Crypto World

The Next PM Could Decide Britain’s Crypto Future

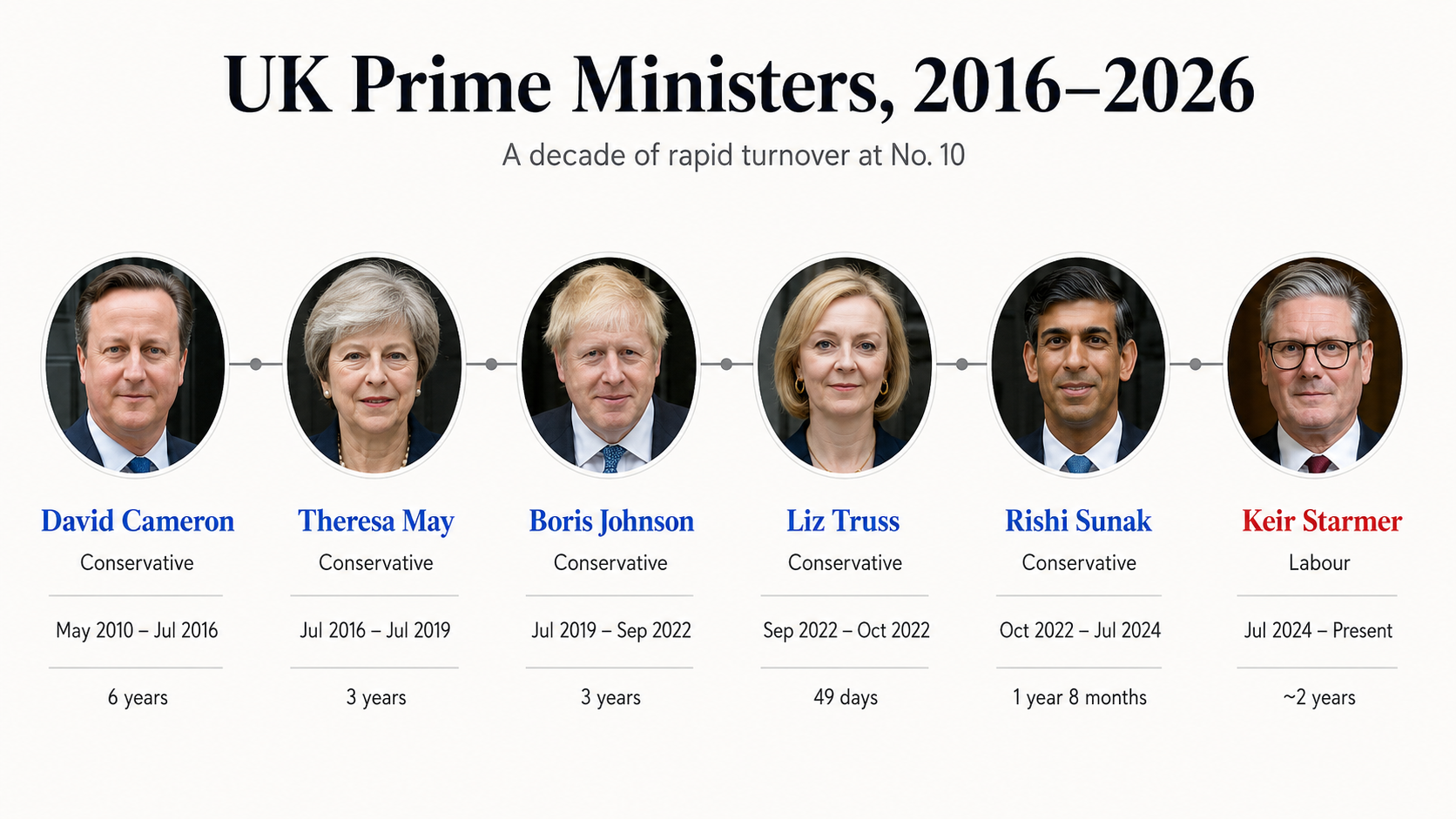

On Monday morning, June 22, Keir Starmer finally acknowledged what his Cabinet, parliamentary colleagues and the public had already concluded: he no longer had the authority to lead.

In doing so, he became the sixth prime minister in a decade – a level of political instability unmatched in modern British history. Every sector is now asking the same question: Who and what comes next? So, for digital assets, let’s unpack that.

Direction of Travel

From a policy perspective, the ship has largely set sail. Regulators are in the final stages of formalising a comprehensive framework, officials are listening, and engagement has been genuinely constructive.

This week’s announcement from the Bank of England illustrates the point well, even if it was partly overshadowed by political noise. Its policy statement and draft rules on sterling-denominated systemic stablecoins marked a clear step forward.

The required proportion of backing assets held in central bank deposits has been sensibly reduced from 40% to 30%, while the caps on holdings have been replaced by issuance limits.

“Each systemic stablecoin will be subject to an initial issuance maximum of £40 billion,” wrote The Bank of England.

We are imminently expecting a handful of policy statements from the FCA – covering everything from cross-cutting handbook reforms and the Regulated Activities Order. These will likely land much before a new Ministerial HM Treasury team is installed.

I mention this because political cycles may be volatile, but regulatory frameworks are built through sustained, technical engagement.

Politically speaking, we have navigated seven City Ministers since 2022 alone. Yet despite the political turbulence, the notion of a “global cryptoasset hub”, first coined by former PM Rishi Sunak, has survived.

Whoever walks through the door of No 10 – and whichever team follows them – will not reverse this. The wheel has already turned.

UK Crypto Sector Needs a Clear Political Wall

While we have made great progress on several ‘sticky’ issues for the sector, there are still some critical areas that need clear political will: the future direction for DeFi, a workable prudential regime for firms, workable FinProms rules, and a level tax playing field for stablecoins to name a few.

We must keep engaging at a political level to keep this momentum and keep landing messages around growth, productivity and jobs – all areas that transcend personnel. It is incumbent on industry to ensure that message carries through. We will certainly be playing our part.

More crucially, the digital asset agenda must not become politicised and dragged into the culture wars in the way it did in the US and as we’ve begun to see this year in the UK, thanks to so-called ‘crypto donations’.

This latest news shows how quickly the conversation descends into many of the usual tropes industry is familiar with, which are largely based on misunderstanding and misinformation.

Because strip away the headlines and the memes, and what we are actually talking about is rather prosaic. This is plumbing.

Financial infrastructure required to ensure the City of London remains a global centre of finance. With yesterday marking the tenth anniversary of Brexit, the point feels all the more pertinent.

That objective should transcend party lines. Encouragingly, there are signs that it does. Just last week, Conservative Party peers tabled amendments to the Financial Services and Markets Bill calling for a wholesale tokenisation strategy and a dedicated digital asset framework.

Meanwhile, the Liberal Democrats are actively developing their own policy platform for the sector.

And it must remain that way. The long-term success of the UK’s digital asset ecosystem will depend not on partisan point-scoring.

Who Steers the Ship?

It is too early to call who might stand against Burnham, but a coronation rather than a contest looks like the most probable outcome, especially following the early backing of Wes Streeting, himself long touted as a likely contender.

To add a layer of Westminster intrigue, sections of the media have been quick to elevate Al Carns as a possible dark horse contender. Yet the arithmetic looks challenging. Without the backing of the 81 MPs needed to trigger a contest, his route to the ballot is narrow.

So, with Burnham a few steps from No.10, attention inevitably turns to who might take up the keys to No.11, where the UK’s finance minister lives.

At this stage, Ed Miliband, Wes Streeting and Shabana Mahmood all appear to be in the frame as favourites.

On the face of it, Burnham is keeping his cards close to his chest. Whether this reflects genuine indecision or carefully managed ambiguity remains unclear.

More likely, it reflects an internal debate within his team about the future ideological direction of the Labour Party, with Reform UK waiting in the wings, buoyed by recent local election successes.

For now, the picture is one of competing centres of gravity rather than a settled plan, with No. 11 still very much up for grabs.

Other names are circulating. Yvette Cooper as a steady hand for markets, Miatta Fahnbulleh with her more radical economic vision, or even Louise Haigh, who is helping Burham run his campaign, as a wildcard.

What Does the Next UK PM Bring for Crypto?

For our sector, the jury is out. None of the frontrunners has meaningfully engaged with the digital assets industry to date.

The bookies’ favourite is a 2029 election, giving any new leader up to three years. That window must be used wisely, and it won’t be plain sailing for Burnham. A sharp lurch to the left risks alienating the very New Labour voices that brought Stamer’s Labour back to power.

