Crypto World

XRP slips 4% below $1.20 after breakout rally stalls near key resistance

XRP’s push toward $1.25 ran into the same problem that has capped every rally since the spring selloff: sellers waiting overhead. After briefly trading above $1.22, the token lost the $1.20 level on heavy volume and spent the rest of the session trying to stabilize above support near $1.18.

The pullback doesn’t fully undo last week’s breakout, but it does show buyers still have work to do before the market can challenge higher resistance levels.

News Background

• XRP remains in focus after recent ETF inflows and growing institutional participation helped drive last week’s rally above $1.20.

• Analysts continue to watch the $1.11-$1.15 demand zone that launched the latest recovery, viewing it as the line separating a correction from a larger breakdown.

• Longer-term charts still show XRP trading beneath major moving averages despite the rebound from early June lows.

Price Action Summary

• XRP fell from $1.2170 to $1.1869 during the 24-hour session, losing 2.5%.

• Selling intensified during the June 17 19:00 UTC session when volume surged to 128.7 million XRP, more than double normal levels, breaking support at $1.20.

• The token later found buyers near $1.1750 and recovered modestly into the close, holding above the session low of $1.1747.

Technical Analysis

• The loss of $1.20 is the key development. That level had acted as support after XRP’s breakout above $1.14 and $1.18 earlier in the week.

Bitcoin momentum is rebuilding, but confirmation has not arrived yet, said analytics platform Swissblock on Monday as BTC tapped a five-week high of $65,700.

“Bitcoin has exited its capitulation regime and is once again inside the transition area,” they added.

Swissblock identified the current area as “where a new impulse begins, or momentum fades back into weakness.”

Where to Next for Bitcoin?

It added that the next test is clear and it needs to “reclaim the ignition line” to push above the “next Inflection point.” “Every sustained rally began with this sequence, but not every transition has succeeded,” it said.

Bitcoin has been in the capitulation zone since early June when it fell below $70,000, having remained below it ever since. It hit a current cycle low of around $58,000 at the end of June and has been trending higher ever since, gaining 12% over the past three weeks, which has moved it into a higher momentum or transition zone.

Is a bitcoin:native breakout on the verge of happening?

Momentum is rebuilding, but confirmation has not arrived yet.

Bitcoin has exited its Capitulation regime and is once again inside the Transition Area.

This is where a new impulse begins or momentum fades back into… pic.twitter.com/m0GBVttR7n

— Swissblock (@swissblock__) July 20, 2026

CryptoQuant analyst ‘Darkfost’ said on Monday that Bitcoin has spent 95% of its time at a higher MVRV. This metric compares market cap, calculated as price multiplied by supply, with its realized value, which reflects the price of each coin when it last moved.

“This shows just how significantly undervalued BTC is today compared to its historical evolution.”

Meanwhile, crypto trader ‘Daan’ said the $65,000 level has capped price for the entirety of July so far, before adding:

“But I do think the longer price spends here, the more likely the $65K level is to break. Especially with the higher lows being made over the past 3 weeks.”

BTC Price Outlook

Bitcoin was trading at $65,500 at the time of writing, following a 1% gain on the day. It tapped $65,700 in late trading on Monday, which is its highest level since June 15 when it topped $67,000 briefly.

Zooming out shows that the asset remains within a seven-week range-bound channel, but at resistance at the upper bounds of that channel.

“If BTC breaks above $66K, the next key level to watch is $66,700,” said Alphractal founder and CEO Joao Wedson.

“This is the Structural Midline, a key on-chain level from the Structural Market Bands that has historically acted as a highly reliable reaction zone,” he said before adding that bears will likely try to regain control around this area.

The post Bitcoin Has Exited Capitulation Regime as Momentum Rebuilds: Analysts appeared first on CryptoPotato.

The U.S. Commodity Futures Trading Commission ordered KalshiEX, LLC to fulfill trades that a Michigan state court had directed the prediction-market operator to cancel, escalating a fight over whether states can reach into federally regulated derivatives venues. In Release Number 9267-26, dated… Read the full story at The Defiant

Two other supports lined up behind the move. U.S. spot bitcoin ETFs have now drawn inflows for five straight sessions totaling more than $600 million, the most sustained institutional buying since mid-July and a reversal of the eight-week outflow run that ran through late June.

