Crypto World

Stablecoin issuers get closer to U.S. federal rules with FDIC’s new proposal

The U.S. Federal Deposit Insurance Corp. formally proposed its approach to stablecoin issuers as one of the federal financial regulators required to write and oversee rules under last year’s Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act.

The FDIC’s proposal —meant to align closely with what its sister banking agency, the Office of the Comptroller of the Currency, proposed in February — will be open for a 60-day public comment period on the lengthy list of 144 questions posed Tuesday by the agency.

The FDIC’s job is to police U.S. depository institutions, and under the GENIUS Act, its role is to regulate such institutions issuing stablecoins from their subsidiaries. To that end, it posed capital, liquidity and custody standards for those firms, though the details won’t be set in stone until the rule is finalized — not likely to occur until the agency spends further months reviewing input and writing the final language. This is the second GENIUS Act proposal from the banking agency after its December pitch on the issuer application process.

As expected under the law, stablecoins won’t enjoy the deposit insurance that the banks maintain on traditional banking accounts, according to the proposal.

The OCC’s earlier proposal had a section that caused some initial concern among crypto policy experts wondering how the agency would allow for rewards programs managed by third-party stablecoin relationships, such as exchanges. In the same vein, the FDIC said that issuers wouldn’t be able to represent that their tokens pay interest or yield “simply for holding or using a payment stablecoin,” according to the staff presentation, including via arrangements with third parties. But crypto insiders have grown comfortable that properly tailored rewards programs shouldn’t run afoul of the rules.

The FDIC’s Tuesday proposal also suggested the capital that issuers will need to maintain to manage the risk of the business, plus “an operational backstop, separate from the capital requirement,” based on the previous year’s operating expenses.

The agency also addressed “the applicability of pass-through insurance to deposits held as reserves backing payment stablecoins,” proposing that “tokenized deposits that satisfy the statutory definition of ‘deposit’ would be treated no differently” than other deposits.

While the regulators work to implement GENIUS, some of its details are potentially already being overhauled by the work on the Senate’s Digital Asset Market Clarity Act. A clash between the banking and crypto industries over yield-bearing stablecoin holdings turned into a months-long debate that lawmakers have said they’re close to resolving, though the bill hasn’t yet advanced to a needed hearing. Congress comes back from a break later this week.

The OCC, FDIC and other agencies involved in implementing the rule, including the Treasury Department and the markets regulators, have few impediments in crafting regulations the way the Republican appointees want it. President Donald Trump’s White House has broken with past practice and declined to name any Democrat appointees to the many vacancies across the agencies, so there are no Democrats to raise objections to regulatory language.

But the GENIUS Act itself had drawn significant bipartisan support in both chambers of Congress when it was passed into law.

Read More: U.S. FDIC proposes first U.S. stablecoin rule to emerge from GENIUS Act

According to the bureau, a large number of minors aged 17 and younger were included in complaints related to crypto or crypto ATMs, resulting in more than $5 million in losses.

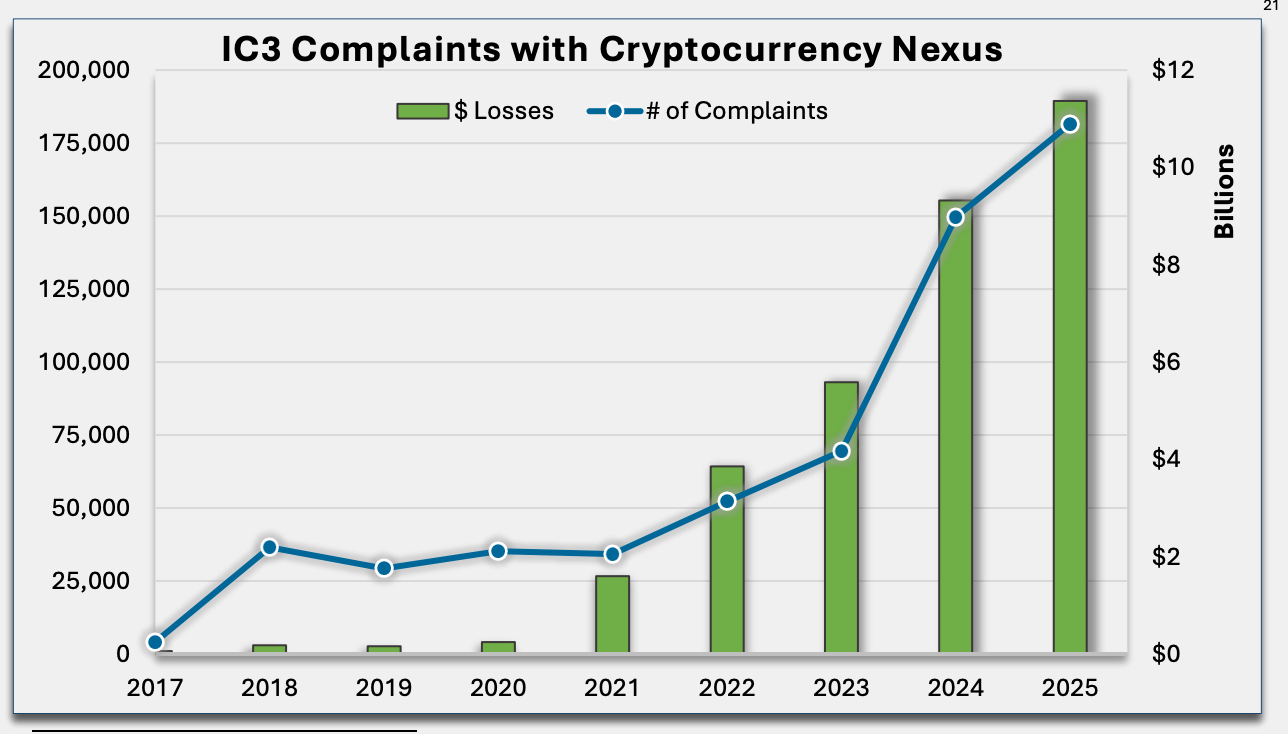

The US Federal Bureau of Investigation (FBI) reported that Americans’ losses from crypto-related scams increased to more than $11 million in 2025.

