Crypto World

Why Zcash crashed even after the bug was fixed

Here is the puzzle. On May 29, 2026, a security researcher hired by Zcash developers found a critical bug in the network’s Orchard privacy pool, a flaw that could have let an attacker mint unlimited, undetectable counterfeit ZEC.

The development team moved fast: they disclosed it, coordinated an emergency fix, disabled the vulnerable component within days, and re-enabled it with a patched circuit through a hard fork by June 1. No funds were stolen.

No inflation was detected. By almost any standard of incident response, this was a model of how to handle a critical vulnerability. And the market punished ZEC anyway. The token, which had been trading above $600 earlier in the week, has crashed roughly 45% to around $314, wiping more than $3 billion off its market value. The bug was fixed, and the price collapsed regardless.

Summary

- Zcash fixed a critical Orchard bug that could have allowed unlimited counterfeit ZEC, but the token still fell about 45% as investors questioned whether the flaw had been exploited before it was discovered.

- Developers said there is no cryptographic way to prove the vulnerability was never used during the four years it remained hidden, leaving uncertainty over the network’s supply integrity.

- The incident has renewed debate over the trade-off between privacy and auditability, a challenge that extends beyond Zcash to the wider privacy coin sector.

Understanding why reveals something fundamental about privacy coins that the celebratory “we patched it” framing misses entirely. This piece explains the paradox, and what it means for every privacy coin, not just Zcash.

What the bug was

To grasp why the fix did not save the price, you first need to understand what the bug actually threatened.

The vulnerability lived in Orchard, Zcash’s most advanced privacy pool, specifically in the cryptographic circuit that makes its shielded transactions work. Zcash’s whole purpose is private transactions: using zero-knowledge cryptography, it lets users send and receive funds without revealing addresses or amounts.

Orchard is the engine that delivers that privacy. The bug was a flaw in that engine, and its consequences were severe. As Shielded Labs, the nonprofit developer that disclosed it, described, the flaw could have allowed an attacker to create an unlimited number of counterfeit ZEC tokens, completely undetected.

The cleanest analogy comes from the disclosure itself: think of it as someone secretly gaining access to the Federal Reserve’s dollar printing press, except in this case, even the Fed could not tell the extra dollars had been printed. A security engineer named Taylor Hornby, brought on specifically to hunt for protocol vulnerabilities, found the flaw on May 29 using an advanced AI model to conduct a targeted review of the Orchard circuit.

He wrote a complete working exploit and confirmed that, in a local testing environment, it generated unlimited, undetectable counterfeit ZEC. Shielded Labs stated plainly that if the same tool had been run on the live Zcash network, it would have produced counterfeit tokens in the attacker’s wallet.

This is about the worst kind of bug a cryptocurrency can have. The entire value proposition of a fixed-supply digital asset rests on the supply being exactly what everyone believes it is. A flaw that lets someone secretly mint unlimited counterfeit coins attacks that foundation directly. So the severity was real. But severity alone does not explain the crash, because the bug was caught and fixed before any known exploitation. The explanation lies in two words: “undetected” and “undetectable.”

The fix worked. So why did it crash?

By the numbers, the response was a success. The flaw was found by the team’s own hired researcher before any malicious actor was known to have used it. It was disclosed responsibly. It was patched within days through coordinated emergency action. Some analysts even framed the episode as cautiously bullish, evidence that Zcash’s developers could rapidly coordinate a critical security fix without funds being stolen or inflation occurring. Robust crisis management, in other words.

And yet the market did the opposite of rewarding it. The reason is a problem the fix could not touch, and Shielded Labs was admirably honest about it. Because of Orchard’s privacy properties and the nature of the bug, there is no definitive way, using cryptography alone, to determine whether the flaw was exploited before it was discovered and fixed. The developers patched the door, but they cannot prove no one walked through it during the four years it was unlocked. They themselves stressed this uncertainty rather than hiding it.

That is the crux of the paradox. With a transparent blockchain like Bitcoin, if a similar bug were found, auditors could examine the public ledger and verify whether the total supply matched what it should be. The transparency that privacy advocates often criticize is exactly what would allow a clean “we checked, no counterfeits exist” conclusion.

Zcash cannot do that. The shielded transactions that protect users by hiding amounts and addresses also hide whether counterfeit coins were created. The privacy is the feature, and in this moment, the privacy is the problem. You cannot audit what is designed to be unauditable.

So the market was not reacting to the bug, which was fixed. It was reacting to the permanent, unresolvable uncertainty the bug exposed. Investors were asked to hold a token whose supply integrity can never be fully proven, in the specific knowledge that a counterfeiting vulnerability existed undetected for four years. The fix addressed the future. It could do nothing about the doubt it cast over the past, and that doubt is what crashed the price.

Four years is the part that stings

The detail that turned a serious situation into a confidence crisis is the timeline. The bug was not introduced last month. It had been present since Orchard’s activation in May 2022. It existed, undetected, for four years.

This matters for two reasons, and both are corrosive to trust. The first is the obvious one: four years is a long window. Even if exploitation is unlikely, the sheer length of time during which the flaw sat open expands the space of “what if.” Anyone who used Orchard over those four years operated on a system that could, in theory, have been compromised, and there is no way to retroactively verify it was not. The longer the window, the harder it is to wave away the possibility with “it was probably never exploited.”

The second reason cuts deeper. The bug evaded years of scrutiny by experienced cryptographers. Zcash is not an obscure project; it is one of the most respected privacy coins, built and reviewed by some of the most capable cryptographers in the industry. That such a severe flaw survived four years of that scrutiny, and was found only through a deliberate, AI-assisted hunt by a specifically hired researcher, raises an uncomfortable question.

If a bug this serious could hide for four years in a system this heavily reviewed, what confidence can anyone have that there are not others? Shielded Labs is now pursuing formal verification, a mathematical proof that no further bugs exist in the Orchard circuit, precisely because the four-year miss shattered the assumption that expert review was sufficient.

Shielded Labs makes a reasonable case that exploitation probably did not happen. The bug evaded everyone for years and surfaced only with cutting-edge tools and a skilled researcher working deliberately to find it, then was fixed quickly, leaving little window for anyone else to have found and used it in the gap.

As they put it, they think their researcher “probably succeeded” in finding it before any malicious actor. But notice the language. “Probably.” In a system built on cryptographic certainty, the best the developers can honestly offer about the supply is a probability, and markets pricing a privacy asset do not like paying full price for “probably.”

What it means for every privacy coin

The Zcash episode is not just a Zcash problem. It exposes a structural tension that sits at the heart of every privacy-focused cryptocurrency, and that is why it deserves attention beyond ZEC holders.

The tension is this: privacy and auditability are in direct conflict. The more completely a coin hides its transactions, the more completely it also hides whether its supply is sound. A fully transparent chain can always prove its supply integrity by public inspection, at the cost of user privacy. A fully private chain protects its users absolutely, at the cost of ever being able to prove, to a skeptic, that no counterfeiting has occurred.

This is not a flaw in Zcash’s implementation that better engineering eliminates. It is a fundamental trade-off baked into the concept of private money. Monero, the other major privacy coin, faces the same structural reality: its privacy guarantees are also its auditability limits.

What Zcash is now attempting is the industry’s most serious effort to thread that needle, and it is worth watching. Shielded Labs has proposed a network upgrade that would let anyone independently verify the integrity of the ZEC supply, involving a new shielded pool and “turnstile” accounting that tracks coins moving out of the compromised Orchard pool.

The goal is to restore provable supply integrity without abandoning privacy. If it works, it could become a template for how privacy coins handle the auditability problem. If it proves clunky or incomplete, it will underline how hard the trade-off is to escape. Either way, Zcash is being forced to solve in public a problem the entire privacy-coin category has mostly been able to ignore.

The market’s reaction also surfaced a colder truth about privacy coins as investments. The selloff was sharpened by news that a prominent privacy-coin holder, BitMEX co-founder Arthur Hayes, sold his entire ZEC position. When a flagship holder exits over an unresolvable supply question, it signals that even sophisticated believers have a limit to how much “probably fine” they will tolerate. For a privacy coin, trust is not a soft attribute; it is the entire product, because you cannot verify the thing yourself. Once that trust takes a hit that cannot be cryptographically repaired, the discount can be severe and durable.

The honest read

Zcash did almost everything right and still got punished, and that is the lesson worth sitting with.

The developers hired a researcher to hunt for exactly this kind of flaw before attackers could. The researcher found it. The team disclosed it transparently, fixed it within days, and is now proposing a supply-integrity upgrade and pursuing formal verification to prevent a repeat. As a piece of security response, it is close to a best-case playbook, and in a transparent system it might even have been a confidence-building moment, proof the network’s defenses worked.

