Crypto World

what it means for BTC

On June 1, 2026, Strategy disclosed in an 8-K filing that it sold 32 Bitcoin between May 26 and May 31 at an average price of $77,135, raising about $2.5 million. It was the company’s first Bitcoin sale since December 2022, and for an outfit built on Michael Saylor’s promise never to sell, the symbolism landed harder than the number.

Summary

- Strategy sold 32 Bitcoin for about $2.5 million, marking its first Bitcoin sale since December 2022.

- Proceeds from the sale are expected to fund preferred stock dividends as the company’s mNAV premium has narrowed.

- The transaction represented just 0.0038% of Strategy’s Bitcoin holdings, but it signaled a change from an unconditional buying approach to a more active balance sheet strategy.

Bitcoin (BTC) slipped below $72,000 within hours. More than $93 million in futures positions liquidated in a single hour, 95% of them longs. MSTR stock fell around 5%. And yet the sale itself was almost nothing: 32 coins out of 843,706, roughly 0.0038% of the stack, sold to help fund a preferred-stock dividend.

This piece separates what actually happened from what the headline implies, explains the dividend machine that forced the sale, and works through what it does and does not mean for Bitcoin holders.

What actually happened

Strip away the reaction and the event is small. Strategy sold 32 Bitcoin over six days in late May, averaging $77,135 a coin, for about $2.5 million total. The 8-K signed by general counsel Thomas Chow is blunt about the reason: proceeds are expected to fund distributions on preferred stock.

The scale is almost comically minor against the company’s position. Strategy still holds 843,706 BTC, worth roughly $61 billion at current prices, acquired at a blended cost of $75,699 per coin. The 32 coins sold represent about 0.0038% of that.

In the same week, the company raised $128.3 million selling its own common shares through its at-the-market program, which dwarfs the Bitcoin sale by a factor of fifty.

So if you are picturing Saylor dumping Bitcoin, recalibrate. This was a rounding error executed to cover a cash obligation, and it was flagged in advance.

Saylor telegraphed the possibility on the Q1 earnings call in early May, and CEO Phong Le spelled out the mechanism plainly: Bitcoin would be sold to finance dividends under specific conditions. The market knew this was coming. It still flinched when it arrived.

The reason it flinched is doctrine, not arithmetic.

Why a tiny sale broke a big rule

For five years, Saylor’s pitch was absolute. Strategy buys Bitcoin and never sells. That promise was the spine of the whole thesis, the thing that made MSTR a leveraged Bitcoin proxy rather than a fund that might trade around its position. Holders bought the stock partly because they trusted the company would ride out any drawdown without capitulating.

The December 2022 sale, the only prior one, came with an asterisk that preserved the doctrine. The company sold 704 BTC near the cycle bottom, then bought back 810 two days later in what everyone read as a tax-loss harvest. Sell to bank the loss for tax purposes, rebuy immediately, end up with more coins. It was a maneuver, not a retreat, and the “never sell” story survived it.

This time there is no asterisk. The sale funds a dividend, and the company has explicitly said future sales are part of how it will manage the balance sheet. That is a different posture. Saylor has reframed it around a new metric he calls Bitcoin per share, or BPS, which he describes as “EPS on the Bitcoin Standard.” The idea is that what matters for shareholders is not the absolute size of the stack but how much Bitcoin each share represents, and that selectively selling Bitcoin to fund obligations can, under the right conditions, protect or even raise that per-share number.

Whether you find that convincing or not, the practical point is clear: “never sell” is over, replaced by “sell when the math says to.” The market reacted to the death of the doctrine, not to the loss of 32 coins.

The dividend machine that forced it

To understand why Strategy sold anything at all, you have to look at what the company has become. It is no longer just a firm with a big Bitcoin pile. It is the largest issuer of what it calls Digital Credit in the world, with more than $13.5 billion of preferred equity outstanding across five series.

The biggest of these is STRC, branded Stretch, a perpetual preferred stock that has scaled to $8.5 billion in nine months and now pays an 11.50% annual dividend. Add the other series (STRF at 10%, STRK at 8%, STRD at 10%, and the euro-denominated STRE), and Strategy carries roughly $1.5 billion in annual dividend obligations. Those are fixed cash commitments. They come due whether Bitcoin is up or down, and the company has now met 23 consecutive distributions totaling over $693 million.

Here is the engine. Strategy normally funds those dividends by issuing new MSTR common shares through its at-the-market program and using the cash. That works as long as the stock trades at a high enough premium to the underlying Bitcoin, a ratio the company tracks as mNAV. At Q1 2026, the breakeven threshold sat around 1.22x. Above that line, issuing shares to raise cash is accretive in Bitcoin-per-share terms. Below it, the arithmetic reverses, and selling shares to pay dividends starts destroying per-share value.

The problem is that mNAV has compressed hard. It ran as high as 3.89x in late 2024. By mid-2026 it had fallen to around 1.2x, right at or below the breakeven line. When the premium gets that thin, the share-issuance engine sputters, because every share sold is barely accretive or outright dilutive. So the company reaches for the next lever: selling a small amount of Bitcoin directly to cover the cash need. That is exactly what the 32-coin sale was. Not a change of heart about Bitcoin, but the dividend machine switching fuel sources when its primary fuel got expensive.