In its annual internet crime complaint report released on Monday, the FBI said that cryptocurrency and AI-related scams were “among the costliest” for Americans in 2025, with 181,565 complaints totaling more than $11 billion. According to the bureau, it received more than one million complaints in 2025 reporting losses of about $21 million due to cyber-enabled crimes.

The FBI’s Internet Crime Complaint Center reported that investment scams resulted in the highest percentage of victims reporting losses in crypto as opposed to cash, debit cards, gift cards and other media of exchange. In addition, about 10% of the 13,168 complaints involving cybercrimes targeting minors aged 17 and younger were related to crypto or crypto ATMs, resulting in more than $5 million in losses.

The complaints the FBI received were despite the bureau’s efforts to “identify and notify people who are currently falling victim to cryptocurrency investment fraud” through its Operation Level Up in 2024. Globally, blockchain analytics platform Chainalysis reported in March that illicit addresses received $154 billion in 2025, driven in part by sanctions evasions.

Related: Cambodian lawmakers propose severe prison time for crypto scammers

Scammers use Tron blockchain token to con users using FBI

According to the FBI report, there were 32,424 complaints involved in impersonation of government officials, resulting in about $800 million in losses. However, the report did not mention bureau officials issuing a March notice warning Americans that a token on the Tron blockchain was impersonating the FBI with the goal of obtaining personal information.

Tron users reported receiving a token with the FBI logo claiming that their wallet was “under investigation.” The users were then prompted to enter personal information under the guise of an FBI anti-money-laundering verification to avoid their accounts being frozen.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

A fresh wave of online backlash is now building around Pakistan’s request to extend Trump’s Iran deadline, with users questioning whether the move was genuinely independent.

The speculation centers on the edit history of Prime Minister Shehbaz Sharif’s post on X. History shows an earlier version of the message, followed by a more detailed “draft” version that explicitly calls for a two-week extension and reopening of the Strait of Hormuz.

Some users claim this suggests coordination behind the scenes. The theory is simple: if the US agrees to extend the deadline, framing it as a response to Pakistan’s request allows Washington to avoid appearing to back down under pressure.

There is no evidence supporting this claim. Neither the White House nor Pakistani officials have indicated any coordinated messaging strategy.

Still, the timing has fueled suspicion. The post appeared just hours before Trump’s deadline, as negotiations intensified and markets reacted sharply.

In volatile geopolitical moments like this, narratives form quickly. Right now, this one is being driven by inference, not confirmation.

The post Internet Questions Pakistan’s Role in Trump’s Iran Deadline Twist appeared first on BeInCrypto.

TLDR

- Charles Schwab outlines two approaches for integrating cryptocurrencies into investment portfolios.

- The return-based approach focuses on expected returns, volatility, and asset correlations.

- Schwab recommends modest allocations to bitcoin and ether based on expected returns.

- The risk-based approach focuses on managing overall portfolio risk from crypto exposure.

- Schwab warns that even small allocations to crypto can significantly raise portfolio risk.

Charles Schwab, the leading U.S. brokerage firm managing over $12 trillion in assets, recently outlined two approaches for integrating cryptocurrencies into investment portfolios. The firm emphasized that while there is no fixed method for crypto allocations, investors should carefully consider their risk tolerance and long-term objectives. Schwab’s research highlights the potential for diversification, though it warns that even small allocations to crypto can significantly increase portfolio risk.

Return-Based Approach to Crypto Investments

In its white paper, Charles Schwab detailed a return-based approach to crypto investing, which is rooted in expected returns. This method examines the anticipated returns, volatility, and correlations with traditional assets like stocks and bonds. Schwab suggests that if investors expect a return of 15% per year from Bitcoin, a conservative portfolio might allocate around 1%, while a more aggressive one could allocate up to 8.8%.

The firm noted that ether, due to its higher volatility, would warrant smaller allocations. For example, a conservative portfolio might allocate just 0.1% to ether, while a more aggressive portfolio might allocate up to 2.5%. Schwab also stressed that if returns for either bitcoin or ether fall below 10%, it might not justify any allocation, even for more risk-tolerant investors.

Risk-Based Approach to Crypto Exposure

Charles Schwab also presented a risk-based approach to crypto allocation, where the focus shifts from returns to managing overall portfolio risk. In this approach, the crypto exposure is determined by the amount of total portfolio risk that comes from cryptocurrencies. For instance, in a conservative portfolio, a 1.2% allocation to bitcoin or 0.9% to ether could represent 10% of the total portfolio risk.

For moderate to aggressive portfolios, Schwab suggests allocating up to 4% in bitcoin and nearly 3% in ether to achieve similar risk levels. Schwab explained that this risk-based method is particularly useful for investors who want to understand how crypto fits into their broader asset mix. While crypto may offer diversification benefits, Schwab cautioned that increasing exposure comes with heightened portfolio concentration risk.

