Crypto World

The Beginner’s Yield Farming Ladder: From $0 to Sustainable Passive Income in DeFi

Introduction

Decentralized finance has unlocked something traditional finance never could: permissionless income generation. No bank approvals, no gatekeepers — just you, your capital, and smart contracts.

But there’s a problem.

Most beginners enter yield farming the same way:

They see 100%+ APY, ape in… and learn about risk the expensive way.

This guide fixes that.

Instead of throwing random strategies at you, we’ll walk through a step-by-step “Yield Farming Ladder” — a structured path from beginner to advanced, designed to help you earn sustainably while understanding the risks.

Why Most Beginners Lose Money in Yield Farming

Before we talk profits, let’s talk reality.

Most beginners lose money because they:

- Chase high APYs without understanding the source

- Ignore risks like impermanent loss

- Trust unaudited or hype-driven protocols

- Overcommit capital too early

Here’s the uncomfortable truth:

High yield isn’t free money — it’s risk in disguise.

If you don’t know where the yield comes from, you are the yield.

Level 1: Training Wheels — Stablecoin Lending

Best for: Absolute beginners

Risk level: Low

Typical returns: 3–8% APY

This is where you start.

You deposit stablecoins (like USDC or USDT) into lending protocols, and borrowers pay interest to use your funds.

Why this works for beginners:

- No exposure to price volatility

- No impermanent loss

- Simple mechanics

What you’re learning:

- How DeFi protocols work

- How yield is generated (real demand vs incentives)

Think of this as your DeFi savings account — except it actually pays.

Level 2: Liquidity Pools — Where Real Yield Begins

Best for: Beginners ready to level up

Risk level: Medium

Typical returns: 5–20% APY

Now you step into liquidity provision (LP).

You deposit token pairs into decentralized exchanges, and earn:

- Trading fees

- Incentives (sometimes)

Example:

Provide ETH + USDC → earn fees every time someone trades that pair.

New concept unlocked: Impermanent Loss

This is the “gotcha.”

If token prices move unevenly, you might earn fees… but still lose compared to holding.

Simple analogy:

You’re running a currency exchange booth. If exchange rates swing wildly, your inventory value changes too.

What you’re learning:

- Market exposure

- Fee-based yield vs incentive-based yield

Level 3: Yield Optimization — Work Smarter

Best for: Intermediate users

Risk level: Medium

Typical returns: Variable (often higher due to compounding)

At this stage, you stop doing everything manually.

You use yield aggregators that:

- Automatically reinvest your rewards

- Optimize across pools

- Save time and gas fees

Why this matters:

Manual farming is like watering plants one by one.

Aggregators?

They install an irrigation system.

What you’re learning:

- Capital efficiency

- Compounding strategies

- Protocol diversification

Level 4: Advanced Strategies — The Danger Zone

Best for: Experienced users only

Risk level: High

Typical returns: 20%–100%+ (with serious risk)

This is where things get spicy — and risky.

Strategies include:

- Leveraged yield farming

- Farming new/high-incentive protocols

- Looping (borrow → farm → repeat)

The trade-off:

Higher returns = higher chance of:

- Liquidation

- Smart contract exploits

- Total loss

Let’s be blunt:

This is where people either multiply their capital… or become a Twitter warning thread.

Proceed with caution.

The Risks You Cannot Ignore

If you skip this section, you’re basically speedrunning losses.

1. Smart Contract Risk

Bugs or exploits can drain funds instantly.

2. Impermanent Loss

LPs can underperform simple holding.

3. Protocol Risk

Not all platforms are audited or trustworthy.

4. Market Volatility

Crypto moves fast. Your yields can vanish just as quickly.

5. Overexposure

Putting everything into one strategy = one point of failure.

The Perfect Beginner Yield Farming Path

Here’s the roadmap that actually works:

Step-by-step progression:

- Start with stablecoin lending

- Move into ETH or major asset exposure

- Try stable liquidity pools

- Explore volatile LPs

- Experiment (carefully) with advanced strategies

The key principle:

Start simple. Scale with understanding — not hype.

Example: A Beginner-Friendly $1,000 Yield Portfolio

Let’s make this practical.

Sample allocation:

- $500 (50%) → Stablecoin lending

- $300 (30%) → Stable LPs

- $200 (20%) → Experimental strategies

Why this works:

- The majority of low-risk yield

- Some exposure to higher returns

- Limited downside if experiments fail

This isn’t about maximizing gains.

It’s about staying in the game long enough to learn.

Final Thoughts

Yield farming isn’t a shortcut to wealth.

It’s a system — one that rewards:

- Patience

- Understanding

- Risk management

The real edge isn’t finding the highest APY.

It’s knowing:

- Which yields are sustainable

- Which risks are worth taking

- When to scale… and when to step back

Because in DeFi, survival is the strategy.

And once you survive long enough?

That’s when the real compounding begins.

