Crypto World

The era of easy money in crypto is over as DeFi yields are failing to compete with a simple savings account

Crypto investors who once turned to decentralized finance for easy passive income through juicy yields are running into a new reality: the numbers no longer add up.

DeFi, or onchain finance, is essentially conducting banking transactions on a blockchain, cutting out middlemen like banks and letting investors borrow, lend, and trade in minutes. Back in 2021-2022 (and even through the subsequent crypto winter), DeFi’s returns were more than promising; rates reached 20% on protocols like Aave and thousands of percent on other emerging protocols, which would justify parking some cash for high interest rates, albeit with a higher risk of hacks, exploits and quick liquidations.

Read more: What is DeFi?

Fast forward to 2026, Aave, the largest DeFi lending protocol by total value locked, is currently offering an APY of around 2.61% on USDC deposits. That sits below the 3.14% offered on idle cash at Interactive Brokers, one of the most popular traditional platforms among crypto-native investors. The gap may not seem huge on paper, but it undermines one of DeFi’s core theses: higher returns for higher risk. Instead, money sitting in DeFi is now facing a higher risk for lower returns.

“DeFi: earn 1% below T-bills and lose all your money one time per year,” wrote trader James Christoph on X on March 22.

That blunt take reflects a broader shift. For years, DeFi sold itself as a place where higher returns justified new kinds of risk. Today, that trade-off looks harder to defend.

Where the yield went

It was not always this way.

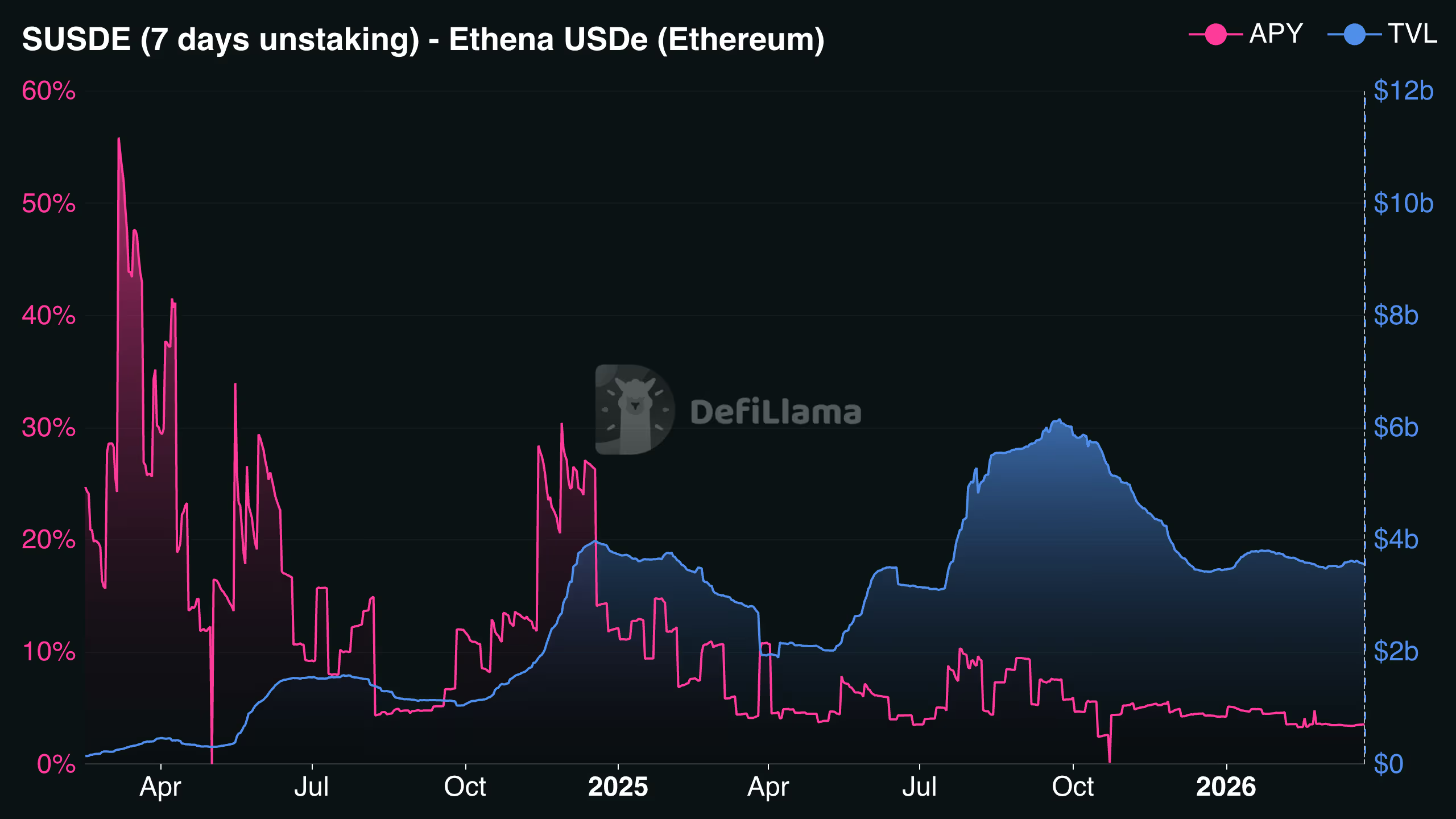

In 2024, DeFi yield looked genuinely competitive. Ethena — a protocol that issues a synthetic dollar stablecoin, USDe, backed by assets and hedged through derivatives positions — saw its sUSDe product offer more than 40% APY at its peak and pulled billions in deposits. But those returns were largely a product of ENA (Ethena’s native token) incentives and trading strategies that didn’t last.

Ethena’s APY has since compressed to around 3.5%, while its total value locked (TVL) has fallen from a peak of roughly $11 billion to $3.6 billion. Ethena didn’t immediately respond to the request for a comment by press time.

The CoinDesk Overnight Rate, which tracks daily borrowing costs across DeFi lending markets, tells the same story — spiking above 35% during the 2023 bull run before collapsing to roughly 3.5% today.

Across the rest of the stablecoin lending market, yields have followed a similar path lower.

Aave’s largest USDT pool yields 1.84%, while several other pools sit below 2%. The extra reward that once boosted returns have largely disappeared. What remains is organic yield driven by borrowing demand, and it is not strong enough to push yields higher.

Data from vaults.fyi shows how far things have fallen. Aave’s two largest stablecoin pools — USDT and USDC on Ethereum — are yielding just over 2% on a combined $8.5 billion in deposits. Lido’s stETH, the largest pool, returns 2.53%, while Ethena’s staked USDe has fallen to 3.47%.

Only a handful of protocols are still beating Interactive Brokers’ 3.14% rates. These are largely private credit products or strategies tied to real-world assets such as Sky’s USDS Savings rate of 3.75%, which has emerged as one of the more attractive refuges in this environment, sitting above the Aave average and drawing $6.5 billion in deposits.

But the rate comes with a caveat: around 70% of Sky’s income derives from offchain sources, including U.S. Treasury products, institutional credit lines, and Coinbase USDC rewards. For investors who came to DeFi specifically to avoid that kind of exposure, the distinction matters.

Aave does still offer more competitive rates on select stablecoins beyond its flagship USDC pool. Its sGHO product currently yields 5.13%, while other options of V3 Core Ethereum include USDG at 5.9%, RLUSD AT 4.4% AND USDTB AT 4.0%. But these sit outside the headline figures that most comparisons focus on.

Paul Frambot, co-founder of Morpho, a lending infrastructure protocol, says this bleak outcome for yields was inevitable.

“Undifferentiated lending converges toward risk-free rates because when every depositor shares the same collateral, the same parameters, and the same outcome, there is limited room for specialization and returns compress,” he told CoinDesk.