But Zcash is not a transparent system, and that is the whole point. Its privacy, the feature that gives it its reason to exist, is also what makes it impossible to prove the bug was never exploited during the four years it existed.

The crash from above $600 to around $314 is the market pricing of that unresolvable uncertainty: not the bug itself, which is gone, but the permanent doubt it cast over a supply that can never be fully audited. The four-year window made the doubt larger, and a flagship holder’s exit made it concrete.

For ZEC specifically, the path back runs through the supply-integrity upgrade. If Shielded Labs can deliver a credible way to verify the supply independently, some of the fear should fade, because the core wound, unprovability, would begin to heal. If it cannot, the discount may persist as a permanent risk premium on an asset that asks you to trust what you cannot check.

For the broader privacy-coin category, the episode is a reminder that the privacy guarantee and the supply guarantee are two sides of the same coin, and you cannot strengthen one without weakening the other.

Zcash just learned, in public and at the cost of $3 billion, what that trade-off looks like when it goes wrong. The bug is fixed. The question it raised is not, and may never be.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 5, 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

Google Gemini AI is not being subtle about this prediction. From $75 today, the price prediction is $450 to $600 by the end of 2026, a move that would multiply Solana price six to eight times over.

The engine behind it is a single piece of infrastructure. Full deployment of Firedancer, Jump Crypto’s independent validator client, is expected to push network throughput past 1 million transactions per second.

That kind of capacity does more than speed things up. Gemini argues it virtually eliminates the outage risk that has dogged Solana’s reputation for years, positioning the network as the default high frequency execution layer for global finance.

Institutional interest is stacking on top of that technical shift. Potential spot SOL ETF approvals, deep payment integration with names like Visa and Shopify, and dominance in decentralized physical infrastructure networks like Helium and Render all point the same direction.

Gemini also flags something worth sitting with. Solana’s DEX transaction volume routinely outpaces Ethereum’s, which is a real usage metric rather than a speculative one.

The bear case is not vague either. Persistent validator centralization critiques, potential delays in ETF approvals, or aggressive liquidity cannibalization from low fee Ethereum Layer 2s could all cap Solana’s downside near $45 to $50.

Gemini still frames the unmatched consumer app experience, developer density, and enterprise scale as the deciding factors, positioning Solana as the layer 1 asset built to outperform the broader market through 2026.

Solana Price Prediction: SOL Needs A Number It Has Not Touched Since Winter

The daily chart tells a rougher story than the prediction does. SOL topped near $257 in September 2025, and what followed was a mostly uninterrupted decline into a low near $60 by February 2026.

Since that crash, price has spent five months building a wide, choppy range. Two separate rallies, one in December and one in May, both stalled almost exactly at $100, and both rolled over hard afterward.

Today closed at $75.29, up 1.11%, with the session ranging between $74.40 and $75.91. That is a modest green day sitting in the lower half of a range that has trapped this coin since winter.

Support sits at $70, then the June low near $60 that has now held twice. Resistance stacks at $85, then $95, then the persistent $100 ceiling that has rejected every real breakout attempt this year.

Momentum here is neither compressed nor extended, sitting in a neutral zone that reflects a market still deciding whether the June low was the actual bottom. For Gemini’s $450 target to have any grounding, Solana first needs to do something it has failed to do twice in 2026, close above $100 and actually hold there.

That single level is the entire gap between where this prediction lives and where the chart currently sits.

Discover: The Best Crypto to Diversify Your Portfolio

You Might Like What Gemini AI Predicts About This New Layer 3 Called LiquidChain

The money that wins cycles never waits at resistance.

Large caps are stuck. Bitcoin, Ethereum, and XRP keep testing the same ceilings with nothing breaking through. Every macro catalyst has a new arrival date. Every institutional wave has a new quarter attached. Waiting on someone else’s decision is not a trade.

Small market cap infrastructure plays operate on completely different physics. A rotation that vanishes as noise at Bitcoin’s scale reprices an undiscovered project by multiples. The opportunity lies in the gap between what something is genuinely worth and what the market has assigned it. That gap closes permanently the moment discovery happens.

Multi-chain fragmentation is one of the most expensive unsolved problems in DeFi. Bitcoin, Ethereum, and Solana run as completely isolated systems. No shared architecture. No native interoperability. Every time value crosses those boundaries it pays in fees, slippage, and failed transactions.

LiquidChain makes the crossing free. Gemini AI predicts and agrees. All 3 networks within a single execution environment. Single deployment. Complete ecosystem access. No tax on any interaction.

The presale is at $0.01454 with just over $890,000 raised. Early and undiscovered. That combination does not last long.

Explore the LiquidChain Presale

The post Google Gemini AI Predicts Solana Price Could 8x Before End of 2026 appeared first on Cryptonews.

SpaceX stock (SPCX) is now worth less than it was on day one. Shares closed near $115 last week. That is about 15% below the $135 price the company set for its June 12 debut.

Anyone buying at the listing is underwater. The obvious question is whether it comes back, and there is one good place to look for the answer.

What Just Happened to SpaceX Stock

SpaceX sold 555.6 million shares at $135 each. That raised almost $75 billion and valued the company near $1.77 trillion, according to its prospectus.

The start was strong. Shares opened at $150 and closed the first day around $161. By June 16 they hit $225.64.

Then the mood turned. The stock fell 6.7% on July 22 to $115.26. That is roughly 49% below the June high.

The company is now worth about $1.52 trillion. An earlier part of the slide had already wiped $500 billion from Musk’s fortune.

Three things went wrong at once:

- Starship slipped

- Rival Blue Origin raised new money, and

- China caught a rocket booster.

That last one stung. On July 10, China landed a Long March 10B booster in a net on a sea platform. It became only the second country to bring an orbital booster home. SpaceX did it first in December 2015, so China is about a decade behind.

Peter Schiff called the drop a broader market crash warning. Now, IPO investors are sitting on nearly 20% loss.

Why Two Dates in August Matter So Much

SpaceX reports earnings for the first time on August 4. Two trading days later, on August 6, a lot of shares become sellable.

Here is why that matters. When a company lists, insiders sign a lock-up. It stops them selling for a set period.

SpaceX built its lock-up around earnings instead of the calendar. Once results are out, up to 911.5 million shares are free to trade.

Elon Musk is not one of the sellers. His shares are locked for 366 days, with no early exit, so he cannot sell until June 2027.

Follow us on X to get the latest news as it happens

The Huge Batch of Shares That Will Not Be Sold

A second batch of 455.8 million shares was also lined up for August. Almost nobody has noticed that it will not arrive.

Those shares only unlock if the stock trades 30% above the IPO price. In cash terms, that means $175.50.

It has to close there on five of the 10 days ending on the earnings date. The stock is near $115, so it cannot happen.

The fall has therefore cut the amount of stock hitting the market. Roughly half the expected August supply is already gone.

Why Meta Fits Better Than Tesla

Most people compare SpaceX to Tesla. That comparison does not work.

Tesla listed in June 2010. It sold 13.3 million shares at $17 and raised $226 million. SpaceX raised about 330 times more.

Facebook, now Meta, is the better match. It priced at $38 in May 2012 and raised $16 billion.

Both put the founder firmly in charge. Musk holds 82.4% of the voting power at SpaceX while owning less than half the shares.

He does it with a second class of stock worth 10 votes each. Ordinary shares get one vote.

Small investors piled into both deals. Early reports said SpaceX would give retail buyers 30% of the offering. CNBC later reported the real figure came in at just over 20%.

SpaceX, 2026

Meta, 2012

Tesla, 2010

IPO price

$135.00

$38.00

$17.00

Money raised

$75.0B

$16.0B

$226M

Value at listing

$1.77T

$104B

About $2B

First-day close

$161, up 19%

$38.23, up 0.6%

$23.89, up 41%

Founder voting power

82.4%

Majority

None special

Worst fall below IPO price

15% so far

53.3%

Recovered fast

Time to get back to IPO price

Pending

14.5 months

Weeks

What Meta’s Lock-Up Actually Did to the Stock

This is the part worth remembering. Meta went through the same fear in 2012, twice.

The first unlock came on August 16, 2012, covering 271 million shares. The stock fell 6.3% that day.

The second was far bigger. On November 14, 2012, some 1.19 billion shares came free.

The stock went up 12.6%. The biggest wave of selling turned into the best day.

The damage had already been done in advance. Meta bottomed on September 4, 2012, closing at $17.73. That was 53.3% below its IPO price, more than three times the fall SpaceX holders have seen.