Charles Schwab’s Crypto Exposure Options

As Schwab moves forward with its new crypto offering, Schwab Crypto, it has also been providing exposure through various products like crypto-related stocks and exchange-traded products. Schwab has introduced a waitlist for clients interested in buying and selling bitcoin and ether directly. For now, the brokerage firm offers crypto exposure through over-the-counter trusts and futures for approved clients.

Despite initially dismissing cryptocurrencies as “purely speculative” in 2019, Schwab has evolved its stance on digital assets over time. The firm now encourages investors to carefully evaluate the role that crypto could play in their portfolios, keeping in mind the elevated risks associated with even a small allocation.

Crypto World

Next Crypto to Explode as Bitcoin Stands Firm Above $68K and Solana ETFs Hold $1.5 Billion, but Pepeto Is the Entry That Defines This Cycle

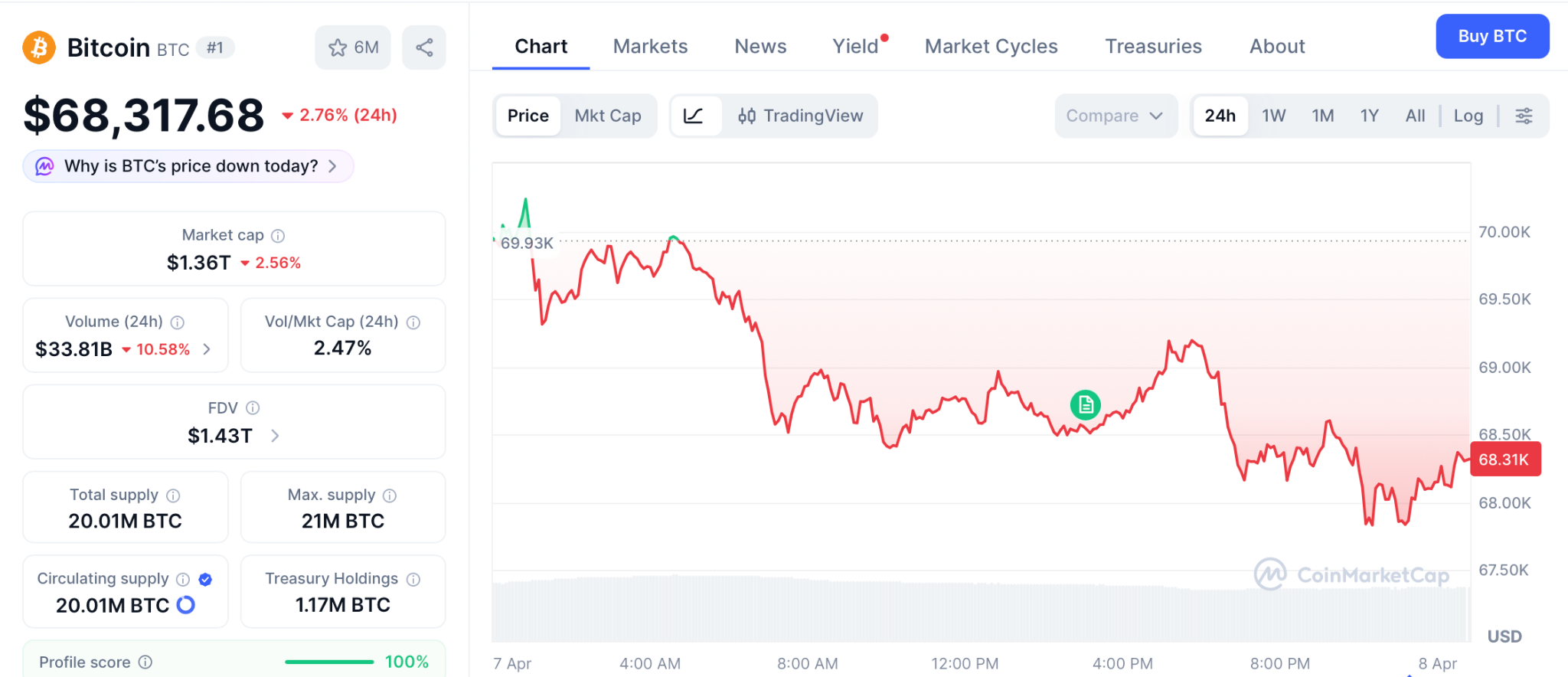

The crypto market is heating up, and the prices sitting in front of you right now will not be here when the rally kicks in. Bitcoin held $68,317 on April 7 after Iran rejected the ceasefire, per CoinDesk, and Solana ETFs kept $1.5 billion in total inflows despite SOL crashing 57% from its peak. Every indicator that marks the start of a rally is lighting up.

But the next crypto to explode is never the coin everybody already holds at a trillion-dollar valuation. It is the presale where listing day creates the gain and exchange revenue locks it in. Here is which one ticks every requirement.

Bitcoin sat at $68,317 on April 7 after absorbing Iran.s ceasefire rejection, per CoinDesk, while BTC ETFs pulled $471 million on April 6. The Fear and Greed Index sits at 9, and altcoins bounced broadly.

The market is shifting bullish, and the traders who connect those dots are searching for the breakout alt at presale cost before the listing turns cheap entries into the bags everybody else spends the cycle regretting.

The Next Crypto to Explode Sits Below the Rally While Large Caps Grind

Pepeto: Revenue Sharing That Pays From Every Trade, at a Price the Bull Market Will Erase

Bull runs pay the people who bought during panic. The wallets that loaded Pepeto during the crash are now watching the market prove them right. Revenue sharing gives every presale holder a lasting share of trading fees based on position size, confirmed by Business Insider. BTC, SOL, and XRP generate zero income for holders. Pepeto earns on every single transaction.

