Crypto World

What is the Howey test? Crypto securities explained

The most important legal test in crypto was written in 1946 to settle a dispute about orange groves. That single sentence explains most of the past decade of American crypto regulation: the confusion, the lawsuits, the exodus of projects to friendlier jurisdictions, and the legislative fight now playing out in the United States Senate.

\Every argument about whether a token is a security eventually arrives at the same four questions, and those questions come from a Supreme Court case decided before the transistor was invented.

The Howey test is the legal standard American courts and regulators use to decide whether an arrangement counts as an investment contract, one of the categories of security defined in federal law. If a crypto token sale meets the test, the full weight of securities regulation applies: registration, disclosure, liability, and the jurisdiction of the Securities and Exchange Commission. If it does not, the token falls outside the SEC’s core authority and, increasingly, into the hands of the Commodity Futures Trading Commission. Billions of dollars, entire business models, and the architecture of pending legislation turn on which side of the line an asset lands.

This guide explains where the test came from, what its four prongs actually require, how the SEC applied it to crypto through a decade of enforcement, what the landmark cases decided and left undecided, how the March 2026 joint SEC and CFTC interpretation reshaped the analysis, and how the CLARITY Act now moving through Congress would change the rules again.

The orange groves that defined a security

In the 1940s, the W. J. Howey Company owned large citrus groves in Florida. To raise money, it sold small tracts of the groves to visitors, mostly tourists with no farming experience, and offered each buyer a service contract under which Howey’s own company would cultivate the land, harvest the oranges, pool the fruit, and remit a share of the profits. Buyers owned land on paper, but in substance they were handing money to a business and waiting for returns.

The Securities and Exchange Commission sued, arguing that these land sales were unregistered securities. The case, SEC v. W. J. Howey Co., reached the Supreme Court in 1946, and the Court agreed with the regulator. It held that an investment contract exists when there is an investment of money in a common enterprise with an expectation of profits derived from the efforts of others. The Court stressed that substance beats form: it does not matter what a scheme is called, what asset is nominally being sold, or how the paperwork is dressed. If the economic reality matches the definition, it is a security.

That flexibility was the point. Congress wrote the securities laws of 1933 and 1934 broadly, after a crash fueled by opaque investment schemes, and the Howey test gave courts a tool that could reach any new packaging of the same old arrangement: money in, promises made, profits expected from someone else’s work. Eighty years later, that packaging includes tokens, and the same interpretive flexibility that let the test reach franchise schemes, whiskey warehouse receipts, and payphone leaseback programs across the twentieth century is what let regulators reach token sales in the twenty first.

The four prongs, one at a time

The test has four elements, and all four must be satisfied. The first is an investment of money. Courts read this liberally: cash qualifies, but so do other crypto assets, property, services, or anything else of value given up in exchange. Buying a token with ether is an investment of money. Even effort, in some framings, can qualify, which is why free distributions raise their own questions, discussed below.

The second prong is a common enterprise. The investor’s money must be pooled with others, or the investor’s fortunes must be tied to those of the promoter, such that everyone rises and falls together. Courts have developed competing doctrines here, horizontal commonality focusing on pooled funds and shared outcomes, vertical commonality focusing on the link between investor and promoter, and the disagreement matters in crypto cases because token buyers do not always have any formal relationship with each other or with the issuer.

The prongs interact, which is why the test resists mechanical application. A strong showing on reliance can compensate for a fuzzy common enterprise; a purely consumptive purchase can defeat the whole analysis even where a promoter exists. Courts weigh the total mix of facts, and small factual differences flip outcomes, which is exactly what makes the test flexible for regulators and maddening for anyone trying to comply in advance.

The third prong is an expectation of profits. The buyer must be motivated primarily by the prospect of financial return, capital appreciation, dividends, yield, instead of by consumption or use. Someone who buys a token to pay for computation on a network looks like a customer; someone who buys the same token because they expect the price to rise looks like an investor. The same asset can be both things to different buyers, which is one of the deep awkwardnesses of applying Howey to tokens.

The fourth prong is that profits must come from the efforts of others. If returns depend predominantly on the managerial or entrepreneurial work of a promoter, a founding team, a company, the arrangement points toward a security. If value arises from broad market forces or the holder’s own activity, it points away. This prong carries most of the weight in crypto disputes: the more a token’s value story depends on a specific team shipping a roadmap, the more it resembles the orange grove.

Why crypto and Howey collided

For its first decade, crypto mostly sold itself as something new, and the law mostly did not care. That ended with the initial coin offering boom of 2017, when thousands of projects raised money by selling tokens to the public on the strength of whitepapers and roadmaps. Functionally, many of these sales were indistinguishable from Howey’s service contracts: money in, a team promising to build, buyers expecting the token to appreciate through that team’s efforts.

The SEC responded first with the DAO Report of 2017, concluding that tokens sold by a decentralized fundraising vehicle were securities, then with a 2019 staff framework listing dozens of factors relevant to applying Howey to digital assets, and then with years of enforcement. The commission’s central position hardened into a slogan associated with its then chairman: nearly every token except Bitcoin looked to the agency like a security, because nearly every token had a team whose efforts buyers relied on. The industry’s counterargument was equally simple: a token is just an asset, like a commodity or a collectible, and an asset is not a contract. The sale of a token might create an investment contract in some circumstances, but the token itself, trading hands years later between strangers on an exchange, carries no promises with it.

Courts spent years sorting between these views, one enforcement action at a time, in what the industry came to call regulation by enforcement. The commission brought actions against issuers over unregistered sales, against exchanges over listing alleged securities, against staking services over yield programs, and against promoters over undisclosed paid touting, naming along the way dozens of specific tokens it considered securities in complaint after complaint. The pattern imposed enormous costs: projects could not know their legal status without being sued, exchanges could not know which listings were lawful, and the question of who regulates crypto, the SEC or the CFTC, stayed unresolved because the answer depended on an asset by asset legal test from 1946.

The cases that drew the map

A handful of decisions define the current terrain. The fundraising cases came first and went badly for issuers. Telegram raised 1.7 billion dollars selling contracts for future tokens and was enjoined in 2020; Kik lost on summary judgment the same year over its token sale; LBRY lost in 2022 despite arguing its token had genuine utility. Together they settled the easy half of the question: selling tokens to fund development, with buyers expecting profit from that development, satisfies Howey.

The hard half arrived with the Ripple litigation. In 2023, a federal judge split the difference in a way that reorganized the entire debate: Ripple’s direct sales of XRP to institutional buyers were securities transactions, because those buyers knew they were funding Ripple’s efforts, but programmatic sales on exchanges to anonymous buyers were not, because a purchaser on an exchange has no idea whether their money goes to Ripple at all and relies on no specific promises. The decision was contested and other judges pushed back on parts of its reasoning, but the core distinction, between a primary sale that creates an investment contract and a secondary trade in the bare asset, became the intellectual center of the reform argument. The token is not the security; the transaction might be. Readers following the XRP saga watched this distinction move billions of dollars in market value in a single afternoon.