And oil, which had climbed for two days on the war, pulled back, with Brent falling 1% to about $88.58 as Iran said mediators were circulating proposals to ease hostilities, including a reported suggestion for a 10-day halt in strikes.

“Current bitcoin and ether prices are low but fair, given the macro uncertainties pervading markets,” said Jeff Mei, chief operating officer at BTSE, who pointed to the Fed meeting as the event traders are positioned around.

“Traders expect rates to hold steady but are looking for more signals as to what’s to come later in the year,” Mei added.

The read on that meeting is where the rally meets its limit. The Federal Reserve gathers July 28 and 29, and markets put the odds of a July rate increase at about 15%, though a September move is still live.

Spot-market volume across crypto stayed subdued even as prices rose, the sign of a tape lifted by returning risk appetite rather than fresh conviction, and higher oil and Treasury yields remain the levers that could keep the Fed hawkish and cap risk assets.

US voters remain deeply skeptical of the federal government owning stakes in American companies, a new poll found.

Their doubt comes as the government has made 30 deals worth $26.7 billion since 2025, according to the Council on Foreign Relations.

Follow us on X to get the latest news as it happens

US Voters Sour on Government Ownership Stakes in Companies

The CNBC survey polled 1,000 registered voters from July 8 to 12, with a 3.1-point margin of error. Only 19% found government stakes appropriate, while 49% did not. In addition, 32% stayed undecided.

Partisan gaps were wide. Some 66% of Democrats called the stakes inappropriate, against 34% of Republicans.

Even Trump’s base wavered. MAGA Republicans split evenly, with 31% in favor and 31% opposed. Another 38% held no view.

Opposition has softened since October 2025, when 56% of voters called government ownership inappropriate, against just 13% who approved. Disapproval has since fallen seven points as approval climbed, and a third of voters stayed on the fence.

CNBC noted that the Trump administration has treated some stakes as opportunistic bets and others as part of a broader economic strategy.

The largest arrived in August 2025. The government took a 10% stake in chipmaker Intel by giving $8.9 billion in grants approved under the Biden administration. That position has since climbed 372%. It was worth $42 billion at Thursday’s close.

Meanwhile, OpenAI has also reportedly pitched a 5% government stake, a position worth about $42.6 billion at its $852 billion valuation.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Half of US Voters Reject Government Taking Stakes in American Companies appeared first on BeInCrypto.

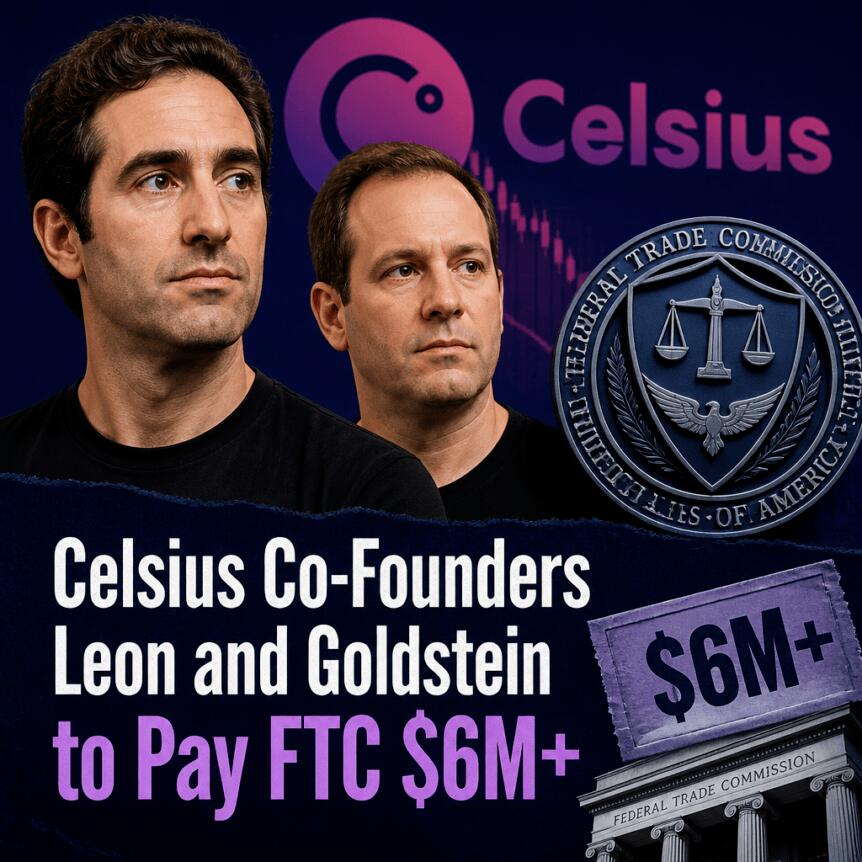

Federal regulators have extended the legal fallout from Celsius’ 2022 collapse by ordering two of the company’s former co-founders to pay more than $6 million to resolve Federal Trade Commission (FTC) allegations that they misrepresented the safety of the crypto lending platform.

