Crypto World

Ripple Treasury Becomes First TMS to Offer Native Digital Asset Capabilities for Corporate CFOs

TLDR:

- Ripple Treasury is the first TMS to embed native digital asset capabilities directly into an enterprise platform.

- Digital Asset Accounts support XRP and RLUSD with 15-decimal precision and automated real-time transaction recording.

- Unified Treasury connects multiple custodians via ClearConnect, giving CFOs one real-time dashboard for all positions.

- Ripple’s 2026 survey found 72% of finance leaders say a digital asset solution is now needed to stay competitive.

Ripple Treasury has officially launched Digital Asset Accounts and Unified Treasury. The launch marks the first native digital asset capabilities embedded in an enterprise treasury management system.

CFOs and their teams can now view, hold, and manage both fiat and digital assets in one place. It follows Ripple’s 2025 acquisition of GTreasury, which brought over 40 years of enterprise treasury expertise. Multiple customers completed beta testing ahead of the April 1 global launch.

Digital Asset Accounts Integrate Onchain Balances Into Enterprise Treasury Workflows

Digital Asset Accounts allow treasury teams to create and manage a regulated digital asset account directly within the platform.

No external setup, third-party custody relationship, or separate system is required. XRP and Ripple USD (RLUSD) balances appear alongside cash accounts in real time.

The platform applies live fiat valuation, refreshed within seconds of each transaction. Exchange rates come from leading market data providers and update automatically.

The system also works across multiple data providers simultaneously, maintaining accuracy during volatile market conditions. Teams no longer need manual calculations or separate tools for valuation.

Transactions are recorded with 15-decimal precision, capturing onchain amounts exactly as they exist. This prevents rounding errors that typically cause reconciliation gaps.

An automated audit trail is generated for every transaction, supporting finance and control teams. Treasury managers maintain full control of records without relying on external reconciliation tools.

Each record captures the native notional amount, fiat equivalent, and market price at the moment of the event. This provides a complete, time-stamped transaction history without manual data entry. The automated recording process also supports compliance across multiple reporting frameworks.

Renaat Ver Eecke, SVP of Ripple Treasury, spoke on the shift in how CFOs now approach digital assets. “Digital assets have arrived at the CFO’s desk, and the question has shifted from whether to engage to how to do so advantageously without disrupting existing operations,” he said.

He added that the platform gives the office of the CFO a trusted place to hold and manage digital and fiat assets, with no separate interface or new workflows needed.

Unified Treasury Gives CFOs Real-Time Visibility Across All Liquidity Positions

Unified Treasury consolidates digital asset and cash positions into a single real-time dashboard. Teams holding assets across multiple custodians can connect providers through Ripple Treasury’s ClearConnect connectivity layer.

This layer is the same one already used for existing bank integrations within the platform. No new infrastructure or changes to current banking arrangements are required.

API connectivity to digital asset providers can be completed in minutes through the platform. Once connected, balances reflect automatically as transactions occur onchain.

Treasury teams no longer depend on manual imports or batch data processing to see positions. This also eliminates delays that have made digital asset reporting difficult for corporate finance teams.

Market rates are applied to digital asset balances in the reporting currency of each organization’s choice. No separate data sources or manual currency conversions are required.

The entire process runs automatically within the system, streamlining day-to-day operations. This gives treasury teams in different regions a consistent reporting experience.

Mark Johnson, VP of Global Product at Ripple Treasury, described the core design principle behind both capabilities. “The design principle behind both capabilities is that digital assets should behave exactly like cash within the platform,” he said.

Johnson further noted that treasury teams should not have to think about whether a balance is onchain or in a bank account. “They should simply see their position,” he added.

Ripple’s 2026 survey of 1,000+ global finance leaders found that 72% now consider a digital asset solution a competitive necessity.

Most, however, lack a starting point that fits within current workflows. Stablecoins processed $33 trillion in volume last year, rising 72% from 2024, showing strong demand already in the market.

Former Celsius founder and former chief executive Alex Mashinsky has moved to vacate his 12-year prison sentence in a New York federal court, arguing that he received ineffective counsel and that the conviction rests on tainted evidence. The motion, filed in the Southern District of New York, follows Judge John Koeltl’s May 2025 ruling imposing a 144-month term for commodities fraud and securities fraud tied to the Celsius network’s downfall. Mashinsky filed the paperwork without new representation, after announcing on May 5 that he would proceed pro se.

In his filing, Mashinsky contends that his defense was compromised by ineffective assistance of counsel and that the evidence underpinning his guilty pleas was tainted by a “fruit of the poisonous tree” scenario—a legal doctrine referring to evidence obtained through misconduct. He also noted that his counsel ceased communication with him at a critical juncture, forcing him to submit his reply directly to the court without new guidance.

Beyond the legal procedural questions, Mashinsky’s motion reiterates claims about the broader forces he believes influenced Celsius’s fate. He asserts that former FTX chief executive Sam Bankman-Fried intended to destroy Celsius and that the market manipulation surrounding Celsius’s CEL token on the FTX exchange was a central factor in the crisis. In support of his position, Mashinsky attached messages with Celsius’s former chief revenue officer, Roni Cohen-Pavon, alleging a “hostile takeover” attempt at the platform.

Celsis filed for bankruptcy in 2022 after a period of distress across the crypto sector, a year that saw a wave of exchange failures. In July 2023, U.S. authorities charged Mashinsky and Cohen-Pavon with fraud and market manipulation related to Celsius’s operations; both executives later pleaded guilty. The legal actions against them formed a broader narrative of accountability in a sector that had been rocked by collapses and restructuring.

In a separate piece of the Celsius saga, Cohen-Pavon was sentenced to time served after pleading guilty in September 2023. Prosecutors cited her “substantial assistance” to the government, including willingness to testify against Mashinsky, as a key factor in the sentence and in concluding the criminal case against the Celsius executives.

