Crypto World

Why HYPE is different: inside Hyperliquid’s buyback

Most crypto tokens have “buyback” mechanisms that are either nominal, sporadic, or theoretical. HYPE has something genuinely different.

Summary

- Hyperliquid’s Assistance Fund uses 97% of protocol trading fees to buy HYPE tokens directly from the open market through an automated on-chain system.

- The fund has spent more than $1.3 billion on HYPE buybacks, with the mechanism running at an annualized rate estimated near 7% of the token’s market cap.

- Analysts tracking HYPE’s tokenomics say the continuous buyback structure has created one of the most aggressive revenue-driven value accrual models in the crypto market.

The Assistance Fund directs 97% of Hyperliquid’s protocol fees into continuous, automated market purchases of (HYPE), removing tokens from circulation every day. By May 2026, the Fund had spent over $1.3 billion buying back HYPE, holding roughly 28.5 million tokens worth $1.5 billion at peak prices.

At an annualized rate of roughly 7% of market cap, HYPE’s buyback intensity is four to five times Ethereum’s and BNB’s. That math is the structural reason behind the rally that most price commentary cannot explain. This is how the mechanism actually works, why it scales differently from every other major crypto token, and what would have to break for the model to fail.

The mechanism in plain terms

The Hyperliquid Assistance Fund is a part of the protocol that makes HYPE’s tokenomics genuinely different from every other large-cap cryptocurrency, and almost no coverage explains it properly.

In plain terms: every time someone trades on Hyperliquid, they pay a fee. That fee gets aggregated into a protocol-controlled pool called the Assistance Fund. The Fund then uses 97% of those accumulated fees to buy HYPE tokens directly from the open market. The purchases run continuously, automated by on-chain logic, with no manual intervention from the team. The HYPE bought back is held by the Fund itself, removing those tokens from the active circulating supply.

The numbers are not theoretical. By October 2025, the Assistance Fund’s total purchases had passed $1.3 billion. Daily buybacks averaged around $1 million, with single-day peaks reaching $3.97 million. By Q3 2025, the Fund held nearly 29.8 million HYPE tokens, valued at over $1.5 billion. By March 2026, the Fund had accumulated roughly 28.5 million HYPE through systematic open-market purchases.

Hyperliquid accounted for 46% of all token buyback activity across the crypto industry in 2025, with monthly buybacks averaging $65.5 million.

That last statistic is worth pausing on. Almost half of all crypto buyback activity in 2025 came from a single protocol. The scale is genuinely different from anything else in the industry.

The mechanism is automated and transparent. Validators publish the rules. The smart contracts execute the purchases. Every buyback transaction is visible on chain. There is no “we will buy back tokens when we feel like it” element. The 97% allocation is encoded in the protocol’s economic design, and the Fund operates as a continuous market participant, always bidding, always buying.

A December 2025 governance vote, passed by 85% of validators, raised the allocation to 99% for certain fee categories and committed to permanent token burns on a portion of the Fund’s holdings.

The vote was significant for two reasons. First, it took the buyback model from “policy that could change” to “governance-enforced commitment.” Second, it added a deflationary component: tokens bought back and then burned are permanently removed from supply, which is structurally different from tokens bought back and held in a treasury that could theoretically be resold.

This is the engine. The rest of the piece explains why it matters more than most readers realize.

Why this is not just another buyback program

Crypto has a long history of token buyback announcements that turn out to be less than they appear. Some are one-time events. Some are sporadic and tied to discretionary team decisions. Some are funded by token treasury sales rather than real revenue, which is roughly equivalent to printing money to buy back money. The market has, reasonably, learned to discount buyback announcements as marketing rather than substance.

HYPE is genuinely different on three dimensions.

First, the source of the funding is real. The Assistance Fund’s purchases are funded entirely by trading fees from actual transactions. Hyperliquid’s protocol revenue runs at roughly $1.3 billion in annualized fees as of mid-2026, with the platform regularly beating Ethereum and Solana on weekly blockchain fee generation. The buybacks are not subsidized by token issuance, treasury depletion, or external capital.

They come from users actually using the protocol and paying actual fees. If trading volume goes up, buybacks go up. If trading volume goes down, buybacks go down. The mechanism is mechanically tied to real economic activity, not to founder discretion or marketing cycles.

Second, the share of revenue going to buybacks is exceptional. Most crypto tokens with buyback or burn mechanisms route a small percentage of revenue toward token economics. BNB burns roughly 20% of its quarterly profits. Ethereum burns a variable share of gas fees via EIP-1559, with the rate depending on network congestion. Solana directs roughly 50% of priority fees to burns. HYPE’s 97% allocation is, by a wide margin, the most aggressive fee-to-token-economics ratio of any major crypto asset. The protocol effectively treats trading fees as token holder revenue rather than operating budget.

Third, the execution is fully automated and transparent. The Assistance Fund runs on chain. Every purchase is visible. Every transaction is verifiable. There is no off-chain accounting, no discretionary timing, no “we’ll announce the burn next quarter” framing. The mechanism runs like an algorithmic market participant always bidding for HYPE, funded by the trading activity of the network it runs on.

To use a comparison that makes the difference concrete: when Binance burns BNB, it makes a quarterly announcement, calculates the burn amount based on metrics it controls, and executes a single transaction. When Hyperliquid buys back HYPE, it happens every day, in continuous small purchases, funded by every trade that ran since the last buyback. The Binance model gives BNB holders four discrete moments of supply reduction per year. The Hyperliquid model gives HYPE holders a constant supply-reduction force that scales with network usage.

The implications of that difference are substantial, and they show up in the math.

The math compared to other major tokens

The clearest way to see why HYPE is structurally different is to look at the buyback or burn rate as a%age of market capitalization, annualized. This normalizes for the fact that bigger tokens can buy back more in absolute terms while still doing less relative to their size.

Ethereum burns approximately 1.5% of its market cap annually through EIP-1559, depending on network usage. The burn rate scales with congestion, so it varies, but the long-term average sits in that range.

BNB burns approximately 1.2% of its market cap annually through its quarterly burn program. The rate is moderately stable because it is tied to Binance’s overall profitability, which scales more slowly than network usage.

Solana burns roughly 0.5% of its market cap annually through priority fee burns. The rate is lower than Ethereum’s because the share of fees burned is smaller and the protocol relies more heavily on issuance for validator rewards.

HYPE’s buyback rate is approximately 7% of market cap annually at current revenue levels. This is four to five times Ethereum’s rate, six times BNB’s rate, and fourteen times Solana’s rate. The disparity is not marginal. It is structurally different.

What this means in practice is straightforward. For every $100 of HYPE you hold, the Assistance Fund is, on average, buying back roughly $7 worth of HYPE from the market each year on your behalf. That buy pressure is funded by protocol revenue, scales with trading volume, and runs regardless of HYPE’s price or your individual actions. It is the closest thing to a dividend that exists in major crypto, except it shows up as supply reduction and accumulated treasury holdings rather than as cash distributions.

The 7% figure understates the structural intensity in another way. The buyback rate is computed against current market cap. As Hyperliquid’s trading volume grows, the absolute size of the buybacks grows. As the buybacks grow against a finite supply, the supply shrinks. As the supply shrinks against constant or rising demand, the price rises. As the price rises, the same absolute buyback in dollar terms removes fewer tokens, which means the supply pressure stabilizes at higher prices rather than running away to infinity. The math is self-balancing, but the balance point is meaningfully higher than what a pure fundamental valuation would suggest.

This is what Arthur Hayes meant when he called HYPE “fundamentally de-risked” in his Valhalla thesis from earlier in 2026. He was not saying HYPE has no risk. He was saying the buyback mechanism creates a structural floor that scales with adoption, which is a feature most tokens do not have.

Why this matters for the token unlock schedule

One of the most common bear arguments against HYPE is the token unlock schedule. The argument goes like this: HYPE has a maximum supply of approximately 1 billion tokens. The circulating supply is around 254 million as of late May 2026. That means roughly 75% of the total supply has not yet entered circulation. As tokens vest from team, investor, and reward allocations, they will enter the market over the coming years and create persistent selling pressure that the protocol cannot offset.

The argument is not wrong, but it is incomplete. The honest analysis requires comparing the inflation rate from unlocks against the deflation rate from buybacks.

The token unlock schedule for HYPE is back-loaded. The largest tranches of vesting do not begin until 2027 and beyond, with team and investor allocations subject to multi-year cliffs and gradual release. This is different from many recent crypto tokens, where significant unlocks hit in the first 12 to 18 months of trading and produce structural selling pressure during the period when the token is most fragile.

Between now and the start of major team and investor unlocks, the Assistance Fund keeps buying. At the current rate of roughly $65.5 million per month in buybacks, the Fund accumulates approximately 1.3 million HYPE per month at current prices, or roughly 15 to 16 million HYPE per year. If that pace holds unchanged through the next eighteen months, the Fund will have absorbed an additional 25 million HYPE from the market by the time major unlocks begin.

