Crypto World

Strategy’s BTC sale sends Polymarket into disarray

The sale of 32 bitcoin (BTC) by Michael Saylor’s Strategy (formerly Microstrategy) has led to a dispute among Polymarket users who’ve been betting on whether or not the company would sell any of its BTC by May 31, 2026.

A Securities and Exchange Commission filing revealed that Strategy sold the BTC (despite Saylor’s promises to never sell) between May 26 and May 31.

However, the firm’s Form 8-K wasn’t filed until June 1.

Before the filing was noted, the market had a proposed outcome of “No.” It then resolved to “No” again, after the original outcome was disputed.

Some UMA tokenholders in Discord attempted to justify the decision by pointing out that the announcement came after the market deadline, despite the market explicitly referring to when the sale occurs, not when it’s announced.

Needless to say, the decision by UMA token holders is controversial.

This second “No” outcome has also been disputed, and we are now in the “final review” window.

Polymarket itself has added a note to the market that says, “No information from MSTR, on-chain data, or consensus of credible reporting confirmed that MicroStrategy sold BTC within the market’s timeframe. Confirmation achieved outside of the market’s time frame does not qualify.”

Read more: Are Polymarket and Kalshi decentralized?

Similar disputes have popped up on Polymarket before. One prominent example was dubbed “Suitgate” and centered around whether or not an outfit that Volodymyr Zelenskyy wore to a NATO meeting counted as a suit.

Despite multiple outlets describing it as a suit, UMA tokenholders were reluctant to consider it as such, and it resolved to “No.”

In another example, Polymarket created a market that was meant to determine whether or not the Elon Musk-connected Department of Government Efficiency (DOGE) would “cut $3 billion of DEI contracts before March.”

The rules for this market explicitly pointed to whether or not “doge-tracker.com” showed that amount or more in cuts.

That website did show more than $3 billion in cuts, but this display was rooted in lies propagated by DOGE, and so Polymarket and UMA holders were placed between the explicit resolution criteria and reality.

Broadly, this Strategy market controversy combines with the previous failures of Polymarket resolution to undermine Polymarket’s tether to reality.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

- Toncoin price jumped as Bitcoin revisited support below $72,000.

- Bulls took advantage of Telegram-related news of a rebrand to GRAM token to push TON above $2.27.

- If buyers dominate, Toncoin could edge past $3.00 next.

Toncoin rose by nearly 20% and touched highs of $2.27 on Monday, June 1, as traders digested a surprise rebrand announcement from Telegram’s founder.

The gains for TON came even as Bitcoin and major altcoins fell sharply amid institutional capital outflows.

BTC slid to lows near $71,380 after news that Strategy had sold 32 BTC, its first sale since 2022.

Toncoin’s uptick signalled persistent market interest in the Telegram-backed TON blockchain despite broader market weakness.

Toncoin price gains amid GRAM rebrand news

Double-digit gains in TON’s price followed an announcement that the native token of the TON blockchain will be rebranded from Toncoin to “Gram.”

The move, expected to be completed over the next three weeks, will restore a name Telegram had previously abandoned under regulatory pressure from the US Securities and Exchange Commission.

“Gram was the original name of TON’s currency in the first white paper,” Durov wrote. “We’re returning to our roots — and starting a new chapter. This rebranding will pave the way for what comes next.”

The rebrand is part of a “Make TON Great Again” roadmap the company recently published, which includes deeper operational involvement by Telegram.

As part of that plan, Telegram disclosed its intent to become TON’s primary validator.

Investors view this as a shift that could materially affect network security and on-chain activity.

A community vote on the move is live.

Toncoin (TON) -> Gram (GRAM)

Community vote is live.

Since Telegram took a leading role in TON’s development, the chain got 10× faster, fees 6× lower.

And now Telegram proposes one more change: renaming Toncoin to Gram – the name from the original TON White Paper that never…

— TON 💎 (@ton_blockchain) June 1, 2026

As was the case then, Toncoin price rose on Monday as market participants reacted to the rebrand news.

Many see this as a signal of renewed institutional and consumer alignment between Telegram’s user base and TON’s native token.

Telegram serves more than 950 million users worldwide; tying the token more directly to the platform increases the potential utility and distribution vectors for Gram, from in-app payments to token-based services and developer integrations.

Traders interpreted the announcement as positive for token demand, prompting the swift price appreciation even as macro-driven selling pressured broader crypto markets.

Toncoin price outlook: Is a new all-time high next?

Technically, TON’s daily chart shows bullish momentum but with caveats.

The relative strength index (RSI) on the weekly timeframe has climbed to 57, indicating strong buying pressure but approaching overbought territory.

The MACD histogram remains positive, with the MACD line above the signal line, suggesting trend continuation in the short term.

These indicators together point to momentum that could extend the rally while warning that a pullback or consolidation is possible if momentum exhausts.

Key levels to watch

If TON holds above the $2.10 support established during Monday’s session, the next near-term resistance zone sits around $3.00.

As the chart shows, this is a level above which bulls could target traction towards $3.70 (100SMA) and then $6.00. TON’s all-time high is above $8.

On the downside, a decisive breakdown below $2.00 would increase the likelihood of a deeper retracement.

If bears breach lower support levels, losing $1.90 could significantly impact the probability of an immediate push toward previous highs.

Given broader market volatility and ongoing institutional flows, traders should monitor on-chain activity and Telegram’s next operational moves for confirmation that the rebrand materially increases utility and adoption.

There’s a scene in the new film Obsession (2026) that’s been living rent-free in a lot of heads since its release. A character gets a fragile little novelty toy, the “One Wish Willow”, and wishes for a billion dollars. (Spoiler alert) and cash literally rains from the ceiling. It’s absurd, it’s funny, and for about three seconds, everyone watching thinks: what would I wish for?

Here’s a better question: what if you didn’t need a wish at all?

The crypto market has always attracted dreamers. That’s not a criticism; it’s how generational wealth gets built. But there’s a difference between dreaming and deciding. Between waiting for the moment to feel right and recognizing that the moment is already here, already moving, already filling up.

