Crypto World

US Lawmakers Move to Codify Permanent CBDC Ban in Housing Bill

According to Cointelegraph, a bipartisan initiative in the U.S. Congress is advancing a permanent ban on a central bank digital currency (CBDC) issued by the Federal Reserve, to be codified in the 21st Century ROAD to Housing Act. The House is poised to vote on an amended version of the measure this week, following a Senate bill that would delay any CBDC issuance until December 31, 2030. The development underscores enduring regulatory and governance concerns about state-issued digital money and its implications for financial privacy, supervisory oversight, and the role of the Fed.

The amended House legislation aims to eliminate what its sponsors describe as a potential “backdoor green light for a CBDC” and seeks a permanent prohibition. The debate arrives at a moment when lawmakers are weighing how a digital sovereign currency would interact with housing programs, housing affordability policy, and broader financial-system regulation.

Key takeaways

- The House proposes a permanent ban on the Federal Reserve or its banks issuing a CBDC, embedded in the amended ROAD to Housing Act; the Senate’s March document proposed a CBDC prohibition through 2030, alongside housing program revisions.

- Key lawmakers are advancing distinct anti-CBDC positions: Rep. Warren Davidson supports a permanent prohibition, while House Majority Whip Tom Emmer is promoting an alternative “Anti-CBDC Surveillance State Act.”

- The legislation must clear both chambers before it can reach the president’s desk; passage in the House would send the measure back to the Senate for potential further changes.

- Global context remains limited: the Atlantic Council tracker identifies only three countries with official CBDCs (Nigeria, Jamaica, Bahamas) and notes 41 others in pilot or testing phases, highlighting a risk analysis framework for U.S. policy choices.

- Regulatory and compliance implications are central for banks, non-bank financial institutions, and crypto firms, with potential downstream effects on licensing, AML/KYC regimes, and cross-border operations.

Legislative trajectory and policy debate

The Senate Banking, Housing and Urban Affairs Committee released a bill in March largely focused on housing program revisions but included a section barring the Federal Reserve System or any Federal Reserve bank from issuing a CBDC or similar instrument until the end of 2030. In parallel, the House has crafted its own amended version, which Rep. Mike Flood described as reversing a perceived “backdoor green light for a CBDC” and pushing for a permanent ban. The House bill is expected to reach a floor vote this week, with prospects of returning to the Senate for potential amendments before any final enactment.

Legal and regulatory analysts are watching the interplay between the two chambers closely. If enacted, the measure would establish a statutory framework that could constrain the Fed’s monetary tools and the broader development of a government-backed digital currency in the United States. The path forward remains uncertain, given possible Senate resistance to a permanent ban and the broader policy considerations that have characterized CBDC discussions for years.

Policy positions, privacy, and governance concerns

Policy voices on both sides of the aisle have framed CBDCs as a matter of governance, privacy, and state oversight. Rep. Warren Davidson has argued that a sunset or “2030 pre-launch development period” fails to create a robust, lasting constraint on CBDC development, describing the House effort as a potential bipartisan win on housing policy that should not become a vehicle for a central-bank digital currency. He characterized the current approach as drifting toward a CBDC policy that could be construed as a functional launch date rather than a sincere ban.

On the other side, Rep. Tom Emmer—one of the House Republican leadership figures—has pressed for the Anti-CBDC Surveillance State Act, which would block the Fed from creating or issuing a CBDC. He has framed the issue in terms of privacy and governance, arguing that a U.S. CBDC could be used to surveil and control economic behavior, drawing explicit contrasts with models observed in other jurisdictions. A representative statement from Emmer included, “My Anti-CBDC Surveillance State Act bans our government from ever creating this Orwellian tool. The House passed it. Now, the Senate must act.”

“My Anti-CBDC Surveillance State Act BANS our government from ever creating this Orwellian tool. The House passed it. Now, the Senate must act.”

The policy discourse also takes into account broader privacy and civil-liberties considerations. The Human Rights Foundation has highlighted the dual nature of CBDCs: potential benefits for financial inclusion and the risks related to privacy infringement and the possibility of expanding government control. This framing informs ongoing debates about how any federal digital monetary instrument would interface with existing AML/KYC obligations, banking relationships, and cross-border payments—areas where U.S. regulatory posture increasingly intersects with international standards and comparative regimes.

Global landscape and regulatory context

Beyond the United States, global CBDC activity remains uneven. The Atlantic Council’s CBDC tracker identifies Nigeria, Jamaica, and the Bahamas as the only jurisdictions with officially deployed CBDCs, while 41 additional countries are in various pilot stages. This landscape informs the regulatory and political calculations in Washington, as lawmakers weigh the domestic benefits and risks of a sovereign digital currency against potential international policy alignments and competitive considerations.

The CBDC debate in the United States unfolds alongside ongoing regulatory discussions on related digital-finance issues, including stablecoins, cross-border payments, and the role of licensing regimes for digital-asset firms. While not all details are identical across jurisdictions, the U.S. regulatory model increasingly emphasizes a rigorous framework for oversight, protection of consumer data, and the integrity of the financial system—considerations that will shape how any future CBDC policy is designed, implemented, and if necessary, restrained.

Within the broader policy ecosystem, lawmakers and observers continue to reference regulatory pillars and cross-border dynamics relevant to MiCA-type frameworks, U.S. securities and exchange authorities, and the Department of Justice’s enforcement posture. The evolving balance between monetary sovereignty, financial inclusion, and civil-liberties protections remains central to the debate over whether the United States should, or should not, pursue a CBDC strategy at all.

Closing perspective

As Congress advances or revises these proposals, the central questions revolve around legality, governance, and regulatory alignment. Whether a permanent ban gains approval—and how it would be reconciled with ongoing domestic housing initiatives and international CBDC developments—will shape the trajectory of U.S. digital-money policy for years to come. Monitoring votes in the House, potential Senate amendments, and the administration’s stance will be essential for institutions assessing compliance requirements and strategic considerations related to central-bank digital currencies.

A Pump.fun token airdropped to a famous trader’s wallet is up tens of thousands of percent in days. Here is the honest version: this is a high-risk memecoin with no product, and most tokens like it go to zero.

Summary

- The Black Bull (ANSEM) is a Solana memecoin launched on Pump.fun in mid-June 2026, trading near $0.13 with a market cap around $56 million after a move of roughly 26,000% in a week.

- The token was not created by the trader it is named after. An anonymous developer airdropped a large share of the supply to the wallet of Ansem, a well-known Solana influencer, who later embraced it rather than launching his own coin.

- There is no product, roadmap, team, or revenue behind the token. Its price is driven entirely by attention, one influencer’s involvement, and speculative trading, which makes it a casino bet, not an investment.

- On-chain analysis tools have flagged manipulation risk and heavy holder concentration; liquidity is thin relative to the market cap, and the trader associated with it has faced market-manipulation allegations.

- Third-party forecasts that exist for ANSEM are wide and speculative, spanning roughly $0.03 to $0.25, and the most realistic base case for any token of this type is a sharp drawdown, with a real chance of going to near zero.

Before anything else, the blunt version. The Black Bull, traded under the ticker ANSEM, is a memecoin. It has no underlying business, no cash flows, and no roadmap that would anchor a valuation. Its price exists because a famous trader is associated with it and the internet is paying attention.

Tokens like this can produce life-changing gains and total losses inside the same week, and the overwhelming majority of Pump.fun launches lose nearly all their value, many within a single day. Any “price prediction” for an asset like this is closer to handicapping a roulette spin than forecasting a company. Read the rest with that frame fixed in place.

