Crypto World

Tesla (TSLA) Secures UK Electricity Supply License to Power Homes and Businesses

Key Takeaways

- Ofgem has approved Tesla Energy Ventures’ application for a UK electricity supply license, now in effect.

- The licensing procedure spanned from July 2025 through March 2026 before final authorization.

- Tesla is now authorized to retail electricity to residential and commercial properties throughout Great Britain.

- The company enters competition with major British energy providers including Octopus Energy, British Gas, and EDF.

- A different Tesla entity, Tesla Motors Limited, previously obtained an electricity generation license in the UK.

Tesla Energy Ventures Limited has received authorization from Ofgem to retail electricity throughout Great Britain. The regulatory approval became effective Wednesday following a review process that commenced in July 2025.

The authorization encompasses both residential and commercial customer segments, enabling Tesla to distribute electricity directly to British households and enterprises.

This positions Tesla as a new competitor against Britain’s established energy retailers, including Octopus Energy, British Gas, and EDF.

Tesla has existing operations within the UK energy sector. Through Tesla Motors Limited, the company maintains an electricity generation license, and customers with Powerwall batteries can already monetize surplus solar generation through grid feed-in.

The newly granted supply license represents a logical progression — enabling Tesla to manage the entire cycle and distribute electricity directly as a retail provider.

Market Entry During Price Volatility

The authorization arrives during a challenging period for British consumers. Energy costs across Britain have increased following conflict in Iran, creating widespread concern about escalating utility expenses.

Most British households currently enjoy temporary protection from volatile gas prices through July under regulated pricing structures. However, this safeguard is temporary.

Tesla’s entrance into the market provides consumers with an additional choice among retail energy providers, although competitive pricing details have not been disclosed.

The automaker brings international energy market experience. Tesla Energy currently maintains operations in Australian and American energy markets.

Tesla’s British Market Standing

Tesla’s automotive sales in the UK have faced headwinds. Vehicle deliveries declined 8.9% year-over-year during 2025, impacted by competitive pressure from budget-friendly Chinese electric vehicle manufacturers.

Additionally, some markets have experienced consumer resistance connected to Elon Musk’s involvement in political discourse.

The energy sector provides Tesla an alternative growth channel in Britain — one independent of automotive performance.

Tesla has yet to reveal pricing structures, rate plans, or an official launch timeline for its electricity retail services in Great Britain.

Ofgem confirmed the license approval through an official regulatory announcement released this week.

Crypto World

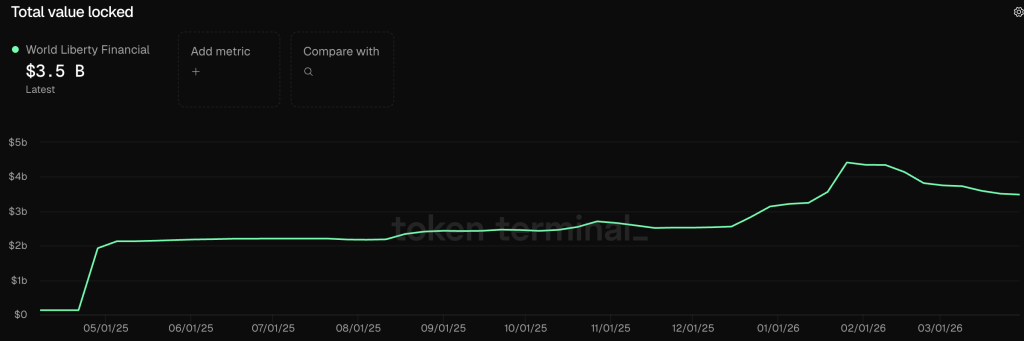

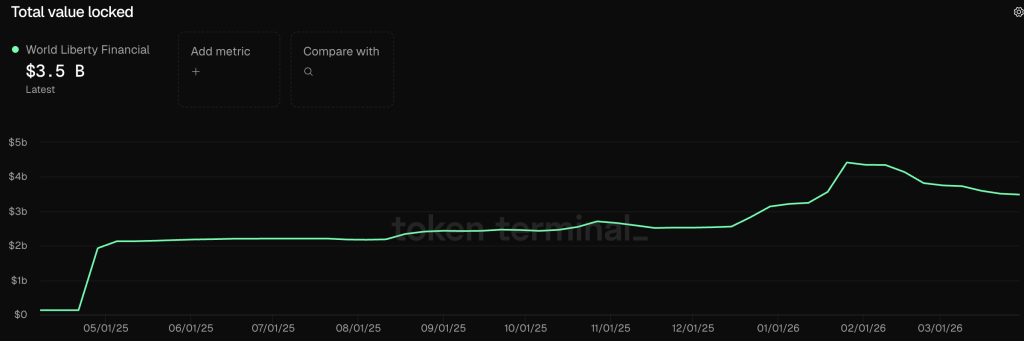

World Liberty Financial Under Ethics Fire: Can WLFI Crypto Survive Corruption Allegations?

World Liberty Financial (WLFI) crypto is structured to funnel 75% of net revenues to DT Marks DEFI LLC, a Delaware entity tied directly to Donald Trump and his family, while insulating them from any legal or financial liability for the project’s operations.

House Democrats published a staff report on November 24 describing WLFI as the centerpiece of what it calls presidential self-dealing on an unprecedented scale, with Representative Jamie Raskin stating that Trump has “turned the Oval Office into the world’s most corrupt crypto startup operation.”

The conflict-of-interest mechanism is direct and unambiguous. Donald Trump simultaneously controls crypto policy from the White House and holds a dominant financial stake in a DeFi project whose commercial value depends on the regulatory environment he shapes. That is not a perception problem – it is a structural one.

Discover: Best Crypto to Diversify Your Portfolio

Key Takeaways:

- Revenue structure: 75% of WLFI net revenues flow to DT Marks DEFI LLC, a Trump family-linked entity, with no personal liability attached.

- Scale of extraction: The Trump family has collected at least $890 million in revenues and holds WLF tokens valued at $3.8 billion, with no evidence of personal capital investment.

- Foreign money: Justin Sun invested $75 million in WLFI tokens before his SEC fraud case was dropped; UAE-based Aqua 1 Foundation wired $100 million in stablecoins with unclear origins.

- Token performance: WLFI tokens are down 50% from all-time highs; Trump and Melania memecoins have collapsed 91% and 99% respectively.

- Banking expansion: On January 9, 2026, WLFI applied to the OCC for a national trust bank charter under World Liberty Trust Company, with Zach Witkoff listed as proposed president.

- Political exposure: House Democrats’ Anti-Crypto Corruption Week scrutiny is escalating, with the November 24 report naming obstruction of justice, foreign influence, and self-dealing as core allegations.

What WLFI’s Revenue Structure Actually Means – and Why Ethics Experts Are Alarmed

The mechanics of World Liberty Financial’s compensation structure are what drive the ethics concerns, not the politics surrounding them.

