Crypto World

Visa & Stripe’s Bridge Plan Expands Stablecoin Cards to 100+ Countries

Visa is expanding its stablecoin-linked card program with Bridge, broadening its geographic reach and pushing toward onchain settlement. The latest move lifts the program from its initial Latin American rollout to 18 countries, with a plan to surpass 100 countries across Europe, Asia-Pacific, Africa and the Middle East by year-end. The expansion builds on the program’s April 2025 debut in markets including Argentina, Colombia, Ecuador, Mexico, Peru and Chile, and comes as the two companies test settlement directly in stablecoins through a pilot tied to Visa’s rails and Bridge’s banking partner. The broader industry context features heightened activity around stablecoins in payments, with rival initiatives in the space highlighting a competitive push toward real-time, programmable settlement.

Key takeaways

- Visa and Bridge are extending the stablecoin-linked card program to 18 countries, with a target of more than 100 countries by year-end across Europe, Asia-Pacific, Africa and the Middle East.

- The program’s initial launch in 2025 covered Latin American markets, including Argentina, Colombia, Ecuador, Mexico, Peru and Chile.

- Settlement is moving toward onchain processing, enabled by Bridge’s collaboration with Lead Bank, allowing transactions to be settled in stablecoins instead of fiat.

- Visa is evaluating potential support for Bridge-issued assets, which are created programmatically by businesses rather than by a traditional issuer.

- The move comes amid broader payments-industry activity around stablecoins, including Mastercard’s recent stablecoin card enablement with MetaMask in the United States.

Tickers mentioned: $USDT, $USDC

Market context: The expansion aligns with a wider shift toward crypto-enabled payments and onchain settlement rails, as major incumbents test how tokens can streamline merchant settlements and reduce counterparty risk in everyday purchases.

Market context: Linked to broader USDt and USDC usage in payments, the push also sits against a backdrop of regulatory scrutiny and ongoing experimentation with tokenized settlement in traditional rails.

Why it matters

The enhanced collaboration between Visa and Bridge underscores a strategic bet on programmable, onchain settlement as a means to speed up merchant settlements and improve transparency for card programs built on stablecoins. By enabling issuers and acquirers to settle transactions directly in stablecoins, the network could reduce latency and friction inherent in fiat conversions, especially for cross-border transactions or cross-currency purchases. The approach also signals an appetite to expand the set of tools available to fintechs and brands that want to issue their own digital dollars or stable assets tailored to their customer base, without relying solely on a third-party issuer.

Bridge’s participation remains central to the evolution of these rails. The program leverages Bridge’s infrastructure to enable onchain settlement, with Lead Bank providing the regulatory and banking framework necessary to move transactions from card networks into the onchain ecosystem. In practice, this arrangement allows card issuers to settle in stablecoins rather than converting transactions to local fiat post-authorization, aligning settlement timelines with blockchain realities and potentially improving settlement finality for merchants and consumers alike.

From a competitive standpoint, the Visa-Bridge expansion sits alongside a broader trend in the payments space: the growing willingness of major processors to experiment with crypto rails. Mastercard, for example, has recently enabled stablecoin card spending in the US through a partnership with the MetaMask wallet, illustrating how traditional payment networks are responding to consumer interest in crypto-backed payments and the desire for real-time settlement capabilities. The juxtaposition of these efforts signals a broader industry push toward integrating crypto-native settlement with fiat-backed consumer spending, while navigating the regulatory and risk considerations that come with such a transition.

Visa’s crypto leadership has been clear about meeting businesses where they operate. Cuy Sheffield, Visa’s head of crypto, has framed the expansion as part of a broader strategy to bring the speed, transparency and programmability of stablecoins into the settlement process. The company is exploring how Bridge-issued assets—stablecoins that are created programmatically by businesses on Bridge’s platform—could be supported more broadly within Visa’s network, a path that could unlock new programmable currency options for merchants and brands that want to control settlement terms or tokenized reward structures. Unlike the most widely used stablecoins issued by independent entities, Bridge-issued assets are designed to be created and managed via Bridge’s infrastructure, a model that could appeal to fintechs seeking bespoke token strategies.

Bridge has positioned the expansion as a step toward more seamless, on-chain settlement for digital-asset-enabled card programs. The practical effect is a potential reduction in the time and complexity involved in moving value from a customer’s stablecoin balance to a merchant’s local currency—an outcome that could matter for shoppers who want near-instant payments and for issuers seeking tighter control over settlement economics. The program’s onchain settlement is described as a natural extension of Bridge’s rail, with Lead Bank acting as the bridge between traditional banking and the onchain settlement layer. In a mid-February update, Bridge noted that it had received conditional approval from a regulator to become a national trust bank, a milestone that underscores the regulatory dimensions of this kind of expansion and the careful navigation required to scale such rails.

As part of the broader, ongoing stablecoin race in payments, Visa’s initiative adds to a landscape where banks and fintechs are willing to experiment with programmable money at the point of sale. The expansion’s strategic rationale rests on creating more options for merchants to accept stablecoins without abandoning familiar payment interfaces, and for consumers to transact with tokens that can be settled efficiently. By aligning with Bridge’s architecture and Lead Bank’s regulatory framework, Visa is building a more integrated model where stablecoins do not live only in wallets or exchanges but become a practical settlement instrument for everyday card purchases.

The announcement also highlights a broader industry trend: the move toward enhanced interoperability between card rails and blockchain settlement. If the onchain settlement pilot proves scalable, issuers may gain more flexibility in structuring rewards, fees and settlement terms around stablecoins, potentially broadening the appeal of crypto-enabled cards to a wider audience of merchants and cardholders. While regulatory considerations remain a constant backdrop, the practical demonstrations of speed and transparency in settlement have kept this initiative in the spotlight as a potential blueprint for future integrations across the payments ecosystem.

What to watch next

- Timeline and results of the onchain settlement pilot with Lead Bank and Bridge; potential adjustments to settlement cadence and liquidity requirements.

- Progress toward the goal of reaching 100+ countries by year-end, and which markets will be prioritized in the near term.

- Details on Visa’s potential support for Bridge-issued assets and any regulatory approvals that shape that path.

- Regulatory developments regarding Bridge’s national trust bank status and how they affect cross-border card programs.

Sources & verification

- Visa and Bridge expansion to over 100 countries: official Visa investor relations announcement.

- Original Latin American rollout: Visa and Bridge collaboration announcement outlining the April 2025 launch.

- Onchain settlement pilot and Bridge-Lead Bank collaboration: Visa press materials and Bridge announcements, including regulatory status updates.

- Industry context: Mastercard’s stablecoin card spending in the US via MetaMask—contextual reference in related coverage.

Key figures and next steps

Market reaction and key details

Why it matters

The Visa-Bridge collaboration represents a deliberate push to embed stablecoins deeper into everyday payments while testing the viability of onchain settlement for consumer card programs. If the pilot demonstrates efficiency gains and regulatory viability, issuers and merchants could gain access to more flexible settlement terms and new token-based monetization options. For users, the prospect of faster settlement and more predictable funds availability could enhance the appeal of stablecoins as a practical payments tool, particularly for cross-border purchases and commerce that spans multiple currencies.