SolidProof cleared the contract before the presale opened, and a former Binance executive is leading the listing plan for the exchange with its cross-chain bridge, zero-cost swaps, and token risk scoring. The $8.82 million raised came from wallets that checked every alternative and picked this one. The founder who took the original Pepe coin to $7 billion is channeling that same viral pull into tools that generate actual revenue.

At $0.0000001863, the gap between presale and listing gives a floor that no large cap can offer. 186% APY staking adds to your position while the listing gets closer, but that is just the extra.

The real payoff comes when a revenue-earning exchange token hits live bull market trading, and every bag at this price turns into supply that post-listing buyers have to purchase from you. The next crypto to explode door is closing quicker than anyone expects.

Solana: $1.5 Billion in ETF Inflows but SOL Stuck at $79

SOL trades near $79 with $1.5 billion in cumulative ETF capital proving institutional belief even as the price dropped 57% from its high, per CoinGecko. A break above $86 could push toward $100 as the broader market builds.

Strong base, but from $79 the upside is capped for anyone searching for the next crypto to explode that transforms a portfolio.

Bitcoin: Holding $68K With $80,000 as the Next Major Target

BTC held $68,317 on April 7 per CoinMarketCap and $74,500 is the final resistance before a clean run to $80,000. The $471 million in ETF capital on April 6 proves institutional appetite, and analysts keep their sights above $150,000 by December 2026.

Bitcoin is out front with clear strength, but the next crypto to explode requires numbers that go past what a $1.3 trillion coin can deliver.

The Bull Market Is Here and the Entry That Defines It Is Still Open

Step back and the whole picture becomes clear. The market tips bullish, Bitcoin refuses to break, institutions keep arriving, and Pepeto is sitting in the setup that appears once per cycle: permanent revenue sharing, SolidProof audit, a founder who generated $7 billion in demand, and exchange tools the Binance listing switches on.

Every massive crypto winner follows one pattern: a few wallets entered first, everyone else found out after, and the cheap price was gone. That sequence is playing out right now, and once the listing drops the presale cost disappears forever. Visit the Pepeto official website and make the move that puts you on the side that caught this cycle instead of the side that watched it happen. The next crypto to explode never waits for the crowd to agree, it moves while they debate, and Pepeto at $0.0000001863 is already moving.

Click To Visit Pepeto Website To Enter The Presale

FAQs

Why is the crypto market turning bullish right now?

Bitcoin held $68,317 after Iran rejected ceasefire, ETFs pulled $471 million on April 6, and Fear and Greed at 9 historically marks the bottom before major rallies.

Where can I find the next crypto to explode before listing?

Visit the Pepeto official website at $0.0000001863 with 186% APY staking and exchange tools ready for bull market volume.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The latest AI news artificial intelligence US military Iran war 2026 debate has crystallized around one figure: in the first 24 hours of Operation Epic Fury on February 28, the US military struck more than 1,000 targets in Iran using Palantir’s Maven Smart System with Anthropic’s Claude embedded inside it — a pace CENTCOM head Admiral Brad Cooper confirmed publicly, and one that human rights experts say has raised serious questions about AI-assisted targeting and civilian harm.

Summary

- CENTCOM Commander Admiral Brad Cooper confirmed in a March 11 video statement that US forces are “leveraging a variety of advanced AI tools” that allow commanders to make decisions “faster than the enemy can react,” with tasks that previously took hours or days now completed in seconds

- Palantir’s Maven Smart System with Anthropic’s Claude embedded processes satellite imagery, drone feeds, radar data, and signals intelligence into prioritized target lists with GPS coordinates, weapons recommendations, and automated legal justifications — what previously required roughly 2,000 intelligence analysts now reportedly requires approximately 20

- A US strike on a girls’ elementary school in Minab killed over 165 civilians, according to Iranian reports; the Pentagon is investigating whether the school was on an AI-assisted target list, and more than 120 House Democrats have demanded answers

The latest AI news artificial intelligence US military Iran war 2026 story is both a technological milestone and a humanitarian reckoning. According to IBTimes, more than 1,000 targets were struck in the first 24 hours of Operation Epic Fury on February 28 — more than double the air power deployed during the entire opening phase of the 2003 Iraq invasion. That pace is only possible with AI. A human-led targeting process would have required thousands of analysts working for weeks to generate and validate that many aim points.

The system at the center of it is Palantir’s Maven Smart System, running on Anthropic’s Claude large language model. Maven fuses classified feeds from satellites, surveillance drones, and archived intelligence into a unified platform. Claude synthesizes that information into prioritized target lists, complete with precise GPS coordinates, weapons recommendations, and automated legal justifications for strikes.

Admiral Brad Cooper confirmed the AI role in a publicly released video statement: “These systems help us sift through vast amounts of data in seconds so our leaders can cut through the noise and make smarter decisions faster than the enemy can react. Humans will always make final decisions on what to shoot and what not to shoot and when to shoot. But advanced AI tools can turn processes that used to take hours and sometimes even days into seconds.”

Cooper did not identify specific AI systems by name. What the statement left unaddressed was Maven’s reported accuracy rate: approximately 60%, compared with 84% for human analysts in some assessments.

