Crypto World

What are “the trenches”? Solana memecoin culture

If you spend any time around Solana memecoins, you will hear about “the trenches.” It is where traders called degens fight over brand-new tokens that mostly go to zero, in a culture with its own language, rituals, and brutal economics. Here is what the trenches are, the slang you need to follow them, and the hard reality behind the romance.

Summary

- “The trenches” is crypto slang for the chaotic, high-risk frontier of on-chain memecoin trading, especially brand-new Solana tokens on launchpads like Pump.fun.

- The traders who operate there are called trenchers or degens, and the culture has its own dense vocabulary, rituals, and a war-themed self-image of survival against the odds.

- The trenches run on launchpads, decentralized exchanges, and fast trading tools, where tokens can rocket and collapse within minutes and bots compete for the first buys.

- The romance of life-changing gains is real but rare, and is built on heavy survivorship bias, since the large majority of tokens die fast and most participants lose money.

- Understanding the trenches and its slang is useful for following crypto culture and protecting yourself, but the honest framing is that it functions more like a casino than a market.

“The trenches” is crypto slang for the chaotic, high-risk frontier of on-chain memecoin trading, especially the world of brand-new Solana tokens launched on platforms like Pump.fun, where traders fight for fast profits amid rampant scams, bots, and a flood of coins that mostly go to zero. The phrase is a war metaphor, and it is chosen deliberately. To be “in the trenches” is to be down in the mud of the riskiest, fastest, most unforgiving part of crypto, trading tokens that are minutes old, against opponents who include automated bots and seasoned predators, where fortunes are made and lost in the time it takes to read a chart. It is a culture as much as an activity, with its own dense vocabulary, its own rituals and heroes, and its own grim economics.

The term has spread well beyond its origins, and you will now hear it used for the early, high-risk stage of any speculative crypto play, but its heartland is the Solana memecoin scene, where the conditions that birthed it, instant token creation, near-zero fees, and a permanent firehose of new coins, are most intense. This guide is a map of the trenches for people who want to understand the culture without necessarily entering it, or who are entering it and want to know what they are walking into. It explains what the trenches are and where they physically exist on-chain, the mindset and culture that define the people in them, a working glossary of the slang you need to follow any trenches conversation, how a typical trench play actually unfolds from launch to death or survival, a recent episode that captures the culture in motion, and, most importantly, the hard reality behind the romantic self-image.

That last part matters more than all the slang, because the trenches present themselves as a place of opportunity and camaraderie, and they are also a place where the overwhelming majority of participants lose money to a structure designed to extract it. Learning the language is the easy part. Understanding the economics is what protects you. This guide tries to do both, in that order, so that the culture is legible and the danger is unmistakable.

What the trenches are and where they live

At its core, the trenches refers to the earliest and riskiest stage of memecoin trading, where tokens are brand new and the action is fastest. The phrase captures both a place and a phase. As a phase, it means trading coins in their first minutes and hours of life, before they have established markets, when prices move violently and information is scarce. As a place, it refers to the venues and channels where this happens.

The trenches live on launchpads, above all the dominant Solana launchpad, where anyone can deploy a token in seconds and it begins trading immediately against a bonding curve. For readers new to that pricing model, the mechanism under every launch is the bonding curve, which automatically changes a token’s price as buyers and sellers move in and out. The trenches extend to the decentralized exchanges where tokens move after they graduate from those launchpads, and to the social channels, especially memecoin-focused chat groups, that are themselves often called the trenches, because that is where traders gather to share tips and coordinate.

The infrastructure of the trenches is built for speed, which shapes the entire experience. Traders use specialized tools and bots that let them buy a token within seconds of its launch, read on-chain data in real time, and execute faster than a human could click, because in a world where a coin can rise and fall in minutes, milliseconds of timing translate into enormous differences in entry price. This is why the trenches are not a level playing field: automated snipers and bots routinely buy into a token in its first moments, ahead of the humans who see it trending later. The reason all of this concentrated on Solana is structural: Solana’s very low fees and fast transaction speeds make it cheap and quick to launch coins and to trade them rapidly, which is exactly what a high-frequency, high-churn memecoin culture needs.

The launchpads that lowered the barrier to creating tokens did the rest. The trenches, then, are the on-chain frontier where the cheapest, fastest, most permissionless token creation meets the most speculative trading culture in crypto. The combination produces both the energy and the carnage the term implies. It is why the trenches feel like a live market, a chatroom, and a casino floor at the same time.

The mindset and the culture

The trenches have a distinct culture, and understanding the mindset is as important as understanding the mechanics, because the culture is part of what keeps people in a game that mostly loses them money. The self-image is heroic and martial: participants cast themselves as warriors surviving in hostile territory, enduring losses, hunting for the one coin that will pay for all the others. There is genuine camaraderie in it, a shared identity among people who understand a world outsiders find baffling or repellent, and a folklore of legendary trades and legendary traders. The dominant ethos is captured in the word degen, short for degenerate, which trenchers wear as a badge rather than an insult.

To be a degen in the trenches is to accept that you are gambling and to lean into it with a certain dark humor. That humor and identity are woven through the culture’s language and rituals. Trenchers talk about “locking in,” meaning to focus intensely on the goal of making money quickly with minimal effort, and about hunting for a “gem,” an undervalued coin spotted before the crowd. The culture prizes “alpha,” valuable information or insight shared among insiders, and it runs on a constant cycle of fear of missing out and fear of being wrong, the twin emotions that drive impulsive buying and panic selling.

There is a player-versus-player quality to it, an awareness that in a zero-sum scramble over a worthless token, your profit is someone else’s loss, which the culture acknowledges with a kind of cheerful brutality. All of this creates a powerful social pull. The trenches are not just a market; they are a community with a language, a value system, and an emotional rhythm. That social dimension is a large part of why people stay even as they lose, because belonging and the thrill of the hunt are their own rewards.

Recognizing the culture’s grip is important, because the same camaraderie that makes the trenches compelling is also what makes them hard to walk away from. The community tells itself stories about survival and conviction, and some of those stories are true. But many of them are also retrospective myths built around the tiny number of trades that worked. That is why the culture has to be understood together with the economics, not separately from them.

A working glossary of trench slang

To follow any conversation in the trenches, you need the vocabulary, and the slang is dense enough that an outsider can find a discussion incomprehensible. What follows is a working glossary of the most important terms, enough to read a typical trenches exchange. Begin with the people: a trencher or degen is a high-risk memecoin trader; a jeet is a derisive term for someone who sells too early or panic-sells, dumping on others; and a whale is a holder large enough to move a token’s price with their trades. The verbs of entry and exit matter too: to ape, or ape in, is to buy a token impulsively without much research; to snipe is to buy in the very first moments of a launch, usually with a bot; and to bundle is to coordinate multiple wallets to buy at launch, often to create a false impression of demand.

The lifecycle of a coin has its own terms. A fair launch means a token released with no presale or insider allocation, where everyone enters through the same curve. Graduation is the moment a token completes its bonding curve and moves to a normal exchange. A rug, or rug pull, is the most common trench ending: a scam where the creator pulls liquidity or dumps their holdings, collapsing the price to near zero.

A CTO, or community takeover, is when holders take over a coin the original creator abandoned, running it themselves to try to revive it. The emotional and evaluative vocabulary rounds it out: a gem is an undervalued find; alpha is valuable insight; FOMO and FUD are the fear of missing out and fear, uncertainty, and doubt that drive buying and selling; bags are the tokens you hold; to be underwater is to hold at a loss; and to moon or send it is to rise sharply or to take the plunge on a risky buy. Newer coinages appear constantly, such as a stimmy, slang adopted from stimulus payments to describe handing money to traders, which entered wide use when an influencer pledged to airdrop fees to the trenches. The vocabulary keeps evolving, but these terms form the durable core, and knowing them turns an impenetrable trenches conversation into something you can actually follow.

