Crypto World

what a special arrangement means

Asked on a podcast whether XRP holders could receive equity in a Ripple public offering, Brad Garlinghouse nodded and floated a “special arrangement.” It was vague, unpromised, and electrifying to a community starved for catalysts. Here is what it could actually mean, and what it almost certainly cannot.

Summary

- Garlinghouse hinted at a possible “special arrangement” for XRP holders.

- He did not announce an IPO, a holder reward, or any concrete mechanism.

- Ripple equity and XRP remain legally separate assets.

- The most realistic benefit to XRP holders is still indirect utility, not equity.

In a June 2026 interview on the “Crypto In America” podcast, Ripple chief executive Brad Garlinghouse was asked a question the XRP community has wanted answered for years: if Ripple ever goes public, could XRP holders get a piece of it?

He did not say no. He nodded, and offered a single tantalizing phrase: that perhaps there would be a “special arrangement.”

That was the entire substance of it, four words wrapped in a maybe, with no detail, no commitment, and no timeline. And yet within hours it had rippled across XRP social media as though a promise had been made, because for a token that has spent 2026 grinding sideways near a dollar while Ripple collects institutional wins, even a hint of direct reward lands like a lightning strike.

This piece takes that hint apart: what a “special arrangement” could plausibly mean, why each version of it runs into a wall, and how a holder should read an offhand remark without getting played by it.

The honest framing matters from the start, because the gap between what was said and what was heard is the whole story. Garlinghouse described a possibility, not a plan, attached to an event, a Ripple public offering, that has not been announced and that he has repeatedly suggested is not close.

The community heard a catalyst. The reality is closer to a maybe attached to a maybe.

That does not make the question worthless, because the answer reveals a great deal about how Ripple equity and the XRP token actually relate, and about why the two keep diverging. This guide covers the moment itself, the legal wall between a company and its token, the genuine ways Ripple’s incentives align with holders, the menu of things a “special arrangement” could be, the obstacles each faces, and the framework for reading the hint with clear eyes.

The four words that lit up XRP social media

To understand why a vague phrase moved sentiment, you have to understand the state of mind it landed in.

XRP holders spent 2026 watching Ripple rack up exactly the kind of institutional milestones the community long predicted: settlements with JPMorgan, stablecoin launches with major partners, a steady drumbeat of bank deals, while the token itself stayed pinned near a dollar and change, beneath every major moving average.

That combination, corporate triumph paired with token stagnation, breeds a particular hunger: the sense that the wins are real but somehow are not reaching holders, and that some missing mechanism could finally connect the two.

Into that hunger dropped Garlinghouse’s nod and his “special arrangement,” and the phrase did what catalysts do in a starved market. It gave people something to hope for.

It helps to be precise about what was actually said, because precision is the first casualty of excitement. Garlinghouse did not announce a holder allocation. He did not describe a structure, a size, or a date.

He responded to a direct question about whether holders could gain equity by acknowledging the possibility in the softest available terms.

Days earlier, at an industry conference, he had been notably cooler on the idea of going public at all, observing that many listed crypto companies have struggled in public markets and that staying private gives Ripple more operational flexibility, while stopping short of ruling an offering out.

Put those two moments together and the picture is not a company preparing to reward token holders. It is a chief executive keeping every option open in public, declining to close a door without committing to walk through it.

The market chose to focus on the open door.

Why a public offering does not normally touch the token

The reason a holder allocation would be remarkable, rather than routine, is that an initial public offering has nothing to do with a token by default.

Ripple the company and XRP the token are legally separate things, and this is the single most important fact in the entire discussion. Ripple is a private company that sells software and payment services, signs deals with banks, holds a large treasury, and has shareholders.

XRP is a cryptocurrency that trades on its own supply and demand. Owning XRP makes you neither a shareholder nor a creditor of Ripple; it gives you no claim on the company’s profits, assets, or equity.

When a company goes public, it sells shares to investors, and the people rewarded are the holders of those shares, the existing equity owners, employees with stock, and early backers. Token holders are simply not part of that transaction, because they own a different asset entirely.

This is why a token is not company equity. A token can be associated with a company, used by a network, and held by that company, but it does not automatically become a claim on the company’s cap table.

This separation is not a technicality Ripple could wave away if it wanted to; it is the structure that governs everything. It is also exactly why XRP has spent the year failing to rally on Ripple’s corporate wins: the market, correctly, prices Ripple’s success as accruing first to Ripple, and only indirectly and slowly to the token.

A public offering would be the purest expression of that disconnect, a moment when Ripple converts its corporate value into tradeable equity for equity holders, with XRP holders watching from outside the deal.

So when Garlinghouse floats a “special arrangement,” he is gesturing at something that would deliberately break the normal pattern, a way to route some benefit of an equity event to holders of a non-equity asset.

That is a genuinely unusual thing to propose, which is part of why the phrase drew so much attention, and also why it deserves hard scrutiny instead of celebration.

The case that Ripple’s incentives already align with holders

Before dismissing the hint as empty, it is worth taking seriously the strongest version of the bullish argument, because it has real merit.

Garlinghouse and many in the community make the point that Ripple’s interests and XRP holders’ interests are already aligned, even without any special mechanism, because Ripple is the largest single holder of XRP in the world.

The company keeps an enormous quantity of the token, much of it in escrow, which means Ripple profits when XRP rises in exactly the way ordinary holders do. Whatever raises the price of XRP raises the value of Ripple’s own holdings.

This alignment is not imaginary, and it should not be dismissed as spin. Ripple’s actual day-to-day work, the partnerships, the payment integrations, the institutional adoption of its ledger and its stablecoin, plausibly increases XRP’s long-term utility and demand, which is a real if indirect benefit to anyone holding the token.

A holder is, in a loose sense, riding alongside the largest XRP whale on earth, one with deep pockets and a decade-long commitment to making the asset useful. That is a meaningful thing to have on your side.

But notice the precise shape of the benefit: it is indirect, gradual, and conditional on Ripple’s broader strategy actually translating into token demand, which, as 2026 has shown, is far from automatic.

That is why Ripple’s wins do not move XRP. The company can succeed, the ledger can gain credibility, and XRP can still wait for direct demand.

Alignment of incentives is not the same as a payment. “Ripple wants XRP to go up” is a very different proposition from “Ripple will hand XRP holders a slice of its IPO.”

The first is structural and real. The second is the speculative leap the “special arrangement” comment invites.

What a “special arrangement” could actually look like

So what could Garlinghouse plausibly mean?

Since he gave no detail, the honest approach is to map the realistic possibilities and weigh each, treating them as a menu of speculation rather than a forecast.

The most direct version would be some form of allocation to holders: a mechanism by which verified XRP holders receive shares, or the right to buy shares, in a Ripple offering, perhaps proportional to holdings. This is the version the community dreams of, because it would convert XRP ownership into a claim on Ripple equity, the very link that does not currently exist.

A softer variant would be priority access instead of free equity, letting XRP holders into an offering ahead of the general public, a perk without a giveaway.

Other versions stay within the token world instead of crossing into equity. Ripple could, in principle, pair any public listing with a token-side reward, an airdrop of XRP or of a new instrument to holders, timed to the event, which would sidestep the thorniest securities problems of distributing actual shares.