Strategy also has context that softens the picture. Le said the company has about 18 months of dividend coverage at the current run rate, backed by nearly $60 billion in Bitcoin. The 32 coins were even sold at a small profit, about 1.9% above the blended cost basis. This is not a company scrambling. It is a company optimizing its cash position, drawing down an oversized reserve and supplementing it with selective sales rather than sitting on idle capital.

What it means for Bitcoin: the honest read

Now the question that matters for most readers. Does a Bitcoin holder need to care that Strategy sold?

In the immediate, mechanical sense, no. Thirty-two coins is nothing. It does not move supply, it does not represent meaningful selling pressure, and the price drop that followed was a sentiment and leverage reaction, not the weight of $2.5 million hitting the order book. The $93 million in liquidations came from over-leveraged longs getting flushed on a headline, which is a story about positioning and fragility, not about Bitcoin’s fundamentals.

In the larger sense, there is something real to watch, and it is not this sale. It is the precedent and the structure behind it. Strategy is the single largest corporate holder of Bitcoin, and it has now established that it will sell Bitcoin to meet fixed dollar obligations when its preferred premium compresses. As long as mNAV stays healthy, those sales remain tiny and occasional, funded mostly by share issuance. But the model has a stress point: if Bitcoin stays depressed, mNAV stays compressed, and the share-issuance channel stays expensive, the company leans harder on Bitcoin sales to service a dividend stack that does not shrink.

That dynamic is worth understanding precisely because it runs opposite to the way Strategy supported Bitcoin on the way up. For years the company was a one-way buyer, absorbing supply and amplifying rallies. The new posture introduces, for the first time, a scenario where the largest corporate holder becomes a price-sensitive seller during weakness rather than a buyer. The amounts today are trivial. The direction of the incentive is what changed.

The reassuring part: the structure has real buffers. Eighteen months of coverage, a $60 billion Bitcoin backstop, $26 billion in remaining share-issuance capacity, and a preferred-stock product that, whatever you think of its complexity, has kept paying for 23 straight distributions. None of that points to forced large-scale selling at current levels. The bears’ nightmare, a cascade where Strategy has to dump Bitcoin into a falling market to survive, would require a much deeper and longer drawdown than what exists today.

So the balanced read is this. The 32-coin sale itself is noise. The shift it confirms, from an unconditional buyer to a balance-sheet manager that will sell when the math demands, is signal. For Bitcoin holders, it means the Strategy backstop is conditional now, not absolute. That is a meaningful change in the market’s structure even though this particular sale changes almost nothing.

The 2022 parallel, and why it is shakier this time

Some bulls have seized on the timing. The last time Strategy sold, in December 2022, it marked almost the exact bottom of that cycle. Sell, rebuy two days later, and the market bottomed within weeks. The pattern-match is tempting: Strategy sells, therefore bottom.

Be careful with it. The 2022 sale was a deliberate tax maneuver executed near a known cycle low, with an immediate rebuy. This sale is a dividend-funding operation driven by a compressed premium, with no rebuy and an explicit statement that more sales may follow. The mechanism is different, the intent is different, and the company is a far more complex financial machine than it was three and a half years ago. A coincidence of “Strategy sold and price was low” is not a reliable bottoming indicator. If Bitcoin does bottom here, it will be for macro and flow reasons, not because 32 coins changed hands.

The honest bottom line

Michael Saylor sold Bitcoin, and the accurate version of that sentence is much smaller than the headline. Strategy sold 32 coins, 0.0038% of its holdings, at a small profit, to help cover a preferred-stock dividend, and it told everyone in advance that it would. The market dropped on the symbolism of a broken “never sell” promise and on leveraged longs getting liquidated, not on the weight of the sale.

What changed is the doctrine. Strategy is no longer an unconditional Bitcoin buyer. It is now a balance-sheet manager that will sell Bitcoin when its premium compresses below the level where issuing shares makes sense.

At today’s mNAV, with 18 months of dividend coverage and a $60 billion backstop, that means tiny, occasional sales. In a prolonged bear market, it could mean more. The amounts are trivial now. The incentive structure is what flipped.

For Bitcoin holders, the practical takeaway is to ignore this sale and watch the mechanism. The number that matters is not 32 coins. It is Strategy’s mNAV, the health of its preferred-stock issuance, and how long Bitcoin stays below the company’s cost basis.

As long as those stay sound, the largest corporate holder remains a net accumulator. If they deteriorate, the market will have to price in something it never had to before: a Saylor who sells.

Frequently Asked Questions

How much Bitcoin did Michael Saylor’s Strategy actually sell?

Strategy sold 32 Bitcoin between May 26 and May 31, 2026, at an average price of $77,135, for roughly $2.5 million total. That represents about 0.0038% of the company’s 843,706 BTC holdings. It was the first sale since December 2022.

Why did Strategy sell Bitcoin?

The 8-K filing states the proceeds are expected to fund distributions on the company’s preferred stock. Strategy carries roughly $1.5 billion in annual dividend obligations across five preferred series. It normally funds these by issuing common shares, but with its mNAV premium compressed to around 1.2x, selling a small amount of Bitcoin directly became the more efficient way to raise the cash.

Does this mean Saylor lost faith in Bitcoin?

No. The sale was 32 coins out of more than 843,000, executed for a specific cash-management reason and flagged in advance. Saylor has reframed strategy around a metric he calls Bitcoin per share, arguing that selective sales to fund obligations can protect per-share value. The company still holds about $61 billion in Bitcoin and remains the largest corporate holder.

Why did Bitcoin’s price drop so much on such a small sale?