How a trench play unfolds

To see the culture and mechanics together, follow how a typical trench play unfolds from birth to death, because the lifecycle is remarkably consistent. It begins with a launch: someone deploys a new token on a launchpad, giving it a name, an image, and a ticker, and it starts trading instantly against its bonding curve. In the first seconds, before any human has really noticed, automated snipers and bots may buy in, taking the earliest and cheapest positions, sometimes coordinated across bundled wallets to create the look of organic demand. This is the first hard truth of the trenches: by the time a human sees a coin, bots have often already moved.

Next comes the attention phase. If the coin has a catchy theme, a connection to a trending narrative, or a push from an influencer or a coordinated group, it begins to spread across social channels, and human traders start to ape in, sending the price climbing up the curve as buying accelerates. If the momentum builds far enough, the coin graduates, its accumulated liquidity moving to a normal exchange, which can attract a fresh wave of traders who treat graduation as a sign of legitimacy. Then comes the decisive phase, which for the overwhelming majority of coins is the end.

As the early buyers and any insiders take profit, selling into the latecomers, the price stalls and reverses. If a creator or whale dumps a large position, or pulls liquidity outright in a rug, the price collapses toward zero, often within hours of the peak. Most coins simply fade as attention moves to the next launch and buyers stop arriving, the price bleeding down the curve as holders capitulate. A small number survive, and an even smaller number, occasionally, get a second life through a community takeover, when stubborn or spiteful holders seize the abandoned coin and try to rebuild momentum themselves, which usually fails but can, if executed well, give the holders a better exit.

This lifecycle, launch, snipe, hype, climb, distribution, collapse, plays out thousands of times a day, and recognizing its shape is the difference between understanding what you are watching and being its raw material. It is also why who profits from the churn matters. Launchpads, creators, and early entrants can profit from volume and timing even when the token itself has no lasting value. Late buyers often discover that the chart they are chasing is already in its distribution phase.

The trenches in action

A recent episode captures the culture vividly and ties the abstractions to a concrete moment. In late June 2026, a frenzy erupted around a cluster of Solana memecoins using the name of a prominent influencer, and it played out as a textbook trenches event. Multiple competing tokens using the same name launched at once, and the trading community flipped between them in exactly the player-versus-player scramble the culture is known for, with no single coin crowned the real one for a stretch as trenchers fought over which version would win. One version went parabolic, running to tens of millions in market cap within days, while dramatic individual outcomes, including a trader turning a few thousand dollars into hundreds of thousands, became the kind of folklore that draws more people into the next launch.

The episode also showcased the culture’s vocabulary and rituals in real time. The influencer at the center publicly took the side of the trenches against the launchpad, criticizing how it handled rewards and pledging to airdrop his accumulated fees back to traders, framing it in the community’s own slang as giving the trenches a stimmy because the platform would not. The word stimmy, the framing of small traders as a community owed a payout, the swarm of copycat tokens, the parabolic run, and the rapid churn all embodied the trenches in a single story. It also showcased the danger.

The same influencer disavowed other tokens trading on his name, copycats and impersonations proliferated, and the headline pump figures often did not survive a look at the actual on-chain data. The episode was the trenches in miniature, the camaraderie and the opportunity and the manipulation and the carnage all braided together, which is exactly why it drew such attention. For a student of the culture, it was a live demonstration of every dynamic this guide describes. It was also a reminder that behind the romance of the heroic trade sits a machine that mostly transfers money from latecomers to insiders and platforms.

The reality behind the romance

Strip away the war metaphors and the folklore, and the trenches are, in hard economic terms, a place where most participants lose money to a structure built to extract it, and saying so plainly is the most useful thing this guide can do. The data is unambiguous. Studies of Solana memecoin launches have found that roughly two out of three coins are effectively dead within their first day, with the vast majority of their liquidity gone, and that on the order of 80% or more lose over 90% of their value within about a week. Recent Pump.fun lifespan data showed the same pattern, with nearly seven in 10 reviewed launches recording their final bonding-curve trade on launch day.

By some estimates, the overwhelming majority of tokens launched on the dominant launchpad are scams, pump-and-dumps, or jokes with no lasting value. The life-changing gains that make the folklore are real, but they are extraordinarily rare, and they are visible precisely because they are rare, while the millions of losing trades are invisible. That produces a powerful survivorship bias: you hear about the trader who turned a few thousand into a fortune, never about the thousands who did the opposite. This is the same dynamic that makes the assets traded in the trenches so culturally powerful and financially dangerous.

The structural reality reinforces this. The platforms that host the trenches earn from trading volume regardless of whether any coin succeeds, so the house profits from the churn itself, much like a casino. Bots and insiders routinely get the earliest, cheapest positions, leaving the human trader who arrives on a trending coin to buy from people already in profit. Creator fees and large insider holdings give those who launch and promote coins tools and motives to manufacture hype around tokens they benefit from.

The emotional culture, the FOMO, the camaraderie, the heroic self-image, is itself part of what keeps people trading through losses. None of this means the trenches are not real or that no one ever profits; some skilled and disciplined traders do, and the culture has genuine creativity and community in it. But the honest framing, shared by the more responsible voices in the space, is that the trenches function far more like a casino than like an investment market, that the odds are structurally against the individual, and that anyone entering should treat it as gambling with money they can afford to lose entirely, not as a path to wealth. The slang is fun and the stories are thrilling, but the math is brutal, and the math is what determines what happens to almost everyone who goes in.

Frequently asked questions

What does “the trenches” mean in crypto?

The trenches is slang for the chaotic, high-risk frontier of on-chain memecoin trading, especially brand-new Solana tokens on launchpads like Pump.fun. It is a war metaphor: to be in the trenches is to trade coins that are minutes old, in the fastest and most unforgiving part of crypto, against opponents that include automated bots. The term refers to both a phase, the earliest and riskiest stage of a token’s life, and a place, the launchpads, exchanges, and chat groups where this trading happens. Memecoin-focused chat channels are themselves often called the trenches. The phrase has spread to mean the early high-risk stage of any speculative crypto play. In practice, though, its strongest association remains Solana memecoin trading, because Solana’s speed, low fees, and launchpad culture created the conditions where the slang took hold. It is less a formal market category than a cultural label for the most chaotic edge of on-chain speculation.

Who are “trenchers” and “degens”?

Trenchers are the traders who operate in the trenches, buying and selling brand-new memecoins. Degen, short for degenerate, is a closely related term that trenchers wear as a badge rather than an insult; it describes someone who takes large speculative risks, does minimal research, and embraces gambling openly. The culture is built around this identity: a self-image of risk-taking warriors hunting for the one coin that pays for all the losses. There is real camaraderie and folklore among them, a shared language and value system. That social identity is part of what makes the trenches compelling and part of what keeps people trading even as the structure causes most of them to lose money over time. It gives the activity a story larger than the trade itself. The danger is that the story can make repeated losses feel like proof of toughness rather than evidence that the odds are bad.

Where do the trenches actually happen?

On-chain, primarily on Solana. The trenches live on launchpads, above all the dominant Solana launchpad, where anyone can deploy a token in seconds and it trades instantly against a bonding curve, and on the decentralized exchanges where tokens move after they graduate. They also live in social channels, especially memecoin-focused chat groups that are themselves called the trenches. The infrastructure is built for speed, with specialized tools and bots that let traders buy within seconds of a launch and read on-chain data in real time. Solana became the heartland because its very low fees and fast transactions make it cheap and quick to launch and rapidly trade coins, which is exactly what the high-churn memecoin culture needs. The chain’s infrastructure makes small, fast trades economically possible in a way that would be harder on more expensive networks. That is why the trenches are as much a product of technical design as they are of internet culture.

