Crypto World

Tokenized Stocks and Bonds Move Toward Crypto’s Strongest Institutional Product

Tokenized stocks, ETFs, Treasuries, and corporate bonds are now firmly rooted in regulated market tests and consumer products. RWA.xyz data places distributed real-world asset value at $26.71 billion and represented asset value at $345.07 billion across the wider tokenization market.

Consumer-facing adoption is expanding as Robinhood EU offers more than 2,000 stock tokens as derivative contracts linked to stocks and ETPs, while Kraken says xStocks reached 100 fully backed tokenized US stocks and ETFs and passed $25 billion in transaction volume after its June 2025 launch.

Traditional market institutions are now testing similar models. DTCC received SEC staff relief in December 2025 for a three-year tokenization service covering highly liquid DTC-custodied assets, including Russell 1000 constituents, major ETFs, and US Treasury bills, bonds, and notes. Nasdaq’s tokenized securities proposal also points toward a regulated model where tokenized shares trade with the same CUSIP, order book priority, and investor rights as traditional shares.

BeInCrypto spoke with experts from 8Blocks, BloFin Research, Phemex, and Zoomex to assess adoption paths and remaining limits on investor trust.

Global Liquidity, Programmability, and Settlement

The early pitch for tokenized stocks centered on extended trading hours, yet experts see the stronger institutional use case in liquidity, distribution, collateral use, and settlement.

Anton Efimenko, Co-Founder and Lead Expert at 8Blocks, links tokenized securities to deeper global order books.

“Beyond speed and higher trading frequency, tokenized securities can trade globally. More investors can access and invest in the same stocks, ETFs, Treasuries, or corporate bonds.” Efimenko said.

In his view, global access gives the same stock, ETF, Treasury, or bond a larger buyer base. If regional stress causes local selling, buyers from another market can enter sooner, helping absorb pressure before panic spreads. Deeper participation can also support larger tickets, giving funds more room to buy securities with less price disruption.

Edward Wu, Head of BloFin Research, places the main value in three areas: distribution, programmability, and settlement efficiency.

“The real value is distribution, programmability, settlement efficiency, beyond 24/7 trading,” Wu said.

Distribution can move securities through wallets, fintech apps, crypto exchanges, and wealth platforms. Programmability can make a tokenized Treasury fund usable inside lending vaults, margin accounts, structured products, or collateral systems. Settlement can also become more efficient when the securities side and cash side move through compatible digital systems, reducing operational friction across execution, transfer, payment, and custody.

Federico Variola, CEO of Phemex, sees tokenized stocks as part of DeFi’s composability trend.

“Apart from 24/7 trading, these tokenized instruments can potentially be used as collateral for other positions, for example leveraged or derivatives positions, borrowing and lending, or even within centralized systems,” Variola said.

Variola said many of these use cases are difficult for average retail users inside traditional banking or trading apps, while DeFi already has much of the technical base needed to support them.

Apps and Exchanges Can Move Early, While Brokerages Hold the Largest Investor Pools

The first wave of tokenized securities is likely to come from crypto exchanges, fintech apps, and permissioned DeFi venues because they can launch products faster, reach global users, and use stablecoins for funding and settlement.

8Blocks expects the largest growth to come through traditional brokerages and banks, where investor capital and trust are already concentrated.

“Tokenized securities will grow fastest where there is already a large concentration of investors and capital: traditional brokerages and banks,” Efimenko said.

Efimenko expects existing brokerage users to adopt tokenized securities when they can diversify portfolios inside accounts they already use. The product becomes easier to accept when it appears inside a trusted brokerage experience.

Wu sees a two-stage adoption path in which crypto exchanges, fintech apps, and permissioned DeFi platforms can move faster in the near term, while established brokerages will decide long-term market size. Interactive Brokers reported 4.646 million client accounts and $789.4 billion in client equity as of Q1 2026, showing the amount of capital established brokers can bring once tokenized securities become part of standard brokerage products.

Permissioned DeFi may also serve institutional users who need compliant access to on-chain settlement, collateral movement, and automated portfolio activity. Its growth will depend on regulation, asset eligibility, and the willingness of institutions to use blockchain-based venues.

Investor Rights Separate Ownership From Price Exposure

Tokenized securities need precise rights because investors must understand the claim attached to the token. A product can offer shareholder-style ownership, a securities entitlement, redemption, dividends, coupons, voting or proxy access, corporate-action treatment, or price exposure through a derivative contract.

8Blocks expects many global users to prioritize financial outcomes over delivery of the underlying asset. A token buyer in one jurisdiction may have little use for a traditional share listed and settled in another country, especially when local brokerage access, tax treatment, or custody options create friction.

Efimenko expects investors to prefer products with “the financial result and a guaranteed claim to it,” including dividends, gains from price appreciation, or coupon payments.

Wu argues product rights should match product marketing. A true tokenized stock should give the holder the same economic and legal position as a traditional shareholder or a defined securities entitlement, including dividends, corporate actions, voting or proxy rights, transferability, and a redemption or conversion path where feasible.

Nasdaq’s proposal follows a similar standard, where a tokenized equity security would need to convey equity interest, dividend rights, voting rights, and residual asset rights upon liquidation to receive treatment equivalent to a traditional security. A product based on price exposure would belong in a separate category.

Robinhood EU’s model shows the difference because its stock tokens are derivative contracts linked to underlying stocks and ETPs, giving price exposure instead of shareholder rights. The product can still serve investors, provided the market description matches the actual claim.

Mainstream Adoption Depends on Familiar Outcomes

Tokenized securities can reach mainstream investors when the crypto elements fade into the background of a normal brokerage or fintech account. The user experience should center on familiar assets and outcomes, such as Treasury yield, Apple exposure, an S&P 500 ETF, a corporate bond, or coupon income.

Fernando Lillo Aranda, CMO at Zoomex, sees this as the most realistic path to mass adoption because investors usually care about what a product delivers, rather than the technical system behind it.

“Mainstream investors historically don’t adopt infrastructure; they adopt outcomes. Most people never cared whether payments ran on SWIFT rails or card networks. They cared that money moved.”