“This is an example of why it’s so dangerous to rush into buying a heavily hyped IPO during its first few days of trading,” Peter Schiff noted.

What Would Turn SpaceX Stock Around

Meta did not recover on hope. It recovered on one number.

On July 24, 2013, it reported that mobile made up about 41% of its ad sales. Three quarters earlier the figure was near 14%.

Revenue grew 53% in a year. The stock jumped almost 30% the next day.

It finally closed back above $38 on August 2, 2013. That took 14.5 months.

SpaceX needs a number of its own. Starlink profits, launch numbers, and Starship progress are the candidates.

Analysts cannot agree on what any of it is worth. Their price targets run from $156 all the way to $239.

Morgan Stanley says a drop to $100 would price the company’s AI work at almost nothing. Chart watchers point to a falling wedge pattern that often breaks upward.

Cathie Wood still calls SpaceX her favorite long-term holding. Meanwhile Google’s SpaceX stake stays locked up for longer.

Meta took 14.5 months and one very good earnings report. SpaceX gets its first shot at that on August 4, two days before the selling can start.

The post The Closest IPO Parallel to SpaceX Is Not Tesla But This Stock appeared first on BeInCrypto.

Cointelegraph is committed to providing independent, high-quality journalism across the crypto, blockchain, AI, and fintech industries.

All news, reviews, and analyses are produced with full journalistic independence and integrity. For more details on our standards and processes, please read our Editorial Policy.

Bitcoin (BTC) heads into the end of July juggling volatility catalysts as the Federal Reserve reacts to US inflation.

Key points:

- The Fed will deliver its latest decision on interest rates as US bond yields spike, with markets seeing a September hike as likely.

- June PCE inflation is due on Thursday after hitting a three-year high of 4.1% last month

- Signs of a shift in the equities uptrend places the focus on Bitcoin’s macro correlation.

- Whales exchange inflows cool by 44% since June

Markets remain split on rate outlook

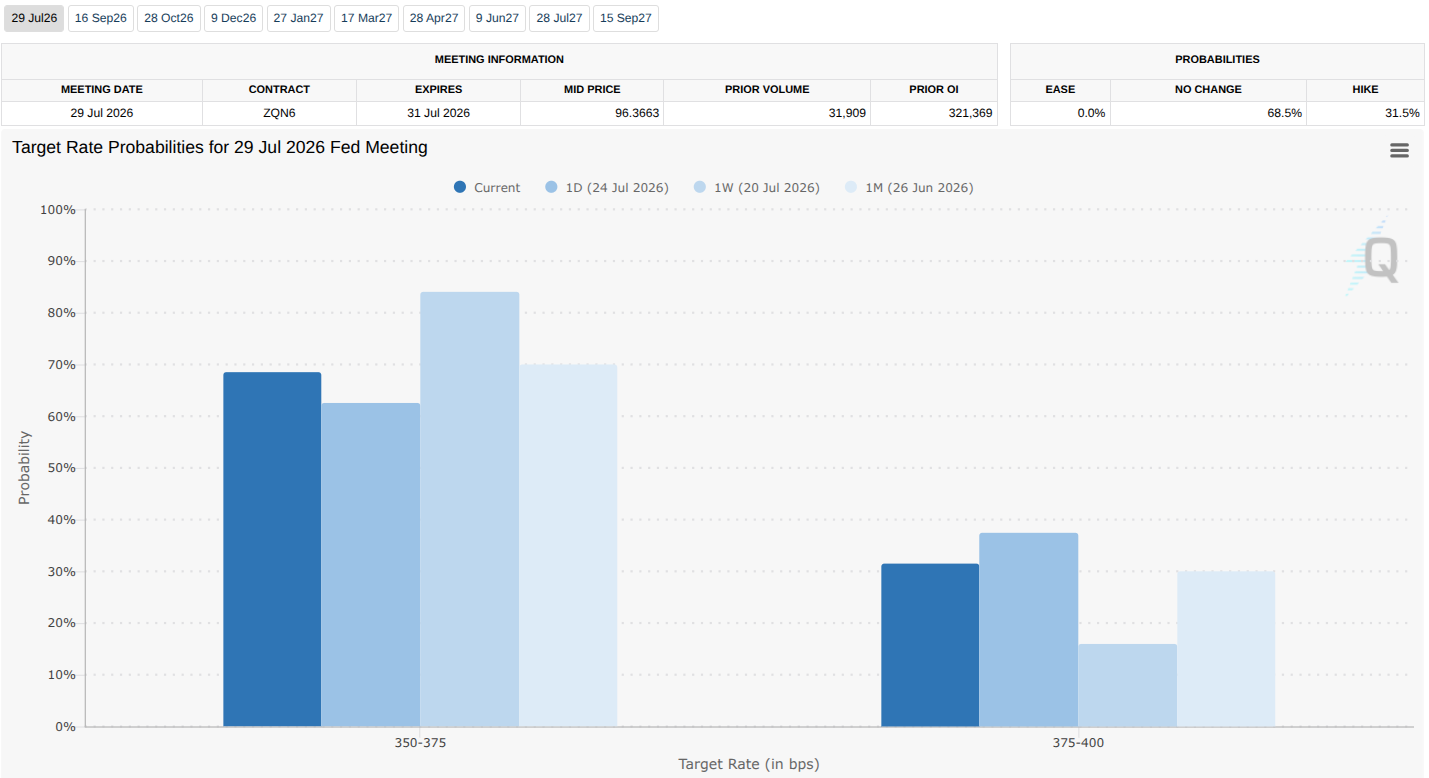

Attention turns once more to the US Federal Reserve this week, with the Federal Open Market Committee (FOMC), chaired by Kevin Warsh, set to announce its latest interest rate decision on Wednesday, July 29.