What does “stimmy” mean, and other common slang?

A stimmy is slang, adopted from stimulus payments, for handing money to traders; it entered wide use when an influencer pledged to airdrop fees to the trenches. Other core terms include ape, to buy impulsively without research; snipe, to buy in a launch’s first moments, usually with a bot; rug, a scam where the creator collapses the price; CTO, a community takeover of an abandoned coin; jeet, a derisive term for someone who panic-sells; whale, a holder big enough to move the price; bags, the tokens you hold; alpha, valuable insight; and FOMO and FUD, the fear of missing out and the fear and doubt that drive buying and selling. The vocabulary evolves constantly, but these form its durable core. The slang matters because it does more than describe trades. It builds identity, signals belonging, and compresses complex market behavior into quick phrases that move through chats fast. Understanding it helps you follow the culture, but it should not make the activity seem safer than it is.

Can you actually make money in the trenches?

Some people do, but the odds are structurally against the individual, and most participants lose money. The data is stark: roughly two of three Solana memecoins are effectively dead within a day, and 80% or more lose over 90% of their value within about a week, while the overwhelming majority of launchpad tokens are scams, pump-and-dumps, or jokes. The life-changing gains that fuel the folklore are real but extremely rare, and they create survivorship bias because the countless losses are invisible. Bots and insiders get the earliest positions, platforms profit from the churn regardless of outcomes, and creator fees give promoters motives to manufacture hype. Skilled, disciplined traders exist, but the structure resembles a casino more than an investment market. The rare wins are easy to screenshot and share, while the typical losses disappear into wallet history. That imbalance is exactly why the romance of the trenches can be so misleading.

Is trading in the trenches a good idea?

This guide does not recommend it, and the honest framing is that the trenches function far more like a casino than an investment market, with the odds structurally against the individual participant. The platforms profit from trading volume regardless of whether coins succeed, bots and insiders take the best positions, and most tokens are designed to extract money from latecomers. The culture’s camaraderie and heroic self-image are genuine and are also part of what keeps people trading through losses. If someone chooses to participate anyway, the only responsible approach is to treat it strictly as gambling, risking only money they can afford to lose entirely, verifying contracts and holder concentration, and never mistaking the rare success stories for the typical outcome. That means treating every new coin as hostile until proven otherwise. It also means understanding that speed, information, and discipline matter, but even those do not erase structural disadvantages. The safest way to learn the trenches is as a culture and a warning before treating it as a trading venue.

This article is educational information about crypto culture, not financial advice or encouragement to trade memecoins. Descriptions of trenches culture, slang, and failure statistics reflect reporting available as of June 29, 2026, and can change. Memecoin trading is extremely high-risk, resembles gambling, and causes most participants to lose money. Verify any specific token or platform independently and consult a qualified professional before making any financial decision.

Singapore-based Bitcoin mining pool Poolin and two of its US affiliates filed for Chapter 11 bankruptcy in a New Jersey court on Wednesday.

Poolin’s court filing shows that the mining pool operator has estimated liabilities of $100 million to $500 million, assets of $1 million to $10 million and 10,001 to 25,000 creditors.

Poolin and its affiliates are also seeking court approval to sell two West Texas mining sites to Thor CALAP LLC under a proposed $52 million stalking-horse bid. This includes $37 million for the Tarbush assets, including assumed liabilities, and $15 million for the Pyote site, including the power rights, equipment and all other assets tied to the mining facilities.

The proposed sale would be subject to a court-supervised auction, with a bid deadline of Sept. 8 under the proposed bidding procedures.

Poolin was once the world’s largest Bitcoin mining pool in 2019. It now ranks as the 17th largest mining pool operator by hashrate, with a 0.2% market share, according to Hashrate Index.

Related: Hobby-level miner bags $200K solo BTC block with budget Bitaxe rig

Bitcoin miners increasingly turn to restructuring and AI

Bitcoin mining operations are facing growing financial constraints due to rising electricity costs, forcing some operations to shut down while others are seeking new revenue sources.

In February, NFN8 Group and two of its affiliates filed for Chapter 11 bankruptcy in the Western District of Texas.

Other miners have sought to diversify into AI infrastructure. In November 2025, Bitfarms initiated a complete wind-down of its Bitcoin mining operations to pivot to AI and high-performance computing data centers.

On Monday, Bitcoin mining companies Hut 8 and IREN announced major AI infrastructure deals. Hut 8 announced a 15-year, $9.8 billion lease for its AI data center campus and IREN disclosed $2.8 billion in cloud services contracts with AI developers. Earlier in July, MARA Holdings announced plans to acquire a Texas site with up to 2 gigawatts of capacity to expand its AI and digital infrastructure business.

Wealth management company Bernstein said that deals with third-party providers, such as Bitcoin miners, will be necessary for AI companies seeking to address the computing power limits of AI data centers.

