Crypto World

World Liberty-Linked AI Financial Flags Going Concern

AI Financial Corp., a World Liberty Financial token treasury company, said a deficit in working capital and liabilities is casting significant doubt on its ability to continue over the next year.

The company, which has World Liberty CEO Zach Witkoff as its chairman, reported a net loss of $271.5 million in its first-quarter results on Monday, compared to losses of $2.4 million a year ago.

The firm, formerly known as ALT5 Sigma, said that as of March 28, it had a working capital deficit of around $5.5 million, with $39.1 million in liabilities against $32.2 million in assets.

“These conditions raise substantial doubt about the Company’s ability to continue as a going concern within one year after the date these financial statements are issued,” AI Financial said.

AI Financial was one of the many companies swept up in the craze of crypto-buying public firms, becoming a buyer of World Liberty Financial (WLFI), the token of the Trump family-backed crypto platform of the same name.

To meet its obligations, AI Financial said it held 7.3 billion WLFI tokens at a value of $703.4 million as of March 28, which it could use to firm up its liquidity.

However, the value of AI Financial’s WLFI holdings has fallen by a third since late December, when the fair value of the tokens was at over $1 billion, leading to an unrealized loss of $348.3 million. The company paid nearly $1.46 billion to acquire its WLFI holdings.

AI Financial added that it also borrowed nearly $15 million from World Liberty in January, drawing down the cash under a loan agreement with the Trump-linked firm, which it said it could use in a share repurchase program and to buy more WLFI tokens.

Shares in AI Financial (AIFC) ended trading down nearly 6.3% on Tuesday at 85 cents, extending its 10% drawdown over trading on Monday.

Source: Google Finance

Related: Trump-backed Truth Social pulls bids for crypto ETFs

The company’s stock has fallen by nearly 87.5% over the past 12 months. It first looked to become a WLFI treasury company in early August after closing a $1.5 billion direct offering and private placement led by World Liberty Financial.

At the time of the deal closing, Witkoff became AI Financial’s chairman, while World Liberty co-founder Zak Folkman became a board observer.

US President Donald Trump’s son, Eric Trump, joined the company’s board, but was quietly removed from the leadership section of its website late last month.

Magazine: Trump’s crypto ventures raise conflict of interest, insider trading questions

Everyone is building non-dollar stablecoins. But data shows that compared to USD-denominated stablecoins, almost no one is using them.

Banks crash. Payment platforms freeze at the worst possible moment. Trading systems lag during market spikes. Financial software has quietly become the most critical — and most unforgiving — software category in existence.

One bug costs millions. One compliance gap shuts a company down. This guide covers what financial software development actually involves, what the market looks like today, and how to build something that survives contact with reality.

The State of the Market Right Now

JPMorgan employs more technologists than many software companies have total staff. Goldman Sachs has been calling itself a tech company for years — and at this point, arguing with that framing feels pointless. The demand for software development for financial services has spread across three segments: retail banking, institutional finance, and compliance infrastructure. Each has its own rules. Each punishes bad decisions differently.

The shift isn’t just about startups disrupting banks anymore. Established players are moving too, and fast. Companies building at enterprise scale — where platforms covering financial services technology solutions span everything from core banking modernization to AI-driven analytics — face a specific kind of pressure: modernize legacy COBOL systems without taking them offline. That constraint shapes almost every architectural decision.

What’s actively being prototyped and tested right now?

- Real-time payment rails — FedNow launched in the US in 2023. Instant payments have stopped being a differentiator and started being a baseline expectation.

- Embedded finance APIs — Stripe, Plaid, and Unit are letting non-financial companies offer banking features inside their own products. The line between “fintech” and “tech company with a bank account” keeps blurring.

- Tokenized assets — JPMorgan’s Onyx platform processes short-term loan transactions on distributed ledger infrastructure. Whether blockchain becomes foundational or stays niche in finance is still genuinely open.

- Cloud-native core banking — Thought Machine’s Vault platform runs with no mainframes. That’s still unusual enough to be notable.

- Post-quantum cryptography — NIST finalized its first post-quantum standards in 2024. Long-horizon financial firms are already planning migration timelines.

What Financial Software Actually Covers

“Financial software” gets used as if it means one thing. It doesn’t.

Core Banking Platforms

Core banking systems handle transactions, accounts, and ledgers — often still running on IBM Z mainframes in large institutions. Modernizing them is genuinely one of the hardest problems in enterprise software. Temenos, FIS, and Finastra sell packaged solutions. Challenger banks like N26 and Revolut built custom. Both paths come with real costs.

Trading Systems

Low-latency trading infrastructure operates in microseconds. Firms like Virtu Financial have built reputations on near-flawless execution over long stretches — that kind of consistency comes from software precision, not luck. C++ dominates here, and in some cases FPGA programming moves logic to hardware to shave off the latency that matters.

Risk and Payments

BlackRock’s Aladdin manages risk analytics for a substantial share of global institutional assets. Building something comparable isn’t a short engagement — it’s a sustained investment in data science and infrastructure. Payments are a different beast: every card swipe triggers authorization, fraud checks, settlement, and reconciliation in under two seconds. Stripe has turned that complexity into a clean developer API. The infrastructure underneath is anything but simple.

The Technical Stack

No vague “Java is a solid choice” framing here. Here’s what actually gets used.

