Crypto World

What are liquid staking tokens? stETH and the depeg risk, explained

Staking locks your crypto and earns yield. Liquid staking hands you a tradeable receipt for that locked position, so the same capital can earn twice. It is one of DeFi’s largest markets, and it comes with a specific danger most guides skip: the receipt can trade below what it represents. Here is how liquid staking tokens work, and where the risk actually lives.

Summary

- Liquid staking tokens let users keep earning staking rewards while using a tradeable token across DeFi without unlocking the original assets.

- The biggest risk comes when liquid staking tokens trade below the value of the assets backing them, especially during periods of market stress and heavy withdrawals.

- Higher yields from liquid staking strategies often involve leverage, increasing the risk of liquidations if the token temporarily loses its peg.

Staking a proof-of-stake asset like Ether involves a trade-off that used to be absolute: lock your tokens to help secure the network and earn rewards, and accept that the locked tokens are frozen and useless for anything else. Liquid staking removes the second half of that bargain. You deposit your tokens with a protocol, the protocol stakes them for you, and in return you receive a new token, a liquid staking token, that represents your staked position and can be freely traded, sold, or put to work elsewhere in decentralized finance. The original capital keeps earning staking rewards; the receipt token lets that same capital do a second job.

That double-duty is why liquid staking became one of the largest categories in all of DeFi, with tens of billions of dollars flowing into it. It is also why it carries a risk that plain staking does not. The receipt token is only useful if the market treats it as equal in value to the asset it represents, and there are moments, usually the worst possible moments, when the market does not. A liquid staking token can trade below the value of the staked asset behind it, an event called a depeg, and understanding when and why that happens is the difference between using this tool safely and being surprised by it.

This guide explains what liquid staking tokens are, the two designs they come in, how the peg is supposed to hold and how it breaks, the concentration risk hiding behind the biggest provider, the way these tokens get stacked into leverage across DeFi, and the practical questions to ask before holding one. The star example throughout is stETH, the largest liquid staking token, but the mechanics apply across the category, from Rocket Pool’s rETH on Ethereum to the staked-asset tokens on other proof-of-stake networks. The goal is to leave you able to hold one of these tokens understanding exactly what it is, what backs it, and under what conditions its price can part ways with the asset it represents.

The problem liquid staking solves

To see why liquid staking exists, start with the friction of ordinary staking. On Ethereum, running your own validator requires locking thirty-two ether, operating node software with constant uptime, and accepting that your stake is subject to exit queues when you want out. For most holders this is impractical: they lack thirty-two ether, do not want to run infrastructure, and dislike freezing capital they might need, especially as Ethereum reworks its staking and consensus layers in ways that will reshape validator economics for years.

Staking pools solved the first problems by letting many users combine smaller amounts under professional validators, but the funds were still locked. Liquid staking solves the last problem, the lock itself. When you deposit into a liquid staking protocol, it pools your tokens with everyone else’s, stakes them across a set of validators, and mints you a token representing your share of the staked pool plus its accruing rewards. You no longer need thirty-two ether, you never touch validator software, and, crucially, your position is now liquid: the receipt token sits in your wallet and can move freely while the underlying stake keeps earning.

A coat-check analogy captures it. You hand over your coat and receive a claim ticket. The coat stays safely in the cloakroom earning nothing, but the ticket is now in your hands, and while you cannot wear the ticket, you can hold it, hand it to a friend, or even sell it. Liquid staking works the same way: the staked asset stays locked and productive, while the token proving your claim to it circulates freely. Whoever holds the ticket holds the claim, so selling the token means selling the staked position along with it.

The result is capital efficiency that plain staking cannot match. A holder can stake, receive the token, and then lend it, use it as collateral, or provide it as liquidity, earning a second layer of return on top of the base staking reward, all without unstaking. That stacking is the appeal and, as later sections show, the source of the systemic worry.

Two designs: rebasing and value-accruing

Liquid staking tokens come in two flavors, and the difference matters for how rewards show up in your wallet and how the token behaves in DeFi.

A rebasing token keeps its price pegged to the underlying asset one to one and delivers rewards by increasing the number of tokens you hold. Lido’s stETH is the classic example: hold it, and your stETH balance grows a little each day, with each stETH meant to remain worth roughly one ether. The appeal is transparency, since your balance visibly climbs, but the growing balance complicates integrations, because many DeFi protocols were not built to handle a token quantity that changes on its own.

A value-accruing token keeps the token count fixed and delivers rewards by rising in value against the underlying asset. Rocket Pool’s rETH works this way, as does the wrapped version of stETH, wstETH. You hold the same number of tokens over time, but each one is redeemable for progressively more ether as rewards accumulate; stake when one token equals one ether and, a year later, that token might redeem for meaningfully more. This design integrates more smoothly across DeFi because the balance is stable, which is why wrapped, value-accruing versions dominate in lending and liquidity protocols and increasingly appear in the institutional DeFi rails being built on other ledgers too.

The distinction is easy to miss and important in practice. A rebasing token used as collateral can behave strangely because its balance shifts; a value-accruing token trades at a price that is intentionally above one-to-one and rising, so seeing rETH or wstETH quoted above the price of ether is normal and correct, not a premium to fear. Knowing which design you hold prevents misreading its price and misusing it in a protocol.

How the peg holds, and how it breaks

The entire usefulness of a liquid staking token rests on the market valuing it close to the staked asset it represents. That relationship is a soft peg, maintained by arbitrage and redemption instead of any hard guarantee, and understanding the mechanism explains exactly when it can slip.

In normal conditions the peg holds tightly because of a redemption path. A stETH is a claim on staked ether, and once the protocol’s withdrawal queue is functioning, that claim can be redeemed for actual ether. If stETH ever trades meaningfully below one ether on the open market, arbitrageurs buy the discounted stETH, redeem it for a full ether through the queue, and pocket the difference, and that buying pressure pushes the price back toward parity. Deep secondary-market liquidity reinforces this: research on stETH has found that most deviations beyond a small threshold correct within hours, because the arbitrage is reliable and the market is deep.

The peg breaks when the redemption path is slow and the market panics faster than arbitrage can act. Redeeming a liquid staking token for the underlying asset is not instant; it runs through the network’s validator exit queue, which can take days when many people withdraw at once. In a stressed market, holders who want out immediately cannot wait for the queue, so they sell on the open market instead, and a wave of forced selling can push the token below the value of the asset behind it. This is a depeg: not a loss of the underlying stake, but a temporary discount on the receipt.

