Crypto World

OpenAI vs Anthropic IPO Showdown: Which AI Giant Makes the Smarter Investment?

Key Takeaways

- OpenAI has submitted a confidential filing for its U.S. public offering, seeking a potential valuation reaching $1 trillion

- The company posted $5.7 billion in first-quarter 2026 revenue while spending $3.7 billion during that timeframe

- Anthropic submitted its IPO paperwork on June 1 following a $65 billion funding round at a $965 billion valuation

- Anthropic reported annualized revenues exceeding $30 billion, outpacing OpenAI’s previously announced $24 billion annual run rate

- Market experts indicate Anthropic could present a more attractive entry valuation given its enterprise focus and revenue pricing

The artificial intelligence sector is preparing for two landmark public offerings as both OpenAI and Anthropic have submitted confidential IPO filings with U.S. regulators. These parallel listings represent potentially the most significant tech market debut in years, though each company presents distinct investment propositions.

OpenAI carries stronger brand recognition globally. As the creator of ChatGPT, it has established unparalleled consumer awareness in the AI space. According to Reuters, the company is pursuing a valuation that could reach $1 trillion, with a possible market debut scheduled for September 2026.

Revenue figures demonstrate substantial commercial traction. OpenAI recorded $5.7 billion in revenue during the first quarter of 2026. However, operating expenses hit $3.7 billion in the identical period, revealing significant cash burn as the company scales.

This profitability gap represents a critical consideration for potential shareholders. While the brand commands impressive market position, the financial structure remains capital-intensive.

Why OpenAI’s Consumer Dominance Matters

ChatGPT stands as the most widely adopted artificial intelligence application globally. This market penetration provides OpenAI with consumer recognition that Anthropic cannot currently match.

OpenAI is expanding well beyond its flagship chatbot. The company is advancing into enterprise solutions, developer infrastructure, and platform-as-a-service offerings. This positions it as a diversified play on AI penetration across multiple industries.

The valuation presents the primary challenge. A $1 trillion market capitalization means investors would pay a substantial premium for anticipated expansion. This bet pays off if OpenAI maintains market leadership. The equation becomes problematic if rivals narrow the competitive gap.

Why Anthropic Emphasizes Enterprise Clients

Anthropic has pursued a more concentrated strategy. Its Claude language models have captured significant market share in corporate software, developer environments, and business process automation.

According to Reuters, Anthropic’s annualized revenue exceeded $30 billion, surpassing OpenAI’s previously reported $24 billion annual figure. While both companies measure revenue through different methodologies, the directional trend appears clear.

Anthropic completed a $65 billion funding round at approximately $965 billion pre-IPO valuation. This positions the company nearly on par with OpenAI in private market assessment.

Breakingviews analysis suggests Anthropic’s valuation translates to roughly 30x revenue. Depending on how OpenAI’s revenue run-rate is interpreted, this could position Anthropic as the less aggressively priced option at public debut.

Enterprise software companies typically command more predictable valuations than consumer-driven growth narratives. This dynamic favors Anthropic if its revenue composition remains stable.

Investors prioritizing entry valuation may view Anthropic as the more transparent opportunity. Its enterprise traction is demonstrable and its pricing may offer marginally better value relative to OpenAI’s anticipated debut price.

OpenAI represents the broader platform narrative with superior consumer penetration. Anthropic appears as the more conservative choice for investors emphasizing valuation discipline.

Both public offerings are anticipated to generate substantial investor demand upon market entry.

Although the landscape is quietly and slowly improving, the spot exchange-traded funds tracking bitcoin’s performance ended the week once again in the red.

Ethereum’s negative trend was also extended, as the funds behind the two largest cryptocurrencies haven’t seen a single week in the green in a month and a half.

Bitcoin ETFs in Red (Again)

Even Monday recorded substantial net outflows, with $64.09 million leaving the BTC ETFs. This was somewhat surprising since the cryptocurrency’s price actually rose past $67,000 on that date, fueled by optimism from the deal announced by US President Trump between his country and Iran.

The only day in the green was actually Tuesday, with investors inserting $10.06 million into the financial vehicles. However, the trend reversed once again on Wednesday and Thursday, with withdrawals of $82.16 million and $90.66 million, respectively.

With Friday being a non-trading day, the week ended with a total net outflow of $226.84 million, marking the sixth consecutive week in the red since the one that ended on May 15. The total cumulative net inflows have declined during this time by a whopping $5 billion.

Perhaps the only positive conclusion from this is that the total outflows have declined from $1.72 billion during the first week of June to $316 million and the aforementioned $226.84 million in the last two.

The other notable development in the past week on the ETF front, aside from BlackRock’s new product, came from Franklin Templeton. The financial behemoth filed for two ETFs that will invest in US stocks and buy BTC with the dividends from those stocks.

Equity Bitcoin DRIP: proposed ETFs will invest in US stocks but then broad index of stocks pay out dvds the ETF will buy btc with that money. Trying it w innovation stocks too. Interesting.. https://t.co/bDpWOqijKK

— Eric Balchunas (@EricBalchunas) June 19, 2026

ETH ETFs in Red, Too

The spot Ethereum ETFs also ended the week in red, thus seeing a similar 6-week outflow-dominated streak. They had two days in the green, with Monday being the first as $22.50 million entered the products amid the growing peace optimism at the time.

Another $9.59 million went into the funds on Tuesday, but the tides turned once again on Wednesday and Thursday. The total net outflows for those days were $29.37 million and $12.77 million, as the week closed with a negative $10.05 million.

The cumulative total net inflows for the ETH ETFs are down from $12.09 billion on May 8 to $11.18 billion on June 18.

The post Bitcoin ETFs in Red for 6 Weeks in a Row Amid Major Filings From Franklin Templeton appeared first on CryptoPotato.

Ethereum traded near $1,731 at press time, leaving the asset close to the same area it occupied in March 2021.

Summary

- Ethereum traded near $1,731 on crypto.news, with buyers still waiting for stronger daily confirmation.

- Ali Martinez sees $1,060 as a value zone before larger rebound targets emerge for ETH.

- Binance exchange outflows suggest some holders moved ETH away from spot selling venues recently again.

According to crypto.news market data, the token rose 0.48% over 24 hours, with a daily range between $1,708 and $1,742.

The current level keeps ETH in a wide debate. Some analysts see a base forming after months of weakness. Others say the chart still needs to defend deeper support before a larger rebound can develop. For now, buyers have slowed the decline, but they have not confirmed control.

Ethereum price stays close to its 2021 level

Ali Martinez pointed out that Ethereum traded around $1,700 in March 2021 and is near the same area today. He said a “$10,000 investment made five years ago would still be worth approximately $10,000 today.”

That view captures Ethereum’s long macro reset. ETH reached new highs after 2021 and later returned to the same zone after sharp drawdowns. The move does not mean the network stopped growing, but it shows that price has not held those gains over the full period.

“Despite five years of severe volatility, explosive bull runs, and deep bear-market liquidations, ETH has posted zero net gains from that baseline,” Martinez also said.

The comment reflects the main problem for ETH bulls. They need proof that the current zone is a base, not another pause before lower levels.

Ethereum’s current market cap still sits above $200 billion, so the asset remains one of crypto’s largest markets. Yet its weak long-term return from the 2021 baseline explains why traders now focus more on levels than narratives.

Ethereum analysts watch $1,060 support and $4,630 target

Martinez said $1,060 stands out as a value zone to watch if Ethereum fails to hold higher support. That level would mark a deeper correction and could become the area where long-term buyers test demand again.

