Business

NVII: Weekly Distributions From Nvidia Options (BATS:NVII)

JHVEPhoto/iStock Editorial via Getty Images

Fast Facts

REX NVDA Growth & Income ETF (NVII) is an actively managed ETF launched on 05/28/2025 with a primary objective of weekly income and a secondary objective of leveraged exposure to the common stock of NVIDIA Corporation (NVDA) with a daily factor between 1.05 and 1.5. NVII has a total expense ratio of 1.49% and an extremely high distribution rate: 48.12%. Distributions are paid on a weekly basis. NVII is a small but quite liquid ETF, with $102 million in assets under management and an average daily trading volume of $3.6 million. The fund’s issuer, REX Shares, specializes in alternative strategy ETFs and ETNs, in particular thematic, leveraged, and options income products.

Strategy

As described in the prospectus by REX Shares, the fund maintains notional exposure to the common stock of Nvidia between 105% and 150% of NAV using derivatives such as options, swap agreements, and leveraged ETFs on Nvidia, and may also hold the stock itself. The exact leverage factor may change based on real-time technical analysis. The portfolio is rebalanced on a daily basis to attain the targeted exposure every single day.

Additionally, the fund writes covered call options to generate income from premiums. These options may limit participation in the upside potential of the underlying stock. The fund also holds treasuries and cash equivalents as collateral for derivatives.

The fund may use a synthetic covered call strategy, with exposure in Nvidia obtained by a “synthetic long” using a combination of options designed to replicate the asset’s price return. A synthetic long consists of buying call options and selling put options on the underlying asset with the same expiration date and strike price.

There is no guarantee that the objectives of exposure and weekly distributions will be met. Distributions may have a high rate of ROC (return of capital), reducing NAV and therefore the amount of future distributions. Moreover, the daily rebalancing generates leveraged drift (“beta-slippage”), making unpredictable the leverage factor measured on a period longer than one day.

Portfolio

NVII has a 1.25 leverage factor, 120% of net asset value in cash equivalents and treasuries, and three positions in NVDA options, which currently are:

- A long call and a short put corresponding to a synthetic long expiring on 6/18/2026 with a strike price of 235.74.

- A short call (covered call) expiring the same day with a strike price of 208.97.

This is an example from 6/12/2026. Portfolio constituents and leverage may have changed by the time you read this and will, of course, change over time.

Fundamentals

Nvidia is the publicly traded company with the largest market capitalization in the world at the time of writing (about $5 trillion) and is classified by GICS in the Information Technology sector and in the Semiconductors industry. Its share price has been multiplied by 13 since January 2023, propelled by the company’s leadership in AI chips and market sentiment. Based on Seeking Alpha’s quantitative factor grades, NVDA has excellent growth and profitability characteristics, but stretched valuation.

NVDA quantitative factor grades (Seeking Alpha)

Seeking Alpha’s aggregate quantitative ranking puts NVDA in 28th position in its industry among 69 companies, with Micron Technology, Inc. (MU), Intel Corporation (INTC), and Advanced Micro Devices, Inc. (AMD) in the top ranks. As the tech environment changes, so can these rankings.

Historical Performance

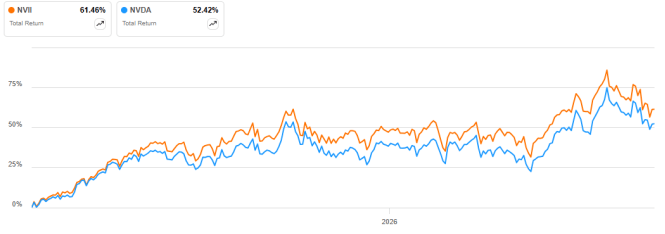

Currently, NVII is 9% ahead of Nvidia in total return between its inception and 6/12/2026. It is encouraging, but the fund has a short history, and this gap may not be representative of its long-term potential.

NVII vs. NVDA total return (Seeking Alpha)

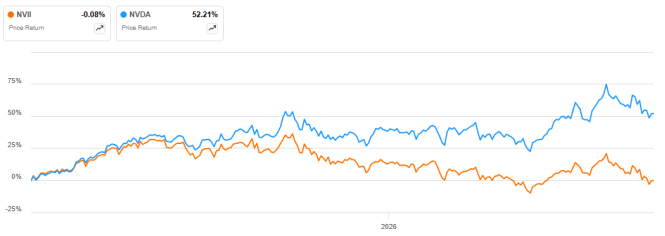

In this time frame, the share price is close to flat, all the gains coming from distributions.