The drop was driven by sentiment and leverage, not the size of the sale. The end of Saylor’s “never sell” doctrine spooked the market, and over $93 million in futures positions liquidated in a single hour, 95% of them longs. A small headline triggered a cascade among over-leveraged traders. The $2.5 million sale itself had no meaningful effect on supply.

What is mNAV and why does it matter here?

mNAV measures Strategy’s stock-market value relative to its Bitcoin holdings. When it trades at a high premium, the company can issue shares to fund dividends accretively. The breakeven threshold was around 1.22x at Q1 2026. As of mid-2026 it had compressed to around 1.2x, near the line where share issuance stops being accretive, which is why the company turned to selling Bitcoin instead.

Is this the same as the 2022 sale?

Not really. The December 2022 sale was a tax-loss harvest near the cycle bottom, with an immediate rebuy two days later, which preserved the “never sell” narrative. This sale funds a dividend, has no rebuy, and comes with an explicit statement that more sales may follow. The mechanism and intent are different, so the “this marks the bottom” comparison is shakier than it looks.

Should Bitcoin holders be worried?

The sale itself is negligible. What is worth watching is the precedent: the largest corporate Bitcoin holder has established it will sell when its premium compresses. At current levels, with 18 months of dividend coverage and a $60 billion backstop, that means tiny occasional sales. The risk only grows if Bitcoin stays depressed for a long stretch, which would pressure the structure further. The incentive has shifted from unconditional buying to conditional selling.

Could Strategy be forced to sell large amounts of Bitcoin?

Not under current conditions. The company has about 18 months of dividend coverage, nearly $60 billion in Bitcoin, and around $26 billion in remaining share-issuance capacity. Forced large-scale selling would require a much deeper and longer Bitcoin drawdown than exists today. The structure has real buffers, even if the new willingness to sell at all is a change.

This article is for informational purposes and does not constitute financial or investment advice. Cryptocurrency markets are highly volatile. The figures and analysis described reflect data available as of June 1, 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

A wave of selling in the technology sector that emerged earlier this week has weighed on European equities. The trigger was investor concern over the profitability of large-scale debt-funded investments by major US tech companies in AI infrastructure. The Nasdaq and S&P 500 fell to their lowest levels in more than a week, with semiconductor manufacturers bearing the brunt of the decline.

In Germany, Infineon Technologies (-5.86%), Siemens Energy (-3.93%) and Vonovia (-3.21%) were among the worst performers, while SAP and Airbus ended the session in positive territory, gaining around 2% each. Geopolitical factors also remain in the background: a memorandum signed in June between the United States and Iran has yet to remove uncertainty, with implementation of the agreement still subject to ongoing negotiations.

Technical picture

On the H4 chart of the DAX 40 index (GDAXIm on FXOpen), after peaking around 25,450 at the end of May, price declined towards the 23,970 area, forming a downward trend structure. Following an attempted breakout of the downtrend and a gap on 15 June, the index moved into a sideways range, forming a POC zone at 24,940–24,950 and an upper boundary of the current profile at 25,070, with price now trading between these levels.

The nearest resistance is located around 25,210, which could cap the market if the upper boundary of the profile is breached. Support is seen in the 23,970 area, which could be reached if the lower boundary at 24,460 is broken. Volume remains moderate, confirming the consolidation phase. The RSI and moving averages are at 48, 54 and 54 respectively; the oscillator is below its moving averages, while the averages are converging towards neutral levels, indicating a lack of clear momentum within the current range.

Summary

Pressure on the DAX 40 is driven by a global reassessment of AI infrastructure valuations, which has triggered a sell-off in the semiconductor sector worldwide, including German equities. Price has returned to a balance area after the rebound, while the RSI remaining below its moving averages signals a lack of directional momentum on either side.

Trade global index CFDs with zero commission and tight spreads (additional fees may apply). Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

