Crypto World

What is a mempool? Crypto’s transaction waiting room

![]()

You press send on a crypto transaction and nothing happens. The wallet says pending. The block explorer shows your transaction floating in limbo, unconfirmed, with no clear indication of when, or whether, it will land.

Most people meet the mempool for the first time in exactly this moment of mild panic, and most of the advice they find assumes they already know what a mempool is. This guide starts from zero.

The mempool, short for memory pool, is the waiting room where every blockchain transaction sits between the moment you broadcast it and the moment a miner or validator writes it into a block. It is one of the least glamorous components of a public blockchain and one of the most consequential. The mempool decides how much you pay in fees, how long you wait, and, on some networks, whether a trading bot gets to see your order before it executes and profit at your expense. Understanding it turns confirmation delays from a mystery into a readable market signal.

This guide explains what the mempool actually is, why blockchains need a waiting room at all, how transactions move through it step by step, how fee markets decide who gets confirmed first, why there is no single mempool but thousands of slightly different ones, what happens when the queue overflows, how the mempool became the hunting ground for extractive trading bots, why Solana took the radical step of removing the public mempool entirely, and what practical steps you can take when your own transaction gets stuck.

What a mempool actually is

A mempool is a database of unconfirmed transactions that every full node on a blockchain network maintains in its working memory. When you sign a transaction in your wallet and hit send, the transaction does not travel to some central server for processing, because no such server exists. Instead, your wallet hands the signed transaction to a node, and that node begins spreading it to its peers, who spread it to their peers, until most of the network has a copy. Each node that receives the transaction runs a series of checks and, if the transaction passes, places it in its local mempool to wait.

The word itself is a contraction of memory and pool, and the memory part matters. Nodes keep the mempool in RAM instead of writing it to disk, because speed is the point. When a miner assembles a candidate block, it needs to sort thousands of pending transactions by fee and select the most profitable set in a fraction of a second. When a new block arrives from elsewhere on the network, a node can validate it faster if most of the block’s transactions are already sitting in its own mempool, checked and ready.

The mempool is a staging area, a buffer between the chaotic, continuous stream of user activity and the rigid, periodic heartbeat of block production.

Why blockchains need a waiting room

A traditional payment processor confirms transactions the instant they arrive because a single company controls the ledger and can simply write the entry. A public blockchain has no such authority. Thousands of independent nodes must agree on a single history, and they reach that agreement in discrete steps, one block at a time. Between blocks, the network needs a shared, informal picture of what users want to happen next, and the mempool provides it.

The waiting period also does critical security work. Before a node admits a transaction to its mempool, it verifies that the digital signature is valid, that the sender actually controls the funds being spent, that the transaction is correctly formatted, and that the same coins are not being spent twice. This last check matters more than it sounds. It is entirely possible for two conflicting transactions, both spending the same coins, to enter the network at the same time from different points. Some nodes see one first, some see the other. Each node rejects whichever conflicting transaction arrives second, and the conflict is finally settled when a miner includes one of the two in a block. The mempool is where these races are held and resolved.

The mempool also functions as the network’s early warning system. A rapidly filling mempool signals a surge of demand, a panic, an airdrop claim window, or a fee spike before any of it shows up in confirmed blocks. Traders, miners, and wallet fee estimators all read the mempool the way meteorologists read pressure systems.

The life of a transaction, step by step

Following a single transaction through the pipeline makes the mechanics concrete. First comes creation: your wallet constructs the transaction, specifying the amount, the recipient, and the fee you are willing to pay, and signs it with your private key. The signature proves ownership without revealing the key itself.

Second comes broadcast. The wallet sends the signed transaction to one or more nodes, which begin relaying it across the peer to peer network. Propagation to most of the network typically takes a few seconds, and nothing about this step requires trust in the first node, since every subsequent node re-validates the transaction independently before passing it along.

Third comes validation. Every node that receives the transaction independently checks it. Invalid transactions, bad signatures, insufficient funds, malformed data, are dropped on the spot and never reach a mempool.

Fourth comes the wait. The transaction now sits in thousands of mempools across the network, visible to anyone running a node or using a public mempool explorer. How long it waits depends almost entirely on the fee attached relative to everyone else’s fees.

Fifth comes selection. A miner on a proof of work chain, or a validator on a proof of stake chain, assembles a candidate block by picking pending transactions from its mempool, almost always sorting by fee density so the block earns the maximum reward.

Sixth comes confirmation. The block is mined or proposed, propagated, and accepted by the network. Every node removes the block’s transactions from its mempool, and your transaction is now part of the chain. Each additional block built on top adds another confirmation and makes reversal exponentially harder.

How the fee market decides who goes first

Block space is scarce and demand fluctuates, so blockchains ration space by auction. On Bitcoin, fees are measured in satoshis per virtual byte, a unit of transaction data size, so a transaction’s fee rate depends on both what you pay and how much space the transaction occupies. On Ethereum, the fee is gas, with a base fee that the protocol burns and a priority tip that goes to the validator. In both systems the logic is identical: block producers are profit maximizers, so they fill blocks with the highest paying transactions first.

This means your position in the queue is not fixed. A transaction that looked competitively priced at noon can be hopelessly underpriced by evening if demand surges. Wallets estimate fees by reading the current mempool, looking at what pending transactions are offering and how full recent blocks have been, then suggesting a rate likely to confirm within your chosen time window. Those estimates are educated guesses, not guarantees, and they go stale quickly during volatile markets. A fee that clears in the next block during a quiet Sunday can leave you waiting hours during a liquidation cascade, because everyone else’s willingness to pay moved while yours stood still. The auction never closes, and it reprices continuously.

When you underpay, most networks offer escape hatches. Bitcoin supports replace by fee, which lets you rebroadcast the same transaction with a higher fee that supersedes the original. A related trick, child pays for parent, attaches a high fee follow up transaction that spends the stuck one’s output, giving miners an incentive to confirm both together. Ethereum wallets let you resubmit a transaction with the same nonce and a higher gas price, which replaces the pending version. Knowing these tools exist converts a stuck transaction from an emergency into an inconvenience.

There is no single mempool

People say the mempool as if one canonical queue existed somewhere, but the reality is messier and more interesting. Every node maintains its own mempool, and no two are exactly identical. Transactions reach different nodes at different times, nodes apply slightly different acceptance policies, and each node manages its own memory limits. What we call the mempool is really the loose statistical overlap of thousands of private ones.

In practice the overlap is large, because most node operators run default settings. A typical Bitcoin node caps its mempool around 300 megabytes, keeps transactions for up to two weeks, and refuses anything paying less than a minimum relay fee of roughly one satoshi per virtual byte. When the pool exceeds its size cap, the node evicts the lowest fee transactions first and raises its minimum acceptance rate, which is why very cheap transactions can vanish entirely during congestion instead of merely waiting. Once evicted everywhere, a transaction is effectively cancelled, and the funds simply remain unspent in the sender’s wallet.

The distributed nature of the mempool has a subtle consequence: pending status is not a promise. A transaction shown as pending in an explorer exists only as a claim in some nodes’ memory. It can be evicted, replaced, or double spent until it lands in a block. Merchants who accept zero confirmation payments learn this lesson the hard way, and it is exactly the mechanism a 51% attack exploits at chain level, where an attacker rewrites recent blocks and dumps the reversed transactions back into the mempool as if they had never confirmed. The 2025 reorganization attacks on Monero pushed more than one hundred confirmed transactions back into the pending queue in exactly this way.

Policy, standardness, and why nodes reject valid transactions

Consensus rules define what a blockchain will accept in a block. Mempool policy defines what an individual node will hold and relay, and the two are not the same thing. A transaction can be perfectly valid under consensus rules and still be refused by most mempools because it violates what Bitcoin developers call standardness: informal policy rules that filter dust outputs, oversized scripts, absurdly low fees, and exotic transaction shapes that could burden the network. Policy is a node level immune system, a first line of defense that keeps the shared queue usable.

This distinction produces real world confusion. A transaction rejected by public mempools can still be mined if it reaches a miner directly, which is why services exist that accept nonstandard transactions out of band and submit them straight to mining pools. It also means the mempool you observe through an explorer reflects that node’s policy, not some universal truth. Two explorers can disagree about whether your transaction is pending simply because their nodes apply different filters.

Policy also evolves faster than consensus. Nodes have tightened and loosened relay rules around data inscriptions, dust limits, and replacement behavior repeatedly over the years, each change reshaping what the pending queue looks like without touching consensus at all. For users the practical takeaway is simple: if a wallet warns that a transaction is nonstandard, the problem is usually the transaction’s construction, not the funds behind it.

The mempool also has a quieter institutional audience. Exchanges watch pending deposits to credit accounts faster, compliance teams screen incoming transactions before confirmation, and payment processors estimate risk on zero confirmation transfers by checking how well a transaction is propagating and whether any conflicting spend is circulating. A transaction that most of the network’s mempools agree on is far less likely to be double spent than one propagating poorly, and firms price that difference.

Congestion, spam, and what a full mempool feels like

Mempool congestion is the network catching its breath. Demand exceeds block space, the queue grows, and the fee needed for timely confirmation climbs. Users experience it as expensive transactions and long waits. Bitcoin’s late 2017 mania, the DeFi summer of 2020, NFT minting waves, and the ordinals inscription craze of 2023 each produced mempool backlogs measured in days, with hundreds of thousands of transactions queued and fee rates multiplying overnight. During the worst stretches, low fee transactions waited more than a week, and node operators watched their mempools hit size limits and begin shedding the cheapest traffic.

Congestion can also be manufactured. Spam attacks flood the network with masses of low value transactions to clog the queue and degrade service for everyone else, a cheap form of denial of service. Networks defend themselves with the minimum relay fee, with eviction policies, and ultimately with economics, since sustained spam costs the attacker real money in fees. The 2017 spam attack on an Ethereum test network showed how effective flooding could be against a chain with weak fee pressure, and it pushed fee market design higher up the research agenda.