Under the project’s Gold Paper, DT Marks DEFI LLC – the Trump family’s designated revenue vehicle – receives 75% of net revenues generated by the DeFi platform, while the legal wrapper around that entity specifically protects the Trump family from operational liability. The distinction matters because it creates a one-way financial relationship: profit flows to the Trumps, risk does not.

Citizens for Responsibility and Ethics in Washington (CREW) and other watchdog organizations have flagged this arrangement as without precedent in the relationship between a sitting president and an active commercial enterprise.

The Trump family has extracted at least $890 million in revenues from WLFI while holding tokens currently valued at approximately $3.8 billion – with no documented personal capital investment at inception. That is not a founder’s equity stake built through risk-taking. It is a revenue claim backed by name recognition and political positioning.

The foreign investment dimension compounds the structural problem significantly. Justin Sun, charged by the SEC for fraud and market manipulation, invested $75 million in WLFI tokens. His multibillion-dollar SEC case was subsequently dropped.

The UAE-based Aqua 1 Foundation, linked by analysts to entities with ties to China’s state-owned CNPC, wired $100 million in stablecoins to the project in summer 2025 – with Reuters reporting that the origins and expectations attached to that transfer remain opaque. A 60 Minutes report on November 17, 2025 further connected a $2 billion Binance-MGX deal settled in WLFI’s USD1 stablecoin to Binance founder Changpeng Zhao’s Trump pardon.

Crypto insiders have described WLFI as a mechanism for global influence-buying dressed as a DeFi project. Some institutional players, approached with what sources describe as “mutual investment” pitches, declined after concluding the arrangement crossed ethical lines.

The absence of institutional whales in WLFI’s order books – with retail participants dominating token purchases – suggests sophisticated capital has reached a similar conclusion.

Discover: The Best Crypto to Buy Right Now

Can a President Profit From Crypto Policy? The Conflict WLFI Can’t Shake

Trump’s administration has moved aggressively on crypto-friendly policy reform since January 2025, and each legislative win that benefits the broader industry also directly benefits World Liberty Financial.

The GENIUS Act, which Trump endorsed to establish a stablecoin regulatory framework, creates legitimacy infrastructure for USD1 – WLFI’s own stablecoin – at exactly the moment the project needed it.

The FIT21 regulatory framework, which restructures SEC and CFTC jurisdiction over crypto assets, would materially ease the compliance burden on DeFi platforms like WLFI.

The SEC’s dramatically softened enforcement posture under the Trump administration is not a coincidence critics are willing to overlook, particularly given the Sun case. A president whose family holds $3.8 billion in tokens tied to a DeFi project has quantifiable financial incentives to reduce regulatory friction on DeFi.

The White House maintains that Trump’s assets are held in a trust managed by his children and that no conflicts exist. That framing is deliberate: a trust managed by the president’s children, in a project co-founded by those same children, is not a meaningful separation under any conventional ethics standard.

The evolving legal frameworks for DeFi entities make WLFI’s structural opacity harder to dismiss as a technicality. WLFI’s January 2026 OCC application for a national trust bank charter – listing Zach Witkoff as proposed president – would, if approved, extend the project’s reach into federally regulated banking infrastructure. The political and financial interests at stake are not abstract. They are denominated in billions and written into legislation.

Discover: The Best Crypto Presales Live Right Now

The post World Liberty Financial Under Ethics Fire: Can WLFI Crypto Survive Corruption Allegations? appeared first on Cryptonews.

