Crypto World

Wendy’s shares soar for a second day as retail investors pile into their new meme darling

A Wendy’s restaurant sign is seen on Nov. 10, 2025 in Austin, Texas.

Brandon Bell | Getty Images

Wendy’s shares extended their rally for a second day on Thursday, as retail traders continued piling into the heavily shorted fast-food chain.

Shares surged another 12% in premarket after a 25.7% gain in the previous session, their biggest advance since June 2021. The rally appeared largely disconnected from company fundamentals and instead reflected a burst of social-media enthusiasm that has transformed Wendy’s into the latest meme-stock favorite.

“Reddit crowd hijacks stock,” Don Bilson, head of event-driven research at Gordon Haskett, wrote in a note.

“GameStop is inarguably the OG of meme stocks. It earned that distinction during Covid and credit for this is owed to the army of apes that get their marching orders from Reddit’s WallStreetBets thread,” Bilson said. “This army happens to be on the move again this morning outside of Columbus, Ohio. That is where Wendy’s makes its home and its stock.”

The rally began Wednesday after Wendy’s announced the appointment of former Potbelly executive Steven Cirulis as chief financial officer and chief strategy officer.

Traders on Reddit forums increasingly portrayed Wendy’s as a company worth “saving” after years of stock-market underperformance. One widely shared WallStreetBets post titled “We need to save Wendy’s” and urged fellow traders to rally behind the restaurant chain.

Vanda Research flagged Wendy’s as the most extreme case of abnormal retail buying on Thursday, with net purchases running more than seven times recent norms after a viral “Save Wendy’s” campaign swept through Reddit trading communities.

One Reddit user posted a screenshot showing a roughly $350,000 position in Wendy’s stock under the headline “$WEN to the moon – 350K YOLO,” drawing hundreds of comments and upvotes from fellow traders. Another post featured a meme image encouraging investors to “pump those numbers up,” joking that buying only one meal’s worth of Wendy’s stock amounted to “rookie numbers.”

— CNBC’s Nick Wells and Michael Bloom contributed reporting.

Ripple’s token is showing signs of stabilization after the sharp decline from higher levels, but the recovery remains limited by a series of resistance zones that continue to attract sellers. While buyers have defended the recent lows, the market still needs a clear structural breakout before a stronger upside move can be considered.

Ripple Price Analysis: The Daily Chart

On the daily timeframe, XRP continues to trade inside a broader descending channel that has shaped the price action for months. The recent rebound from the $1.02 to $1.04 demand zone has helped the asset recover, but the move has not yet changed the larger bearish structure.

The main challenge for buyers remains the $1.17 to $1.2 supply zone, which sits near the upper boundary of the descending channel. A successful breakout above this region could open the path toward the next resistance area around $1.28. However, as long as XRP remains below this level, the current recovery may still represent a corrective move within the broader downtrend.

A rejection from the current resistance area could send the price back toward the $1.05 to $1.07 support region, while a deeper decline would bring the $1.02 to $1.04 buyers’ base back into focus.

XRP/USDT 4-Hour Chart

The 4-hour chart highlights the ongoing struggle between buyers attempting to build a base and sellers defending the overhead supply. XRP recently pushed toward the $1.16 to $1.18 resistance zone but failed to secure a breakout, keeping the short-term structure vulnerable.

The $1.16 – $1.18 supply range remains an important barrier, with price action still showing difficulty reclaiming the area above it. Until the asset breaks above this price region and confirms strength above it, upside attempts may continue to face selling pressure.

On the downside, the ascending wedge’s lower trendline remains the key support area. Holding above this zone would preserve the possibility of another recovery attempt, while a breakdown below it would weaken the current setup and increase the risk of further downside.

The post Ripple Price Analysis: XRP Could Be Heading for a Major Move Next Week appeared first on CryptoPotato.

After staging an impressive rebound from its local bottom, Ethereum is beginning to test increasingly important resistance levels. The coming sessions should provide more clarity on whether this recovery has enough momentum to continue.

Ethereum Price Analysis: The Daily Chart

The daily chart shows ETH holding above the previously broken descending trendline, confirming that the medium-term structure has improved compared to the aggressive selloff seen in June. Following the breakout, the market has successfully established a sequence of higher highs and higher lows while consolidating above the $1.76K to $1.82K support region.

However, the recovery is now approaching a major technical barrier. The $1.88K to $1.91K supply zone is acting as the first resistance, while the declining 100-day moving average sits just overhead near the $1.95K area. This creates a confluence of resistance that could cap the current rally before ETH attempts to challenge the broader long-term supply zone between roughly $2K and $2.15K.

