Crypto World

Treasury advances GENIUS Act, tightening illicit-finance oversight

The United States Treasury’s Financial Crimes Enforcement Network (FinCEN) and the Office of Foreign Assets Control (OFAC) have jointly proposed a rule to implement provisions of the GENIUS Act, bringing payment stablecoin issuers under a comprehensive anti-money laundering (AML) and countering the financing of terrorism (CFT) regime. The draft rule would require issuers to establish and maintain AML/CFT programs, implement a formal sanctions compliance program, and possess the authority to block, freeze, or reject certain stablecoin transactions. Under the rule, issuers would be treated as financial institutions for purposes of the Bank Secrecy Act (BSA).

“Bringing stablecoin issuers into full BSA/OFAC compliance effectively turns them into bank-like gatekeepers,” said Snir Levi, CEO of blockchain intelligence firm Nominis. “That means significantly more wallet freezes, transaction blocking and asset seizures at scale.”

The Treasury notice forms part of the GENIUS Act’s implementation, a stablecoin payments framework signed into law by the White House last July. The legislation outlines the regulatory pathway for issuers and is generally viewed as a potential turning point for crypto markets, with the regime slated to take effect 18 months after signing or 120 days after the related regulations are issued by federal authorities.

In parallel, the Federal Deposit Insurance Corporation (FDIC) issued its own proposed rule as part of GENIUS Act implementation. The FDIC noted that while stablecoin holders would not be insured under the act, reserve deposits held by issuers would receive protection. This creates a nuanced layer of risk management for issuers and a different hurdle for users seeking safety for their stablecoin reserves.

Key takeaways

- Regulatory scope expands for stablecoins. Payment stablecoin issuers would be required to run AML/CFT programs, sanctions compliance, and a mechanism to block, freeze, or reject transactions, placing them on a comparable footing with traditional banks under the BSA.

- Issuer as a financial institution. Under the draft framework, stablecoin issuers would be treated as financial institutions for BSA purposes, elevating regulatory scrutiny and enforcement potential.

- FDIC protections limited to reserves, not holders. The FDIC proposal clarifies that stablecoin holders would not be insured, but reserve deposits backing issuers would receive protection, signaling a nuanced risk shield for some stablecoins.

GENIUS Act in motion: what changes for players now

The rulemaking activity underscores a broader shift in how the U.S. authorities intend to oversee digital assets that function as money-like instruments. By requiring AML/CFT programs and sanctions screening, issuers would need to implement robust monitoring, customer due diligence, and rapid response capabilities to comply with OFAC sanctions lists. The “block, freeze and reject” authority enshrined in the proposal is designed to curb illicit finance and align stablecoins with existing fiat- and crypto-related enforcement tools. These capabilities could, in practice, translate into more frequent inter-wallet restrictions and more aggressive response to compliance lapses across issuer networks.

For market participants, the changes mean a heightened compliance burden, with potential impacts on product design, liquidity provisioning, and customer experience. Issuers may need to invest significantly in transaction screening, on-chain analytics, and incident response playbooks to meet the new standards. Regulators, meanwhile, will be watching for practical trade-offs between user accessibility and the prevention of illicit finance, a balance that’s already a recurring topic in crypto policy debates.

Rendezvous with CLARITY and the politics of yield

Even as GENIUS Act implementation unfolds, lawmakers have stalled on a separate front: a broader digital asset market framework often referred to as the CLARITY Act, which cleared the House last year but awaits Senate markup. Industry participants and policymakers have been quietly negotiating around questions of stablecoin yields, tokenized securities, and ethics in crypto markets. The absence of a Senate timetable means the policy landscape remains uncertain, even as regulators press ahead with GENIUS Act rules.

In a recent White House briefing, the Council of Economic Advisers argued that banning stablecoin yields under any future framework would “do very little to protect bank lending,” suggesting that a yield ban would likely impose costs on users without delivering meaningful gains for traditional lenders. The stance illustrates a broader tension: policymakers aim to curb risk and protect the financial system while avoiding measures that could unduly constrain innovation or curtail access to stablecoins for ordinary users. As of now, the Senate Banking Committee has not announced a formal reschedule for markup on the CLARITY Act, leaving the sector in a wait-and-see mode.

What investors and users should watch next

Two strands will shape the near-term trajectory of stablecoin regulation in the United States. First, the GENIUS Act rulemaking process will continue to define the practical obligations for issuers, including the design of AML/CFT programs and the mechanics of sanctions enforcement. Observers will be keen to see how issuers adapt their onboarding flows, risk controls, and transaction controls to fit the regulator’s expectations, and how firms balance user experience with compliance complexity.

Second, the broader regulatory push around digital assets—most notably the status of the CLARITY Act in the Senate and any ensuing executive feedback—will determine whether the sector gains a clearer, predictable framework or remains mired in policy ambiguities. The White House signals that certain approaches to stablecoin governance may be acceptable if they preserve financial stability while fostering innovation, a stance that could influence how agencies and Congress calibrate future measures.

For market participants, the combined effect could be higher compliance costs and tighter operating protocols for stablecoin issuers, along with a more predictable, if still evolving, regulatory baseline. In the near term, attention will center on the timing of the GENIUS Act regulations’ finalization and the political timetable for CLARITY Act actions, as both will shape the pace and shape of stablecoin adoption and risk management in the United States.

As the regulatory clock ticks, stablecoin developers, custodians, and users should stay alert to any shifts in enforcement expectations and the potential for more aggressive takedown or blocking actions in cases of suspected illicit activity. The coming months will reveal how aggressively authorities intend to police on-chain money movement, and whether issuers can align product design with a rapidly expanding compliance regime without sacrificing user access or innovation.

Readers should keep an eye on updates from FinCEN and OFAC as well as the FDIC’s ongoing rules process, which together will illuminate how the GENIUS Act reshapes the operating landscape for stablecoins in the United States.

Grayscale Research has labeled Aave (AAVE) a potential “household name,” describing the Decentralized Finance (DeFi) lending protocol as “a bank without bankers” in a new blog.

“Aave is not yet a household name, but we think it will be eventually. Aave is essentially a bank without bankers—a decentralized lending marketplace on Ethereum and other blockchains that takes deposits and makes loans without any human operators,” Grayscale’s Head of Research Zach Pandl wrote.

Pandl pointed to the Bank of Canada’s report. Researchers found that Aave operates with a notably lower net interest margin (NIM) than leading US and Canadian banks, largely due to its lower intermediation costs.