The bullish path needs ETH to protect macro support and then recover lost resistance levels. Martinez said a successful defense could open the door to $2,850 and $4,630 in the short-to-mid term. The second target sits close to the prior all-time high area.

Michaël van de Poppe took a more constructive view. He said this could be “one of the best times to be buying ETH,” adding that investors may look back in five to ten years and wish they had bought more.

Those comments support the long-term accumulation case, but they do not remove near-term risk. ETH must first reclaim key resistance levels. A move above $1,825 would be an early sign of strength, while a clean push through $2,000 would give buyers a stronger setup.

MACD and RSI show early recovery

The short-term technical picture has improved, but it is not fully bullish. The MACD histogram is positive near 21.25, while the MACD line sits around -69.09 and above the signal line near -90.35.

That setup shows a bullish crossover and weaker bearish momentum. Still, both MACD lines remain below the zero line. This means Ethereum is showing an early recovery attempt rather than a confirmed trend reversal.

The RSI also shows a similar message. It sits near 40.45, above its moving average near 35.91. That means momentum has improved from weaker levels.

However, the RSI remains below the neutral 50 mark. Buyers have not taken full control yet. A move above 50 would show stronger demand, especially if it comes with rising volume and a close above nearby resistance.

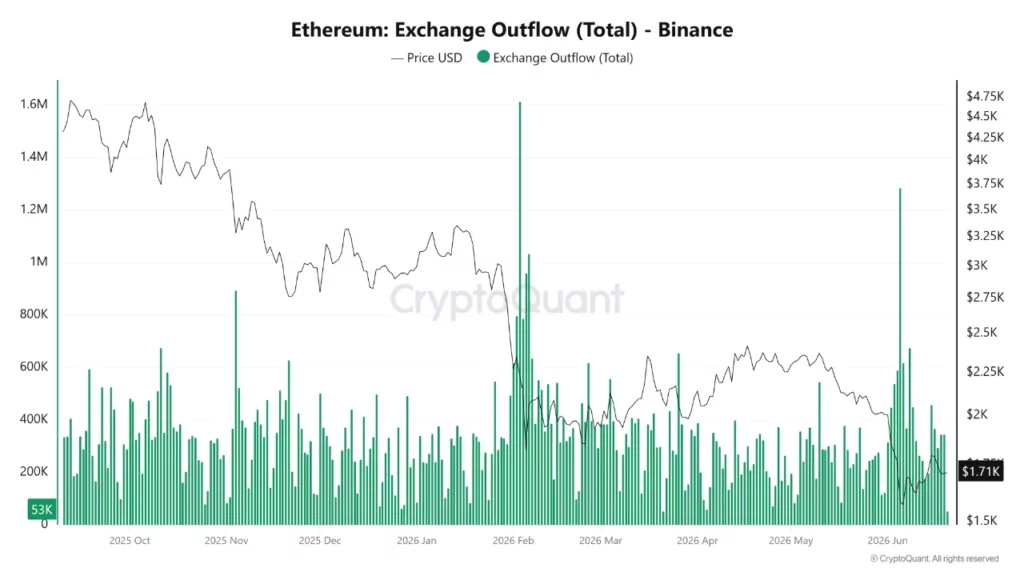

Binance outflows may ease selling pressure

CryptoQuant analyst Rei Researcher reported a spike in Ethereum exchange outflows from Binance in June 2026. The analyst said a large amount of ETH left the exchange while price traded around the $1.71K area.

Large outflows from exchanges can mean users are moving coins into cold wallets or staking. That can reduce spot sell pressure because fewer tokens remain available for immediate sale on exchanges.

This does not guarantee a price rally. Outflows can support the market only if demand also improves. If macro conditions weaken or Bitcoin loses support, ETH can still retest lower levels.

Recent crypto.news coverage also showed that ETH had already tested lower areas near $1,500 and $1,680 during earlier sell-offs. That history keeps traders cautious until price closes above resistance with stronger volume and broader market support.

For now, Ethereum is trading between early technical recovery and unresolved macro weakness. Bulls need to hold the $1,700 zone, reclaim $1,825, and then push toward $2,000. A failure to hold the range would bring $1,500, $1,300, and the $1,060 value zone back into focus.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

XRP price prediction is getting bullish as Ripple expands to Southeast Asia. Yet, the price hasn’t caught up to the story. A resurfaced SBI Remit announcement confirms live XRP-powered remittance infrastructure across Indonesia, the Philippines, and Vietnam, three of the highest-volume remittance markets on the planet.

Crypto researcher SMQKE posted documentation on X showing SBI Remit’s official announcement of an XRP-based international money transfer service covering all three markets, built through a collaboration between SBI Remit, SBI VC Trade, Ripple, and SBI Ripple Asia.

Ripple —

SBI Remit Indonesia

SBI Remit Indonesia  $XRP ODL Bridge Usage

$XRP ODL Bridge Usage  https://t.co/f7z4ShC4iO pic.twitter.com/T5diPRbmeN

https://t.co/f7z4ShC4iO pic.twitter.com/T5diPRbmeN

ChartNerd

ChartNerd  (@ChartNerdTA) June 17, 2026

(@ChartNerdTA) June 17, 2026

The timing is good as Indonesia’s Financial Services Authority (OJK) is actively developing a regulatory framework for real-world asset tokenization, which puts Ripple’s existing infrastructure in a strategically advantageous position.

— Indonesia Crypto Network (@idcryptonetwork) June 17, 2026

JUST IN: Indonesia's Financial Services Authority (OJK) Is Set to Release a Real World Asset Tokenization Regulation in Q3 2026. pic.twitter.com/ZuDQ5NhnF1

The service itself is designed to enable quick, low-cost, scalable cross-border bank account transfers using XRP’s architecture.

Discover: The Best Crypto to Diversify Your Portfolio

XRP Price Prediction: Break $1.50 Before Year-End?

XRP’s current price is in a $1.10–$1.25 consolidation range. Our analysts believe that XRP is in a projected grind toward $1.62 by the end of 2026, a 40% move from current levels. But this is assuming the narrative catalysts materialize into demand.

One of our analysts also cited the current spot price, with RSI attempting a reversal near 30, an oversold territory that historically precedes bounces but doesn’t guarantee them. Both VWAP and SMA20 sit above the current price, confirming the near-term bias remains to sell the rip until those averages are reclaimed.

Key resistance stacks up at $1.3 and $1.50, the levels to clear in sequence before any sustained upside becomes viable. Recent breakout attempts have already been rejected at resistance, which demands respect.

The Ripple Swell 2026 event represents another near-term catalyst that could shift the narrative, especially with Hollywood joining the case.

Discover: The Best Token Presales

LiquidChain Targets Early-Mover Upside as XRP Consolidates

XRP at here with end-year target offers just 40% upside “if the base case plays out” is respectable, but not the asymmetric setup active traders are typically hunting. That gap between fundamentals and price is exactly where early-stage infrastructure plays tend to attract capital rotation.

LiquidChain is a Layer 3 infrastructure project with a specific architectural bet: fusing Bitcoin, Ethereum, and Solana liquidity into a single execution environment, eliminating the fragmentation that kills capital efficiency across chains.

LiquidChain is always cooking something new.

This is what happens when a great idea meets innovation.pic.twitter.com/qYbth0impA

— LiquidChain (@getliquidchain) June 15, 2026

The Unified Liquidity Layer enables single-step cross-chain execution with verifiable settlement, so developers deploy once and access all three ecosystems. This is a genuine technical differentiator in a market where bridging friction still costs traders real money.

The presale is live at $0.01471 per $LIQUID, with $853,150.42 raised to date.