As long as the price remains above the $1.76K to $1.82K support, buyers maintain the short-term advantage. Losing that area, however, would expose the next support around $1.55K to $1.64K and weaken the current bullish structure.

ETH/USDT 4-Hour Chart

On the 4-hour timeframe, Ethereum has slipped slightly below the ascending trendline that had guided the recovery throughout July. While the break is not yet decisive, it signals that bullish momentum is beginning to weaken as the price trades inside the $1.88K to $1.91K supply zone. The current structure suggests that buyers are losing some control after failing to extend the recent rally.

If ETH remains below the broken trendline, the move could evolve into a deeper retracement toward the notable demand zone around $1.76K to $1.79K, where buyers would be expected to step in. Conversely, reclaiming the trendline and securing a breakout above the $1.88K to $1.91K resistance would invalidate the short-term weakness and increase the probability of another push toward the $1.95K to $2K region.

Sentiment Analysis

The one-month Binance ETH liquidation heatmap shows a substantial concentration of liquidity around the $1.5K level. Although Ethereum is currently trading well above that region, this cluster remains an important magnet from a derivatives perspective.

If the current rally loses momentum and sellers regain control, a deeper correction toward the $1.5K liquidity pocket could attract price as leveraged long positions are unwound.

Such a move would likely coincide with a break below the key technical supports visible on the chart. Until then, the prevailing structure remains constructive, but the presence of this large liquidity cluster highlights that downside risk has not completely disappeared despite the recent recovery.

The post Ethereum Price Analysis: ETH Hits a Decision Point as Major Resistance Comes Into Play appeared first on CryptoPotato.

Dormant Bitcoin activity fell to its lowest level since Q3 2022, suggesting long-term holders have slowed distribution after heavy profit-taking.