Languages. Java still dominates enterprise banking — after decades, it’s not going anywhere. Python runs most quant finance and ML workloads. C++ handles latency-sensitive trading. COBOL still processes a significant share of daily global commerce. Yes, in 2025. Kotlin and Swift handle mobile banking. Rust is gaining ground in payment infrastructure where memory safety is non-negotiable.

Databases. PostgreSQL and Oracle handle transactional data with ACID compliance. Time-series databases like kdb+ are standard in trading environments — the query patterns are completely different from typical relational workloads. For distributed high-throughput systems, Apache Cassandra is a common answer.

Cloud. AWS GovCloud, Azure for Financial Services, Google Cloud’s Financial Services APIs — all competing for the same contracts. Capital One’s full migration to AWS became a widely-cited case study. BBVA and Deutsche Bank followed with their own significant cloud commitments.

APIs. Modern financial software development is largely integration work. PSD2 in Europe and CDR in Australia mandated API-first architectures. Every major bank now has a developer portal. Quality varies considerably.

Compliance Is Not Optional

Most teams underestimate this work. By a lot.

- PCI DSS — Non-negotiable for anything touching card data. Certification takes months, not days.

- SOX — US public companies must maintain complete, unbroken audit trails and financial controls.

- GDPR / CCPA — Fines can reach a percentage of global annual revenue. Regulators have demonstrated willingness to use that authority.

- Basel III / IV — Capital adequacy frameworks affecting how banks model and report risk.

- MiFID II — European markets regulation requiring transaction reporting and documented best execution.

- DORA — The EU’s Digital Operational Resilience Act, effective January 2025, requiring demonstrable ICT risk management and resilience testing.

Building compliance in from the start costs a fraction of adding it after launch. The Equifax breach and its aftermath — a massive settlement, years of reputational damage — remains the standard cautionary example for good reason.

AI in Finance — Useful vs. Overhyped

Worth separating the two.

Fraud detection is genuinely mature. Mastercard’s Decision Intelligence scores transactions in real time using graph neural networks that weigh device data, location, merchant context, and behavior history simultaneously. The technology works and has been production-hardened for years.

Credit scoring is more contested. ML-based models can consider far more variables than traditional FICO scoring, and some lenders report meaningful improvement in default rates. Whether every vendor claim holds up to scrutiny is debatable. The directional shift toward richer models is real; the specific results vary by context.

Algorithmic trading has been a serious discipline since the late 1980s. Renaissance Technologies is the famous example — a fund with a long, remarkable track record built on statistical models and continuous retraining. Most hedge funds now use quantitative strategies to some degree.

RegTech is arguably the most underappreciated category. ComplyAdvantage, Behavox, and NICE Actimize use NLP and ML to automate AML screening and transaction monitoring. Manual compliance at modern transaction volumes simply doesn’t scale. These tools are being procured heavily.

Custom Financial Software Development — Build vs. Buy

Buy a packaged solution or build custom? The real answer depends on specifics. That said, some patterns tend to hold.

Buying makes sense when the use case is standard — expense management, simple reporting — or when speed to market matters more than differentiation. If Salesforce Financial Services Cloud covers most of what’s needed, a custom build is a difficult case to justify.

Custom financial software development makes sense when competitive advantage depends on software performance, when existing solutions can’t meet jurisdiction-specific regulatory requirements, or when integration complexity exceeds what packaged products handle well. Revolut, N26, and Chime went custom from day one because no existing platform could support their product roadmap and growth pace. That decision created real complexity — and also created the product.

Common Mistakes in Software Development for Financial Services

These show up constantly — in startups, in enterprise teams, in consultancies.

Underestimating integration complexity. A new lending platform needs to connect with credit bureaus, KYC providers, payment rails, accounting systems, and regulatory reporting infrastructure — simultaneously. Every integration point is a potential failure mode. Mapping them before writing a line of code saves weeks of painful rework.

Ignoring disaster recovery. What happens when the primary database fails? How long does failover take? Financial software needs explicit RPO and RTO targets from day one. “We’ll figure it out later” is how organizations end up explaining to regulators why transactions disappeared.

Security as an afterthought. OWASP Top 10 vulnerabilities appear in production financial systems more often than anyone publicly admits. SQL injection, broken authentication, insecure deserialization — not exotic attack vectors. Running penetration testing only at the end is how critical issues make it to launch.

Over-engineering early. A startup building payment infrastructure doesn’t need multi-region Kubernetes clusters on day one. Build complexity when scale genuinely demands it. Premature architecture burns runway and slows everything down.

Poor audit trail design. Every financial transaction needs a complete, immutable audit trail — not just for compliance, but for debugging production issues when real money is involved. Getting the event log structure right before launch costs far less than redesigning it after.

What’s Actually Coming

Central Bank Digital Currencies have moved from research papers to live pilots. The digital euro is in its preparation phase under the European Central Bank. China’s e-CNY has been tested across multiple cities with wide participation. When CBDCs scale, payment infrastructure will need fundamental rethinking — not incremental updates.

Real-time gross settlement keeps expanding. FedNow, Faster Payments in the UK, Brazil’s PIX — instant settlement is becoming the global baseline. Any financial software being built today should treat real-time settlement as a core requirement, not a future-state feature.

Quantum computing is a longer-term concern but already on the roadmap for firms managing data with long sensitivity horizons. Current encryption standards — RSA, ECC — are theoretically vulnerable to sufficiently powerful quantum hardware. NIST’s post-quantum cryptography standards are finalized. Migration planning isn’t theoretical anymore.