Beyond Visa, the broader payments ecosystem is watching how these rails will coexist with existing fiat-based settlement, risk controls, and compliance regimes. The tension between innovation and regulation remains a key driver, but the ongoing experiments with stablecoins at the point of sale reflect a maturing phase in crypto-enabled payments where real-world usage and governance concerns are increasingly aligned. As more institutions participate, the competence and reliability of onchain settlement in consumer contexts will be tested under a variety of market conditions, from everyday retail transactions to cross-border remittances.

What to watch next

- End-of-year milestones for country expansion and the potential scaling of onchain settlement.

- Regulatory updates on Bridge’s national trust bank status and related compliance requirements.

- Adoption metrics from merchants and issuers participating in the program, including any changes in settlement times and cost structures.

Viral “predictive historian” Jiang recasts Bitcoin as a CIA war‑surveillance tool and hinge of U.S. imperial decline, mixing sharp geopolitical reads with conspiratorial leaps.

Summary

- Viral “predictive historian” ties Bitcoin to U.S. imperial decline and a coming monetary reset

- Jiang claims BTC is a Pentagon/CIA surveillance weapon even as markets treat it as digital gold

- Critics say his “predictive history” blends accurate war calls with speculative crypto conspiracies

Beijing-based teacher Jiang Xueqin, the self-styled “predictive historian” who shot to fame for forecasting Donald Trump’s return to the White House and a disastrous U.S.–Iran conflict, is now recasting Bitcoin (BTC) as a tool of American empire and a hinge of a looming new world order. In recent lectures and clips circulating across YouTube, TikTok and X, Jiang argues that the world is witnessing “the end of U.S. imperial overextension” and that the monetary fallout will drive Bitcoin into “a structurally different regime” rather than another cyclical boom. He frames his analysis as “predictive history,” a fusion of structural geopolitics and game theory designed, in his words, to “test models against reality, just like artificial intelligence systems.”

In a widely shared breakdown of his Bitcoin thesis, Jiang claims that the cryptocurrency was not the work of a lone cypherpunk, but a Pentagon project engineered as “the ultimate surveillance technology,” echoing variations of the line that “Bitcoin was created by the CIA and the Deep State.” He tells audiences that Satoshi Nakamoto’s anonymity is “institutionally suspicious,” arguing that only an agency-backed team would have “the time, money, servers, and technical expertise” to deploy a global monetary network. At the same time, he leans on a factual point that mainstream analysts and chain‑forensics firms agree on: Bitcoin’s public ledger enables authorities to trace flows of illicit funds with far more granularity than cash.

Jiang’s crypto worldview is tightly bound to his geopolitical script. In multiple interviews and classroom talks repackaged online, he links U.S. “imperial overreach” in the Persian Gulf to a sequence of events in which military failure accelerates dollar erosion, pushes capital out of Treasuries and into hard assets and ultimately sends Bitcoin “nuclear.” One popular YouTube macro-finance explainer built around his framework describes Bitcoin as “the most liquidity-sensitive asset on the planet,” noting that “every dollar of monetized conflict cost is a dollar that enters the global financial system searching for hard assets with fixed supply,” with Bitcoin’s 21 million cap presented as the end of that chain. In that scenario, the video argues, the Bitcoin cycle is “not driven by the halving” but “by the fiscal response to imperial overextension,” applying Jiang’s method directly to BTC’s trajectory.

That framing has resonated with traders already treating Bitcoin as a barometer of war risk. Bloomberg recently reported that “crypto markets are once again serving as the only open window into how traders are pricing the continuing conflict” in Iran, as spot and derivatives flows react in real time to escalation headlines. Bitcoin has traded around the mid‑$60,000 to low‑$70,000 range in March, with some market forecasts projecting a possible move toward roughly $73,000–$79,000 this month while volatility remains high. Even mainstream price coverage now routinely situates BTC within a matrix of war risk, dollar policy and ETF‑driven institutional demand.

Jiang’s rise has been turbocharged by the perception that he “called” both Trump’s 2024 victory and the subsequent U.S.–Iran war, predictions that have been amplified by crypto traders, TikTok creators and even long‑form podcasts. An in‑depth profile notes that his YouTube channel, Predictive History, consists largely of unedited classroom lectures in which he maps great‑power cycles and “world order changes” for Beijing high‑school students. But academic critics and archaeologists have pushed back hard, warning that his method replaces evidence with grand narrative. In a recent debunking video, archaeologist Flint Dibble described Jiang as “a wacko who spreads insanely harmful conspiracy theories,” stressing that “his predictions about the future are mostly not accurate… a broken clock is right twice a day.”

The same tension defines his Bitcoin work. A detailed breakdown of “Professor Jiang’s Theory on Bitcoin’s Origins” acknowledges that he “mixes verifiable facts with baseless leaps of logic,” conceding that while DARPA did seed the early internet and Bitcoin’s transparency does aid law enforcement, there is “no public evidence linking Bitcoin’s creation to DARPA, the Pentagon, or the CIA.” Instead, Jiang’s narrative slots crypto into a larger story about the end of U.S. hegemony, the rise of a multipolar order and the search for new monetary anchors—a story that is shaping how a growing slice of retail traders interpret every tick in Bitcoin’s price chart, whether or not his “predictive history” ultimately passes its own reality test.

Stablecoin issuer Circle’s (CRCL) shares tumbled on Tuesday, after a draft version of U.S. stablecoin legislation raised concerns about limits on yield.

The stock of the USDC issuer fell as much as 18% in the early U.S. session, snapping a weeks-long rally that saw more than 100% gain. Meanwhile, crypto platform Coinbase (COIN), which shares revenue coming from the stablecoin, dropped about 8%.

The key catalyst behind the move was the latest version of the Clarity Act, as reported by CoinDesk, which would restrict offering rewards on stablecoin balances, analysts pointed out.

“Clarity Act could potentially ban yield payments for simply holding a stablecoin (e.g. passive balances) and restrict any approach that makes the program in any way equivalent to a bank deposit,” said Mizuho analyst Dan Dolev.

According to Dolev’s analysis, a potential ban could reduce the use case for Circle in the near-term, while not paying rewards would reduce the long-term attractiveness of holding USDC on Coinbase’s platform.

Stablecoin yield — whether through onchain lending or platform incentives — has been a big part of the pitch to investors. Taking that away makes it harder for tokens like USDC to evolve beyond simple payments.

“That weakens a key part of the bull case,” said Shay Boloor, chief market strategist at Futurum Equities, arguing it limits USDC’s path toward becoming a true store-of-value product.

The stablecoin-focused GENIUS Act banned issuers from paying yield directly to users, but they’ve built ways to pass through income earned on reserves. Circle collects interest on USDC’s backing assets and shares it with Coinbase, which in turn funds rewards for users.