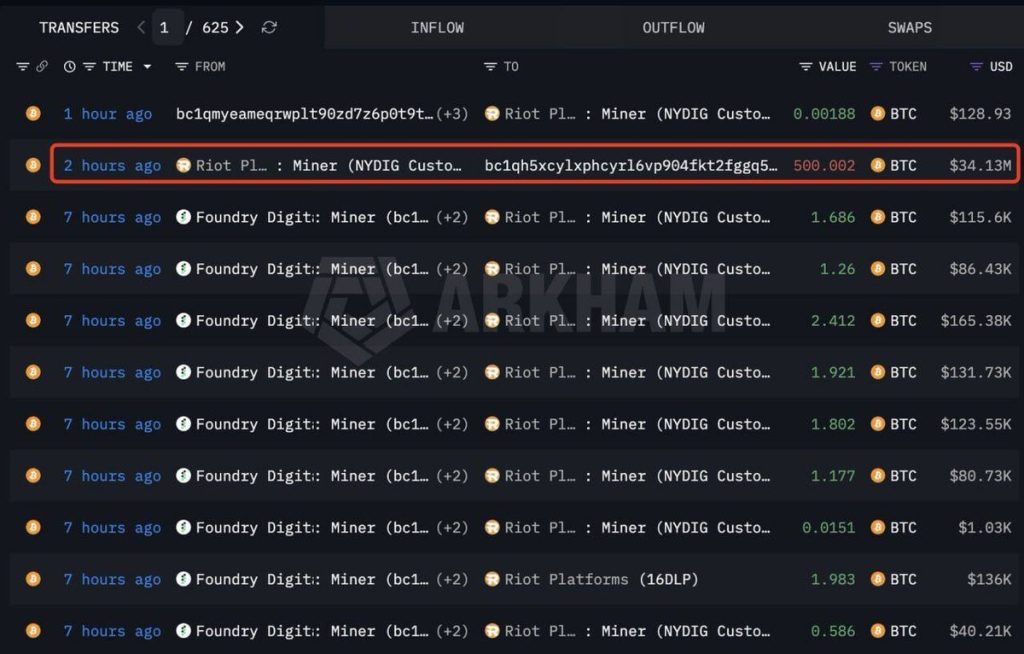

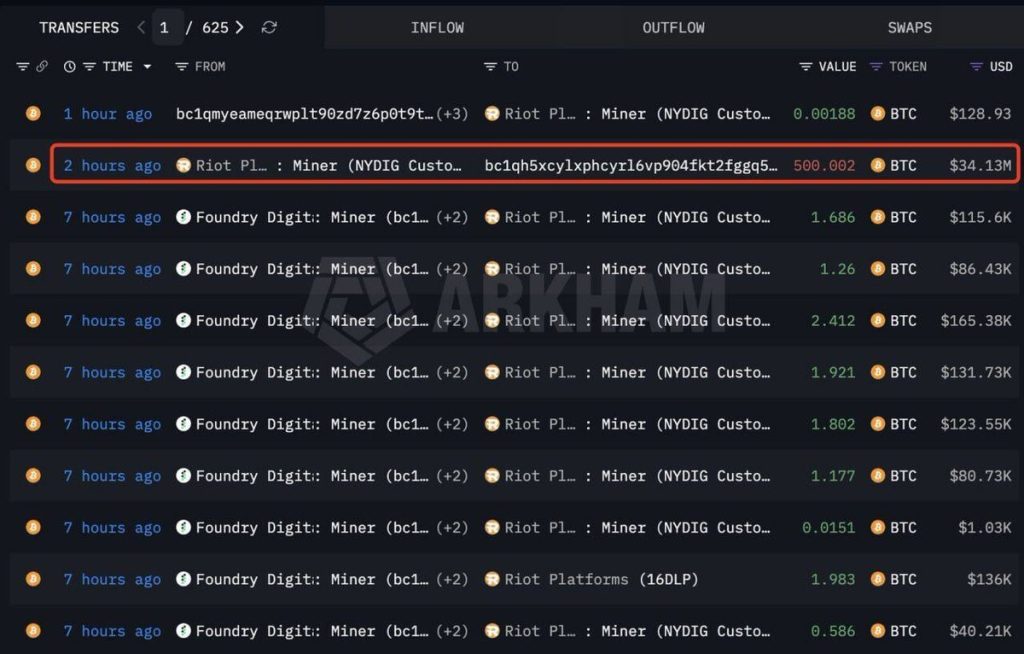

Riot Platforms sold 3,778 Bitcoin in Q1 2026, netting $289.5 million-a volume that dwarfs its 1,473 BTC production for the same period by 2.6x.

The company ended Q1 with 15,680 BTC on its books, down 18% from the 18,005 coins it held at the close of 2025. That gap between what Riot mined and what it sold is the number that demands explanation.

Blockchain intelligence platform Arkham flagged a separate 500 BTC outflow from a wallet attributed to Riot on Thursday, suggesting the selling didn’t stop when Q1 closed.

The company is also pushing deeper into high-performance computing colocation, shifting its business model beyond pure mining toward infrastructure hosting-a pivot that requires capital, which partially explains the aggressive liquidation pace.

Energy costs are the other half of the story. Kadan Stadelmann, blockchain developer and co-founder of AI company Compance, said miners are selling because rising energy costs-worsened by the escalating Middle East conflict since February-are compressing margins across the industry.

“This leads to a fall in hashrate and difficulty in Bitcoin mining. This makes it easier and more profitable to mine Bitcoins for those miners who remain online,” Stadelmann said, predicting further capitulation from less efficient operators.

- Sales volume: Riot sold 3,778 BTC in Q1 2026, generating $289.5 million against quarterly production of just 1,473 BTC.

- Treasury drawdown: BTC holdings fell 18% quarter-over-quarter, from 18,005 to 15,680 BTC.

- Power cost improvement: All-in power cost dropped 21% year-over-year to 3.0¢/kWh, even as selling accelerated.

- Hash rate expansion: Deployed hash rate grew 26% to 42.5 EH/s, signaling infrastructure reinvestment over accumulation.

- Power credits: Riot generated $21.0 million in power credits during Q1-more than double the prior year period.

- Industry-wide selling: MARA Holdings, Genius Group, and Nakamoto Holdings sold a combined 15,501 BTC in the last week alone.

Discover: The Best Crypto to Get Right Now

Selling Above Production Rate – Operational Pivot or Distress Signal?

Selling 2.6x your quarterly production isn’t treasury management in the traditional sense-it’s a structural drawdown.

That matters because it signals Riot isn’t just covering operating costs; it’s funding something larger, whether that’s hash rate expansion, colocation infrastructure buildout, or balance sheet repair ahead of continued Bitcoin price pressure.

The operational data cuts against a pure distress read, though. Riot improved its all-in power cost 21% year-over-year to 3.0¢/kWh and grew deployed hash rate 26% to 42.5 EH/s. It also generated $21.0 million in power credits during Q1-more than double the year-ago period-by leveraging renewable energy agreements and grid services.

That’s not the profile of a miner bleeding out; it’s a miner reallocating capital aggressively into infrastructure while conditions remain volatile.

Riot isn’t alone. MARA Holdings, Genius Group, and Nakamoto Holdings sold a combined 15,501 BTC in the past week.

Genius Group went further-liquidating its entire Bitcoin stash. The industry is clearly in a rotation away from passive accumulation toward active treasury management, a departure from the hodl-first playbook that defined miner strategy through the 2021 bull cycle. If Bitcoin prices don’t recover in Q2, watch for Riot’s treasury to test the 14,000 BTC level within two quarters at the current drawdown rate.

Discover: The Best Crypto Presales Live Right Now

Miner Selling and BTC Supply Pressure: How Much Does It Move the Market?

Bitcoin mining difficulty dropped from approximately 145 trillion to 133 trillion on March 20-a 7.7% decline-while network hash rate fell from 1,160 exahash to roughly 990 exahash as of Friday.

Weaker miners are going offline, exactly as Stadelmann predicted, which structurally benefits survivors like Riot with lower difficulty and higher per-block rewards.

The supply side picture is more complicated when viewed against demand. Bitcoin ETFs snapped a four-month outflow streak with $1.32 billion in March inflows, meaning institutional demand is partially absorbing the miner supply hitting the market.

Riot alone doesn’t move BTC price-but Riot plus MARA plus Genius Group plus Nakamoto in the same week represents a coordinated pressure event that on-chain miner outflow metrics will reflect clearly.

The invalidation condition here is simple: if BTC reclaims and holds above $90,000 in Q2, Riot’s treasury logic flips from defensive liquidation to premature selling at cycle lows. Until that happens, the selling looks rational given the broader market pressure on holders and the rising cost environment compounding miner margin squeeze globally.

Explore: The best pre-launch token sales with asymmetric upside potential

The post Riot Platforms Sells 3,778 Bitcoin in Q1 as Miner Strategy Shifts appeared first on Cryptonews.

The U.S. employment market rebounded in a big way from February’s sizable losses.

According to a Friday morning release from the Bureau of Labor Statistics, the country added 178,000 jobs in March, after losing 133,000 positions the previous month. Economist forecasts had been for 60,000 jobs to have been added.

The unemployment rate fell to 4.3% versus 4.4% in February and expectations for 4.4%.

At least part of the beat was due to a sizable downward revision in the February data from an originally reported decline of 92,000.

Trading quietly near the $67,000 level in the hours ahead of the data, bitcoin remained there in the minutes just following the report.

Expectations about the future course of interest rates, of late, have been far more influenced by events in the Middle East and the price of crude oil than by the outlook for domestic economic growth.

As recently as last week, oil’s surging price had markets forecasting imminent rate hikes by the U.S. Federal Reserve. Speaking earlier this week, though, Fed Chairman Jerome Powell said the central bank recognized that oil price shocks — while initially making headline inflation numbers look worse — can depress economic activity. He indicated the Fed would be in no hurry to raise rates in response to short-term moves in the price of crude.