This does not eliminate the unlock pressure. It does shift the balance. The unlocks will create selling pressure when they arrive. The buybacks have been creating buying pressure all along. The question is which force is larger at any given moment, and the answer depends on how Hyperliquid’s trading volume scales between now and then.

If trading volume keeps growing, the Assistance Fund’s buying pressure grows proportionally, and may offset more of the unlock supply than skeptics expect. If trading volume stagnates, the unlock pressure dominates. The protocol’s success or failure as a derivatives venue is therefore the key variable. The tokenomics are not the bull case in isolation. They are the bull case conditional on continued protocol growth.

The HLP, the Assistance Fund, and the staking layer

There are three distinct components of Hyperliquid’s tokenomics that get conflated in most coverage, and they are worth distinguishing because each operates differently.

The Assistance Fund is the buyback engine described above. It collects 97% of trading fees and uses them to buy HYPE from the open market. The Fund holds the purchased HYPE in a protocol-controlled wallet. A portion of holdings is subject to governance-approved permanent burns.

HLP (Hyperliquidity Provider) is the protocol’s market-making vault. Users deposit USDC into HLP and earn returns from market-making activities, including spreads, funding payments, and liquidation profits. HLP serves as the counterparty to traders on the protocol. Its returns are inversely correlated with trader profitability, meaning HLP earns more when traders lose money and earns less when traders are profitable. HLP is separate from the Assistance Fund. It does not buy HYPE. It is a yield-generating product for USDC depositors.

HYPE staking lets HYPE holders stake their tokens to earn additional rewards. Stakers receive a portion of certain protocol fees not routed to the Assistance Fund, plus inflationary rewards from the network’s reserve allocation. Staking also confers governance rights, including voting on protocol changes and Assistance Fund parameters. As of mid-2026, HYPE staking is increasingly used by ETF issuers (Bitwise, in particular) to enhance fund returns and align with the protocol.

The interaction between these three components is what creates Hyperliquid’s full economic flywheel. Traders pay fees. Fees fund the Assistance Fund buybacks. HLP captures the counterparty side of trading activity. Stakers earn from fees not routed to the Assistance Fund. The flywheel is self-reinforcing: more trading produces more buybacks, which support price, which attracts more capital, which enables more trading.

The May 14 AQAv2 deal added a fourth component: reserve yield from USDC balances on the platform, redirected back to the protocol and ultimately to HYPE holders. This is structurally separate from the Assistance Fund but adds to the total economic value flowing to the token. The combined effect is that HYPE holders capture revenue from three distinct streams: trading fees (via buybacks), stablecoin reserves (via AQAv2), and ETF management fees (via the Bitwise allocation).

Three structural revenue streams are unusual in crypto. Most tokens have one source of value accrual, if any. HYPE has three. Each runs continuously. Each scales with adoption.

What could break the model

A fair piece on HYPE’s buyback mechanism has to name the conditions under which the model could fail or degrade. There are several worth taking seriously.

The first risk is trading volume decline. The buyback mechanism is mechanically tied to trading fees. If Hyperliquid’s trading volume drops significantly (because of competition, regulatory pressure, or a broader crypto market downturn), the Assistance Fund’s purchases drop proportionally. The mechanism does not have a floor. It scales with usage in both directions. A sustained 50% drop in trading volume would cut buyback intensity from 7% of market cap annually to roughly 3.5%. Still better than most tokens. Less compelling than the current rate.

The second risk is fee compression. Hyperliquid’s competitive position currently lets it charge meaningful fees for trading. If centralized exchanges (Binance, Coinbase, OKX) lower their fees aggressively, or if competing decentralized perpetual protocols (Aevo, dYdX, GMX) capture market share, Hyperliquid may need to reduce fees to stay competitive. Lower fees would mean lower buybacks at the same volume.

The third risk is governance changes. The 97% allocation is set by validator vote. A future governance vote could lower the allocation, redirect fees to other purposes, or alter the Fund’s burn policy. The December 2025 vote that raised the allocation toward 99% was supportive, but the same governance system could reduce it. The protocol’s commitment to the buyback model is real but not constitutional. It is policy, not bedrock.

The fourth risk is technical or operational failure. The Assistance Fund runs on Hyperliquid’s Layer-1 blockchain. A serious failure of the chain, the validator set, or the smart contracts that automate the buyback would interrupt the mechanism. Hyperliquid has run cleanly so far, but the protocol is younger than Ethereum or Solana, and the next major operational issue is, by base rate, eventually coming.

The fifth risk is regulatory. Token buybacks funded by protocol fees occupy an ambiguous space in U.S. securities law. If a regulator chose to characterize the buyback mechanism as a security distribution to token holders, the legal pressure on Hyperliquid would be significant. The protocol’s defense (it is a permissionless decentralized exchange and the buybacks are automated by smart contracts) is similar to Uniswap’s defense and has held up so far, but the broader regulatory environment for DeFi tokenomics in the U.S. is still evolving.

None of these risks invalidates the model. They are the conditions under which it could weaken. The honest read is that HYPE’s buyback mechanism is the most aggressive and structurally interesting in major crypto, but its continued effectiveness depends on Hyperliquid’s trading volume holding up, governance keeping the policy intact, and regulators not taking adverse action. All three conditions can be met. None is guaranteed.

The comparison nobody runs

The most useful exercise for understanding HYPE’s tokenomics is one nobody in mainstream crypto coverage runs: comparing HYPE directly to a hypothetical equity with similar cash flow characteristics.

Consider Hyperliquid’s economics in equity terms. The protocol generates roughly $1.3 billion in annualized revenue (trading fees). 97% of that revenue is used to buy back the token, which is the equivalent of an equity issuer using 97% of its revenue to buy back its own stock from the open market.

For a public equity, this would be extraordinary. Apple, by comparison, returns roughly 25 to 30% of its revenue to shareholders through buybacks and dividends. Berkshire Hathaway returns close to 0% (Buffett famously prefers reinvestment). The typical S&P 500 company returns somewhere between 5 and 15%. A company that returned 97% of revenue to shareholders would be an outlier so extreme that analysts would assume either fraud or imminent operational collapse.

HYPE’s “operational expenditure” is largely covered by the network’s validator and infrastructure rewards, which come from inflationary token allocation rather than trading fees. This is what makes the 97% number sustainable in a way it would not be for a traditional company. The protocol’s growth investments, validator payments, and ecosystem development are funded by token issuance to specific allocations, while trading fees flow almost entirely to existing token holders via buybacks.

In equity terms, this is a structure where the company’s growth is funded by issuing new shares while existing shareholder value is supported by aggressive buybacks of existing shares. The combined effect is dilution for new participants and concentration for existing holders. Whether this is sustainable depends on whether the growth funded by issuance generates enough new value to offset the dilution.

So far, it has. Hyperliquid’s revenue has grown faster than its dilution, which means existing holders have benefited net-net from the structure. The question is whether this keeps going as the protocol matures and as the token unlock schedule accelerates.

The comparison to traditional equity is imperfect (crypto tokens are not equity, and the legal structures differ in important ways), but it is useful for understanding what HYPE’s tokenomics are actually doing economically. The token is, in effect, a high-payout-ratio claim on a fast-growing piece of financial infrastructure. The closest traditional analog might be a high-yield REIT that retains very little capital and distributes nearly everything to shareholders, except that HYPE distributes via buybacks rather than dividends, and the underlying business is decentralized derivatives trading rather than real estate.

That is what makes HYPE genuinely different. Most crypto tokens are either pure speculation (no underlying cash flow) or low-payout infrastructure plays (Ethereum, Bitcoin). HYPE is a high-payout, high-growth cash flow claim. It is not pretending to be something else. The tokenomics are real, the cash flow is real, and the math is unusual enough that most crypto coverage simply does not have a framework for it.

What this means going forward

For HYPE holders specifically, the buyback mechanism implies a few things.

The structural buy pressure is real and continuous. As long as trading volume holds up, the Assistance Fund will keep absorbing HYPE from the market every day. This is supportive of price during normal market conditions and somewhat protective during downturns, because the buyback keeps running regardless of sentiment.

The unlock schedule is a real concern, but partially offset. The team and investor unlocks beginning in 2027 will add selling pressure. The buyback mechanism will offset some of that pressure, but how much depends on trading volume at that point. Holders watching the unlock schedule should also be watching the buyback run-rate.

The governance commitment to the model is the variable to monitor. The 97% allocation is not constitutional. A future governance vote could change it. So far, the validator base has consistently voted to keep or strengthen the buyback policy, but this is the lever that matters most for long-term HYPE holders.

For the broader crypto market, the implications are larger than they appear. Hyperliquid’s model is being studied by other DeFi protocols as a template. If similar fee-to-buyback mechanisms get adopted by other major venues, the era of “token economics as marketing” may finally be giving way to “token economics as cash flow.” That would be a significant shift in how crypto tokens are valued, and Hyperliquid would be the inflection point.

