Business

The Top 5 Small Private Jet Companies Operating in the UK

The United Kingdom occupies a highly strategic position in the global aviation market. Serving as the primary gateway between North America and mainland Europe, its airspace is some of the busiest in the world.

For the discerning traveller, however, the traditional commercial airport experience at major hubs like Heathrow or Gatwick has become increasingly fraught with delays, security queues, and overcrowding. This friction has fueled a surge in demand for small, boutique private jet companies operating across the UK.

Boutique aviation – unlike the massive corporate fractional ownership programmes – offers a highly personalised, agile service. These smaller operators specialise in short to medium-haul flights, perfectly suited for the typical British travel profile, which frequently involves quick hops to Geneva for skiing, the French Riviera for summer holidays, or Frankfurt for business.

Bypassing the Commercial Chaos

The primary advantage of utilising a smaller charter operator is access to regional airfields. Instead of navigating the M25 to reach a major hub, clients can depart from discreet, dedicated business aviation airports such as Farnborough, London Biggin Hill, or even smaller regional strips like Oxford and Gloucester. The process is remarkably seamless. A passenger can pull their car directly up to the terminal, complete a private security check in minutes, and be airborne shortly after.

The Rise of the Light Jet

In the UK market, the light and super-light jet categories dominate. Aircraft such as the Embraer Phenom 300, the Cessna Citation Mustang, and the Learjet 75 are the workhorses of these boutique fleets. They offer exceptional efficiency for flights under three hours, striking the perfect balance between luxurious comfort and operational cost-effectiveness. These aircraft are specifically designed to perform exceptionally well on the shorter runways characteristic of Britain’s smaller airfields.

Profiling the UK’s Top 5 Small Private Jet Providers

The British charter market is populated by several outstanding boutique operators. Here are the top five companies currently defining the standards for small-scale private aviation in the UK.

Zenith Aviation: The Biggin Hill Specialists

Operating out of London Biggin Hill Airport, Zenith Aviation has built a formidable reputation in the light jet sector. They are particularly well-known for their extensive fleet of Learjet 75 aircraft. This specific aircraft choice allows Zenith to offer a highly competitive service for trips across Europe, providing a fast, quiet, and exceptionally comfortable cabin. Zenith focuses heavily on operational agility, catering to clients who require rapid dispatch times for last-minute business meetings or spontaneous weekend getaways. Their location just outside central London makes them a premier choice for city-based executives.

Execaire Aviation: The Transatlantic Bridge

Securing the second position in our overview is a company with a robust international footprint that provides excellent service within the British market. Those looking for tailored charter solutions frequently utilise Execaire Aviation, an operator that brings decades of rigorous aviation management experience to the UK. While they boast a diverse fleet capable of heavy, ultra-long-range missions, their charter division expertly manages smaller, agile aircraft ideal for European routes. They stand out for their comprehensive approach to flight management, ensuring that safety, privacy, and dispatch reliability meet the highest international standards, whether you are flying from London to Edinburgh or venturing further afield.

Centreline: The South West Hub

Based at Bristol Airport, Centreline dominates the private aviation market in the South West of England. They operate a highly versatile fleet, with a particular emphasis on the Embraer Legacy and Phenom aircraft families. Centreline is an excellent example of a boutique operator that provides an end-to-end service, boasting their own VIP terminal and maintenance facilities. Their regional base makes them highly attractive to clients residing outside the London commuter belt, offering direct, private access to Europe without the need to travel to the capital first.

SaxonAir: The East Anglian Innovators

Headquartered at Norwich Airport, SaxonAir is a unique player in the UK market. Initially founded to serve the offshore energy sector in the North Sea, the company has expanded its portfolio to include a luxurious fleet of light jets and helicopters. SaxonAir is notable for its aggressive push towards sustainability. They are heavily involved in the transition towards greener aviation, actively promoting the use of Sustainable Aviation Fuel (SAF) and exploring electric aircraft technology for short-range training and transport.

Luxaviation UK: The Heritage Operators

Formerly known as London Executive Aviation (LEA), Luxaviation UK operates primarily out of Stapleford Aerodrome and London Luton. They possess a deep heritage in the British charter market and have grown to become one of the most trusted names in the business. Their fleet includes a vast array of light and mid-size jets, making them incredibly adaptable to varying client needs. Their integration into the wider global Luxaviation network allows them to offer boutique, localised service while leveraging the resources and purchasing power of a massive international aviation group.