On Monday, the FTC announced that Hanoch “Nuke” Goldstein, Celsius’ former chief technology officer, was ordered to pay $2.014 million. Shlomi Daniel Leon, the firm’s former chief strategy officer, was ordered to pay $4.1 million under a separate stipulated order entered on June 29.

Key takeaways

- Goldstein and Leon have been ordered to pay a combined $6.114 million to settle FTC consumer protection allegations tied to Celsius’ failure.

- The orders include marketing and sales bans affecting products or services that could be used to deposit, exchange, invest, or withdraw crypto assets.

- The FTC’s claims focus on alleged misstatements about Celsius’ reserves, insurance coverage, and whether loans were unsecured.

- The settlements build on a separate FTC resolution involving Alex Mashinsky, which already included a $10 million payment and a permanent marketing ban.

- Payments from the co-founders are also set to be credited against the FTC’s consumer-harm judgment tied to the case.

What the FTC says the co-founders got wrong

According to the FTC’s allegations, Celsius made assurances to customers about the platform’s financial safety that were not consistent with the company’s actual position as it moved toward bankruptcy. The regulator said Celsius falsely told customers it maintained sufficient reserves to satisfy withdrawal demands, claimed it had a $750 million insurance policy covering customer deposits, and represented that it did not issue unsecured loans.

The FTC further alleged that these public assurances persisted even shortly before the company’s collapse. As the agency put it in its statement Monday, the promises were allegedly false and “its top executives continued to claim that customers’ deposits were safe days before the company filed for bankruptcy.”

Goldstein and Leon are being held responsible for the misconduct the FTC described in connection with how Celsius marketed its operations during the period leading up to the shutdown.

Court-ordered bans restrict Celsius-related promotion and sales

Beyond the monetary payments, the FTC’s settlement terms also impose restrictions designed to limit future involvement in crypto custody and dealing workflows. The agency said the orders bar Leon from marketing or selling products or services that could be used to deposit, exchange, invest, or withdraw assets.

For Goldstein, the restrictions are similarly broad. The FTC’s statement Monday said Goldstein agreed to a ban on marketing or selling retail products or services that can be used to buy, sell, deposit, withdraw, distribute, or trade cryptocurrency.

“Similarly, Goldstein has agreed to a ban on marketing or selling retail products or services that can be used to buy, sell, deposit, withdraw, distribute or trade cryptocurrency.”

How the payments fit into the wider Celsius settlements

The settlements add another layer to the ongoing enforcement picture surrounding Celsius’ collapse and its impact on customers. The platform, which the settlement narrative places in a much larger consumer-harm context, held $25 billion in assets at its peak and owed $4.7 billion to users when it filed for bankruptcy in July 2022.

The FTC’s co-founder orders also relate directly to an earlier resolution involving Alex Mashinsky. In April, Mashinsky agreed to an FTC settlement that included a permanent ban from promoting asset-related products and a requirement to pay $10 million, alongside a broader, partially suspended $4.72 billion judgment.

In the current cases, the FTC said that the $2.014 million and $4.1 million payments from Goldstein and Leon, respectively, will be credited against the $4.72 billion judgment. That crediting mechanism is intended to prevent double-counting of consumer-harm-related penalties across related FTC outcomes.

Criminal case developments underscore the regulatory focus

While these are FTC consumer protection resolutions, other enforcement tracks have also advanced. Separately, US prosecutors have pursued criminal charges against Mashinsky. The filing timeline described in the source indicates Mashinsky pleaded guilty to commodities and securities fraud charges and was sentenced to 12 years in prison in May 2025.

Prosecutors, as described in the reporting referenced in the source, said he misled Celsius customers about the company’s profitability, investment risks, and the safety of customer funds. That criminal framing aligns with the FTC’s core theory in the co-founder cases: that customers were allegedly given assurances about safety and risk management that did not match reality.