NVII price return (Seeking Alpha)

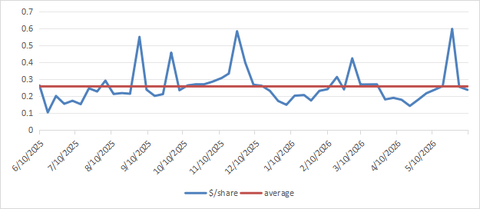

The weekly distributions have been very variable, with an average of $0.26 per share, as plotted below.

Distribution history (Chart: author; data: REX Shares)

For 2026 until 6/12, distributions have been classified as 97.7% return of capital (“ROC”). High ROC may have a negative impact on a shareholder’s tax. For example, non-resident aliens (“NRA accounts”) may be initially submitted to withholding tax, with an adjustment at year-end that is not always automatic, depending on the broker. High return of capital over time can also indicate potential NAV decay.

NVII Vs. Competitors

The next table compares characteristics of NVII and four derivative income ETFs based on NVDA:

- YieldMax NVDA Option Income Strategy ETF (NVDY).

- Roundhill NVDA WeeklyPay™ ETF (NVDW).

- GraniteShares YieldBOOST NVDA ETF (NVYY).

- GraniteShares Autocallable NVDA ETF (ANV).

NVII has the highest expense ratio and the lowest yield, but the best total return.

Market Interest

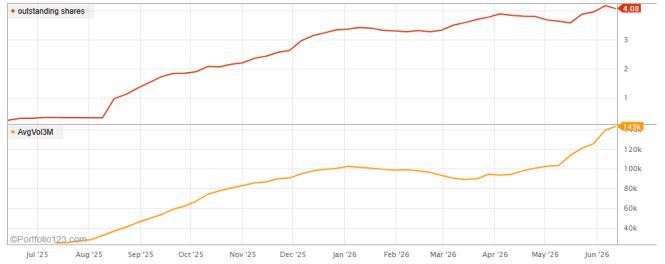

The fund had a solid start in asset growth and investor interest, represented by outstanding shares and average volume on the next chart. As the popularity of the underlying (Nvidia) changes, this ETF could be affected. Waning investor interest would hurt NVII in terms of asset growth, and AUM could shrink. If implied volatility falls, this would diminish its income generation potential. Additionally, due to the leverage factor, price drops in Nvidia would be magnified.

Outstanding shares in million and 3-month average daily volume (Portfolio123)

Strengths And Risks

The strengths of NVII are:

- A very high yield.

- Weekly distributions.

- Sufficient liquidity.

- Outperformance compared to peers.

The risk factors of investing in the fund include:

- High expense ratio.

- Low AUM.

- Short history.

- Single stock exposure (company-specific risk).

- Active management (limited transparency).

Takeaway

NVII is best suited for investors who are bullish on Nvidia and seek to combine income and capital appreciation. The latter may only be achieved by reinvesting a part of distributions. Due to the risk factors listed above, this ETF is better used as a satellite rather than a core holding.

This article answers these three main questions about NVII:

- How does NVII incorporate income and Nvidia’s price action?

- How has NVII performed compared to its underlying stock and similar ETFs?

- What type of investor is NVII best suited for?

Editor’s note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

Business

Sunrise Energy Metals Shares Surge 14% on Critical Minerals Momentum and Strategic Project Advances

SYDNEY — Sunrise Energy Metals Ltd shares jumped 14.14% on Monday to close at $16.87, extending a remarkable rally as investor enthusiasm for critical minerals and the company’s scandium project continued to drive strong buying interest in the Australian resources sector.

The significant gain pushed the company’s market capitalization higher, reflecting sustained market optimism around its Syerston project in New South Wales, which is positioned to become a major Western producer of scandium. The metal, used in aerospace, defense and clean energy applications, has seen heightened demand amid global supply chain diversification efforts away from dominant producers.