The defining real-world case came in 2022, when stETH traded as low as roughly a nickel under parity during a broad market crisis. Large holders facing liquidation needed liquidity immediately, the withdrawal path at the time did not allow direct redemption, and the resulting sell pressure drove stETH to a visible discount to ether. Critically, the underlying staked ether was never lost or impaired; the discount reflected the mismatch between an instant desire to exit and a redemption process that could not move instantly. Once redemption became possible and panic subsided, the peg restored. The episode is the template: a liquid staking token depeg is almost always a liquidity-and-timing event, not a solvency event, but that distinction is cold comfort to someone forced to sell at the discount.

How the yield actually stacks

A concrete walk-through of the returns shows both why liquid staking is popular and where the layers of risk enter, because each layer of yield is also a layer of exposure.

Start with the base. Staking ether on Ethereum earns a network reward, a modest annual percentage that comes from new issuance and transaction fees paid to validators for securing the chain. A holder who simply stakes and holds a liquid staking token captures this base reward with almost none of the friction of solo staking: no thirty-two-ether minimum, no node to run, no direct exit-queue management. For many holders, that is the entire appeal, and it is a reasonable, relatively conservative use of the tool.

The second layer comes from putting the token to work. Because the liquid staking token is freely tradeable, a holder can deposit it into a lending protocol to earn interest, supply it to a liquidity pool to earn trading fees, or use it as collateral, each adding a return on top of the base staking reward. This is the capital efficiency that plain staking cannot match: the same underlying ether earns its staking reward and a second yield simultaneously. It is also where smart-contract risk begins to compound, because the token now passes through a second protocol’s code in addition to the staking protocol’s own.

The third layer, and the dangerous one, is leverage, described earlier: borrowing against the token to acquire more of it and repeating the loop. Each turn of the loop multiplies the base yield, which is why advertised returns on some liquid staking strategies look far higher than the underlying staking reward could ever justify. The arithmetic that produces those headline numbers is leverage, and leverage is precisely what converts a survivable depeg into a forced liquidation.

The practical takeaway is to read any liquid staking yield as a signal of how many layers are involved. A return close to the base staking reward is a plain, relatively safe position. A return well above it means the token is deployed into other protocols, adding smart-contract exposure. A return far above the base almost always means leverage, and therefore liquidation risk in a depeg. The yield number is not just a reward; it is a readout of the risk stack beneath it, and matching the layer you accept to the risk you understand is the whole discipline of using these tokens well. The same logic governs every layered yield strategy in DeFi: more yield is always more of something else at risk.

The concentration problem

Beyond the depeg risk sits a subtler, more structural concern: one protocol dominates Ethereum liquid staking to a degree that worries people who think about the network’s health.

Lido, the issuer of stETH, has for long stretches controlled roughly a third of all staked ether, a share large enough that Ethereum researchers openly discuss it as a risk to the network itself. The reasoning is about consensus: if a single staking entity controls too large a fraction of validators, it gains outsized influence over block production and could, in extreme scenarios, threaten the neutrality or censorship-resistance the network depends on. This is not an accusation that Lido would misbehave; it is a structural observation that concentration itself is a vulnerability, regardless of the operator’s intentions, and it is why parts of the community actively encourage stakers to choose smaller providers.

Concentration also compounds the token-level risks. When one liquid staking token is embedded as collateral across nearly every major lending protocol, a serious problem with that token, a smart-contract bug, a governance failure, or a severe depeg, is not one protocol’s problem but a shock that ripples through all of DeFi at once. The dominant token’s ubiquity, which is a convenience in calm markets, becomes a transmission channel in stressed ones. The same dynamic appears wherever a single asset becomes foundational infrastructure, from stablecoins to the restaking protocols that layer additional yield on top of staked positions: dominance buys efficiency and sells fragility.

For an individual holder, concentration risk is mostly about awareness. Using the largest, most liquid token gives the tightest peg and the deepest DeFi integration, which is a real benefit; it also means holding the asset most entangled with everything else, so a systemic event touches it first. Diversifying across providers reduces personal exposure and, in aggregate, improves the network’s health, at the cost of slightly thinner liquidity in the smaller tokens.

The leverage stack, and why it magnifies everything

The feature that makes liquid staking tokens powerful, their usability across DeFi, also enables a leverage loop that turns a modest depeg into a cascade. Understanding this loop is essential to understanding why depegs matter beyond the inconvenience of a discount.

The loop works like this. A user stakes ether and receives a liquid staking token. They deposit that token as collateral in a lending protocol and borrow ether against it. They stake the borrowed ether, receive more of the liquid staking token, deposit that as collateral, and borrow again. Repeated, this stacks several layers of leverage on a single underlying position, each layer amplifying the yield in calm markets. It is a popular strategy precisely because the base staking reward, multiplied by leverage, produces attractive returns.

The danger is what happens when the token depegs. Each borrowing position has a liquidation threshold tied to the value of the collateral, and a depeg lowers that value. As the token slips below parity, leveraged positions approach liquidation; liquidations force the collateral token to be sold; that selling deepens the depeg; the deeper depeg triggers more liquidations. In stressed markets this becomes a self-reinforcing spiral, a domino run dressed in yield-farm packaging. The 2022 depeg was made sharper by exactly this dynamic, as leveraged holders were forced to unwind into a falling market.

The lesson for holders is that a liquid staking token held plainly is a fairly conservative instrument: it earns staking yield and, absent a solvency failure in the protocol, its worst realistic outcome is a temporary discount that arbitrage eventually closes. The same token levered several times over is a very different risk, one where a discount that a plain holder could simply wait out becomes a forced liquidation. The token did not change; the leverage around it did. Anyone evaluating liquid staking yields that look unusually high should assume leverage is involved and price the liquidation risk accordingly.

What to check before holding one

Liquid staking is a genuinely useful tool, and using it well comes down to a handful of concrete checks, not blanket caution.

Confirm the token design. Know whether you hold a rebasing token, whose balance grows, or a value-accruing one, whose price rises, because the two behave differently in your wallet and in any protocol you deposit them into. Value-accruing wrapped versions are generally the smoother choice for DeFi use.