Major foreign policy questions on Ukraine and Gaza remain unanswered and will prove divisive. On the economic front, whispers of significant cost-of-living interventions, particularly on energy bills and VAT, with limited financial headroom, suggest that borrowing may rise.

The markets’ reaction, as we saw with the pound strengthening and borrowing costs easing on news of Starmer’s departure, will be telling. History shows that bond market confidence can make or break an administration.

However, expect Burnham to make overtures to the City and roll back on some of his more hardline agenda in advance of coronation day to ensure he lands softly in No.10 and markets don’t give him a headache.

His team is already briefing about seeking guidance from well-known establishment figures such as Andy Haldane, a former Bank of England economist, to do just this.

But stepping back from the personalities, the task now is not to reopen the argument over digital assets, but to finish it properly, without losing focus on the inevitable noise that surrounds any moment of political transition.

Here at the UKCBC, we will keep fighting the good fight.

The post The Next PM Could Decide Britain’s Crypto Future appeared first on BeInCrypto.

Binance has informed European Union users that it will restrict access to certain services after a MiCA-related authorization deadline of July 1. According to user-shared notices attributed to the exchange, Binance will limit onboarding for EU customers and reduce the range of services available to EU-based accounts from that date, while directing users to ensure their assets can be withdrawn in accordance with applicable requirements.

The transition follows Binance’s earlier decision to withdraw a MiCA license application in Greece, underscoring how the EU’s Markets in Crypto-Assets (MiCA) framework is forcing operators to reassess their regional compliance status and service models. Cointelegraph reported on Binance’s MiCA license withdrawal ahead of this development, while the exchange did not respond to Cointelegraph for comment before publication.

Key takeaways

- Binance says it will restrict onboarding and certain services for EU users effective July 1 due to lack of MiCA authorization from an EU member state.

- The exchange’s notices indicate that withdrawals will remain available after the deadline.

- Binance advises users to consider self-custody or transferring assets to other licensed crypto asset service providers (CASPs).

- Questions remain for users about how restricted services will affect products such as staking and other yield-related positions.

- Industry commentary highlights uncertainty around how MiCA enforcement may apply to existing customers versus new users.

MiCA compliance timeline and Binance’s service restrictions

Under MiCA, crypto asset service providers offering services within the European Union must meet authorization and conduct requirements tied to specific activities, such as exchange services and related custody functions. Binance’s latest EU-facing notices frame July 1 as the point after which its ability to provide full services in the bloc depends on whether it holds the necessary MiCA authorization in an EU member state.

User-shared notices state that Binance will halt onboarding new EU users and curtail certain services for EU-based accounts from July 1 onward. The notices also emphasize continued access to withdrawals, stating that “all digital assets are still available for withdrawal,” aligning with obligations typically expected during service transitions and regulatory disengagement.

In practical terms, this approach shifts the operational risk to users: while the exchange indicates assets can be withdrawn, reduced service availability can affect customer workflows—particularly where users rely on the platform for ongoing positions or account-level operations. For compliance teams, the key issue is the operational continuity of customer asset access during regulatory transitions, alongside clear communications on what is changing and what is not.

Binance’s guidance: self-custody and shifting to licensed CASPs

Binance circulated guidance suggesting users may move assets to self-custodial wallets or transfer funds to other crypto asset service providers (CASPs). The exchange described the transition as intended to be “orderly,” with services reduced to position management and withdrawals after the deadline.

The broader market context is that other MiCA-licensed platforms have been competing for EU user attention ahead of the transition date. Some actively marketed services in EU member states, positioning themselves as regulated alternatives. For EU-focused firms, this is a reminder that MiCA compliance is not only a legal permissioning process—it also functions as a competitive differentiator in distribution and customer acquisition.

From a regulatory monitoring perspective, Binance’s communications also raise questions that institutions may need to address: for example, what specific account features remain available post-deadline, how user instructions are processed, and how staking-like arrangements are treated when service categories are restricted under MiCA conditions. Clear delineation of permitted versus restricted functions is crucial for consumer protection and audit readiness.

Staking and active positions: unresolved operational questions

Binance users have sought clarity on how the restriction phase will affect specific services, particularly staking and yield-related exposure. In public replies, a Binance representative reportedly told at least one user that balances remain “available and safe,” but did not provide granular details about the status of staked assets, staking rewards, or any ongoing yield generation mechanisms once restricted services begin.

This gap matters for both users and institutional counterparties. Staking arrangements can involve distinct custody and contractual terms, and the regulatory characterization under MiCA may vary depending on how the service is structured. Even if withdrawals remain open, uncertainty around whether reward distribution continues—or whether assets are automatically unwound or frozen—can create operational risk and complicate internal reporting requirements for regulated entities.

Additionally, uncertainty about account-level outcomes can trigger heightened customer support loads and potential disputes. For compliance stakeholders, such scenarios can elevate the importance of documented policy changes, customer notice archives, and evidence that the firm provided clear, timely and accurate information about service discontinuation and asset access.

Legal interpretation debate: existing users vs. new onboarding

Commentary from executives involved in the EU crypto market points to the legal nuance of how MiCA obligations are applied. Dominik Tomczyk, CEO of SIA AlphaRoute operating as Kanga Exchange EU, told Cointelegraph that platforms without MiCA authorization might still serve existing users under the concept of “reverse solicitation.” He suggested that, from a user perspective, the main change would be restrictions tied to marketing and user acquisition within the EU rather than immediate disruption to existing account access.

Other industry voices expressed less concern about near-term user impact, arguing that some public expectations about MiCA effects may be overstated. They also suggested that competitive positioning may influence how different actors frame the transition.

Still, for institutions, these perspectives do not eliminate uncertainty. Regulatory enforcement patterns can vary by jurisdiction and by supervisory interpretation, especially when service restrictions are linked to authorization status. Organizations monitoring counterparty risk should consider that compliance posture can shift quickly—through licensing outcomes, supervisory scrutiny, or operational restructuring—even where legal theories suggest continued access for existing customers.

What users and counterparties should watch next

As July 1 approaches, the most important items for analysts and compliance monitoring are Binance’s detailed implementation of restricted services for EU accounts, the operational treatment of staking and other yield-related positions, and the practical process for withdrawals and any transfers to third-party CASPs. Institutions should also track how EU supervisors respond to the transition and whether additional guidance clarifies the boundary between serving existing customers and limiting marketing or onboarding under MiCA.

About 60% of users who placed their first World Cup bets on Polymarket had never interacted with blockchain protocols before, suggesting prediction markets are becoming an entry point into crypto.

The finding is based on a 90-day Bitget Wallet study shared with Cointelegraph on Thursday that tracked the onchain activity of 857,000 active Polymarket users.

Bitget Wallet said the findings suggest some users are entering crypto through prediction markets instead of beginning with token trading or DeFi protocols.

Alvin Kan, chief operating officer at Bitget Wallet, told Cointelegraph that earlier crypto onboarding efforts largely focused on making blockchain technology easier to understand through simpler wallets and better user interfaces, but users were still expected to learn how crypto worked before they could participate.

“Prediction markets shifted that dynamic. Users show up because they have a view on something happening in the world,” Kan said.

