Crypto World

Truist Financial (TFC) Stock Climbs on Strong Q1 Performance with EPS Jump and Loan Portfolio Expansion

Key Highlights

-

TFC shares rally 3.7% following robust Q1 performance with earnings growth and expanding loan book

-

First quarter delivers elevated EPS, consistent revenue generation, and enhanced capital position

-

Truist achieves positive momentum with rising profitability and continued balance sheet expansion

-

Financial institution demonstrates enhanced operational efficiency alongside stable deposit base

-

Quarterly performance showcases EPS advancement while maintaining consistent credit metrics

Truist Financial (TFC) advanced to $51.26, posting a 3.70% increase following the release of first-quarter financial results that demonstrated profitability improvements and ongoing lending growth. The banking institution generated $5.15 billion in total revenue, marking a 5.2% year-over-year increase, while earnings per share climbed to $1.09 compared with $0.87 in the prior-year period. The quarterly report underscored operational consistency, expense management discipline, and maintained financial strength.

Truist Financial Corporation, TFC

Profitability Advancement and Revenue Performance

Truist delivered net income attributable to common shareholders totaling $1.38 billion, demonstrating ongoing profitability momentum. Diluted earnings per share advanced to $1.09, driven by enhanced operational productivity and diversified income generation. The institution achieved a 13.8% return on tangible common equity, showcasing productive capital deployment.

Total revenue experienced a marginal sequential decline while maintaining year-over-year growth momentum. Net interest income totaled $3.60 billion, reflecting moderate sequential headwinds associated with shifts in deposit composition. Noninterest income remained stable at $1.55 billion, benefiting from heightened trading volumes and investment banking contributions.

The efficiency ratio declined to 57.9%, demonstrating enhanced cost management throughout the period. Expense reductions across staffing and professional service categories drove the overall cost decrease. Consequently, pre-provision net revenue exhibited strength, validating the bank’s operational execution.

Lending Portfolio Growth and Financial Position Enhancement

Truist grew its lending operations, with average loans and leases climbing to $327 billion throughout the quarter. Commercial lending segments drove the majority of growth, while consumer portfolios experienced modest contraction. Period-end loans totaled $329.2 billion, demonstrating sustained yet measured expansion.

The deposit base exhibited consistent growth, with average deposits ascending to $399 billion. Period-end deposits reached $404.1 billion, illustrating stable funding dynamics. Declining deposit costs also enhanced margins, with the average deposit cost decreasing to 1.55%.

Average earning assets expanded to $486.35 billion, reflecting incremental balance sheet progression. The loan yield compressed to 5.71%, influenced by repricing trends within the prevailing interest rate landscape. Reduced borrowing expenses and an optimized funding composition helped mitigate margin compression.

Credit Metrics and Financial Strength Remain Resilient

Truist preserved consistent credit quality, with net charge-offs registering 0.61% during the period. Nonperforming assets decreased to $1.79 billion, signaling managed credit exposure. Nonaccrual loans similarly declined to $1.72 billion, reinforcing overall portfolio consistency.

The allowance for loan losses maintained stability, with the ALLL ratio holding steady at 1.53%. Loans delinquent beyond 90 days remained flat, confirming consistent credit performance. These indicators reflected prudent risk oversight across lending operations.

Capital metrics remained robust, with the CET1 ratio maintaining a 10.8% level. The Tier 1 capital ratio achieved 11.9%, while the Tier 1 leverage ratio registered 9.9%. The company executed $1.1 billion in share repurchases, reinforcing shareholder returns and financial position strength.

Truist produced a well-rounded quarterly performance, merging profitability growth, expense discipline, and consistent lending expansion. Despite modest margin headwinds, the stable deposit base and solid capital foundation underpinned continued operational durability.

Roland Lescure, France’s finance minister, backed an initiative by European banks to launch a euro-pegged stablecoin in 2026 to compete with US dollar-backed tokens, which currently dominate the market.

According to a Friday Reuters report, Lescure supported the euro-pegged Qivalis stablecoin plan launched in September 2025 by EU banks, including Dutch lender ING and Italy’s UniCredit.

The goal of the banks was to create a stablecoin in compliance with the EU’s Markets in Crypto Assets (MiCA) regulatory framework; the MiCA-compliant euro stablecoin is expected to be launched in the second half of 2026.

“That is what we need, and that is what we want,” said Lescure, according to Reuters. “I also strongly encourage banks to further explore the launch of tokenized deposits.”

EU banks are collaborating to create an alternative to the US-dominated stablecoin market, led by Tether’s USDt (USDT) and Circle’s USDC (USDC). As of Friday, USDT had a market capitalization of about $186 billion, according to CoinMarketCap.

Related: SocGen brings MiCA-compliant USDCV dollar stablecoin to MetaMask

Lescure, who reportedly made the comments in a pre-recorded message, said the relatively small volume of euro-pegged stablecoins compared to dollar-pegged ones was “not satisfactory.”

