Crypto World

Inside the Strategic Bitcoin Reserve: promise vs reality

President Trump signed the executive order establishing the Strategic Bitcoin Reserve on March 6, 2025.

Summary

- Trump’s Strategic Bitcoin Reserve exists as a no-sell directive, not an active acquisition program yet.

- The U.S. government reportedly holds about 328,372 BTC, but custody and legal questions remain unresolved.

- Lummis’s BITCOIN Act targets 1 million BTC, while ARMA offers a more conservative legislative path.

- The next announcement may formalize custody and legal frameworks, not authorize direct Bitcoin purchases.

Fourteen months later, in May 2026, White House digital asset advisor Patrick Witt told the audience at Consensus Miami that a “major announcement” on the reserve is coming “in the next few weeks.” Witt characterized the underlying legal and custody work as a “breakthrough” and disclosed for the first time the government holds approximately 328,372 BTC worth roughly $25.4 billion.

Meanwhile, the gap between what has been promised and what has been operationally delivered is the structural story of the SBR. Trump’s order halted sales of seized Bitcoin and mandated centralized custody. The administration has conducted an audit revealing cold wallets stored in desk drawers across federal agencies and a $60+ million exploit of US Marshals Service holdings in late 2025.

Treasury Secretary Scott Bessent confirmed in August 2025 the US “won’t be buying” additional Bitcoin, contradicting the “Bitcoin superpower” rhetoric of former White House crypto advisor Bo Hines, who stepped down that same month amid SBR scrutiny. Senator Cynthia Lummis’s BITCOIN Act would mandate purchases of 1 million BTC over five years funded by gold revaluation. The bipartisan ARMA bill introduced May 2026 (Begich-R/Golden-D) dropped the specific 1M target and added a 20-year lockup.

Senate Banking Committee markup of competing bills is expected by May 31. The honest read is the SBR exists as legal directive but does not yet exist as operational acquisition program. The next several weeks will determine whether it becomes the latter or stays primarily the former. This is what the documented record shows, what the structural questions are, and what the imminent announcement might actually contain.

What the executive order actually established

The executive order signed on March 6, 2025 deserves careful unpacking because the gap between what it formally established and what most coverage characterized it as creating is structurally significant.

The order created two separate entities. The Strategic Bitcoin Reserve (SBR) is the entity holding Bitcoin specifically. The US Digital Asset Stockpile is a separate entity holding non-Bitcoin cryptocurrencies (Ethereum, XRP, Solana, Cardano, and other forfeited digital assets). The two entities have different operational mandates: the SBR cannot sell its Bitcoin holdings under the order’s terms, while the Digital Asset Stockpile lets the Treasury Department liquidate non-Bitcoin assets at its discretion.

The funding mechanism is the most consequential structural element. The reserve is “capitalized with all BTC held by the Department of the Treasury that was finally forfeited as part of criminal or civil asset forfeiture proceedings or in satisfaction of any civil money penalty imposed by any executive department or agency.” In plain English: the reserve consists of Bitcoin the government already had from law enforcement seizures. The executive order did not authorize and did not fund any active acquisition of additional Bitcoin.

The order does direct the Secretaries of Treasury and Commerce to “develop strategies for acquiring additional Government BTC, provided that such strategies are budget-neutral and do not impose incremental costs on United States taxpayers.” This is permissive language inviting policy development, not mandatory language requiring action. The Treasury and Commerce departments were tasked with studying whether budget-neutral acquisition mechanisms exist, not with implementing them.

The audit mandate is what produced the first concrete operational deliverable. The order required each federal agency to “provide the Secretary of the Treasury and the President’s Working Group on Digital Asset Markets with a full accounting of all Bitcoin and other digital assets in the agency’s possession” within 30 days. The audit deadline was April 5, 2025. The audit was completed but the detailed findings were not made public until the White House report released on July 30, 2025.

The structural questions the executive order left unresolved are the ones now being addressed through the May 2026 Witt announcement and the pending congressional legislation. Which specific legal authorities permit federal agencies to hold Bitcoin long-term rather than liquidating it through standard forfeiture procedures? Can Congress reclaim the assets through appropriations or other legislative action? What custody framework will protect the holdings from operational risks? How is “budget-neutral acquisition” actually defined and implemented?

These questions are not trivial. The executive order can set a policy direction, but it cannot by itself create the legal and operational infrastructure required to make a strategic Bitcoin reserve function comparably to other strategic reserves like the Strategic Petroleum Reserve or the gold holdings at Fort Knox. The infrastructure work is what Witt was referring to when he characterized the May 2026 announcement as a “breakthrough.”

What the executive order did establish, clearly and definitively, is the federal government’s policy of not selling its Bitcoin holdings. The Treasury Secretary’s August 2025 confirmation that the US “won’t be buying” additional Bitcoin reinforced the operational reality: the SBR is a directive to hold, not a directive to accumulate. The “digital Fort Knox” rhetoric from White House crypto czar David Sacks describes the aspirational endpoint. The current operational state is more accurately characterized as “do not sell what we already have.”

What the audit actually revealed

The audit conducted between March and July 2025 produced findings more revealing than the formal report acknowledged, and the documented operational realities deserve attention because they shape what the imminent SBR announcement can realistically deliver.

The headline number is the government holds approximately 328,372 BTC worth roughly $25.4 billion as of February 2026, according to Witt’s Consensus Miami disclosure on May 6, 2026. This is the first time the White House has confirmed a specific holdings figure since the executive order was signed. Previous third-party estimates from Arkham Intelligence and Bitcoin Treasuries had ranged from 198,012 to 328,000 BTC, with the variance reflecting confusion between officially forfeited assets and merely seized assets that might be returned to victims.

The composition of the holdings comes primarily from three major law enforcement actions. The Silk Road marketplace takedown produced the original anchor of government Bitcoin holdings starting in 2013. The Bitfinex hack recovery in 2022 added 94,636 BTC seized by the DOJ. Various smaller criminal forfeitures over the past decade contributed the remaining holdings. The composition has implications for the legal status of individual coins: some are fully forfeited (legally owned by the US government) while others are technically seized but still subject to potential restitution to crime victims.

The operational state of the holdings was more chaotic than the public might have expected. Witt acknowledged at Consensus the audit process revealed agency-level custody practices were “messy” in his characterization. “We’ve heard stories and confirmed some of them of cold wallets that were being stored in drawers of desks in various agencies,” Witt said publicly. This is not a routine custody finding. It indicates for years, federal agencies were holding crypto assets worth potentially billions of dollars without the kind of institutional custody framework required for any other government-held strategic asset.

The January 2026 US Marshals Service incident reinforced the custody concerns. Bloomberg reported the Marshals Service was investigating a possible hack of government digital-asset accounts following allegations from on-chain investigator ZachXBT that a hacker had stolen more than $60 million from government seizure wallets in late 2025. The incident is part of the public record now and is one of the specific operational events Witt cited as motivation for centralized custody architecture.

David Sacks revealed in early 2025 the government had previously held approximately 400,000 BTC through cumulative civil and criminal asset forfeitures over the past decade. The current holdings (approximately 328,372 BTC) reflect both ongoing seizures and the substantial liquidations conducted under the prior administration. Sacks characterized the prior administration’s auctions as “fire sale” liquidations wasting significant taxpayer value. At current prices, the difference between holding all 400,000 BTC and the current 328,372 BTC represents approximately $5.5 billion in foregone value if the auctioned coins had been retained. The political framing of “fire sale” liquidations has been a recurring theme in administration rhetoric about why the no-sell policy is fiscally important.

The audit findings establish two structural realities. First, the government’s actual Bitcoin holdings are substantial (over $25 billion at current prices) but smaller than they would have been absent prior auctions. Second, the operational infrastructure required to hold these assets safely has been inadequate, and the centralization and custody work the Witt team has been conducting addresses real operational gaps rather than just political theater. The combination matters for evaluating what the imminent announcement can credibly deliver.

