoing gas subsidy.

Is the 10% calculated on gross or net revenue?

Net, after network operating costs, which ties the payment to a chain’s actual profitability rather than to transaction volume. The revenue base is sequencer profits, and if the chain adopts Arbitrum’s Timeboost mechanism for capturing value from transaction ordering, those revenues may fall under the arrangement as well.

Why did Robinhood not just build its own chain from scratch?

Time, risk, and ecosystem. Building independently means owning all the revenue and also owning the security, auditing, and defence of a settlement layer holding customer-adjacent assets, with no existing tooling, bridges, or wallet support. Orbit delivered a branded, controlled chain with 100-millisecond block times and technical support from Offchain Labs, live within a week, at the cost of a tenth of net revenue.

Does the payment matter financially to Robinhood?

Not currently. At present run rates the Arbitrum share is roughly $4 million a year against quarterly company revenue near $1.27 billion. The chain itself contributes a low single-digit share of annual revenue at best. The arrangement matters structurally rather than financially, because it defines what the chain is and who it depends on.

What is unusual about paying a DAO?

The counterparty structure. The 8% flowing to the Arbitrum DAO treasury is controlled by token holders voting through governance, and those same holders influence the roadmap of the technology stack Robinhood’s chain runs on. A federally regulated public company holding a revenue-sharing obligation to, and infrastructure dependency on, a decentralized organization is a novel arrangement with unsettled disclosure and risk-management questions.

Does this give Robinhood any advantage over competitors?

Not through the arrangement itself, which is available to anyone on identical terms. Any brokerage can build an Orbit chain and pay the same 10%. Robinhood’s advantages, if they hold, come from distribution and from operating the venue where its own products trade, and the tokenized-equity market is already attracting incumbent exchanges building comparable infrastructure.

What should investors watch?

The first unsubsidized quarter after the gas subsidy expires around October, whether Timeboost is adopted and MEV revenue enters the sharing arrangement, how the chain’s economics and the Arbitrum obligation appear in regulatory filings, and any governance proposal to change the Expansion Program’s rates. This is educational analysis, not investment advice.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Revenue figures reflect third-party trackers and company statements available at the time of writing and are subject to revision, and chain activity is currently affected by a temporary fee subsidy. Nothing here is a recommendation to buy, sell, or hold any security or asset. Always do your own research. Information is accurate as of July 29, 2026.