Choosing the Right Boutique Operator

Selecting the ideal private jet company requires more than just requesting a quote. The discerning client must consider the specific operational capabilities of the provider to ensure a flawless journey.

Understanding Fleet Capabilities

Not all light jets are created equal, and matching the aircraft to the specific mission is vital. A client travelling to the Swiss Alps for a ski holiday requires an aircraft capable of handling high-altitude approaches and potentially steep descents. In these scenarios, the technical specifications of the operator’s fleet become the most critical factor.

Runway Requirements and Regional Airports

Furthermore, if your destination is a remote Scottish island or a small Mediterranean airfield, runway length restrictions will dictate your choice of aircraft. Some operators possess fleets with exceptional short-field performance, allowing them to access runways that are strictly off-limits to larger, heavier jets. A quality boutique operator will actively consult with you on these technical constraints rather than simply selling you an available seat.

The Importance of Personalised Service

The defining characteristic of a boutique operator is the level of bespoke service provided. When you are flying privately, the journey should be an extension of your own living room or boardroom.

Bespoke Catering and Ground Handling

This extends to the minutiae of the in-flight experience. Top-tier UK operators will organise highly specific catering – from sourcing a particular vintage of wine to arranging afternoon tea from a preferred London bakery. Additionally, they handle the complexities of ground transportation, ensuring a chauffeur is waiting on the tarmac the moment the aircraft engines spool down. For clients travelling with pets, which is highly common in the UK, boutique operators manage the complex DEFRA paperwork and ensure the aircraft cabin is fully prepped to accommodate four-legged passengers safely and comfortably.

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

SEOUL — In the fiercely competitive world of K-pop girl groups, BLACKPINK and TWICE remain the two dominant forces heading into mid-2026, with BLACKPINK reclaiming momentum through a blockbuster comeback while TWICE sets attendance records on the road. The eternal debate — which group reigns supreme globally — shows BLACKPINK holding a slight edge in overall metrics, though TWICE’s dedicated fanbase and live draw keep the race compelling.

BLACKPINK, under YG Entertainment, made a triumphant return in early 2026 with their third mini-album DEADLINE. The release shattered first-day sales records for a K-pop girl group, moving over 1.46 million copies worldwide on day one and surpassing 1.77 million in the first week. The title track “JUMP” and follow-up “GO” dominated global charts, with “GO” claiming No. 1 on YouTube’s global weekly chart and strong Spotify performance.

As of mid-May 2026, BLACKPINK leads as the most-streamed K-pop girl group on Spotify for the year, surpassing 800 million streams and becoming the first female act to hit that milestone in 2026. The group boasts approximately 23 million monthly listeners, with a massive catalog advantage from hits like those on DEADLINE. Their world tour supporting the album spans major stadiums across 16 cities and 33 shows, building on the success of the record-breaking Born Pink tour that drew over 1.8-2.1 million fans previously.

Brand reputation rankings reinforce BLACKPINK’s position. In January and February 2026 analyses, they consistently ranked No. 1 or No. 2 among girl groups, ahead of TWICE. Their global digital artist rank remains in the top five, driven by international appeal, solo successes from Jennie, Lisa, Rosé and Jisoo, and massive YouTube presence.

TWICE, from JYP Entertainment, counters with consistency and unmatched touring strength. Their This Is For world tour shattered records in 2026, drawing an estimated 550,000 fans across the North American leg alone — the highest attendance for a K-pop girl group in the region. The tour expanded to Europe and Japan, with three shows at Tokyo National Stadium pulling 240,000 attendees. Overall, TWICE has demonstrated robust ticket power, often outpacing newer acts in live revenue and scale.

Streaming-wise, TWICE trails BLACKPINK slightly in 2026 but remains competitive, reaching 600-700 million Spotify streams early in the year and ranking as the second-most streamed girl group in several periods. Their album This Is For performed strongly in the U.S., becoming one of the top-selling K-pop girl group releases there. TWICE also leads in longevity metrics, with extended charting on platforms like Spotify and Apple Music.

Fanbases tell a nuanced story. BLINKs benefit from BLACKPINK’s broader casual recognition and solo stardom, which boosts group visibility. ONCEs pride themselves on loyalty and organized support, fueling TWICE’s touring success. Social media debates rage, with some arguing TWICE has gained ground in the U.S. and Japan through consistent releases, while BLACKPINK dominates overall global searches, brand deals and cultural impact.