The later enforcement wave against exchanges, targeting the listing of dozens of alleged securities, raised the stakes further, because it put the secondary market question directly in play. If tokens themselves were securities, most of the American crypto market was operating illegally. If only certain sales were, most of it was fine. That was the unstable equilibrium the current reform era inherited. Notably, the courtroom record itself stayed mixed: judges in different districts reached different conclusions about secondary sales, some rejecting the Ripple court’s programmatic sales reasoning outright, which guaranteed that without either a definitive appellate ruling or a statute, the question would stay open indefinitely. Uncertainty, not hostility, became the binding constraint on the American market.

The March 2026 interpretation: Howey, narrowed

On March 17, 2026, the SEC issued a formal interpretation of how Howey applies to crypto assets, with the CFTC issuing companion guidance the same day, and it marked the most significant regulatory repositioning since the enforcement era began. The interpretation runs in the industry’s direction on almost every contested point, and although it is not legislation and not binding rulemaking, a Commission level interpretation carries real weight with courts and total weight with the agency’s own staff.

Three moves matter most. First, the interpretation centers the analysis on the issuer’s own representations and promises. A buyer’s expectation of profit counts only if it rests on what the issuer said and did, not on hype from third parties, influencers, or the market at large. Second, it reaffirms that a common enterprise is a genuine, independent requirement, narrowing a prong the agency had previously treated as nearly automatic, and making it harder for secondary market transactions between strangers to satisfy the test. Third, and most consequentially, it describes a pathway for separation: a token born inside an investment contract can shed that status once the issuer’s original promises have been fulfilled or abandoned and no reasonable buyer still relies on them. The asset and the contract can come apart over time, which is exactly what the industry had argued since the Ripple decision.

The interpretation also addressed activities. Protocol mining, protocol staking without discretionary management or guaranteed returns, wrapping of assets, and airdrops generally do not involve the offer or sale of securities when conducted as described. Alongside the interpretation, the agencies jointly classified a first group of sixteen assets, including Bitcoin, Ethereum, and XRP, as digital commodities falling under CFTC jurisdiction. The classification was a watershed and also a warning: what an interpretation gives, a future commission can take back. Only statute is permanent, which is why the legislative fight matters more than any agency document.

What Howey does not cover

Understanding the test also means understanding its limits, because three misconceptions do most of the damage in public debate. The first is that Howey is the whole definition of a security. It is not. Federal law lists dozens of instruments that are securities on their face, stocks, bonds, notes, options, and the investment contract category that Howey defines is the catch all at the end of the list. Tokenized stocks are securities because they are stocks, no Howey analysis required. The test matters for crypto because most tokens resemble nothing on the enumerated list, so everything turns on the catch all.

The second misconception is that failing the Howey test makes an asset unregulated. A digital commodity escapes SEC registration requirements, but it lands in CFTC territory, where fraud and manipulation rules still apply, and it remains subject to tax law, sanctions law, and money transmission rules regardless. The Howey question decides which regulator and which rulebook, not whether rules exist.

The third is that passing or failing is permanent. Because the analysis attaches to transactions, an asset’s status can change as facts change. A network that decentralizes can grow out of its investment contract origins, which the 2026 interpretation now recognizes explicitly, and a dormant project that resumes making promises can walk back into securities territory. Lawyers describe tokens as existing on a spectrum with a direction of travel, not in fixed categories.

One more boundary matters in practice: the test only reaches offers and sales. Simply holding a token, building software, or validating a network is not a securities transaction. This is why so much legal engineering in crypto concentrates on the moment of distribution, the single point where the securities laws attach or do not.

The CLARITY Act: replacing the test with a statute

The Digital Asset Market Clarity Act is Congress’s attempt to answer by statute the question Howey answers by litigation. The bill passed the House in July 2025 by a bipartisan 294 to 134 vote and cleared the Senate Banking Committee in May 2026, and as of mid July 2026 it awaits a Senate floor vote that must clear a sixty vote threshold. Its core mechanism is a formal division of the asset universe: digital commodities, defined largely by reference to decentralization and function, fall to the CFTC, while tokens sold as part of capital raising remain with the SEC, with defined pathways for assets to migrate from one category to the other as networks mature.

In effect, the bill writes the Ripple distinction and the 2026 interpretation into law: primary fundraising is securities territory, sufficiently decentralized assets trading in secondary markets are commodities territory, and the boundary is defined by criteria a project can evaluate in advance instead of a four part test applied after the fact by a court. Supporters call this the end of regulation by enforcement. Opponents, including state securities regulators, argue it weakens investor protection by letting issuers structure their way out of disclosure obligations. Prediction markets currently price passage this session as roughly a coin flip, and the market’s live odds, which fell sharply through early July as the Senate calendar tightened, have become the industry’s real time barometer of whether the Howey era is actually ending, a story crypto.news has tracked closely in its coverage of the CLARITY Act’s odds and what they mean for major assets.

Until a statute passes, Howey remains the operative standard. Committee votes do not reclassify tokens, and interpretations do not bind future commissions. The 1946 test is still the law of the land, which is precisely why it is still worth understanding.

Why free tokens still raise Howey questions

Airdrops look like the easy case, no money changes hands, so the first prong fails, but the analysis proved more tangled than that. The SEC argued in several matters that free distributions can still involve an investment of value, because recipients often provide something, promotional activity, network usage, personal data, or because the issuer benefits by creating a trading market for the remainder of its supply. Courts entertained versions of this theory as far back as internet stock giveaways in the 1990s, and the uncertainty was severe enough that some projects excluded American users from airdrops entirely for years, a self imposed geofence that became a running symbol of the enforcement era.

The 2026 interpretation defused most of this. Airdrops conducted as genuine distributions, without payment and without the issuer soliciting value in return, generally do not involve the offer or sale of securities under the interpretation, and the same logic extends to network rewards from protocol mining and staking. The reasoning follows the interpretation’s core move: securities law attaches to the issuer’s representations and the exchange of value, and a distribution lacking both sits outside the perimeter.

The practical consequence arrived quickly. Projects that had walled off American users began including them again, and airdrop design shifted from legal risk management back toward marketing mechanics. The episode stands as a compact illustration of how much economic behavior a single legal test can shape: for half a decade, the geography of free token distribution on the internet was drawn by a 1946 precedent about oranges.