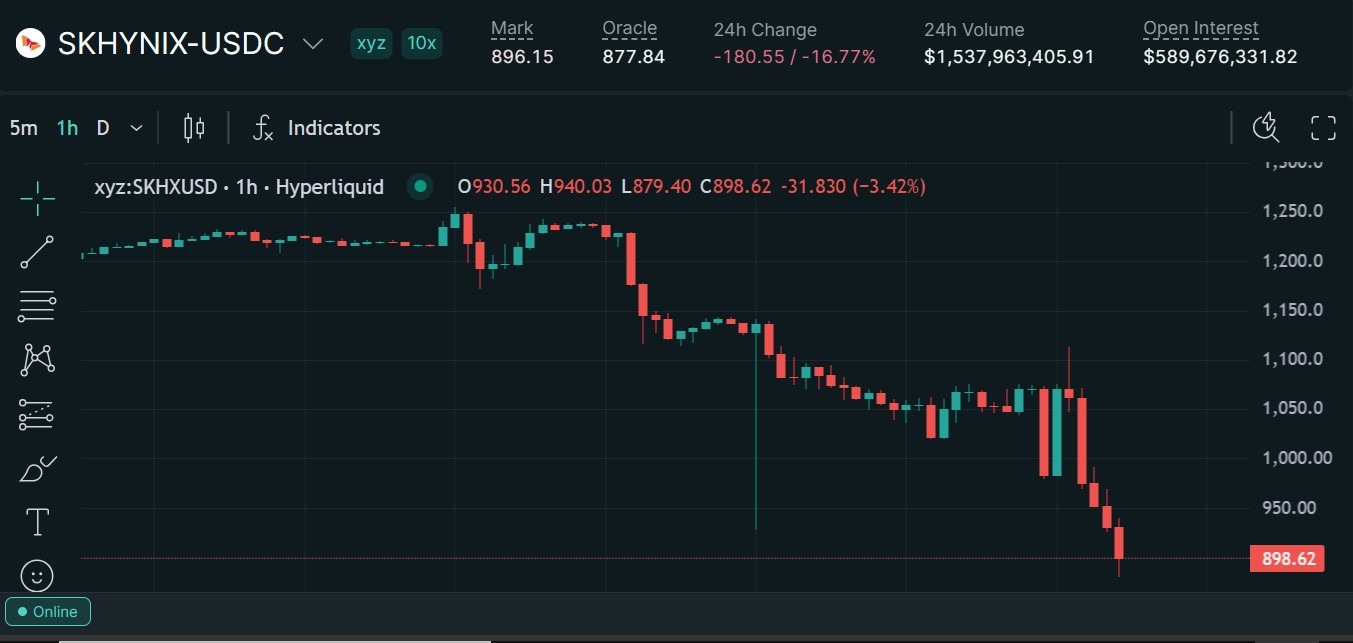

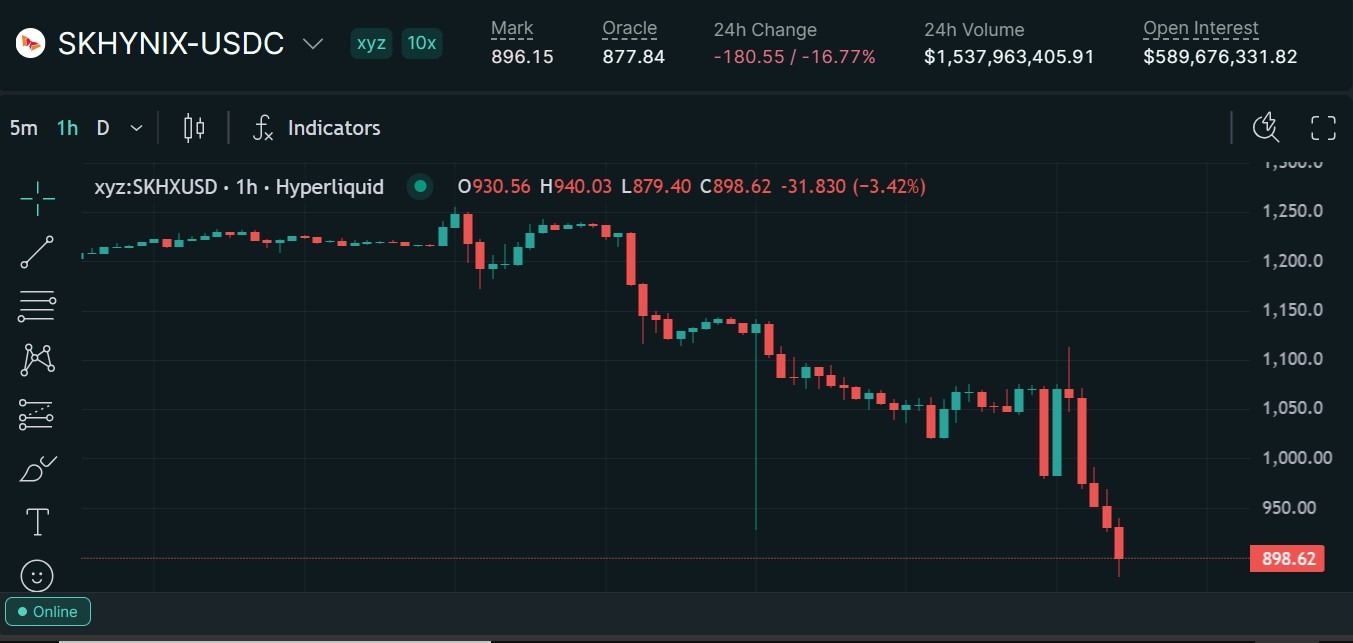

Trade.xyz, an operator of onchain perpetual markets on Hyperliquid, said it will cover eligible liquidation losses after a price anomaly hit its contract tracking SK Hynix, a South Korean chipmaker and producer of high-bandwidth memory for artificial intelligence.

Trade.xyz said the SKHYNIX contract’s mark price fell from $1,127.90 to $917.25 at 23:01 UTC on Monday after an executed trade was relayed by multiple independent data providers. Eligibility requirements will be announced soon, with distributions expected in the coming days.

The SK Hynix contract ranks among Hyperliquid’s most active markets. On Wednesday, Hyperliquid data showed the contract had generated over $1.5 billion in 24-hour volume and held nearly $600 million in open interest at the time of writing.