Sunrise Energy Metals has benefited from several positive catalysts in recent months, including strategic partnerships and government interest in securing reliable supplies of critical minerals. The company’s focus on developing what could be one of the first major primary scandium operations outside China has attracted attention from investors seeking exposure to materials essential for advanced manufacturing and the energy transition.

Project Developments and Strategic Partnerships

The Syerston project remains central to Sunrise’s value proposition. Recent updates on resource estimates and development plans have reinforced its potential as a significant scandium producer. The company has made progress toward a final investment decision, targeting early production in the coming years.

A notable highlight has been the involvement of major defense and industrial players. Lockheed Martin secured a multi-year supply option for scandium oxide from the project, underscoring the material’s strategic importance for aerospace and defense applications. Such partnerships provide validation and potential revenue visibility that investors have rewarded.

The company has also pursued financing and offtake discussions to support project development. Recent capital raises have strengthened its balance sheet, enabling continued advancement of pre-construction activities while minimizing dilution concerns for existing shareholders.

Analysts have highlighted the compelling long-term thesis for Sunrise, citing tight global scandium supply, growing demand in solid oxide fuel cells, aluminum alloys and other high-performance applications. The stock’s dramatic rise over the past year reflects the market’s recognition of this potential, though volatility remains high given the project’s development stage.

Market and Sector Context

The resources sector on the ASX has seen renewed interest amid stabilizing commodity prices and positive global sentiment following recent geopolitical developments. Critical minerals, in particular, have attracted attention as governments and industries seek to secure supplies for clean technology and defense needs.

Sunrise’s performance stands out even within this context. The company’s focus on scandium differentiates it from more traditional mining plays, offering investors exposure to a niche but strategically important market with limited Western supply alternatives.

Broader interest in battery materials and critical minerals has supported related stocks, but Sunrise’s specific advancements and partnerships have driven outsized gains. The stock has shown remarkable momentum, with significant percentage increases reflecting both fundamental progress and speculative interest in the critical minerals theme.

Company Background and Strategy

Sunrise Energy Metals, formerly known as Clean TeQ, has repositioned itself around the Syerston scandium project after earlier work on other battery materials. The company benefits from experienced leadership and a location in a stable jurisdiction with established infrastructure.

Its strategy centers on developing a world-class scandium operation while exploring complementary opportunities in related materials. Management has emphasized responsible development, community engagement and environmental considerations as the project advances toward construction.

Recent announcements, including equity investments and applications for quotation of securities, have supported ongoing development activities. The company continues to engage with potential partners and offtake customers to de-risk the project and secure long-term revenue streams.

Analyst and Investor Views

Market observers have noted the stock’s strong performance while cautioning about the risks inherent in development-stage mining companies. Execution on project timelines, securing financing and navigating regulatory requirements will be critical to realizing the full potential of Syerston.

Valuation metrics have expanded significantly with the share price rise, reflecting optimism but also raising questions about near-term catalysts. Investors are closely watching for updates on construction financing, additional offtake agreements and technical studies that could further validate the project’s economics.

For long-term believers in the critical minerals story, Sunrise offers leveraged exposure to scandium market growth. However, the stock’s volatility underscores the need for careful position sizing and thorough due diligence.

Broader Industry Trends

The global push for supply chain security in critical minerals has created opportunities for Western producers like Sunrise. Governments in the United States, Europe and Australia have implemented policies to support domestic and allied production of materials essential for defense, electronics and clean energy.

Scandium’s unique properties — strength, lightness and corrosion resistance when alloyed with aluminum — make it attractive for aerospace and automotive applications. Growing interest in hydrogen technologies and fuel cells could provide additional demand drivers in the coming years.

Sunrise’s progress contributes to a more diversified global supply picture, reducing reliance on single sources and enhancing supply chain resilience. The company’s success could encourage further investment in similar projects across Australia and other stable jurisdictions.

Risks and Considerations

As with any junior to mid-tier mining company, Sunrise faces risks including project delays, cost overruns, commodity price fluctuations and regulatory challenges. The capital-intensive nature of mine development requires careful financial management and access to funding on reasonable terms.

Market sentiment toward critical minerals can shift rapidly based on macroeconomic conditions, policy changes and technological developments. Investors should monitor quarterly updates, exploration results and partnership announcements for signals on project momentum.