Aranda said tokenized securities could follow the same pattern. If users can access stocks, bonds, funds, private credit, or structured products with faster settlement, lower minimum tickets, programmable ownership, programmable distributions, and global access, the blockchain side becomes part of the background experience.

“Wallets, chains, and DeFi become backend plumbing rather than the product,” Aranda added.

Wu made a similar point, arguing that real adoption depends on making tokenized securities feel familiar to users who already understand brokerage and fintech accounts.

“Tokenized securities need to feel like a normal brokerage or fintech account. Most users do not care about how DTCC, transfer agents, clearing brokers, or payment rails work today.”

In Wu’s view, users should see recognizable financial products first: Treasury yield, Apple, an S&P 500 ETF, or a corporate bond. The chain, wallet, custodian, compliance checks, and settlement mechanics can operate behind the interface.

“The user sees ‘Treasury yield,’ ‘Apple,’ ‘S&P 500 ETF,’ or ‘corporate bond,’ while the chain, wallet, custodian, compliance checks, and settlement mechanics run in the background.”

8Blocks is more cautious about tokenization as a standalone adoption driver. Efimenko expects investors to judge tokenized stocks primarily as stocks, with the token wrapper playing a secondary role.

“Investors know how to assess risk, and for them, tokenized stocks will still be stocks, not tokens. Tokenization is just a wrapper.”

For 8Blocks, this means tokenized securities may improve access, liquidity, and execution, while the underlying asset remains the main source of risk and return.

Trust Depends on Regulation, Custody, and Liquidity

Tokenized public markets need stronger trust conditions before investors treat them like traditional brokerage accounts. Regulation, rights, issuer quality, custody, liquidity, and price consistency remain the main concerns.

8Blocks sees regulation as the biggest barrier because unclear rules force issuers into more complex product designs.

“Regulation is the main barrier,” Efimenko said. “Because regulation is still unclear, RWA issuers are forced to get creative with the structure.”

Efimenko pointed to one possible model where an issuer sells tokenized shares in its own company while using its balance sheet to hold Apple stock. Such a product can give investors economic exposure, but it also places the issuer between the investor and the underlying asset.

BloFin Research sees rights ambiguity as another major weakness in current stock-token markets.

“Many stock tokens track price without giving ownership, voting, dividends, or a direct claim on the underlying company,” Wu said.

For Wu, this creates a trust problem because investors may buy a product linked to a familiar public company while relying on an unfamiliar issuer, custodian, or venue.

“Counterparty and custody risk are also a consideration. Investors are not familiar with the issuers, which are often startup companies.”

Liquidity creates another concern. Wu said tokenized stocks can diverge from the underlying market price when the main exchange is closed or when market-maker support is thin.

“A tokenized stock could drift away from the stock price when the underlying market is closed. Thin order books, fragmented venues, and uneven market-maker support can make tokenized markets feel less reliable.”

Regulators have raised similar concerns. ESMA warned in 2025 about investor misunderstanding in tokenized stocks when buyers receive exposure to listed shares rather than shareholder status. The regulator also noted many tokenization projects remain small and illiquid.

Final Thoughts

Tokenized securities give crypto one of its strongest institutional stories because they connect blockchain-based systems with assets investors already understand. The strongest case comes from global distribution, programmable ownership, collateral use, faster settlement, and enforceable investor claims.

Early growth may come from crypto exchanges, fintech apps, and permissioned DeFi venues, while long-term adoption will depend on banks, brokers, custodians, and regulated market institutions. The strongest products will make chains, wallets, and settlement mechanics fade into the background while placing investor rights at the center of the experience.

Tokenized stocks and bonds can become a major institutional product when buyers can identify their ownership claim, the custodian of the underlying asset, income payment rules, redemption mechanics, and claim protection during market stress. The platforms most likely to win are the ones offering familiar assets with precise rights, dependable custody, and liquidity strong enough to support real investor demand.

The post Tokenized Stocks and Bonds Move Toward Crypto’s Strongest Institutional Product appeared first on BeInCrypto.

Bitmine Immersion Technologies says it has boosted its Ether holdings by nearly 10,000 ETH over the past week, bringing its treasury to 5.79 million Ether. In a new disclosure, the company described how most of those holdings are deployed to earn staking yield through its validator operations.

According to Bitmine’s filings, the latest purchases take its exposure to Ether to roughly 4.8% of the cryptocurrency’s total supply. The company also indicated that its overall balance sheet—covering crypto holdings, cash, and marketable securities—totaled $11.8 billion as of July 26.

Key takeaways

- Bitmine reported holding 5.79 million ETH after buying nearly 10,000 ETH in the prior week.

- About 4.9 million ETH—approximately 85% of Bitmine’s Ether—are staked via its validator operations.

- Bitmine projected annualized staking rewards of about $299 million once all Ether is deployed across staking infrastructure and partner validators.

- The move coincides with Ether outperforming Bitcoin over the same seven-day period, based on CoinGecko data.

Bitmine’s growing Ether treasury

Bitmine Immersion Technologies said Monday that it currently holds 5.79 million Ether, following purchases of nearly 10,000 ETH over the past week. The company framed the accumulation as a continuation of its strategy to build a large corporate Ether treasury, placing it among the biggest public holders in the sector.

In its disclosure, Bitmine quantified the scale of its holdings: 5.79 million ETH represents about 4.8% of Ether’s total supply. The report also emphasized deployment readiness, noting that a large portion of its Ether is already working to generate staking rewards.

Staking deployment and yield projections

Bitmine said roughly 4.9 million ETH—around 85% of its Ether holdings—are staked through its validator operations. The company added that it expects annualized staking rewards of approximately $299 million once all of its Ether is deployed across its staking infrastructure and through partner validators.

For investors, the practical importance of that figure is that it ties Bitmine’s treasury strategy to a recurring value engine rather than relying solely on spot price appreciation. Staking also introduces its own set of variables, including network conditions and validator performance, but Bitmine’s disclosure makes clear that a majority of its ETH is already earning yield.

Why the ETH/BTC outperformance matters

Bitmine’s purchases arrive during a week when Ether has held up better than Bitcoin. CoinGecko data cited by Bitmine’s announcement shows ETH gaining about 2.4% over the past seven days while Bitcoin declined roughly 0.7%.

