Crypto World

Trump Sues JPMorgan, CEO Dimon for $5B Over Debanking

Join Our Telegram channel to stay up to date on breaking news coverage

US President Donald Trump sued JPMorgan Chase & Co. and its chief executive officer, Jamie Dimon, for at least $5 billion, alleging that the lender stopped offering him and his business banking services for political reasons.

According to the complaint filed on Thursday, Trump accuses the bank of trade libel and breach of the implied covenant of good faith. It also states that Dimon violated Florida’s Deceptive and Unfair Trade Practices Act.

BREAKING: Trump sues JPMorgan Chase and CEO Jamie Dimon for $5B over alleged ‘political’ debanking

“President Donald Trump is suing JPMorgan Chase and its CEO Jamie Dimon in a $5 billion lawsuit filed Thursday, accusing the financial institution of debanking him for political… pic.twitter.com/9LQPYFJBoF

— Steve Guest (@SteveGuest) January 22, 2026

The lawsuit, filed in Miami-Dade County court in Florida, alleges that JPMorgan abruptly closed multiple accounts in February 2021 with just 60 days’ notice and no explanation.

By doing so, Trump claims JPMorgan and Dimon cut the president and his businesses off from millions of dollars, disrupted their operations, and forced them to open bank accounts elsewhere urgently.

However, JPMorgan has since denied all allegations. “While we regret that President Trump has sued us, we believe the suit has no merit. We respect the President’s right to sue us and our right to defend ourselves – that’s what courts are for,” said a JPMorgan spokesperson.

Meanwhile, the Trump family has continued to reiterate that the banks had debanked his family for political reasons.

Trump And The Fight Against Debanking

Since retaking office, Trump has signed an executive order against debanking. His appointed regulators, including Comptroller of the Currency Jonathan Gould, have similarly warned banks against engaging in any activities that appear to be debanking, a concern the crypto industry at large has had over the past few years.

“You shouldn’t be debanked,” Trump said to reporters while aboard Air Force One on Thursday. “It’s so wrong. I don’t know what their excuse would be. Maybe their excuse would be the regulators.”

Trump on JPMorgan Chase CEO, Jamie Dimon:

“He de-banked me. I guess it’s a good lawsuit because every pundit has come out and said Trump has a great lawsuit here. You’re not allowed to do what they did.”pic.twitter.com/bC9zOMygwX

— Red Line News (@RedLineNewsUSA) January 22, 2026

Meanwhile, the family has since turned to crypto as a hedge.

“We got into crypto because we were debanked,” Donald Trump Jr. said in a Fox News interview last year. “We had to come up with solutions,” he continued, adding that crypto was the most efficient way to go and “absolutely the future of banking.”

Related News:

Best Wallet – Diversify Your Crypto Portfolio

- Easy to Use, Feature-Driven Crypto Wallet

- Get Early Access to Upcoming Token ICOs

- Multi-Chain, Multi-Wallet, Non-Custodial

- Now On App Store, Google Play

- Stake To Earn Native Token $BEST

- 250,000+ Monthly Active Users

Join Our Telegram channel to stay up to date on breaking news coverage

The South Korean central bank has called for cryptocurrency exchanges to implement their own “circuit breakers” to pause trading and prevent market panic after a clerical error at Bithumb led to the accidental transfer of $42 billion in Bitcoin to its customers.

Summary

- The Bank of Korea is urging the government to mandate trading curbs on cryptocurrency platforms to prevent market destabilization caused by operational failures.

- The central bank reports that the lack of internal controls led to a February incident where Bithumb accidentally distributed $42 billion in Bitcoin due to a clerical error.

- New regulatory proposals suggest that exchanges should implement automated systems to detect human mistakes and verify internal asset balances against the blockchain in real time.

The Bank of Korea (BOK) stated in a payments report released Monday that officials should adopt trading curbs modeled after the Korea Exchange to freeze activity during sudden price swings.

This recommendation follows a massive clerical error in February, where Bithumb, one of the country’s largest platforms, accidentally distributed over $40 billion in Bitcoin to its users.

The central bank highlighted a significant gap in oversight between digital asset platforms and traditional finance. “Currently, the virtual asset industry lacks internal control mechanisms and faces lower regulatory intensity compared to established financial institutions,” the BOK noted.

Officials argued that new rules are essential to prevent a repeat of recent disruptions, stating, “Consequently, as similar incidents could occur at other virtual asset exchanges, it is necessary to strengthen relevant regulations to prevent them in advance.”