It could create a loyalty or staking-style program that rewards long-term holders around the listing. Or “special arrangement” could be far more modest than any of this, a governance gesture, a symbolic recognition, or simply Ripple structuring its business so that more value flows through XRP over time.

The range is enormous precisely because the phrase was empty, stretching from a genuine equity allocation at one end to a vague promise of goodwill at the other.

The community heard the first. Sober reading has to consider that the truth, if there is one at all, could sit anywhere along that spectrum, and that the most dramatic interpretations are also the least likely.

Why each version runs into a wall

The reason to temper expectations is that almost every concrete version of a “special arrangement” collides with serious obstacles, which is likely why Garlinghouse spoke in hints instead of specifics.

Distributing actual equity to XRP holders would be a securities and compliance nightmare. XRP holders number in the tens of millions, scattered across the globe in every regulatory jurisdiction imaginable, many anonymous, many in countries where Ripple cannot easily offer securities at all.

Identifying who qualifies, verifying them, and distributing shares in compliance with the securities laws of dozens of nations would be staggeringly complex. An offering is already one of the most heavily regulated events a company undertakes, and layering a novel token-holder allocation on top invites exactly the kind of legal risk that underwriters and regulators recoil from.

Token-side rewards avoid the equity problem but introduce others. An airdrop to holders raises its own securities questions in some jurisdictions and does nothing to address the fundamental issue that the token and the company remain separate.

Priority access to an offering is more feasible but far less exciting, and even that requires a workable, compliant way to identify genuine holders.

Fairness is another wall. Any arrangement that rewards holders as of a certain date invites accusations of favoring insiders or enabling gaming, and Ripple has spent years cultivating a reputation for regulatory caution it would be loath to jeopardize.

There is also a simple precedent vacuum. No major company has paired a public offering with a direct reward to holders of a separate, associated token, because the structure is awkward, legally fraught, and of uncertain benefit to the company doing it.

The absence of precedent is not proof it cannot happen. But it is a strong signal that “special arrangement” is far easier to say into a microphone than to build into a deal.

The catalyst-stack problem: not all catalysts are equal

The “special arrangement” comment is best understood as one entry in a larger habit, the tendency of the XRP community to treat every Ripple-related signal as part of a single, accumulating stack of catalysts that will eventually send the token higher.

In that mental model, a settlement with JPMorgan, an ETF inflow, a favorable regulatory development, and a hint about an IPO reward all get tossed into the same bucket labeled “reasons XRP will moon.”

The problem is that the items in that bucket are not equal, and treating them as interchangeable is how holders end up disappointed when the price does not respond the way the headline count suggests it should.

The useful distinction is between observable catalysts and speculative ones. CLARITY Act passage, ETF inflows, exchange-reserve changes, and real settlement volume are observable: they either happen or they do not, and when they happen they can be measured and priced.

A possible reward attached to a possible public offering is a different category entirely. It is a speculative possibility layered on a corporate decision that has not been made, with no structure, no size, and no date.

That is why where real XRP demand comes from matters more than IPO speculation. ETF inflows, exchange reserves, and actual XRP usage are measurable; a possible arrangement is not.

Stacking that on top of observable catalysts as though it carries equal weight inflates the apparent bull case without adding anything solid to it.

The discipline that protects a holder is to sort the stack honestly: give real weight to things that are happening and can be tracked, and treat a hint about an unannounced arrangement tied to an unannounced offering as what it is, a low-probability, high-uncertainty maybe that belongs at the very bottom of the pile, not the top.

Why Ripple may stay private anyway

There is a further reason to keep the hint in perspective, and it sits one level up: the public offering the “special arrangement” is attached to may not happen any time soon.

Garlinghouse has been openly ambivalent about going public, noting that staying private gives Ripple operational flexibility and pointing out that many crypto companies have not fared well in public markets.

He has said plainly that an offering is not something happening very soon, even while declining to rule it out. Ripple is also not a company under pressure to list: it is well capitalized, profitable in its core business, and sitting on a large XRP treasury, which removes the usual urgency that pushes firms toward public markets to raise cash.

This is the part the excitement tends to skip. A reward to holders is conditional on an offering, and the offering itself is uncertain, which makes the reward doubly contingent.

If Ripple chooses to stay private for years, as its chief executive’s comments suggest is entirely possible, then the “special arrangement” remains permanently hypothetical, a thing that could only exist alongside an event that may never come in the form imagined.

Even in the bullish scenario where Ripple does eventually list, the company would face every obstacle described above when deciding whether to build a holder mechanism. The path of least resistance for any firm going public is the conventional one that rewards equity holders and leaves token holders out.

None of this means Ripple will never reward holders. It means the hint sits behind two locked doors, an uncertain offering and an uncertain mechanism, and a holder banking on both opening is betting on a long chain of maybes.

The deeper reason the equity-token wall exists

It is worth pausing on why the separation between Ripple equity and XRP is so firm, because the community often treats it as an inconvenience Ripple could simply choose to overcome, when in fact it is a protective firewall that serves XRP holders even as it frustrates them.

The wall is not an accident of paperwork. It is the product of years of legal struggle, and dismantling it casually could undo the very thing that makes XRP investable today.

Recall that XRP spent years under a cloud because regulators argued it was an unregistered security, a claim that turned on whether buying the token amounted to investing in Ripple’s efforts and expecting profit from them.

The token’s hard-won legal clarity rests precisely on the finding that XRP, as traded on public exchanges, is not a stake in Ripple. The distance between the company and the token is what lets XRP be treated as a commodity instead of a security.

Now consider what a direct equity link would do to that settlement. If Ripple created a mechanism that tied XRP ownership to a claim on the company’s equity or profits, it would be handing regulators a fresh argument that the token is, after all, a security, an investment in Ripple’s success with an expectation of profit from the company’s efforts.

The arrangement the community dreams of could, in the worst case, drag XRP back toward the exact classification it just escaped, with all the trading restrictions and institutional hesitancy that status carries.

This is the paradox buried in the “special arrangement” hope: the cleanest way to reward holders, by linking the token to the company, is also the way most likely to damage the token’s legal standing.

That is why the catalyst that could codify XRP’s status matters more than a speculative equity link. Legal certainty is valuable precisely because it keeps XRP out of the securities bucket.

It helps explain why Ripple, a company famous for its regulatory caution, would speak only in vague hints rather than concrete plans. A real equity link is not just operationally hard; it is legally hazardous to the asset it would be meant to reward.

This is why the indirect alignment described earlier is not a consolation prize but, in a sense, the safer form of benefit. Ripple driving XRP’s utility and value through its business activity raises the token without making it a security, because the gains come from the token’s own usefulness and demand, not from a contractual claim on the company.

A holder who understands this should be careful what they wish for. The firewall that keeps Ripple’s wins from flowing directly into the token is the same firewall that keeps XRP a commodity, and a “special arrangement” clever enough to breach one might breach the other.

The most valuable thing Ripple can do for holders may be exactly what it is already doing, building utility around the token. The least valuable, or even harmful, may be the dramatic equity link the hint seemed to dangle.

How to read the hint without getting played

The way to handle a moment like this is to separate sentiment from substance, because the two move on very different timescales.

As sentiment, the “special arrangement” comment is genuinely meaningful: it shows Ripple’s chief executive is aware of holder frustration, willing to gesture toward addressing it, and keen to keep the community engaged, all of which matter for a token whose price is heavily driven by community conviction.