“The Bank of Canada concluded that ‘lending without traditional intermediaries is viable in a technical and operational sense,’ and that Aave ‘operates continuously, transparently, and with minimal overhead, demonstrating the potential of protocol-based credit markets.’ The combination of lower operational costs, attractive rates, and ‘always on’ banking could be a powerful combination for adoption and long-term growth,” the blog added.

Pandl noted that Aave is still “young” and has yet to address complex challenges like credit scoring and undercollateralized lending. However, no lending system is flawless, as recent stress in private credit markets highlights.

“We believe that Aave, a leading onchain lending platform, and its native AAVE token, are poised for long-term growth,” he concluded.

Follow us on X to get the latest news as it happens

Analyst Nick highlighted the protocol’s strengths in a recent post. It generated approximately $142 million in net revenue in 2025, with cumulative lending volume surpassing $1 trillion. Fees reached over $885 million, putting it on track for a strong run rate into 2026.

Token Terminal data showed its TVL has declined since late 2025 to $42.6 billion in April. Despite this, Aave remains the top lending protocol, controlling around 50% of the market share.

“Aave is becoming the onchain credit layer that survives cycles and pulls in real-world capital imo,” he said.

However, on-chain data paints a more cautious picture. AAVE exchange reserves surged to 2.23 million tokens, reversing a year-long declining trend and signaling potential sell pressure.

Whales have also been offloading the token this year, while recent contributor departures have impacted investor confidence. AAVE trades near $90, down roughly 5% over the past day amid a broader market downturn.

Whether Grayscale’s long-term thesis plays out may depend less on protocol metrics and more on whether market sentiment can catch up to the fundamentals.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Grayscale Predicts This DeFi Token Will Become a ‘Household Name’ in Crypto appeared first on BeInCrypto.

US Federal Reserve members were split on whether the war in the Middle East could spur further interest rate cuts before the end of 2026, according to minutes from the Federal Open Market Committee’s (FOMC) March meeting.

On Wednesday, the Fed released minutes from its last FOMC meeting on March 17 and 18. The meeting ended with an 11-1 vote to keep rates steady at 3.5% to 3.75%, with many officials cautious about the potential impacts of war and what it could mean for the economy.

Amid a risk of further conflicts, the official consensus pointed to a potential rate cut this year, but as Fed officials noted in the minutes, only if inflation does not get out of control.

“Many participants judged that, in time, it would likely become appropriate to lower the target range for the federal funds rate if inflation were to decline in line with their expectations,” according to the Fed minutes.

Rate cuts are generally seen as a positive catalyst for crypto as they free up investment liquidity and can spur demand for speculative investments. The last interest rate cut was Dec. 10, 2025, with the Fed slashing rates by 25 basis points.

While a cut may still be on the table for this year, the general feeling from the FOMC meeting was that it was “too early to know how developments in the Middle East would affect the U.S. economy.”

The FOMC’s next meeting is scheduled for April 28-29.

Cuts still possible, but so are hikes

While some officials were cautiously optimistic about a rate cut, others warned that the opposite might be necessary.

“Some participants judged that there was a strong case for a two-sided description of the Committee’s future interest rate decisions … reflecting the possibility that upward adjustments to the target range for the federal funds rate could be appropriate if inflation were to remain at above-target levels.”

Related: Iran weighing crypto tolls for ships using Strait of Hormuz: Report

Inflation was not the only concern, as many officials pointed to potential downside risks in the labor market, arguing that “in the current situation of low rates of net job creation, labor market conditions appeared vulnerable to adverse shocks.”

According to the CME Group’s FedWatch tool, there is currently a 75.6% chance that the Fed will keep rates at 3.5% to 3.75% during the Fed’s Dec. 8 meeting later this year.

Meanwhile, the chance of a rate cut is 20.4%, while the chance of a rate hike is 2.4% at the time of writing.

Magazine: AI agents will kill the web as we know it: Animoca’s Yat Siu

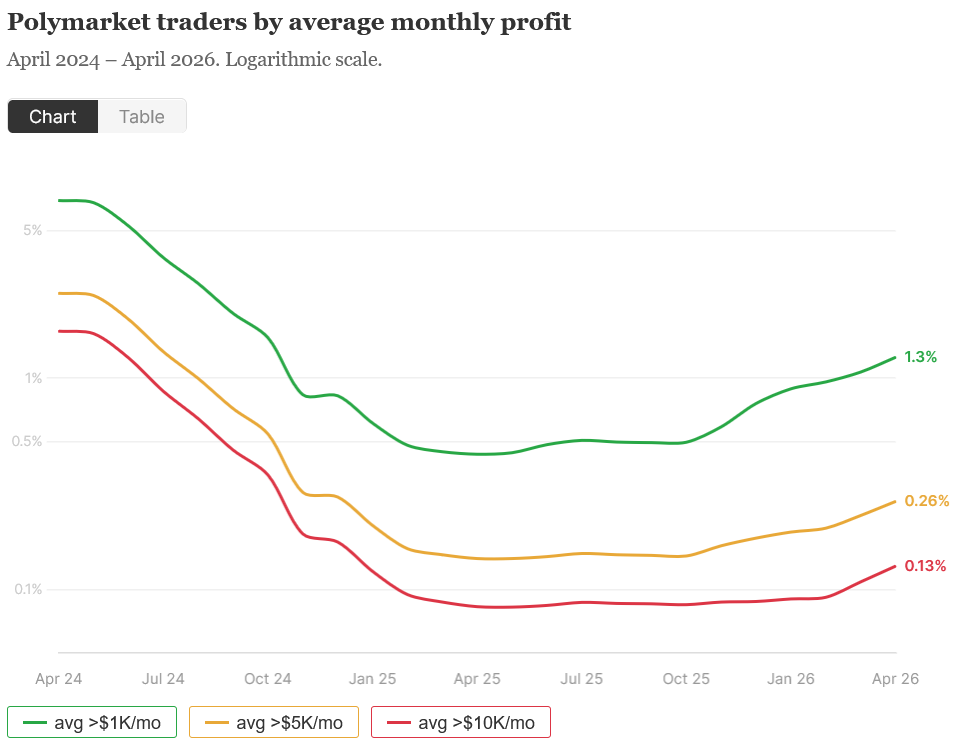

Just 0.015% of Polymarket traders can reliably make $5,000 or more a month, according to new data, meaning the idea of quitting a full-time job to trade prediction markets is unrealistic for most.

Data from crypto analyst Andrey Sergeenkov on Monday found that while nearly 1% of Polymarket traders earned more than $5,000 in a single month, only 0.1% managed to repeat that the following month and just 0.015% were able to sustain it for four consecutive months.