Diversification remains important when considering exposure to individual mining stocks. While Sunrise’s story is compelling, balancing it with other assets helps manage sector-specific risks.

Outlook for Sunrise Energy Metals

The company is transitioning from explorer to developer, with key milestones ahead including final investment decisions and construction timelines. Successful execution could position Sunrise as a significant player in the Western scandium market, with potential for substantial value creation.

Management’s focus on strategic partnerships and disciplined project advancement provides a solid foundation for growth. As global demand for critical minerals expands, Sunrise is well-placed to benefit from its advanced project and strong technical credentials.

Monday’s strong share price performance reflects continued market enthusiasm for the company’s potential. While near-term volatility is likely, the longer-term outlook remains positive for investors aligned with the critical minerals thesis.

As Sunrise Energy Metals advances its Syerston project, the company stands at the forefront of efforts to develop secure, Western sources of scandium. Its recent market performance underscores investor belief in the strategic importance of its assets and the potential for significant returns as the project moves toward production.

The mining sector’s evolution toward critical minerals for modern technologies creates exciting opportunities, and Sunrise Energy Metals is emerging as a notable participant in this shift. Investors will continue to watch closely as the company delivers on its development plans and capitalizes on growing global demand.

Siegfried shares down 3% at UBS on weak H1 local currency growth trend

Business

RIL shares jump 6% in 3 days, market cap soars by Rs 1 lakh cr ahead of AGM. Why Morgan Stanley still sees 38% upside

Reliance Industries (RIL) shares jumped to Rs 1,333.40 apiece on NSE on Tuesday. The recent surge in the shares of the Mukesh Ambani-led company added more than Rs 1 lakh crore to its total market capitalisation since the stock hit a 52-week low of Rs 1,253.20 apiece on June 11.

Morgan Stanley on Reliance Industries share price

Morgan Stanley maintained its ‘Overweight’ rating on the shares of Reliance Industries, with a target price of Rs 1,803 apiece. The international brokerage in its note released on Monday said that energy security policies and tighter refining markets should keep product spreads structurally stronger for longer, supporting Oil to Chemicals’ (O2C) earnings despite higher logistics costs.

“We think Reliance remains well positioned given its ability to process heavy and sour crude grades, access cheaper feedstocks and maintain one of the most diversified crude sourcing portfolios globally. We also see the chemical cycle recovering, with advantaged feedstocks through US ethane and captive naphtha supporting a 6-8% uplift to earnings this year,” Morgan Stanley said.

Beyond O2C, the international brokerage highlighted that Monetisation 4.0 is underway as solar modules and cell manufacturing, and energy storage manufacturing ramp up, and the company begins monetising investments, which it believes is not fully reflected in valuations. Reliance’s AI monetisation and AI datacenter investments also remain a “show me” story for investors, according to Morgan Stanley.

“RIL is trading at 1.1x EV/IC and is trading at a 68% discount compared to domestic peers across all verticals, similar to its position in 2018 before recording significant outperformance,” it added.

Also read: US-Iran peace deal! Reliance Industries, ONGC; which other oil & gas stocks will emerge as top winners and losers?

Reliance Industries AGM

Reliance Industries is set to hold its 49th Annual General Meeting (AGM) on June 19 (Friday) as investors await updates on the group’s growth plans, the much-awaited Jio Platforms IPO, retail expansion strategy and progress in its new energy business.

The meeting will be conducted through video conferencing and other audio-visual means, continuing the format adopted by the company in recent years. The AGM remains one of the most closely watched corporate events in India as it often serves as a platform for major business announcements from Reliance and its subsidiaries.

The AGM address by Chairman Mukesh Ambani is expected to be the key highlight, with updates from senior leadership across businesses, including telecom, retail and new energy.

Also read: RIL AGM 2026 this week! Date, time, where to watch live and what to expect

Reliance Industries share price

Reliance Industries shares have gained around 5% in one week but are down around 16% in 2026 so far. The stock tumbled more than 7% in one year, but gained over 3% in three years and 20% in five years.

The company currently has a market cap of more than Rs 18 lakh crore.