Solana Unchained ($UCHN) is in Phase 1 of its presale. The price is $0.05. The listing target is $0.50. That’s a 10x multiple, not a projection, not a promise, a number locked into the structure of the raise before a single token hits an exchange. Phase 1 is already over 30% sold, and the window closes June 6, 2026.

Phase 2 Opens At $0.07. Math Doesn’t Get Easier From Here

$UCHN is a utility-driven token built on Solana, one of the fastest, most battle-tested blockchains in the world. The kind of infrastructure that doesn’t flinch when volume spikes. The kind of network that institutional money has started to take seriously. Solana Unchained is designed to operate inside that ecosystem with purpose, not as a meme, not as a gamble, but as a project built for what comes after the hype cycle settles.

The tokenomics are transparent. The roadmap is public. The presale is structured into 10 phases with incrementally rising prices, each phase rewarding those who moved earlier rather than those who wished they had.

And about that billion-dollar wish

(Spoiler alert) In Obsession, the wish works, but nobody’s in control of what happens next. A $1 billion market cap for Solana Unchained is a different kind of story. With a total supply of 100 million, a $1B market cap would put $UCHN at $10 per token. A long way from current numbers, but crypto has seen even more fascinating stories.

So, What Does Solana Unchained Do?

Solana Unchained isn’t chasing a trend; it’s building infrastructure.

At the core of the ecosystem is the AI Tool Hub, a token-gated platform giving $UCHN holders access to premium AI tools for trading insights, content automation, and DeFi workflows, live during 2026, and some will be live during presale and upon launch, not promised for someday.

Stack that with the Unchained Vault, which offers presale investors a tiered yield account paying 15% to 150% APR weekly, directly to users’ wallets in USDC or $UCHN, with zero lockup requirements. Then there’s the Unchained Wallet, a non-custodial, mobile-first wallet with built-in crypto commerce, social recovery, and on-chain inheritance, solving one of the most overlooked problems in the space: permanent loss of access.

Underneath all of it runs a Native Commerce Protocol that enables real crypto transactions without KYC or middlemen, on Solana’s fast, low-fee network. The supply is fixed to100 million tokens, and 60% is allocated to the presale. There’s no hidden inflation.

The Community Is Paying Attention, And So Are the Auditors.

Trust in crypto isn’t claimed; it’s verified. Solana Unchained has passed independent security audits by Solidproof, Spywolf, and Cyberscope, three of the most recognized names in blockchain contract verification. The team verified their identities to Spywolf, and it is on record. The audit reports are public. Some analysts have already produced coverage on the project, like Crypto League and Crypto Volt. Coverage has also landed across Fidelity, Business Insider, and Benzinga, putting Solana Unchained in front of audiences well beyond the typical crypto bubble. The foundation is audited, the community is growing, and Phase 1 closes June 6, 2026.

Website: https://www.solanaunchained.com/

X (Twitter): https://x.com/Unchained_Token

Telegram: https://t.me/Solana_unchained

Disclaimer: The above article is sponsored content; it’s written by a third party. CryptoPotato doesn’t endorse or assume responsibility for the content, advertising, products, quality, accuracy, or other materials on this page. Nothing in it should be construed as financial advice. Readers are strongly advised to verify the information independently and carefully before engaging with any company or project mentioned and to do their own research. Investing in cryptocurrencies carries a risk of capital loss, and readers are also advised to consult a professional before making any decisions that may or may not be based on the above-sponsored content.

Readers are also advised to read CryptoPotato’s full disclaimer.

The post New Obsession: Why Solana Unchained Could be the Only Wish That Makes Sense Right Now appeared first on CryptoPotato.

Shares of Michael Saylor’s Strategy fell Monday after the company disclosed its first Bitcoin sale since adopting a “never sell” philosophy, prompting fresh scrutiny of the corporate Bitcoin treasury model.

Nasdaq-traded MSTR stock was down more than 6.5% to start off the week before paring back some of that decline by early afternoon on Monday.

Although short-term price action rarely determines broader trends, Strategy’s sale of 32 Bitcoin (BTC) last week challenged the long-held perception that the company would only accumulate BTC and never liquidate its holdings, according to digital asset research and advisory firm Delphi Digital.

“The market learned that Strategy is no longer read as a pure one-way accumulation vehicle,” Delphi Digital said in a Monday commentary.

Instead, investors may increasingly view the Tysons Corner, Virginia-based business as a leveraged corporate treasury company whose decision-making is shaped not only by its Bitcoin holdings but also by preferred-share dividends, market-to-Bitcoin net asset value (mNAV) dynamics, equity issuance and broader balance-sheet considerations.

The shift has reframed the debate around Strategy’s role in the Bitcoin market. Rather than asking whether the company can sell Bitcoin, investors are now evaluating how to price a company whose BTC reserves may serve as a source of liquidity when financial obligations or capital-management needs arise.

“The old ‘never sell’ meme is now broken in practice, not just in conference call language,” Miami Beach, Florida-based Delphi said.

While the sale represented only a tiny fraction of Strategy’s Bitcoin holdings, Delphi said its significance lies in what it signals about the flexibility of the company’s treasury strategy and its potential impact on Bitcoin market dynamics.