Assess the redemption path. The peg’s strength depends on being able to redeem the token for the underlying asset, so check that direct withdrawals are live and how long the exit queue runs. A token with a fast, functioning redemption path has a stronger peg than one where exit depends entirely on selling into secondary-market liquidity.

Gauge the liquidity and the provider. Deep secondary-market liquidity is what lets arbitrage defend the peg between redemptions, so a token with thin liquidity is more prone to slipping and slower to recover, the same slippage dynamics that govern any thinly-traded swap. Weigh the largest provider’s tight peg and deep integration against its concentration risk, and consider whether spreading across providers suits your risk tolerance and, incidentally, helps the network.

Respect the layered smart-contract risk. Your capital passes through the staking protocol’s contracts, and if you deploy the token into lending or liquidity protocols, through those as well. Each layer is code that can contain bugs, and stacking layers stacks the places something can break, the same concentration-of-risk lesson that runs through every major bridge exploit. Favor audited, long-lived protocols, and treat any strategy promising outsized yield as a signal that leverage, and its liquidation risk, is present.

Held with these checks in mind, a liquid staking token does what it promises: it unlocks the value of a staked position so the same capital can work twice, earning a base reward while remaining liquid and productive. The depeg risk that defines the category is real but specific, a timing-and-liquidity event instead of a loss of the underlying stake, and it is most dangerous not to plain holders but to those who lever the token into a stack that turns a temporary discount into a forced sale. Understand which of those two users you are, and the risk becomes something you can size instead of something that surprises you.

The broader significance is worth a closing thought. Liquid staking tokens have become foundational plumbing for proof-of-stake economies: tens of billions of dollars of staked value now circulate as these receipts, and they underpin lending, trading, and collateral across DeFi. That ubiquity is a genuine achievement, turning otherwise idle staked capital into productive infrastructure. It also means the health of a few dominant tokens matters to the whole system, which is why the concentration and depeg risks discussed here are not merely individual concerns but systemic ones.

Using these tokens knowledgeably, favoring strong redemption paths, deep liquidity, and audited protocols, and staying alert to the leverage hiding behind unusually high yields, is how an individual participates in that system without being surprised by its failure modes.

Frequently asked questions

What is a liquid staking token?

A liquid staking token is a tradeable token you receive when you stake a proof-of-stake asset through a liquid staking protocol. It represents your staked position plus its accruing rewards, and it can be freely sold or used in DeFi while the underlying asset stays staked and earning. stETH from Lido and rETH from Rocket Pool are the best-known examples on Ethereum.

How is liquid staking different from regular staking?

Regular staking locks your tokens, making them unavailable for anything else until you unstake through an exit queue. Liquid staking gives you a receipt token that keeps your capital liquid, so you can trade it or use it elsewhere in DeFi while the underlying stake continues to earn rewards. The trade-off is added smart-contract risk and the possibility that the receipt token depegs.

What does it mean when stETH depegs?

A depeg means the liquid staking token trades below the value of the staked asset it represents, such as stETH trading below one ether. It usually happens when many holders want to exit faster than the redemption queue allows, so they sell on the open market and push the price to a discount. Importantly, a depeg is generally a liquidity and timing event, not a loss of the underlying staked asset.

Is my staked asset lost if the token depegs?

No. A depeg reflects a temporary market discount on the receipt token, not destruction of the underlying stake. The staked asset remains intact and continues earning, and once the redemption path clears and panic subsides, arbitrage typically restores the peg. The real risk is being forced to sell at the discount, which mainly affects leveraged holders facing liquidation.

Are rebasing and value-accruing tokens different?

Yes. A rebasing token like stETH stays pegged one-to-one and pays rewards by increasing your token balance over time. A value-accruing token like rETH or wrapped stETH keeps the balance fixed and pays rewards by rising in value against the underlying asset. Value-accruing versions integrate more smoothly into DeFi because their balance does not change unexpectedly.

Why is Lido’s dominance considered a risk?

Lido has often controlled roughly a third of all staked ether, and Ethereum researchers worry that any single staking entity holding too large a share of validators could gain outsized influence over the network’s consensus. It also means the dominant token is embedded across most of DeFi, so a serious problem with it would ripple widely. The concern is structural rather than an accusation of misconduct.

Can I lose money with liquid staking tokens?

Yes, through several channels: a smart-contract bug in the staking or DeFi protocols you use, a severe depeg that forces you to sell at a discount, or liquidation if you lever the token in a borrowing loop. Held plainly in an audited, liquid protocol, the risk is relatively modest, but stacking leverage on top substantially raises the chance of a forced loss.

What is the leverage loop with liquid staking tokens?

The loop involves staking to get the token, using it as collateral to borrow the underlying asset, staking that to get more of the token, and repeating to stack leverage and amplify yield. It works in calm markets but is dangerous in a depeg, because falling collateral value triggers liquidations that force selling, which deepens the depeg and triggers more liquidations in a self-reinforcing cascade.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 7, 2026.

Key Highlights

- MasTec (MTZ) is purchasing electrical contracting firm The Superior Group in a $1.65 billion transaction

- Transaction terms include $1.175 billion cash plus $475 million in MTZ shares, with additional earnout provisions

- Superior anticipates generating between $1.6 billion and $1.7 billion in revenue throughout 2026

- Shares of MTZ declined 5.72% in response to the acquisition news

- Investment firm Mizuho increased MTZ price target to $502 while keeping Outperform status

On July 7, 2026, MasTec (MTZ) unveiled plans to acquire The Superior Group, an electrical contracting company based in Ohio, for roughly $1.65 billion.

Following the announcement, shares tumbled 5.72%, dropping $21.78 to close at $358.85.

The transaction structure includes $1.175 billion in cash payments and $475 million worth of MasTec shares. Additionally, an earnout component based on Superior’s performance metrics over the following 36 months has been incorporated.

Based on Superior’s projected 2026 adjusted EBITDA, the acquisition represents approximately 6.9 times that figure.

Operating from Columbus, Ohio, Superior maintains a workforce of approximately 3,000 employees. As an IBEW-signatory electrical contractor, the firm delivers comprehensive solutions spanning design, construction, engineering, prefabrication capabilities, and project oversight.