REQUEST AN ARTICLE

Ripple is moving digital assets from the periphery of corporate finance into the heart of treasury operations. The company announced an update to its treasury management platform that adds native digital asset capabilities, enabling finance teams to hold, track and manage cryptocurrencies alongside traditional fiat balances within a single system.

The upgrade introduces Digital Asset Accounts and a unified dashboard that aggregates balances across bank accounts, custody providers and on-chain wallets. The result is real-time visibility into both cash and digital assets, all reconciled within Ripple’s treasury interface, according to the company. The platform supports XRP and Ripple USD (RLUSD), with balances updated in real time and recorded alongside fiat transactions. APIs connect external custodians and sync activity back into the platform.

Ripple emphasizes that embedding digital asset functionality directly into its treasury system reduces the need for separate crypto tools, potentially cutting manual reconciliation and fragmented reporting across banking and custody systems. “The shift is about making digital assets a core part of treasury operations,” said Mark Johnson, Ripple’s chief product officer, noting use cases such as stablecoin settlement and yield on idle cash.

The rollout follows Ripple’s October acquisition of GTreasury for $1 billion, a deal that signaled a strategic push into enterprise treasury software. The company described the product as live for customers in beta ahead of a broader rollout, with availability varying by jurisdiction depending on regulatory requirements and geography.

Key takeaways

- Ripple adds native digital asset accounts and a unified dashboard to its treasury platform, enabling real-time visibility of fiat and crypto balances in one system.

- The platform supports XRP and RLUSD, with live balance updates and on-chain activity reconciled alongside traditional transactions.

- Digital asset functionality is embedded directly into treasury operations, potentially reducing reliance on separate crypto tools.

- The feature is in beta with phased rollout by jurisdiction, following Ripple’s GTreasury acquisition for $1 billion.

Ripple’s crypto-enabled treasury in practice

The integration of digital assets into treasury workflows is designed to streamline how enterprises manage liquidity, settlement, and treasury operations. By presenting XRP and RLUSD side by side with cash balances, treasurers can execute cross-asset transactions and approval workflows without leaving the platform. The real-time updates ensure that treasury teams see the latest asset positions, while the unified reporting helps reduce fragmentation across banking partners, custody providers and on-chain wallets.

In describing the move, Ripple’s Mark Johnson framed it as a natural evolution of treasury infrastructure. “Making digital assets a core part of treasury operations allows companies to manage them alongside traditional balances while enabling practical use cases such as stablecoin settlement and yield on idle cash,” he told Cointelegraph.

Strategic momentum behind the GTreasury tie-in

The product’s release aligns with Ripple’s broader enterprise strategy following its October purchase of GTreasury for $1 billion. Ripple said the treasury product is already accessible to select customers in beta, with broader availability contingent on regulatory considerations and geography.

The enterprise focus fits a wider pattern in the financial sector, where institutions are pushing to bring digital assets into mainstream financial infrastructure rather than keeping them siloed in crypto-native systems. The shift toward integrated asset classes mirrors a wave of institutional activity across payments and capital markets, as practitioners explore how tokenized representations can streamline settlement and custody.

Wider industry context: digital assets becoming part of financial infrastructure

A Ripple-published survey conducted in March found that 72% of more than 1,000 global finance leaders believe companies must offer digital asset solutions to stay competitive, signaling a move from mere experimentation to integration. The findings underscore growing emphasis on custody, security and robust infrastructure as institutions seek end-to-end visibility over crypto and fiat in a single platform.

In parallel, cross-industry moves illustrate the broader trend toward tokenized money and on-chain settlement. In July, Visa expanded its settlement platform to support additional stablecoins and blockchain networks, building on its early use of USDC for settlement in 2021. JPMorgan expanded access to its JPM Coin deposit token in November, enabling real-time settlement for institutional clients on blockchain rails. Meanwhile, Securitize and BNY Mellon announced plans to bring tokenized assets such as collateralized loan obligations on-chain. These developments collectively reflect a growing push to embed digital assets within traditional financial infrastructure rather than treating them as a standalone playground.

As the industry advances, the pace and scope of adoption will hinge on regulatory clarity and the ability of platforms to deliver secure, auditable, and scalable treasury workflows that can operate across jurisdictions.

Readers should monitor how quickly this integrated approach gains traction across sectors and geographies, and how regulators shape the rules for cross-border asset management and settlement in the enterprise space.

Federal Reserve Governor Michael Barr invoked a “long and painful history of private money created with insufficient safeguards” in remarks Tuesday, making the most pointed Fed case yet for aggressive stablecoin oversight under the newly enacted GENIUS Act.

The comments land directly on the two largest issuers in a $200 billion market – Tether and Circle – and signal that the Fed’s implementation posture will be harder-edged than the legislation’s passage suggested.

Barr addressed the GENIUS Act specifically, acknowledging that Congress’s stablecoin framework could accelerate development – then spending the bulk of his remarks cataloguing the risks that framework must contain. That sequencing was deliberate.