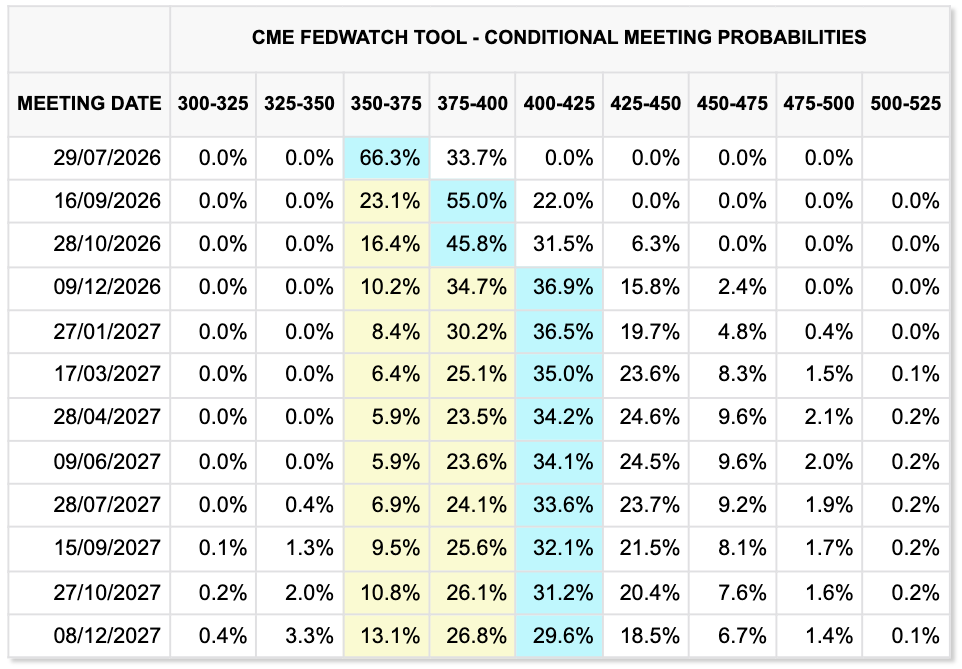

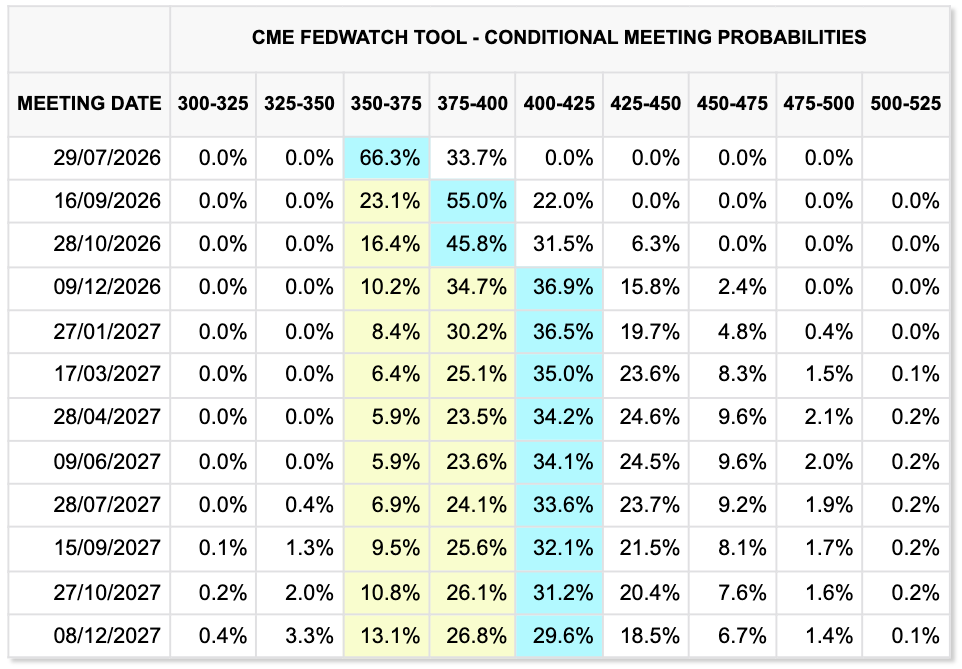

A combination of geopolitical tensions and persistent inflation pressures has reshaped expectations for Fed policy and put the possibility of further rate hikes back on the table as the US 2-year Treasury yield climbed to 4.3% last week. The latest data from the CME Group’s FedWatch Tool currently sees a 31% chance of a hike this week, with a hike at the September meeting having odds as high as 50%.

Fed target rate probabilities (screenshot). Source: CME Group

These rate hike expectations were tempered slightly as oil prices dropped 8% in the early hours of Monday as the US and Iran paused strikes. Rate hike odds therefore shifted from 37.4% to 33.7%. Ongoing developments in the Middle East thus continue to introduce volatility into the macroeconomic outlook, even as PPI inflation data released earlier in the month came in below expectations.

Fed target rate probability comparison for July FOMC meeting (screenshot). Source: CME Group

Commenting, trading resource Mosaic Asset Company also noted a pending upward breakout in 30-year bonds. Although the long end of the bond curve now plays a diminished role in funding the US government, this could notionally add to pressure on Warsh as he shapes his language at the post-FOMC press conference.

“The 30-year Treasury yield is also testing a key breakout level once again. In May, the 30-year yield saw a false break above the 5% level which has served as resistance since late 2023,” it summarized in the latest edition of its regular newsletter, The Market Mosaic.

US 30-year bond-yield data. Source: Mosaic Asset Company

Even before the latest turmoil, new Fed chair Warsh had steered clear of dovish language on the economy and kept his post-FOMC statement and press conference notably brief.

“Inflation remains elevated relative to the Committee’s 2 percent goal, in part reflecting supply shocks that have driven price increases in certain sectors, including energy,” he said at the time.

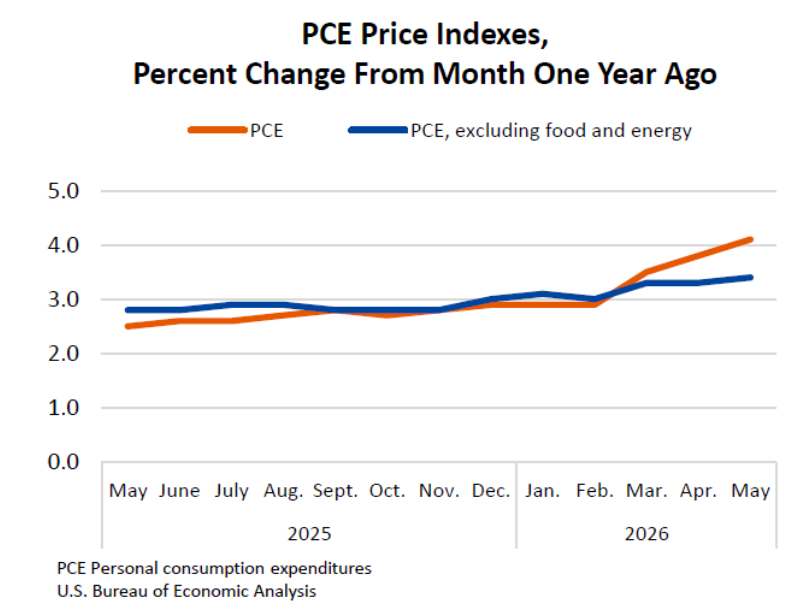

PCE inflation seen falling from three-year high

Beyond the FOMC, markets will be watching the Personal Consumption Expenditures (PCE) index on Thursday for fresh signals over the impact of the US-Iran war on inflation trends. The June print of the index, currently sits at three-year highs.

PCE volatility can have a snap impact on risk-asset performance as traders reprice potential Fed reactions. June’s release coincided with Bitcoin dropping to macro lows around $58,000.

Prefacing its latest analysis, the International Monetary Economics Network (IMEN) predicted that PCE would be moderately lower compared to May’s 4.1% year-on-year tally. “U.S. inflation: We currently expect June PCE inflation to be 3.7% year‑over‑year,” it wrote on X.

US PCE inflation data (screenshot). Source: Bureau of Economic Analysis

Correlation between Bitcoin and equities remains absent

On higher timeframes, correlations between Bitcoin and major equity indices have largely disappeared. Data from TradingView currently puts the daily correlation between BTC/USD and the S&P 500 with a 20-week loopback window as practically absent, at its lowest levels since March. Against the tech-heavy Nasdaq Composite Index, meanwhile, its current correlation coefficient of 0.11 was last observed in mid-February. While correlations on the weekly timeframe move slowly, bearish geopolitical and macro events have the potential to make the two asset classes move in lockstep again.

BTC/USD one-week chart with rolling 20-week stocks correlation. Source: Cointelegraph/TradingView

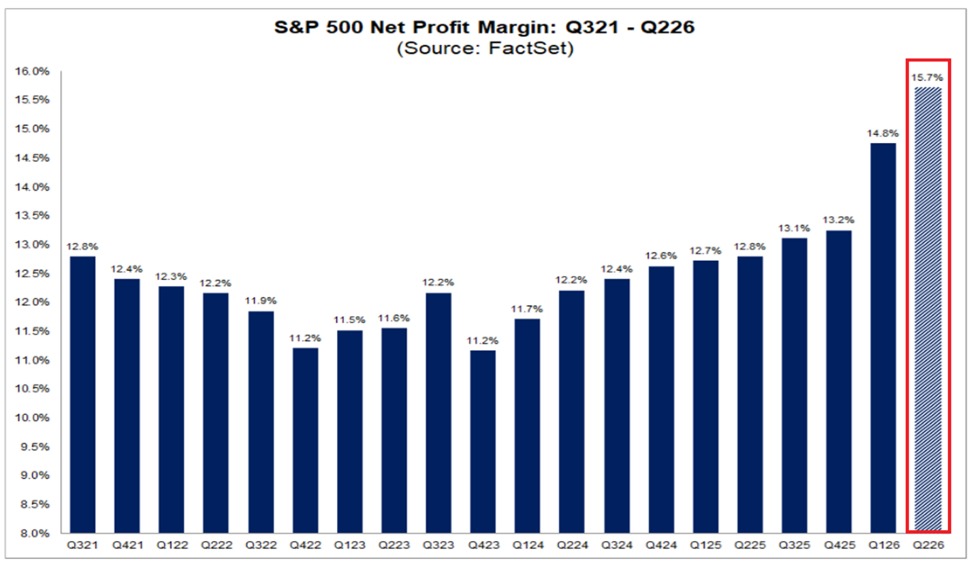

For now, corporate earnings in the US have continued to surpass expectations. However, given the historically high valuations, this is unlikely to shield the market from potential pullbacks. Several major US tech stocks saw significant drawdowns last week. The Magnificent 7 falling by an aggregate 5.3% through Friday after $GOOGL and $TSLA had already suffered sell-offs earlier in the week.

In spite of this, “Alphabet, $GOOGL , is the single largest margin contributor after significantly beating earnings estimates,” the Kobeissi Letter commented on the topic at the weekend.

“Meanwhile, 86% of reporting S&P 500 firms have so far beaten EPS estimates, while 80% have exceeded revenue expectations. AI is driving historic earnings growth.”