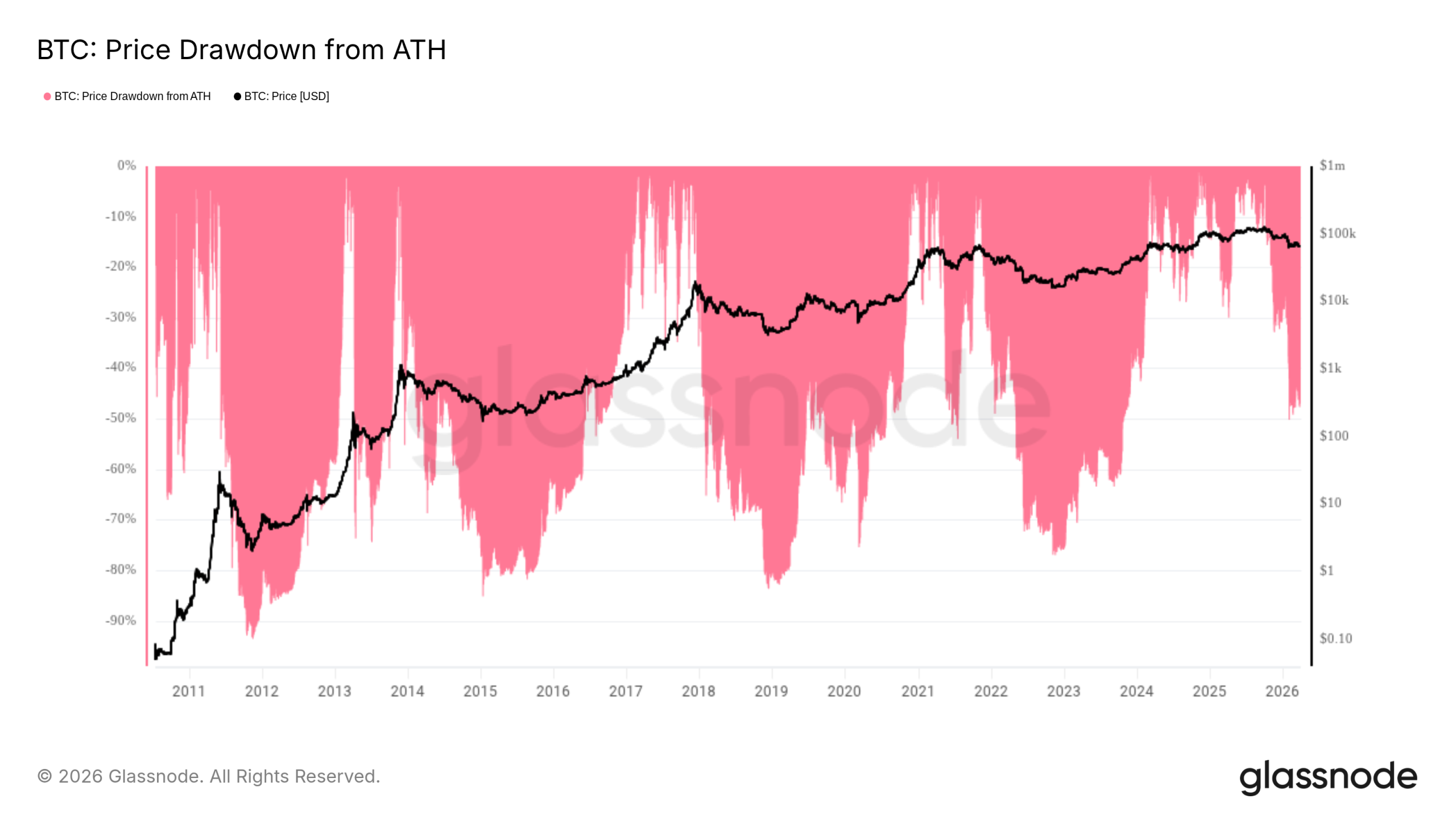

Bitcoin’s drawdown narrative is shifting from a pattern of extreme collapses to a more mature market dynamic, according to Cathie Wood, the founder and CEO of ARK Invest. In a CNBC appearance on Squawk Box dated April 1, Wood argued that the era of 85% or greater corrections may be behind BTC, framing the asset as a proven technology and monetary tool rather than a volatile tech experiment.

Speaking amid a price backdrop around the 69,000 level—the prior all-time high reached in 2021—Wood’s remarks come after a long bear market that wiped out roughly 80% of BTC’s value before a bottom near 15,600. On-chain data, however, suggest the current downturn has not yet mirrored the depth seen in prior cycles. Glassnode data indicate the bear market’s maximum drawdown from BTC’s peak remains well short of past extremes, around 52% from the record high of about 126,200 in October 2025.

Key takeaways

- ARK Invest’s Cathie Wood argues Bitcoin is past the era of 85%+ price collapses, framing BTC as a proven technology and monetary asset rather than a speculative fad.

- Analysts disagree on the next significant price level: a chartist forecast points to roughly $34,000 as a bottom (a 72% drawdown), while consensus from broader coverage points to a range of roughly $40,000 to $50,000.

- On-chain data show the bear market depth to date is shallower than in some previous cycles, with maximum drawdown around 52% from the all-time high, suggesting a potentially different extinction-like pattern for BTC.

- April seasonality and near-term momentum remain in focus: some analysts see historical patterns of spring recoveries during bear phases, while macro headlines and liquidity conditions continue to influence the path forward.

Wood’s view: BTC’s maturation and the new normal

Wood’s comments came during a dialogue about Bitcoin’s long-run narrative. She stressed that the 85–95% declines associated with earlier, less mature markets are unlikely to recur for Bitcoin, a narrative she frames as evidence of BTC’s transformation into a validated monetary system and a new asset class. The remarks echo her longstanding bullish stance on Bitcoin, which has been a hallmark of ARK’s research orientation toward disruptive technologies.

At the time of her appearance, Bitcoin was hovering near the post-2021 high watermark—an area that previously marked the transition into a multi-quarter bear cycle. Wood’s perspective contrasts with the more cautious or range-bound themes that have dominated much of the current trading backdrop, where macro conditions, policy signals, and sector rotation often determine day-to-day moves.

That said, Wood’s optimism sits alongside a chorus of caution from other analysts who note that the road ahead remains data-driven and uncertain—a reminder that even as BTC stabilizes, macro headwinds can quickly reassert themselves.

Forecasts diverge on the floor of the bear market

While Wood’s stance centers on BTC’s maturation, other voices point to specific downside scenarios. Tony Severino, a veteran market technician, floated a bottom near $34,000, implying a 72% drawdown from the peak. He summarized the trajectory in a post on X, suggesting that a decline to that level would mark a “max drawdown” consistent with a new phase for the asset.

Beyond Severino’s projection, broader market commentary remains split. A section of traders and analysts continues to anticipate a bottom in the higher $40,000s to low $50,000s, a range that Cointelegraph has cited in prior coverage as a common region for a generational floor rather than a catastrophic collapse. For some observers, the 40k–50k zone remains the anchor for a long-term re-rating of Bitcoin’s risk profile.