Key takeaways

- Alice Mashinsky seeks to vacate his 12-year sentence in SDNY, arguing ineffective assistance of counsel and tainted evidence as grounds for relief.

- The motion arrives in the wake of Mashinsky’s May 2025 sentencing and follows a 2022 Celsius bankruptcy and 2023 indictments of Celsius executives.

- Mashinsky alleges that Sam Bankman-Fried sought to destroy Celsius and points to internal communications suggesting a hostile takeover attempt at Celsius.

- Cohen-Pavon was sentenced to time served after pleading guilty; prosecutors highlighted substantial cooperation, with penalties including more than $1 million in fines and a $40,000 fine.

- Financial consequences for Mashinsky include a $48 million forfeiture from a criminal case and a separate $10 million FTC settlement tied to a multibillion-dollar Celsius judgment, most of which is suspended.

Legal tides around a fallen platform

The Celsius case sits at the intersection of criminal accountability and corporate collapse in a market still grappling with the aftershocks of the 2022 downturn. The move to vacate hinges on nuanced questions about representation and the admissibility of evidence, but it also underscores continuing scrutiny of how individuals and teams behind high-profile crypto platforms are held to legal standards. Mashinsky’s pro se stance adds a layer of procedural complexity, potentially prolonging a series of court filings that have already stretched across years.

From a regulatory perspective, the saga—spanning bankruptcy, indictments, guilty pleas, and settlements—illustrates the breadth of federal interest in the sector’s actors, not just the exchanges themselves. The case also intersects with the broader narrative of post-FTX accountability, where prosecutors have pursued multiple fronts to address alleged deception and market manipulation in the crypto economy.

The financial penalties connected to Celsius’s leadership also illustrate the penalties that can accompany wrongdoing in this space. Mashinsky’s $48 million forfeiture and the $10 million FTC settlement linked to Celsius’s broader judgment reflect the dimensions of civil and criminal consequences that can persist long after a platform’s immediate collapse. Cohen-Pavon’s time-served sentence, alongside more than $1 million in penalties, reinforces that executives may face significant costs even when criminal convictions are resolved.

What investors and crypto builders should watch next

For creditors, investors, and users connected to Celsius assets, the ongoing legal proceedings add a layer of uncertainty to an already unsettled chapter in the company’s history. The pending motion to vacate could, if granted, alter aspects of the sentencing posture and the potential financial exposure linked to the case. Even if the motion does not succeed, the process highlights the persistent risk of legal and reputational disruption surrounding failed platforms and their leadership.

Looking ahead, observers will be watching for a decision on Mashinsky’s vacatur bid, which could influence related sentencing or forfeiture orders. The proceedings also sit within a larger regulatory frame—where authorities are increasingly focused on executive accountability in the wake of major market disruptions. As the Celsius matter continues to unfold, market participants should monitor any formal court rulings, potential settlements, and how these developments might impact remaining creditors, unsecured claims, and the broader narrative around crypto lending platforms’ risk management and governance standards.

Readers should stay attentive to forthcoming court filings and rulings, as they will signal whether the motion to vacate moves forward or stalls. The case remains a key datapoint in understanding how the legal system handles complex criminal and civil actions tied to high-profile crypto platform failures—and what that means for the trajectory of crypto accountability in the years ahead.

Coinbase CEO Brian Armstrong replied to JPMorgan chief Jamie Dimon’s broadside on the CLARITY Act with a hockey-themed meme that drew swift backing from across the crypto industry.

The viral exchange on Friday turned a regulatory fight over stablecoin rewards into a rallying moment for digital asset leaders pushing the bill to the Senate floor.

Crypto Industry Closes Ranks Behind CLARITY Act

Industry leaders pushed back fast after Dimon’s CLARITY Act broadside on Fox Business Friday. Mike Novogratz of Galaxy Digital argued elected lawmakers, not banks, should write financial laws.

Peter Van Valkenburgh of Coin Center pointed out that roughly $3 trillion was laundered through banks in 2025. He called Dimon’s anti-money-laundering framing nonsense.

“The second issue is not really related to rewards and interest on stablecoins. It’s also about AML, BSA, KYC. Because when you are in a bank system, it’s already been through all that. We do that. We have to [do it] for the federal government. So if they want to be moving money around… on any basis, you should have to question: ‘Can that be used illegitimately?’ Answer: Yes, unless they’re following the same rules,” Dimon had said in the interview.

Other crypto voices cited JPMorgan’s track record of regulatory fines and settlements totaling tens of billions.

The defense came with the Digital Asset Market Clarity Act before the full Senate. It cleared the Senate Banking Committee in a 15-9 vote on May 14.

The bill needs 60 votes on the Senate floor before returning to the House.

Armstrong’s Meme Becomes the Rally Cry

Armstrong’s poster cast Dimon as #2 for tradition and himself as #1 for economic freedom. The image went viral within minutes.

“Heated Rivalry” is also the title of a 2019 gay hockey romance novel adapted for television in late 2025.

The meme amplified the industry’s underlying argument. Bank opposition to stablecoin yield rewards looks like incumbent protectionism, not consumer protection.

Amid the escalating feud, Coinbase now compares to Charles Schwab’s late-1970s disruption of brokerage commissions. The comparison resonates with crypto traders who see Coinbase eroding traditional bank margins.

“Coinbase is to current finance/banking what Charles Schwab was to finance/trading in the late 70’s and 80’s. Schwab radically disrupted Wall Street then. Coinbase is radically disrupting Wall Street now. Schwab ultimately destroyed commissions and fees on transactions. Coinbase is destroying market hours, access, tech, and margins/interest,” remarked Andrew, co-founder of Arch Public.

Industry figures argue the existing framework already imposes Bank Secrecy Act rules on exchanges.