Speaking at the World Economic Forum in January, Banque de France Governor François Villeroy de Galhau said that tokenization and stablecoins were likely to be “the name of the game” in 2026, highlighting benefits of blockchain infrastructure for finance.

However, he opposed interest-bearing stablecoins, claiming that they could destabilize financial systems, a criticism shared by several EU and US policy makers, as well as central bank officials, as stablecoin yield continues to be a contentious regulatory topic.

Stablecoin yield is still an issue in US market structure talks

As of Friday, lawmakers in the US Senate had not announced any compromise that would allow a crypto market structure bill to move closer to a vote.

The CLARITY Act, a crypto market structure bill that passed in the US House of Representatives in July, has been stalled amid disagreements on how to address stablecoin yield, tokenized equities, ethics and other concerns.

Singapore Gulf Bank (SGB) has introduced a service that lets institutional clients mint and redeem stablecoins directly from their bank accounts, using the Solana layer-1 blockchain network to enable round-the-clock settlement between fiat and digital assets.

The service will initially support Circle USDC (USDC) transactions above $100,000 and includes temporary fee waivers for minting and redemption on the Solana network, according to SGB’s announcement.

Additional assets such as Tether’s USDT (USDT), Ethena’s USDe (USDe) and Global Dollar (USDG) are expected to follow, the company said.

The new feature is integrated into the bank’s internal clearing system, allowing funds to move between onchain and traditional balances without relying on intermediary banking networks, SGB said.

The launch comes as payment networks, regulators and banks around the world move to integrate stablecoin settlement and blockchain infrastructure into the traditional financial system to reduce costs and settlement times.

Related: Related: Euro stablecoins dominate non-dollar market, Visa-backed report finds

Banks, payment networks and regulators push stablecoin integration

In March, Mastercard agreed to acquire stablecoin infrastructure company BVNK in a deal valued at up to $1.8 billion.

Jorn Lambert, Mastercard’s chief product officer, said “most financial institutions and fintechs” are moving toward services built around stablecoins and tokenized deposits.

Separately, Visa began operating validator nodes on the Tempo network on Tuesday. Validators on the network can earn stablecoin-based rewards for processing transactions.

A Visa spokesperson told Cointelegraph the company is focused on the technical and strategic aspects of operating a validator, rather than generating revenue.

Regulatory frameworks around the world are also beginning to catch up. In April, Pakistan’s central bank allowed banks to serve licensed crypto firms, ending years of legal restrictions.

Earlier this year, the country signed an exploratory agreement to assess World Liberty Financial’s USD1 (USD1) stablecoin and its potential use for cross-border payments.

Meanwhile in Europe, where euro-denominated stablecoins still lag far behind dollar-backed tokens, a consortium of banks including ING, UniCredit and BBVA is developing a euro-pegged stablecoin.

The banks plan to distribute the stablecoin across crypto exchanges and banking channels, with a launch targeted for the second half of 2026.