Morpho, with over $10 billion in deposits, offers a different model. Its platform lets curators build lending vaults – essentially customized pools with their own risk parameters, collateral choices and yield strategies, managed by specialist teams rather than governed by a single set of rules. Some of these curated vault models can still generate relatively higher yields. Its Steakhouse Prime USDC and Gauntlet USDC Prime vaults are both yielding 3.64%, while one vault, Sentora’s PYUSD offering, is at 6.48%.

Frambot says the difference comes down to how risk is managed. “What makes the vault and curator model different is that it externalizes risk curation and opens it up to real competition,” he said. “That creates an open marketplace for yield, where returns are driven by the quality and differentiation of strategies rather than liquidity alone. That is also why bluechip stablecoin yields on Morpho are on average higher than in pooled models and backed by straightforward collateral like BTC and ETH.”

Still, the yields are nowhere near what they were in previous years.

Aave frames the current weakness as cyclical rather than structural. The protocol points to unusually depressed crypto sentiment – with the Fear and Greed Index below its 2022 lows – as a key driver of reduced borrowing demand, which in turn weighs on deposit rates. “Stablecoin rates on Aave have largely tracked leverage demand,” a spokesperson told CoinDesk. “We do not see them as structurally lower going forward.”

The company also notes that its weighted-average stablecoin deposit yield over the past year has still beaten Interactive Brokers’ top offering, meaning depositors who entered before 2025 would still be ahead today.

‘Really dark’

Lower yields, though, are only part of the story. Confidence across DeFi has also taken a hit.

Balancer Labs, once one of the most recognizable names in decentralized exchange infrastructure, has recently shut down after a $110 million exploit. Governance tokens across the sector are trading at low valuations. For many, it feels like energy has been drained out of the space.

Jai Bhavnani, a prominent DeFi investor, wrote on X that the space is feeling “really dark,” describing the combination of yield compression, protocol shutdowns, and recent exploits as a perfect storm.

“LPs are realizing most protocols are too much risk too little reward,” he wrote. “There is no catalyst on the horizon to change things.”

Some in the same thread pushed back, arguing that market downturns tend to flush out the weakest projects and leave behind only those protocols that can genuinely sustain themselves. This counterpoint has historical precedent; DeFi has survived prior cycles and emerged with more resilient infrastructure. That may be true, but it offers little comfort to investors sitting on compressed returns today.

Then there is smart contract risk, or more precisely, the growing range of risks that smart contract audits cannot catch.

Last month, Resolv, a yield-bearing stablecoin protocol, was exploited for roughly $25 million. An attacker deposited 100,000 USDC into the protocol’s minting contract and received 50 million USR in return, roughly 500 times the expected amount. The issue was not a flaw in the smart contract code itself. Instead, the system lacked basic safeguards such as oracle checks and minting limits.

The protocol now holds $113 million in assets against $173 million in liabilities. USR is trading at $0.13, having lost its $1.00 peg and continuing to tumble into the end of March.

The Resolv hack sits within a broader pattern. Hackers stole more than $2.47 billion worth of cryptocurrency in the first half of 2025 alone, already exceeding all of 2024, according to CertiK’s Hack3d report. Wallet compromises accounted for $1.7 billion of that total. Immunefi CEO Mitchell Amador told CoinDesk earlier this year that onchain code is actually getting harder to exploit, but that attackers are adapting, pivoting to operational failures, stolen keys, and social engineering instead. For example, the more recent $270 million exploit on Drift protocol was part of a social engineering program by North Korea.

For investors weighing up a 2%-3% yield on DeFi against 3.14% at a traditional brokerage, that context is hard to ignore. The extra return that once justified the exposure has largely disappeared.

But the deposit rate comparison only tells part of the story. An Aave spokesperson said: “For borrowers and margin traders, Aave offers much more competitive rates than IBKR — currently 3.2% on Aave vs. up to 6.14% on IBKR. Borrowers on Aave also benefit because their collateral continues to earn yield, further reducing effective borrowing costs compared to IBKR.”

Regulatory ‘Clarity’

On top of compressed yields and persistent security risks, DeFi is now facing a regulatory threat targeting its yield model.

The Digital Asset Market Clarity Act, the crypto industry’s most significant pending legislation, includes a provision that would ban passive stablecoin yield earned simply for holding a dollar-pegged token. That would mean rewards tied to activity, such as payments or transfers, would still be allowed, although the distinction remains unclear. Something that crypto industry insiders who reviewed the draft described to CoinDesk as “overly narrow and unclear.”

Recently, 10x Research’s Markus Thielen said that if the Clarity Act is passed, it could re-centralize yield into traditional finance and regulated products, creating a headwind for DeFi.

Bottom line: the DeFi provisions of the bill remain unresolved, with several Senate Democrats citing concerns about illicit finance. But the direction of travel on yield is clear enough: at a moment when DeFi returns are already struggling to justify the risk, Washington is potentially moving to narrow the options further.

That leaves DeFi in a tight spot. Yields are down. Risks remain. And new rules could limit what returns are left.

For now, the math that once drew investors in is looking much less convincing.

Read more: How North Korea’s 6-month-long secret espionage program has crypto community rethinking security

The Iran US ceasefire deal update news today is contradictory and fast-moving: the New York Times reported that Iran halted ceasefire negotiations entirely after Trump’s “civilization will die” post, while Iran’s own Tehran Times simultaneously insisted that “diplomatic and indirect channels of talks with the US are not closed.”

Summary

- The New York Times, citing three senior Iranian officials, reported that Iran informed Pakistani mediators it was ending ceasefire negotiations after Trump’s 8 AM ET Truth Social post on April 7

- The Wall Street Journal separately reported that Iran cut off “direct communications with the US,” while Iran’s ambassador to Pakistan said mediation efforts had reached a “critical, sensitive stage”

- Iran submitted a 10-point peace proposal through Pakistani intermediaries rejecting a temporary ceasefire and calling instead for a permanent end to the war, the lifting of all sanctions, and reconstruction

The Iran US ceasefire deal update news today reflects a conflict between what different governments are saying publicly and what is happening through back channels. According to CNBC, citing the New York Times directly: “The New York Times, citing three senior Iranian officials, reported that Iran has stopped negotiation efforts with the U.S. and told Pakistan, which has acted as a mediator, that it would end ceasefire talks.” The Wall Street Journal added that Iran cut off “direct communications with the US.” But Iran’s Tehran Times posted on X that “diplomatic and indirect channels of talks with the US are not CLOSED” — and Iran’s ambassador to Pakistan said the peace efforts had reached a “critical, sensitive stage.”

The immediate trigger was Trump’s Truth Social post just after 8 AM ET on April 7, in which he wrote that “a whole civilization will die tonight.” Iranian officials cited the post as incompatible with negotiation. Foreign Ministry spokesperson Esmail Baghaei had already stated the day before that talks were “entirely incompatible with ultimatums, crimes and threats of war crimes.”

Before the breakdown, Iran submitted a formal 10-point proposal through Pakistani mediators. The proposal rejected any temporary 45-day ceasefire and instead demanded a permanent end to the conflict, a protocol governing safe passage through the Strait of Hormuz, the lifting of all US sanctions, and Iranian reconstruction funding. Trump publicly acknowledged the proposal on Monday, calling it “a significant step” but “not good enough.”

Why the 45-Day Ceasefire Was a Non-Starter for Iran

Iran’s refusal to accept a temporary ceasefire is rooted in its experience during Israel’s 12-day war in June 2025, which Iran argues showed it that ceasefire agreements do not prevent future attacks. As crypto.news reported, Iran has consistently demanded that any deal include guarantees against future attacks — not just a pause — and that the Strait of Hormuz’s full reopening would happen only under a final, comprehensive agreement, not as a confidence-building measure in a preliminary phase.