Congestion is also information. A swollen mempool alongside rising fees signals urgent demand, often around exchange runs, liquidation cascades, or major market moves. Sophisticated observers watch mempool depth the way bond traders watch yields, and several analytics firms sell exactly that feed.

The dark forest: MEV and the watchers in the pool

The mempool’s defining feature, total transparency, is also its greatest vulnerability. Every pending transaction is public before it executes, which means anyone can read your intentions and act on them first. On smart contract chains this gave rise to an entire extractive industry built around maximal extractable value, or MEV, the profit available to whoever controls transaction ordering.

The canonical attack is the sandwich. A bot spots your large pending swap on a decentralized exchange, buys the same token first to push the price up, lets your trade execute at the worse price, then immediately sells for a profit carved directly out of your execution. Front running, back running, and liquidation sniping follow the same principle: see the pending transaction, position around it, capture the difference. One researcher famously described the public mempool as a dark forest, a place where anything visible gets hunted. Researchers estimate that MEV extraction on Ethereum alone has run into the billions of dollars since 2020.

The defense industry that grew in response is now substantial. Private transaction relays, such as Flashbots Protect, let users submit transactions directly to block builders, skipping the public mempool entirely so bots never see the order. Batch auction exchanges settle many trades at a single clearing price, removing the ordering advantage. Wallets increasingly route large trades through protected channels by default. None of this eliminates MEV, but it changes who can be hunted. The economics are straightforward: the value of hiding an order grows with its size, so large traders now treat mempool privacy the way traditional funds treat dark pools, as basic operational hygiene. Retail users moving small amounts face far less risk, but a single large swap through the public queue on a thin trading pair can pay a triple digit toll to a sandwich bot in a matter of seconds.

Solana’s answer: delete the mempool

Solana made the most radical design choice of any major network: it has no public mempool at all. Instead of gossiping pending transactions across the whole network, Solana’s Gulf Stream protocol forwards transactions directly to the validator scheduled to produce the next block, called the leader. The leader schedule is known in advance, so wallets and nodes know exactly where to send traffic. Transactions go from user to leader with almost no public waiting period.

The design serves speed above all, and it removes the classic observation window that sandwich bots depend on, since pending transactions are never broadcast for public inspection. It did not eliminate MEV, which instead matured into a private auction economy where searchers pay tips through infrastructure such as Jito to have their transaction bundles placed favorably by leaders. The lesson generalizes: ordering has value on any blockchain, and removing the public queue changes where that value is captured, not whether it exists.

Other networks are converging on middle paths. Encrypted mempools hide transaction contents until ordering is locked. Proposer builder separation on Ethereum splits the job of choosing transactions from the job of proposing blocks, pushing MEV into a more transparent auction. The mempool of 2030 will likely look very different from the open bazaar of 2020. What will not change is the underlying constraint: some component of every blockchain has to hold transactions between creation and confirmation, and whoever can observe or influence that component holds power over everyone who cannot.

Reading the mempool yourself

You do not need to run a node to watch the queue. Public mempool explorers visualize pending transactions, fee distributions, and projected confirmation times in real time, and they are the fastest way to answer the two questions every stuck user asks: how busy is the network, and what fee actually clears right now.

When your own transaction is stuck, the diagnosis is almost always the same: your fee is below the going rate. Your options, in rough order of preference, are to wait for congestion to ease, to bump the fee using replace by fee or a nonce replacement, to use child pays for parent where supported, or, on Bitcoin, simply to wait for eviction if the payment no longer matters. What you should not do is panic. The funds are not lost. An unconfirmed transaction either confirms or effectively ceases to exist, and in the latter case the coins never left your wallet.

It also helps to understand what explorers actually display. The fee histogram shows how much pending volume sits at each fee level, which tells you where the clearing price is right now. The projected blocks view shows which transactions would fill the next several blocks if they were produced immediately, which tells you how deep the queue runs ahead of you. And the purge line, on Bitcoin explorers, shows the fee rate below which nodes are actively evicting transactions, the effective floor of the market. Ten minutes spent learning these three readouts pays for itself the first time fees spike.

One final habit worth adopting: check the mempool before you transact, not after. Thirty seconds of looking at current fee rates saves both overpaying during quiet periods and underpaying during storms. The queue is public. Very few people bother to read it, which is exactly why the ones who do have an edge. It is the same reason a network upgrade that splits the chain, covered in our guide to hard forks and soft forks, always produces a flurry of mempool drama, as wallets and nodes on both sides of the split sort out which pending transactions belong where.

Frequently asked questions

What is a mempool in simple terms?

A mempool is the waiting room for blockchain transactions. After you send a transaction, it sits in the mempool, visible and pending, until a miner or validator includes it in a block. Every full node keeps its own copy of this queue in memory.

Why is my transaction stuck in the mempool?

Almost always because the fee attached is lower than what other pending transactions are offering. Block producers pick the highest paying transactions first, so underpriced ones wait until demand falls or until they are evicted from the queue entirely.

Can a transaction in the mempool be cancelled?

Sometimes. On Bitcoin, replace by fee lets you supersede a pending transaction with a new version, and a stuck transaction that gets evicted from all mempools is effectively cancelled. On Ethereum, you can replace a pending transaction by sending a new one with the same nonce and a higher fee.

Is there one mempool for the whole network?

No. Every node maintains its own mempool, and the contents differ slightly between nodes based on timing, settings, and memory limits. The mempool people refer to is the rough overlap of thousands of independent queues.

How long can a transaction stay in the mempool?

On Bitcoin, default node settings keep transactions for up to two weeks before dropping them, though eviction can happen sooner if the pool fills and the fee is low. Other networks have their own retention and eviction rules.

What is the connection between the mempool and MEV?

Pending transactions in a public mempool are visible before they execute, so bots can read them and trade around them, extracting value through sandwich attacks and front running. This visibility is the raw material of most MEV on chains like Ethereum.

Does Solana have a mempool?

Not a public one. Solana forwards transactions directly to the upcoming block leader instead of broadcasting them across the network, which removes the public waiting room. MEV on Solana instead flows through private bundle auctions run by infrastructure providers.

Are funds lost if a transaction never confirms?

No. A transaction that never confirms is eventually dropped from mempools, and the coins simply remain in the sending wallet as if the transaction had never been made. Nothing is deducted until a transaction is included in a block.

This article is for educational purposes only and does not constitute financial or investment advice. Network rules, fee mechanics, and default node policies change over time. Details are accurate as of July 14, 2026.

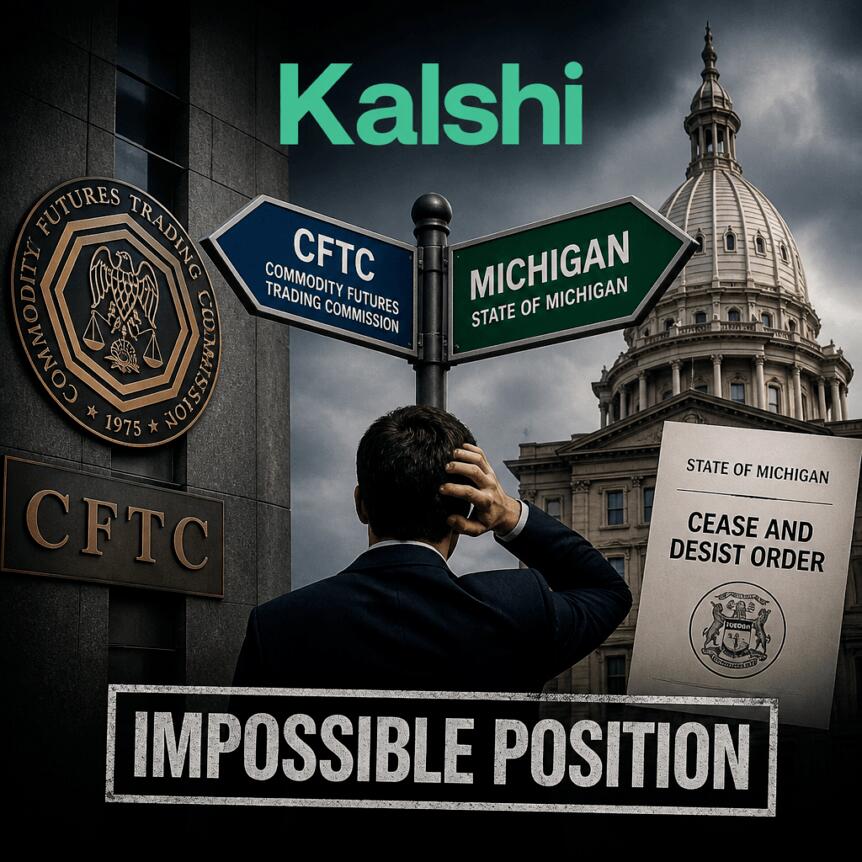

The U.S. commodities regulator has moved to prevent Kalshi, a registered prediction market platform, from reversing Michigan trades—sparking fresh legal friction between federal oversight and a state court order. The dispute centers on whether Kalshi must unwind already executed sports betting contracts for Michigan users while litigation over Michigan’s sports betting laws continues.

On Tuesday, the Commodity Futures Trading Commission (CFTC) ordered Kalshi not to comply with the Michigan order and instead continue operating. The clash follows an earlier ruling on June 29 by Ingham County Circuit Court Judge Rosemarie Aquilina, who directed Kalshi to stop offering sports betting contracts to Michigan users during the ongoing case.

Key takeaways

- The CFTC says canceling already executed prediction market trades would disrupt market certainty and create a cascading effect across derivatives markets.

- Kalshi argues the situation forces it to choose between conflicting obligations: comply with a state court directive or follow federal regulatory requirements.

- The controversy underscores an ongoing jurisdictional tension between the CFTC and multiple state regulators regarding prediction markets.

- CFTC Chair Michael Selig warned that the agency will continue legal action against states that attempt to impose penalties on CFTC-registered exchanges.