S&P 500 net profit-margin data. Source: The Kobeissi Letter on X.com

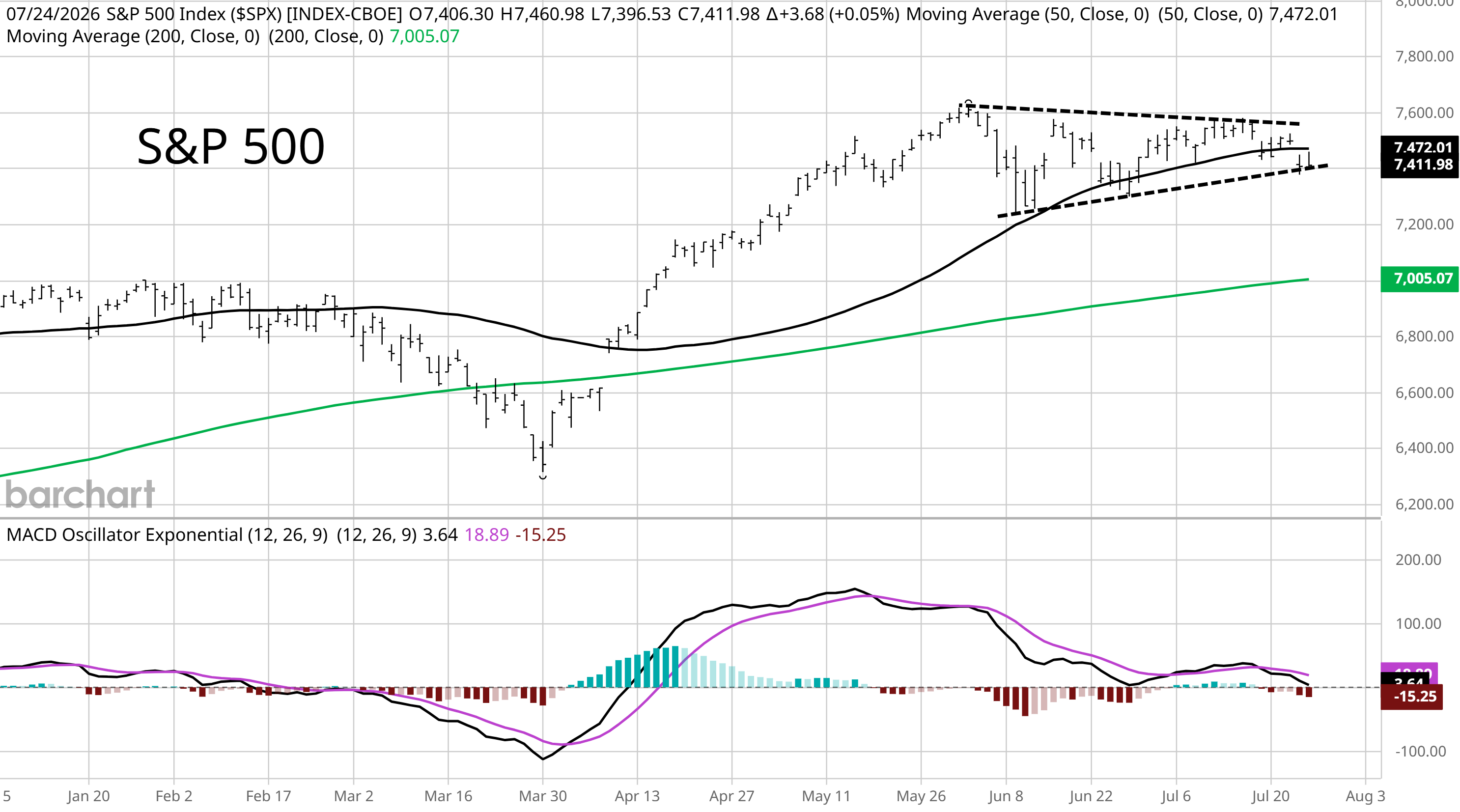

Mosaic Asset Company highlighted the risks that the rate environment may exert on US equities.

“Rising rates across the yield curve could keep pressuring stock prices, where indexes like the S&P 500 and Nasdaq peaked in early June and are now losing key support levels. At the same time, market breadth is deteriorating while the backdrop for seasonality is transitioning from a bullish tailwind to bearish headwind. Seasonality during mid-term election years also tends to produce lower average returns and larger drawdowns.”

With these emerging hurdles, the S&P 500 is at risk of losing its bullish setup altogether, Mosaic warns.

“The S&P already lost one key support level with the 50-day moving average (MA – black line). If trendline support in the triangle gives way, that could set up a test of the 200-day MA (green line) that’s currently near the 7,000 level (or 5% downside from current levels),” it added alongside an explanatory chart.

S&P 500 data. Source: Mosaic Asset Company

On shorter time frames, the picture remains fluid, with a pause in hostilities between the US and Iran providing a bullish impulse across risk assets. US WTI crude oil dropped as low as $83 per barrel to start the week, having previously eyed $95.

“The market is beginning to price-in a peace deal again,” Kobeissi responded.

CFDs on US WTI crude oil one-hour chart. Source: Cointelegraph/TradingView

“Boring” BTC price range tests 50-month trend line

Bitcoin went on to seal new local highs after Sunday’s weekly close, reaching $65,680 on Bitstamp. Still in a familiar range, BTC/USD battled its 50-month exponential moving average (EMA) trend line, having previously flipped it to resistance in a copycat move from the 2022 bear market.

BTC/USD one-day chart with 50-month EMA. Source: Cointelegraph/TradingView

Commenting on the current market setup, trader and analyst Rekt Capital flagged resurgent sell-side pressure.

“The more seller-dominant the volume becomes while Bitcoin is at resistance, the greater the chances for a rejection from here,” he warned X followers on Sunday.

Rekt Capital brought the 200-week simple moving average (SMA) into the equation, describing price as “sandwiched” between it and its 50-month counterpart.

“Continued price compression here is unsustainable and will eventually force major volatility,” he forecast.

“And if the seller volume keeps coming in at this rate, then there’ll likely be a breakout on seller volume to precede a rejection from this local resistance area.”

BTC/USD one-week chart. Source: Rekt Capital on X.com

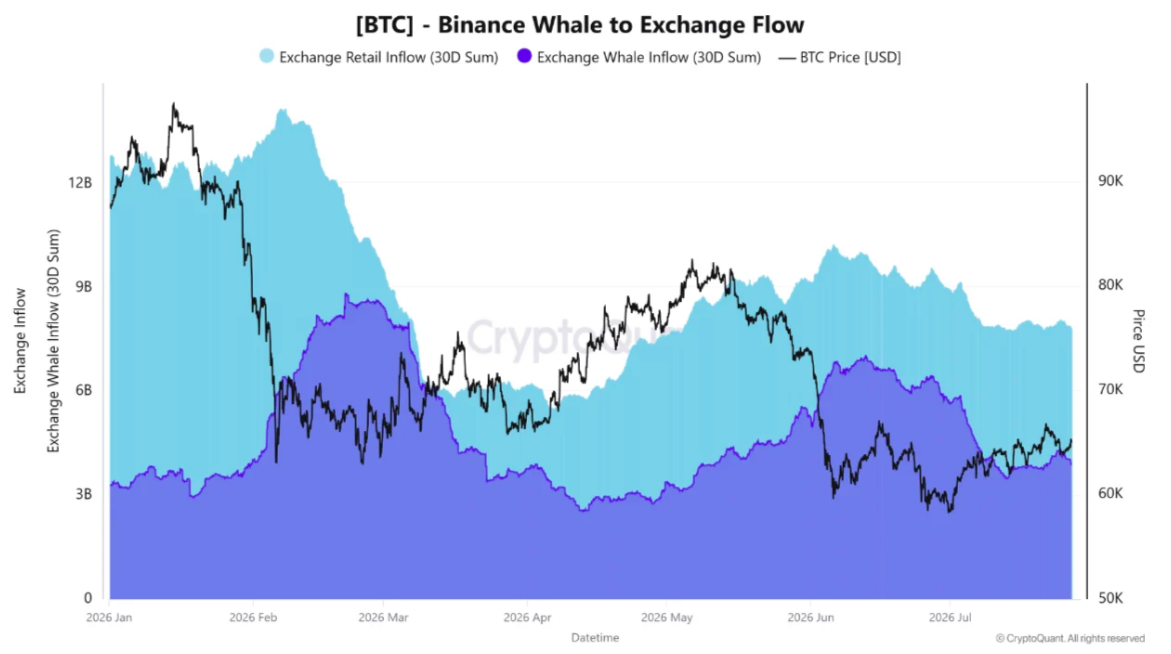

Binance whale inflows nearly halve since mid-June

Commenting on the FOMC meeting and its impact on crypto markets, onchain analytics platform CryptoQuant sees a potential knock-on effect for sell-side pressure on major exchanges.