A hint like this can move sentiment and short-term price action regardless of whether anything concrete ever follows, and a trader watching narrative flows should not ignore it.

But sentiment is not the same as a plan, and confusing the two is the trap.

As substance, the honest reading is that almost nothing has changed. There is still no public offering announced, no holder mechanism designed, no legal pathway cleared, and no commitment made, only a chief executive declining to close a door while standing well back from it.

For the hint to become real, a holder would need to see two concrete things follow: an actual decision by Ripple to go public, with a filing and a timeline, and then an actual, structured mechanism for involving holders that survives the securities, fairness, and practicality obstacles laid out here.

Until both exist, “special arrangement” is a phrase, not a payout.

The disciplined position is to enjoy the signal for what it reveals about Ripple’s posture toward its community, to give it appropriate, which is to say minimal, weight in any view of XRP’s actual prospects, and to keep one’s attention on the observable catalysts that truly move the token.

The community heard a promise. What Garlinghouse offered was a maybe, and the difference is everything.

Frequently asked questions

What did Garlinghouse actually say about XRP holders and a Ripple IPO?

On a June 2026 podcast, asked whether XRP holders could gain equity if Ripple went public, Brad Garlinghouse nodded and said perhaps there would be a “special arrangement.” That was the full substance: a vague acknowledgment of a possibility, with no structure, size, or timeline attached. Days earlier, at an industry conference, he had been cooler on going public at all, saying staying private gives Ripple flexibility. So the remark was a hint, not a plan or a promise.

Would a Ripple IPO normally benefit XRP holders?

No, not by default. Ripple the company and XRP the token are legally separate. A public offering sells shares and rewards equity holders, employees, and early investors, while XRP holders own a different asset with no claim on Ripple’s equity or profits. This is exactly why XRP has not rallied on Ripple’s institutional wins through 2026: the market prices those wins as accruing to the company first, and only indirectly to the token. A holder reward would be a deliberate break from the normal structure.

What could a “special arrangement” actually be?

Since Garlinghouse gave no detail, the possibilities range widely. The most dramatic would be allocating shares, or the right to buy shares, to verified XRP holders. Softer versions include priority access to an offering, a token-side airdrop timed to a listing, or a loyalty program for long-term holders. The most modest reading is a symbolic gesture or simply structuring Ripple’s business so more value flows through XRP over time. The community assumes the dramatic version, but the truth, if any, could sit anywhere on that spectrum.

Why might a holder reward be hard to deliver?

Distributing actual equity to tens of millions of anonymous, globally scattered XRP holders would be a securities and compliance nightmare across dozens of jurisdictions, layered on top of an already heavily regulated offering. Token-side airdrops raise their own legal questions and do not bridge the company-token gap. Any holder-as-of-a-date reward invites fairness and gaming concerns. There is also little precedent for pairing a public offering with a reward to holders of a separate token, which signals how awkward the structure is in practice.

Is Ripple even going public soon?

Probably not soon, by Garlinghouse’s own account. He has said an offering is not something happening very soon and has emphasized that remaining private gives Ripple operational flexibility, noting that many public crypto companies have underperformed. Ripple is well capitalized and profitable in its core business and holds a large XRP treasury, so it faces little pressure to raise cash through a listing. Because any holder reward is conditional on an offering, an uncertain offering makes the reward doubly contingent.

How should XRP holders treat this hint?

Separate sentiment from substance. As sentiment, the comment matters: it shows Ripple is aware of holder frustration and wants to keep the community engaged, which can move short-term sentiment. As substance, almost nothing has changed, since there is no announced offering, no designed mechanism, and no commitment. For the hint to become real, a holder would need an actual decision to go public and an actual, compliant holder mechanism to follow. Until both exist, it is a phrase, not a payout, and deserves minimal weight.

This article is information, not investment advice. It concerns speculative, unannounced possibilities, and corporate plans, statements, and market conditions can change. Prices and details reflect reporting available as of June 25, 2026. Verify current information with official sources before relying on anything described here.

Bitcoin (BTC) dropped below $60,000, a key psychological support, on Thursday as losses in megacap technology stocks weighed on investors’ broader risk appetite, adding pressure to an already fragile crypto market.

BTC/USD vs. Nasdaq and S&P 500 daily performance chart. Source: TradingView

The decline has triggered a classic bearish reversal setup that may push the BTC price under the $54,000 mark in the coming days.

Key takeaways:

- Bitcoin’s break below $60,000 has erased its June gains and activated multiple bearish setups.

- Bitcoin’s rounded top and daily bear flag breakdowns are both projecting a downside target below $54,000.

BTC’s rounded top breakdown signals more pain ahead

The BTC/USD pair fell as much as 4.8% on Thursday, hitting an intraday low near $58,000 and erasing its entire June advance. The pullback also completed what appears to be a rounded top pattern on the four-hour chart.

BTC/USD four-hour chart tracking the rounded top bearish setup. Source: TradingView

In technical analysis, a rounded top forms when buying momentum gradually exhausts, shifting the asset from an uptrend to a downtrend in an inverse-U-shaped structure. The pattern officially resolves when the price breaks below the “neckline” or the structure’s base support.

By measuring the distance from the top of the dome to the neckline and projecting that same distance downward from the breakdown point, analysts calculate a clear target.

For Bitcoin, this measured downside target sits just under the $54,000 level, representing an approximate 8.9% drop from current prices.

On the daily chart, Bitcoin has simultaneously triggered a bear flag breakdown.

BTC/USD daily chart tracking the bear flag breakdown setup. Source: TradingView

This secondary pattern independently projects an identical move toward the $54,000 zone, adding substantial weight to the bearish case.