Related: Bitcoin treasury space still has fair share of ‘carnival barkers’: BSTR founder

Strategy says sale supports shareholder value, not shift away from Bitcoin

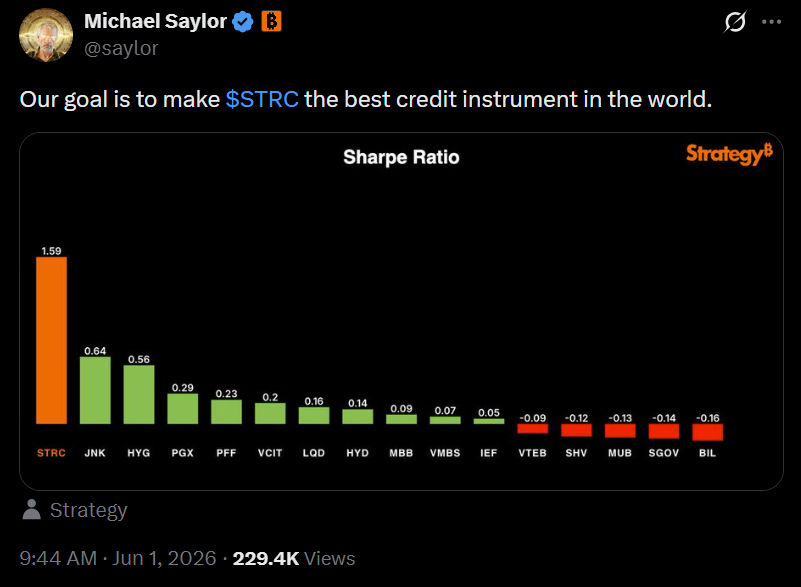

Despite criticism from some market participants, Strategy executive chairman Michael Saylor framed the sale as part of a broader effort to support STRC, the company’s yield-bearing preferred stock that offers investors income backed by Strategy’s Bitcoin holdings.

According to Saylor, the move reflects a more active approach to balance-sheet management aimed at maximizing shareholder value and improving the company’s Bitcoin-per-share metric — a key measure that tracks how much BTC backs each fully diluted share.

Source: Michael Saylor on X.com

Saylor hinted at the strategy in May, suggesting that selectively managing the company’s Bitcoin holdings could help optimize returns for shareholders. Strategy CEO Phong Le also said selling Bitcoin near the company’s cost basis could reduce potential tax liabilities associated with STRC, benefiting investors in the income-focused security.

The average cost of the company’s holdings is $75,701 per BTC, according to Iceland-registered StrategyTracker.com.

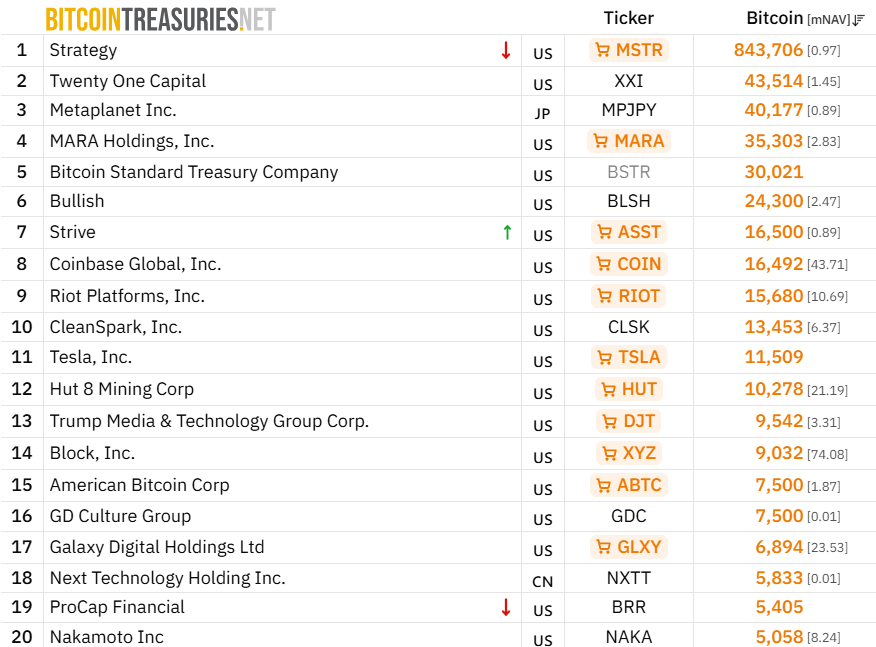

The sale does little to alter Strategy’s broader Bitcoin treasury portfolio. The company remains the world’s largest corporate Bitcoin holder by a wide margin, with more than 843,000 BTC on its balance sheet, according to BitcoinTreasuries.NET.

Related: Crypto Biz: Crypto infrastructure spending rises as ETF appetite cools

The world’s largest public Bitcoin holders. Source: BitcoinTreasuries.NET

Twenty One Capital, a Tether-controlled bitcoin (BTC) treasury company that’s paid Strike’s Jack Mallers to be its spokesperson, has until Friday to comply with an independent director rule under threat of the New York Stock Exchange (NYSE) flagging its stock with code BC, Below Compliance.

It doesn’t help that its stock has lost 83% of its value over the past year.

This morning, Twenty One Capital disclosed the Friday deadline. It’s known about the deficiency for about two weeks, including a formal non-compliance notice it received from NYSE last week.

Although a BC flag by NYSE is a clear warning, it is not an automatic halt or delisting. The company typically receives a time period to regain compliance.

The trigger for NYSE’s warning was Twenty One’s May 19 transaction. On that day, Tether bought out SoftBank’s entire 89,106,748 Class A share position and cancelled its matching Class B shares.

That same deal terminated a governance agreement that had given SoftBank a veto on board composition and other material corporate actions.

SoftBank’s two directors, Jared Roscoe and Vikas Parekh, resigned the same day.

Read more: The more Jack Mallers says Twenty One is ‘different,’ the more its stock falls

Importantly, Roscoe sat on the audit committee. As a result, his departure left only one independent member of the two required by NYSE on that particular committee during Twenty One’s post-listing transition period.

Twenty One must remedy audit committee non-compliance

On May 29, the NYSE formally sent Twenty One a non-compliance notice.

The deadline for remedying the situation is Friday. If not cured by that date, a BC indicator will accompany Twenty One to XXI’s NYSE profile, market data, and news pages on June 9, with further enforcement to come.

Twenty One says it expects to appoint an additional independent audit committee member promptly. It didn’t specify who has the power to pick a sufficiently independent director.

It is a so-called bitcoin (BTC) treasury company, last disclosing 43,514 BTC in holdings. Although its BTC is worth $3.1 billion, the entire market cap of Twenty One is less than $2.5 billion.

