Crypto World

What is MEV? Maximal Extractable Value, the invisible tax on crypto

Every time you trade on-chain, an invisible competition decides the order of transactions in the next block, and whoever controls that order can extract value from yours. That is MEV. It funds a hidden industry, quietly taxes ordinary users, and shapes the design of every modern blockchain.

Summary

- MEV lets block producers profit by controlling transaction order, creating opportunities such as arbitrage, liquidations, and sandwich attacks.

- Flashbots and MEV Boost transformed MEV into a structured marketplace, allowing validators to earn rewards without directly extracting value themselves.

- Private transaction routes and MEV aware trading platforms can help users reduce exposure to predatory forms of MEV and improve trade execution.

MEV, which stands for maximal extractable value, is the profit that can be captured by whoever controls the ordering of transactions within a block on a blockchain. Because the entity that builds a block can choose which transactions to include, exclude, and in what order, that power can be turned into money by slotting a profitable trade ahead of yours, squeezing a transaction between two others, or grabbing an arbitrage the moment it appears.

The term was originally “miner extractable value,” coined when miners ordered blocks, and it became “maximal extractable value” after Ethereum moved to validators, but the idea is the same: transaction ordering is valuable, and that value gets extracted. MEV is often called crypto’s invisible tax, because most users never see it even as they pay for it through worse prices and higher fees.

This guide explains MEV in plain English, with no technical background assumed. It covers what MEV actually is, why it exists at all, the main forms it takes from harmless arbitrage to predatory sandwich attacks, the hidden supply chain of searchers, builders, and validators that has grown up around it, the Flashbots infrastructure that reshaped how MEV works, the difference between MEV that helps markets and MEV that harms users, and the tools that ordinary people and protocols now use to fight back.

By the end, you will understand why MEV is a permanent feature of any public blockchain, why billions of dollars have flowed through it, and why the battle is not to eliminate it but to control who captures it and how.

What MEV actually is

At its core, MEV comes from a simple fact about blockchains: transactions do not settle the instant you send them. They wait, and someone decides the order in which they are processed, and that someone can profit from the decision.

When you submit a transaction, a swap on a decentralized exchange, a loan repayment, a token purchase, it does not go straight into the permanent record. It enters a waiting area, and eventually a block producer gathers a batch of pending transactions, arranges them in an order, and adds them to the chain as a block. Here is the key: the block producer has discretion over that order.

They can put your transaction first or last, include it or leave it out, and slip their own transactions, or transactions from others who pay them, into any position they like. Whenever the order of transactions affects how much money can be made, that potential profit is MEV, and the people who chase it design their actions specifically to win the ordering game.

The clearest way to grasp it is by analogy. In traditional stock markets, a broker who can see your large order coming and trade ahead of it is front-running, which is illegal. On a public blockchain, your pending transaction is visible to everyone, and reordering it for profit is not against any law, it is just how the system works, so the same behavior that is banned in regulated markets is an open, competitive industry on-chain.

One researcher famously called the public mempool a “dark forest,” a place where any transaction you broadcast can be hunted by predators watching for prey. MEV is the value those predators, and also some entirely useful actors, extract from the simple power to order transactions.

Why MEV exists: the mempool and ordering

To understand why MEV is unavoidable, you have to look at the waiting room where transactions sit before they are confirmed, because that is where the whole game is played.

On a chain like Ethereum, a transaction you broadcast lands first in the mempool, a public, shared pool of pending transactions that have not yet been included in a block. The mempool is visible to anyone running a node, which means that for a brief window your intended trade is public knowledge before it is final.

Specialized bots watch this pool constantly, scanning every pending transaction for opportunities, and when they spot one, they craft their own transactions designed to profit from the order in which everything will be processed. They then compete, often by bidding higher fees, to have their transactions placed in exactly the right position relative to yours.

This is why MEV is intrinsic to public blockchains rather than a bug to be patched away. As long as there is a gap between sending a transaction and finalizing it, as long as that pending transaction is visible, and as long as someone has the power to order the block, the opportunity to extract value from ordering will exist.

The mechanics differ by network: Ethereum has a public mempool that makes pending transactions visible, Solana has no mempool in the Ethereum sense and routes transactions straight to validators, and Layer 2 networks often use a single sequencer that orders transactions first come first served.

But the underlying dynamic, that whoever controls ordering can extract value, follows the structure of how blockchains reach agreement, which is why researchers describe MEV as a permanent feature of the technology rather than a temporary flaw.

