Crypto World

What is a token unlock? Vesting and cliffs explained

Every few weeks, a token that has done nothing wrong falls ten percent in a day, and the explanation turns out to have been sitting in public view for years. A tranche of supply, promised to early investors back when the project raised money, hit its scheduled release date.

Insiders who bought at a fraction of the market price suddenly held tokens they could sell, and enough of them did. Traders call these events unlocks, and they are among the most predictable forces in crypto markets, which makes it strange how many investors get blindsided by them.

A token unlock is the moment previously locked supply becomes transferable and enters circulation under rules the project set in advance. The rules themselves are called a vesting schedule, and together they answer a question every serious investor should ask before buying any token: who is going to be allowed to sell, how much, and when. This guide explains what unlocks and vesting are, why projects lock tokens in the first place, the difference between cliffs and linear releases, who actually receives unlocked supply and how differently each group behaves, how unlocks move prices, the low float trap that defined the current market cycle, how to read an unlock calendar like a professional, and the honest limits of unlock analysis.

What a token unlock actually is

When a crypto project creates its token, it almost never releases the full supply into the market on day one. Instead, the total supply is divided into allocations: a slice for the founding team, a slice for the venture investors who funded development, a slice for advisors, a slice for the community, a slice for an ecosystem fund or treasury. Most of these allocations start locked, meaning the tokens exist on paper, and often on chain, but cannot be transferred or sold.

An unlock is the scheduled event that releases some of that locked supply. On the appointed date, or continuously according to a formula, tokens move from the locked state to the liquid state, and their owners can finally do what owners do: hold, stake, or sell. Nothing about an unlock is secret. The schedule is typically published in the project’s tokenomics documentation before the token ever trades, and modern vesting is usually enforced by smart contracts that release tokens automatically, with the whole timetable verifiable on chain.

The distinction between vesting and unlocking trips up newcomers. Vesting is the rulebook, the full timetable governing how allocations are earned and released over months or years. An unlock is a single event within that timetable, the moment a specific batch becomes tradable. A project has one vesting schedule and many unlocks. When traders say a token has an unlock next week, they mean one identifiable batch is crossing from locked to liquid, and the size, recipient, and context of that batch are what analysis is about.

Why projects lock tokens at all

Locking is a credibility device. Imagine a project that raised money by selling thirty percent of its supply to venture funds at an early stage price, then listed the token publicly at twenty times that price. If the investors could sell immediately, the rational move would be to dump everything into the listing hype, crush the price, and move on. Everyone who bought at listing would be exit liquidity. Projects that allowed this quickly found that nobody wanted to buy their tokens at all.

Vesting schedules exist to make the promise of long term alignment enforceable. A team whose tokens unlock over four years has four years of reasons to keep building. An investor with a one year cliff cannot flip the token at listing no matter how tempting the price. The lock converts a verbal commitment into a mechanical one, and because the schedule is public, the market can price the commitment instead of guessing at it.

Locking finally serves a signaling function that has nothing to do with mechanics. When a team accepts a four year schedule and investors accept a one year cliff, they are publishing their own confidence interval. Short schedules whisper that insiders want optionality. Long schedules, especially ones the team imposed on itself beyond what any exchange required, tell the market that the people with the most information expect the token to be worth holding. Markets read these signals imperfectly, but they read them.

Locking also manages the physics of supply. A token’s price is set at the margin, by the balance of buying and selling in liquid markets. Releasing supply gradually gives demand time to grow into it. Releasing it all at once is a flood, and floods move prices the way floods move everything else. The entire discipline of tokenomics, the economic design of a token’s supply, distribution, and incentives, treats the release schedule as one of its central levers.

Cliffs, linear vesting, and the shapes of release

Vesting schedules come in a small number of recognizable shapes, and the shape matters as much as the size. A cliff is a period, commonly six to twelve months after the token generation event, during which nothing unlocks at all. When the cliff ends, a large batch releases at once. Cliffs concentrate sell pressure into a single known date, which is why cliff expiries are the unlock events traders circle on calendars.

Linear vesting releases tokens continuously or in small regular steps, daily, weekly, or monthly, over a defined period. The drip is gentler on price because no single day carries a large release, but it creates persistent background pressure, a steady trickle of new supply that demand must absorb month after month.

Most real schedules are hybrids: a cliff followed by linear release. A typical structure for team tokens might be a one year cliff, then monthly unlocks over the following two or three years. Investor allocations often vest faster than team allocations, and community or ecosystem allocations sometimes have no lock at all, or unlock based on milestones instead of dates. Some projects add non linear schedules, with releases that accelerate or step up at intervals, and a few tie unlocks to performance conditions such as product launches. The token generation event, usually shortened to TGE, marks day zero for most schedules, and many tokens release a small percentage at TGE so that a market can exist at all.

Reading a vesting chart is mostly about learning to see these shapes. A wall of supply at a single future date is a cliff. A smooth ramp is linear release. The steeper the ramp and the taller the walls, the more supply the market will be asked to digest, and the more the token’s future depends on demand showing up on schedule.

Who receives unlocked tokens, and why it matters

The same unlock size can produce completely different market outcomes depending on whose tokens are being released, because different holders face different incentives. Venture investors are the most reliable sellers. Funds have limited lifespans and partners to repay, and a position bought at an early stage price that now trades far higher represents a return that fund managers are professionally obligated to realize. When a large investor tranche unlocks, systematic selling is the base case, not the exception.

Team allocations behave less predictably. Founders and employees have reputational reasons to avoid visible dumping, and many hold for belief or for optics, but personal diversification is a powerful force, and team selling after long cliffs is common enough that markets price it in. Ecosystem and treasury unlocks are different again: those tokens usually flow to grants, market making, or incentives instead of directly to exchanges, though grant recipients frequently sell what they receive, so the pressure arrives second hand and on a lag. Advisors sit somewhere in between, small in size but often quick to exit. Community allocations, including airdrops, scatter supply across thousands of small holders whose behavior varies from instant selling to permanent holding.

Sophisticated unlock analysis therefore never stops at the headline number. The question is not how many tokens unlock, but how many unlock into hands that are likely to sell, at what cost basis, and into how much liquidity.

How unlocks actually move prices

The mechanical story is simple: unlocks increase liquid supply, and if demand does not rise to meet it, price falls. But the mechanism deserves one more sentence of precision. Price is set by transactions, not by existence, so an unlock only moves the market to the degree that unlocked tokens are sold or that traders act on the expectation of selling. Supply that unlocks into wallets and stays there changes the risk picture without changing the order book. The market story is more interesting, because unlocks are public information, and public information gets traded in advance.

Ahead of a large unlock, traders who expect selling pressure sell first, or open short positions in perpetual futures to profit from the anticipated decline. This front running spreads the price impact across the weeks before the event, and it occasionally produces the counterintuitive pattern traders call sell the rumor, buy the news, where a token falls into an unlock and bounces after it, because the sellers finished selling early. Empirically, the price damage from major unlocks tends to arrive before and during the event, with the days after determined by how much of the released supply actually hits exchanges.

Context decides magnitude. The ratio of the unlock to average daily trading volume matters more than the ratio to market capitalization, because volume measures the market’s absorption capacity. An unlock worth three days of trading volume is a problem; an unlock worth an hour of volume is noise. Market regime matters just as much. Bull markets swallow unlocks that would crater the same token in a bear market, because absorption is a function of demand, and demand is cyclical. And holder cost basis sets the temptation: supply unlocking at a hundred times its purchase price wants to sell far more than supply unlocking underwater.