The average US monthly salary is around $5,220, according to Consumer Shield.

Prediction markets have become one of the fastest-growing use cases in crypto, enabling users to speculate on outcomes across politics, sports, finance and cultural events.

Most prediction markets use binary “yes” and “no” shares priced between $0 and $1 that reflect perceived probabilities. Traders can profit by buying undervalued shares and selling higher or holding winning outcomes that settle at $1 when the event has concluded.

Sergeenkov’s findings were framed alongside a report about Logan Sudeith, a former financial risk analyst who quit his job and turned to prediction markets, where he profited $100,000 in December.

Sergeenkov also highlighted an X post from former Messari analyst “Tulip King,” who claimed in November that “Polymarket is the easiest place in crypto to make six figures right now.”

Related: Three Polymarket traders made timely bets on US-Iran ceasefire

However, Sergeenkov’s data found that only 840 wallets (roughly 0.033% of Polymarket traders) have profited over $100,000.

Not all of these wallets would be retail traders, either, as professional traders working at hedge funds and other firms are also trading in prediction markets.

“Less experienced users tend to trade less successfully,” Sergeenkov noted.

Most successful traders make profits and bounce

The more successful traders don’t stick around long either, Sergeenkov said, pointing out that only 172 of 6,600 wallet addresses with average monthly profits above $5,000 remained active more than a year.

“That’s 2.6%,” Sergeenkov said. “Most traders show up, trade for a short period, and leave.”

Sergeenkov’s analysis didn’t come without limitations. The researcher noted that he only factored in realized profits and losses, though he claimed that 96% of trading volume comes from already resolved markets.

Data was taken from April 2024 through to April 1, 2026.

Magazine: Asia Express: Phantom Bitcoin checks, China tracks tax on blockchain

A single geopolitical policy announcement may have just rewritten Bitcoin price prediction. Iran is reportedly requiring ships transiting the Strait of Hormuz to pay tolls in Bitcoin, instantly transforming the world’s most critical oil chokepoint into a live crypto settlement corridor.

According to the Financial Times report confirmed by Bitcoin Magazine, Iran’s Oil, Gas and Petrochemical Products Exporters’ Union spokesperson Hamid Hosseini confirmed the toll is set at $1 per barrel, with a fully loaded supertanker could face a charge approaching $2 million per transit.

Vessels have only seconds to complete payment once approved; the compressed window is explicitly designed so transactions cannot be traced or seized under existing sanctions. The policy applies during a two-week ceasefire window, with empty tankers exempted.

JUST IN: — Watcher.Guru (@WatcherGuru) April 8, 2026

Iran to require ships passing through the Strait of Hormuz to pay tolls in Bitcoin, FT reports. pic.twitter.com/6yoIEys139

Iran to require ships passing through the Strait of Hormuz to pay tolls in Bitcoin, FT reports. pic.twitter.com/6yoIEys139

BTC had already surged past $72,000 on ceasefire news alone, recovering sharply from the $67,000 range where it held during Trump’s April 4 ultimatum weekend. The Hormuz toll announcement adds a second, structurally different catalyst, adding Bitcoin’s role in geopolitical infrastructure.

Discover: The best pre-launch token sales

Bitcoin Price Prediction: Hormuz Toll and Geopolitical Tension

Bitcoin’s technical setup entering this week was already constructive. Price reclaimed $69,000 Monday after volatile swings between $65,000 and $74,000 tied to Operation Epic Fury strike updates and oil price moves.

Support is well-defined as institutional bids have clustered at the $65,800–$66,000 zone, which held during the worst of the escalation fear in early April. Resistance sits at $71,000–$75,000, a range BTC is currently pressing against.

Oil crashed 16% from its $100+/barrel peak as ceasefire signals emerged, a deflationary impulse that historically benefits risk assets. Bitcoin’s resilience relative to equities during the Hormuz escalation period signals decoupling behavior in a bullish structural read.

If the ceasefire holds through the two-week window, Hormuz BTC tolls process live transactions, adoption narrative ignites, and the price can then target $100,000 after, with analysts flagging exactly this level on sustained risk-on sentiment.

The ceasefire expires in approximately 12 days. Every day it holds is a day BTC tolls process, and a day the “Bitcoin as sovereign payment rail” narrative compounds. Tick, tock.

Discover: The best crypto to diversify your portfolio with

Hyper Targets Bitcoin’s Bullish Outlook

Bitcoin at $71,000 is a strong position, but the math of a move to $100K from here represents roughly 40% upside for spot holders. For traders who missed the run from $65K, that asymmetry feels thinner than it looks. The rotation question becomes: where does the upside of early-stage Bitcoin infrastructure lie?

Bitcoin Hyper ($HYPER) is making a case for exactly that allocation. Positioned as the first-ever Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, the project targets Bitcoin’s core structural weaknesses. Bitcoin is known for slow finality, high fees, and the absence of programmable smart contracts.

The SVM integration is the technical differentiator: it delivers sub-second transaction processing, faster than Solana’s base chain itself, with low-cost execution and a Decentralized Canonical Bridge for native BTC transfers.

The presale has raised $32 million at a current price of $0.0136 per $HYPER, with staking available at a high APY during the presale window. If the Hormuz toll story accelerates institutional and retail focus on Bitcoin’s infrastructure layer, early-stage Layer 2 projects absorb that attention before spot BTC does.

Research Bitcoin Hyper here before the presale window closes.

The post Bitcoin Price Prediction: Iran Hormuz Toll Might Spark BTC USD Rally to $100K appeared first on Cryptonews.

Cardano price fell over 5% towards $0.25 on Thursday, paring off a part of its gains seen on the previous day.

Summary

- Cardano price fell 5.7% to around $0.25 as a broader crypto market sell-off triggered profit-taking after the U.S. Iran ceasefire news.

- Nearly $545K in long positions were liquidated over 24 hours, significantly outweighing short liquidations and adding downward pressure.

- Whale wallets holding over 10M ADA rose to a four-month high, signalling continued accumulation despite recent price weakness.

According to data from crypto.news, Cardano (ADA) price fell 5.7% from $0.263 on Wednesday to $0.248 on Thursday morning before settling at the $0.25 mark.

This decline occurred amid a broader sell-off across the cryptocurrency market as investors booked profits after they sold the U.S.-Iran ceasefire news. Bitcoin (BTC), the bellwether asset, was down 1.2% below the $71,000 figure. Ethereum (ETH) fell by 3.4% while other major crypto assets, such as BNB (BNB), XRP (XRP), and Solana (SOL), were all in the red with even more significant losses.