It tells markets that the regulatory rulemaking phase, now underway at the Fed and FDIC, will define what the GENIUS Act actually means in practice.

Key Takeaways:

- Barr’s Position: The Fed governor warned that stablecoins will only remain stable if they can be redeemed at par under stress conditions – including during Treasury market volatility and issuer-specific strain.

- Legislative Context: The GENIUS Act, signed into law in July 2025, established the first federal stablecoin framework; Barr’s March 31 remarks focus on implementation gaps that federal agencies must now fill through rulemaking.

- Reserve Risk: Barr flagged issuer incentives to maximize returns on reserve assets as a structural vulnerability – a direct warning applicable to Tether’s reserve composition history.

- Issuer Implications: The GENIUS Act mandates monthly reserve reporting and restricts backing assets to high-quality liquid instruments like U.S. Treasuries; Barr’s remarks signal strict Fed enforcement of those limits.

- Broader Regulatory Landscape: Stablecoin friction is already blocking progress on the Clarity Act, a separate digital asset bill – meaning Barr’s warnings have downstream effects beyond stablecoins alone.

Discover: Top Crypto Presales to Watch Before They Launch

What Barr Actually Said – and Why the Framing Matters

The phrase “long and painful history” is not rhetorical decoration. Barr is pointing at a specific lineage – the 19th-century free banking era when private bank notes traded at discounts and collapses wiped out depositors, money market fund runs in 2008 and 2020, and the 2022 TerraUSD collapse that erased $40 billion in weeks.

That history matters because it tells us exactly how Barr conceptualizes stablecoin risk: as a monetary problem, not just a consumer protection problem.

His core warning was precise: “Stablecoins will be stable only if they can be reliably and promptly redeemed at par in a wide range of conditions, including during stress in the market that can put pressure on the value of otherwise liquid government debt and during episodes of strain on the individual issuer or its related entities.”

That framing matters because it directly challenges the assumption that Treasury-backed reserves are automatically safe – even U.S. Treasuries face liquidity pressure during acute market stress, as March 2020 demonstrated.

Barr also named the incentive problem explicitly: issuers profit from stretching reserve asset quality, and that pressure intensifies as the market grows.

His formulation – “stretching the boundaries of permissible reserve assets can increase profits in good times but risks a crack in confidence during inevitable bouts of market stress” – is a pre-emptive argument against any industry lobbying to broaden the GENIUS Act’s permitted asset list during rulemaking.

Congress and regulators now have a Fed governor on record with a specific structural critique. The question is whether that critique shapes the rulemaking text or gets absorbed as boilerplate.

Explore: Best Crypto Projects With High Growth Potential in 2026

What the GENIUS Act Actually Covers – and Where the Fed’s Position Creates Friction

The GENIUS Act sounds clean on paper, but what matters now is how it actually gets enforced, because the rules it set are pretty strict.

Stablecoin issuers have to show their reserves every month, keep those reserves in safe and liquid assets like short term U.S. Treasuries, make it clear there is no FDIC protection, and follow real banking style rules around capital, liquidity, and AML.

Barr is now pushing the next phase, and his focus is very direct. He wants tight control over what counts as safe reserves, especially under stress, stronger rules to stop companies from escaping into weaker jurisdictions, and capital requirements that actually match real redemption risk. On top of that, he is doubling down on AML and limiting what stablecoin firms can do outside of issuing, to reduce spillover risk.

But the real story is not the law itself, it is the rulemaking that comes next, because that is where things either stay strict or get loosened. The big question is how narrow regulators define “safe assets,” since that decides how flexible issuers can be, and right now Barr is clearly leaning toward a tighter definition.

That tension is already spilling into other legislation, with negotiations slowing as regulators push a more cautious stance, so what we are seeing is not just policy being written, but a broader shift in how seriously the system wants to control crypto going forward.

Explore: Best Crypto Projects With High Growth Potential in 2026

The post Fed’s Barr Calls for Strong Stablecoin Oversight, Citing ‘Long and Painful’ History appeared first on Cryptonews.

Aave V4 is live on Ethereum with a hub-and-spoke design that keeps liquidity pooled while routing credit to bespoke RWA and structured credit markets for institutions.

Summary

- Aave has launched V4 on Ethereum mainnet, introducing a “hub-and-spoke” architecture aimed at real‑world asset (RWA) collateral and institutional structured credit markets.news.

- The protocol, which secures more than $24 billion in total value locked (TVL), is positioning V4 as core infrastructure for regulated RWA pipelines and on‑chain credit products rather than purely speculative leverage.

- V4 debuts with three liquidity hubs—Core, Prime and Plus—that route credit to specialized “spokes,” allowing bespoke risk policies without fragmenting Aave’s pooled liquidity.governance.