Trade.xyz said its oracle was tracking the external venue used as the primary South Korean pre-market and had “worked as intended according to its specification.” It acknowledged traders’ frustration and described the reimbursement as a “one-time discretionary decision,” adding that it would review how prices are formed during extreme market events.

The platform did not disclose how many traders would qualify for reimbursement or the total amount it expects to distribute.

SK Hynix trading chart. Source: Hyperliquid

How the anomaly reached the perpetual market

Trade.xyz said the sharp move originated from an executed transaction on an external market rather than its own order book. Its SK Hynix oracle tracks the US dollar value of one SKHX common share by converting the underlying Korean won price using the prevailing exchange rate, according to its documentation.

The external print fed into the oracle and contributed to the contract’s mark-price move. Hyperliquid uses the mark price to value positions for margin purposes and determine when leveraged positions should be liquidated.

The platform said it is considering giving more weight to prices formed on its own order books, which it said now provide meaningful liquidity and market signals.

Related: Onchain commodity trading is here to stay, but liquidity remains an issue

Trade.xyz operates under Hyperliquid’s HIP-3 framework, which allows builders to launch perpetual contracts tied to assets with external price feeds.

The platform accounted for more than $22 billion of HIP-3’s first $25 billion in cumulative volume and later launched an officially licensed S&P 500 perpetual using S&P Dow Jones Indices data.

Magazine: How Hong Kong is turning tokenized bonds into real market infrastructure

Gabriel Perez, who was accused of profiting from Kalshi bets tied to President Donald Trump’s speeches, is no longer employed by the federal government.

Trade.xyz said it will cover liquidation losses linked to the sudden collapse of its SK Hynix perpetual contract on July 27, following an incident that affected nearly 1,000 leveraged positions on Hyperliquid.

Recall that the other day, the mark price for the stock dropped from $1,127.90 to $917.25. The move triggered a massive liquidation cascade, which caused about $57 million in liquidations with about $17.3 million in realized losses, according to preliminary analysis.

The team behind the Hyperliquid HIP-3 operator said the price originated from an executed transaction carried by several independent data providers. Its oracle was tracking an external venue responsible for the trade, which the platform described as the main Korean pre-market venue.

According to them, the oracle operated according to its existing specifications. However, the resulting mark price caused liquidations before the underlying market recovered from the isolated print.

On July 27 at 23:01 UTC, SKHYNIX mark price dropped from $1,127.9 to $917.25. This print was based on an executed trade which was relayed by multiple independent data providers. The XYZ oracle was live in external pricing and tracking that venue, which serves as the primary…

— trade.xyz (@tradexyz) July 29, 2026

Trade.xyz outlined that they will reimburse liquidation losses attributable to the anomaly. The platform will announce eligibility requirements soon and expects to complete distributions within the coming days.

The company also described the compensation as a one-time discretionary measure. It stressed that the decision does not guarantee reimbursements following similar incidents in the future.

The announcement also addressed the immediate financial impact on traders but doesn’t change how leveraged positions were automatically closed when the oracle price fell.

In addition, the firm also plans to strengthen its pricing systems against similar tail events. The review will scope the platform’s reliance on external venues and the assumptions used when constructing mark prices.

The team said they will also consider giving more weight to activity on its own order books.

The post Trade.xyz Will Cover Losses From SK Hynix Liquidation Anomaly on Hyperliquid appeared first on CryptoPotato.

Trade.xyz, the operator behind onchain perpetual markets on Hyperliquid, says it will reimburse eligible liquidation losses after an abrupt price move affected its Hyperliquid-traded SK Hynix (SKHYNIX) contract. In a post on X, the platform linked the incident to an external market trade that its oracle incorporated into the contract’s mark price, triggering liquidation mechanics.

According to Trade.xyz, the SKHYNIX mark price dropped from $1,127.90 to $917.25 at 23:01 UTC on Monday after a trade on a separate venue was relayed through multiple independent data providers. The operator said it will announce eligibility criteria soon, with reimbursement expected over the following days.

Key takeaways

- Trade.xyz plans to cover liquidation losses tied to an SKHYNIX mark-price dislocation on Hyperliquid.

- Trade.xyz attributes the move to an external market print that flowed into its oracle, not to changes in its own order book.