The clearest evidence that unlocks bind projects came during the 2024 and 2025 cycle, when several teams paused or restructured their own vesting schedules mid stream after watching unlock pressure grind their tokens down. A project that has to renegotiate its own tokenomics to defend its price is admitting that the original schedule asked the market to absorb more than it could.

From ICO free for all to institutional vesting

Vesting was not always standard. During the initial coin offering boom of 2017 and 2018, projects routinely sold tokens with no lockups at all: a whitepaper, a wallet address, and a promise. Teams and early buyers could sell the moment tokens listed, and many did, with predictable results. The wreckage of that era, thousands of tokens that listed, dumped, and died, is the reason vesting became a market requirement instead of a courtesy. Exchanges began expecting lockup disclosures before listing. Venture funds began accepting, and then demanding, multi year schedules as evidence of seriousness. By the early 2020s a token launching without published vesting for insiders read as a warning label.

The professionalization cut both ways. Structured vesting made token launches more credible, but it also standardized the low float playbook, in which a polished schedule defers the supply problem instead of solving it. A four year lockup does not remove twenty five times the float from the future; it just puts the future on a calendar. The modern unlock calendar industry, with dashboards, alerts, and analytics products tracking every scheduled release across the market, exists precisely because vesting became universal. What was once a question of whether insiders were locked at all became a question of exactly when the locks expire, and an entire analytical discipline grew in the gap.

The next stage of that evolution is already visible: on chain vesting contracts that anyone can audit, third party verification services, and standardized disclosure formats. The direction of travel is toward supply schedules as verifiable public infrastructure, which raises the analytical bar. When everyone can see the calendar, seeing it is no longer an edge. Interpreting it is.

The low float, high FDV trap

The defining supply structure of the recent cycle was the low float, high FDV launch. A project lists with a small fraction of total supply circulating, sometimes under ten percent, while the fully diluted valuation, the price of all tokens that will ever exist, implies a number many multiples higher. The small float makes the price easy to support at listing. The enormous locked overhang means years of scheduled unlocks stand between the listing price and the day the token’s market cap honestly reflects its supply.

The arithmetic is unforgiving. If a token trades at a two billion dollar fully diluted valuation with eight percent circulating, then over the coming years roughly twenty five times the current float will be released. For the price simply to stay flat, new demand must absorb all of it. Buyers of such tokens are, whether they realize it or not, betting that demand will grow faster than a supply schedule designed years earlier by people who bought at a fraction of the current price. The bet occasionally pays. The base rate does not favor it.

Markets learned this lesson expensively. Token after token from the low float era spent months in structural decline as unlocks arrived on schedule and demand did not, and by the middle of the cycle, unlock calendars had become one of the most watched datasets in DeFi and beyond. Aggregate unlock volume across the market now runs into billions of dollars in heavy months, and traders treat clusters of large unlocks as a marketwide supply headwind, particularly for assets far down the liquidity curve.

What big unlocks look like in practice

A few well known episodes show the full range of outcomes. Arbitrum’s ARB, one of the largest airdropped tokens of its generation, spent much of its first two years grinding lower as investor and team tranches unlocked month after month into demand that never matched the schedule, becoming the reference example of structural unlock pressure on a fundamentally serious project. The token’s technology kept shipping; the supply kept arriving; the price reflected the arithmetic.

AltLayer provided the reference example of a project blinking. After its first major unlock in mid 2024 hit the price hard, the team announced a six month vesting pause covering investors, team, advisors, and treasury. The pause relieved the calendar but not the market, and the token’s struggles afterward became a case study in why rescheduling supply does not manufacture demand.

Pump.fun’s PUMP token compressed the entire lifecycle into months. The July 2025 sale raised over a billion dollars at a valuation the open market immediately began stress testing, and every subsequent tranche movement from team and treasury wallets was tracked by thousands of traders in real time, a reminder that for high profile tokens, unlock analysis now happens wallet by wallet, not just date by date.

And Pi Network became the retail era’s unlock story: roughly 1.21 billion tokens scheduled to release across 2026 against thin exchange liquidity, an overhang so large relative to volume that the unlock calendar itself became the primary narrative around the asset. Whatever one thinks of the project, the episode taught millions of retail holders the vocabulary of cliffs, floats, and absorption for the first time.

The pattern across all four is consistent. Unlocks did not decide whether these projects mattered. They decided when the market was forced to render a verdict on how much demand actually existed at the prevailing price.

Reading an unlock calendar like a professional

Several platforms track unlock schedules across the market, including Tokenomist, CryptoRank, DropsTab, and CoinGecko, and they present broadly the same data: upcoming unlock dates, sizes in tokens and dollars, percentages of circulating supply, and the allocation buckets involved. The skill is in the interpretation, and it reduces to five questions.

First, how large is the unlock relative to circulating supply? Below one percent is usually noise; above five percent deserves attention. Second, how large is it relative to daily trading volume? This is the absorption test, and it is the single most predictive ratio. A useful rule of thumb: if the unlocked value exceeds three to five days of average volume, absorption will be slow and the price will likely do the absorbing. Third, who receives the tokens? Investor and team tranches carry the highest sell risk; ecosystem and treasury tranches are slower burning. Fourth, what is the recipients’ cost basis? Deeply profitable supply sells harder. Fifth, what happened at this token’s previous unlocks? Past behavior around identical events is the closest thing unlock analysis has to a controlled experiment.

Two practical refinements separate careful traders from calendar tourists. Cliff events deserve more respect than equivalent linear amounts, because concentration in time is what overwhelms order books. And exchange flow data, where available, tells you whether unlocked tokens are actually moving toward venues where they can be sold, or sitting in the same wallets that received them. Tokens that unlock and do not move are potential supply; tokens that unlock and flow to exchanges are incoming supply. On chain analytics platforms make this distinction observable in near real time, and the gap between the two is often where the actual trade lives.

What unlock analysis cannot tell you

Unlock data describes supply mechanics, and supply is only half of any price. A token with a brutal unlock schedule and explosive demand growth can rise through every release date, which is exactly what the strongest projects of every cycle have done. A token with a clean, fully vested supply and no demand will still go to zero, just without a schedule announcing it. Unlocks set the height of the wall; they say nothing about whether the buyers on the other side can climb it.

The data also cannot capture private arrangements. Locked tokens are routinely hedged through over the counter deals and derivatives, meaning the economic selling may have happened long before the unlock date, with the on chain release a mere formality. Conversely, some unlocked supply is contractually committed to market makers or custody and cannot hit the market as fast as the calendar implies. On chain vesting contracts have also occasionally diverged from published schedules, in both directions, which is why serious analysts verify the contract instead of trusting the documentation.

Treat unlocks the way professionals treat them: as one high quality, freely available input among several. In a market where edges are scarce and expensive, a public calendar of exactly when supply arrives, from Solana majors to the long tail of meme coins, is a gift. It is not a trading system. It is a schedule of when the questions get asked; demand still writes the answers.

Frequently asked questions

What is a token unlock in crypto?

A token unlock is a scheduled event in which previously locked tokens become transferable and enter circulating supply. Unlocks follow a vesting schedule the project defined in advance, and they typically release tokens to teams, early investors, advisors, or ecosystem funds.

What is the difference between vesting and unlocking?

Vesting is the overall timetable that governs how locked allocations are released over time. An unlock is a single event within that timetable. A project has one vesting schedule but many individual unlock events.

What is a cliff in a vesting schedule?

A cliff is an initial period, often six to twelve months, during which no tokens from an allocation are released. When the cliff ends, a large batch unlocks at once, which concentrates potential sell pressure into a single date.

Are token unlocks always bearish?

No. Unlocks add supply, but the price outcome depends on demand, on how much of the released supply actually gets sold, and on how much was priced in beforehand. Some tokens fall into an unlock and recover afterward once the anticipated selling clears.