The proposal arrives as South Korean legislators work on a new regulatory framework for the industry. The BOK urged that these specific safety measures be woven into the upcoming laws “to enhance the safety and transparency of virtual asset exchange operations.”

The Bithumb incident

The push for reform stems from an early February event where Bithumb mistakenly sent out 620,000 Bitcoin—valued at roughly $42 billion at the time—to customers. The error occurred when the system processed a transfer as cryptocurrency instead of the intended 620,000 Korean won, a sum worth only about $400.

The massive influx of coins triggered an immediate market crash on the platform. As recipients began selling their windfall, other investors panicked, further dragging down the price.

While Bithumb managed to halt trading and reverse most of the transfers within minutes, 1,788 BTC had already been liquidated. The exchange had to use its own corporate reserves to cover the resulting $125 million shortfall.

To mitigate such risks, the central bank suggested that platforms must deploy systems specifically designed to catch “erroneous payments caused by human error.”

The report also recommended a requirement for exchanges to run automated checks that sync internal records with blockchain data to immediately spot any asset discrepancies.

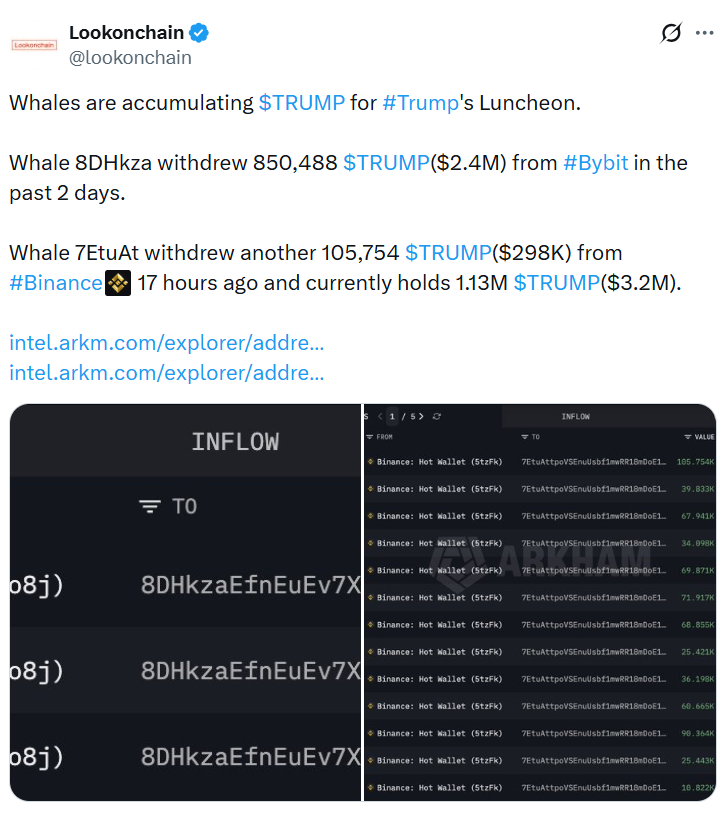

Crypto whales have continued to load up on the TRUMP memecoin ahead of the luncheon at US President Donald Trump’s Mar-a-Lago residence in Florida this month, which offers entry to the largest holders.

One whale withdrew about 105,754 TRUMP from Binance on Saturday to add to its stash of 1.13 million TRUMP, worth about $3.2 million, according to blockchain analytics firm Lookonchain said in an X post on Sunday.

Two days earlier, another whale withdrew 850,488 Trump from the crypto exchange Bybit.

On Monday, another holder increased their TRUMP stash to more than 368,000 tokens after withdrawing from BitMart, and a fourth whale boosted their stash to over one million tokens after withdrawing from Bybit, according to blockchain explorer Solscan.

Critics have accused Trump of using his position as US president for personal financial gain through the scheme. Democratic lawmakers have introduced bills to limit political influence and profits from memecoins.

The top 297 token holders are invited to a luncheon on April 25 at Trump’s Mar-a-Lago residence. The event has billed the president as the keynote speaker and offered a private reception for the top 29 holders, despite the White House Correspondents’ Association Dinner in Washington, D.C., being the same day.

TRUMP drops 33% since March announcement

Trump’s announcement of the luncheon in March saw TRUMP spike more than 50% to a peak of $4.35. However, the memecoin has since dropped by over 33% to trade at $2.80 as of Monday, according to CoinGecko.