This piece explains what The Black Bull actually is, the numbers behind its move, why it is a casino rather than an investment, the bull thesis stated fairly, the specific ways it could go to zero, what the few forecasters tracking it say, and then bull, base, and bear scenarios. It closes with a short FAQ.

What The Black Bull (ANSEM) actually is

The Black Bull is a Solana token launched on Pump.fun, the memecoin launchpad, around June 16 to 17, 2026, with the on-chain contract address ending in “pump” as Pump.fun tokens do. The story that gave it life is specific. An anonymous developer created the token and airdropped a large portion of the supply, by some accounts around 65%, directly to the wallet of Ansem, a prominent Solana trader and influencer also known by the handle blknoiz06, whose real name is Zion Thomas. Ansem is one of the best-known memecoin personalities on Solana, with roughly a million followers and a reputation as an early caller of tokens like WIF and BONK.

Crucially, Ansem did not create the token, and it is not officially his project. The developer essentially bet that putting the supply in a famous wallet would manufacture attention. It worked. Rather than dump the airdrop or launch a competing coin of his own, Ansem leaned in, reportedly pledging to airdrop creator fees back to holders instead of cashing out, and his wallet holds a very large position, on the order of 600 million tokens that at points represented the bulk of his visible on-chain portfolio. That alignment, a recognizable figure with skin in the game, is the entire bull narrative. It is also the entire risk, because the token’s fate is tethered to one person’s continued involvement.

The numbers behind the move

As of late June 2026, ANSEM trades near $0.13, having reached a peak around $0.14 on June 29. The 7-day move was roughly 26,000%, the kind of figure that only appears in freshly launched memecoins coming off a near-zero base. The market cap sits around $56 million, with roughly 410 million of a 1 billion total supply in circulation, implying a fully diluted valuation closer to $136 million. The token ranks somewhere around #374 by market cap, and daily trading volume has run between roughly $60 million and $94 million, which against a $56 million cap produces a volume-to-market-cap ratio above 2.

That ratio is itself a warning light: it means the token turns over its entire value more than twice a day, the signature of frantic speculative churn rather than steady holding. ANSEM trades across venues including PumpSwap and Meteora on Solana, with perpetual futures listed on some offshore exchanges such as MEXC and others, and it has appeared as a verified token on Solana interfaces like Jupiter and Phantom. The presence of leveraged perps on a token this young amplifies the volatility in both directions, because liquidations can cascade fast when the price moves.

These numbers describe a token in the most volatile possible phase of its life. The percentage gains are real, and so is the fragility underneath them.

Why this is a casino, not an investment

This section is the heart of the piece, and it is deliberately heavier than the bull case, because the risks here are not footnotes. They are the main event.

First, there is nothing to value. ANSEM has no product, no revenue, no roadmap, and no team in the conventional sense. There is no cash flow to discount, no user base to grow, no utility that creates demand for the token beyond speculation. Its price is a pure function of attention and belief, both of which can evaporate without warning.

Second, on-chain analysis has flagged it. Token-screening tools such as Rugcheck have raised manipulation warnings tied to supply concentration in wallets that are not clearly identified. Heavy concentration means a small number of holders could move the price violently or exit into the liquidity that retail buyers provide. Thin liquidity relative to the market cap compounds this: when real liquidity is shallow, a few large sells can collapse the price far faster than the order book suggests.

Third, the person at the center carries his own controversy. The trader associated with the token has faced market-manipulation allegations in the broader memecoin context, which adds reputational and regulatory risk to an asset whose entire thesis rests on his involvement. If he steps back, sells, or is forced to distance himself, the narrative that supports the price can vanish.

Fourth, the base rate is brutal. The large majority of Pump.fun memecoins lose almost all their value, frequently within hours or days of launch. Survivorship bias makes the winners loud and the thousands of dead tokens silent. Treating ANSEM as likely to be one of the rare survivors, instead of one of the many that fade, is the single most common and most expensive mistake buyers of tokens like this make.

Put together, these are not reasons to never touch a memecoin. They are reasons to size any exposure as money one is fully prepared to lose, and to never confuse a fast chart with a sound investment.

The bull thesis, stated fairly

For balance, the case the buyers make deserves a fair hearing, even inside a risk-first frame. The bull argument has 3 legs. The first is reach: Ansem commands a large, engaged audience, and in memecoins, attention is the scarce resource that drives price. A token he is actively associated with has a built-in distribution advantage that most launches never get.

The second is alignment. By reportedly pledging to route creator fees back to holders instead of launching a separate token to cash in, Ansem signaled that his incentives point in the same direction as the people holding the coin, at least for now. In a category defined by developers dumping on their communities, an influencer choosing to share fees is a comparatively constructive signal.

The third is the Solana memecoin meta itself. Solana has repeatedly produced memecoins that ran far longer and higher than skeptics expected, and the ecosystem’s culture, low fees, and fast launches keep the speculative engine fed. In a market where attention rotates quickly, a token with a recognizable face and an active community can sustain a narrative longer than a faceless launch.

None of this changes the absence of fundamentals. The bull case is a bet that attention and alignment persist long enough to matter, which is a real but fragile proposition.

What could make it go to zero

The bear mechanics are concrete and worth naming, because they are the most probable outcome for tokens of this kind. Concentration is the first: if large holders, identified or not, decide to sell into the thin liquidity, the price can fall faster than buyers can react, and early entrants exit at the expense of late ones. Liquidity withdrawal is the second: if liquidity providers pull their positions, the token can become nearly untradeable at anything close to the quoted price.

Narrative death is the third and most likely slow killer. Memecoins live on attention, and attention is finite. When the crowd rotates to the next launch, volume dries up, the chart bleeds, and the token drifts toward irrelevance even without a dramatic crash. Copycats accelerate this, as the inevitable wave of imitation tokens splits the speculative capital and dilutes the original’s mindshare. Finally, the single-person dependency is the acute risk: if Ansem sells, goes quiet, or is forced to distance himself for legal or reputational reasons, the one pillar holding up the price is removed, and there is nothing fundamental left to catch it.

Any one of these can take a token like this down by 80% or more in short order, and several can combine. This is not a tail risk for ANSEM. It is the central scenario that any honest forecast has to treat as the base case.

What forecasters say

A handful of exchange-affiliated outlets have published speculative ANSEM ranges, and they should be read as guesses about a chaotic asset, not as analysis grounded in fundamentals, because there are no fundamentals to ground them in. These are 3rd-party figures, not endorsements.

Some short-term models from venues such as WEEX have sketched a near-term base band roughly between $0.085 and $0.135, a momentum upside toward $0.15 to $0.18 if attention holds, and a downside toward $0.06 to $0.075 if it fades. Broader 2026 ranges floated by outlets including BTCC and WEEX span roughly $0.03 to $0.25. The width of these ranges, a possible multiple up or a collapse of more than half, is the most honest thing about them: it concedes that the outcome is dominated by reflexive sentiment, not by anything that can be modeled. For an asset like this, the error bars are the message.

The pattern this fits: influencer memecoins before ANSEM

The Black Bull is not the first token to run on a famous name, and the history of the pattern is the most useful guide to its likely path. Solana has produced a long line of influencer-linked and celebrity memecoins, some tied to the same callers who built reputations on early WIF and BONK trades. The recurring shape is familiar: a token attaches itself to a recognizable figure, attention floods in, the price goes parabolic on a near-zero base, and a wave of buyers arrives late expecting the early gains to repeat. What happens next sorts almost entirely on whether attention and the figure’s involvement persist.