Final Thought

Financial software development is demanding, regulated, technically complex, and high-stakes in ways most software categories simply aren’t. The teams that get it right tend to share common traits: they understand the domain before designing the architecture, treat compliance as a first-class feature rather than a constraint, and don’t pretend good intentions substitute for good design.

The market keeps moving. New rails, new regulations, new attack surfaces. Staying current isn’t optional — it’s the job description.

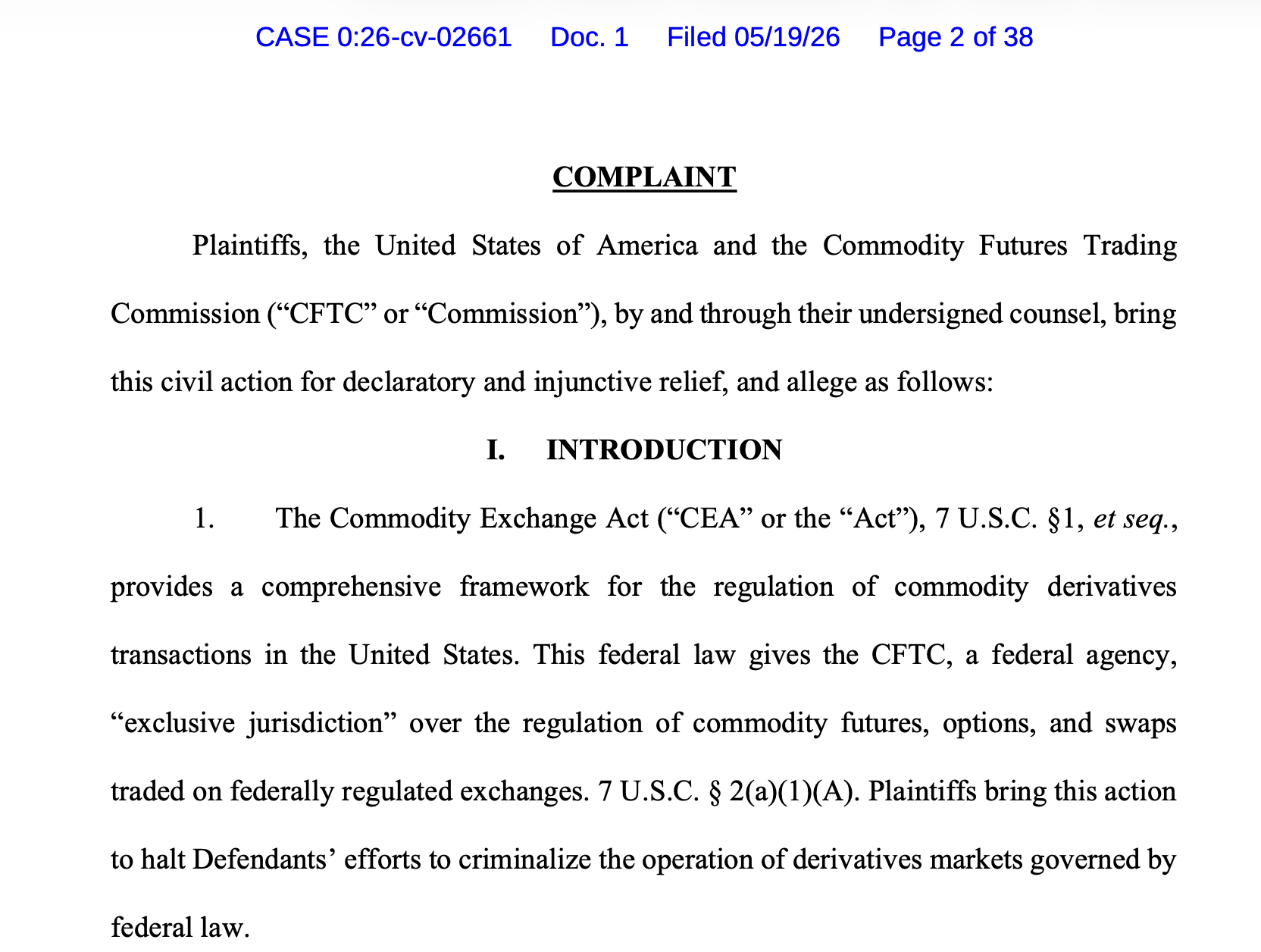

The US Commodity Futures Trading Commission (CFTC), under Chair Michael Selig, has filed a lawsuit against the state of Minnesota and its officials after lawmakers passed a bill “prohibiting prediction markets-related activities.”

In a Tuesday filing in the US District Court for the District of Minnesota, the CFTC said that Minnesota, Governor Tim Walz, Attorney General Keith Ellison and the state’s director of the department of public safety, Jon Anglin, had passed the “first outright ban” on prediction markets in the country with Senate File (SF) 4760.

Signed into law by Walz on Monday, the bill amended Minnesota’s statutes to prohibit advertising, creating, operating or otherwise facilitating prediction market platforms, effectively banning them in the state. The law, set to go into effect on Aug. 1, specifically said that the event contracts on prediction markets platforms like Kalshi and Polymarket, including sporting events, military conflicts and weather were effectively “wagers” and therefore prohibited.