Dominick John, an analyst at Zeus Research, told Cointelegraph the price is likely being pushed lower as retail-driven market selling overwhelms already thin liquidity, forcing continuous repricing.

“At the same time, insider supply overhang means even small distributions from concentrated wallets can absorb whale bids, limiting any meaningful upside follow-through,” he added.

Crypto data analytics platform CoinCarp lists 642,882 TRUMP holders, with over 91% of the supply concentrated among the top 10 wallets and over 97% among the top 100 wallets.

Token spiked after the crypto gala announcement last year

Trump held his first “crypto gala” dinner in May 2025, a few months after his Jan. 20 inauguration as US president, which drew concern from critics who accused him of using his position for personal financial gain.

Related: Bessent ramps up pressure on Congress to pass CLARITY Act

The token peaked at $15.59 about a month before the event, but fell as the event drew closer, gradually falling to $8.90 a month after the event.

John said this time around, the token could stage a recovery, with the 2026 midterms acting as a potential sentiment multiplier and other positive announcements. Catalysts and early signs of institutional accumulation could help establish a floor and trigger reflexive upside, he said.

“One catalyst to watch is the potential for event-driven launches like the Trump Billionaire Game, which could generate the social buzz needed to drive short-term upside momentum,” John added.

Magazine: Bitcoin quantum-safe without upgrade? CZ’s 2031 crypto vision: Hodler’s Digest, April 5 – 11

Key Takeaways

- A cybercriminal created 1 billion unauthorized bridged DOT tokens on Ethereum through a fraudulent message exploit

- The illegitimate tokens were liquidated in a single swap, generating approximately 108.2 ETH (roughly $237,000)

- The security breach involved the Hyperbridge gateway smart contract operating on Ethereum

- Polkadot’s core relay chain and authentic DOT tokens remained completely secure

- Shallow liquidity in the bridged token market prevented more substantial financial losses

A malicious actor capitalized on a security flaw within the Hyperbridge gateway smart contract deployed on Ethereum, creating 1 billion bridged Polkadot tokens through unauthorized means.

Cybersecurity monitoring company CertiK identified and reported the breach. Their analysis revealed the perpetrator deployed a fabricated message to assume administrative privileges over the bridged DOT token contract operating on Ethereum.

https://twitter.com/CertiKAlert/status/2043557571609731268?s=20

Leveraging these elevated permissions, the hacker generated 1 billion tokens through a single malicious transaction.

Onchain analytics platform Lookonchain documented that this massive token supply was immediately liquidated through one comprehensive transaction.

[[LINK_START_1]]https://twitter.com/lookonchain/status/2043558598111048126?s=20[[LINK_END_1]]

The perpetrator obtained 108.2 ETH from this mass sale, valued at approximately $237,000 during the transaction.

This comparatively modest profit demonstrates the shallow liquidity available for the bridged asset on Ethereum.

Since the wrapped variant had minimal holders and trading volume, the market lacked sufficient depth to purchase a billion tokens at anything approaching fair value.

Scope of Impact Analysis

The security incident exclusively affected the Ethereum-based representation of DOT and did not compromise Polkadot’s primary relay chain infrastructure. The legitimate DOT cryptocurrency on the Polkadot ecosystem sustained zero damage.

Only the synthetic, cross-chain representation of DOT existing on [[LINK_START_0]]Ethereum[[LINK_END_0]] fell victim to this attack.

Bridged cryptocurrencies serve as blockchain-agnostic representations of native assets. Their integrity relies entirely on the security architecture of underlying smart contracts.

The Hyperbridge infrastructure facilitates interoperability between disparate blockchain networks. A security weakness in its gateway contract seemingly provided the vulnerability exploited in this incident.

Official Responses and Ongoing Analysis

At the time this report was compiled, neither Polkadot’s development team nor Hyperbridge protocol operators had released formal public statements.

The precise technical methodology employed remains under investigation. Complete confirmation of the attack vector is pending.

Cross-chain bridge exploits and interoperability infrastructure vulnerabilities have emerged as persistent security challenges throughout the cryptocurrency ecosystem.

For this particular incident, the monetary impact remained relatively contained when compared against other bridge compromises, where malicious actors have successfully extracted hundreds of millions in digital assets.

CertiK’s preliminary assessment identified message forgery as the technique enabling administrative privilege escalation, though comprehensive post-incident analysis documentation has not yet been published.