The latest draft of the Clarity Act targets that structure by banning anything “economically equivalent to interest,” effectively cutting off a key incentive for holding stablecoins, according to Amir Hajian, a digital asset researcher at Keyrock

“It pulls the rug on the pass-through model that has been driving stablecoin adoption,” Hajian said.

There was another development in the background. Tether, issuer of the USDT stablecoin and main rival of Circle, said it has hired one of the ‘Big Four’ accounting firms to conduct a long-promised full audit of its reserves. If successful, the audit could improve USDT’s image among institutional users by demonstrating stronger risk management, potentially eating into USDC’s market share.

Not ‘as bad’

The selloff comes after a strong run, during which Circle shares gained 170% since early February, far outpacing other crypto stocks and the struggling broader stock market. That setup left the stock vulnerable to a sharp pullback on any negative headlines.

Still, analysts aren’t seeing this as an existential crisis.

According to Mizuho’s Dolev, recent outperformance of USDC’s volume means “use cases [for stablecoins] are starting to proliferate, which is a positive for the long-term” for Circle. Meanwhile, Coinbase could see a boost in profitability in the near-term as USDC accounts for about 20% of Coinbase’s revenue, and a large part of it is paid out as rewards.

In fact, Owen Lau, an analyst at Clear Street, said that “the actual situation doesn’t appear to be as bad as the headline indicates. “It looks like an overreaction, but the market tends to shoot first and ask questions later.”

Ryan Rasmussen, head of research at digital asset manager Bitwise, agreed that investors should see past today’s short-term headwinds. Circle is still up more than 30% this year after Tuesday’s drop, and remains a major player in a fast-growing market, he noted. “There will be workarounds,” such as loyalty programs that could replicate similar incentives as yield, Rasmussen said.

“With that in mind, Circle’s long-term outlook has never been better; they hold a 30% share of a market projected to grow 10x over the next four years,” he added.

UPDATE (March 24, 15:46 UTC): Adds analyst comments.

TLDR

- Missouri lawmakers advanced HB 2080 to create a state-managed Crypto Strategic Reserve Fund.

- The bill includes XRP alongside Bitcoin, Ethereum, Solana, and USDC as approved reserve assets.

- The State Treasurer would have authority to buy, hold, and manage digital assets using state funds.

- The legislation requires the Treasurer to hold acquired cryptocurrencies for at least five years.

- Missouri agencies could accept USDC for taxes, fees, and fines with approval from the Department of Revenue.

Missouri lawmakers have moved to create a state-managed crypto reserve that would include XRP. The House Committee Substitute for HB 2080 cleared the Commerce Committee in a 6–2 vote. The proposal now advances with a “Do Pass” recommendation and outlines direct authority for the State Treasurer.

Missouri Advances Bill to Establish Crypto Strategic Reserve Fund

Representative Ben Keathley sponsored HB 2080 to establish a Crypto Strategic Reserve Fund. The House Committee Substitute outlines how the State Treasurer would manage approved digital assets. Lawmakers advanced the measure after a 6–2 committee vote, and no member voiced opposition during hearings.

Under the bill, the Treasurer can buy, hold, and manage selected cryptocurrencies using state funds. The proposal requires the Treasurer to store acquired digital assets for at least five years. After that period, the Treasurer may sell, convert, or allocate holdings based on state strategy.

The fund can also receive digital assets through donations, grants, or transfers from residents and public entities. The legislation authorizes partnerships with third-party custodians to secure state-held assets. It also requires the Treasurer to publish transparency reports every two years.

Lawmakers included compliance measures to restrict transactions tied to foreign or illegal entities. The Department of Revenue would oversee approval for crypto payment systems within state agencies. These provisions aim to ensure oversight while enabling digital asset management.

XRP Included Alongside Bitcoin, Ethereum, Solana, and USDC

HB 2080 lists XRP among the digital assets eligible for state reserve holdings. The bill places XRP alongside Bitcoin, Ethereum, Solana, and USDC in the proposed fund. This classification allows the Treasurer to treat XRP as part of a long-term reserve strategy.

The Treasurer may purchase XRP directly with allocated state funds under the bill. The office may also accept XRP transfers from residents or other government bodies. The legislation frames these holdings as part of a structured reserve plan.

The proposal does not set a fixed dollar cap for XRP acquisitions. Instead, it grants the Treasurer discretion within existing state financial controls. The five-year minimum holding period applies to XRP and other approved assets.

Lawmakers structured the bill to mirror traditional reserve management models. The framework allows conversion or liquidation after the mandatory holding period. Officials must document these actions in the required biennial reports.

The committee vote advanced the bill without recorded public opposition. Representative Keathley stated that the measure supports “long-term financial strategy for the state.” The bill now proceeds through the legislative process for further consideration.

USDC Payments and Federal Digital Asset Reserve Efforts

The legislation also authorizes Missouri agencies to accept USDC for certain payments. Government entities may process USDC for taxes, fees, and fines with Department of Revenue approval. This step integrates stablecoin payments into state systems.

State agencies must follow strict compliance standards when accepting USDC. The bill prohibits transactions involving sanctioned or unlawful entities. Agencies may coordinate with approved custodians to manage payment processing securely.

The measure aligns with broader federal digital asset initiatives announced in 2025. President Donald Trump signed an executive order to establish a national Bitcoin reserve and an altcoin stockpile. Federal authorities continue to work to implement that directive.

Missouri lawmakers now await further legislative action on HB 2080. The bill outlines clear authority for reserve creation and digital asset management. Lawmakers will determine the next procedural steps in the current session.

The Solana Foundation has revealed it has secured Mastercard, Worldpay, and Western Union as early users of its newly launched developer platform, as part of ongoing efforts to attract enterprises to build on its blockchain.

The Solana Developer Platform (SDP) was announced on Tuesday to enable enterprise developers to build on the blockchain using a unified interface.

Much of the focus is on real-world asset tokenization, including stablecoins, which is currently a $328 billion market, according to rwa.xyz. More than half of the total value is held on Ethereum; however, with Solana holding 6.3% share of the tokenized real-world asset market.

“The early interest we’ve seen from enterprises and institutions signals strong demand,” said Catherine Gu, the head of product at the Solana Foundation.

The SDP will initially have three core modules: an issuance module to deploy tokenized real-world assets, a payments module to facilitate fiat and stablecoin flows, and a trading module due later this year that will support atomic swaps, vaults, and onchain forex.

Early users of the SDP include Mastercard for stablecoin settlement, Worldpay for merchant payments and settlement, and Western Union for cross-border payments, said the Solana Foundation.

Solana’s efforts to attract institutions

Solana invested in making the network enterprise-ready on a technical level with the Alpenglow upgrade in 2025, boosting transaction throughput. Meanwhile, in December, Visa launched USDC (USDC) settlement for US banks on the Solana blockchain.