Related: BTC supply in profit eyes 60%, but analysis hints recovery may ‘roll back over’

According to their data, BTC inflows from whales to Binance, have dropped by up to 44% since June 12, while retail inflows fell 22%.

“This leaves retail inflows at roughly twice the level of whale inflows, with a gap of $3.9 billion,” contributor Amr Taha wrote in a blog post on Monday.

“The divergence suggests that the composition of BTC transfers into Binance has shifted: retail participants are currently significantly more active than whales in sending BTC to the exchange.”

Bitcoin whale inflows to Binance (screenshot). Source: CryptoQuant

Taha described the FOMC meeting as a “major macro catalyst” that could reshape the approach of all investor cohorts to the market.

“With retail inflows now running at 2x whale inflows, Wednesday’s Fed decision could provide an important test of whether the current divergence between the two BTC cohorts persists or begins to converge,” he concluded.

As Cointelegraph reported, Binance saw single-day withdrawals of over 9,000 BTC last week.

The deal brings wallet technology to Payward’s enterprise platform, potentially reducing the number of infrastructure providers businesses need to integrate with.

Nic Carter reportedly almost joined World Liberty Financial (WLFI), the Trump family crypto venture. He allegedly walked away when cofounder Steve Witkoff said “memecoin” as “me-me” coins.

Carter described the 2024 Miami meeting to New York magazine. World Liberty says his account is wrong, and that it never offered him the job.

Witkoff Could not Explain the Product

Carter invests for Castle Island Ventures. He also voted for Trump in 2024. Witkoff wanted him as an advisor. But Witkoff could not describe the decentralized finance (DeFi) business.

“He didn’t know what crypto or DeFi was. He didn’t know what the pitch was,” the New York feature reported, citing Nic Carter.

Witkoff had one clear goal, Carter says. The launch had to happen before the election. That way Trump was still a private citizen.

Carter turned the role down. He warned the project could cost Trump votes. That is when Witkoff’s tone hardened.

World Liberty’s own Gold Paper supports part of that read. It says the sole utility of WLFI is governance. Holders get no right to any return or dividend.

WLFI Holders are Still Locked In

WLFI trades near $0.055, against a record of $0.3313 on Sept. 1, 2025. That was the first day of open trading. The price fell 40% before it ended.

World Liberty released only 20% of each investor’s tokens that day. Just 31.8% of the supply trades now. An April plan unlocks the rest from 2028. Holders who vote against it stay locked.

The company also added a contract function letting it freeze any wallet. That change landed eight days before trading opened.

Justin Sun was the largest early backer. He sued World Liberty Financial in California for fraud. The company countersued for defamation in Miami. Both cases remain at an early stage.

The venture has been lucrative for the family even as the token sank. Reporting on the Trump family crypto windfall tracks how little of it reached ordinary holders.

Carter saw a token with no business behind it. Two years on, most of the supply is still frozen. The unlock schedule runs past the end of Trump’s term.

The post VC Reportedly Rejected Trump Crypto Venture After Steve Witkoff’s Memecoin Blunder appeared first on BeInCrypto.

New York City just published a list of 31,000 homes. It names the streets, the buildings, and the apartment numbers. Crypto founders say it is a map to rich people’s front doors.

The city released the file on July 24. It exists to find second homes that owe a new tax. Officials expected about 10,000 properties. They got three times that.

What New York City Actually Published

The tax started July 1. It targets homes that are not where the owner actually lives.

A condo or co-op lands on the list at $1 million. A house has to be worth $5 million.

That $1 million line matters. It is why the roll holds 24,700 apartments but only 6,800 houses.

State law told the city to name every property that “may be subject” to the tax. It also told the city to identify co-op apartments by street address and unit number.

So the file does not just flag a building. It flags the apartment.

Ben Williams is a property tax lawyer at Rosenberg & Estis. He testified at the city’s hearing on the rules. He told Bloomberg the list is far too broad, and that many homes will come off it on appeal.

Spectrum News NY1 reporter Bernadette Hogan flagged the file, noting that owner names sit in the spreadsheet as well.

Bills go out by August 30. Owners then get 30 days to object. The final list is due December 31.

Crypto Founders Call It a Mass Doxxing

Uniswap founder Hayden Adams searched a few luxury buildings. He found the homes of people he knows. He also found nearly every other unit in those towers.

“Not only were their units listed, but nearly every unit in the entire building was listed. They clearly took an incredibly expansive view of ‘could be’ and just doxxed a huge percentage of all expensive apartments in new york city,” wrote Adams.

That is the law working as written. The city has to list every unit that might owe the tax. At a $1 million threshold, that pulls in whole buildings.

Helius CEO Mert Mumtaz made a narrower point. The data was already public, he said. It was just messy. Now it is clean, sorted, and easy to download.

Castle Island Ventures partner Nic Carter went further. He pointed to the France crypto kidnapping toll, which has climbed all year.

“So this is a list of wealthy people and their addresses. As we’ve seen in France and Sweden this leads to crypto kidnappings torturings and murders. Yes real estate records are semi public but this is an easily searchable database and target list,” Carter stated.

Attack Data Gives the Warning Weight

CertiK counted 52 wrench attacks in the first half of 2026. A wrench attack is simple. Criminals use force or threats to make someone hand over their crypto.

The count was 39 a year earlier. It follows the most violent year recorded for crypto crime.

The sums got much bigger too. Victims faced $124.2 million in the first half of 2026, up from $10.5 million. The average case jumped from $270,000 to $2.39 million.

One number stands out. Home invasions rose from a single case to 20.

But the map does not point at New York. France had 33 of the 52 attacks. Europe had 39. The United States had four. Sweden, which Carter named, had two.

The risk is about method, not place. CertiK calls it “data-driven targeting.” Attackers stitch together leaked databases, property records, and tax files. They build a full profile before they ever knock on a door.

That is not theory. French investigators say a tax office employee sold crypto investor data to criminal networks. The same fear followed new UK tax rules that make exchanges hand over user data.

CertiK now urges regulators to lock down government databases that tie people to crypto and addresses.

New York’s list holds no crypto data at all. What it adds is the address. That only helps someone who already knows you own crypto.

The final roll arrives December 31. How far it falls below 31,000 will show how seriously the city took the warning.

The post Finding Crypto Millionaires in New York Just Got Easier appeared first on BeInCrypto.

“Crypto + AI” is the new “blockchain + [anything].” A desperate rebrand for failing business models, and investors aren’t buying it.

The Pattern We’ve Seen Before

2017: Every company added “blockchain” to their name and watched their stock price triple.

Kodak became KodakCoin. Long Island Iced Tea became Long Blockchain Corp. A company that made fruit juice rebranded to blockchain and saw its shares surge 200% overnight.

None of it was real. All of it eventually collapsed.

2026: The same thing is happening with AI. Except this time, it’s crypto companies doing the rebranding—and it’s failing faster.

What’s Actually Happening Right Now

Bloomberg reported it today: the once-hot market for cryptocurrency treasury stocks has imploded. Companies that bet their entire identity on Bitcoin accumulation are now pivoting to artificial intelligence to win back investors.

The numbers are brutal:

K Wave Media, a former Bitcoin accumulator that shifted to data center development, has seen its shares fall 71% since rebooting in May.

Satsuma Technology approved the full liquidation of its 668 BTC. The move was so drastic it triggered the company’s delisting from the London Stock Exchange. A company deleted itself from a major exchange to exit crypto.

Sequans Communications sold 1,025 BTC, along with almost 80% of its remaining holdings, just to repay convertible debt.

MARA Holdings and Bitdeer have been selling Bitcoin to repay debts while simultaneously redirecting resources toward AI data centers.

Even Strategy, formerly MicroStrategy, the loudest evangelist for the corporate Bitcoin treasury model, sold approximately 3,620 BTC and authorized further sales. They still hold over 840,000 BTC, making them the largest corporate holder. But even the true believer is selling.

The corporate Bitcoin treasury model isn’t just struggling. It’s unwinding in real time.

Why The AI Pivot Isn’t Working

Here’s what these companies are betting on: if we say “AI” enough times, investors will forget we said “Bitcoin” and give us another chance.

It’s not working. K Wave Media’s 71% decline happened after the pivot, not before.

Why? Because investors aren’t stupid. They’ve seen this movie before.