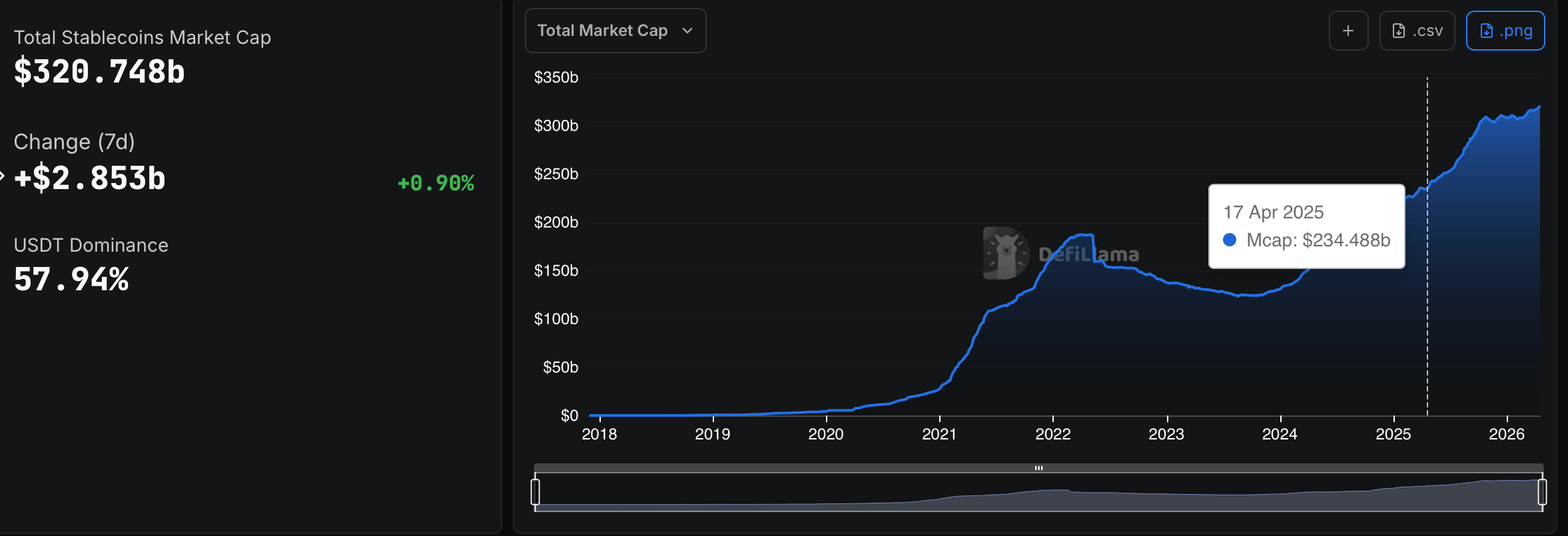

The moves come as the stablecoin market cap, which exceeds $320 billion at the time of publication, according to data from DeFiLlama, continues to grow.

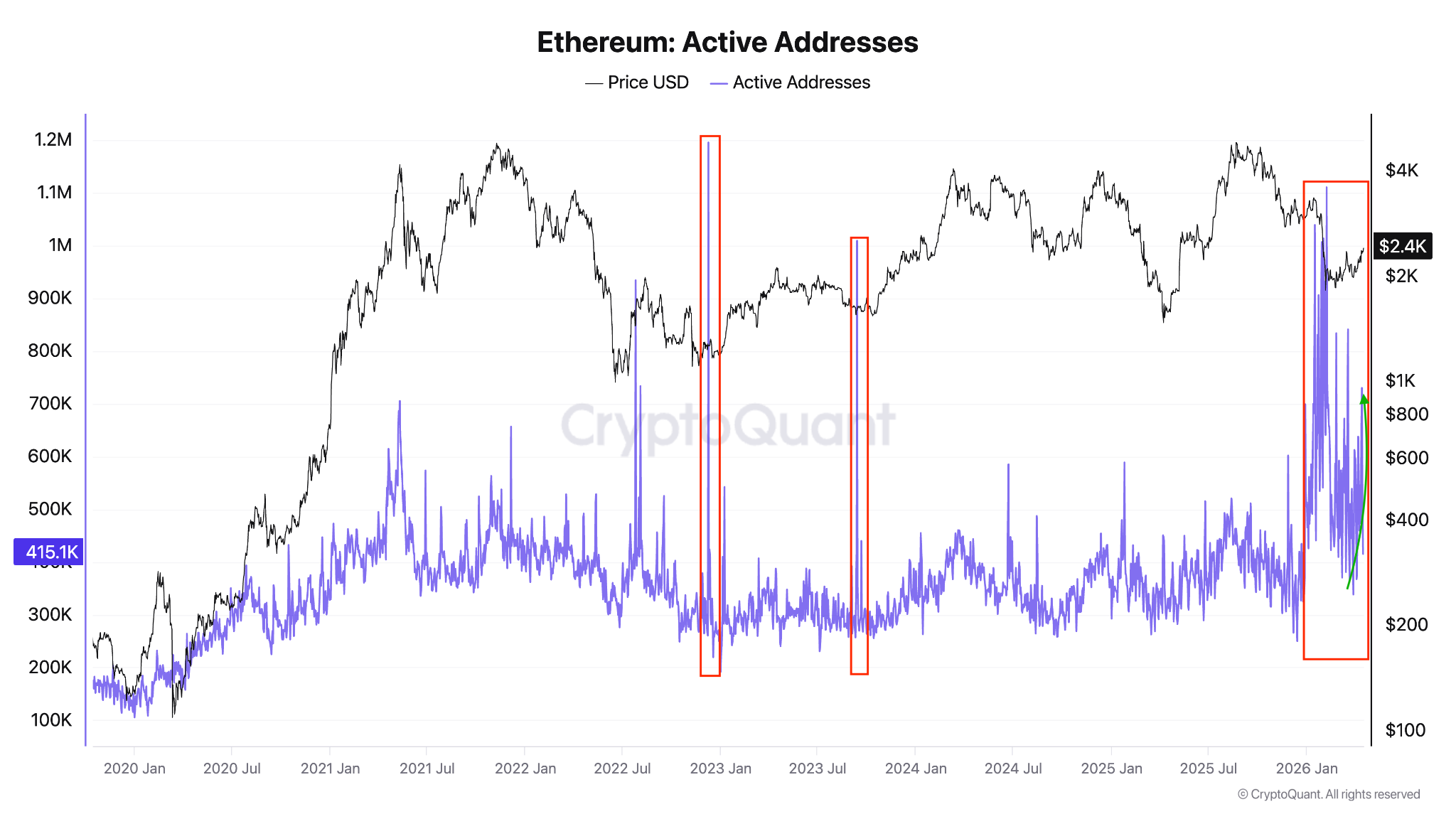

Ether’s (ETH) rally to $2,400 is nearly 38% above its swing low at $1,750, but is ETH’s price move simply a momentum trade, or do longer-term data points suggest a paradigm shift at play?