Meanwhile, Bloomberg Intelligence analyst Mike McGlone has warned that prices could be trending toward seven-year lows, underscoring the risk that macro developments—such as central-bank policy and global liquidity—could extend the bear phase even as on-chain metrics offer a more nuanced view of drawdown depth.

Seasonality, on-chain signals, and what to watch next

Seasonality has long been cited as a potential internal driver of Bitcoin’s price path. Timothy Peterson, a network economist and commentator, highlighted a pattern in which April historically functions as a turning point during bearish cycles. A chart he shared on X illustrates April as a potential inflection month in past bear phases, though whether that dynamic repeats remains contingent on broader market conditions.

March’s monthly close added a modest, 1.8% gain for BTC/USD, effectively ending a five-month losing streak. The move, while not dramatic, keeps the door open for a spring rebound, provided macro momentum aligns with technical and on-chain signals.

On-chain context adds another layer to the discussion. Glassnode’s analysis shows that the current bear market’s depth—though material—is not yet aligned with the most severe declines observed historically. The all-time high of roughly 126,200 in October 2025 has given way to a drawdown of about 52%, a figure that suggests the market could behave differently than in previous cycles if macro conditions stay supportive or liquidity improves.

For investors, this combination of on-chain resilience and mixed macro signals creates a nuanced backdrop. A Bitcoin trading environment shaped by a less severe drawdown yet ongoing external headwinds could translate into a more protracted consolidation rather than a sharp capitulation or a swift breakout. Observers will be watching for signs of sustained demand, improving liquidity in risk markets, and any shifts in policy that could alter the risk-reward calculus for crypto exposure.

As the calendar turns to April, market participants will parse a mix of seasonality whispers, data-driven cautions, and evolving macro narratives. The next several weeks could prove decisive in whether BTC resumes a broader uptrend, remains range-bound, or teeters on renewed volatility as external conditions shift.

This article synthesizes observations from multiple sources, including Cathie Wood’s CNBC discussion, on-chain data from Glassnode, and commentary from market analysts such as Tony Severino and Mike McGlone, as well as prior coverage from Cointelegraph on price floors and seasonality in Bitcoin’s bear markets. Investors should treat forecasts as probabilistic scenarios rather than certainties and remain mindful of the evolving macro landscape that continues to shape crypto markets.

Cartesi token soared over 100% to a 3-month high of $0.049 on Friday. Will the Layer 2 token edge higher over the coming sessions, or will it succumb to profit-taking?

Summary

- Cartesi price surged over 100% to a three-month high amid a sharp rise in trading volume and a short squeeze.

- The rally was driven by progress toward L2BEAT Stage 2 status and growing developer activity around Cartesi Machine deployments.

- Technical indicators show overbought conditions and profit-taking signals, with CTSI price at risk of a pullback toward $0.030 support.

According to data from crypto.news, Cartesi (CTSI) price rallied nearly 110% to $0.049 on Friday, reaching its highest level since November 2022.

The rally came in a high-volume trading environment. In the past 24 hours, the daily trading volume of Cartesi rose 1,260%, suggesting a sharp rise in demand from traders that likely buoyed the token toward its highs today.

There are three main reasons why Cartesi price broke out today.

First, Cartesi’s Permissionless Refereed Tournament fraud-proof system is reportedly nearing the Stage 2 classification by L2BEAT. This milestone would rank it among the most secure and decentralized Layer 2 scaling solutions, setting it apart from competitors that still rely on permissioned validators.

Second, the project’s recent initiative to ship high-throughput applications reached critical implementation deadlines in April. Tangible developer interest in the Cartesi Machine, which allows decentralized apps to run on Linux, is finally translating from theoretical potential into live deployments.

Third, after months of trading in a narrow range of $0.02 to $0.025, the sudden break above long-term resistance triggered a volatility spike. This caused a short squeeze, forcing bearish traders to buy back their positions and further fueling the massive gains seen today.

On the daily chart, Cartesi price has broken out of a multi-month descending parallel channel pattern, a sign that bulls have finally gained control of the market. It has already attained the target level from the breakout, suggesting there could be some selloff on the horizon.

Such selloff risks also come as the relative strength index has crossed the overbought threshold. Crypto rallies often face some pullback when this metric hits an overbought state.

Additionally, the Chaikin Money Flow index showed a negative reading, a sign that investors have started to rotate capital or take profits at these higher levels.

Hence, the Cartesi token could likely retest its immediate support of $0.030 before its next leg higher.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Bitcoin (BTC) is “done” with drawdowns of 85% or more from all-time highs, says ARK Invest CEO, Cathie Wood.

Key points:

-

Bitcoin will not see another correction of 85% or more versus its latest all-time high, Cathie Wood argues.

-

A new prediction sees $34,000 becoming the next BTC price bottom.

-

Bitcoin bear-market seasonality hints that a reversal could come this month.

Wood on BTC price: No more 85% “collapses”

In an interview with CNBC’s Squawk Box segment on April 1, Wood stayed calm about double-digit BTC price losses.

“Believe it or not, in the Bitcoin community, down 50% — if that’s as far as it goes — they’ll consider that a real victory,” she said.

“Because you’re right; the 85-95% collapses associated with a very new technology — that’s done. This is a proven technology, it’s a proven monetary system and it’s a new asset class.”

Wood, a longtime Bitcoin bull, was speaking as Bitcoin circled its old $69,000 all-time highs from 2021.

Those preceded a year-long bear market in which BTC/USD lost nearly 80% before bottoming at $15,600. That marked the latest such correction, with bear markets typically bringing losses around the 80% mark.

Data from onchain analytics platform Glassnode shows that the current bear market has yet to match historical patterns with maximum downside versus Bitcoin’s $126,200 record from October 2025 at 52%.

Responding to Wood, analyst Tony Severino predicted that 2026 would bring a price bottom equal to a 72% drawdown.

“Correct, -72% max drawdown next =$34,000,” he wrote on X.

That figure exceeds commonly held predictions by traders for where Bitcoin’s next generational floor will be. As Cointelegraph reported, consensus favors the area between $40,000 and $50,000.

This week, however, Bloomberg Intelligence analyst Mike McGlone warned that price may already be trending toward seven-year lows.

Bitcoin historically rebounds in April

Continuing the bear-market comparison, data from network economist Timothy Peterson revealed that April could mark some form of inflection point for price.

Related: Bitcoin risks new lows as US dollar targets highest level since April 2025

A chart uploaded to X this week shows April typically being a recovery month during bearish phases.

The March monthly close, meanwhile, ended a five-month losing streak for BTC/USD with modest gains of 1.8%.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Crypto World

AccuQuant launches automated trading of Ethereum contracts, enabling users to earn $7k a day through swing trading

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Ethereum drops below key support as traders turn to automated systems like AccuQuant for intraday strategies.