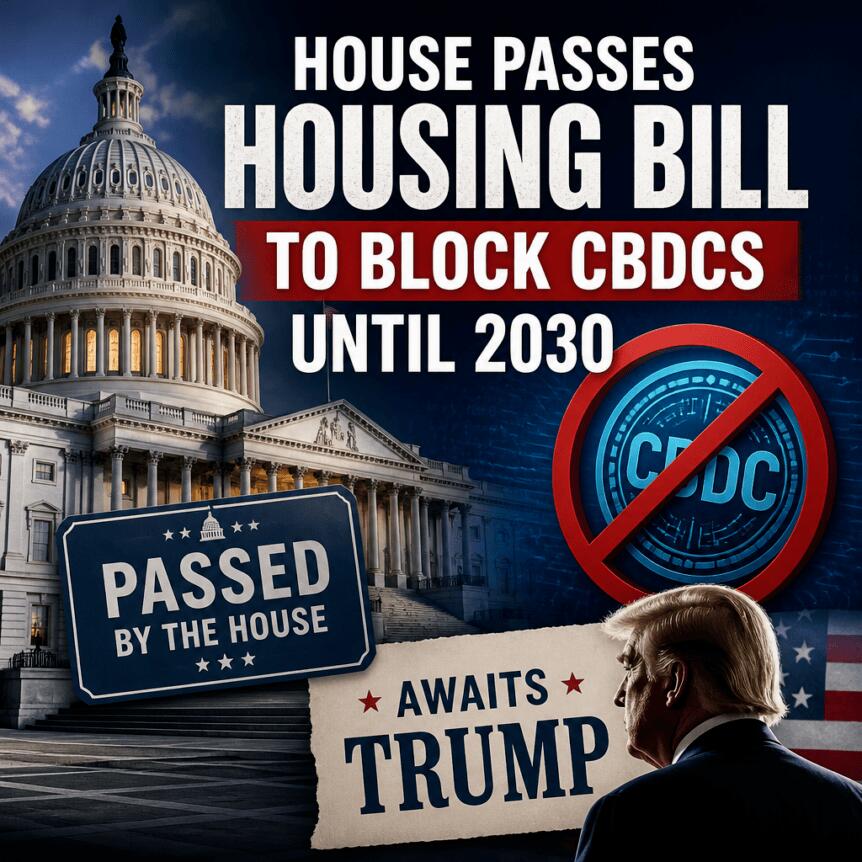

The US Senate passed sweeping bipartisan housing legislation Monday by a vote of 85-5, sending a package that includes a statutory ban on a Federal Reserve central bank digital currency through December 31, 2030 toward the president's desk. The 21st Century ROAD to Housing Act (H.R. 6644), led by… Read the full story at The Defiant

Strategy’s perpetual preferred stock Stretch (STRC) is under serious financial stress due to two simultaneous pressures, reported onchain analytics firm CryptoQuant on Tuesday.

The Bitcoin bear market means that all BTC purchased between 2024 and 2026 is underwater, with $10.6 billion in unrealized losses, and cash reserves are depleted, down 38% since early 2026 after a $1.5 billion convertible senior note repurchase in May.

Strategy pays dividends on its Stretch product, which offers an 11.5% yield and is designed to trade at $100. However, it fell to a record low of $82.5 last week, a record 17.5% below par.

At current prices of $87.4, the current effective yield is 13.2%, according to the STRC tracker.

Stop Buying Bitcoin

The core problem is that Strategy’s dividend obligations have nearly quadrupled to $1.2 billion per year, while the cash to cover them has shrunk, collapsing dividend coverage from more than seven years to just 14 months.

Last week, Strategy claimed that it had 32 years of dividend coverage using its $55 billion Bitcoin stash, but the argument was flawed.

At current dividend obligations, restoring just 24 months of coverage would require a cash reserve of approximately $2.8 billion, roughly twice what Strategy holds today, said CryptoQuant.

STRC issuance has been an effective capital-raising mechanism for Bitcoin purchases, but the rapid growth of dividend obligations has become a structural liability that could weigh on its sustainability.

“The market appears to be pricing this risk; the STRC price decline reflects not only near-term cash reserve weakness but also long-term concerns about the company’s ability to service its growing dividend burden.”

They added that any forced Bitcoin sale at current prices would crystallize its unrealized losses scale, destroy shareholder value, and potentially catalyze another leg down for BTC spot markets.

CryptoQuant recommended that the company “pause Bitcoin purchases until cash reserves and dividend coverage are restored.”

Strategy’s annualized dividend obligations have nearly quadrupled to $1.2B, while its cash reserve has fallen 38% in 2026.

Dividend coverage collapsed from 7+ years to just 14 months.

The company needs to stop buying Bitcoin and rebuild cash. pic.twitter.com/TR0oaAnT5k

— CryptoQuant.com (@cryptoquant_com) June 23, 2026

Saylor seems adamant, however, with the firm’s latest purchase of 520 BTC for $35 million while increasing its USD reserve by $300 million to $1.4 billion on Monday.

STRC, MSTR, and BTC Declining

The move gave some brief respite to STRC, which returned to $88 on Tuesday, but it remains in trouble, trading below par.

Company stock (MSTR) has also taken a beating, tanking a further 5% on Tuesday to end the day trading at $103.84, its lowest level since early 2024, according to Google Finance.

The move coincided with another Bitcoin dip as the asset failed to hold $64,000 and fell to $62,000 on Tuesday. BTC reclaimed $63,000 during the Asian trading session on Wednesday, but had already started to fall back from that level at the time of writing.

The post Saylor Should Stop Buying Bitcoin, Says CryptoQuant appeared first on CryptoPotato.

The Ethereum Foundation has cut 54 employees, roughly 20% of its staff, in the most concrete austerity measure the organization has taken since pledging to reduce its treasury spending rate. The Foundation announced the changes Tuesday, saying the cuts conclude a months-long reorganization tied to… Read the full story at The Defiant

Cboe Global Markets has launched its new prediction markets platform, Cboe Predicts, as the company enters the prediction trading market with a new suite of securities-based products.

The new offering includes binary option contracts tied to the Mini-S&P 500 Index, trading under the symbols XSPBW and XSPBX, which are already available through Interactive Brokers. Access through Charles Schwab is expected in the coming months. Cboe also said additional brokerage firms are likely to add support over time, broadening access to the new contracts.

New Prediction Markets Suite

According to the official press release, the new products allow traders to make predictions on where the Mini-S&P 500 Index, or XSP, will settle at expiration. Traders can take a “yes” position if they believe the index will close at or above a specified level or choose a “no” position if they expect it to finish below that level. The XSP index tracks the performance of the S&P 500 Index but is scaled to one-tenth the size of the larger SPX contract, which makes it a smaller, more retail-friendly alternative.