How do I check when a token unlocks?

Unlock schedules appear in project tokenomics documentation and on tracking platforms such as Tokenomist, CryptoRank, DropsTab, and CoinGecko. These tools show upcoming dates, sizes, percentages of supply, and which allocation groups receive the tokens.

What is a low float, high FDV token?

It is a token that lists with a small share of total supply circulating while its fully diluted valuation implies a much larger market value. The structure supports the listing price but leaves years of scheduled unlocks that future demand must absorb.

Why do venture capital unlocks cause more selling?

Venture funds have finite lifespans and obligations to return capital to their partners, and their tokens were typically bought at prices far below market. Realizing those gains when tokens unlock is standard practice, so investor tranches carry the highest sell risk.

Can a project change its vesting schedule?

Sometimes, if governance or the token contract allows it. Several projects have paused or extended vesting to relieve price pressure. Any change should be publicly disclosed, and unexplained deviations between the published schedule and on chain behavior are a warning sign.

This article is for educational purposes only and does not constitute financial or investment advice. Vesting structures and unlock data vary by project and change over time. Details are accurate as of July 14, 2026.

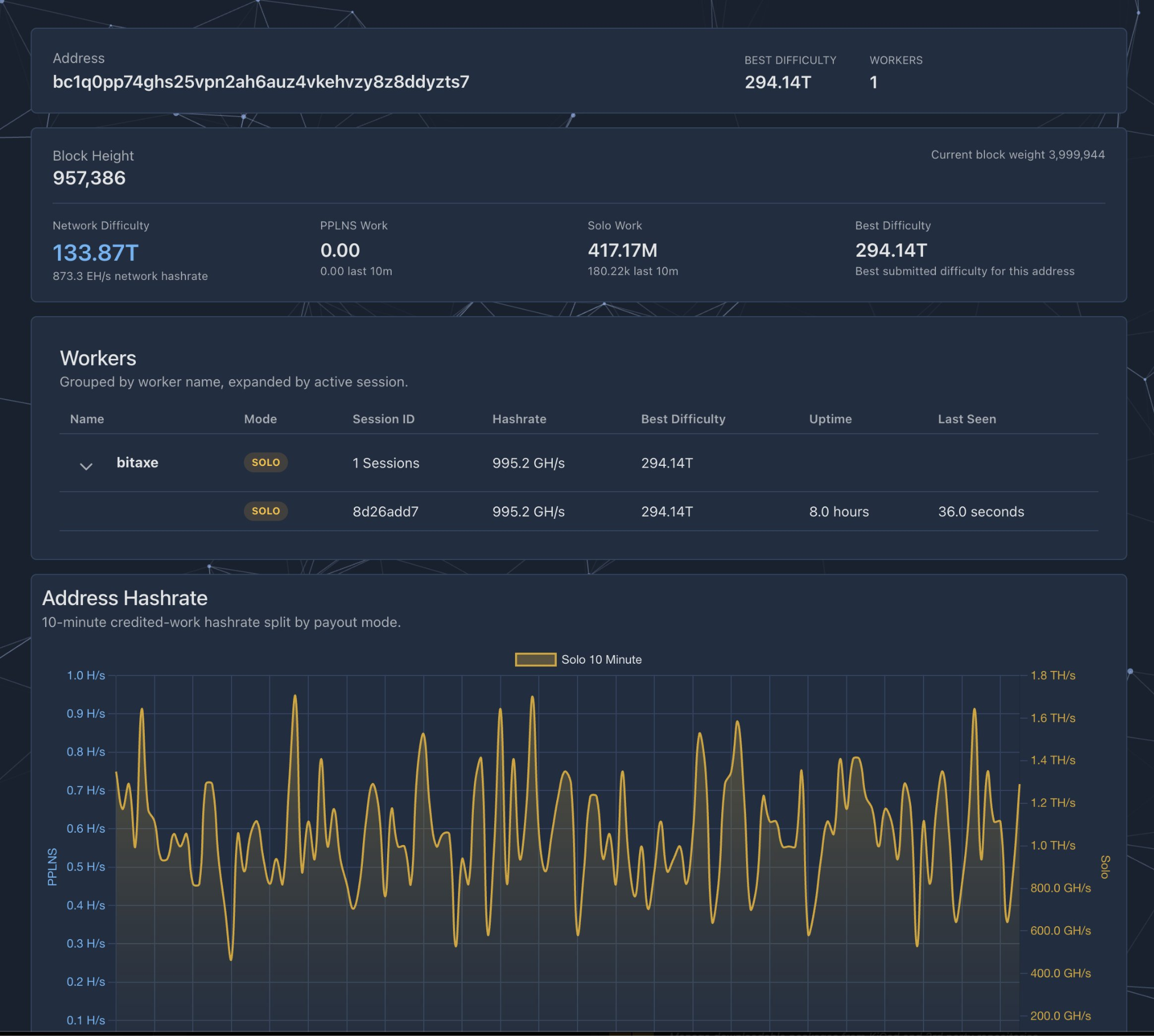

A solo Bitcoin miner hit the jackpot and validated a solo block with a single Bitaxe mining rig, marking a rare win that beat massive statistical odds.

The retail Bitcoin miner secured a 3.125 Bitcoin (BTC) block reward, currently worth about $200,000, on Friday at block number 957382, according to blockchain data from mempool.space.

The miner was using a single Bitaxe mining rig, according to the BTC mining pool Public Pool. The Bitaxe was a budget, lower-power Bitcoin miner that costs less than $200 and has a hashrate of about 1 terahash per second (TH/s), which is a tiny fraction of the global Bitcoin network.

The solo block reward shows that even a sub-$200 investment in a mining rig can lead to a statistically rare payday for retail miners.

Another solo Bitcoin miner validated a solo block in April, through CKPool’s solo mining service. Earlier in February, another retail miner validated a solo block using rented hashrate from a mining provider, meaning that he didn’t own the physical mining rig that solved the block.

Source: Public Pool

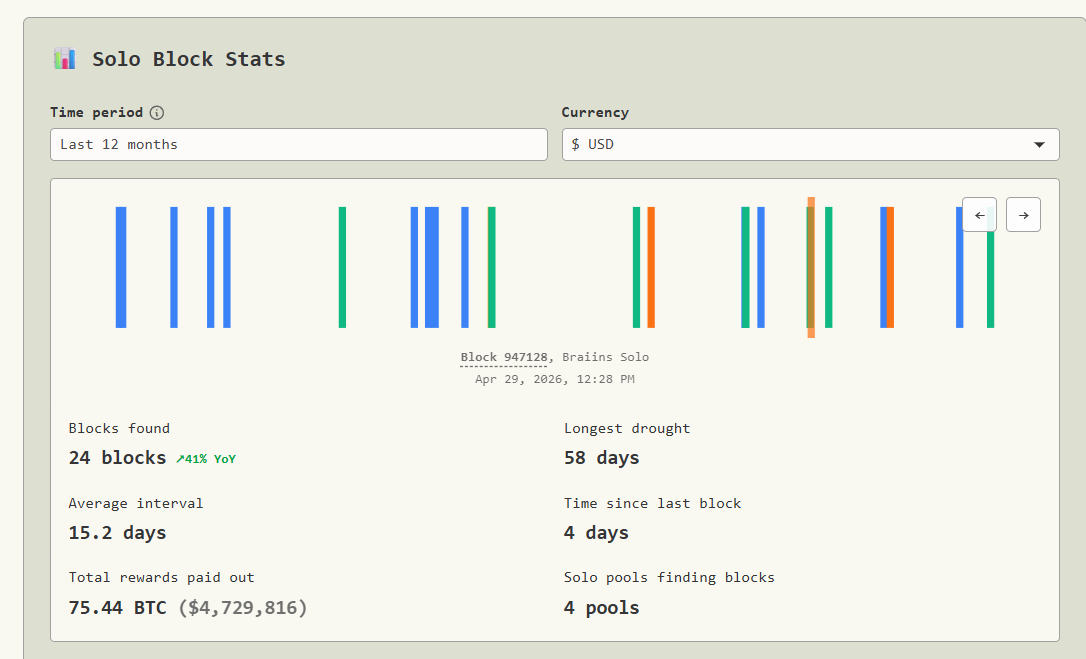

Solo BTC miners bag $4.7 million during the past year

While mining a solo block is statistically rare, this marks the 12th Bitcoin block validated by a hobby-level miner so far in 2026, pushing the past 12 months’ total payouts to more than $4.7 million for retail miners.