Summary

- Ethereum drops below key support as bearish momentum builds, while traders watch resistance near 2200 for reversal signals

- AccuQuant launches automated Ethereum trading system targeting intraday gains amid heightened market volatility

- Automated crypto strategies gain traction as traders seek emotion-free execution and consistent small-profit accumulation

Ethereum experienced a sharp drop yesterday, with the price breaking below support near the daily moving average. The MACD bearish momentum intensified again, and other technical indicators remained relatively flat.

If the price rebound fails to break through the previous high near 2200, a further pullback could potentially trigger a fifth wave retracement. In such volatile markets, relying solely on manual judgment is often susceptible to emotional biases and makes it difficult to capture market rhythms in a timely manner. To address this pain point, AccuQuant launched a fully automated Ethereum contract trading system, enabling users to earn $7,000 per day through intraday trading.

What is AI automated trading?

AI cryptocurrency automated trading uses algorithms and data models to replace manual market analysis. It continuously monitors the cryptocurrency market 24 hours a day, accurately identifies trading opportunities, automatically makes long and short trading decisions, and executes buy and sell operations. It is an intelligent trading system that operates around the clock, delivering high efficiency without emotional interference.

How to start AI-powered fully automated trading?

1. Register now and claim a $20 welcome bonus.

2. Choose a suitable strategy and start automated trading.

3. Withdraw profits or continue trading.

- Beginner Experience: Amount: $100 | Period: 2 days | Daily Return: $3 | Return at Maturity: $100 + $6

- Starter: Amount: $500 | Period: 5 days | Daily Return: $7 | Return at Maturity: $500 + $35

- Advanced: Amount: $3,000 | Period: 15 days | Daily Return: $45.3 | Return at Maturity: $3,000 + $679.5

- Premium: Amount: $5,000 | Period: 20 days | Daily Return: $78.50 | Return at Maturity: $5,000 + $1,570

- Pro: Amount: $10,000 | Period: 25 days | Daily Return: $162 | Return at Maturity: $10,000 + $4,050

- Expert: Amount: $30,000 | Period: 30 days | Daily Return: $516 Maturity Payout: $30,000 + $15,480

- Elite: Amount: $100,000 | Lifetime: 42 days | Daily Payout: $2,000 Maturity Payout: $100,000 + $84,000

(Click here to see more automated trading strategies)

Case study: How to achieve a daily profit of $7,000

An AccuQuant user, after enabling an automated Bitcoin trading strategy, saw the system complete multiple trades throughout the day.

Given the day’s highly volatile market, the strategy achieved a cumulative profit of approximately $7,000 by consistently capturing small fluctuations.

The key was not in a single large profit, but rather in:

- High-frequency, small-amount profit accumulation

- Strict adherence to strategy discipline

- Avoid emotional trading

- Continuously participate in market fluctuations

- Sign Up and Receive Rewards, Easily Start Trading

New users receive a $20 reward upon registration and can earn an additional $0.50 daily upon login. Experience automated trading with zero barriers to entry.

- No Need to Monitor the Market, the System Works for You 24/7

Say goodbye to staying up all night watching market data. The AI system runs automatically 24/7, avoiding emotional interference and giving you back your time.

- Simple and Easy to Use, Even Beginners Can Quickly Get Started

The interface is intuitive and clear, requiring no complicated operations. Whether someone is a beginner or a professional trader, they can easily use it.

- Earn Money Through Referrals, Multiple Ways to Reward

Join the affiliate program and earn up to 3% + 1.5% referral rewards, diversifying income streams.

- Transparent Fees, No Hidden Costs

No extra transaction fees or management fees. All fees are clearly visible, making every profit safer.

- Multi-currency support, flexible and convenient deposits and withdrawals

Supports deposits and withdrawals of various mainstream cryptocurrencies, including:

BTC, ETH, DOGE, SOL, XRP, USDC, LTC, and USDT (TRC20/ERC20), meeting the needs of different users.

In the volatile cryptocurrency market, where volatility equals opportunity, the key is not predicting prices but rather how to efficiently participate in the volatility itself.

AccuQuant empowers users to participate more systematically in intraday cryptocurrency market movements through automated and quantitative strategies.

For more information, visit the official website.

Media contact: [email protected]

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Crypto World

Ethereum Foundation stakes $93 million of ether in a day, reaching its 70,000 ETH target

The Ethereum Foundation staked roughly $93 million in ether (ETH) on Thursday in several batches, bringing its total staked position to approximately $143 million and nearly completing the 70,000 ETH staking target it announced in February, according to Arkham data.

The total deposit of 45,034 ETH was split into uniform chunks of 2,047 ETH, each worth roughly $4.23 million, sent from the foundation’s treasury multisig to the Eth2 Beacon Chain deposit contract.

At roughly $2,059 per ETH, the $143 million total staked position works out to approximately 69,500 ETH, nearly the full 70,000 ETH commitment.

The foundation had been building toward the target incrementally since February, starting with an initial 2,016 ETH deposit and adding roughly 20,470 ETH on Monday. Thursday’s batch covered the remaining balance in one shot.

The foundation’s Arkham-tracked portfolio shows approximately $270.9 million in total assets across 14 addresses, with ETH as the dominant holding at roughly 102,400 ETH ($210.9 million). Smaller positions include USDC, BNB, and a fraction of a bitcoin.

Yield income

Staking is the process of locking up cryptocurrency to help secure a blockchain and earn rewards. It’s analogous to buying bonds and lending money to the government in return for fixed income yields.

At current staking rates, the position would generate roughly $3.9 million to $5.4 million annually at the 2.7% to 3.8% APY range typical for institutional stakers. With MEV-boost, returns could run higher.

That is modest relative to the foundation’s annual operating expenses, which have historically run near $100 million, but it converts a dormant treasury into a productive one without selling ETH.

Why staking?

The Ethereum Foundation is putting its ETH to work through staking, earning rewards that help fund research, grants, and operations — all without needing to sell its coins, creating a long-term, self-sustaining treasury.

This replaces the earlier model where the foundation resorted to ETH sales that weighed over valuations. The foundation faced criticism for the same through 2024 and early 2025.

With staking, the foundation earns yield. The shift, however, does not fully eliminate the need to sell entirely.

At the same time, completing the 70,000 ETH target does not mean staking is done. The foundation still holds over 100,000 unstaked ETH. Whether it expands the program beyond the initial commitment or holds the rest as liquid reserves has not been announced.

Ether traded at $2,059 at the time of the deposits, down roughly 4.3% over the past week.

The path from Stake.com to ZunaBet is becoming one of the most well-traveled routes in crypto gambling. It starts with a question that more players are asking in 2026 than at any point before: is there a better option? That question leads to a search. That search leads to comparisons. And those comparisons increasingly lead to the same destination. ZunaBet launched in 2026 and has quickly established itself as the platform that crypto gamblers discover when they decide to look beyond what they already know. Stake.com continues to operate at scale — its brand and traffic remain significant. But a growing number of its users are no longer content with what the platform provides, and ZunaBet has built exactly what those users are looking for. Here is why the path keeps leading to the same place.