The Bo Hines pivot and what it revealed

The transition from Bo Hines to Patrick Witt as the operational lead on the SBR happened in August 2025 and tells a structural story about how the SBR rhetoric evolved into operational reality. The story deserves attention because it clarifies what the administration’s actual capabilities and intentions are.

Bo Hines was the executive director of the President’s Council of Advisors for Digital Assets through the first half of 2025. He was a central voice in the early SBR rhetoric, characterizing the United States as needing to become “the Bitcoin superpower of the world” and describing a “space race” for Bitcoin accumulation. In April 2025 remarks, Hines outlined acquisition methods focused on rapid scaling and budget-neutral mechanisms, framing the SBR as an active acquisition program rather than just a holding directive.

The Hines rhetoric clashed with the executive order’s actual provisions. The order did not authorize Bitcoin purchases. It directed Treasury and Commerce to study budget-neutral mechanisms. The gap between Hines’s “Bitcoin superpower” framing and the executive order’s “explore strategies” language created public expectations the administration could not deliver on without congressional action.

Treasury Secretary Scott Bessent’s August 14, 2025 Fox Business interview was the moment the gap became unsustainable. When asked about the Bitcoin reserve, Bessent said directly: “We’re not going to be buying that [bitcoin] but are going to use confiscated assets and continue to build that up, we’re going to stop selling that.” He estimated the reserve was “somewhere between $15 and $20 billion” at the time. This was a direct contradiction of the Hines framing. The Treasury Secretary, the senior administration official responsible for the actual financial operations, was clarifying the US would not be actively buying Bitcoin.

Bo Hines stepped down from his White House role within days of the Bessent comments, in August 2025. The stated reason was the standard “pursue other opportunities” framing used in such departures. The actual context was the SBR scrutiny intensifying around the gap between the rhetoric and the operational reality. Hines subsequently joined Tether’s US operations and eventually became CEO of USAT (the Anchorage Digital-issued GENIUS-compliant stablecoin from Tether) when it launched in January 2026.

Patrick Witt took over as executive director of the President’s Council of Advisors for Digital Assets following Hines’s departure. The transition shifted the SBR’s operational character significantly. Witt’s public framing has been substantially more measured than Hines’s. Where Hines stressed acquisition and scale, Witt stresses “getting our house in order” through custody centralization, legal framework development, and operational infrastructure. The shift reflects a more accurate accounting of what the executive order actually enabled and what congressional action would be required to expand.

Witt’s deputy Harry John conducted the legal framework development producing the May 2026 “breakthrough.” The framework addresses specific legal questions the executive order did not resolve: which authorities permit federal agencies to hold Bitcoin long-term, for how long, and whether Congress could reclaim the assets through legislative action. The legal work is the kind of detailed administrative state work not producing headlines but determining whether the SBR can function as a credible strategic reserve over time.

The structural lesson from the Hines-Witt transition is the SBR moved from rhetoric to operational reality through personnel change. The “Bitcoin superpower” framing required legislative action not forthcoming. The more measured “centralize custody, develop legal framework, prepare for future congressional action” framing reflects what the executive branch can actually deliver. The May 2026 “breakthrough” announcement will likely formalize this more measured framing rather than restore the maximalist accumulation rhetoric.

For market observers, the structural implication is the SBR’s near-term impact is likely smaller than the early Hines rhetoric suggested but more durable than the maximalist framing would have produced. A formal centralized custody architecture for 328,372 BTC, combined with a legally robust no-sell policy and a clear pathway for future congressional acquisition authorization, is a real structural shift in the US government’s relationship with Bitcoin. It just runs on a slower timeline than the Bitcoin maximalist community had hoped.

The legislative pathway: BITCOIN Act and ARMA

The executive order can establish policy direction but cannot create permanent legal infrastructure or fund active acquisition. Both functions require congressional action. The two competing bills currently in play deserve careful examination because they will determine whether the SBR becomes an active acquisition program or stays primarily a passive holding directive.

Senator Cynthia Lummis (R-WY) reintroduced the BITCOIN Act (S.954) in March 2025, formalizing legislation she had introduced in the prior Congress. The bill’s full title is the Boosting Innovation, Technology, and Competitiveness through Optimized Investment Nationwide Act. The core provisions are substantive. The Treasury would be required to buy one million Bitcoin over a five-year period and hold the assets in trust for the United States. At March 2025 prices, the one million BTC target represented approximately $80 billion in acquisition cost. At current prices, the cost would be roughly $80 billion (Bitcoin price has fluctuated but the order of magnitude is similar).

The funding mechanism in the BITCOIN Act is the structural innovation. The bill proposes funding the purchases through the net earnings of the Federal Reserve, which historically transfers surplus revenues to the Treasury, and through Treasury issuance of new gold certificates reflecting current market prices for the Federal Reserve’s gold holdings. The gold revaluation mechanism is technically interesting. The Federal Reserve’s gold holdings are currently valued on Treasury books at the statutory rate of $42.22 per ounce, which dramatically understates current market value (approximately $3,000+ per ounce). Revaluing the gold holdings would produce a paper accounting gain the Treasury could theoretically use to fund Bitcoin purchases without new appropriations.

The 20-year holding period is the second structural provision. All Bitcoin acquired by the United States and placed into the Strategic Bitcoin Reserve must be held for at least 20 years under the bill’s terms. After the holding period expires and upon Treasury recommendation, up to 10 percent of the holdings could be sold to reduce the national debt in any two-year period. The 20-year lockup turns the SBR from a flexible reserve asset into a long-term strategic position similar to the gold reserves.

The American Reserve Modernization Act of 2026 (ARMA) was introduced in May 2026 by Representative Nick Begich (R-AK) and Representative Jared Golden (D-ME) as a bipartisan alternative to the Lummis bill. ARMA is structurally similar to the BITCOIN Act in core mandates (Strategic Bitcoin Reserve, Digital Asset Stockpile, 20-year lockup, budget-neutral acquisition) but has important differences in scope and approach.

The most significant ARMA difference is the bill dropped the specific 1 million BTC target. Rather than mandating purchase volumes, ARMA directs Treasury and Commerce to “study whether additional acquisitions could be carried out through budget-neutral mechanisms” without specifying outcomes. This is a substantially more conservative legislative posture that may make the bill more politically viable but provides less certainty about actual acquisition levels.

ARMA also strengthens custody standards explicitly. The bill includes specific provisions about secure storage requirements, custody protocols, and operational safeguards meant to prevent incidents like the US Marshals Service exploit. The custody focus reflects the operational reality the Witt audit revealed and aligns the legislative work with the operational concerns the administration has been addressing.

The Senate Banking Committee markup of the BITCOIN Act is expected by May 31, 2026, per Witt’s Consensus statements and other administration signals. The markup is the first substantive legislative step. If the bill passes committee with reasonable bipartisan support, the path to floor consideration becomes plausible. If the bill stalls in committee, the legislative pathway becomes more difficult and the executive branch’s incremental approach (centralized custody, no-sell directive, audited holdings) becomes the de facto SBR for the foreseeable future.

The political dynamics around the legislation are complicated. The BITCOIN Act has primarily Republican backing despite the strong fiscal conservative argument for the bill (acquisition through gold revaluation rather than new debt issuance, long-term store of value, no taxpayer impact). Democrats have generally been skeptical of the executive order and the broader crypto-friendly policy direction, though the ARMA bill’s bipartisan structure (Golden as Democratic co-sponsor) suggests some Democratic support is achievable for a more modest version of the SBR concept.

For market observers, the key question is whether legislative action produces the active acquisition program the Bitcoin maximalist community has hoped for, or whether the legislative window closes with the SBR remaining primarily a passive holding directive. The May 31 markup and the subsequent legislative trajectory will likely answer this question over the next few months.

What the “breakthrough” announcement might actually contain

Witt’s May 2026 “breakthrough” characterization at Consensus Miami signals an imminent announcement, but the specific content the announcement will contain has not been publicly confirmed. Based on the documented public statements and the structural work the administration has been conducting, several likely components can be inferred.