Research LiquidChain and assess the technical documentation before the presale ends.

The post XRP Price Prediction: Ripple Taps Indonesia, Philipines, and Vietnam Market appeared first on Cryptonews.

Dash is evaluating the Philippines as a potential destination for crypto payments, positioning the project’s technology as a way to reduce transaction costs in a market where users may be accustomed to high fees.

Speaking to Cointelegraph at Philippine Blockchain Week 2026, Daria Chernozub, global adoption lead at Dash Blockchain, said Dash is focusing on emerging markets that need simpler, lower-cost payment options and where people can adopt new financial tools more easily.

Key takeaways

- Dash says it is exploring the Philippines for crypto payments, citing demand for lower-cost transactions and easier-to-use payment tools.

- Dash’s team is still assessing local conditions and prioritizing legal compliance before pursuing any launch.

- Philippine Securities and Exchange Commission (SEC) officials describe corporate registration for foreign investors as fast via online processes, while crypto-specific compliance is expected to be more complex.

- Industry participants note that crypto firms entering regulated channels can face multi-year preparation and obligations.

Why Dash sees the Philippines as a fit for payments

Chernozub framed Dash’s approach around practical payment needs—especially in places where users encounter “high commissions” and want options that are straightforward to use. In her view, the Philippines aligns with that demand because consumers appear willing to learn about new technologies.

She also emphasized that Dash has not committed to a launch yet. Instead, the project is conducting an on-the-ground market assessment and treating compliance as a prerequisite for moving forward.

As part of its preparations, Chernozub said Dash has begun discussions with major local market participants and prepared a legal opinion letter intended to support conversations with relevant regulatory and financial industry bodies.

From quick corporate setup to tougher crypto compliance

At Philippine Blockchain Week 2026, Philippine SEC Commissioner Rogelio Quevedo told Cointelegraph that foreign investors can register a corporation online from anywhere in the world in approximately 20 to 30 minutes. He characterized this as part of the SEC’s broader digitization and innovation push.

Quevedo’s remarks point to a meaningful improvement at the corporate formation stage—setting up a local entity may now be far less time-consuming than it once was. However, the same process does not automatically translate into permission to operate in crypto markets. Crypto firms may still need additional approvals and licensing depending on what they plan to do.

That distinction matters for investors and operators because the “first gate” (legal presence) can be quick, while the “second gate” (sector-specific regulatory clearance) may still be slow and resource-intensive.

Earlier coverage from Cointelegraph on the Philippines’ regulatory posture has also highlighted how readiness varies by activity—whether the work is framed around tokenization, exchange activity, or other regulated functions. In Dash’s case, its stated focus is on payments, which typically means regulators will look closely at how value transfers are handled, how risks are managed, and what customer protections apply.

Regulated entry is possible—but timelines can be long

In a separate interview at the same event, Marie Antonette Quiogue, head of legal and CEO of Arden Consult, said the SEC has created a framework for foreign crypto exchanges to enter a regulated environment.

Still, Quiogue stressed that compliance comes with substantial obligations. She cited that BlockShoals spent roughly two years developing its arrangement with Binance, describing it as an example of how much work can be required to align with regulatory expectations.

For market participants, this “two-speed” reality—fast corporate registration on one hand and longer regulatory development on the other—helps explain why projects may take time even when the legal baseline is improving. It also suggests that investors should treat early regulatory engagement as a project-critical path rather than an afterthought.

What could attract foreign firms beyond regulation

Quiogue pointed beyond regulatory infrastructure, highlighting demographic and market characteristics that may make the Philippines attractive for foreign crypto-related businesses. She referenced the country’s young population, high mobile usage, and widespread English proficiency as factors that could support adoption.

For a payments-focused project like Dash, these elements can be especially relevant. Mobile-first behavior can reduce friction in payment experiences, while English proficiency can make onboarding and product communication easier across regions.

At the same time, adoption drivers do not eliminate compliance requirements. Even with strong user demand, Dash’s own comments indicate that it intends to proceed only after it completes legal groundwork and confirms how its proposed payment approach fits the local regulatory expectations.

Looking ahead

Dash’s next step will likely be less about announcing a market and more about clearing the compliance path it has already started discussing—particularly as the Philippines continues to modernize corporate processes while crypto oversight remains more demanding. Readers should watch for updates on Dash’s legal positioning and whether its payment model can align smoothly with Philippine regulatory expectations.

A preferred stock that was supposed to behave like a steady, high-yield bond fell to 82 cents on the dollar in a single session. The issuer says it was a leverage flush, not a credit problem. Either way, the new world of Bitcoin-backed “digital credit” just met its first stress test.

Summary

- STRC and SATA showed that Bitcoin-backed preferred stocks can trade violently under stress.

- Issuers blamed the selloff on forced deleveraging, not credit deterioration.

- The episode exposed thin liquidity, leverage, and Bitcoin volatility inside digital credit.

- High yields in these products compensate investors for risks that are now visible.

On June 18, 2026, a security that was designed to be boring did something deeply un-boring. STRC, the perpetual preferred stock issued by Michael Saylor’s company Strategy, the firm formerly known as MicroStrategy, fell to an intraday low of $82.50, far below the roughly $100 par value such an instrument is meant to trade near, before recovering to close around $88.59.

On the same day, a sister instrument called SATA, the preferred stock of a Bitcoin treasury company called Strive, tumbled from its $100 par into the low $90s. Strive’s chief executive, Matt Cole, called it “the most difficult day in the history of Digital Credit,” and was quick to insist that nothing was actually wrong.

No one had defaulted, no issuer’s fundamentals had deteriorated, and the damage was the result of a leverage-driven liquidation, a cascade of margin calls and forced selling, not a real credit event. Whether you believe that reassurance or not, something important happened: the new world of Bitcoin-backed “digital credit” met its first real stress test, and it wobbled.

This piece explains what STRC and SATA actually are and why they exist, what happened on that difficult Thursday and the leverage-liquidation explanation, why these instruments are more fragile than their steady-yield design suggests, what the episode reveals about the broader Bitcoin treasury model that Saylor pioneered and others have copied, and what it means for anyone watching this corner of the market.

The issuers’ reassurance may well be accurate, that this was a mechanical dislocation and not a sign of distress. But the episode is a window into a young, leveraged, thinly traded market built on top of Bitcoin’s volatility, and understanding its first stress test is understanding a risk that has been building quietly beneath the Bitcoin treasury boom.

What STRC and SATA actually are

To understand why the selloff matters, you have to understand these instruments, because they are a new kind of security and their design explains both their appeal and their fragility.

STRC and SATA are perpetual preferred stocks issued by Bitcoin treasury companies, and they sit at the intersection of two worlds: the steady, income-paying world of preferred equity and the volatile world of corporate Bitcoin accumulation. A perpetual preferred stock is a security that pays a fixed or variable dividend indefinitely, with no maturity date, and is meant to behave somewhat like a high-yield bond, trading near its par value and delivering a steady stream of income.

STRC, issued by Strategy, yields roughly 11.5% and pays dividends twice a month. SATA, issued by Strive, offers a variable yield of around 13% and pays dividends every business day, a remarkably frequent payout designed to make the instrument attractive to income-seeking investors.

Both are designed to trade near their $100 par and to throw off generous, regular income, which is why they appeal to investors hunting for yield.

Strategy has also moved STRC toward semi-monthly dividends, reinforcing the product’s pitch as a frequent-income instrument. The first record date for the new schedule is June 30.