ETH accumulation addresses absorb 6.5 million Ether

Ether’s recent rally was preceded by an 89% surge in daily active addresses (DAA), which jumped to 730,278 from 384,763 on April 5.

The increase in Ethereum’s active addresses indicates increased user interaction with the network, which is generally a positive.

The chart below shows that activity increased significantly as Ether price rose to $2,300.

Similar activity has been consistently observed near macro bottoms since 2022, preceding significant ETH price rallies.

Daily inflows into accumulation addresses have also increased since mid-2025, reaching an all-time high of 1.14 million ETH in November 2025. The inflows have continued to climb in 2026, averaging 200,000 ETH per day, with a spike to over 358,000 on Thursday.

Related: ETH/BTC ratio hits 10-week high as Ether outpaces Bitcoin: Are new price highs next?

The amount of ETH held in accumulation wallets, or holders with no history of selling, has increased by 6.5 million to 26.16 million from 19.64 million on Jan. 1, representing a 33% increase.

The ETH supply held in accumulation addresses is a key indicator for traders and market participants, as it reflects overall confidence in Ether’s long-term outlook.

The total value of ETH staked further reinforces this outlook. The metric now stands at 39.2 million ETH, signaling growing investor confidence.

As Cointelegraph reported, Ether supply held on exchanges has fallen to multi-year lows, further tightening liquidity on order books.

Ether cup-and-handle chart breakout targets $3,150

The ETH/USD pair may resume its prevailing bullish trend after breaking out of a cup-and-handle (C&H) chart pattern, as shown in the chart below. A 12-hour candlestick close above the cup’s neckline at $2,400 may signal the start of a stronger uptrend.

The target is set by adding the cup’s depth to the breakout point, which comes to around $2,960, an approximately 22% increase from the current price.

The relative strength index has risen to 68, suggesting that ETH bulls are back in control.

Trader TheSkayeth spotted a larger C&H pattern forming over the last two months on the daily time frame, saying ETH was “setting up for a massive move.”

“If the cup and handle pattern continues, I think we get to the golden zone next.”

The measured target of this larger formation is $3,150, which is 30% above the current level.

Applying this framework, ETH bulls will need to hold above the $2,350-$2,400 zone to confirm a sustained upward breakout.

As Cointelegraph reported, a close above the $2,400 level would increase the prospects of the ETH/USDT pair rising to $2,800 and later to $3,050.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

TLDR

- XRP price trades near $1.45 while Binance funding rates remain negative throughout 2026.

- Persistent bearish positioning on Binance raises the possibility of a short squeeze.

- XRP price has gained 7.89% over the past seven days despite heavy short exposure.

- A similar negative funding rate setup preceded a 127% rally in 2025.

- Analysts identify $1.80 as the next key liquidity zone for XRP price.

XRP derivatives data shows heavy short positioning on Binance as funding rates stay negative in 2026. At the same time, spot prices rise and institutional flows return to XRP-linked products. Traders now assess whether this setup could trigger a short squeeze in the near term.

XRP Price Faces Heavy Short Bias on Binance

CryptoQuant data shows Binance XRP funding rates have remained negative for most of the year. Funding rates represent payments between long and short traders to balance futures and spot prices.

When funding rates turn negative, short traders pay long traders at regular intervals. This structure shows that more traders expect price declines and open bearish positions.

A similar pattern appeared after XRP fell sharply in the first quarter of 2025. During that period, Binance traders increased short exposure while funding rates stayed below zero.

Soon after, XRP price reversed and climbed from about $1.60 to above $3.60. That rally delivered a 127% gain over several months and reached a new all-time high.

Current data shows XRP funding rates again hover in negative territory on Binance. Therefore, traders now question whether persistent bearish positioning could create squeeze conditions.

Rebound and ETF Flows Support XRP Price Momentum

XRP price has gained 7.89% over the past seven days. At the time of reporting, the token trades near $1.45.

Despite dominant short positions on Binance, spot prices have moved higher. This divergence often increases pressure on traders who hold leveraged short contracts.

A short squeeze occurs when rising prices force short sellers to close positions. As they buy back contracts, their activity can accelerate upward price movement.

Analysts note that the next liquidity zone stands near $1.80. That level acted as firm support during trading activity in 2025.

Meanwhile, institutional demand has shown recovery over the past week. Spot XRP exchange-traded funds recorded renewed inflows, according to recent reports.