Bitmine Chairman Tom Lee pointed to the rising ETH/BTC ratio as a signal of strengthening momentum. He described the ratio as being at a three-month high, suggesting that relative demand for Ether has been improving rather than Ether simply tracking broader market direction.

Relative performance can matter for corporate treasury strategies because it affects the opportunity cost of accumulating one asset versus another. If ETH is strengthening against BTC—as Bitmine suggested—it potentially reinforces the company’s decision to allocate incremental capital toward Ether rather than pausing to concentrate on Bitcoin.

Strategy’s pivot and the shifting corporate crypto playbook

Bitmine also used its announcement to highlight how its accumulation approach is diverging from Strategy, another major public player. While Bitmine has continued adding Ether, the company said Strategy has paused Bitcoin purchases in recent weeks, marking a contrast in how these large treasuries are deploying capital.

Earlier coverage from Cointelegraph noted that Strategy announced it raised $544.5 million through stock sales, repurchased $25 million of its STRC preferred shares, and increased its US dollar reserve to $3.75 billion—while maintaining holdings of 843,775 BTC. That set of actions underscores a broader theme in corporate crypto: balance-sheet management can shift the pace of buys even when long-term conviction remains unchanged.

For market participants watching treasury behavior, the key takeaway is that accumulation is not always linear. Bitmine’s continued Ether buying—paired with the emphasis on staking deployment—shows a model where holding and earning yield can progress in parallel. Strategy’s pause on Bitcoin purchases, meanwhile, suggests corporate allocations can be influenced by funding, liquidity targets, and operational constraints.

Next, readers should watch whether Bitmine’s stated staking plan—covering deployment across infrastructure and partner validators—fully catches up to its forecast, and whether the ETH/BTC strength referenced by Tom Lee persists alongside Ether’s price action. That combination—ongoing net accumulation plus higher relative performance—could further shape how investors evaluate corporate crypto treasuries moving into the next quarter.

Ondo Finance has launched the Ondo Network, replacing its planned blockchain with an execution layer built for fast, private, and non-custodial trading.

Summary

- Ondo Network replaces Ondo Chain as the company shifts its focus from settlement to execution.

- Secure hardware enclaves process trades privately, while decentralized attestors verify the approved code.

- Ondo Perps is the first application, supporting 24/7 equity and commodity perpetual futures.

- Recent FINRA authorizations give Ondo separate infrastructure for regulated tokenized securities in the U.S.

Ondo Network replaces the planned Ondo Chain

Ondo Finance publicly introduced the Ondo Network on July 27, describing it as an execution layer that combines centralized exchange-like speed with self-custody, privacy and blockchain-based settlement.

Ian De Bode, CEO of Ondo Finance, described the product as an evolution of Ondo Chain, a previously announced Layer 1 blockchain designed for tokenized real-world assets. Ondo will not operate both systems at the same time.

“I’d frame it more as an evolution, but we will not be running the Ondo Network and the Ondo Chain in parallel.”

Ondo changed its approach while building Ondo Perps and consulting potential users. According to the company, those discussions showed that execution speed, rather than settlement capacity, was the main obstacle preventing onchain trading platforms from competing with centralized exchanges.

Traditional blockchains generally execute, verify, and settle transactions through the same public ledger. That structure provides transparency and a durable transaction history but can expose order flow and slow applications that require rapid trade matching.

The Ondo Network separates these functions, allowing trade execution to occur away from a public ledger while asset transfers still settle onchain.

How Ondo Network verifies private execution

Applications on the network run inside trusted execution environments, also known as secure hardware enclaves. These isolated environments process application code without revealing sensitive information, such as open positions and order flow, to the public.

A decentralized group of attestors determines which code the enclaves may run. The network also uses a multi-party structure under which no single operator can approve unauthorized code, reconstruct a signing key, or independently transfer user assets.

Asset transfers currently settle on Ethereum, while Ondo plans to support other public blockchains. The network’s settled state remains inside the enclaves for now, but the company intends to commit that record to public blockchains as the system develops.

Ondo also plans to introduce more attestors, independent watchers, bonded participation, and additional cryptographic proofs. The ONDO token is expected to support incentives and governance as those responsibilities become more decentralized.

The system is general-purpose rather than limited to trading. Ondo said developers could use it for spot markets, lending, structured products, settlement systems and non-financial applications requiring fast and verifiable private execution.

Ondo Perps becomes the first network application

Ondo Perps is the first application running on the network. The platform provides round-the-clock perpetual futures linked to equities and commodities while allowing traders to use tokenized real-world assets as collateral.

Perpetual futures allow users to take leveraged long or short positions without a fixed expiry date. The product launched earlier in July for users outside the United States and supports up to 20 times leverage on selected markets.

The platform’s initial role demonstrates how Ondo wants to use the network: trading takes place privately at near-centralized-exchange speeds, users retain control of their funds and transfers settle through public blockchain infrastructure.

Ondo said the network launch does not immediately alter the ONDO token’s role. The asset remains the governance and ecosystem token for the company’s real-world asset and market infrastructure.

Ondo (ONDO) traded near $0.40 following the announcement, up 1.1% over the past 24 hours with a market capitalization of approximately $1.96 billion, according to data from CoinGecko.

FINRA permissions support a separate U.S. rollout

Ondo’s network launch follows new U.S. regulatory permissions for Oasis Pro Markets, its SEC-registered broker-dealer subsidiary.

Oasis Pro received FINRA authorizations covering National Market System stocks, ETFs, mutual funds, index funds and securities issued through initial public offerings. The permissions cover activities including retail over-the-counter transactions, private placements and underwritten primary offerings.

The framework also supports settlement through fiat currencies or selected stablecoins, including transfers between blockchain wallets. It could allow eligible U.S. retail and institutional investors to access tokenized securities through existing brokers, advisers and retirement accounts.

However, the permissions do not automatically make Ondo Perps or every existing Ondo product available to U.S. residents. They provide regulated infrastructure through Oasis Pro Markets for securities offered under SEC and FINRA oversight, while individual products remain subject to separate eligibility and compliance requirements.