Amid uncertainty about Tether’s leadership and Tether-aligned Raphael Zagury taking over many of Mallers’ former responsibilities, as well as Mallers’ broken promises to launch a variety of profitable business operations under the Twenty One umbrella over the past year, its stock has lost more than four-fifths of its value over the past 12 months.

Tether CEO Paolo Ardoino reiterated on May 20 that his company’s conviction in Twenty One had only deepened, and that he looked forward to building on that foundation.

Nine days later the foundation was out of compliance with NYSE rules. Twenty One has until Friday to find a sufficiently independent director.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

A group of lawmakers within Japan’s Liberal Democratic Party (LDP) are seeking reforms to the country’s cryptocurrency taxation system, as well as support for initiatives for the development and adoption of yen-denominated stablecoins.

According to a Monday Nada News report, the LDP’s Parliamentary Association for the Promotion of Blockchain delivered recommendations to Finance Minister Satsuki Katayama, including provisions on stablecoins, exchange-traded funds (ETFs), central bank digital currencies (CBDCs), and applications for blockchain technology.

The document proposes doubling the leverage cap for retail cryptocurrency derivatives trading and establishing a framework for ETFs tied to digital assets.

Katayama reportedly responded to the proposals by saying Japan “must move forward without falling behind global developments,” referencing crypto legislation and frameworks in the United States.

“We must advance initiatives to expand on-chain finance across Asia — including the development and adoption of yen-denominated stablecoins,” LDP member Junichi Kanda said at a Monday press conference.

Finance Minister Satsuki Katayama (second from left) in a December 2024 meeting on Promotion of a Digital Society. Source: LDP

The recommendation came about two months after the Japanese government approved changes to allow classification of crypto assets as financial instruments rather than solely as a method of payment. The country’s financial watchdog, the Financial Services Agency, also reportedly planned to amend its regulatory framework to allow crypto ETFs.

Related: Japan PM Takaichi disavows ‘Sanae Token’ after memecoin hits $28M peak

Japan’s potential entry into the global $320 billion stablecoin market, now dominated by tokens pegged to the US dollar, comes after US lawmakers enacted legislation for a payment stablecoin framework, the GENIUS Act. According to an April report from the Bank for International Settlements, the market capitalization of Japanese yen-denominated stablecoins was less than 0.01% of US dollar-pegged coins.

Source: Pexels

Polymarket reported eyeing Japanese market

Prediction markets platform Polymarket, already facing regulatory scrutiny in the US amid state-level lawsuits and while supported at the federal level, was reportedly looking at approval to operate in Japan by 2030. Japan’s strict laws covering online and in-person gambling could prove a challenge for the company.

Magazine: 50K investors fight Korean crypto tax, Singapore cancels Bsquared: Asia Express

Vitalik Buterin criticized frontier AI companies for embracing AI nationalism on the same day that Senator Bernie Sanders unveiled a plan to push 50% of those firms into a federal sovereign wealth fund.

The Ethereum (ETH) co-founder posted his rebuke as a quote-reply to the Sanders proposal, which would impose a one-time equity tax on OpenAI, Anthropic, xAI, and other frontier labs and transfer their shares into public ownership.

Bernie Sanders Proposes 50% Public Stake in Top AI Firms

Writing in the New York Times, Sanders outlined the American AI Sovereign Wealth Fund Act, planned for introduction within weeks.

The fund would hold public equity, give the government voting shares, and seat representatives on each company’s board.

Sanders argued that AI is trained on humanity’s collective knowledge, art, code, and conversations, so the wealth should not flow only to a few executives. He named Sam Altman and Elon Musk as figures whose ownership would shrink.

“Let us be clear. Artificial intelligence was not created out of thin air. The data and language used by generative A.I. tools didn’t just pop into Sam Altman’s head or Elon Musk’s imagination…Since A.I. is built on the collective knowledge of humanity, the wealth it generates must benefit humanity. Not just Mr. Musk, Mr. Altman, Dario Amodei and other moguls whose companies are positioned to dominate the industry,” he wrote.

Follow us on X to get the latest news as it happens

The targeted firms, several of which recently entered the trillion-dollar pre-IPO club, have not publicly responded.

The proposal builds on his earlier AI regulation push and on the AI Data Center Moratorium Act, which he co-sponsored with Alexandria Ocasio-Cortez.

Sanders cited Norway’s oil sovereign wealth fund as a precedent.

Vitalik Calls Out AI Nationalism Frame

Against this backdrop, Vitalik Buterin attacked the rhetoric driving frontier AI policy. He argued that labs, which once promised to serve all of humanity, now justify their concentration of power by pointing to China.

“One of the many things I dislike about the style of ‘make AI go well’ discourse from frontier AI companies is how nationalist the whole thing has gotten. In the 2010s, it was: ‘we’re here to benefit all of humanity’. In the 2020s, ‘we’re here to benefit all of 4% of humanity’,” the Ethereum executive stated.

His earlier writing on Vitalik AI totalitarian risks pushed back against zero-sum framings. The US-China AI race has dominated industry lobbying.

Legal Experts Warn of Public Backlash

Kevin Frazier, a law professor focused on AI policy, said Sanders’ essay reads as a warning shot to an industry that has avoided public input.

“Absent more meaningful mechanisms for people to share their views on AI and shape its development, the backlash will grow and ‘missed uses’ will become the default…,” he suggested.

The global AI regulation debate has split along familiar lines, with progressives backing public ownership and industry voices warning of a dampened investment climate.

Sanders said the full bill text will follow soon.

The post Vitalik Buterin Criticizes AI Nationalism as US Senator Pushes for 50% Stake in OpenAI appeared first on BeInCrypto.

SpaceX has added new IPO filing language that gives the company room to issue large amounts of stock for future deals.

Summary

- SpaceX’s amended S-1/A filing states that the company may issue significant amounts of equity for future acquisitions, divestitures, and strategic transactions.

- The filing shows SpaceX is targeting a Nasdaq listing under the ticker SPCX, with a potential $75 billion raise and a minimum valuation of $1.8 trillion.

- SpaceX’s pending acquisition of Cursor shows how the company may use Class A stock as deal currency after the IPO.