How to think about any token under Howey

For a practical read on any asset, walk the prongs in order and be honest about the facts. Was there a sale in which buyers handed over value? Almost always yes. Were funds pooled toward a shared venture whose success buyers share? Usually yes for fundraising sales, murkier for secondary trades. Did buyers primarily expect profit? Marketing tells you: materials emphasizing price potential, scarcity, and listings point one way, materials emphasizing use point the other. And do those profits depend on a specific team’s ongoing efforts? This is where decentralization matters legally, not aesthetically: a network that would keep functioning and accruing value if its founding team vanished makes a weak Howey case, and a token whose entire value story is a company’s roadmap makes a strong one.

Two cautions complete the picture. First, labels are irrelevant. Calling something a utility token, a governance token, or a meme changes nothing; courts look at economic reality, and the regulatory history is littered with projects that discovered this in court. Second, the analysis is transaction by transaction, not asset by asset. The same token can be sold as a security in a fundraising round, trade as a non security on an exchange years later, and be offered as a security again if the issuer restarts making promises. The question is never what is this token. The question is always what was this transaction, and that is the insight the orange groves have been teaching for eighty years.

Frequently asked questions

What is the Howey test in simple terms?

It is the four part legal standard American courts use to decide whether an arrangement is an investment contract, and therefore a security. The four elements are an investment of money, in a common enterprise, with an expectation of profits, derived from the efforts of others. All four must be met.

Where does the name Howey come from?

From SEC v. W. J. Howey Co., a 1946 Supreme Court case about a Florida company that sold citrus grove plots along with service contracts to manage them. The Court ruled the packages were investment contracts, creating the test that still applies today.

Is Bitcoin a security under the Howey test?

No. Regulators have consistently treated Bitcoin as a commodity, because there is no central issuer or promoter whose efforts drive returns. The March 2026 joint SEC and CFTC action formally listed Bitcoin among the first group of digital commodities.

Why did the SEC treat most other tokens as securities?

Because most tokens were originally sold by identifiable teams to raise money, with buyers expecting the token to appreciate through those teams’ work, a fact pattern that maps closely onto the Howey prongs. That view drove years of enforcement actions against issuers and exchanges.

What did the Ripple ruling actually decide?

A federal court held in 2023 that Ripple’s direct institutional sales of XRP were securities transactions while its anonymous exchange based sales were not. The decision popularized the distinction between a token sale that creates an investment contract and the token itself trading later.

What changed in March 2026?

The SEC issued a formal interpretation narrowing how Howey applies to crypto: profit expectations must rest on the issuer’s own representations, common enterprise is a real requirement, and tokens can separate from their original investment contracts over time. Mining, staking, wrapping, and airdrops conducted as described generally fall outside securities offerings.

Would the CLARITY Act replace the Howey test?

For crypto assets, largely yes. The bill creates statutory categories, digital commodities under CFTC oversight and capital raising tokens under SEC oversight, with defined criteria replacing case by case Howey analysis. Until it becomes law, Howey remains the operative standard.

Does the Howey test apply outside the United States?

No. It is a doctrine of American federal law. Other jurisdictions use their own frameworks, such as the European Union’s MiCA regulation, though the underlying question of whether a token functions as an investment product appears in some form almost everywhere.

This article is for educational purposes only and does not constitute legal or investment advice. Securities law is fact specific, and regulatory positions change. Details are accurate as of July 14, 2026.

Crypto World

Finassets Raises Affiliate Revenue Share to 40%, Becoming One of the Highest-Paying Crypto Affiliate Programs

[PRESS RELEASE – Marbella, Panama, July 15th, 2026]

Finassets, a crypto payment gateway for businesses, announced an increase to its partner revenue share. The first-year referral rate rises to 40% of the processing revenue a referred merchant generates. From year two, the rate continues at 20% for five additional years while the merchant keeps processing, extending the total partner earning window to six years per referral, with the term extendable based on the merchant profile.

Payout speed, contract length, and dashboard visibility are among the key considerations affiliate marketers weigh when comparing crypto affiliate programs, and this update puts Finassets among the top crypto affiliate programs open to B2B partners.

A different model from trading-based programs

Many crypto exchange affiliate programs and trading platforms base payouts on trading fees generated by active traders, tying affiliate income to short-term trading volume through a fixed commission plan or a minimum payout threshold. Finassets ties partner earnings to a merchant’s ongoing processing volume instead — a relationship that can continue for the full six-year term.

One agreement, six years of revenue share

- Apply to become a partner. Submit an application and our team handles onboarding and sets clear terms from day one, with a personal referral link and dashboard account.

- Finassets onboards the merchant. KYB, compliance, and integration are handled entirely by Finassets.

- The partner earns. Revenue share is calculated per merchant and paid same-day, in crypto. The term can be extended based on the referred user profile.

A merchant referred through a partner’s affiliate link and processing $500,000 a month generates about $2,000 a month in processing fees at Finassets’ 0.40% rate. Here’s how that translates into partner earnings:

Based on a merchant processing $500,000/month at Finassets’ 0.40% fee. Illustrative; actual earnings depend on the merchant’s processing volume.

“Most cryptocurrency affiliate programs ask partners to keep generating referrals just to keep earning,” said Vitalijs F., CEO of Finassets. “We built this revenue share model so one merchant relationship can keep paying out for years, without additional marketing efforts from the partner after the introduction.”

Real-time visibility, reliable payouts

The agent dashboard tracks referral volume and revenue share per merchant in real time, with a full transaction history for reconciliation and one-click withdrawals. Deposits are typically credited within about 30 seconds of network confirmation, and partners are supported by dedicated account managers who respond quickly. Payouts are same-day, in crypto. Finassets supports 70+ cryptocurrencies across its full product suite, the same infrastructure referred merchants use to process payments.

The affiliate program is open to eligible B2B participants in selected international markets, subject to Finassets programme terms and applicable jurisdictional requirements.

More information and the partner application: https://www.finassets.io/en/affiliate-program/

About Finassets

Founded in 2021, Finassets is a Panama-registered crypto payment gateway supporting cross-border and crypto-driven businesses across eligible markets. Finassets provides crypto invoicing, payment links, payment buttons, mass payouts, API integration, crypto checkout, and an affiliate program within a structured, transparent environment for crypto payment processing.

Website: https://www.finassets.io

The post Finassets Raises Affiliate Revenue Share to 40%, Becoming One of the Highest-Paying Crypto Affiliate Programs appeared first on CryptoPotato.

The United Kingdom and United States have agreed to pursue closer coordination on stablecoin regulation, cross-border payments and tokenized financial markets.

Summary

- UK and US regulators seek aligned stablecoin rules while preserving competition and cross-border market access.

- Stablecoins used as money should hold one-to-one reserves and protect holders during issuer insolvency proceedings.