As Cardano price fell, it caught highly leveraged long traders off guard across the derivatives market. Data from CoinGlass show that nearly $545K worth of long positions were liquidated in the past 24 hours, which is nearly nine times the amount of short positions liquidated in the same timeframe.

Long liquidations occur when traders who bet bullish are caught by falling prices and are forced to sell their positions to cover their margins. When long liquidations significantly outweigh short liquidations, the asset’s price often faces intense downward pressure as the forced selling creates a cascading effect.

Despite this volatility, reports indicate that whales are still betting on the token to go up. Notably, data from Santiment shows that the number of whales holding over 10 million ADA tokens has hit a four-month high of 424 at press time. That represents a 5.2% jump over the past nine weeks, a clear sign that whales have been accumulating the token during these dips.

As such, if the whale accumulation trend continues to gain strength, they could attract the attention of retail investors. This, in turn, could potentially change the course of ADA’s current price trajectory.

On the daily chart, Cardano price has entered a horizontal channel pattern where the price was previously trading since early February.

The altcoin broke below the pattern earlier on March 29 as risk-on sentiment withered from the crypto market amidst geopolitical concerns at that time. However, the recent Cardano rebound back into the channel suggests that bulls are attempting to reclaim control.

While the Supertrend indicator still points to some lingering bearishness as it remains red, the MACD line points to a slightly bullish momentum with a bullish crossover while still remaining under the zero line.

For now, the two trendlines of the channel mark the key resistance and support areas for the token. As such, a break below the lower trendline at $0.24 could signal a deeper correction, while if bulls manage to push the price above $0.30, it could spark a fresh rally toward previous highs.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

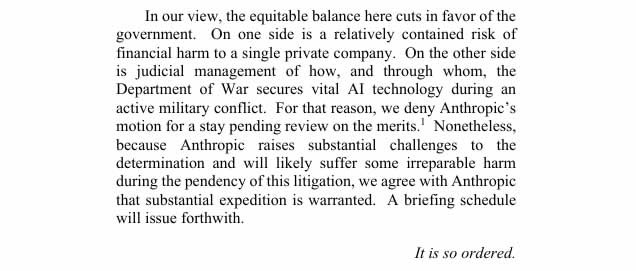

The US Court of Appeals for the DC Circuit rejected Anthropic’s request to pause a Pentagon designation labeling the firm a national security supply chain risk.

The three-judge panel denied the emergency motion for a stay on Wednesday, ruling that the government’s interest in controlling how it secures AI technology during active military conflict outweighed any financial or reputational harm Anthropic may suffer from the label.

The decision means that part of the US Department of Defense’s official designation of Anthropic’s products as a “supply-chain risk to national security” remains in place.

This designation has never been applied to an American company before and also restricts contractors who work with the Pentagon from using Anthropic’s AI models. It could set a chilling precedent for other tech companies that do not comply with government demands.

“In our view, the equitable balance here cuts in favor of the government,” wrote the three-judge panel.

“On one side is a relatively contained risk of financial harm to a single private company. On the other side is judicial management of how, and through whom, the Department of War secures vital AI technology during an active military conflict.”

Challenging the label in two courts

The dispute stems from a deal between the AI firm and the Pentagon in July 2025 on a contract to make Anthropic’s AI model Claude the first large language model approved for use on classified networks.

However, negotiations collapsed in February, with the government seeking to renegotiate and insisting that Anthropic allow military use of Claude without restrictions. Anthropic maintained that its technology should not be used for lethal autonomous weapons and mass domestic surveillance of Americans.

US President Donald Trump ordered all federal agencies to stop using Anthropic products in late February, stating that the company had made a “disastrous mistake trying to strong-arm the Department of War.”

Anthropic sued the Trump administration in March in what it termed an “unlawful campaign of retaliation.”

In late March, the District Court for the Northern District of California ordered a preliminary injunction against the Pentagon over the designation and temporarily halted Trump’s directive, branding it “Orwellian.”

Related: Anthropic limits access to AI model over cyberattack concerns

However, because of the way federal procurement law is written, Anthropic had to challenge the designation on two separate legal tracks — in a California district court on constitutional grounds and directly at the D.C. Circuit under the specific statute that authorized the designation.

The ruling acknowledged that Anthropic will “likely suffer some degree of irreparable harm absent a stay,” and stated that “substantial expedition is warranted.”

Acting US Attorney General Todd Blanche said on X that it was a “resounding victory for military readiness.”

“Military authority and operational control belong to the Commander-in-Chief and Department of War, not a tech company.”