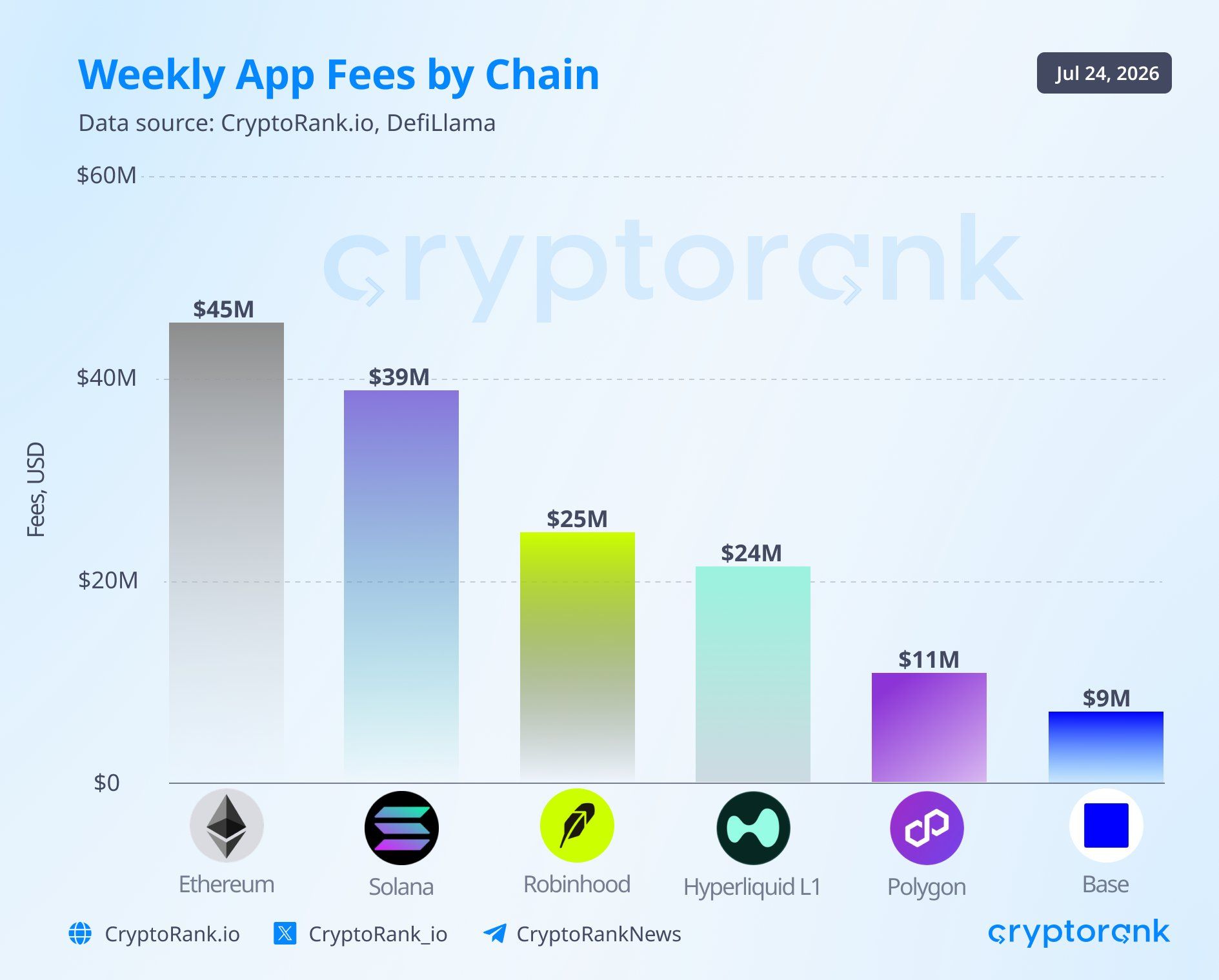

Robinhood Chain ranked 3rd by weekly application fees in the week ending July 24. Meme coins and tokenized assets trade side by side on the 4-week-old network.

Now Robinhood is pushing deeper into prediction markets, widening its bets across 3 crypto sectors.

Fees Hit $25 Million as Meme Coins Outpace the RWA Pitch

Applications on Robinhood Chain generated $25 million in fees over the week ending July 24. Only Ethereum (ETH) at $45 million and Solana (SOL) at $39 million ranked higher, per CryptoRank.

“Robinhood Chain’s third-place position makes it one of the strongest blockchain launches in recent years,” CryptoRank said.

Follow us on X to get the latest news as it happens

Robinhood built a layer-2 network for tokenized real-world assets (RWA). Recent activity shows a different mix. According to data from Dune, Cash Cat (CASHCAT) ranks first among the top traded tokens on the network.

The meme coin has logged $824.89 million in lifetime volume across 1.37 million trades. Tokenized assets are growing, too, though rarely on their own.

Daily RWA trading peaked at $61.1 million on July 23. Meme coin and tokenized stock pairs supplied $46.1 million, or about 75%.

The chain’s tokenized asset base also grew. The total RWA value on the chain climbed to $25.4 million on July 24, the highest since launch. Tokenized stocks made up $21.9 million.

Prediction Markets Sit Off the Chain

As meme coin and RWA trading grow, Robinhood is also pushing deeper into prediction markets in its app. The Journal reported that Robinhood is in talks with Crypto.com. A partnership would let users trade the exchange’s yes-or-no contracts on Robinhood’s trading platform.

Robinhood began carrying Kalshi contracts in early 2025. Its partners also include ForecastEx, owned by Interactive Brokers, and Rothera. Robinhood runs Rothera through a joint venture with Susquehanna International Group.

Robinhood said it will keep working with several exchanges. No agreement with Crypto.com has been reached, and the talks may not produce one.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Robinhood Bets on 3 Crypto Sectors as Blockchain Fees Hit $25 Million appeared first on BeInCrypto.

The U.S. Commodity Futures Trading Commission, which has claimed a role as the leading regulator of prediction markets firms run by companies such as Kalshi, Coinbase, Polymarket and Crypto.com, issued an advisory on Friday reminding the businesses that they shouldn’t cut corners with far-ranging contract certifications meant to encompass a wide array of events.

The agency said that “broad, template-style certifications should not be submitted,” marking the second time in recent months that the regulator has had to warn about overly generalized submissions.

Many of the “designated contract markets” regulated by the CFTC “continue to self-certify event contracts” (in other words, prediction market contracts) as broad templates “without supplying the terms and conditions of each proposed permutation and a concise explanation and analysis with respect to the product’s terms and conditions, the underlying commodity, and the product’s compliance,” the agency said.

The regulator said skirting the process can undermine its ability to work out whether the firm “has supplied all information, explanation and analysis required” and has “adequately evaluated the settlement methodology, data sources, and core-principles compliance of all permutations of the contract.”

The US and Iran both stopped their strikes, ending 13 consecutive nights of American bombing and leaving crypto traders holding the only liquid read on the pause.