Michigan judge’s order vs. federal directive

Michigan’s court case began with a directive that targeted Kalshi’s ability to provide sports betting contracts to residents of the state. According to Cointelegraph reporting, Judge Aquilina ordered Kalshi to cease offering those contracts to Michigan users while the lawsuit proceeds over whether Kalshi’s offerings violate state sports betting laws. Earlier coverage from Cointelegraph described the scope of that order and the legal context surrounding it.

But on Tuesday, the CFTC intervened. In a press statement, the regulator ordered Kalshi not to comply with the Michigan directive and to continue operating despite the state order. The CFTC press release frames the issue as one of maintaining federal authority over registered entities and executed derivatives contracts.

Kalshi says it unwound trades—and now faces contradictions

Kalshi’s response highlights the practical dilemma regulators rarely address directly: companies caught between courts can end up violating one authority while trying to obey another.

In a statement posted on X, Robert DeNault, Kalshi’s head of enforcement and legal counsel, said the company is “disappointed” and described the federal action as placing Kalshi in an “impossible position.” DeNault’s statement on X argues that Kalshi already followed the Michigan court order by unwinding the trades, but the new CFTC directive appears to contradict that requirement.

DeNault’s wording underscores the core problem: Kalshi believes it is being pushed into a compliance conflict, where it may be required to reverse actions taken under state instructions while also meeting federal regulatory expectations.

Reuters reported that Kalshi is reviewing the CFTC’s order and considering its next steps. According to Reuters, the company is weighing how to respond given the opposing directives.

Why the regulator says “canceling” is a market-breaking precedent

The CFTC’s position is grounded in the mechanics of derivatives contracting. The regulator argues that canceling trades already executed is not just a procedural change—it threatens contract certainty across the marketplace.

In the same dispute framing, the CFTC characterized cancelation of executed trades as unprecedented and potentially destabilizing. The regulator’s message is that prediction markets operate through contractual certainty, and that undermining that certainty would ripple outward beyond any single platform.

The CFTC also emphasized that it will not allow states or state courts to pressure registered entities into violating the Commodity Exchange Act and CFTC regulations. That argument is aimed directly at the core tension at the center of the Michigan case: whether states can effectively override federal rules through injunctions and court orders applied to an exchange that is already registered with the CFTC.

Broader conflict: federal authority vs. state-by-state attempts

This is not presented by the CFTC as an isolated disagreement. The regulator has repeatedly argued that prediction markets fall within the federal scope when they are run through CFTC-registered structures.

As the dispute is framed, Michigan is described by the CFTC as the first state to attempt interference with executed derivatives transactions through a court order. That characterization matters because it suggests the CFTC views the issue as moving from “licensing and legality” arguments—traditionally handled at the state level—into the domain of how executed federal derivatives contracts must be honored.

During an appearance on Fox Business, CFTC Chair Michael Selig said it is “critical” that the regulator maintains its authority over prediction markets. Selig also stated that the agency has sued nine states and indicated it would continue to challenge states that attempt to impose criminal or civil fines against CFTC-registered exchanges. According to Selig’s remarks, the CFTC’s stance is that state actions cannot be allowed to erode the federal regulatory framework for these markets.

For investors and market participants, the practical implication is that prediction market compliance may remain a moving target. Even where a state court order appears clear, a federal regulator may step in to enforce a different standard. That dynamic increases uncertainty for platforms operating across state lines and could affect how traders evaluate jurisdictional risk when participating in events-based contracts.

What to watch next is how Kalshi navigates the contradiction between the Michigan directive and the CFTC’s order—and whether additional courts or appeals clarify which obligations control when state and federal requirements diverge for already executed derivatives contracts.

This is Part 4 in the technical article series about Bitcoin covenants by Cointelegraph Research. To read the previous article, click here.

The following opcodes do not independently implement full covenant functionality. Instead, they are building blocks for constructing covenants when combined with other opcodes or script elements.