The new products also expand Cboe’s existing S&P 500 offerings. The company said it plans to add XSP vertical spreads in the future through its Quoted Spread Book system, which is designed to make more complex options strategies easier to understand. The framework aims to help traders who are familiar with simple yes-or-no contracts gradually learn more advanced trading strategies while keeping risks defined.

The products are cleared through the Options Clearing Corporation, which manages the settlement process. According to the company, the contracts will also operate under the same regulatory rules that apply to other options listed in the United States.

Commenting on the latest development, James Kostulias, Head of Trading Services, Charles Schwab, said,

“We support approaches that bring transparency, defined risk, and investor education to financial-related prediction markets. We plan to offer clients access to these binary options contracts in the coming months, building on our existing platform and demand from active traders.”

Earlier Skepticism

The latest development comes months after Charles Schwab CEO Rick Wurster expressed skepticism about prediction markets. In December, Wurster told The Wall Street Journal that event contracts tied to sports or entertainment could blur the line between investing and gambling, while adding that prediction markets were “not high on our list at the moment.”

Charles Schwab has also been expanding into new asset classes in recent months. Earlier this year, the brokerage rolled out Schwab Crypto, allowing retail clients in most US states to directly trade Bitcoin and Ethereum alongside traditional investments through the same platform.

The post CBOE Launches Prediction Markets With S&P 500 Binary Contracts appeared first on CryptoPotato.

Quick Overview

- Meta is building “Arena,” a forecasting platform enabling users to predict outcomes using points rather than actual currency.

- The platform will encompass political events, sporting matches, cultural happenings, and global news, functioning as a standalone product separate from Instagram and Facebook.

- CEO Mark Zuckerberg has designated Arena as a high-level internal initiative, despite its experimental classification.

- The company previously launched and discontinued a comparable service named Forecast between 2020 and 2022.

- While prediction markets continue expanding rapidly, they’re encountering heightened regulatory oversight concerning gaming regulations and potential market manipulation.

Meta, the organization behind Facebook, is constructing a mobile application named Arena designed as a forecasting platform. The service will enable participants to predict results of actual events spanning electoral contests, athletic competitions, and cultural phenomena. The New York Times reported details from two informed employees, noting the application will employ a points mechanism instead of monetary transactions.

Founder and CEO Mark Zuckerberg personally directed Arena’s creation, according to sources. The New York Times’ contacts characterized the initiative as simultaneously experimental and strategically significant for the corporation.

Arena will operate as an independent entity distinct from Meta’s current portfolio, which includes Facebook and Instagram. This standalone approach differs from Meta’s typical strategy of incorporating new capabilities into established platforms.

A Second Attempt at Forecasting

This represents Meta’s second venture into prediction platforms. In 2020, the company introduced Forecast, allowing participants to make predictions about current affairs and developments during the Covid-19 outbreak. The service was discontinued in 2022.

Meta has previously explored cryptocurrency and financial technology initiatives. The company unveiled Libra, a digital currency project, in 2019, which became Diem before being abandoned in 2022. Recently, Meta introduced USDC payment options for content creators in Colombia and the Philippines.

Should Arena launch successfully, it would enter direct competition with established platforms including Polymarket and Kalshi, both experiencing substantial growth. Polymarket attracted significant attention throughout the 2024 presidential election cycle, processing billions in transaction volume. With Meta recording 3.56 billion daily active participants across its ecosystem by March 2026, Arena could access an enormous existing user base.

Additional major technology companies have entered the forecasting sector. Coinbase and Kraken have investigated opportunities in this market, while Robinhood has launched event contracts connected to political developments and economic indicators.

Regulatory Challenges Intensify

The forecasting platform sector faces mounting legal challenges across the United States. The Commodity Futures Trading Commission continues disputes with state-level authorities regarding whether specific event contracts constitute illegal gambling activities.

Congress is evaluating proposed legislation addressing insider trading concerns on forecasting platforms. These efforts intensified following allegations against U.S. soldier Gannon Ken Van Dyke, who reportedly earned over $400,000 through a Polymarket position related to Venezuelan President Nicolás Maduro’s potential capture. Van Dyke’s trial is scheduled for December 2026.

Meta hasn’t announced a definitive launch timeline for Arena, nor has the company dismissed the possibility of incorporating real-money wagering features in the future.