Asia Express: Phantom Bitcoin checks, China tracks tax on blockchain

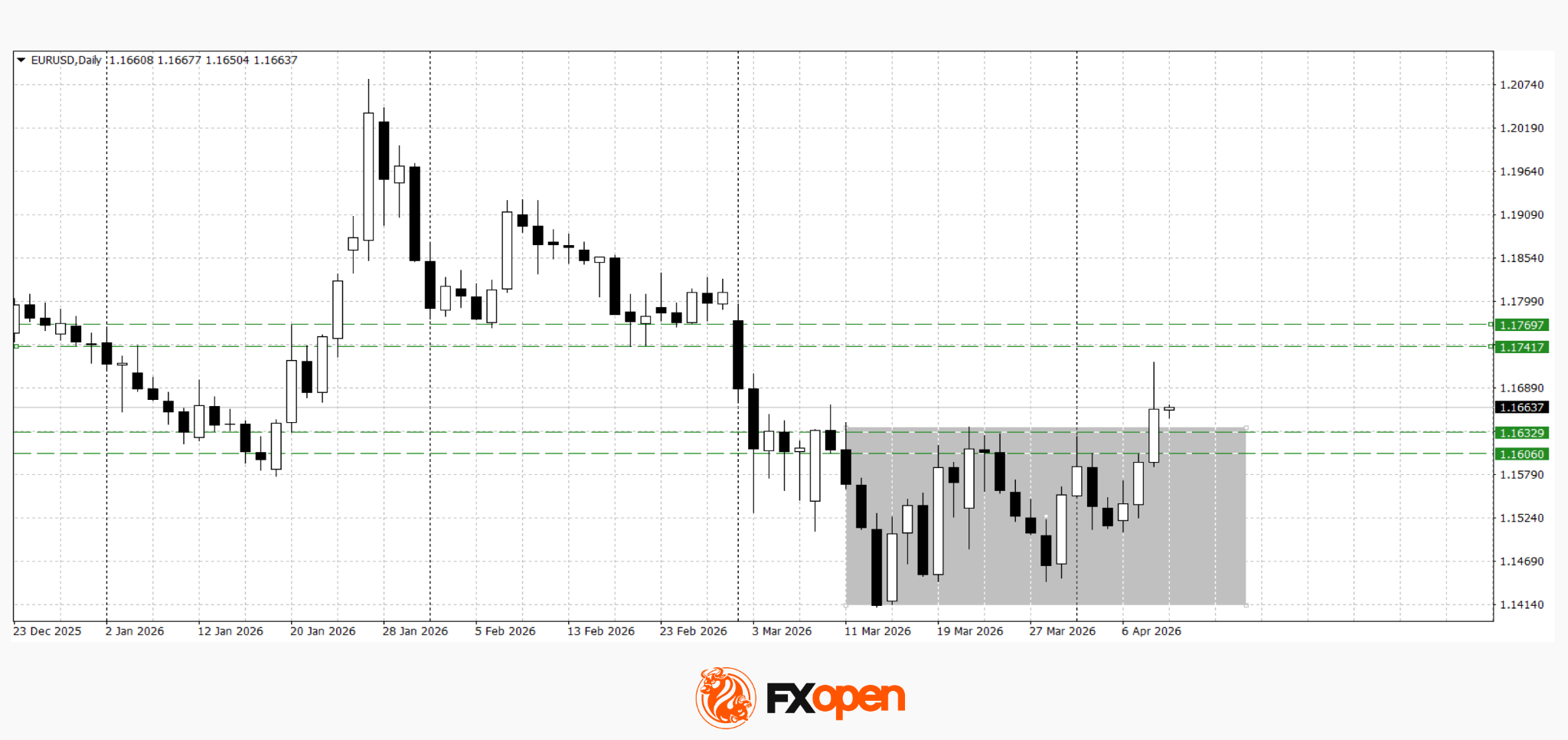

European currencies posted solid gains, while the US dollar came under pressure amid easing geopolitical tensions following reports of a two-week ceasefire agreement between the United States and Iran. Reduced demand for so-called safe-haven assets acted as the primary driver, prompting a reallocation of capital flows towards risk-sensitive instruments and developed market currencies.

Additional pressure on the dollar came from a sharp decline in oil prices, driven by expectations of stabilised supply through the Strait of Hormuz. This has lowered inflation risks and reinforced expectations of a more accommodative stance from the Federal Reserve. At the same time, US Treasury yields declined, further supporting a reassessment of the Fed’s policy outlook. Against this backdrop, money markets are once again pricing in the probability of rate cuts before year-end, limiting the dollar’s recovery potential and reinforcing the current downward momentum.

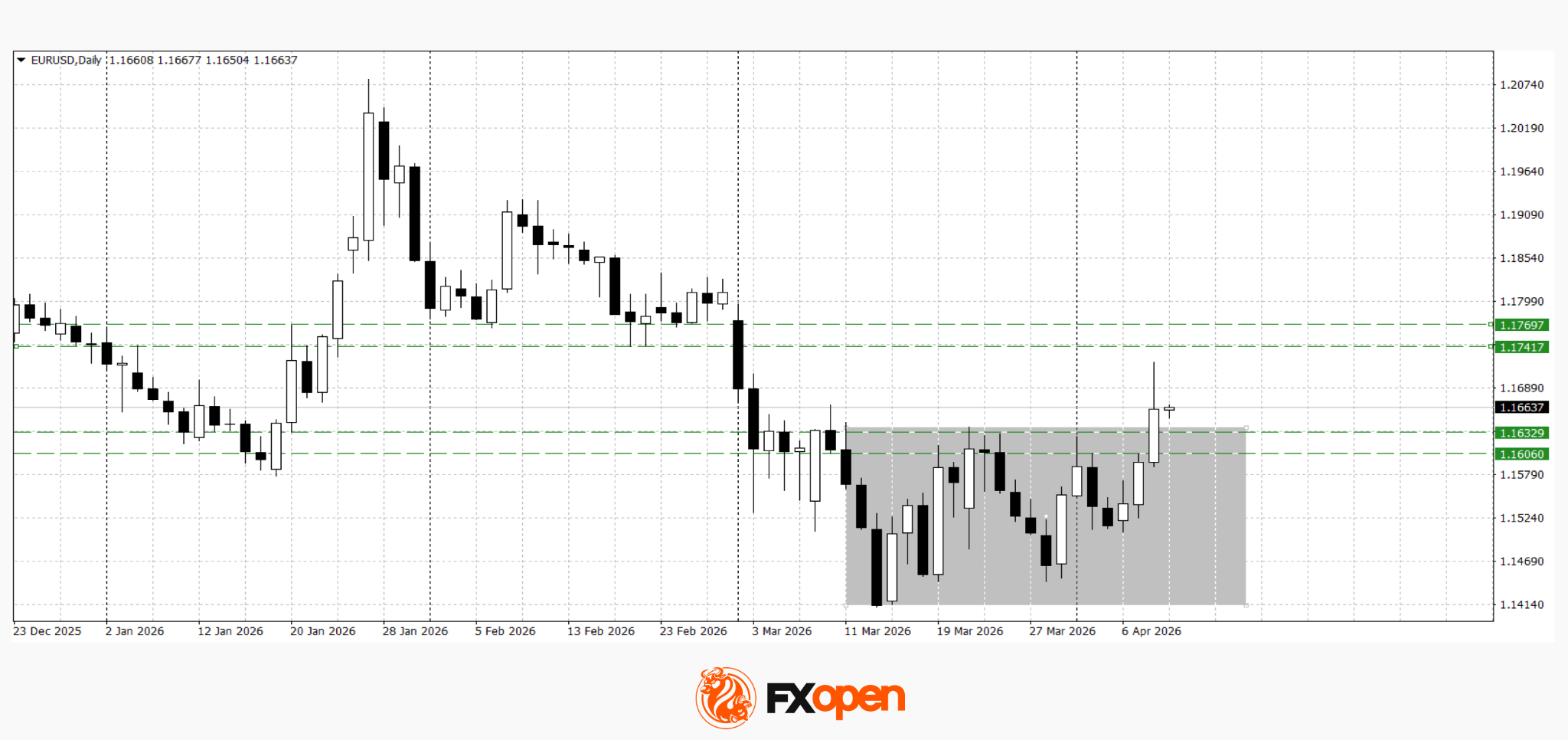

EUR/USD

The EUR/USD pair broke out of its recent range, moving higher in line with broad-based dollar weakness. The price could continue rising towards 1.1740–1.1770. However, a short-term corrective pullback towards former resistance at 1.1610–1.1630 could happen. A daily close below 1.1600 may signal a return to the previous consolidation range.