- Officials will explore pathways allowing regulated stablecoins from either jurisdiction to enter the other market.

The two governments also plan to explore how regulated stablecoins issued in one country could gain access to the other market.

The commitments appear in a joint UK-US statement on stablecoins released on July 14. The statement forms part of recommendations from the Transatlantic Taskforce for Markets of the Future, which the two governments established in September 2025.

UK and US set common stablecoin principles

The two governments said stablecoins can support payments, settlement and capital market transactions when regulators apply proper safeguards. They plan to seek “comparable outcomes for comparable risks and activities” while allowing each country to develop requirements under its own legal framework.

The approach does not require identical regulations. Instead, officials want to reduce unnecessary differences that could block cross-border activity. The governments also said they would avoid rules that impose costs out of proportion to the risks or create unnecessary barriers for new competitors.

As reported by crypto.news, the agreement comes as stablecoin rules remain a major policy issue in Washington. U.S. lawmakers and banking groups continue to debate how digital dollar products should interact with traditional banks and financial markets.

Stablecoins should maintain at least 1:1 backing

The joint statement says stablecoins presented as money should hold at least one dollar or equivalent in high-quality liquid assets for every unit issued. Each country will decide which reserve assets qualify under its domestic framework.

Issuers should also separate reserve assets from their own corporate funds. The governments said holders should receive timely redemptions and clear information about their legal rights. In an issuer failure, holders should have a protected claim on reserves, including priority over other creditors where domestic law allows it.

The principles broadly match the direction of U.S. stablecoin regulation under the GENIUS Act. The Treasury began proposing implementation rules in 2026 as the United States prepares its federal framework for payment stablecoin issuers.

Governments explore cross-border stablecoin access

The UK and US plan to examine a clear pathway that could allow stablecoins regulated in either jurisdiction to reach customers and markets in the other. Any access arrangement would remain subject to each country’s laws and regulatory processes.

Both governments also support fair, risk-based access to banks and other financial services for lawful regulated digital asset companies. They said stablecoins could serve as settlement instruments in securities and commodities markets when firms meet the required safeguards.

The statement does not create automatic mutual recognition or approve any specific stablecoin for cross-border distribution. Regulators still need to develop the legal routes and standards required to put the plan into practice.

Tokenized finance forms part of wider cooperation

The agreement extends beyond stablecoins. Under the broader Transatlantic Taskforce recommendations, the two countries plan to work with a private-sector group to test cross-border uses for tokenized assets over a one-year period.

The SEC, CFTC, FCA and Bank of England will also seek common approaches to areas including tokenized securities settlement and the possible use of stablecoins or tokenized money market funds as collateral at clearing houses.

The recommendations leave both countries free to complete their own regulatory processes. Their stated aim is to reduce cross-border friction while giving regulated stablecoins and tokenized financial products clearer routes between two major global financial markets.

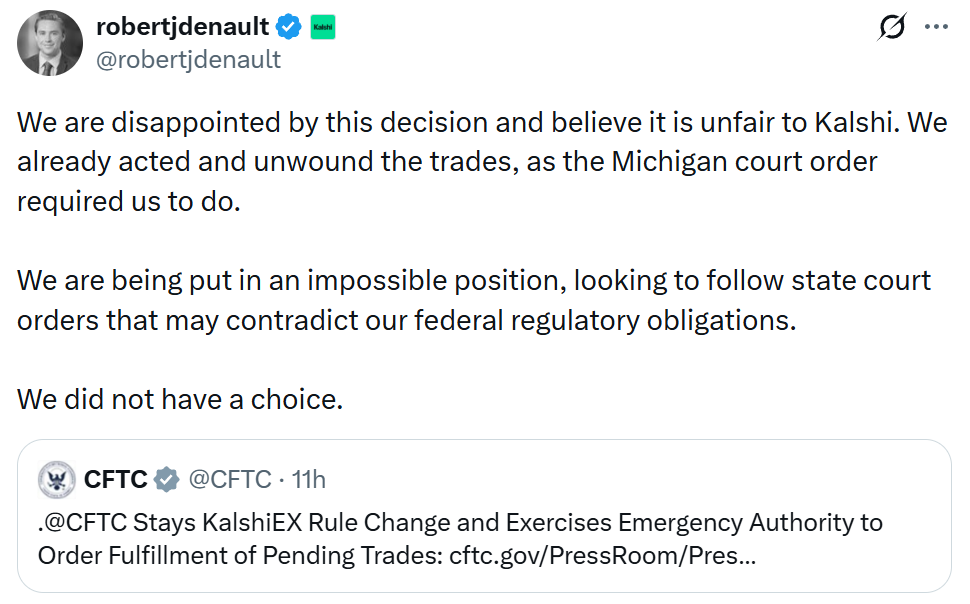

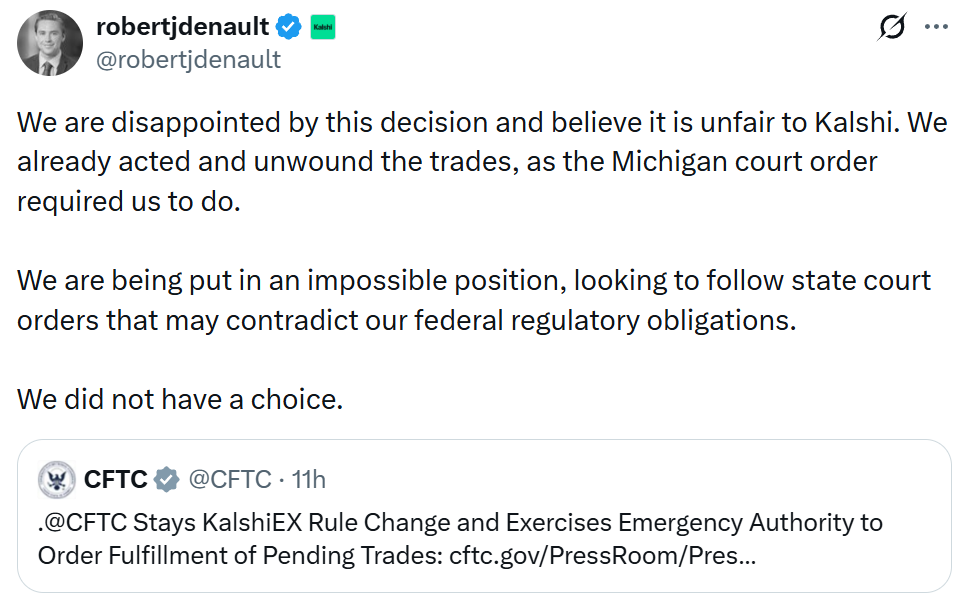

Kalshi says it is being put in an “impossible position” after the US commodities regulator on Tuesday said it was blocking the prediction market platform from canceling trades in Michigan, contradicting a recent state court order.