The most likely component is formalization of centralized custody architecture for the 328,372 BTC currently held across various federal agencies. The audit revealed cold wallets in desk drawers and the Marshals Service exploit showed the operational risks of decentralized custody. A formal architecture would consolidate the holdings into purpose-built institutional custody (likely involving regulated custodians like BitGo, Anchorage, or Coinbase Custody) with multi-signature controls, geographic distribution of custody locations, and standardized operational procedures.

The legal framework Harry John’s team developed is the second likely component. The framework addresses the executive branch’s authority to hold the Bitcoin long-term without congressional appropriations, the legal status of seized versus forfeited assets, the procedural requirements for transferring assets between agencies, and the protections against legislative claw-back of the holdings. The framework’s specific provisions will be technically detailed but politically significant, as they determine what the executive branch can do without congressional action.

The no-sell policy formalization is the third likely component. The executive order set the policy direction, but the operational implementation requires specific regulatory and procedural changes at the agency level. The announcement may include formal regulations or memoranda specifying how individual agencies must handle Bitcoin holdings, the requirements for transferring assets to centralized SBR custody, and the prohibitions on auction or sale without specific Treasury authorization.

The integration with congressional legislation is the fourth likely component. The announcement will probably express administration support for either the BITCOIN Act or the ARMA bill (or both, with the ARMA bill positioned as a fallback if the more ambitious BITCOIN Act stalls). The timing of the announcement around the May 31 Senate Banking Committee markup is probably not coincidental. The administration may be coordinating with congressional sponsors to maximize legislative momentum.

What the announcement is unlikely to contain is authorization for active Bitcoin purchases. The executive branch does not have the legal authority to use appropriated funds for Bitcoin acquisition without congressional action. Treasury Secretary Bessent’s August 2025 confirmation the US “won’t be buying” is still the operational reality until Congress acts. The announcement will likely stress what the executive branch has done (custody centralization, legal framework, no-sell directive) and what congressional action could enable in the future.

The market response to the announcement will likely depend on whether it contains specific operational milestones or just process commitments. Specific operational milestones (custody contracts signed, holdings transferred, audit results published) would be substantively meaningful. Process commitments (committee markups expected, frameworks under development, announcements coming) would be incremental. The “breakthrough” characterization suggests the former, but the actual content remains to be seen.

For Bitcoin price specifically, the structural impact of the formalized no-sell policy is positive but limited. Removing seized-coin auctions as a recurring supply event (the prior administration sold approximately 70,000 BTC across multiple auctions) eliminates one form of structural selling pressure. But the no-sell policy was already operational in practice since the executive order, so formalizing it has limited additional impact. The more significant price catalyst would be congressional authorization of active acquisition, which the announcement will not contain.

For the broader policy trajectory, the announcement’s most significant content may be establishing a clear path from the current passive holding state to a potential future active acquisition program. If the announcement positions the executive branch as having completed its custody and legal foundation work, it puts the responsibility for the next stage squarely on Congress. The political dynamics of the Senate Banking Committee markup and subsequent legislative work become the determinative variables.

The structural questions still unresolved

Several substantive questions about the SBR remain unresolved regardless of what the imminent announcement contains, and the questions deserve attention because they shape the long-term viability of the reserve concept.

The first unresolved question is what “budget-neutral acquisition” actually means in practice. The executive order, the BITCOIN Act, and ARMA all invoke budget-neutral mechanisms, but the specific operational definition varies. Gold revaluation (the BITCOIN Act mechanism) is technically budget-neutral in accounting terms but creates real economic effects. Federal Reserve net earnings (also in the BITCOIN Act) would redirect funds otherwise flowing to general Treasury revenue. Other proposed mechanisms (tariff revenue allocation, asset sales of other federal holdings) have different implications. The definitional question matters because different definitions enable different acquisition scales.

The second unresolved question is whether sovereign Bitcoin holdings create market manipulation concerns. If the United States accumulates 1 million BTC (the BITCOIN Act target), it would hold approximately 5 percent of the total Bitcoin supply. The concentrated holdings could create market manipulation incentives where US policy decisions about Bitcoin (custody, accounting treatment, regulatory framework) affect the asset’s price in ways benefiting US holdings. This is the same concern applying to government gold holdings and other strategic reserves, but the relatively smaller size of the Bitcoin market makes the concentration effects more pronounced.

The third unresolved question is how other sovereign nations will respond to US accumulation. If the United States becomes the largest sovereign Bitcoin holder, other major economies will likely consider similar reserves. El Salvador has held Bitcoin reserves since 2021. The UAE through Abu Dhabi has been accumulating crypto exposure through various channels. China has historically been opposed to crypto but has shown signs of softening on Bitcoin specifically through Hong Kong-based vehicles. The “Bitcoin space race” Hines invoked may actually be a real geopolitical dynamic if US accumulation prompts competitive sovereign accumulation by other major economies.

The fourth unresolved question is the relationship between the SBR and the broader US dollar position. Treasury Secretary Bessent has framed Bitcoin as complementary to gold as a strategic asset rather than as competition for the dollar. Larry Fink and other major financial figures have argued tokenization broadly strengthens dollar dominance rather than weakening it. But Bitcoin accumulation does represent a partial diversification away from pure dollar-denominated reserve assets. The structural implications for dollar hegemony are debated and depend on accumulation scale, parallel actions by other reserve holders, and the broader evolution of the international monetary system.

The fifth unresolved question is the political durability of the SBR across administrations. The executive order can be reversed by a future administration. The no-sell policy could be reversed. The custody arrangements could be unwound. Codification through congressional legislation (the BITCOIN Act or ARMA) would provide more political durability, but even legislation can be amended or repealed. The structural question is whether the SBR can develop the kind of bipartisan support making it durable across political transitions, or whether it stays a partisan policy future administrations could dismantle.

These questions do not have clean answers in 2026. The next several years of operational implementation, legislative action, and broader policy evolution will determine how the questions get resolved. The Witt announcement will address some of them (custody, legal framework) but cannot resolve others (international response, political durability, dollar implications). The questions are worth keeping in mind as the SBR story develops, regardless of how the imminent announcement is received.

What the SBR means for Bitcoin specifically

The market implications of the SBR for Bitcoin price, adoption, and structural positioning deserve direct engagement because they shape how investors and observers should interpret the imminent announcement and the broader policy trajectory.

The supply impact is the most concrete dimension. The no-sell policy removes approximately 328,372 BTC from potential auction supply, representing approximately 1.6 percent of total Bitcoin supply (which is approximately 19.9 million coins as of May 2026). The supply removal is not new to the market (the executive order has been in effect for 14 months and prior administration auctions were already disclosed in advance), but the formal policy codification removes the residual uncertainty about whether seized coins might be auctioned in the future.

If the BITCOIN Act passes and the 1 million BTC acquisition target is implemented over five years, the cumulative supply impact would be much larger. The 1 million BTC target represents approximately 5 percent of total supply. Acquiring this amount over five years would require approximately 200,000 BTC per year of accumulation, which represents substantial structural demand. For comparison, Bitcoin spot ETFs accumulated approximately 1.1 million BTC across their first 18 months of trading, so US government acquisition at the BITCOIN Act target would be roughly equivalent in scale to the ETF accumulation having driven much of Bitcoin’s institutional adoption.

The demand catalyst would be significant but not transformative for Bitcoin price. At current trading volumes of approximately $50-80 billion per day in spot Bitcoin markets, government acquisition of 200,000 BTC per year (averaging perhaps $40-50 billion in annual value) would represent meaningful but not overwhelming demand. The price impact depends substantially on how the acquisition is structured (announced auctions versus quiet accumulation, OTC versus exchange-based purchases) and how other market participants respond to the government activity.

The structural signaling effect may matter more than the direct supply or demand impact. US government accumulation of Bitcoin as a strategic reserve signals to other sovereign actors, institutional investors, and the broader market that Bitcoin has achieved a level of legitimacy comparable to other strategic assets. The signaling effect could catalyze additional institutional adoption beyond what the direct US government purchases would produce.