For investors and industry participants, the practical takeaway is that Celsius-related enforcement is not confined to one executive or one courtroom. The FTC’s added restrictions on future marketing and sales of crypto asset-related products suggest regulators are targeting the ability of former insiders to re-enter similar distribution and promotion channels. Readers should watch whether additional Celsius-linked proceedings—civil or criminal—continue to expand the circle of accountability and how courts treat the scope of the marketing bans as the industry adapts to ongoing compliance demands.

Cuy Sheffield, Visa's head of crypto, said x402 has processed roughly $19 million across roughly 134 million transactions on an adjusted basis, according to a thread he posted Wednesday on X. x402 is a payments protocol for agent- and machine-initiated onchain transactions. The figures come from a… Read the full story at The Defiant

A federal judge approved Anthropic’s $1.5 billion settlement with authors on Monday, finalizing the largest known payout in a US copyright case.

US District Judge Araceli Martinez-Olguin granted final approval and overruled objections from authors who called the sum too small.

How Anthropic’s $1.5 Billion Settlement Reached Approval

Authors sued the artificial intelligence (AI) company Anthropic in 2024. They alleged that it used pirated copies of their books to train its Claude chatbot.

Now-retired Judge William Alsup ruled last June that training on the books was fair use. However, he found that Anthropic had broken the law by storing more than 7 million pirated books.

Martinez-Olguin took over after Alsup retired. She signed the final order on Monday.

“We reached this settlement in 2025, after the court’s landmark ruling that training AI on books is fair use under copyright law — which remains the law today,” Anthropic deputy general counsel Aparna Sridhar said.

Follow us on X to get the latest news as it happens

What the Payout Covers

The settlement pays roughly $3,000 per-work payment for over 480,000 works. Martinez-Olguin noted that the sum is four times the $750 minimum for standard copyright infringement.

Claimants covered 440,490 works, or 91.3% of the list, as of April. The deal also requires Anthropic to destroy the pirated book files. The judge rejected objections that the $1.5 billion figure was too low. According to her, the complaints were

“Not grounded in a realistic assessment of the overall risks and rewards of a trial.”

Some authors opted out and continue separate lawsuits against the company. The case is the first major US AI copyright dispute to settle.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Court Signs Off on Record $1.5 Billion Anthropic Copyright Payout appeared first on BeInCrypto.

Celsius co-founders Shlomi Daniel Leon and Hanoch “Nuke” Goldstein will pay a combined $6.5 million to settle Federal Trade Commission charges tied to the collapsed crypto lender.

Summary

- Leon and Goldstein will pay $6.5 million combined under separate FTC settlements over Celsius claims.

- The FTC accused Celsius executives of falsely promoting customer deposits as safe and readily available.

- Mashinsky’s earlier $10 million settlement brings total payments from three Celsius co-founders to $16.5 million.

The FTC said Leon will pay $4.1 million, while Goldstein will pay $2.4 million under separate court orders.

The settlements end the FTC cases against the two executives and follow former Celsius CEO Alex Mashinsky’s $10 million agreement in April. The three co-founders will pay a combined $16.5 million under their respective settlements. The FTC accused them of misleading customers about the safety, availability and management of assets deposited with Celsius.

Leon, Celsius’ former chief strategy officer, must pay $4.1 million under an order entered by U.S. District Judge Denise Cote on June 29. The order also enters a $4.72 billion judgment against him, with most of that amount suspended if he meets the settlement terms and provided accurate financial disclosures to the FTC.

Goldstein, who served as Celsius’ chief technology officer, will pay $2.4 million, according to the FTC’s latest release. Both men also face limits on future business activities. Leon cannot market or sell services used to deposit, exchange, invest or withdraw assets. Goldstein faces a similar ban covering retail crypto products used to buy, sell, deposit, withdraw, distribute or trade digital assets.

The orders also prohibit the two executives from making false statements about products or services. They cannot violate provisions of the Gramm-Leach-Bliley Act by obtaining customer financial information through false or fraudulent representations. Leon also faces restrictions on sharing consumers’ nonpublic personal information without informed consent.

FTC case focused on Celsius safety and reserve claims

The FTC filed its case against Celsius and its executives in July 2023. The regulator alleged that the company presented itself as a safer alternative to traditional banks while making claims about its reserves, lending practices and insurance coverage that were not accurate.