The School Strike and the Accountability Gap

The most serious accountability question surrounds a US strike on the Shajareh Tayyebeh girls’ elementary school in Minab that killed over 165 civilians. The school was reportedly on a target list generated with AI assistance. Pentagon officials said outdated intelligence contributed to the strike and a full investigation is underway. More than 120 House Democrats have formally demanded answers about AI’s role. As warfare expert Craig Jones told Democracy Now!, AI targeting is “reducing a massive human workload of tens of thousands of hours into seconds and minutes” — but “automating human-made targeting decisions in ways which open up all kinds of problematic legal, ethical and political questions.”

The conflict carries direct implications for commercial tech. Iran has explicitly named Palantir, Google, Microsoft, Amazon, and other US companies as legitimate military targets because of their infrastructure’s role in the war. Iranian strikes have already damaged AWS data centers in the UAE and Bahrain. As crypto.news reported, Iran has demonstrated willingness to strike economic and technology infrastructure across the Gulf — a threat that now extends to the commercial cloud backbone powering US AI military systems.

What the Iran war has confirmed, as analysts have begun calling it “the first AI war,” is that commercial AI and warfare are no longer separate domains. As crypto.news noted, every escalation in this conflict reaches financial markets within hours. The AI targeting dimension adds a new layer of systemic risk: not just military escalation, but the weaponization of commercial technology infrastructure itself.

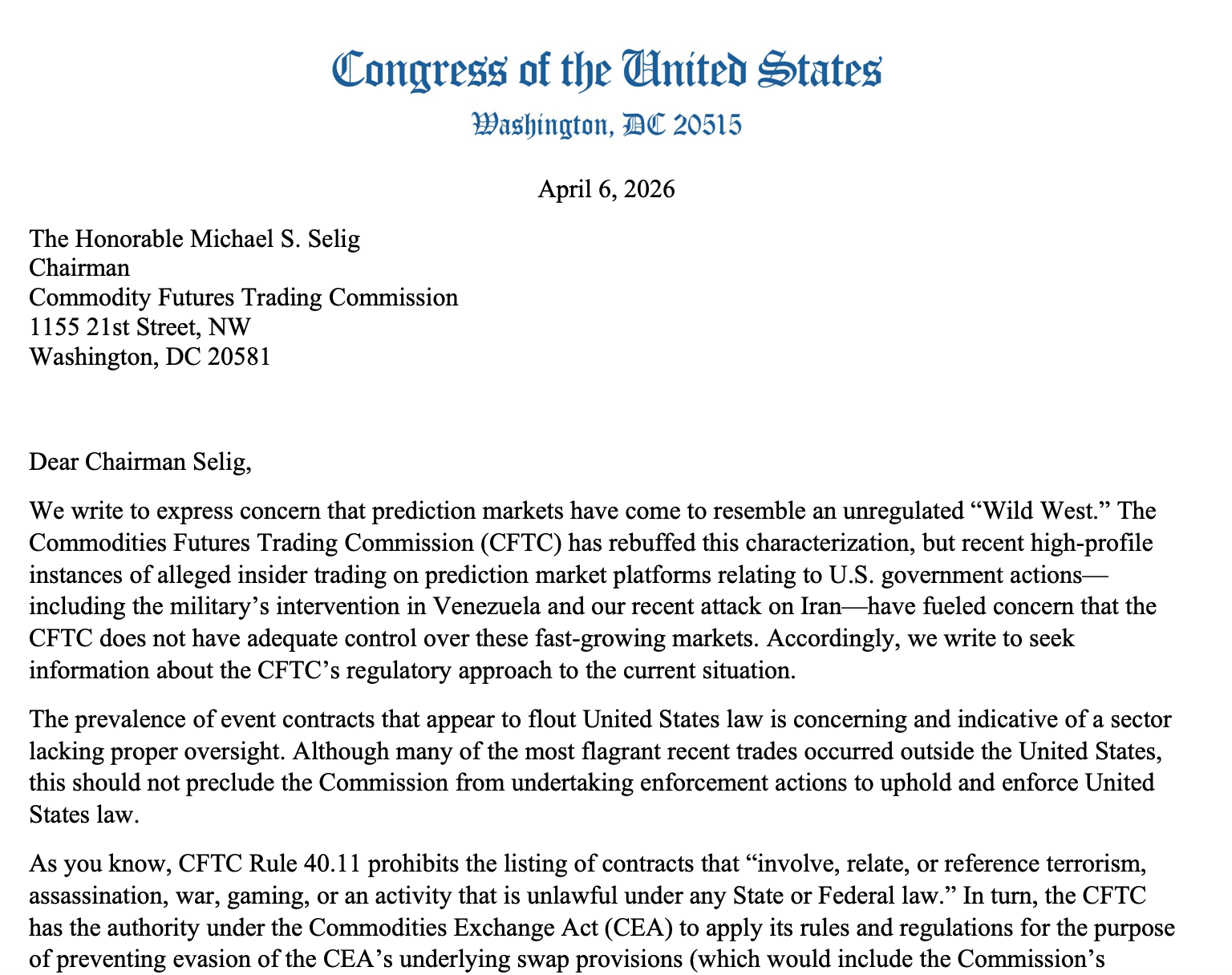

The seven House members may have affirmed the commission‘s authority over prediction markets, but asked questions about its inaction on insider trading.

Seven members of the US House of Representatives sent a letter to Commodity Futures Trading Commission (CFTC) Chair Michael Selig, asking for information on the agency’s inaction on insider trading on prediction markets and event contracts related to war and conflicts.

In a Monday letter, the seven US lawmakers said that the CFTC had the authority under the Commodities Exchange Act “to apply its rules and regulations for the purpose of preventing evasion of the [act’s] underlying swap provisions.” The statement signaled that the representatives affirmed Selig’s position that the commission had jurisdiction over prediction markets.