The regulatory and policy implications extend beyond just the SBR. The administration’s broader crypto-friendly direction (the GENIUS Act, the Bitcoin reserve, the CLARITY Act work, the SEC enforcement shift under Chair Atkins) creates a policy environment supporting Bitcoin adoption across multiple channels simultaneously. The SBR is one component of this broader policy framework, not a standalone driver.

The risks to Bitcoin from SBR developments deserve equal attention. If the BITCOIN Act stalls in Congress and the legislative pathway closes, the SBR stays primarily a passive holding directive without the active acquisition dynamics. If a future administration reverses the executive order, the no-sell policy and centralized custody could be unwound. If the budget-neutral acquisition mechanisms (gold revaluation, Federal Reserve net earnings) face legal or political challenges, the funding pathway for active acquisition becomes uncertain.

The honest read is the SBR provides Bitcoin with structural support not existing before the March 2025 executive order, but the scale of the support is more modest than the maximalist rhetoric suggested. The imminent Witt announcement will likely formalize the existing support without dramatically expanding it. Significant additional support depends on congressional action having not yet happened and may or may not happen in the current legislative window.

For Bitcoin investors specifically, the practical implication is the SBR is a positive structural development should be factored into long-term thesis but should not be treated as a near-term price catalyst with specific magnitude. The structural story develops over years through operational implementation and legislative action rather than through any single announcement.

The bottom line

The Strategic Bitcoin Reserve as it actually exists in May 2026 is a legal directive setting a government policy of not selling approximately 328,372 BTC currently held across various federal agencies, with a centralized custody framework under active development and a legal framework recently completed addressing the questions left unresolved by the original executive order.

The Strategic Bitcoin Reserve as it has been rhetorically characterized (the “digital Fort Knox,” the “Bitcoin superpower” framing, the active accumulation program targeting 1 million BTC) is an aspirational endpoint requiring congressional action not yet happened.

The gap between these two characterizations is the structural story of the SBR over the past 14 months. The Bo Hines maximalist framing collided with the executive order’s actual provisions and the Treasury Secretary’s operational reality. The Patrick Witt measured framing reflects what the executive branch can actually deliver. The imminent announcement will formalize what Witt and his team have built rather than restore the more ambitious Hines vision.

The documented facts are clear. Executive order signed March 6, 2025. Audit completed by April 2025, findings detailed in the July 30, 2025 White House report. Approximately 328,372 BTC currently held worth roughly $25.4 billion. Cold wallets stored in desk drawers across federal agencies. A $60+ million exploit of US Marshals Service holdings in late 2025. Treasury Secretary Bessent’s August 2025 confirmation of no purchases. Bo Hines departure in August 2025. Patrick Witt’s Consensus Miami breakthrough announcement May 6, 2026. Senate Banking Committee markup of the BITCOIN Act expected by May 31, 2026. The bipartisan ARMA bill introduced May 2026 as alternative to the Lummis BITCOIN Act.

The structural questions stay open. Will Congress codify the SBR through legislation? Will budget-neutral acquisition mechanisms (gold revaluation, Federal Reserve net earnings) be authorized? Will future administrations keep or reverse the policy? How will other sovereign actors respond? What does sovereign Bitcoin accumulation mean for the broader dollar position?

For Bitcoin holders, the practical implication is the SBR provides modest structural support that should be factored into long-term thesis without being treated as a near-term price catalyst. The supply removal (328,372 BTC effectively off the market under the no-sell policy) is real but not transformative. The potential demand catalyst (1 million BTC acquisition if BITCOIN Act passes) would be significant but depends on legislative outcomes not yet materialized.

For policy observers, the SBR is one of the clearest examples of how crypto policy actually evolves under administrative implementation versus political rhetoric. The executive order set direction. The audit revealed operational realities. The personnel transitions reflected mismatch between rhetoric and capability. The measured operational approach Witt and his team have taken is producing real but incremental progress. The legislative work runs in parallel with uncertain outcomes.

For market observers, the imminent Witt announcement is unlikely to produce dramatic price movement in either direction. It will probably formalize the centralized custody architecture, the legal framework, and the no-sell directive. It will probably express administration support for congressional legislation. It will probably stress the operational progress over the past 14 months. It will probably not contain authorization for active acquisition because that requires congressional action.

The honest assessment is the SBR is real but smaller than promised, operational but incomplete, structurally important but not yet transformative. The next several months will determine whether congressional action expands it into the active accumulation program the maximalist rhetoric described, or whether it stays primarily a passive holding directive with formal custody and legal infrastructure.

For now, what is established is the United States government holds approximately 328,372 BTC worth roughly $25.4 billion under a no-sell policy with developing centralized custody and a recently completed legal framework. The reserve exists. The promise of active accumulation has not yet been delivered. The reality of operational implementation keeps unfolding.

The Witt announcement will provide the next data point. The Senate Banking Committee markup will provide the next legislative signal. The eventual outcome will be determined over the coming months and years through specific operational milestones and political developments rather than through any single defining event.

The Strategic Bitcoin Reserve is real. It is also incomplete. Both can be true simultaneously, and the honest reading of the documented record requires holding both characterizations at once.

What happens next is being decided now, in legal memos prepared by Harry John’s team, in Senate Banking Committee hearings yet to take place, in operational decisions about custody contracts not yet signed, and in the broader political dynamics determining whether US Bitcoin policy stays its current course or evolves further. The story is consequential, ongoing, and worth following carefully through the specific structural milestones rather than through the rhetorical framing on either side.

The promise versus reality gap will narrow over time. Which side it narrows toward is the question the next several months will answer.

This article is for informational purposes and does not constitute financial or investment advice. The Strategic Bitcoin Reserve’s policy framework, congressional legislation, and operational implementation continue to evolve; the figures and milestones described reflect reporting available as of late May 2026. Always do your own research.

Apyx's apxUSD, a dividend-backed stablecoin collateralized largely by the preferred shares of bitcoin-treasury companies, broke its $1 peg this week, falling to about 92 cents as Strategy's STRC preferred stock dropped below par and bitcoin extended a steep selloff. The stablecoin slipped to… Read the full story at The Defiant

Bitcoin briefly dropped below the critical $60,000 mark on Binance on June 5, marking the pioneer crypto’s first break beneath that level since October 2024.

The move comes amid a broader risk-off selloff across financial markets, as investors react to strong U.S. employment data, persistent fund outflows, and growing concerns over liquidity conditions.

Bitcoin Loses Key Support as Market Pressure Intensifies

Bitcoin fell to a low below $60,000 during Friday trading, breaking a psychological support level that had largely held throughout 2026.

The crash saw BTC bottom out at $59,750 on Coinbase and $59,799 on Binance against the US dollar (USD). Against USDT, the pioneer crypto bottomed out at $59,786 on Binance, as of this writing.

The drop represents the first confirmed move under $60,000 since October 10, 2024, when BTC bottomed near $58,863 before recovering.

The decline pushed Bitcoin into a key technical zone that many traders have been watching for months, renewing debate over whether the market is experiencing a temporary sentiment shock or a deeper correction.

The latest decline follows a difficult stretch for digital assets. Bitcoin has lost more than 17% over the past week, while broader crypto markets have also faced heavy selling pressure.

Market participants pointed to a combination of macroeconomic and crypto-specific factors behind the move.

A stronger-than-expected U.S. jobs report reduced expectations for near-term interest-rate cuts, prompting investors to move away from risk assets.

Billions Exit Crypto Investment Products

Recent data from CoinShares highlighted the scale of the market retreat. The asset manager reported that digital asset investment products experienced approximately $5.8 billion in outflows over the past four weeks.

According to CoinShares, the withdrawals were driven by geopolitical uncertainty, changing interest-rate expectations, and capital rotating toward artificial intelligence-related investments.

“Sentiment has taken a clear turn for the worse over the past month…the asset class remains close to flat for the year. This is a sentiment shock,” CoinShares said, while emphasizing that current conditions appear to reflect a sentiment-driven shock rather than a structural breakdown in crypto fundamentals.