Album sales favor BLACKPINK in headline moments, but TWICE excels in cumulative physical and digital units over time. TWICE has moved millions in Japan and maintains strong domestic support. BLACKPINK’s DEADLINE era not only set sales benchmarks but also revived their dominance in digital points on charts like Circle.

Global metrics highlight BLACKPINK’s lead. They boast higher YouTube subscribers and views, stronger Google Trends in many regions, and more universal name recognition. Solo activities amplify this: Lisa and Jennie frequently trend worldwide. TWICE, however, shines in dedicated markets like North America for live events and maintains a wholesome, approachable image that resonates with multi-generational fans.

Industry observers note both groups benefit from the post-BTS K-pop boom. BLACKPINK’s four-year hiatus before DEADLINE built anticipation that paid off massively, while TWICE’s steady output prevented any dip in relevance. Newer acts like IVE and LE SSERAFIM challenge them in brand rankings, but the veterans hold the top spots in cumulative influence.

Touring revenue underscores live power. TWICE’s 2026 North American success sets benchmarks, yet BLACKPINK’s stadium-scale ambitions position them for even larger grosses when fully deployed. Both groups excel where newer acts struggle — translating streams into ticket sales and sustained careers.

Social sentiment and polls often split along generational lines. Older fans lean BLACKPINK for pioneering global breakthroughs; younger ones appreciate TWICE’s relatability. Fan-voted rankings frequently place BLACKPINK higher overall, though TWICE wins in specific territories.

Looking ahead, BLACKPINK’s momentum from DEADLINE and the ongoing tour likely solidifies their position as the more popular group globally in 2026. Their blend of massive digital impact, brand power and star quality gives a broader reach. TWICE, however, proves unmatched consistency and fan connection, particularly in live settings, ensuring they remain a powerhouse.

The rivalry elevates both. BLACKPINK sets records in sales and virality; TWICE in attendance and loyalty. Neither shows signs of fading, with potential for joint or competitive dominance in the years ahead. For now, BLACKPINK holds the slight global edge, but TWICE’s resilience makes the contest far from over.

As K-pop matures, these two groups exemplify different paths to success: explosive global phenomena versus steadfast, fan-driven empires. Fans win either way, enjoying high-quality music, spectacular performances and the thrill of the ongoing debate.

Plant manufactures Silk and So Delicious brands.

Business

RWE Aktiengesellschaft 2026 Q1 – Results – Earnings Call Presentation (OTCMKTS:RWEOY) 2026-05-13

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

Changes to the research and development tax incentive have received a mixed review from industry and experts, with some warning it risked legitimate research missing out on funds.

London’s Alphonso mango supply is down this year due to fewer imports and higher prices for shoppers.