The amended S-1/A filing states that SpaceX may issue a significant amount of equity in connection with future transactions, including acquisitions, divestitures, and other strategic moves. The disclosure gives investors a clearer view of how the company may use its publicly traded shares following a planned Nasdaq debut under the ticker SPCX.

SpaceX adds deal language before listing

According to the updated filing, SpaceX is preparing for an offering that could raise up to $75 billion. The filing pegs the company’s valuation at a minimum of $1.8 trillion, down from earlier internal discussions that had set the target above $2 trillion.

SpaceX filed its amended IPO filing (S-1/A) today.

Here's everything new that I found:

• In relation to acquisitions, divestitures, or other strategic transactions, @SpaceX says they "may issue a significant amount of equity in connection with future transactions." 👀— Sawyer Merritt (@SawyerMerritt) June 1, 2026

Reuters previously reported that SpaceX was targeting a June 12 listing, with pricing expected around June 11. The company first confidentially submitted its IPO paperwork to the U.S. Securities and Exchange Commission on April 1, according to public filing details cited in the registration statement. SpaceX later made its full S-1 public on May 20.

The amended filing does not say SpaceX has finalized any additional transaction beyond those already disclosed. However, the company’s wording gives it flexibility to issue Class A stock in major corporate moves after the IPO.

Cursor deal shows how shares may be used

The clearest example in the filing is SpaceX’s pending acquisition of Cursor, the AI coding assistant. According to the S-1/A, the transaction is expected to close after the IPO and will be paid entirely in Class A common stock.

The filing places Cursor’s implied equity value at $60 billion. It also says Cursor is entitled to a $1.5 billion termination fee and an $8.5 billion deferred services fee under a separate compute agreement.

Through that structure, SpaceX is telling investors that its public equity may serve as more than IPO fundraising stock. The filing shows the company could use its shares to acquire technology, deepen its AI operations, and expand its post-listing business structure.

SpaceX’s filing describes the company as an AI services and infrastructure business, not only a launch and satellite operator. The wording follows its February 2026 merger with xAI, which valued the combined company at about $1.25 trillion, according to the filing.

The company also outlines planned work with Tesla and Intel through Terafab. According to the registration statement, those plans include modular orbital AI compute infrastructure before the end of the decade.

SpaceX also lists long-term projects tied to asteroid mining and manufacturing infrastructure on the Moon and Mars. The company presents those plans as part of its future market opportunity, although the filing notes that many goals remain subject to execution, funding, and technical risks.

Elon Musk keeps voting control

Regarding ownership, the amended filing states that Elon Musk holds about 42% of SpaceX’s equity and controls 85% of the voting power through a dual-class share structure. As a result, the filing indicates that future equity issuance would not necessarily reduce Musk’s control over the company’s decisions.

The S-1/A also reserves up to 5% of IPO shares for a directed share program covering employees, friends, and family of executive officers. The filing says friends-and-family participants will not face lock-up limits, while more than 60% of pre-IPO shares, including Musk’s holdings, will remain under an extended lock-up after the listing.

Crypto investment products recorded their second-largest weekly outflow of 2026 by the end of May, with investors pulling $1.67 billion from digital asset funds as geopolitical tensions and a broader risk-off mood weighed on markets, according to a report from CoinShares.

The withdrawals marked the third consecutive week of net outflows and brought total redemptions over the past three weeks to $4.21 billion. CoinShares said concerns surrounding Iran had overwhelmed any positive sentiment generated by recent progress on the CLARITY Act, a U.S. crypto market structure bill.

Assets under management across digital asset investment products fell to $141 billion from $148 billion the previous week, their lowest level since early April.

The latest outflows coincide with a sharp decline in crypto prices. Bitcoin fell close to the $70,000 mark on Monday after reports that Iran had halted talks with the United States in protest over Israel’s continued incursions into Lebanon. The move coincided with Strategy (MSTR), the largest holder of bitcoin, selling some of its stack after years of its executive chairman Michal Saylor vowing he wouldn’t do so. The largest cryptocurrency dropped about 3% over the past 24 hour period, adding pressure to digital asset investment products.

The United States accounted for nearly all of last week’s withdrawals, with investors pulling $1.63 billion from crypto funds. Germany, which had largely avoided earlier bouts of selling, recorded $25.7 million in outflows. Sweden and Hong Kong posted withdrawals of $6.6 million and $4.5 million, respectively.

Bitcoin investment products saw the largest share of the selling, losing $1.44 billion during the week. According to CoinShares, that was the largest weekly bitcoin outflow of 2026, surpassing both the previous week’s record and the peak reached during January’s selloff. Year-to-date bitcoin inflows have fallen sharply to $1.19 billion, down from $2.6 billion a week earlier and $3.9 billion two weeks ago.

Ethereum (ETH) funds also came under pressure, recording $257.3 million in outflows. Meanwhile, investor appetite for alternative cryptocurrencies weakened considerably. CoinShares noted that only five digital assets attracted more than $1 million in inflows, down from 11 assets three weeks ago. XRP (XRP) led with $20.3 million in inflows, followed by Hyperliquid (HYPE) at $10.8 million and Near at $7.6 million.

Despite the recent pullback, crypto investment products still hold roughly $142 billion in assets globally, underscoring how much institutional capital remains invested in the sector even as market sentiment deteriorates.

Vitalik Buterin has proposed an options-based design for crypto index products that could reduce DeFi’s dependence on forced liquidations.

Summary

- Vitalik Buterin proposed an options-based DeFi design to reduce reliance on sudden liquidation systems.

- Buterin said options contracts could help create crypto index assets without the need for collateralized debt positions.

- The proposed model could use slower oracles to reduce risks associated with manipulated price feeds.

Buterin’s research post, published Monday, set out a model where index-tracking crypto assets use options contracts instead of collateralized debt positions, the structure used across many DeFi lending and synthetic asset systems.