Current verified data confirms the attacker’s wallet address collected 108.2 ETH following the token liquidation, with no additional malicious activity detected at publication time.

Aave Labs is set to receive a massive capital injection following the approval of a strategic roadmap designed to scale the protocol.

Summary

- The Aave DAO has approved a $25 million stablecoin grant and a 75,000 AAVE token allocation for Aave Labs to fund ongoing protocol development.

- Aave Labs will transition to a DAO-funded operating model where revenue from specific products flows directly into the treasury rather than being retained by the core team.

- The approved framework establishes Aave V4 as the long-term technical foundation and introduces a new governance structure to manage the protocol brand and institutional expansion.

According to the governance dashboard, the Aave DAO voted on Saturday to grant the development team $25 million in stablecoins and 75,000 AAVE tokens. The funding, part of the “Aave Will Win” framework, passed with roughly 75% support.

The stablecoins will be distributed over the next 12 months to cover operational costs, while the token package will vest over a four-year period to keep developers incentivized.

This decision changes how the protocol handles its finances. Under the new model, revenue from products like Aave Pro will go directly to the DAO treasury rather than staying with Aave Labs.

In exchange, the DAO takes over the responsibility of funding the lab’s core operations. The protocol, which currently holds over $25 billion in total value locked, also officially recognized Aave V4 as its long-term technical architecture.

Founder Stani Kulechov described the move as a defining moment for the ecosystem.

“Aave Will Win is the most important proposal in Aave’s history and it just passed with a landslide,” Kulechov shared on X.

“If you own AAVE, you own not just the economic rights of the protocol, but the brand, the users, and the integrations,” he added.

Aave Labs noted that the industry is changing as traditional fintech firms and institutions move on-chain. With regulatory clarity improving in several regions, the team plans to focus exclusively on Aave-linked products to stay ahead of the competition. They believe the winners of the next decade will be the ones who can capture new markets quickly.

Despite the successful vote, the path to approval was not without tension. Some community members questioned the sheer size of the $25 million package and the voting power tied to the 75,000 tokens. These disagreements previously led the Aave Chan Initiative, a prominent delegate, to scale back its involvement with the DAO, citing concerns over how the proposal process was handled.

Looking ahead, the framework also includes plans for a new foundation to manage the Aave brand. This follows a failed attempt in January to transfer intellectual property to the DAO, a topic that has sparked ongoing debate about how much control the community should have over the protocol’s identity. Future grants for specific product launches will still require separate votes from the DAO.

Polkadot’s (DOT) bridged token on Ethereum has reportedly fallen victim to an exploit. According to reports, an attacker minted 1 billion bridged DOT.

Onchain tracker Lookonchain noted that after this, the attacker dumped the entire supply in a single transaction, netting 108.2 ETH (approximately $237,000).

Follow us on X to get the latest news as it happens

Blockchain security firm CertiK flagged the exploit targeting the Hyperbridge gateway contract. An attacker used a forged message to gain unauthorized control. According to the firm, the attacker was able to manipulate the admin role of a Polkadot token contract on Ethereum, enabling the minting of 1 billion tokens.

The attack did not compromise Polkadot’s native relay chain or the DOT token on Polkadot itself. It targeted only the bridged, or wrapped, representation of DOT.

The incident raises fresh concerns about crypto security. Neither Polkadot nor Hyperbridge had issued an official response at the time of writing. This is a developing story, and further details will be updated as more information becomes available.

The post Bridged Polkadot Reportedly Hit by Exploit as Attacker Mints 1 Billion DOT Tokens appeared first on BeInCrypto.

The European Central Bank has thrown its weight behind a proposal to give the EU’s markets watchdog direct control over the continent’s largest crypto firms.

Summary

- The European Central Bank has endorsed a plan to transfer oversight of large crypto firms and cross-border trading platforms to the European Securities and Markets Authority.

- The central bank warned that centralized supervision is necessary to prevent financial shocks from migrating into the traditional banking system as the two sectors become increasingly linked.

- Implementation of the new regime faces opposition from member states like Malta that argue the current regulatory framework is too new to be overhauled.

The ECB issued a formal opinion on Friday stating that it fully supports moving the oversight of “systemically important” cross-border entities, including major trading platforms and crypto-asset service providers (CASPs), to the European Securities and Markets Authority (ESMA).

According to the central bank, these proposals “constitute an ambitious step towards deeper integration of capital markets and financial market supervision within the Union.”