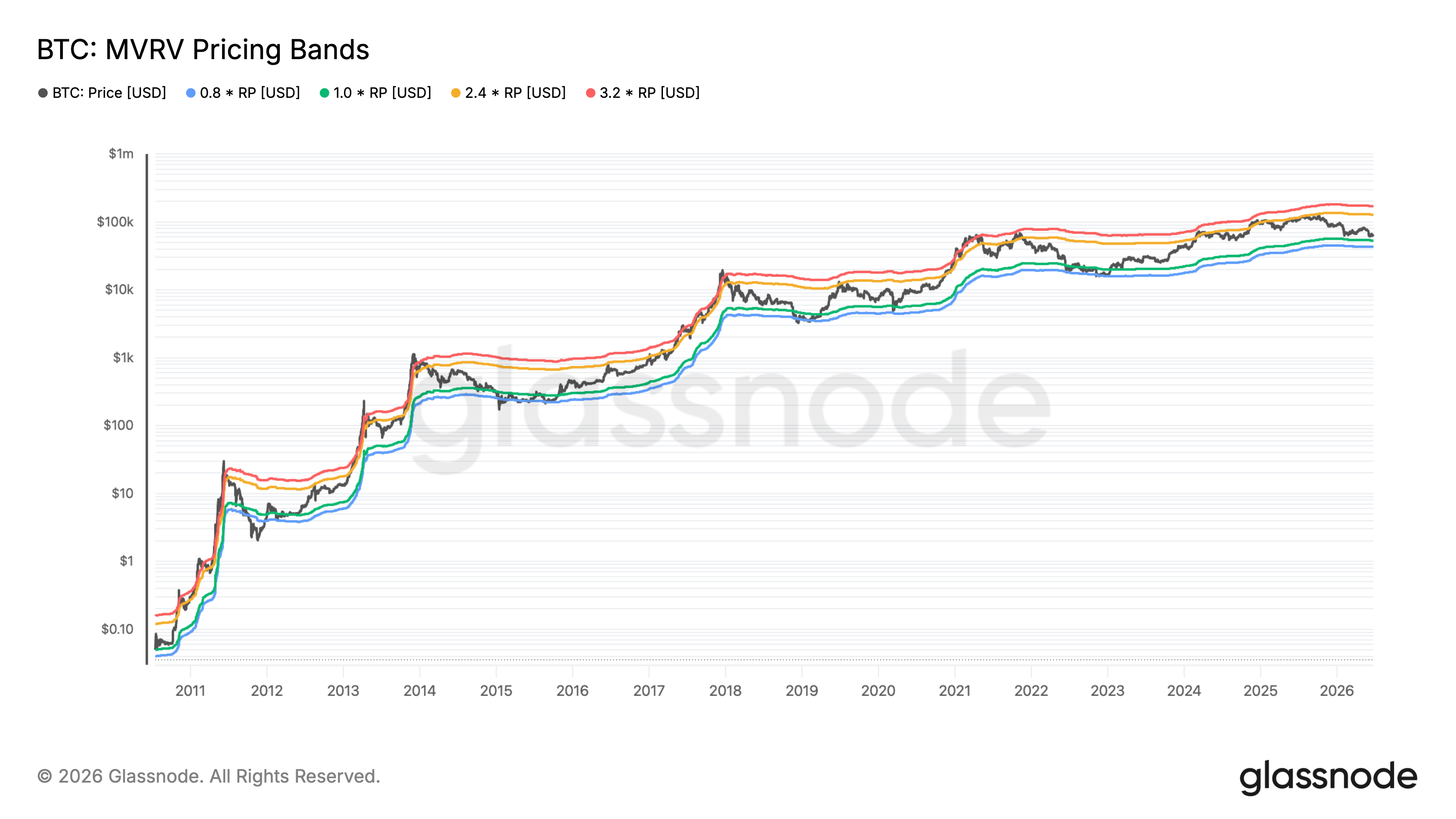

Bitcoin MVRV bands increase $54,000 target odds

Bitcoin’s on-chain price bands also point to the same downside area highlighted by the rounded-top and bear-flag setups.

Glassnode’s MVRV pricing bands compare Bitcoin’s market price with its realized price, or the average price at which coins last moved on-chain. In simple terms, they show whether the market is trading at unusually high profit or loss levels.

BTC MVRV pricing bands vs. price. Source: Glassnode

As of Wednesday, Bitcoin was trading near $60,997, while the 1.0 MVRV band, shown in green, sat around $53,390. That level closely matches the technical downside target near $54,000, making it an important support zone if BTC extends its decline.

Related: Bitcoin nearly loses $59K as DXY surges: Are traders bracing for more pain?

A deeper selloff, however, could push Bitcoin toward the 0.8 MVRV band, shown in blue, near $42,700. Historically, Bitcoin’s major bear-market bottoms have formed around this lower blue band, where unrealized losses become extreme, and capitulation risk rises.

Amid recent bouts of stock volatility and a new Fed chair coming into a complex inflation environment, the action in bond ETFs is sending an important signal to the market.

“Flows tell the story,” Steve Laipply, global co-head of iShares fixed-income ETFs at BlackRock, told CNBC’s Dominic Chu this week. And that is a story of rising investor interest in yield across the fixed-income market. “In the U.S., bond ETF flows are up a shocking 60% relative to last year,” Laipply said.

Laipply said a significant share of the flows are going into U.S. treasuries, but there also has been a significant move by investors into multi-sector income ETFs.

“The income story is very robust and enduring, because rates will continue to move around and ‘real yields’ are definitely an opportunity,” he said, a reference to bond yields net the rate of inflation. “Real yields reflect a growth story,” he said, led by the AI boom and the anticipated increase in productivity that is tied to it.

Investor interest in multi-sector income funds, according to Laipply, is also an indication of greater emphasis on “income per unit of duration.”

“The idea of getting a little more duration, but really still focusing on income … that’s sort of the sweet spot,” he said.

“As a bond investor, real yield is your very good friend,” George Bory, chief investment strategist of fixed income at Allspring Global Investments, told Chu.

How the Fed fits into the fixed-income investment picture

New Federal Reserve chairman Kevin Warsh has put the market on watch for signs of greater volatility in bonds as he shapes a new approach at the Fed. “The most significant one, at least right now, is about the lack of forward guidance,” Bory said. When the Fed telegraphed its every move, managing duration risk was a less active process for investors. Now there will be more of an “uncertainty premium” built into the market, he said.

At his first FOMC meeting last week, Warsh was clear about maintaining the Fed’s inflation-fighting credentials for the time being, Bory said.

“The very front end of the curve is now very steep, as the market is now pricing in multiple rate hikes from the Fed. You don’t have to move very far out the curve to start to see a very material increase in yields,” Bory said.

Laipply said recent declines in what is known as the breakeven inflation rate, which have been falling “very, very sharply” at both the short and long end of the treasuries curve, say to him that “the market is sniffing out something here.”

The breakeven inflation rate is a measure of the difference between standard treasury yields and treasury- inflation protected securities.

Laipply said with “breakevens’ where they are, it is not necessarily a bad time for investors still worried about inflation to consider short-dated TIPS. But many bond investors, he said, are “looking past this volatility, and no matter what yields are, they are at a level where income is very attractive relative to what it has been,” he said.

U.S. 10-year treasury bond yield performance in 2026.

One of the biggest recent debates in the market among investors is the declining risk premium for holding stocks over bonds.

Bory described it as a “pretty attractive” environment for bond investors, but said there are caveats. “We need to be a little careful because credit spreads are very tight,” he said, and he added that he thinks those spreads are likely to “stick with us.”

Tighter credit spreads between various bonds along the traditional risk spectrum are typically a sign of higher investor confidence, but some worry potentially a sign of market complacency.

“Modest inflation is a meaningful tailwind to credit worthiness and I think we are in bit of a super-cycle for credit more broadly,” Bory said. He added that as a fixed-income investor he would be “happy to take the extra income, but won’t be too aggressive in going after it.”

The latest core inflation data from the government was at the highest level since October 2023, but it was in line with market expectations and reinforced the need for the inflation-fighting stance to remain at the Fed.

Oil prices are back at their pre-war level as tankers flow through the Strait of Hormuz again, though gas prices are likely to remain elevated, according to Chevron.

The labor market complicates the story for investors and the Fed as it attempts to balance its dual mandate of maximum employment and price stability. Laipply said about 90% of recent job creation has been in healthcare, government services, and leisure. “Most of the labor market is soft,” he said.

“The real trick is … how much weight do you put on that near-term inflation concern versus a softening labor market, or if you want to put it another way, a labor market that’s very, very concentrated,” Laipply added.

Sign up for our weekly newsletter that goes beyond the livestream, offering a closer look at the trends and figures shaping the ETF market.