Aave (AAVE) has used EthCC 2026 in Cannes as the launchpad for its long‑anticipated V4 upgrade, activating a new “hub‑and‑spoke” architecture on Ethereum (ETH) mainnet that is explicitly designed to serve real‑world assets and institutional credit strategies. The decentralized lending protocol, which Phemex notes already holds more than $24 billion in TVL, is betting that its next phase of growth will come from RWA‑backed lending and structured products, not just yield‑farming loops.

In The Block, V4 is described as a system in which a central liquidity “Hub” extends credit lines to multiple lending markets, with Aave establishing three main hubs—Prime, Core and Plus—to segregate assets and use cases by risk level. Governance documentation on the Aave forum explains that “V4 allows each Spoke to define its own risk appetite, collateral policies, and liquidation rules while drawing on shared Hub liquidity,” likening the model to “a supranational bank allocating capital to regional facilities, each operating under its own mandate.” In practice, that means RWAs, fixed‑rate lending and more complex credit structures can sit in their own spokes, with conservative caps and isolation mechanisms, without splintering Aave’s overall liquidity or forcing users to choose between entirely separate pools.governance.

Coverage from Bitcoin.com and Me3 frames Aave V4 as a fundamental redesign rather than a minor version bump, highlighting that the new architecture “supports new market types like fixed‑rate lending and tokenized real‑world asset collateral” and “enables institutional borrowing against RWAs without fragmenting the protocol’s existing liquidity pool.” Those capabilities tie directly into Aave’s 2026 “master plan,” where founder Stani Kulechov outlined three pillars: the V4 upgrade, Horizon—an RWA platform tailored to institutions—and a new front‑end app aimed at onboarding mainstream users. Horizon is already focused on regulated, compliance‑aligned lending, targeting tokenized treasuries, real estate and private credit, with Kulechov’s goal to grow that platform beyond $1 billion in assets and deepen partnerships with firms like Circle, Ripple, Franklin Templeton and VanEck.

Those ambitions are underpinned by scale that is unusual even within DeFi. According to figures shared by Aave and cited by MEXC, the protocol has processed more than $3.33 trillion in total deposits since launch and issued close to $1 trillion in loans, generating around $885 million in fee revenue and capturing roughly 59% of the decentralized lending market. In that context, the decision to anchor V4’s debut to EthCC—amid a broader institutional turn at the conference—signals that Aave sees itself less as a pure crypto‑native money market and more as a candidate backbone for an on‑chain credit system that can handle both degen leverage and Basel‑sensitive collateral flows.

The launch comes after months of governance work and a sizeable funding push. In March, Aave Labs submitted the “Aave Will Win” framework, asking the DAO for $25 million in stablecoins and 75,000 AAVE tokens—about $42.5 million in total—to finance V4 development, a new independent foundation and growth initiatives targeting fintechs and institutions. A separate governance proposal set out the V4 activation path and initial asset range on Ethereum, with Kulechov telling the community on X that V4 is a “full redesign of the protocol’s structure” aimed at moving “the next trillion dollars in assets” on‑chain.

For users, the immediate changes include a more modular risk framework and the prospect of borrowing against a broader set of tokenized assets while still benefiting from Aave’s deep, shared liquidity. For the broader DeFi market, the upgrade cements a narrative shift: as more protocols chase RWA flows and institutional capital, flagship money markets like Aave are quietly turning into on‑chain credit utilities, with EthCC now serving as the stage where that transition is announced.

Key Takeaways

- Bernstein elevated Western Digital to Outperform from Market Perform, raising its price target from $170 to $340.

- A sharp 21% decline followed concerns about Google’s TurboQuant compression technology — which Bernstein argues poses zero threat to hard drive demand.

- The firm projects Western Digital and Seagate will achieve combined revenue growth of 24% CAGR between fiscal 2025 and 2030.

- Western Digital announced an extended timeline for its ePMR technology, potentially indicating a delayed shift to HAMR drives.

- Seagate remains Bernstein’s preferred stock in the segment, with its price target elevated to $620.

Despite recent volatility, Western Digital maintains a year-to-date gain of approximately 57%, showcasing resilience even through the latest correction.

Western Digital Corporation, WDC

The stock plunge was triggered when Google Research introduced TurboQuant — an advanced compression method designed to optimize KV cache during AI inference operations. Market participants worried this innovation could reduce storage hardware demand.

Bernstein’s Mark Newman firmly rejected this narrative. “There is zero impact to HDD demand,” Newman stated in his research note. He emphasized that TurboQuant’s influence on NAND flash storage, utilized solely for offloading inactive caches, is minimal at best.

According to Bernstein, the market reaction was excessive and unwarranted. Western Digital had tumbled 21% from its recent peak before the analyst’s upgrade. Related companies including Seagate and Sandisk experienced similar pressure.

Upgraded Revenue Projections for Storage Industry

Bernstein has adopted a more constructive stance on the broader storage industry. The research firm now forecasts that Western Digital and Seagate will achieve a combined revenue compound annual growth rate of 24% spanning fiscal years 2025 through 2030.