For analysts, the lesson is that the standard frameworks for valuing crypto tokens (multiples of TVL, multiples of trading volume, comparisons to similar tokens) do not capture what is happening with HYPE. The token is closer to a high-payout-ratio financial instrument than to a typical L1 governance token.

Valuing it requires modeling the cash flow, the buyback rate, and the unlock schedule, then comparing the result to traditional equity benchmarks. Most analysts have not done this work, which is part of why coverage of HYPE is still structurally underdeveloped.

The bottom line

HYPE’s buyback mechanism is not a marketing gimmick. It is not a sporadic burn program. It is not a discretionary commitment that can be reversed when convenient.

It is a continuously running, on-chain, automated mechanism that takes 97% of Hyperliquid’s protocol revenue and converts it into open-market purchases of HYPE. The Assistance Fund has accumulated $1.3 billion in HYPE since launch. It buys roughly $1 million worth of HYPE per day on average. It scales with trading volume. It is governance-enforced. It produces an annualized buyback rate of approximately 7% of market cap, four to five times Ethereum’s burn rate and six times BNB’s.

That is the structural reason behind the rally that most price commentary cannot explain. The protocol generates real revenue. The revenue funds real buybacks. The buybacks support the token. The token’s value reflects the cash flow.

This is unusual in crypto. Most tokens have value accrual mechanisms that are theoretical, sporadic, or marketing-driven. HYPE has one that operates continuously, scales with adoption, and converts protocol success directly into token holder value.

Whether this justifies HYPE at $58 (its level as of late May 2026, after retracing from the $62.24 all-time high) is a separate question. The argument for “yes” is the cash flow generation, the back-loaded unlock schedule, and the multiple structural revenue streams (buybacks, AQAv2 reserve yield, ETF allocation). The argument for “no” is the fully diluted valuation against eventual unlock supply and the conditionality of the model on continued trading volume growth. Reasonable analysts disagree on the valuation, and many do.

What is not reasonable is to evaluate HYPE without understanding the buyback mechanism. The price chart shows what happened. The Assistance Fund explains why.

This is the part most readers have not internalized yet. The crypto press has spent eighteen months treating HYPE as another speculative altcoin rally. The structural picture is that HYPE has the most aggressive and durable cash flow mechanism of any major crypto token, and the protocol that generates that cash flow is currently the dominant venue for on-chain derivatives.

That is not a meme. That is not speculation. That is real economics, encoded in smart contracts, running every day.

The buyback mechanism is the part that most people do not understand. Once you understand it, everything else about HYPE makes more sense.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets and protocol dynamics evolve quickly; the figures and milestones described reflect reporting available as of late May 2026. Always do your own research.

Robinhood (HOOD) is giving retail traders a new way to automate investing: letting artificial intelligence make decisions and place trades on their behalf.

Customers can now connect third-party AI agents to Robinhood accounts to manage trading activity and even complete purchases through virtual credit cards, Robinhood announced Wednesday. The rollout includes two products, Agentic Trading and the Agentic Credit Card.

The tools effectively turn AI assistants into automated financial operators that can monitor markets, rebalance portfolios or execute strategies without requiring constant attention from the customer.

A trader who wants exposure to artificial intelligence stocks could instruct an AI agent to build and maintain a portfolio focused on the sector. Another user could ask an agent to automatically buy oversold stocks based on a predefined trading strategy.

Automated AI trading

The company said users will also be able to automate purchases through AI-connected virtual credit cards. Customers can direct agents to monitor prices for products or complete purchases once certain conditions are met.

Robinhood is pitching the tools as a way to reduce the amount of time customers spend researching investments or tracking deals manually.

The new products mark clear examples of AI-driven financial automation moving from hedge funds and institutional trading desks into mainstream retail investing apps.

Until now, automated AI trading systems have largely been confined to Wall Street firms with dedicated risk-management teams and quantitative trading infrastructure. Robinhood’s move opens those capabilities to smaller investors using consumer-grade AI tools.

That shift also raises questions about how much control retail users should hand over to autonomous systems, especially in volatile markets.

Robinhood said it designed the products with several guardrails. AI agents operate through separate trading accounts with access limited to only the funds customers allocate. Users receive notifications whenever trades occur and can disable agents instantly.

The company also added spending controls and optional manual approvals for AI-driven purchases.

Initially, Agentic Trading will support stock trading only while it remains in beta. Robinhood said support for options, crypto and futures trading is planned later.

HOOD shares climbed 1.5% to $75.20 during the U.S. morning on Wednesday’s following the announcement.

Crypto-backed political groups have strengthened their position in Texas after several candidates supported by industry-funded PACs secured victories in key primary runoff races.

Summary

- Crypto-backed PACs spent millions supporting candidates in Texas runoff races, with Christian Menefee and Ken Paxton among the winners.

- Fairshake affiliate Protect Progress spent about $5 million backing Menefee and $2.8 million opposing Representative Al Green, according to Federal Election Commission filings.

- The Texas races unfolded as Congress continues debating crypto market structure and stablecoin legislation, including the GENIUS Act and the Clarity Act.

According to Texas primary runoff results released Tuesday, Texas Attorney General Ken Paxton defeated four-term Senator John Cornyn in the Republican Senate runoff and will now face Democratic state Representative James Talarico in November’s general election.