Key events for EUR/USD:

- Today at 09:00 (GMT+3): German industrial production

- Today at 15:30 (GMT+3): US Core PCE Price Index

- Today at 15:30 (GMT+3): US GDP

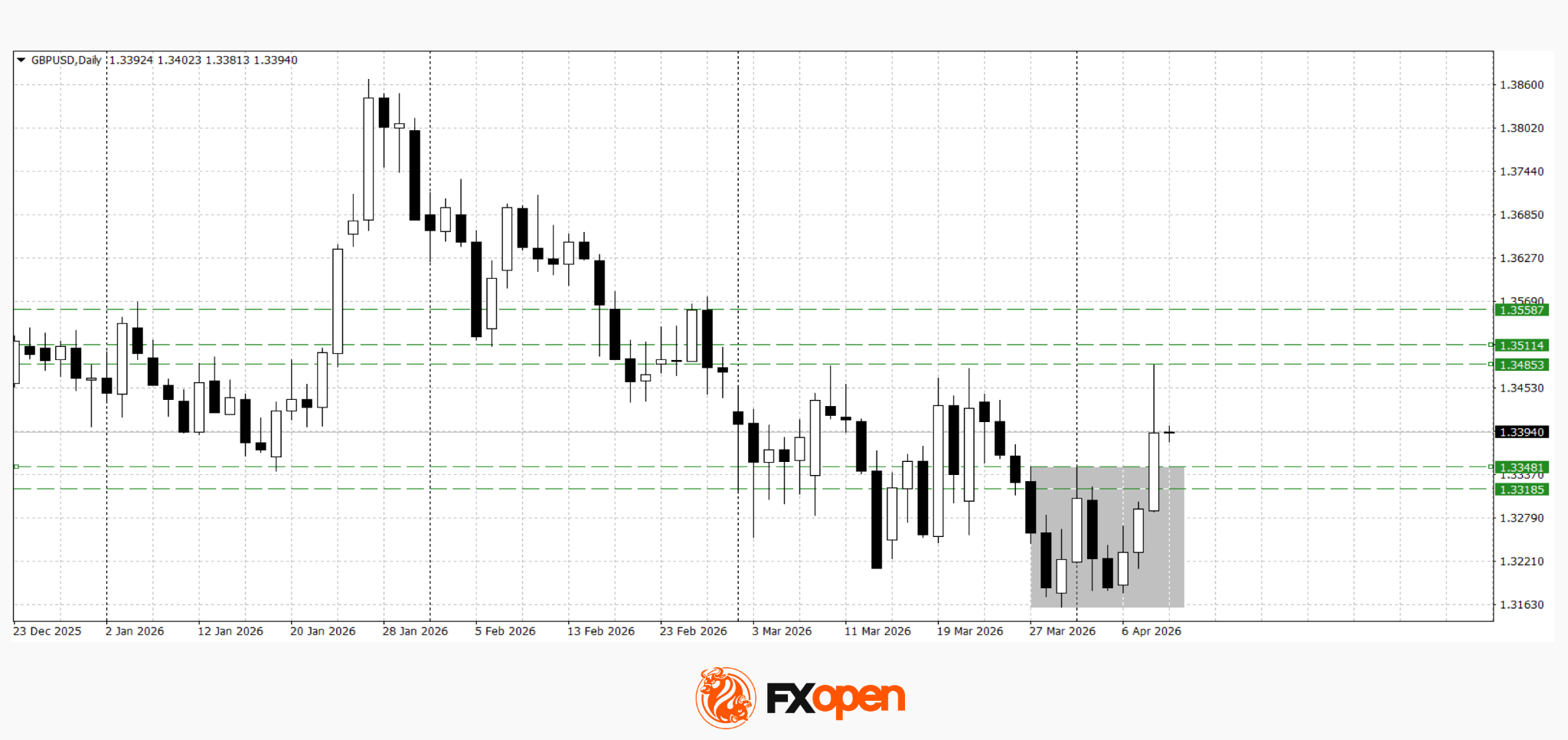

GBP/USD

The GBP/USD pair also broke out to the upside, following the broader trend of dollar weakness. After such a sharp move, a corrective pullback towards the recent highs at 1.3320–1.3350 might be possible. A sustained move above yesterday’s high could open the way for further gains towards 1.3510–1.3560.

Key events for GBP/USD:

- Today at 11:30 (GMT+3): Bank of England Credit Conditions Survey

- Today at 12:00 (GMT+3): UK mortgage rate data

- Today at 15:30 (GMT+3): US initial jobless claims

Summary

The appreciation of European currencies is being driven by a combination of easing geopolitical tensions, declining oil prices, and a reassessment of the Federal Reserve’s policy outlook. The upside breakouts in EUR/USD and GBP/USD reflect a shift in market balance towards risk assets. However, further direction will depend on confirmation from incoming US macroeconomic data. Should downward pressure on yields persist and rate cut expectations strengthen, the dollar may continue to weaken. Conversely, stronger-than-expected data could trigger short-term stabilisation and a return to consolidation.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Asset management firm Canary Capital is looking to launch a spot exchange-traded fund (ETF) tied to the PEPE memecoin.

On Wednesday, Canary filed a Form S-1 for the CANARY PEPE ETF with the US Securities and Exchange Commission. The ETF would track the performance of Pepe (PEPE), with all of the trust’s PEPE held by a custodian.

It noted that the ETF trust may hold up to 5% of the trust’s assets in Ether (ETH) to pay the transaction fees on the Ethereum network.

Canary Capital, which also offers several other crypto ETFs tracking XRP (XRP), Solana (SOL), Hedera (HBAR) and Sei (SEI), has filed for several other niche crypto ETF products in recent months.

In November 2025, Canary Capital filed to launch an ETF tracking the price of a memecoin called Mog Coin, the 353rd-largest crypto token by market cap, far behind PEPE, which is ranked 45th.

PEPE, a memecoin based on Pepe the Frog, gained traction on social media in 2024. The token is roughly 9% the size of the largest memecoin by market cap, Dogecoin (DOGE).

Grayscale’s Dogecoin ETF made its debut in November but fell well short of initial volume expectations. ETF analyst Eric Balchunas predicted at the time that the ETFs would get at least $12 million in volume. However, the ETF only saw $1.4 million on its first day.

The proposed ETF also comes despite the Pepe token, which is down almost 85% from its December 2024 all-time high of $0.00002368, according to CoinMarketCap.