Magazine: Bitcoin nearing late stages of bear market: Jamie Coutts, Real Vision

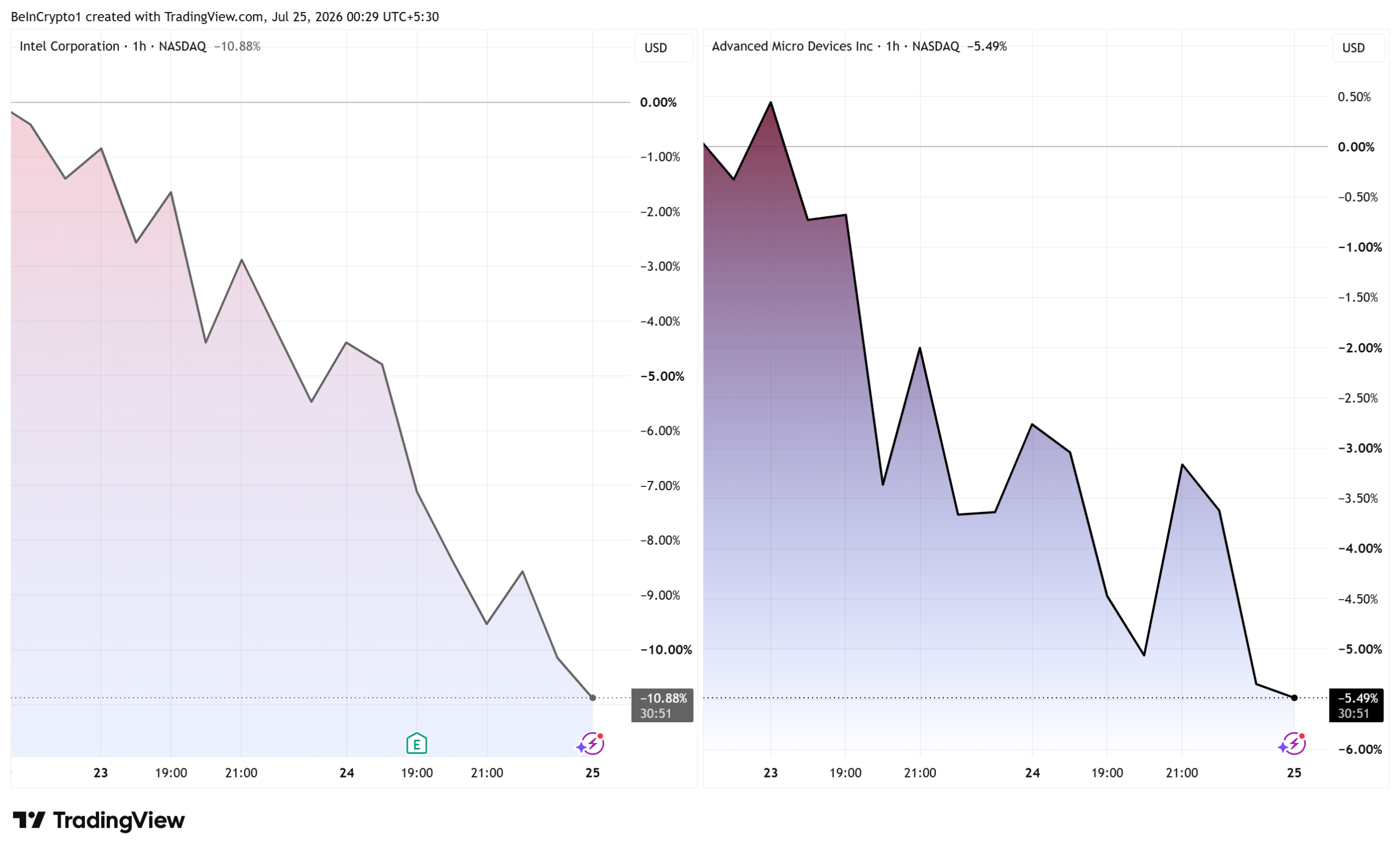

Intel beat revenue forecasts by $1.7 billion and posted its best growth in over fifteen years. The stock fell 11% anyway.

AMD had good news of its own and fell 5.5% too. When both drop at once, the cause is usually money leaving the sector.

Intel Stock Fell Through Its Own Earnings Beat

Intel reported revenue of $16.1 billion, up 25%. Analysts had expected $14.42 billion. Its data center and AI unit grew 59% to $6.3 billion. Adjusted earnings hit 42 cents a share.

Our Q2 results represent our strongest revenue growth in more than fifteen years…,” said Lip-Bu Tan, Intel chief executive, in the earnings release.

Finance chief Dave Zinsner went further, promising more spending on factory equipment and materials. Then the selling started. Intel has dropped 10.88% since the results landed.

Its RSI, a momentum gauge, sits at 29.07. Readings that low point to heavy selling.

AMD Fell Too, on Opposite News

AMD had momentum going in. It had just pledged 2 gigawatts of chips to an Anthropic supply deal, backed by a $5 billion investment.AMD still lost 5.49%. Its RSI sits at 40.99.

The whole sector was already weak. The SOXX chip fund trades about 15.7% below its June high. Scott Rubner, head of equity derivatives strategy at Citadel Securities, called it a rare chip signal.

The Inverse Cramer Effect Does Not Scale

Cramer posted “Intel’s the one” after the results. The inverse-Cramer allusion followed.

The research says the opposite. A Management Science study found his picks jump 2.4% overnight on average. Those gains then fade over the following months. The effect is strongest in small stocks that are hard to trade.

Size is the catch. That average move was worth $77.1 million. Intel lost 10.88%.

Cramer had also dumped tech before earnings. He turned cautious on the whole market that morning.

“I’m struggling to have reasons to buy, and I certainly have a lot of reasons to sell,” Jim Cramer said.

He blamed oil, interest rates, and the Middle East. Not chips. The 10-year Treasury yield hit its highest level since January.

Monday’s open will settle it.

The post Intel Beat Earnings by $1.7 Billion and Fell 11% as Cramer Turned Bullish appeared first on BeInCrypto.