What Markets Are Doing With the Conflicting Signals

The contradiction between the official walkout and the back-channel communication is exactly what has made this conflict so difficult for markets to price. As crypto.news noted, Bitcoin pulled back below $69,000 when Trump confirmed Iran’s earlier proposal was insufficient, as traders returned to bearish positioning. The pattern throughout this conflict has been the same: ceasefire signals produce brief relief rallies, and their collapse reverses those gains within hours.

With 8 PM ET rapidly approaching, the credibility of any remaining indirect channel depends almost entirely on whether Iran uses the next few hours to signal something concrete to Pakistani mediators — or whether tonight sees the military escalation Trump has threatened.

“All elements need to be agreed today,” a source aware of the proposals told Reuters early Tuesday. “The initial understanding would be structured as a memorandum of understanding finalized electronically through Pakistan, the sole communication channel in the talks.”

In a high-stakes move that sharpens the focus on developer responsibility in crypto tooling, prosecutors in the U.S. Attorney’s Office for the Southern District of New York have asked a federal court to reject Tornado Cash co-founder Roman Storm’s bid for acquittal. The filing centers on the contention that Storm’s alleged actions go beyond a civil copyright dispute and implicate conspiracies to commit money laundering and sanctions violations.

Jay Clayton, the SDNY attorney who previously led the U.S. Securities and Exchange Commission, argued in court papers that Storm’s use of Tornado Cash was “window dressing at best and outright misdirection at worst.” The filing criticized Storm’s attempt to frame his defense around a civil copyright case, insisting there is no evidentiary basis for equating his conduct with civil liability and that such a line of defense is irrelevant to the criminal charges at hand. The motion responded to Storm’s plan to cite a 2026 Supreme Court case, Cox Communications, Inc. v. Sony Music Entertainment, as part of an argument about Storm’s intent to participate in the criminal activity prosecutors allege.

According to the SDNY, Storm’s alleged conduct bears little resemblance to the facts in the Cox case, which dealt with copyright infringement in a civil context. The government contends there is no evidence that Storm or Tornado Cash’s developers implemented any effective anti-money-laundering controls, a point Clayton stressed in the filing.

“The defendant’s conduct simply is not comparable to the conduct at issue in Cox,” Clayton said. “In any event, a civil copyright case has no relevance here in the first place.”

Last August, a jury convicted Storm of conspiracy to operate an unlicensed money transmitting business, but the panel deadlocked on two other charges — conspiracy to commit money laundering and conspiracy to violate sanctions — leaving the possibility of a retrial on those counts. The case has become a flashpoint in the broader debate over whether developers of open-source crypto tools can be held legally liable for how their code is used in illicit finance schemes.

Prosecutors and Storm’s defense team were slated to meet on the following Thursday to discuss the path ahead, including the possibility of a retrial date. In the meantime, the government has signaled continued pursuit of the remaining charges, while the defense has pressed for a dismissal or a narrow resolution based on civil-law considerations.

In a contemporaneous political thread surrounding the case, the conversation extended beyond the courtroom doors. Last week, reports circulated that U.S. lawmakers were advancing proposals intended to shield blockchain developers from broad prosecution, signaling a regulatory ambition to distinguish between personal risk and platform-level liability.

Key takeaways

- The SDNY explicitly rejects Roman Storm’s attempt to leverage Cox Communications as a defense, asserting the criminal nature of the alleged activity is not comparable to civil copyright disputes.

- Storm was convicted on conspiracy to operate an unlicensed money transmitting business, while two related charges ended in a mistrial, keeping the door open for a retrial on those counts.

- The case amplifies the ongoing debate about whether developers behind open-source crypto projects can be held criminally liable for how others use their code.

- News of a potential October retrial underscores the government’s intent to pursue the remaining charges, even as questions about evidentiary standards and defense strategy persist.

- In parallel, U.S. policymakers continue to explore protections for blockchain developers, highlighting tensions between enforcement goals and innovation incentives.

- The evolving DOJ posture, including commentary associated with acting Attorney General Todd Blanche, could influence how aggressively prosecutors pursue similar cases and how they frame regulatory boundaries around crypto platforms.

Courts, cases and a shifting DOJ posture

Clayton’s filing frames the Storm case within a larger legal question: when, if ever, does enabling code cross the line into criminal participation? The defense’s tactic of invoking a civil copyright precedent appears designed to downplay Storm’s alleged role in facilitating illicit activity, but prosecutors argue that the underlying conduct extends far beyond such civil concerns. The government’s stance rests on an assertion that there was no adequate safeguard against abuse by Tornado Cash’s tools, a factor central to charges of money laundering conspiracies and sanctions violations.

The legal strategy in play here matters beyond one defendant. It tests the boundaries of developer liability for open-source projects and raises critical questions about how prosecutors evaluate intent and control in decentralized tooling. If civil analogies or civil-law defenses fail to translate to criminal contexts, the door may remain open for tougher scrutiny of developers whose code can be used for illicit ends—even when they claim no direct involvement in wrongdoing.

Meanwhile, the timing of the potential retrial adds a layer of strategic calculus for both sides. The SDNY has requested October as a possible window for re-presenting the evidence on the two previously deadlocked counts, but no date has been officially set as of now. The outcome could influence how similar cases are positioned in the future and how aggressively prosecutors pursue open-source projects that enable or facilitate illicit activity, including cross-border sanctions evasion.

DOJ policy signals and the broader regulatory backdrop

The Storm case sits at the intersection of criminal enforcement and policy signaling within a changing regulatory landscape. Last week, headlines centered on how a reshuffled Justice Department might recalibrate its approach to crypto. Acting Attorney General Todd Blanche, who has previously commented on the need to end what he termed “regulation by prosecution,” laid out a vision that could affect enforcement priorities in the crypto space. While Blanche did not name Storm specifically, he argued that the department should avoid pursuing actions against platforms that criminals leverage to conduct illegal activity and called for alignment between enforcement actions and overarching policy goals. The implications for Tornado Cash and similar tooling are indirect but notable, as prosecutors weigh how to apply anti-money-laundering and sanctions laws to decentralized technologies.

Storm himself has publicly framed the stakes in stark terms. In March, after prosecutors indicated a path toward retrying the two deadlocked counts, he argued that the charges could carry substantial maximum penalties — up to 40 years in federal prison — for actions tied to writing open-source code for a protocol he says he didn’t control and transactions he didn’t touch. The rhetoric underscores the tension between a developer-centric view of code as a public good and a prosecutorial view that code can be weaponized for financial crime when used in unintended or illicit ways.

Beyond the courtroom, the case feeds into a broader policy dialogue about how to balance innovation with enforcement. Lawmakers have floated measures designed to protect blockchain developers from punitive prosecution while maintaining guardrails against illicit finance. The tension between protecting innovation and deterring abuse remains a central theme in crypto regulation discussions, a dynamic that could shape how the industry negotiates risk, compliance, and governance in the years ahead.

As the legal process unfolds, observers will be watching the interaction between civil-law arguments, criminal liability standards, and the practical realities of open-source development. The Storm case is not just about a single set of charges; it is a bellwether for how courts interpret developer intent, how anti-money-laundering controls are evaluated in decentralized systems, and how policymakers balance the dual aims of fostering innovation and safeguarding financial integrity.

Readers should keep an eye on timing updates from the SDNY as it relates to potential retrial dates and any new motions from either side. The outcome could influence not only this case but the broader approach to crypto tooling and developer accountability as enforcement bodies navigate a rapidly evolving technical landscape.

For policymakers and market participants alike, the central question remains: where should the line be drawn between legitimate open-source development and actions that trigger criminal liability in an environment built on privacy, pseudonymity, and permissionless participation?

As the courtroom drama continues, the crypto community will be watching closely to assess how the balance between innovation and enforcement is negotiated in this era of rapid technological change.

The U.S. Federal Deposit Insurance Corp. formally proposed its approach to stablecoin issuers as one of the federal financial regulators required to write and oversee rules under last year’s Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act.