Also read: Stocks to buy in 2026 for long term

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Dalal pointed out that elevated crude prices over an extended period continue to filter through the economy in indirect ways. Even companies not directly linked to fuel retail are facing cost pressures as petroleum derivatives are used as key inputs. This, he said, is either compressing margins or forcing price increases that could eventually weigh on consumption demand. As a result, he expects the first half of the year to remain weak on earnings, with Q1 and Q2 likely under pressure.

He further cautioned that global oil trends are only one part of the inflation picture, with domestic monsoon conditions emerging as another critical variable. A weak or delayed monsoon, he said, could push food inflation higher, potentially forcing the RBI into a tighter monetary stance. Given these overlapping uncertainties, Dalal believes markets are unlikely to sustain a one-way rally and instead may remain rangebound, with Nifty oscillating between 23,000 and 24,500 over the next several months.

On portfolio strategy, Dalal emphasised a diversified approach with a strong tilt toward structural growth themes. He sees the power sector as a long-term beneficiary of electrification, rising data centre demand and reduced reliance on fossil fuels, suggesting an allocation of around 10% to 15%. Consumption, despite short-term softness, remains a core structural theme in his view, given India’s low per capita income and long runway for demand growth.

He is also constructive on financials, which he believes should form a significant portion of portfolios, as credit growth is closely tied to India’s capex cycle. Banking and financial services, he suggested, could account for 20% to 25% of allocations, supported by improving lending growth trends and structural demand for credit in the economy.

Within the banking space, Dalal maintains a clear preference for private sector lenders over PSU banks. While acknowledging the appeal of public sector banks, he highlighted risks arising from policy intervention during stress periods, particularly in agriculture-linked credit cycles. Private banks, in contrast, operate with more independent risk frameworks and stronger control over balance sheets. He highlighted HDFC Bank as a key large-cap preference, citing potential margin expansion and franchise strength. Among mid-tier names, he remains positive on IndusInd Bank, noting that concerns have largely been priced in and exposure risks have moderated. He also sees opportunity in IDFC First Bank, while suggesting selective exposure to financial plays linked to infrastructure and power financing.

He further highlighted opportunities in NBFCs and infrastructure lenders such as Power Finance Corporation and REC, where strong exposure to government-linked lending and improving demand outlook could support steady growth. He also mentioned Sammaan Capital and Shriram Finance as beneficiaries of strong capital positions, which could enable multi-year growth without the need for frequent equity dilution.On Sammaan Capital, Dalal expressed caution on near-term return ratios, particularly the ambitious 3%–4% ROA guidance, calling it aggressive given rising operating costs associated with business diversification into new lending segments. However, he acknowledged that significant past write-offs could potentially support future profitability through write-backs, while improving credit ratings could lower funding costs and enhance spreads over time. He also noted that a shift toward higher-yielding loan segments such as gold and personal loans could support earnings, although he expects the full benefits to play out gradually rather than immediately.

Overall, Dalal’s view is that while structural growth drivers in India remain intact, the market is currently navigating a complex mix of inflation risks, weather uncertainty and global commodity trends. This, he believes, makes a strong breakout unlikely in the near term, with a more stable earnings-driven phase likely to emerge only as visibility improves into FY28.

Aman Chowhan said monsoon concerns are not a major risk for earnings at this stage, but crude oil remains the dominant macro variable. He noted that even in a scenario where geopolitical tensions ease, oil prices could remain elevated, keeping pressure on corporate earnings. “Monsoon is not a big worry. A weak monsoon may have some impact. The bigger issue is crude oil. Even if there is a deal with Iran, oil can stay around 80. That is the real risk.” He added that the impact of higher oil prices is likely to show up more clearly in upcoming quarters. “March quarter was fine due to inventory. June will show the impact. We see a 100–200 bps hit from higher oil prices.”

On the earnings outlook for FY27, Chowhan said visibility remains limited and companies themselves are still assessing the impact. “Earnings revision is yet to happen. Companies themselves are unsure of the impact. We will know more in a few weeks.” He added that the key pressure point is likely to be margins rather than demand. “The risk is more on margins than topline. Demand is holding up well.”

On portfolio positioning, he said allocation has shifted toward defensive and structural themes, especially in a high crude oil environment. “We are buying renewables—solar, wind, ethanol. That is a key theme.” He also highlighted increased exposure to pharma and domestic manufacturing as preferred areas for incremental investment.