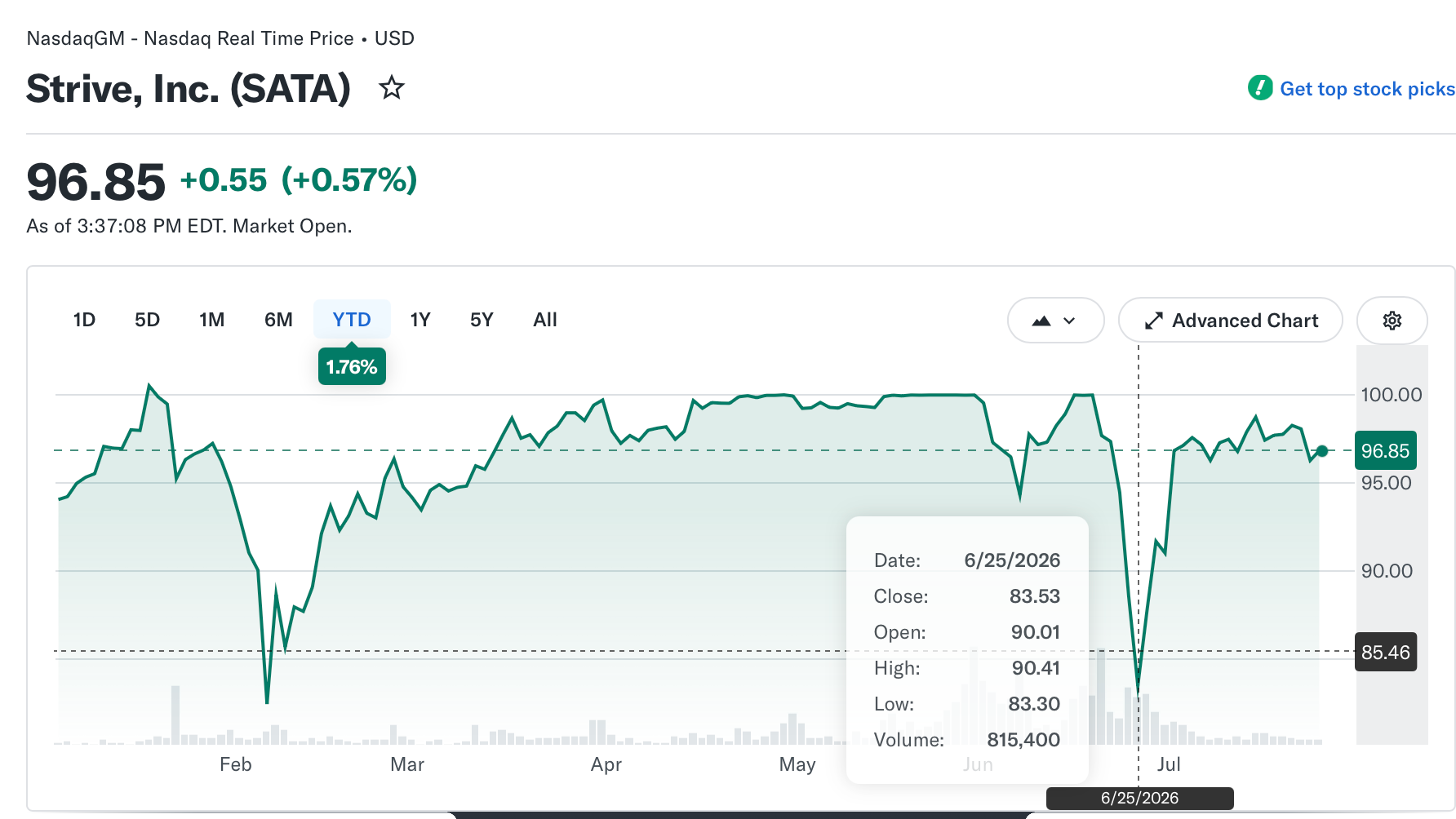

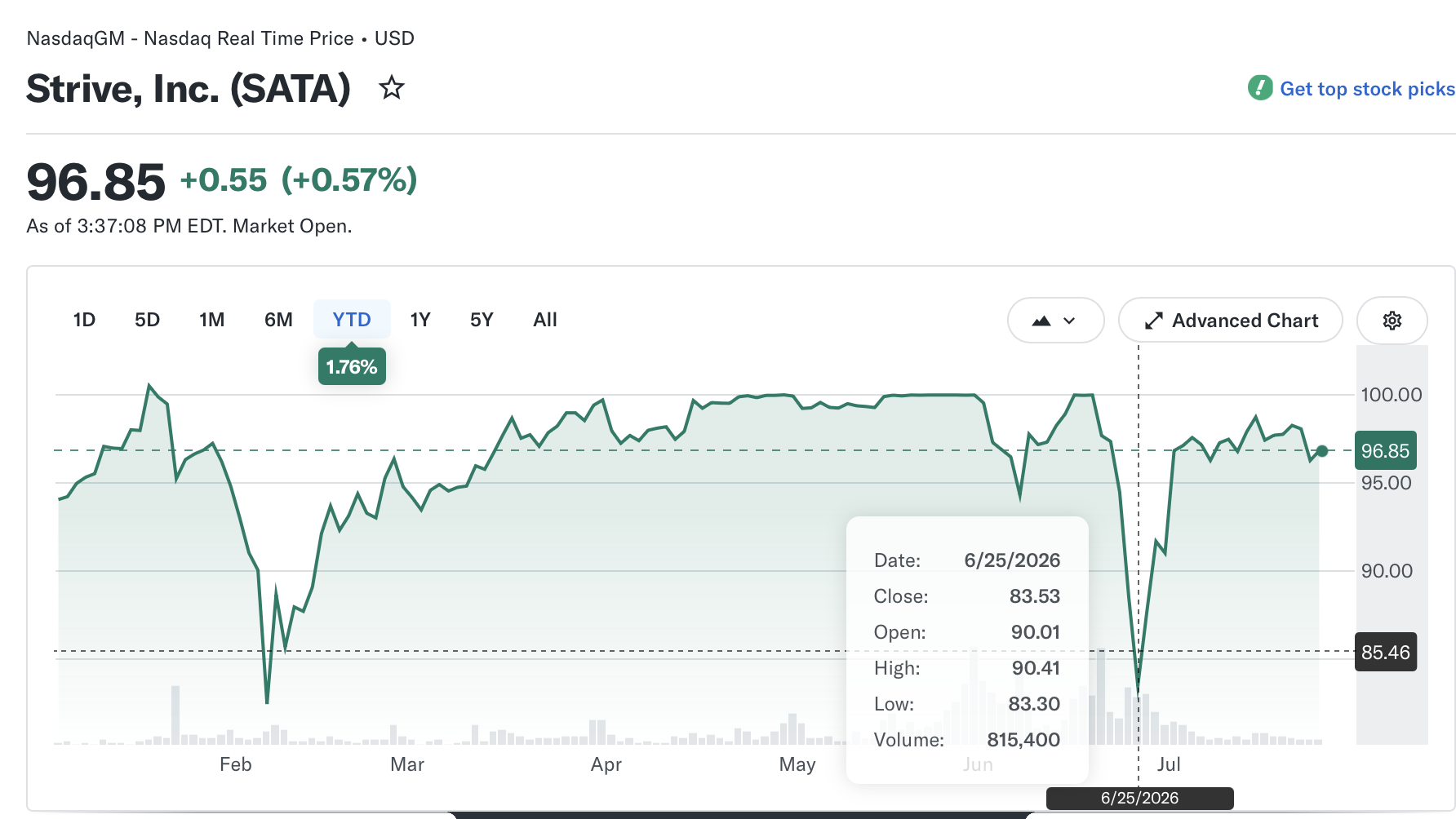

Strive’s SATA preferred shares have rebounded from a June low of $83.30 to about $97, recovering most of the selloff and moving back within roughly 3% of their $100 par value, according to Yahoo Finance data.

Strive introduced SATA in November 2025 as part of its strategy to finance the expansion of its Bitcoin treasury through preferred equity. The variable-rate perpetual preferred stock is intended to trade near its $100 par value by adjusting its dividend rate, allowing Strive to raise capital for its Bitcoin (BTC) treasury without issuing additional common shares.

SATA is one of a growing number of preferred-share products tied to Bitcoin treasury strategies, an emerging segment that companies such as Strategy describe as “digital credit.”

Strategy’s STRC, launched in 2025 with a similar objective of maintaining a $100 share price through a variable dividend, also fell sharply during the late-June selloff before recovering, though it continues to trade below par at around $87.

SATA year-to-date price chart. Source: Yahoo Finance

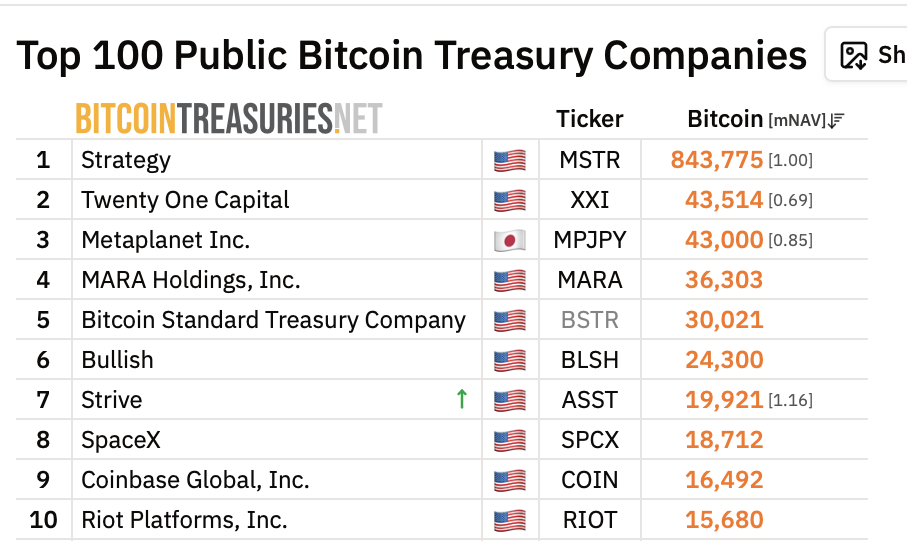

While Strategy remains the world’s largest public corporate Bitcoin holder with 843,775 BTC, Strive has climbed to seventh place with 19,921 BTC, according to BitcoinTreasuries.NET.

Top 10 Bitcoin treasury companies. Source: BitcoinTreasuries.NET

Related: Strategy raises $263.5M through MSTR sales, holds 843,775 Bitcoin

SATA recovery could help lift Strategy’s STRC, says Mow

Jan3 founder and CEO Samson Mow told Cointelegraph that recent adjustments by Bitcoin treasury companies are beginning to restore confidence in preferred-share products, supporting his view that Bitcoin has already found its bottom.

“I think every action that Strategy has undertaken to strengthen their balance sheet and encourage STRC to go back to par is also working,” Mow said, adding:

But everything sort of works in tandem. I think as SATA returns to par, you’re going to see STRC return to par too, because people say, ‘OK, this model’s not broken.’ Everyone is capitalized for three or more years of dividend payments… there was no reason to panic all along.

Mow said the improving performance of preferred-share products is part of a broader shift in the Bitcoin treasury sector, where companies have continued refining their capital-raising strategies.

He pointed to Lyn Alden’s Orange Juice treasury company, which launched on July 15 with plans to operate a Bitcoin treasury, as another example of firms entering the market with different approaches and a lower Bitcoin cost basis.

Samson Mow interview with Cointelegraph. Source: Cointelegraph

Magazine: A quantum roadmap would push Bitcoin much higher: Charles Edwards

Ripple, a blockchain-focused fintech company, has launched Ripple Mint, a platform that gives institutions new ways to access, mint, redeem and manage its US dollar-pegged stablecoin, Ripple USD (RLUSD).