The FDIC’s proposal —meant to align closely with what its sister banking agency, the Office of the Comptroller of the Currency, proposed in February — will be open for a 60-day public comment period on the lengthy list of 144 questions posed Tuesday by the agency.

The FDIC’s job is to police U.S. depository institutions, and under the GENIUS Act, its role is to regulate such institutions issuing stablecoins from their subsidiaries. To that end, it posed capital, liquidity and custody standards for those firms, though the details won’t be set in stone until the rule is finalized — not likely to occur until the agency spends further months reviewing input and writing the final language. This is the second GENIUS Act proposal from the banking agency after its December pitch on the issuer application process.

As expected under the law, stablecoins won’t enjoy the deposit insurance that the banks maintain on traditional banking accounts, according to the proposal.

The OCC’s earlier proposal had a section that caused some initial concern among crypto policy experts wondering how the agency would allow for rewards programs managed by third-party stablecoin relationships, such as exchanges. In the same vein, the FDIC said that issuers wouldn’t be able to represent that their tokens pay interest or yield “simply for holding or using a payment stablecoin,” according to the staff presentation, including via arrangements with third parties. But crypto insiders have grown comfortable that properly tailored rewards programs shouldn’t run afoul of the rules.

The FDIC’s Tuesday proposal also suggested the capital that issuers will need to maintain to manage the risk of the business, plus “an operational backstop, separate from the capital requirement,” based on the previous year’s operating expenses.

The agency also addressed “the applicability of pass-through insurance to deposits held as reserves backing payment stablecoins,” proposing that “tokenized deposits that satisfy the statutory definition of ‘deposit’ would be treated no differently” than other deposits.

While the regulators work to implement GENIUS, some of its details are potentially already being overhauled by the work on the Senate’s Digital Asset Market Clarity Act. A clash between the banking and crypto industries over yield-bearing stablecoin holdings turned into a months-long debate that lawmakers have said they’re close to resolving, though the bill hasn’t yet advanced to a needed hearing. Congress comes back from a break later this week.

The OCC, FDIC and other agencies involved in implementing the rule, including the Treasury Department and the markets regulators, have few impediments in crafting regulations the way the Republican appointees want it. President Donald Trump’s White House has broken with past practice and declined to name any Democrat appointees to the many vacancies across the agencies, so there are no Democrats to raise objections to regulatory language.

But the GENIUS Act itself had drawn significant bipartisan support in both chambers of Congress when it was passed into law.

Read More: U.S. FDIC proposes first U.S. stablecoin rule to emerge from GENIUS Act

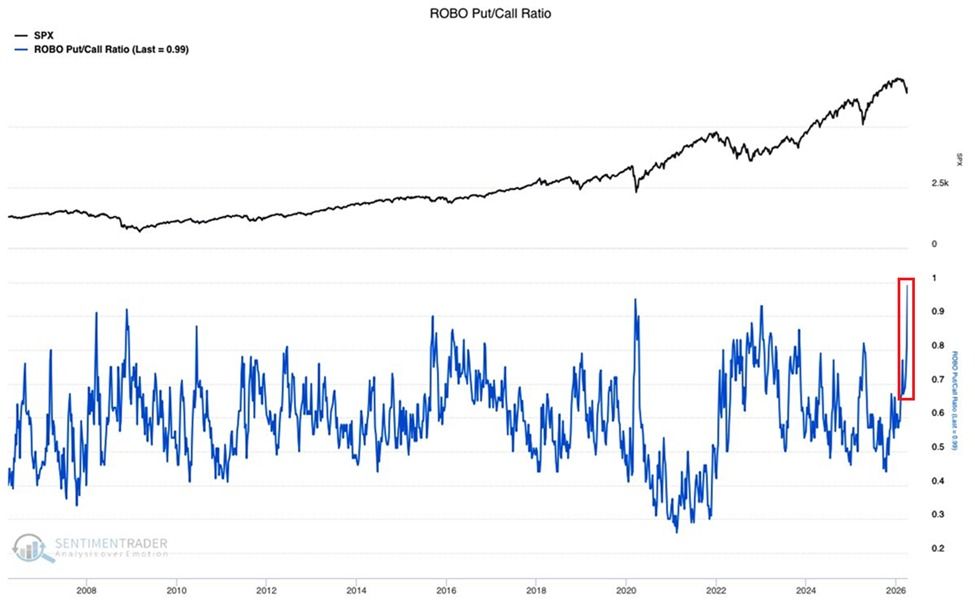

Retail fear across US equity markets has reached levels not seen in over two decades. The ROBO Put/Call Ratio has jumped to 1.0 for the first time in at least 20 years.

The reading exceeds the 0.91 peak during the 2008 Financial Crisis and the 0.95 reached during the 2020 pandemic selloff. The ratio has doubled since December, marking the sharpest rise since the 2022 bear market began.

“This ratio tracks retail opening buy orders in options, with the current reading showing retail traders buying nearly equal amounts of puts and calls…Fear is becoming overdone in this market,” The Kobeissi Letter noted.

Follow us on X to get the latest news as it happens

Market sentiment is also evidenced by the CNN Fear & Greed Index, which has fallen to 23, placing it at the threshold of extreme fear territory.

Bearish Positioning Reaches Rare Extremes

The surge comes amid a broad rise in short interest across all major US indexes. According to data from Global Markets Investor, the median short interest for the S&P 500 now stands at approximately 3.7%, its highest level in 11 years.

The Nasdaq 100 has reached roughly 2.7% short interest, a 6-year high. The Russell 2000 sits near 5.0%, its highest in 15 years.

The last time all three indexes showed such elevated short positioning simultaneously was during the 2010-2011 European debt crisis. That convergence is significant because it suggests bearish conviction extends beyond any single sector or market-cap segment.

“All three indexes have seen short interest rise sharply since mid-2024, accelerating further in 2026,” the post added.

BeInCrypto recently reported that hedge funds shorted global equities at the most aggressive pace in 13 years, with short sales outpacing long purchases by a ratio of 7.6 to 1.

The simultaneous alignment of extreme retail fear, a near-extreme Fear & Greed reading, and elevated institutional short positioning creates a notable asymmetry. Even a modest positive catalyst could trigger forced covering across multiple indexes, triggering a rapid, potentially disorderly rally.

The contrarian case is building, but a catalyst is needed. Sentiment alone doesn’t reverse markets. The critical question is whether current fear reflects genuine, fundamental deterioration or an overshoot driven by peak-fear psychology.

A resolution in the escalating US-Iran tensions could be the kind of macro shock that flips the narrative, but for now, with no signs of de-escalation, the market remains in a holding pattern between peak fear and potential inflection.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post US Equity Fear Gauge Tops 2008 Crisis Levels as Short Interest Hits Multi-Year Highs appeared first on BeInCrypto.

The US Iran war latest news oil prices today tells a sharply escalating story: American forces struck more than 50 military targets on Kharg Island, the hub through which Iran exports 90% of its crude, sending oil surging more than 3% to nearly $116 per barrel within minutes of the first reports.

Summary

- The US military struck dozens of military targets on Kharg Island early Tuesday, Iran’s semi-official Mehr News Agency was first to report explosions, and Vice President JD Vance confirmed the strikes during a press conference in Budapest

- Oil jumped over 3% to nearly $116 per barrel immediately, while Brent crude crossed $110; Vance said the strikes did not include oil infrastructure and did not represent a change in strategy ahead of Trump’s 8 PM ET deadline

- The IRGC warned it would “deprive the US and its allies of the region’s oil and gas for years” if Trump follows through with threatened strikes on Iran’s civilian power and water infrastructure tonight

The US Iran war latest news oil prices today sent a fresh shock through global energy markets on Tuesday as US forces struck more than 50 military targets on Kharg Island, Iran’s largest oil export hub, hours before President Trump’s 8 PM ET deadline expired. Iran’s semi-official Mehr News Agency reported multiple explosions on the island as early as 1:30 PM local Tehran time, and oil surged immediately, with US crude jumping over 3% to nearly $116 per barrel and Brent crossing $110.