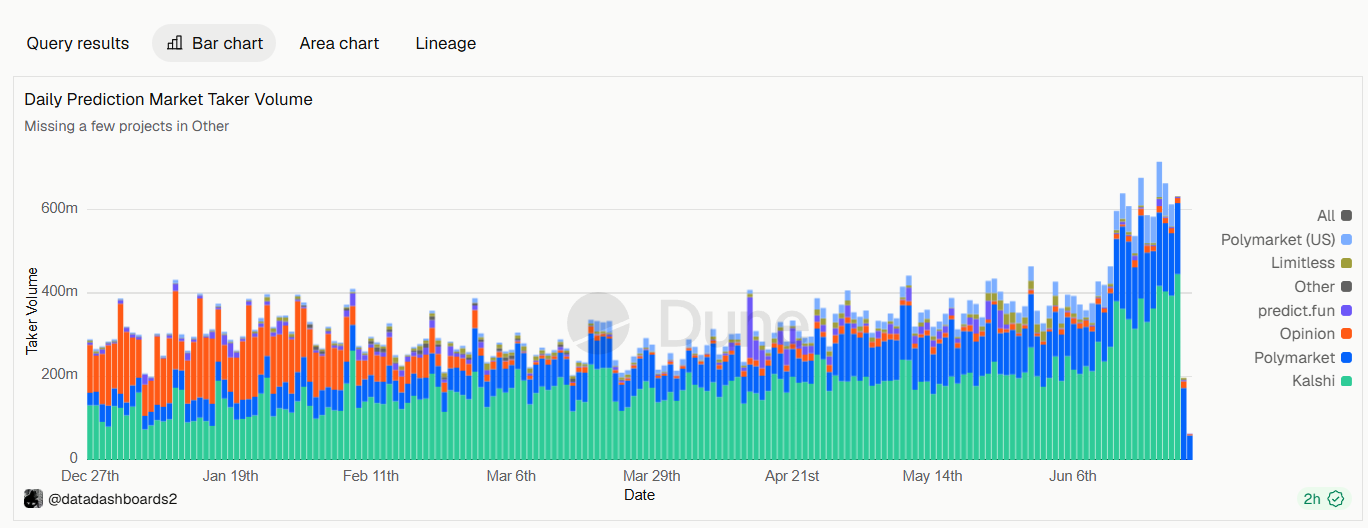

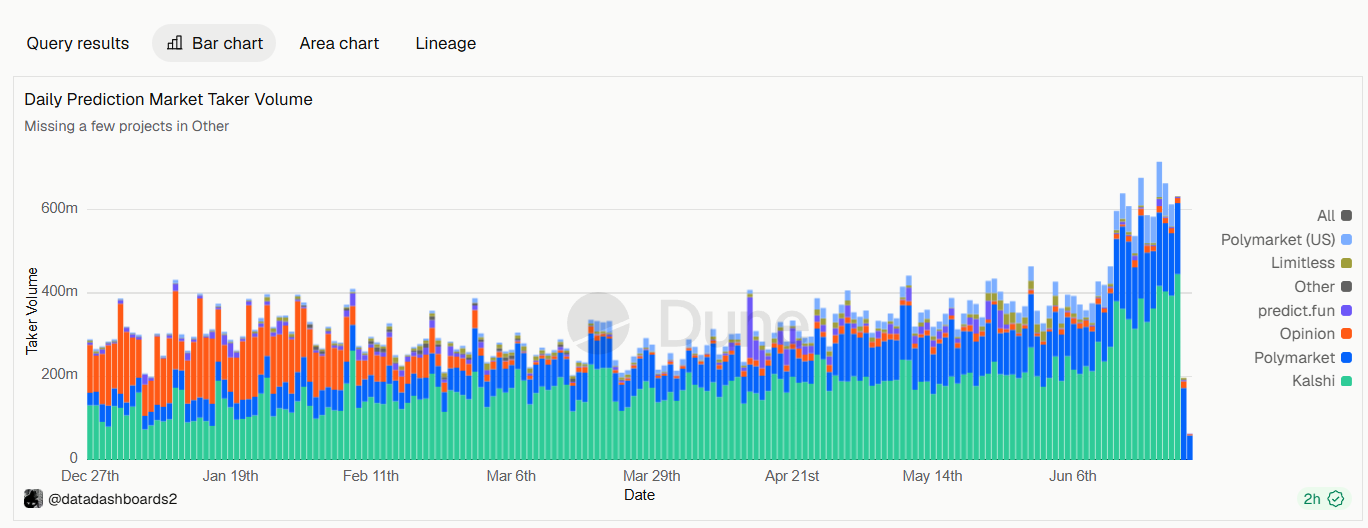

Daily prediction market taker volume. Source: Dune

Daily taker volume, which measures contracts bought or sold by traders filling existing orders, reached a record $713 million on Saturday, according to Dune data. The milestone came more than a week after the World Cup kicked off on June 11.

Related: CBOE debuts prediction market with S&P 500 contracts

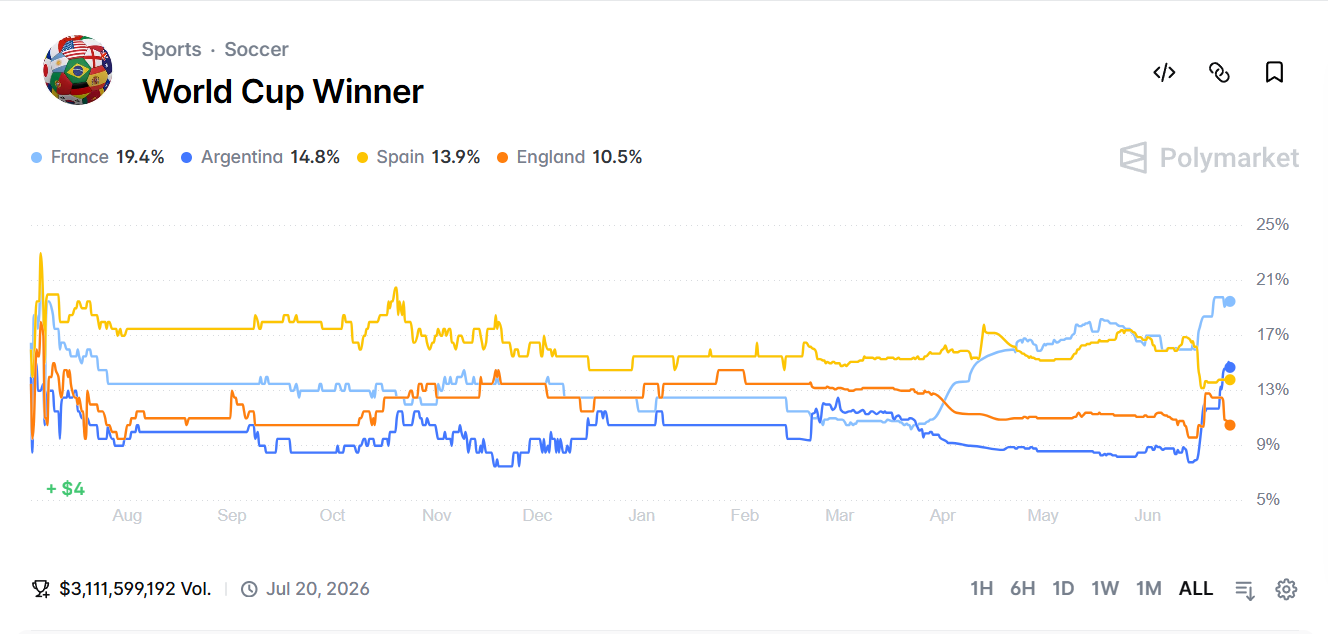

World Cup contracts drive $3.1 billion in volume to Polymarket

A June 11 Bernstein report predicted that the 2026 FIFA World Cup would generate more than $3 billion in incremental sports betting handle and between $5 billion and $10 billion in additional consumer prediction market volume. The World Cup winner contract alone has generated more than $3.1 billion in trading volume on Polymarket, according to platform data.