Follow us on X to get the latest news as it happens

Investors Watch Whether $60,000 Becomes Resistance

Bitcoin’s fall below $60,000 is particularly significant because the level has acted as a major psychological threshold throughout the current market cycle.

Previous tests of the area in February 2026 held above support, helping stabilize prices.

Analysts are now monitoring whether Bitcoin can reclaim the level quickly or whether it transforms into a resistance zone heading into the weekend.

What’s Next for Bitcoin?

Attention is likely to remain focused on macroeconomic data, Federal Reserve expectations, and institutional fund flows.

Investors will also watch whether digital asset investment products continue to experience outflows or begin attracting fresh capital.

Bitcoin’s break below $60,000 represents one of the market’s most important developments of 2026, placing a critical support zone back in focus as traders assess the next phase of the cycle.

The post Bitcoin Falls Below $60,000 on Binance for First Time Since 2024 appeared first on BeInCrypto.

Bitcoin (BTC) extended losses after Friday’s Wall Street open as traders prepared for a retest of $60,000.

Key points:

- Bitcoin begins a battle to protect $60,000 support as sell-side pressure refuses to cool.

- Analysis sees early signals that “seller exhaustion” is here.

- US nonfarm payrolls data produce a stronger-than-expected picture of US labor market conditions.

Bitcoin battles for $60,000 support

Data from TradingView showed daily BTC price downside approaching 5% as sellers stayed in the driving seat.

BTC/USD one-hour chart. Source: Cointelegraph/TradingView

“Rapidly approaching its February low at $60K. Now in its 6th red daily candle and down more than the entire April/May rally,” trader Daan Crypto Trades noted in a reaction on X.

“Really was a case of stairs up elevator down which is something we often see in these larger bear trends. Eyes on that $60K area for now.”

BTC/USDT perpetual contract one-day chart. Source: Daan Crypto Trades/X

Commentator Expitump referenced the Coinbase Premium, the difference in price between Coinbase’s BTC/USD and Binance’s BTC/USDT pairs and a key yardstick for US demand.

“Price is still under controlled selling, but seeing funding getting almost into negative and coinbase discount decreasing,” they summarized in their latest market coverage.

“Early signs of seller exhaustion.”

Binance Bitcoin futures 30-minute chart with order-book data. Source: Exitpump/X

Trader Morin said that BTC/USD was now “frontrunning a key range low” with the key $60,000 mark in sight.

“Swept 61.3k internal low but failed to make higher high. Consistent lower highs -> Sellers in Control,” he told X followers.

“Wouldn’t be surprised to see 60s traded or even ran through.”

BTC/USD 30-minute chart. Source: Morin/X

risk assets

Nonfarm payrolls further reduce Fed rate-cut odds

Crypto bulls were not helped by macro data, with US nonfarm payrolls considerably outpacing expectations to suggest a stronger labor market.

Related: Bitcoin needs one more thing to happen to spark BTC price ‘rally:’ Analysis

The economy added 172,000 jobs in May, more than double the anticipated 85,000.

“April’s jobs number was also revised UP by +64,000 jobs. This marks the second strongest US jobs report in 13 months,” trading resource The Kobeissi Letter responded.

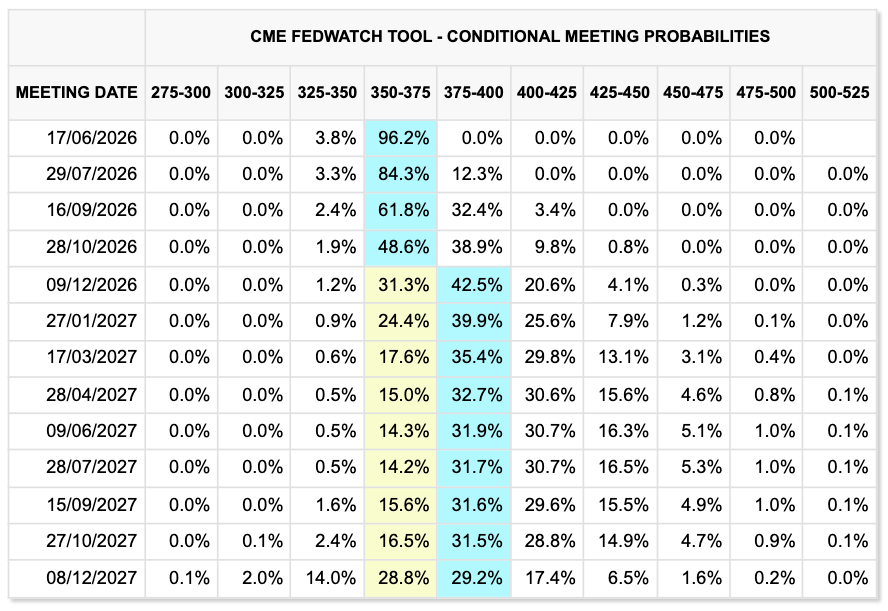

Fed target rate probabilities (screenshot). Source: CME Group

Higher jobs numbers notionally reduce the need for the Federal Reserve to cut interest rates and provide crypto and risk assets with a liquidity tailwind. Data from CME Group’s FedWatch Tool showed markets pricing in a rate hike before the end of the year.

Commenting, trading resource Mosaic Asset Company argued that strong labor-market data would in fact complicate the Fed’s task.

“If the payrolls report for the month of May confirms underlying strength in the economy and labor market, the outlook for monetary policy will grow more uncertain given the recent jump in consumer and producer inflation,” it wrote previously in its latest Mosaic Chart Alerts update.

“At the same time, evidence of solid economic activity is helping the average stock catch up to the gains in the S&P 500 and Nasdaq.”

TLDR

- BlackRock recorded $47.66 million in Bitcoin ETF inflows on June 5.

- The inflow ended a 13-day streak of consecutive outflows for the fund.

- Bitcoin traded near $61,000 during the same session.

- The asset declined more than 15% over the past week.

- The broader Bitcoin ETF market continued to face pressure.

BlackRock ended a 13-day outflow streak with fresh capital entering its Bitcoin ETF on June 5. The fund attracted $47.66 million in new inflows during its latest session. The reversal occurred as Bitcoin retested $61,000 and extended weekly losses beyond 15%.

BlackRock ETF Posts $47.66M Daily Inflow

Data from SosoValue showed BlackRock’s Bitcoin ETF added $47.66 million on Friday. The inflow marked the product’s first positive session in nearly two weeks. The fund had recorded consecutive red days as institutions reduced exposure.

The broader Bitcoin ETF market experienced steady withdrawals for almost three weeks. However, BlackRock reversed that pattern with a single day of fresh allocations. Market data confirmed that other issuers still faced pressure during the same session.

Bitcoin price traded near $61,000 when the inflow occurred. The price level matched levels last seen in February 2024. Over the past week, Bitcoin declined more than 15% as volatility persisted.

Bitcoin Price Weakness Continues Across Market

Bitcoin extended its decline as traders reassessed risk exposure. The asset moved lower during the week and tested support near $61,000. Market charts reflected sustained selling pressure across major exchanges.

The broader crypto market also remained under strain. Major tokens retested 2024 price levels during recent sessions. Total market capitalization contracted as liquidity tightened.

Despite falling prices, BlackRock attracted fresh ETF capital. The timing contrasted with earlier sessions when funds saw redemptions. Market participants linked prior outflows to ongoing volatility and reduced institutional appetite.

BlackRock’s reversal sparked discussion across trading desks. Some analysts cited positioning ahead of potential price stabilization. However, no official statement explained the sudden inflow.

SosoValue data confirmed that BlackRock led daily inflows within the ETF segment. Other products posted either neutral or negative flows during the session. The update highlighted a divergence within the ETF landscape.

Bitcoin remained below its October 2025 peak of $126,000. The asset traded more than 50% lower than that record. Weekly declines compounded the broader market drawdown.