Crypto World

U.S. Senate puts off crypto Clarity Act for now as it focuses limited bandwidth elsewhere

Bottom line: Clarity isn’t likely to come up for voting before next week — the final days before the chamber’s summer break is set to start on August 8. The hotly debated market structure bill isn’t yet ready for a vote, anyway, as the parties continue to try to seek a compromise on a contentious provision that’s stood in the way of a deal: the ban against senior government officials, including President Donald Trump, backing crypto projects.

Thune’s office had told CoinDesk last week that his next floor-time priority would go to the Russia legislation. While the majority leader also said he hopes to get to Clarity before the break, he said the leadership would have to “see where the votes are.”

At this point in the Senate calendar, every hour of floor time is a precious commodity, and the debate over the Clarity Act still hasn’t settled some of the major outstanding points — especially the section on government ethics, which was the topic of a Monday event hosted by Democrats opposing the Clarity Act and the president’s crypto activities.

Having significant disagreements at this stage could narrow the chances that Clarity can become law in 2026, potentially throwing the industry into some uncertainty over the timeline for U.S. regulations. If this legislation tanks, the next best avenues for regulatory legitimacy is the ongoing implementation of the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act and the policy efforts at the U.S. Securities and Exchange Commission and the Commodity Futures Trading Commission.

Securitize, the tokenized-assets platform, said its subsidiary Securitize Capital has registered with the U.S. Securities and Exchange Commission (SEC) as an investment adviser—an update that expands the firm’s regulated advisory offering for institutional clients.

The company framed the move as a way to deepen regulated investment-advisory capabilities around onchain capital markets, building on an existing lineup of market infrastructure and financial-services licenses already held within the Securitize group.

Key takeaways

- Securitize Capital’s SEC investment adviser registration adds formal advisory capabilities to the firm’s current regulated business stack.

- The subsidiary previously operated as an exempt reporting adviser and is now subject to additional disclosure, compliance, recordkeeping, and examination duties.

- Securitize says the change is meant to support institutions designing and managing investment strategies that use tokenized, onchain capital markets.

- The registration complements existing regulated entities at Securitize, including an SEC-registered broker-dealer, alternative trading system, transfer agent, and fund administration services.

What the SEC investment adviser registration changes

According to Securitize, Securitize Capital’s SEC registration broadens how the subsidiary can serve institutional investors. The key operational shift is that the business is no longer relying on exempt status—meaning it must comply with the Investment Advisers Act’s baseline requirements for regulated advisers.

Securitize said the company previously operated as an exempt reporting adviser. Under the Investment Advisers Act, that status generally implies more stringent expectations around disclosure, compliance, recordkeeping, and SEC examination. For institutional participants, those obligations matter because they shape governance, supervisory controls, and documentation standards that regulators typically look for in adviser oversight.

The firm also positioned the upgrade as an expansion of “investment advisory capabilities” tied to Securitize’s broader infrastructure. In practice, that means institutions may be able to engage with Securitize not only as a platform for tokenization and related market services, but also through a more explicitly regulated advisory channel.

A regulated platform built around tokenized capital markets

Securitize said the adviser registration is being added to existing regulated businesses within the group. The company cited an SEC-registered broker-dealer, an alternative trading system, a transfer agent, and fund administration services—capabilities that are often described together in tokenization business models because they can support issuance, custody/transfer mechanics, trading venues, and ongoing fund administration.

By bringing adviser registration under the same umbrella, Securitize is effectively tightening the regulatory alignment across multiple layers of its tokenized-asset ecosystem. That matters for institutions deciding whether they want exposure to tokenized structures under familiar compliance frameworks, rather than relying on a less standardized set of arrangements across different vendors.

Industry scale and the broader push for RWA infrastructure

Securitize also reiterated its market position in the “tokenization” category. The company described itself as the largest tokenization platform by onchain asset value, citing around $4.8 billion in tokenized assets across funds from BlackRock, Apollo, KKR, VanEck, Hamilton Lane and other asset managers.

This context is important: as the real-world assets (RWA) sector continues to develop, competition is increasingly about more than token issuance. Platform operators are trying to combine issuance rails with trading, transfers, and governance that fit within U.S. financial regulation. Securitize’s move suggests it wants to add another leg to that structure—advisory oversight—while keeping the rest of its regulated-services suite in place.

NYSE listing follows a merger, while the stock faces pressure

The registration comes as Securitize’s public-company status continues to play out. Securitize began trading on the New York Stock Exchange under the ticker SECZ on July 2 after completing a business combination with Cantor Equity Partners II.

Following the listing, the article notes that the shares have fallen about 46% from their first-day closing price.

While the SEC investment adviser registration is a regulatory milestone, it may also be read by investors as part of a broader effort to strengthen institutional credibility and expand monetizable services. At the same time, the stock’s drawdown since the NYSE start date underscores that market participants may be watching not only compliance progress, but also whether that compliance translates into durable demand and measurable business growth.

What to watch next

For institutions and market participants, the immediate question is how Securitize Capital’s adviser status will expand real advisory workflows—particularly how compliance, oversight, and recordkeeping will be implemented as clients engage with tokenized strategies. For investors, the next signal to track is whether the additional regulated capability converts into higher adoption, clearer revenue drivers, and continued traction across its tokenized-asset partnerships.

HashKey Holdings says it has consolidated its crypto exchange operations into a single platform and application, aiming to give customers one seamless entry point while keeping regulatory compliance tailored to local jurisdictions.

In a Monday announcement, the Hong Kong-based digital asset services firm said it has merged its HashKey Exchange and HashKey Global businesses. The change brings core hubs—including Hong Kong, Singapore, the Middle East (Dubai), and Bermuda—under one platform experience.

Key takeaways

- HashKey is unifying separate exchange branches into one platform and one app for multiple regions.

- The company says it will use a “unified entry, localized compliance” model rather than region-by-region front ends.

- Customers across Hong Kong, Global, Singapore, and Dubai/Bermuda should download the same application.

- Compliance and controls are described as being managed based on each user’s legislative domain.