World Cup winner event contract. Source: Polymarket

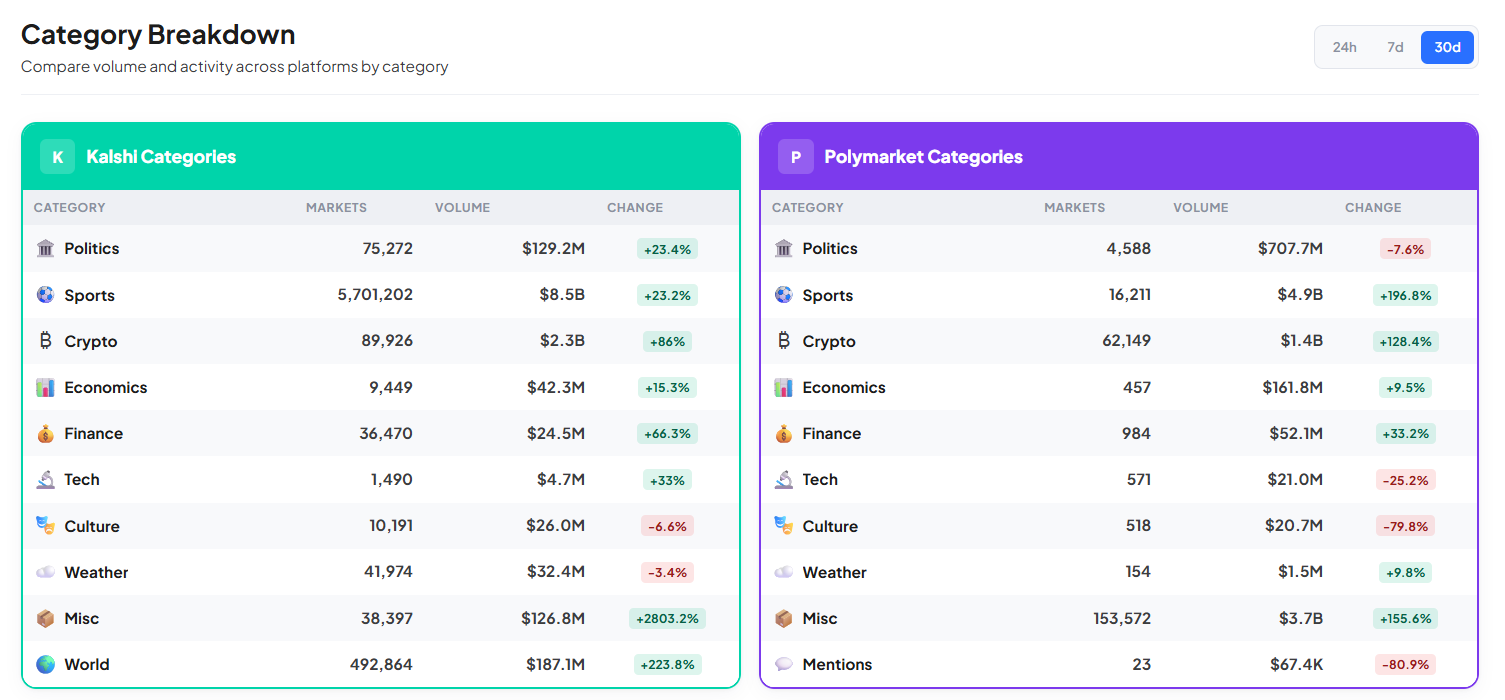

Sports contracts ranked among the biggest drivers of prediction market trading over the past 30 days. On Kalshi, they generated $8.5 billion over the past 30 days, making them the platform’s largest category. On Polymarket, sports also ranked first with more than $4.9 billion in trading volume during the same period, according to Defirate data.

Top categories on Kalshi and Polymarket. Source: Defirate

The surge in sports-related trading has also intensified regulatory scrutiny in the US.

On June 17, Kentucky sued five prediction market platforms, including Kalshi and Polymarket, accusing them of operating unlicensed sports betting platforms. At least 17 other states have taken prediction market operators to court, attracting the involvement of the Commodity Futures Trading Commission and the White House.

The CFTC later sued eight states, arguing they had interfered with the federal regulator’s exclusive authority over federally regulated event contracts.

Magazine: Should users be allowed to bet on war and death in prediction markets?

Decentralized finance (DeFi) protocol Spark has deployed approximately $150 million in stablecoin liquidity across two Uniswap v4 pools on Ethereum as part of a collaboration aimed at creating shared liquidity and exchange infrastructure for stablecoin issuers.

A Spark spokesperson told Cointelegraph that the initial deployment is live in two pools pairing USDS with PayPal USD (PYUSD) and USDT, with USDS serving as the foundation. Spark described the deployment as one of the largest automated market maker (AMM) liquidity migrations in DeFi.

“These pools represent the initial deployment of approximately $150 million of liquidity and establish the first phase of the Stablecoin FX Layer,” the spokesperson said. “This initial deployment focuses on bootstrapping shared liquidity on Uniswap v4.”

Earlier this month, Standard Chartered identified Uniswap as a potential beneficiary of tokenized assets moving into DeFi. It forecast that total assets held in DeFi could reach $2.7 trillion by 2030, with Uniswap potentially emerging as a liquidity venue for the growing market.

The deployment announced Thursday lays the groundwork for a planned programmable liquidity system that could reduce the need for banks, financial technology firms and stablecoin issuers to build separate liquidity networks while testing whether Uniswap can make onchain capital more efficient without weakening market depth.

Spark plans programmable liquidity expansion

Spark said it plans to introduce its Shared Liquidity Layer and DualPool hook in subsequent phases using Uniswap v4’s programmable architecture to coordinate how liquidity is distributed across stablecoin markets.

A liquidity hook enables protocols to seamlessly integrate with platforms for capital access and developing yield and trading strategies.

Spark said a hook is intended to allow capital not immediately needed for trades to be deployed into governance-approved products, liquidity venues and yield-generating strategies.

The implementation of the DualPool hook will go through a separate security review, testing and production-readiness process before deployment. The first phase uses standard Uniswap v4 pools rather than the planned programmable framework.

Related: Aave positioned to capture tokenized asset growth in DeFi: Standard Chartered

Spark said the planned framework is intended to give future stablecoin issuers access to shared liquidity rather than requiring them to individually bootstrap pools, coordinate market makers and manage inventory across different venues.

The spokesperson told Cointelegraph that Spark is working with additional partners across the stablecoin ecosystem but is not yet ready to disclose those integrations.

Uniswap seen as winner as tokenized assets move onchain

In a June 15 note to clients, StanChart’s bank’s head of digital assets research, Geoff Kendrick, said that tokenized treasures, equities, bonds and other assets could bring more trading activity and liquidity to decentralized exchanges as their DeFi use expands.

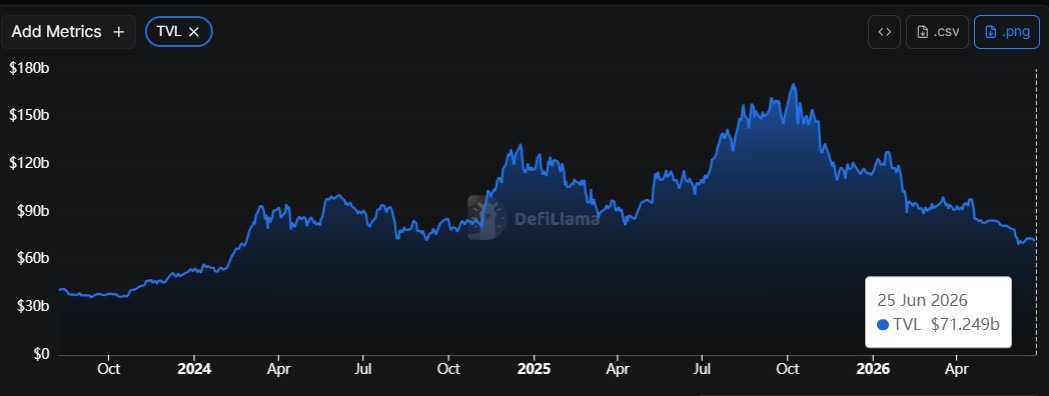

DeFi total value locked as of June 25. Source: DefiLlama

This new $150 million migration offers a more immediate test of StanChart’s infrastructure thesis, though it involves stablecoins rather than tokenized securities.

The migration also follows Uniswap’s push into institutional tokenized-asset trading. On Feb. 12, BlackRock said it would bring its $2.1 billion tokenized Treasury fund, BUIDL, to Uniswap, allowing eligible institutional investors and market makers to trade the security through decentralized infrastructure.

Magazine: Japanese pension fund tips 1% in crypto, G7 urges action on NK hackers: Asia Express

Crypto World

Post-prison CZ says time behind bars didn’t hurt the billionaire’s business after Binance

![]()

“I don’t hold grudges or anything, right? I just want to help to grow crypto anywhere in the world, and to do that, we need to help grow crypto in America.”

The Canadian national said he won’t participate at any level in U.S. politics, despite his industry’s growing reputation for political campaigning and influence. But he supports the U.S. aim to be the world’s crypto capital, and he sat for the interview during a trip to Washington.

In the meantime, he’s focused on the early backing of “highly impactful companies that may not be highly profitable companies.” So far, his criminal-justice experience hasn’t been a drag on those relationships.

“I had guys who apologized to me that they had a misunderstanding before,” CZ recalled. “They said, ‘Well, I thought there was some financial fraud.’”

If anything, he said, it’s been helpful.

“Sometimes it actually works as a plus,” he said. “It kind of builds your character that you went through this really difficult time and this unfair time, and you were tested and you were scrutinized, but they didn’t find any real issues, really. Well, there was the violation of the BSA, which I do not dispute, but there’s no fraud.”