The company announced Ripple Mint on Thursday, describing it as a unified platform that lets institutions manage RLUSD through a web interface or direct application programming interface (API) integrations.

“Ripple Mint is built to give institutions flexible access to digital dollars through the workflows that fit their needs,” Ripple said, adding that the platform is designed to support both manual operations and automated integrations as institutions adopt stablecoins for payments, trading and treasury activities.

RLUSD launched in December 2024 with a focus on institutional use, although the stablecoin has also gained traction among retail users. The token has grown into one of the larger US dollar-based stablecoins by market capitalization, reaching the top 10 less than one year after launch.

The token reached its all-time high market capitalization on June 1, 2026, when it surpassed $1.8 billion, according to CoinGecko. Around the Ripple Mint launch, RLUSD’s market cap briefly rose from about $1.54 billion to $1.64 billion before settling near $1.59 billion.

At the time of publication, RLUSD ranked as the ninth-largest USD-pegged stablecoin by market capitalization.

Related: Kakao taps Circle to explore won stablecoin payment infrastructure

The US House of Representatives has passed the Stop Insider Trading Act, a bill aimed at preventing members of Congress and their immediate families from buying publicly traded stocks. The measure cleared the House on Wednesday by a vote of 232–198 and now heads to the Senate for consideration.

Sponsoring Republican Representative Bryan Steil said the legislation is designed to stop lawmakers from profiting from potential insider information and to set penalties for violations. The bill would next be reviewed by the Senate, where key critics argue it still leaves room for conflicts of interest.

Key takeaways

- The House approved the Stop Insider Trading Act in a 232–198 vote, moving the proposal to the Senate.

- Under the bill, Congress members and their spouses and dependent children would be barred from purchasing publicly traded stocks.

- Penalties described by the bill sponsor include a $2,000 fine or 10% of the transaction, plus disgorgement of profits.

- Democratic lawmakers have criticized the bill for allowing members to keep and sell stocks already owned, arguing it does not fully solve the underlying conflict risk.

- Separate from the insider-trading effort, Steil is also linked to legislation addressing prediction market trading by public officials.

House passage and the bill’s penalty structure

According to the House vote results, the legislation advanced on Wednesday after the chamber approved Steil’s bill HB 7008, according to the official Congress.gov record. Steil, speaking on the House floor, framed the measure as a first for the current House on the specific issue and emphasized enforcement.

In describing how violations would be punished, Steil highlighted a penalty that includes a fine of $2,000 or 10% of the transaction, along with disgorgement of profits. He also stated that violators would forfeit gains if they failed to comply with the legislation’s requirements.

The bill’s practical aim is to reduce the possibility that lawmakers could benefit from non-public information gained through their roles. That intention is central to why supporters see the act as a meaningful guardrail against insider trading.

Criticism over “loopholes” and stock ownership rules

Even as the bill cleared the House, criticism emerged quickly from Democrats who argue it does not go far enough to eliminate conflict-of-interest concerns.

Representative and Senate critic Senator Elizabeth Warren said on Thursday that the legislation contains major loopholes because lawmakers could still own and sell stocks. Warren’s concern is that allowing ongoing ownership and sale—rather than an outright ban—may not sufficiently address the risk that creates incentives around insider information.

Steil responded to part of that critique by describing a compliance mechanism for members who already hold stocks. He said the bill would require a seven days’ notice before selling assets that lawmakers already own, arguing the notice requirement would deter trading driven by private information.

It remains to be seen how the Senate will treat these competing positions. In practice, the question will likely be whether the seven-day notice and penalties are viewed as adequate deterrence or whether senators will push for a stricter model—such as extending the restrictions beyond purchases to broader ownership rules.

What’s next in the Senate

After House passage, the Stop Insider Trading Act was received in the Senate for consideration on Thursday. The outcome in the upper chamber may hinge on whether enough senators support the bill’s narrower scope—aimed at members of Congress rather than other senior federal officials.

As described in the source, Steil’s measure is limited to restricting investments for members of Congress and does not cover the president or vice president and their families. That distinction matters for how this proposal fits into a broader debate about public official ethics and whether restrictions should be uniform across top executive and legislative roles.

In contrast, the source notes that a separate Senate proposal—associated with the Digital Asset Market Clarity Act—has included restrictions reaching public officials more broadly, including language that would bar certain officials from issuing or sponsoring tokens until 2029. While that crypto-market structure bill is distinct from the stock-trading measure, it illustrates how ethics and market-related restrictions are being considered across different legislative packages.

Link to prediction market trading legislation

The House action on insider stock trading arrives after Steil sponsored another related effort focused on prediction markets. The source reports that Steil previously backed the Stop Lawmakers from Predicting Act, introduced in June to prevent certain public officials, their spouses, and children from “wagering on public policy issues and political outcomes.”

That proposal drew attention amid real-world incidents highlighted in earlier coverage. The source points to an alleged episode involving a soldier who reportedly placed more than $400,000 betting on Venezuela President Nicolás Maduro on Polymarket, as well as reports that a teleprompter operator for former President Donald Trump allegedly made more than $100,000 betting on Kalshi event contracts connected to words and phrases in speeches.

While these examples are not about Congress members trading on stocks, they reflect the same underlying theme: lawmakers and political insiders face special scrutiny when bets can appear tied to information advantage or influence. In that context, the prediction markets proposal mirrors the stock bill’s penalty framing, including a $2,000 fee or 10% of the value of prohibited bets on the relevant platforms.

Investors and builders in crypto markets may see this as part of a wider regulatory pattern: legislators are increasingly testing whether restrictions should reach political actors using financial rails that operate outside traditional stock exchanges, even when the mechanism is “betting” rather than buying equities.

As the Stop Insider Trading Act moves through the Senate, the key uncertainty is whether senators will accept the bill’s approach—bans on new purchases with notice requirements for existing holdings—or push for stricter rules that would go further on ownership and trading.

The US House of Representatives has passed a bill that would ostensibly prohibit members of Congress, their spouses and dependent children from purchasing publicly traded stocks.

In a 232-198 vote in the House on Wednesday, lawmakers approved the Stop Insider Trading Act, sending the bill to the Senate for consideration. Representative Bryan Steil, the Wisconsin lawmaker who sponsored the bill, said that the legislation “ensures no lawmaker can profit off of insider information” and “institutes strict penalties for any violation.”

“We have not had a bill on the House floor on this topic with this opportunity before,” said Steil from the House floor on Wednesday, describing the penalties:

“A fine equal to $2,000 or 10% of the transaction, as well as a disgorgement of profits. Violators would be forfeiting any gain realized if they failed to comply with this legislation.”

Some Democrats are saying that the bill does not go far enough to address potential conflicts of interest, because it allows lawmakers to keep and sell stocks they already own. According to Steil, the bill would require members of Congress to provide seven days’ notice before selling stocks if they already hold assets, creating a deterrent for insider trading.

Related: Only KYC can stop insider trading on prediction markets, Messari says

“[The] bill has major loopholes,” said Senator Elizabeth Warren on Thursday. “Lawmakers can continue owning and selling stocks — so it won’t solve the problem. Not gonna fly in the Senate. Members of Congress should not own, buy, or sell stocks.”

The Stop Insider Trading Act was received in the US Senate for consideration on Thursday after passage in the House.

Unlike the proposed text for the Digital Asset Market Clarity Act, a cryptocurrency market structure bill under consideration in the Senate, Steil’s bill was limited to restricting investments for members of Congress and not the president or vice president and their families. Under CLARITY’s proposed text, all US public officials could be barred from issuing or sponsoring tokens until 2029.