- The affected contract is a high-activity Hyperliquid market, with $1.5B+ in 24-hour volume and about $600M open interest shown by Hyperliquid data.

- Reimbursement is described as a one-time discretionary decision, with eligibility and total amounts yet to be disclosed.

- Trade.xyz is reviewing how it forms prices during extreme events, including whether to weight its own order-book liquidity more heavily.

What happened to the SKHYNIX contract

Trade.xyz said the incident began with an executed transaction on an external market rather than activity directly in Hyperliquid’s SKHYNIX order book. The platform’s oracle tracks the US dollar value of one SKHX common share by translating the underlying Korean won price into USD using the prevailing exchange rate, based on its published documentation.

In this case, Trade.xyz said the oracle received the external print and that the mark price moved sharply as a result. On Hyperliquid, the mark price is used for margin valuation and for determining when leveraged positions should be liquidated—meaning sudden oracle-driven shifts can quickly cascade into liquidation outcomes for traders holding risk on the contract.

Trade.xyz did not specify how many traders will qualify, nor did it disclose the total amount it expects to distribute. It said the market will be eligible only under criteria to be released soon.

Why Hyperliquid mark pricing matters for liquidations

Hyperliquid’s design relies on mark prices to keep leverage risk measurable and liquidation thresholds predictable. While that approach can work smoothly during normal market conditions, it can be exposed to abrupt external price dislocations—especially when oracles pull in values that may not immediately reflect the trading dynamics on the contract’s own venue.

Trade.xyz acknowledged trader frustration and framed its response as a “one-time discretionary decision” to cover eligible liquidation losses. At the same time, it said the oracle “worked as intended according to its specification,” emphasizing that the system performed the task it was built to do—incorporating the external venue pricing feed and converting it via the exchange rate.

Looking ahead, Trade.xyz said it will review how prices are formed during extreme market events. The operator also indicated it is considering adding more weight to prices formed on its own order books, saying those order books now provide meaningful liquidity and market signals.

Scale of exposure: a top Hyperliquid market

The SKHYNIX contract is among the most actively traded offerings on Hyperliquid. Hyperliquid data shared by the platform showed that the contract had produced more than $1.5 billion in 24-hour volume and held nearly $600 million in open interest at the time of writing (Wednesday).

That level of activity matters because it increases the number of traders potentially affected when margin and liquidation thresholds change quickly. It also raises the stakes for oracle and mark-price methodology: even when a disagreement is rooted in external venue pricing, the on-chain mechanics that rely on mark prices can convert the move into immediate forced position closures.

Trade.xyz’s reimbursement plan is therefore aimed at mitigating the downstream consequence of the mark-price shift rather than disputing the oracle’s intended behavior.

Where the price feed fits in Hyperliquid’s ecosystem

Trade.xyz operates under Hyperliquid’s HIP-3 framework, which allows builders to launch perpetual contracts tied to assets using external price feeds. In other words, the contract’s mark price doesn’t come purely from the local order book—it can be driven by an external reference intended to reflect the underlying asset’s value.

Trade.xyz has also been active within the HIP-3 launch phase: Cointelegraph previously reported that the firm accounted for more than $22 billion of HIP-3’s first $25 billion in cumulative volume. It later launched an officially licensed S&P 500 perpetual using S&P Dow Jones Indices data, according to earlier coverage.

In practical terms, the SKHYNIX episode highlights a core tension in this model. External feeds can help anchor derivatives to real-world reference prices, but they can also import sudden prints that may not line up with the contract’s own trading behavior at the moment the print lands.

Trade.xyz’s comments suggest it recognizes that mismatch and is open to adjusting weighting—potentially blending external feed inputs with the signals derived from the order book where liquidity is now deeper than it may have been earlier in the platform’s growth.

Traders watching Hyperliquid next should focus on when Trade.xyz publishes eligibility criteria and how it decides what counts as “eligible liquidation losses.” They should also watch for any technical or policy changes around mark-price formation in extreme events, particularly whether the platform moves toward a higher reliance on local order-book pricing during volatile or anomalous periods.

Binance will open trading for 10 new bStocks tokenized stock pairs today. The batch adds Apple, Amazon, Goldman Sachs, and PayPal.

The exchange launched bStocks in June with several listings, including Circle Internet Group, NVIDIA, and Tesla. Since then, it has continued to add pairs in batches.