The brutal majority outcome is decay. Most of these tokens fade within days or weeks as the crowd rotates to the next launch, leaving holders who bought the peak deeply underwater. A small number sustain a community and trade sideways at a fraction of their high for longer. A rare few extend into something more durable, and those are the cases the next round of buyers remembers, which is exactly how survivorship bias keeps the cycle turning. The honest framing is that ANSEM is drawing from the same deck, and the base rates for that deck are unforgiving.

What makes The Black Bull slightly different from a faceless launch is the creator-fee airdrop dynamic, which gives the central figure a reason to stay engaged instead of dumping immediately. That can extend the attention window. It does not change the category math.

An influencer can prolong a memecoin’s life, but no influencer has reliably prevented the eventual reversion that defines the type. Treating ANSEM as exempt from that pattern, because this time the figure seems aligned, is the precise belief that has separated late buyers from their money in every prior cycle.

If you choose to speculate anyway

This is not a recommendation to buy ANSEM or any memecoin. But because people will trade tokens like this regardless of warnings, the harm-reduction principles that disciplined speculators apply are worth stating plainly, since they are the difference between a survivable loss and a damaging one.

The first principle is sizing. Money committed to an asset like this should be money one can lose in full without affecting rent, savings, or obligations, because total loss is a realistic outcome, not a worst case. The second is that the position should be treated as already gone the moment it is opened, which removes the emotional pressure that leads people to average down into a falling token or chase it higher. The third is that taking profits on the way up is the only way speculative gains become real; a paper gain in a token with thin liquidity is not a realized gain until it is sold, and the same shallow liquidity that let the price spike can prevent an exit at the quoted price on the way down.

The fourth principle is to distrust leverage entirely here. The presence of perpetual futures on a token this young and this volatile is a fast path to liquidation, because the swings that make memecoins exciting also trigger margin calls in minutes.

The fifth is to verify instead of assume: checking the contract, the liquidity, and the holder concentration before committing, instead of trusting a chart or a name. None of this makes a memecoin a sound investment. It makes the gamble less likely to cause real damage, which is the most honest advice anyone can give about an asset with no fundamentals.

Bull, base, and bear scenarios for ANSEM

These scenarios are illustrative and speculative. For a memecoin with no fundamentals, they describe possible paths driven by attention and holder behavior, not valuations. The bear case is weighted as the most probable, consistent with how tokens of this type typically resolve.

Bull case

In the bull scenario, Ansem stays actively involved, the creator-fee airdrops keep holders engaged, and the Solana memecoin meta stays hot enough to keep attention flowing. Volume holds, new buyers keep arriving faster than early holders exit, and the token sustains or extends its level, pushing toward the upper speculative bands near $0.15 to $0.25 that the most optimistic 3rd-party ranges describe. This case requires attention to persist, concentration not to unwind, and no reputational or regulatory shock to the figure at its center. It is possible, and in memecoins it does happen, but it is the minority outcome.

Base case

In the base scenario, the initial frenzy cools as it almost always does. Volume fades from its launch peak, the chart gives back a large portion of the parabolic move, and the token settles into a lower, choppier range, perhaps the $0.06 to $0.13 zone, while it searches for whether a durable community remains after the hype. From there it either grinds out a smaller, attention-dependent existence or slowly bleeds lower as the crowd moves on. Even this “survives but deflates” path involves a substantial drawdown from the peak for anyone who bought the top.

Bear case

In the bear scenario, which is the most likely for a token of this kind, the attention rotates away, concentration unwinds into thin liquidity, or the single-person narrative breaks. The price falls 80% or more from its highs and continues toward near zero as volume disappears, joining the large majority of Pump.fun launches that do not survive. A liquidity pull, a large holder exit, a wave of copycats, or the central figure stepping back are each sufficient to trigger this, and they often compound. Anyone holding into this scenario should expect to lose most or all of the position.

Frequently Asked Questions

Did Ansem create The Black Bull token?

No. The token was created by an anonymous developer who airdropped a large share of the supply to Ansem’s wallet to attract attention. Ansem, the Solana trader also known as blknoiz06, did not launch it, and it is not officially his project. He later embraced it and reportedly pledged to share creator fees with holders, but the origin was a 3rd party using his name and wallet.

Why has ANSEM risen so much?

The move, roughly 26,000% in a week, reflects a freshly launched memecoin coming off a near-zero base combined with the attention of a well-known influencer. There is no product or revenue driving it. The price is a function of speculation, social momentum, and one person’s involvement, which is exactly why it can reverse just as violently.

Is The Black Bull a safe investment?

No. It is a high-risk memecoin with no fundamentals, flagged manipulation and concentration risk, thin liquidity, and a price dependent on a single person’s involvement. The large majority of tokens like it lose nearly all their value. It should be treated as a speculative gamble with money one is fully prepared to lose entirely, not as an investment.

What are the biggest risks?

The biggest risks are holder concentration selling into thin liquidity, liquidity providers withdrawing, attention rotating away and the narrative dying, copycat tokens splitting interest, and the central figure selling or stepping back for legal or reputational reasons. Any one can cause an 80%-plus decline, and they often combine.

What price targets do forecasters give?

Speculative 3rd-party ranges from exchange-affiliated outlets span roughly $0.03 to $0.25 for 2026, with short-term bands near $0.06 to $0.18. These are guesses about a chaotic, sentiment-driven asset, not fundamentals-based analysis. The wide ranges reflect that the outcome cannot be modeled with any confidence.

What is the most likely outcome?

For a memecoin of this type, the most likely outcome is a sharp drawdown from the peak, with a meaningful chance of trending toward near zero as attention fades. A minority of such tokens sustain a smaller community-driven existence, and a rare few extend higher. Betting on the rare outcome is the most common and costly mistake.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice. Memecoins are extremely high-risk, speculative assets with no underlying value, and most lose nearly all of their value. Prices are highly volatile, and the figures here, accurate as of June 30, 2026, will change rapidly. Nothing here is a recommendation to buy or sell any asset. Never invest more than you can afford to lose entirely, and consider consulting a licensed professional before making financial decisions.

Key Highlights

- MetaMask introduces Money Account featuring mUSD yield generation and payment capabilities

- Users can earn, transact, and trade using a unified balance

- mUSD holdings may generate up to 4% variable APY following fee deductions

- MetaMask Card users could receive up to 3% cashback rewards in mUSD

- Monad blockchain enables sponsored transaction fees for efficient stablecoin operations

MetaMask has introduced its Money Account feature, integrating mUSD yield opportunities, payment functionality, and trading capabilities within a single self-custody balance. This new offering transforms the platform from a basic wallet and exchange tool into a comprehensive financial solution as stablecoins become increasingly mainstream in everyday transactions. Eligible users now have access to a streamlined method for generating returns, making purchases, and executing trades without transferring assets between different accounts.

mUSD Yield Integration Powers Money Account

The Money Account centers on mUSD, MetaMask’s proprietary stablecoin engineered for transaction processing and account management. Users have the ability to exchange compatible stablecoins for mUSD at a one-to-one exchange rate with no conversion charges. Additionally, mUSD can be acquired through approved fiat payment channels in jurisdictions where the service is available.

The platform distributes opted-in funds through third-party vault systems overseen by Veda. Initially, assets are channeled into Morpho protocols, with Aave integration planned for subsequent releases. Yield calculations refresh within the account interface and may achieve up to 4% variable annual percentage yield after applicable fees.