The pushback signals a coordinated response to months of bank lobbying. The Senate floor vote is expected in June.

The post Coinbase vs. JPMorgan Feud Escalates Over the CLARITY Act appeared first on BeInCrypto.

The United States has seized roughly $1 billion in Iranian cryptocurrency assets, Treasury Secretary Scott Bessent announced at the Reagan National Economic Forum. He characterized the action as a direct disruption of illicit financial activity, describing it as an outright grab of wallets that some owners may not yet realize have been emptied. The disclosure situates the seizures within a multiyear effort to constrain Iran’s access to international financial networks and to press its leadership economically.

Bessent said the seizures are part of a broader pressure campaign against Iran, known as Operation Economic Fury. Launched in March 2025, the operation combines cryptocurrency takedowns, banking account freezes, and coordinated asset confiscation with European partners. He framed the effort as a sustained, comprehensive push designed to “cut them off” financially, noting that the trajectory over the past five-and-a-half to six weeks has been remarkably effective. “Between five and a half to six weeks of an incredibly successful military campaign and Operation Economic Fury, where we have really cut them off. They are at the end of their Tether now financially,” he stated.

Key takeaways

- The United States reports roughly $1 billion in Iranian crypto assets seized through Operation Economic Fury, including wallet-level takedowns.

- The newly disclosed figure is about twice the $500 million previously announced in late April and well above the $344 million disclosed earlier in the month.

- Officials describe Iran’s financial situation as dire, with high inflation, internal funding pressures, and disruptions to state services and military payrolls.

- The seizures illustrate intensified cross-border enforcement and international cooperation, with implications for crypto compliance, sanctions screening, and banking access for sanctioned states.

- Policy conversations around crypto-enabled shipping and revenue mechanisms—such as Bitcoin-based incentives for Hormuz transit—signal broader state-influenced use cases for digital assets, pending regulatory scrutiny.

Asset seizures: scale, method, and regulatory context

According to officials, the $1 billion in Iranian crypto assets seized under Operation Economic Fury represents a significant escalation in exploiting blockchain-traceable funds linked to sanctioned activity. The strategy appears to rely on identifying wallets associated with state-backed or proxy actors, then applying enforcement measures that repurpose or redirect the assets through compliant channels. The approach also reflects the United States’ broader sanctions toolkit, which increasingly treats certain digital assets as subject to traditional financial and export-control regimes.

The Treasury’s disclosures underscore a shift in how authorities frame enforcement risk for crypto-asset holders connected to sanctioned regimes. By publicly detailing wallet-level seizures and the scale of the assets involved, policymakers and regulated institutions gain a clearer baseline for due diligence, screening, and ongoing monitoring. For exchanges, custodians, and banks with crypto-related business lines, the development raises questions about the diligence required to identify sanctioned wallets, the treatment of seized or frozen crypto, and the timing of any redress or remediation for affected customers.

The previously reported figures provide context for the current disclosure. Officials had announced roughly $500 million in Iranian crypto assets seized in late April and about $344 million in crypto assets seized earlier in the month. The latest figure, therefore, suggests a substantial acceleration in enforcement activity within a relatively short window. These milestones have implications for cross-border regulatory coordination, including parallel actions by allied regulators and law enforcement partners in Europe and beyond. For market observers, the trend highlights the growing intersection of sanctions policy with digital-asset compliance requirements and the need for rigorous KYC/AML controls across custody and exchange ecosystems.

Iran’s economic strain and the geopolitical backdrop

Secretary Bessent painted a picture of severe economic strain within Iran, describing a regime that has allegedly siphoned hundreds of millions of dollars monthly and allocated proceeds among a broad leadership cadre. He suggested inflation could exceed 200 percent, with social subsidies being deployed to mitigate cost-of-living pressures and widespread internet restrictions affecting communications. Reports cited by officials indicate that a substantial portion of Iranian troops have faced delayed or disrupted pay, further complicating the regime’s capacity to project authority and sustain external influence flows.

The statements also reflect the strategic complexity of negotiating with a fractured leadership structure following recent strikes against senior regime figures. While Bessent did not hinge policy outcomes on these internal dynamics alone, the comments underscore how enforcement actions intersect with diplomatic channels, sanctions policy, and potential leverage in any future negotiations surrounding Tehran’s regional posture and long-term security considerations.

These disclosures come at a moment when the U.S. and its allies continue to calibrate sanctions pressure against Iran, balancing the aims of disrupting illicit financial networks with broader regional stability goals. The clearly articulated message is that crypto assets are not beyond the reach of conventional sanctions enforcement, and that dynamic, rapid actions can be employed to disrupt stated objectives even when actors pivot to digital instruments. For compliance teams and risk managers at financial institutions, the implications are twofold: a heightened emphasis on tracing cross-border crypto flows and an expanded mandate to screen counterparties against sanctioned-entity lists in near real time.

Policy implications and regulatory coordination

Beyond the immediate asset seizures, observers are examining the regulatory and policy ramifications for the crypto industry. The operation demonstrates a continued hard line on sanction enforcement, potentially accelerating the development of best practices around sanctions screening, wallet clustering analysis, and the cross-jurisdictional sharing of intelligence related to illicit fund flows. Firms engaged in custody, exchange, or payment processing face heightened expectations to implement robust monitoring, rapid response protocols, and transparent reporting mechanisms when dealing with funds that may be implicated by sanctions regimes.