According to the regulator, Celsius told customers they could withdraw deposits at any time and claimed it maintained a $750 million insurance policy covering customer funds. The company also said it held enough reserves to meet customer obligations and did not make unsecured loans. The FTC alleged that Celsius instead made $1.2 billion in unsecured loans by April 2022 and lacked the insurance policy it advertised.

The FTC also accused executives of continuing to reassure customers as Celsius moved closer to bankruptcy. The regulator said they “continued to claim that customers’ deposits were safe days before the company filed for bankruptcy.” Celsius suspended customer withdrawals in June 2022 and filed for bankruptcy the following month.

Mashinsky faces separate bans after $10 million FTC deal

The latest settlements follow the FTC’s April agreement with Mashinsky.The former CEO agreed to pay $10 million and accepted a permanent ban on promoting or offering asset-related products. His order also included a $4.72 billion judgment, although most remains suspended under conditions set by the settlement.

Mashinsky later received another permanent restriction from the Commodity Futures Trading Commission. As crypto.news reported in June, a federal court barred him from trading in markets overseen by the CFTC or registering with the agency. That settlement closed the regulator’s civil enforcement case against him and Celsius.

His criminal case remains separate from the FTC settlements. A federal judge sentenced Mashinsky to 12 years in prison in May 2025 after he pleaded guilty to commodities fraud and securities fraud. Prosecutors said he misled customers about Celsius’ financial condition, investment risks and yield-generating activities. The court also ordered him to forfeit more than $48 million.

Celsius creditors continue recovering funds after the collapse

Celsius held about $25 billion in assets at its peak before its business deteriorated during the 2022 crypto market downturn. When the company stopped withdrawals, hundreds of thousands of customers had about $4.7 billion in inaccessible assets on the platform, according to the U.S. Department of Justice.

The bankruptcy recovery process has continued separately from the cases against former executives. As previously reported, Celsius began a third creditor distribution worth about $220.6 million in August 2025, bringing total recoveries at the time to nearly 65% of eligible claims.

Another former Celsius executive, Roni Cohen-Pavon, also faced legal action over his role at the company. Crypto.news reported in May that he avoided additional prison time after cooperating with prosecutors in the Mashinsky case.

With the Leon and Goldstein orders now entered, the FTC has reached settlements with all three Celsius co-founders named in its 2023 case. The agency’s official case page still lists the broader proceeding as pending, while separate bankruptcy, securities and criminal matters have followed their own legal processes.

White House crypto adviser Patrick Witt will remain in his post after his scheduled military training was deferred, keeping the administration’s lead CLARITY Act negotiator in Washington during the final weeks before the Senate’s summer break.

Summary

- Patrick Witt deferred military training, keeping the White House’s lead CLARITY Act negotiator in place.

- The Senate faces a narrow timeline as unresolved ethics language still threatens the bill’s vote.

- Harry Jung plans to leave government, removing the deputy once expected to cover Witt’s absence.

Witt had planned to begin Judge Advocate General training with the Georgia Army National Guard on July 27.

Witt confirmed the change in a July 20 post on X. He said he remained committed to his military service but added that “my training has been deferred, and that I will be able to see this effort through to the end.” The decision reverses a plan that would have shifted many of his responsibilities to White House Crypto Council deputy director Harry Jung.

Witt stays as the Senate calendar narrows

Witt serves as executive director of the President’s Council of Advisors for Digital Assets and has played a central role in talks involving the White House, lawmakers, banks and crypto companies. As previously reported by crypto.news, he had already postponed the same training in April while CLARITY Act negotiations continued.

The Senate now has little room left on its calendar. Aug. 7 is the final scheduled session day before a state work period begins on Aug. 10. Supporters have treated that window as an important target because election-year politics could make a later vote harder to arrange.

The CLARITY Act would create federal rules for digital asset markets and divide oversight between the Securities and Exchange Commission and Commodity Futures Trading Commission. Senate staff still need to resolve differences before leaders can bring a final version to the floor, where the bill would likely need Democratic support.

Ethics dispute still blocks a final Senate agreement

Witt’s decision to stay does not resolve the policy disputes holding up the bill. Senate negotiators still lack a final agreement over ethics rules that would restrict elected officials from profiting from crypto-related businesses. The White House had not accepted the proposed language as of that report.