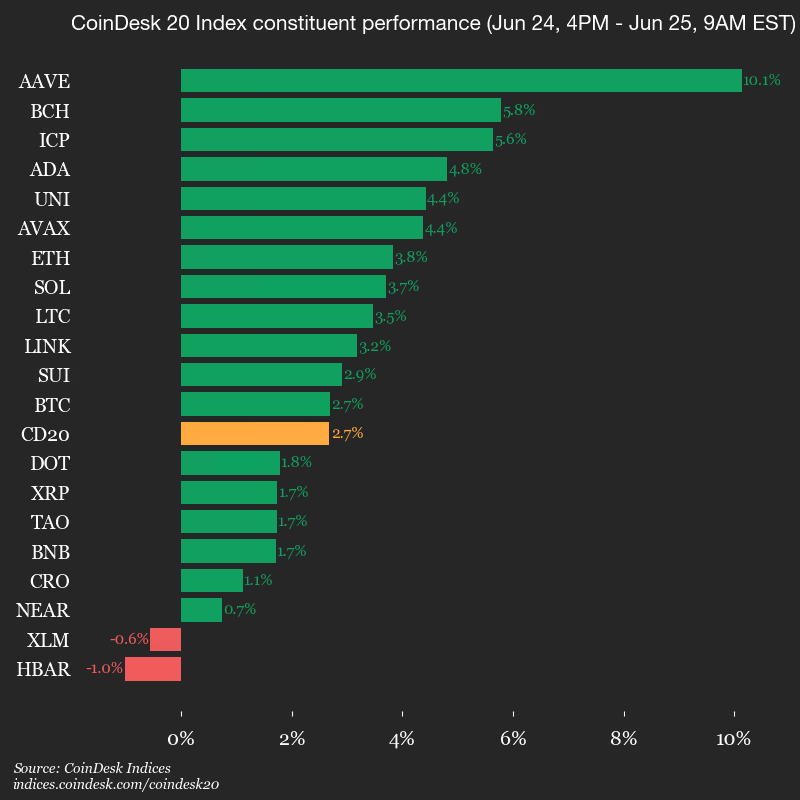

CoinDesk Indices presents its daily market update, highlighting the performance of leaders and laggards in the CoinDesk 20 Index.

The CoinDesk 20 is currently trading at 1646.0, up 2.7% (+42.96) since 4 p.m. ET on Wednesday.

Eighteen of 20 assets are trading higher.

Leaders: AAVE (+10.1%) and BCH (+5.8%).

Laggards: HBAR (-1.0%) and XLM (-0.6%).

The CoinDesk 20 is a broad-based index traded on multiple platforms in several regions globally.

Japan’s SBI Holdings has signed agreements to acquire full control of crypto exchange Bitbank through a 46.7 billion Japanese yen ($289 million) transaction, advancing a deal first disclosed in May that would create the country’s biggest crypto exchange.

On Thursday, SBI said that its wholly owned subsidiary SBICAH will acquire shares from Bitbank CEO Noriyuki Hirosue and other shareholders before subscribing to a third-party share allotment. The exchange will then buy back shares held by MIXI and Ceres, leaving SBI with 100% indirect ownership. SBI expects the transaction to close around October, subject to regulatory clearance.

The acquisition would expand SBI’s regulated crypto exchange footprint and customer base, giving it another potential distribution channel for the stablecoins, tokenized assets and onchain financial products.

Bitbank’s daily trading volume has hovered below $50 million for most of the last four months, CoinGecko data showed. Volume is dominated by the BTC/JPY pair (39.5%), followed by XRP/JPY and ETH/JPY (both at 19.7%).

SBI said combining Bitbank with SBI VC Trade would give the group about 1.1 trillion yen in assets under custody and roughly 2.92 million crypto accounts, based on figures from the end of April. The company said the combined business would rank first among Japanese crypto exchanges by assets under custody and among the largest by account numbers.

Bitbank trading volume has hovered below $50 million for most of the last four months. Source: CoinGecko

SBI builds broader digital asset ecosystem

The Bitbank deal is the latest in a series of moves by SBI to build infrastructure, including crypto trading, stablecoins and tokenized financial markets.

In February, SBI and Startale Group unveiled Strium, a layer-1 blockchain designed to support around-the-clock trading and settlement of tokenized equities and real-world assets.

Related: Circle, Nomura eye Japan corporate FX with stablecoin settlement: Report

On Wednesday, SBI and Startale launched the yen-pegged stablecoin, JPYSC. The token is issued by SBI Shinsei Trust Bank and distributed by SBI VC Trade. The stablecoin is initially limited to transfers within SBI VC Trade accounts, while public blockchain circulation will roll out after resolving outstanding legal and tax conditions, according to SBI.

The same day, Ripple and SBI Group launched the dollar-backed Ripple USD (RLUSD) stablecoin in Japan also through SBI VC Trade. At launch, RLUSD became available to institutional and retail customers after receiving approval under Japan’s regulatory framework for foreign-issued stablecoins.

Magazine: Japanese pension fund tips 1% in crypto, G7 urges action on NK hackers: Asia Express

Asked on a podcast whether XRP holders could receive equity in a Ripple public offering, Brad Garlinghouse nodded and floated a “special arrangement.” It was vague, unpromised, and electrifying to a community starved for catalysts. Here is what it could actually mean, and what it almost certainly cannot.

Summary

- Garlinghouse hinted at a possible “special arrangement” for XRP holders.

- He did not announce an IPO, a holder reward, or any concrete mechanism.

- Ripple equity and XRP remain legally separate assets.

- The most realistic benefit to XRP holders is still indirect utility, not equity.

In a June 2026 interview on the “Crypto In America” podcast, Ripple chief executive Brad Garlinghouse was asked a question the XRP community has wanted answered for years: if Ripple ever goes public, could XRP holders get a piece of it?

He did not say no. He nodded, and offered a single tantalizing phrase: that perhaps there would be a “special arrangement.”

That was the entire substance of it, four words wrapped in a maybe, with no detail, no commitment, and no timeline. And yet within hours it had rippled across XRP social media as though a promise had been made, because for a token that has spent 2026 grinding sideways near a dollar while Ripple collects institutional wins, even a hint of direct reward lands like a lightning strike.

This piece takes that hint apart: what a “special arrangement” could plausibly mean, why each version of it runs into a wall, and how a holder should read an offhand remark without getting played by it.

The honest framing matters from the start, because the gap between what was said and what was heard is the whole story. Garlinghouse described a possibility, not a plan, attached to an event, a Ripple public offering, that has not been announced and that he has repeatedly suggested is not close.

The community heard a catalyst. The reality is closer to a maybe attached to a maybe.

That does not make the question worthless, because the answer reveals a great deal about how Ripple equity and the XRP token actually relate, and about why the two keep diverging. This guide covers the moment itself, the legal wall between a company and its token, the genuine ways Ripple’s incentives align with holders, the menu of things a “special arrangement” could be, the obstacles each faces, and the framework for reading the hint with clear eyes.

The four words that lit up XRP social media

To understand why a vague phrase moved sentiment, you have to understand the state of mind it landed in.

XRP holders spent 2026 watching Ripple rack up exactly the kind of institutional milestones the community long predicted: settlements with JPMorgan, stablecoin launches with major partners, a steady drumbeat of bank deals, while the token itself stayed pinned near a dollar and change, beneath every major moving average.

That combination, corporate triumph paired with token stagnation, breeds a particular hunger: the sense that the wins are real but somehow are not reaching holders, and that some missing mechanism could finally connect the two.

Into that hunger dropped Garlinghouse’s nod and his “special arrangement,” and the phrase did what catalysts do in a starved market. It gave people something to hope for.

It helps to be precise about what was actually said, because precision is the first casualty of excitement. Garlinghouse did not announce a holder allocation. He did not describe a structure, a size, or a date.

He responded to a direct question about whether holders could gain equity by acknowledging the possibility in the softest available terms.

Days earlier, at an industry conference, he had been notably cooler on the idea of going public at all, observing that many listed crypto companies have struggled in public markets and that staying private gives Ripple more operational flexibility, while stopping short of ruling an offering out.

Put those two moments together and the picture is not a company preparing to reward token holders. It is a chief executive keeping every option open in public, declining to close a door without committing to walk through it.

The market chose to focus on the open door.

Why a public offering does not normally touch the token

The reason a holder allocation would be remarkable, rather than routine, is that an initial public offering has nothing to do with a token by default.

Ripple the company and XRP the token are legally separate things, and this is the single most important fact in the entire discussion. Ripple is a private company that sells software and payment services, signs deals with banks, holds a large treasury, and has shareholders.

XRP is a cryptocurrency that trades on its own supply and demand. Owning XRP makes you neither a shareholder nor a creditor of Ripple; it gives you no claim on the company’s profits, assets, or equity.

When a company goes public, it sells shares to investors, and the people rewarded are the holders of those shares, the existing equity owners, employees with stock, and early backers. Token holders are simply not part of that transaction, because they own a different asset entirely.