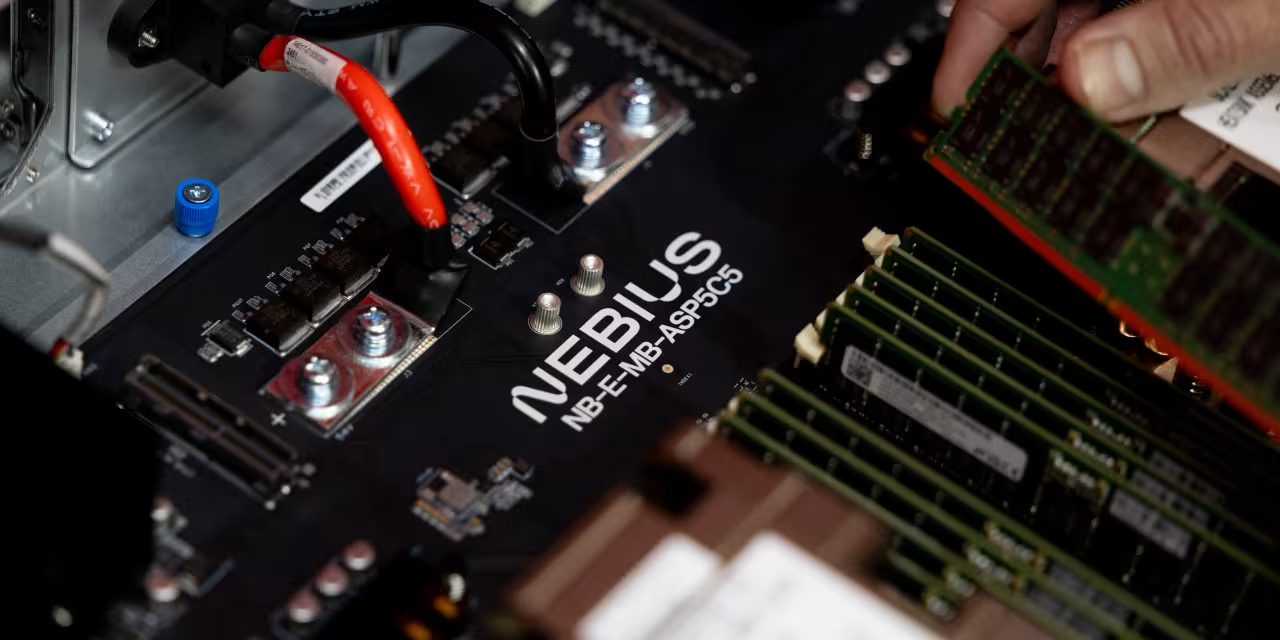

Nebius Stock Spikes After Earnings. The AI Neocloud Sees ‘Unprecedented Demand.’

SEOUL — As 2026 unfolds, the K-pop world remains gripped by the ultimate showdown: BTS, the undisputed kings of global domination, versus Stray Kids, the self-producing 4th-generation juggernaut rewriting records during BTS’ military hiatus. While BTS boasts unmatched legacy metrics and a powerful March comeback, Stray Kids flexes superior current momentum in touring, album sales and active fan engagement.

BTS, formed in 2013 under Big Hit Music (now HYBE), redefined K-pop’s global reach. Their catalog continues to dominate long-term streaming, with Spotify monthly listeners hovering around 24.6 million in early 2026 — roughly double Stray Kids’ 12.1 million. The septet — RM, Jin, Suga, J-Hope, Jimin, V and Jungkook — completed mandatory military service by mid-2025, paving the way for their full-group return.

In March 2026, BTS unleashed their comeback album “Arirang,” blending Korean roots with global pop sounds. The release sparked massive YouTube and streaming surges, with the group dominating U.S. and global charts. Their “Arirang” world tour quickly became one of the most anticipated in K-pop history, with analysts projecting over 5 million tickets and nearly $2 billion in revenue across 82 shows. Early stops, including massive Mexico City dates drawing 150,000 fans, reaffirmed their unparalleled draw.

Social media metrics underscore BTS’ enduring empire. The group holds over 82 million YouTube subscribers and 44.5 million X followers. Their fandom, ARMY, remains the largest and most organized in K-pop, driving consistent catalog streams even without new material. In March 2026 alone, BTS racked up 1.38 billion Spotify streams as a group, far outpacing others.

Yet Stray Kids, debuting in 2018 under JYP Entertainment, has capitalized on BTS’ absence to claim the throne of active dominance. The eight-member group — Bang Chan, Lee Know, Changbin, Hyunjin, Han, Felix, Seungmin and I.N. — self-produces much of its music, fostering deep authenticity that resonates with younger fans. In 2025, they sold approximately 7 million albums, a staggering figure compared to BTS’ lower output during the hiatus period.

Their “dominATE” world tour in 2025 shattered K-pop records, selling over 2 million tickets across 56 shows and grossing hundreds of millions. The tour set benchmarks in North America (over 600,000 tickets), Latin America and Europe, often outdrawing previous BTS legs in specific markets. Stray Kids became the first K-pop act to headline major venues like London’s Tottenham Hotspur Stadium and sold out stadiums globally.

Streaming data reveals a nuanced picture. While BTS leads in total monthly listeners and historical catalog, Stray Kids frequently ranks as the second-most streamed K-pop act. In March 2026, they achieved 304 million streams, and they crossed 12.8 billion lifetime Spotify streams — only the third Korean act to do so after BTS. Their hit “God’s Menu” surpassed 500 million streams, cementing longevity.

Social platforms tell another story. Stray Kids boast around 22.7 million YouTube subscribers and 11.2 million X followers — impressive for a younger group but trailing BTS significantly. Their fandom, STAY, is among the fastest-growing, known for intense loyalty and rapid mobilization.

Billboard and IFPI charts highlight Stray Kids’ commercial peak. They secured multiple No. 1 debuts on the Billboard 200, including eight consecutive albums, and landed second on the 2025 IFPI Global Artist Chart. Their ability to sell out arenas without the same decade-long buildup demonstrates remarkable current popularity.