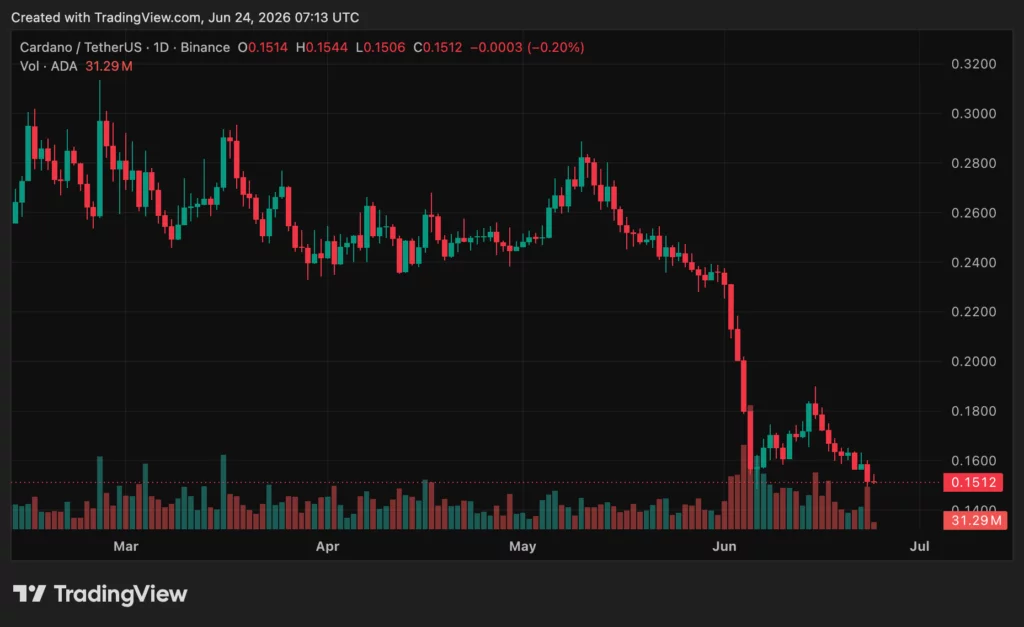

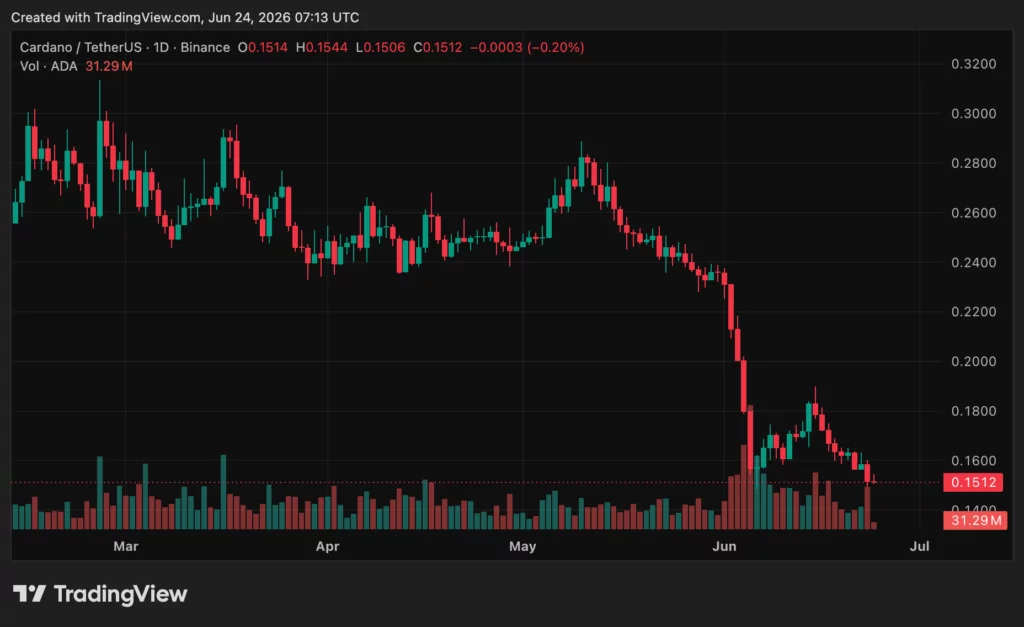

SecondFi, a Cardano ecosystem wallet project, said it has traced a recent security incident to its native Cardano web wallet generation software.

Summary

- SecondFi traced the breach to its Cardano wallet generation software after pausing platform activity Tuesday.

- SlowMist founder Cos said suspected hacker wallets suggest potential losses could exceed $20 million overall.

- The incident adds pressure on Cardano as ADA trades near multi-year lows again this month.

The team said it had contained the issue and paused affected services while it reviewed the full scope.

“We have isolated the root cause of the recent security incident,” said SecondFi in a security update. “The issue was confined to our native Cardano web wallet generation software.”

SecondFi said its on-chain review put the preliminary scale at around 16 million ADA. The team also said it was working with a blockchain security firm on an independent technical review.

SlowMist founder sees larger loss risk

SlowMist founder Cos, also known as Yu Xian, said the damage could be far larger than SecondFi’s early figure. He said the estimate depends on whether two Cardano addresses he tracked are confirmed as attacker wallets.

“The users of this wallet have likely lost over $20 million,” said SlowMist founder Cos in an X post. He said the possible loss may involve more than 129 million ADA and other tokens.

Cos later said the transaction pattern suggested an attacker may have obtained a batch of mnemonic phrases or private keys before moving funds over many hours. He said the transfers appeared to move from larger amounts to smaller ones.

Users wait for final review

SecondFi has not yet released a final technical report or a detailed compensation plan. The project said it would continue to share updates as the independent review confirms the scope and cause.

The case has drawn attention because the issue involves wallet generation, not only a smart contract or front-end error. If key generation fails, wallets created through the affected software may face direct risk.

SecondFi is the successor to Yoroi and was launched by EMURGO as a self-custody neofinance app for spending, trading, earning and saving. Cardano’s official app catalog lists SecondFi as a self-custody platform built by EMURGO.

As previously reported by crypto.news, Cardano has already faced market and ecosystem pressure this month. ADA fell below $0.20 in June, while several Cardano projects and governance fights drew wider attention. At press time, ADA traded at around $0.15, down almost 3% in the past 24 hours.

Security concerns spread beyond Cardano

The SecondFi case adds to a wider run of crypto wallet and platform security issues. In a recent update, crypto.news covered Trezor Safe 7 after Ledger Donjon found a chip flaw, though Trezor said user funds remained safe.