However, the House members expressed concerns about how the CFTC was policing “morally obscene” event contracts, including those on US military actions in Iran and Venezuela — in those cases, there were suspicious trades related to the timing and outcomes of US military involvement.

“Such corrupt trades deserve swift and decisive oversight,” said the letter. “Allowing these contracts to persist raises troubling concerns about the Commission’s desire and capacity to fulfill a global regulatory role.”

The legal battles over regulating prediction market platforms like Kalshi and Polymarket are being waged both at a federal and state level. Several US state gaming authorities have filed lawsuits alleging that the companies are illegally offering sports bets, while the CFTC, under Selig, claims that the event contracts on the platform amount to swaps and fall under its federal regulations.

The seven House members requested that Selig respond to their six questions by April 15.

Related: Polymarket bags 97% of onchain prediction market fees after pricing overhaul

In one of the most recent legal decisions, the US Court of Appeals for the Third Circuit affirmed a lower court ruling blocking New Jersey gaming authorities from filing enforcement actions against Kalshi. Two out of three circuit judges said that the company had a ”reasonable chance of success” in arguing that federal commodities laws preempted state authorities.

CFTC enforcement director says agency is “watching” for insider trading

The Monday letter followed CFTC enforcement director David Miller responding to concerns over insider trading, which has also resulted in legislation proposed by Democrats. According to Miller, the commission would only prosecute instances “against those who tip or trade with misappropriated information,” but not dedicate resources to “trivial” cases.

Magazine: All 21 million Bitcoin is at risk from quantum computers

TLDR

- Anthropic unveiled its new AI model, Claude Mythos, designed to enhance cybersecurity by identifying high-severity vulnerabilities in systems.

- The Mythos model has already detected thousands of flaws across major operating systems and web browsers.

- Anthropic launched Project Glasswing, a partner program offering select organizations early access to the Mythos model for defensive tasks.

- The company committed up to $100 million in usage credits and $4 million in donations to support open-source security initiatives.

- Anthropic decided not to release the Mythos model widely, citing the need for further safeguards to ensure its safe deployment.

Anthropic introduced its latest AI model, Claude Mythos Preview, on Tuesday, focusing on cybersecurity. The model aims to strengthen defenses against cyber threats by identifying vulnerabilities and developing exploits with little human oversight. This move comes weeks after a security lapse exposed Claude’s code, which drew significant attention to Anthropic’s internal security measures.

New AI Model Targets Cybersecurity Threats

Claude Mythos Preview represents Anthropic’s cutting-edge effort in cybersecurity, designed to uncover high-severity vulnerabilities. In its testing, Mythos has already identified thousands of flaws across major systems, including operating systems and web browsers. According to the company, this new model aims to equip defenders with advanced tools before cyber attackers can harness similar AI capabilities.

Project Glasswing, a partner program, was also announced alongside the Mythos model. It offers early access to the new AI system for select companies like AWS, Google, and Microsoft, among others. More than 40 organizations will be part of the initiative, with Anthropic committing up to $100 million in usage credits to support the program.

Anthropic Pushes for Secure Deployment

Despite Mythos’s promising capabilities, Anthropic has decided against a wide release. The company emphasized the need for further safeguards before deploying Mythos at scale. “Our goal is to ensure that this powerful tool can be deployed safely and responsibly,” an Anthropic representative stated.

This caution follows a mishap earlier this year when a packaging error exposed Claude’s code. The incident led to the accidental release of over 500,000 lines of code, causing a significant security breach. Anthropic’s attempt to take down the leaked files further escalated the issue, as it mistakenly removed thousands of GitHub repositories.

Large-Scale Support for Cybersecurity Defenders

Project Glasswing’s partner organizations will be among the first to test Claude Mythos. These partners include some of the largest players in technology and infrastructure, with the Linux Foundation and Palo Alto Networks joining the program. The initiative aims to harness Mythos’s ability to identify and exploit vulnerabilities while prioritizing the security of its deployment.

Along with the partner program, Anthropic has pledged $4 million in donations to open-source security groups. The company’s focus on supporting cybersecurity initiatives highlights its commitment to safeguarding against advanced cyber threats. However, Mythos’s future remains uncertain, as Anthropic continues to refine its defensive capabilities before making the model more widely available.

The development of Mythos marks a significant step in the AI-driven defense against cybersecurity risks, though Anthropic remains cautious about its broader use.

Three suspects in a crypto wrench attack ring have been charged, according to reporting from the San Francisco Chronicle.

According to the reporting, the three men have been charged in two specific crimes, but police believe that they’re part of a larger operation and are tied to several similar crimes.

The criminals apparently used a similar technique for these crimes, namely:

- Identifying a major cryptocurrency holder.

- Researching and surveilling that cryptocurrency holder. A detective who spoke to the Chronicle described this, saying, “They figure out your trends, your life cycle, what do you normally order online, What do you normally order for takeout?”

- The criminals attempt to gain access to accounts; in the case of one victim who spoke to the Chronicle, “for me, it was my DoorDash and Uber Eats accounts.”

- The criminals would then create a fake delivery, meet the victim at the door, and then threaten them.

Wrench attacks are inherent risk

Cryptocurrency’s censorship-resistant transfers as well as its pseudonymous nature make holders an attractive target for these types of attacks.

These attacks that don’t try to bypass the cryptographic security that protects the assets but use threats and violence to influence the person who has access to the keys.