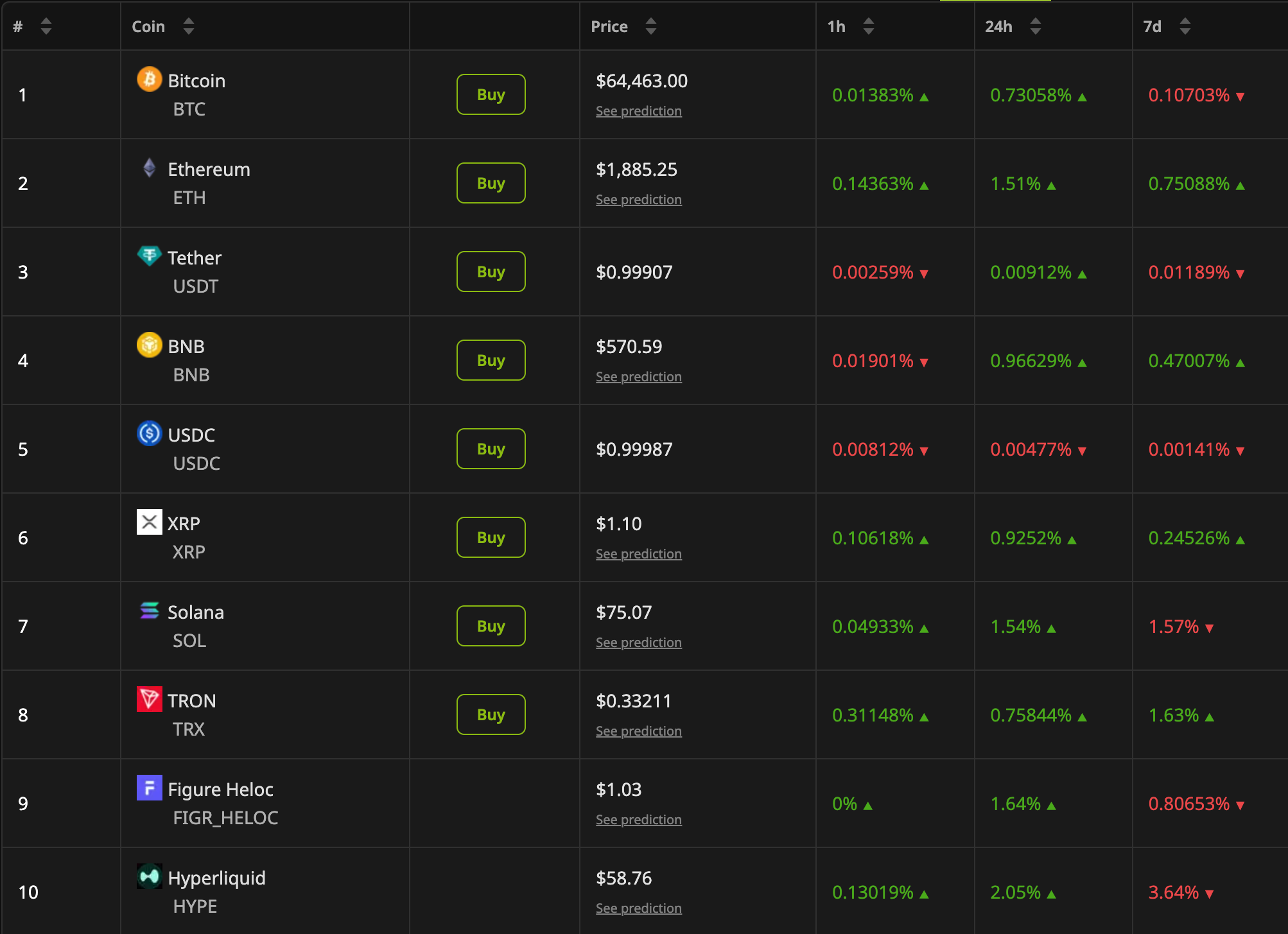

Bitcoin (BTC) traded near $64,463 on Sunday, up 0.7% over the past 24 hours, while the 10 largest digital assets posted modest gains. Oil and equity markets, however, closed before the strikes stopped.

US and Iran Pause Strikes

AP reported that the US paused its airstrikes on Friday after nearly two weeks of intensifying attacks. A US Department of Defense source told CNN that operations were on hold.

Iran has also stated that strikes on Gulf states and US interests in the region would be halted. Army spokesman, Amir Akraminia, confirmed it on Sunday.

“Our strategy has essentially been retaliatory, we have also halted our retaliatory operations,” Akraminia said.

The New York Times reported that Trump shelved plans for a broader campaign due to dwindling US air defense supplies. CNN noted that Gen. Dan Caine flagged concerns about munitions stockpiles.

Despite the de-escalation, it remains a pause rather than a formal ceasefire. US Central Command (CENTCOM) confirmed that its naval blockade of Iranian ports remains in place.

Follow us on X to get the latest news as it happens

Why Monday’s Asian Open Matters

Brent crude fell about 4% Friday to roughly $96.7. The benchmark had closed above $100 on Thursday for the first time since May.

Crypto, therefore, absorbed the weekend headlines alone. Total market capitalization reached $2.29 trillion on Sunday, up 0.84% over 24 hours.

Trading resumes on Monday, and the first prints will carry three days of news. Oil sets the direction for risk assets from there.