On the IT sector, Chowhan remained cautious despite recent corrections, citing structural concerns around artificial intelligence and valuations. “We exited IT six months ago. No hurry to re-enter. Upside is limited.” He said AI-led efficiency improvements could challenge India’s traditional low-cost advantage, keeping valuation multiples under pressure. “AI will improve efficiency, but it pressures India’s low-cost model. Valuations may stay under pressure.”

On consumption, he maintained a constructive view on demand but flagged near-term margin pressure due to rising input costs, particularly metals. “Demand is strong. We like discretionary and durables.” However, he added that higher metal prices could weigh on profitability in the short term.

On other sectors, he said capital market-linked businesses such as wealth and broking remain attractive due to strong business models, while infrastructure has turned neutral due to fiscal pressures arising from higher oil prices. “Infra is neutral due to fiscal pressure from higher oil.”In financials, Chowhan said fundamentals remain healthy but foreign institutional investor (FII) selling continues to weigh on sentiment. “Banking is good, but FII selling is a headwind.” Within the space, he continues to prefer NBFCs and private banks over PSU banks.

He also highlighted FCNR inflows as a supportive factor for the currency, noting that attractive yields could draw meaningful foreign inflows. “FCNR inflows are positive for the rupee. Returns can be attractive, even 12–15% with leverage.”

On tactical opportunities, Chowhan pointed to chemicals, defence, and select engineering stocks as areas of interest, supported by currency benefits and relative valuation comfort.

BrandywineGLOBAL – Corporate Credit Fund Q1 2026 Commentary

Giotto.ai opens AI model access to Europe and Switzerland

Business

A mother wanted to keep her six children connected forever. The unique names she gave them became a symbol of their success

A mother’s unusual idea behind six unique names

Xaviera Greene-Davis was raising six children in Newport News, Virginia, while facing challenges that had also shaped her own early life. She wanted her children to grow up believing they were capable of achieving more than what people around them expected.

The names of six US states became her way of creating a shared identity for her children. For Greene-Davis, those places represented opportunities, growth and possibilities beyond the neighbourhood where her family lived.

During difficult phases of her life, including periods when she was in and out of jail, she hoped the names would keep her children connected and remind them that they belonged together.

“It worked,” Montana Jones, 26, tells TODAY.com. “We’ve been close our whole lives. It’s always been the six of us.”

Names that made the siblings stand out

The unique names quickly attracted attention as the children grew up. Montana Jones often heard jokes and comparisons linked to the popular Disney character Hannah Montana.However, the reactions never changed how she felt about her name. Instead, she sees it as a meaningful gift from her mother and is even thinking about continuing the tradition in her own way.

“I plan on doing something similar,” Montana says. “If not states, maybe cities.”

Six children, six different journeys

Greene-Davis later moved away from Virginia, got married and relocated with her family to North Carolina. According to Montana, the move helped her mother transform her life.

“She completely turned her life around.”

Greene-Davis also believes the decision changed the direction of her family.

“It was a great decision,” Greene-Davis agrees.

Today, she looks at her children’s achievements as proof of that journey. All six children completed high school, and each has followed a different career or education path.

Montana works as a deputy sheriff, while Nevada, 27, is employed with a restoration company. Indiana, 23, works as a veterinary technician, and Arizona, 21, is a 911 dispatcher. Missouri, 20, works at a daycare centre, while Dakota, 18, plays football at Virginia State University.

A family story built around hope

For Montana, the names are more than just unusual choices. They represent her mother’s belief that her children could create a different future.

“She always felt in her heart that her six states were going to be something,” Montana says. “Everybody is going to remember our names.”

USA Rare Earth: Strategic Importance Is Not A Valuation Framework

Business

IFCI shares rally 30% in 3 days, hit fresh record high amid buzz around NSE filing IPO papers by Thursday

IFCI shares hit a new record high of Rs 91.49 apiece on the NSE today. The sharp surge over the three sessions has added more than Rs 5,660 crore to the company’s market capitalisation, pulling it up to more than Rs 24,650 crore.

The rally was driven by the fact that IFCI owns a 52.86% stake in Stock Holding Corporation of India (SHCIL), which, in turn, holds 4.4% of NSE as of the December quarter. Through its controlling interest in SHCIL, IFCI enjoys indirect exposure to NSE, making its stock particularly sensitive to developments related to the exchange’s IPO.