Institutional ETF flows often track broader sentiment shifts. This session broke a 13 day sequence of capital withdrawals. BlackRock’s daily report reflected renewed allocation activity.

The crypto market continued trading in the red zone. Prices across leading assets remained under pressure. Exchange volumes reflected cautious positioning.

BlackRock’s Bitcoin ETF recovery arrived during heightened volatility. The inflow stood at $47.66 million for the trading day. SosoValue published the data on Friday, June 5.

Bitcoin held near $61,000 at the close of the session. The weekly decline exceeded 15% at that point. ETF flow data remained the latest confirmed update from market trackers.

Memecoins are usually where traders go looking for risk. This week they’re where risk is getting cut first. Dogecoin and Shiba Inu both shed roughly 9% as bitcoin drifted toward the $60,000 level, with the sharpest selling concentrated in the most speculative corners of the market.

News Background

• Broader crypto sentiment deteriorated as bitcoin slipped toward the psychologically important $60,000 level, triggering liquidations across altcoins and memecoins.

• Derivatives traders moved into defensive positioning, with DOGE futures open interest falling and SHIB open interest hovering near cycle lows.

• Despite the selloff, both tokens continue to show conflicting signals underneath the surface, with DOGE and SHIB seeing sizeable exchange outflows that would normally be associated with accumulation.

Price Action Summary

• Dogecoin fell from $0.0891 to $0.0830, breaking the ascending channel that had guided price action since February.

• Shiba Inu dropped from $0.000004997 to $0.000004630, slicing through support near $0.000004780 on heavy selling pressure.

• Both tokens saw their biggest volume spikes during breakdowns rather than recoveries, a sign sellers remained in control throughout the session.

Technical Analysis

• DOGE’s breakdown below channel support is the more important development than the percentage decline itself. The ascending structure had held for four months, and losing it shifts attention toward lower support levels near $0.067.

• SHIB’s chart looks weaker still. The token remains below every major moving average and continues printing lower highs and lower lows despite aggressive token burns and ecosystem growth.

• In both cases, exchange outflows failed to support price. That usually means traders are paying more attention to macro conditions and momentum than longer-term accumulation signals.

• Oversold readings are beginning to appear across momentum indicators, but neither DOGE nor SHIB has shown convincing evidence of a durable reversal.

What traders should watch

• For DOGE, the key level is $0.0819. A clean break below it would strengthen the case for a move toward $0.067.

• For SHIB, support sits near $0.000004575. Losing that area exposes the next downside zone around $0.000004500.

• Recovery attempts face immediate resistance at $0.0883 for DOGE and $0.000004780 for SHIB, both former support levels that have now turned into overhead supply.

• Until buyers start reclaiming broken support rather than merely bouncing from oversold conditions, the path of least resistance remains lower.

A set of seven crypto tax bills are being circulated in advance of a hearing of the U.S. House Ways and Means committee next week, with each of the legislative drafts tackling its own narrow aspect of digital assets tax treatment, including relaxing demands for taxes on small transactions and the assets gains in mining and staking.

The committee that oversees tax issues is set to discuss the ideas on June 9, and the legislative text indicates that the panel is targeting a number of areas with focused bills. The various proposals include eliminating tax demands on certain small ( or “de minimis”) transactions, stablecoin activity and network fees; governing the taxation of assets acquired through crypto mining; melding digital assets with existing tax treatment of securities; applying so-called wash sale rules to crypto; and cutting out an appraisal requirement in digital asset donations to charity.

Reducing the mining and staking tax burden is a major component of the industry’s tax-policy strategy, focused on eliminating double taxation in which the assets are taxed both at the time of acquisition and at the point of sale. One of the draft bills seeks to address that issue.

Cody Carbone, the CEO of the Digital Chamber, said in a statement he welcomes the coming hearing as a chance “to refine these proposals and keep the bipartisan tax effort moving forward.” He added that his organization will work with the committee “to strengthen the drafts and deliver the tax clarity and fairness digital assets deserve.”

Though the Digital Asset Market Clarity Act has been the top U.S. policy focus of the crypto industry, Washington lobbyists have routinely said that crypto tax policy was next in line. There have been a number of previous efforts to tackle the lack of clarity on what should constitute a taxable gain in the digital assets space, including an initiative pushed by Senator Cynthia Lummis, a Wyoming Republican who leads a digital assets subcommittee in the Senate Banking Committee.

Lummis has sought and failed to get traction on the ideas several times, including an unsuccessful attempt to get them attached last year to the Republican’s One Big Beautiful Bill spending package.

The arrival of bipartisan crypto tax efforts in the House comes fairly late in the congressional session, though there will be a number of must-pass bills this year that could have items attached to them.

Tokenized stocks, ETFs, Treasuries, and corporate bonds are now firmly rooted in regulated market tests and consumer products. RWA.xyz data places distributed real-world asset value at $26.71 billion and represented asset value at $345.07 billion across the wider tokenization market.

Consumer-facing adoption is expanding as Robinhood EU offers more than 2,000 stock tokens as derivative contracts linked to stocks and ETPs, while Kraken says xStocks reached 100 fully backed tokenized US stocks and ETFs and passed $25 billion in transaction volume after its June 2025 launch.

Traditional market institutions are now testing similar models. DTCC received SEC staff relief in December 2025 for a three-year tokenization service covering highly liquid DTC-custodied assets, including Russell 1000 constituents, major ETFs, and US Treasury bills, bonds, and notes. Nasdaq’s tokenized securities proposal also points toward a regulated model where tokenized shares trade with the same CUSIP, order book priority, and investor rights as traditional shares.

BeInCrypto spoke with experts from 8Blocks, BloFin Research, Phemex, and Zoomex to assess adoption paths and remaining limits on investor trust.

Global Liquidity, Programmability, and Settlement

The early pitch for tokenized stocks centered on extended trading hours, yet experts see the stronger institutional use case in liquidity, distribution, collateral use, and settlement.

Anton Efimenko, Co-Founder and Lead Expert at 8Blocks, links tokenized securities to deeper global order books.

“Beyond speed and higher trading frequency, tokenized securities can trade globally. More investors can access and invest in the same stocks, ETFs, Treasuries, or corporate bonds.” Efimenko said.

In his view, global access gives the same stock, ETF, Treasury, or bond a larger buyer base. If regional stress causes local selling, buyers from another market can enter sooner, helping absorb pressure before panic spreads. Deeper participation can also support larger tickets, giving funds more room to buy securities with less price disruption.

Edward Wu, Head of BloFin Research, places the main value in three areas: distribution, programmability, and settlement efficiency.

“The real value is distribution, programmability, settlement efficiency, beyond 24/7 trading,” Wu said.

Distribution can move securities through wallets, fintech apps, crypto exchanges, and wealth platforms. Programmability can make a tokenized Treasury fund usable inside lending vaults, margin accounts, structured products, or collateral systems. Settlement can also become more efficient when the securities side and cash side move through compatible digital systems, reducing operational friction across execution, transfer, payment, and custody.

Federico Variola, CEO of Phemex, sees tokenized stocks as part of DeFi’s composability trend.

“Apart from 24/7 trading, these tokenized instruments can potentially be used as collateral for other positions, for example leveraged or derivatives positions, borrowing and lending, or even within centralized systems,” Variola said.

Variola said many of these use cases are difficult for average retail users inside traditional banking or trading apps, while DeFi already has much of the technical base needed to support them.

Apps and Exchanges Can Move Early, While Brokerages Hold the Largest Investor Pools

The first wave of tokenized securities is likely to come from crypto exchanges, fintech apps, and permissioned DeFi venues because they can launch products faster, reach global users, and use stablecoins for funding and settlement.

8Blocks expects the largest growth to come through traditional brokerages and banks, where investor capital and trust are already concentrated.

“Tokenized securities will grow fastest where there is already a large concentration of investors and capital: traditional brokerages and banks,” Efimenko said.