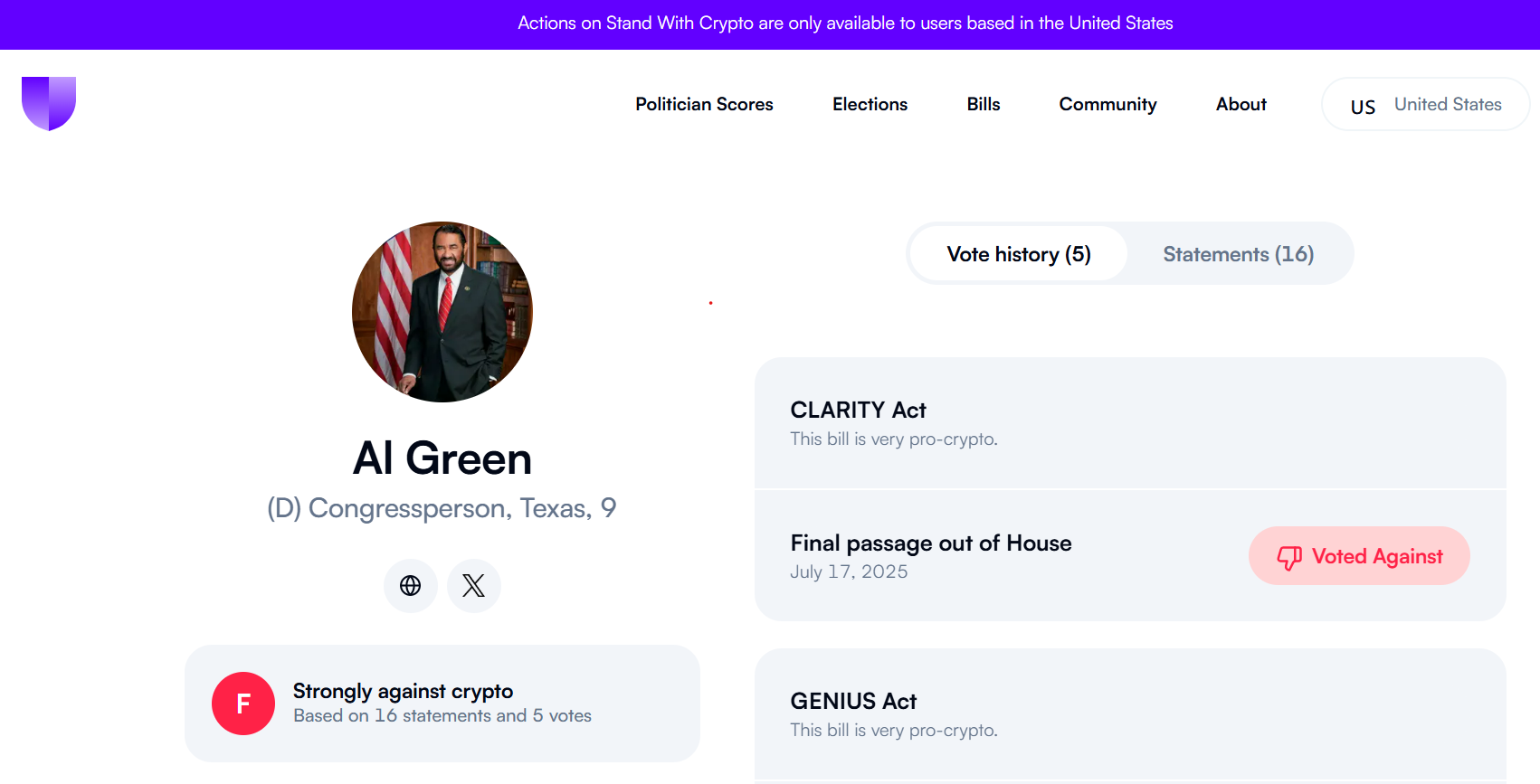

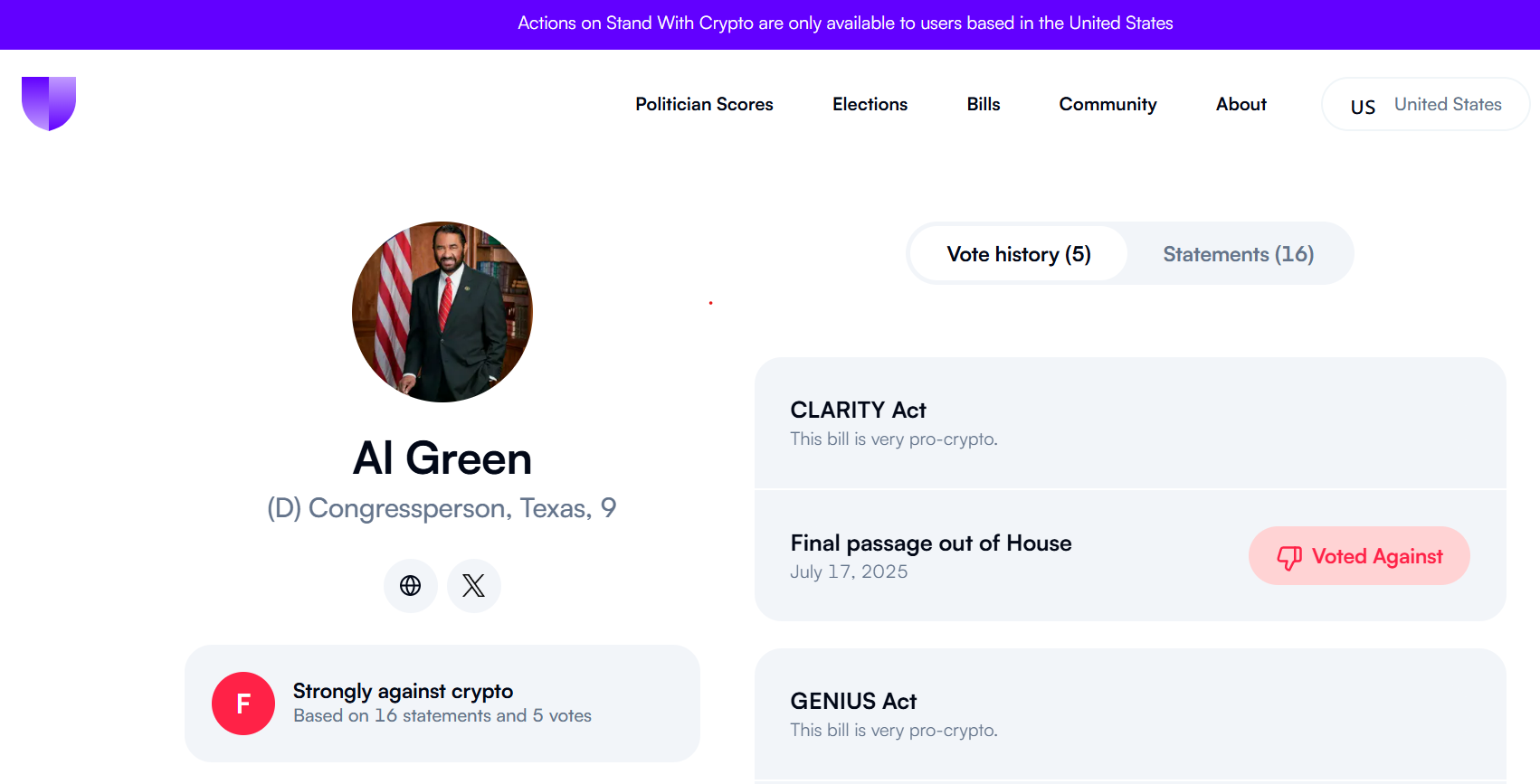

In Houston’s 18th Congressional District, Democrat Christian Menefee defeated longtime Representative Al Green after Republican-led redistricting placed both incumbents in the same district. The result removed one of Texas’s senior Democratic lawmakers from the House race.

Federal Election Commission filings showed that Protect Progress, an affiliate of the crypto-backed Fairshake PAC, spent about $5 million supporting Menefee while directing another $2.8 million toward advertisements opposing Green. Fairshake, which receives backing from crypto firms including Ripple and Coinbase, reported holding roughly $193 million in cash ahead of the 2026 election cycle.

At the same time, Fellowship PAC, which receives funding from financial services firm Cantor Fitzgerald and crypto custodian Anchorage Digital, spent nearly $500,000 backing Paxton in the Senate contest.

Crypto PAC spending reshapes Texas congressional races

Prediction markets heavily favored the crypto-supported candidates before election day. Data from Kalshi gave Menefee roughly a 91% probability of victory, while crypto-based platform Polymarket posted similar odds. Betting activity tied to the Paxton-Cornyn race exceeded $16 million, according to market data cited by crypto.news.

Green had become a major target for crypto advocacy groups after opposing several industry-backed bills in Congress. Congressional voting records show he voted against the GENIUS Act stablecoin bill and the Clarity Act, both of which are central to ongoing negotiations over US digital asset regulation.

Crypto advocacy organization ‘Stand With Crypto’ assigned Green an F grade because of his opposition to crypto legislation, while Menefee received a favorable rating from the group for supporting digital asset innovation policies.

During remarks on the House floor, Green accused Menefee of benefiting from crypto industry funding. Green said he remained “unbought” by crypto money and criticized Fairshake’s involvement in the race. His comments came after the Blockchain Leadership Fund, supported by Anchorage Digital and Chainlink Labs, endorsed Menefee’s campaign.

Meanwhile, Fairshake’s Republican affiliate, Defend American Jobs, supported several Republican candidates who also won their runoff races, including Alex Mealer, Jon Bonck, Tom Sell and Carlos De La Cruz.

Congress continues work on crypto legislation

The Texas runoff outcomes arrive as lawmakers in Washington continue debating legislation that would establish rules for digital asset markets and stablecoin issuers.

Crypto.news previously reported that Congress is working through a compressed legislative schedule ahead of the 2026 midterm elections, with lawmakers considering the Clarity Act alongside the GENIUS Act. The publication also reported on proposed Treasury Department anti-money laundering requirements for stablecoin issuers under the GENIUS framework.

Bitcoin policy advocate Dennis Porter commented on Menefee’s victory after the results became clear. Porter described the race as an example of a pro-crypto Democrat defeating a long-serving lawmaker who opposed the industry.

For crypto-backed PACs, the Texas races offered another opportunity to support candidates from both major parties while Congress continues debating how digital asset businesses will operate under future US regulations.

FTSE Russell has placed Sharplink, Forward Industries, Gemini, Bitmine, and Galaxy Digital on preliminary consideration lists for inclusion in its small-cap benchmarks, a structural development that carries direct implications for Ethereum traders watching institutional flow build on the equity side.

The 2026 U.S. index reconstitution becomes effective in late June, with the final rebalancing expected on June 27, and passive funds tracking the Russell 2000 and Russell 3000 will be forced buyers of any confirmed additions.

LATEST: — CoinMarketCap (@CoinMarketCap) May 27, 2026

SharpLink and Forward Industries will join the Russell 2000 and 3000 in late June, expanding index exposure to non-Bitcoin crypto treasury firms. pic.twitter.com/isgTrk1Ge8

SharpLink and Forward Industries will join the Russell 2000 and 3000 in late June, expanding index exposure to non-Bitcoin crypto treasury firms. pic.twitter.com/isgTrk1Ge8

Estimated passive ownership in Russell-benchmarked vehicles runs at 20–25% of float for newly included names, mechanical demand that hits regardless of price.

Discover: The Best Crypto to Diversify Your Portfolio

Index Rebalancing Mechanics: How Forced Buying Creates the Catalyst Window for Ethereum

FTSE Russell’s annual U.S. index reconstitution runs on a fixed calendar. Preliminary lists surface in May, final membership is set after the late-May ranking date, and the rebalancing becomes effective in the final week of June, one of the largest single-day mechanical trading events in U.S. equities, historically generating hundreds of billions of dollars in turnover as passive managers adjust to match new index weights.

For crypto-linked names, the mechanics are straightforward but the implications are layered. Once a company like Sharplink or Forward Industries is confirmed for the Russell 2000, every ETF and mutual fund benchmarked to that index must purchase shares before the close on reconstitution day. There is no discretion involved.

The size of the forced buy scales directly with market cap relative to the index weight, and for small-cap crypto equities that have recently appreciated, those weights can be meaningful.

Bitmine’s position makes this concrete. The company disclosed 5.28 million ETH in holdings, with combined crypto and cash reserves valued at roughly $12.6 billion, positioning it as a de facto Ethereum treasury stock just weeks ahead of the reconstitution window.

A passive fund buying Bitmine equity is acquiring indirect Ethereum exposure whether or not it has a mandate to hold digital assets directly. That transmission channel is the structural novelty here.