Prediction markets bill also under consideration

House approval of the Stop Insider Trading Act followed Steil’s sponsorship of a similar bill targeting members of Congress trading on prediction market platforms like Kalshi and Polymarket. The Wisconsin lawmaker introduced the Stop Lawmakers from Predicting Act in June to prevent certain public officials, their spouses and children from “wagering on public policy issues and political outcomes.”

Prediction markets drew attention from the public after an incident involving a soldier who allegedly made more than $400,000 betting on Venezuela President Nicolás Maduro, who was removed by US forces in January. Donald Trump’s teleprompter operator also reportedly made more than $100,000 betting on Kalshi event contracts tied to words and phrases in the president’s speeches.

Like the stock trading bill, the prediction markets legislation proposed that violators pay a $2,000 fee or 10% of the value of the prohibited bets on the platforms.

Magazine: Why Wall Street values some crypto firms for AI power, not just crypto

World Foundation, the nonprofit behind the World protocol, has raised an initial $52.5 million by selling locked WLD tokens to strategic investors, with Pantera Capital leading the round. The fundraising—announced on Friday and shared with Cointelegraph—adds fresh capital to World’s push to scale World ID, its biometric-based system for helping platforms verify whether an online user is a real person.

According to the announcement, the WLD tokens sold in the round are subject to a 12-month lockup. Other participants reportedly include Bain Capital Crypto, Eightco Holdings, Selini Capital, and Susquehanna Crypto, alongside additional investors.

Key takeaways

- $52.5 million raised through a sale of locked WLD tokens, with Pantera Capital leading.

- The sold tokens come with a 12-month lockup, limiting immediate liquidity from the strategic investors.

- World Foundation says new funding will go toward expanding World ID, its biometric credential system for distinguishing humans from AI agents.

- World ID relies on users completing biometric verification at a World Orb device to generate a digital credential.

- The broader market context reflects intensified investor focus on AI infrastructure and agent-era tooling, including security and verification solutions.

Locked token sale funds World ID expansion

World Foundation’s fundraising centers on WLD, the token ecosystem associated with the World protocol. In its announcement, the organization said the initial $52.5 million proceeds from the locked token sale will be used to expand World ID—a system meant to verify online identities in an era where synthetic content and automated agents are becoming more prevalent.

World describes World ID as a credential that can be issued after users complete biometric verification at a hardware point called a World Orb. Once verified, users receive a digital credential intended to help services determine that the account engaging with them is tied to a real person rather than an automated agent.

The stated motivation is practical: the nonprofit argues that demand for verification infrastructure is rising as AI-generated content and autonomous agents increase. Instead of trying to detect bots purely through behavior, the approach aims to anchor identity claims to a biometric verification step completed through the World Orb workflow.

Why verification matters as AI agents proliferate

World’s fundraising lands amid a broader shift in crypto and adjacent investment toward AI-related infrastructure and agent-first applications. That shift has been visible across multiple recent deals highlighted in Cointelegraph coverage.

For example, brokerage infrastructure provider Alpaca raised $135 million in equity financing earlier this month and reportedly secured access to up to $300 million in debt financing. The company said the funding would support infrastructure for AI-powered financial applications—an indication that agent-driven workflows are moving from experimentation toward more robust system-building.

Similarly, Cointelegraph previously reported that Coinbase introduced tools enabling businesses to accept USDC payments from autonomous AI agents. That update was framed in the context of AI-generated activity growing on its Base developer ecosystem, including a claim that AI-generated traffic exceeded human traffic on its Base developer documentation for the first time last month.

In this environment, identity and trust layers become more than a niche tooling problem. As more commerce, messaging, and platform interactions become automatable, the ability to verify whether an interaction represents a human user becomes increasingly relevant to everything from onboarding to fraud prevention to resource allocation.

Regulatory sensitivity remains part of the World ID story

World’s identity approach is not without controversy. The organization was originally conceived by Sam Altman, Max Novendstern, and Alex Blania, with World protocol efforts later drawing regulatory scrutiny in multiple jurisdictions over its biometric identity verification system.

While the current fundraising announcement focuses on scaling World ID, the mention of regulatory pressure underscores a critical uncertainty investors and builders should consider: biometric verification often intersects with privacy expectations, data protection requirements, and consent frameworks that can vary widely by jurisdiction. That reality can influence rollout speed, compliance costs, and the design of how credentials are issued and used.

For market participants, the token lockup may offer some near-term stability, but it does not resolve the core question of how World ID will navigate legal and regulatory constraints as it expands.

AI investment momentum extends to security and frontier tech

The investment climate around AI is also showing up in broader funding patterns, including cybersecurity. Cointelegraph notes that capital is increasingly flowing into AI-adjacent security efforts, with one example being AegisAI, a cybersecurity startup that raised $36 million in Series A funding to expand AI-powered email security. The company said the financing is intended to improve defenses against more sophisticated AI-generated phishing attacks.

Meanwhile, large crypto investment vehicles have been repositioning toward AI and frontier technologies. According to Cointelegraph reporting, Paradigm raised a $1.2 billion fund in July to invest across crypto, artificial intelligence, robotics, and other frontier technologies. Framework Ventures also reportedly closed a $400 million fund in June with a mandate spanning crypto, AI, robotics, and energy.

Taken together, these moves suggest a sector-wide bet: in an agent-driven future, infrastructure, trust, and security will be treated as interconnected components rather than separate silos. World ID’s biometric verification pitch fits into this larger landscape as one possible “human verification” layer for systems confronting rising automation.

Looking ahead, the key question for readers is how quickly World Foundation can scale World ID beyond its initial verification workflow while maintaining compliance in the jurisdictions that have already scrutinized biometric identity verification. With AI agents becoming more common—and platforms increasingly adapting payment and interaction tools for them—investors and builders should watch for concrete adoption milestones for World ID and any updates on regulatory posture as World expands.

The company announced the launch of a new platform, dubbed ‘Ripple Mint,’ that gives institutional customers a single way to access, mint, redeem, and manage RLUSD.

It said the main objective is to make digital dollars easier to access, integrate, and operate at scale as stablecoins become more deeply embedded in trading, payments, and treasury operations.

Pushing RLUSD’s Institutional Reach

According to the official blog post, Ripple Mint expands RLUSD access beyond traditional platform-based workflows by allowing institutions to manage the stablecoin either through a user interface or through programmatic integrations.

With Ripple Mint, institutions can mint and redeem RLUSD directly from the issuer, bridge the stablecoin across supported blockchains, monitor funds throughout the full transaction lifecycle, and integrate RLUSD operations into their own internal systems and workflows.

The rollout will not affect existing customers of the stablecoin, who will now be able to use the platform for both manual operations and automated integrations. The company has also introduced new APIs and webhook notifications that allow customers to automate RLUSD workflows, query transaction status throughout the minting and redemption process, access account balances programmatically, and receive real-time updates on important events such as fiat receipt, mint processing, on-chain settlement, and payout completion.

Alongside the launch of Ripple Mint, Ripple also made a strategic investment in Notabene, a company focused on regulated on-chain transaction infrastructure.

The two companies said they will work together to grow enterprise stablecoin payments by integrating RLUSD into Notabene Flow, the firm’s B2B stablecoin payments platform. The focus will also be on exploring how trusted payment authorization can complement Ripple Payments.

The partnership combines Ripple’s enterprise payments ecosystem and RLUSD with Notabene’s institutional network, which reportedly spans more than 2,300 connected institutions across over 100 jurisdictions, serves more than 280 customers, and facilitates more than $2 trillion in annualized transaction volume.

Expansion

Ripple’s RLUSD has continued to expand its presence since launching and now has a market capitalization of nearly $1.6 billion. Last August, Ripple partnered with Japan’s SBI Holdings to distribute the stablecoin in the country through SBI VC Trade starting in the first quarter of 2026.