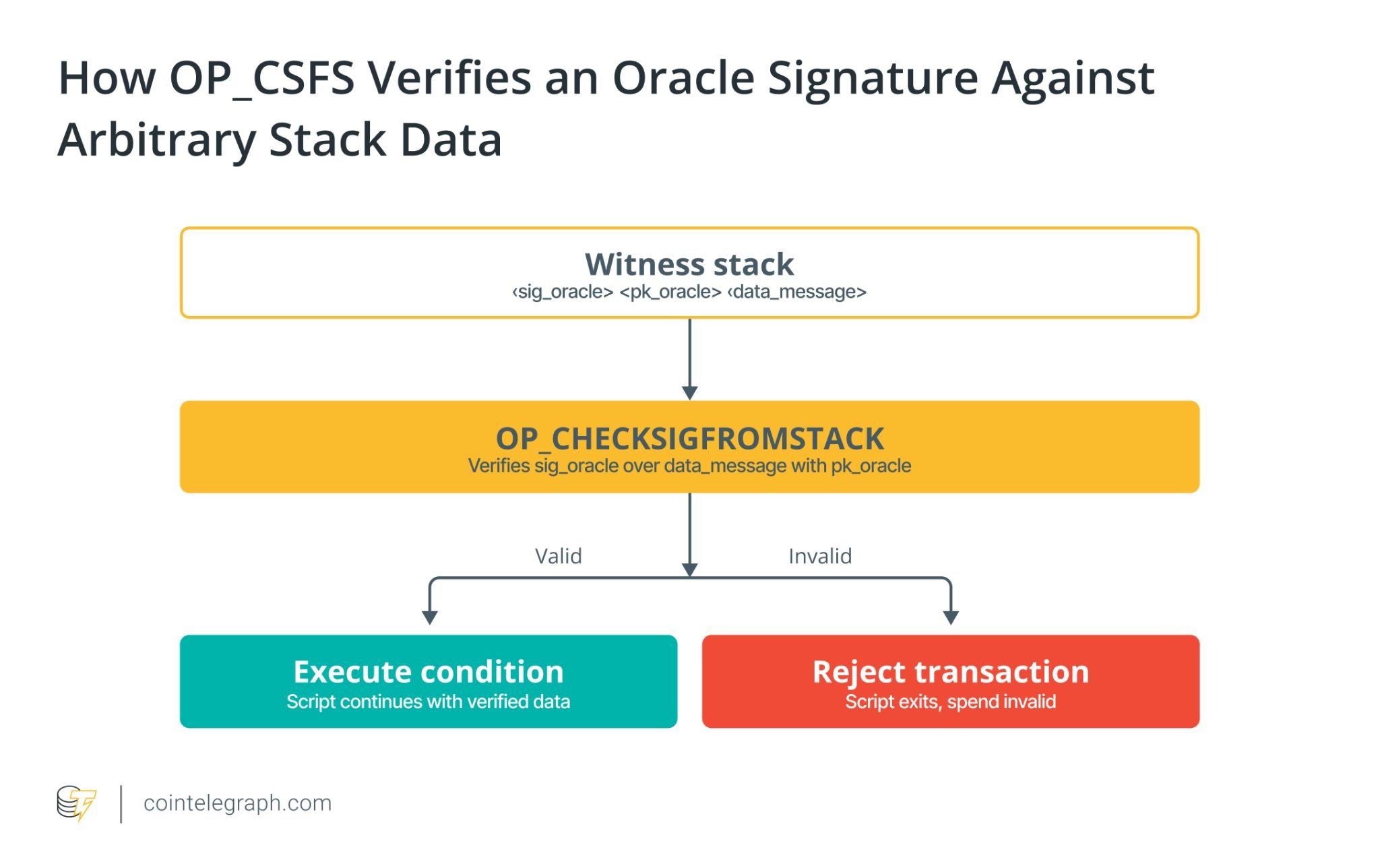

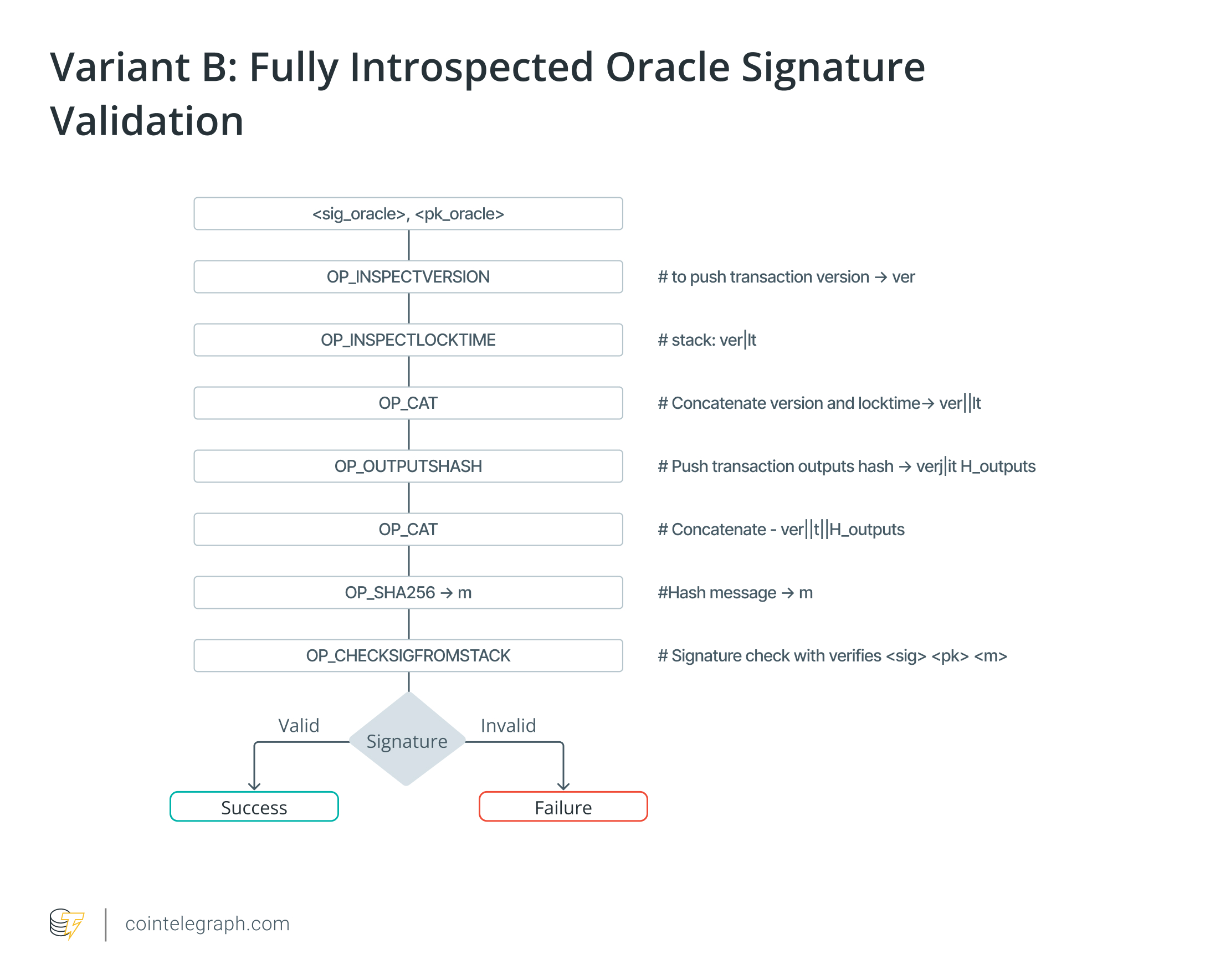

OP_CHECKSIGFROMSTACK (OP_CSFS) and OP_CAT

OP_CSFS is a proposed opcode that would allow Bitcoin script to verify signatures over arbitrary messages supplied on the stack. It is different from OP_CHECKSIG, which verifies signatures over the spending transaction according to the active SIGHASH mode. By enabling signature verification for data other than the serialized transaction details, OP_CSFS enables a broader class of constructions, including oracle-based scripts where an external party signs off-chain messages that represent real-world events. For example, a trusted oracle could publish Schnorr signatures over messages that encode external outcomes, and an OP_CSFS-based script could condition payments on the presence of a valid oracle signature.

On its own, OP_CSFS does not implement covenants. It can authenticate external data, but it does not bind that data to the structure of the spending transaction. That binding requires OP_CAT.

OP_CAT is a proposed opcode that enables the concatenation of two values on the script stack to form a single byte sequence instead of two distinct ones. When combined with OP_CSFS, it allows the script to assemble selected transaction fields into a canonical message and verify that a provided signature commits to that message.

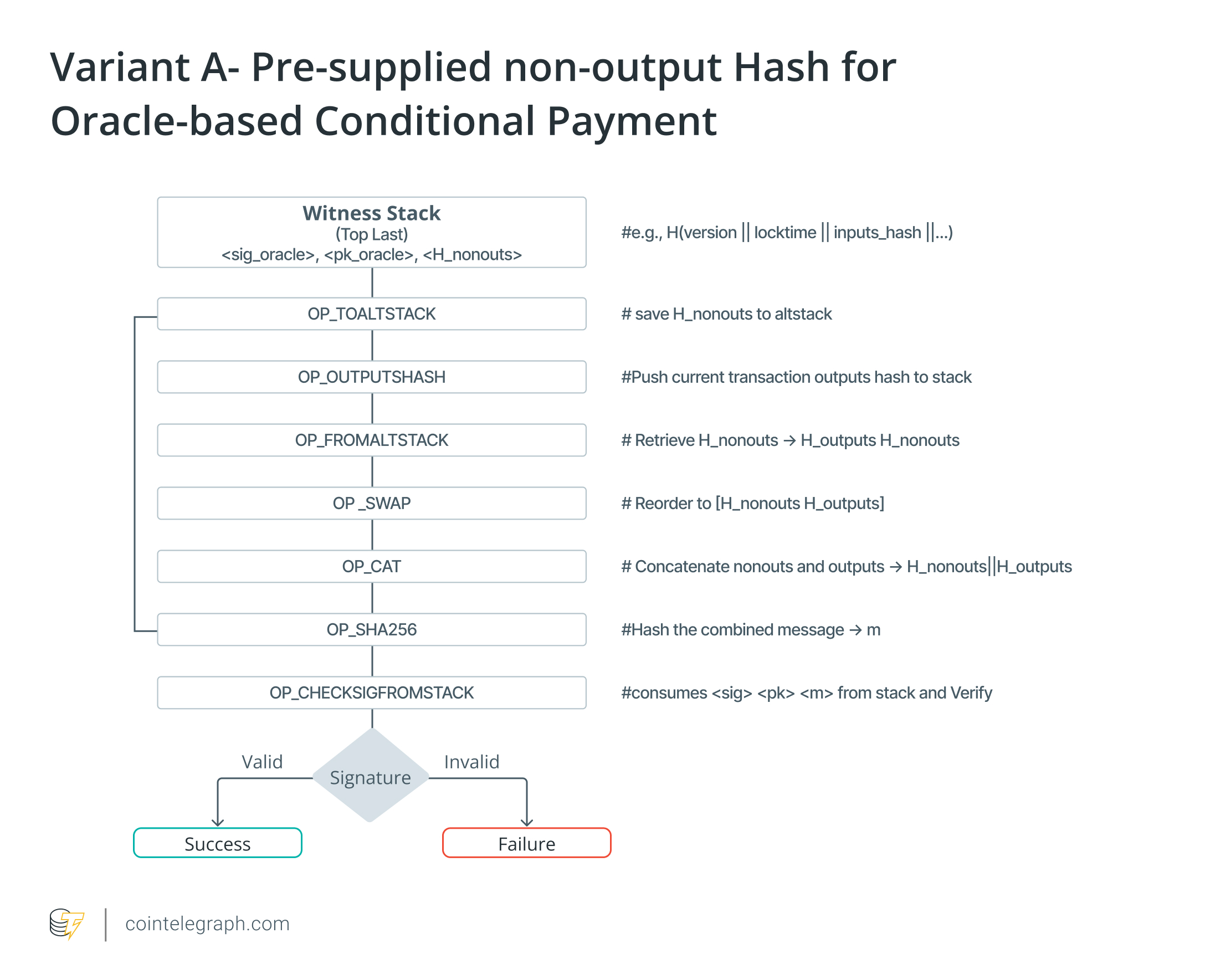

OP_CSFS and OP_CAT taken together can perform introspection by compelling the spender to provide transaction details on the witness stack. If both OP_CSFS and OP_CHECKSIG succeed for the same signature, it proves that the correct transaction details have been passed on to the witness stack and can be further reasoned about. By checking the transaction against a predefined template, a covenant construction, similar to OP_CTV, can be enforced. Two minimal assemblies show how this works:

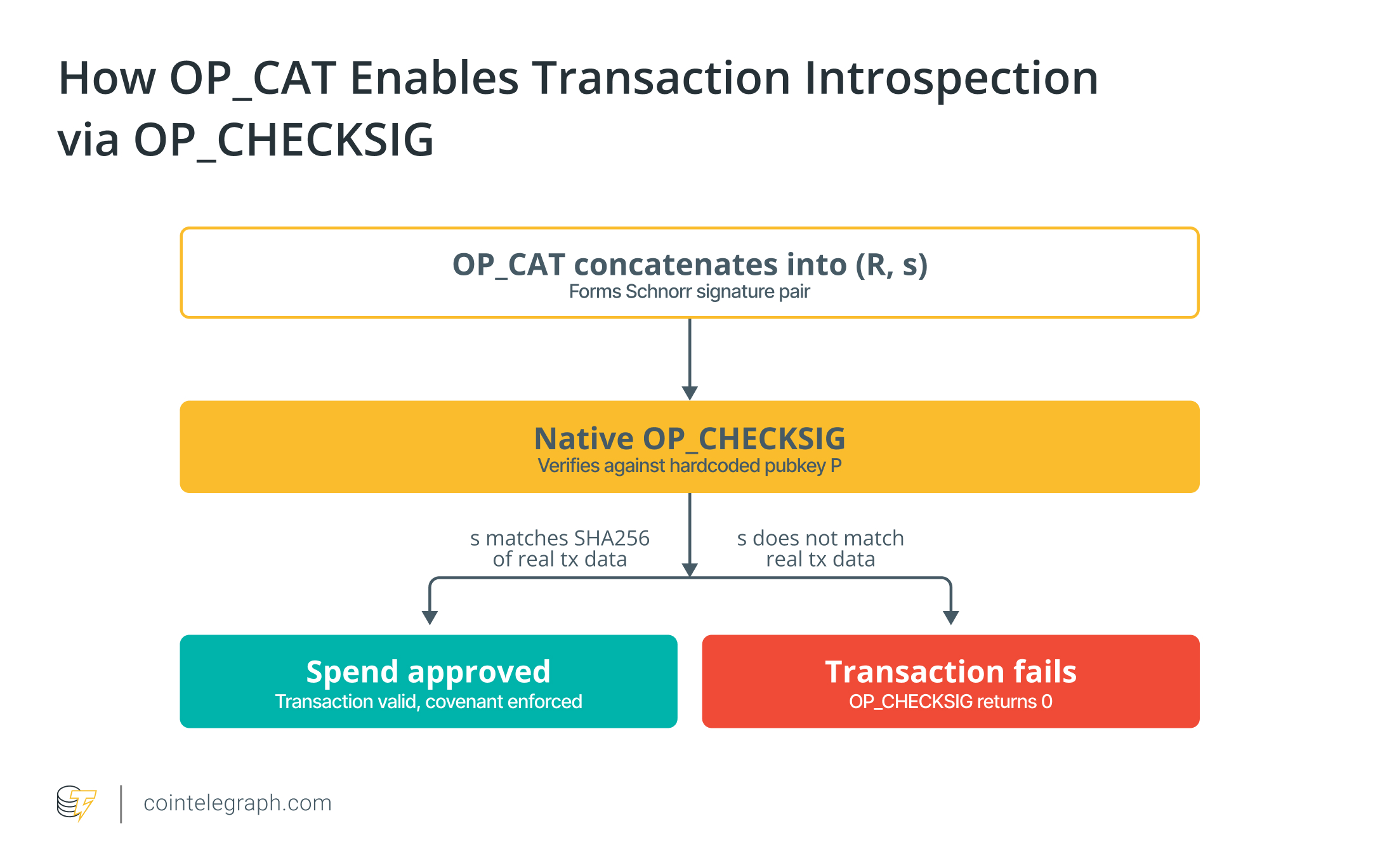

OP_CAT + Schnorr Tricks

Using OP_CAT, covenant-like constructions can be enforced under Taproot without OP_CSFS by exploiting how Schnorr signatures interact with the Taproot sighash rules defined in BIP 341. The construction repurposes OP_CHECKSIG which is ordinarily used to authenticate ownership of a private key, to a transaction introspection tool.