Higher crude lifts inflation expectations, which, in turn, shape the Federal Reserve’s policy and appetite for risk.

Analysts have warned against reading too much into a short lull. Michael Singh of the Washington Institute for Near East Policy told AP that duration is what matters.

“If it turns into a multiday pause, that’ll be something significant,” he said.

Houthi attacks in the Red Sea remain a second source of pressure on crude. The June ceasefire has not returned, and traffic through the strait remains halted. Monday’s crude open will show whether traders treat the pause as durable or as an operational gap.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post US and Iran Pause Strikes as Markets Wait for Monday’s Verdict appeared first on BeInCrypto.

KB Kookmin Bank will launch a blockchain-based cross-border payment service for import and export companies in August 2026.

Summary

- KB Kookmin will initially launch Kinexys-based U.S. dollar payments across ten countries during August 2026.

- The service links blockchain settlement with SWIFT while supporting corporate transfers beyond normal banking hours.

- KB becomes South Korea’s first financial institution using Kinexys for corporate import and export payments.

The South Korean lender will use Kinexys by J.P. Morgan to support U.S. dollar payments across 10 countries.

The service will connect Kinexys with existing SWIFT payment rails. It will support near-real-time transfers and foreign exchange settlement throughout the day. Customers will access the service through KB Kookmin Bank’s domestic branches and its Singapore branch.

KB Kookmin becomes first Korean bank to use Kinexys

KB Kookmin Bank announced the service on July 26 after signing an agreement with J.P. Morgan on blockchain remittance services. According to Yonhap News Agency, it will become the first South Korean financial institution to use Kinexys for payment services aimed at import and export companies. The agreement focuses on faster cross-border remittances for businesses managing overseas trade, supplier payments and foreign exchange settlement needs.

The first phase will prioritise U.S. dollar transfers. The supported markets are South Korea, the U.S., Singapore, Saudi Arabia, India, Thailand, Qatar, the United Arab Emirates, Bahrain and South Africa. The bank has not published customer fees, transaction limits or an exact August launch date.

Kinexys adds blockchain settlement to existing bank rails

J.P. Morgan describes Kinexys as a bank-led blockchain platform for payments, asset tokenisation and near-real-time settlement. The network operates around the clock and lets approved institutions move funds without waiting for traditional banking cut-off times. It was previously known as Onyx.

The KB service will not replace SWIFT. Instead, it will link Kinexys with the existing messaging and correspondent banking system. This model allows banks to use blockchain for faster movement and settlement while retaining established compliance checks, account structures and foreign exchange processes.

J.P. Morgan has expanded Kinexys across several markets. In June, the bank added blockchain deposit accounts in Australian dollars, Hong Kong dollars, Japanese yen, Chinese yuan and Singapore dollars. It said the expansion created support for eight currencies and enabled 24/7 payments, programmable treasury operations and onchain foreign exchange.

Other banks have already used the platform for corporate payments. Qatar National Bank adopted Kinexys for U.S. dollar payments in 2025. The service allowed corporate transfers outside normal banking hours and reduced some settlement times to minutes.

KB expands its institutional blockchain activity

The payment launch follows several blockchain projects across KB Financial Group. In June, KB Kookmin Bank completed a $100 million digital bond sale through HSBC’s Orion platform. The two-year U.S. dollar bond settled in three business days, compared with five days under the earlier process.

KB Kookmin also participates in South Korea’s tokenised deposit work. The Ministry of Economy and Finance selected nine banks for a project linking tokenised deposits with government spending systems. The planned test will use programmable conditions and a shared record of public payments.

Meanwhile, KB Kookmin Card has been developing a payment system that links stablecoins with traditional credit. Crypto.news reported that the project uses Avalanche and OpenAsset infrastructure. The design aims to let users pay from stablecoin wallets while keeping standard card settlement for merchants.

Large banks move blockchain into live payment services

KB Financial Group ranked as South Korea’s largest lender by assets in S&P Global Market Intelligence’s 2026 Asia-Pacific bank review. The group placed 28th in the region with about $552.76 billion in assets. That scale gives the bank an established corporate network for introducing the new service.

The launch also adds to wider bank use of tokenised deposits and blockchain settlement. J.P. Morgan, Mastercard, Ripple and Ondo Finance tested a cross-border Treasury redemption in May. Kinexys handled the payment instructions and U.S. dollar settlement while the tokenised asset moved on the XRP Ledger.

J.P. Morgan has also used Kinexys with companies such as Axis Bank, Mitsubishi Corporation and EBANX. In July, EBANX said the platform reduced some internal cross-border transfers from more than 24 hours to minutes by removing local cut-off restrictions.