Buterin Proposes Options-Based DeFi Structure

In the post, the Ethereum co-founder asked whether DeFi products could use options as their base layer instead of systems built around debt and liquidation engines. According to Buterin, such a model could allow users to gain exposure to a basket of crypto assets, similar to an index product, without suffering the sudden loss of a position when collateral values fall sharply.

Many DeFi protocols today allow users to borrow against crypto collateral. When collateral drops below a required level, the protocol can automatically liquidate the position. Buterin’s post said this structure can create abrupt outcomes for users and can add pressure during volatile market periods.

Under the options-based design described by Buterin, a user’s exposure would not end through an immediate liquidation event. Instead, the position would gradually move away from its target allocation as market prices change. Buterin presented that difference as a possible way to make crypto investment products less dependent on leverage-based failure points.

Slow Oracles Could Reduce Manipulation Risk

Buterin also linked the proposal to the oracle problem in DeFi. According to his research post, many DeFi applications rely on fast price feeds because liquidation systems need current market prices to decide when positions should be closed.

Those fast feeds can become a weak point when markets move quickly or when attackers try to distort prices. Buterin said an options-based structure could work with slower-moving oracles, similar to the type used in prediction markets.

In his view, slower oracles may reduce the need for protocols to act on price updates within seconds. Buterin also said he would feel much safer holding algorithmic stablecoins built with an options-based design than holding stablecoins that depend on real-time oracles, which could be manipulated.

Algorithmic Stablecoins Remain a Key Use Case

The proposal has clear relevance for algorithmic stablecoins, which have often depended on collateral systems, price feeds, and automated market actions. Buterin’s post did not name a specific stablecoin project, and the model remains theoretical rather than deployed on Ethereum.

Buterin also acknowledged practical limits. According to the post, an options-based system would still require regular portfolio rebalancing. He said it remains unclear whether those trades can happen cheaply enough to avoid high costs, poor execution, or slippage.

The research post comes as Buterin has also changed his plans for publishing long-form work. As previously covered by crypto.news, Buterin said he will stop writing regular blog posts and instead plans to try writing science fiction stories about decentralized governance.

Buterin’s past essays have covered DAOs, Layer 2 systems, voting models, and governance design across crypto and public institutions. In the latest proposal, he returned to a familiar theme, questioning whether DeFi systems can become safer by relying less on fragile automated debt structures.

On June 1, 2026, Strategy disclosed in an 8-K filing that it sold 32 Bitcoin between May 26 and May 31 at an average price of $77,135, raising about $2.5 million. It was the company’s first Bitcoin sale since December 2022, and for an outfit built on Michael Saylor’s promise never to sell, the symbolism landed harder than the number.

Summary

- Strategy sold 32 Bitcoin for about $2.5 million, marking its first Bitcoin sale since December 2022.

- Proceeds from the sale are expected to fund preferred stock dividends as the company’s mNAV premium has narrowed.

- The transaction represented just 0.0038% of Strategy’s Bitcoin holdings, but it signaled a change from an unconditional buying approach to a more active balance sheet strategy.

Bitcoin (BTC) slipped below $72,000 within hours. More than $93 million in futures positions liquidated in a single hour, 95% of them longs. MSTR stock fell around 5%. And yet the sale itself was almost nothing: 32 coins out of 843,706, roughly 0.0038% of the stack, sold to help fund a preferred-stock dividend.

This piece separates what actually happened from what the headline implies, explains the dividend machine that forced the sale, and works through what it does and does not mean for Bitcoin holders.

What actually happened

Strip away the reaction and the event is small. Strategy sold 32 Bitcoin over six days in late May, averaging $77,135 a coin, for about $2.5 million total. The 8-K signed by general counsel Thomas Chow is blunt about the reason: proceeds are expected to fund distributions on preferred stock.

The scale is almost comically minor against the company’s position. Strategy still holds 843,706 BTC, worth roughly $61 billion at current prices, acquired at a blended cost of $75,699 per coin. The 32 coins sold represent about 0.0038% of that.

In the same week, the company raised $128.3 million selling its own common shares through its at-the-market program, which dwarfs the Bitcoin sale by a factor of fifty.

So if you are picturing Saylor dumping Bitcoin, recalibrate. This was a rounding error executed to cover a cash obligation, and it was flagged in advance.

Saylor telegraphed the possibility on the Q1 earnings call in early May, and CEO Phong Le spelled out the mechanism plainly: Bitcoin would be sold to finance dividends under specific conditions. The market knew this was coming. It still flinched when it arrived.

The reason it flinched is doctrine, not arithmetic.

Why a tiny sale broke a big rule

For five years, Saylor’s pitch was absolute. Strategy buys Bitcoin and never sells. That promise was the spine of the whole thesis, the thing that made MSTR a leveraged Bitcoin proxy rather than a fund that might trade around its position. Holders bought the stock partly because they trusted the company would ride out any drawdown without capitulating.

The December 2022 sale, the only prior one, came with an asterisk that preserved the doctrine. The company sold 704 BTC near the cycle bottom, then bought back 810 two days later in what everyone read as a tax-loss harvest. Sell to bank the loss for tax purposes, rebuy immediately, end up with more coins. It was a maneuver, not a retreat, and the “never sell” story survived it.

This time there is no asterisk. The sale funds a dividend, and the company has explicitly said future sales are part of how it will manage the balance sheet. That is a different posture. Saylor has reframed it around a new metric he calls Bitcoin per share, or BPS, which he describes as “EPS on the Bitcoin Standard.” The idea is that what matters for shareholders is not the absolute size of the stack but how much Bitcoin each share represents, and that selectively selling Bitcoin to fund obligations can, under the right conditions, protect or even raise that per-share number.

Whether you find that convincing or not, the practical point is clear: “never sell” is over, replaced by “sell when the math says to.” The market reacted to the death of the doctrine, not to the loss of 32 coins.

The dividend machine that forced it

To understand why Strategy sold anything at all, you have to look at what the company has become. It is no longer just a firm with a big Bitcoin pile. It is the largest issuer of what it calls Digital Credit in the world, with more than $13.5 billion of preferred equity outstanding across five series.