A schnorr signature is a pair ⟨R, s⟩. Under normal circumstances, this schnorr signature is generated by selecting a secret nonce k, deriving the point R = kG, and computing the signature value s as a function of the message hash and the private key. The verifier then checks the signature pair ⟨R, s⟩ against a public key P and the message being signed. The randomness of k ensures that s is unpredictable and non-reproducible without knowledge of the private key.

The introspection trick works by eliminating randomness by fixing some of these variables in advance. Instead of choosing R randomly during signing, the script commits to a predetermined value of R and to a fixed public key P. Because Schnorr verification follows a deterministic equation, it becomes possible to construct these values so that the signature scalar s must equal a hash of specific transaction parameters.

The spender provides R and s on the witness stack. OP_CAT concatenates them into the signature pair ⟨R, s⟩ in the format OP_CHECKSIG expects. The script verifies this against the hardcoded public key P. Because R and P are fixed to the base point G, OP_CHECKSIG will only accept the pair if s equals the SHA256 hash of the actual transaction data computed by the protocol. The spender cannot fabricate an s that passes OP_CHECKSIG unless it genuinely reflects the real transaction data. The spender must grind the transaction data until its SHA256 hash ends in a specific byte, which takes roughly 256 attempts on average and adds negligible cost.

In this way, OP_CHECKSIG is no longer used to authenticate ownership of a secret private key but instead to enforce that the transaction matches a specific template. The expressiveness is broadly comparable to OP_CTV.

Because this approach depends on Schnorr signatures and the taproot sighash algorithm, it applies only to SegWit v1 outputs and does not extend to SegWit v0 outputs which uses the BIP-143 digest and ECDSA signatures.

In our next article we will commence our discussion of OP_CCV, which is even more capable than OP_CSFS and OP_CAT combined.

Bitcoin (BTC) tipped to $65,000 briefly, according to Coin Gecko, even as fresh US-Iran tensions flared. Meanwhile, Korean crypto trading volume skyrocketed as AI memory stocks struggle. Crypto traders, it seems, are shrugging these macro conditions off.

Bitcoin’s rally came as softer than expected US inflation data eased pressure on the Federal Reserve to keep rates higher for longer. That gave the coin room to push toward multi-week highs even as fresh US-Iran strikes continued.

Bitcoin Rally Signals Iran Fatigue

President Trump ordered airstrikes on Iran last weekend and threatened to reinstate a blockade on the Strait of Hormuz. That is the kind of headline that hammered crypto prices earlier this year.

This time the reaction was muted. Bitcoin recovered above $63,000 within days of the strikes. That marked a sharp contrast to past episodes, when similar headlines sent prices sharply lower.

The Bitcoin rally has held near that recovered range into this week before its recent spike on promising inflation data. Traders appear to be growing desensitized to the tit for tat in the Middle East rather than panicking every time tensions flare.

The pattern lines up with a broader rotation. The Altcoin Season Index has climbed to 58 while Bitcoin dominance has slipped toward key support as capital spreads into other tokens.

South Korea Adds Fuel to the Rotation

South Korea offers the clearest real-world evidence. The KOSPI is technically in a bear market, down more than 20% from its June record. Retail investors appear to be looking elsewhere for returns.

Much of that weakness traces back to just two stocks. Samsung and SK Hynix now account for roughly half the KOSPI’s total weight. eToro market analyst Zavier Wong said that a sharp swing in either name now drags the whole index with it.

At the same time this week, trading volume on Upbit, the country’s largest crypto exchange saw volume surge 1,318% in 24 hours to $4.2 billion as the stock rout deepened. XRP alone recorded more volume than Bitcoin.

Not all of it is conviction buying. Korea’s Financial Supervisory Service said 1.2 million leveraged accounts triggered margin calls this week. That’s a reminder that some of this is forced selling, not a clean bet on crypto.

SK Hynix’s Swings Point to a Brewing AI Bubble Debate

SK Hynix sits at the center of the KOSPI’s chip-driven volatility. Its own chart tells an AI bubble story in miniature. The stock climbed almost 233% from the start of 2026 to a June 25 record. It then retreated over 34% from that peak by July 13.

The swings intensified after SK Hynix listed American depositary receipts on Nasdaq on July 10. The $26.5 billion offering ranks among the largest foreign listings in US history. Investors are weighing surging demand for AI memory chips against how much of that demand is already priced in.

Iran tensions have not gone away, and neither has the AI bubble debate. But for now, crypto looks less like an asset caught in the crossfire. It looks more like the place traders go when headlines get tiring, whether from Tehran or Seoul’s chip floor.

The post Is Crypto Finally Shrugging Off Iran and AI Hype? Bitcoin and Altcoins Suggest Yes appeared first on BeInCrypto.

Bitcoin (BTC) should repeat history and put in a bear-market bottom when a classic indicator hits zero, a trader says.

Key points:

- Bitcoin classic two-month stochastic RSI signals are valid this bear market, Max Crypto said.

- The bear market will be over once the indicator reaches zero again.

- RSI divergences provided advance notice of the BTC price rebound beyond $64,000 this month.

Bitcoin stochastic RSI bottom signal “will happen again”

In an X post at the weekend, Max Crypto went on record to forecast the end of the 2026 bear market when the stochastic relative strength index (RSI) hits a new swing low.

“Stoch” RSI is a derivative of RSI, a popular leading indicator, with a greater bias on recent price moves.

“Every time the 2M Stoch RSI had a bullish cross and dropped to 0, $BTC bottomed,” Max Crypto wrote in accompanying commentary.

“This happened in 2014, 2018, and 2022, and it will happen again.”

BTC/USD two-month chart with stochastic RSI data. Source: Cointelegraph/TradingView

Two-month stoch RSI measures 4.81, having dropped into its sub-30 “oversold” zone during March, data from TradingView confirms. Current levels were last observed just over three years ago.

Stoch RSI has already formed a focus for market participants this year, with daily moves previously drawing comparisons to the 2022 bear market.

In April, crypto trader Quantum Ascend described BTC price history as “playing out nearly perfectly.”

Bear-market RSI cues keep coming

Turning to traditional RSI data, traders continue to look for bullish cues as BTC/USD treads water above $60,000.

Related: BTC price bull market to begin in September? Five things to know in Bitcoin this week

On Sunday, trader and investor BitcoinHyper eyed a bullish divergence against the S&P 500.

At the start of June, daily RSI dropped to just 15, marking one out of just six of what trader Osemka later called “extremely powerful selling events.”

“There’s been one case where extreme $BTC RSI (1D at 15) failed to break the lows and only managed to sweep it. That was at the end of accumulation range in 2015,” he continued on Tuesday.

“I’m mentioning it now since we have also only swept the low on such powerful move down.”

BTC/USD one-day chart with RSI data. Source: Osemka/X

Osemka implied that a deeper RSI retracement could still emerge, marking a price reversal in-line with previous bear markets.

Bitcoin’s return above $64,000 this month, meanwhile, came after bullish RSI divergences across multiple time frames.