In parallel, the focus on state-led crypto strategies—such as potential monetization schemes tied to strategic chokepoints—highlights the need for clear regulatory guardrails around crypto-based insurance, settlement, and revenue-sharing models used by states. As reported by Cointelegraph, Iran has been weighing a Bitcoin-based insurance framework to monetize shipping through the Strait of Hormuz, a project that could generate substantial revenue if implemented at scale and supported by compliant, auditable mechanisms. The proposed platform, termed “Hormuz Safe,” would sell digital marine insurance payable in Bitcoin and settled on the blockchain, potentially enabling more than $10 billion in revenue for the country, subject to regulatory approval and international compliance constraints. A separate report cited that some ships could pass Hormuz in exchange for a Bitcoin-denominated tariff of about $1 per barrel of oil. The development underscores the convergence of sovereign financing strategies and digital asset infrastructure, inviting scrutiny from licensing authorities and international financial regulators alike.

For regulated entities, the evolving environment implies a need for heightened vigilance around sanctioned counterparties, as well as clearer guidance from regulators on the permissibility and treatment of crypto assets tied to state operations. The cross-border dimension—where U.S. actions, European cooperation, and potentially other jurisdictions intersect—will likely shape licensing decisions, oversight practices, and the rigor of AML/KYC programs across the global crypto ecosystem. In this context, ongoing updates from U.S. agencies and international partners will be critical reference points for risk managers, legal counsel, and compliance leaders assessing exposure to sanctioned activities or users with ties to Iran or other restricted regimes.

Closing perspective

The scale of the recent seizures, coupled with Iran’s stated economic and strategic pressures, signals a pronounced trend: cryptocurrency is increasingly entangled with state-level sanctions enforcement and foreign policy aims. As authorities pursue more aggressive asset recovery and cross-border cooperation, firms across the crypto value chain must strengthen their compliance programs, enhance real-time monitoring, and prepare for evolving guidance on sanctioned assets and state-backed financial activities. The coming months will likely reveal further operational details and regulatory responses that define how digital assets interface with traditional sovereignty and enforcement mechanisms.

For further context, authorities and industry observers continue to monitor related developments, including prior disclosures and coverage of Iran-related crypto actions. In particular, Cointelegraph has reported on related seizures and policy discussions, illustrating the ongoing convergence of sanctions policy, crypto regulation, and geopolitical risk management.

The cryptocurrency market has steadied somewhat over the past 24 hours, following a painful correction that pushed Bitcoin and most large-cap altcoins lower during the week.

However, Stellar (XLM) continues to be the clear outlier from the top alts, posting yet another massive daily surge while the broader market remains under pressure.

BTC Price Calms Above $73K

Bitcoin’s most recent weekly correction took the asset south when it slipped below $73,000 amid renewed pressure across crypto markets. The primary cryptocurrency has recovered since then and gained some ground, now trading at $73,400.

Its intraday moves have not been without volatility, however. The price ranged between $72,200 and $74,200 before finally settling down at the current levels as the weekend starts.

Bitcoin’s market capitalization remains above $1.47 billion, while its dominance over altcoins is more or less unchanged, suggesting they failed to capitalize on BTC’s weakness. The latter could have been induced by weakening ETF flows, which have posted record outflows in the past few days.

For now, the $73,000 zone has become the key area to watch. A decisive loss of that level could trigger another leg lower, potentially to $70,000, while a move above $74K may ease some of the short-term pressure.

Stellar (XLM) Continues to Lead the Altcoin Market

The altcoin market shows a mixed picture today, with most large-cap assets posting relatively modest moves over the past 24 hours rather than sharp recoveries.

Ethereum (ETH) is trading close to $2,000, while SOL, XRP, and several other majors are showing only limited changes. BNB has fared the best from the top alts, rising by more than 5% on the day.

XRP is also slightly in the green, while ETH and SOL remain almost flat compared to their levels from 24 hours.

Stellar (XLM), however, is in a completely different category. The altcoin has exploded by roughly 25% over the past day and is trading near $0.20, making it one of the strongest performers among mid-cap cryptocurrencies.

The move comes shortly after DTCC announced that its tokenization service will connect with the Stellar public blockchain. The move is expected to support tokenized DTC-custodied assets, including stocks, ETFs, treasuries, and corporate bonds, with availability targeted for the first half of 2027.

Other notable performers for the day include LAB, up 37.5%; Algorand’s ALGO, up 9.5%; and XDC Network (XDC), up 9%.

The post Bitcoin Calms at $73,000, Stellar Explodes by 25% Daily: Weekend Watch appeared first on CryptoPotato.