The company’s revenue stream is heavily concentrated in the data center sector, representing about 90% of operations, with hyperscale clients accounting for roughly 70% of business.

For calendar year 2026, Superior forecasts revenue ranging from $1.6 billion to $1.7 billion, alongside adjusted EBITDA between $225 million and $250 million. MasTec anticipates Superior will generate $2.2 billion to $2.5 billion in revenue during 2027.

Through the balance of 2026, Superior is positioned to contribute $800 million to $900 million in revenue and $100 million to $115 million in adjusted EBITDA to MasTec’s financial performance.

Superior brings a substantial $1.4 billion project backlog and maintains a 300,000-square-foot prefabrication center — strategic assets that enhance MasTec’s operational capabilities.

Integration Into MasTec’s Power Delivery Division

The acquisition will establish Superior as a distinct group within MasTec, functioning under the Power Delivery segment umbrella. This segment’s profit margins are projected to expand into the low double-digit range from the current level of approximately 9%.

Bryan Stewart, who currently serves as Superior’s Chairman and CEO, will continue in leadership alongside the company’s existing executive team.

To finance the cash component, MasTec will utilize available cash reserves, its current credit line, and two delayed draw term loan facilities arranged in conjunction with the transaction.

The transaction is anticipated to finalize in mid-to-late July 2026, subject to antitrust regulatory clearance.

Wall Street Response

Mizuho elevated its MTZ price objective to $502 from the previous $498 target following the deal announcement, maintaining its Outperform recommendation. The investment bank observed that this acquisition completes the data center strategy MasTec presented during its May 12 analyst presentation.

Several other Wall Street firms had already adjusted their targets upward prior to this transaction. KeyBanc established a $500 target with an Overweight stance. Stifel upgraded its objective to $455, while TD Cowen advanced its target to $445 from $320. Jefferies currently maintains a $493 price target.

During Q1 2026, MasTec disclosed a 28% year-over-year expansion in backlog, with new contract awards climbing 18% compared to the prior-year period. The company’s backlog reached a record $20.3 billion as of the end of March.

MasTec conducted a conference call on Wednesday at 9:00 a.m. ET to provide details on the acquisition. Lazard served as financial advisor to MasTec in the transaction; UBS represented Superior.

Citadel told the New York court the decision to stop pursuing the case had nothing to do with the merits of its claims. Instead, it said it had already prevailed in a separate London arbitration against Portofino’s founders on employment-related claims including breach of contract, unlawful means conspiracy and deceit, winning damages and legal costs that the High Court later recognized and made enforceable.

Despite that victory, Citadel said it has been unable to collect the award, leading to the bankruptcy petition against Lancia.

In the filing, Citadel says Lancia owes 5.98 million pounds of the 2025 award by the London Court of International Arbitration as well as interest and costs.

The petition says the awards were recognized by England’s High Court in February, a statutory demand served in April went unsatisfied, and Lancia’s attempt to set aside that demand was dismissed in May.

Citadel estimates it holds security worth only about 21,886 pounds against the debt, mostly small bank accounts and minority interests in French companies.

In the letter accompanying the U.S. dismissal, Citadel also noted that Lancia is subject to a worldwide freezing order and faces bankruptcy proceedings, adding that evidence presented at a June 26 High Court hearing failed to persuade the court that his ownership stake in Portofino held significant value.

Vessels off the coast of the Khor Fakkan Container Terminal, the only natural deep-sea port in the region and one of the major container ports in Sharjah Emirate, along the Gulf of Oman on June 28, 2026.

– | Afp | Getty Images

President Donald Trump said the ceasefire with Iran is “over” after the U.S. conducted strikes against the Islamic Republic following attacks on commercial vessels in the Strait of Hormuz.

Now, traders on prediction market platform Kalshi are recalibrating their outlook for when they see traffic in the passageway returning to normal.

Speculators now see just a 44% chance that traffic flows will return to normal by Dec. 1. The earliest they forecast normal traffic by is Jan. 1, 2027, when odds rose to 53%.

Kalshi defines normal traffic flows as a 7-day moving average of transit calls through the strait above 60. The outcome is verified using data reported from IMF PortWatch.

Odds of when traffic will return to normal have tumbled sharply over the last few days. As recently as July 4, traders on Kalshi placed more than 50% odds that flows would return to normal by Oct. 1.

Traders on Polymarket are slightly more optimistic, with speculators there seeing a 59% chance that traffic flows return to normal in the vital maritime passage by Dec. 31. Polymarket uses the same definition and data as Kalshi to resolve contracts related to traffic in the Strait of Hormuz.

Traffic in the strait is “suddenly very far from normal,” Piper Sandler analyst Jan Stuart at Piper Sandler wrote in a Wednesday note.

“With the Strait back in play, global oil supply is again way short,” Stuart wrote. “Any hope of commercial insurers reducing ‘war risk’ assessments in months has been sunk.”

Disclosure: CNBC and Kalshi have a commercial relationship that includes customer acquisition and a minority investment.

Bitcoin sentiment is sliding to a level Lyn Alden describes as the weakest she has personally seen, as the latest market phase has become more corporate- and leverage-influenced rather than driven by fresh spot demand. In an interview with Natalie Brunell on Tuesday, Alden argued that Bitcoin’s long-term case cannot depend on outside saviors—it must be able to “survive on its own merits.”

The comments also arrive as Strategy, Michael Saylor’s flagship corporate Bitcoin vehicle and the largest public holder, disclosed another round of selling. Strategy’s Monday weekly 8-K filing said it sold 3,588 BTC, a disclosure that has intensified scrutiny of how corporate structures and yield-style products interact with Bitcoin’s volatility.

Key takeaways

- Lyn Alden said current Bitcoin sentiment is at the lowest point she has seen, and she expects a year that is “flat to up” rather than “flat to down.”

- Alden emphasized Bitcoin must stand on core fundamentals—liquidity, permissionless transfer, and value storage—rather than new external catalysts.

- While Alden sees a role for Strategy’s STRC preferred stock, she cautioned that BTC-linked products can encourage leverage.

- On protocol change proposals, Alden urged caution and criticized the “existential issue” framing used to push faster rule modifications.

Why Alden thinks this cycle feels different

Alden contrasted the present mood with the 2022 bear market, when Bitcoin fell as low as the mid–$16,000 range but investor enthusiasm remained comparatively steadier. In her view, the current drawdown has come alongside a fading of narratives and a market cycle that has leaned more heavily on corporate balance sheets and institutional-style structures.