While the opinion does not legally bind lawmakers, it provides significant political momentum for what would be the most substantial change to EU digital asset rules since the Markets in Crypto-Assets (MiCA) framework began its rollout in 2023.

Curbing “forum shopping” in the crypto sector

Under current MiCA rules, crypto firms can obtain a license in a single EU member state and then “passport” those services across the entire bloc. This setup has led to a fragmented landscape where companies select specific countries based on favorable local oversight.

For instance, Kraken operates out of Ireland, while Coinbase and Bitstamp are based in Luxembourg. Bitpanda maintains its primary presence in Austria, though its asset management division is registered in Germany.

The central bank argues that “transferring authorisation, monitoring and enforcement powers for all CASPs” from national bodies to ESMA would “ensure supervisory convergence, reduce fragmentation and mitigate cross-border risks in crypto-asset markets, thereby supporting financial stability and the integrity of the single market.”

Opposition to the change has emerged from countries like Malta, a prominent hub for digital asset firms. Critics there argue the move is premature, noting that specific MiCA requirements for service providers only became fully active in December 2024.

The ECB, however, pointed to the growing ties between traditional lenders and the crypto industry as a reason for urgency. It warned that banks offering crypto services or partnering with digital asset firms could allow volatility to transmit “shocks into the financial system.”

To prevent this, the bank highlighted “the need for a centralised Union supervisory regime for CASPs, capable of addressing the systemic risks posed by CASPs with significant activities, preventing risk migration into the banking system and safeguarding financial stability.”

For the plan to succeed, the ECB noted that ESMA must receive enough funding and personnel to manage the increased workload of policing the sector. The proposal now moves to a period of negotiation between EU governments and lawmakers, meaning it will likely be several months before the changes are finalized in law.

Bitcoin’s (BTC) price dropped nearly 3% since the weekend after US-Iran ceasefire talks failed in Islamabad.

The largest cryptocurrency slipped below $71,000 today. It was trading at roughly $70,960 at press time.

On-Chain Data Reveals a Wealth Transfer as Bitcoin Drops on US-Iran News

However, on-chain data tells a different story beneath the surface-level panic. According to an analyst, the military tension spooked retail investors, but institutional capital kept buying. Five key metrics support this thesis.

First, Bitcoin’s Total Netflow on Binance (SMA-30) registered an average of roughly -1,350 BTC, worth about $96 million. Negative netflow indicates coins leaving Binance at an aggressive pace.

Follow us on X to get the latest news as it happens

Second, the Short-Term Holder Spent Output Profit Ratio (SOPR) across all exchanges sits at 1.0018.

“The mathematical verdict is irrefutable: realizing losses predominated over the last 182 days, of which 148 (81.32%) were below 1.00. Today, these investors liquidate their positions practically at ‘breakeven’ to escape the volatility, delivering cheap liquidity into the hands of those who dictate the rules of the game,” the analyst wrote.

Third, global exchange reserves fell to about 2.69 million BTC, sitting below the seven-day moving average. That gap represents roughly 4,500 BTC, about $316 million, withdrawn to cold storage during peak geopolitical uncertainty.

“The scenario proves that today’s drop is not a trend reversal, but a brutal wealth transfer disguised as macroeconomic panic. The data shows that betting against the market in the face of this structural liquidity drought is putting yourself in front of an institutional steamroller,” the post added.

Bitcoin Whale Behavior Confirms the Shift

A separate analysis by Amr Taha reinforced this reading. The 30-day whale inflow to Binance fell to $2.96 billion. The inflow fell below $3 billion for the first time since June 2025.

Declining whale inflows suggest large holders have stopped sending BTC to exchanges for potential sale.

At the same time, Long-Term Holder (LTH) Realized Cap Change over 30 days rose to $49 billion on April 9. That marked its second return to that level since March 26.

Meanwhile, Short-Term Holder (STH) Realized Cap Change fell to -$54 billion, its third drop below -$50 billion since early March. According to the analyst, weaker holders distribute while long-term holders absorb available supply.

Whether this accumulation translates into a price recovery will depend on whether the US-Iran stalemate escalates further or yields a diplomatic breakthrough in the days ahead.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post 5 On-Chain Signals Suggest Bitcoin’s War-Driven Dip Masks a Quiet Wealth Transfer appeared first on BeInCrypto.