On June 29, Kalshi was ordered by Ingham County Circuit Court Judge Rosemarie Aquilina to cease offering sports betting contracts to Michigan users while a lawsuit over whether Kalshi violated the state’s sports betting laws plays out. The Commodity Futures Trading Commission ordered Kalshi on Tuesday not to comply with the state order and continue operating.

“We are disappointed by this decision and believe it is unfair to Kalshi,” Robert DeNault, the company’s head of enforcement and legal counsel said in a statement on X.

“We already acted and unwound the trades, as the Michigan court order required us to do. We are being put in an impossible position, looking to follow state court orders that may contradict our federal regulatory obligations. We did not have a choice.”

Source: Robert DeNault

The conflicting orders highlight an unresolved regulatory divide between the CFTC and nearly two dozen state regulators over which authorities have jurisdiction over prediction markets. The CFTC said Michigan was the first state to attempt to interfere with executed derivatives transactions.

“Canceling trades that have already been executed is an unprecedented step that risks a cascading effect on the entire marketplace and undermines the certainty in contracting that is a necessary component of a functioning market,” said Selig.

“The Commission will not allow states or state courts to bully registered entities into violating the Commodity Exchange Act and CFTC regulations.”

A Kalshi spokesperson said it was reviewing the CFTC’s order and considering its next steps, according to Reuters.

Related: OpenAI quietly adds Kalshi World Cup odds to ChatGPT: Report

Speaking on Fox Business on Friday, CFTC Chair Michael Selig said it is “critical” that the regulator maintains its regulatory authority over prediction markets.

“We’ve sued nine states now, and we’ll continue to sue any state that attempts to impose criminal or civil fines against CFTC-registered exchanges.”

Magazine: Strategy became a symbol of the dot-com crash: Could history repeat?

Mizuho has downgraded Circle Internet Group from Neutral to Underperform and cut its price target from $85 to $50, citing competition from Open USD.

Summary

- Mizuho cut Circle’s price target to $50, warning Open USD could further squeeze stablecoin margins.

- Open USD shares reserve earnings with partners, challenging Circle’s existing distribution economics around USDC globally.

- Circle also faces margin pressure from Hyperliquid revenue-sharing terms despite recent federal banking approval milestone.

The Japanese investment bank said the stablecoin model could pressure the economics behind Circle’s USDC business.

According to a CoinDesk report, analysts led by Dan Dolev said Open USD “could fundamentally alter CRCL’s business model” by changing how reserve income flows to distributors. Circle shares traded at $62.63 when the report was published.

Mizuho cuts Circle’s 2027 earnings outlook

Mizuho raised its estimate for Circle’s distribution and transaction expense ratio in 2027 from 64% to 73%. The bank also lowered its adjusted EBITDA forecast from $1.09 billion to $699 million, about 25% below the analyst consensus cited in the report.

The bank said higher interest rates could support reserve income but may not fully offset pressure from changing stablecoin economics. Its concern centers on how much yield Circle can retain after paying distribution partners, including companies that help USDC reach users and financial platforms.

Open USD challenges the existing stablecoin model

Open USD was announced on June 30 by Open Standard, with more than 140 companies participating in its ecosystem. Partners include Coinbase, Mastercard, Stripe and BlackRock. The project says businesses will be able to mint and redeem the stablecoin without fees or artificial volume limits.

Under the model, partners receive reserve earnings after a small management fee covers operating costs. That differs from Circle’s structure, where reserve income is generated before revenue-sharing payments to major distribution partners. As previously reported, Open USD’s announcement raised questions over whether Circle’s own partners could support a rival while continuing to distribute USDC.

Coinbase relationship adds another pressure point

Mizuho also pointed to Circle’s revenue-sharing relationship with Coinbase. The bank said the agreement is expected to come up for renegotiation in August, and Coinbase’s participation in Open USD could give it more leverage in future talks.

A separate warning came from JPMorgan. As reported by crypto.news, the bank cut earnings forecasts for Circle and Coinbase after a new USDC revenue-sharing arrangement with Hyperliquid. JPMorgan said the deal could reduce reserve income retained by both companies even if USDC usage grows.

Circle continues to expand USDC infrastructure

The downgrade comes as Circle expands its regulatory and payments footprint.Circle data showed USDC circulation at about $73 billion as of July 13, down from $77 billion at the end of the first quarter.

Circle also recently received final approval to establish Circle National Trust. The federally regulated entity will initially focus on digital asset custody for Circle and its affiliates, with possible future services for selected institutional clients.

The company is also expanding USDC use in Asia. JCB and Circle announced a pilot covering cross-border treasury transfers and possible merchant payments in Japan. The project will start with JCB’s internal transfers before the companies assess wider retail payment uses.

Mizuho’s downgrade focuses on Circle’s ability to protect margins as stablecoin competition changes how reserve income is shared. Open USD has not proved it can match USDC’s distribution or liquidity, but its partner-led model creates a new pricing benchmark. Circle’s earnings path will depend partly on USDC supply, interest rates and future revenue-sharing agreements.

A solo Bitcoin miner has validated a block using just one low-cost Bitaxe machine, landing the standard 3.125 BTC reward in what looks like a statistically unlikely outcome. The win underscores how, even in today’s highly competitive mining environment, hobby-scale setups can still occasionally hit the lottery.

According to blockchain data from mempool.space, the miner solved block number 957382 on Friday and received 3.125 BTC, worth roughly $200,000 at current market valuations. The miner’s setup reportedly consisted of a single Bitaxe rig, as noted by the mining pool Public Pool in a post on X.

Key takeaways

- A retail solo miner validated block 957382 and received the 3.125 BTC reward, per data from mempool.space.

- The winning setup reportedly used a single Bitaxe miner, credited by Public Pool on X.

- Bitaxe is positioned as a low-power, budget device—its hashrate is about 1 TH/s, tiny compared to the network.

- Solo block wins remain rare but are still happening regularly enough to add up: Bennet data places the last 12 months’ solo payouts above $4.7 million.

How a single miner found a solo block

The defining detail in this case is not the size of the reward—every successful solo miner receives the standard block subsidy—but the scale of the hardware involved. Public Pool attributed the find to a lone Bitaxe mining rig.

As described by Bitaxe, the device is a budget, lower-power Bitcoin miner with an estimated hashrate around 1 TH/s, according to the article’s referenced materials. In practical terms, that figure is extremely small relative to the overall Bitcoin network hashrate, which is why solo block wins are usually framed as long-shot events for individual miners.