Market participants also responded to easing geopolitical tensions in the Middle East. As risk appetite improved, some capital returned to digital assets.

The combination of negative funding rates and rising spot prices has drawn market attention. Traders now monitor Binance positioning data for further shifts.

If short exposure remains elevated while prices climb, forced liquidations could increase. Such activity would directly impact derivatives markets and short-term volatility.

For now, XRP price trades near $1.45 while funding rates stay below zero. Binance derivatives data continues to show that short traders hold the upper hand in positioning.

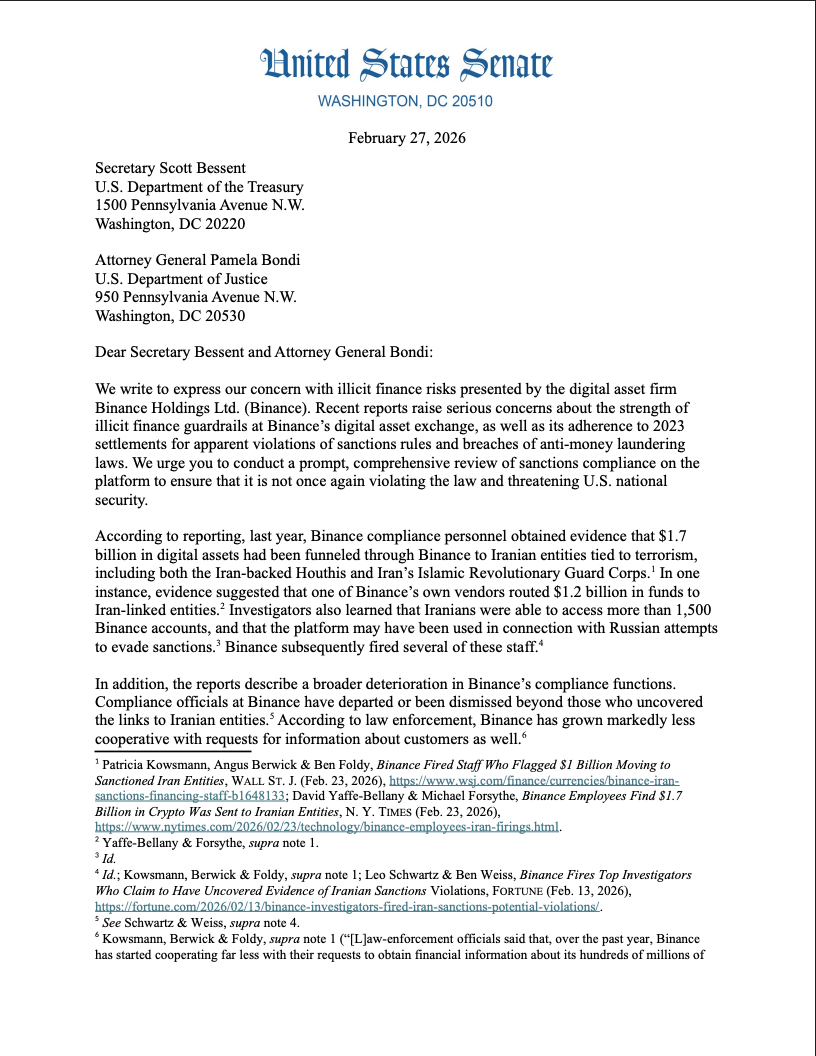

Connecticut Senator Richard Blumenthal questioned US authorities responsible for overseeing Binance about whether the company is complying with anti-money laundering laws and sanctions under its 2023 court-imposed monitoring program.

According to a report published by Fortune on Friday, Blumenthal sent letters to the Justice Department and the US Treasury’s Financial Crimes Enforcement Network (FinCEN), asking for details on Binance’s compliance.

Binance and its former CEO Changpeng “CZ” Zhao reached a deal in 2023, in which the exchange would pay $4.3 billion to settle civil regulatory enforcement actions, and CZ would plead guilty to one felony charge.

The deal also required that Binance be subject to monitoring and reporting requirements by US officials.

Blumenthal’s letter said he was concerned about “mounting allegations of dangerously lax anti-money laundering prevention by Binance.” Fortune reported that DOJ and FinCEN officials responsible for overseeing the exchange as part of the deal would not comment.

Related: Crypto billionaire to prison: CZ’s autobiography revisits turbulent Binance era

The letter followed reports that Binance was under scrutiny regarding US sanctions imposed on Iran.

The crypto exchange reportedly fired individuals responsible for telling Binance executives that $1 billion flowed through the platform to entities tied to Iran. A spokesperson for the exchange has denied the claims.

In February, a group of senators urged Treasury Secretary Scott Bessent and former Attorney General Pamela Bondi, who was fired by US President Donald Trump in April, to complete a “prompt, comprehensive review” of Binance’s compliance controls.