“The next phase of digital asset innovation will be defined by practical use cases that integrate seamlessly with existing financial systems,” said Raj Dhamodharan, executive vice president, blockchain and digital assets, at Mastercard.

Related: Agentic AI commerce may spell the end of internet ads: a16z Crypto

Meanwhile, Malcolm Clarke, vice president of digital assets at Western Union, said the SDP is “not a replacement for our network,” but allows it to expand use cases and bring more cross-border activity.

Solana enters a crowded enterprise blockchain space

Enterprise-grade blockchain solutions are not new, and Solana’s latest platform enters a crowded market.

The Ethereum ecosystem has several strong offerings targeting the same enterprise audience, including Consensys’ Infura, a scalable API infrastructure powering thousands of decentralized applications.

Consensys also has the Linea layer-2, which is positioning itself as an institutional on-ramp to crypto.

Coinbase’s Ethereum layer-2 platform Base has modular components for checkout, APIs, and commerce payments that directly compete with SDP’s payments module.

Meanwhile, Ripple’s blockchain offerings, such as XRP Ledger, also primarily target enterprise and financial institutions, as it aims to become the standard for cross-border payments.

Magazine: Google flags crypto malware, retiree loses $840K in ‘expert’ scam: Hodler’s Digest

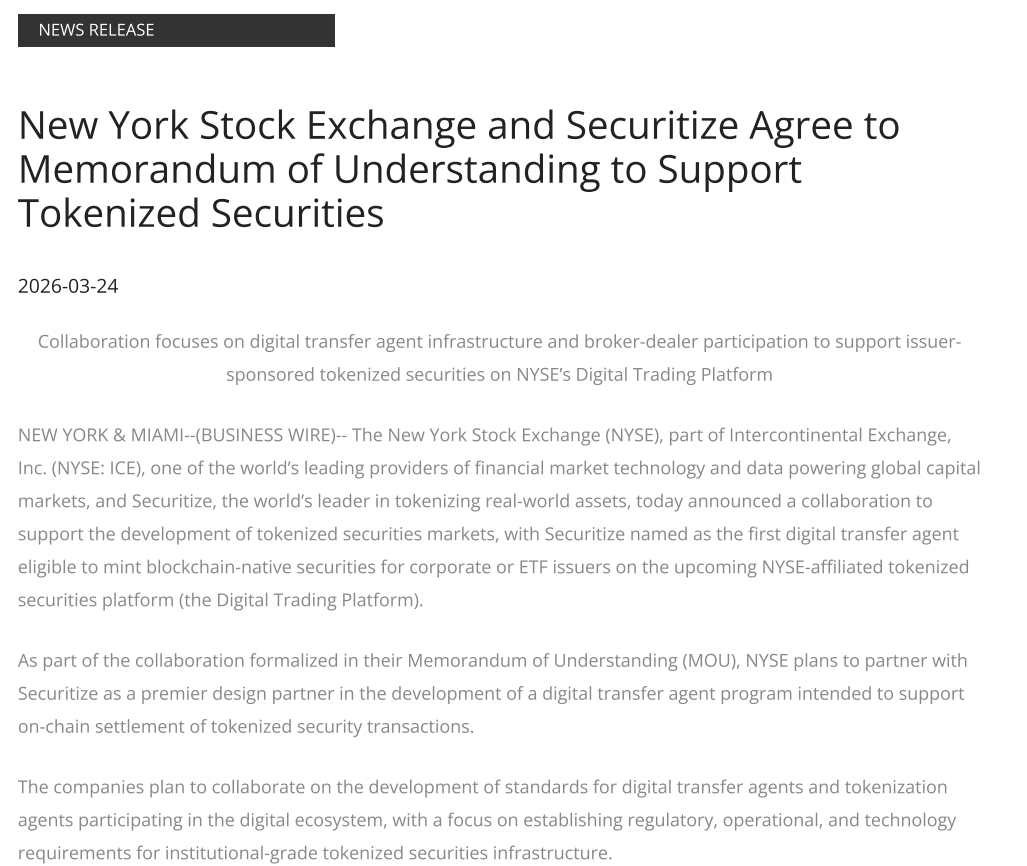

The New York Stock Exchange (NYSE) has signed a memorandum of understanding (MoU) with tokenization platform Securitize, as part of a broader effort to develop blockchain-based stock trading infrastructure for Wall Street.

Securitize will become the first digital transfer agent, enabling it to mint blockchain-based shares for stocks and exchange-traded funds (ETFs) on the upcoming tokenized securities platform, the Digital Trading Platform, according to a Tuesday announcement from Intercontinental Exchange (ICE), parent company of the NYSE.

Under the MoU, the companies plan to develop a digital transfer agent program and standards for digital transfer agents and tokenization agents, with a focus on regulatory, operational and technology requirements for tokenized securities infrastructure.

The announcement builds on ICE’s Jan. 19 plan for a tokenized securities venue designed for 24/7 trading, instant settlement, stablecoin-based funding and onchain settlement.

ICE said the planned venue is designed to support both tokenized shares that are fungible with traditionally issued securities and securities issued natively as digital tokens, while preserving traditional shareholder dividends and governance rights. Tokenized stocks are shares of traditional company stocks minted on the blockchain ledger, offering investors exposure to stock prices with advantages including 24/7 accessibility and fractional ownership.

The agreement is the latest sign that major exchange operators are building blockchain-based trading and settlement infrastructure, even as the regulatory and market structure for tokenized public securities is still taking shape.

The news follows the US Securities and Exchange Commission giving the regulatory greenlight to Nasdaq’s pilot proposal on Thursday to support the trading of tokenized versions of high-volume stocks and securities.

“As we explore how tokenization can enhance capital markets, it is critical that new infrastructure is developed in a way that preserves the trust, transparency, and protections investors expect,” said Lynn Martin, president at NYSE Group.

Related: US financial markets ‘poised to move on-chain’ amid DTCC tokenization greenlight

Tokenized stocks surpass $1 billion amid rising demand

Investor demand for blockchain-based tokenized stocks is increasing. The total value of tokenized stocks surpassed $1 billion on March 10, in a significant milestone for the real-world asset (RWA) sector.

Over the past 30 days, tokenized stockholders rose by 16% to 193,140, while the monthly transfer volume increased by 45% to $2.5 billion, according to data from RWA.xyz.

Still, tokenized stocks are only the sixth-largest segment of the $26 billion value locked into tokenized RWAs. Tokenized treasury debt was ranked first with $11.8 billion, and tokenized commodities second with over $5 billion.

Some of the leading crypto exchanges are also racing to launch tokenized stock offerings. Coinbase launched 24/7 stock perpetual futures for non-US traders on Friday, offering cash-settled exposure to major US stocks and indices, including Apple and Nvidia.

Crypto exchanges Binance and Kraken have also launched tokenized perpetual futures trading for non-US traders, along with numerous other offshore platforms.

Magazine: Can Robinhood or Kraken’s tokenized stocks ever be truly decentralized?