This is why a token is not company equity. A token can be associated with a company, used by a network, and held by that company, but it does not automatically become a claim on the company’s cap table.

This separation is not a technicality Ripple could wave away if it wanted to; it is the structure that governs everything. It is also exactly why XRP has spent the year failing to rally on Ripple’s corporate wins: the market, correctly, prices Ripple’s success as accruing first to Ripple, and only indirectly and slowly to the token.

A public offering would be the purest expression of that disconnect, a moment when Ripple converts its corporate value into tradeable equity for equity holders, with XRP holders watching from outside the deal.

So when Garlinghouse floats a “special arrangement,” he is gesturing at something that would deliberately break the normal pattern, a way to route some benefit of an equity event to holders of a non-equity asset.

That is a genuinely unusual thing to propose, which is part of why the phrase drew so much attention, and also why it deserves hard scrutiny instead of celebration.

The case that Ripple’s incentives already align with holders

Before dismissing the hint as empty, it is worth taking seriously the strongest version of the bullish argument, because it has real merit.

Garlinghouse and many in the community make the point that Ripple’s interests and XRP holders’ interests are already aligned, even without any special mechanism, because Ripple is the largest single holder of XRP in the world.

The company keeps an enormous quantity of the token, much of it in escrow, which means Ripple profits when XRP rises in exactly the way ordinary holders do. Whatever raises the price of XRP raises the value of Ripple’s own holdings.

This alignment is not imaginary, and it should not be dismissed as spin. Ripple’s actual day-to-day work, the partnerships, the payment integrations, the institutional adoption of its ledger and its stablecoin, plausibly increases XRP’s long-term utility and demand, which is a real if indirect benefit to anyone holding the token.

A holder is, in a loose sense, riding alongside the largest XRP whale on earth, one with deep pockets and a decade-long commitment to making the asset useful. That is a meaningful thing to have on your side.

But notice the precise shape of the benefit: it is indirect, gradual, and conditional on Ripple’s broader strategy actually translating into token demand, which, as 2026 has shown, is far from automatic.

That is why Ripple’s wins do not move XRP. The company can succeed, the ledger can gain credibility, and XRP can still wait for direct demand.

Alignment of incentives is not the same as a payment. “Ripple wants XRP to go up” is a very different proposition from “Ripple will hand XRP holders a slice of its IPO.”

The first is structural and real. The second is the speculative leap the “special arrangement” comment invites.

What a “special arrangement” could actually look like

So what could Garlinghouse plausibly mean?

Since he gave no detail, the honest approach is to map the realistic possibilities and weigh each, treating them as a menu of speculation rather than a forecast.

The most direct version would be some form of allocation to holders: a mechanism by which verified XRP holders receive shares, or the right to buy shares, in a Ripple offering, perhaps proportional to holdings. This is the version the community dreams of, because it would convert XRP ownership into a claim on Ripple equity, the very link that does not currently exist.

A softer variant would be priority access instead of free equity, letting XRP holders into an offering ahead of the general public, a perk without a giveaway.

Other versions stay within the token world instead of crossing into equity. Ripple could, in principle, pair any public listing with a token-side reward, an airdrop of XRP or of a new instrument to holders, timed to the event, which would sidestep the thorniest securities problems of distributing actual shares.

It could create a loyalty or staking-style program that rewards long-term holders around the listing. Or “special arrangement” could be far more modest than any of this, a governance gesture, a symbolic recognition, or simply Ripple structuring its business so that more value flows through XRP over time.

The range is enormous precisely because the phrase was empty, stretching from a genuine equity allocation at one end to a vague promise of goodwill at the other.

The community heard the first. Sober reading has to consider that the truth, if there is one at all, could sit anywhere along that spectrum, and that the most dramatic interpretations are also the least likely.

Why each version runs into a wall

The reason to temper expectations is that almost every concrete version of a “special arrangement” collides with serious obstacles, which is likely why Garlinghouse spoke in hints instead of specifics.

Distributing actual equity to XRP holders would be a securities and compliance nightmare. XRP holders number in the tens of millions, scattered across the globe in every regulatory jurisdiction imaginable, many anonymous, many in countries where Ripple cannot easily offer securities at all.

Identifying who qualifies, verifying them, and distributing shares in compliance with the securities laws of dozens of nations would be staggeringly complex. An offering is already one of the most heavily regulated events a company undertakes, and layering a novel token-holder allocation on top invites exactly the kind of legal risk that underwriters and regulators recoil from.

Token-side rewards avoid the equity problem but introduce others. An airdrop to holders raises its own securities questions in some jurisdictions and does nothing to address the fundamental issue that the token and the company remain separate.

Priority access to an offering is more feasible but far less exciting, and even that requires a workable, compliant way to identify genuine holders.

Fairness is another wall. Any arrangement that rewards holders as of a certain date invites accusations of favoring insiders or enabling gaming, and Ripple has spent years cultivating a reputation for regulatory caution it would be loath to jeopardize.

There is also a simple precedent vacuum. No major company has paired a public offering with a direct reward to holders of a separate, associated token, because the structure is awkward, legally fraught, and of uncertain benefit to the company doing it.

The absence of precedent is not proof it cannot happen. But it is a strong signal that “special arrangement” is far easier to say into a microphone than to build into a deal.

The catalyst-stack problem: not all catalysts are equal

The “special arrangement” comment is best understood as one entry in a larger habit, the tendency of the XRP community to treat every Ripple-related signal as part of a single, accumulating stack of catalysts that will eventually send the token higher.

In that mental model, a settlement with JPMorgan, an ETF inflow, a favorable regulatory development, and a hint about an IPO reward all get tossed into the same bucket labeled “reasons XRP will moon.”

The problem is that the items in that bucket are not equal, and treating them as interchangeable is how holders end up disappointed when the price does not respond the way the headline count suggests it should.

The useful distinction is between observable catalysts and speculative ones. CLARITY Act passage, ETF inflows, exchange-reserve changes, and real settlement volume are observable: they either happen or they do not, and when they happen they can be measured and priced.

A possible reward attached to a possible public offering is a different category entirely. It is a speculative possibility layered on a corporate decision that has not been made, with no structure, no size, and no date.

That is why where real XRP demand comes from matters more than IPO speculation. ETF inflows, exchange reserves, and actual XRP usage are measurable; a possible arrangement is not.

Stacking that on top of observable catalysts as though it carries equal weight inflates the apparent bull case without adding anything solid to it.

The discipline that protects a holder is to sort the stack honestly: give real weight to things that are happening and can be tracked, and treat a hint about an unannounced arrangement tied to an unannounced offering as what it is, a low-probability, high-uncertainty maybe that belongs at the very bottom of the pile, not the top.

Why Ripple may stay private anyway

There is a further reason to keep the hint in perspective, and it sits one level up: the public offering the “special arrangement” is attached to may not happen any time soon.

Garlinghouse has been openly ambivalent about going public, noting that staying private gives Ripple operational flexibility and pointing out that many crypto companies have not fared well in public markets.

He has said plainly that an offering is not something happening very soon, even while declining to rule it out. Ripple is also not a company under pressure to list: it is well capitalized, profitable in its core business, and sitting on a large XRP treasury, which removes the usual urgency that pushes firms toward public markets to raise cash.

This is the part the excitement tends to skip. A reward to holders is conditional on an offering, and the offering itself is uncertain, which makes the reward doubly contingent.

If Ripple chooses to stay private for years, as its chief executive’s comments suggest is entirely possible, then the “special arrangement” remains permanently hypothetical, a thing that could only exist alongside an event that may never come in the form imagined.

Even in the bullish scenario where Ripple does eventually list, the company would face every obstacle described above when deciding whether to build a holder mechanism. The path of least resistance for any firm going public is the conventional one that rewards equity holders and leaves token holders out.

None of this means Ripple will never reward holders. It means the hint sits behind two locked doors, an uncertain offering and an uncertain mechanism, and a holder banking on both opening is betting on a long chain of maybes.

The deeper reason the equity-token wall exists

It is worth pausing on why the separation between Ripple equity and XRP is so firm, because the community often treats it as an inconvenience Ripple could simply choose to overcome, when in fact it is a protective firewall that serves XRP holders even as it frustrates them.

The wall is not an accident of paperwork. It is the product of years of legal struggle, and dismantling it casually could undo the very thing that makes XRP investable today.

Recall that XRP spent years under a cloud because regulators argued it was an unregistered security, a claim that turned on whether buying the token amounted to investing in Ripple’s efforts and expecting profit from them.