When a company pivots its entire identity to chase a hot trend, it signals one thing: the original strategy failed, and management has no real conviction about what comes next.

A Bitcoin treasury company that suddenly loves AI data centers isn’t a tech innovator. It’s a company trying to survive by attaching itself to whatever narrative is currently attracting capital.

The market can tell the difference between a genuine AI company and a crypto company that bought a few Nvidia chips and updated its press release.

Turns out, so can Bloomberg.

Brian Armstrong Saw This Coming

Coinbase CEO Brian Armstrong said it this week, publicly:

Crypto startups that rebrand to AI are missing the point. Blockchain technology isn’t competing with AI; it’s the infrastructure that will underpin future automation.

Armstrong’s argument is precise: these aren’t two separate things you can choose between. AI needs infrastructure. Blockchain provides trustless, verifiable infrastructure for AI agents, AI transactions, AI governance.

Companies pivoting from “crypto” to “AI” as if they’re alternatives are making a category error. And they’re making it because they’re panicking, not because they have a strategy.

The companies that will survive aren’t the ones that abandoned crypto for AI. They’re the ones that understood crypto is the infrastructure for AI and built accordingly.

The Real Problem: Business Models Built On Hype

Let’s be honest about what the corporate Bitcoin treasury model actually was.

Companies like MicroStrategy (now Strategy) made a bet: buy Bitcoin, hold it, watch the price go up, use the appreciation to justify your existence as a company.

That’s not a business. That’s a leveraged Bitcoin position dressed up as corporate strategy.

When Bitcoin price goes up, you look like a genius. When it stagnates, as it has for much of 2026, hovering around $64–65K, you look like a company with no real business model, sitting on an asset that isn’t moving, with investors asking uncomfortable questions about your actual operations.

The crypto treasury model required perpetual Bitcoin appreciation to work. The moment appreciation slowed, the model broke.

And now those same companies are trying to claim they were always AI companies really.

The Difference Between Real AI And AI Panic

There’s a meaningful difference between companies building genuine AI infrastructure and companies slapping “AI” on a failing crypto strategy.

Real AI infrastructure companies:

- Have actual compute resources being used by actual customers

- Generate revenue from AI services, not just from asset appreciation

- Have technical teams building real AI products

- Can explain what their AI actually does

Crypto companies pivoting to AI:

- Announce plans to build AI data centers

- Haven’t yet generated meaningful AI revenue

- Are selling Bitcoin to fund the pivot

- Can’t clearly explain how AI fits their original thesis

K Wave Media’s 71% decline after its pivot tells you which category investors think it falls into.

The Deeper Pattern: What Happens When A Narrative Breaks

Every market cycle has a dominant narrative. The narrative attracts capital. Capital inflates valuations. Valuations attract more capital. Until the narrative breaks.

2021–2022 crypto narrative: Bitcoin is digital gold, crypto is the future of finance, every company should have a Bitcoin treasury.

Companies built entire identities around that narrative. Stock prices reflected narrative premium, not business fundamentals.

2023–2025: Narrative weakens. Institutional adoption happens but stabilizes rather than explodes. Bitcoin sits at $60–65K instead of going to $200K as predicted. The narrative premium evaporates.

2026 desperation move: Attach to the new dominant narrative (AI) before investors fully price in that the old narrative failed.

The problem: AI investors are sophisticated. They know what real AI companies look like. A Bitcoin accumulator with an Nvidia press release isn’t one of them.

Who’s Actually Winning

While crypto treasury stocks implode, two categories of companies are doing well:

1. Companies that built genuine products on blockchain infrastructure

Coinbase, whatever its challenges, built an actual exchange with actual users generating actual revenue. It has a real business that doesn’t depend on Bitcoin price appreciation alone.

2. Companies building AI infrastructure that happens to use blockchain

The companies Armstrong is describing: building the trustless infrastructure layer that AI agents will need to transact, verify, and operate at scale. This is real. It has genuine demand. It’s not a rebrand.

The companies failing are the ones that were never really building anything, just accumulating an asset and hoping appreciation would substitute for operations.

The Uncomfortable Question For Every Crypto Company

If your business model requires the price of Bitcoin to keep going up forever to justify your existence, what do you actually do?

That’s the question the imploding treasury stocks can’t answer.

And “we’re pivoting to AI” isn’t an answer. It’s a postponement.

The companies that survive the current shakeout will be the ones that had actual operations, actual users, actual revenue— that happened to use blockchain or crypto as infrastructure.

The ones that don’t survive will be the ones that confused “holding Bitcoin” with “building a company.”

The AI rebrand just delays the reckoning by a quarter or two.

What Comes Next

Expect more of this: crypto companies announcing AI pivots, investors not being fooled, stock prices continuing to decline, companies eventually running out of runway.

Expect fewer of this: genuine companies built on blockchain infrastructure, serving real users, generating real revenue—that will be fine.

The shakeout was always coming. The Bitcoin treasury model worked during appreciation. It was never a real business. Now that appreciation has slowed, the reality is visible.

The AI pivot is the last gasp. Not a new beginning.

The Lesson That Never Gets Learned

Every market cycle produces the same story:

Narrative attracts capital. Capital inflates valuations beyond fundamentals. Smart money exits. Companies desperately rebrand to the next narrative. Doesn’t work. Collapse.

2017: Blockchain everything. 2021: NFT everything, metaverse everything. 2024–2025: Bitcoin treasury everything. 2026: AI everything.

The companies that survive every cycle are the ones that were never chasing the narrative in the first place. They were building something real that happened to use the technology everyone else was hyping.

Those companies exist in crypto. They’re just not the ones making headlines this week.

If your crypto strategy requires Bitcoin to go up forever, you don’t have a strategy. You have a bet. And bets eventually lose.

Cantor Fitzgerald is advising Swiss digital asset lender AMINA Bank on a possible public listing as the Wall Street firm expands its role in crypto capital markets.

Summary

- AMINA Bank is considering a public listing, although its valuation and preferred exchange remain undisclosed.

- Cantor’s mandate follows its onchain IPO partnership with Securitize, announced earlier in July.

- AMINA recorded 69% revenue growth in 2024 and holds regulatory approvals in Switzerland and Europe.

- Cantor is also reportedly pursuing a separate deal involving up to 30,000 Bitcoin from Blockstream.

AMINA Bank considers a public listing

According to reports, Cantor Fitzgerald is advising AMINA Bank, formerly known as SEBA Bank, as the Swiss crypto lender assesses a potential entry into public markets.

Discussions remain at an early stage, and neither company has disclosed a target valuation, timetable or possible listing venue. A completed transaction would make AMINA one of the few publicly traded banks focused primarily on digital asset services.

The bank operates under a licence from the Swiss Financial Market Supervisory Authority, or FINMA. Its services include cryptocurrency custody, trading, lending and staking for institutional and private clients.

AMINA reported a 69% increase in revenue during 2024. That performance positioned it as Switzerland’s fastest-growing crypto bank at the time, although updated financial figures for 2025 and 2026 were not provided.

A listing would expose the bank to greater financial disclosure and corporate governance requirements. It could also give public-market investors direct exposure to a regulated crypto banking business rather than a cryptocurrency exchange, miner or treasury company.

Cantor expands its crypto capital markets business

The advisory role builds on Cantor’s wider attempt to connect traditional capital markets with blockchain-based financial infrastructure.

As previously reported by crypto.news, Cantor partnered with tokenization company Securitize on July 15 to support blockchain-based initial public offerings and follow-on share sales.

Cantor will provide equity capital markets and trading services under that agreement. Securitize will supply the technology needed to issue, distribute and service securities onchain, while its SEC-registered broker-dealer, Securitize Markets, will participate in offerings and settlements.

That structure differs from platforms that create blockchain-based versions of shares already trading on public exchanges. The partnership aims to use blockchain infrastructure during the original issuance process while keeping offerings within existing securities rules.

Advising AMINA fits that strategy, although no indication has emerged that the bank would use Securitize’s infrastructure for its potential listing.

AMINA builds its European regulatory reach

AMINA’s regulatory position could form an important part of its case to public investors.

Alongside its Swiss banking licence, the group secured authorization under the European Union’s Markets in Crypto-Assets framework through its Austrian subsidiary. AMINA described itself as the first international crypto banking group to obtain a MiCA licence.

The approval allows the subsidiary to offer regulated crypto services across European Economic Area markets through MiCA’s passporting system, subject to applicable local requirements.

AMINA expanded its asset support in May 2026 by becoming the first regulated bank to provide custody and trading services for Canton Coin. Canton Network focuses on blockchain infrastructure for regulated financial institutions.