According to Consensys, Bridge maintains the reserve assets supporting mUSD through U.S. dollar holdings and short-duration Treasury securities. The stablecoin operates on M0 infrastructure, while yield production functions independently from reserve backing mechanisms. MetaMask emphasizes that users retain full control over their private keys, preventing the company from accessing or moving user funds.

Payment Functionality Via Monad Integration

Money Account operates on the Monad blockchain, which facilitates rapid settlement times and consistent transaction expenses. The architecture employs sponsored gas fee models, enabling users to manage their balances without incurring network costs. This framework supports seamless payment processing, yield generation, and trading activities from a consolidated balance.

MetaMask has integrated the account with its MetaMask Card in regions where the card service operates. Transactions automatically settle using the Money Account balance without requiring additional conversion procedures. Qualified card transactions may also generate up to 3% cashback rewards distributed in mUSD.

The service accommodates multiple stablecoins, including USDC, USDT, DAI, aUSDC, aUSDT, and aDAI across compatible blockchain networks. Account funding options include cryptocurrency transfers and approved fiat on-ramp services. MetaMask has deployed this functionality worldwide, excluding the United Kingdom and certain restricted territories.

Crypto Wallets Evolve Toward Full Banking Services

MetaMask’s Money Account debut reflects intensifying competition among wallet providers and exchanges to capture more comprehensive financial services. Cryptocurrency platforms are increasingly incorporating payment systems, savings mechanisms, and trading features centered around stablecoin balances. This evolution parallels growing stablecoin adoption among traditional banks, payment processors, and established financial institutions.

The launch coincides with ongoing regulatory discussions surrounding stablecoin yield offerings in the United States. Government agencies and legislative bodies continue examining how cryptocurrency companies can provide returns on stablecoin deposits. These deliberations may significantly influence future products that merge payment processing, asset custody, and decentralized finance returns.

MetaMask has simultaneously expanded into automated financial tools through its Agent Wallet product. This solution enables AI agents to execute transactions according to user-established parameters and restrictions. Collectively, these initiatives demonstrate MetaMask’s strategic transformation from a simple cryptocurrency wallet into a comprehensive financial management platform.

TLDR

- Avalanche Treasury Corp told regulators it may not survive the year due to financial strain.

- The company cited “substantial doubt” about its ability to continue as a going concern.

- AVAX price declines led to major writedowns and over $26 million in quarterly losses.

- The firm’s AVAX holdings dropped to nearly half of their original purchase value.

- Shares collapsed over 90% within a month and now trade below $0.73.

Avalanche Treasury Corp told regulators it may not survive the year after a steep decline in its finances. The company disclosed material losses and liquidity pressure linked to falling AVAX prices. It also warned that current conditions raise “substantial doubt” about its ability to continue operations.

AVAX Holdings Decline and Balance Sheet Pressure

The company previously promoted a large AVAX treasury valued near one billion dollars during last year’s expansion phase. However, market conditions changed, and the value of its AVAX holdings dropped sharply over recent months. As a result, its market capitalization fell below thirty million dollars, reflecting severe investor concern.

Its operating unit reported losses exceeding twenty-six million dollars in one quarter due to AVAX writedowns. The firm bought AVAX for about two hundred sixty-five million dollars, yet the holdings fell to nearly one hundred twenty-three million dollars. This gap left the company holding assets worth far less than their original purchase cost.

AVAX prices declined forty-seven percent this year and nearly two-thirds over the past twelve months. Consequently, the treasury strategy weakened as asset values dropped and reduced the firm’s financial flexibility. The company stated that these conditions created ongoing uncertainty regarding its financial stability.

Stock Collapse Follows AVAX Treasury Strategy

Avalanche Treasury Corp completed a merger with a blank check company and entered public markets with high expectations. However, investor sentiment turned negative as disclosures revealed risks tied to its AVAX exposure and financial position. The stock fell from above ten dollars to below two dollars within days of additional filings.

Shares continued to decline and traded below seventy-three cents, entering penny stock territory. In total, the stock lost more than ninety percent of its value within one month. This decline reflected market concern over the sustainability of its AVAX treasury model.

The company also pledged a large portion of its AVAX holdings as collateral for a loan agreement. It committed nearly seven point eight million AVAX tokens from a total of thirteen point eight million holdings. This move increased financial risk as falling prices could pressure collateral requirements.

Other AVAX Treasury Firms Show Similar Declines

Other firms pursuing AVAX treasury strategies reported similar declines in value after initial expansion plans. AgriFORCE Growing Systems rebranded as AVAX One and announced a large capital raise to acquire more AVAX. The company aimed to build a significant AVAX treasury supported by strategic investors and advisors.

Despite those plans, its market value dropped sharply and now stands near forty-three million dollars. The firm’s shares declined sixty-eight percent this year and over ninety percent in the past year. These figures highlight the broader pressure affecting companies holding large AVAX reserves.

Data across the sector shows a consistent downward trend in treasury company valuations linked to AVAX exposure. Companies that accumulated AVAX during earlier market optimism now face reduced asset values and weaker investor confidence. This trend underscores the risks tied to concentrated digital asset treasury strategies.

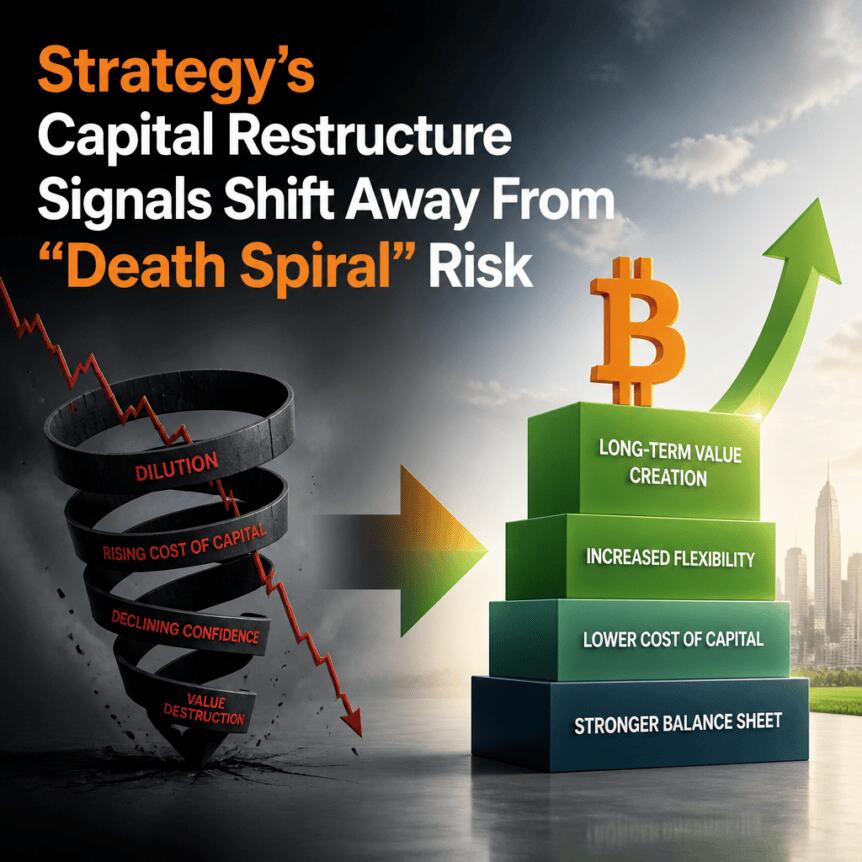

Strategy, the publicly traded firm behind the Strategy (formerly MicroStrategy) Bitcoin treasury model, has moved to reassure investors after a steep drop in both Bitcoin and its own shares intensified fears about the company’s complex capital structure. With Bitcoin trading below $60,000 and Strategy’s stock down more than 70% from its highs, attention has turned to STRC—Strategy’s preferred-like security—and the possibility that its funding mechanics could amplify downturns.