Also read: Bonus bonanza! Last date to buy Brigade Enterprises shares for 1:3 bonus issue reward

NSE to file IPO papers tomorrow?

The National Stock Exchange is likely to file its draft red herring prospectus (DRHP) for its maiden public issue by Thursday, CNBC-TV18 reported, citing sources. The report said that the DRHP will be finalised by today, after which NSE’s board will meet and ratify the filing of the DRHP. People familiar with the matter further told the business news channel that the IPO valuation is set to be higher than Rs 5 lakh crore, and the exchange is planning to list by November this year, between Navratri and Diwali.

The Economic Times couldn’t independently verify the report.

NSE, along with Reliance Industries’ Jio Platforms, is likely to file its respective IPO papers with SEBI this week, Business Standard reported earlier, citing people familiar with the matter.

The proposed public issue is expected to rank among the biggest IPOs in India’s capital market history. The listing would provide a liquidity event for several long-term institutional investors while marking a major milestone for the country’s leading stock exchange.

Also read: NSE’s mega IPO! Who can sell shares via OFS? Check eligibility, deadlines and more

Earlier this year, SEBI granted a no-objection certificate (NOC) for NSE’s much-awaited IPO, removing a key regulatory hurdle that had delayed the process for years. The development is particularly significant for IFCI given its indirect ownership in the exchange through SHCIL.

IFCI share price performance

IFCI shares have gained 68% so far in 2026 and have rallied 41% in the past one month alone. Over a longer horizon, the stock has delivered returns of 638% in three years and 577% in five years.

The company currently has a market capitalisation of more than Rs 24,650 crore.

Also read: Will SpaceX’s $75 billion IPO set the ball rolling for Reliance Jio and NSE listings in India?

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

XRP: They Don’t Expect This

When does Sara Cox’s BBC Radio 2 Breakfast show start?

Sunrise Energy Metals Shares Surge 14% on Critical Minerals Momentum and Strategic Project Advances

-

Business2 days ago

Business2 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Crypto World5 days ago

Crypto World5 days agoOppenheimer backs SpaceX as $70 billion retail frenzy builds

-

Crypto World5 days ago

Crypto World5 days agoMarkets Rally as SpaceX IPO Looms Amid Iran Tensions and Inflation Surge

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World1 day ago

Crypto World1 day agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Entertainment7 days ago

Entertainment7 days agoThe Ryan Gosling True Crime Thriller On Netflix That Gets Even Stranger, Stream It Now

-

Tech3 days ago

Tech3 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Sports7 days ago

Sports7 days agoBangladesh beat Australia after 20 years in ODIs, register only their second win over six-time world champions | Cricket News

-

Crypto World3 days ago

Crypto World3 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech4 days ago

Tech4 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

Tech5 days ago

Tech5 days agoDutton Ranch star claims they ‘didn’t see any disruption’ on set following Chad Feehan’s exit from Yellowstone spinoff fueled by Taylor Sheridan clash rumors

-

NewsBeat4 days ago

NewsBeat4 days agoEl Nino has formed in the Pacific and could set records, forecasters say

-

Politics5 days ago

Politics5 days agoPolitics Home | Healey Resignation Is “Colossal Failure Of Government”, Says Former Labour Defence Secretary

-

Tech6 days ago

Tech6 days ago‘This is Seattle’s position on AI’: City Council votes unanimously to pause big new data centers

-

Business6 days ago

Business6 days agoThailand Ranks Second Worldwide for AI Adoption Growth, Microsoft Reports

-

Entertainment5 days ago

Entertainment5 days agoDonnie Wahlberg & More Heat Up Las Vegas at Circa’s Barry’s Downtown Prime

-

Tech5 days ago

Tech5 days agoOpendoor Ends India Operations, Fueling a Bigger Conversation About AI and Outsourcing

-

Sports5 days ago

Sports5 days agoFirst Time Since 1971: Australia Register Historic Low In ODI Cricket

-

Politics5 days ago

Politics5 days agoBelfast burns, while Met chief points finger at Iran and Russia

-

NewsBeat4 days ago

NewsBeat4 days agoFBI searches office of Ohio voter registration group

You must be logged in to post a comment Login