For US investors, access to AMINA shares would depend on where the bank lists and whether American brokerages support the security. A US listing would also bring additional Securities and Exchange Commission registration and disclosure requirements, but the parties have not identified the United States as a venue.

Cantor pursues a separate $3 billion Bitcoin deal

Cantor is also reportedly negotiating with Blockstream co-founder Adam Back over a transaction that could place more than $3 billion in Bitcoin into a publicly traded vehicle.

Under the proposed deal, Blockstream would contribute as many as 30,000 BTC to Cantor Equity Partners 1, a special purpose acquisition company that raised $200 million in January. Blockstream would receive shares in return, while the vehicle would be renamed BSTR Holdings.

The agreement could reportedly be signed as early as this week, although its terms remain subject to change.

Cantor has not disclosed when AMINA might decide whether to proceed with its listing. The bank’s chosen exchange, valuation and offering structure will determine whether the plan develops into a conventional IPO, another public-market transaction or an onchain issuance tied to Cantor’s tokenization strategy.

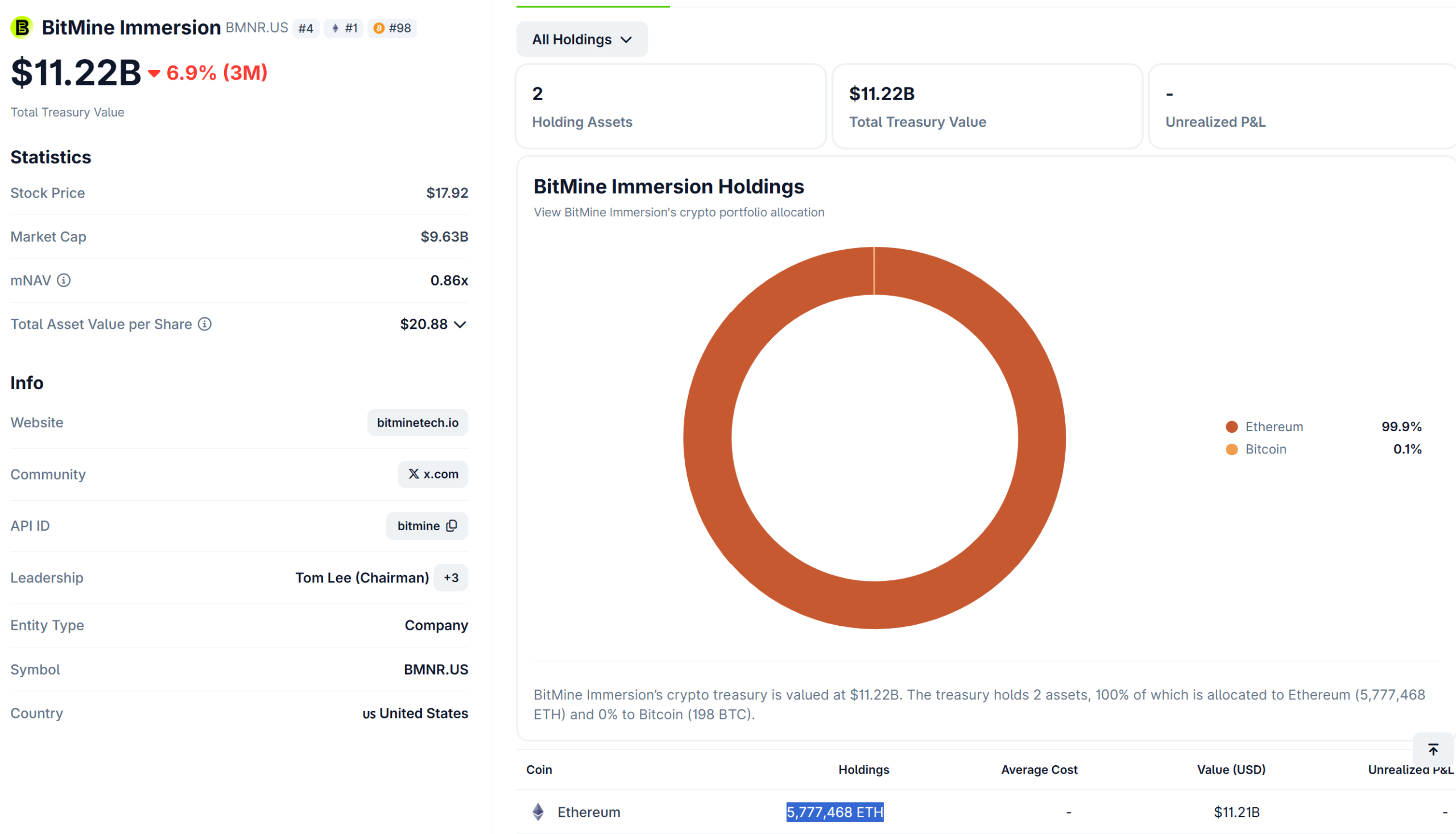

Tom Lee has called Lighter (LIT) a breakout success and a critical piece of Ethereum’s infrastructure. The remarks follow a new Bankless interview with the exchange’s founder.

Lee is no casual voice here. He chairs BitMine, which calls itself the world’s largest Ethereum treasury. The firm holds 5.79 million ether.

Why Does Tom Lee’s Lighter Call Matter?

Lee co-founded the research firm Fundstrat. He also chairs BitMine, listed on the NYSE as BMNR.

BitMine disclosed 5.79 million ether on Monday. Nearly 4.92 million of those coins are staked. So Lee holds a huge bet on Ethereum getting used.

Ether (ETH) now trades near $1,944. It is down about 49% in a year.

“Lighter is a massive breakout success and a critical infrastructure layer for Ethereum,” said Tom Lee, chairman of BitMine Immersion Technologies.

Follow us on X to get the latest news as it happens

Here is what makes the post notable. Lee’s July investor message listed Robinhood, Coinbase and Kraken’s Ink as Ethereum’s layer-2 winners. Lighter was not on it. Now he calls Lighter critical.

That is a new name on the list he uses to argue Ethereum’s Wall Street case.

What Is Lighter?

Lighter is an Ethereum layer-2 perp DEX. In plain terms, it lets people trade crypto with leverage, without a company holding their coins.

It runs on zero-knowledge proofs. These let anyone check that trades and liquidations were handled fairly.

The scale is real. Lighter handled $43 billion in trading volume over 30 days. It holds $822 million in open bets and $525 million in deposits.

Founder Vlad Novakovski finished Harvard at 18. He later traded at Citadel and ran engineering at Addepar. He told Bankless the system took 18 months to build.

Lighter began as a networking app called Lunch Club. It switched direction in 2022. It later raised a $68 million funding round from Founders Fund, Ribbit Capital and Robinhood Ventures.

But Is Lighter Growing?

Lighter (LIT) trades near $2.19. It is up 4.7% today and 23.7% this month. Its market value sits near $547 million.

The earnings trend is weaker. Quarterly revenue fell from $39.7 million to $19.7 million, then to $9.6 million.

LIT also sits far below its $7.86 high from December. It stays above its $0.78 low from March.

Lee calls Lighter infrastructure, not a trade. He has also said BitMine wants to invest in crypto unicorns. That gives his praise a second meaning.

The post Tom Lee Says This Ethereum Project Could Be a Game-Changer appeared first on BeInCrypto.

Daily horoscope July 28, 2026: Predictions for your star sign

LARRY KUDLOW: Surely the GOP can defeat big government socialism and weird values

Google Gemini AI Predicts Solana Price Could 8x Before End of 2026

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World7 days ago

Crypto World7 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat6 days ago

NewsBeat6 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech23 hours ago

Tech23 hours agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Tech7 days ago

Tech7 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech7 days ago

Tech7 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

Business6 days ago

Business6 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment6 days ago

Entertainment6 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World5 days ago

Crypto World5 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics12 hours ago

Politics12 hours agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

NewsBeat7 days ago

NewsBeat7 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Sports4 days ago

Sports4 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Sports1 day ago

Sports1 day agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

News Videos4 days ago

News Videos4 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Fashion4 days ago

Fashion4 days ago16 Dresses for the High Summer Event

-

Politics1 day ago

Politics1 day agoSpain sweeps the board at 2026 World Cup with individual awards

-

Crypto World7 days ago

Crypto World7 days agoAndrew Cuomo joins OKX board as crypto exchange expands in U.S.

-

Entertainment3 days ago

Entertainment3 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos1 day ago

News Videos1 day agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger adds $2.6B as RWA inflows rank second

You must be logged in to post a comment Login