Yet the nature of mining is that the network doesn’t “know” how small your share is—only probability matters. That’s what makes these events notable for retail miners: even when odds are against you, the process can still produce occasional, outsized payoffs.

Why this case stands out among recent solo wins

This isn’t the first time a solo Bitcoin block has been found with retail-level participation, but it adds another example of how DIY mining setups continue to surface wins.

Earlier coverage referenced by the source notes that another solo Bitcoin miner validated a block in April through CKPool’s solo mining service. In February, another retail miner reportedly found a solo block using rented hashrate—meaning the miner may not have owned the physical hardware performing the work.

The difference matters because “solo mining” can be implemented in different ways. Solo mining technically means the miner is working toward their own block candidate rather than sharing block rewards with a pool. But the hardware—and whether it is owned outright, rented, or handled through a service—changes the economic reality: electricity costs, capital risk, and the probability profile investors associate with each approach.

In this latest instance, the emphasis is on an owned, single-rig setup using Bitaxe, making it a closer analog to the traditional idea of a hobbyist miner aiming at a solo prize.

Solo mining trends: frequency, droughts, and annual totals

While any single solo block is a rare event, aggregators show that wins are not disappearing. The source points to a year-long tally using Bennet’s solo miner tracking.

According to Bennet data cited in the article, solo blocks mined increased by 41% year-on-year. Over the past year, solo miners validated 24 blocks, pushing total rewards paid to 75.4 BTC—stated as more than $4.7 million in the referenced coverage.

Timing also remains a crucial detail for anyone planning for long horizons. The source reports an average interval of 15.2 days between successful solo blocks, while the longest drought without a solo win was 58 days. These numbers are useful because they help retail participants calibrate expectations: solo mining doesn’t deliver predictable returns, but it also doesn’t mean “never.” The distribution of outcomes can be lumpy—short streaks and longer gaps can both occur.

For investors and builders watching Bitcoin’s ecosystem, this matters because solo participation—even if small—reflects ongoing access to mining at the consumer end. It also highlights that, despite industrial-scale competition, individual miners can still engage meaningfully, at least occasionally, with affordable hardware.

What to watch next for retail solo miners

Retail solo mining remains a game of probability, but the most practical question for the near term is whether these Bitaxe-style, small-hashrate successes keep showing up with enough regularity to sustain interest. Readers should watch the spacing between solo wins and the reported hardware profiles behind them, since both determine how realistic solo mining feels for hobby participants after each new cycle of difficulty adjustments.

Higher rates hurt bitcoin and risk assets as when the Fed raises rates, cash and Treasury bonds start paying a decent, guaranteed return, so investors have less reason to hold something that pays no yield and swings 5% in a session.

On the other hand, cooler inflation means the Fed has less reason to raise, so that pull weakens and money flows back the other way.

Elsewhere, brent crude advanced 1% to above $85 a barrel, a third consecutive day of gains, after President Trump threatened further strikes on Iran and the U.S. resumed its blockade of Iranian shipping through the Strait of Hormuz. Crude has now surged 11% in two sessions.

Equities took the same cue as crypto. MSCI’s Asia Pacific gauge climbed 2.3%, its biggest advance in a month, with technology shares leading. South Korea’s Kospi jumped 8.2%, retaking its position as the world’s best-performing major benchmark this year, and SK Hynix rose 13% in Seoul after its American depositary receipts surged 27%.

“Bitcoin remains a rate-sensitive risk asset rather than a macro hedge,” said Jeff Ko, chief analyst at CoinEx, who said the print as reducing ‘“immediate downside pressure without building a durable breakout.”

Core inflation at 2.6% is still above the Fed’s 2% target, so the print buys the central bank room to hold rather than reason to cut. Ko pointed to the September FOMC meeting as the next real macro test, along with the direction of the dollar and whether bitcoin ETF flows can sustain themselves.

XRP’s price dipped below $1.07 yesterday, but the impressive market rebound helped it erase most losses. However, it still needs to reclaim a key level before it turns more bullish.

Ripple (XRP) Price Predictions: Analysis

Key support levels: $1.00

Key resistance levels: $1.3, $1.6, $2

Bears About to Retest $1 Support

After a brief bounce, sellers returned and managed to take control of price action around the $1.18 level. The asset went into an evident downtrend in the following weeks that drove it to the aforementioned low of under $1.07. Although it appeared primed to retest the $1.00 support, it has rebounded swiftly, and there’s no immediate danger in sight.

While another drop to $1 could be considered bearish, it is too early to call it until this level turns into resistance. Buyers will also have another chance to show up at this key level and push bears away.

Can XRP Make a Higher Low?

To turn bullish on this price action, XRP will need to hold above $1.00 and make a higher low. Given that sell volume has been declining for months, this could provide buyers with an opening to regain control.

The current low is at $1.01. As long as buyers can stop bears before they reach that level, they have a chance to reverse the downtrend and regain momentum on their side. However, that will also require an increase in buy volume.

RSI Bullish Divergence

Another interesting signal that could put buyers back in control appears on the 3-day RSI, which shows a clear bullish divergence. While the XRP price made lower lows, the RSI made higher lows.

This is an early signal that could hint at a major reversal ahead. For that to happen, XRP’s correction needs to stop at $1.00 and then slowly recover its most recent losses. A higher high above $1.18 would confirm the reversal.

The post Ripple (XRP) Price Predictions for This Week (July 15) appeared first on CryptoPotato.

The United States has frozen more than $130 million in cryptocurrency held in wallets linked to the Central Bank of Iran, according to Treasury Secretary Scott Bessent.

Summary

- US authorities froze more than $130 million in crypto tied to Iran’s central bank wallets.

- On-chain data showed four Tron wallets holding about $131 million in USDT were frozen Tuesday.

- The action follows April’s $344 million USDT freeze and wider US pressure on Iranian crypto.

The action adds to a broader U.S. campaign targeting Iran’s use of digital assets and other financial channels.In a July 14 post on X, Bessent said the Treasury Department’s Office of Foreign Assets Control sanctioned multiple wallets tied to Iran’s central bank. The sanctions resulted in more than $130 million being frozen.

Four Tron wallets held about $131 million

On-chain investigator Specter identified four wallets on the Tron network holding a combined total of roughly $131 million in USDT. Reports based on the analysis said Tether had frozen the addresses, preventing the stablecoins from being transferred.

Bessent did not identify the individual addresses in his statement. He said Treasury remained “committed to disrupting and degrading Iran’s illicit financial activities, including its abuse of digital assets.” He added that authorities would continue to “follow the money” and restrict access to funds that Washington links to Iranian government revenue networks.