This represents a substantial upgrade from earlier projections that anticipated 18.7% bits growth accompanied by 3.6% annual price erosion. The updated model incorporates 24% bits expansion with pricing holding steady.

Newman pointed to several structural growth drivers: expanding AI computational workloads, increasingly sophisticated content production, extended data retention requirements, and strengthening data sovereignty regulations that support both volume growth and pricing power.

Regarding product developments, Western Digital’s 2026 Innovation Day revealed plans to extend its ePMR technology roadmap. The company essentially prolonged the lifecycle of its existing drive architecture by one to two additional years beyond prior expectations.

Questions About HAMR Rollout Timeline

The upgrade contains an important qualification. Newman interprets Western Digital’s continued emphasis on ePMR as an implicit indication that the company’s migration to heat-assisted magnetic recording — commonly referred to as HAMR — might be progressing slower than initially anticipated.

Bernstein’s financial model anticipates Western Digital will begin scaling HAMR production in 2027, representing approximately 5% of nearline exabyte shipments during that year.

This contrasts sharply with Seagate’s trajectory, where Bernstein projects roughly 70% of nearline volume will utilize HAMR technology by 2027. Seagate continues as the firm’s preferred investment, with its price target increased to $620 from $500.

Western Digital shares climbed approximately 2.3% during Wednesday’s premarket session following the upgrade before accelerating gains throughout regular trading hours.

Gnosis’ push behind the Ethereum Economic Zone shows DAOs moving from tuning parameters to voting on whether whole chains become Ethereum L2s, tying governance to market structure.

Summary

- Gnosis and Zisk’s Ethereum Economic Zone (EEZ) emerged directly from a GnosisDAO R&D mandate to explore turning Gnosis Chain into a natively integrated Ethereum layer‑2.

- The framework, co‑funded by the Ethereum Foundation and unveiled at EthCC 2026, aims to fix Ethereum’s “fragmentation problem” by enabling synchronous composability across L2s while keeping ETH as the core gas and settlement asset.

- The process marks a new phase in on‑chain governance, with DAOs effectively voting on the technical and economic destiny of entire chains, not just on parameter tweaks.

The Ethereum Economic Zone did not appear out of thin air at EthCC 2026; it is the visible tip of a governance process inside Gnosis that has been wrestling with a single strategic question for months: should a long‑running sidechain effectively become a native Ethereum layer‑2. GnosisDAO governance records from February 2026 show community discussions around a six‑month R&D collaboration with zero‑knowledge engineer Jordi Baylina to explore “converting Gnosis Chain (GNO) into a natively integrated Ethereum (ETH) L2 with synchronous composability,” as summarized by analytics site Crypto Whale Data. According to a subsequent note on that same site, “EEZ appears to be the product of that exploration,” effectively weaponizing Gnosis’ internal L2 thesis into a shared framework for the broader ecosystem.

At EthCC in Cannes on March 29, Gnosis co‑founder Friederike Ernst and Baylina formalized that pivot by unveiling the Ethereum Economic Zone, a rollup framework co‑funded by the Ethereum Foundation and pitched as a way to “reassemble Ethereum” into “One Ethereum.” As Binance’s coverage of the announcement notes, the “core commitment” of EEZ is “synchronous composability,” allowing smart contracts on connected rollups to interact with each other and with Ethereum mainnet “within a single atomic transaction” and using ETH as the default gas token. In an EtherWorld write‑up, Ernst is quoted telling the audience that “Ethereum does not have a scaling problem, it has a fragmentation problem,” arguing that every new L2 has become “its own island, separate liquidity, separate deployments, separate bridges that take a cut every time you try to move between them.”

What makes the Gnosis story different from a routine technical upgrade is the way governance and infrastructure are now fused. As MEXC’s summary of the initiative points out, Gnosis has been active as a layer‑1 for seven years, and its decision to help build EEZ means “a governance‑driven blockchain is actively choosing to tie its future to Ethereum’s rollup‑centric roadmap rather than compete as a standalone L1.” The same report stresses that development is being led by contributors from Gnosis and Baylina’s proving‑stack project Zisk, with the Ethereum Foundation co‑funding the work and a Swiss‑based EEZ Association created to maintain neutrality and invite broader participation.

Market commentators within the ecosystem have seized on the shift. In a widely circulated post, the Bankless account described EEZ as “Ethereum’s fragmentation problem [getting] its most serious answer yet,” emphasizing that it is “led by Gnosis and ZisK, funded by the EF.” A longer explainer published on Binance’s content platform asks, “Can this new framework bring Ethereum back together?” and frames EEZ as an attempt to stop building “more walled gardens” and instead connect existing rollups into “something that actually behaves like a single DeFi economy.”