Bitcoin price is ripping. BTC USD reclaimed $71,000 Tuesday afternoon, erasing weekend losses immediately after President Trump ordered a five-day delay on strikes against Iranian energy infrastructure.

The sudden de-escalation signal triggered a violent capital rotation: oil futures collapsed nearly 10%, gold prices retreated 3.7%, and crypto assets surged in a classic risk-on relief rally.

Traders were positioned for immediate escalation following the expiration of a 48-hour ultimatum, but the pause caught bears offside.

While West Texas Intermediate (WTI) crude plummeted to $85.45 on the news, Bitcoin decoupled from the broad commodity sell-off, validating its role as a liquidity gauge rather than a pure safe haven in this cycle.

- Price Action: Bitcoin rallied from a low of $67,436 to a high of $71,782 within hours of the announcement.

- Macro Shift: Oil and gold plunged as war risk premiums evaporated, boosting risk asset liquidity.

- Market Signal: Short sellers were liquidated as sentiment flipped from fear to greed in under 60 minutes.

Can Bitcoin Price Reclaim $72,000 Price Resistance?

Bitcoin held $68,000 through peak uncertainty and is now pushing into the supply zone above $71,500.

Bulls need one thing: a confirmed 4-hour close above $72,000. That invalidates the lower-high structure built earlier this month and opens the next leg up.

Daily RSI has reset from overbought and is trending up near 58. Room for continuation exists. The 50-day EMA is the critical floor. Lose it and this rally gets exposed as a headline-driven bull trap.

Bull case: reclaim $72,000, consolidate, retest the March high at $75,620. Bear case: rejection at $71,800 sends price back to $68,500. Lose that and $65,000 opens up.

The short squeeze did the heavy lifting on the way up. CoinGlass data shows over $271 million in short positions liquidated in the hours after the White House announcement. Traders positioned for a breakdown below $67,000 got wiped and their forced covering poured fuel on the move.

Funding rates have ticked up but open interest has not reclaimed year-to-date highs. Spot buying and short covering are driving this, not leveraged froth. That is a healthier signal for trend sustainability than a derivatives-led pump.

The Macro Pivot: Why $85 Oil Matters

The correlation between Bitcoin and energy markets has inverted. While oil prices tumbled 9.8%—with Brent crude falling to $98.66—Bitcoin surged. This highlights the market’s current logic chain: lower oil prices reduce the risk of sticky inflation, which in turn lowers the probability of a hawkish Federal Reserve response.

Gold, traditionally the primary safe haven, dropped 3.7% as the immediate war premium exited the market. This divergence is critical.

While Bitcoin and gold decoupled during the Hormuz crisis, today’s action confirms that crypto is trading on liquidity dynamics rather than fear. When the threat of $150 oil vanished, the liquidity outlook improved, and Bitcoin pumped.

Investors should monitor the five-day deadline closely. If tensions flare again and oil reclaims $100, the headwinds for risk assets will return.

Traders are watching $70,000 holding as support into the daily close. Maintain this level, and the path to new highs is open. Fail here, and the market returns to choppy consolidation. The trend is up, but the geopolitical fuse is still lit.

BTC USD Price Is Bullish, And Investors Are Ready to Rotate to Infrastructure as Hyper Targets SVM Scalability

As the gold price crash and Bitcoin rally reshape portfolio allocations, smart money is beginning to rotate profits into high-growth infrastructure plays.

While Bitcoin secures its position as digital collateral, attention is turning to Bitcoin Hyper (HYPER), a protocol focused on bringing scalability to the Bitcoin network through high-performance Layer 2 solutions.

Bitcoin Hyper has now raised over $32 million in its ongoing presale, signaling strong institutional appetite for Bitcoin-native DeFi.

The project targets the scalability dilemma by integrating Solana Virtual Machine (SVM) architecture directly with Bitcoin’s security layer. With the token currently priced at $0.0136 and staking APY exceeding 89%, early entrants are positioning for the next phase of the Bitcoin ecosystem evolution.

Investors looking to hedge against spot volatility are diversifying into infrastructure layers that capture transaction volume regardless of short-term price action.

Visit the Official Bitcoin Hyper Website Here

The post Bitcoin Price Reacts as Trump Delays Iran Strike, Oil and Gold Volatile appeared first on Cryptonews.

NEW YORK — Amy Oldenburg, the head of digital asset strategy at Morgan Stanley (MS), rejected the idea that Wall Street is only now embracing crypto due to fear of missing out, arguing that large banks are acting after years of preparation.

“TradFi is getting FOMO and is now getting involved … it really isn’t accurate,” Oldenburg said during a panel at the Digital Asset Summit in New York on Tuesday. “We’ve been on a journey around the entire modernization of financial infrastructure for years.”

Her comments come as major U.S. banks, long seen as cautious on crypto or latecomers to the industry, begin to expand their offerings. For years, firms like Morgan Stanley restricted activity to indirect exposure, such as offering wealthy clients access to bitcoin funds.

More recently, that’s included spot bitcoin exchange-traded funds (ETFs) on its E*Trade platform and the bank this month even filed to launch its own spot bitcoin ETF.

Broader participation was slowed by regulatory uncertainty and concerns around custody, compliance and market structure. That stance has started to shift, and Morgan Stanley has now outlined a more defined digital asset strategy, with efforts spanning trading, asset management and infrastructure.

Oldenburg said the bank is preparing to support tokenized equities trading on its alternative trading system.

“One of the things that we are planning for the second half of 2026 is turning on our trajectory cross … to support tokenized equities later this year,” she said. The platform already handles equities, ETFs and American depositary receipts (ADRs), which she described as a natural base for expansion.

Inside the firm, the transition requires reworking core systems. “We are having to re-teach ourselves what legacy infrastructure, pipes and plumbing look like,” Oldenburg said, pointing to the challenge of upgrading decades-old financial architecture to support faster settlement and continuous trading.

She also highlighted a gap between crypto startups and large institutions.

“There’s so many other connectivity points that we need to plug in around it,” she said, noting that founders often underestimate how complex bank systems are.

Even so, areas like stablecoins are gaining traction as a way to move money faster and at lower cost than traditional systems.

Adoption, however, depends on coordination across the financial system. “We can’t just modernize on our own,” Oldenburg said. “This is an incredibly complex, integrated global network.”

Despite weak token prices, she said activity continues to build. “It really is very early innings,” Oldenburg said, signaling that Wall Street’s deeper integration with crypto may be gradual, but its underway.