VP JD Vance confirmed the strikes during a press conference with Hungarian Prime Minister Viktor Orbán in Budapest, characterizing them as “re-strikes” on previously targeted sites. “I don’t think the news about Kharg Island changes anything,” Vance said, insisting the attacks did not touch oil infrastructure and did not alter the president’s strategy ahead of the evening deadline.

Kharg Island handles roughly 90% of Iran’s crude oil exports and carries a loading capacity of about 7 million barrels per day, making it the primary financial lifeline of Tehran’s war-era economy. Iran earns an estimated $53 billion in net oil export revenues annually, about 11% of its GDP, almost entirely flowing through the island’s pipelines and terminals.

The US has now struck the island twice since the war began February 28. The first attack in mid-March destroyed naval mine storage facilities, missile bunkers, and air defense systems while preserving oil infrastructure. Tuesday’s strikes hit some of the same sites, according to a US official, again stopping short of targeting the oil terminal itself. Whether that restraint holds after 8 PM is the question driving markets.

What an Oil Infrastructure Strike Would Mean

Analysts have warned that striking Kharg’s oil terminal would have immediate and lasting consequences. “A direct hit on Iran’s export terminal would instantly shut down most of its 1.5 million barrels per day crude exports,” JPMorgan data cited by CNBC showed. “Destruction of its oil infrastructure would take years to rebuild, leaving the country deprived of its most critical source of revenue,” Vandana Hari of Vanda Insights told CNBC.

Iran has already telegraphed its response. The IRGC warned Tuesday that it would “deprive the US and its allies of the region’s oil and gas for years” if the civilian infrastructure strikes go forward. It also signaled that restraint toward Gulf Arab states hosting US military assets is now over, saying “all such considerations have been lifted” — a direct threat to regional energy facilities in Saudi Arabia, Kuwait, and the UAE.

Bitcoin and Crypto Markets Under Fresh Pressure

As crypto.news reported, each round of escalation in this conflict has pushed oil higher and Bitcoin lower, with the Strait of Hormuz closure already keeping crude above $100 for weeks and compressing Federal Reserve flexibility on rate cuts. Crypto.news also noted that major cryptocurrencies have dropped 3 to 5% during prior escalation phases, as higher oil prices feed directly into inflation expectations and reduce appetite for risk assets.

Tonight’s 8 PM deadline, and what follows it, will determine the next major move for both energy and crypto markets.

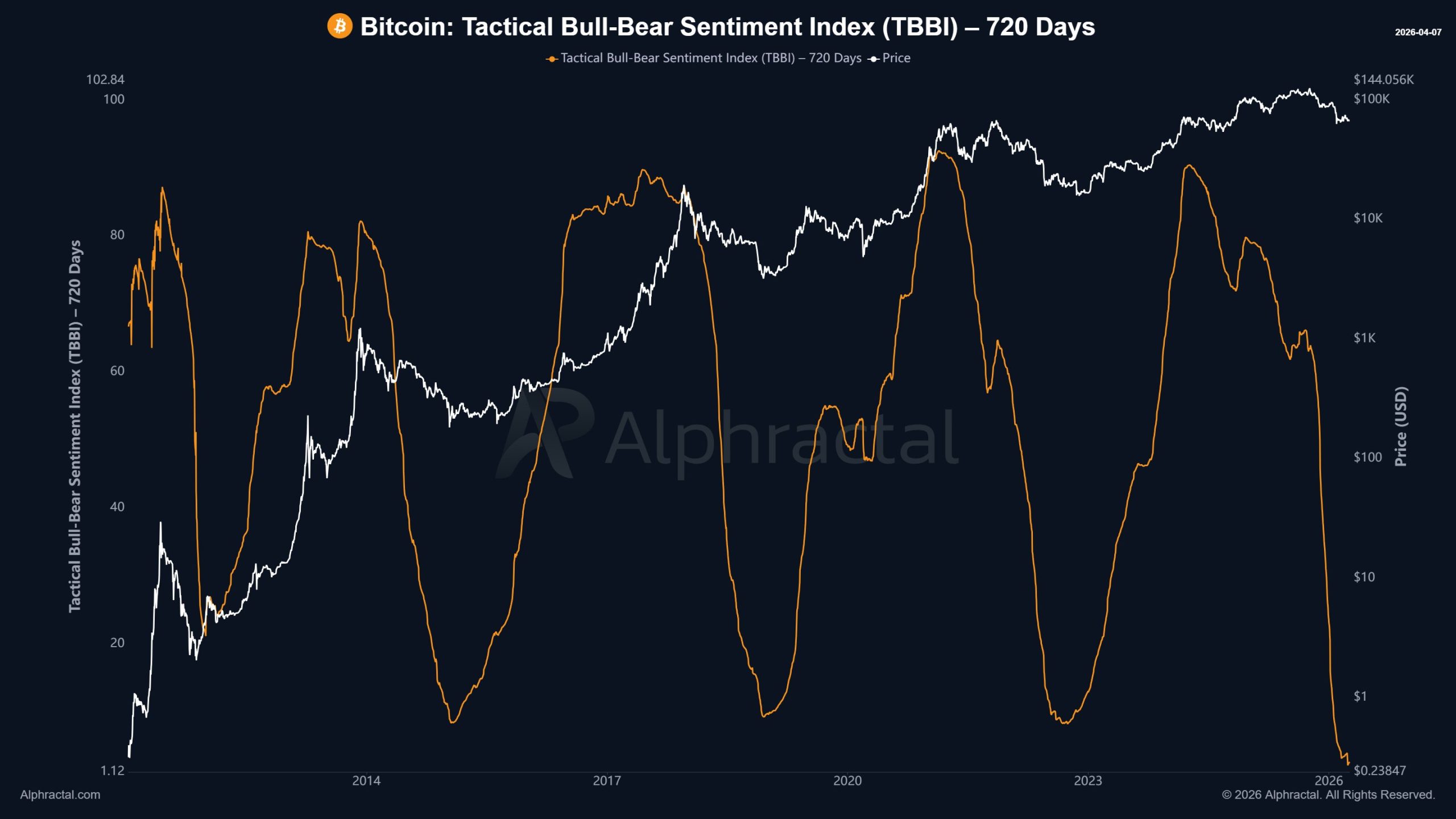

Multiple Bitcoin indicators, including a bull-bear sentiment index and realized price metric, point to a possible final BTC shakeout toward $54,000

Bitcoin (BTC) is showing signs of the bear market’s late stages but could see another leg lower in the coming months, says Joao Wedson, founder and CEO of on-chain analytics platform Alphractal.

Key takeaways:

-

BTC may still see one last big drop before recovering, based on one sentiment indicator.

-

The next likely downside target is near Bitcoin’s realized price at $54,000.

BTC index hints at a drop toward $54,000

In a Tuesday post, Wedson said Bitcoin’s 720-day Tactical Bull-Bear Sentiment Index (TBBI), a long-term indicator that tracks multi-year cycles of fear and greed, had dropped into an extreme bearish zone below 20.

Historically, such readings have reflected “late-stage fear” among traders, a phase that can still produce one final shakeout before Bitcoin begins a more durable recovery.

In 2022, for instance, Bitcoin fell more than 20% after the indicator reached similarly depressed levels.

A comparable setup also appeared before Bitcoin lost around 50% in 2018, prompting Wedson to see a similar possibility in 2026.

Related: Bitcoin RSI ‘nearly perfectly’ copying end of 2022 bear market: Analysis

He warned that Bitcoin could still face “a sharp move like a –$15K shakeout” over the next six months, implying a roughly 20% decline from current levels toward the $54,000 area.