Follow us on X to get the latest news as it happens

Binance Keeps Expanding Its Tokenized Stock Shelf

bStocks are tokenized securities issued by a Binance affiliate, BTech Holdings Limited. They are certificates that track the performance of underlying stocks rather than representing direct share ownership.

Each token is fully backed by a corresponding US share held by a regulated custodian, allowing holders to gain price exposure and economic benefits, including dividend reinvestment, without owning the stock itself.

The exchange has steadily expanded its bStocks offering throughout July, adding tokenized versions of companies including Coinbase, Alphabet, Robinhood, IBM, and Nokia.

Today, Binance announced that it will list 10 additional bStocks. The latest expansion adds Apple, Amazon, Applied Materials, Bloom Energy, Dell, Fluence Energy, Goldman Sachs, and PayPal, as well as two semiconductor ETFs.

Spot trading and Spot Algo Trading Bots will open at 12:00 UTC. All 10 pairs will be tradeable against Tether (USDT).

Within one hour of the Spot listing, users will also be able to trade tokenized stocks against Bitcoin (BTC) and other supported assets via Binance Convert, with zero conversion fees. Binance is also waiving maker fees on all bStocks trading pairs until August 31, 2026, at 23:59 UTC.

Users can already tokenize eligible stock holdings into bStocks on a one-to-one basis without conversion fees. Withdrawals for the newly listed assets will open at 13:00 UTC on July 29.

“bStocks are subject to liquidity risk, issuer risk, custody risk, broker risk, operational risk, technology risk, regulatory risk, tax risk, fees, withholding, transfer restrictions, and possible loss of the entire investment,” the announcement read.

Binance’s bStocks platform has seen rapid growth since its launch, with assets under management surpassing $100 million in just 15 days. The expansion also reflects the broader momentum behind tokenized equities, which are gaining traction across the tokenization market.

Among them, AI and semiconductor stocks have emerged as the fastest-growing segment, increasing their share of the tokenized stock market from 0.3% to 15.5% over the past year.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Binance Adds 10 More Tokenized Stocks to Its bStocks Lineup appeared first on BeInCrypto.

The Cerebras Systems and SpaceX listings follow a period of months where the volume of RWAs onchain has been steadily multiplying, and traditional financial press has been covering how crypto derivatives platforms now allow traders to price commodities outside of market hours — weekends, holidays, and the 4PM-to-9:30AM dead zone.

Solana already has the speed, throughput, and cost structure to support these markets. Solana handles more daily transactions than all other blockchains combined. There is no version of this argument where someone credibly claims Solana can’t support high-frequency global derivatives trading. It obviously can. The gap is execution and focus. Hyperliquid has taken an early lead, not because they had better infrastructure, but because they were built specifically for derivatives traders. They shipped a product that was purpose-built for a specific user, and that specific user showed up.

The reality is that markets form where products are usable, liquid, and trusted, and not necessarily where infrastructure is strongest. CoinMarketCap is a graveyard of projects that hung their hats solely on technical advantages. Solana, despite its advantages, is not the default venue for this category, and that gap has been compounding.

Liquidity begets liquidity. Traders go where other traders already are. Every week that passes without a competitive Solana-native answer to the Hyperliquid trading experience is a week where the gravitational pull of the alternative gets harder to reverse.

Russia’s FSB says Telegram founder Pavel Durov faces a terrorism-related charge and an international arrest warrant, while a separate French case remains open.

US spot Bitcoin ETFs recorded four straight sessions of outflows totaling $526 million as Bitcoin faced renewed selling pressure after failing to hold $65,000.

Crypto World

The Most Unpredictable FOMC Meeting in Years Is Here: What Bitcoin Investors Should Know

The United States Federal Reserve will announce its interest-rate decision later today, but, unlike essentially every meeting in the past six years, markets remain divided over what comes next.

Bitcoin investors seemingly de-risked yesterday in what appeared to be a blatant sell-off ahead of the key event. The question now is what follows.

Why So Much Unpredictability Now

The Federal Open Market Committee began its two-day meeting on July 28 and will publish its decision at 2:00 p.m. ET today. Chairman Kevin Warsh’s press conference will follow approximately 30 minutes later, in which investors will seek clues for what the central bank’s policy will be for the remainder of 2026.