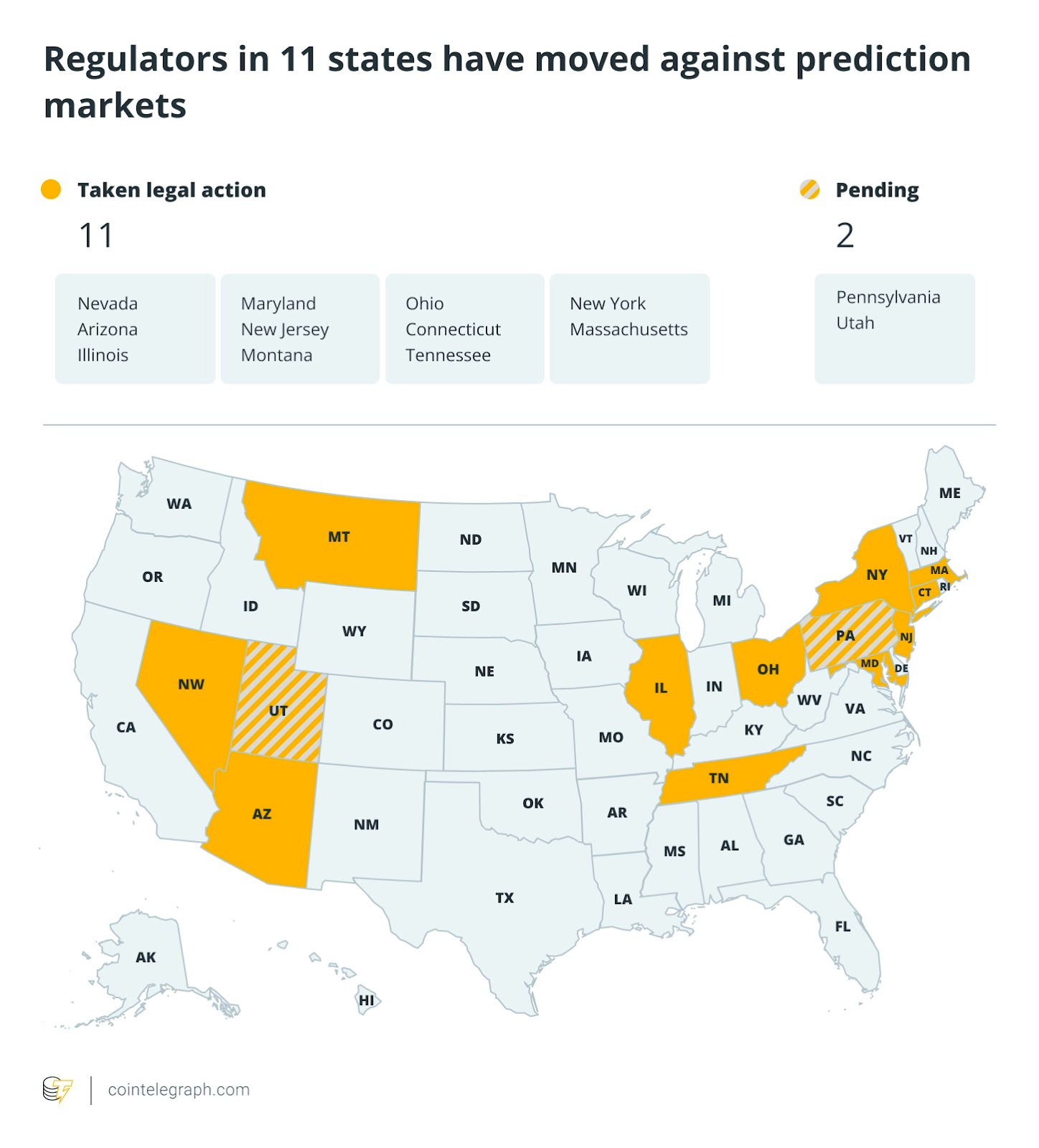

Momentum is building across US states to regulate or restrict prediction markets, with multiple legal actions targeting platforms such as Kalshi.

On March 20, Carson City District Court Judge Jason Woodbury in Nevada made his state the first to issue a temporary ban on prediction market Kalshi from operating. Gaming officials said that the platform violated state gambling laws.

Nearly a dozen other states have also issued various forms of legal proceedings. Most have filed cease-and-desist letters, while Arizona has even brought criminal charges against Kalshi. Other states are considering new legislation for prediction markets.

The patchwork enforcement across states has brought national attention, and regulations at the federal level are looming.

Nevada bans Kalshi while Arizona opens criminal charges

In 11 states across the US, local authorities have taken legal action against prediction markets like Kalshi and Polymarket.

The state of Nevada managed to initiate a temporary ban, which blocked Kalshi from operating in the state for 14 days. The motion was initially put forward by the Nevada Gaming Control Board.

The board’s chair, Mike Dreitzer, said that prediction markets “facilitate unlicensed gambling” and are therefore illegal in the state. “We have a statutory duty to protect the public,” he said.

Sports betting and gaming lawyer Daniel Wallach wrote that the order prevents Kalshi from offering “event-based contracts relating to sports, politics and entertainment to people within Nevada without first obtaining all required licenses.”

Just a few days earlier, the neighboring state of Arizona filed criminal charges against the firms behind Kalshi. Arizona Attorney General Kris Mayes’ office filed a complaint, alleging that Kalshiex LLC and Kalshi Trading LLC were “running an illegal gambling operation and taking bets on Arizona elections, both of which violate Arizona law.”

The announcement claimed Kalshi ”accepted bets from Arizona residents on a wide range of events in violation of Arizona law. These events included professional and college sporting contests, proposition bets on individual player performance, and whether the SAVE Act would become law.”

Betting on sports requires a gaming license, and Arizona law outright bans bets on elections.

Other states have either put forward or are considering new regulations. In Utah, State Representative Joseph Elison put forward HB243, which would define proposition betting as “a gambling bet on an individual action, statistic, occurrence, or non-occurrence.”

In Pennsylvania, Representative Danilo Burgos announced plans to introduce legislation that would regulate prediction markets and put them under the regulatory purview of the Pennsylvania Gaming Control Board. The bill will propose:

-

a 34% state tax and 2% local share assessment on gross revenue,

-

to ban underage users,

-

to include self-exclusion lists for user protection, and

-

strict Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols.

Numerous other states have issued cease-and-desist letters to prediction markets and attempted to block their activities through the courts. Not all of them have been successful. In Tennessee, Judge Aleta Trauger of the US District Court for the Middle District of Tennessee blocked a state injunction that would prevent Kalshi from operating there. The court concluded that the event contracts were “swaps” under the Commodity Exchange Act (CEA), which gives the US Commodity Futures Trading Commission (CFTC) exclusive jurisdiction.

Kalshi did not respond to Cointelegraph’s request for comment at publishing time.

Who should regulate prediction markets?

The patchwork of different enforcement actions — and varying reactions to them by different courts — has brought into question who should regulate prediction markets and how. Prediction markets and their proponents believe that the power should lie with the federal government and the CFTC.

Elison, the sponsor of the law in Utah, told local media, “It’s a huge gray area and there’s lots of lawsuits all over the country right now […] debating this very thing, trying to find out what are the actual definitions.”

“They’re flying under what’s called prediction markets, and prediction markets are regulated by the Federal Commodities Exchange [sic]. That’s why they’re able to do it,” he said.