Previously, crypto.news explored Bo Shen’s reopened $42 million wallet hack case. SlowMist had linked that theft to a compromised mnemonic seed phrase, showing how seed phrase exposure can leave lasting recovery problems.

SecondFi users now need to follow only official project channels and avoid support scams. Breach events often trigger fake recovery accounts that ask for seed phrases, private keys or transfers.

The final loss figure remains unconfirmed. For now, SecondFi’s public estimate stands near 16 million ADA, while SlowMist’s Cos says suspected hacker activity could push possible user losses above $20 million.

Crypto World

ENS DAO Delegates Call Foundation Proposal a Governance Attack as Johnson Self-Delegates

Delegates to the ENS DAO escalated opposition to a governance proposal that would hand the ENS Foundation broad control over the protocol's treasury Monday, with one Security Council member calling it a governance attack and ENS Labs founder Nick Johnson having already self-delegated enough tokens… Read the full story at The Defiant

The U.S. House of Representatives has approved sweeping housing legislation that also contains a temporary prohibition on central bank digital currencies (CBDCs), delivering a significant policy victory for lawmakers who have sought to limit central-bank involvement in tokenized money. The measure now moves to President Donald Trump, who is expected to sign the bill into law.

According to the official House roll call, the chamber passed the 21st Century ROAD to Housing Act by a wide margin of 358–32 on Tuesday, following a similarly large vote in the Senate the day before. The bill is designed primarily to address housing affordability, but its CBDC provision—and its stablecoin carve-out—has become the most closely monitored part for the crypto and financial-services sector.

Key takeaways

- The House passed the 21st Century ROAD to Housing Act, with a CBDC restriction aimed at preventing the Federal Reserve from issuing or creating a CBDC or substantially similar digital asset until Dec. 31, 2030.

- The ban is not absolute across all crypto activity: the legislation includes a carve-out for certain dollar-denominated stablecoins described as open, permissionless, and private.

- Congressional leaders reached agreement on the bill only after earlier disagreements, indicating that the CBDC language remained a negotiable but preserved feature.

- The legislation now goes to the president for final approval, potentially shaping how financial institutions and crypto firms prepare for compliance over the 2020s.

What the bill does: a time-limited CBDC prohibition

The CBDC clause included in the housing act would bar the Federal Reserve from, “directly or indirectly,” issuing or creating a central bank digital currency—or any digital asset “substantially similar” to a CBDC—until Dec. 31, 2030. While the language is time-bound, it is intended to constrain central-bank experimentation or deployment of a tokenized central-bank form of money during the remainder of the decade.

In practice, such a restriction can influence institutional planning in several ways. Banks and other regulated financial intermediaries typically rely on clear regulatory signals for product development and risk management. By limiting the Federal Reserve’s ability to pursue a CBDC initiative through direct issuance or creation, the statute aims to reduce uncertainty for firms that view CBDCs as a shift toward centrally controlled settlement rails.

At the same time, the clause’s “substantially similar” formulation may raise interpretive questions about what qualifies as prohibited activity. Institutions subject to supervision may need to evaluate not only explicit CBDC proposals, but also any related digital-asset products that could arguably be characterized as CBDC-like. That creates compliance demand even without a CBDC being launched.

Stablecoin carve-out: narrowing the scope of the restriction

The act also incorporates a carve-out for crypto stablecoins, permitting “dollar-denominated currency” that is described as open, permissionless, and private. This drafting choice signals a legislative intent to avoid an outright ban on stablecoin functionality while still constraining the central-bank issuance of a tokenized form of fiat.

From a policy perspective, the carve-out may be read as an attempt to separate the stablecoin market—particularly private-sector dollar-linked tokens—from central-bank-issued digital currencies. For compliance teams, this distinction matters because it suggests that the bill focuses on the Federal Reserve’s role rather than imposing a blanket prohibition on stablecoin issuance or use.

However, the carve-out’s descriptors—open, permissionless, and private—could require further interpretation depending on how regulators treat access, governance, and transaction privacy. Regulated firms generally maintain compliance controls around transparency, recordkeeping, and supervisory reporting; “private” systems may require additional legal and operational review to ensure they do not undermine auditability or AML obligations.

Legislative momentum and the path to law

The bill’s rapid movement reflects a last-minute agreement among House and Senate leadership on the broader housing measure. According to reporting by Cointelegraph, the House passage followed a prior Senate vote, with the CBDC language carried through negotiations and preserved from earlier versions.

Senate Banking Committee Chairman Tim Scott praised the outcome, framing it as a victory for families while emphasizing that Congress had delivered on a long-standing policy objective. The inclusion of the CBDC prohibition has been repeatedly pursued by Republican lawmakers for years, including through earlier legislation that did not advance to enactment.

One notable precursor was a CBDC-focused proposal from Representative Tom Emmer, the Anti-CBDC Surveillance State Act, introduced in June 2025 and passed by the House in July. Despite clearing the House, it did not move forward in the Senate. The housing bill therefore represents a different legislative route—embedding the CBDC restriction within a must-pass or priority bill—suggesting lawmakers may be using vehicle legislation to achieve digital-asset policy goals when standalone bills stall.

Broader compliance and regulatory implications

For regulated entities, the immediate compliance relevance is the signal the statute sends about congressional boundaries around central-bank digital money. Although the restriction targets the Federal Reserve directly, its presence can affect how other regulators interpret the policy environment in which they supervise payments, tokenized assets, and stablecoins.