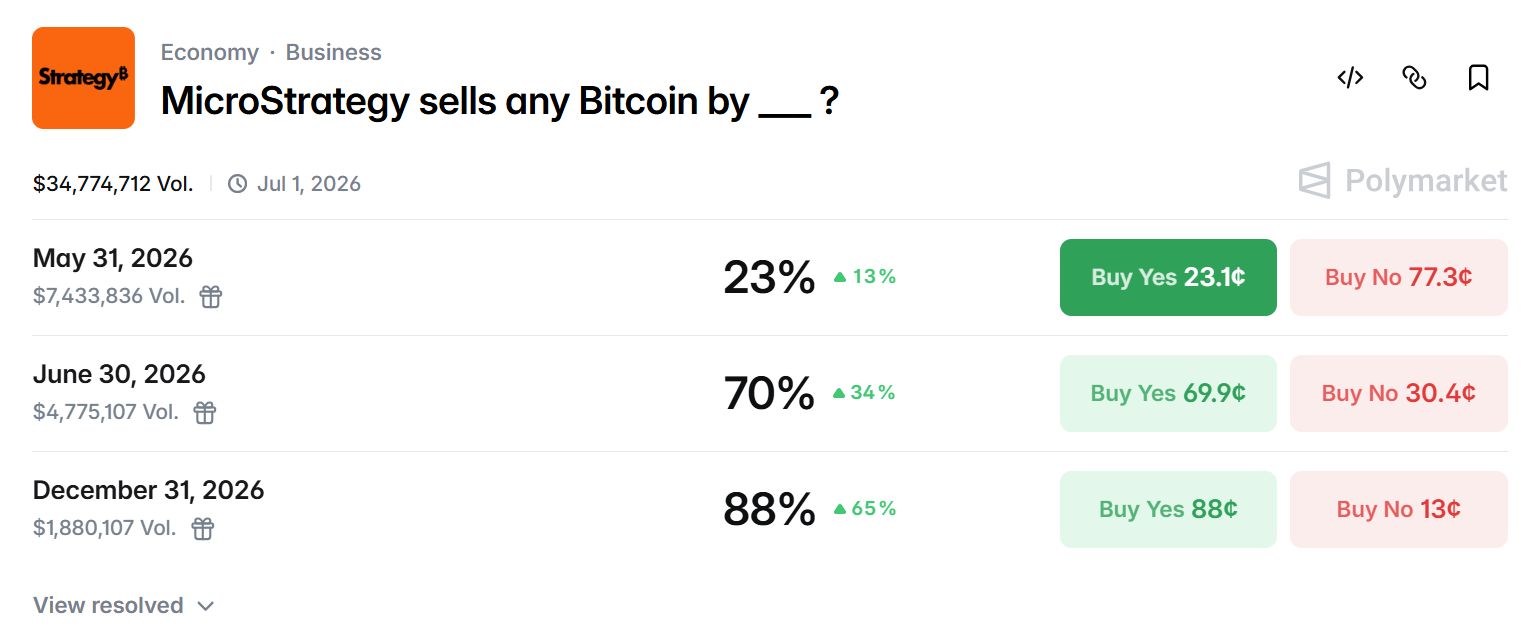

MicroStrategy, the largest corporate Bitcoin (BTC) holder, withdrew 411.5 BTC from Coinbase Prime hours after depositing it. The reversal cooled fears that Michael Saylor’s firm was preparing its first BTC sale in years.

Meanwhile, Tom Lee’s BitMine Immersion Technologies bought 25,000 Ethereum (ETH) for $50.6 million on the same day. The purchase extended one of the largest corporate ETH accumulation programs in markets.

MicroStrategy Reverses Brief Coinbase Prime Deposit

On-chain trackers flagged the initial deposit as MicroStrategy’s first direct exchange move in nearly two years.

The transfer was split into two batches near 205 BTC each, with smaller wallet transactions also active.

Saylor signaled this week that Strategy could sell some BTC before year-end, citing dividend and capital needs. The remark had shifted prediction-market pricing even before the Coinbase Prime move.

The deposit pushed Polymarket odds on Strategy selling any Bitcoin in 2026 above 90%. Those odds eased after the withdrawal but stayed elevated.

“Did Michael Saylor’s Strategy cancel its BTC sale? Strategy withdrew 411.5 BTC ($30.2M) back from Coinbase Prime 5 hours ago,” Lookonchain posed.

Follow us on X to get the latest news as it happens

BTC trades near $73,532, with the broader Bitcoin treasury stocks split showing limited contagion.

Strategy still holds 843,738 BTC, valued above $62 billion. The firm has bought no Bitcoin since May 18. That pause is the longest in its weekly accumulation as corporate Bitcoin treasury demand softens.

BitMine Doubles Down on Ethereum Amid Price Weakness

BitMine bought the dip below $2,100, lifting its aggressive ETH accumulation to roughly 5.39 million ETH. That sum represents about 4.47% of supply, near Tom Lee’s 5% target for the year.

“Tom Lee’s Bitmine bought another 25,000 ETH ($50.56M) 6 hours ago,” Lookonchain noted.

The firm stakes more than 4.7 million ETH through its Made in America Validator network. The position generates an annualized yield of about $276 million. Ether trades near $2,011 after a 10% monthly decline.

Lee frames the weakness as a buying window, pointing to tokenization growth and AI demand for compute.

Backers including ARK Invest and Founders Fund maintain exposure. BMNR trades below net asset value despite unrealized BitMine ETH losses.

However, even as Tom Lee’s Bitmine buys the Ethereum dip, old wallets are dumping, with one selling $112 million worth of ETH in the last week.

“Ethereum OG is dumping ETH! Over the past week, an Ethereum OG sold 55,000 ETH ($112.25M) and 9,442 wstETH ($24M) at an average price of $2,041 per ETH,” the on-chain analytics account highlighted.

The post MicroStrategy Corrects Bitcoin Sell-Off Fears With $30 Million Withdrawal appeared first on BeInCrypto.

Hyperliquid is best known for its on-chain perps exchange, but did you also know there are vaults where users can deposit funds and follow specific trading strategies?

One of these vaults, currently enjoying a total value locked of more than $3 million, delivered 638% APY last month. Let’s examine.

What Are Hyperliquid Vaults?

Hyperliquid vaults are one of the more closely watched features on the decentralized derivatives exchange. They allow traders to participate in shared strategies.

Think about it this way – a vault works more like a pooled trading account. A vault leader runs a strategy, while other users can deposit funds into the vault and gain exposure to the results.

If the strategy makes money, depositors would share in the profits. If it loses money, they also share in the losses.

What makes vaults interesting is that, unlike a basic yield product that simply lends or rebalances assets, they are built directly into HyperCore. This means that vault strategies can tap into existing infrastructure available to traders on the exchange, including leverage, liquidations, perps, high-throughput execution, and everything Hyperliquid provides.

This can make them powerful instruments for those seeking more passive avenues, but they can also be risky. Returns can move very sharply in both directions, especially when vaults use leverage or take concentrated directional bets.

An interesting way to think about it is to equate it to on-chain copy trading with pooled capital. The strategy is fully visible, performance can be tracked, and users can choose whether the risk profile is fit for their own portfolio.

Long HYPE and BTC, Short “Garbage” Yields 638% APY Past Month

One particular vault built on Hyperliquid has drawn attention after returning an APY of 638% over the past month.