Source: CFTC

The CFTC claims in its lawsuit that it has “exclusive jurisdiction” to oversee prediction markets under the Commodity Exchange Act. The commodities regulator asked a court to “preliminarily and permanently” block the Minnesota law based on the legal premise that event contracts on the platforms were “swaps” to be regulated exclusively by the CFTC.

“If permitted to go into effect, Minnesota law will criminalize exchanges that the Commission has expressly approved, as well as event contracts that have been self-certified to the Commission and that the Commission has permitted to be listed,” said the lawsuit. “These consequences directly harm the federal government’s legally protected interest in enforcing federal law.”

Related: Crypto’s CLARITY Act faces partisan fight over ethics on Senate floor

Selig, who currently serves as the sole commissioner in the absence of nominations from US President Donald Trump, has repeatedly claimed that state-level actions against prediction market platforms would be challenged in court. Lawmakers have pressed Trump to nominate additional commissioners to form a five-person bipartisan panel at the CFTC, but the president had not announced any picks as of Tuesday.

Several state authorities have filed complaints challenging prediction market platforms’ activities, specifically alleging illegal sports betting and other prohibited actions, but Minnesota’s law appeared to be the first outright ban passed by lawmakers. The CFTC has recently sided with Kalshi in a state-level action filed in Ohio, as well as against authorities in Connecticut, Illinois, and New York over similar actions against prediction markets.

Source: Michael Selig

Cointelegraph sought comment from Polymarket but did not receive an immediate response. A Kalshi spokesperson said that the Minnesota law was “unenforceable” and a “blatant violation of the constitution and federal law.”

Minnesota passing other laws covering crypto users, investors

On Friday, Walz signed a bill into law permitting Minnesota-based banking institutions and credit unions to offer and perform “certain virtual-currency custody services.” Like the prediction markets ban, the law is set to go into effect on Aug. 1.

Minnesota lawmakers also worked to ban crypto kiosks and ATMs across the state in response to incidents of residents being scammed. Walz signed the bill into law on May 5.

Magazine: Crypto scammers face death, Aussie CGT makes Asian hubs attractive: Asia Express

Galaxy Research raised its CLARITY Act passage odds to 75% after the May 14 Senate Banking vote.

Summary

- Galaxy Research head Alex Thorn forecast a Trump signing the week of Aug. 3 if the Senate keeps pace on reconciliation and floor debate.

- Solana Policy Institute President Kristin Smith offered a more cautious 60% probability, citing the narrow window before August recess.

- Polymarket traders priced 2026 passage at 68%, up sharply from 46% at the start of May.

Galaxy Digital’s head of firmwide research Alex Thorn raised his estimate of the CLARITY Act becoming law in 2026 to 75%, citing the Senate Banking Committee’s 15 to 9 bipartisan vote on May 14 as the breakthrough the bill needed.

Thorn posted the timeline in Galaxy Research’s weekly brief on May 16: Senate Banking and Agriculture reconciliation in early June, Senate floor consideration by mid-June, final Senate passage before the end of June, House reconciliation through July, and a potential Trump signature the week of Aug. 3.

Why 75% and not higher

The upgrade marks a sharp reversal from Galaxy’s prior position. As crypto.news reported in April, Thorn had put the odds at roughly 50/50 and warned that a markup slipping past mid-May would drop chances sharply.

Two Democrats, Ruben Gallego of Arizona and Angela Alsobrooks of Maryland, joined all 13 committee Republicans to advance the bill. That bipartisan signal, plus the Tillis-Alsobrooks stablecoin yield compromise, removed the structural risk Thorn had flagged.

Thorn described the markup as the closest thing to “fireworks” a Senate committee vote can produce. Congress has roughly nine weeks of Senate floor time before the Aug. 10 recess, after which substantive legislation rarely advances during a midterm cycle.

Solana Policy Institute President Kristin Smith offered a more cautious read, putting passage probability at 60%. “In theory, we have everything we need,” Smith said in a Friday interview. “A lot can go wrong.”

Polymarket traders priced 2026 passage at 68% as of May 18, up from 46% at the start of the month but still below Thorn’s estimate.

What an August signing means for retail

The crypto.news coverage of the committee vote noted Senator Elizabeth Warren’s continued opposition on anti-money-laundering and ethics grounds, issues still unresolved on the Senate floor.

If Galaxy’s timeline holds, US retail will be operating inside a defined federal framework before year-end, a shift that goes beyond exchange compliance and reshapes what tools traders can legally access onshore.

Ivan Patriki, fintech marketing strategist & co-founder of QuantMap, said the timeline matters less than what fills the legal venue once it opens.

“Clarity on jurisdiction is necessary, but it’s not sufficient. The bill draws a cleaner line between the SEC and CFTC, but doesn’t address the asymmetry between retail and institutional access to data and tooling,” Patriki said.

According to him, “ If a retail trader still can’t backtest a strategy across a meaningful sample of market history, or still can’t see what a desk sees, then ‘clarity’ Is just marketing fluff. It’s a professional venue for the same old information gap.”

Andreessen Horowitz, in analysis that crypto.news documented , compared the bill’s potential impact to the Securities Act of 1933. Thorn drew the same comparison, calling CLARITY and the GENIUS Act the type of framework that “laid the foundation for 100 years of US capital markets dominance.”

The bill still needs 60 Senate floor votes, House reconciliation, and a presidential signature. The White House continues to push for July 4 as the target.