The token’s hard-won legal clarity rests precisely on the finding that XRP, as traded on public exchanges, is not a stake in Ripple. The distance between the company and the token is what lets XRP be treated as a commodity instead of a security.

Now consider what a direct equity link would do to that settlement. If Ripple created a mechanism that tied XRP ownership to a claim on the company’s equity or profits, it would be handing regulators a fresh argument that the token is, after all, a security, an investment in Ripple’s success with an expectation of profit from the company’s efforts.

The arrangement the community dreams of could, in the worst case, drag XRP back toward the exact classification it just escaped, with all the trading restrictions and institutional hesitancy that status carries.

This is the paradox buried in the “special arrangement” hope: the cleanest way to reward holders, by linking the token to the company, is also the way most likely to damage the token’s legal standing.

That is why the catalyst that could codify XRP’s status matters more than a speculative equity link. Legal certainty is valuable precisely because it keeps XRP out of the securities bucket.

It helps explain why Ripple, a company famous for its regulatory caution, would speak only in vague hints rather than concrete plans. A real equity link is not just operationally hard; it is legally hazardous to the asset it would be meant to reward.

This is why the indirect alignment described earlier is not a consolation prize but, in a sense, the safer form of benefit. Ripple driving XRP’s utility and value through its business activity raises the token without making it a security, because the gains come from the token’s own usefulness and demand, not from a contractual claim on the company.

A holder who understands this should be careful what they wish for. The firewall that keeps Ripple’s wins from flowing directly into the token is the same firewall that keeps XRP a commodity, and a “special arrangement” clever enough to breach one might breach the other.

The most valuable thing Ripple can do for holders may be exactly what it is already doing, building utility around the token. The least valuable, or even harmful, may be the dramatic equity link the hint seemed to dangle.

How to read the hint without getting played

The way to handle a moment like this is to separate sentiment from substance, because the two move on very different timescales.

As sentiment, the “special arrangement” comment is genuinely meaningful: it shows Ripple’s chief executive is aware of holder frustration, willing to gesture toward addressing it, and keen to keep the community engaged, all of which matter for a token whose price is heavily driven by community conviction.

A hint like this can move sentiment and short-term price action regardless of whether anything concrete ever follows, and a trader watching narrative flows should not ignore it.

But sentiment is not the same as a plan, and confusing the two is the trap.

As substance, the honest reading is that almost nothing has changed. There is still no public offering announced, no holder mechanism designed, no legal pathway cleared, and no commitment made, only a chief executive declining to close a door while standing well back from it.

For the hint to become real, a holder would need to see two concrete things follow: an actual decision by Ripple to go public, with a filing and a timeline, and then an actual, structured mechanism for involving holders that survives the securities, fairness, and practicality obstacles laid out here.

Until both exist, “special arrangement” is a phrase, not a payout.

The disciplined position is to enjoy the signal for what it reveals about Ripple’s posture toward its community, to give it appropriate, which is to say minimal, weight in any view of XRP’s actual prospects, and to keep one’s attention on the observable catalysts that truly move the token.

The community heard a promise. What Garlinghouse offered was a maybe, and the difference is everything.

Frequently asked questions

What did Garlinghouse actually say about XRP holders and a Ripple IPO?

On a June 2026 podcast, asked whether XRP holders could gain equity if Ripple went public, Brad Garlinghouse nodded and said perhaps there would be a “special arrangement.” That was the full substance: a vague acknowledgment of a possibility, with no structure, size, or timeline attached. Days earlier, at an industry conference, he had been cooler on going public at all, saying staying private gives Ripple flexibility. So the remark was a hint, not a plan or a promise.

Would a Ripple IPO normally benefit XRP holders?

No, not by default. Ripple the company and XRP the token are legally separate. A public offering sells shares and rewards equity holders, employees, and early investors, while XRP holders own a different asset with no claim on Ripple’s equity or profits. This is exactly why XRP has not rallied on Ripple’s institutional wins through 2026: the market prices those wins as accruing to the company first, and only indirectly to the token. A holder reward would be a deliberate break from the normal structure.

What could a “special arrangement” actually be?

Since Garlinghouse gave no detail, the possibilities range widely. The most dramatic would be allocating shares, or the right to buy shares, to verified XRP holders. Softer versions include priority access to an offering, a token-side airdrop timed to a listing, or a loyalty program for long-term holders. The most modest reading is a symbolic gesture or simply structuring Ripple’s business so more value flows through XRP over time. The community assumes the dramatic version, but the truth, if any, could sit anywhere on that spectrum.

Why might a holder reward be hard to deliver?

Distributing actual equity to tens of millions of anonymous, globally scattered XRP holders would be a securities and compliance nightmare across dozens of jurisdictions, layered on top of an already heavily regulated offering. Token-side airdrops raise their own legal questions and do not bridge the company-token gap. Any holder-as-of-a-date reward invites fairness and gaming concerns. There is also little precedent for pairing a public offering with a reward to holders of a separate token, which signals how awkward the structure is in practice.

Is Ripple even going public soon?

Probably not soon, by Garlinghouse’s own account. He has said an offering is not something happening very soon and has emphasized that remaining private gives Ripple operational flexibility, noting that many public crypto companies have underperformed. Ripple is well capitalized and profitable in its core business and holds a large XRP treasury, so it faces little pressure to raise cash through a listing. Because any holder reward is conditional on an offering, an uncertain offering makes the reward doubly contingent.

How should XRP holders treat this hint?

Separate sentiment from substance. As sentiment, the comment matters: it shows Ripple is aware of holder frustration and wants to keep the community engaged, which can move short-term sentiment. As substance, almost nothing has changed, since there is no announced offering, no designed mechanism, and no commitment. For the hint to become real, a holder would need an actual decision to go public and an actual, compliant holder mechanism to follow. Until both exist, it is a phrase, not a payout, and deserves minimal weight.

This article is information, not investment advice. It concerns speculative, unannounced possibilities, and corporate plans, statements, and market conditions can change. Prices and details reflect reporting available as of June 25, 2026. Verify current information with official sources before relying on anything described here.

Partnership targets a key adoption gap: connecting on-chain custody with funding rails

On-chain self-custody remains one of crypto’s defining value propositions, but it often runs into a practical problem: getting funds in and out smoothly. This is the gap a new partnership between stablecoin infrastructure provider Noah and self-custody wallet startup Bron is attempting to narrow.

Both companies announced they are integrating Noah’s stablecoin on- and off-ramp capabilities into the user experience around Bron’s non-custodial wallet. The goal, according to the companies, is to make it easier for users to fund their self-custody wallets with stablecoins and to withdraw back when needed, while keeping the wallet’s security model intact.

Noah brings stablecoin rails, Bron focuses on MPC security

Noah describes its role as payments infrastructure for fintechs, exchanges, marketplaces, and other businesses operating across jurisdictions. The company says its platform supports account issuance, settlement, and global payouts, and that it is used for stablecoin-based money movement through blockchain payment rails.

Bron, meanwhile, positions its wallet as non-custodial and built on multi-party computation (MPC). In the company’s model, the wallet is designed to eliminate seed phrases and reduce single points of failure. The announcement outlines a three-party MPC architecture for transaction authorization, with separate cryptographic components distributed across the user’s device, Bron’s platform, and an independent third party selected by the user for recovery. Bron says no single party can reconstruct signing material or initiate transactions unilaterally.

What the integration changes for users

The companies say the integration will enable Bron users to access “seamless” stablecoin on- and off-ramp functions powered by Noah’s network. In practical terms, the addition is aimed at streamlining the steps involved when a user wants to move from traditional money sources into stablecoins, then into self-custody, or do the reverse for withdrawals.

For high-net-worth individuals and other users who transact across markets, stablecoins can serve as a bridge between different currencies and payment environments. Noah’s stated emphasis is on enabling virtual accounts for dollar origination and payouts across international jurisdictions, which aligns with broader industry patterns where stablecoins are increasingly used for remittances, cross-border transfers, and other time-sensitive value movement use cases.

The companies also frame the partnership as a way to reduce friction between conventional financial infrastructure and self-custody experiences. That positioning reflects a recurring theme in crypto payments: security and ownership models can be compelling, but mainstream adoption depends on smoother rails, clearer compliance workflows, and fewer operational steps for end users.

Why stablecoin rails plus self-custody is gaining attention

Stablecoins have evolved from speculative instruments into infrastructure for real payments and treasury activity. Industry participants frequently point to stability relative to major fiat currencies, faster settlement compared with legacy systems, and programmability on public blockchains as reasons for adoption.