The main forms of MEV

MEV is not one behavior but a family of them, and they range from useful to openly predatory. Sorting them out is the difference between fearing MEV and understanding it.

Arbitrage is the most common and the least controversial. When the same asset trades at slightly different prices on two decentralized exchanges, a bot can buy on the cheaper one and sell on the dearer one in the same block, pocketing the difference. This is MEV, but it is widely seen as neutral or even helpful, because it pushes prices on different venues back into line and makes markets more efficient.

Liquidations are similar. In lending protocols, when a borrower’s collateral falls below the required threshold, their position becomes eligible to be liquidated, and bots compete to be the one that repays the loan and claims the collateral at a discount. This too is generally seen as beneficial, because prompt liquidations keep lending protocols solvent and protect lenders. These two forms are sometimes called “good” MEV, since the extraction performs a function the system actually needs.

Then there is the predatory end. The most notorious form is the sandwich attack, where a bot spots your large pending swap, buys the asset just before you to push the price up, lets your trade execute at that worse price, and then sells immediately after for a profit, leaving you with a worse rate than you would have gotten.

Your transaction is the filling, squeezed between the bot’s buy and sell. Front-running more broadly means jumping ahead of a known transaction to profit from it, and back-running means slipping in immediately after a transaction to capture an opportunity it created.

These forms extract value directly from ordinary users, worsening their prices and inflating fees, which is why this is the MEV that earns the “invisible tax” label. The same power to order transactions enables both the helpful arbitrage that keeps markets efficient and the harmful sandwich that quietly skims from regular traders, which is exactly why MEV is so hard to simply ban.

The MEV supply chain: searchers, builders, validators

What began as lone bots has matured into a structured, multi-party industry, and knowing the roles makes the whole system legible.

At the front are searchers, the operators who run sophisticated bots scanning the mempool and the chain for profitable opportunities, arbitrage, liquidations, sandwiches, and who construct bundles of transactions designed to capture that value. Searchers are the prospectors, finding the gold.

They do not usually build blocks themselves; instead, they hand their bundles, along with a fee they are willing to pay, to builders. Builders are specialists who assemble complete, profit-maximizing blocks out of the transactions and bundles they receive, competing to construct the single most valuable block possible.

They are the ones who actually solve the ordering puzzle at scale. Finally, the assembled block goes to a validator, the participant chosen by the network to propose the next block. The validator does not need to do the complex work of finding and arranging MEV; it simply selects the most valuable block offered to it and proposes it, collecting a share of the value as reward.

This division of labor, searchers find, builders assemble, validators propose, is the modern structure of MEV, and it exists because separating these roles turned out to be more efficient and, importantly, fairer than the alternative where every validator had to extract MEV themselves. That separation is not an accident. It was deliberately engineered, and the system that engineered it is the most important piece of MEV infrastructure in existence.

Flashbots, MEV-Boost, and proposer-builder separation

The story of how MEV went from a chaotic free-for-all to an organized market is largely the story of one organization, Flashbots, and the infrastructure it built.

In the early days, MEV extraction was destructive in a way that threatened the whole network. Searchers competing for the same opportunity would wage “gas wars,” bidding transaction fees up by ten or twenty times to win the ordering race, which spiked costs for every ordinary user and clogged the chain with failed attempts.

Worse, the competition risked pushing power toward whoever could extract MEV most aggressively, threatening to centralize the network. Flashbots, a research organization, set out to defang this by moving the MEV competition off the public chain and into a private, orderly auction, so searchers could bid for transaction ordering without flooding the network with gas wars.

The centerpiece is the architecture known as proposer-builder separation, or PBS, implemented through software called MEV-Boost. PBS splits the job of proposing a block from the job of building it, exactly the searcher-builder-validator structure described above. A validator running MEV-Boost does not build its own block; it connects to a marketplace of competing builders, receives their best offers through intermediaries called relays, and simply chooses the most valuable one to propose.

This lets even a small, solo validator earn a fair share of MEV without the technical sophistication to extract it, which keeps validating accessible and the network more decentralized. Adoption has been overwhelming, with well over ninety percent of Ethereum validators running MEV-Boost, because outsourcing block construction to specialists pays better than building blocks themselves.