- The approach aligns with broader industry moves toward shared user interfaces over fragmented legal structures.

One app, multiple legal environments

HashKey’s stated goal is to reduce friction for users who would otherwise need to navigate different exchange offerings depending on where they operate. The company said the rollout follows a “unified entry, localized compliance” principle: the platform experience is meant to be consistent for end users, while compliance is handled according to the applicable regulatory framework for each jurisdiction.

Practically, HashKey says users in Hong Kong, Global, Singapore, or the Middle East can download the same application. From there, the platform would manage compliance across each user’s specific legislative domain—supporting the firm’s claim that the single front end can still remain aligned with local rules.

HashKey framed the move as a shift away from the early-era virtual asset industry pattern, when licensed exchanges often maintained siloed regional models to simplify compliance at the time.

How HashKey’s model compares with other exchanges

HashKey’s consolidation mirrors a trend visible in other major platforms: presenting a single consumer interface while distributing legal responsibilities across multiple entities behind the scenes.

For example, the company pointed to market precedents such as OKX, which markets its website and mobile apps as one platform. However, OKX’s terms historically allocate customers to different providers based on residence. In that setup, the outward experience is unified, but the legal backend remains fragmented across regions.

Similarly, HashKey referenced Kraken’s approach in Europe. Kraken previously consolidated its Dutch broker BCM into its platform following an acquisition in September 2024, and later began serving the European Economic Area through its Irish MiCA entity as part of a unified regulatory framework described in its own updates.

While HashKey’s announcement focused on front-end unification and localized compliance management, the comparisons underline a recurring industry reality: even when users see one platform, regulatory coverage often still depends on separate entity structures by region.

Why the consolidation matters for users and operators

For traders and other market participants, a single platform experience can reduce confusion—especially for users who operate across multiple regions or relocate. It can also streamline onboarding workflows by limiting differences in user interfaces, login flows, and product access that often vary between regional exchange branches.

From an operator standpoint, unifying applications can simplify support, infrastructure choices, and product delivery. Rather than maintaining parallel front ends and workflows for each jurisdiction, the firm can focus on one user experience and then apply compliance controls based on user location or jurisdictional classification.

Still, HashKey’s announcement also highlights a key tension in exchange consolidation: customer-facing simplicity does not necessarily mean one set of rules. The “localized compliance” framing suggests that while the application is shared, users may be governed by different legal and compliance arrangements depending on where they fall within HashKey’s described jurisdictional domains.

What to watch next after HashKey’s rollout

As HashKey moves to the unified platform, users should pay close attention to how access, account requirements, and compliance checks behave in each jurisdiction—particularly whether the transition changes onboarding steps or documentation expectations for customers in Hong Kong, Singapore, or the Middle East.

For the broader market, the move signals that exchange operators are continuing to modernize the customer layer of their businesses, even while regulatory requirements remain inherently local. The next phase to monitor will be how smoothly the migration completes across all described regions and whether HashKey expands the approach to additional products or services tied to licensing constraints.

New York Attorney General Letitia James has urged Congress to revise the CLARITY Act, warning that the crypto market structure bill could restrict states from prosecuting fraud and enforcing investor protection laws.

Summary

- James said the bill could preempt state investor protection laws and weaken local enforcement.

- State and local authorities account for about 98.8% of arrests nationwide, according to her testimony.

- Senate Republicans need 60 votes to advance the legislation through the cloture process.

- Banking, ethics and enforcement disputes remain unresolved before the Senate’s August recess.

James challenges the CLARITY Act’s enforcement rules

James raised the concerns in written testimony submitted to a Senate committee as lawmakers continued negotiations over the federal crypto bill.

She argued that the CLARITY Act would interfere with state investor protection laws and reduce the authority of state and local agencies to prosecute misconduct involving digital assets.

“This is a mistake,” James wrote.

The New York attorney general said state and local law enforcement agencies conduct most enforcement work across the United States. According to figures included in her testimony, those authorities are responsible for about 98.8% of arrests, compared with roughly 1.2% by federal agencies.

“Despite this, CLARITY would neuter state and local law enforcement by preempting states and preventing them from fully prosecuting rampant fraud and violations of law by actors in the cryptocurrency marketplace.”

Her intervention adds to Democratic concerns about whether the bill gives state authorities enough power to pursue crypto fraud and enforce its proposed ethics restrictions. James has asked Congress to add stronger investor protection, anti-money-laundering and ethics safeguards to the legislation.

State enforcement becomes a Senate sticking point

Some Democratic senators have objected to giving the Department of Justice sole responsibility for enforcing provisions that restrict digital asset activities by public officials. They want state prosecutors to share that authority rather than relying entirely on federal enforcement.

The dispute matters for New York because the state has its own financial laws and an active enforcement record covering crypto companies. Federal preemption could limit how New York and other states apply their existing laws when federal and state standards overlap.

For US investors, the disagreement centers on who can act when a crypto company is accused of fraud. Supporters of state authority argue that local prosecutors provide another route for enforcement, while advocates of a national framework say consistent federal rules could reduce conflicting requirements across states.

The CLARITY Act would establish a broader federal market structure for digital assets and divide oversight responsibilities between the Securities and Exchange Commission and the Commodity Futures Trading Commission. The Senate Banking Committee advanced the legislation 15–9 in May, but Democratic support at the committee stage does not guarantee enough votes on the floor.

Republicans still face a 60-vote hurdle

Senate Majority Leader John Thune is considering starting the floor process before lawmakers leave Washington for the August recess, even though passage before the break appears unlikely.

The process could begin with Thune filing cloture on a motion to proceed. That filing would typically set up a vote two Senate session days later, with at least 60 senators needed to advance.

If cloture succeeds, the Senate could debate the motion for up to 30 hours before voting on whether to formally take up the bill. Clearing that stage would not pass the CLARITY Act, but it would bring the measure closer to a full floor debate.

Republicans hold 53 seats and therefore need Democratic support even if the party remains largely united. Senator Mitch McConnell is expected to remain absent, while Republican Senators Josh Hawley and Rand Paul have not confirmed whether they would support the measure.