For GnosisDAO and other token‑holder communities watching closely, the implications are clear. Governance is no longer just about changing interest‑rate curves or fee switches; it is about making existential choices over whether entire chains migrate into tightly coupled rollup frameworks, which settlement asset they prioritize, and how closely they bind themselves to Ethereum’s monetary and security model. The Gnosis‑EEZ path suggests that future DAO votes may increasingly resemble corporate strategy decisions—approve an R&D mandate, explore a structural pivot, then ratify an architecture that can redefine the chain’s economic role—rather than the parameter fine‑tuning that defined DeFi’s first era.

Visa Inc. signage on the floor of the New York Stock Exchange (NYSE) in New York, US, on Wednesday, Jan. 28, 2026.

Michael Nagle | Bloomberg | Getty Images

Visa is launching six new tools using artificial intelligence to modernize the process of disputing credit card charges, the company told CNBC exclusively.

The digital payments company said the tools are designed to reduce the costs and frustration of “outdated” dispute processes for multiple entities involved in the payments process: merchants, issuers and acquirers.

“Some of the challenges are these back-office systems are still largely manual,” Andrew Torre, Visa’s president of value-added services, told CNBC. “We really had to think differently about how we approach this at scale.”

In 2025, Torre said, Visa processed more than 106 million charge disputes globally, marking a 35% increase since 2019.

“Our goal is to streamline this as much as possible,” Torre said. “We’d love to be able to see that growth rate come down.”

Visa’s new tools are part of a larger push by major banks and financial institutions to incorporate AI into their businesses — both internally and in consumer-facing applications. JPMorgan Chase and Goldman Sachs have both said they’re already using AI to hire fewer people. BNY spent $3.8 billion on technology in 2025, or about 19% of its revenue.

Visa said three of its six new tools focus on merchants, allowing them to address potential disputes before they escalate, managing disputes with generative AI responses and providing a deeper level of detail on order insights to manage confusion over unfamiliar charges.

For example, Torre said, many disputes are borne out of cardholders not recognizing a specific charge on their statements. With the new tool, Visa will be able to provide further details to financial institutions to show cardholders that data at a deeper level, according to the company.

The other three tools are built for issuers and acquirers, using predictive AI models to aid in case-by-case analysis, analyzing documents for summaries and auto fill and establishing an AI-powered dispute platform to manage the entire process in one location, Visa said.

“We’ll be able to get them insights and data so they can move from being reactive to proactive,” Torre said.

Torre said Visa’s new AI tools are part of a broader host of solutions for consumers, including a subscription manager announced last week that allows cardholders to cancel unnecessary subscriptions directly on the manager.

The automation will save time, money and unnecessary confusion for both parties, he added. Most of the tools will be generally available later this year, the company said.

“We really believe that disputes in this solution makes it much easier to manage and resolve,” Torre said. “We think it has better outcomes for everyone.”

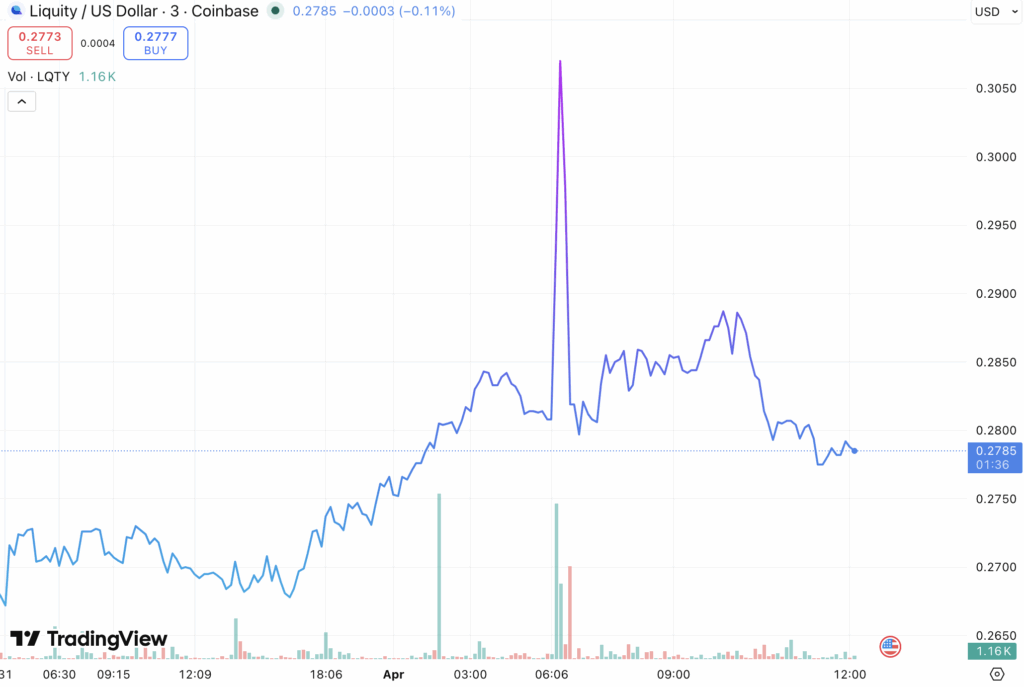

A crypto April Fool’s bit from protocol firm Liquity, which claimed it was being bought by stablecoin giant Circle, has led to allegations of “market manipulation” after it pumped the price of its in-house token.