The crucial detail is what backs them and what they fund. These preferred stocks are issued by companies whose core strategy is accumulating Bitcoin, and the capital raised by selling the preferred shares helps finance that Bitcoin accumulation.

This is corporate Bitcoin treasuries explained through a credit instrument rather than a normal stock filing. The company raises capital, links the balance sheet to Bitcoin, and then asks public-market investors to tolerate the volatility inside a familiar wrapper.

This is the model Strategy pioneered and that companies like Strive have adopted: raise money through instruments like preferred stock and convertible debt, use it to buy Bitcoin, and amplify Bitcoin exposure through this financial structure, what Strive’s leadership calls an “amplification” strategy. Strive, for instance, has built its structure around preferred equity as the primary form of this amplification, holding roughly 13,000 Bitcoin and maintaining a multi-month dividend reserve to ensure it can keep paying.

These instruments, in other words, are a way for Bitcoin treasury companies to raise capital from yield-seeking investors and channel it into Bitcoin, offering the investors a high income stream in exchange. They are the credit layer of the Bitcoin treasury world, a new market that links steady income products to volatile Bitcoin balance sheets, and that linkage is exactly where the fragility lives.

What happened on the difficult Thursday

The events of June 18 are worth walking through carefully, because the sequence reveals how a security meant to be stable can crater in a single session.

These instruments, which are supposed to trade near their $100 par, dropped sharply and suddenly. STRC fell to an intraday low of $82.50, a steep discount to par for an instrument designed to behave like a steady bond, before recovering to close near $88.59.

SATA fell from par into the low $90s, with one company executive noting it touched as low as $92.88 intraday before recovering toward $97.71. Both instruments, in other words, suffered sharp intraday plunges and then partially recovered, the kind of violent round trip that does not happen to a truly stable income security in normal conditions.

Selling came on heavy volume and cascaded through these thinly traded instruments, and it happened as the broader market was weak. Bitcoin itself slid around the same time toward roughly $62,900, and the United States was heading into a holiday weekend with no equity trading the following day.

Strive’s chief executive offered an explanation that same day, and it is important to take it seriously while also weighing it critically. Matt Cole attributed the plunge not to any deterioration in the creditworthiness of the issuers but to a leverage-driven liquidation.

In plain terms, some investors had bought these preferred shares using borrowed money, posting the shares as collateral, and when prices started to fall, those investors got margin calls. That forced them to sell, which pushed prices down further, triggering more margin calls in a cascade.

This is a mechanical dynamic, a leverage flush, not a fundamental one, and Cole stressed that the issuers’ balance sheets were intact, their dividend reserves full, and their ability to keep paying undisturbed. Strategy has also framed its reserve position as more than sufficient to support dividends over the long term.

Cole characterized the selloff as a temporary market dislocation, the most difficult day in the young history of digital credit, but not a sign of financial distress. The partial recovery of both instruments by the close lends some support to this reading, since a true credit event would not typically bounce back within the session.

The leverage-liquidation explanation is plausible and may well be correct. But as the next section argues, it is also not entirely reassuring.

Why these instruments are more fragile than they look

Here is the heart of the matter, because even if the leverage-liquidation explanation is accurate, the episode exposes a fragility built into these instruments that their steady-yield design obscures.

That reassurance, “it was just a leverage liquidation, not a credit problem,” is meant to calm investors, but it contains its own warning. Their ability to fall nearly 20% in a session on forced selling, regardless of the issuer’s fundamentals, is itself the risk.

An instrument designed to trade near par and behave like a steady bond should not be capable of a violent intraday plunge to $82.50. The fact that it is reveals that these securities are thinly traded and vulnerable to becoming magnets for exactly the kind of leverage that can flush them.

A market thin enough that a wave of margin-called selling can crater the price is a market where holders face real price risk even when nothing is wrong with the issuer. That is not the risk profile yield-seeking investors expect from a bond-like preferred.

That explanation, in other words, identifies the mechanism but does not eliminate the danger. It confirms that these instruments live in a market where mechanical forces can produce sudden, large losses.

A deeper fragility comes from what sits underneath these instruments: Bitcoin. These issuers are Bitcoin treasury companies whose balance sheets rise and fall with Bitcoin’s price, and although the preferred dividends are backed by reserves, the entire structure is ultimately tied to Bitcoin’s volatile value.

When Bitcoin falls, as it has substantially in 2026, the issuers’ balance sheets weaken, the broader sentiment around Bitcoin treasury strategies sours, and the appetite for their leveraged income instruments can fade. All of those pressures can hit the preferred shares at the same time.

This is the Bitcoin downturn behind the stress: a weaker Bitcoin market does not just affect the spot price, it tests every structure built on top of Bitcoin exposure.

They combine three sources of fragility at once: thin liquidity that amplifies any selling, leverage that can cascade into forced liquidations, and an underlying tie to Bitcoin’s volatility. A steady-yield preferred stock is supposed to be insulated from this kind of drama.

The design of STRC and SATA, perpetual preferreds throwing off generous regular income, presents them as stable, income-producing securities. The episode showed that beneath that steady surface lies a young, leveraged, Bitcoin-linked market that can move violently, and that is a fragility the high yields are, in part, compensation for.

What it reveals about the Bitcoin treasury model

The STRC and SATA episode is a window into something larger than two instruments: the Bitcoin treasury model itself, pioneered by Saylor’s Strategy and now widely copied, and the stresses building within it.

This model is, at its core, a leverage play on Bitcoin. Companies like Strategy raise capital through debt and preferred equity and use it to buy Bitcoin, amplifying their Bitcoin exposure so that the company’s value rises faster than Bitcoin when Bitcoin climbs.

Strategy’s goal has been to turn products like STRC into durable Bitcoin-backed credit instruments, not just temporary financing tools. That ambition is what makes the stress test matter: the market is now testing whether the instrument can behave like credit when Bitcoin behaves like Bitcoin.

The strategy made Strategy a market sensation during Bitcoin’s bull runs. Strategy now holds an enormous Bitcoin position, around 846,842 Bitcoin acquired at an average cost of roughly $75,656 per coin, which at a Bitcoin price near $62,500 represents a large unrealized loss, on the order of $11 billion.

That is the other side of leverage: it amplifies losses as well as gains. In 2026, with Bitcoin down sharply on the year, the amplification has been working in reverse, putting the model under a kind of pressure it did not face during the bull market.

The preferred instruments like STRC are part of how this leverage is financed, which is why stress in them is a signal about stress in the model.

The episode is best understood as the model meeting its first real test in a sustained Bitcoin downturn. During Bitcoin’s rises, the Bitcoin treasury strategy looked brilliant, and instruments like STRC and SATA could be issued readily to fund more Bitcoin buying, with investors happy to collect high yields backed by appreciating Bitcoin balance sheets.

A prolonged Bitcoin decline changes the picture: balance sheets show large unrealized losses, recent capital raises draw criticism as dilutive, sentiment sours, and the leveraged income instruments become vulnerable to exactly the kind of flush that hit them. This is also the macro pressure on leverage, because a hawkish rate environment makes every leveraged product harder to support.

Both companies insist their structures are conservatively leveraged or debt-light and their reserves intact, and that may be true, with Strategy and Strive both characterizing their balance sheets as sound. But the episode reveals that the whole edifice, the treasury companies and the digital-credit instruments built on top of them, is being tested by Bitcoin’s downturn in a way it never was during the boom.

The cracks in STRC and SATA are an early reading on how that test is going. The model worked beautifully on the way up; its behavior on the way down is now being discovered in real time.

The honest counterpoint

A fair account has to take the issuers’ reassurance seriously, because there is a real case that this episode was exactly what they say it was and not a sign of deeper trouble.