On Monday, Strategy unveiled a new capital framework designed to address concerns around liquidity, financing reflexivity, and the company’s ability to meet obligations during stress. The plan includes up to $1 billion of buybacks for MSTR, up to $1 billion of buybacks for STRC and related securities, an increase in STRC’s dividend to roughly 12%, and expansion of the company’s cash buffer to $2.55 billion. Strategy also disclosed that it may sell up to $1.25 billion in BTC holdings if needed to satisfy dividend or debt requirements.

Key takeaways

- Strategy’s new framework combines buybacks (MSTR and STRC) with a larger cash reserve, aiming to reduce uncertainty during market stress.

- STRC’s dividend is expected to rise to roughly 12%, supported by expanded cash resources under the plan.

- Strategy added a contingency option: selling up to $1.25 billion in Bitcoin if required for dividend or debt obligations.

- Short-term trading activity improved after the announcement, with STRC and MSTR both rallying more than 12% in after-hours trading, according to Yahoo Finance.

- Debate continues over whether the company’s structure can withstand prolonged tightening in funding markets—even if it is not expected to face near-term insolvency.

What Strategy outlined in its capital framework

Strategy’s announcement centers on a restructuring of how it intends to manage risk across its Bitcoin-linked balance sheet and its layered security offerings. The company says the package includes up to $1 billion in buybacks for MSTR and up to $1 billion in buybacks for STRC and related securities.

In addition to buybacks, Strategy is increasing the STRC dividend rate to roughly 12% and expanding its cash buffer to $2.55 billion. Strategy’s filing—an 8-K submitted June 29—spells out the mechanics and priorities management would follow in its capital allocation framework, including an emergency pathway that allows BTC sales if needed to meet obligations.

Crucially for investors who worry about “reflexive” downside dynamics, Strategy also said it may sell up to $1.25 billion in BTC holdings to meet dividend or debt requirements. That disclosure is notable given Strategy’s long-standing “Bitcoin maximalist” positioning and the recurring argument that selling BTC during stress could worsen market conditions.

Following the release, markets reacted positively. As reported with reference to Yahoo Finance, STRC and MSTR shares rose more than 12% in after-hours trading. The piece notes STRC was trading at $84.86 after the announcement, up from $72.06 on June 26.

Why STRC is a flashpoint for investors

STRC sits in the middle of Strategy’s capital structure—positioned as a perpetual preferred-like instrument linked to the broader Bitcoin treasury strategy. Strategy describes STRC as paying an annual dividend of about 12% on a $100 par value, supported by cash and its Bitcoin-linked capital framework.

This design has drawn skepticism from critics who argue that the instrument’s stability depends less on Strategy’s underlying solvency and more on the health of secondary-market demand and liquidity conditions. In other words, even if STRC is not a classic stablecoin, its market behavior can still be sensitive to tightening access to capital.

Earlier concerns have focused on how Strategy’s treasury approach could interact with market stress. Bitcoin critic Peter Schiff has repeatedly challenged Strategy’s model, warning that Strategy can’t sell Bitcoin without negatively affecting Bitcoin’s price and pointing to potential spillover effects if purchasing activity slows or selling accelerates.

At the same time, some analysts and market participants argue the risk framing is overstated. Taran Dhillon, head of digital assets at Kula, told Cointelegraph that Bitcoin volatility alone is unlikely to break the structure; he suggested the more important test is whether Bitcoin remains under pressure while funding becomes progressively more expensive or difficult.

The bear case: liquidity dependency and potential feedback loops

Much of the controversy around Strategy’s structure relates to how its financing cycle can behave in both directions. The core bear argument is that the same momentum that fuels expansion in calmer conditions can intensify stress when investors pull back, funding costs rise, or liquidity in secondary markets deteriorates.

Cointelegraph reported that Brad Garlinghouse, CEO of Ripple, made a similar point on CNBC, criticizing financial engineering as a driver of long-term value. Kyle Rodda, senior analyst at Capital.com, characterized Strategy as a momentum-driven accumulation vehicle: capital raises funds for Bitcoin purchases, and those purchases support the company’s valuation. But he warned the dynamic can reverse when market conditions weaken, funding costs rise, and investor appetite declines.

Rodda also emphasized that secondary market liquidity is a structural dependency. If refinancing pressures or forced selling forces larger adjustments elsewhere, the spillover effects could extend beyond Strategy itself.

Some prominent Bitcoin commentators have compared the scenario to prior stress-tested leveraged structures in crypto. Charles Edwards, founder of Capriole Investments, has been among the critics drawing parallels to Terra/LUNA-era dynamics during drawdowns, framing the situation as potential “feedback loop” risk rather than a purely price-driven story.

The neutral and bull positions: stress may target funding markets first

Not all observers agree that the primary threat is Bitcoin price movement. Dhillon suggested that any early instability would likely show up first in funding conditions—such as widening discounts, higher yields, and reduced issuance capacity—rather than immediate solvency failure tied directly to Bitcoin valuation.

He also highlighted a key distinction: STRC is not a stablecoin pegged mechanically to $100. Instead, its yield profile is designed to adjust with market pricing. The logic, in theory, is that when STRC trades below par value, the effective yield becomes more attractive to buyers, eventually pulling pricing back toward $100.

Cointelegraph also referenced a Bitfire Research report shared with the outlet, which argued that recent STRC price dislocations should not automatically be treated as structural failure. The report stated that Strategy faces no near-term insolvency risk, attributing de-pegging events largely to sentiment and liquidity conditions rather than a sudden change in fundamentals or solvency profile.

On the bull side, the article describes a “three-year MSTR stress test” conducted by Bitcoin supporter Adam Livingston. His model assumes extreme conditions—including a 55% Bitcoin drawdown, closed capital markets, and continued cash burn requiring large Bitcoin sales. The simulation also tracks a dramatic compression in “common equity Bitcoin exposure” (CEBE) and estimates that Strategy would sell approximately 115,727 BTC over three years to meet obligations before stabilization returns.

In Livingston’s scenario, the company survives the cycle and ends with over 700,000 BTC on its balance sheet, with a recovering net asset structure once conditions normalize. The takeaway from this model, regardless of how an investor views its assumptions, is that proponents believe the balance-sheet framework could be robust enough to survive even severe drawdowns—particularly if contingency mechanisms are executed as planned.

What changed—and what remains uncertain

Strategy’s new framework can be viewed as an attempt to make its stress-response playbook more concrete. According to the article’s references to Strategy’s June 29 8-K filing, management is focusing on transparency around how it would act during liquidity or capital-market disruptions—especially through cash buffer expansion, buybacks for both MSTR and STRC, and the ability to monetize Bitcoin up to $1.25 billion if required.

Dhillon described the changes as a meaningful improvement to transparency and confidence, pointing to the enlarged $2.55 billion reserve and a clearer plan for how Bitcoin monetization would work under pressure.

However, critics argue the fundamental dependency remains. Schiff, as cited in the piece, pointed to market-cap vs. Bitcoin value asymmetries—arguing that as long as MSTR’s market cap remains below the value of its Bitcoin holdings, newly issued capital could imply a “negative Bitcoin yield.” In other words, for some skeptics, the debate is not whether contingency tools exist, but whether the market structure will persistently price exposure in a way that helps—or harms—long-term holders.