However, stablecoin usage often still depends on off-chain connections to regulated entities. On-ramps and off-ramps are one of the most important interfaces in that chain, because users typically need compliant ways to convert fiat into digital assets and back. Meanwhile, self-custody wallets emphasize user control and cryptographic safeguards, but they can be harder to use if funding and withdrawal paths are fragmented.

By combining Noah’s on/off-ramp infrastructure with Bron’s MPC-based wallet design, the companies are effectively trying to address two sides of the same problem: access and control. The integration does not change the underlying custody model described by Bron, which remains non-custodial and centered on MPC authorization and recovery mechanics, according to the announcement.

Institutional-style security claims, and the compliance question

Both companies highlight trust and security. Bron emphasizes protections such as delayed transfer features, hidden vault concepts, biometric authentication, and guardian-based recovery mechanisms, in addition to its MPC approach. Noah’s role, as described, is tied to regulated infrastructure for money movement and partner services.

What remains unclear from the announcement is the depth of integration at the product and jurisdiction levels. For example, on- and off-ramp availability can vary depending on local regulations, user verification requirements, and partner routing. The companies do not provide a list of supported countries, token types beyond stablecoins generally, or integration timelines beyond the partnership announcement date.

For users and enterprise partners evaluating similar deployments, the operational details are typically as important as the cryptography. Stablecoin onboarding, withdrawal timing, fee structures, and compliance controls can determine whether the “frictionless” promise translates into a consistent experience.

Industry implications: fewer steps to custody, potentially wider participation

If the integration performs as intended, it could make self-custody more accessible for users who do not want to rely on exchange custody. It also fits a broader market direction where wallet providers increasingly partner with payment and compliance layers, rather than trying to build end-to-end fiat connectivity themselves.

At the same time, the partnership illustrates how stablecoin infrastructure is becoming a core layer for crypto user journeys. As stablecoins are used more frequently in payments and cross-border value transfers, the companies that control the user-facing rails, whether through APIs, checkout flows, or treasury payouts, may play outsized roles in mainstream adoption.

What’s next

Noah and Bron framed the partnership as a step toward connecting traditional finance infrastructure with secure self-custody, without compromising on the ownership model the wallet is designed around. For the market, the key question will be practical: whether the integrated on- and off-ramp experience is consistent across jurisdictions and whether it meaningfully reduces the operational burden for users.

As stablecoin adoption continues to expand beyond trading, integrations like this one signal a shift toward complete user journeys, from onboarding through custody and onward to withdrawals, rather than treating each stage as a separate product.

Crypto World

Wendy’s shares soar for a second day as retail investors pile into their new meme darling

A Wendy’s restaurant sign is seen on Nov. 10, 2025 in Austin, Texas.

Brandon Bell | Getty Images

Wendy’s shares extended their rally for a second day on Thursday, as retail traders continued piling into the heavily shorted fast-food chain.

Shares surged another 12% in premarket after a 25.7% gain in the previous session, their biggest advance since June 2021. The rally appeared largely disconnected from company fundamentals and instead reflected a burst of social-media enthusiasm that has transformed Wendy’s into the latest meme-stock favorite.

“Reddit crowd hijacks stock,” Don Bilson, head of event-driven research at Gordon Haskett, wrote in a note.

“GameStop is inarguably the OG of meme stocks. It earned that distinction during Covid and credit for this is owed to the army of apes that get their marching orders from Reddit’s WallStreetBets thread,” Bilson said. “This army happens to be on the move again this morning outside of Columbus, Ohio. That is where Wendy’s makes its home and its stock.”

The rally began Wednesday after Wendy’s announced the appointment of former Potbelly executive Steven Cirulis as chief financial officer and chief strategy officer.

Traders on Reddit forums increasingly portrayed Wendy’s as a company worth “saving” after years of stock-market underperformance. One widely shared WallStreetBets post titled “We need to save Wendy’s” and urged fellow traders to rally behind the restaurant chain.

Vanda Research flagged Wendy’s as the most extreme case of abnormal retail buying on Thursday, with net purchases running more than seven times recent norms after a viral “Save Wendy’s” campaign swept through Reddit trading communities.

One Reddit user posted a screenshot showing a roughly $350,000 position in Wendy’s stock under the headline “$WEN to the moon – 350K YOLO,” drawing hundreds of comments and upvotes from fellow traders. Another post featured a meme image encouraging investors to “pump those numbers up,” joking that buying only one meal’s worth of Wendy’s stock amounted to “rookie numbers.”

— CNBC’s Nick Wells and Michael Bloom contributed reporting.

Jiang Zhuoer, co-founder of BTC.TOP mining pool, on June 25 published a long-term prediction for Bitcoin (BTC), saying it could bottom between $42,000 and $44,000 sometime in the October-to-December 2026 window.

Jiang made the call while the OG cryptocurrency was trading near $62,000, down about 51% from its all-time high above $126,000, which was set in October 2025.

MSTR Sentiment May Lead to the Next Bitcoin Bottom

According to the miner, Strategy’s mNAV ratio, which compares its share price with the value of its BTC holdings per share, has entered the same range seen during the previous bear market. An mNAV reading above 1 suggests that investors are paying a premium, while a figure below 1 means there’s pessimism brewing.

Per Jiang’s assessment, that metric has fallen to 0.72, very close to the 0.70 level recorded in May 2022. He argued that the current reading may signal a sentiment low for Strategy investors, although not necessarily for Bitcoin itself.

When mNAV bottomed in May 2022, as the analyst explained, BTC was trading near $31,000 and went on to reach a cycle low six months later when it dropped to around $15,000. If that same lag applies now, Jiang postulated that the flagship crypto will reach a low in Q4 2026, with prices falling to roughly $42,000 to $44,000.

His prediction also relied on a 4-year market model that compares Bitcoin’s long-term price swings to a bouncing ball, where each bounce results in the loss of amplitude. According to the model, as BTC’s total market cap grows, its volatility naturally decreases cycle by cycle.

Strategy MSTR stock recently fell to its lowest level since February 2024, and was changing hands at just above $94 at the time of writing. Meanwhile, the company’s preferred STRC shares have also been trading below their par value of $100, with data from the firm showing it stood at $80.84, and this, Jiang says, has also contributed to the current market stress, with other analysts suggesting it could pressure Strategy to sell some of its Bitcoin.

Market Context Around Jiang’s Call

Bitcoin’s current weakness is not hard to see in the data, with Santiment noting earlier today that wallets holding between 10 and 10,000 BTC had dumped 45,074 coins over an 8-day period, helping push the asset below $60,000 for the first time since October 2024. CoinGlass data showed nearly $416 million in Bitcoin liquidations in the last day, with long positions accounting for more than $319 million.

Analyst Wise Crypto described the move as a leverage flush, with more than 175,000 traders affected when BTC briefly touched $59,000. The asset has since made some recovery from that dip and was trading close to $62,000 at press time, although it was still down about 4% in the last week and almost 20% over the past month.

Meanwhile, another market watcher, Ali Martinez, flagged that the Coinbase Premium Index has been negative for 46 straight days. The metric compares the price of Bitcoin on Coinbase with offshore exchanges, with a negative reading suggesting weaker demand from American investors and institutions.

The post Prediction: Bitcoin Could Bottom Between $42K and $44K This Year appeared first on CryptoPotato.

Chile! Claressa Shields Speaks On Papoose’s Whereabouts & Some Folks Are Dragging Remy Ma Into It (VIDEO)

STAY ALERT: EUROPE JUST NUKED CRYPTO! XRP HOLDERS PLEASE LISTEN

Best watch deals this Amazon Prime Day, found by a fashion writer

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment5 days ago

Entertainment5 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports2 days ago

Sports2 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech3 days ago

Tech3 days agoMicrosoft accidentally kills epic Outlook email threads

-

Business5 days ago

Business5 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics5 days ago

Politics5 days agoAndy Burnham and the meaning of Makerfield

-

Crypto World1 day ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Politics7 days ago

Politics7 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Crypto World1 day ago

Crypto World1 day agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business2 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

NewsBeat6 days ago

NewsBeat6 days agoKeir Starmer Allies Question His Chances For No 10

-

Business5 days ago

Business5 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Crypto World5 days ago

Crypto World5 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Tech7 days ago

Tech7 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World5 days ago

Crypto World5 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World5 days ago

Crypto World5 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Entertainment5 days ago

Entertainment5 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech4 days ago

Tech4 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Tech3 days ago

Tech3 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Sports7 days ago

Sports7 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

You must be logged in to post a comment Login