GBP/USD started a downside correction from 1.3480. USD/CAD is gaining bullish momentum and might clear 1.3880 for more upside.

Important Takeaways for GBP/USD and USD/CAD Analysis Today

· The British Pound rallied toward 1.3500 before the bears appeared.

· There was a break below a rising channel with support near 1.3410 on the hourly chart of GBP/USD at FXOpen.

· USD/CAD is showing positive signs above the 1.3835 pivot zone.

· There was a break above a key bearish trend line with resistance at 1.3830 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair gained pace for a move toward 1.3300. The British Pound even climbed above 1.3450 before the bears appeared against the US Dollar.

A high was formed at 1.3485, and the pair started a minor downside correction. The pair traded below 1.3440, a rising channel, the 50-hour simple moving average, and the 23.6% Fib retracement level of the upward move from the 1.3176 swing low to the 1.3485 high.

Finally, the bulls appeared near 1.3380, and the pair started a consolidation phase. Immediate hurdle on the upside is near 1.3410 and the 50-hour simple moving average.

The first major resistance is 1.3480. The main sell zone sits at 1.3500. A close above 1.3500 might spark a steady upward move. The next stop for the bulls might be near 1.3620. Any more gains could lead the pair toward 1.3650 in the near term.

If there is a fresh decline, initial bid zone on the GBP/USD chart sits at 1.3365. The next major area of interest could be 1.3330, the 50% Fib retracement, and a connecting bullish trend line, below which there is a risk of another sharp decline. In the stated case, the pair could drop toward 1.3175.

USD/CAD Technical Analysis

On the hourly chart of USD/CAD at FXOpen, the pair formed a strong base above 1.3800. The US Dollar started a fresh increase above 1.3820 and 1.3850 against the Canadian Dollar.

More importantly, there was a break above a key bearish trend line with resistance at 1.3830. The pair even climbed above the 50% Fib retracement level of the downward move from the 1.3928 swing high to the 1.3799 low.

The pair is now consolidating above the 50-hour simple moving average. If there is another increase, the pair might face hurdles near 1.3880 and the 61.8% Fib retracement.

A clear upside break above 1.3880 could start another steady increase. In the stated case, the pair could test 1.3900. A close above 1.3900 might send the pair toward 1.3930. Any more gains could open the doors for a test of 1.3980.

Initial support is near the 50-hour simple moving average and 1.3835. The next key breakdown zone could be 1.3810. The main hurdle for the bears might be 1.3800 on the same USD/CAD chart.

A downside break below 1.3800 could push the pair further lower. The next key area of interest might be 1.3765, below which the pair might visit 1.3720.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

escalated its dispute with Justin Sun into a potential legal fight late Sunday, as tensions over its recent loan to a connected DeFi project spilled into public confrontation.

“Does anyone still believe @justinsuntron?” the project wrote on X. “We have the contracts. We have the evidence. We have the truth. See you in court pal.”

Does anyone still believe @justinsuntron ?

Justin’s favorite move is playing the victim while making baseless allegations to cover up his own misconduct.

Same playbook, different target. WLFI isn’t the first.

We have the contracts. We have the evidence. We have the truth.

See…

— WLFI (@worldlibertyfi) April 12, 2026

The legal threat came after Sun accused the Donald Trump-linked WLFI team of treating its users as personal ATMs after the latter deposited 5 billion WLFI tokens as collateral on the DeFi lending platform Dolomite to.borrow about $75 million in stablecoins.

“Every action taken by the WLFI team to extract fees from users and to treat the crypto community as a personal ATM is illegitimate,” Sun wrote on Sunday.

In September, Sun had his WLFI tokens frozen with the project alleging the Tron founder attempted to sell the tokens to cash out early. Sun denied the allegations, and on-chain data backs him up.

“Whoever is hiding behind this official account, step forward and identify yourself,” Sun wrote back to WLFI.

Whoever is hiding behind this official account, step forward and identify yourself. Every action taken by the WLFI team to secretly implant backdoor controls over user assets, to freeze investor funds without disclosure or due process, and to treat the crypto community as a…

— H.E. Justin Sun 👨🚀 🌞 (@justinsuntron) April 12, 2026

“As the largest investor in this project, I demand that those responsible come forward by name, instead of hiding in the shadows,” he continued.

The clash marks a sharp escalation in a feud between WLFI and one of its earliest backers, shifting the dispute from governance and capital use into open legal territory.