She also flagged investor disappointment as a contributor to sentiment deterioration. Even so, Alden laid out a tempered base case: she does not expect Bitcoin to print a new all-time high within the year, while also acknowledging the asset’s historic volatility leaves room for a sharp upside move.

Her “hope” scenario is not a fast recovery to new highs, but the prevention of further sustained declines—what she described as a “lack of new bottoms in place.” Technically, she suggested the broader path could look more sideways to upward rather than trending lower, though she did not frame that as a guarantee.

Strategy’s sale and the debate over leverage

Corporate adoption has been one of Bitcoin’s dominant themes in recent cycles, and Strategy has been central to that story. However, Alden said Strategy’s STRC preferred stock has increasingly become part of the market’s trading and positioning toolkit—especially for investors who want exposure to the company’s Bitcoin strategy without holding BTC directly or taking on the full volatility profile.

At the same time, she warned that the presence of higher-yielding BTC-linked products can unintentionally pull more leverage into the system. That dynamic matters because the more investors rely on layered exposure structures, the more sensitive performance can become when market conditions tighten—even if the underlying asset remains unchanged.

Her remarks land amid ongoing discussion about Strategy’s capital structure and the perceived risks tied to Bitcoin-backed preferred stock products. Alden characterized recent actions by Strategy to rebuild reserve coverage and add safeguards as reasonable reactions to market stress, but she also stressed that the long-term behavior of such products still ultimately depends on Bitcoin’s price action.

In practical terms, Alden’s framing suggests investors should distinguish between a product’s access benefits and the risk it may add to portfolio behavior during drawdowns. For traders, that translates into being more precise about the source of exposure—spot versus structured yield versus leverage—and how each tends to react when sentiment breaks.

BIP-110 and Alden’s stance on faster protocol changes

Alden also addressed Bitcoin Improvement Proposal 110 (BIP-110), a proposal aimed at reducing network spam by restricting data-heavy transactions, including those used for storing images. Her position was notably cautious: she said she is generally wary of efforts to change Bitcoin’s rules quickly, arguing that some proposals could increase network complexity or alter existing safeguards.

Rather than rejecting technical scrutiny outright, Alden said she would evaluate the arguments for and against protocol changes. Still, she criticized how some proposals are presented publicly, especially when they are framed as an “existential issue” for Bitcoin. In her view, that kind of language exaggerates the stakes and can amount to “incorrect marketing.”

The takeaway from her comments is not simply that all rule changes are bad, but that the way proposals are communicated can affect how investors and users interpret urgency—particularly during periods when sentiment is already fragile.

What to watch next

With sentiment at a cycle-low level in Alden’s assessment and Strategy’s selling now firmly in focus, traders and long-term holders will likely watch whether Bitcoin stabilizes without additional “new bottoms,” and whether BTC-linked structured products become a source of fragility—or a stabilizing bridge—during the next leg of market direction.

Bitcoin is facing its weakest sentiment cycle yet, according to Lyn Alden, a Bitcoin-focused macroeconomist who said the asset must stand on its own as Strategy disclosed a $216 million Bitcoin sale earlier this week.

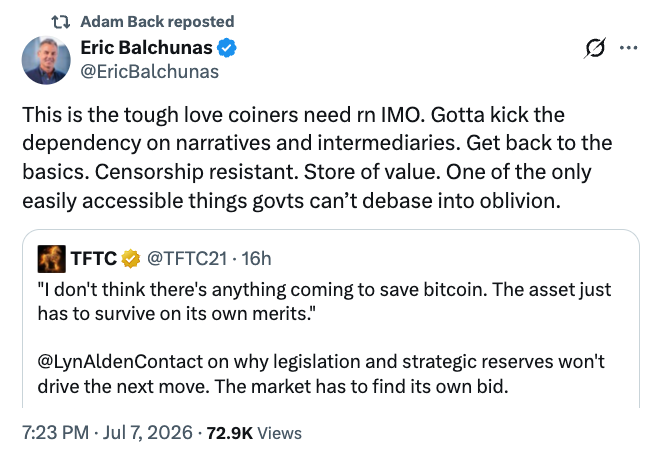

“I don’t think there’s anything coming to save Bitcoin,” Alden said in a Tuesday interview with journalist and Bitcoin educator Natalie Brunell, saying the asset’s long-term success must come from its own fundamentals rather than external catalysts.

“The asset just has to survive on its own merits,” Alden said, pointing to Bitcoin’s underlying properties as a liquid, permissionless way to store and send value, instead of relying on a new source of demand.

Her comments come as institutional adoption and corporate treasury strategies have become features of Bitcoin’s latest market cycle. On Monday, Strategy’s weekly 8-K filing disclosed that it sold 3,588 BTC.

Bitcoin sentiment falls to a cycle low

Alden said the current downturn feels different from the 2022 bear market, when Bitcoin dropped to as low as $16,000 but enthusiasm among Bitcoin investors remained relatively strong.

“This is the lowest sentiment that I’ve personally seen on Bitcoin,” Alden said, pointing to a combination of fading narratives, a more corporate-driven market cycle and disappointment among investors.

Alden said her base case is that Bitcoin will not reach a new all-time high this year, though she acknowledged that the asset’s volatility leaves room for a sharp move higher.

“The base case that I would hope to see is just a lack of new bottoms in place” and a technical picture that points “flat to up rather than flat to down,” Alden said.

STRC found demand, but leverage remains a risk

Michael Saylor’s Strategy, the world’s largest corporate Bitcoin holder, has come under increased scrutiny during the downturn as investors reassess the risks around its Bitcoin-backed capital structure and preferred stock products.

Alden said Strategy’s STRC preferred stock has a role for investors who want exposure to the company’s Bitcoin strategy without holding the asset directly or taking on Bitcoin’s full volatility.

Source: Matthew Sigel

She noted that STRC has become the biggest preferred security in the market, but warned that higher-yielding BTC-linked products can encourage investors to take on additional leverage.

Related: Strategy’s Bitcoin sale may give BTC a ‘durable bottom,’ Grayscale says

She added that Strategy’s recent steps to rebuild its reserve coverage and introduce additional safeguards were reasonable responses to the market stress, though the long-term performance of the product still depends on Bitcoin’s price action.