It’s named “Long HYPE & BTC, Short Garbage,” and it currently manages around $3.03 million in total value locked.

Its strategy is designed to be 70% HYPE and 30% BTC on the long side. It also maintains shorts in a basket of at least 10 high-FDV and high-emission coins, with the short side representing about 60% of notional exposure.

As you can see from the position table, the only underperforming trade is the BTC long, though it has been offset by the funding payout.

The vault’s overall PnL chart shows a steep rise over the prior 30 days, nearing the $1.2 million area.

Of course, this shouldn’t be interpreted as a low-risk yield. On the contrary, it reflects a rather aggressive leveraged long-short crypto trade, which depends heavily on HYPE’s price performance.

The post This Crypto Trade Printed 638% APY Last Month: Details appeared first on CryptoPotato.

The past seven days saw Pi Network’s native cryptocurrency move more or less in line with the rest of the market, declining by a total of 4.7%.

A few important project-oriented developments also took place, so let’s have a look at some of the more important news around the project.

Important Protocol Update for Pi Network

Undoubtedly, the main development story for the past few days centered on an important protocol upgrade for mainnet node operators. As CryptoPotato reported, all Pi mainnet nodes are required to move to version v24. The deadline is set for June 2nd, 2026.

The team described the update as very quick to complete, with downtime expected of about 15 minutes. However, the warning around it is significant, because nodes that fail to update risk being disconnected from the canonical chain.

That could create instability if enough operators delay the process. Developers have also advised operators not to upgrade all nodes at once, instead routing traffic through other nodes during the transition.

For Pi Network, the move comes at an important stage, because the project continues to focus on infrastructure and utility, while the market continues to watch for signs of technical progress that can translate into more confidence in the native token Pi.

CiDi Games Beta Draws Engagement

The second major update is coming from the ecosystem side of things. CiDi Games – a Pi Network Ventures portfolio company – launched its beta application within the Pi Browser. The move is supposed to bring Pioneers 10 instant-access games across puzzle, idle, action, and competitive categories.

The move also introduced skill-based tournaments, platform progression through CiDiScore, the Pi ELF companion experience, and more.

The early traction was notable. In less than a week, CiDi Games attracted more than 81,000 Pioneers across more than 160 countries and regions, generating over 1.2 million game sessions. The launch also showed that Pi-based applications can reach users organically, build engagement, and test monetization through real utility rather than speculation.

CiDi Games, a Pi Network Ventures portfolio company, launched their beta app in the Pi Browser!

This brought Pioneers 10 instant-access games along with skill-based tournaments, platform progression through CiDiScore, the Pi ELF companion experience, Elf Continent, and developer… pic.twitter.com/7iqdZxUoIb

— Pi Network (@PiCoreTeam) May 28, 2026

Pi Price Remains Under Pressure

Despite the notable ecosystem updates, PI’s market performance remained depressed today. At the time of this writing, the token is trading at around $0.143, down about 4.7% over the past week, with a market capitalization of nearly $1.53 billion and daily trading volume of around $8.7 million – a far cry from its former days of massive activity.

The cryptocurrency continues to reflect broader caution observed in altcoins this week, with traders weighing technical progress against weaker market momentum.

As it stands, PI’s price action suggests that investors are not easily swayed by announcements.

The post Pi Network News and PI Price Update May 30 appeared first on CryptoPotato.

Retail investors remain central to Bitcoin’s demand dynamics, even as institutional players deepen exposure through regulated products. In a Cointelegraph interview conducted at BitcoinVegas 2026 and published to YouTube, Swan Bitcoin CEO Cory Klippsten argued that the market’s backbone is still retail-driven, not solely controlled by the big players.

“It’s not like BlackRock owns the Bitcoin and Fidelity owns the Bitcoin. It’s a bunch of retail accounts mostly that actually buy that,” Klippsten said during the conversation, underscoring that real on-chain demand underpins price movements even when ETFs and wrappers provide access. He noted that even buyers via institutional wrappers still have to take real supply and custody it, which implies the demand is genuine and exits supply as bitcoins move from sellers to holders.

Data points surrounding the evolving ETF landscape add nuance to the story. US-based spot Bitcoin ETFs have posted a combined $2.90 billion in net outflows since May 15, according to Farside data, while Bitcoin has fallen about 9.5% over the same period. At the time of publication, Bitcoin was trading around $73,630 per CoinMarketCap. The broader market has also cooled: Bitcoin has declined about 2.87% over the past 30 days, per CoinMarketCap. Amid this backdrop, market sentiment remains fragile, with the Crypto Fear & Greed Index oscillating toward the lower end of the spectrum and signaling cautious positioning among investors.

Klippsten’s reflections on the year intersect with a cautious mood among traders. The interview took place against a backdrop of ongoing volatility in 2026, and the outlook for a fresh Bitcoin all-time high has grown more conservative since Bitcoin traded near $95,000 earlier in the year. He estimated a roughly 50% chance of a new high at that time, but as the price slipped and traded in the 70s, he adjusted the odds downward to about 20–25% for a new high within 2026.

Key takeaways

- Retail demand remains a primary driver of Bitcoin markets, even as institutional products gain traction.

- US spot Bitcoin ETFs have posted about $2.90 billion in net outflows since May 15, according to Farside data, while BTC has fallen roughly 9.5% over the same period.

- Bitcoin’s price hovered near $73,630 at the time of reporting, with a ~2.87% 30-day decline on CoinMarketCap data.

- The Crypto Fear & Greed Index sat in “Extreme Fear” territory, reflecting a cautious market mood in 2026.

- Klippsten’s revised view for 2026 places the odds of a new Bitcoin all-time high at around 20–25%, down from earlier expectations near 50% when prices were higher.