Ultimately, Strategy’s framework strengthens the company’s toolkit for short-term stress, but it does not remove its reliance on access to capital markets over time. The key unresolved question is whether expanded liquidity buffers, buybacks, and contingency BTC sales can stand up to a prolonged period of tightening across both equity and credit-style markets—precisely the environment where feedback-loop concerns tend to matter most.

For investors, the next watch items are straightforward: whether STRC’s pricing relationship to par value stabilizes, how funding conditions evolve if Bitcoin stays under pressure, and whether Strategy’s disclosed order of operations holds up in practice during the next stress test.

The United States just lifted export controls on Anthropic’s Claude Fable 5 and Mythos 5. The Commerce Department cleared both models on June 30, paving the way for a swift restoration of full global access starting July 1.

The resolution ends nearly three weeks of tense negotiations between Anthropic and the White House.

What the Lifted Export Controls Actually Mean

An export control is a US rule that restricts who can access sensitive technology, including advanced AI models, based on national security concerns. The Commerce Department imposed one on Claude Fable 5 and Mythos 5 shortly after the models launched. It has now been formally reversed.

The original directive landed on June 12, just three days after the models went live on June 9. Furthermore, it cited national security concerns reportedly tied to potential model jailbreaks. As a result, Anthropic suspended access for foreign nationals worldwide across every product surface.

The rule caused immediate operational chaos. Segmenting users by nationality in real time proved impossible in practice. Consequently, Anthropic took both models entirely offline for customers on Claude.ai, the API, AWS Bedrock, and other partner platforms until the situation could be resolved.

The company confirmed the reversal directly. “We’ve received notice that the Department of Commerce has lifted export controls on Claude Fable 5 and Mythos 5. We’ll begin restoring access tomorrow, and will share an update soon,” Anthropic posted on June 30.

Why Claude Fable 5 and Mythos 5 Matter So Much

Claude Fable 5 stands as Anthropic’s most capable widely available model. It is built on the powerful Mythos-class architecture but ships with enhanced safeguards for general use. Furthermore, it excels at demanding reasoning tasks, long-horizon agentic work, software engineering, and advanced vision capabilities.

Mythos 5 targets more sensitive workloads. The model shares the same underlying architecture but comes with lifted safeguards for cybersecurity applications. Moreover, access was originally reserved for trusted partners through Project Glasswing across high-stakes government and enterprise deployments.

Pricing keeps both models competitive across the industry. Anthropic charges 10 dollars per million input tokens and 50 dollars per million output tokens. Additionally, built-in classifiers automatically route high-risk queries to safer fallbacks, especially on cybersecurity and biology-related tasks across every product surface.

The resolution highlights a broader shift in the AI industry. Anthropic held intensive talks with Commerce Department and White House officials throughout the standoff. As a result, the swift lifting signals both effective advocacy and a maturing regulatory framework for advanced AI systems across the entire United States.

The post US Lifts Export Controls on Anthropic’s Claude Fable 5 and Mythos 5 Models appeared first on BeInCrypto.

XRP is down 6% on the weekly chart. Where will it stop?

Ripple (XRP) Price Predictions: Analysis

Key support levels: $1

Key resistance levels: $1.3, $1.6, $2

XRP is Back at $1

Despite the best efforts from buyers, XRP has returned to the $1 support. This is the third time in the past two weeks that this cryptocurrency tested this level. This is somewhat bearish since bulls have failed to push the price away from the key support.

If seller pressure intensifies this week, then this support may eventually crack and turn into resistance. If so, buyers will most likely retreat to 80 cents, where the next major support level is found.

Momentum Remains Bearish

With clear lower highs and lower lows, XRP is in a bearish trend that is still to find a bottom. Because of this, the price has a good chance to drop lower in the coming weeks and turn $1 into resistance.

Moreover, the momentum indicators remain on the bearish side, with the 3-day RSI close to 30 points, which also indicates a bearish trend. As long as the RSI remains under 50, bears retain the upper hand.

Weekly MACD About to do a Bearish Cross

Another concerning signal can be seen on the weekly MACD. The moving averages are about to do a bearish cross. This would be the first time it happens in 2026, and if confirmed, it’s unlikely XRP will enter a recovery in the future.

Considering the above, the outlook for the second half of the year is negative, with lower lows likely. Best to wait for a bottom confirmation before considering an entry on XRP.

The post 3 Things to Watch for in Ripple’s (XRP) Price This Week appeared first on CryptoPotato.

A Massachusetts judge has allowed state authorities to expand their lawsuit against prediction markets platform Kalshi, extending the legal fight over whether the company’s sports event contracts should be regulated as online sports wagering.

In a Tuesday filing in Suffolk County Superior Court, associate justice Peter Krupp permitted Massachusetts regulators to submit a 71-page amended complaint, adding new allegations to the state’s initial case that Kalshi violated Massachusetts law by offering sports-related wagering without the required authorization.

Key takeaways

- A Massachusetts judge allowed the state to file a 71-page amended complaint against Kalshi, keeping the case active.

- The expanded allegations claim Kalshi’s product effectively functions as sports wagering and that its marketing may reach people under 21.

- Massachusetts’ argument hinges on whether Kalshi must be licensed through the Massachusetts Gaming Commission to comply with state rules.

- The dispute also sits within a wider US battle over whether the CFTC has “exclusive jurisdiction” over prediction markets.

- Gaming and tribal groups are separately pushing Congress for clearer rules through the CLARITY Act.

Expanded allegations in the Massachusetts case

The Tuesday ruling clears the way for Massachusetts authorities to strengthen their claims as the case continues. According to the court filing, the amended complaint builds on earlier allegations that Kalshi engaged in sports wagering in a way that violates state law.

The state’s updated pleading includes accusations that the platform “targets those under 21 years of age” and does not do enough to prevent underage users from accessing the product. The complaint points to Kalshi’s marketing practices and to ad creative that, the filing alleges, shows individuals who appear younger than 21.

Massachusetts authorities also reiterated that Kalshi permits users from age 18 to create accounts and place wagers on sports events by purchasing event contracts, framing that accessibility as incompatible with the state’s approach to online sports wagering.

How the dispute started—and what the judge previously ordered

Massachusetts Attorney General Andrea Joy Campbell announced the lawsuit in September 2025, arguing that Kalshi needed to be licensed by the Massachusetts Gaming Commission to comply with state rules governing online sports wagers.

Earlier developments escalated the dispute quickly. In January, a judge issued a preliminary injunction barring Kalshi from offering sports event contracts while the case was reviewed.

With the latest amended complaint allowed by the court, Kalshi now faces a more detailed version of the state’s allegations as it continues fighting the legality of its sports contracts under Massachusetts law.

Cointelegraph reached out to Kalshi for comment, but did not receive an immediate response. After the initial complaint was filed, a Kalshi spokesperson had said the company was “ready to defend” itself in court.

The federal-versus-state jurisdiction fight over prediction markets

The Massachusetts case is only one part of a broader regulatory tug-of-war in the US. In parallel with state-level enforcement efforts, the CFTC has supported the view that prediction markets fall within its authority.

In April, the CFTC filed a brief in Massachusetts arguing that it had “exclusive jurisdiction” over prediction markets. The agency’s position, under Chair Michael Selig, is that event contracts offered by platforms like Kalshi are “swaps” under the Commodity Exchange Act and therefore should not be governed by state regulation.