More BTC indicators converge on $50,000–$55,000

The implied target matches earlier BTC downside calls that see Bitcoin falling toward the $50,000–$55,000 area on war-led oil inflation and quantum security risks.

The $54,000 level also nearly coincides with Bitcoin’s realized price (purple) on Glassnode’s MVRV Extreme Deviation Pricing Bands, suggesting any final shakeout could send BTC toward a key on-chain cost-basis support level.

More bearish forecasts have also surfaced, with analysts such as Bloomberg Intelligence’s Mike McGlone warning that Bitcoin could eventually slide to as low as $10,000.

Still, Strategy’s aggressive Bitcoin purchases in recent weeks have helped absorb selling pressure and limit BTC’s downside, raising the possibility that the broader bearish scenario may fail to play out.

As Cointelegraph reported, Bitcoin could reverse sharply and climb back toward $100,000 or higher if the Michael Saylor firm continues its buying spree.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

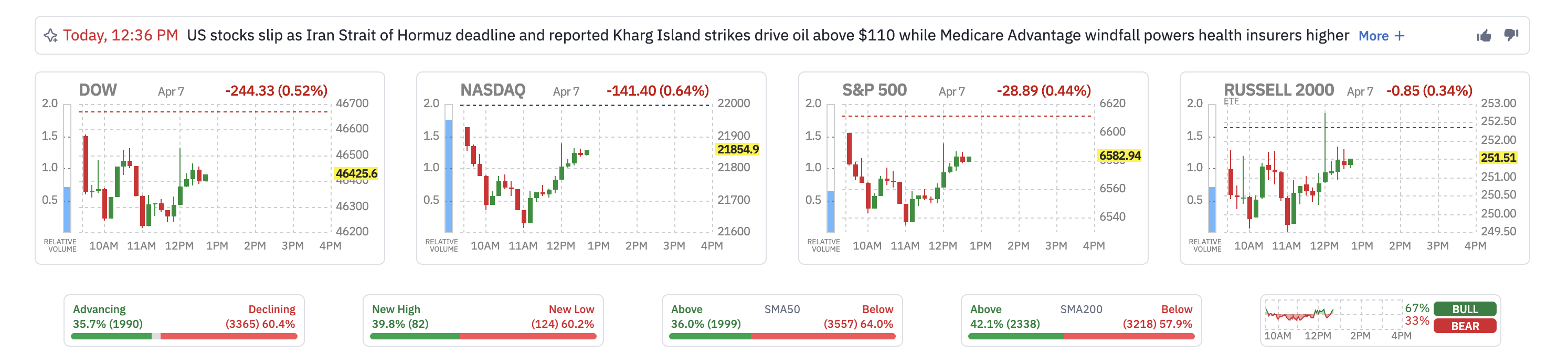

The US stock market dropped on April 7 as Trump’s warning that “a whole civilization will die tonight” ahead of the Iran Strait of Hormuz deadline injected fresh fear into equities.

WTI crude surged to $115.19, up 13% in a single week, as reports of Israeli strikes on Iran’s Kharg Island petrochemical infrastructure removed the remaining de-escalation hopes that had given stocks a brief lift in recent sessions.

Three forces drove selling on April 7, all tracing back to the same root cause. Oil above $115 is feeding into inflation expectations, keeping the Fed locked, and crushing consumer and growth stocks simultaneously.

1. Trump’s “Civilization” Warning Kills De-Escalation Narrative

Markets had been pricing in partial de-escalation after Iran’s earlier diplomatic exchanges through mediators. Trump’s statement, made ahead of his self-imposed Tuesday deadline for Iran to reopen the Strait of Hormuz, killed that narrative and reignited fears of direct strikes on Iranian energy infrastructure.

The Hormuz closure has already disrupted roughly one-fifth of global oil and LNG supplies. Trump’s demand for immediate reopening, paired with reports of Kharg Island strikes, signals that the conflict is entering a more dangerous phase rather than winding down.

Risk assets sold off as the “war ending soon” trade unwound.

2. WTI at $115 Tightens the Oil-Inflation-Rates Chain

WTI crude at $115.19 is 13% higher in a single week. Oil at these levels functions as a direct tax on consumers and businesses, raising input costs across every sector and feeding into the inflation data the Federal Reserve is watching.

The March CPI report due Friday is expected to show the sharpest monthly increase since 2022, making rate relief even less likely.

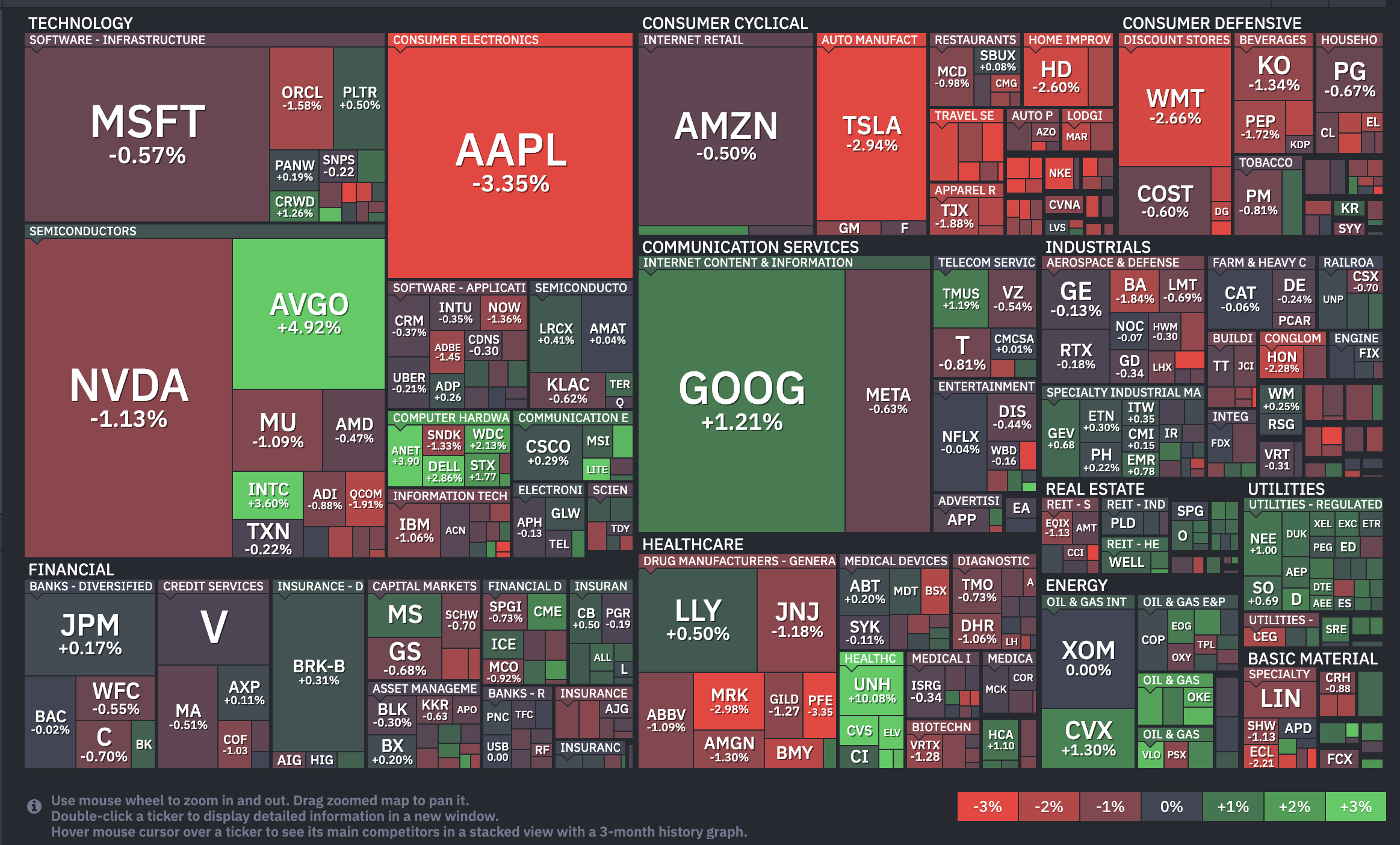

3. Apple’s 3.35% Drop Drags the Index

Apple (AAPL) fell 3.35% after Nikkei Asia reported engineering setbacks in the foldable iPhone that could push back production timelines. Apple carries the largest weighting in the S&P 500, so a nearly 4% decline mechanically drags the index regardless of broader conditions.