Trump-Binance ties are still under scrutiny

Some US lawmakers have alleged that connections between Binance and Trump create conflicts of interest for the US President and his family’s crypto businesses.

In March 2025, a United Arab Emirates-based entity purchased a $2 billion stake in Binance using the USD1 stablecoin issued by World Liberty Financial, the company co-founded by Trump and his sons.

Trump also pardoned Binance’s former CEO, CZ, in October 2025 after he served four months in prison as part of his 2023 guilty plea.

Leading bitcoin treasury company Strategy (MSTR) has filed a proxy that, if approved, would allow for semi-monthly dividends on its STRC “Stretch” series of preferred stock.

The move would have no effect on STRC’s annual dividend obligations or dividend rate (currently 11.5%), noted Executive Chairman Michael Saylor. Instead, he said, “[the] proposed changes are intended to stabilize price, dampen cyclicality, drive liquidity, and grow demand.”

The high-yielding stock has been exceptionally popular, with outstanding notional value rising to $6.4 billion as of this afternoon’s filing, according to a presentation.

Volatility has dropped to just 2.1% over the past two months versus 13% in the first eight months after the series’ launch. But Saylor and team argue that volatility could be further dampened with semi-monthly payments.

Voting on the amendment will close on June 8, with July 15 as the expected first payment date under the new plan.

MSTR shares rose 11.8% on Friday alongside bitcoin’s 3% rise to $77,400.

TLDR

- France’s finance minister urged European banks to accelerate the development of euro stablecoins and tokenized deposits.

- He said the current volume of euro-pegged tokens remains too low compared to dollar-linked stablecoins.

- Lescure backed a joint initiative by ING, UniCredit, and BNP Paribas to launch a euro stablecoin in 2026.

- Dollar-pegged stablecoins exceed $300 billion in total supply, led by USDT and USDC.

- Euro-pegged stablecoins total about $912 million in market value, according to CoinGecko data.

France’s finance minister called on European lenders to speed up digital currency projects, according to Reuters. He urged banks to expand euro stablecoins and tokenized deposits to reduce reliance on U.S. payment rails. He delivered the remarks in recorded comments at a Paris crypto conference on Friday.

European Banks Pressed to Expand Euro Stablecoins and Tokenized Deposits

Roland Lescure said the current scale of euro-pegged tokens falls short of expectations. He stated that the gap with dollar-pegged tokens was “not satisfactory,” Reuters reported. He linked the imbalance to Europe’s reliance on U.S.-dominated infrastructure.

He backed a joint project by ING, UniCredit, and BNP Paribas to issue a euro stablecoin. The three banks formed a company to launch the token in the second half of 2026. Lescure said, “That is what we need and that is what we want.”

He also encouraged lenders to develop tokenized deposits for digital transactions. He said banks should further explore these instruments within existing regulatory frameworks. He framed the effort as part of Europe’s financial modernization strategy.

Dollar Tokens Dominate while Euro-pegged Coins Trail

Dollar-linked stablecoins continue to lead the global market by supply. Total circulation has surpassed $300 billion, based on The Block’s dashboard data. Tether’s USDT holds nearly $186 billion in market value.

Circle’s USDC ranks second with about $78.8 billion in capitalization. Together, the two tokens account for most stablecoin liquidity. They dominate trading, payments, and cross-border settlements.

By contrast, euro-pegged tokens account for less than $1 billion combined. CoinGecko data shows the euro stablecoin market at $912 million. Circle’s EURC leads with $426.9 million in market capitalization.

STASIS’ EURS follows with $150.3 million in value. Societe Generale launched EURCV in 2023, and it holds $126.7 million. These figures highlight the limited scale of euro-denominated digital tokens.

Reuters cited RBC Capital Markets research on European bank sentiment. Two-thirds of surveyed banks reported limited customer demand for stablecoins. The findings reflect cautious adoption across traditional lenders.

Other studies show rising consumer engagement with digital assets. A February survey by BVNK with Coinbase and Artemis covered 4,658 adults in 15 countries. The YouGov-based study found that 54% held stablecoins in the past year.

The same report said 56% plan to acquire more stablecoins. It added that holders allocate about one-third of their savings to crypto and stablecoins. The data indicates sustained retail participation in digital assets.

Borderless, a payment infrastructure firm, tracked stablecoin foreign exchange pricing. It reviewed over 1.1 million pricing observations across 51 currencies. By March, 14 of 21 blockchain-based currencies traded within 100 basis points of interbank FX rates.

TLDR:

- Solana trades between $78 and $90, forming a tight range that signals compression before a likely breakout move.

- Bollinger Bands have narrowed sharply, indicating low volatility and increasing probability of a strong price expansion.

- MACD shows early bullish momentum returning, though confirmation depends on a sustained crossover and price strength.