There are currently 513,392 holders of the PEPE, according to Etherscan data. Canary Capital warned investors that ownership of the token is “highly concentrated.” “As of January 2026, the ten largest PEPE wallet addresses collectively held approximately 41% of the total circulating supply,” the filing said.

Altcoin season may hinge on more ETFs launching

Analysts have previously said that the next altcoin cycle may hinge on more crypto ETFs launching further down the risk curve.

However, Matt Hougan, chief investment officer at investment firm Bitwise, said in March that traditional altcoin cycles are over, and that institutional investors are focused on yield-bearing digital instruments or crypto assets that capture revenue.

Fabian Dori, chief investment officer at Sygnum Bank, told Cointelegraph in December that the number of new ETF filings is expected to surge in 2026, driven by US crypto regulations.

Related: Spot Bitcoin ETF inflows top $471M but BTC is pinned under $70K: Here’s why

“On the basis of the potential passing of the Clarity Act, we would expect that new filings continue to go beyond BTC and ETH,” Dori said.

However, the US CLARITY Act has not passed as quickly as industry participants had hoped, largely due to an ongoing disagreement over stablecoin yields.

Canary’s filing warned that regulations in the US for the use of Pepe and the Ethereum network “continues to evolve,” which may impact the use of Pepe and its demand.

Magazine: Asia Express: Phantom Bitcoin checks, China tracks tax on blockchain

Bored Ape Yacht Club creator Yuga Labs has settled its long-running lawsuit with a pair of artists accused of profiting off lookalike NFTs.

According to documents filed in the District Court for the Central District of California on Tuesday, Yuga Labs and artists Ryder Ripps and Jeremy Cahen told the court they had reached a settlement agreement.

As part of the settlement, Ripps and Cahen are permanently banned from using Yuga Lab’s imagery and trademarks and will transfer control of the smart contracts, domains and any remaining NFTs associated with their RR/BAYC project to Yuga Labs within the next 10 days.

The court has also ordered the pair not to “transfer, assign, conceal, or otherwise dispose of any NFTs, domains, accounts, or other assets referenced in this Injunction, or cause any of the foregoing, for the purpose of avoiding or frustrating compliance.”

Legal saga ends after nearly four years

The matter was initially scheduled for a jury trial after a court ruled in favor of Yuga Labs, and Ripps and Cahen appealed the judgments.

Yuga Labs first filed a lawsuit in June 2022, accusing Ripps and Cahen of copying its Bored Ape Yacht Club cartoon ape images, selling lookalike NFTs, and profiting millions as users confused the two projects.

Lawyers acting for Ripps and Cahen argued the RR/BAYC NFTs, first minted in May 2022, were satire and a parody of the real Bored Ape Yacht Club collection and were protected under free speech laws.

Related: Judge tosses lawsuit against Yuga Labs over failure to satisfy Howey test

In April 2023, the court ruled in favor of Yuga Labs and found that Ripps and Cahen had violated copyright laws by creating unauthorized versions of Bored Ape Yacht Club NFTs and ordered them to pay $1.37 million out of their profits, plus an additional $200,000.

The penalty later grew to $9 million after Ripps and Cahen lost a counterclaim in 2024. An appeals court later tossed the judgment in 2025 and ruled that a jury trial was required to resolve the matter and decide whether Yuga’s trademarks were infringed.

Magazine: Asia Express: Phantom Bitcoin checks, China tracks tax on blockchain

Yuga Labs has brought a nearly four-year legal dispute to a close with a settlement that bars its rivals from using its imagery and trademarks and pivots control of the related assets back to the crypto creator. Court filings this week show that Yuga Labs and artists Ryder Ripps and Jeremy Cahen have reached an agreement, ending the long-running case over lookalike NFTs tied to the Bored Ape Yacht Club (BAYC) brand.

Under the settlement, Ripps and Cahen are permanently prohibited from using Yuga Labs’ imagery and trademarks. In addition, they will transfer control of the RR/BAYC smart contracts, domain names, and any remaining NFTs associated with the RR/BAYC project to Yuga Labs within the next 10 days. An injunction from the court also restricts the pair from transferring, concealing, or disposing of any linked assets to evade compliance.

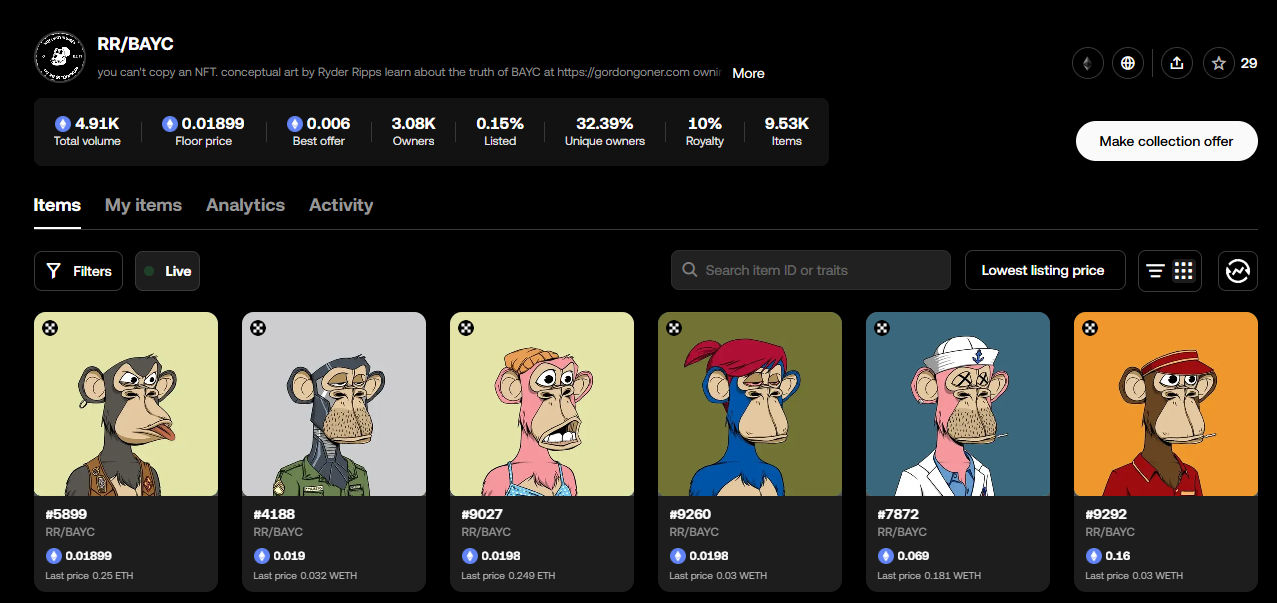

The RR/BAYC NFTs themselves remain accessible for holders and curious onlookers; as of this writing, they are still live on OKX Wallet, underscoring how the asset layer sits at the intersection of branding protection and active markets. OKX Wallet’s NFT collection page for RR/BAYC provides a live snapshot of those tokens still circulating in wallets.