Quant and arbitrage desks have been trading anticipated Russell inclusions and deletions for years, often building positions in the weeks before the ranking date and unwinding after reconstitution.

With crypto-linked names now on the preliminary lists, that same arb activity will layer on top of whatever is happening in ETH spot and futures markets.

The volatility window around late June is already on the calendar, the only question is how many of these names survive to the final list.

The post Russell 2000 Rebalancing: How Index Inclusion Could Move Crypto-Equities and Ethereum appeared first on Cryptonews.

China’s Supreme People’s Court (SPC) has signaled a broader initiative to standardize how digital economy disputes are adjudicated, with new research focused on rulings for virtual currencies and cross-border finance. The move aims to produce clearer judicial guidelines that can handle a rising tide of crypto- and AI-related cases, according to Liu Guixiang, a member of the SPC Judicial Committee. He told Yicai that the court would study adjudication rules for these evolving areas and, as soon as possible, formulate interpretations governing civil compensation in cases such as insider trading and market manipulation.

In addition to crypto and cross-border finance, the SPC outlined plans to examine judicial protections for artificial intelligence cases and data property rights—encompassing disputes over data ownership, data transactions, and AI-generated content. The overarching forecast is to build internal standards that bring greater consistency to a growing slate of digital economy disputes in China, potentially shaping how crypto-related IP and liability are addressed in Chinese courts.

The timing of the comments aligns with a broader enforcement and policy backdrop that has long defined China’s approach to digital assets and related technologies. The same period has seen high-profile cross-border legal activity and a tightening stance on digital assets within and beyond the mainland, underscoring the stakes for investors, developers, and users navigating China’s evolving regulatory terrain.

Key takeaways

- The SPC plans to draft judicial interpretations on civil compensation in insider trading and market manipulation tied to crypto activity, signaling a move toward clearer liability standards for crypto cases in China.

- New research will also cover AI-related disputes and data property rights, potentially shaping how ownership and licensing of data and AI-generated content are treated in court.

- China’s longstanding crypto stance remains restrictive, with a history of bans on crypto transactions, mining, and related activities, even as the country advances its CBDC program.

- Regulatory developments are accompanied by high-profile enforcement activity abroad, including cross-border cases linked to crypto operators and the use of crypto to facilitate illicit schemes.

- Observers should monitor the SPC’s forthcoming judicial interpretations for crypto and AI IP rights, which could influence both legal risk and market behavior in China’s digital economy.

China’s judicial push tallies with a cautious crypto policy backdrop

China’s relationship with cryptocurrency has been cautious and often forbidding. Since 2013, the People’s Bank of China (PBOC) has barred financial institutions from providing Bitcoin-related services and has declined to recognize Bitcoin as a currency. This stance hardened in 2021 when a coordinated set of regulators, including the PBOC and securities authorities, issued a blanket ban on all crypto transactions, as well as Bitcoin mining and ICO activities within the country.

Further tightening followed in February, when the PBOC prohibited the issuance of unauthorized offshore yuan-pegged stablecoins and the unapproved tokenization of real-world assets. The move reflected a broader emphasis on maintaining monetary sovereignty and limiting financial experimentation outside state channels. The country’s trajectory toward a centralized, state-controlled digital fiat system has continued to influence how Chinese policymakers balance innovation with regulation.

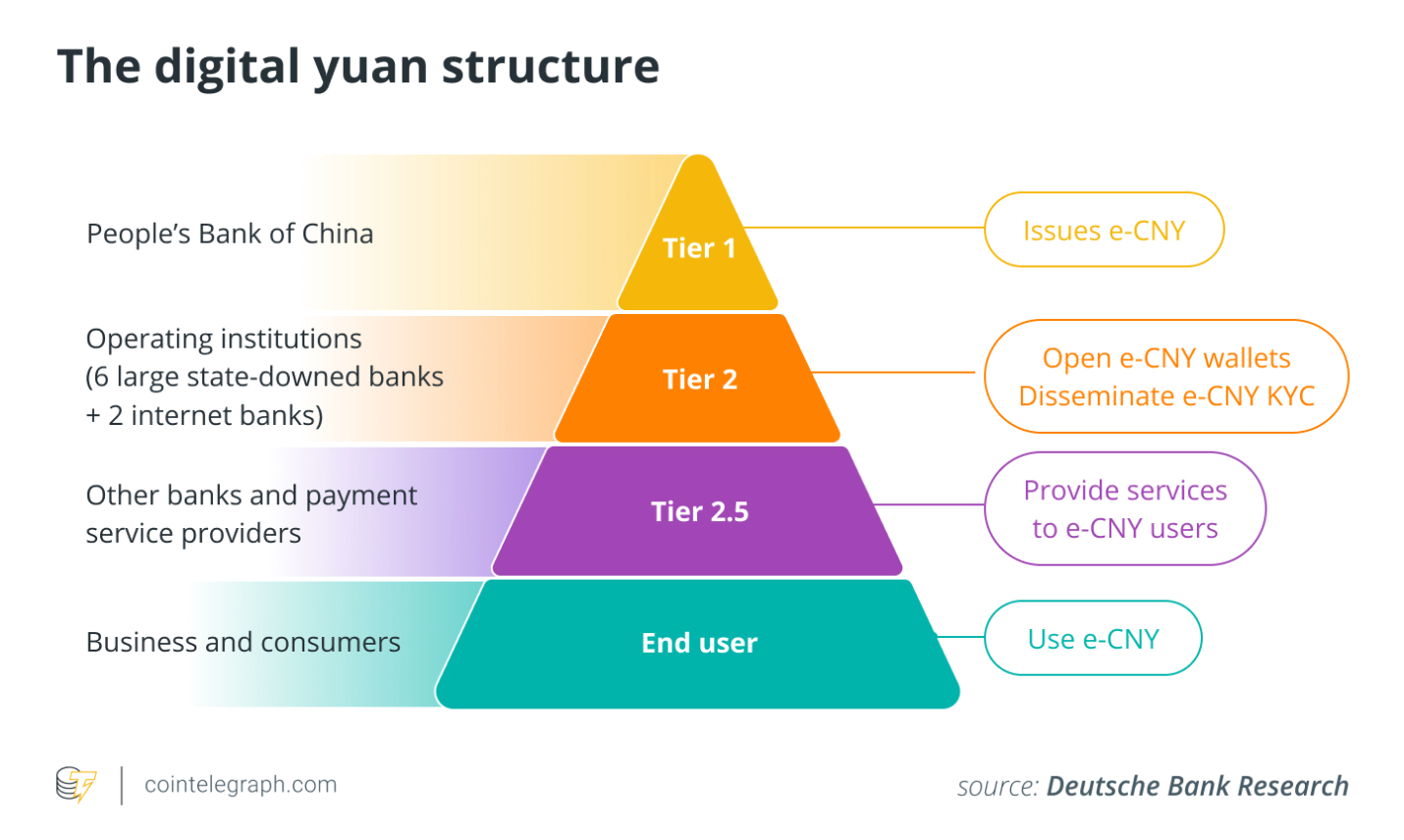

Amid these regulatory headwinds, China has steadily advanced its own digital currency framework. The country is actively developing the digital yuan, a central bank digital currency (CBDC) managed by state authorities. This CBDC initiative is frequently cited as the centerpiece of China’s digital money strategy, positioning the digital yuan as a replacement or complement to traditional stablecoins as the regime’s preferred vehicle for digital payments and financial inclusion.

Enforcement signals and the broader policy environment

The SPC’s remarks come on the heels of ongoing cross-border enforcement activity that underscores the global dimension of crypto-related risk. In recent months, U.S. authorities pursued cases involving alleged crypto-linked schemes with ties to illicit operations. Notably, the U.S. Department of Justice seized about $15 billion worth of Bitcoin from a Chinese-linked operator in connection with a major investigation that has continued to unfold in the public record. Separately, a prominent Chinese-born executive associated with a regional business group faced arrest abroad and subsequent extradition to China on charges linked to operating illicit financial schemes. These enforcement actions highlight the intensifying cross-border cooperation and the reputational and financial risks that accompany crypto-related activity for multinational actors.

For investors and builders, the juxtaposition of stricter domestic adjudication standards and aggressive international enforcement signals a need for caution and precision. Clarity from the SPC could reduce ambiguity in civil litigation over crypto disputes, making it easier for market participants to assess risk, allocate liability, and determine remedies. At the same time, the broader push for CBDC development and the continued prohibition of unauthorized crypto activities suggest that China’s regulatory environment will remain bifurcated—supportive of technological advancement within a tightly controlled financial ecosystem, while restricting broader use of decentralized or offshore crypto instruments.

What readers should watch next

The central question in the near term is how the SPC will translate its research into concrete judicial interpretations. The timing of those guidelines could influence transactional risk, enforcement priorities, and the strategic decisions of firms operating in or with China’s digital economy. Observers should also monitor whether the ongoing cadence of cross-border enforcement actions or the CBDC push will shape a more predictable or more restrictive environment for crypto and AI-related activities in China. As the SPC moves from study to interpretable rules, the practical impact on disputes, compensation standards, and IP rights in crypto and AI will emerge more clearly.