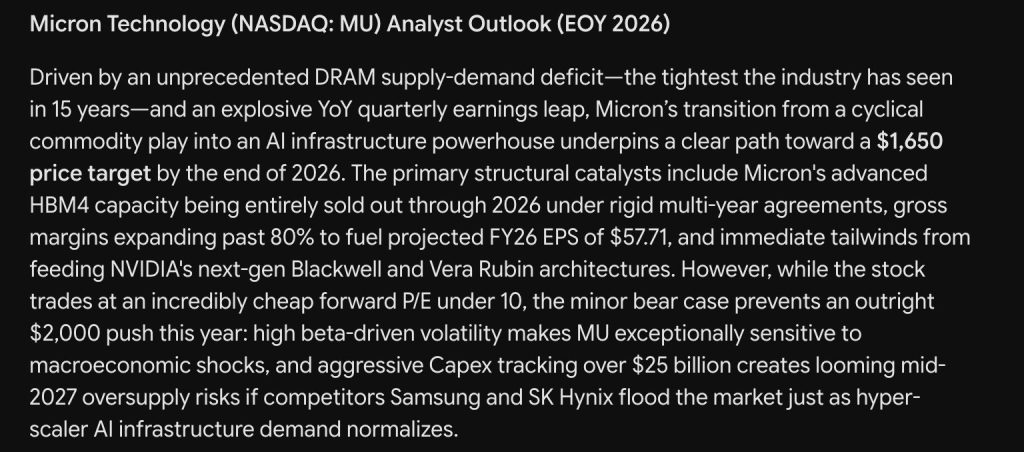

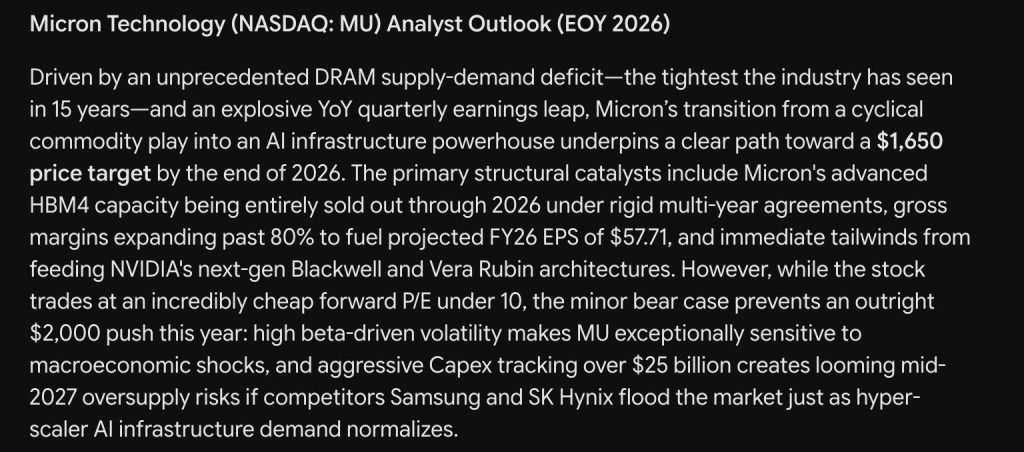

Google Gemini AI just predicts a number to Micron price prediction that treats the stock’s wild run this year as the beginning rather than the peak. The model sees $1,650 by the end of 2026, a fresh high for a name that started the year trading nowhere close to these levels.

The bull case centers on a supply crunch unlike anything the memory industry has seen in over a decade. Micron is riding an unprecedented DRAM supply demand deficit, described as the tightest the industry has experienced in 15 years.

That scarcity is showing up directly in the numbers, with an explosive year over year quarterly earnings leap fueling the entire move.

The bigger story, though, is a transformation in how the market views this company. Micron is shifting from a cyclical commodity play to something closer to an AI infrastructure powerhouse, and that shift in identity underpins the path toward $1,650.

The most important structural catalyst is that Micron’s advanced HBM4 capacity is entirely sold out through 2026 under rigid multi-year agreements, which lock in demand regardless of short-term market swings. Gross margins are expanding past 80%, fueling a projected fiscal 2026 earnings per share of $57.71.

On top of that, Micron is getting immediate tailwinds from feeding Nvidia’s next-generation Blackwell and Vera Rubin architectures, putting it directly in the supply chain of the biggest names in AI computing. Even with the stock’s massive run already behind it, it still trades at a forward price to earnings ratio under 10, which the model frames as remarkably cheap given the growth on display.

The bear case is fairly narrow but worth noting. High beta-driven volatility makes this stock exceptionally sensitive to any broader macroeconomic shock, meaning a market-wide pullback could hit shares harder than most.

Aggressive capital expenditures tracking over 25 billion dollars also create a real risk of oversupply by mid 2027 if competitors like Samsung and SK Hynix flood the market right as hyperscaler AI infrastructure demand eventually normalizes.

That combination of risks is exactly why the model stops short of calling for an outright push toward $2,000 this year.

Micron Rides A Supply Crunch Straight Into Uncharted Territory

The daily chart shows Micron at $1,048.51 after one of the most dramatic runs in this entire series, climbing from around $200 late last year to briefly touching highs above $1,230 just this week.

That kind of vertical move, especially the acceleration visible from May onward, is the definition of a parabolic breakout rather than a typical grinding uptrend.

Price recently pulled back from that intraday high near $1,232 down to the current level around $1,048, which looks like healthy profit taking after an earnings driven spike rather than a trend reversal.

The chart shows clear support building near $1,000, a round number level that price has tested and held multiple times over the past few sessions. Resistance now sits at that recent high near $1,232, with the broader trendline from the entire 2026 run continuing to point sharply upward.

Given the size and speed of this move, momentum on the daily candles still looks strongly bullish overall, even with this short term cooling off period factored in.

The pullback from the highs reflects normal digestion after a binding multi year HBM4 contract story and a blowout earnings beat, not a change in the underlying trend.

If Micron can hold the $1,000 level and push back toward its recent highs, the climb toward that $1,650 target starts looking like a continuation of the same story that has driven this stock all year rather than a stretch into new territory.

Bitcoin Hyper: Building the Layer Bitcoin Was Always Missing, Here is Why Gemini AI Predicts Its The Next Big Thing

The largest returns in crypto rarely go to the people who wait for confirmation. They go to early supporters who back the infrastructure before the rest of the market catches on.

Bitcoin Hyper is positioned for exactly that. The project brings Solana-grade smart contracts and execution speed directly to Bitcoin, without touching the security model that makes Bitcoin the most trusted network in crypto.

Lower fees, higher throughput, full programmability, all running on top of Bitcoin rather than competing with it.

Inside the ecosystem, users can stake for rewards, swap assets, and interact with smart contracts while their funds stay secured within the Bitcoin network itself.

The presale has already raised $32.8 million, pulling attention from major investors and prominent crypto platforms. That momentum has made $HYPER one of the most talked-about presales this year.

The price is still fixed at early-stage levels. To participate, head to the official Bitcoin Hyper website and connect a supported wallet such as Best Wallet. Credit and debit card purchases are also accepted directly on the site.

The post Google Gemini AI Predicts Jaw-Dropping Micron Technology Stock Price by End of 2026 appeared first on Cryptonews.