Stake.com: The Platform That Opened the Door

Stake.com deserves its place in the history of crypto gambling. Launching in 2017 under a Curaçao license, it was among the first platforms to demonstrate that a full-scale gambling operation could function entirely on cryptocurrency. Bitcoin, Ethereum, Litecoin, Dogecoin, and other major coins were accepted from the beginning, which gave crypto holders something the rest of the gambling industry was not yet willing to offer — a native place to play.

Original games gave Stake a soul. Crash, Plinko, Mines, and Dice became iconic within the crypto gambling community, building a player base that was loyal not just to the platform but to the specific experience those games created. Provably fair mechanics and clean design made them endlessly replayable. Third-party content from providers including Pragmatic Play, Evolution, and Hacksaw Gaming eventually expanded the casino with slots and live dealer options.

A sportsbook covering football, basketball, tennis, MMA, esports, and additional markets rounded out the product with competitive odds and an interface that kept things simple for experienced bettors.

Stake opened a door that the entire crypto gambling industry walked through. The complication is that some of the platforms that followed walked through it with better offerings.

What Sends Players Looking

The search for alternatives always starts with something specific. In Stake’s case, three recurring frustrations have created enough collective momentum to turn individual dissatisfaction into a visible market trend.

The absence of a welcome bonus is the trigger that initiates most searches. Stake has never offered deposit matching, free spins, or sign-up promotions of any kind. In the platform’s earlier years, this was a minor inconvenience because few crypto casinos were doing things differently. In 2026, with competitors extending welcome packages worth thousands of dollars, the inconvenience has matured into a genuine competitive weakness. Every player who learns about a multi-thousand dollar bonus on another platform while holding a bonusless Stake account faces a question that gets harder to ignore each time it comes up.

The concealed VIP program transforms mild frustration into active disengagement. Stake rewards its most valuable players through an invitation-only system that includes rakeback, recurring bonuses, and dedicated account management. For that small group, the program works well. For everyone else — which is the overwhelming majority — the program does not visibly exist. No tiers are published. No requirements are disclosed. No progress is shown. Playing regularly on Stake while receiving no structured recognition for that regularity creates a slow-building sense that the platform does not value your presence unless you are already in the top tier of spenders.

Game catalog size has become an increasingly common point of comparison. Platforms entering the market in 2025 and 2026 have arrived with game libraries that are dramatically larger than what Stake maintains. Players who enjoy exploring new games, testing different providers, and accessing a wide range of styles find themselves constrained on Stake in ways they no longer need to tolerate.

What Players Find When They Arrive at ZunaBet

ZunaBet went live in 2026 under Strathvale Group Ltd with an Anjouan gaming license. The founding team has more than 20 years of combined experience in online gambling. The platform was not bolted onto existing fiat infrastructure — it was designed natively around cryptocurrency, making digital assets the default for every function.

The game library hits first. Over 11,000 titles from 63 content providers fill the platform. Pragmatic Play, Hacksaw Gaming, Yggdrasil, BGaming, and Evolution sit among 60+ studios that contribute slots, RNG table games, and live dealer content. The catalog is not inflated with filler — the range of mechanics, visual styles, volatility profiles, and themes provides genuine variety that sustains interest over months of regular play.

Sports betting is a built-in feature rather than an add-on. The sportsbook handles football, basketball, tennis, NHL, combat sports, virtual sports, and esports markets covering CS2, Dota 2, League of Legends, and Valorant. A single account with a shared balance keeps everything connected, so moving between a slot session and a live match bet takes seconds.

More than 20 cryptocurrencies are accepted: BTC, ETH, USDT on multiple blockchain networks, SOL, DOGE, ADA, XRP, and others. No processing fees are charged. Withdrawals are engineered to settle quickly. Native apps for iOS, Android, Windows, and MacOS provide consistent access, and live chat operates around the clock.

The First Thing That Changes Their Mind

The welcome bonus is typically the moment a browsing Stake player becomes a depositing ZunaBet player.

On Stake, there is no bonus. Your deposit equals your balance and nothing is added. Every session from your first bet onward is funded entirely by your own money.

On ZunaBet, new players receive up to $5,000 in matched deposits plus 75 free spins across three transactions. First deposit: 100% match up to $2,000 with 25 free spins. Second: 50% match up to $1,500 with 25 spins. Third: 100% match up to $1,500 with 25 spins. The three-deposit format means the welcome period extends across multiple sessions, building engagement gradually rather than exhausting the bonus in one shot.

For someone who has never received a bonus on any platform, the impact goes beyond the financial. Seeing a deposit doubled communicates something about how the platform views the player relationship. It says your business is worth competing for. That message alone is enough to shift a player’s mindset from casually browsing to genuinely considering a permanent switch.

The Thing That Makes Them Stay

Welcome bonuses attract attention. Loyalty programs earn commitment. The gap between how Stake and ZunaBet handle ongoing rewards is what turns a ZunaBet trial into a ZunaBet home.

Stake keeps its loyalty system behind a barrier that most players will never cross. The VIP program is by invitation only, governed by criteria nobody can see. Those inside it benefit from rakeback, regular bonuses, and personal account management. Those outside it — the vast majority of the player base — receive nothing beyond the standard gambling experience. No tiers to track. No milestones to chase. No feedback that their play is generating any return beyond what the games themselves provide.

ZunaBet shows you everything before you place your first bet. The dragon evolution loyalty program has six tiers published in full: Squire at 1% rakeback, Warden at 2%, Champion at 4%, Divine at 5%, Knight at 10%, and Ultimate at 20%. Free spins increase with each tier up to 1,000. VIP club access and double wheel spins add additional layers. A dragon mascot called Zuno gives the progression personality and makes climbing tiers feel like part of the fun rather than background accounting.

Nothing is hidden. Nothing is invitation-only. Every player sees the complete structure from day one and can track exactly where they stand within it. At 20% rakeback, the Ultimate tier returns a substantial portion of the house edge on every wager, creating ongoing value that compounds across every session. For a player who spent their Stake tenure with zero structured loyalty recognition, discovering a system that rewards them openly and progressively is usually the deciding factor in making ZunaBet their permanent platform.

Where Both Platforms Sit in the Wider Market

Stake and ZunaBet occupy the crypto-native tier of online gambling, which separates them fundamentally from traditional operators like DraftKings, BetMGM, FanDuel, and Caesars. Fiat platforms carry the overhead of bank processing, card network fees, and withdrawal timelines that can stretch across multiple business days. For players who hold and transact in crypto, those platforms represent a step backward.