A bullish reading is that this was a real leverage flush, a mechanical dislocation in a thin market, and not a fundamental problem. On this view, the issuers’ balance sheets really are intact, their dividend reserves really are full, and their ability to keep paying really is undisturbed.

The sharp drop was a temporary technical event caused by overleveraged investors being forced out, not a judgment on the creditworthiness of Strategy or Strive. Partial recovery within the same session supports this, since a real credit deterioration would not typically bounce back so quickly.

The high yields these instruments pay, 11.5% on STRC and around 13% on SATA, are attractive precisely because they compensate for the volatility that episodes like this represent. Strive maintains a multi-month dividend reserve and has characterized its structure as built on long-duration preferred equity matched to the long-duration nature of Bitcoin.

That is an argument that the financing is sensibly structured, not recklessly leveraged. For an investor who believes in the Bitcoin treasury model and can tolerate volatility, a forced-selling dip might even look like an opportunity, not a warning.

A bearish reading does not dispute the mechanics but questions the comfort. Even granting that this was a leverage liquidation and not a credit event, the episode shows that these instruments can lose a fifth of their value in a session, that the market for them is thin enough to cascade, and that they are tied to a Bitcoin treasury model under real pressure from Bitcoin’s decline.

That reassurance, “nothing is fundamentally wrong,” sits uneasily next to the fact that a supposedly stable income security behaved like a volatile one. The worry is that in a young, leveraged, thinly traded market, the line between a mechanical flush and a fundamental problem can blur if Bitcoin keeps falling and the stress compounds.

Both readings have merit, and the honest position is that the issuers may be entirely right about this specific episode while the episode still reveals a fragility worth respecting. These instruments offer high yields for a reason, and that reason was on display on June 18, whatever the precise cause.

An investor should weigh the generous income against the proven capacity for sudden, sharp losses, and decide accordingly.

What it means for investors

For anyone watching or holding these instruments, or the Bitcoin treasury companies behind them, the episode offers concrete lessons regardless of which reading proves correct.

One lesson is that high-yield Bitcoin-linked preferred stocks are not the stable, bond-like income securities their design might suggest. Those generous yields, 11.5% and 13%, are compensation for real risks, including thin liquidity, leverage cascades, and an underlying tie to Bitcoin’s volatility.

An investor attracted by the income should understand that it comes with the proven possibility of sharp price drops. Treating these instruments as equivalent to a safe bond, because they are called preferred stock and pay steady dividends, misreads them.

They are a higher-risk, higher-yield instrument in a young and volatile market, and the June episode is the evidence. Anyone holding them for income should size the position to the reality that the price can move violently and that the market is thin, not to the comforting impression of a steady payout.

Another lesson is about the broader Bitcoin treasury exposure. The episode is a reminder that the Bitcoin treasury model is a leverage play that amplifies losses in a downturn as much as gains in a rally, and that the instruments financing it, and the companies issuing them, carry that amplified risk.

An investor exposed to this corner of the market, whether through the preferred instruments, the treasury companies’ shares, or the broader theme, should hold it understanding that it is leveraged Bitcoin exposure with extra layers of fragility, not a conservative income or equity position. That is why regulated Bitcoin exposure compared is important: a preferred stock tied to a Bitcoin treasury balance sheet is not the same risk as a spot ETF or a simple Bitcoin wrapper.

The broader product-design trend also matters. STRC and SATA are part of the same market impulse that produced another Bitcoin-financial-engineering product, but the risk profile is very different when leverage and dividend obligations sit inside the wrapper.

Watching Bitcoin’s price, the issuers’ balance sheets and dividend coverage, and the behavior of these instruments under stress gives a clearer read on the risk than the steady-yield marketing suggests. None of this is investment advice, and the issuers may be right that the specific episode was benign.

The prudent stance is to respect the fragility the episode revealed and to treat these instruments and the model behind them as the leveraged, volatile, Bitcoin-tied bets they fundamentally are.

A stress test, passed for now

STRC falling to $82.50 and SATA into the low $90s in a single session was, by the issuers’ account, a leverage flush rather than a credit event, and the partial recovery by the close lends that explanation real support.

The companies insist their balance sheets are intact, their reserves full, and their ability to pay undisturbed, and they may be entirely correct that this specific episode was a mechanical dislocation in a thin market and not a sign of distress. In that narrow sense, the Bitcoin dividend machine passed its first stress test: it shook, but it did not break.

But the episode revealed a fragility that the reassurance does not dissolve. Instruments designed to trade near par and behave like steady bonds showed they can lose nearly a fifth of their value in a session.

The market for them is thin enough to cascade under forced selling, and they sit on top of a Bitcoin treasury model now under real pressure from Bitcoin’s decline, with Strategy carrying billions in unrealized losses as leverage works in reverse. The high yields these instruments pay are compensation for exactly this kind of volatility, and June 18 was a vivid display of what that compensation is for.

An honest conclusion holds both truths at once: the issuers are probably right about this episode, and the episode still exposed a young, leveraged, Bitcoin-linked credit market that can move violently and that is being tested in a downturn for the first time. The machine kept running, but it was the first real test.

How it behaves through a sustained Bitcoin decline is a question now being answered in real time, one difficult Thursday at a time.

Frequently asked questions

What are STRC and SATA?

They are perpetual preferred stocks issued by Bitcoin treasury companies. STRC, issued by Michael Saylor’s Strategy, formerly MicroStrategy, yields roughly 11.5% and pays dividends twice a month. SATA, issued by Strive, offers a variable yield around 13% with daily dividend payments. Both are designed to trade near their $100 par and provide steady high income, and both help finance the issuers’ Bitcoin accumulation. They form a new “digital credit” layer linking income products to volatile Bitcoin balance sheets.

What happened to STRC and SATA on June 18, 2026?

Both fell sharply in a single session. STRC dropped to an intraday low of $82.50, well below its roughly $100 par, before recovering to about $88.59. SATA fell from par into the low $90s before partially recovering. Selling came on heavy volume and cascaded through these thinly traded instruments as Bitcoin slid toward roughly $62,900. Strive’s CEO called it “the most difficult day in the history of Digital Credit,” attributing it to forced selling, not a credit problem.

What does leverage liquidation, not a credit event, mean?

It means the plunge was caused by mechanical forced selling rather than any deterioration in the issuers’ creditworthiness. Some investors had bought the preferred shares with borrowed money, posting them as collateral; when prices fell, they got margin calls, forcing them to sell, which pushed prices down further and triggered more margin calls in a cascade. The issuers say their balance sheets and dividend reserves are intact. The partial same-session recovery supports this reading, since a true credit event would not typically bounce back so fast.

Why are these instruments considered fragile?

Even if June 18 was a leverage flush, the episode showed these instruments can lose nearly 20% in a session, which a truly stable bond-like security should not do. They combine three fragilities: thin liquidity that amplifies selling, leverage that can cascade into forced liquidations, and an underlying tie to Bitcoin’s volatility through the issuers’ balance sheets. The high yields they pay are compensation for exactly these risks, which their steady-income design tends to obscure.

What does this say about the Bitcoin treasury model?

The Bitcoin treasury model, pioneered by Strategy and copied by others, raises capital through debt and preferred equity to buy Bitcoin, amplifying exposure. That leverage amplifies losses as well as gains, and with Bitcoin down sharply in 2026, Strategy carries a large unrealized loss, around $11 billion on roughly 846,842 BTC bought near a $75,656 average. The STRC and SATA stress is an early sign of the whole model being tested in a sustained Bitcoin downturn for the first time, after looking brilliant during the boom.