Key Takeaways

- GF Securities’ Jeff Pu downgraded Dell from Buy to Hold following a nearly 200% stock surge, saying upside potential is now constrained

- Despite keeping a $445 price target, Pu warned that valuations exceeding 20x FY28 consensus earnings leave little room for error

- Dell director Lynn Radakovich offloaded $5.06 million worth of shares on June 22, exercising options priced at $31.14 and selling at $421.00

- The analyst expressed concern that Super Micro may capture Dell’s market position in SpaceX’s upcoming deployment phase beginning in 2027

- Shares of Dell were hovering around $434 Thursday, marking approximately a 5% decline following the rating cut

Dell Technologies (DELL) saw its shares slip to around $434 on Thursday, falling more than 5% after GF Securities analyst Jeff Pu downgraded the stock from Buy to Hold.

The rating change comes on the heels of an impressive nearly 200% rally in Dell shares following the company’s fiscal fourth-quarter earnings release in February.

While Pu maintained his $445 price objective, he indicated that the current risk-reward profile has become less favorable given recent price appreciation.

“Despite near-term momentum from GB300/HGX orders, we believe upside potential is constrained given already lofty market expectations,” Pu stated. He pointed out that projections for AI revenue reaching $70 billion or higher, along with corresponding boosts to overall revenue and earnings per share, are already factored into current valuations.

Trading at over 20x consensus fiscal 2028 earnings estimates—or applying a sum-of-the-parts methodology of 25x for AI operations and 15x for legacy business—the analyst concluded the valuation no longer justifies a bullish stance.

Competitive Threats Cloud Long-Term Prospects

Pu also flagged a significant long-term headwind that contributed to Thursday’s negative market reaction. He anticipates Super Micro (SMCI) will capture a larger share of SpaceX’s next-generation gigawatt-scale infrastructure rollout scheduled to commence in 2027.

Dell presently maintains a substantial supply relationship with SpaceX and serves as the exclusive server provider to CoreWeave (CRWV). However, Pu observed that both organizations are exploring an ODM-direct procurement strategy, which could gradually erode Dell’s dominant market position.

This competitive risk appears to have caught investors off guard, amplifying Thursday’s decline.

The downgrade coincided with a regulatory disclosure revealing that Dell director Lynn Radakovich disposed of $5.06 million in company shares on June 22. The transaction involved exercising stock options at $31.14 per share and immediately selling 12,022 shares at $421.00 each.

These trades were executed through a pre-established Rule 10b5-1 trading plan set up in March 2026. After the sale, Radakovich continues to own 25,267 shares directly while maintaining options on an additional 51,979 shares.

Impressive Gains Create High Bar for Future Performance

Dell has delivered exceptional returns this year. Shares have surged more than 247% year-to-date, pushing the company’s market capitalization to approximately $277 billion.

The technology giant recently unveiled its PowerEdge XE8812 server featuring Nvidia’s Vera Rubin NVL4 architecture, capable of supporting up to 144 GPUs per rack. Additionally, Dell secured a substantial $1.4 billion contract with the U.S. Air Force to provide Microsoft enterprise software licenses.

The company also closed a $3 billion senior notes offering, distributed across three separate tranches maturing in 2031, 2034, and 2037.

Despite these achievements, certain analysts have raised red flags regarding Dell’s substantial debt burden and negative equity position, which could become problematic should credit market conditions deteriorate.

Dell’s stock was trading down approximately 5.36% Thursday afternoon, changing hands near the $434 level.

Strategy faces new legal pressure after Rosen Law Firm opened a securities investigation into the Bitcoin treasury company this week. The review follows a steep MSTR selloff and a deeper Bitcoin decline across the wider crypto market and related shares. Together, the events place Michael Saylor’s firm under legal, market, and balance sheet pressure during a volatile trading week.

Strategy Faces Securities Investigation

Rosen Law Firm said it began an investigation into potential securities claims against Strategy and related securities. The firm linked the review to allegations of misleading business information shared with market participants during recent disclosures. It said affected shareholders may seek compensation through a contingency fee arrangement if claims move forward in court.

The firm also said it is preparing a class action to recover possible market losses through the planned lawsuit. Therefore, the legal process could add another challenge for Strategy and its securities program during a weak market. The company already faces pressure because its business model depends heavily on Bitcoin prices, capital markets, and equity sentiment.

The investigation comes after Peter Schiff criticized Saylor’s Bitcoin-backed securities push in recent public comments as Bitcoin prices weakened. Schiff argued that STRC buyers could bring claims tied to promotional statements and offering materials for the security. However, that argument remains separate from Rosen Law Firm’s planned legal action and any future court filing.

Mstr Stock Slides To New Lows

MSTR fell to a new low near $86 after breaking below $100 earlier this week. TradingView data showed the stock dropped more than 5% on the day during regular trading as pressure accelerated. The stock also lost about 23% across the past week as sellers controlled momentum.

The decline reflects heavy selling pressure across crypto-linked equities and Bitcoin treasury names during the current session. Moreover, MSTR often trades as a leveraged proxy for Bitcoin exposure in public markets during volatile trading. That link strengthens during rallies, but it also magnifies losses during sharp selloffs as market risk rises.

Market commentator Zerohedge pointed to heavy put buying across the latest trading session as prices fell today. That options activity added pressure as traders positioned for more downside in the stock during the session. Meanwhile, Bitcoin also weakened after PCE inflation reached 4.1%, the highest level since 2023.

Bitcoin Drop Tests Strategy Treasury Model

Bitcoin’s drop below $60,000 deepened concern over Strategy’s treasury-heavy structure and balance sheet risk. The company holds a large Bitcoin reserve on its balance sheet, so BTC price moves affect sentiment. As a result, every major Bitcoin selloff can weigh on MSTR shares and financing conditions.

Strategy reportedly carries an unrealized Bitcoin loss of more than $13.6 billion after the latest crash. That figure reflects current market prices rather than completed asset sales by the company. Still, it raises questions about leverage, liquidity, and future capital decisions if market stress continues.

Schiff has suggested that Strategy may sell Bitcoin to fund stock buybacks if pressure increases. However, Strategy has not announced any plan to sell its Bitcoin reserves despite the market pressure. Saylor has instead said current reserves exceed debt by over $40 billion, unlike the 2022 downturn.

The self-proclaimed Dogecoin killer followed the red wave sweeping through the broader crypto market, with its price collapsing to its lowest level since May 2021.

In a sudden twist of events, though, it reclaimed its position as the second-biggest meme coin.

Trailing Behind DOGE Again

SHIB has slipped by another 15% over the past week and currently trades at around $0.000004104 (per CoinGecko). Perhaps the most evident reasons for the pullback are the bearish conditions across the entire market and waning interest in the meme coin niche.

Other potential factors include the recent whale activity. The X account BSCN revealed that a Shiba Inu investor who purchased 17.4% of the token’s supply in August 2020 for less than $14,000 has moved 600 billion SHIB (worth $2.83 million) to a ForwarderV4 address.

While some interpreted the move as a pre-sale step, BSCN clarified that nothing has been confirmed yet and promised to unveil further details in time. The X account also noted that the whale’s position was worth a whopping $9.1 billion when SHIB’s price reached an all-time high in 2021.

Speaking on the meme coin was also James Wynn. The trader, known for his highly risky crypto bets, described the asset as “old, dead, and boring,” predicting a potential revival in 5-10 years when “a bit of nostalgia” can bring it back.

Despite its price slump, SHIB has once again secured its position as the second-largest meme coin. This happened after MemeCore (M) nosedived by 76% in a single day amid allegations of manipulation. Dogecoin (DOGE) remains the undisputed leader of the niche with a market capitalization of almost $11.5 billion, while SHIB has less than $2.5 billion.