Efimenko expects existing brokerage users to adopt tokenized securities when they can diversify portfolios inside accounts they already use. The product becomes easier to accept when it appears inside a trusted brokerage experience.

Wu sees a two-stage adoption path in which crypto exchanges, fintech apps, and permissioned DeFi platforms can move faster in the near term, while established brokerages will decide long-term market size. Interactive Brokers reported 4.646 million client accounts and $789.4 billion in client equity as of Q1 2026, showing the amount of capital established brokers can bring once tokenized securities become part of standard brokerage products.

Permissioned DeFi may also serve institutional users who need compliant access to on-chain settlement, collateral movement, and automated portfolio activity. Its growth will depend on regulation, asset eligibility, and the willingness of institutions to use blockchain-based venues.

Investor Rights Separate Ownership From Price Exposure

Tokenized securities need precise rights because investors must understand the claim attached to the token. A product can offer shareholder-style ownership, a securities entitlement, redemption, dividends, coupons, voting or proxy access, corporate-action treatment, or price exposure through a derivative contract.

8Blocks expects many global users to prioritize financial outcomes over delivery of the underlying asset. A token buyer in one jurisdiction may have little use for a traditional share listed and settled in another country, especially when local brokerage access, tax treatment, or custody options create friction.

Efimenko expects investors to prefer products with “the financial result and a guaranteed claim to it,” including dividends, gains from price appreciation, or coupon payments.

Wu argues product rights should match product marketing. A true tokenized stock should give the holder the same economic and legal position as a traditional shareholder or a defined securities entitlement, including dividends, corporate actions, voting or proxy rights, transferability, and a redemption or conversion path where feasible.

Nasdaq’s proposal follows a similar standard, where a tokenized equity security would need to convey equity interest, dividend rights, voting rights, and residual asset rights upon liquidation to receive treatment equivalent to a traditional security. A product based on price exposure would belong in a separate category.

Robinhood EU’s model shows the difference because its stock tokens are derivative contracts linked to underlying stocks and ETPs, giving price exposure instead of shareholder rights. The product can still serve investors, provided the market description matches the actual claim.

Mainstream Adoption Depends on Familiar Outcomes

Tokenized securities can reach mainstream investors when the crypto elements fade into the background of a normal brokerage or fintech account. The user experience should center on familiar assets and outcomes, such as Treasury yield, Apple exposure, an S&P 500 ETF, a corporate bond, or coupon income.

Fernando Lillo Aranda, CMO at Zoomex, sees this as the most realistic path to mass adoption because investors usually care about what a product delivers, rather than the technical system behind it.

“Mainstream investors historically don’t adopt infrastructure; they adopt outcomes. Most people never cared whether payments ran on SWIFT rails or card networks. They cared that money moved.”

Aranda said tokenized securities could follow the same pattern. If users can access stocks, bonds, funds, private credit, or structured products with faster settlement, lower minimum tickets, programmable ownership, programmable distributions, and global access, the blockchain side becomes part of the background experience.

“Wallets, chains, and DeFi become backend plumbing rather than the product,” Aranda added.

Wu made a similar point, arguing that real adoption depends on making tokenized securities feel familiar to users who already understand brokerage and fintech accounts.

“Tokenized securities need to feel like a normal brokerage or fintech account. Most users do not care about how DTCC, transfer agents, clearing brokers, or payment rails work today.”

In Wu’s view, users should see recognizable financial products first: Treasury yield, Apple, an S&P 500 ETF, or a corporate bond. The chain, wallet, custodian, compliance checks, and settlement mechanics can operate behind the interface.

“The user sees ‘Treasury yield,’ ‘Apple,’ ‘S&P 500 ETF,’ or ‘corporate bond,’ while the chain, wallet, custodian, compliance checks, and settlement mechanics run in the background.”

8Blocks is more cautious about tokenization as a standalone adoption driver. Efimenko expects investors to judge tokenized stocks primarily as stocks, with the token wrapper playing a secondary role.

“Investors know how to assess risk, and for them, tokenized stocks will still be stocks, not tokens. Tokenization is just a wrapper.”

For 8Blocks, this means tokenized securities may improve access, liquidity, and execution, while the underlying asset remains the main source of risk and return.

Trust Depends on Regulation, Custody, and Liquidity

Tokenized public markets need stronger trust conditions before investors treat them like traditional brokerage accounts. Regulation, rights, issuer quality, custody, liquidity, and price consistency remain the main concerns.

8Blocks sees regulation as the biggest barrier because unclear rules force issuers into more complex product designs.

“Regulation is the main barrier,” Efimenko said. “Because regulation is still unclear, RWA issuers are forced to get creative with the structure.”

Efimenko pointed to one possible model where an issuer sells tokenized shares in its own company while using its balance sheet to hold Apple stock. Such a product can give investors economic exposure, but it also places the issuer between the investor and the underlying asset.

BloFin Research sees rights ambiguity as another major weakness in current stock-token markets.

“Many stock tokens track price without giving ownership, voting, dividends, or a direct claim on the underlying company,” Wu said.

For Wu, this creates a trust problem because investors may buy a product linked to a familiar public company while relying on an unfamiliar issuer, custodian, or venue.

“Counterparty and custody risk are also a consideration. Investors are not familiar with the issuers, which are often startup companies.”

Liquidity creates another concern. Wu said tokenized stocks can diverge from the underlying market price when the main exchange is closed or when market-maker support is thin.

“A tokenized stock could drift away from the stock price when the underlying market is closed. Thin order books, fragmented venues, and uneven market-maker support can make tokenized markets feel less reliable.”

Regulators have raised similar concerns. ESMA warned in 2025 about investor misunderstanding in tokenized stocks when buyers receive exposure to listed shares rather than shareholder status. The regulator also noted many tokenization projects remain small and illiquid.

Final Thoughts

Tokenized securities give crypto one of its strongest institutional stories because they connect blockchain-based systems with assets investors already understand. The strongest case comes from global distribution, programmable ownership, collateral use, faster settlement, and enforceable investor claims.

Early growth may come from crypto exchanges, fintech apps, and permissioned DeFi venues, while long-term adoption will depend on banks, brokers, custodians, and regulated market institutions. The strongest products will make chains, wallets, and settlement mechanics fade into the background while placing investor rights at the center of the experience.

Tokenized stocks and bonds can become a major institutional product when buyers can identify their ownership claim, the custodian of the underlying asset, income payment rules, redemption mechanics, and claim protection during market stress. The platforms most likely to win are the ones offering familiar assets with precise rights, dependable custody, and liquidity strong enough to support real investor demand.

The post Tokenized Stocks and Bonds Move Toward Crypto’s Strongest Institutional Product appeared first on BeInCrypto.

Crypto.com broadens sports tie-ups and adds TradingView trading to its exchange

Crypto.com used its latest affiliate newsletter to highlight a string of commercial and product moves intended to raise mainstream visibility and improve the trading experience for active users. The updates include partnerships that put the platform closer to sports fans, a direct execution integration with TradingView on the Crypto.com Exchange, and a weekly market snapshot showing a pullback in prices alongside rising volatility and pockets of outperformance.

Sports and collectibles: Fanatics and SailGP agreements

In the newsletter, Crypto.com announced a collaboration with Fanatics Collectibles to develop what it described as the first UEFA Champions League activation between the two companies. Separately, Crypto.com and OG Prediction Markets were named global partners of the United States SailGP team. Both moves underscore an ongoing strategy among major crypto platforms to lean on high-profile sports partnerships to reach mainstream audiences and lend legitimacy to their brands.

For affiliates and content creators, the company framed the deals as opportunities to appeal to sports-focused communities. Industry observers say such sponsorships can increase short-term brand recognition and drive user acquisition if paired with compelling customer journeys, such as collectible drops or co-branded promotions. However, the marketing lift from sponsorships can vary depending on execution, local regulatory constraints and the degree to which the partnerships translate into active product use.

TradingView integration aims at active traders

Crypto.com confirmed that the Crypto.com Exchange now supports direct trade execution from TradingView. The integration lets users place orders from TradingView’s charting interface while routing executions through the Crypto.com Exchange, combining advanced technical analysis tools with the exchange’s order flow.