For KB Kookmin’s corporate clients, the main change will be access to longer operating hours and faster settlement across selected trade corridors. The bank has not said whether it will add more currencies or countries after the first phase. Its August rollout will show how the service works alongside existing SWIFT processes for commercial payments.

Europe’s crypto market has moved beyond the race to secure a Markets in Crypto-Assets licence.

Summary

- MiCA’s transition ended July 1, leaving unlicensed firms to exit, sell, or transfer European clients.

- U.K. crypto firms face FCA authorisation, prudential controls, governance rules, and client-asset safeguards from 2027.

- Banks already hold compliance systems and networks, making partnerships or acquisitions cheaper than greenfield builds.

The next test is whether authorised firms can afford the staff, capital and controls required to keep operating under the European Union’s full rulebook.

The cost pressure may push smaller crypto companies towards mergers, sales or bank partnerships. The same pattern could develop in the U.K., where the Financial Conduct Authority will open its authorisation gateway on September 30, 2026.

MiCA moves Europe from licensing to long-term compliance

The MiCA transition ended across the EU on July 1, 2026. The European Securities and Markets Authority said any company serving EU clients without authorisation must stop covered crypto services. Unlicensed firms must execute wind-down plans and help customers move assets to an authorised provider or self-hosted wallet.

A licence gives a crypto-asset service provider access to MiCA’s passporting system, but it also brings continuing duties. Firms must maintain governance, capital, market conduct, complaint handling, cybersecurity and anti-money laundering systems. These fixed costs weigh more heavily on smaller exchanges, brokers and custodians.

Notably, more than 3,000 crypto firms held registrations under earlier national systems, while only 194 had obtained MiCA approval by May. ESMA’s register later reached about 300 authorised providers after approvals around the July deadline.

U.K. rules could raise the cost of remaining independent

The U.K. has chosen to place crypto inside its existing financial-services framework rather than build a separate MiCA-style regime. The FCA said trading platforms, custodians, intermediaries, stablecoin issuers and firms arranging staking will need authorisation. Applications will run from September 30, 2026, to February 28, 2027, before the regime starts on October 25, 2027.

Steven Lightstone, a Morgan Lewis partner quoted by CoinDesk, said the FCA keeps “very high standards” where consumers are involved. He said a crypto company would be “treated like any normal traditional financial institution.” Banks already operate many required governance, reporting and financial-crime systems.

The FCA’s final crypto rules also extend client-asset protections to crypto custody. Its CASS 17 framework covers safeguarding duties for authorised custodians. Building key management, reconciliations, segregation and recovery procedures from scratch may cost more than joining a regulated group.

Banks and larger firms gain a route into crypto

Banks can use acquisitions to gain technology, licences and specialist teams without building every service internally. Crypto firms can gain capital, compliance staff, distribution and customer relationships. Partnerships may offer a middle route when neither side wants a full takeover.

Recent European activity shows both models. France’s CACEIS was nearing a deal for MiCA-licensed crypto platform Meria. Portugal’s Bison Bank became a MiCA-authorised provider after integrating its digital-asset subsidiary. Spain’sCecabank also launched regulated crypto custody for financial institutions.

A group of European banks selected Fireblocks to support a planned MiCA-compliant euro stablecoin, while Qivalis expanded its consortium to 37 financial institutions across 15 countries.

Simon Schneider, chief executive of Sygnum Europe, told CoinDesk that fewer than 20% of European banks offer crypto services. Bank executives expect regulatory certainty to move more client assets towards licensed institutions. Banks already have customer networks and compliance frameworks, creating room for partnerships in custody, brokerage, staking and tokenisation.

Scale may become Europe’s next competitive advantage

A BCG and FT Partners report found that fintech M&A value rose from $105 billion in 2023 to $251 billion in 2025. Scaled fintech companies completed 659 acquisitions in 2025, compared with 589 by banks and other established institutions. Digital assets and compliance ranked among the areas attracting buyers.

MiCA may add another reason to pursue deals. A buyer can spread compliance costs across a larger customer base, while an acquired company can avoid maintaining duplicate licences and systems. Regulators will still review ownership, governance, outsourcing and customer protection after any transaction.

Consolidation does not mean banks will replace all crypto-native companies. Specialist providers still supply technology and market knowledge that many banks lack. Self-custody will also remain outside regulated custodians’ business models. The likely change is fewer standalone providers and more groups combining banking distribution with crypto infrastructure.

The final shape will depend on authorisation decisions, operating costs and customer migration. MiCA has separated authorised providers from firms that must leave the EU market. The FCA’s 2027 regime may apply similar pressure in Britain. Smaller companies may need to raise capital, share infrastructure, sell or leave regulated markets. This could make scale more valuable than speed for firms seeking long-term regulated European access.