Both Hawley and Paul opposed the GENIUS Act during its initial Senate procedural vote in 2025, increasing uncertainty over how many Democratic votes Republicans may ultimately need.

Banking dispute adds pressure before the recess

Stablecoin rewards remain another obstacle in the negotiations. Thune told reporters that lobbying by banking groups over provisions allowing crypto platforms to offer stablecoin yield was affecting the talks.

Banks have argued that yield-bearing stablecoin products could pull deposits away from traditional financial institutions. Crypto companies have resisted broad limits, treating rewards as an important way to attract and retain customers. The same disagreement previously contributed to delays in the market structure talks.

Thune has also indicated that senators could offer numerous amendments if leadership files cloture. Meanwhile, other bills, including the SAVE America Act and proposed sanctions against Russia, are competing for limited floor time.

Charles Schwab has joined crypto industry groups in supporting the CLARITY Act, but James’s warning shows that enforcement powers remain a barrier to a bipartisan agreement. Without a deal on state authority, ethics rules and stablecoin rewards, starting the floor process may expose the Senate’s divisions without producing final passage before the recess.

X Money has begun rolling out to Premium and Premium+ subscribers in the United States, adding deposit accounts, instant transfers, and a Visa debit card directly to the social media platform.

Summary

- X Money offers annual yields of up to 6% and free transfers between users.

- Eligible X Card purchases can earn 3% cashback, with free ATM withdrawals also available.

- A cash sweep program provides eligible users with up to $10 million in FDIC coverage.

- X has not announced support for Bitcoin, Dogecoin, or any other cryptocurrency.

X Money brings banking tools inside the social platform

X Money combines peer-to-peer payments with financial services commonly offered by banks and digital payment applications. Users can send funds instantly to other X accounts without paying a transfer fee.

The service also includes interest-bearing deposit accounts with annual percentage yields of up to 6%. Eligible purchases made through the X Card, a Visa debit card connected to the account, can receive 3% cashback.

Subscribers can receive direct deposits as many as two days early. Other features include wire transfers, checks, free ATM withdrawals, and access to dedicated customer support.

X described the launch as the first peer-to-peer payment service built directly into a US social media platform. The company also claimed it is the first US social network to combine insured deposit accounts, interest earnings, a debit card, and broader payment tools inside its main product.

The rollout is initially limited to Premium and Premium+ subscribers in the United States. X has not provided a timetable for extending the service to free users or international markets.

Cross River Bank powers accounts and transfers

Cross River Bank provides the regulated banking infrastructure behind X Money. The bank holds customer deposits and connects the service to the payment networks needed to move funds.

Cross River operates an application programming interface-based banking system supporting accounts, transfers, and compliance services. The bank said the infrastructure can serve X’s large user base and support additional financial products as the platform expands.

Individual deposits held directly at Cross River receive Federal Deposit Insurance Corporation protection of up to $250,000. X Money also automatically places deposits in a cash sweep program that distributes customer funds among participating insured banks.

Eligible customers can receive aggregate pass-through FDIC insurance of up to $10 million through that program. However, X Payments is not itself a bank or an FDIC-insured institution.

Coverage applies only if a participating insured bank fails and the customer meets all applicable requirements. Users would therefore depend on the underlying banks and the sweep program’s records to establish their eligibility.

X Money uses passkeys to authenticate accounts and allows customers to create individual transaction limits and additional approval requirements. Visa provides security and risk-management protections for transactions completed with the X Card.

Musk previously outlined broader payment ambitions

X owner Elon Musk has discussed turning the platform into a hub for communications and financial services since acquiring the company, then called Twitter, in 2022.

During an internal meeting in October 2023, Musk described payments as covering more than transfers between friends.

“When I say payments, I actually mean someone’s entire financial life,” Musk said.

He added that services involving money or securities could eventually operate through X, arguing that users might no longer need a conventional bank account. The new rollout advances that plan, although its current features continue to rely on regulated banks and established payment networks.

Musk also announced in March that X Money would enter early public access in April. The wider rollout to eligible US subscribers follows that initial testing phase.

Bitcoin and Dogecoin remain outside X Money

Musk has previously supported cryptocurrency payments through his other companies. Tesla began accepting Dogecoin for selected merchandise in 2022, while Musk had earlier proposed allowing users to pay for Twitter Blue subscriptions with DOGE.

He has also described Dogecoin as better suited to routine transactions than Bitcoin, which he views primarily as a store of value. Tesla briefly accepted Bitcoin for vehicle purchases in 2021 before suspending the option over concerns about the energy used for mining.

Those comments have repeatedly fueled expectations that crypto could become part of X’s payment system. However, X has not announced support for Bitcoin, Dogecoin, stablecoins, or any other digital asset within X Money.

Musk has also rejected the idea of an X-issued cryptocurrency. Responding to warnings about unauthorized tokens in 2023, he said X had never launched a crypto token and “never will.”

For now, X Money operates as a dollar-based US financial service supported by Cross River and Visa. Any future crypto integration would require a separate announcement from X.

A federal judge ruled that Minnesota’s law banning prediction markets likely runs afoul of the Commodity Exchange Act, granting a preliminary injunction against the law to Kalshi, Polymarket and the Commodity Futures Trading Commission.

Judge Katherine Menendez, of the U.S. District Court for the District of Minnesota, ruled Monday that Minnesota’s recently passed law that would ban prediction market operators from offering their products in the state seems to be preempted by the federal CEA, and that the companies and federal regulator “are likely to succeed” in showing so after a full trial.

Kalshi, Polymarket and the CFTC sued Minnesota earlier this year after the state passed the law criminalizing the operation of prediction markets, arguing that the statute violated the CFTC’s jurisdiction to oversee “swaps,” which prediction market contracts are structured as.

In her ruling, Judge Menendez said that the three parties had shown they were likely to succeed in their arguments that the law underpinning U.S. commodities exchanges preempts the state law, that the CFTC has jurisdiction over these products and that the plaintiffs would likely succeed on the merits of the case.