The biggest of these is STRC, branded Stretch, a perpetual preferred stock that has scaled to $8.5 billion in nine months and now pays an 11.50% annual dividend. Add the other series (STRF at 10%, STRK at 8%, STRD at 10%, and the euro-denominated STRE), and Strategy carries roughly $1.5 billion in annual dividend obligations. Those are fixed cash commitments. They come due whether Bitcoin is up or down, and the company has now met 23 consecutive distributions totaling over $693 million.

Here is the engine. Strategy normally funds those dividends by issuing new MSTR common shares through its at-the-market program and using the cash. That works as long as the stock trades at a high enough premium to the underlying Bitcoin, a ratio the company tracks as mNAV. At Q1 2026, the breakeven threshold sat around 1.22x. Above that line, issuing shares to raise cash is accretive in Bitcoin-per-share terms. Below it, the arithmetic reverses, and selling shares to pay dividends starts destroying per-share value.

The problem is that mNAV has compressed hard. It ran as high as 3.89x in late 2024. By mid-2026 it had fallen to around 1.2x, right at or below the breakeven line. When the premium gets that thin, the share-issuance engine sputters, because every share sold is barely accretive or outright dilutive. So the company reaches for the next lever: selling a small amount of Bitcoin directly to cover the cash need. That is exactly what the 32-coin sale was. Not a change of heart about Bitcoin, but the dividend machine switching fuel sources when its primary fuel got expensive.

Strategy also has context that softens the picture. Le said the company has about 18 months of dividend coverage at the current run rate, backed by nearly $60 billion in Bitcoin. The 32 coins were even sold at a small profit, about 1.9% above the blended cost basis. This is not a company scrambling. It is a company optimizing its cash position, drawing down an oversized reserve and supplementing it with selective sales rather than sitting on idle capital.

What it means for Bitcoin: the honest read

Now the question that matters for most readers. Does a Bitcoin holder need to care that Strategy sold?

In the immediate, mechanical sense, no. Thirty-two coins is nothing. It does not move supply, it does not represent meaningful selling pressure, and the price drop that followed was a sentiment and leverage reaction, not the weight of $2.5 million hitting the order book. The $93 million in liquidations came from over-leveraged longs getting flushed on a headline, which is a story about positioning and fragility, not about Bitcoin’s fundamentals.

In the larger sense, there is something real to watch, and it is not this sale. It is the precedent and the structure behind it. Strategy is the single largest corporate holder of Bitcoin, and it has now established that it will sell Bitcoin to meet fixed dollar obligations when its preferred premium compresses. As long as mNAV stays healthy, those sales remain tiny and occasional, funded mostly by share issuance. But the model has a stress point: if Bitcoin stays depressed, mNAV stays compressed, and the share-issuance channel stays expensive, the company leans harder on Bitcoin sales to service a dividend stack that does not shrink.

That dynamic is worth understanding precisely because it runs opposite to the way Strategy supported Bitcoin on the way up. For years the company was a one-way buyer, absorbing supply and amplifying rallies. The new posture introduces, for the first time, a scenario where the largest corporate holder becomes a price-sensitive seller during weakness rather than a buyer. The amounts today are trivial. The direction of the incentive is what changed.

The reassuring part: the structure has real buffers. Eighteen months of coverage, a $60 billion Bitcoin backstop, $26 billion in remaining share-issuance capacity, and a preferred-stock product that, whatever you think of its complexity, has kept paying for 23 straight distributions. None of that points to forced large-scale selling at current levels. The bears’ nightmare, a cascade where Strategy has to dump Bitcoin into a falling market to survive, would require a much deeper and longer drawdown than what exists today.

So the balanced read is this. The 32-coin sale itself is noise. The shift it confirms, from an unconditional buyer to a balance-sheet manager that will sell when the math demands, is signal. For Bitcoin holders, it means the Strategy backstop is conditional now, not absolute. That is a meaningful change in the market’s structure even though this particular sale changes almost nothing.

The 2022 parallel, and why it is shakier this time

Some bulls have seized on the timing. The last time Strategy sold, in December 2022, it marked almost the exact bottom of that cycle. Sell, rebuy two days later, and the market bottomed within weeks. The pattern-match is tempting: Strategy sells, therefore bottom.

Be careful with it. The 2022 sale was a deliberate tax maneuver executed near a known cycle low, with an immediate rebuy. This sale is a dividend-funding operation driven by a compressed premium, with no rebuy and an explicit statement that more sales may follow. The mechanism is different, the intent is different, and the company is a far more complex financial machine than it was three and a half years ago. A coincidence of “Strategy sold and price was low” is not a reliable bottoming indicator. If Bitcoin does bottom here, it will be for macro and flow reasons, not because 32 coins changed hands.

The honest bottom line

Michael Saylor sold Bitcoin, and the accurate version of that sentence is much smaller than the headline. Strategy sold 32 coins, 0.0038% of its holdings, at a small profit, to help cover a preferred-stock dividend, and it told everyone in advance that it would. The market dropped on the symbolism of a broken “never sell” promise and on leveraged longs getting liquidated, not on the weight of the sale.

What changed is the doctrine. Strategy is no longer an unconditional Bitcoin buyer. It is now a balance-sheet manager that will sell Bitcoin when its premium compresses below the level where issuing shares makes sense.

At today’s mNAV, with 18 months of dividend coverage and a $60 billion backstop, that means tiny, occasional sales. In a prolonged bear market, it could mean more. The amounts are trivial now. The incentive structure is what flipped.

For Bitcoin holders, the practical takeaway is to ignore this sale and watch the mechanism. The number that matters is not 32 coins. It is Strategy’s mNAV, the health of its preferred-stock issuance, and how long Bitcoin stays below the company’s cost basis.

As long as those stay sound, the largest corporate holder remains a net accumulator. If they deteriorate, the market will have to price in something it never had to before: a Saylor who sells.

Frequently Asked Questions

How much Bitcoin did Michael Saylor’s Strategy actually sell?