Key Highlights

- Firefly Aerospace (FLY) shares surged 18.81% on Tuesday, reaching $58.81

- The company secured a $75 million NASA subcontract for the MoonFall mission

- Mission involves transporting four drones to the lunar south pole via Elytra spacecraft

- Scheduled launch window set for 2028 as part of NASA’s Moon Base program

- Elytra will complete a 45-day journey before releasing drones 50km above the south pole

Shares of Firefly Aerospace (FLY) climbed 18.81% to finish at $58.81 on Tuesday following the announcement of a $75 million NASA subcontract focused on lunar exploration activities.

The agreement assigns Firefly responsibility for transporting four specialized drones to the Moon’s south pole region under NASA’s MoonFall mission framework. The target launch date is set for 2028.

MoonFall represents the initial phase of NASA’s ambitious Moon Base program, which seeks to establish a permanent human footprint and foster both scientific research and commercial operations at the lunar south pole.

The drones themselves are being developed by NASA’s Jet Propulsion Laboratory, which will also oversee mission operations. NASA plans to secure the launch vehicle through a separate procurement process.

Following liftoff, Firefly’s Elytra vehicle will transport the four drones during a 45-day journey to lunar space. After achieving orbit around the Moon, the spacecraft will initiate a deorbit sequence and perform a controlled braking burn.

Drone deployment is planned at approximately 50 kilometers altitude above the Moon’s southern polar region. The operation demands precise technical execution, and Firefly believes its Elytra platform is uniquely qualified for this assignment.

CEO Jason Kim referenced the company’s proven capabilities with Blue Ghost, which achieved a successful lunar landing. “Built upon the same proven systems that landed Blue Ghost on the Moon, our Elytra spacecraft are equipped to deploy critical high-mass payloads across cislunar space,” he stated.

Elytra Takes Center Stage in Lunar Operations

Kim characterized the MoonFall award as aligned with Firefly’s core mission objectives. “This subcontract underscores our commitment to executing challenging missions that push the boundaries of lunar exploration,” he remarked in Tuesday’s announcement.

Elytra functions as a cislunar transfer system engineered to transport cargo between Earth orbit and lunar destinations. Its assignment on MoonFall marks its most prominent operational deployment since supporting the Blue Ghost mission.

The mission architecture demands that Elytra execute both deorbit and braking procedures prior to releasing the drones — a more technically challenging sequence than conventional lunar surface delivery missions.

MoonFall Advances NASA’s Broader Lunar Vision

MoonFall isn’t an isolated endeavor. It supports NASA’s comprehensive Moon Base initiative, which targets the development of permanent infrastructure at the lunar south pole.

The southern polar region has emerged as a priority destination for lunar missions due to potential water ice reserves located within permanently shadowed crater formations. Aerial drones offer survey capabilities in terrain that wheeled rovers struggle to access.

Firefly’s earlier Blue Ghost lander mission, which successfully touched down on the Moon earlier this year, validated the company’s lunar delivery capabilities. This proven track record likely influenced NASA’s decision to select Firefly for the MoonFall subcontract.

The $75 million award expands Firefly’s existing portfolio of NASA collaborations. The company has steadily strengthened its position within the commercial lunar services marketplace in recent years.

FLY stock closed Tuesday’s trading session up 18.81% at $58.81.

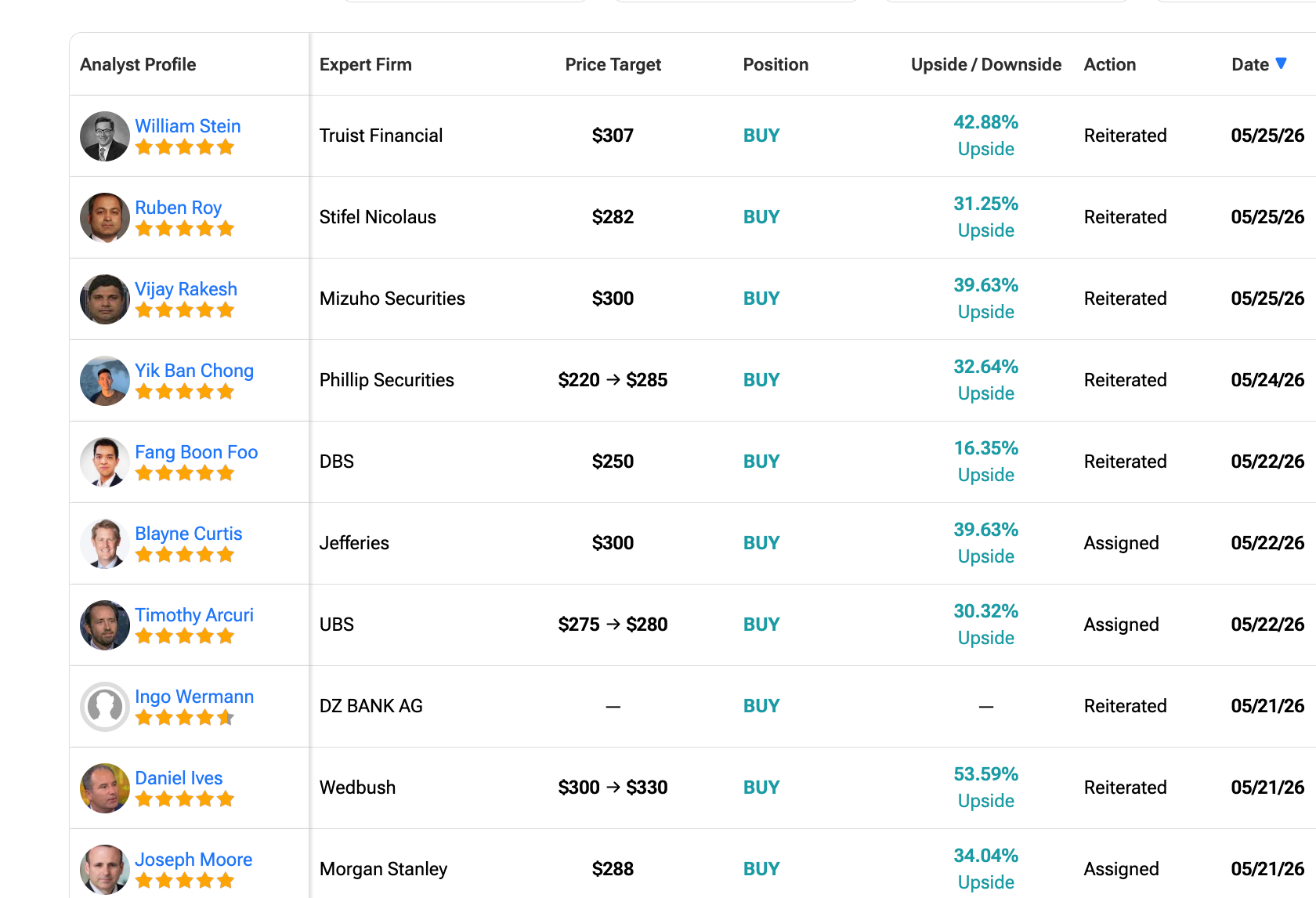

NVIDIA stock received fresh buy ratings from multiple Wall Street firms in just a 7-day span. Wedbush stamped the highest target at $330, Jefferies and Mizuho at $300, and Morgan Stanley at $288.

Yet the stock is rolling over from a $236 peak. Institutional money turned negative on May 27, and retail volume turned red on May 15. The buyers Wall Street wants appear to have walked out.

Wall Street Just Stacked Buy Ratings on NVIDIA Stock

The case for NVIDIA stock is loud right now.

Wedbush analyst Daniel Ives raised his target on May 21 to $330, the highest figure on the street. That implies 53.59% upside from the current $214.86 close. Morgan Stanley’s Joseph Moore reiterated his $288 buy on the same day.

Jefferies came in at $300 on May 22, Mizuho at $300 on May 25, and Truist Financial at $307. Even the more conservative shops are positive. DBS holds $250, and UBS raised its figure from $275 to $280.

Of the 10 firms tracked this week, every single one rates NVIDIA stock a buy. The chart has been telling a different story.

NVIDIA Stock’s Institutional Money Walked Out First

NVIDIA stock rallied 44.18% from $164.27 in late March to a $236.84 peak on May 19. Since then, it has consolidated within a tight downward channel that resembles a bullish pole-and-flag pattern.

Want more insights like this? Sign up for Editor Harsh Notariya’s Daily Newsletter here.

Yet, the money flow profile has shifted. Institutional buying pressure, as tracked by the Chaikin Money Flow indicator, fell below zero on May 27. The last time that gauge broke zero was mid-March, right before NVIDIA stock fell 13.06%.

Retail volume turned red on May 15, and sales volume across the consolidation has held steady instead of fading. These two flow signals now point in the same direction, while Wall Street targets point in the opposite direction.