In March 2026, the company joined the Monetary Authority of Singapore’s BLOOM initiative with Unloq to test RLUSD and the XRP Ledger for programmable cross-border trade settlement.

A month later, OKX listed the stablecoin to expand its global access, liquidity, and trading utility. More recently, it was also included in Mastercard’s expanded stablecoin settlement program.

The post Ripple Doubles Down on RLUSD With Mint Launch and Notabene Investment appeared first on CryptoPotato.

Depending on the scale you are looking at BTC, you can determine that the asset is either almost 50% away from its all-time high or it’s actually millions of percentages above its price observed a decade ago.

From a technical perspective, the current $65,000-$66,000 region could actually mean that there’s a massive opportunity on the table, at least according to popular analyst Crypto Rover.

… Like Buying at $2

The analyst outlined a specific chart to his 1.6 million followers on X that uses a long-term logarithmic regression curve to claim that the cryptocurrency’s price has followed a predictable upward trajectory for over a decade with little deviation. The green markers show historical touchpoints after which the asset went on a massive run as its price continued along the curve.

Some of the previous instances where it touched the lower level included $2 over a decade ago, $10, $200, $3,500, and, most recently, $16,000, during the bear cycle in 2022. Each of those was followed by tremendous rallies that led to subsequent all-time highs.

Rover’s chart now argues that BTC’s current range at $65,000-$66,000 means the asset has slipped into this same familiar territory, suggesting it’s a comparable ‘on-curve’ entry point rather than an overextended top. Consequently, he concluded that buying BTC now is “no different from buying it at $16,000, $3,500, $200, $10, or even $2,” implying similar long-term upside potential relative to the historical growth path.

WOW: According to this Bitcoin chart, buying Bitcoin at $66K is no different from buying it at $16K, $3.5K, $200, $10, or even $2. pic.twitter.com/cFpLOQ5K8n

— Crypto Rover (@cryptorover) July 24, 2026

What About the Bottom?

Debating whether BTC’s bottom is already in or not has been most analysts’ favorite topic in the past several months. Jelle also weighed in on the matter today, indicating that the asset is still working on it, with its price now “turning the previous local consolidation into support.” He predicted another leg up to fill a void left at $70,000 soon. However, that resistance level could become too strong for the rather minimal bullish sentiment now, he warned.

Michaël van de Poppe noted that the cryptocurrency has dipped into the “oversold territory on the Puell Multiple.” History shows that similar occasions in the past have led to the bottom formation “shortly after,” such as the bear cycles in 2015, 2018, 2020, and 2022.

The popular analyst predicted that this time it “won’t be different,” as BTC prepares for a more profound leg up. For now, though, its upside rallies have been halted at inception levels.

The post Buying Bitcoin Today Is Like Buying It at $2, Says Analyst appeared first on CryptoPotato.

Jack Mallers says Bitcoin’s bear market has left him “getting my ass kicked,” but the Strike founder believes that is exactly what makes the asset different from traditional financial systems.

In an essay published Friday, just days after stepping down as CEO of Twenty One Capital, Mallers argued that Bitcoin’s painful downturns expose reality instead of hiding it.

Mallers Says Bitcoin’s Pain Has a Purpose

Mallers wrote that he originally drafted the essay on July 11, before resigning from Twenty One Capital, intending to publish it the following Monday. That plan changed after he was told to wait until his departure became public.

In the opening note, he acknowledged that the company he believed he was building and the direction it ultimately took “were no longer the same,” leading him to step away. He also accepted responsibility for helping create expectations that “were not ultimately fulfilled,” while making clear that the essay was not intended as a defense of his decision.

Instead, Mallers used Bitcoin’s latest bear market as a lens through which to examine leadership, conviction, and failure. Although BTC is trading almost 50% below its all-time high, he argued that the emotional toll extends far beyond financial losses.

“I am not writing this from the peaceful other side of the storm,” he wrote. “I am still in it.”

Drawing a contrast with traditional finance, Mallers said governments, banks, and institutions frequently soften the consequences of poor decisions through interventions such as bailouts and refinancing. Bitcoin, by comparison, refuses to do that.

“The world I am used to keeps trying to protect me from the lesson,” he noted. “Bitcoin does not.”

He described volatility as information rather than weakness, maintaining that price swings expose excessive leverage, poor decisions and fragile business models instead of concealing them.

Bear Markets Expose Weakness, They Don’t Create It

Looking back at the collapse of FTX in 2022, the former Twenty One CEO contended that BTC did not create the fraud, as the bear market simply removed conditions that had allowed weak businesses and unsustainable leverage to survive.

He also admitted that previous bull markets had shaped his own behavior. Reflecting on product announcements made during the 2022 Bitcoin Conference, Mallers wrote that he had started confusing “attention for proof of work” and “vision for execution,” calling the admission one of the hardest sentences he had written.

His resignation from Twenty One became another example of that same lesson. While declining to explain every detail behind his departure, Mallers said the experience forced him to test whether the principles he had spoken about publicly were genuine when faced with easier alternatives.

His comments come amid ongoing debate as to whether Bitcoin’s bear market has already bottomed out. Some analysts, including those from Grayscale, say the macroeconomic conditions are more important now than the classic four-year cycle. However, others still expect one last dip before a sustained recovery.

But Mallers didn’t spend a lot of time predicting prices, with his argument being much simpler: the discomfort of a bear market is precisely what keeps Bitcoin honest.

The post After Twenty One Exit, Jack Mallers Says Bitcoin Taught Him Hard Lessons appeared first on CryptoPotato.

Bitcoin Miner Poolin Files for Chapter 11 Bankruptcy

Blue Jays’ Addison Barger to have season-ending elbow surgery

VentureBeat Research: Where enterprise AI agent governance hasn’t caught up

-

Politics6 days ago

Politics6 days agoThe House | The City of London can help the new chancellor deliver growth in every postcode

-

Crypto World6 days ago

Crypto World6 days agoRipple Payments Joins MiCA With 14 Firms, Does It Mean Anything For XRP?

-

Politics5 days ago

Politics5 days agoDemocrats look to World Cup watch parties to register thousands of voters

-

Fashion4 hours ago

Fashion4 hours agoWeekend Open Thread: Brooks Brothers

-

Crypto World7 days ago

Crypto World7 days agoRipple wins EU-wide access as ESMA adds it to MiCA register

-

Crypto World4 days ago

Crypto World4 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

Tech4 days ago

Tech4 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

NewsBeat4 days ago

NewsBeat4 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Tech4 days ago

Tech4 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

News Videos5 days ago

News Videos5 days agoBig Money Is Entering XRP

-

Business3 days ago

Business3 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Crypto World6 days ago

Crypto World6 days agoKaspersky exposes OkoBot’s 20-module crypto wallet attack

-

Entertainment3 days ago

Entertainment3 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

NewsBeat7 days ago

NewsBeat7 days agoDurham County Council to send out electoral registration emails

-

Crypto World2 days ago

Crypto World2 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Crypto World7 days ago

Crypto World7 days agoMiCA Licensing Faces Delays as ESMA Adds 14 CASPs to Register

-

NewsBeat4 days ago

NewsBeat4 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Crypto World6 days ago

Crypto World6 days agoChip Stocks Enter Bear Market After Moonshot Ai Unveils Kimi K3 Model

-

Tech4 days ago

Tech4 days agoWatch Flock Safety CEO Garrett Langley discuss the future of surveillance at TechCrunch Disrupt 2026

-

Tech5 days ago

Tech5 days agoSubway Sandwich Computers Get a Second Life as Gaming Machines

You must be logged in to post a comment Login