This animosity between the two is a start contrast from last year, where WLFI credited Sun at Consensus Hong Kong with helping lift the project out of a slow start.

“This guy,” WLFI co-founder Zak Folkman said on stage at Consensus, “saw that regardless of the outcome, this project is a monumental move forward for the entire crypto community.”

Aave Labs, the core development team behind the Aave protocol, has secured a substantial financing package from its own DAO to accelerate growth and product development. In a governance vote that closed with strong support, the Aave community approved a plan that allocates $25 million in stablecoins to Aave Labs, complemented by a grant of 75,000 AAVE tokens. The framework, dubbed “Aave Will Win,” envisions a shift toward a DAO-funded operating model with revenue generated by Aave products flowing into the DAO treasury.

The proposal passed on Saturday with nearly 75% in favor. Under the terms, the stablecoins will be disbursed over 12 months, while the 75,000 AAVE tokens will vest linearly over four years. The governance dashboard confirms the timing and vesting schedule, marking a formal reconfiguration of how Aave allocates resources for development and growth.

In announcing the decision, Aave founder Stani Kulechov used social media to frame the moment as a watershed for the protocol. “Aave Will Win is the most important proposal in Aave’s history and it just passed with a landslide,” he wrote on X. “If you own AAVE, you own not just the economic rights of the protocol, but the brand, the users, and the integrations. This is the direction we are committing to, a multi-year journey. The foundation is set. Now it’s time to build. Aave will win.”

Beyond the immediate funding, the framework sets out a broader reorganization. Aave V4 is designated as the protocol’s long-term technical foundation, and a new foundation would steward the Aave brand. Aave Labs would focus exclusively on Aave-related products, while the DAO treasury would receive revenue from products such as Aave Pro, ensuring ongoing financial support independent of the centralized development entity.

In parallel, the framework provides room for separate governance proposals to fund growth and development tied to product launches and milestones. These could take the form of targeted grants or milestone-based disbursements, allowing the community to steer investments toward specific features or initiatives without reworking the core operating model each time.

Historically, Aave’s governance has been a balancing act between centralized development control and decentralized decision-making. The current plan marks a notable shift: it moves the funding engine from Aave Labs’ balance sheet toward a DAO treasury funded by the protocol’s own activity, explicitly tying future success to broad community governance and alignment of incentives among developers, users, and builders.

Key takeaways

- DAO-backed funding of Aave Labs: $25 million in stablecoins disbursed over 12 months to support operations and growth.

- Incentivized ownership: 75,000 AAVE tokens vest over four years to align developer incentives with long-term protocol success.

- DAO treasury model: Revenue from Aave products would flow to the DAO treasury, signaling a shift toward a DAO-funded operating model.

- Aave V4 and brand stewardship: The framework codifies Aave V4 as the core technical foundation and creates a separate foundation to manage the brand.

- Process and governance dynamics: The proposal followed a historical arc of governance debates, including prior concerns about funding size, token allocations, and revenue definitions.

What the vote changes for Aave Labs and the broader DAO

The core aim of the Aave Will Win framework is to de-emphasize centralized control in day-to-day operations while expanding the community’s role in funding and guiding development. By moving revenue from products such as Aave Pro into the DAO treasury, the community gains a more direct stake in the protocol’s ongoing evolution. This could translate into faster iteration on user-facing tools, tighter alignment between feature delivery and community priorities, and potentially more resilient funding during market downturns, as treasury resources are not solely dependent on a single entity’s balance sheet.

At the same time, the plan introduces new governance dynamics. The 75,000 AAVE tokens carry voting power and represent a tangible commitment by the community to align incentives with long-term outcomes. Some participants voiced concerns during the lead-up to the vote about the size of the funding package and the concentration of voting power in tokens, which could influence future protocol decisions. The governance process also flagged questions about how revenue is defined and counted for treasury allocations.

Looking back, the path to this moment included earlier tensions within the Aave ecosystem. A major governance delegate, the Aave Chan Initiative, stepped back from the DAO due to governance standard concerns and voting dynamics. Earlier in the year, a proposal to transfer brand assets and intellectual property to a DAO structure likewise failed, underscoring the challenges of translating aspiration into an operational model that the entire community can rally around. The team has argued that the new structure would streamline operations, accelerate development, and position Aave to compete more effectively as fintechs and institutions increasingly move on-chain in regulated environments.