BTS’ brand power remains unmatched in broader recognition. The group has amassed over 500 global awards and dozens of daesangs. Their influence extends beyond music into fashion, diplomacy and social causes, with the United Nations and global brands seeking partnerships. Even in 2026, casual audiences worldwide recognize BTS more readily than Stray Kids.

Analysts debate metrics of “popularity.” Legacy favors BTS: cumulative streams, social following, cultural impact and name recognition. Current activity favors Stray Kids: recent sales, touring revenue, active chart performance and younger demographic penetration. In South Korea, polls sometimes show Stray Kids leading in popularity points among active idols, with one metric giving them 20.5 million versus BTS’ 19.5 million.

The 2026 landscape shifts with BTS’ full return. Their March comeback already boosted streams dramatically, with some reports noting monthly listeners climbing toward 46 million post-release. The “Arirang” tour promises to eclipse previous records, potentially reclaiming the crown in live attendance.

Stray Kids show no signs of slowing. Their consistent comebacks, global tours and self-sufficient creative model sustain momentum. As members approach military service age in coming years, questions linger about their ability to maintain dominance like BTS did.

Fan communities fuel the rivalry. ARMY emphasizes BTS’ pioneering role in bringing K-pop mainstream, while STAY highlights Stray Kids’ innovation and resilience. Social media debates rage daily, with hashtags comparing streams, sales and concert footage. Both fandoms demonstrate impressive organization, though ARMY’s scale often tips viral moments.

Industry experts view the competition as healthy for K-pop. BTS elevated the genre globally; Stray Kids and peers like ENHYPEN prove the ecosystem thrives without sole reliance on one act. Hybrid metrics — combining streams, sales, touring and social data — show BTS leading overall but Stray Kids closing gaps in key 2025-2026 windows.

Looking forward, BTS’ 2026-2027 activities could widen their lead again. A full world tour alongside new music promises historic numbers. Stray Kids will counter with fresh releases and continued touring innovation. The “who is more popular” question depends on timeframe: all-time favors BTS overwhelmingly; right-now momentum tilts toward Stray Kids.

Global K-pop consumption has evolved. Streaming favors catalog depth (BTS advantage), while physical sales and live events reward active groups (Stray Kids edge). TikTok virality, brand deals and regional strength further complicate comparisons. BTS dominates Japan, parts of Latin America and brand power; Stray Kids excel in North America and Europe touring.

Ultimately, 2026 underscores K-pop’s maturation. BTS remains the benchmark, but Stray Kids prove a new generation can achieve massive success. As BTS fully re-enters the fray, the friendly rivalry elevates both acts, benefiting fans and the industry. Whether measured by streams, tickets or cultural footprint, both groups stand as titans — one built on unmatched legacy, the other on relentless current excellence.

Business

SBI shares extend fall to 20% from peak after Q4 NIMs contraction rattles investors. What’s ahead for investors?

SBI shares have lost momentum since hitting their 52-week high of Rs 1,235 on the NSE. The stock rallied 60% between May and February, outperforming the sector and most of its PSU bank peers. But its underperformance is not an isolated event as domestic markets have had a rough ride in 2026, so far. While Nifty and Bank Nifty are down 10% year-to-date, the sectoral benchmark Nifty PSU bank has declined over 5% in this period.

After the state-lender reported its quarterly earnings, the Street responded negatively, worried about the margins. The country’s largest PSU bank saw its net interest margins (NIMs) contract both year-on-year and sequentially, while net interest income (NII) declined 1.4% quarter-on-quarter. SBI also reported a fall in operating profit for Q4FY26.

The operating profit stood at Rs 27,704 crore, falling 16% YoY and 11.5% QoQ versus Rs 31,286 crore in Q4FY25 and Rs 32,862 crore in Q3FY26.

The PSU lender’s net interest income (NII) stood at Rs 44,380 crore, sliding 1.35% QoQ. The NII, which is the difference between interest earned and interest expended, rose 4% YoY.

Commenting on the current trends, Dr. Ravi Singh, Chief Research Officer from Master Capital Services said selling pressure in SBI followed its latest quarterly results, with the stock slipping sharply from the Rs 1,100 zone. “Although the bank continues to report strong overall profitability and stable asset quality, investors appeared concerned about pressure on margins and slower earnings momentum going ahead. The sharp decline in the stock reflects profit booking after a strong rally seen over the past year,” he said.