Solo block stats, one-year. Source: Bennet.org

Solo blocks mined increased by 41% year-on-year, as solo miners have validated a total of 24 blocks during the past year, according to solo miner data aggregator Bennet. This brings total rewards paid to solo miners to 75.4 Bitcoin, or $4.7 million, for the past year.

Related: Bitcoin whale moves $188M for first time in 7 years

The average interval for solo Bitcoin blocks stands at 15.2 days, while the longest drought without a successful solo block stands at 58 days.

Magazine: Bitcoin nearing late stages of bear market: Jamie Coutts, Real Vision

BitMine Immersion Technologies posted revenue of $46.5 million in the three months ended May 31, a 22x jump from a year earlier, even as a $9.1 billion nine-month net loss dominated its latest filing.

The loss stems almost entirely from a non-cash markdown on the company’s Ethereum (ETH) holdings. Underneath it, BitMine’s staking business scaled from almost nothing into the firm’s dominant revenue source.

Staking Drives BitMine’s Revenue

According to BitMine’s filing, revenue from staking and validation reached $45.7 million, about 98% of the total. A year earlier, that line was zero. The rest came from small self-mining and consulting lines, together under $800,000.

Follow us on X to get the latest news as it happens

As of the latest data, BitMine has staked 4.9 million ETH, roughly 85% of its holdings, through its MAVAN validator platform. The company projects annualized staking revenue near $242 million.

“Annualized staking revenues are now projected at $242 million. And this 4.9 million ETH is 85% of the 5.77 million ETH held by Bitmine. Bitmine’s own staking operations generated a 7-day yield of 2.70% (annualized),” said Tom Lee.

That income rests on a large ETH position. As of July 12, BitMine holds 5.77 million ETH, worth roughly $10.5 billion and equal to 4.8% of supply. The stake makes it the largest corporate ETH treasury.

The trend extends well beyond BitMine. One recent study found that staking accounted for 60% of disclosed revenue across listed ETH treasury firms in 2025.

A $9 Billion Loss That Missed the Numbers

The headline loss looks alarming, but the timing matters. BitMine’s $9.1 billion nine-month net loss came almost entirely from a $9.04 billion unrealized markdown on its digital assets, according to its SEC filing.

That damage landed as the value of its ETH holdings fell. In the three months ended May 31, the net loss narrowed to $83.6 million.

The period’s operating loss was $11.9 million. The bigger hit came from a $92 million loss on derivative contracts.

The split screen defines BitMine’s model. Its reported earnings will swing with ETH’s price, while its staking operation generates a growing revenue stream. The coming months will test whether staking income can offset that volatility.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post BitMine Revenue Jumps 22x Even as It Posts $9 Billion Net Loss appeared first on BeInCrypto.