Indeed, kidnappings and extortion have become an international problem for cryptocurrency holders and firms.

Read more: French crypto tax firm targeted in ShinyHunters extortion attempt

These attacks have included French firm Waltio and UK-based Sillytuna.

France has become something of a leader when it comes to this type of activity, with even Ledger co-founder David Balland targeted.

The utility of cryptocurrency for this type of attack has resulted in even non-cryptocurrency holders having ransoms demanded in bitcoin (BTC). Prominently, Nancy Guthrie, the mother of TODAY Show host Savannah Guthrie, has been kidnapped and her apparent kidnappers have sought the ransom in BTC.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

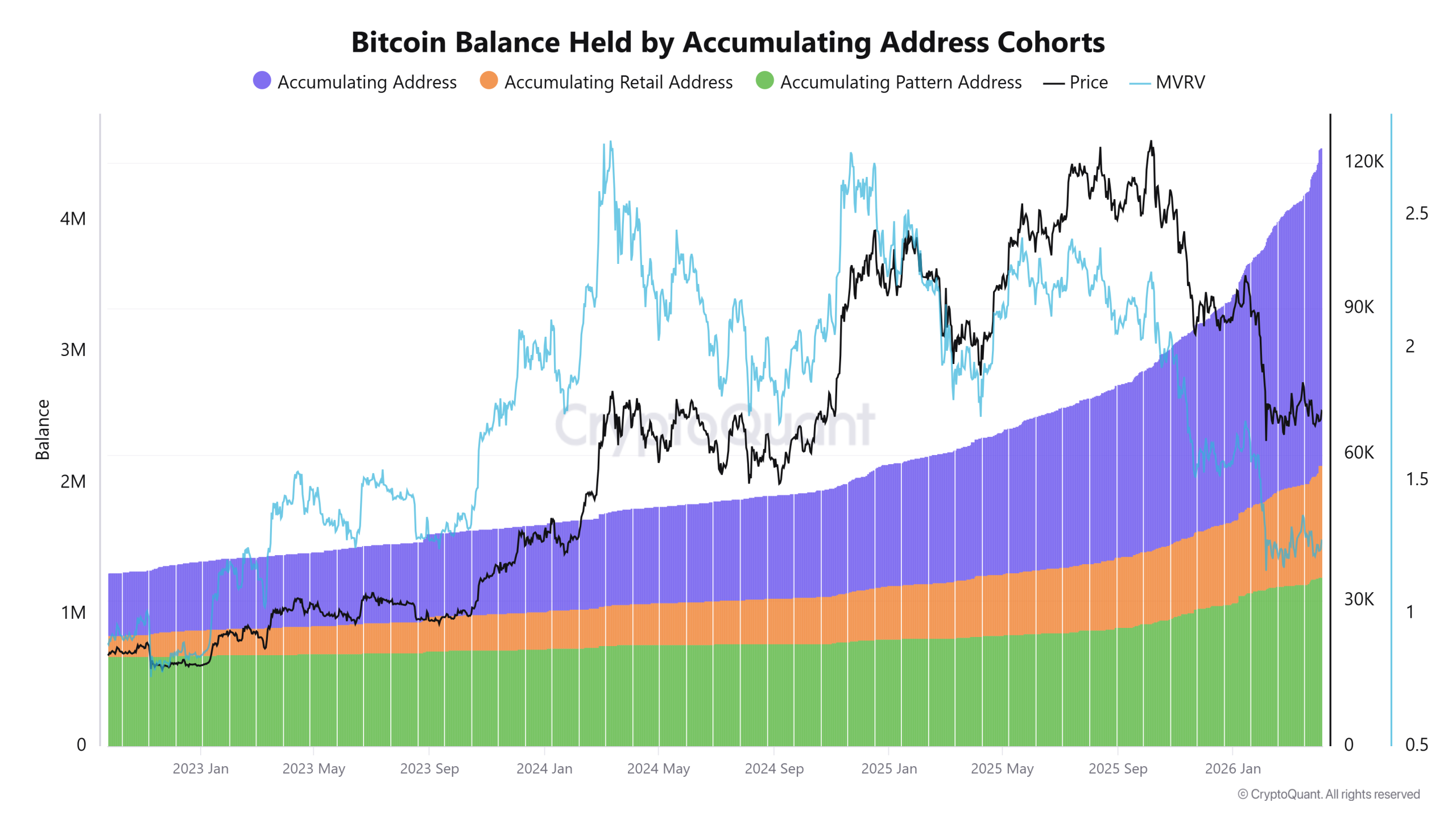

New data suggests that Bitcoin (BTC) could be moving closer to a bull market phase as its supply slowly shifts back into long-term, retail-investor-linked wallets. The figure surpassed 4 million BTC in Q1 2026.

The accumulation trend aligns with a rise in Bitcoin network activity index to levels last seen in April 2025, signaling a return of stronger network activity.

Bitcoin long-term wallets expand holdings

CryptoQuant data shows that balances held by accumulating address cohorts continued to rise into Q1 2026. The total BTC held by these cohorts has crossed 4.37 million BTC as of April 7, up from about 2 million BTC in early 2024, signaling sustained supply absorption.

The retail-investor-linked accumulation addresses added roughly 857,000 BTC, while the accumulating pattern wallets, defined as addresses that steadily add BTC at recurring intervals with minimal outflows, expanded to 1.29 million BTC.

This growth occurred while the price remained capped below $70,000 throughout the first quarter of 2026.