Liquity announced on April 1 that it was acquired by Circle in a deal that would allow Circle to offer users “a non-freezable stablecoin and directly distribute yield under the Clarity Act.”

The joke pokes fun at Circle’s ability to freeze tokens and the fact that the Clarity Act, in its current form, seeks to ban yield on stablecoins.

Read more: ‘Bad actor’ Circle slammed for letting stolen $3M USDC sit unfrozen

Its freezing powers were ridiculed by the crypto investigator ZachXBT last week, who claimed Circle wrongly froze 16 wallets as part of a civil lawsuit.

Despite the buyout announcement being a joke on Liquity’s part, it still boosted its $LQTY token by 5%.

The price, however, pulled back in just a few minutes, and is now down 6% from its April 1 peak.

Crypto users on X weren’t too impressed with the joke, describing it as an “April Fool’s pump and dump.”

Read more: WIF fundraiser says Vegas Sphere refunds will start on April Fools

Some said it was an ultra-thin line between a joke and “market manipulation,” while others described the day as an opportunity to “do crime and it’s totally legal!”

Others were more forgiving. DeFi researcher Ignas said that crypto users were losing their minds over a “mere” 5% pump.

They added, “Good taste joke, IMHO. And good project.”

Other users warned not to base your trading on headlines, as on a day like April Fools’, most of them are “facetious.”

Read more: ‘Bad actor’ Circle slammed for letting stolen $3M USDC sit unfrozen

In response to the April Fools’ post, Liquity made it clear that it was just a joke, while also promoting its own stablecoin BOLD.

Additionally, Circle clarified to Protos that the announcement was false, and said “Circle has not acquired Liquity.”

The theme of crypto April Fools’ is phony acquisitions

There were at least two more fake crypto acquisitions announcements today. Crypto wallet firm Frontrun Pro announced that it had been acquired by AI giant Anthropic as part of a $141 million deal.

Crypto copy trading account PolyGun also announced that it had been acquired by Anthropic, this time in a transaction worth $69 million.

Dogecoin also did its own corporate April Fools’ joke, announcing that it would restructure the firm into “DogeCoin Financial Solutions LLC™.”

Read more: Memescope traders have been left with a case of Monday blues

As part of this, it said it would drop its Shiba Inu logo for something navy blue, stop saying words like “wow,” “much,” and “very,” and rebrand its “Doge army” as “Stakeholders.”

Some users thought it would be funny to pretend that memecoin launcher Pump Fun is finally dropping an airdrop in the form of “Pump Fun rewards.”

The platform announced an airdrop would be coming “soon” 266 days ago.

Others joked that Bored Ape Yacht Club had replaced the images of all of its NFTs with photos of actual monkeys and chimps.

Read more: BAYC goes full ‘laser eyes’ and allegedly blinds ApeFest attendees

A bitcoiner called Didi Taihuttu claimed, while wearing his Bitcoin hat and strutting around a luxury villa, that he would be switching back to traditional banks after crypto had become too volatile.

All these examples demonstrate that trading headlines on a day like today is risky business, and that firms with financial assets to their names should be careful about just what kind of April Fools’ they run.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Artificial intelligence giant OpenAI has closed $122 billion in committed capital at an $852 billion post-money valuation, a round that dwarfs anything raised in private markets and cements the company as the most valuable startup in history by a wide margin.

The funding was anchored by Amazon, Nvidia, and SoftBank, with continued participation from Microsoft. SoftBank co-led alongside a16z, D.E. Shaw Ventures, MGX, TPG, and accounts advised by T. Rowe Price.

The investor list reads like a who’s who of global capital — BlackRock, Blackstone, Fidelity, Sequoia, Temasek, Coatue, and ARK Invest all participated.

For the first time, OpenAI opened participation to individual investors through bank channels, raising over $3 billion from that tranche alone.

OpenAI said it is generating $2 billion in revenue per month, up from $1 billion per quarter at the end of 2024. ChatGPT has more than 900 million weekly active users and over 50 million subscribers. The company claims 6x the monthly web visits and mobile sessions of the next largest AI app, and 4x the total time spent of all other AI apps combined.

Enterprise now makes up more than 40% of revenue and is on track to reach parity with consumer by end of 2026. The company’s APIs process more than 15 billion tokens per minute. Codex, its coding agent, serves over 2 million weekly users, up 5x in three months.

OpenAI also expanded its revolving credit facility to approximately $4.7 billion, supported by JPMorgan Chase, Citi, Goldman Sachs, Morgan Stanley, and others. That facility remains undrawn as of March 31.