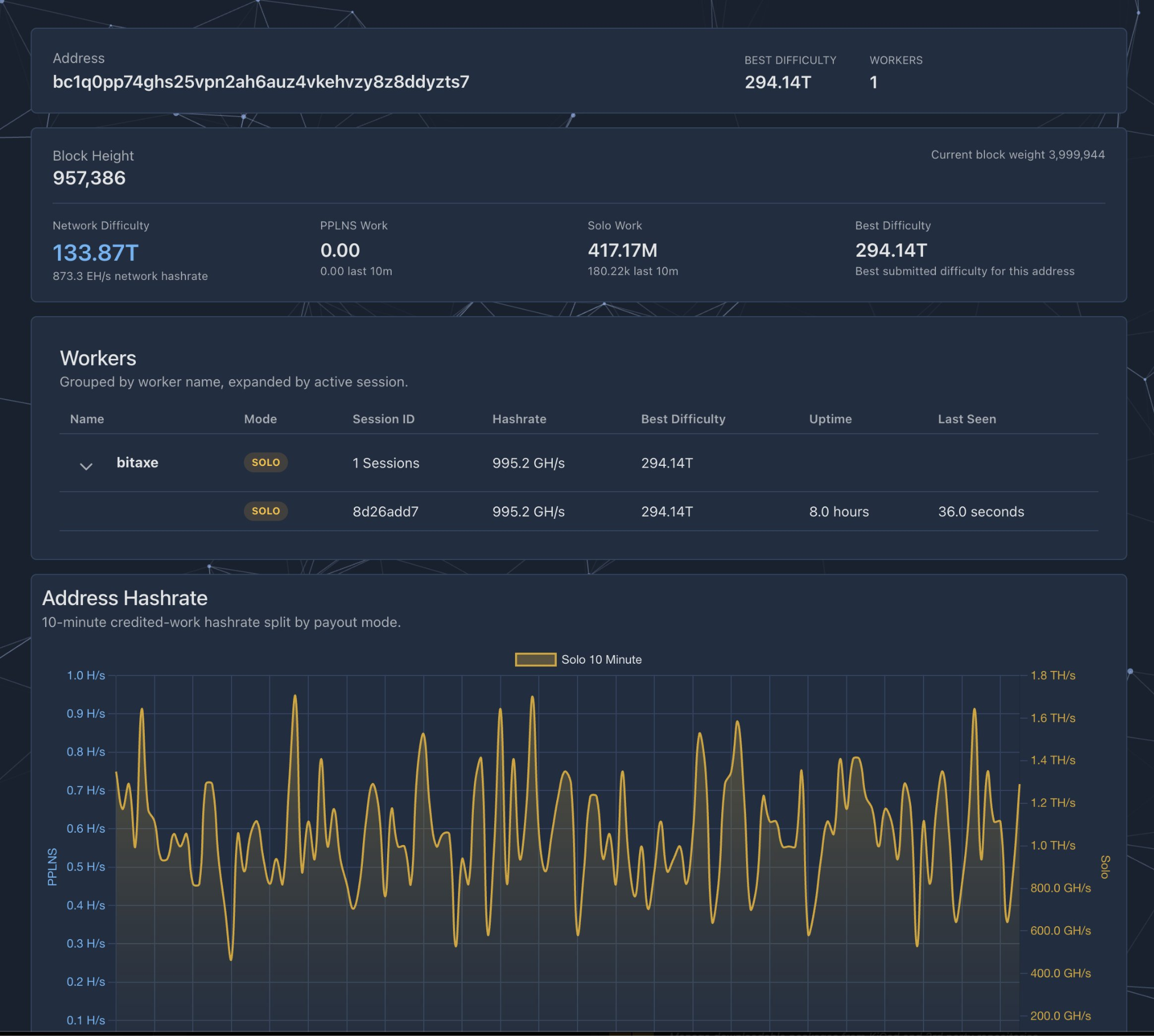

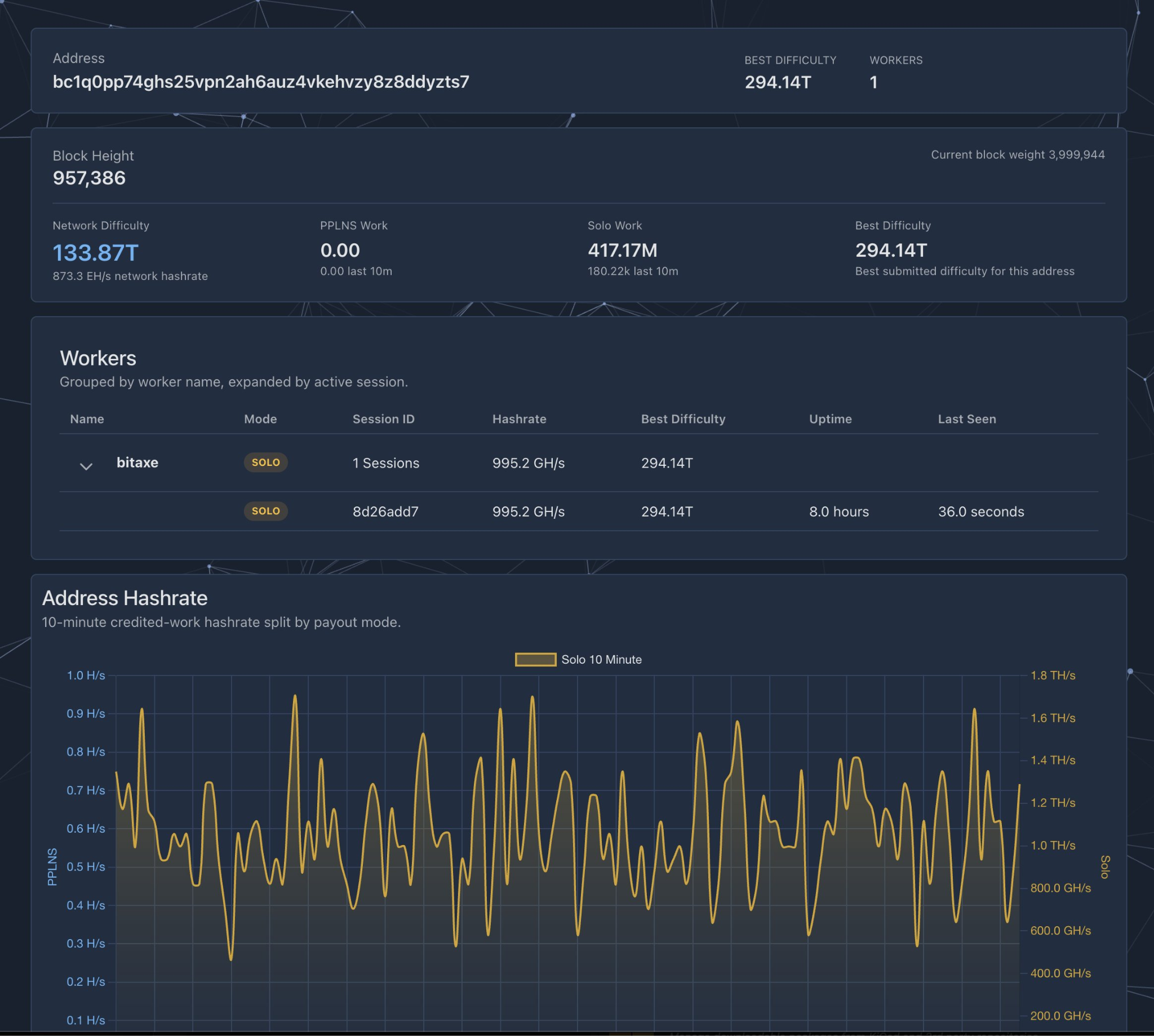

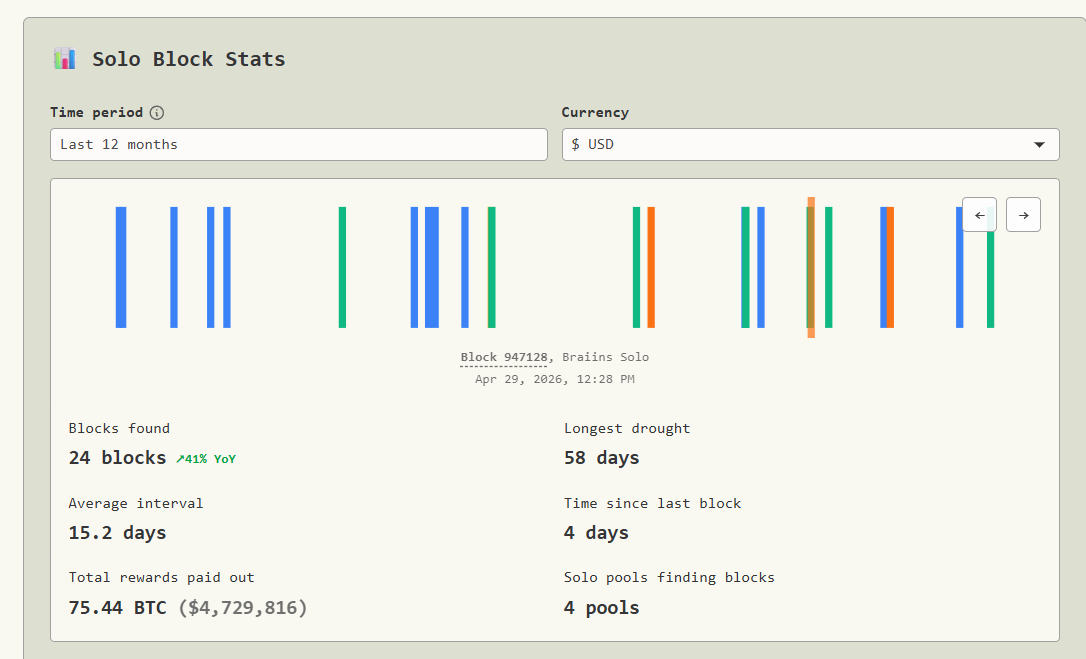

A solo Bitcoin miner hit the jackpot and validated a solo block with a single Bitaxe mining rig, marking a rare win that beat massive statistical odds.

The retail Bitcoin miner secured a 3.125 Bitcoin (BTC) block reward, currently worth about $200,000, on Friday at block number 957382, according to blockchain data from mempool.space.

The miner was using a single Bitaxe mining rig, according to the BTC mining pool Public Pool. The Bitaxe was a budget, lower-power Bitcoin miner that costs less than $200 and has a hashrate of about 1 terahash per second (TH/s), which is a tiny fraction of the global Bitcoin network.

The solo block reward shows that even a sub-$200 investment in a mining rig can lead to a statistically rare payday for retail miners.

Another solo Bitcoin miner validated a solo block in April, through CKPool’s solo mining service. Earlier in February, another retail miner validated a solo block using rented hashrate from a mining provider, meaning that he didn’t own the physical mining rig that solved the block.

Source: Public Pool

Solo BTC miners bag $4.7 million during the past year

While mining a solo block is statistically rare, this marks the 12th Bitcoin block validated by a hobby-level miner so far in 2026, pushing the past 12 months’ total payouts to more than $4.7 million for retail miners.

Solo block stats, one-year. Source: Bennet.org

Solo blocks mined increased by 41% year-on-year, as solo miners have validated a total of 24 blocks during the past year, according to solo miner data aggregator Bennet. This brings total rewards paid to solo miners to 75.4 Bitcoin, or $4.7 million, for the past year.

Related: Bitcoin whale moves $188M for first time in 7 years

The average interval for solo Bitcoin blocks stands at 15.2 days, while the longest drought without a successful solo block stands at 58 days.

Magazine: Bitcoin nearing late stages of bear market: Jamie Coutts, Real Vision

BitMine Immersion Technologies posted revenue of $46.5 million in the three months ended May 31, a 22x jump from a year earlier, even as a $9.1 billion nine-month net loss dominated its latest filing.

The loss stems almost entirely from a non-cash markdown on the company’s Ethereum (ETH) holdings. Underneath it, BitMine’s staking business scaled from almost nothing into the firm’s dominant revenue source.