What Is Happening to Major US Indexes?

At press time, all four major indexes are in the red.

- S&P 500 fell 28.89 points (−0.44%) to 6,582.94. The index dipped over 1% earlier in the session before recovering.

- Dow Jones Industrial Average dropped 244.33 points (−0.52%) to 46,425.60.

- Nasdaq Composite declined 141.40 points (−0.64%) to 21,854.90.

Russell 2000 slipped 0.85 points (−0.34%) to 251.51, confirming that small-cap weakness mirrors the broader index decline.

Market breadth is negative, with 3,365 stocks declining (60.4%) versus 1,990 advancing (35.7%).

The S&P 500 trades at 6,580 on the daily chart, grappling with two converging Exponential Moving Averages (EMAs), trend indicators that give greater weight to recent price action.

The 20-day EMA sits at 6,601 and the 200-day EMA at 6,587. When the shortest and longest EMAs compress this tightly, it reflects a market that has lost directional conviction and is waiting for a catalyst to force resolution.

The intraday low of 6,534 found support near 6,518 at the 0.382 technical level. A daily close below 6,518 opens the path toward 6,441 and the previous swing low at 6,316.

On the upside, the US stock market needs a daily close above 6,643 to show recovery strength, with 6,845 as the next target above that.

Which Sectors Are Holding Up?

Energy led with a +0.54% gain as WTI stayed above $115. The sector remains the only group with a structural tailwind from the Iran conflict, as elevated oil prices directly increase producer revenue.

Utilities added +0.35% as defensive positioning continued. Risk aversion is overriding the sector’s traditional rate sensitivity, making yield-paying defensives attractive as a parking spot for nervous capital.

Communication Services gained +0.30%, supported by Google (GOOG) rising 1.21%.

Which Sectors Are Falling?

Consumer Cyclical led losses at −1.48%. Higher oil prices compress discretionary spending power by raising fuel and transportation costs. Tesla (TSLA) fell 2.94%, Home Depot (HD) dropped 2.60%, and Walmart (WMT) lost 2.66%.

Consumer Defensive also fell 1.30%, an unusual decline for a traditionally safe sector that signals selling pressure is broad enough to hit even conservative holdings. Coca-Cola (KO) lost 1.34% and Procter & Gamble (PG) dropped 0.67%.

Basic Materials declined 0.63% despite gold holding above $4,400. The decline reflects that commodity-linked equities are not fully insulated from the broader selling pressure.

Major Stock News Investors Are Watching

Broadcom (AVGO) jumped 4.92% after Anthropic signed an agreement with Google and Broadcom for multiple gigawatts of next-generation TPU capacity starting in 2027.

The deal signals that AI infrastructure demand remains strong enough to override the macro headwinds for companies directly tied to capacity buildout.

UnitedHealth Group (UNH) surged 10.08% on Medicare Advantage windfall news, making it the day’s standout gainer in the S&P 500 and providing a floor for the Healthcare sector that would have otherwise fallen further.

What Are Investors Watching Next?

Trump’s self-imposed Tuesday deadline for Iran to reopen the Strait of Hormuz arrives within hours. If Iran signals compliance or a negotiated pathway, oil could retreat sharply, lifting equities by Wednesday’s open.

If the deadline passes without resolution and strikes on Iranian energy infrastructure begin, WTI could push higher. That scenario would further compress the oil-inflation-rates chain. It would push the 10-year yield toward new highs, and bring the S&P 500’s 6,316 swing low firmly into play.

The March CPI data arrives on Friday. A hot print would reinforce the “higher for longer” narrative, while a softer number could provide relief to growth stocks.

The combination of the Iran deadline and CPI makes this week one of the most event-dense for the US stock market.

The post Why Is the US Stock Market Down Today? appeared first on BeInCrypto.

CME Group is expanding its suite of cryptocurrency futures products, as more traditional finance (TradFi) entities launch regulated crypto trading products.

On Tuesday, CME Group announced plans to launch Avalanche (AVAX) and Sui (SUI) futures contracts on May 4, pending regulatory review.

Market participants will be able to trade both micro-sized and larger-sized contracts, including AVAX futures sized at 5,000 AVAX and Micro AVAX futures sized at 500 AVAX, as well as SUI futures sized at 50,000 SUI and Micro SUI futures sized at 5,000 SUI.

CME expands altcoin futures lineup

The news follows CME Group’s announcement in January of its plans to launch crypto futures contracts tied to Cardano (ADA), Chainlink (LINK) and Stellar (XLM).

The move is the latest sign that traditional financial firms are broadening their regulated crypto product offerings.

CME Group’s continued expansion of its crypto derivatives suite reflects “growing demand for regulated, institutionally-sound products in this asset class,” said Justin Young, CEO and Co-founder of Volatility Shares.

During an earnings call in early February, CME Group CEO Terry Duffy said the exchange is mulling plans to launch its own digital token that could operate on a decentralized network.

CME Group is the largest derivatives exchange by volume, and reported a record average daily trading volume of 28.1 million contracts in 2025, according to a Jan. 7 announcement.

Related: Crypto exchanges gain as tokenized commodity market climbs to $7.7B

CME Group prepares to launch 24/7 trading for crypto products

More TradFi entities are exploring ways to issue tokenized investment products with 24/7 trading. CME said on Feb. 19 that its cryptocurrency futures and options products will begin trading 24/7 on May 29.

Unlike traditional stocks and equities constrained to trading hours, cryptocurrencies are natively tradable 24/7 through cryptocurrency exchanges and decentralized venues.

On March 24, the New York Stock Exchange (NYSE) announced it was partnering with tokenization platform Securitize to mint blockchain-based shares of stocks and exchange-traded funds (ETFs), Cointelegraph reported. The initiative is part of its parent company, Intercontinental Exchange’s (ICE) plan for a tokenized securities venue designed for 24/7 trading and instant onchain settlement.

Meanwhile, crypto exchanges are also venturing into tokenized TradFi products. Coinbase launched 24/7 stock perpetual futures for non-US traders on March 20, offering cash-settled exposure to major US stocks and indices, including Apple and Nvidia.

Crypto exchanges Binance and Kraken have also launched tokenized perpetual futures trading for non-US traders, along with other offshore platforms.

Magazine: Can Robinhood or Kraken’s tokenized stocks ever be truly decentralized?

Bitcoin (BTC) stayed near a key long-term trend line at Tuesday’s Wall Street open as markets waited for US-Iran war cues.

Key points:

-

Bitcoin and US stocks attempt to shrug off claims by US President Donald Trump that a “whole civilization will die” after his Iran deadline expires.

-

Oil eyes a rematch with multiyear highs as escalation fears take control.

-

Bitcoin traders see lower levels resulting from current indecision.

Bitcoin attempts to ignore Trump Iran comments

Data from TradingView showed BTC price action focusing on its 200-week exponential moving average (EMA) near $68,300.

Volatility briefly entered prior to the US trading session as President Donald Trump said that “a whole civilization will die tonight,” referring to his 8pm Eastern time deadline for a deal with Iran.