Retail demand vs. ETF access: a persistent tension

The Swan Bitcoin chief framed the narrative as a tension between accessible fiat wrappers and the underlying on-chain reality. While ETFs and futures provide entry points for a broader audience, the actual flow of coins—withdrawn, held, and controlled by investors—drives real supply dynamics. That distinction, he argued, matters for how investors should assess risk and opportunity in a market that remains closely tied to on-chain realities rather than purely paper products.

In this framing, the accessibility of Bitcoin through traditional financial products coexists with the necessity for custody and settlement that characterizes on-chain activity. The result is a market in which paper constructs can widen participation but cannot replace the fundamental mechanics of supply and demand that move Bitcoin’s price.

ETF flows, price action, and the mood of 2026

Farside’s data showing $2.90 billion in net outflows from US spot Bitcoin ETFs since mid-May highlights a critical headwind for ETF-driven narratives. Yet price action suggests a more nuanced picture: BTC has fallen roughly 9.5% over the same window, even as retail and non-traditional buyers continue to transact on-chain. The current price around $73,630 contrasts with the year’s earlier peaks, underscoring the danger of extrapolating from episodic inflows or outflows alone.

Market sentiment has reflected the scramble for direction. The Crypto Fear & Greed Index, a sentiment gauge tracking whether investors are cautiously pessimistic or aggressively optimistic, registered in the Extreme Fear zone on the latest reading, signaling a period of conservative positioning and heightened risk aversion among participants.

Outlook for 2026: a tempered trajectory for a new high

Looking ahead, Klippsten’s view on Bitcoin’s potential to make a new all-time high in 2026 leans toward caution. After seeing Bitcoin retreat from roughly $95,000 earlier in the year, the odds of a fresh high have narrowed. He estimated a roughly 20–25% chance of hitting a new peak within the year, down from a more sanguine 50% when prices were higher. The evolution of ETF flows, macro risk signals, and on-chain metrics will be critical to watch as the year unfolds.

These dynamics come as investors weigh the relative strength of on-chain demand against the noise of regulated access products and evolving market structure. The conversation around retail participation, custody realism, and the path to mass adoption remains central to how market participants interpret price action and risk in the months ahead.

What to watch next

As 2026 progresses, readers should monitor several developments to gauge the balance between on-chain demand and institutional access: incoming and outgoing flows in spot Bitcoin ETFs, shifts in on-chain transaction activity and custody patterns, and quarterly updates on investor sentiment as new data arrives. The ongoing debate over the role of regulated wrappers versus pure on-chain demand will continue to shape how traders position for potential volatility and how builders design services that align with real supply and demand dynamics.

In the near term, attention will likely center on ETF-related activity, price catalysts around macro headlines, and evolving retail participation. Whether retail demand can sustain constructive pressure on supply will be a key variable for readers watching Bitcoin’s longer-term trajectory into the second half of 2026.

The S&P 500’s longest weekly winning streak since 2023 and Brent crude settling near $92 on U.S.-Iran ceasefire hopes have failed to pull bitcoin and ether (ETH) higher, with the two largest cryptocurrencies finishing the week down nearly 3% as cooling spot bitcoin ETF inflows reinforced the pullback.

The S&P 500 posted its ninth consecutive weekly gain on Friday, the longest such run since 2023 and a streak matched only a handful of times in the past four decades, putting the index up almost 20% from its March lows.

Brent crude settled around $92 a barrel and Treasuries climbed on the week, trimming some of their war-driven losses.

The macro tailwind has come on hopes the U.S. and Iran will sign off on a 60-day ceasefire extension. President Donald Trump said Friday he was ready to make a “final determination” on a preliminary agreement but restated his demand that any deal require Iran to abandon its nuclear program, surrender its enriched uranium and open the Strait of Hormuz.

Crypto did not move with the tape. Bitcoin slipped 2.6% over the past seven days to $73,445, ether 2.5% to $2,011, solana (SOL) 2.2% to $82.42 and TRON’s TRX 5.6%, its worst weekly drop in the top 10, according to CoinDesk data.

finished roughly flat. The slide came alongside softer spot bitcoin ETF inflows, which was flagged this week as adding to the downward pressure even as macro conditions improved.

The exception was the smaller side of the leaderboard. Hyperliquid’s HYPE token ripped 19.4% on the week to $65 as sentiment for the asset continues to grow. Intercontinental Exchange chief Jeffrey Sprecher praised the decentralized perpetuals venue at a Bernstein conference and calling it “bigger than NASDAQ.” BNB closed up 1.9% and XRP eked out a 0.7% weekly gain.

The Iran deal still needs Trump’s signature, and the red lines he restated on Friday sit well beyond what Iran has indicated it would accept publicly. The macro rally is one bad headline from reversing.

Crypto World

Bitcoin’s biggest quantum risk may not be wallet keys. An early investor fears something bigger

A venture capitalist who has spent a decade backing deep-tech and quantum hardware startups says the bitcoin industry is fixated on the wrong half of the quantum problem, the wallet keys instead of the encrypted messages already moving between exchanges, bridges and custodians today.

“The financial system’s most dangerous vulnerability isn’t stored data, it’s the data

moving between institutions right now,” Andrew Gault, CEO of networking firm ZeroTier, told CoinDesk in a recent chat.

“Every interbank message, every payment authentication record, and every digital signature traveling across a network today is being collected by sophisticated adversaries who don’t need to read it yet,” he noted.

“CISOs and security teams have been trained to protect data at rest. What nobody wants to say out loud is that the adversary’s strategy has changed. They’re patient, they have storage, and they’re building a library of today’s encrypted traffic to decrypt the moment quantum capability crosses the threshold,” he added.

Gault is CEO of networking firm ZeroTier and a founding partner of 7percent Ventures, a London- and San Francisco-based deep-tech firm whose portfolio includes British quantum-computing startup Universal Quantum.