Alden pushes back on urgency around Bitcoin changes

Alden also discussed Bitcoin Improvement Proposal 110 (BIP-110), which aims to reduce network spam by limiting data-heavy transactions, including those used to store images.

Alden said she is generally cautious about efforts to change Bitcoin’s rules quickly, warning that some proposals could make the network more complex or affect its existing safeguards.

Source: Eric Balchunas

She said she would analyze the technical arguments for and against protocol changes, but criticized the way some proposals are presented to the public. Alden argued that framing a protocol change as an “existential issue” for Bitcoin exaggerates the stakes, calling that approach “incorrect marketing.”

Magazine: Has Bitcoin bottomed for this cycle? Analysts say ‘not yet’

Futures for the Dow Jones Industrial Average and other major stock indexes traded sharply lower Wednesday after President Donald Trump said the U.S.-Iran ceasefire was “over.” Memory stocks Micron Technology (MU) and Sandisk (SNDK) were early losers on the stock market today, threatening to extend their sell-offs amid recent weakness in artificial intelligence stocks. Ahead of Wednesday’s opening bell, Dow…

Copyright ©2026 Investor’s Business Daily, LLC. All rights reserved. 87990cbe856818d5eddac44c7b1cdeb8

Australian crypto exchange Swyftx says it has received an Australian Financial Services License (AFSL), giving it regulatory permission to offer certain crypto-linked products to retail customers and to provide non-cash payment services to businesses and individuals. The move is also tied to Swyftx’s stated shift away from a “spot-only” model, with management pointing to upcoming changes in Australia’s card payment surcharge rules.

According to Swyftx, the license allows it to support derivative offerings—such as crypto options and futures—for retail users, alongside authorization for non-cash payment facilities. The AFSL does not, however, cover spot crypto trading.

Key takeaways

- Swyftx has obtained an AFSL from Australia’s market regulator, enabling retail derivatives and non-cash payment services.

- The company says it does not intend to remain a pure spot exchange, citing room in crypto payments after credit-card surcharge reforms.

- From Oct. 1, Australian merchants are set to face new restrictions on Visa and Mastercard debit/credit surcharges, potentially pushing demand toward alternative payment rails.

- AFSL compliance obligations are expected to become central for most crypto firms, with legislation setting an April 9, 2027 deadline.

Swyftx’s AFSL enables derivatives and payment-facility services

Swyftx announced on Wednesday that it has been granted its AFSL, positioning it among a growing group of crypto companies already operating under Australia’s broader financial-services framework. The license places Swyftx in the same regulatory category as exchanges previously licensed for comparable activities, including Coinbase, BTC Markets and Crypto.com.

In an interview with Cointelegraph, Swyftx interim co-CEO Andrea Yuen said the firm does not plan to remain “a pure crypto spot exchange.” Instead, Swyftx is aiming to broaden its product set and pursue opportunities in payments—particularly in areas it believes could benefit from local regulatory and cost changes affecting card payments.

Operationally, the AFSL matters because it expands what Swyftx can offer within the Australian market. As the company described, the license supports two major directions: derivative products for retail customers (for example, options or futures) and non-cash payment facility authorization, which could allow Swyftx to serve both business and retail clients with payment services.

At the same time, Swyftx’s AFSL does not cover spot crypto trading. That distinction is important for users and investors: the licensing step is not simply a blanket endorsement of all crypto activities, but a permission tied to specific regulated functions.

Why card surcharge changes are driving a push toward crypto payments

A core part of Swyftx’s strategy is directly linked to expected changes to how merchants can recover card payment costs. From Oct. 1, Australian businesses will be banned from adding surcharges to Visa and Mastercard debit and credit card payments. For many merchants, that removes a common mechanism used to pass card transaction costs to customers.

In that environment, Swyftx says it sees potential for alternative payment rails—specifically crypto and stablecoins. Yuen told Cointelegraph that crypto payments and stablecoins could provide merchants with an opportunity to lower transaction costs they may otherwise have to absorb.

The logic is straightforward: when a payment network’s pricing can’t be “passed through” via surcharges, businesses may look for ways to reduce net payment expenses. Stablecoins and regulated crypto payment flows are often discussed as one possible alternative, but the practical impact will depend on merchant adoption, integration pathways, and how regulators supervise payment-related activity.

For the market, Swyftx’s license could also help it participate in payments-based competition rather than relying only on trading volumes. If merchants do move search for cheaper rails following Oct. 1, exchanges with the right authorization may find new distribution channels—especially where stablecoin settlement can be paired with compliant payment tooling.

AFSL deadline pressure builds as ASIC extends a licensing grace window

Beyond Swyftx’s immediate products, the AFSL is tied to a wider regulatory timetable for the Australian crypto sector. Legislation passed in April requires most crypto firms to obtain an AFSL from April 9, 2027, according to earlier coverage by Cointelegraph (https://cointelegraph.com/news/australia-pass-bill-mandate-crypto-exchange-license).

Until now, many crypto exchanges were required primarily to maintain anti-money laundering (AML) and know-your-customer (KYC) controls rather than full financial-services licensing duties. With the AFSL framework, firms are expected to follow compliance standards comparable to other regulated financial institutions.

Yuen described the shift as “an enormous responsibility to be a regulated financial service,” underscoring that obtaining the license is not simply a marketing milestone—it comes with ongoing obligations.

At the regulator level, ASIC has also been working to manage the transition. The Australian Securities and Investments Commission recently extended its grace period for crypto businesses to apply for an AFSL until Sept. 30. ASIC said it has received around 30 license applications from crypto businesses since October last year (ASIC statement: https://www.asic.gov.au/about-asic/news-centre/news-items/asic-extends-no-action-position-for-digital-asset-businesses-to-30-september-2026/).

Only a limited number of crypto exchanges have so far obtained AFSLs, including Coinbase, BTC Markets, Crypto.com and KuCoin, based on prior Cointelegraph reporting (https://cointelegraph.com/news/ripple-eyes-australian-financial-license-through-acquisition).

For investors, traders, and builders, this is a key inflection point: licensing progress can influence which firms can expand into derivatives retail distribution and regulated payment services, while laggards may be constrained by timelines and regulatory uncertainty as April 2027 approaches.