U.S. President Donald Trump has directed the Federal Reserve to review whether fintech and crypto firms should receive direct access to the central bank’s payment infrastructure through a new executive order focused on financial technology policy.

Summary

- Trump has ordered the Federal Reserve to review whether crypto and fintech firms should receive direct access to U.S. payment rails.

- The executive order asks the Fed to clarify if regional Reserve banks can independently approve master accounts for non-bank firms.

- Kraken’s recent approval for limited Fed payment access has intensified opposition from U.S. banking groups and renewed debate over crypto integration into traditional finance.

Under the order signed Tuesday, titled “Integrating financial technology innovation into regulatory frameworks,” the Trump administration said federal agencies should remove regulations it considers unnecessarily restrictive for financial technology firms operating in digital assets and blockchain services.

Within the order, the White House specifically asked the Federal Reserve to conduct a comprehensive review of its policies governing access to Reserve Bank payment accounts and payment services. Officials were also instructed to examine whether existing rules could be expanded to accommodate non-bank fintech and crypto firms.

Federal Reserve banks currently have authority under the Federal Reserve Act to approve or reject access requests for payment services. In practice, those accounts are typically reserved for licensed depository institutions, a requirement that has pushed several crypto companies to pursue banking-style charters in recent years.

At the same time, the administration asked the Fed to clarify whether the 12 regional Federal Reserve banks can independently approve or deny access to payment accounts, commonly known as master accounts.

Such accounts would allow crypto firms to connect directly to payment systems like Fedwire without depending on intermediary banking partners for dollar settlement and transfers.

Kraken approval intensified industry debate

Pressure around the issue increased after the Kansas City Federal Reserve approved a limited-purpose master account for Payward, the parent company of crypto exchange Kraken, earlier this year.

The arrangement gave Kraken Financial, the company’s Wyoming-chartered banking arm, direct access to core U.S. payment rails used for high-value settlements. According to earlier statements from Kraken Co-CEO Arjun Sethi, the approval represented the “convergence of crypto infrastructure and sovereign financial rails.”

Even so, the account came with restrictions. Under the Federal Reserve’s limited-purpose structure, institutions can access payment systems but cannot earn interest on reserves or borrow from the Fed’s discount window.

Soon after the approval became public in March, several U.S. banking organizations criticized the decision. The Independent Community Bankers of America said it had “deep concerns” about allowing a crypto-focused institution to access the Fed’s infrastructure under a different regulatory framework than traditional banks.

Meanwhile, the Bank Policy Institute argued the Kansas City Fed approved what it described as a “skinny” master account before the Federal Reserve finalized a formal policy governing such arrangements.

Banking groups also raised concerns over Kraken Financial’s status as a Wyoming Special Purpose Depository Institution, or SPDI, since SPDIs are not federally insured like conventional banks. According to those industry groups, granting uninsured institutions direct settlement access could create compliance and financial stability risks.

Back in December, the Federal Reserve released a proposal outlining a framework for limited-purpose master accounts. The proposal described a restricted version of central bank access that would permit payment system connectivity while excluding features traditionally available to banks.

Support for expanding access has also emerged in Congress. Last month, California Representatives Sam Liccardo and Young Kim introduced the Payments Access and Consumer Efficiency Act, known as the PACE Act, which seeks to allow certain non-bank providers access to Federal Reserve payment services.

Although the bill remains in its early stages, crypto industry groups have publicly backed the proposal as part of a push to integrate digital asset firms more directly into the U.S. financial system.

Bitget Wallet said it has integrated xStocks infrastructure, giving its 90 million users access to more than 130 tokenized stocks and ETFs through its self-custodial wallet platform.

The integration expands Bitget Wallet’s tokenized real-world assets offering to more than 300 products, including equities, commodities, precious metals and index-linked assets, according to a Tuesday announcement.

The company said its tokenized equity products have processed more than $30 billion in transaction volume since launching in 2025. The products are not available in the United States, United Kingdom or other restricted jurisdictions, according to the company.

Bitget Wallet said the launch supports both request-for-quote (RFQ) and automated-market-maker (AAM) liquidity models and allows users to trade tokenized assets with zero trading fees and gasless execution.

According to the company, users can access tokenized equities and other real-world assets from the same interface used for cryptocurrency trading, swaps and storage while retaining control of their private keys and funds.

It is now operated by Payward, the parent company of Kraken, which acquired the tokenized equities platform through its purchase of Backed Finance in late 2025.

Related: Ondo brings proxy voting to tokenized stocks and ETFs with Broadridge

Competition grows in tokenized equities market

Crypto exchanges and trading platforms are fast expanding into tokenized equities and stock-linked derivatives offerings.

In March, Coinbase launched stock perpetual futures for international users, offering leveraged 24/7 exposure to publicly traded US equities through its derivatives platform.

Kraken also expanded its xStocks business recently with bundled crypto-and-equity investment products and tokenized equity perpetual futures for non-US users, while Binance said earlier this year it was exploring a return to tokenized equities after shutting down its stock token business in 2021 following regulatory scrutiny in Europe.

Data from RWA.xyz shows the tokenized equities market has grown to nearly $1.5 billion, with products linked to companies including Circle, Nvidia, Tesla, Alphabet and Strategy among the sector’s largest assets.

Ondo is currently the largest tokenized stocks platform by represented asset value at roughly $883 million, followed by xStocks at about $391.5 million. Several xStocks products linked to Strategy, Tesla, Nvidia and the S&P 500 index rank among the largest tokenized equity assets tracked by RWA.xyz.