Implications for investors, users, and builders

From an investor and builder standpoint, the framework represents both opportunity and risk. On the upside, a formalized, DAO-backed funding mechanism could unlock more aggressive product development cycles, improved coordination across teams, and clearer long-term incentives for engineers and product teams. For users, the potential is a faster cadence of feature releases, improved risk management tools, and more robust integrations with on-chain products as the ecosystem matures around a centralized yet widely distributed governance model.

However, the transition is not without uncertainties. The DAO treasury’s performance will hinge on the protocol’s revenue streams and the community’s ability to govern effectively in a broader regulatory and macroeconomic context. Governance fatigue, misaligned incentives, or disputes over future revenue definitions could complicate execution. Market participants will want to watch how the separate grants tied to specific product launches are structured and how quickly they translate into tangible deliverables.

Macro context matters as well. Aave remains one of DeFi’s largest players by total value locked, with DeFiLlama data showing a multi-billion dollar footprint. A successful transition to a DAO-led operating model could serve as a blueprint—and a test case—for other major DeFi projects exploring similar governance and funding arrangements in an increasingly regulated, investor-driven landscape.

What comes next

With the “Aave Will Win” framework approved, attention shifts to the execution phase. The DAO will need to translate the approved funding and vesting schedules into concrete operational milestones, establishing governance processes for ongoing treasury management, grant distribution, and product roadmaps. The community will also be watching for how the new Aave foundation and the renamed or restructured Aave Labs interface with product teams, risk management, and compliance-related considerations as markets evolve.

As Stani Kulechov signaled, the foundation has been set for a multi-year journey. The coming quarters will reveal how effectively the protocol can scale its governance-driven model without sacrificing speed and user-centric innovation. Investors and builders should remain attentive to how the DAO governs revenue definitions, how milestones are operationalized, and how the broader ecosystem responds to a more decentralized yet financially empowered Aave.

Overall, the vote represents a deliberate step toward embedding the protocol’s growth within a community-led framework. If the model succeeds, it could recalibrate expectations for how DeFi projects fund development and align incentives across developers, users, and strategic partners in the years ahead.

Watch for forthcoming governance proposals that will detail the distribution of growth and development grants, the specifics of the Aave V4 roadmap, and the formal establishment of the new foundation to steward the brand. The coming updates will indicate how quickly this ambitious transition translates into measurable product outcomes and wider market adoption.

Fabio Wardley open to battle of KO artists if he beats Dubois: “He’s on the list”

Someone Turned This Tiny 1970s Car Into A Lamborghini-Beating Machine

Donald Trump lashes out at the Pope again before praising his brother for being ‘all MAGA’ | News US

-

Politics3 days ago

Politics3 days agoUS brings back mandatory military draft registration

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Veronica Beard

-

Sports3 days ago

Sports3 days agoMan United discover Nico Schlotterbeck transfer fee as defender reaches Dortmund agreement

-

Tech5 days ago

Tech5 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Politics16 hours ago

Politics16 hours agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World4 days ago

Crypto World4 days agoCanary Capital Files SEC Registration for PEPE ETF

-

Fashion7 days ago

Fashion7 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Business2 days ago

Business2 days agoTesla Model Y Tops China Auto Sales in March 2026 With 39,827 Registrations, Beating Cheaper EVs and Gas Cars

-

Fashion6 days ago

Fashion6 days agoLet’s Discuss: DEI in 2026

-

Crypto World5 days ago

Crypto World5 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics3 days ago

Politics3 days agoMalcolm In The Middle OG Turned Down ‘Buckets Of Money’ To Appear In Reboot

-

NewsBeat8 hours ago

NewsBeat8 hours agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Business3 days ago

Business3 days agoOpenAI Halts Stargate UK Data Centre Project Over Energy Costs and Copyright Row

-

Business2 days ago

Business2 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Tech7 days ago

Tech7 days agoItalian court says Netflix must refund customers up to $576 over price hikes

-

Tech7 days ago

Tech7 days agoHaier is betting big that your next TV purchase will be one of these

-

Tech7 days ago

Tech7 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

-

Tech7 days ago

Tech7 days agoThe Xiaomi 17 Ultra has some impressive add-ons that make snapping photos really fun

-

Tech7 days ago

Tech7 days agoSamsung just gave up on its own Messages app

-

Tech7 days ago

Tech7 days agoSave $130 on the Samsung Galaxy Watch 8 Classic: rotating bezel, sleep coaching, and running coach for $369

You must be logged in to post a comment Login