In contrast, the inflows from centralized exchanges and highly active addresses have slowed. During the 2023–2024 expansion phases, the inflows often exceeded 1.2 million to 1.5 million BTC. The recent activity has averaged 300,000 to 350,000 BTC.

The divergence shows a shift in coin distribution. More BTC is moving into long-term wallets, while fewer coins are circulating on the exchanges. This indicates a tightening of the liquid supply and a reduction in short-term trading turnover.

Related: Bitcoin holds $67K support as data exposes price to sentiment divergence

Bitcoin network activity index highlights the trend

The CryptoQuant Bitcoin network activity index has climbed to 3,600 from 3,320 on March 22. The index aggregates broader usage signals, including transaction counts and network throughput.

As observed in the chart, it has moved above its 365-day moving average for the first time since December 2024 and entered the “bull-phase” classification for the first time since April 2025.

In parallel, Bitcoin’s active addresses momentum dropped to -0.25 on April 6, the lowest reading since April 2018. The metric tracks the rate of change in active addresses, with negative values pointing to declining user participation.

The low activity levels have persisted since July 2025, echoing a similar stretch in 2024 that preceded a 35% price decline.

According to crypto analyst Gaah, the drop in activity signals the absence of short-term participants, or “tourists.” The network usage is now dominated by long-term holders focused on accumulation.

Historically, low readings have aligned with profitable accumulation phases. The reduced activity often coincides with lower sell pressure as the coins move into long-term wallets.

Related: Bitcoin’s quantum challenges are ‘more social than technical’: Grayscale

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

U.S. spot Bitcoin exchange-traded funds (ETFs) experienced substantial inflows at the beginning of the week, marking the strongest single-day performance in over six weeks. On Monday, Bitcoin ETFs attracted $471.3 million in net inflows. This surge reversed the previous month’s outflows and underscored renewed investor interest.

The strong inflows on Monday were primarily driven by BlackRock and Fidelity. Other prominent funds, including Ark 21Shares, Grayscale, Bitwise, and VanEck, also contributed to the influx. The total inflow for Bitcoin ETFs represents the highest daily intake since late February, signaling a potential shift in market sentiment.

The positive momentum in Bitcoin-related assets has injected optimism into the market. The latest data indicates that spot Ethereum products also saw significant inflows. While uncertainty remains due to broader macroeconomic conditions, the trend could support further upside potential for Bitcoin.

BlackRock and Fidelity Lead the Charge

BlackRock’s Bitcoin ETF, IBIT, led the pack with $181.9 million in inflows on Monday. Fidelity’s FBTC followed with $147.3 million, securing a significant portion of the daily total. Together, these two funds accounted for more than half of the day’s inflows, signaling the strength of institutional support for Bitcoin.

ARK Invest and 21Shares’ ARKB also contributed meaningfully, with $118.7 million in inflows. These funds, which focus on offering innovative financial products, are benefiting from growing interest in cryptocurrency investments. Their substantial contributions reflect the continued expansion of Bitcoin’s presence in the mainstream financial ecosystem.

This surge in investments coincides with the release of positive market data and could further bolster Bitcoin’s price performance. As the leading players in the ETF space continue to drive interest, the momentum for Bitcoin is expected to continue. Analysts predict that this trend could propel Bitcoin past its current trading range if the macroeconomic climate stabilizes.

Spot Ethereum Products See Uptick

Ethereum ETFs also experienced a surge in demand on Monday, with $120.2 million in inflows. This marked the highest single-day net inflow since mid-March. The increase highlights growing investor interest in Ethereum as an alternative to Bitcoin.

Ethereum’s price has faced increased volatility in recent months, but these inflows signal a resurgence of confidence. Investors appear to be looking at Ethereum as a strong performer amid the broader cryptocurrency market’s rally. The combination of rising interest in both Bitcoin and Ethereum products could be a sign of a broader recovery in the digital asset space.

However, macroeconomic challenges, such as ongoing geopolitical tensions and economic uncertainty, continue to loom over the market. If these external pressures ease, it could further fuel positive sentiment for cryptocurrencies like Bitcoin and Ethereum.

Prime Video’s Most Brutal Sci-Fi Series Is Dominating the Top 10 Before Its Final Season

I’m a Celebrity South Africa viewers issue same plea over campmate’s behaviour

Leifheit Aktiengesellschaft 2025 Q4 – Results – Earnings Call Presentation (OTCMKTS:LFHTF) 2026-04-07

-

NewsBeat5 days ago

NewsBeat5 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business5 days ago

Business5 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business2 days ago

Business2 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business4 days ago

Business4 days agoExpert Picks for Every Need

-

Sports3 days ago

Sports3 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business6 days ago

Business6 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech2 hours ago

Tech2 hours agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business3 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Crypto World7 days ago

Bitcoin stalls below key resistance as technical signals skew bearish

-

Tech5 days ago

Tech5 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Politics7 days ago

Politics7 days agoStarmer’s centre has collapsed, and the left was right all along

-

Crypto World6 days ago

Crypto World6 days agoRipple rolls out enterprise crypto treasury platform for corporates

-

Fashion2 days ago

Fashion2 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Crypto World6 days ago

Crypto World6 days agoWhy It’s Partnering, Not Issuing

-

Tech6 days ago

Tech6 days agoDrawing Tablet Controls Laser In Real-Time

-

Business3 days ago

Business3 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Tech7 days ago

Tech7 days agoSolo Leveling: Ranking All Sung Jinwoo Shadows by Power

-

Sports6 days ago

Tom Pelissero Drives the Final Nail in the Coffin

You must be logged in to post a comment Login