Key takeaways

- The dispute over lookalike BAYC imagery ends with a settlement that imposes a permanent ban on using Yuga Labs’ branding and requires asset transfers to Yuga Labs within 10 days.

- The settlement closes a saga that stretched from a June 2022 filing through multiple court rulings, reversals, and appeals, including a 2023 ruling favoring Yuga and a subsequent shift in judgments on damages and trademark questions.

- Despite the injunction and transfers, RR/BAYC NFTs continue to function on live marketplaces, illustrating the persistence of lookalike projects in secondary markets even after legal action.

- The case highlights how IP enforcement plays out in NFT ecosystems, where branding and originality are central to project value and user trust.

Settlement marks a culmination of a high-stakes IP fight

The legal entanglement began when Yuga Labs filed suit in mid-2022, alleging that Ripps and Cahen copied BAYC’s distinctive ape artwork and sold lookalike NFTs to profit from brand confusion. The plaintiffs argued that the mimicry undermined Yuga Labs’ IP rights and damaged the value of the original BAYC ecosystem.

Earlier in the litigation, a court sided with Yuga Labs, finding that Ripps and Cahen had created unauthorized versions of BAYC NFTs and ordered the pair to pay damages. The initial judgment set damages at $1.37 million plus $200,000, tied to profits from the infringing NFTs. The post-judgment landscape grew more complex as outcomes from subsequent proceedings added layers of appeal and retrial expectations.

In 2024, the court’s order expanded the penalties, and the total rose to about $9 million after Ripps and Cahen lost a counterclaim related to the matter. An appeals court later tossed that judgment in 2025, ruling that a jury trial would be necessary to determine whether Yuga Labs’ trademarks had been infringed and to resolve related issues. The latest settlement then brings the case to a close, avoiding a further retrial while preserving the injunctions against the defendants.

What this means for IP in NFT ecosystems

The resolution underscores an important precedent for how branding and copyright claims are treated in the NFT space. Yuga Labs has repeatedly asserted that protecting its avatar-based IP is essential to maintain product integrity and user trust across a fast-evolving market. The settlement affirms that such protections can be backed by enforceable injunctions and asset transfers, even as markets continue to trade lookalike or derivative tokens in parallel to legitimate projects.

From an investor and builder perspective, the outcome reinforces a critical point: brand equity in digital collectibles matters as much as the underlying code and artwork. Projects seeking to capitalize on a well-known IP must navigate not only smart-contract functionality but also the legal boundaries of trademark and copyright. The case also demonstrates that even when a lookalike project garners attention and liquidity, the original IP owner may pursue a legal remedy that includes branding restrictions and asset handovers.

Transient markets meet durable rights

The fact that RR/BAYC NFTs remain visible on major wallets and marketplaces despite the injunction speaks to a nuanced dynamic in crypto markets. While the court order restricts the use of Yuga Labs’ branding and directs the transfer of domain and contract control, the assets already minted and circulating in wallets can continue to trade unless further restrictions are imposed by platform policies or additional court actions. This tension—between legal rights and ongoing market activity—illustrates how IP enforcement interacts with decentralized liquidity and public recordkeeping in real time.

For traders, holders, and creators, the settlement signals a potential re-emphasis on authenticating provenance and respecting IP boundaries before minting or marketing derivative projects. It also raises questions about how future settlements might structure ongoing obligations, such as royalties, licensing, or clear demarcations between parody, satire, and infringement in the NFT landscape.

What to watch next

With control of the RR/BAYC assets transferring to Yuga Labs within about a week, observers will want to track how the company integrates these elements back into its ecosystem. Will there be additional revivals or revocations tied to RR/BAYC tokens, and how will platforms handle branding-sensitive content tied to a well-known IP? The ongoing governance and ecosystem implications for BAYC’s broader community, as well as for other IP-heavy NFT projects, will be worth monitoring as more settlements of this type appear in the crypto legal arena.

Additionally, the market for lookalike NFTs in the wake of this case may reflect evolving risk assessments among buyers and traders. Even with a favorable outcome for IP owners, the persistence of lookalikes in wallets and marketplaces suggests a continuing need for diligence on authenticity and provenance in NFT collections.

As this saga concludes, investors can expect closer scrutiny of branding and copyright claims in NFT launches and a clearer path for IP holders to pursue enforcement when necessary. The case serves as a reminder that in the rapidly expanding NFT space, the boundaries of legal rights and market activity are increasingly intertwined, and that regulatory and judicial clarity will continue to shape how projects operate and compete.

Source data and developments referenced here draw on filings and reporting surrounding the settlement announced this week, including the permanent injunction barring use of Yuga Labs’ imagery and trademarks and the transfer timeline for RR/BAYC assets. The live RR/BAYC NFT collection, as noted, remains accessible on OKX Wallet during this transition.

British boy, 9, stuck abroad after distraught family told he can’t return home with them

Rupee at risk? BOP pressure, oil shock and capital flows hold the key, says Rahul Bajoria

Grayscale Predicts This DeFi Token Will Become a ‘Household Name’ in Crypto

-

NewsBeat7 days ago

NewsBeat7 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business6 days ago

Business6 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business5 days ago

Business5 days agoExpert Picks for Every Need

-

Business3 days ago

Business3 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports4 days ago

Sports4 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech1 day ago

Tech1 day agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business4 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion3 days ago

Fashion3 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Tech7 days ago

Tech7 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Politics6 days ago

Wings Over Scotland | The quality of mercy

-

Business4 days ago

Business4 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion6 days ago

Fashion6 days agoStatement Sunglasses: The Accessory Shaping Modern Fashion

-

Sports7 days ago

Justin Jefferson’s Situation Remains Unchanged after JSN’s Deal

-

Politics6 days ago

Politics6 days agoEast Jerusalem Palestinian families eviction orders

-

Fashion7 days ago

Fashion7 days agoThursday’s Workwear Report: Merino Wool Blend Short-Sleeved Sweater

-

Fashion6 days ago

Fashion6 days agoFor Love & Lemons’ Spring 2026 Line is for the Romantics

-

Crypto World18 hours ago

Crypto World18 hours agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Fashion7 days ago

Fashion7 days agoCoffee Break: Santa Croce Tote

You must be logged in to post a comment Login