As Selig put it in remarks associated with the agency’s stance, Congress has entrusted the CFTC with sole authority to regulate commodity derivatives markets, including prediction markets—and he warned that states attempting to override federal law would face legal challenges.

Why this matters beyond Kalshi: a policy push for the CLARITY Act

Even as the legal arguments could eventually move toward higher courts, some industry and stakeholder groups are urging lawmakers to address the jurisdictional uncertainty with legislation.

Earlier this month, national gaming and tribal organizations and labor groups asked US senators to add language to the Digital Asset Market Clarity (CLARITY) Act. Their request is aimed at explicitly prohibiting event contracts tied to sports and casino-style gaming.

The CLARITY Act—currently under consideration in the Senate—is expected to shape how the CFTC’s authority over digital assets and related market activities is defined. In that context, stakeholders pushing for restrictions on sports and casino-style event contracts are effectively seeking legislative clarity to reduce the need for repeated state-by-state court battles.

Cointelegraph has also reported that the legal landscape for Kalshi and similar platforms has varied by jurisdiction, including instances where the company was blocked from offering sports bets in certain locations.

What to watch next

For market participants and platform users, the next key developments are procedural and strategic: Massachusetts will attempt to sustain its expanded claims after the preliminary injunction, while Kalshi’s defense will likely continue confronting the CFTC’s argument for exclusive federal oversight. At the same time, the direction of the CLARITY Act could determine whether US prediction markets face a patchwork of state litigation or a more uniform regulatory framework.

According to on-chain indicators reviewed by analysts at the crypto exchange Bitfinex, bitcoin (BTC) still has some way to go before it bottoms out in this bear cycle.

The latest Bitfinex Alpha report revealed that the leading digital asset could decline further into the $40,000s by the end of this year as more investors exit the spot market.

A Possible Drawdown Into the $40Ks

In past market cycles, BTC has always declined at least 70% from its all-time highs (ATHs) before bottoming out and recovering. During the 2022 bear market, BTC fell 78% from $69,000, while in 2018, it plummeted 86% below cycle highs near $20,000.

Based on previous drawdown patterns and the time horizons between tops and bottoms, BTC is likely to extend its ongoing decline into the $40,000s. The asset is currently 53.9% down from its ATH of $126,000; dropping into the $40,000s will bring the decline to at least 68%. Additionally, analysts believe BTC could reach its bear-cycle bottom in the fourth quarter of 2026 if cycle estimates account for price moves relative to moving averages.

Analysts say BTC’s structural levels remain unchanged, even though the asset’s floor gave way over the weekend. With the coin trading near $60,000 at press time, it is positioned beneath the True Market Mean of $77,000, a level representing the average cost basis for active investors. This level also serves as a demarcation between bullish and bearish market regimes, so bitcoin’s price action will continue to be defined by a structural bear market environment.

Spot Demand Still Weak

After breaking below the $61,500 support level and falling to a new bear cycle low of $58,136 last week, $53,400 is now the key support level to watch. The move towards $58,000 reflects weakening spot demand as seen in short-term holder selling, exchange-traded fund (ETF) outflows, the collapse of the digital asset treasury channel, and negative gamma pressure.

Unlike previous declines, there were no large-scale liquidations and flushes in open interest as BTC fell below $60,000 last week. This substantiated the fact that the fall was a structural exodus within the spot markets. With the market’s primary demand engine missing, bitcoin’s price is likely to remain weak and continue a downtrend in the coming weeks.

“But the market awaits a resurgence of spot demand to be able to find a floor and potentially turn higher,” analysts explained.

The post Bitcoin Could Fall Into the $40,000s Before Bottoming: Bitfinex Analysts appeared first on CryptoPotato.

Key takeaways:

- The Spot Ether ETF outflows overwhelmed BitMine’s ETH accumulation, raising the chance of a drop below the $1,500 support.

- Falling DApps revenue and weak staking yields highlight limited ecosystem incentives despite tokenization potential.

Ether (ETH) has failed to sustain prices above $1,600 since Thursday, following the broader cryptocurrency market’s downtrend. Lower oil prices created a positive tone that fueled investors’ hopes for more expansionist monetary policy. That setup favors stocks and pushes bond yields higher.

Traders now fear that ETH will not hold the $1,500 support level for long. Spot Ether ETF outflows void the impact of accumulation from Ether treasury companies.

ETH/USD (orange) vs. Total crypto market cap (blue). Source: TradingView

Ether price has declined 31% since May and underperformed the total cryptocurrency market capitalization by 8% over that period. US-listed Ether ETFs saw $345 million in net outflows since June 17, which more than offset the $182 million in ETH accumulation from BitMine Immersion (BMNR US) and Sharplink (SBET US) during the same period.

Regulatory setbacks, AI competition and weak Ethereum onchain metrics

Several factors appear to have held back investor appetite, including regulatory uncertainty in the United States. Meanwhile, the stock market continues to draw attention thanks to strong earnings and lower inflation expectations.

The Digital Asset Market CLARITY Act has awaited a Senate vote since May 15. The bill ends regulation-by-enforcement and clarifies which tokens count as securities. Yet it has faced pushback from lawmakers over provisions regarding stablecoin yields and anti-money-laundering standards.

Democratic lawmakers voiced ethical concerns about the Trump family’s ties to crypto and its role in the World Liberty Financial platform. Most view the CLARITY Act as a positive catalyst for the decentralized finance (DeFi) sector. So ongoing uncertainty around approval hurts institutional demand for ETH.

The artificial intelligence sector now competes with blockchain for data processing as cloud providers deliver services through agentic architectures. Enterprise software leader SAP (SAP DE) has integrated autonomous, modular AI agents natively across multi-vendor clouds, enabling peer-to-peer collaboration.

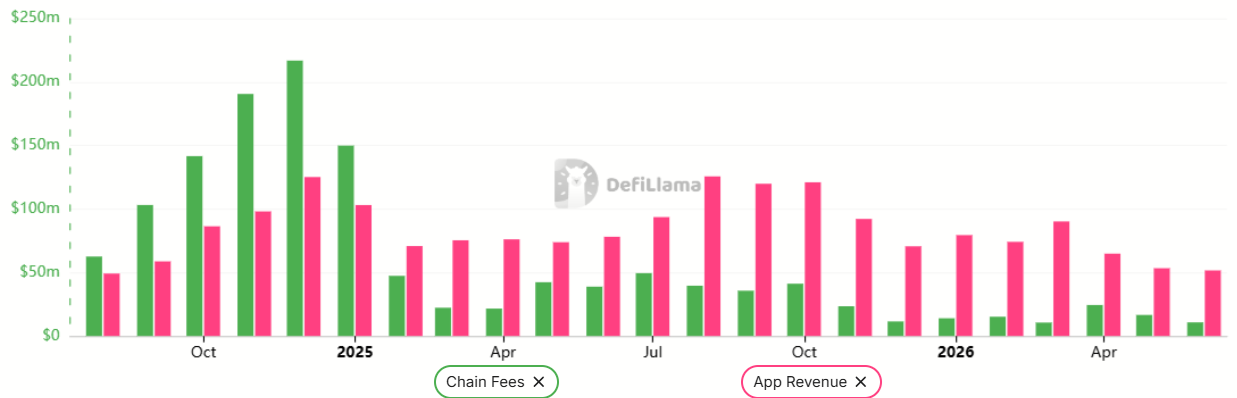

Ether investors also feel disappointment from stagnant Ethereum network fees and decentralized applications (DApps) revenues. As a result, ETH supply becomes inflationary, staking yields remain limited, and fewer incentives exist for ecosystem growth, since part of DApps’ revenue flows back to users.