Should investors treat these as safe income securities?

No. Despite being called preferred stock and paying steady dividends, they are higher-risk, higher-yield instruments in a young, leveraged, thinly traded market tied to Bitcoin’s volatility. The June episode showed they can drop sharply and suddenly. The 11.5% and 13% yields are compensation for that risk. Investors attracted by the income should size positions to the reality that prices can move violently, rather than to the impression of a stable payout. This is not investment advice.

As of June 21, 2026. Markets move quickly and figures change; verify current data before relying on this analysis. This article is information, not investment advice.

Dash is exploring the Philippines as a potential market for crypto payments, citing demand for lower-cost transactions and the country’s openness to digital finance tools.

In an interview with Cointelegraph at the Philippine Blockchain Week 2026, Daria Chernozub, global adoption lead at Dash Blockchain, said the project focuses on emerging markets where users face high fees and need simpler payment options.

“We believe that Dash brings the technology and the payment solutions for people who are suffering from high commissions [and] who need something easy to use,” Chernozub said, adding that the Philippines fits that profile because consumers are open to learning about new technologies.

She said Dash is still assessing the local market and prioritizing legal compliance before any launch. She said Dash had begun communicating with major market participants and had prepared a legal opinion letter for discussions with regulatory and financial industry bodies.

Dash’s assessment comes as the Philippines seeks to attract foreign technology companies, though industry participants say the regulatory process for crypto firms remains significantly more demanding than basic corporate registration.

Daria Chernozub (left) with Cointelegraph’s Ezra Reguerra (right) at the Philippine Blockchain Week. Source: Daria Chernozub

Corporate registration takes minutes, crypto compliance can take years

Philippine Securities and Exchange Commission Commissioner (SEC) Rogelio Quevedo told Cointelegraph during an interview at Philippine Blockchain Week 2026 that foreign investors can register a corporation online from anywhere in the world in about 20 to 30 minutes.

Quevedo said the government is ready to assist foreign investors and described the SEC’s online registration system as part of the agency’s broader push toward digitization and innovation. His comments suggest that formally setting up a local entity has become easier, though crypto companies may still face additional licensing and compliance requirements before operating.

Related: Dash Evolution chain integrates Zcash Orchard privacy pool

Marie Antonette Quiogue, BlockShoals’ head of legal and CEO of Arden Consult, said during a separate interview at the event that the SEC has created a framework for foreign crypto exchanges willing to enter a regulated environment.

Quiogue said the regulated path comes with significant obligations and cited the roughly two years BlockShoals spent developing its arrangement with Binance.

Beyond regulation, Quiogue pointed to the Philippines’ young population, high mobile usage and widespread English proficiency as factors that could attract overseas crypto companies.

Magazine: China’s 107 Bitcoin memory thief, Bithumb CEO booked: Asia Express

A Japanese corporate pension fund that serves roughly 1,200 small and medium-sized businesses plans to add cryptocurrency exposure to its portfolio starting fiscal year 2026, according to Nikkei. The proposal calls for allocating about 1% of the fund’s assets to crypto through a passive investment vehicle managed by a “major” hedge fund holding multiple crypto assets.

Nikkei reports the Nationwide Business Corporate Pension Fund oversees approximately 21.3 billion yen (around $130 million). CoinPost, in a separate report, said the pension fund is incorporating the allocation as part of its diversification effort, with a planned allocation split of 80% to yen, 15% to US dollars, and 5% to other currencies.

Key takeaways

- The Nationwide Business Corporate Pension Fund plans to dedicate roughly 1% of assets to cryptocurrency in fiscal year 2026.

- According to reports, the investment will be made via a passive fund managed by a hedge fund holding a basket of crypto assets.

- The move adds crypto exposure inside Japan’s more conservative institutional money pool, suggesting gradual mainstreaming.

- It comes as Japanese lawmakers advance legislation that would bring crypto assets under rules closer to those for traditional financial products.

- Investors should watch how the pension allocation is implemented, including whether it aligns with broader ETF and tax policy changes.

A cautious allocation inside Japan’s pension system

Crypto adoption among mainstream institutions typically proceeds in measured steps—especially in jurisdictions where pensions and other conservative vehicles are heavily regulated. In this case, the 1% target is small relative to the fund’s overall size, but the decision is significant because it places digital assets on the radar of an entity designed to meet long-term obligations for participating companies.

As described by Nikkei, the fund would not pick individual coins directly. Instead, it would use a passive fund managed by a hedge fund described as a “major” player, with holdings spanning multiple crypto assets. That structure could matter for implementation: passive vehicles can be easier to administer within institutional investment frameworks than bespoke strategies, even if underlying market exposure remains volatile.

CoinPost’s coverage, meanwhile, frames the decision as part of broader portfolio diversification rather than a standalone bet on crypto. With yen still projected to account for 80% of the fund’s exposure, the planned allocation suggests the pension fund is treating cryptocurrency as an incremental diversifier rather than a core allocation—at least for now.

Policy momentum: crypto moves closer to traditional market rules

The pension allocation aligns with a wider push in Japan to integrate digital assets more firmly into the country’s regulated financial ecosystem. On June 11, Japan’s House of Representatives passed legislation that would bring crypto assets under the Financial Instruments and Exchange Act, as coverage discussed by Cointelegraph noted. Under the proposal, crypto would fall under rules more closely aligned with those applied to conventional financial products.

The legislation is expected to move to the House of Councillors. If approved, it could open a pathway for crypto exchange-traded funds, while also strengthening the case for reforms that would lower the tax rate applied to digital-asset gains. The draft framework referenced in coverage includes a potential shift toward a 20% flat tax on gains from the current maximum rate of 55%.

For institutional investors, regulatory proximity can be as important as performance. When crypto assets sit outside the same legal and compliance environment as other financial products, long-term allocation decisions become harder—particularly for entities with strict governance and oversight requirements. A framework under the Financial Instruments and Exchange Act may reduce friction and help pension administrators justify allocations and risk controls.

Broader institutional access: experiments in retail and yield

Beyond pensions, Japan has seen other efforts aimed at making crypto exposure more accessible to investors in ways that fit established financial channels. Earlier this year, SBI Shinsei Bank began testing a deposit-linked rewards program that offers vouchers redeemable for Bitcoin, Ether, or XRP. The bank reportedly planned a permanent launch in autumn, highlighting a trend toward bundling crypto access with mainstream banking products.

In parallel, Metaplanet—described as Japan’s largest publicly listed Bitcoin holder—took steps to expand its financial toolkit. On June 12, Metaplanet agreed to acquire Siiibo Securities for 2.1 billion yen. The company said the deal would support the development and distribution of Bitcoin-linked yield products through a newly formed securities arm.

Together, these moves point to a gradual shift: crypto is no longer only an exchange and custody story. It’s increasingly being packaged into products and structures that resemble traditional finance—whether through rewards programs, yield-linked instruments, or, in this case, pension allocations.

What to watch next for pension-linked crypto

While the pension fund’s planned 1% allocation is modest, it could set an example for other conservative institutions if the implementation is smooth and governance concerns are addressed. The critical details investors will want to understand as fiscal year 2026 approaches include how the passive crypto fund is selected, what risk management and rebalancing policies apply, and whether the pension’s approach harmonizes with the evolving regulatory path in Japan.

More broadly, readers should monitor whether the legislation currently advancing through Japan’s political process translates into practical market infrastructure—such as regulated products that institutions can more easily deploy within their existing compliance frameworks.