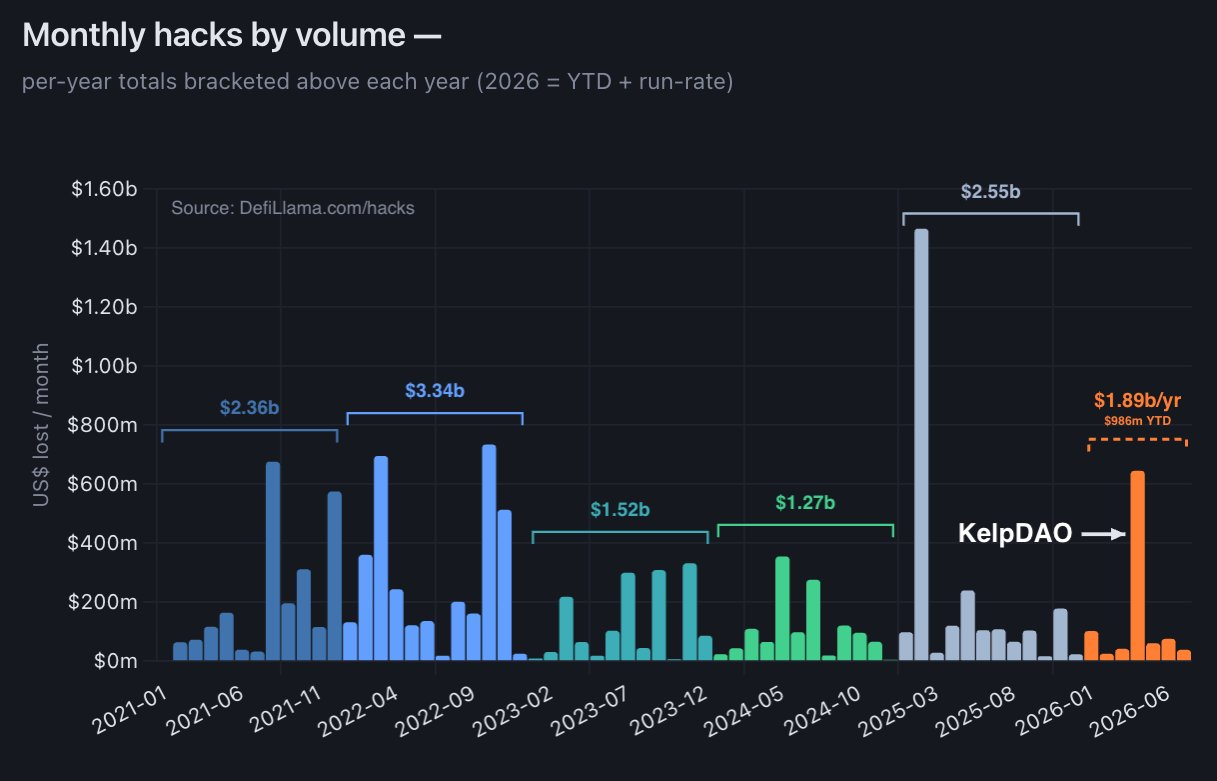

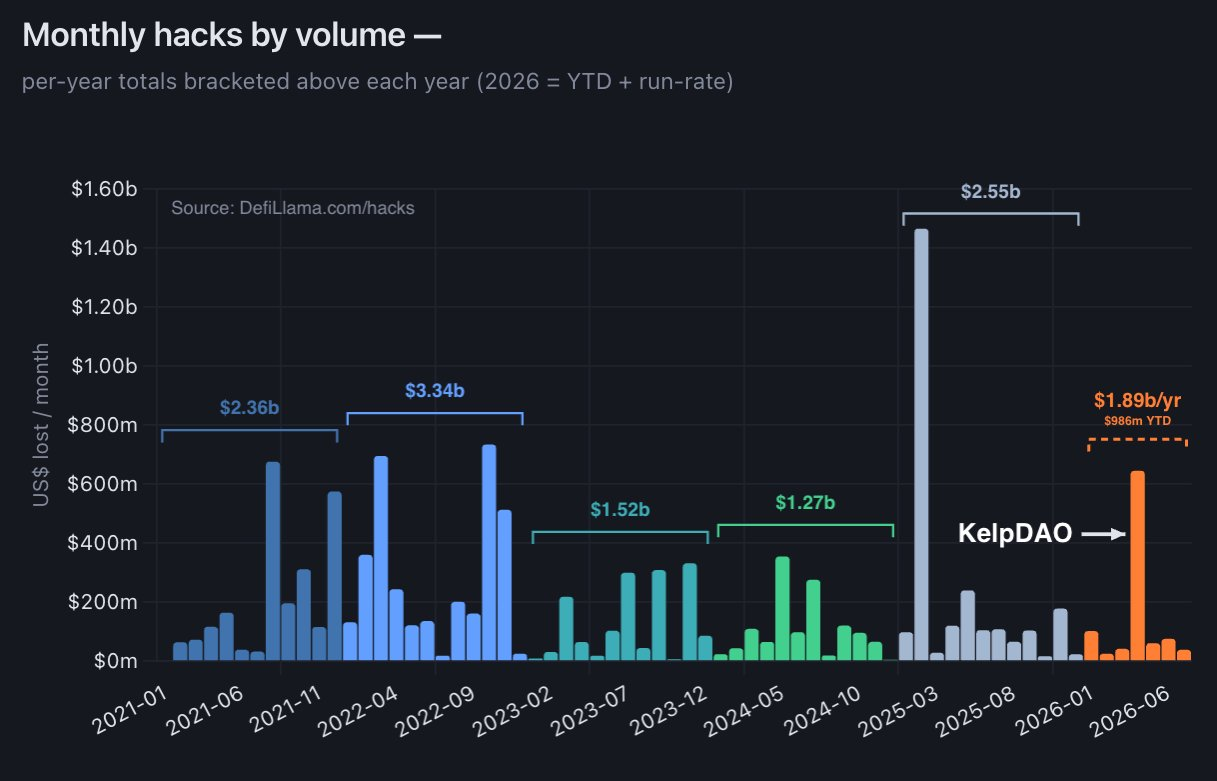

Fears that artificial intelligence would trigger a wave of catastrophic decentralized finance (DeFi) hacks in what was coined as a “hackpocalypse” have not materialized, according to Dragonfly managing partner Haseeb Qureshi.

While the incident count grew to a record high, the median size of hacks has dipped below $500,000 this year, down from over $2 million in 2025. Qureshi argued that this shows malicious actors using AI are targeting “small protocols and abandonware” while larger DeFi protocols have fortified themselves against AI’s threat.

Excluding outlier months with large incidents, such as the Bybit hack in February 2025 along with the Drift Protocol and KelpDAO exploits in April of this year, 2026 has still seen less value hacked per month than the previous year, said Qureshi.

The comments come in response to concerns shared by blockchain security platform OpenZeppelin’s founder, Manuel Aráoz, who said that he considers “all of DeFi unsafe,” citing the growing ability of AI coding agents to identify smart contract vulnerabilities.

Broader industry datasets, which include centralized platforms, wallet compromises and phishing, as well as DeFi exploits, offer a less reassuring picture. In April, crypto hacks surged, resulting in losses of around $644 million, marking an over one-year high last seen in February 2025 when the $1.4 billion Bybit hack pushed monthly losses to $1.46 billion, according to DefiLlama.

Source: Haseeb

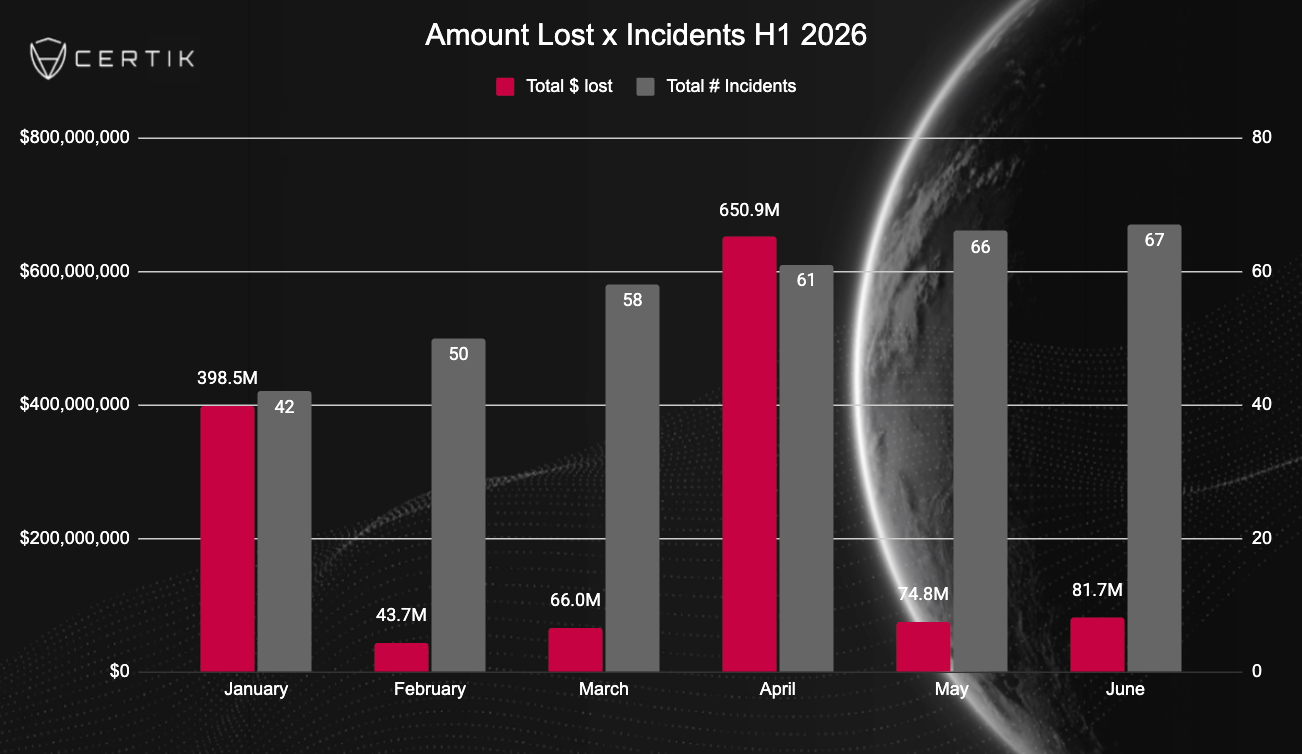

Crypto hacks fall 47% in H1, but crypto industry not necessarily safer: CertiK

Losses to cryptocurrency hacks fell 46.8% year-on-year to $1.32 billion in the first half of 2026, but blockchain security company CertiK argued that the Web3 industry’s lower headline losses do not necessarily mean the industry is safer.

Related: Belgian police arrest suspected phishing gang leader tied to $572K theft

While it marks a significant drop in dollar value, last year’s figures were skewed by the $1.4 billion Bybit hack, the largest in crypto history, CertiK told Cointelegraph.

During the second quarter of 2026, over 70% of the losses stemmed from the KelpDAO and Drift Protocol exploits, which were largely attributed to North Korean state-sponsored hackers.

Monthly change in crypto exploit amounts and number of incidents across H1. Source: CertiK

The data underscores the continued threat that North Korean hackers pose to the crypto industry, having stolen more than $6 billion worth of crypto since 2017, TRM Labs estimated in April.

Magazine: Does Botanix’s failure prove Bitcoiners don’t care about DeFi?