Staking Drives BitMine’s Revenue

According to BitMine’s filing, revenue from staking and validation reached $45.7 million, about 98% of the total. A year earlier, that line was zero. The rest came from small self-mining and consulting lines, together under $800,000.

Follow us on X to get the latest news as it happens

As of the latest data, BitMine has staked 4.9 million ETH, roughly 85% of its holdings, through its MAVAN validator platform. The company projects annualized staking revenue near $242 million.

“Annualized staking revenues are now projected at $242 million. And this 4.9 million ETH is 85% of the 5.77 million ETH held by Bitmine. Bitmine’s own staking operations generated a 7-day yield of 2.70% (annualized),” said Tom Lee.

That income rests on a large ETH position. As of July 12, BitMine holds 5.77 million ETH, worth roughly $10.5 billion and equal to 4.8% of supply. The stake makes it the largest corporate ETH treasury.

The trend extends well beyond BitMine. One recent study found that staking accounted for 60% of disclosed revenue across listed ETH treasury firms in 2025.

A $9 Billion Loss That Missed the Numbers

The headline loss looks alarming, but the timing matters. BitMine’s $9.1 billion nine-month net loss came almost entirely from a $9.04 billion unrealized markdown on its digital assets, according to its SEC filing.

That damage landed as the value of its ETH holdings fell. In the three months ended May 31, the net loss narrowed to $83.6 million.

The period’s operating loss was $11.9 million. The bigger hit came from a $92 million loss on derivative contracts.

The split screen defines BitMine’s model. Its reported earnings will swing with ETH’s price, while its staking operation generates a growing revenue stream. The coming months will test whether staking income can offset that volatility.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post BitMine Revenue Jumps 22x Even as It Posts $9 Billion Net Loss appeared first on BeInCrypto.

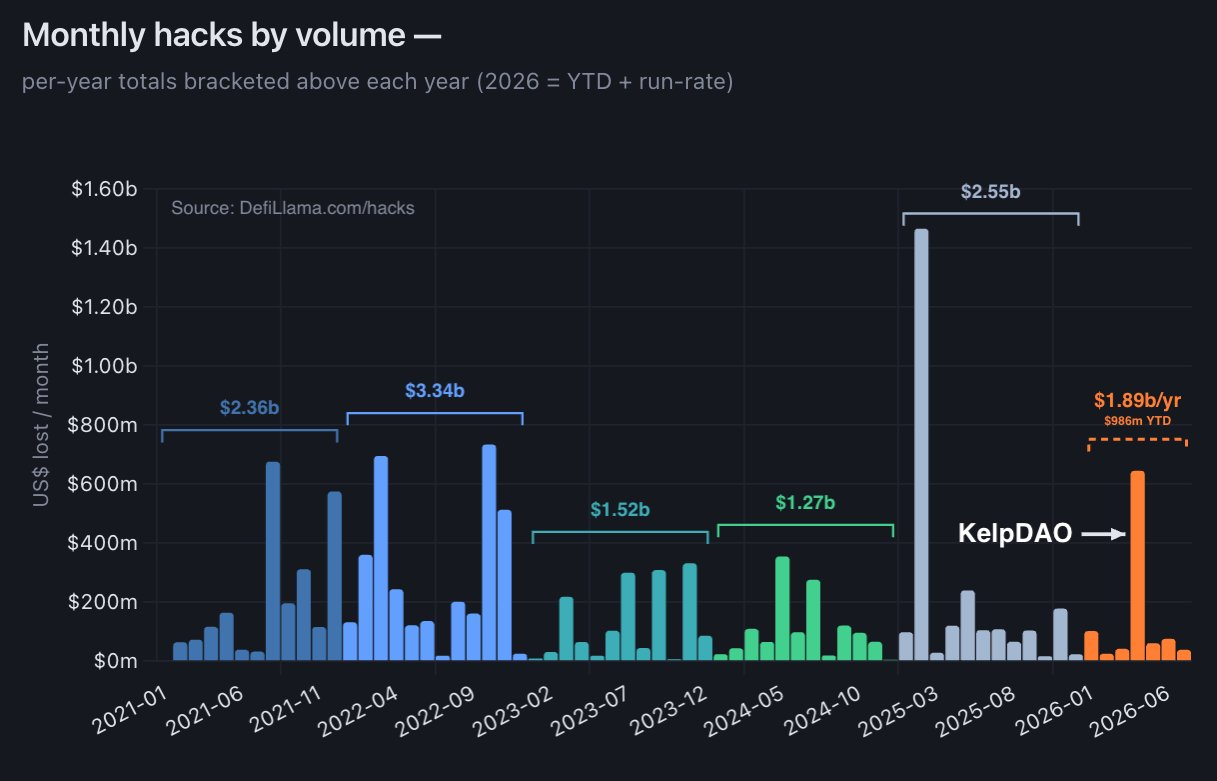

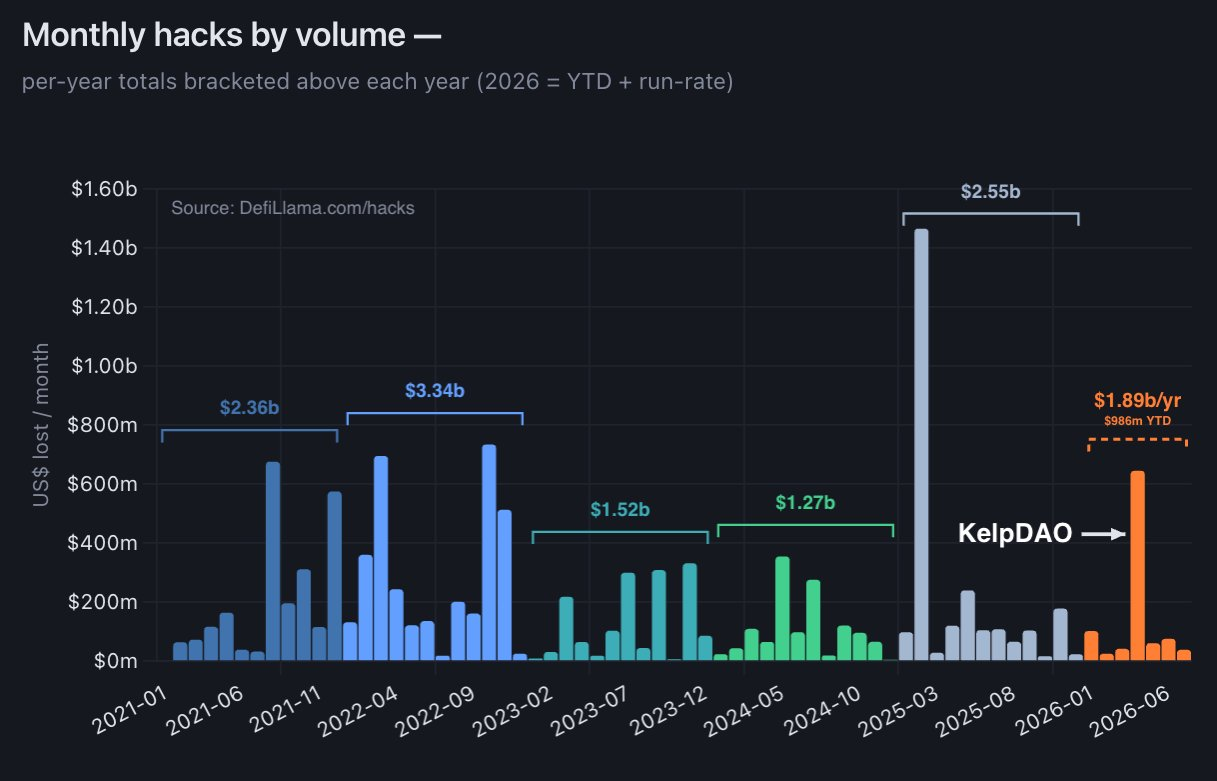

Fears that artificial intelligence would trigger a wave of catastrophic decentralized finance (DeFi) hacks in what was coined as a “hackpocalypse” have not materialized, according to Dragonfly managing partner Haseeb Qureshi.

While the incident count grew to a record high, the median size of hacks has dipped below $500,000 this year, down from over $2 million in 2025. Qureshi argued that this shows malicious actors using AI are targeting “small protocols and abandonware” while larger DeFi protocols have fortified themselves against AI’s threat.

Excluding outlier months with large incidents, such as the Bybit hack in February 2025 along with the Drift Protocol and KelpDAO exploits in April of this year, 2026 has still seen less value hacked per month than the previous year, said Qureshi.

The comments come in response to concerns shared by blockchain security platform OpenZeppelin’s founder, Manuel Aráoz, who said that he considers “all of DeFi unsafe,” citing the growing ability of AI coding agents to identify smart contract vulnerabilities.

Broader industry datasets, which include centralized platforms, wallet compromises and phishing, as well as DeFi exploits, offer a less reassuring picture. In April, crypto hacks surged, resulting in losses of around $644 million, marking an over one-year high last seen in February 2025 when the $1.4 billion Bybit hack pushed monthly losses to $1.46 billion, according to DefiLlama.