Ethereum co-founder Joseph Lubin defended Vitalik Buterin after some community members questioned Buterin’s decision to write a science-fiction novel focused on decentralized governance.

Summary

- Joseph Lubin called Vitalik Buterin Ethereum’s key steward while defending his governance fiction project publicly.

- Crypto.news earlier reported Buterin paused regular essays to write science fiction about decentralized governance online.

- The debate comes as Ethereum faces price pressure and renewed questions over Foundation direction online.

Lubin called Buterin “an enormously effective communicator” and described him as “the most important contributor to and steward of the Ethereum ecosystem.” His comments came after online debate over whether the writing project helps Ethereum at a time when users are focused on price weakness, privacy and the Ethereum Foundation’s direction.

Lubin says fiction can serve Ethereum

Lubin argued that critics are missing the point if they think Buterin is stepping away from Ethereum by writing fiction. In his view, fiction can explain Ethereum’s values in a way that technical posts may not reach.

“Anyone who thinks that by writing fiction Vitalik isn’t choosing the most effective way he can think of to further the growth and adoption of Ethereum is missing the point,” Lubin wrote on X.

He suggested that Buterin could write a cypherpunk story showing how people move through a dark digital future while using Ethereum-related technology. Lubin compared the idea to works such as Cory Doctorow’s Little Brother series.

The post also tied Buterin’s writing to themes that already sit close to Ethereum’s culture, including open source, privacy, censorship resistance and credible neutrality.

Buterin’s novel focuses on governance

As previously reported by crypto.news, Buterin said in May that he would pause regular long-form blog posts and try writing science fiction about decentralized governance. He had already finished the first two chapters and posted them on his personal website.

The draft explores governance in a fictional setting rather than through a normal research essay. Reports said the story deals with topics such as quadratic voting, artificial intelligence-assisted decision-making and the limits of decentralized autonomous organizations.

The shift drew mixed reactions because Buterin’s technical essays have often guided public debate around Ethereum. Some users questioned the timing, while others said the novel could make complex governance ideas easier to understand.

A user posting as 12 said the early chapters already touch on open source and privacy. The user also pointed to the “Veridian Privacy Robe” and suggested the phrase “HOOD UP = Privacy” as a community signal.

Privacy themes gain attention

Privacy has become a recurring topic in Ethereum discussions. As crypto.news reported last year, Ethereum builders were working on privacy tools ahead of the network’s 10-year anniversary, and that Buterin had urged developers to focus on private money, private identity, private voting and private messaging.

That context helps explain why some community members see Buterin’s fiction as more than a side project. A story can test social and political ideas without proposing immediate protocol changes.

Lubin also framed Ethereum as a platform built around neutral settlement, open source work and censorship resistance. His defense suggests that he sees Buterin’s writing as part of Ethereum’s wider communication strategy.

The debate is likely to continue while ETH price action remains weak and users ask for clearer progress. For now, Buterin’s novel has moved Ethereum’s governance and privacy debate into a new format, while Lubin has publicly backed that choice. The project does not change Ethereum’s technical roadmap, but it has made Buterin’s public role a fresh topic for debate.

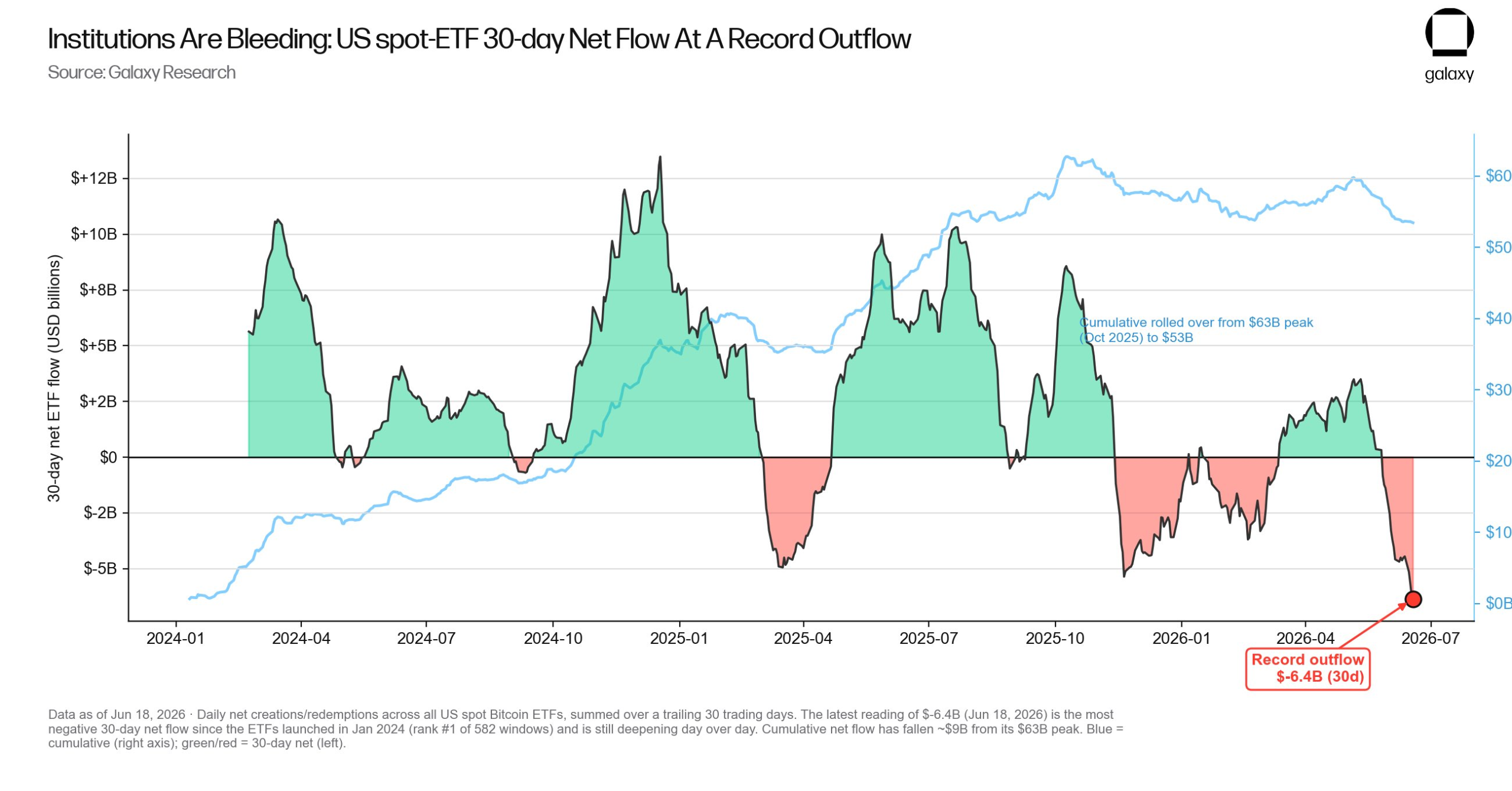

US spot Bitcoin ETFs (exchange-traded funds) posted their largest 30-day net outflow on record. These Bitcoin ETF outflows reached $6.35 billion as institutional investors cut exposure, according to Galaxy Research.

The redemption marks six straight weeks of withdrawals from the funds. Still, the pace has slowed sharply in recent days. That hints that the most intense phase of institutional selling may be passing.

Record Bitcoin ETF Outflow Tops 582 Windows

Galaxy Research said the $6.35 billion drain ranks first across all 582 rolling 30-day windows it tracks. The analysis arm of Galaxy Digital called it the heaviest stretch since the funds launched in January 2024.