Australian retail adoption remains resilient as licensing expands

While regulatory licensing advances, local interest in crypto assets continues to be reflected in consumer surveys. A survey cited by Swyftx’s update from Independent Reserve suggested that 33% of Australians now own cryptocurrency, up from 31% in 2025.

Independent Reserve CEO Adrian Przelozny said younger Australians are increasingly confronting economic pressures that make traditional wealth-building options—particularly home ownership—feel less attainable. He argued that, as a result, many are exploring alternative assets, with cryptocurrency viewed as one option that has historically delivered stronger returns than traditional portfolios.

The same survey indicated that Bitcoin remains the dominant digital asset among respondents, with 71% reporting they hold it.

Taken together, rising participation and accelerating licensing could create a broader market environment: more consumers may seek regulated access, while exchanges that secure AFSL permissions may be better placed to deepen product offerings and payment-related services.

Looking ahead, readers should watch how Swyftx and other newly licensed firms translate AFSL capabilities into real payment integrations and derivative offerings, and whether merchant adoption follows the Oct. 1 surcharge rule change as expected. The regulatory transition toward 2027 will also be a determining factor in how quickly Australia’s crypto market can diversify beyond spot trading.

AngelList, the venture capital platform hosting more than 50,000 funds and 800,000 accredited investors, is terminating its partnership with Rail – the B2B payments platform operated by Ripple – effective July 31, 2026, removing all crypto payment options from the platform in the process. The decision is a direct setback for Ripple’s enterprise payment ambitions, less than a year after it paid $200 million to acquire Rail.

AngelList confirmed the move in a formal notice, stating that USDC, USDT, DAI, and ETH will become completely unavailable after the July 31 deadline. Users have been directed to switch to ACH and wire transfers for any upcoming investments to avoid processing delays. Existing investments, account access, and portfolio data are unaffected.

No explanation was given for the decision beyond the wind-down notice itself.

Discover: The Best Crypto to Diversify Your Portfolio

What Rail Was Built to Do

Ripple acquired Toronto-based Rail in August 2025 for $200 million as part of a broader $2.45 billion M&A push. Rail’s core proposition was enabling enterprise businesses to process stablecoin payments – including USDC and USDT – across multiple fiat currencies without requiring dedicated crypto wallets or exchange integrations. For a platform like AngelList, it was a clean on-ramp for accredited investors to deploy capital using digital assets.

![]()

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The pitch was straightforward: reduce friction for crypto adoption in institutional workflows without asking enterprises to overhaul their backend infrastructure. AngelList’s exit suggests that the pitch didn’t hold up against the platform’s operational priorities.

What makes the timing notable is the broader context around Ripple. The company secured a key European regulatory license in early July 2026, and Clearstream – the European post-trade giant – added XRP and other tokens to its custody offering just days before AngelList’s announcement. Ripple’s institutional footprint is expanding in some directions while contracting in others, and AngelList’s retreat underscores that crypto adoption in enterprise payment stacks remains uneven regardless of headline momentum.

Discover: The Best Token Presales

What This Signals for Ripple Enterprise Strategy

The AngelList exit doesn’t impair Ripple’s balance sheet, but it does damage the Rail narrative. A $200 million acquisition is easier to justify when flagship enterprise clients stay on the platform; losing a name-brand partner like AngelList – a firm synonymous with the startup and venture ecosystem – invites questions about how deep Rail’s enterprise traction actually runs.

The broader XRP market picture has been constructive in 2026, with ETF inflows and volume metrics tracking positively. But asset price momentum and enterprise product adoption are separate variables, and AngelList’s move is a reminder that conventional fiat rails – ACH and wire transfers – still win on simplicity and compliance predictability for many institutional operators, even ones deeply embedded in the tech ecosystem.

The stablecoin market has faced its own headwinds in 2026, and broader uncertainty around stablecoin settlement infrastructure may be a contributing factor in AngelList’s calculus, even if the company hasn’t said so explicitly.

The operational clock is running. AngelList users currently routing investments through crypto payment options, USDC included, have until July 31 to transition. After that date, the platform reverts entirely to traditional financial infrastructure with no stated timeline for reintroducing crypto payment support.

Watch for whether Ripple responds with a replacement enterprise client announcement to blunt the reputational impact, and whether Rail’s remaining partnerships hold as AngelList’s exit gets priced into how the industry assesses Ripple’s enterprise payment ambitions heading into late 2026.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post Ripple’s $200M Rail Acquisition Loses AngelList as Crypto Payments Get Cut appeared first on Cryptonews.

Key Highlights

- The electric vehicle manufacturer executed a public offering of 75 million shares priced at $15.50 each, generating approximately $1.2 billion in gross capital.

- Shares plummeted more than 18% during Tuesday’s session, followed by an additional ~4% decline in Wednesday’s pre-market trading amid shareholder dilution concerns.

- Second-quarter revenue projections range between $1.55B and $1.65B, surpassing Wall Street’s consensus estimate of approximately $1.45B.

- The automaker increased its 2026 annual delivery guidance to 65,000–70,000 units from the previous 62,000–67,000 range.

- Multiple Wall Street firms, including JPMorgan and Mizuho, recently downgraded the stock to Sell, highlighting capital expenditure concerns and EV subsidy elimination risks.

Shares of Rivian (RIVN) experienced a dramatic decline exceeding 18% during Tuesday’s trading session following the company’s announcement of a 75 million-share public offering priced at $15.50 per share, generating roughly $1.2 billion in gross capital. The selloff continued into Wednesday’s pre-market hours, with shares falling an additional 4.7%.

The pricing of the equity raise came in below recent trading levels, and the substantial influx of new shares severely dampened investor sentiment. Investment banks underwriting the deal also secured a 30-day option to purchase up to 11.25 million additional shares. The transaction is scheduled to finalize on Thursday, July 9.

Rivian indicated the capital raised will support general corporate activities, with a designated portion allocated to satisfy requirements under its loan facility with the U.S. Department of Energy.

The timing of the offering came after shares had rallied on stronger-than-anticipated second-quarter delivery performance. The company delivered 12,194 vehicles during the period, exceeding both internal projections and JPMorgan’s estimate of 11,000 units.