Democrats have pushed for tighter limits covering government officials with digital asset interests, while the White House has argued that ethics standards should apply evenly. Senate Majority Leader John Thune has also acknowledged that Republicans still need a bipartisan agreement to move the measure forward.

The uncertainty has affected market expectations. A related crypto.news report said Polymarket traders placed the CLARITY Act’s chance of becoming law in 2026 at 31% on July 20. The figure can change quickly, but it reflected doubts about whether lawmakers could settle the dispute before the August recess.

Consumer protections and stablecoin yield remain in focus

The latest negotiations have also produced changes on customer protections. Coinbase vice chair Ryan VanGrack said Senate Democrats secured stronger safeguards in the revised bill and described the changes as giving the legislation “more teeth.” He did not provide full details, and lawmakers had not released the final Senate text as of July 20.

Other disagreements have centered on stablecoin rewards, decentralized software developers and law enforcement powers. The stablecoin yield debate has drawn strong lobbying from banks and crypto companies. Banking groups have argued that rewards paid on stablecoin balances could pull deposits from traditional banks, while crypto firms have pushed to preserve room for activity-based rewards under a regulated framework.

As previously reported, the Senate Banking Committee cleared a version of the CLARITY Act in May. Witt has worked on several of the unresolved issues, keeping him involved in the administration’s effort to reach a deal with lawmakers from both parties.

Harry Jung’s exit changes the White House staffing plan

Witt’s revised plans come as Harry Jung prepares to leave government service. Jung, the deputy director of the President’s Council of Advisors for Digital Assets, said on July 21 that he would leave his post in two weeks. He had been expected to assume many of Witt’s responsibilities during the planned military leave.

Jung said he was proud of the council’s work and described the past two years as transformative for U.S. crypto policy. His departure means the White House will avoid an immediate leadership gap because Witt is staying. The council is also working on GENIUS Act implementation, the Strategic Bitcoin Reserve and crypto tax policy.

Witt’s continued presence removes one staffing uncertainty, but the legislation still depends on lawmakers resolving ethics provisions, consumer rules and other contested sections. The Senate has not announced a final floor vote, leaving the bill’s path tied to negotiations before lawmakers leave Washington in August.

Ondo Finance, a tokenization platform for real-world assets, said Thursday it has partnered with SBI Group to tokenize Japanese assets, with distribution across SBI's ecosystem and settlement using the group's JPYSC yen stablecoin. "The collaboration covers tokenizing Japanese assets with… Read the full story at The Defiant

New Ryzen 7 7700X3D drops to $279, just days after launch

I Built an AI Financial Operating System for Business #shorts #finance #automation

‘My girl didn’t want to die. My girl wanted to live. But she lived in fear’

-

NewsBeat5 days ago

NewsBeat5 days agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread – Corporette.com

-

Politics3 days ago

Politics3 days agoThe House | The City of London can help the new chancellor deliver growth in every postcode

-

Politics6 days ago

Politics6 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Crypto World5 days ago

Crypto World5 days agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Crypto World4 days ago

Crypto World4 days agoTwo July Windows Left: The CLARITY Act’s Senate Fight and What Failure Means

-

Crypto World3 days ago

Crypto World3 days agoRipple Payments Joins MiCA With 14 Firms, Does It Mean Anything For XRP?

-

Business5 days ago

Business5 days agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Politics2 days ago

Politics2 days agoDemocrats look to World Cup watch parties to register thousands of voters

-

Entertainment6 days ago

Entertainment6 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Crypto World3 days ago

Crypto World3 days agoRipple wins EU-wide access as ESMA adds it to MiCA register

-

Crypto World4 days ago

Crypto World4 days agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Business5 days ago

Business5 days agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

Tech5 hours ago

Tech5 hours agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

Tech3 hours ago

Tech3 hours agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

News Videos6 days ago

News Videos6 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

NewsBeat4 days ago

NewsBeat4 days agoRegistration is now open for March for Men with Kev 2026

-

Tech6 days ago

Tech6 days agoDark Secrets Emerge When Jailbreaking LLMs

-

NewsBeat19 hours ago

NewsBeat19 hours agoUnregistered fitter used Gas Safe logo on business flyers

-

Sports5 days ago

Sports5 days agoNew Cornerback Enters Vikings Trade Rumor Mill

You must be logged in to post a comment Login