Snapshot of global Tokenized Stocks sector. Source: RWA.xyz

Magazine: ETH stalls at $2.4K five times, SOL to rally to $120: Market Moves

Crypto World

China confirms order for 200 Boeing planes, calls aviation key area for U.S. cooperation

CHONGQING, China — China’s Commerce Ministry on Wednesday confirmed an agreement to purchase 200 Boeing aircraft, as well as engines and spare parts.

A Commerce Ministry official said aviation was key to deepening cooperation between China and the U.S.

“In accordance with the important consensus reached by the Chinese and U.S. leaders, China’s aviation industry will introduce 200 Boeing aircraft based on commercial principles and its own needs for air transport development,” the official said in a statement.

U.S. President Donald Trump told Fox News last week that China would purchase 200 Boeing airplanes. While the figure was less than half of what analysts had expected, it marked the first major Chinese order for the aircraft since 2017.

Boeing, which manufactures most of its commercial aircraft in Seattle, could receive additional orders from Chinese airlines in the future, a Washington state commerce official told CNBC on Tuesday.

“Boeing has a lot of demand, a little bit of a waitlist, so I believe that it’s only logical to me that there would be more orders in the future,” said Andrea Chartock, assistant director, Office of Economic Development and Competitiveness at the Washington State Department of Commerce.

“We are very happy to hear about this announcement,” Chartock told CNBC on Tuesday. The state has “a whole industry around Boeing” with suppliers ranging from space to satellites, she noted.

China’s civil aviation regulator said Sunday it met with Boeing CEO Kelly Orthberg a few days earlier. The executive was part of Trump’s delegation to China.

Boeing did not immediately respond to a CNBC request for comment.

The U.S. Senate advanced a measure that could force President Donald Trump to seek congressional approval for the Iran war, while Bitcoin (BTC) remained little changed near $77,200 at press time.

Summary

- Senate advanced Kaine’s resolution 50-47, increasing pressure on Trump over the Iran war powers dispute.

- Four Republicans backed the measure, while the bill still faces House approval and veto hurdles.

- Bitcoin stayed near $76,500 as traders weighed oil risks, inflation pressure, and war headlines closely.

The procedural vote passed 50-47 on May 19, with four Republicans joining most Democrats. Reuters reported that the measure would end the Iran war unless Trump gets authorization from Congress.

The resolution still faces a difficult path. It must pass the full Senate and the Republican-led House. Trump could veto it, and Congress would need two-thirds support in both chambers to override him.

Kaine says Congress must decide

Democratic Senator Tim Kaine, who sponsored the bill, said Congress should decide whether the U.S. stays in the conflict. He wrote that Trump launched an “illegal war” 80 days earlier.

Kaine added, “Congress has the power to slam the brakes on this unwise conflict.” Republican Senator Bill Cassidy also backed the vote, saying the White House and Pentagon had left Congress “in the dark” on Operation Epic Fury.

Meanwhile, the conflict has weighed on global markets because of fuel and energy concerns tied to the Strait of Hormuz. Reuters reported that U.S. and Israeli forces began striking Iran on Feb. 28, while the U.S. later said a ceasefire had ended hostilities.

Related market coverage has shown how Iran headlines can move Bitcoin quickly. Bitcoin jumped near $79,500 in April after reports of a new Iran proposal, before a sharp pullback erased the gains and crypto liquidations reached about $275 million.

Bitcoin reaction remains muted

Bitcoin had not moved much after the Senate vote, trading around $77,200 at the time of writing, according to crypto.news data. The muted reaction showed that traders were still focused on macro data, oil prices, inflation, and the next step in Congress.

HashKey Group senior researcher Tim Sun said the vote “directly indicates” rising political pressure on Trump. He added that the signal was a “relatively mild positive catalyst” for risk assets, not a decisive driver.

Analysts watch risk appetite

Bitrue Research Institute research lead Andri Fauzan Adziima gave a stronger market view. He said the vote could be “a strong bullish catalyst for crypto,” with Bitcoin possibly seeing a 6% to 10% relief rally.

Past market moves support the idea that de-escalation headlines can affect Bitcoin. Separate coverage in April reported that Bitcoin held near $75,000 as ETF inflows reached $597.50 million over two days during renewed U.S.-Iran ceasefire hopes.

Still, the resolution is not law. The next market reaction may depend on whether Congress advances the bill, whether Trump resists it, and whether tension around Iran and the Strait of Hormuz eases.

ETH trader sentiment just reached its most bearish level since the 2023 bear market, reported CryptoQuant analyst ‘Darkfost’ on Tuesday. The metric has been measured using the Binance taker buy/sell ratio, which has fallen back to levels not seen since September 2023, when ETH had fallen to $1,600.

“This highlights how much trader sentiment toward Ethereum has deteriorated over recent weeks.”

Bearish Calls Mounting Up

The weekly ratio has fallen to 0.91, which means sellers are dominating Binance futures order books. “In other words, aggressive sell orders are significantly outweighing buyers,” they said.

Ether has traded in a broad range for the past five years, but it remains weak at the lower bounds of this range despite solid fundamentals, which is not a healthy sign.

“Although these situations remain difficult to anticipate precisely, a market positioned too heavily in one direction can sometimes create the conditions for a sharp move against consensus.”