- A break above $90 may open upside toward $100, while losing $78 support risks a drop to $70 levels.

Solana traded within a narrow band near $88 in April 2026, as volatility declined and momentum indicators showed early recovery signs.

At the same time, growing activity in Solana-linked investment products points to rising institutional participation during this stabilization phase.

Solana Price Structure Signals Consolidation After Extended Decline

Price action reflects a clear shift from the prolonged downtrend seen in late 2025. Solana fell from above $200, forming consistent lower highs and lower lows into early 2026. That decline accelerated before stabilizing near the $80 region.

A market update shared by More Crypto Online on X outlined two possible short-term scenarios for SOL. The analysis noted that both paths allow further upside, depending on how the price reacts near support.

It identified a micro support zone between $78.77 and $81.65. A pullback into this range would support gradual recovery, while a direct move higher would favor a stronger upward continuation.

The current structure shows a well-defined range between $78 and $90. Price continues to trade near $87.99, with repeated tests of resistance around $88.50 to $90. Sellers have defended this level, while buyers have maintained support near the lower boundary.

Bollinger Bands confirm a compression phase. The bands expanded during the earlier sell-off, reflecting high volatility.

They have since tightened, indicating reduced price movement and a potential expansion ahead. Price remains close to the middle band, signaling a balance between buyers and sellers.

Momentum indicators suggest early improvement. The MACD histogram has turned positive again, while the signal lines approach a bullish crossover.

This shift points to gradual buyer participation, though confirmation depends on further price strength.

A move above $90 would likely trigger renewed upside momentum, with $100 as the next psychological level. Further resistance could appear near $115 to $120. On the downside, a break below $78 could expose the $70 to $72 demand zone.

Solana Investment Products Expand as Institutional Access Grows

Alongside price stabilization, investment products tied to Solana continue to expand. A Solana ETF tracker shows a mix of spot and futures-based funds offering exposure to SOL, each with different cost structures and risk profiles.

Spot-based products currently lead in assets under management. Funds such as those issued by Bitwise, Fidelity, and Grayscale attract steady inflows due to direct exposure and relatively lower fees. This trend reflects a preference for simpler investment structures.

Futures-based products show stronger daily price swings. Some funds recorded higher gains in recent sessions, driven by leveraged or derivative exposure. However, these products also carry higher expense ratios and additional risks tied to futures markets.

Fee competition remains active across issuers. Spot products typically maintain lower fees, while futures funds charge higher costs for active strategies. This difference continues to influence investor allocation decisions.

The growth of these investment vehicles aligns with the current price structure. As Solana trades within a tight range, increasing institutional access suggests capital is positioning during a period of reduced volatility. Market direction now depends on whether resistance breaks or support levels give way in the sessions ahead.

A geopolitical breakthrough and strong ETF inflows converged to lift crypto markets on Friday.

Bitcoin climbed back above $77,000 on Friday after Iran declared the Strait of Hormuz fully reopened to commercial shipping, the clearest geopolitical de-escalation since the US-Israel war on Iran broke out in late February.

BTC was changing hands near $77,274, up 3.7% over 24 hours and 5.8% on the week after briefly topping $78,000 earlier in the session, per CoinGecko. The asset remains roughly 39% below its October 2025 all-time high of $126,198. Ether is trading around $2,425, up 4.1% on the day and 8% on the week.

Among other large-caps, XRP added 3.1% to $1.48, Solana rose 2% to $89, and BNB climbed 1.5% to $640. Total crypto market capitalization climbed to $2.7 trillion, with Bitcoin dominance at 57.2%.

Hormuz Reopening Fuels Rally

Iranian Foreign Minister Abbas Araghchi announced the reopening in a social media post on Friday, saying the passage for all commercial vessels through the strait is “completely open for the remaining period of ceasefire.” The announcement followed confirmation late Thursday of a 10-day ceasefire between Israel and Lebanon, a precondition Tehran had set in peace talks.

Oil prices dropped roughly 12% on the news. President Donald Trump said the strait is “ready for full passage,” but added that the US naval blockade of Iranian ports “will remain in full force” until a formal peace deal is signed.

The strait normally carries roughly a fifth of global oil and liquefied natural gas supply, and the weeks-long disruption had been the single largest macro overhang on risk assets since the war began on February 28.

Short Squeeze

The rally triggered a meaningful reset in leveraged positioning.CoinGlass data showed roughly $805 million in futures liquidations over the past 24 hours, with short positions accounting for the lion’s share at $643 million.

Nearly $390 million of Bitcoin derivatives positions were liquidated, along with $181 million of ETH positions.

Big Movers

Among the Top 100 cryptocurrencies, Ethena’s ENA led the charge with a 14% rally, while Morpho gained 10%.

Decliners were shallow. Zcash slipped 1.3% to $332, Toncoin edged 1% lower, and LEO Token gave back 0.6%, per CoinGecko.