Source: Haseeb

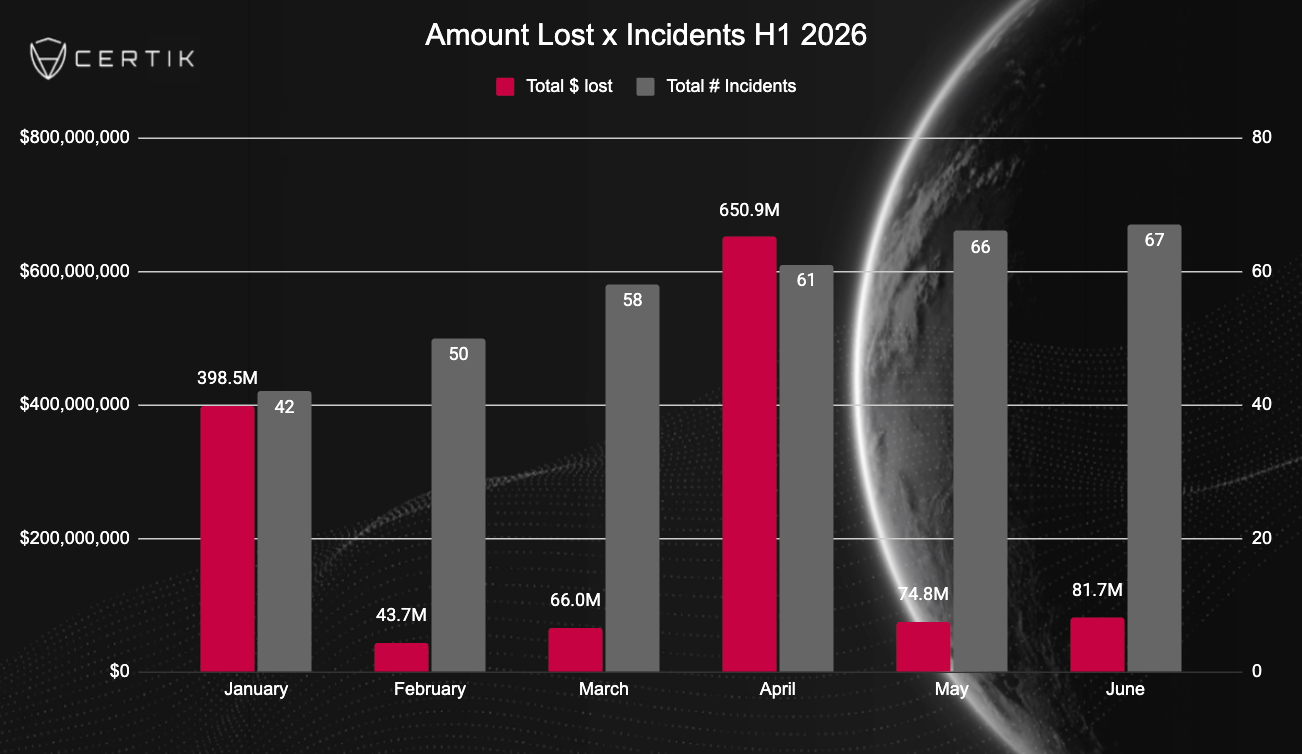

Crypto hacks fall 47% in H1, but crypto industry not necessarily safer: CertiK

Losses to cryptocurrency hacks fell 46.8% year-on-year to $1.32 billion in the first half of 2026, but blockchain security company CertiK argued that the Web3 industry’s lower headline losses do not necessarily mean the industry is safer.

Related: Belgian police arrest suspected phishing gang leader tied to $572K theft

While it marks a significant drop in dollar value, last year’s figures were skewed by the $1.4 billion Bybit hack, the largest in crypto history, CertiK told Cointelegraph.

During the second quarter of 2026, over 70% of the losses stemmed from the KelpDAO and Drift Protocol exploits, which were largely attributed to North Korean state-sponsored hackers.

Monthly change in crypto exploit amounts and number of incidents across H1. Source: CertiK

The data underscores the continued threat that North Korean hackers pose to the crypto industry, having stolen more than $6 billion worth of crypto since 2017, TRM Labs estimated in April.

Magazine: Does Botanix’s failure prove Bitcoiners don’t care about DeFi?

Coinbase, among others, filled that gap in May 2025. Under x402, a server that wants payment answers a request with a 402 and a price. The client signs a stablecoin transfer, usually USDC, resends the request with the payment attached, and gets the data. The exchange takes seconds and needs no account, no card, and no prior relationship between the two sides.

That is why the AI industry cares. An autonomous agent cannot open a bank account, pass a credit check or sign a SaaS contract, but can sign a transaction. Google has wired x402 into its own agent payments protocol, and Cloudflare ships it in its agent toolkit.

The announcement included no usage figures, though x402 publishes them on its own homepage. The protocol handled about 75 million transactions over the past 30 days, or roughly 29 every second, moving about $24 million between some 94,000 buyers and 22,000 sellers.

That works out to an average payment of about 32 cents, meaning the machine-to-machine thesis works as designed, as no card network can process a such small charges profitably.

Still, $24 million a month is a fraction of what any of x402’s premier members move in a day.

PI crashed 40% this week after a massive sell-off that drove it to consecutive all-time lows. However, it has rocketed by 10% since those lows, begging the question of whether the bottom is in.

PI Network (PI) Price Predictions: Analysis

Key support levels: $0.07

Key resistance levels: $0.10, $0.13, $0.16

PI Crashed to $0.07

PI just had one of the worst weeks in 2026 after the price lost support at $0.10. With this level turned into resistance, sellers rushed for the exits and sent the price into a nose-dive to $0.07, which became its latest record low.

With confidence gone, buyers had vanished. For example, in the past 10 days, only one day closed in the green. This shows that the sentiment is extremely bearish and the downtrend has entered a new phase where a bottom could be found much quicker.

More positive news came in the past several hours, with PI finally rebounding to $0.08 as of press time. However, it remains to be seen whether this is another dead-cat bounce.

Sell-Side Volume Exploded

As soon as the support at $0.10 was lost, sell volume began to pick up. This only made things worse and likely led to cascade liquidations that put even more pressure on the falling price.

While the sell pressure has decreased compared to yesterday, the day is not over, and this could still change. The price held above $0.07 and bounced to $0.08, but this could very well be just a temporary pause before new lows.

Momentum Indicators Are at Extremes

Due to heavy selling pressure, the momentum indicators have reached extreme levels. For example, the daily RSI is at 12 points, a level never seen before for this cryptocurrency. Extremes are also the place where bottoms are found.

Hopefully, this price action will bring about an end to the downtrend and allow PI to consolidate and confirm a bottom. If the support at $0.07 won’t hold, then buyers will likely retreat to $0.06 or even $0.05. The current resistance is at $0.10.

The post Pi Network Price Predictions for This Week as PI Surges 10% in 24 Hours (July 15) appeared first on CryptoPotato.

Crypto World

Finassets Raises Affiliate Revenue Share to 40%, Becoming One of the Highest-Paying Crypto Affiliate Programs

[PRESS RELEASE – Marbella, Panama, July 15th, 2026]

Finassets, a crypto payment gateway for businesses, announced an increase to its partner revenue share. The first-year referral rate rises to 40% of the processing revenue a referred merchant generates. From year two, the rate continues at 20% for five additional years while the merchant keeps processing, extending the total partner earning window to six years per referral, with the term extendable based on the merchant profile.

Payout speed, contract length, and dashboard visibility are among the key considerations affiliate marketers weigh when comparing crypto affiliate programs, and this update puts Finassets among the top crypto affiliate programs open to B2B partners.

A different model from trading-based programs

Many crypto exchange affiliate programs and trading platforms base payouts on trading fees generated by active traders, tying affiliate income to short-term trading volume through a fixed commission plan or a minimum payout threshold. Finassets ties partner earnings to a merchant’s ongoing processing volume instead — a relationship that can continue for the full six-year term.

One agreement, six years of revenue share

- Apply to become a partner. Submit an application and our team handles onboarding and sets clear terms from day one, with a personal referral link and dashboard account.

- Finassets onboards the merchant. KYB, compliance, and integration are handled entirely by Finassets.

- The partner earns. Revenue share is calculated per merchant and paid same-day, in crypto. The term can be extended based on the referred user profile.

A merchant referred through a partner’s affiliate link and processing $500,000 a month generates about $2,000 a month in processing fees at Finassets’ 0.40% rate. Here’s how that translates into partner earnings:

Based on a merchant processing $500,000/month at Finassets’ 0.40% fee. Illustrative; actual earnings depend on the merchant’s processing volume.

“Most cryptocurrency affiliate programs ask partners to keep generating referrals just to keep earning,” said Vitalijs F., CEO of Finassets. “We built this revenue share model so one merchant relationship can keep paying out for years, without additional marketing efforts from the partner after the introduction.”

Real-time visibility, reliable payouts

The agent dashboard tracks referral volume and revenue share per merchant in real time, with a full transaction history for reconciliation and one-click withdrawals. Deposits are typically credited within about 30 seconds of network confirmation, and partners are supported by dedicated account managers who respond quickly. Payouts are same-day, in crypto. Finassets supports 70+ cryptocurrencies across its full product suite, the same infrastructure referred merchants use to process payments.

The affiliate program is open to eligible B2B participants in selected international markets, subject to Finassets programme terms and applicable jurisdictional requirements.

More information and the partner application: https://www.finassets.io/en/affiliate-program/

About Finassets

Founded in 2021, Finassets is a Panama-registered crypto payment gateway supporting cross-border and crypto-driven businesses across eligible markets. Finassets provides crypto invoicing, payment links, payment buttons, mass payouts, API integration, crypto checkout, and an affiliate program within a structured, transparent environment for crypto payment processing.

Website: https://www.finassets.io

The post Finassets Raises Affiliate Revenue Share to 40%, Becoming One of the Highest-Paying Crypto Affiliate Programs appeared first on CryptoPotato.

Most mesmerizing money spread

Motorists warned about traffic light outage in Bury centre

Spain’s final 12-month EU-harmonised inflation at 3.6% in June

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports5 days ago

Sports5 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

News Videos11 hours ago

News Videos11 hours agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech1 day ago

Tech1 day agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech11 hours ago

Tech11 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos6 days ago

News Videos6 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Sports7 days ago

Sports7 days ago39-year-old Djokovic wins five-hour thriller to enter Wimbledon semis | Other Sports News

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

Tech2 days ago

Tech2 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Tech6 days ago

Tech6 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World6 days ago

Crypto World6 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World6 days ago

Crypto World6 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

-

Tech6 days ago

Tech6 days agoClaude’s New Reflect Dashboard Wants To Help You Log Off Of Claude

-

Crypto World7 days ago

Crypto World7 days agoMicrosoft Cuts AI Bill by Replacing OpenAI and Anthropic in Software Products

-

Crypto World6 days ago

Crypto World6 days agoFed minutes June 2026: officials split on rates

You must be logged in to post a comment Login