More Pain Ahead?

The crypto market’s conditions remain unstable (to say the least), which could result in further declines for SHIB in the near term. The rising amount of tokens stored on crypto exchanges is another bearish factor.

Earlier in June, the figure dropped to a five-year low, but since then it has headed north sharply, suggesting that investors have been abandoning self-custody solutions and moving to centralized platforms, thereby increasing the likelihood of an additional sell-off.

The post Shiba Inu (SHIB) Crashes to a 5-Year Low, Yet Makes an Unexpected Comeback: Details appeared first on CryptoPotato.

TLDR

- BlackRock transferred 3,410 BTC and 5,132 ETH to Coinbase Prime.

- The combined value of the transfers reached approximately $217 million.

- Bitcoin transfers accounted for about $209.64 million of the total value.

- Ethereum transfers were valued at approximately $8.43 million.

- Lookonchain tracked the transactions across multiple blockchain transfers.

BlackRock transferred another $217 million worth of Bitcoin and Ethereum to Coinbase Prime on June 25. The transactions followed continued ETF outflows across both products and renewed attention on the asset manager’s blockchain activity. Lookonchain tracked the transfers, while BlackRock did not disclose the purpose behind the deposits.

BlackRock Moves Bitcoin and Ethereum to Coinbase Prime

Lookonchain reported that BlackRock deposited 3,410 BTC and 5,132 ETH to Coinbase Prime through several transactions. The transfers carried an estimated value of $209.64 million in Bitcoin and $8.43 million in Ethereum. The movement occurred on Thursday, June 25.

Blockchain data showed about seven transfers during the operation. Nearly every Bitcoin transaction moved 300 BTC to Coinbase Prime. One separate transaction carried the Ethereum holdings to the same platform.

Market participants linked the transfers with recent ETF withdrawals because similar activity appeared during previous outflow sessions. However, BlackRock did not issue a statement explaining the latest deposits. The company also provided no public update regarding the destination of the transferred assets.

Exchange deposits often attract attention because they can precede trading activity. However, blockchain transfers alone do not confirm that an asset manager has sold any holdings. The available on-chain data only confirms the movement between wallets.

Bitcoin and Ethereum Transfers Follow ETF Withdrawals

The latest deposits arrived while both Bitcoin and Ethereum exchange-traded funds continued recording withdrawals. BlackRock has transferred digital assets to Coinbase Prime during earlier outflow periods. Those previous transactions also prompted market discussion about possible sales.

Some traders interpreted the latest deposits as preparation for another disposal of holdings. Others pointed out that Coinbase Prime supports institutional custody and settlement services. Therefore, wallet transfers alone cannot establish whether any sale occurred.

BlackRock has not confirmed any direct sale connected to the June 25 transfers. The company also has not addressed market speculation surrounding the transactions. As a result, only the blockchain records remain publicly available.

Lookonchain’s published wallet activity showed that the combined transfers reached about $217 million. Bitcoin represented most of the transferred value, while Ethereum accounted for a smaller portion. The deposits reached Coinbase Prime through multiple wallet movements.

Previous blockchain records showed similar transfer patterns during sessions with ETF redemptions. Those observations have contributed to continued discussion whenever BlackRock moves assets to Coinbase Prime. Still, no public filing connected the latest transfers to completed market sales.

The recorded transfers included 3,410 BTC and 5,132 ETH. Based on prices during execution, the combined value reached approximately $217 million. BlackRock has not released any further information regarding the June 25 wallet activity.

Jiang Zhuoer, one of China’s best-known Bitcoin (BTC) miners, sees the Bitcoin bottom landing between $42,000 and $44,000 in late 2026, closely matching Arthur Hayes’ recent $40,000 call.

The founder of mining pool BTC.TOP laid out the forecast in a post, building it on a bearish signal from Strategy’s stock, MSTR. His timing and target both land near the BitMEX co-founder’s.

Strategy’s mNAV Discount Echoes the 2022 Low

Jiang’s case rests on Strategy’s mNAV, which he pegs at 0.72. The metric weighs the stock against the Bitcoin the company holds per share. A reading under 1.0 leaves the firm valued below its own Bitcoin.

The level sits near the 0.7 trough from May 2022, the last time its mNAV collapsed this far. Jiang treats that as the signal, not the timer.

In that cycle, the mNAV bottomed in May with Bitcoin near $31,000. The price then kept sliding to about $15,650 by late November, as the FTX collapse deepened the rout. That gap ran about six months.

“But note that the mNAV low is not the BTC price low,” he added.

Follow us on X to get the latest news as it happens

His broader timing comes from a four-year cycle model, one he likens to a bouncing ball losing height. It points to a bottom around October 31, 2026.

Jiang, who has mined through several halving cycles, is already short and plans to buy back near the low.

Hayes Points to a Similar Bitcoin Bottom

Arthur Hayes reached a similar destination by a different route. The BitMEX co-founder laid out the call to content creator EllioTrades on June 12. He sees the Bitcoin bottom near $40,000 within six months.

The bet is tactical, not structural. Hayes holds put spreads as a hedge even as his core positions stay heavily long. His year-end target still runs above $200,000.

Bitcoin recently traded near $61,345, down 2.3% in 24 hours. Jiang’s range sits roughly 30% below that level, while Hayes’ $40,000 floor implies a drop closer to 35%.

Whether mNAV leads price by six months once more is the real test, and it will shape Bitcoin price forecasts heading into late 2026.

The post China’s Top Bitcoin Miner Suggests Arthur Hayes Is Right About BTC Bottom appeared first on BeInCrypto.

TLDR

- XRP Ledger validators warned users about fake JPYSC tokens using the stablecoin’s ticker.

- SBI launched JPYSC on June 24 through SBI VC Trade for account holders only.

- SBI has not confirmed any JPYSC issuance on the XRP Ledger or other public chains.

- JPYSC currently cannot move to external wallets or public blockchain networks.

- SBI said public-chain circulation is ready but still awaits tax and regulatory approval.

XRP Ledger (XRPL) validators warned users against fake JPYSC tokens after SBI launched its yen stablecoin. The alert followed claims about a possible XRPL issue. SBI has not confirmed any release.

XRP Ledger Community Flags Fake JPYSC Claims

XRPL validator Vet, Hussein Zangana, said SBI has made no public JPYSC issue on XRPL. Therefore, any current JPYSC ticker remains suspicious.

The warning followed the June 24 launch of JPYSC by SBI Holdings through SBI VC Trade. The launch drew attention because SBI has links with Ripple.

Another XRP community member said monitoring tools now track trustlines linked to known SBI addresses. Those systems could help detect official activity later.

Community checks focus on issuer addresses, trustlines, and token metadata on the XRP Ledger. However, validators said users need SBI confirmation before treating any asset as valid.

The alerts target scam tokens that may copy the JPYSC name or ticker. Such tokens can appear quickly on public ledgers because anyone can create assets.

Vet said JPYSC has received no public XRPL announcement from SBI. As a result, he urged users to verify sources before any interaction.

JPYSC Remains Limited to SBI VC Trade

SBI launched JPYSC as a yen stablecoin for SBI VC Trade account holders. SBI Shinsei Trust Bank issues the token, while SBI VC Trade distributes it.

The stablecoin came from a joint effort between SBI and Startale Group. It operates as a trust-type electronic payment instrument under Japan’s framework.