Within the crypto tier, ZunaBet extends further. Over 20 supported coins, including USDT across several blockchain networks, reflect how crypto users actually manage their holdings in 2026. Zero platform fees on every transaction and fast withdrawal processing keep the financial experience frictionless. Stake supports fewer coins and offers a narrower payment framework, which increasingly matters to players whose crypto activity spans multiple tokens and chains.

Why the Path Keeps Leading Here

The reason ZunaBet keeps appearing at the end of Stake alternative searches is straightforward — it was built to be found there. Every feature addresses a documented frustration. The $5,000 welcome bonus fills the void Stake leaves empty. The 11,000+ game library from 63 providers replaces a catalog players have outgrown. The transparent six-tier loyalty program with up to 20% rakeback replaces an invisible system that most players never benefit from. The 20+ supported cryptocurrencies with zero fees outpace Stake’s payment infrastructure.

Stake created the foundation for crypto gambling and earned every bit of its reputation. But foundations are meant to be built upon, and ZunaBet represents the next floor. More games, more value at sign-up, more transparency in rewards, and more flexibility in payments — delivered by a platform that treats earning player loyalty as an ongoing responsibility rather than a settled achievement.

The players finding ZunaBet through alternative searches are not leaving crypto gambling. They are upgrading it. And in 2026, ZunaBet is where that upgrade lives.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Web3 careers evolve as professionals adopt new framework to evaluate mature, capital-driven organizations.

Summary

- Web3 matures into regulated global finance, shifting careers from hype to fundamentals and structured growth

- In 2026, crypto firms favor diversified revenue models over token-driven growth and short-term momentum

- Security leads, with firms like WhiteBIT setting standards through audits and top-tier certification

By 2026, web3 will have become the backbone of global finance. The industry has matured into a regulated, capital-heavy, and globally competitive landscape. While many professionals still evaluate web3 employers based on 2020-style hype, this outdated logic no longer works.

To help professionals navigate their next career move, we have outlined the five pillars of a mature web3 organization.

1. Look beyond growth headlines, focus on business structure

Rapid expansion isn’t always a sign of strength. In 2026, a resilient company demonstrates diversified revenue foundations and scalability that withstands market cycles.

- Green Flag: The company has multiple revenue streams (B2B, B2C, RWA integrations).

- Red Flag: Growth depends solely on a single-token model or favorable market conditions.

Candidate Tip: It is worth asking, “How does the company generate value beyond its native token or core trading fees?”

2. Prioritize regulatory and security infrastructure

Compliance and cybersecurity are no longer “optional” — they are the company’s DNA. Today’s leaders operate under evolving frameworks and strict global security standards.

- The Industry Standard: Leading organizations do not just “claim” security; they prove it. WhiteBIT, for instance, was the first crypto exchange to achieve the highest level of CCSS (Cryptocurrency Security Standard) certification, reinforced by regular independent audits.

Interview Question: “What independent security certifications or regulatory licenses does the company currently hold in Tier-1 jurisdictions?”

3. Seek ecosystem thinking, not single-product focus

Standalone products are fragile. Mature companies build ecosystems — interconnected services that reinforce each other.

- Ecosystem Synergy: Evaluation should focus on the integration between a blockchain (e.g., Whitechain), crypto-acquiring (Whitepay), and the core exchange services.

- Global Reach: Serious players form strategic partnerships beyond crypto, proving global credibility and financial stability.

Interview Question: “How does this role interact with other products in the company’s ecosystem, and what are the strategic priorities for cross-product integration this year?”

4. Analyze governance and decision-making discipline

Speed without structure leads to volatility. In a mature web3 industry, disciplined decision-making isn’t bureaucracy; it’s performance-enhancing infrastructure.

The “red flag vs. green flag” checklist:

- Green Flag: Clear ownership, coordinated execution across distributed teams, and transparent leadership communication.

- Red Flag: Using the “move fast and break things” mantra as an excuse for lack of planning and constant team burnout.

Candidate Tip: A professional should ask, “How are strategic pivots communicated to the team, and how is accountability defined in cross-functional projects?”

5. Focus on talent investment, not just role scope

Web3 can offer broad responsibility, but that doesn’t always equal growth. The key in 2026 is whether the company treats talent as long-term capital.

- Development: Are there defined career pathways?

- The Maturity Indicator: Companies like WhiteBIT build internal pipelines and nurture future leaders who can navigate the intersection of finance, law, and AI.

Interview Question: “Can you provide an example of someone who has transitioned between different ecosystem products or moved into a leadership role internally? What did their development path look like?”

Final decision-making checklist

Before signing an offer, professionals should check these four boxes:

- Ecosystem: Is the product part of a larger, stable infrastructure?

- Security: Is there a CCSS Level 3 or equivalent independent validation?

- Sustainability: Does the revenue model work in a “bear” market?

- Growth: Does the company invest in cross-functional skills?

- Compliance: Does the company adhere to legal and regulatory requirements?

Closing perspective

The question in 2026 is no longer “Who is moving fastest?” but rather “Who is built for the long term?” Companies like WhiteBIT have spent years building a global presence focused on security, operational discipline, and ecosystem-driven growth. In a mature market, these factors are the only reliable indicators of a sustainable and rewarding career path.

Explore current career opportunities at WhiteBIT here.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

World Liberty Financial Under Ethics Fire: Can WLFI Crypto Survive Corruption Allegations?

Carlos Alcaraz said to possess a rare skill that could lead to massive Grand Slam success

Backstreet Boys singer Brian Littrell ‘denies using homophobic slur’ after backlash to heated argument

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

LIVE : New Financial Year 2026, Major Changes From April 1st | V6 News

Ethereum to $40,000 by 2030: Why ETH Could MASSIVELY Outperform Bitcoin

Cathie Wood & Larry Lepard: “This Is Exactly What Happened Before Bitcoin Did a 10x”

-

NewsBeat7 days ago

NewsBeat7 days agoThe Story hosts event on Durham’s historic registers

-

NewsBeat18 hours ago

NewsBeat18 hours agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Sports7 days ago

Sports7 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment4 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World2 days ago

Crypto World2 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business13 hours ago

Business13 hours agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Entertainment6 days ago

Entertainment6 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Tech4 days ago

Tech4 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World3 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports3 days ago

Sports3 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Fashion5 days ago

Fashion5 days agoAmazon Sundays: Soft Spring Layers

-

Business1 day ago

Business1 day agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech4 days ago

Tech4 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Fashion6 days ago

Fashion6 days agoWhen Evening Dressing Gets Colorful for Spring

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech5 days ago

Tech5 days agoElon Musk’s last co-founder reportedly leaves xAI

-

Tech4 days ago

Tech4 days agoApple will hide your email address from apps and websites, but not cops

-

Crypto World4 days ago

Crypto World4 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Politics4 days ago

Politics4 days agoShould Trump Be Scared Strait?

You must be logged in to post a comment Login