A Kalshi spokesperson previously told Cointelegraph, “States like Arizona want to individually regulate a nationwide financial exchange, and are trying every trick in the book to do it. As other courts have recognized and the CFTC affirms, Kalshi is subject to federal jurisdiction.”

“It’s different from what sportsbooks and casinos offer their customers, and it should not be overseen by a patchwork of inconsistent state laws,” they stated.

Aaron Brogan, founder of crypto-focused law firm Brogan Law, wrote, “Prediction markets’ ‘crime,’ the reason that so many states have pursued and will continue to pursue action against them until they win or are stopped, has nothing to do with the merits of these markets.”

Since they are currently regulated under the CEA, and therefore under the oversight of the CFTC, “states will not be able to control them, and more importantly, may not be able to tax them,” Brogan said. According to the American Gaming Association, at stake is billions of dollars in tax revenue across the 40 states where online sports betting is legal.

Some state lawmakers aren’t so shy about this. Burgos wrote that the “regulatory arbitrage” of prediction markets skirting state laws “leaves our constituents vulnerable and deprives the commonwealth of significant tax revenue.”

Speaking to local media, he said that the state should have the ability to tax an activity, particularly when it can harm constituents. “It’s another opportunity to expand the tax base. […] And like everything else that has a potential harm for our community, for our communities. It can create bad habits or worse habits in our communities. That’s one of the dangers that I see.”

There is also pressure at the federal level on prediction markets. Senator John Curtis of Utah introduced a bill called the Prediction Markets Are Gambling Act. This would amend the CEA to prevent “event contracts involving sports and casino-style games.”

Curtis told Utah state media that the act would put power back with the states. “Our bipartisan legislation clarifies regulatory jurisdiction, ensuring that states can maintain their authority over sports betting and casino gaming. The Prediction Markets Are Gambling Act is about respecting states’ authority, protecting families and keeping speculative financial products out of spaces where they don’t belong.”

In the meantime, the CFTC is seeking public input on its rulemaking for prediction markets. The CFTC currently has just one sitting commissioner, Chair Michael Selig. He has previously stated the agency would defend prediction markets.

According to Brogan, if the CFTC further liberalizes prediction markets, and the issue of preemption goes to the Supreme Court, “all that counts, through all the sound and fury, is counting to five.”

Magazine: Banks want to run Vietnam’s crypto exchanges, Boyaa’s $70M BTC plan: Asia Express

Network Strength Signals Growth

Monero continues to show strong network performance alongside rising demand. Its hash rate has climbed steadily, reflecting increased miner participation and confidence in the network. Moreover, consistent transaction activity indicates sustained user engagement rather than short-term speculation across the ecosystem. Search data highlights growing interest in private crypto conversions. Queries related to Bitcoin to Monero exchanges have reached their highest levels since 2022. Consequently, this trend aligns with increased awareness of financial privacy risks tied to transparent blockchain systems.

Blockchain tracking capabilities have advanced rapidly across global markets. Firms like Chainalysis and Elliptic now provide real-time monitoring tools used by authorities in multiple jurisdictions. As a result, Bitcoin transactions linked to regulated exchanges often create traceable records tied to user identities. Governments have introduced stricter rules governing digital asset transfers. The European Union and the United States have expanded reporting obligations for crypto transactions. Furthermore, similar frameworks in Asia and Australia have increased compliance requirements, limiting anonymous activity on regulated platforms.

Security incidents involving centralized exchanges have heightened privacy concerns. Several breaches exposed sensitive user information, including identification documents and transaction histories. Consequently, affected users face increased risks related to fraud and targeted attacks. The ecosystem supporting Bitcoin to Monero swaps has matured significantly. Non-custodial platforms now offer fast conversions without requiring user accounts or identity verification. Additionally, decentralized protocols and atomic swap tools have improved accessibility for users seeking direct cross-chain exchanges. Market behavior shows a clear preference for financial privacy features. Users increasingly treat Monero as a reserve for private transactions rather than speculative investment. Moreover, the ability to move funds discreetly has become a key consideration in portfolio strategies.

Strength of Network Data Signals

Monero also records consistent network traffic throughout this season of demand. The day-to-day transactions exceed 40,000, which is near the network’s high. The hash rate is constantly increasing, indicating sustained miner support and long-term confidence in the network. Search activity shows growing attention to private crypto conversions. The number of queries for Bitcoin-to-Monero swaps has been the highest since 2022. This trend aligns with heightened sensitivity to traceable financial transactions in financial records.

Chainalysis and Elliptic are examples of blockchain analytics firms that continue to expand their monitoring capabilities. They are now used to aid regulators and tax authorities across regions. Consequently, transactions involving regulated exchanges often leave a trace. Authorities have proposed broader reporting requirements for digital asset transactions. Compliance rules have been extended to exchanges by the European Union and the United States. Moreover, the same regulations have been enforced in Asia and Australia, increasing pressure on users within regulated systems.

Breaches in centralized platforms’ security have contributed to users’ concerns. Several breaches exposed personal identification data and transaction histories. As a result, users are increasingly concerned about privacy to reduce risks from data exposure and targeted attacks. The service that facilitates Bitcoin-to-Monero conversion has also developed. Swaps such as GhostSwap do not require account creation or identity verification. Additionally, decentralized protocols like THORChain offer more liquidity for cross-chain transactions.

Market Behavior Adjusts

The behavior of users is now characterized by an increased emphasis on financial privacy. The use of Monero by many holders is as a means of conducting confidential transactions rather than a speculative instrument. Furthermore, fast and immediate conversion features have become a major necessity for active crypto users. Increasing surveillance, growing regulations, and recurring data breaches continue to influence user preferences. As a result, Bitcoin-to-Monero swaps have become a key component in facilitating private transactions in the digital asset market.