Unlike the previous major bear market in which numerous cryptocurrency exchanges reduced their staff number, the current cycle turned out to be more violent and requires a different sort of reaction.

The latest to close shop, with an announcement earlier today, was BitMart.

BitMart to Shut Down

The exchange saw the light of day during the 2017 big bull market and expanded its services to over 1,700 cryptocurrencies as of today. However, it followed the recent negative trend, stating that it has begun to “orderly” wind down its trading operations.

New registrations have already been halted, as well as deposits and opening new trading orders. A month later, the exchange will stop all trading services. The official shutdown will be at the end of January at 15:59 UTC, when the platform operations will cease. In contrast, withdrawals will remain available.

The company urged all users to close their trading positions, complete KYC if needed, and transfer out the available funds as soon as possible.

Important Notice

After a careful evaluation of the Company’s operating conditions, market environment, and future strategic direction, BitMart has made the difficult decision to commence an orderly wind-down of its trading platform operations. We deeply regret having to make… pic.twitter.com/KX3zczIrAh

— BitMart (@BitMartExchange) July 26, 2026

The exchange’s native token reacted with an immediate price drop, plunging by over 60% on a 24-hour scale. BMX traded at $0.32 before the news went live, and dumped to $0.09 as of press time. It also remains 90% away from its all-time high at $0.619 (CoinGecko data) recorded in early 2024.

BitMEX and Who Else?

Just a few days ago, the Arthur Hayes-co-founded cryptocurrency derivatives platform BitMEX said it will shut down on September 23. The creator of the 100x perpetual swap was active for nearly a decade, but it has fallen out of traders’ grace in the past couple of years.

The crypto shutdowns continued with popular DEX aggregator Odos. The project announced on July 24 that it will halt all of its services at the end of July.

One of its competitors, Dango, made a similar statement on the same day. The self-proclaimed ‘Endgame Exchange’ informed that the team has made the difficult decision to wind down its services, outlining “various reasons” without actually specifying them. It will stop trading on July 29, while the Dango L1 blockchain will halt on August 13.

The post Another Major Crypto Exchange Is Shutting Down After BitMEX appeared first on CryptoPotato.

Strategy says its current capital structure could withstand a prolonged Bitcoin decline while continuing to fund interest payments and preferred stock dividends.

Summary

- Strategy says its current structure can fund obligations through 5.8 years of steady Bitcoin declines.

- Company data shows a $3.225 billion cash reserve supporting preferred dividends and debt interest payments.

- The stress test uses Strategy’s internal BTC Rating rather than an independent credit agency assessment.

In a July 24 post on X, the company said Bitcoin could fall 11.4% each year for 5.8 consecutive years without pushing its company-defined BTC Rating below 1.0x.

The claim arrived as Bitcoin traded near $64,463 and Strategy shares closed at $91.67 on July 24. Bitcoin remained below Strategy’s average purchase price, while MSTR had fallen sharply from its previous peak. The exercise describes a steady multi-year decline, not a sudden crash or a guarantee that Strategy could meet every obligation under all market conditions.

What Strategy’s Bitcoin stress test measures

Strategy’s model uses a measure called BTC Floor ARR. The company defines it as the lowest constant annual Bitcoin return that would preserve 1.0x coverage of net debt and preferred stock over the weighted duration of its credit structure. The calculation includes interest and preferred dividend payments. Its current credit metrics dashboard places that floor at negative 11.4% over 5.8 years.

Strategy wrote: “At today’s capital structure, BTC could fall 11.4% annually for 5.8 years” while the company continued funding interest and preferred dividends. A 1.0x BTC Rating means the measured Bitcoin reserve still matches the claims included in Strategy’s formula. The company uses the calculation to describe balance-sheet coverage, not Bitcoin’s likely future price.

The calculation also differs from a traditional credit rating. Strategy developed the metric itself and publishes it for illustrative purposes. The company does not present it as proof that Bitcoin will decline at a steady rate or that its financing structure can withstand every type of market disruption.

Cash reserve and Bitcoin sales support the model

Strategy held 843,775 BTC as of July 19. It acquired the coins for about $63.69 billion at an average price of $75,476. The company also reported a $3.225 billion U.S. dollar reserve after raising $263.5 million through common-stock sales. As crypto.news reported, Strategy did not buy or sell Bitcoin during that week.

The reserve supports preferred dividends and interest on outstanding debt. Strategy’s current figures place annual interest and dividend obligations near $1.7 billion. The cash balance therefore provides less than two years of direct coverage before the company needs new financing, Bitcoin sales or other capital actions.