The public sector lender reported a standalone net profit rose 6% YoY to Rs 19,684 crore in the fourth quarter. The same stood at Rs 18,643 crore in the last year’s quarter. The profit beat the analysts’ estimates of Rs 18,898 crore.SBI’s Q4FY26 earnings missed estimates on the back of a collapse in margins despite healthy growth on both sides of the balance sheet and a strong fee income profile, said HDFC Securities in a note, echoing a similar sentiment.

The loan book grew 17% YoY continuing to outpace the system, led by the corporate and overseas segment but deposit growth of 11% YoY raises liquidity risks.

Brokerage view

HDFC Securities expects SBI to continue benefiting from productivity and efficiency gains along with stable asset quality, helping sustain RoA at around 1.1%. It reiterated its ‘Buy’ rating on the stock with a revised target price of Rs 1,195 and maintained SBI as its top pick among PSU banks.

The brokerage further noted that asset quality improved across segments and credit costs moderated despite a slight uptick in gross slippages.

Axis Securities believes SBI remains well-placed to deliver healthy medium-term earnings growth supported by steady credit expansion, improving fee income and stable asset quality. While margins saw some pressure in Q4, the brokerage highlighted management’s confidence in sustaining domestic NIMs near 3% through a better asset mix, stronger CASA mobilisation and lower reliance on expensive bulk deposits.

Axis Securities also pointed to multi-decade low asset quality stress levels across domestic and overseas portfolios and expects the transition to the Expected Credit Loss framework to remain smooth. It further expects improving operational efficiency and rising cross-sell intensity to support profitability, enabling SBI to sustainably deliver around 1% RoA through the cycle.

What charts suggest?

Decoding the charts, Dr. Singh said the SBI chart has turned weak from the near term perspective as the stock has broken below key short-term support levels, while RSI has moved close to the oversold zone, indicating bearish momentum is still dominant. Rising volumes during the fall suggest institutional selling as well.

In his view, SBI’s strong fundamentals, healthy loan growth, improving balance sheet quality, and strong leadership within the banking sector augur well for the stock’s prospects. The Rs 960 area now becomes an important support zone, while recovery above Rs 1,000 could help sentiment stabilise again, he added.

(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

Bristol Blue Glass says rising energy costs and taxes have forced its closure.

Paysafe Limited 2026 Q1 – Results – Earnings Call Presentation (NYSE:PSFE) 2026-05-13

Nigeria confirmed to host 2026 CAF Awards and General Assembly

Ultimate High-end Audio and Home Theater Gifts That Will Seriously Impress in 2026

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World5 days ago

Crypto World5 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Marianne Dress

-

Crypto World6 days ago

Crypto World6 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

NewsBeat6 days ago

NewsBeat6 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Fashion2 days ago

Fashion2 days agoCoffee Break: Travel Steam Iron

-

Fashion2 days ago

Fashion2 days agoWhat to Know Before Buying a Curling Wand or Curling Iron

-

Tech3 days ago

Tech3 days agoAuto Enthusiast Carves Functional Two-Stroke Engine from Solid Metal

-

Politics2 days ago

Politics2 days agoWhat to expect when you’re expecting a budget

-

Business4 days ago

Business4 days agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Politics4 days ago

Politics4 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Crypto World7 days ago

Crypto World7 days agoBlackRock CEO Larry Fink Discusses a New Asset Class

-

Tech2 days ago

Tech2 days agoGM Agrees To Pay $12.75 Million To Settle California Lawsuit Over Misuse Of Customers’ Driving Data

-

Entertainment6 days ago

Entertainment6 days agoSarah Paulson Called Out For Met Gala ‘Hypocrisy’

-

Politics6 days ago

Politics6 days agoSimon Cowell Says He Was ‘Horrible’ To Susan Boyle During BGT Audition

-

Entertainment6 days ago

Entertainment6 days agoGeneral Hospital: Ric & Ava Bombshell – Ric’s Massive Secret Exposed!

-

Crypto World6 days ago

Crypto World6 days agoRobinhood says Wall Street is building onchain

-

Sports6 days ago

Sports6 days agoUEFA Champions League final schedule, teams, venue, live time and streaming | Football News

-

Entertainment7 days ago

Entertainment7 days agoBold and Beautiful Early Spoilers May 11-15: Steffy Revolted & Liam Overjoyed!

-

Entertainment6 days ago

Entertainment6 days agoWhy David Letterman Called CBS ‘Lying Weasels’

-

Entertainment7 days ago

Entertainment7 days agoSister Wives: Tony Flings Shade at Robyn in New Post

You must be logged in to post a comment Login