Stock Now Trades More Volatile Than Bitcoin as the Option Traders Take Sides

The tiebreaker between the buy ratings and the bleeding chart sits in volatility. NVIDIA’s 30-day annualized volatility now stands at 33.1%.

That tops Bitcoin at 22.9%, the NASDAQ-100 at 14.1%, and the S&P 500 at 8.6%. It is also higher than Tesla’s 32.2% and roughly level with Alphabet’s 33.7%.

A name moving with that kind of energy can override a technical setup within a session when sentiment shifts. That is the wild card here. Wall Street’s $330 figure assumes a re-rating catalyst lands. The tape currently assumes none. Whichever side gets the next trigger usually wins the week at this level of volatility.

The options market is already taking sides, and it is not the technical chart’s side.

On May 19, NVIDIA’s stock’s put-call volume ratio was 0.49. As of May 26, it has dropped to 0.42. A falling volume ratio means fresh positioning is buying more calls than puts.

Open interest climbed slightly from 0.79 to 0.81, but the volume signal is where new bets show up first.

That move tracks back to the volatility read. Traders are not building hedges. They are building upside exposure into a name moving fast enough if the catalyst lands. Now the chart has to be chosen.

Where NVIDIA Stock Price Goes Next

NVIDIA stock currently sits at $214.86, three dollars above the bull flag’s lower channel at $211. A daily close below $211.88 weakens the pattern.

A break of $194.70 invalidates it entirely and reopens the path back to the $164.27 low. To the upside, the first reclaim sits at $221.81, the 0.236 Fibonacci level.

A close above $221.81, then $227.95, opens the door to $237.89. Beyond that, $244.95 and $253.96 add up to $279.97, the 1.618 extension.

That figure aligns almost exactly with UBS’s $280 target. The move from $221.81 to $279.97 is a 26% increase. For now, NVIDIA stock holding above the $211 zone keeps the bull flag theory active. Losing $194.70 hands the trade back to the bears.

The post Top Wall Street Names See NVIDIA Stock at $330, But Buyers Just Walked Out appeared first on BeInCrypto.

Crypto-backed political groups supported several winning candidates in Texas primary runoffs Tuesday, highlighting the digital asset industry’s growing role in US elections as Congress debates new rules for crypto markets.

Attorney General Ken Paxton won the Republican US Senate runoff against four-term Senator John Cornyn by a wide margin, according to Texas primary runoff results, and will face Democratic state Representative James Talarico in November.

In Houston’s 18th Congressional District, Democrat Christian Menefee unseated fellow Democrat representative Al Green in a decisive win after Republican-led redistricting forced the two incumbents into the same district, ousting one of the state’s most senior House members.

Democrats and Republicans Alex Mealer and Jon Bonck also secured their party’s nominations in competitive Houston-area House races.

The contests drew heavy spending from crypto-aligned political action committees (PACs) focused on a small number of high-stakes races, and come as Congress debates new rules for digital asset markets, including legislation to define crypto market structure and establish a framework for dollar‑pegged stablecoins.

Stand With Crypto assigned Al Green an “F” rating. Source: Stand With Crypto

Victories by candidates backed by crypto-focused PACs in a politically influential state could give the industry additional allies as those measures advance.

Crypto money reshapes key Texas races

Two races in particular show how that money is being deployed. Protect Progress, an affiliate of the Fairshake super PAC backed by firms including Ripple and Coinbase, reported spending about $5 million to support Menefee and a further $2.8 million on advertising opposing Green in the Houston race.

Another crypto-focused group, Fellowship PAC, funded in part by financial firm Cantor Fitzgerald and crypto custodian Anchorage Digital, reported roughly $500,000 in spending to boost Paxton over Cornyn in the Senate runoff.

Fairshake’s Republican affiliate, Defend American Jobs, also backed four winning Republican candidates, Jon Bonck, Tom Sell, Carlos De La Cruz and Alex Mealer.

Related: Texas Lt. Gov. calls for study of crypto, prediction markets

Texas runoffs test crypto’s political power

Bitcoin-focused policy advocate Dennis Porter commented on Menefee’s victory, saying, “A pro crypto Democrat just ousted a 20-year incumbent Democrat who was anti crypto. Nature is healing,” a nod to what many in the industry saw as years of Democratic-led “Operation Choke Point 2.0,” campaigns, in which bank regulators and enforcement agencies have been accused of squeezing crypto firms out of the financial system.

While much of crypto PACs’ recent spending in the state has gone to Republican candidates, Menefee’s win gives the groups a high-profile Democratic ally in Texas.

The crypto advocacy group, Stand With Crypto, assigned Green an F grade for his strong opposition to industry-backed legislation, while Menefee is rated as supportive of digital asset innovation.

Prediction markets had strongly favored the crypto-aligned challengers heading into election day. Contracts on regulated and crypto-native platforms implied odds of over 90% that both Paxton and Menefee would prevail, with nearly $15 million reportedly traded on markets tied specifically to the Paxton vs Cornyn runoff.

Magazine: Guide to the top and emerging global crypto hubs — Mid-2026

China’s Supreme People’s Court (SPC) said it will study new adjudication rules for virtual currency and cross-border finance cases as part of a broader push to clarify how courts handle digital economy disputes.

“We will conduct in-depth research on the adjudication rules for new cases such as virtual currencies and cross-border finance, formulate judicial interpretations on civil compensation involving insider trading and market manipulation as soon as possible,” said Liu Guixiang, Judicial Committee member of the SPC, during a press conference, reported Chinese news outlet Yicai on Wednesday.

The court also plans to study judicial protection rules for artificial intelligence cases and data property rights, including disputes involving data ownership, data transactions and AI-generated content.

The development aims to draft clearer internal judicial standards on how courts should decide disputes and liability in crypto and AI intellectual property rights-related lawsuits. The promised guidelines may improve the court’s consistency in the growing number of crypto and AI-linked cases in the country.

The comments come months after a high-profile lawsuit involving Chen Zhi, the Chinese-born founder and chairman of Cambodia’s Prince Group, who was arrested in Cambodia on Jan. 6, 2026, and extradited to China shortly after, where he faces charges related to operating pig butchering scam compounds.

In October 2025, the US Department of Justice seized about $15 billion worth of Bitcoin (BTC) from Zhi’s suspected operations.

US authorities charge Chen Zhi and seize $15 billion in Bitcoin. Source: Justice.gov

China’s ban on all crypto transactions remains in place

Mainland China has had a rocky relationship with the cryptocurrency industry.

In December 2013, the People’s Bank of China (PBOC) banned financial institutions from offering Bitcoin-related services and stated that Bitcoin was not recognized as a currency, in its first major prohibitive step against the crypto industry.

Related: South Korean funeral company records $33M unrealized loss on leveraged ETH ETFs

In September 2021, ten Chinese agencies, including the central bank and securities regulators, issued a blanket ban on all crypto transactions, Bitcoin mining and activities tied to initial coin offerings (ICOs) in the country.

In February, the PBOC banned the issuance of unauthorized offshore Chinese yuan-pegged stablecoins and the unapproved issuance of tokenized real-world assets (RWAs).

The structure of the digital yuan, China’s CBDC. Sources: Cointelegraph

The latest ban came shortly after the Chinese government approved commercial banks to share interest with clients holding the country’s digital yuan, a central bank digital currency (CBDC) managed by state authorities.

The development signal that the PBOC is doubling down on its efforts to launch its own yuan-backed CBDC as a new form of digital fiat money, instead of stablecoins.

Magazine: 50K investors fight Korean crypto tax, Singapore cancels Bsquared: Asia Express

South Korea, Seoul Southern District Prosecutors’ Office has arrested and indicted operators behind Catfi. This is the country’s first-ever rug pull prosecution tied to a decentralized exchange.

The case, brought under the Virtual Asset User Protection Act, charges the group with market manipulation after 256 investors lost 900 million won($586,000), when liquidity was drained following an artificial price surge.

The scheme began on Pump.fun in early 2025, where the main suspect, identified by the surname Park, operating online as the influencer ‘Eth Father,’ created Catfi before listing it on a decentralized exchange. Park allegedly posed as an unrelated third party to recommend purchases, inflated follower counts, managed project social accounts, and spread tokens across multiple wallets while using circular trading to obscure issuer control.

Catfi’s price surged 1,001-fold within 26 hours of issuance, with 6,000 investors buying in before the liquidity vanished. The group used approximately 10 million won in criminal funds and walked away with 400 million won, or $260,000, in proceeds.

Discover: The Best Crypto to Diversify Your Portfolio

South Korea Catfi Arrest and DeFi Regulation

Until this Catfi case, South Korea virtual asset enforcement had concentrated almost entirely on centralized exchanges. DEX fraud occupied a legally murky space: non-custodial design, pseudonymous wallet operators, and the absence of a regulated intermediary made it structurally difficult to assign criminal liability under frameworks built for traditional finance or even CEX abuse.

The Virtual Asset User Protection Act, which took effect in July 2024, gave prosecutors a statutory basis, covering “the use of fraudulent means, plans, or techniques” and false statements about material facts in digital asset trading, regardless of venue.