The current benchmark rate stands between 3.50% and 3.75%. Although most experts still believe it will be left unchanged, futures markets recently assigned a probability of up to 38% to a surprise 25-basis-point hike. According to the analyst at the Kobeissi Letter, these expectations are among the most divided in recent history.

They explained that nearly every Fed meeting since the COVID-19 pandemic in March 2020 entered decision day with roughly 99% agreement about the outcome. The situation now is different for the first time in over six years, given the aforementioned odds on futures markets and prediction platforms.

The uncertainty partly stems from Warsh’s decision to reduce the central bank’s reliance on forward guidance. Minutes from the June meeting showed that policymakers discussed shortening the Fed’s statement and removing language indicating the likely direction of the next move. Warsh’s approach is expected to preserve flexibility, but it has also left traders without the clear policy signals they became accustomed to under Jerome Powell.

Change or No Change

The Kobeissi Letter analysts said they believe the Fed will leave rates unchanged. A recent Reuters survey of over 100 forecasters reached the same conclusion, with more than three-quarters predicting no policy shift until the end of the year. ING economists shared the same opinion.

One of the reasons for this is the softer-than-expected inflation data for June. The labor market has also shown signs of weakening, giving the Fed another reason not to tighten financial conditions further.

There’s also the opposite side of the coin, though, as some experts believe the central bank might lose credibility if it waits too long. Inflation remains well above the 2% target, while renewed geopolitical tension, tariffs, and energy-market instability could push prices higher again.

Several Fed officials have reportedly become more open to the idea of raising rates if inflation fails to improve. Warsh has also avoided giving markets a clear roadmap, meaning that a hike cannot be easily dismissed simply because officials did not prepare investors for one in advance.

Crypto Impact

Crypto analytics platform Santiment Intelligence outlined a notable rise in social-media discussions about the interest-rate hikes ahead of today’s meeting. The data showed a similar spike in such fears before the previous meeting on June 16. However, as it typically happens, the social chatter was wrong as the Fed left rates unchanged.

“Crowd conviction can get loud right before it gets wrong, especially when traders are trying to price Fed uncertainty into Bitcoin,” said Santiment.

Let’s talk prices. BTC dipped by $3,000 yesterday in a de-risking development ahead of the meeting. It has recovered half of the losses, currently sitting above $64,000.

If the Fed doesn’t change rates and Warsh doesn’t signal strongly for a September hike, BTC could rebound further as the uncertainty might have already been priced in. If there’s no rate change but the Chairman sounds hawkish, bitcoin might jump initially as there would be no hike now, but it’s likely to retreat toward $60,000 in the next few weeks.

A surprise 25-basis-point increase, though, will be the most bearish immediate outcome for the cryptocurrency. The decision will likely strengthen the dollar, push Treasury yields higher, and cause investors to further reduce exposure to speculative assets.

The post The Most Unpredictable FOMC Meeting in Years Is Here: What Bitcoin Investors Should Know appeared first on CryptoPotato.

Costa Coffee adds scones back to menu after 5 years away

Fresh Look Beauty Classes Helps You Build a Successful Beauty Career

Robinhood built its own chain. It still pays rent.

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Brooks Brothers

-

Sports3 days ago

Sports3 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Tech2 days ago

Tech2 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World6 days ago

Crypto World6 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics2 days ago

Politics2 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Sports5 days ago

Sports5 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Politics24 hours ago

Politics24 hours agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Fashion5 days ago

Fashion5 days ago16 Dresses for the High Summer Event

-

Entertainment5 days ago

Entertainment5 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos2 days ago

News Videos2 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

News Videos6 days ago

News Videos6 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Crypto World4 days ago

Crypto World4 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics3 days ago

Politics3 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Business4 hours ago

Business4 hours agoMajor shareholder moves on Canyon

-

Crypto World3 days ago

Crypto World3 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Crypto World6 days ago

Crypto World6 days agoUniswap (UNI) pushes deeper into tokenized RWAs with permissioned trading pools

-

Entertainment14 hours ago

Entertainment14 hours ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Tech4 days ago

Tech4 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

Crypto World6 days ago

SEC Agrees to Overhaul Recordkeeping After Settling Coinbase Lawsuit Over Gensler’s Lost Texts

-

Business5 days ago

Business5 days agoAlliance Entertainment Holding Corporation (AENT) Discusses Evolution Into Omnichannel Distribution and Fulfillment Platform for Media and Collectibles Transcript

You must be logged in to post a comment Login