Concurrent with the capital raise announcement, Rivian disclosed preliminary Q2 revenue guidance of $1.55 billion to $1.65 billion, meaningfully above the Wall Street consensus forecast of around $1.45 billion.

The electric vehicle maker also elevated its full-year 2026 delivery outlook to a range of 65,000–70,000 vehicles, representing an increase from its previous guidance of 62,000–67,000 units.

Analyst Community Remains Skeptical

Notwithstanding the encouraging operational metrics, the analyst community maintains a cautious stance. Three separate firms issued Sell recommendations on RIVN shares in recent trading sessions.

JPMorgan analyst Rajat Gupta maintained his Sell rating, highlighting the company’s substantial capital expenditure requirements as a primary risk factor, despite the delivery beat.

Mizuho analyst Vijay Rakesh similarly retained his Sell recommendation, forecasting that battery-electric vehicle sales could remain flat on a year-over-year basis. His pessimistic outlook stems from the termination of federal EV subsidies in the United States.

Jefferies adopted a somewhat more balanced perspective, upgrading its price target to $17 from $16 while maintaining a Hold rating. The firm observed that the equity offering followed a significant stock price appreciation triggered by the Q2 delivery data.

Layoffs Compound Investor Concerns

Earlier this week, news of workforce reductions added further pressure on the stock. Reports indicate that Rivian eliminated hundreds of positions, primarily concentrated in service and customer-facing operations — representing less than 2% of total headcount.

The company continues to operate at a loss and is banking on its more competitively priced R2 SUV to accelerate sales volume. The R2 model debuted in March, with customer orders commencing last month.

Broader market conditions provided no relief. The Nasdaq Composite declined 1.2% on Tuesday amid semiconductor sector weakness, while the S&P 500 retreated 0.5%.

Among 17 analysts providing coverage over the past three months, the consensus recommendation stands at Hold, comprising eight Buy ratings, five Hold ratings, and four Sell ratings. The mean price target of $18.24 suggests approximately 11% potential upside from present trading levels.

Crypto markets fell Wednesday after fresh airstrikes in Iran spurred a risk-off mood among investors. The CoinDesk 20 Index dropped 2.9% since midnight UTC, with all but one token declining.

Addressing NATO leaders, U.S. President Donald Trump declared the ceasefire “over” and said negotiating with Iran is a “waste of time,” though talks continue, according to news reports.

The U.S. Central Command said it hit more than 60 Islamic Revolutionary Guard Corps small boats to prevent them disrupting international shipping and Iran retaliated with attacks on Kuwait and Bahrain.

The Dollar Index (DXY) rose as the reignited tensions are likely to stoke inflation concerns. Bitcoin and ether (ETH), the two largest cryptocurrencies, fell more than 2%.

There were sharper losses across the more illiquid altcoin sector as JUP, ETHFI and PUMP all losing more than 5%.

U.S. equities also took a hit. Nasdaq 100 index futures and S&P 500 index futures tumbled as much as 1.5%.

Derivatives positioning

- Despite bitcoin’s slide to $62,000, it’s still up 6% this month and there is some good news on the derivatives front: Traders don’t look to be shorting the rally. Open interest (OI) in futures has dropped to 730K BTC from over 740K BTC a day ago.

- Ether is not faring so well. Open interest has held steady at around 13.95 million tokens despite the spot-price drop triggering liquidations of bets worth $90 million. BTC 24-hour liquidations tally just over $100 million.

- The sell-off in Canton Network’s CC token has accelerated, with the token’s price slipping to its lowest level since January just as futures open interest rises to a two-week high. This combination points to the possibility of traders shorting the decline, especially since funding rates remain deeply negative, close to -20%.

- Broadly speaking, the bear grip has tightened across major cryptocurrencies, including BTC and ETH, as indicated by their negative 24-hour OI-adjusted cumulative volume delta. A negative reading indicates that price action is being driven by traders placing market orders rather than passive limit orders.

- The latest decline in BTC and ETH seems to have spurred hedging demand for options, as their respective 30-day implied volatility indexes, BVIV and EVIV, are up for the second straight day.

- Options skew on Deribit confirms that. The one-week skew has jumped to nearly 20% in favor of puts from 16% a day ago. Puts offer protection against a price slide in the underlying asset, in this case, BTC. The same is true for ether.

- However, 24-hour volume figures show the highest activity in BTC call options at the $80,000 strike price.

Token talk

- The altcoin market is reeling, with $350 million worth of the $450 million in liquidations being attributed to altcoin trading pairs, according to CoinGlass.

- Solana (SOL) has now completely retraced a rally that began on July 2, trading back at $77 after challenging $84 on Monday.

- One token bucking the bearish sentiment is MORPHO. The DeFi token is up by 4% since midnight as total value locked (TVL) on the protocol hit a record high 4 million ETH this week, according to DefiLlama.

- A beacon of hope for the altcoin market is that several tokens are now dipping back into “oversold” territory, with the average relative strength index (RSI) dropping to 40/100 from 47/100 on Tuesday.

Claire’s Life: Day 2 at Paris Couture Week Wearing Alaia, Christian Louboutin, and Flore K NY

Vikings Land on NFL’s Must-Watch List

China’s DeepSeek Developing Its Own AI Chip

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: High Hopes

-

NewsBeat3 days ago

NewsBeat3 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Fashion2 days ago

Fashion2 days agoOpen Thread: What Great Books Have You Read Recently?

-

Politics5 days ago

Politics5 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World5 days ago

Crypto World5 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Business2 days ago

Business2 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Tech1 day ago

Tech1 day agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Crypto World6 days ago

Crypto World6 days agoBinance stock trading tops $1B in first month after launch

-

News Videos1 day ago

News Videos1 day agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Crypto World6 days ago

Crypto World6 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

Crypto World3 days ago

Crypto World3 days agoSouth Africa proposes crypto tax guidance under existing rules

-

Crypto World2 days ago

Crypto World2 days agoSK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

News Videos2 days ago

News Videos2 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech3 days ago

Tech3 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business7 days ago

Business7 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

NewsBeat6 days ago

NewsBeat6 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Business5 days ago

Business5 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World6 days ago

Crypto World6 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

-

News Videos2 days ago

News Videos2 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

-

Crypto World5 days ago

ESMA Expands Crypto Register by 37 Firms Following MiCA Transition Period

You must be logged in to post a comment Login