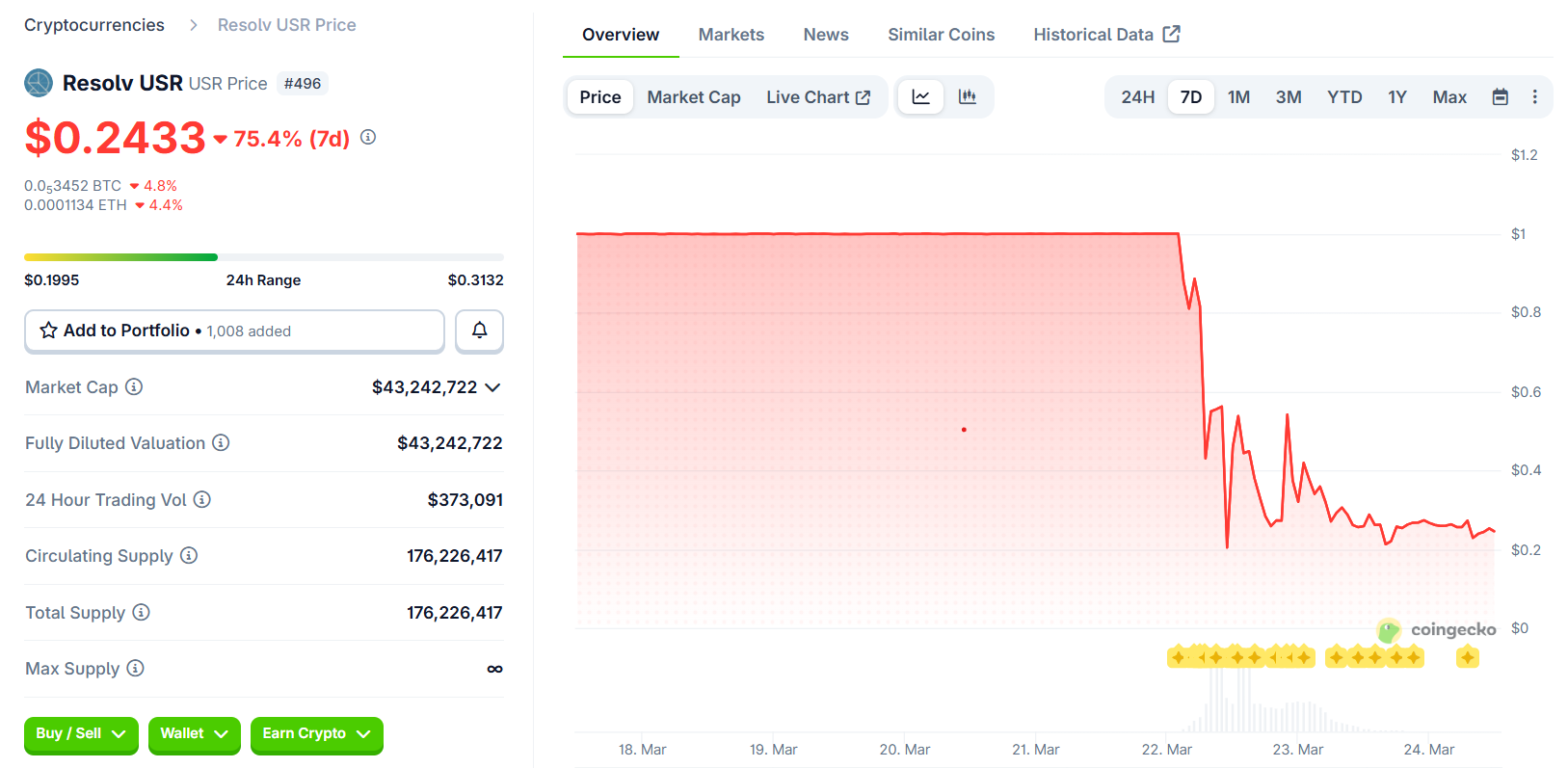

Resolv Labs has temporarily paused its protocol after an exploit on Sunday in which an attacker minted 80 million unbacked tokens, knocking the dollar stablecoin sharply off its peg and briefly plunging the token to $0.14.

The Resolv Foundation team announced on X on Monday evening that all protocol functions, including the app, were temporarily halted “to contain the impact of the exploit,” freezing Season 4 airdrop claims as well as staking and unstaking of RESOLV tokens.

Resolv previously said the collateral pool remained intact with no loss of underlying assets, despite onchain analysis showing that the attacker had successfully converted most of the minted USR into Ether (ETH) and sold around $25 million. USR is currently trading near $0.24, far below its intended dollar peg.

In an onchain ultimatum on Monday, Resolv offered the exploiter a white hat-style deal: return 90% of the converted funds (around $25 million in ETH) plus all remaining USR within 72 hours, keep 10% as a bounty, and cease further activity or face the consequences.

“Failure to comply within the stated timeframe will result in escalation,” the ultimatum states, such as asset freezes coordinated with exchanges and bridges, public tracing and law enforcement action. There have been no movements on the main wallet since.

Michael Pearl, vice president GTM and strategy at Web3 security company Cyvers, told Cointelegraph that redemptions had reopened only for legitimate pre-exploit holders, while Resolv and partners continued to trace “bad USR” and prepare a full post-mortem.

Related: Balancer Labs shuts down 4 months after $100M+ exploit, protocol to continue

Resolv exploit reignites stablecoin PTSD

Beyond Resolv, the incident has rekindled the industry’s unresolved trauma from the Terra ecosystem collapse of 2022, when the Terra USD (UST) algorithmic stablecoin’s death spiral erased tens of billions of dollars in value and reshaped regulatory and risk perceptions around stablecoins.

Pearl said the USR depeg had “opened a Pandora’s box,” noting that it had triggered roughly $180 million in liquidations on lending protocol Morpho and some $334 million in outflows from lending and liquidity platform Fluid, but “limited spillover overall,” as nervous stablecoin issuers revisit their own assumptions about peg reliability.

“We hear many stablecoin platforms that are petrified after this exploit,” he said, and with decentralized finance (DeFi) now deeply intertwined with stablecoins, Pearl warned that while protocols can sometimes absorb hacks and move on, a serious failure at the stablecoin layer “can finish the company,” a risk that USR’s collapse has just put back in sharp focus.

Magazine: South Korea gets rich from crypto… North Korea gets weapons

Professor Jiang’s Bitcoin conspiracy taps into war and empire angst

Taylor Frankie Paul Has ‘Meltdown’ After Arrest Question On ‘Bachelorette’

Millions of pounds fund populist right-wing ecosystem

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Money#alway#ultimate#lifestyle#travel#money#management#life#viral#trend#reservebankofindia#money

SET PRICE FOR XRP $? – RIPPLE EXPANSION CONTINUES – XRP REMAINS UNDERVALUED – CLARITY DELAYED STILL?

Their BIGGEST Financial Flex #financialflex #marlon #relatable #xyzbca #nba

-

Crypto World4 days ago

Crypto World4 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics4 days ago

Politics4 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Crypto World3 days ago

Crypto World3 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

News Videos6 days ago

News Videos6 days agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World3 days ago

Crypto World3 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Politics6 days ago

Politics6 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Tech5 days ago

Tech5 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

Crypto World6 days ago

Crypto World6 days agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

Sports1 day ago

Sports1 day agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

NewsBeat6 days ago

NewsBeat6 days agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

News Videos6 days ago

News Videos6 days agoPARLIAMENT OF MALAWI – PAC MEETING WITH REGISTRAR OF FINANCIAL ON AMARYLLIS HOTEL – INQUIRY LIVE

-

Politics5 days ago

Politics5 days agoGender equality discussions at UN face pushbacks and US resistance

-

Business2 days ago

Business2 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Business6 days ago

Business6 days agoWho Was Alex Pretti? 5 Key Facts About the ICU Nurse Killed by Federal Agents in Minneapolis

-

Sports1 day ago

Sports1 day agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Tech2 days ago

Tech2 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Sports4 days ago

Sports4 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

-

Sports5 days ago

Vikings Free Agency Enters Phase 2 with Key Questions

-

Tech7 days ago

Tech7 days agoSubnautica 2 might finally be entering early access in May

You must be logged in to post a comment Login