Ethereum monthly network chain fees vs. DApps revenue, USD. Source: DefiLlama

Ethereum network fees reached only $10.7 million in June, down from $24.4 million in April. DApps revenue hit $51.7 million in June, down from $64.8 million two months earlier. Top contributors included Sky (formerly Maker) at $12.7 million, Titan Builder at $7.2 million, and Chainlink at $4.6 million.

Ethereum supporters argue that tokenization remains in its early innings. The long-term growth potential should create enough blockchain demand to support a much higher ETH valuation.

Related: Ether treasury Sharplink bought $62.4M ETH last week

Ethereum real world assets (RWA) active market capitalization, USD. Source: DefiLlama

While real world assets (RWA) show real promise, the $14.5 billion in tokenized market cap on Ethereum has yet to spark meaningful DeFi activity. With a 2.7% staking yield and weak onchain metrics, the odds of ETH breaking below $1,500 remain in play.

Crypto World

China-linked actors target more than technology as AI competition with U.S. intensifies

U.S.-based cybersecurity giant CrowdStrike has warned of increasing cyberattacks from China-based entities aimed at stealing artificial intelligence to narrow the tech gap with the U.S.

Bill Hinton | Moment Mobile | Getty Images

Cyberattacks aimed at stealing American artificial intelligence technology are increasingly expanding from tech-based attacks to the exploitation of human-level vulnerabilities, with China-based actors playing a growing role.

“As the AI race has heated up, the [People’s Republic of China] has targeted the tech sector increasingly,” said Matt Pearl, director of the strategic technologies program at the U.S.-based think tank Center for Strategic and International Studies.

Rather than focusing on a specific trade secret, such as hardware designs, the hackers have broadened their interest to anything that could narrow the three- to four-month AI gap with the U.S., Pearl said. That, he said, ranges from understanding a company’s product roadmap, particularly in highly competitive sectors, to identifying weaknesses in supply chains.

The alleged cases are already piling up.

In June, U.S.-based cybersecurity giant CrowdStrike said Chinese entities accounted for more than half of state-sponsored intrusions targeting technology companies, especially their AI assets, in the 12 months through March 31.

American tech start-up Anthropic has also accused Chinese companies, including Alibaba, of illicit attempts to steal its AI capabilities. Alibaba did not respond to a request for comment.

Last year, U.S.-based AI content detection startup Copyleaks said the responses generated by Chinese startup DeepSeek’s R1 model resembled those produced by OpenAI’s ChatGPT nearly three-quarters of the time, suggesting the open-source Chinese model may have been trained on the U.S.-developed one.

“We haven’t seen [the same stylistic match] in other LLMs,” said Alon Yamin, CEO and co-founder of Copyleaks.

DeepSeek and OpenAI did not immediately respond to requests for comment.

Brian Abbott, founder and CEO of U.S.-based start-up Agentiq Capital, told CNBC in June that he believed an employee he hired from China last year was an agent of Beijing who purposely altered code and website content to prevent the company from getting venture capital funding.

Abbott alleged the employee replaced references to “ASI,” or artificial superintelligence, with “fintech,” a once-trending term that many investors have soured on.

The individual was dismissed earlier this year, Abbott said, and the company filed a complaint with the FBI. CNBC was unable to independently verify the allegation.

“China’s economic espionage campaign is a continuing threat that costs the American economy hundreds of billions of dollars per year and puts our national security at risk,” the FBI said in a statement to CNBC.

“The FBI prioritizes investigating any potential theft of US technology by foreign actors and remains unwavering in our commitment to protect the homeland.”

The Cyberspace Administration of China and the U.S. Department of State did not offer a comment when contacted by CNBC. None of the individuals interviewed for this piece said they had heard of a similar instance of state-directed subversion of U.S. technology.

Graham Webster, editor-in-chief of Stanford University’s DigiChina Project, said distinguishing state-sponsored espionage from individual or corporate-level efforts can be difficult.

He also pointed out that the conversation about Chinese AI is also affected by major U.S. companies gearing up for major initial public offerings.

“[The] narrative is overtaking reality in a lot of decisions,” Webster said.

“The U.S. government is trying to hold China back to some extent,” he added, referring to technology export controls. “We should not be surprised that the Chinese government tries otherwise.”

Start-ups more at risk

Capital has been a defining driver of the AI race so far, with start-ups racing to rival tech giants or position themselves for acquisitions.

But that’s also created “cyber poverty lines” where small businesses lack the resources of large companies to defend against cyberattacks, said Cliff Steinhauer, director of information security and engagement at the non-profit National Cybersecurity Alliance.

Human vulnerabilities often pose the greater risk, Steinhauer said, particularly as attackers rely on “social engineering” tactics amplified by AI-powered content campaigns.

Cyberattacks can also target new or contracted employees to breach systems.

“We’ve seen a lot of cases within our company, new employees that are joining the company, immediately they’re a target of cyberattacks to get access to our AI models,” Copyleaks’ Yamin said. He expects to see more such cases.

Government and company-led efforts also impact start-up operating costs.

Anthropic on June 11 announced a program called Claude Corps to train 1,000 people in AI and match them with non-profits in the U.S. Meanwhile in China, policymakers have rolled out significant AI support, including free or subsidized computing power and rent-free office space for start-ups.

Isaac Stone Fish, founder and chief executive of consultancy Strategy Risks, said Beijing tends to focus more heavily on large corporations, but startups remain especially exposed since they don’t necessarily have cyber expertise.

“And Beijing’s attempt[s] have certainly increased over the last 18 months, since the release of DeepSeek really kicked off the US-China AI race,” Stone Fish said.

“Beijing wants to ensure that Chinese companies are at the vanguard of the global AI race,” he said. “One way that it does that is by sometimes working to suppress the development of American AI companies, through supply chain restrictions, employee harassment, hacking, targeted government subsidies of copycat competitors, among other strategies.”

“We’ve seen a lot of cases within our company, new employees that are joining the company, immediately they’re a target of cyberattacks to get access to our AI models,” Copyleaks’ Yamin said. He expects to see more such cases.

For startups, balancing rapid innovation with security remains a challenge.

Abbott said the employee he hired was initially willing to work for free, and eventually received a few thousand dollars a month in addition to stock options, before the firing.

“If we paid everybody market rate, for a scrappy start-up I could never afford to do this,” he said, emphasizing the “need to secure our economy of start-ups stateside.”

Tori Spelling had 'more of an emotional outward reaction' over Shannen Doherty's death than her dad Aaron Spelling's

Starmer’s defence plan is woefully inadequate and the price we could all pay is unthinkable. Will Burnham do any better? Our enemies are watching: GENERAL THE LORD DANNATT

Why is South32 stock rallying today?

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Two goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

How To Become Crypto Millionaire #trading #crypto #bitcoin

RECEIVE UNEXPECTED MONEY IN 10 MINUTES (MONEY FLOWS TO YOU) Music to attract money

Crypto Live Trading| 30 june #vinbullindia #livetrading #vinbulllive #live #trading #cryptotrading

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World22 hours ago

Crypto World22 hours agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics5 days ago

Politics5 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos2 days ago

News Videos2 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech5 days ago

Tech5 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World7 days ago

Crypto World7 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World7 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business7 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World4 days ago

Crypto World4 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Business21 hours ago

Business21 hours agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Sports4 days ago

Sports4 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech4 days ago

Tech4 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World4 days ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

You must be logged in to post a comment Login