This type of connectivity is increasingly common across major venues. For traders, the appeal is straightforward: fewer steps between analysis and execution, plus the ability to use TradingView’s scripting and drawing tools while tapping an exchange’s liquidity. For exchanges, integrations with third-party charting platforms are a defensive and acquisitive play, making it easier to retain active traders who otherwise might prefer platforms offering native advanced charting.

From a competitive standpoint, the move positions Crypto.com’s Exchange alongside peers that already provide charting and execution linkups. Execution quality, latency and fee structure will determine whether the feature materially shifts market share among professional and semi-professional users.

Market snapshot: small price declines, higher volatility, token winners

Crypto.com’s research dashboard data included in the newsletter showed a modest weekly pullback: the price index fell about 3.53% while the volume index dropped roughly 3.97%. At the same time, the volatility index increased by about 27.6%, signaling choppier trading conditions over the period.

Bitcoin and Ether were cited as down around 4.4% and 4.5% respectively for the week, while smaller-cap or niche tokens produced the biggest moves. Hyperliquid (HYPE), Toncoin (TON) and Hedera (HBAR) were highlighted as leaders in price gains. The newsletter attributed HYPE’s momentum in part to increased whale activity and flows into recently launched U.S. spot ETFs connected to the project, noting more than $100 million in inflows during May.

Rising volatility and selectively strong token performance underline a bifurcated market: major-cap assets remain sensitive to macro headlines and liquidity conditions, while idiosyncratic catalysts can drive outsized moves in specific tokens. Affiliates and traders should weigh the increased dispersion when positioning content or strategies, as headline returns from smaller tokens often come with elevated execution and custody risks.

Affiliate and creator program developments

The newsletter also served operational purposes for partners. Crypto.com flagged a new dedicated creator program for key opinion leaders and influencers, instructing eligible partners to check their inboxes for invitations. The update included a reminder to track mentions of “Crypto.com” to ensure proper attribution in the affiliate system, and listed several top-performing creative assets such as app banners and product-level creative concepts.

These program touches speak to an ongoing professionalization of crypto affiliate channels: firms increasingly provide creators with targeted content, measurement tools and bespoke offers to influence user acquisition. The approach helps platforms manage compliance and performance simultaneously, though creators must remain mindful of local advertising and financial promotion rules when promoting crypto products.

What this means for the market and affiliates

Taken together, the announcements reflect a dual strategy: use consumer-facing partnerships to widen brand reach, while improving product-level features to better serve active traders. For affiliates, the commercial tie-ins create new promotional narratives — sports fandom, collectibles and exclusive creator benefits — that can be leveraged to reach distinct audience segments.

On the product side, TradingView execution capability addresses a clear user need for integrated workflows. Whether it translates to measurable market-share gains will depend on the execution experience, liquidity and whether Crypto.com can combine these features with differentiated pricing or service levels for professional users.

Finally, the market snapshot is a reminder that trading conditions remain mixed: marginal declines in major assets alongside higher volatility and selective winners mean that marketing messages and trading strategies need to be tailored to audience risk tolerance and regional regulatory limits. Crypto.com’s newsletter itself notes jurisdictional constraints in product availability, a practical consideration for affiliates operating across multiple markets.

Source: Crypto.com affiliate newsletter, June 2026.

Crypto World

Inside MEXC’s move to build an all-in-one trading station for digital and traditional assets

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

MEXC expands beyond futures with RealStocks, offering access to U.S. stocks and ETFs via USDT.

Summary

- MEXC reports growing demand for TradFi-linked products, with INTC futures volume rising 1,684% month-over-month and other equity-linked contracts posting strong growth.

- The exchange has launched RealStocks, allowing eligible users to access U.S.-listed stocks and ETFs through broker-backed infrastructure using USDT.

- RealStocks expands MEXC’s multi-asset offering as crypto traders increasingly seek exposure to equities, ETFs, commodities, and broader market themes.

Crypto trading is becoming less isolated from the rest of the market. Users who once came to exchanges mainly for tokens, spot pairs, and futures are now tracking equity themes, macro moves, and alternative assets in the same daily workflow.

MEXC’s April data gives one recent example. INTC futures volume rose 1,684 percent month over month, while AMD, TSM, and NVIDIA-linked futures also posted triple-digit growth. Activity also increased across QQQ, GOOGL, and SP500 futures, showing how traditional market themes are moving deeper into crypto exchange behavior.

For MEXC users, this interest has already been visible through TradFi-linked futures. The exchange says the category now covers more than 130 traditional financial assets, including U.S. equities, stock indices, ETFs, precious metals, commodities, and foreign exchange products. RealStocks extends that path from futures exposure into U.S. stock and ETF access. Eligible users can reach U.S.-listed stocks and ETFs through licensed broker and clearing infrastructure, transact in USDT and use MEXC’s existing interface.

A different route into U.S. stocks

U.S. stock access is now one of the areas where crypto exchanges and RWA platforms are testing different models. Bitget Reality, Ondo Stocks and xStocks have helped shape the tokenized equity narrative. Gate Stocks and Binance’s stock-access plans, including bStocks, point to another route where exchanges bring stock and ETF access closer to existing users.

For users comparing these options, the distinction is practical. Tokenized products may appeal to those who want on-chain portability or DeFi connectivity. Broker-based stock access may appeal to users looking for a route closer to traditional equity ownership, including dividend or distribution eligibility where applicable. RealStocks sits in that second group while keeping the trading flow close to crypto user habits.

How RealStocks fits the MEXC user journey

MEXC says RealStocks was validated by more than 20,000 users during its beta phase before the official launch. The product is connected through Atomic Vaults. MEXC describes the company as a U.S. FINRA-licensed broker-dealer and brokerage infrastructure provider backed by Founders Fund and ARK Invest.

Through that structure, eligible users can access thousands of U.S.-listed stocks and ETFs. Trading hours follow Nasdaq market sessions, and settlement follows a T+1 structure. Where applicable, users may also receive dividends or distributions on their holdings.

| RealStocks at a Glance | |

| Real Stock Access | Crypto Exchange Flow |

| 7,000+ U.S.-listed stocks and ETFs | Trade with USDT |

| Broker-connected access | Existing MEXC interface |

| Nasdaq market sessions | Zero platform fees |

| T+1 settlement | Familiar exchange flow |

| Dividends | Lower entry friction |

For someone who already holds stablecoins, RealStocks keeps U.S. equity access closer to the exchange workflow they already know. Users can test stock and ETF access through USDT-based trading without moving into a separate brokerage environment.

RealStocks makes MEXC’s “Gateway to Infinite Opportunities” initiative easier to understand in product terms. Users already encounter crypto assets, tokenized products, TradFi-linked futures, commodities, precious metals and other market-linked instruments inside the MEXC ecosystem. RealStocks adds U.S. stock and ETF access to that mix.

A trader may begin with spot crypto, then move into futures during periods of higher volatility. When U.S. technology stocks are active, the same user can follow AI semiconductor futures and use RealStocks to access listed U.S. equities or ETFs. For users, the value is straightforward: fewer separate systems when they are following several market themes at once.

Zero Fees and launch incentives lower the first step

Fees matter most when users test a new product for the first time. MEXC says RealStocks carries zero platform trading fees during the launch period where available. For users entering a new asset category, this can reduce concerns around onboarding, funding, currency conversion, and trading costs.

The launch also includes limited-time incentives for eligible users, including activity-based rewards and support for real-time market data access.

MEXC has also used zero-fee positioning across other parts of its ecosystem. In April, the company highlighted user fee savings during its 0-Fee Fest, including activity from TradFi-linked futures products. For active users, the relevance is clear. A new asset category becomes easier to test when they are already moving between different market themes.

From crypto account to wider market access

For exchanges, competition is expanding beyond token availability and trading fees. Users are also looking at how easily a platform lets them move between crypto assets, equity themes and other market-linked products.