Strategy created a broader Digital Credit Capital Framework in June. The plan authorises up to $1.25 billion in Bitcoin sales to build or refill the cash reserve. It also permits selected Bitcoin sales to fund dividends, interest and approved security repurchases. Strategy raised the STRC preferred dividend rate to 12% and approved separate $1 billion buyback programmes for common and preferred securities.

Strategy sold 3,588 BTC for about $216 million between June 29 and July 5. It used the proceeds for preferred distributions and reserve replenishment. The sales reduced its holdings from 847,363 BTC to 843,775 BTC.

Strategy warns its BTC Rating is not a credit rating

Strategy’s metric definitions state that BTC Rating is an internal, illustrative measure. No independent credit rating agency issues it. It does not measure liquidity, solvency or reported financial performance. The company also says the calculation does not account for possible cross-defaults under its debt agreements.

The model uses the notional value of preferred stock, although some securities may carry liquidation preferences above that amount. Its dividend coverage measure also assumes Strategy can refinance existing debt on broadly similar terms without repaying principal. Those assumptions may not hold during a severe funding or market shock.

Strategy’s board must also approve preferred dividends. The company can adjust STRC’s variable rate each month, and it does not guarantee cash payments. Strategy may issue shares, sell Bitcoin, lower distributions where permitted or restructure obligations if its funding position weakens. A 1.0x result therefore does not remove refinancing, dilution, execution or market risks.

Bitcoin and MSTR remain under market pressure

Bitcoin traded around $64,463 on July 26, roughly 49% below its October 2025 peak near $126,000. MSTR closed at $91.67 on July 24. Investors continued to track Bitcoin’s price alongside Strategy’s cash requirements, preferred dividend costs and market value relative to its Bitcoin holdings.

The company’s financing model worked best when MSTR traded above the value of its Bitcoin reserve. That premium allowed Strategy to sell shares and increase Bitcoin per share. A lower market premium made new issuance less attractive and pushed the company to build cash rather than buy more Bitcoin.

The company has also shifted from a mainly accumulation-focused model towards active capital management. Its current framework includes share sales, cash reserves, possible Bitcoin sales and repurchase programmes. Crypto.news analysis noted that Strategy’s market premium, or mNAV, remains central because it determines whether common-stock issuance can increase Bitcoin per share.

The stress test presents Strategy’s view of how long its current assets could support its financing structure under a steady decline. It does not predict Bitcoin’s direction or cover every form of market stress. Future results will depend on Bitcoin prices, access to capital, dividend decisions, debt terms and the company’s use of authorised Bitcoin sales.

Glen Powell’s Underseen 5-Part Sci-Fi Masterpiece Has Aged Like Fine Wine

Ryan Reynolds crashes Comic-Con as Deadpool but fans missed the obvious joke

(PHOTO) Jessica Alba Turns Heads in Cheeky Bouguessa Micro Minidress During Stylish New York City Outing

Renter of Home in Anne Heche Crash Denies Settlement With Son

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Weekend Open Thread: Staud – Corporette.com

Bitcoin Treasuries are COLLAPSING and That’s Bullish! (Here’s Why)

Worst Financial Advisor Ever – Impractical Jokers #shorts #prank #funny

LEC 1 || VBU SEM 5 Financial Management Important Questions 2026 || 100% Most Expected Questions

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Brooks Brothers

-

News Videos7 days ago

News Videos7 days agoBig Money Is Entering XRP

-

Crypto World5 days ago

Crypto World5 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

Tech6 days ago

Tech6 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech5 days ago

Tech5 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat6 days ago

NewsBeat6 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Business4 days ago

Business4 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment5 days ago

Entertainment5 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World4 days ago

Crypto World4 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Tech6 days ago

Tech6 days agoWatch Flock Safety CEO Garrett Langley discuss the future of surveillance at TechCrunch Disrupt 2026

-

NewsBeat5 days ago

NewsBeat5 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Crypto World6 days ago

Crypto World6 days agoCircle’s President Sold Over 360,000 Shares, The Filings Explain Why

-

Tech6 days ago

Tech6 days agoSubway Sandwich Computers Get a Second Life as Gaming Machines

-

Sports2 days ago

Sports2 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

News Videos3 days ago

News Videos3 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Fashion2 days ago

Fashion2 days ago16 Dresses for the High Summer Event

-

Tech7 days ago

Tech7 days agoHow To Use Claude’s Reflect Dashboard And Learn When It’s Time To Touch Grass

-

Tech6 days ago

Tech6 days agoThe 35 Best Board Games for Family Game Night

-

Entertainment6 days ago

Entertainment6 days agoStephen Colbert Returns to Social Media After Late Show End

-

Crypto World6 days ago

Crypto World6 days agoAndrew Cuomo joins OKX board as crypto exchange expands in U.S.

You must be logged in to post a comment Login