Institutions also face a multi-jurisdiction landscape. While the U.S. action is domestic, firms with global operations must continue planning for foreign frameworks such as the EU’s Markets in Crypto-Assets (MiCA) regime. Differences in approach—particularly around token classification, issuer obligations, and stablecoin rules—mean the U.S. CBDC ban may not harmonize with European requirements for reserve management, authorization, and ongoing disclosures.

On enforcement and risk, the bill does not replace existing AML/KYC expectations or consumer-protection rules for crypto and financial intermediaries. Rather, it modifies one dimension of the policy map: the ability of the Federal Reserve to issue or create a CBDC-like digital asset. Compliance programs must therefore remain focused on counterparty due diligence, transaction monitoring, sanctions screening, and recordkeeping, while also tracking whether any new regulatory guidance emerges to clarify how “substantially similar” assets will be treated.

What to watch next

The measure’s next milestone is presidential approval. After the bill becomes law, market participants and supervised entities will likely focus on interpretive clarity around the “substantially similar” standard and the stablecoin carve-out descriptors, as well as any downstream guidance from regulators. The longer-term uncertainty is how these constraints interact with future legislative efforts in U.S. crypto market structure—areas where Congress is still debating rules for trading, custody, and market conduct.

The U.S. House of Representatives passed the 21st Century ROAD to Housing Act on Tuesday, sending the bill to President Donald Trump for final approval.

Summary

- Congress passed a housing bill that blocks the Federal Reserve from issuing a CBDC until 2030.

- The measure now heads to President Donald Trump after strong bipartisan votes in both chambers.

- The CBDC clause follows Trump’s policy against a digital dollar and supports private stablecoins.

The measure passed the House by a 358-32 vote after the Senate cleared it 85-5 one day earlier.

The bill focuses on housing affordability, supply and access to homeownership. It seeks to cut red tape, speed up construction, limit large investor control in parts of the housing market and update some federal housing programs.

“Today, Congress delivered a major win for families working toward the American Dream,” said Senate Banking Committee Chairman Tim Scott. “The 21st Century ROAD to Housing Act will help more Americans put down roots, build a better future, and find not just a house, but a home, and I look forward to President Trump signing it into law.”

CBDC ban moves with the package

The housing bill also includes language blocking the Federal Reserve from issuing or creating a central bank digital currency. The restriction would run until Dec. 31, 2030, unless Congress acts again before that date.

The clause bars the Federal Reserve Board or any Federal Reserve bank from issuing a CBDC or a digital asset that is substantially similar to one. It also applies to issuance through a financial institution or other intermediary.

The bill defines a CBDC as a dollar-denominated digital asset that counts as U.S. currency, is a direct liability of the Federal Reserve System and is widely available to the public. The language includes an exception for dollar-denominated digital currency that is open, permissionless and private.

Trump policy backs CBDC freeze

The CBDC clause fits the Trump administration’s position on a federal digital dollar. President Trump signed an executive order in January 2025 that barred federal agencies from taking steps to establish, issue or promote a CBDC unless required by law.

As previously reported by crypto.news, Treasury Secretary Scott Bessent said a U.S. CBDC was “off the table” under Trump. Bessent also urged lawmakers to move ahead with the CLARITY Act as part of a broader push to bring digital asset activity into the United States.

In a recent update, crypto.news covered the Senate vote that moved the housing bill and CBDC ban toward the House. That report noted that the Fed had not launched a digital dollar program and that the idea had remained closer to research than rollout.

Private stablecoins remain outside the freeze

The CBDC language does not ban private stablecoins. The bill’s carveout keeps the restriction focused on Federal Reserve-issued money, not privately issued dollar tokens that meet the bill’s conditions.

Previously, crypto.news reported that the housing deal included a stablecoin carveout while blocking a Fed digital dollar until 2030. That language matters as Congress continues to work on separate digital asset rules covering stablecoins and market structure.

The U.S. stance also differs from other markets. The European Central Bank has continued work on a digital euro, while China has developed the digital yuan. The United States is now moving toward a legal pause on a retail Fed digital dollar through the end of 2030.

If Trump signs the bill, the CBDC restriction will move from executive policy into federal law. The broader package will also place housing reform and digital dollar limits inside the same statute, linking two policy debates that Congress handled through one bill.

Green’s Greater Manchester Mayor candidate makes Metrolink extension promise

Tata Motors shares jump 5% on strong growth guidance. What are Nomura, other brokerages saying?

DAX 40: consolidation amid technology sell-off

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment3 days ago

Entertainment3 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech2 days ago

Tech2 days agoMicrosoft accidentally kills epic Outlook email threads

-

Business3 days ago

Business3 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Sports13 hours ago

Sports13 hours agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Crypto World4 hours ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Politics6 days ago

Politics6 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Business7 hours ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business4 days ago

Business4 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Politics4 days ago

Politics4 days agoAndy Burnham and the meaning of Makerfield

-

Tech6 days ago

Tech6 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World4 days ago

Crypto World4 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World4 days ago

Crypto World4 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World4 days ago

Crypto World4 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

NewsBeat5 days ago

NewsBeat5 days agoKeir Starmer Allies Question His Chances For No 10

-

Tech2 days ago

Tech2 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Business5 days ago

Business5 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

-

Sports5 days ago

Sports5 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

-

Tech3 days ago

Tech3 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Entertainment4 days ago

Entertainment4 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

You must be logged in to post a comment Login