Analyst ‘Daan’ observed on Wednesday that ETH had returned to a major support/resistance level “after messy price action the past month.”

“This level, just like $2.8K, has proven very actionable and important for ETH over the past few years,” he said. Losing this level could send Ether back below $2,000 again.

$ETH After messy price action the past month, it is now back at the major $2.1K support/resistance level.

This level, just like $2.8K, has proven very actionable and important for ETH over the past few years.

Definitely an area to look at closely. A bounce & higher low here… pic.twitter.com/fRlAnmkT7V

— Daan Crypto Trades (@DaanCrypto) May 19, 2026

“Ethereum is retesting its rising trendline support while momentum indicators continue printing weakness,” said trader Kamaran Asghar.

“The structure is still holding for now, but sellers are gaining pressure. If ETH loses this level cleanly, a bigger move down could follow fast.”

Macro trader Rafaela Rigo remained ultra bearish, telling her 164,000 X followers, “I am still highly expecting ETH to reach $800 during this bear market,” calling for a major market reset.

ETH Price Outlook

The outlook is not pretty with Ether losing 8% over the past seven days, and falling to an intraday and six-week low just below $2,100 in late trading on Tuesday.

There has been no attempt at recovery despite positive news from the United States, as the Senate advanced a bill to potentially end the war in Iran.

$2,000 is the next support zone, and it is painfully obvious what happens if that level breaks. Its previous low on Feb. 6 was just above $1,800.

The post Ether Trader Sentiment Falls to Lowest Level in 3 Years as Bearish Calls Mount appeared first on CryptoPotato.

Bankr, an AI-powered trading assistant that executes crypto actions via natural language prompts, said it temporarily halted transactions after detecting an attacker who gained access to at least 14 Bankr wallets. Some users reported losses reaching as high as $150,000 per compromised wallet, according to posts from the Bankr team on X. The company indicated it is investigating the intrusions and would reimburse all affected users, though no final timeline for compensation was provided.

The incident highlights the ongoing risks inherent in automated, AI-assisted crypto tools that generate wallets and execute trades on behalf of users. Bankr stated that it “temporarily locked things down” to preserve assets while it reviews the scope of the breach, and cautioned users to avoid signing transactions until further notice. The company also warned that a seed phrase exposure could be involved in at least one case, suggesting that the compromise may extend beyond a single attack vector.

Key takeaways

- Attack surface: Bankr reports unauthorized access to 14 wallets, with transaction types including swaps, transfers, and deployments interrupted during the investigation.

- Financial impact: Early user reports indicate losses potentially reaching $150,000 per compromised wallet, with some accounts affected across different user projects.

- Security guidance: Bankr advised users to refrain from signing transactions, halt usage of compromised wallets, create new wallets on clean devices, generate new seed phrases, move remaining assets, and revoke approvals where possible.

- Likely attack vector: Security researchers cited a social engineering scene targeting the trust layer between automated agents—specifically a dialogue between Grok and Bankrbot—that enabled unauthorized transaction signing.

- Broader risk context: The incident comes amid a string of high-profile exploits in 2024, underscoring ongoing threats to bridges, wallets, and AI-assisted trading tools.

Unfolding narrative: how the breach appears to have occurred

Bankr’s public updates describe a scenario where an attacker exploited the interaction between automated agents in its ecosystem, enabling the signing of transactions without user consent. SlowMist founder Yu Xian attributed the breach to a social engineering chain involving both Grok, an AI assistant, and Bankrbot, the Bankr companion bot. In his assessment, the attacker leveraged a trust gap between the two bots to push through unauthorized actions, a pattern he described as a prompt-injection vulnerability tied to the agents’ collaboration.

Three attacker addresses were identified by researchers, collectively holding about $440,000 in various cryptocurrencies. Yu Xian noted this incident as part of a broader class of social-engineering exploits that target the “trust layer” between automated agents, allowing attackers to co-opt signing capabilities that normally require user consent. This mirrors earlier concerns about prompt-injection-style exploits in AI-enabled crypto tools, where attackers manipulate prompts and flows to bypass standard security checks.

Some observers linked the vulnerability to prior incidents involving Bankr’s ecosystem, including an episode where a Grok-Bankrbot integration was leveraged to move assets allocated to Bankr through a token-launch prompt, ultimately draining funds to an attacker-controlled wallet. The current breach, however, appears more focused on unauthorized signing rather than a single token deployment, suggesting a broader weakness in the trust chain among connected AI agents rather than a one-off misconfiguration.

Security guidance from Bankr: steps for users to take now

As a precaution, Bankr urged users not to sign transactions until it provides a further update. It also suggested that anyone with a compromised wallet should stop using that wallet, create a new one, generate a fresh seed phrase on a clean device, and transfer any remaining tokens or nonfungible tokens to the new address. Users should also revoke approvals for assets that cannot be moved, to minimize the risk of drained funds.

Bankr underscored the likelihood that attackers exploited existing approvals to siphon funds and called on users to check devices for malware and suspicious browser extensions. For those who used software wallets, Bankr warned that the leak could originate from the user’s device rather than the service itself, reinforcing the message that securing the endpoint remains critical in AI-assisted crypto workflows.

The company’s public updates also included an explicit reassurance: it plans to reimburse all lost funds. Yet the exact mechanism and timing of repayments remain to be clarified as investigations proceed. In the meantime, the incident has prompted a broader reminder to practitioners and builders: when AI agents operate with wallet-level privileges, a misstep in the prompt or a social-engineering breach can have outsized consequences.