The Catfi prosecution is only the second known matter under the Act, following the January 2025 ACE token manipulation case on Bithumb, but the first to reach into a DEX environment.

Seoul Southern District prosecutors framed the enforcement mandate explicitly, stating the office would “resolutely deal with acts that disrupt the digital asset market and undermine public trust.”

DeFi regulation in South Korea has now moved from exchange oversight to on-chain conduct, and operators who assumed decentralization meant immunity are reading that statement very carefully right now.

The Tracing Mechanism

The Catfi case illustrates the investigative template that makes on-chain forensics increasingly dangerous for rug pull operators. Prosecutors identified circular trading patterns, coordinated wash trades across wallets controlled by the issuing group, which created artificial volume and masked insider ownership concentration.

From there, the off-ramp is typically the exposure point: converting criminal proceeds into fiat or stablecoins requires touching a centralized exchange with KYC obligations, and that intersection is where pseudonymous operators become identifiable individuals.

South Korea’s enforcement bodies have developed this pattern across prior cases; the 149-arrest USDT laundering ring announced earlier this year demonstrated that prosecutors can map complex multi-wallet schemes at scale. The Catfi group’s use of approximately 10 million won in traceable criminal funds suggests the on-chain trail was coherent enough to anchor the indictment.

Two suspects were arrested and indicted for market manipulation; one was indicted without detention; two others were charged for helping the main suspect flee. Similar reconstruction methods were visible in the Squid protocol exploit, where on-chain tracing helped identify the flow of drained funds across multiple hops.

Discover: The Best Token Presales

The post South Korea Makes First DEX Rug Pull Arrest in Catfi Case appeared first on Cryptonews.

South Korean prosecutors have charged a group linked to the Solana-based memecoin CATFI, also known as Catpie, in what local outlets described as the country’s first prosecution tied to a rug pull on a decentralized exchange. The Seoul Southern District Prosecutors’ Office, through its Virtual Asset Crime Joint Investigation Division, arrested the core suspects. The lead figure, identified by the surname Park, allegedly posed online as “Eth Father” and promoted CATFI as an independent third-party project before the scheme unfolded, according to Digital Asset Works.

Investigators say the defendants used social media to hype CATFI, driving the token’s price up more than 1,000-fold within about 26 hours. They then sold their holdings for roughly 400 million won in illicit profits, while the rug pull inflicted about 900 million won ($599,000) in losses on at least 256 investors. The case represents a rare legal action in South Korea against memecoin price manipulation under the Virtual Asset User Protection Act.

Prosecutors noted that rug pulls are deceptive exit scams in which project creators cultivate investor interest, only to abandon the project and siphon away funds. Cointelegraph reached out to the Supreme Prosecutors’ Office for comment but had not received a response by publication as the investigation unfolds.

The case adds to the ongoing scrutiny of domestic crypto markets and comes as South Korea’s crypto trading activity has cooled. Digital Asset Works highlighted a broader market backdrop in which won-based exchanges have seen trading volumes shrink relative to the KOSPI stock market, underscoring heightened regulatory attention to market manipulation and investor protection.

Key takeaways

- .li>First confirmed arrest in a memecoin rug pull under South Korea’s Virtual Asset User Protection Act, tied to the CATFI/Catpie case.

- CATFI surged over 1,000 times in price within 26 hours before promoters sold approximately 400 million won in illegal profits; roughly 900 million won in losses reported across at least 256 investors.

- The token’s market profile collapsed from an all-time peak to a dramatic 99% decline, with on-chain data showing 1,512 holders remaining as of now and the largest holder controlling about 18% of supply.

- Domestic market context features a notable drop in won-based trading volume, highlighting regulatory and market headwinds for memecoins and similar high-risk assets.

- Related incidents this year underscore ongoing risk in meme tokens, including high-profile rug pulls tied to social media-driven hype and influencer-linked projects.

CATFI’s rise and fall in context

CATFI briefly reached an all-time market capitalization of about $8.99 million in February 2025, but the subsequent rug pull and exit scam knocked the token back into a lurching decline. Data from Pump.fun indicates that, despite the collapse, a significant portion of investors—about 1,512 holders—still appear to be holding CATFI in hopes of recovery. The largest known address, a wallet labeled “5Q54,” reportedly held around 18% of the token’s supply at the time data was compiled. The project’s former promoter’s X (Twitter) account has since been deleted, reflecting the erasure of public-facing outreach tied to the campaign.

The legal action signals that authorities are increasingly willing to pursue coordinated manipulation cases in the memecoin space. Rug pulls—where developers promote a token to attract funds and then abruptly abandon the project—have long threatened retail investors, particularly in communities built around social media-driven hype. The CATFI case is positioned as a test of South Korea’s enforcement under evolving crypto consumer protection standards.

However, the CATFI saga is not isolated. In May, Cointelegraph reported on another Solana memecoin linked to Keith Gill’s Roaring Kitty persona that experienced a separate rug pull, with the anonymous developer cashing out about $729,000 while investors saw steep losses. The episode, alongside the CATFI case, underscores the volatility and risk profile of meme-oriented assets even as markets evolve and regulators scrutinize suspicious activity more closely.

For individual traders, the CATFI episode illustrates how quickly momentum-based tokens can flip from rapid gains to devastating losses. One trader reportedly saw a loss approaching six figures in a short period during a recent memecoin event, highlighting the real-world stakes involved in these crowded, speculative spaces.

Regulatory backdrop and market dynamics in South Korea

The CATFI case arrives amid a downturn in domestic digital asset trading activity. Digital Asset Works’ coverage notes that won-based exchanges have seen shrinking volumes, with overall activity in the Korean market growing more cautious in the face of regulatory scrutiny and increased risk awareness among investors. The development underscores a broader tightening environment where authorities emphasize consumer protection, anti-manipulation measures, and accountability for project teams behind high-risk tokens.

South Korea’s enforcement trajectory—with the CATFI investigation marking a potential precedent—could influence how future memecoin launches are treated under existing laws. While the case does not conclusively determine the long-term legality of memecoins themselves, it demonstrates that orchestrated price manipulation and exit schemes are increasingly susceptible to legal repercussions, potentially reshaping project funding dynamics and investor diligence in the domestic market.

What comes next for CATFI and the market

As prosecutors proceed with the case, observers will be watching how charges unfold, whether additional arrests follow, and what implications this may have for the broader memecoin ecosystem in South Korea. The outcome could influence how exchanges assess listing risk, how influencers disclose promotional activity, and how investors evaluate exit risk in hype-driven tokens. In the near term, CATFI’s holders face a challenging landscape: questions about potential refunds, recovery pathways for defrauded investors, and the sustainability of token liquidity in the wake of the rug pull remain unresolved.

Readers should watch for further updates from South Korean authorities as the investigation progresses, along with any court rulings that could redefine enforcement norms for memecoins and similar schemes. The CATFI case may serve as a bellwether for how regulatory regimes balance innovation and investor protection in a fast-moving, social-media-driven segment of the crypto market.

Modine Manufacturing Company 2026 Q4 – Results – Earnings Call Presentation (NYSE:MOD) 2026-05-27

Why Does My House Suddenly Have So Many Flies?

Pictures after fire breaks out in Church Row, in Darlington

-

Crypto World6 days ago

Crypto World6 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion5 days ago

Fashion5 days agoHoliday Weekend Open Thread – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

Business5 days ago

Business5 days agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World4 days ago

Crypto World4 days agoRobinhood crypto COO Tanya Denisova exits

-

Tech2 days ago

Tech2 days agoMicrosoft’s quiet Claude Code retreat and the real cost of enterprise AI

-

Politics5 days ago

Politics5 days agoMakerfield: a tale of two social-media histories

-

Business3 days ago

Business3 days agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

Crypto World5 days ago

Crypto World5 days agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Crypto World5 days ago

Crypto World5 days agoMicroStrategy’s Saylor Says Miners No Longer Set Bitcoin Price, Another Force Has Taken Over

-

Tech6 days ago

Tech6 days agoWhatsApp ads could make Irish debut after discussions with DPC

-

NewsBeat6 days ago

NewsBeat6 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Tech5 days ago

Tech5 days agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Crypto World5 days ago

Crypto World5 days agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

Crypto World2 days ago

Crypto World2 days agoNvidia (NVDA) CEO Calls on Super Micro to Strengthen Export Controls Amid Smuggling Probe

-

Tech2 hours ago

The Samsung pay deal is the moment Korean unions changed register

-

Tech6 days ago

Tech6 days agoYou Can Now Add ChatGPT To PowerPoint

-

Business5 days ago

Business5 days agoTrump Invests $1M-$5M in Kura Sushi USA Chain With 27 California Locations

-

Tech2 days ago

Tech2 days agoWestone Audio and Etymotic Acquired by Fidelity Collective in Major IEM Market Move

-

Sports6 days ago

Sports6 days ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

You must be logged in to post a comment Login