ETF Flows Stay Positive

Spot Bitcoin ETFs logged $26 million in net inflows on April 16, according to SoSoValue. Weekly net flows into Bitcoin ETFs have totaled $332 million so far this week, following a $786 million haul the prior week.

Spot Ether ETFs extended their winning streak to a sixth consecutive session with $18 million in net inflows on April 16, lifting cumulative inflows for the category to $11.82 billion.

The US government has transferred about 8.2 Bitcoin, valued at over $606,000, to Coinbase Prime. The funds are linked to assets seized from the 2016 Bitfinex hack. Blockchain data tracked the movement and confirmed the destination.

The transfer is part of a broader restitution process approved by a federal court. Authorities are returning seized Bitcoin to Bitfinex instead of selling it. This move follows earlier transfers made in March and April 2026.

Bitcoin Transfer Linked to Restitution Process

The transaction was split into two parts, with 7.999 BTC and 0.197 BTC sent in sequence. Both amounts were directed to the same Coinbase Prime address. On-chain data confirmed the movements and timing.

This transfer follows a legal order issued in early 2025. The ruling required that recovered Bitcoin be returned directly to Bitfinex. The court recognized the exchange as the sole victim in the case.

Exchange transfers often raise concerns about possible selling. However, this case differs due to legal restrictions. The transferred Bitcoin is not intended for open market liquidation.

Federal authorities continue to manage a large Bitcoin reserve. As of April 2026, government wallets hold about 328,361 BTC. The latest transfer represents only a small portion of that total.

Background of the 2016 Bitfinex Hack

The Bitfinex hack occurred in August 2016 and significantly impacted the cryptocurrency market at the time. Hacker Ilya Lichtenstein exploited a system weakness and stole over 119,000 BTC. The stolen assets were worth $72 million then.

Over several years, Lichtenstein and Heather Morgan attempted to move the funds through layered transactions. Their actions aimed to hide the origin of the Bitcoin. Authorities tracked the activity over time.

In February 2022, the US government seized about 94,636 BTC. Investigators accessed private keys stored in cloud files. These keys allowed direct control of the stolen assets.

Lichtenstein later received a five-year prison sentence in November 2024. Morgan was sentenced to 18 months. Both had pleaded guilty to money laundering charges earlier.

Bitfinex Plans for Returned Bitcoin

Bitfinex has outlined how it will use the returned Bitcoin. The exchange plans to redeem its Recovery Right Tokens fully. These tokens were issued after the 2016 hack.

In addition, Bitfinex will allocate at least 80 percent of remaining proceeds. The funds will go toward buying back and burning UNUS SED LEO tokens. This plan follows commitments made in its recovery framework.

A statement tied to the plan noted that the process would follow existing agreements. It said, “the funds will be used according to the recovery commitments already defined.” This reflects a structured use of the returned assets.

The recent transfer marks another step in the restitution timeline. While the amount moved is small, it aligns with court directives. Further transfers may follow as the process continues.

Desperate for Financial Help? Pray This Today

Number of investigations into PSNI abuse of position for sex revealed

Cintas: The Valuation Has Come In, But It's Not A Buy Just Yet

-

NewsBeat5 days ago

NewsBeat5 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Politics5 days ago

Politics5 days agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World4 days ago

Crypto World4 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Crypto World4 days ago

Crypto World4 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos3 days ago

News Videos3 days agoSecure crypto trading starts with an FIU-registered

-

Sports12 hours ago

Sports12 hours agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World4 days ago

Crypto World4 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

Business6 days ago

Business6 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

NewsBeat3 days ago

NewsBeat3 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Crypto World7 days ago

Crypto World7 days agoFederal judge blocks Arizona from bringing criminal charges against Kalshi

-

NewsBeat6 days ago

NewsBeat6 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Business7 days ago

Business7 days agoIMF retains floor for precautionary balances at SDR 20 billion

-

Sports6 days ago

Dexter Lawrence, Stefon Diggs, Trading for De’Von Achane

-

Business7 days ago

Business7 days agoFormer Liverpool CEO eviscerates FIFA for World Cup ticket pricing

-

Crypto World5 days ago

Sei Network Enters Quiet Reset Phase as On-Chain Metrics Signal a Slowdown in 2026

-

Crypto World5 days ago

Crypto World5 days agoTrump whales load up ahead of Mar-a-Lago luncheon.

-

Business7 days ago

Coreweave CSO Venturo sells $5.5m in class a common stock

-

Sports7 days ago

1st-Round WR Enters Vikings Mock Draft Orbit

-

Business5 days ago

Kering slides after Morgan Stanley downgrade, Gucci woes loom

-

Sports4 days ago

Sports4 days agoNWFL opens Pathway for new Clubs ahead of 2026 Season

You must be logged in to post a comment Login