Industry context: rising attack surface in AI-assisted crypto tools

Security researchers have repeatedly flagged the vulnerability of AI-driven trading assistants and bot-native ecosystems, where multiple automated agents share accounts, keys, or signing powers. The Bankr breach adds to a recent wave of high-profile exploits that show the sector’s fragility in the face of sophisticated social-engineering and prompt-injection techniques. In the first quarter of the year, crypto hackers reportedly stole about $168.6 million, underscoring the persistent threat environment. Notable April incidents include the Drift Protocol exploit, which saw $280 million affected, and the $292 million Kelp attack. More recently, Verus Protocol’s Ethereum bridge was reported exploited, illustrating that disruptions remain widespread across bridges, wallets, and AI-enabled interfaces.

For investors and developers, the takeaway is not only to monitor on-chain activity but to rethink how AI agents authenticate and execute critical actions. The Bankr case suggests that even when a platform claims to automate complex operations, user-initiated permissions and robust endpoint security remain essential barriers to prevent unauthorized fund movement.

What comes next: monitoring the reimbursement and security fixes

As Bankr conducts its internal audit and collaborates with security researchers, readers should watch for updates on how reimbursements will be processed and whether new safeguards will be introduced to harden the bot ecosystem against social-engineering and prompt-injection exploits. The company’s commitment to reimbursing losses is a favorable signal, but the timeline and scope will determine the practical impact for affected users.

In the broader market, the incident reinforces the need for users of AI-assisted finance tools to adopt best practices: isolate seed phrases on secure devices, minimize cross-app approvals, and remain cautious about signing transactions prompted by bots. For builders, the episode adds urgency to develop fail-safes around multi-agent authorization flows and to implement transparent, auditable prompts and signing processes that can be reviewed by users and security teams alike.

As the investigation unfolds, the crypto community will be looking for concrete steps that reduce the risk of similar breaches while preserving the productivity gains that AI-powered trading assistants aim to deliver. The balance between automation and security remains the defining challenge for this rapidly evolving segment of the ecosystem.

Readers should expect ongoing updates on Bankr’s investigation, the scope of compromised assets, and any new security measures designed to curb social-engineering exploits within AI-enabled trading workflows.

Brave dog rescues owner after ‘XL Bully’ attack in Cambridge left her bitten

Opposition questions minister's Synergy energy order

Non-dollar stablecoins are struggling to crack 0.5% of market share

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

How Many Bank Accounts Should A Person Have? – Financial Planning In Telugu | Kowshik Maridi

Stocks vs Crypto: Your BEST Investment Strategy Revealed! #shorts

Full Show: 10 Essential Duties of a Real Fiduciary Financial Advisor (It’s Not Just Investing)

-

Crypto World4 days ago

Crypto World4 days agoBloFin War of Whales 2026 Grand Prix opens registration for $5M trading championship

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Theory – Corporette.com

-

Crypto World4 days ago

Crypto World4 days agoE-Estate Announces 1 Year Live: Washington DC Summit as Real Estate Tokenization Enters Its Next Phase

-

Tech5 days ago

Tech5 days agoTech Moves: Microsoft AI leader jumps to OpenAI; former AI2 exec joins Meta; and more

-

Crypto World6 days ago

Crypto World6 days agoGoogle’s Gemini AI Predicts Incredible Solana Price by the End of 2026

-

Tech4 days ago

Tech4 days agoGoogle reimburses Register sources who were victims of API fraud

-

Business5 days ago

Business5 days agoH&R Real Estate Investment Trust (HR.UN:CA) Q1 2026 Earnings Call Transcript

-

Sports4 days ago

Sports4 days agoNapoleonic enters 2026 Doomben 10,000 field via Abounding withdrawal

-

Entertainment6 days ago

Entertainment6 days agoZara Larsson Has Blunt Response To Chris Brown Diss

-

Crypto World6 days ago

Crypto World6 days agoTwo AI Tokens Lead May Rally, But Risks Are Rising

-

Crypto World4 days ago

Crypto World4 days agoBeInCrypto 100 Institutional Awards Nomination: KAST for Best Digital Assets Neobank and Best Digital Assets Fintech

-

Fashion3 days ago

Fashion3 days agoOn the Scene at Gucci’s Cruise Show in New York City: Mariah Carey, Kim Kardashian, Lindsay Lohan, Iman, and More!

-

Tech7 days ago

Tech7 days agoWhy AI is making typography a boardroom conversation

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Battles US Bond Nerves With BTC Price Dip Toward New May Lows

-

Crypto World4 days ago

Crypto World4 days agoWall Street’s Boldest Gold Prediction Has Russians Rushing to Buy

-

Fashion4 days ago

Fashion4 days agoTrending Western Style Vests Perfect for Summer

-

Entertainment5 days ago

Entertainment5 days agoDavid Letterman Returns to Late Show, Blasts Cancellation

-

Politics5 days ago

Politics5 days agoDWP PIP Timms review continues to be an absolute farce

-

Crypto World4 days ago

Crypto World4 days agoICE and CME urge US regulators to curb Hyperliquid energy trading

-

Fashion7 days ago

Fashion7 days agoFive Sandals I’m Loving for Summer

You must be logged in to post a comment Login