Coinbase, among others, filled that gap in May 2025. Under x402, a server that wants payment answers a request with a 402 and a price. The client signs a stablecoin transfer, usually USDC, resends the request with the payment attached, and gets the data. The exchange takes seconds and needs no account, no card, and no prior relationship between the two sides.

That is why the AI industry cares. An autonomous agent cannot open a bank account, pass a credit check or sign a SaaS contract, but can sign a transaction. Google has wired x402 into its own agent payments protocol, and Cloudflare ships it in its agent toolkit.

The announcement included no usage figures, though x402 publishes them on its own homepage. The protocol handled about 75 million transactions over the past 30 days, or roughly 29 every second, moving about $24 million between some 94,000 buyers and 22,000 sellers.

That works out to an average payment of about 32 cents, meaning the machine-to-machine thesis works as designed, as no card network can process a such small charges profitably.

Still, $24 million a month is a fraction of what any of x402’s premier members move in a day.

PI crashed 40% this week after a massive sell-off that drove it to consecutive all-time lows. However, it has rocketed by 10% since those lows, begging the question of whether the bottom is in.

PI Network (PI) Price Predictions: Analysis

Key support levels: $0.07

Key resistance levels: $0.10, $0.13, $0.16

PI Crashed to $0.07

PI just had one of the worst weeks in 2026 after the price lost support at $0.10. With this level turned into resistance, sellers rushed for the exits and sent the price into a nose-dive to $0.07, which became its latest record low.

With confidence gone, buyers had vanished. For example, in the past 10 days, only one day closed in the green. This shows that the sentiment is extremely bearish and the downtrend has entered a new phase where a bottom could be found much quicker.

More positive news came in the past several hours, with PI finally rebounding to $0.08 as of press time. However, it remains to be seen whether this is another dead-cat bounce.

Sell-Side Volume Exploded

As soon as the support at $0.10 was lost, sell volume began to pick up. This only made things worse and likely led to cascade liquidations that put even more pressure on the falling price.

While the sell pressure has decreased compared to yesterday, the day is not over, and this could still change. The price held above $0.07 and bounced to $0.08, but this could very well be just a temporary pause before new lows.

Momentum Indicators Are at Extremes

Due to heavy selling pressure, the momentum indicators have reached extreme levels. For example, the daily RSI is at 12 points, a level never seen before for this cryptocurrency. Extremes are also the place where bottoms are found.

Hopefully, this price action will bring about an end to the downtrend and allow PI to consolidate and confirm a bottom. If the support at $0.07 won’t hold, then buyers will likely retreat to $0.06 or even $0.05. The current resistance is at $0.10.

The post Pi Network Price Predictions for This Week as PI Surges 10% in 24 Hours (July 15) appeared first on CryptoPotato.

Crypto World

Finassets Raises Affiliate Revenue Share to 40%, Becoming One of the Highest-Paying Crypto Affiliate Programs

[PRESS RELEASE – Marbella, Panama, July 15th, 2026]

Finassets, a crypto payment gateway for businesses, announced an increase to its partner revenue share. The first-year referral rate rises to 40% of the processing revenue a referred merchant generates. From year two, the rate continues at 20% for five additional years while the merchant keeps processing, extending the total partner earning window to six years per referral, with the term extendable based on the merchant profile.

Payout speed, contract length, and dashboard visibility are among the key considerations affiliate marketers weigh when comparing crypto affiliate programs, and this update puts Finassets among the top crypto affiliate programs open to B2B partners.

A different model from trading-based programs

Many crypto exchange affiliate programs and trading platforms base payouts on trading fees generated by active traders, tying affiliate income to short-term trading volume through a fixed commission plan or a minimum payout threshold. Finassets ties partner earnings to a merchant’s ongoing processing volume instead — a relationship that can continue for the full six-year term.

One agreement, six years of revenue share

- Apply to become a partner. Submit an application and our team handles onboarding and sets clear terms from day one, with a personal referral link and dashboard account.

- Finassets onboards the merchant. KYB, compliance, and integration are handled entirely by Finassets.

- The partner earns. Revenue share is calculated per merchant and paid same-day, in crypto. The term can be extended based on the referred user profile.

A merchant referred through a partner’s affiliate link and processing $500,000 a month generates about $2,000 a month in processing fees at Finassets’ 0.40% rate. Here’s how that translates into partner earnings:

Based on a merchant processing $500,000/month at Finassets’ 0.40% fee. Illustrative; actual earnings depend on the merchant’s processing volume.

“Most cryptocurrency affiliate programs ask partners to keep generating referrals just to keep earning,” said Vitalijs F., CEO of Finassets. “We built this revenue share model so one merchant relationship can keep paying out for years, without additional marketing efforts from the partner after the introduction.”

Real-time visibility, reliable payouts

The agent dashboard tracks referral volume and revenue share per merchant in real time, with a full transaction history for reconciliation and one-click withdrawals. Deposits are typically credited within about 30 seconds of network confirmation, and partners are supported by dedicated account managers who respond quickly. Payouts are same-day, in crypto. Finassets supports 70+ cryptocurrencies across its full product suite, the same infrastructure referred merchants use to process payments.

The affiliate program is open to eligible B2B participants in selected international markets, subject to Finassets programme terms and applicable jurisdictional requirements.

More information and the partner application: https://www.finassets.io/en/affiliate-program/

About Finassets

Founded in 2021, Finassets is a Panama-registered crypto payment gateway supporting cross-border and crypto-driven businesses across eligible markets. Finassets provides crypto invoicing, payment links, payment buttons, mass payouts, API integration, crypto checkout, and an affiliate program within a structured, transparent environment for crypto payment processing.

Website: https://www.finassets.io

The post Finassets Raises Affiliate Revenue Share to 40%, Becoming One of the Highest-Paying Crypto Affiliate Programs appeared first on CryptoPotato.

The United Kingdom and United States have agreed to pursue closer coordination on stablecoin regulation, cross-border payments and tokenized financial markets.

Summary

- UK and US regulators seek aligned stablecoin rules while preserving competition and cross-border market access.

- Stablecoins used as money should hold one-to-one reserves and protect holders during issuer insolvency proceedings.

- Officials will explore pathways allowing regulated stablecoins from either jurisdiction to enter the other market.

The two governments also plan to explore how regulated stablecoins issued in one country could gain access to the other market.

The commitments appear in a joint UK-US statement on stablecoins released on July 14. The statement forms part of recommendations from the Transatlantic Taskforce for Markets of the Future, which the two governments established in September 2025.

UK and US set common stablecoin principles

The two governments said stablecoins can support payments, settlement and capital market transactions when regulators apply proper safeguards. They plan to seek “comparable outcomes for comparable risks and activities” while allowing each country to develop requirements under its own legal framework.

The approach does not require identical regulations. Instead, officials want to reduce unnecessary differences that could block cross-border activity. The governments also said they would avoid rules that impose costs out of proportion to the risks or create unnecessary barriers for new competitors.

As reported by crypto.news, the agreement comes as stablecoin rules remain a major policy issue in Washington. U.S. lawmakers and banking groups continue to debate how digital dollar products should interact with traditional banks and financial markets.

Stablecoins should maintain at least 1:1 backing

The joint statement says stablecoins presented as money should hold at least one dollar or equivalent in high-quality liquid assets for every unit issued. Each country will decide which reserve assets qualify under its domestic framework.

Issuers should also separate reserve assets from their own corporate funds. The governments said holders should receive timely redemptions and clear information about their legal rights. In an issuer failure, holders should have a protected claim on reserves, including priority over other creditors where domestic law allows it.

The principles broadly match the direction of U.S. stablecoin regulation under the GENIUS Act. The Treasury began proposing implementation rules in 2026 as the United States prepares its federal framework for payment stablecoin issuers.