Freeze follows earlier $344 million USDT action

The latest move follows a much larger enforcement action in April.As previously reported, Tether froze about $344 million in USDT across two Tron wallets after U.S. authorities linked the addresses to Iranian networks. One wallet held about $213 million, while another contained roughly $131 million.

Blockchain analysis at the time found transaction patterns associated with wallets linked to Iran’s Islamic Revolutionary Guard Corps and intermediaries connected to the Central Bank of Iran. The funds were blocked through controls built into the USDT token rather than through changes to the Tron blockchain itself.

Treasury expands pressure on Iran’s crypto networks

The United States has increased its focus on Iran’s digital asset infrastructure during 2026. In June, Treasury sanctioned four Iranian crypto exchanges, including Nobitex, which the department said handled more than half of Iranian digital asset inflows during 2025.

As reported, Bessent also said in May that U.S. actions had seized or frozen nearly $1 billion in Iran-linked cryptocurrency. Earlier figures had placed the total near $500 million after the April USDT action.

The Treasury has described the campaign as part of Operation Economic Fury, which targets crypto exchanges, wallets and traditional financial networks that U.S. officials accuse of supporting sanctions evasion and Iranian military financing. Treasury actions have also targeted overseas companies accused of helping move proceeds from Iranian oil sales through cryptocurrency and front companies.

Crypto freeze comes as US-Iran tensions rise

The new wallet action comes during renewed military tensions between Washington and Tehran. U.S. Central Command confirmed fresh strikes against Iranian military targets and the resumption of a blockade of Iranian ports this week after a June pause in hostilities began to break down.

The latest freeze also shows the enforcement role centralized stablecoins can play. Unlike Bitcoin, USDT contains issuer-level controls that can prevent sanctioned addresses from moving tokens. Tether has used those controls in several law enforcement actions, including the April Iran-linked freeze and a July action involving wallets sanctioned over alleged ISIS-K financing.

For the latest $131 million action, Treasury has confirmed that the wallets were tied to the Central Bank of Iran and that the funds were frozen. Public statements have not disclosed how the assets were originally obtained or how authorities determined the intended use of the funds.

Binance is looking beyond cryptocurrency trading as it works to build a broader financial “super app” centered on payments, stablecoins and investment products.

Summary

- Binance plans to expand beyond trading by combining payments, stablecoins, stocks and broader financial services.

- Stablecoin adoption is pushing Binance toward payment services aimed especially at users in emerging markets.

- Binance already offers thousands of US stocks and tokenized equities alongside its core crypto products.

Shunyet Jan, the exchange’s head of spot trading and derivatives, outlined the strategy as Binance marked its ninth anniversary.

In an interview with CoinDesk, Jan said trading remains central to Binance but no longer defines the full market available to the company. “We’re trying to not just be a crypto exchange, but be a super app that involves payment,” he said.

Stablecoins push Binance deeper into payments

Jan linked the strategy to growing stablecoin use for payments and transfers. Stablecoins have expanded beyond their original role as trading assets, giving exchanges a way to serve users who need cross-border payments, spending tools and access to dollar-based digital assets.

“If you think of us as a payment provider, then that number becomes much bigger,” Jan said. Binance Research has also identified payments as a major path for crypto super apps. Its April report said Binance Pay had reached more than 21 million merchants and connected with local payment systems such as Brazil’s Pix.

Binance has also expanded its card services. As previously reported, the exchange launched a Mastercard-linked crypto card in selected CIS markets in February, allowing eligible users to spend Bitcoin, Ether, stablecoins and other supported assets through automatic conversion at checkout.

Binance adds stocks to its financial ecosystem

The exchange has spent 2026 adding products outside traditional crypto markets. Binance said in its ninth-anniversary update that it now wants users to move between digital assets, stablecoins, public markets, payments and onchain services from one platform.

However, Binance opened access to more than 7,000 US stocks and ETFs for eligible users outside the United States in June. Users can buy fractional shares using assets including USDT and USDC, connecting stablecoin balances directly with traditional investments.

Binance said direct stock positions reached $1 billion in assets within about 30 days, with close to $3 billion in cumulative trading volume. More than 73% of first-month trading volume came from emerging markets, according to the exchange.

Tokenized equities add an onchain layer

Binance has also launched bStocks, which convert supported US equity exposure into blockchain-based assets. The initial lineup included tokenized versions of Nvidia, Tesla, Circle, Micron and Sandisk.

The products can trade around the clock and move to supported self-custody wallets. Binance says eligible users can also use them in supported decentralized finance applications. The company reported that bStocks passed $100 million in assets within 15 days, while 47% of trading volume occurred outside normal US market hours.

Emerging markets form a key part of the strategy

Jan said demand for Binance’s broader financial services is particularly strong in emerging economies, where access to foreign investments and traditional banking services can remain limited. The company sees its existing crypto infrastructure as a way to connect those users with more payment and investment products.

Binance Research previously estimated that crypto exchanges could bring nearly 300 million new investors and about $2 trillion into global equity markets by 2031. As per report, stablecoin settlement could help exchanges serve investors who face high costs or limited access to overseas markets.

Binance is not alone in pursuing the model. Coinbase has also outlined a financial super app strategy combining trading, lending, payments and other services. Binance’s approach now centers on linking its large trading business with stablecoin payments, traditional assets and onchain products within one platform.