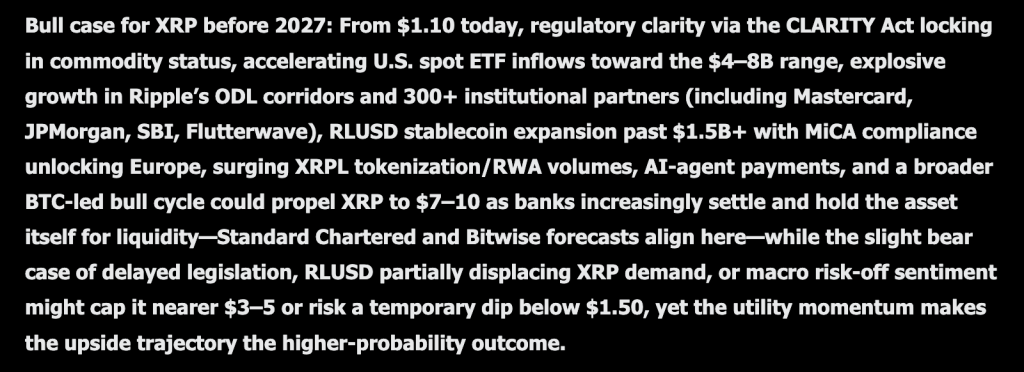

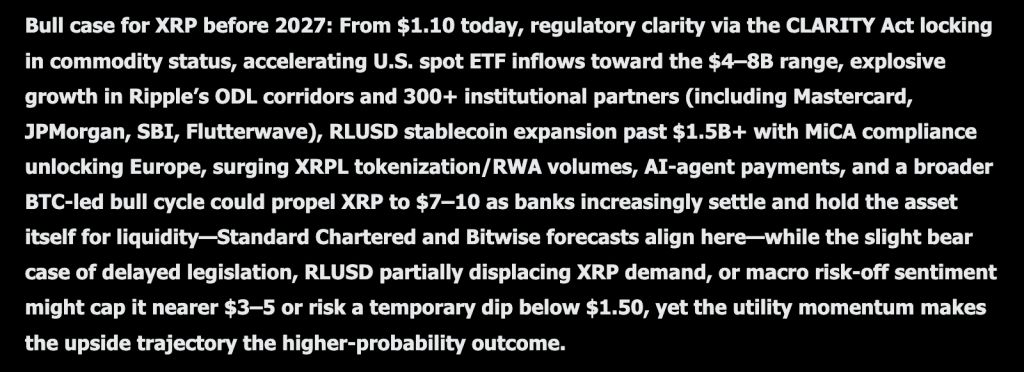

Elon Musk Grok AI is not thinking in quarters for this one either. From $1.10 today, the prediction is a run toward $7 to $10 sometime before 2027, based on the idea that XRP will finally become a bank-held asset rather than just a bank-used rail.

The foundation is regulatory. Grok points to the CLARITY Act, which would lock in XRP’s commodity status and remove the single biggest legal cloud that has hung over this coin for years.

US spot ETF inflows are expected to accelerate toward the $4B to $8B range on the back of that clarity. That kind of institutional plumbing tends to arrive quietly and then show up all at once in the price.

Ripple’s own network numbers back up the utility argument. Explosive growth in ODL corridors, plus more than 300 institutional partners now including names like Mastercard, JPMorgan, SBI, and Flutterwave.

RLUSD stablecoin expansion has pushed past $1.5B, with MiCA compliance opening the door to Europe in a real way. Layer on surging XRPL tokenization and RWA volumes, plus early AI agent payment activity, and Grok sees a network doing meaningfully more than it was two years ago.

The final piece is simply riding the wave. A broader BTC-led bull cycle could pull XRP along with it, and Grok notes that Standard Chartered and Bitwise forecasts land in a similar zone, which is nothing when two independent shops agree on direction.

The bear case is specific rather than dismissive. Delayed legislation, RLUSD partially cannibalizing XRP demand rather than complementing it, or a broader macro risk-off turn could cap the price near $3 to $5, or even force a temporary dip below $1.50.

Grok still calls the upside path the higher-probability outcome, but it does not pretend that the downside scenario is small. A dip below $1.50 from here would erase a meaningful chunk of the current price before any bullish thesis has a chance to play out.

XRP Price Prediction: Five Years Of XRP In One Chart, And It Is Still Fighting The Same Ceiling

Zoom out to the weekly and XRP’s history is really just two enormous spikes separated by long, grinding silence. The 2021 run topped near $1.96, then spent almost three full years drifting between $0.30 and $0.60 with barely any life in it.

Late 2024 changed that completely. Price exploded from under $0.60 to above $3.30 in a matter of weeks, one of the sharpest moves this asset has ever produced, before spending 2025 chopping between $1.80 and $3.65 in a wide, volatile range.

The current pullback has brought XRP back down to $1.10086, up 0.36% for the week, with a range between $1.08229 and $1.16411. That puts the price roughly in the middle of where it sat right before the late 2024 breakout even started.

Support on this weekly chart sits at $1.00, a level that has acted as both a floor and a ceiling multiple times over the last five years. Below that, $0.80 is the next real shelf from the 2025 consolidation.

Resistance is heavier and further away. First at $1.60, then the thick supply zone between $2.20 and $2.60, where the price spent most of 2025 fighting for direction.

Momentum on the weekly is neutral, sitting in the same kind of digestion phase Bitcoin’s own chart is showing right now, which makes sense given how correlated these two assets have become.

For Grok AI $7 to $10 predicts to have any weekly chart support, XRP needs to first reclaim that $2.20 to $2.60 zone that rejected it twice in 2025. Everything above that stays a story about regulation and adoption until the price actually confirms it.

Discover: The best crypto to diversify your portfolio with

Here is what Grok AI Predicts For LiquidChain’s Near Future

Every cycle has a moment where waiting becomes the most expensive decision you can make. That moment is now.

Bitcoin, Ethereum, and XRP are all pinned under the same resistance they have been testing for weeks. The macro unlock is perpetually one data point away. The institutional money keeps arriving next quarter. Large-cap traders waiting for a breakout are queuing for a decision that belongs to someone else entirely.

Grok AI has identified what experienced cycle traders already act on. Capital that registers as statistical background noise at Bitcoin’s market cap can completely reprice a small, undiscovered project.