Governments explore cross-border stablecoin access

The UK and US plan to examine a clear pathway that could allow stablecoins regulated in either jurisdiction to reach customers and markets in the other. Any access arrangement would remain subject to each country’s laws and regulatory processes.

Both governments also support fair, risk-based access to banks and other financial services for lawful regulated digital asset companies. They said stablecoins could serve as settlement instruments in securities and commodities markets when firms meet the required safeguards.

The statement does not create automatic mutual recognition or approve any specific stablecoin for cross-border distribution. Regulators still need to develop the legal routes and standards required to put the plan into practice.

Tokenized finance forms part of wider cooperation

The agreement extends beyond stablecoins. Under the broader Transatlantic Taskforce recommendations, the two countries plan to work with a private-sector group to test cross-border uses for tokenized assets over a one-year period.

The SEC, CFTC, FCA and Bank of England will also seek common approaches to areas including tokenized securities settlement and the possible use of stablecoins or tokenized money market funds as collateral at clearing houses.

The recommendations leave both countries free to complete their own regulatory processes. Their stated aim is to reduce cross-border friction while giving regulated stablecoins and tokenized financial products clearer routes between two major global financial markets.

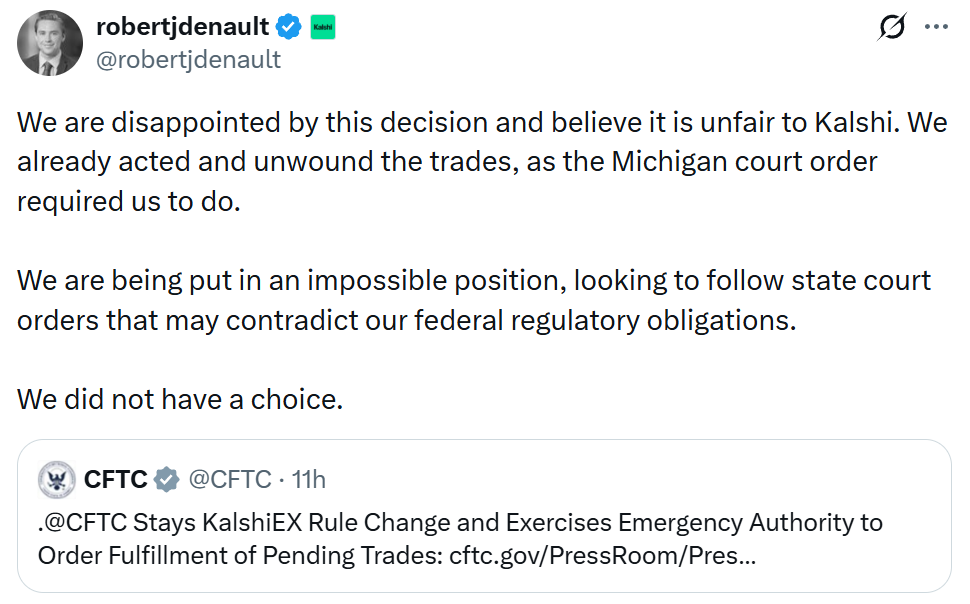

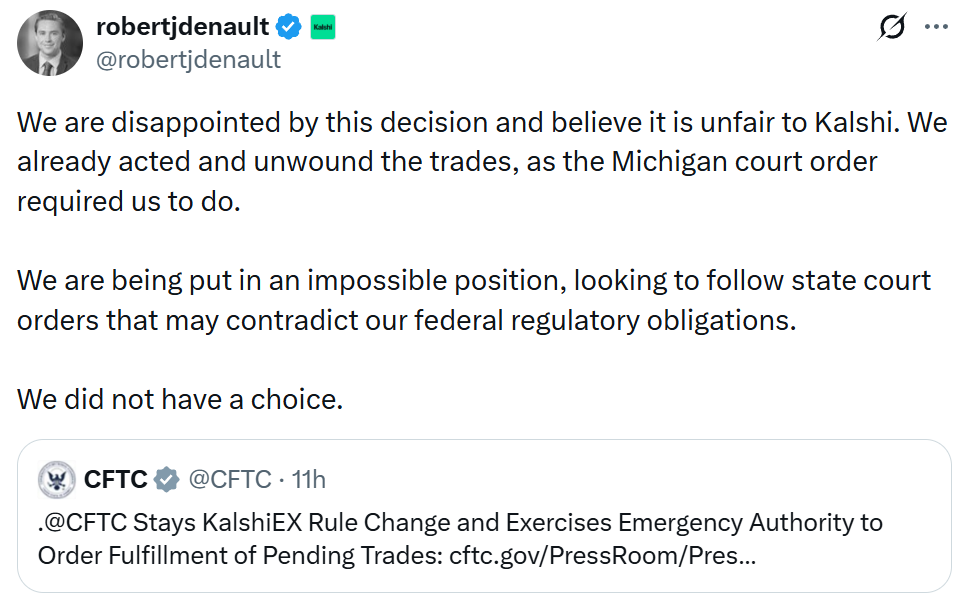

Kalshi says it is being put in an “impossible position” after the US commodities regulator on Tuesday said it was blocking the prediction market platform from canceling trades in Michigan, contradicting a recent state court order.

On June 29, Kalshi was ordered by Ingham County Circuit Court Judge Rosemarie Aquilina to cease offering sports betting contracts to Michigan users while a lawsuit over whether Kalshi violated the state’s sports betting laws plays out. The Commodity Futures Trading Commission ordered Kalshi on Tuesday not to comply with the state order and continue operating.

“We are disappointed by this decision and believe it is unfair to Kalshi,” Robert DeNault, the company’s head of enforcement and legal counsel said in a statement on X.

“We already acted and unwound the trades, as the Michigan court order required us to do. We are being put in an impossible position, looking to follow state court orders that may contradict our federal regulatory obligations. We did not have a choice.”

Source: Robert DeNault

The conflicting orders highlight an unresolved regulatory divide between the CFTC and nearly two dozen state regulators over which authorities have jurisdiction over prediction markets. The CFTC said Michigan was the first state to attempt to interfere with executed derivatives transactions.

“Canceling trades that have already been executed is an unprecedented step that risks a cascading effect on the entire marketplace and undermines the certainty in contracting that is a necessary component of a functioning market,” said Selig.

“The Commission will not allow states or state courts to bully registered entities into violating the Commodity Exchange Act and CFTC regulations.”

A Kalshi spokesperson said it was reviewing the CFTC’s order and considering its next steps, according to Reuters.

Related: OpenAI quietly adds Kalshi World Cup odds to ChatGPT: Report

Speaking on Fox Business on Friday, CFTC Chair Michael Selig said it is “critical” that the regulator maintains its regulatory authority over prediction markets.

“We’ve sued nine states now, and we’ll continue to sue any state that attempts to impose criminal or civil fines against CFTC-registered exchanges.”

Magazine: Strategy became a symbol of the dot-com crash: Could history repeat?

Mizuho has downgraded Circle Internet Group from Neutral to Underperform and cut its price target from $85 to $50, citing competition from Open USD.

Summary

- Mizuho cut Circle’s price target to $50, warning Open USD could further squeeze stablecoin margins.

- Open USD shares reserve earnings with partners, challenging Circle’s existing distribution economics around USDC globally.

- Circle also faces margin pressure from Hyperliquid revenue-sharing terms despite recent federal banking approval milestone.

The Japanese investment bank said the stablecoin model could pressure the economics behind Circle’s USDC business.

According to a CoinDesk report, analysts led by Dan Dolev said Open USD “could fundamentally alter CRCL’s business model” by changing how reserve income flows to distributors. Circle shares traded at $62.63 when the report was published.