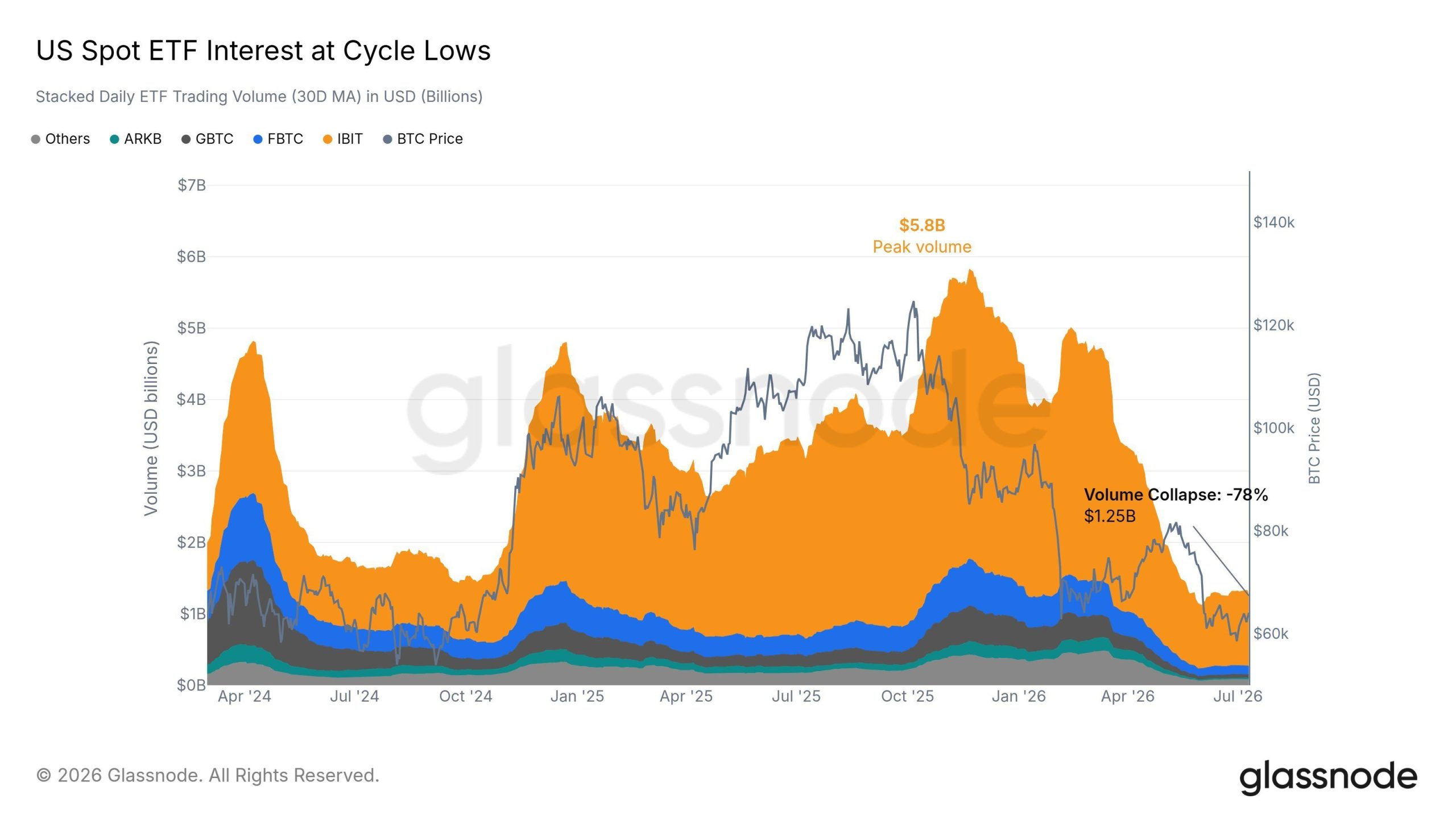

US spot Bitcoin (BTC) ETF outflows reached roughly $430 million on July 13. Fidelity’s FBTC lost $246.3 million and BlackRock’s IBIT shed $186.1 million, according to Glassnode data.

The redemptions hit a market already trading at its quietest levels this cycle. ETF volumes have collapsed 78% from their peak, and analysts warn that attention has rotated to other asset classes.

ETF Trading Volumes Collapse 78% From Peak

Glassnode’s 30-day moving average of daily trading volume across US spot Bitcoin ETFs now sits at $1.25 billion. That marks a 78% collapse from the $5.8 billion peak recorded in late 2025.

Activity has also slipped below 2024 levels. BlackRock’s IBIT still accounts for most of the remaining turnover. However, even its share has thinned in recent months.

The on-chain analytics firm framed the slowdown as a loss of attention rather than a temporary lull. Glassnode shared the observation in a post on X:

“Trading activity in US spot ETFs sits in a quiet regime. Volumes are down 78% from the peak and below 2024 levels. A sustained recovery in $BTC price momentum would likely require attention and market participation to return from other asset classes.”

Bitcoin ETF Outflows Top $430 Million in One Day

Monday’s session showed how one-sided flows have become. Fidelity’s FBTC led the exit with $246.3 million in redemptions. IBIT followed with $186.1 million, while VanEck’s HODL bucked the trend with a $3.5 million inflow.

Grayscale’s GBTC and Franklin Templeton’s EZBC posted smaller losses. Combined, the funds bled roughly $430 million in a single day.

The IBIT figure drew loud reactions. Evan Luthra, entrepreneur and BeInCrypto Experts Council member, reacted to the data in a post on X.

The framing deserves nuance, however. ETF outflows reflect investors redeeming shares, which forces issuers to sell bitcoin held in trust. BlackRock did not liquidate a proprietary position, and Fidelity’s outflow was the larger of the two.

The reversal also stings because of its timing. Bitcoin funds had just attracted $197.4 million in net inflows during the week ending July 10, snapping eight straight losing weeks. June, in contrast, produced record monthly outflows of $4.5 billion.

BTC Price Prediction Hinges on the $58,000 Support

BTC trades near $64,681, up 4.4% over the past 24 hours, per BeInCrypto market data. Glassnode’s flows chart tracks the token’s slide from roughly $78,000 in mid-May to a June 30 low near $58,000.

That $58,000 area remains the level to defend. A daily close below it would put the cycle floor near $57,500 in play, roughly an 11% drop from current prices.

On the upside, bulls must reclaim $68,000, the zone where the early June breakdown began. A recovery above that level would suggest institutional demand is returning after a two-month drought.

There are early signs of absorption elsewhere. Long-term holders flipped back to accumulation on July 11 and 12, adding a net 5,912 BTC.

Sustained positive flows and a volume recovery would confirm renewed participation. Until then, BTC either rebuilds momentum above $68,000 or retests $58,000 with little institutional cushion beneath it.

The post ‘BlackRock Dumped $185M in Bitcoin’ Claim Fuels ETF Panic as Trading Hits Cycle Lows appeared first on BeInCrypto.

All Coronation Street spoilers for next week as shocking arrest has huge consequences for show legend | Soaps

Opinion: More tax tweaks needed for tech

Finassets Raises Affiliate Revenue Share to 40%, Becoming One of the Highest-Paying Crypto Affiliate Programs

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports5 days ago

Sports5 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

News Videos10 hours ago

News Videos10 hours agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech1 day ago

Tech1 day agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech10 hours ago

Tech10 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos6 days ago

News Videos6 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Sports7 days ago

Sports7 days ago39-year-old Djokovic wins five-hour thriller to enter Wimbledon semis | Other Sports News

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

Tech1 day ago

Tech1 day agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Tech6 days ago

Tech6 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World6 days ago

Crypto World6 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World6 days ago

Crypto World6 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

-

Tech6 days ago

Tech6 days agoClaude’s New Reflect Dashboard Wants To Help You Log Off Of Claude

-

Crypto World7 days ago

Crypto World7 days agoMicrosoft Cuts AI Bill by Replacing OpenAI and Anthropic in Software Products

-

Crypto World6 days ago

Crypto World6 days agoFed minutes June 2026: officials split on rates

You must be logged in to post a comment Login