Strategy sold 32 Bitcoin between May 26 and May 31, 2026, at an average price of $77,135, for roughly $2.5 million total. That represents about 0.0038% of the company’s 843,706 BTC holdings. It was the first sale since December 2022.

Why did Strategy sell Bitcoin?

The 8-K filing states the proceeds are expected to fund distributions on the company’s preferred stock. Strategy carries roughly $1.5 billion in annual dividend obligations across five preferred series. It normally funds these by issuing common shares, but with its mNAV premium compressed to around 1.2x, selling a small amount of Bitcoin directly became the more efficient way to raise the cash.

Does this mean Saylor lost faith in Bitcoin?

No. The sale was 32 coins out of more than 843,000, executed for a specific cash-management reason and flagged in advance. Saylor has reframed strategy around a metric he calls Bitcoin per share, arguing that selective sales to fund obligations can protect per-share value. The company still holds about $61 billion in Bitcoin and remains the largest corporate holder.

Why did Bitcoin’s price drop so much on such a small sale?

The drop was driven by sentiment and leverage, not the size of the sale. The end of Saylor’s “never sell” doctrine spooked the market, and over $93 million in futures positions liquidated in a single hour, 95% of them longs. A small headline triggered a cascade among over-leveraged traders. The $2.5 million sale itself had no meaningful effect on supply.

What is mNAV and why does it matter here?

mNAV measures Strategy’s stock-market value relative to its Bitcoin holdings. When it trades at a high premium, the company can issue shares to fund dividends accretively. The breakeven threshold was around 1.22x at Q1 2026. As of mid-2026 it had compressed to around 1.2x, near the line where share issuance stops being accretive, which is why the company turned to selling Bitcoin instead.

Is this the same as the 2022 sale?

Not really. The December 2022 sale was a tax-loss harvest near the cycle bottom, with an immediate rebuy two days later, which preserved the “never sell” narrative. This sale funds a dividend, has no rebuy, and comes with an explicit statement that more sales may follow. The mechanism and intent are different, so the “this marks the bottom” comparison is shakier than it looks.

Should Bitcoin holders be worried?

The sale itself is negligible. What is worth watching is the precedent: the largest corporate Bitcoin holder has established it will sell when its premium compresses. At current levels, with 18 months of dividend coverage and a $60 billion backstop, that means tiny occasional sales. The risk only grows if Bitcoin stays depressed for a long stretch, which would pressure the structure further. The incentive has shifted from unconditional buying to conditional selling.

Could Strategy be forced to sell large amounts of Bitcoin?

Not under current conditions. The company has about 18 months of dividend coverage, nearly $60 billion in Bitcoin, and around $26 billion in remaining share-issuance capacity. Forced large-scale selling would require a much deeper and longer Bitcoin drawdown than exists today. The structure has real buffers, even if the new willingness to sell at all is a change.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 1, 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

Tesco F&F launches ‘laidback’ trousers perfect for travelling this summer

Spotify’s Top 10 Most-Streamed Songs of 2026 (Through May 31) Led by Bruno Mars and Lady Gaga Collab

Toncoin price soars as Telegram eyes TON’s rebrand to GRAM

-

NewsBeat5 days ago

NewsBeat5 days agoIsrael says it has killed new Hamas military leader in Gaza City airstrikes

-

Tech6 days ago

Tech6 days agoNASA taps Blue Origin to deliver lunar rovers for Moon Base initiative

-

Sports7 days ago

Sports7 days ago2026 NBA Finals schedule, odds: Knicks await Thunder or Spurs after winning East

-

News Videos6 days ago

News Videos6 days agoXRP *JUST* SUCCEEDED!!!! CLARITY ACT EXPOSED!!! (SHE EXPOSED IT)

-

News Videos3 days ago

News Videos3 days agoThis is BROKEN! INSANE 5x MONEY CAR WASH WEEK! The NEW GTA Online UPDATE Today! (GTA5 New Update)

-

Crypto World6 days ago

Crypto World6 days agoMicron Crosses $1 Trillion Market Cap as AI Demand Reshapes Memory Sector

-

Business6 days ago

Business6 days agoSelena Gomez Reportedly Upset Over Benny Blanco’s Comments on Her ‘Terrible’ Diet

-

Business7 days ago

Business7 days agoNikkei 225 Surges Past 65,000 for First Time as Iran Peace Hopes Fuel Record Rally

-

Tech7 days ago

Tech7 days agoChina assigns ID codes to 28,000+ humanoid robots

-

Tech4 days ago

Tech4 days agoWaymo dominates autonomous vehicle registrations as Tesla trails behind

-

Entertainment7 days ago

Entertainment7 days ago‘Breaking Bad’ Star’s Easy-to-Binge 6-Part Crime Series Spin-Off Is Finally Heading to Free Streaming

-

Tech2 days ago

Tech2 days agoSpaceX just won a second Golden Dome contract. This one is $4.16 billion.

-

Tech5 days ago

Tech5 days agoThe Samsung pay deal is the moment Korean unions changed register

-

Entertainment6 days ago

Entertainment6 days agoDays of our Lives 2-Week Spoilers May 25-June 5: Gwen Rages, Abe Confesses & 2 Tragic Anniversaries!

-

News Videos3 days ago

News Videos3 days agoSHE IS KILLING XRP!!! WATCH URGENT AND ACT FAST

-

NewsBeat3 days ago

NewsBeat3 days agoFIRST NIGHT REVIEW: Take That bring the Circus back to life in spectacular sun-soaked style

-

Entertainment7 days ago

Entertainment7 days agoTaylor Swift Fans Label Travis Kelce’s Beer-Chugging A ‘Red Flag

-

Tech6 days ago

Tech6 days agoMillions of AI agents imperiled by critical vulnerability in open source package

-

Crypto World5 days ago

SpaceX’s $2 Trillion IPO: Why Tech Giants Nvidia (NVDA), Apple (AAPL), and Microsoft (MSFT) May Face Pressure

-

Crypto World3 days ago

CFTC Has Approved the First Regulated Bitcoin Perpetual Contract in the U.S.

You must be logged in to post a comment Login