SBI said this structure removes the ¥1 million transaction cap applied to some payment products. The company presented JPYSC as a regulated yen stablecoin.

For now, SBI keeps JPYSC inside SBI VC Trade accounts. Users cannot withdraw the token to external wallets or blockchains.

SBI said it has completed technical and operational work for public blockchain circulation. Yet the company still awaits regulatory and tax treatment before transfers.

The company has not named any public chain for JPYSC deployment. Therefore, XRP Ledger links remain unconfirmed despite community speculation.

SBI Chairman and CEO Yoshitaka Kitao called blockchain migration in finance “irreversible.” He described JPYSC as part of Japan’s blockchain finance infrastructure.

Startale founder Sota Watanabe said external wallet transfers are technically ready. He said remaining issues relate mainly to regulation and tax rules.

No SBI statement has connected JPYSC to the XRP Ledger. Community members continue tracking issuer activity while warning users against fake tokens.

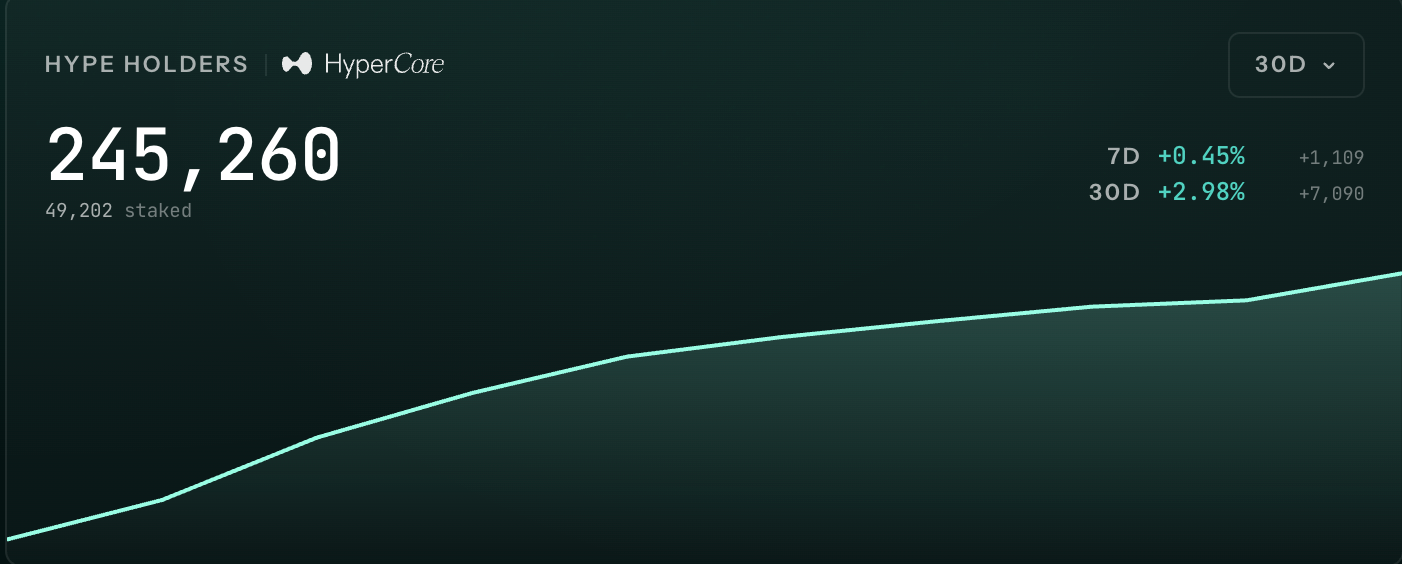

Hyperliquid (HYPE) has trended lower since hitting a record high, shedding 17% amid broader market weakness. Yet, the network behind it tells a steadier story.

Several on-chain and ecosystem metrics indicate that user participation and capital activity have remained resilient despite the recent price decline.

User Growth Continues Despite Price Weakness

Network activity increased even as HYPE moved lower. On-chain data showed that HyperCore daily active addresses rose 17.4% over the past 24 hours to 68,600.

The number of HYPE holders also expanded during the decline. Over the last seven days, wallet count increased by 1,109 addresses, or 0.45%, while the token fell 12.5%.

Follow us on X to get the latest news as it happens

Longer-term growth remained intact as well. Total holders reached 245,260 in June, up roughly 3% over the past month.

Capital trends also paint a different picture from the broader DeFi market. As BeInCrypto reported, DeFi total value locked (TVL) has declined every month in 2026, falling 39% overall.

Hyperliquid has been a notable exception. Alongside TRON, it was one of only two top-10 chains to record TVL growth this year, indicating that capital has continued flowing into the ecosystem despite the wider sector slowdown.

Revenue and Buybacks Support the Ecosystem

Meanwhile, an on-chain analyst noted that Hyperliquid repurchased $135 million of HYPE over 90 days, while $64 million was unlocked for the team.

The imbalance suggests that buy-side demand generated by the protocol has outpaced the additional supply entering the market from token unlocks, helping absorb potential selling pressure.

Protocol revenue backs the trend. DefiLama data shows revenue climbed for three consecutive months, rising from $44.85 million in April to $53.80 million in June.

It’s worth noting that gain is a recovery, not a record. April was the weakest month of 2026, while January revenue was nearly $63.94 million.

HYPE Demand Holds Despite a Broader Downtrend

Lastly, larger market participants remained active despite the correction. According to Lookonchain, a new wallet, 0x987f, withdrew 278,827 HYPE, worth approximately $17.45 million, from Coinbase Prime.

Meanwhile, whale address 0x2386 pulled 96,930 HYPE valued at roughly $6.01 million from BitGo after a month-long pause in activity.

Institutional interest has also remained positive. While spot Bitcoin and Ethereum ETFs have recorded continuous outflows in recent weeks, HYPE investment products attracted $27.9 million in inflows last week. This marked their strongest weekly inflow since late May, according to SoSoValue data.

Price and these signals now point in opposite directions. The coming weeks will test whether they pull HYPE back toward its record high. At press time, HYPE traded at $63.4, up 1.91% over the previous 24 hours.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post HYPE Drops 17% From Record High but Hyperliquid Fundamentals Remain Strong appeared first on BeInCrypto.

Money – Yarma ft-Diekar

Tips for beating the heat, according to Telegraph readers

Rafael Nadal says he won’t come back to tennis like Serena Williams

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment5 days ago

Entertainment5 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports2 days ago

Sports2 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech3 days ago

Tech3 days agoMicrosoft accidentally kills epic Outlook email threads

-

Business5 days ago

Business5 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics5 days ago

Politics5 days agoAndy Burnham and the meaning of Makerfield

-

Crypto World2 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

NewsBeat6 days ago

NewsBeat6 days agoKeir Starmer Allies Question His Chances For No 10

-

Politics7 days ago

Politics7 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Crypto World1 day ago

Crypto World1 day agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business2 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business6 days ago

Business6 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Crypto World5 days ago

Crypto World5 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World6 days ago

Crypto World6 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World5 days ago

Crypto World5 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Entertainment6 days ago

Entertainment6 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech4 days ago

Tech4 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Sports5 hours ago

Sports5 hours agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Tech3 days ago

Tech3 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Sports7 days ago

Sports7 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

You must be logged in to post a comment Login