Mizuho cuts Circle’s 2027 earnings outlook

Mizuho raised its estimate for Circle’s distribution and transaction expense ratio in 2027 from 64% to 73%. The bank also lowered its adjusted EBITDA forecast from $1.09 billion to $699 million, about 25% below the analyst consensus cited in the report.

The bank said higher interest rates could support reserve income but may not fully offset pressure from changing stablecoin economics. Its concern centers on how much yield Circle can retain after paying distribution partners, including companies that help USDC reach users and financial platforms.

Open USD challenges the existing stablecoin model

Open USD was announced on June 30 by Open Standard, with more than 140 companies participating in its ecosystem. Partners include Coinbase, Mastercard, Stripe and BlackRock. The project says businesses will be able to mint and redeem the stablecoin without fees or artificial volume limits.

Under the model, partners receive reserve earnings after a small management fee covers operating costs. That differs from Circle’s structure, where reserve income is generated before revenue-sharing payments to major distribution partners. As previously reported, Open USD’s announcement raised questions over whether Circle’s own partners could support a rival while continuing to distribute USDC.

Coinbase relationship adds another pressure point

Mizuho also pointed to Circle’s revenue-sharing relationship with Coinbase. The bank said the agreement is expected to come up for renegotiation in August, and Coinbase’s participation in Open USD could give it more leverage in future talks.

A separate warning came from JPMorgan. As reported by crypto.news, the bank cut earnings forecasts for Circle and Coinbase after a new USDC revenue-sharing arrangement with Hyperliquid. JPMorgan said the deal could reduce reserve income retained by both companies even if USDC usage grows.

Circle continues to expand USDC infrastructure

The downgrade comes as Circle expands its regulatory and payments footprint.Circle data showed USDC circulation at about $73 billion as of July 13, down from $77 billion at the end of the first quarter.

Circle also recently received final approval to establish Circle National Trust. The federally regulated entity will initially focus on digital asset custody for Circle and its affiliates, with possible future services for selected institutional clients.

The company is also expanding USDC use in Asia. JCB and Circle announced a pilot covering cross-border treasury transfers and possible merchant payments in Japan. The project will start with JCB’s internal transfers before the companies assess wider retail payment uses.

Mizuho’s downgrade focuses on Circle’s ability to protect margins as stablecoin competition changes how reserve income is shared. Open USD has not proved it can match USDC’s distribution or liquidity, but its partner-led model creates a new pricing benchmark. Circle’s earnings path will depend partly on USDC supply, interest rates and future revenue-sharing agreements.

A solo Bitcoin miner has validated a block using just one low-cost Bitaxe machine, landing the standard 3.125 BTC reward in what looks like a statistically unlikely outcome. The win underscores how, even in today’s highly competitive mining environment, hobby-scale setups can still occasionally hit the lottery.

According to blockchain data from mempool.space, the miner solved block number 957382 on Friday and received 3.125 BTC, worth roughly $200,000 at current market valuations. The miner’s setup reportedly consisted of a single Bitaxe rig, as noted by the mining pool Public Pool in a post on X.

Key takeaways

- A retail solo miner validated block 957382 and received the 3.125 BTC reward, per data from mempool.space.

- The winning setup reportedly used a single Bitaxe miner, credited by Public Pool on X.

- Bitaxe is positioned as a low-power, budget device—its hashrate is about 1 TH/s, tiny compared to the network.

- Solo block wins remain rare but are still happening regularly enough to add up: Bennet data places the last 12 months’ solo payouts above $4.7 million.

How a single miner found a solo block

The defining detail in this case is not the size of the reward—every successful solo miner receives the standard block subsidy—but the scale of the hardware involved. Public Pool attributed the find to a lone Bitaxe mining rig.

As described by Bitaxe, the device is a budget, lower-power Bitcoin miner with an estimated hashrate around 1 TH/s, according to the article’s referenced materials. In practical terms, that figure is extremely small relative to the overall Bitcoin network hashrate, which is why solo block wins are usually framed as long-shot events for individual miners.

Yet the nature of mining is that the network doesn’t “know” how small your share is—only probability matters. That’s what makes these events notable for retail miners: even when odds are against you, the process can still produce occasional, outsized payoffs.

Why this case stands out among recent solo wins

This isn’t the first time a solo Bitcoin block has been found with retail-level participation, but it adds another example of how DIY mining setups continue to surface wins.

Earlier coverage referenced by the source notes that another solo Bitcoin miner validated a block in April through CKPool’s solo mining service. In February, another retail miner reportedly found a solo block using rented hashrate—meaning the miner may not have owned the physical hardware performing the work.

The difference matters because “solo mining” can be implemented in different ways. Solo mining technically means the miner is working toward their own block candidate rather than sharing block rewards with a pool. But the hardware—and whether it is owned outright, rented, or handled through a service—changes the economic reality: electricity costs, capital risk, and the probability profile investors associate with each approach.

In this latest instance, the emphasis is on an owned, single-rig setup using Bitaxe, making it a closer analog to the traditional idea of a hobbyist miner aiming at a solo prize.

Solo mining trends: frequency, droughts, and annual totals

While any single solo block is a rare event, aggregators show that wins are not disappearing. The source points to a year-long tally using Bennet’s solo miner tracking.

According to Bennet data cited in the article, solo blocks mined increased by 41% year-on-year. Over the past year, solo miners validated 24 blocks, pushing total rewards paid to 75.4 BTC—stated as more than $4.7 million in the referenced coverage.

Timing also remains a crucial detail for anyone planning for long horizons. The source reports an average interval of 15.2 days between successful solo blocks, while the longest drought without a solo win was 58 days. These numbers are useful because they help retail participants calibrate expectations: solo mining doesn’t deliver predictable returns, but it also doesn’t mean “never.” The distribution of outcomes can be lumpy—short streaks and longer gaps can both occur.

For investors and builders watching Bitcoin’s ecosystem, this matters because solo participation—even if small—reflects ongoing access to mining at the consumer end. It also highlights that, despite industrial-scale competition, individual miners can still engage meaningfully, at least occasionally, with affordable hardware.

What to watch next for retail solo miners

Retail solo mining remains a game of probability, but the most practical question for the near term is whether these Bitaxe-style, small-hashrate successes keep showing up with enough regularity to sustain interest. Readers should watch the spacing between solo wins and the reported hardware profiles behind them, since both determine how realistic solo mining feels for hobby participants after each new cycle of difficulty adjustments.

Storebrand Q2 profit up 26% as insurance growth drives results, launches buybac

Solo Bitcoin Miner Bags $200k Solo Block with Budget Bitaxe Rig

Caleb Banks Lands a Brutal Bust Prediction

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports5 days ago

Sports5 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

News Videos11 hours ago

News Videos11 hours agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech1 day ago

Tech1 day agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech10 hours ago

Tech10 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos6 days ago

News Videos6 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Sports7 days ago

Sports7 days ago39-year-old Djokovic wins five-hour thriller to enter Wimbledon semis | Other Sports News

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

Tech1 day ago

Tech1 day agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Tech6 days ago

Tech6 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World6 days ago

Crypto World6 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World6 days ago

Crypto World6 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

-

Tech6 days ago

Tech6 days agoClaude’s New Reflect Dashboard Wants To Help You Log Off Of Claude

-

Crypto World7 days ago

Crypto World7 days agoMicrosoft Cuts AI Bill by Replacing OpenAI and Anthropic in Software Products

-

Crypto World6 days ago

Crypto World6 days agoFed minutes June 2026: officials split on rates

You must be logged in to post a comment Login