“Bitcoin ETFs set record 30d net outflow at -$6.35 billion over last 30 days (#1 across all 582 30d windows),” they wrote.

The selling has been uneven across the complex. BlackRock’s IBIT has still pulled in $62.1 billion since launch, while Grayscale’s higher-fee GBTC has shed $27 billion.

Together, the funds hold net inflows of $53.4 billion, Farside Investors data shows.

The drawdown tracked a falling market. Bitcoin (BTC) has dropped about 17% over the past month. The token’s spot price near $64,260 sits roughly 49% below the record $126,080 reached on October 6, 2025.

Why Institutions Pulled Back From Bitcoin

Several forces drove the deepening ETF drain. Higher Treasury yields and fading hopes for rate cuts pushed money toward lower-risk assets.

Renewed geopolitical tension and a broad risk-off mood deepened the retreat.

Part of the bleed is structural, not fresh panic. GBTC has been leaking money for months because it charges 1.5% compared to IBIT’s 0.25%.

Other consecutive daily outflows reflected profit-taking and capital leaving Bitcoin for rival assets.

BlackRock’s IBIT still drives the daily swings. On June 18, its $96.7 million redemption outweighed the combined rest of the complex.

Investors had trimmed exposure ahead of the Fed’s interest rate decisions.

Outflows Cool as the Selling Slows

The bleeding has eased in recent sessions. Weekly outflows fell 87% from their early-June peak. They dropped from $1.72 billion in the week ending June 5 to about $226 million last week, according to Farside Investors data.

Bitcoin has held near $64,000 throughout the slowdown. The resilience suggests that long-term holders absorbed much of the supply released by ETF managers.

The sharp drop in weekly redemptions suggests the peak of selling has passed.

Still, outflows remain net negative, and only a swing back to inflows would confirm a bottom.

The post Bitcoin ETF Outflows Hit Record $6.35 Billion: Has Selling Peaked? appeared first on BeInCrypto.

MainStreet Finance-linked MSUSD traded far below its intended dollar peg after a rapid sell-off tied to reserve-verification concerns.

Summary

- MSUSD traded near $0.378 on CoinGecko after falling far below its intended dollar peg.

- PeckShield said the Morpho msY/USDC market reached 100% utilization as liquidity concerns spread quickly online.

- MainStreet said assets remain fully backed, citing a third-party proof-of-reserves dashboard shutdown as cause publicly.

Main Street USD traded at $0.3781 at the time of writing, with a 24-hour range between $0.065 and $0.9995.

The move followed Accountable’s decision to end its service agreement with MainStreet. The verification firm said MainStreet was “unable to meet our verification standards,” while MainStreet said the issue came from the shutdown of a third-party proof-of-reserves dashboard.

MSUSD trades far below its peg

MSUSD had been designed to trade near $1, but the token fell sharply after confidence in its reserve verification weakened. PeckShield said the MainStreet-related token dropped as much as 85%, while CoinGecko data later showed a partial rebound from the day’s low.

CoinGecko listed MSUSD with a market cap of about $27.06 million and 24-hour trading volume near $8.25 million. The token’s wide daily range showed unstable trading as holders tested liquidity and redemption confidence.

Morpho market reaches 100% utilization

The pressure also reached Morpho. According to PeckShield, the msY/USDC market hit 100% utilization, meaning available lending liquidity had been fully used.

AlphaUSDC Delta V2, curated by AlphaPING, reportedly had about 30% exposure to the market, equal to roughly $18 million. That exposure drew attention because stress in one yield-linked market can affect lenders, vault depositors and borrowers using related positions.

In lending markets, full utilization can make withdrawals harder and push borrowing rates higher. It can also leave users waiting for repayments or new deposits before liquidity normalizes.

The issue does not prove that all related positions are impaired. It does show that a stablecoin depeg can quickly move from a token price problem into a wider DeFi liquidity problem.

Accountable exit drives reserve concerns

Accountable said it terminated the MainStreet service agreement immediately after the protocol failed to meet its standards. The statement removed a public verification layer that users had relied on to assess backing.

MainStreet responded by saying that “Mainstreet remains fully backed.” The protocol also said the dashboard shutdown “does not reflect any loss of assets or deterioration in portfolio quality.”

MainStreet said it had deployed more than $8 million in USDC to support liquidity. It also said it was seeking alternative proof-of-reserves providers.

The two statements leave users with competing public claims. Accountable said the protocol failed verification standards, while MainStreet said the assets remain backed and the problem sits with the verification feed.

Stablecoin risks return to focus

The MSUSD case adds to a broader debate around yield-bearing stablecoins and proof-of-reserves tools. Crypto.news recently explained that a stablecoin’s reliability depends on the quality and transparency of the assets backing it.

The case also echoes earlier DeFi stress events where stablecoin-linked assets lost their peg and affected connected lending markets. Crypto.news previously reported on Resolv Labs’ USR depeg and exploit losses, noting how composable stablecoins can spread risk across protocols.

For now, MSUSD’s recovery depends on whether MainStreet can restore trust in its backing, keep liquidity available and replace the verification layer. Until then, traders are likely to watch the peg, Morpho utilization and any new proof-of-reserves update. Users may also watch whether liquidity support narrows the gap between MSUSD’s market price and its intended $1 value.

World Cup 2026: The same but different – the beauty of the first World Cup with your child

FDIS: Consumer Discretionary Dashboard For June

Sharon Osbourne Misses Ozzy Tribute Due to Hospitalization

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Blockchain.com files with SEC for U.S. IPO

Israel says it has killed new Hamas military leader in Gaza City airstrikes

Marriage Money: Can He Support You? Gen Z Speaks Outlines Financial Needs #shorts

Is AI Killing Bitcoin? The Brutal Truth Behind the Crash!

What is Accounting & What is Finance? Simple Explanation #Accounting #Finance #Education #CareerTips

-

Business7 days ago

Business7 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Miami – Corporette.com

-

Crypto World7 days ago

Zimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Business1 day ago

Business1 day agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Entertainment7 days ago

Entertainment7 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Crypto World1 day ago

Crypto World1 day agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Tech7 days ago

Tech7 days agoAs AI companies race to go public, who else is along for the ride?

-

Business7 days ago

Business7 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Crypto World7 days ago

Crypto World7 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

NewsBeat7 days ago

NewsBeat7 days agowhat doctors are seeing in ebike crashes

-

NewsBeat7 days ago

NewsBeat7 days agoWarning of disruption as Cardiff Crossrail works to start

-

NewsBeat7 days ago

NewsBeat7 days agoTributes to former deputy head teacher at Cambridge school among death and funeral notices

-

Entertainment7 days ago

Entertainment7 days agoKate Middleton Glare Goes Viral After Kids Booed At Royal Event

-

Politics7 days ago

Politics7 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

Crypto World7 days ago

Crypto World7 days agoXRP ETFs Outperform As Bitcoin And Ethereum Funds Extend Outflow Trend

-

Tech7 days ago

Tech7 days agoOver 400 Arch Linux packages compromised to push rootkit, infostealer

-

News Videos7 days ago

News Videos7 days agoFinancial Accounting | Last Day Revision Strategy and Booster | CMA Inter – June 2026

-

Business7 days ago

Business7 days agoInvesco Quality Income Fund Q1 2026 Commentary

-

NewsBeat7 days ago

NewsBeat7 days agoSinger Oliver Tree dies aged 32 in helicopter crash in Brazil

-

Sports7 days ago

Sports7 days agoDick Advocaat’s Curacao scores first-ever World Cup goal against Germany

You must be logged in to post a comment Login