The company framed the raise around compute as a strategic moat. Its infrastructure strategy now spans cloud partnerships with Microsoft, Oracle, AWS, CoreWeave, and Google Cloud, silicon through Nvidia, AMD, AWS Trainium, Cerebras, and its own custom chip with Broadcom, and data centers through Oracle, SBE, and SoftBank.

Meanwhile, the company said it is building a “unified AI superapp” that would combine ChatGPT, Codex, browsing, and agentic capabilities into a single product.

The pitch is that as models get more capable, the bottleneck shifts from intelligence to usability, and a single surface lets the company translate model improvements directly into adoption.

The $852 billion valuation places OpenAI above all but a handful of public companies globally. For context, that is roughly the market cap of Berkshire Hathaway, and larger than Visa, JPMorgan Chase, or Samsung.

Crypto World

Non-USD stablecoin senders on Solana nearly tripled year-over-year, led by EURC and BRZ: Dune

Solana’s non-USD stablecoin adoption surged nearly threefold in the past year, driven by EURC and BRZ growth alongside institutional integrations from Visa, Stripe, PayPal, Mastercard, and Western Union.

Key takeaways

- ZCash is one of the worst performers among the top 30 cryptocurrencies by market cap, down 3.5% in the last 24 hours.

- The coin could rally higher in the near term amid demand for privacy-focused cryptocurrencies.

ZEC slips as broader market recovers

ZEC, the native coin of the Zcash ecosystem, is down by 3.5% in the last 24 hours, making it one of the worst performers among the top 30 cryptocurrencies by market cap.

It is trading at $241 per coin, down from the $257 recorded on Tuesday. The bearish performance comes amid a decline in Zcash’s derivatives data.

According to CoinGlass, ZEC’s futures’ Open Interest (OI) reads $438 million, down from the $473 million recorded on Tuesday, reflecting the decreased notional value of open contracts.

Typically, an OI decline during a dip in spot price reaffirms the bearish narrative as traders anticipate further recovery.

Technical outlook: Will Zcash price recover above $250 soon?

The ZEC/USD 4-hour chart is bullish but inefficient as Zcash’s price faced rejection above the $250 psychological level.

It is currently trading below its 50-day EMA of $248c, suggesting that the bulls failed to take advantage of the recent rally.

Despite that, the near-term bias is cautiously bullish as ZEC holds above the recent lows, while remaining capped beneath the long-standing descending resistance line.

If the bulls regain control and ZEC’s daily candle closes above $250, it would confirm the upside breakout and open the path toward the 200-day EMA at $274, followed by the 23.6% Fibonacci retracement level at $362.

The Moving Average Convergence Divergence (MACD) line has turned higher above the signal line and moved back into positive territory on the 4-hour chart, suggesting strengthening upside pressure.

The Relative Strength Index (RSI) at 61 reinforces the recovery of bullish momentum without signaling overbought conditions.

On the downside, if the rejection candle holds, ZEC could drop towards the 38.2% Fibonacci retracement level at $231, followed by the rising trendline near the $200 psychological support level.

Ripple expands treasury platform to include digital asset support

Starmer Shrugs Off Trump’s Threat To Leave Nato

Wayne Rooney sheds light on issues with Bukayo Saka as Arsenal chase PL title

-

News Videos7 days ago

News Videos7 days agoParliament publishes latest register of MPs’ financial interests

-

Business6 days ago

Business6 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Tech6 days ago

Tech6 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

NewsBeat5 days ago

NewsBeat5 days agoThe Story hosts event on Durham’s historic registers

-

Sports5 days ago

Sports5 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment2 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment4 days ago

Entertainment4 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World1 day ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports23 hours ago

Sports23 hours agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Fashion7 days ago

Fashion7 days agoHow to Style Spring Like WeWoreWhat: Easy Outfit Ideas for 2026

-

Entertainment7 days ago

Entertainment7 days agoHBO’s Harry Potter Series Will Definitely Fail For One Big Reason, And It’s Not J.K. Rowling Or Snape

-

Crypto World2 days ago

Crypto World2 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Fashion6 days ago

Fashion6 days agoEn Vogue in Brown Leather and Tailored Neutrals by Atelier Savoir, Styled by J Bolin

-

Tech1 day ago

Tech1 day agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Fashion6 days ago

Fashion6 days agoWhat Are Your Favorite T-Shirts for the Weekend?

-

Fashion5 days ago

Fashion5 days agoWeekly News Update, 3.27.26 – Corporette.com

-

Politics2 days ago

Politics2 days agoShould Trump Be Scared Strait?

-

Fashion3 days ago

Fashion3 days agoAmazon Sundays: Soft Spring Layers

-

Tech3 days ago

Tech3 days agoElon Musk’s last co-founder reportedly leaves xAI

You must be logged in to post a comment Login