The asymmetry is not complicated. It lives in the distance between what something is genuinely worth and what the market has currently assigned it. The moment that distance gets noticed, it collapses. Before that moment, it is fully open.

Cross-chain fragmentation has been quietly taxing every DeFi participant since the first bridge went live. Bitcoin, Ethereum, and Solana were engineered independently with zero shared infrastructure and no design intent to communicate.

Every transaction crossing those ecosystem boundaries absorbs the cost of that decision in fees, failed execution, and slippage that hits before settlement even begins. The bridge industry did not fix this problem. It built a business model on top of it.

LiquidChain removes the business model entirely. Three networks unified inside a single execution layer. One deployment reaches all of them simultaneously. No cross-chain tax is extracted from any interaction anywhere.

Grok AI predicts it as a coin worth watching. The presale sits at $0.01454 with just over $860,000 raised.

Execution is unproven. Adoption is an open question. Established assets offer a smoother path toward a ceiling that the entire market can already see. LiquidChain is the entry point that stops existing once the market finds it.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post Elon Musk Grok AI Predicts XRP Price Prediction That Has Ripple Investors Excited appeared first on Cryptonews.

Google Gemini AI is not being subtle about this prediction. From $75 today, the price prediction is $450 to $600 by the end of 2026, a move that would multiply Solana price six to eight times over.

The engine behind it is a single piece of infrastructure. Full deployment of Firedancer, Jump Crypto’s independent validator client, is expected to push network throughput past 1 million transactions per second.

That kind of capacity does more than speed things up. Gemini argues it virtually eliminates the outage risk that has dogged Solana’s reputation for years, positioning the network as the default high frequency execution layer for global finance.

Institutional interest is stacking on top of that technical shift. Potential spot SOL ETF approvals, deep payment integration with names like Visa and Shopify, and dominance in decentralized physical infrastructure networks like Helium and Render all point the same direction.

Gemini also flags something worth sitting with. Solana’s DEX transaction volume routinely outpaces Ethereum’s, which is a real usage metric rather than a speculative one.

The bear case is not vague either. Persistent validator centralization critiques, potential delays in ETF approvals, or aggressive liquidity cannibalization from low fee Ethereum Layer 2s could all cap Solana’s downside near $45 to $50.

Gemini still frames the unmatched consumer app experience, developer density, and enterprise scale as the deciding factors, positioning Solana as the layer 1 asset built to outperform the broader market through 2026.

Solana Price Prediction: SOL Needs A Number It Has Not Touched Since Winter

The daily chart tells a rougher story than the prediction does. SOL topped near $257 in September 2025, and what followed was a mostly uninterrupted decline into a low near $60 by February 2026.

Since that crash, price has spent five months building a wide, choppy range. Two separate rallies, one in December and one in May, both stalled almost exactly at $100, and both rolled over hard afterward.

Today closed at $75.29, up 1.11%, with the session ranging between $74.40 and $75.91. That is a modest green day sitting in the lower half of a range that has trapped this coin since winter.

Support sits at $70, then the June low near $60 that has now held twice. Resistance stacks at $85, then $95, then the persistent $100 ceiling that has rejected every real breakout attempt this year.

Momentum here is neither compressed nor extended, sitting in a neutral zone that reflects a market still deciding whether the June low was the actual bottom. For Gemini’s $450 target to have any grounding, Solana first needs to do something it has failed to do twice in 2026, close above $100 and actually hold there.

That single level is the entire gap between where this prediction lives and where the chart currently sits.

Discover: The Best Crypto to Diversify Your Portfolio

You Might Like What Gemini AI Predicts About This New Layer 3 Called LiquidChain

The money that wins cycles never waits at resistance.

Large caps are stuck. Bitcoin, Ethereum, and XRP keep testing the same ceilings with nothing breaking through. Every macro catalyst has a new arrival date. Every institutional wave has a new quarter attached. Waiting on someone else’s decision is not a trade.

Small market cap infrastructure plays operate on completely different physics. A rotation that vanishes as noise at Bitcoin’s scale reprices an undiscovered project by multiples. The opportunity lies in the gap between what something is genuinely worth and what the market has assigned it. That gap closes permanently the moment discovery happens.

Multi-chain fragmentation is one of the most expensive unsolved problems in DeFi. Bitcoin, Ethereum, and Solana run as completely isolated systems. No shared architecture. No native interoperability. Every time value crosses those boundaries it pays in fees, slippage, and failed transactions.

LiquidChain makes the crossing free. Gemini AI predicts and agrees. All 3 networks within a single execution environment. Single deployment. Complete ecosystem access. No tax on any interaction.

The presale is at $0.01454 with just over $890,000 raised. Early and undiscovered. That combination does not last long.

Explore the LiquidChain Presale

The post Google Gemini AI Predicts Solana Price Could 8x Before End of 2026 appeared first on Cryptonews.

France Records Its First-Ever Pyrocumulonimbus Cloud Amid Record-Smashing Fires

Kforce Inc. (KFRC) Q2 2026 Earnings Call Transcript

Bitmine Accumulates Ether as ETH Beats Bitcoin on Performance

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World7 days ago

Crypto World7 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat6 days ago

NewsBeat6 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech24 hours ago

Tech24 hours agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Tech7 days ago

Tech7 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech7 days ago

Tech7 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

Business6 days ago

Business6 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment6 days ago

Entertainment6 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World5 days ago

Crypto World5 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics13 hours ago

Politics13 hours agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

NewsBeat7 days ago

NewsBeat7 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Sports4 days ago

Sports4 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Sports1 day ago

Sports1 day agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

News Videos4 days ago

News Videos4 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Fashion4 days ago

Fashion4 days ago16 Dresses for the High Summer Event

-

Politics1 day ago

Politics1 day agoSpain sweeps the board at 2026 World Cup with individual awards

-

Entertainment3 days ago

Entertainment3 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

Crypto World7 days ago

Crypto World7 days agoAndrew Cuomo joins OKX board as crypto exchange expands in U.S.

-

News Videos1 day ago

News Videos1 day agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger adds $2.6B as RWA inflows rank second

You must be logged in to post a comment Login