The Google Quantum AI research that rattled bitcoin in March showed a sufficiently powerful quantum computer could derive a bitcoin private key from an exposed public key in about nine minutes, came from outside his portfolio.

The conversation since that paper has centered on the roughly 6.9 million BTC sitting in addresses with exposed public keys and Bitcoin’s missing post-quantum migration plan.

But Gault says the more urgent exposure is the data already being collected off the open internet for decryption later, regardless of whether a working quantum computer exists yet.

Google’s own security engineers have moved the same direction. In a March post, the company set 2029 as its target for completing a post-quantum cryptography migration, citing progress on quantum hardware, error correction and factoring resource estimates.

The post, written by Google vice president of security engineering Heather Adkins and senior cryptography engineer Sophie Schmieg, said the company has reprioritized its internal threat model to focus on authentication services and digital signatures, the same wire-level signing infrastructure Gault has been pointing at.

“The threat to encryption is relevant today with store-now-decrypt-later attacks,” the post said.

The strategy driving that urgency is known in cryptography circles as “harvest now, decrypt later.” It assumes adversaries don’t need to read encrypted traffic today, only store it cheaply until a sufficiently powerful quantum computer arrives.

Citi modeled the bank-system version of the scenario in February, estimating a quantum-enabled attack on a single top-five U.S. bank’s access to the Fedwire Funds Service payment system could trigger a $2 trillion to $3.3 trillion cascade across the U.S. economy, equal to a 10% to 17% decline in real GDP.

The Global Risk Institute, cited in the same Citi report, puts the probability of a cryptographically relevant quantum computer arriving by 2034 at between 19% and 34%.

For crypto, the wire-level surface is broader than the wallet one. Cross-chain bridge proofs, exchange API authentication packets, signed transactions broadcast and archived in public mempools, and the back-channel signing traffic between cold storage and trading desks all sit on the same vulnerability spectrum as the bank-grade encryption Citi was modeling.

CoinShares argued in a February report that the wallet-key fear is overstated, estimating only about 10,200 BTC are concentrated enough to move markets if stolen.

Gault’s worry is a different one. “The particularly uncomfortable reality for financial institutions is that the authentication records being harvested aren’t just sensitive,” he said. “It’s the proof layer that determines who owns what, who authorized which transaction, and who bears legal liability.”

Ethereum (ETH) has launched a coordinated post-quantum migration, but Bitcoin has not done the same. Major crypto exchanges and custodians, where most of the signing traffic lives, have not publicly committed to one either.

Why Closed Financial Networks Always Lose

Balloon-sucking yobs thundering through the streets of south Manchester were told to ‘go home’ before horror crash claimed innocent man’s life

11 equity mutual funds offer over 10% in May. Have you invested in any for your portfolio?

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

US brings back mandatory military draft registration

Register Renaming | Hackaday

Why Closed Financial Networks Always Lose

The Biggest Financial Mistake Indians Make | Dr. B. Bhaskar Rao | Raj Shamani’s podcast

Billete de dos mil ya es coleccionable! #billetes #billetesvaliosos #coleccion #money #curiosidades

-

Business6 days ago

Business6 days agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

NewsBeat3 days ago

NewsBeat3 days agoIsrael says it has killed new Hamas military leader in Gaza City airstrikes

-

Politics5 days ago

Politics5 days agoBridgerton Season 5: Cast, Release Date And Everything We Know So Far

-

Business3 days ago

Business3 days agoSelena Gomez Reportedly Upset Over Benny Blanco’s Comments on Her ‘Terrible’ Diet

-

Crypto World7 days ago

Crypto World7 days agoRobinhood crypto COO Tanya Denisova exits

-

Crypto World3 days ago

Micron Crosses $1 Trillion Market Cap as AI Demand Reshapes Memory Sector

-

Tech5 days ago

Tech5 days agoMicrosoft’s quiet Claude Code retreat and the real cost of enterprise AI

-

Business5 days ago

Business5 days agoBTS Sells Out Four Las Vegas Shows at Allegiant Stadium for ARIRANG World Tour

-

Tech4 days ago

Tech4 days agoChina assigns ID codes to 28,000+ humanoid robots

-

Tech1 day ago

Tech1 day agoWaymo dominates autonomous vehicle registrations as Tesla trails behind

-

Tech3 days ago

The Samsung pay deal is the moment Korean unions changed register

-

News Videos3 days ago

News Videos3 days agoXRP *JUST* SUCCEEDED!!!! CLARITY ACT EXPOSED!!! (SHE EXPOSED IT)

-

Tech3 days ago

Tech3 days agoMillions of AI agents imperiled by critical vulnerability in open source package

-

Tech5 days ago

Tech5 days agoWestone Audio and Etymotic Acquired by Fidelity Collective in Major IEM Market Move

-

Crypto World5 days ago

Brian Armstrong Outlines Crypto Vision for the Future Financial System

-

Crypto World3 days ago

SpaceX’s $2 Trillion IPO: Why Tech Giants Nvidia (NVDA), Apple (AAPL), and Microsoft (MSFT) May Face Pressure

-

Crypto World5 days ago

Crypto World5 days agoNvidia (NVDA) CEO Calls on Super Micro to Strengthen Export Controls Amid Smuggling Probe

-

Entertainment4 days ago

Entertainment4 days ago‘Breaking Bad’ Star’s Easy-to-Binge 6-Part Crime Series Spin-Off Is Finally Heading to Free Streaming

-

Tech3 days ago

Tech3 days agoNASA taps Blue Origin to deliver lunar rovers for Moon Base initiative

-

NewsBeat5 days ago

NewsBeat5 days agoHottest May day ever as London hits 34.8C in 2C leap from previous records

You must be logged in to post a comment Login