“I don’t want that to happen, but it probably will,” he wrote in a post on Truth Social, while keeping full details sparse.

The post was accompanied by news of strikes on Iranian oil infrastructure on Kharg Island.

Despite this, US stocks managed to avoid major losses on the day, leading commentators to suggest that Iran rhetoric was all but fully priced in.

“Markets have become numb to the headlines,” trading resource The Kobeissi Letter reacted on X.

The day prior, trading company QCP Capital noted that the same geopolitical pattern had been playing out for weeks.

“While the economic and humanitarian consequences of escalation would be severe, particularly via energy market disruption, markets are increasingly discounting the immediacy of this risk,” it wrote in its latest “Market Color” analysis.

QCP described stocks as “broadly stable,” with crypto showing “resilience.”

“After several weeks of weekend escalation rhetoric followed by early-week de-escalation signals, markets are beginning to recognise and fade this pattern,” it continued.

“Despite approaching deadlines and rising rhetoric, crypto markets continue to exhibit resilience rather than panic.”

WTI crude oil nonetheless passed $116 per barrel on the day, coiling below its highest levels in nearly four years.

BTC price surfs liquidity walls

Commenting on Bitcoin and wider market trajectory, crypto trader Michaël Van de Poppe suggested that an inflection point was coming.

Related: Bitcoin RSI ‘nearly perfectly’ copying end of 2022 bear market: Analysis

“Prime question for this is likely whether there will be a ceasefire in the Middle-East or not,” he told X followers.

“From a technical standpoint, it’s more likely that markets are turning downwards as the trend is clearly in that direction and (as I’ve mentioned earlier), sweeping the lows and grabbing that liquidity strengthens a potential reversal on the markets significantly.”

Trader LP flagged overhead resistance making $72,000 a problematic hurdle to clear for bulls.

“Orderbook pressure showed strong buy pressure between 63–66K, which helped drive price toward the 70K region. However, sell pressure is now stepping in around 71–72K, acting as resistance and potentially capping price if it persists,” an X post read.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

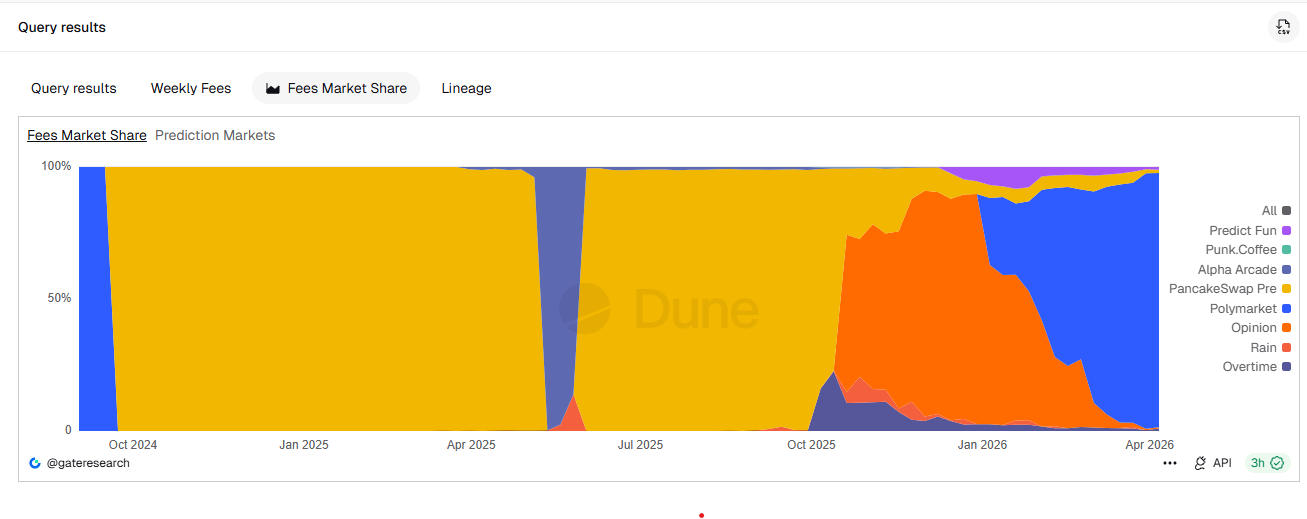

Polymarket has become one of decentralized finance’s most profitable protocols after a pricing overhaul, generating about $7.1 million in fees in the first week of the second quarter, according to new data.

That pace implies an annualized run rate of roughly $365 million if sustained, placing the onchain prediction platform among the industry’s top fee generators and giving it nearly all of the sector’s revenue, at 96.8% of onchain prediction market fees.

The gains follow a March 30 pricing change that pushed daily fees to around $1 million, a level that has largely held as trading activity remains elevated, data from DeFiLlama shows, and make Polymarket the eighth-largest DeFi protocol by fees, along with stablecoin issuers Circle (USDC) and Tether (USDT) and decentralized derivatives exchange Hyperliquid.

Onchain metrics also show Polymarket’s footprint beyond fees. Total value locked on the platform was over $432 million on Tuesday, according to DeFiLlama data, close to its November 2024 US election high of around $510 million, as its share of onchain prediction market revenue rises.

ICE backs Polymarket, but regulation uncertainty remains

Polymarket’s fee engine has started to attract more mainstream partners. Intercontinental Exchange, the owner of the New York Stock Exchange, deepened its bet on Polymarket on March 27, completing a $600 million cash investment as part of a broader $2 billion commitment that will see ICE distribute the platform’s event-driven data to institutional clients.

Related: Iran war bets turn prediction markets into real-time macro radar: Sygnum

At the infrastructure level, Polymarket announced Monday that it is replacing its bridged USDC.e collateral on Polygon with a new 1:1 USDC-backed token called Polymarket USD, which will take over as trading collateral as part of the platform’s April exchange upgrade, as it continues to spin up highly-traded markets on the US-Iran conflict, oil, inflation and equities indices.

Despite its growing revenue, regulation remains a risk. Prediction markets continue to face pushback from some US states and gambling regulators elsewhere, including recent moves by Hungary and Portugal to order local blocking, and Argentina issuing a countrywide block on Polymarket, arguing that the platform operates as an unlicensed gambling site.

Magazine: Bitcoin’s ‘biggest bull catalyst’ would be Saylor’s liquidation — Santiment founder

Iran US ceasefire deal update: Tehran exits peace talks

Drew Barrymore’s Makeover Segment Takes Emotional Turn

How ‘anti-Zionism’ corrupted the arts

-

NewsBeat5 days ago

NewsBeat5 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business5 days ago

Business5 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business2 days ago

Business2 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business3 days ago

Business3 days agoExpert Picks for Every Need

-

Sports3 days ago

Sports3 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business6 days ago

Business6 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Crypto World7 days ago

Crypto World7 days agoBitcoin enters the public bond market as Moody’s gives a first-of-its-kind crypto deal a rating

-

Business2 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Crypto World7 days ago

Bitcoin stalls below key resistance as technical signals skew bearish

-

Tech5 days ago

Tech5 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Politics7 days ago

Politics7 days agoStarmer’s centre has collapsed, and the left was right all along

-

Crypto World6 days ago

Crypto World6 days agoRipple rolls out enterprise crypto treasury platform for corporates

-

Fashion1 day ago

Fashion1 day agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Crypto World6 days ago

Crypto World6 days agoWhy It’s Partnering, Not Issuing

-

Crypto World7 days ago

AI Memory Rout Wipes 9% Off Nvidia Stock: Chart Says More Pain Ahead

-

Sports7 days ago

Sports7 days agoHow to teach yourself the perfect impact position with every club

-

Tech7 days ago

Tech7 days agoSolo Leveling: Ranking All Sung Jinwoo Shadows by Power

-

Tech6 days ago

Tech6 days agoDrawing Tablet Controls Laser In Real-Time

You must be logged in to post a comment Login