The tradeoff is concentration: a handful of builders and relays now route the large majority of blocks, which is its own centralization worry, and it is why the Ethereum community is working to move PBS directly into the protocol itself, an upgrade often called enshrined PBS, as a priority for 2026. Flashbots also pursued more ambitious redesigns, and while some of those research efforts were wound down, the core insight, turn MEV into a transparent, competitive market instead of a destructive scramble, has stuck.

Good MEV, bad MEV, and the invisible tax

It is tempting to treat MEV as simply theft, but the honest picture is more divided, and the division is exactly why the problem is hard.

Some MEV is genuinely useful. Arbitrage keeps prices consistent across exchanges, and liquidations keep lending markets solvent, and both of these are services the decentralized economy needs someone to perform. The searchers who do this work are, in a sense, paid for keeping the system efficient.

The amounts are not trivial: cumulative MEV across chains crossed one billion dollars by 2025, and Flashbots’ tracking found well over six hundred thousand ether of MEV extracted on Ethereum over the years it measured, a reminder that this is real money, not a theoretical edge.

But a meaningful slice of MEV is extracted directly from ordinary users at their expense, and that is the invisible tax. When a sandwich bot worsens your swap price, the difference comes straight out of your pocket, and you may never realize it happened, because the trade still went through, just at a worse rate than it should have. Multiply that across millions of transactions and the cost to regular users is substantial.

The encouraging news is that the harm is shrinking where protection has taken hold. Data from MEV researchers shows the monthly value extracted from sandwich attacks on Ethereum fell sharply through 2024 and 2025, from roughly ten million dollars a month to a fraction of that, as more transactions moved through protected routes.

The picture, then, is not “MEV is theft” but something more nuanced: MEV is the price of having open, ordered, permissionless blockchains, part of it pays for useful work, part of it is skimmed from users, and the entire industry’s effort is now bent toward shifting the balance away from the skimming.

How users and protocols fight back

You are not helpless against MEV, and one of the most useful things a guide can do is explain the practical defenses, because they have become remarkably effective.

The first line of defense is to keep your transaction out of the public mempool entirely. Private transaction services, often called private RPCs, send your transaction directly to builders instead of broadcasting it to the public pool, so the predatory bots never see it coming.

Flashbots Protect is a widely used free option that does exactly this, hiding your transaction and even returning some recovered value, and switching to it is usually a one-line change in your wallet settings; it has shielded tens of billions of dollars of trading volume across millions of accounts.

MEV Blocker, built by the team behind CoW Protocol, is another private route that goes further by running a searcher auction and paying a large share of any recovered value back to you as a rebate, and it too has protected tens of billions in volume.

A second approach is to trade on venues designed to neutralize MEV structurally. CoW Swap settles trades in batches at a single uniform clearing price, so that everyone in a batch gets the same rate regardless of ordering, which removes the front-running advantage by design, and aggregators such as UniswapX use auction mechanisms with a similar protective effect. A third, emerging idea is to flip the model entirely, with systems that capture the MEV your transaction creates and rebate it back to you, turning the invisible tax into a refund.

The networks themselves also shape your exposure. On many Layer 2 networks, a single sequencer currently orders transactions first come first served with no public mempool, which sharply reduces sandwich risk today, though it concentrates ordering power in one operator and that protection will change as those networks decentralize their sequencing. On Solana, the lack of a traditional mempool changes the dynamics, but MEV still exists through validator-level bundle systems.

The practical takeaway for a regular user is concrete: route your important trades through a private RPC like Flashbots Protect or MEV Blocker, prefer MEV-aware venues for large swaps, and you remove yourself from the dark forest for almost no effort and no cost.

A sandwich attack, step by step

The most infamous form of MEV becomes far less abstract when you watch it happen to a single trade, so follow one swap through a sandwich, because it shows exactly how the invisible tax is collected.

You want to swap ten thousand dollars of a stablecoin for a mid-sized token on a decentralized exchange. You set your trade and broadcast it, and for a brief moment it sits in the public mempool, visible to anyone watching, waiting to be included in the next block. A searcher’s bot, scanning the pool constantly, sees your pending swap and recognizes that a trade your size will push the token’s price up on that exchange’s liquidity pool. It has found its prey.

The bot acts in three moves, all landing in the same block, all arranged by the ordering it pays to control. First, the front-run: the bot buys the same token just before your transaction, nudging the price up. Second, your trade executes, but now at the higher price the bot just created, so you receive fewer tokens than you would have, paying more than the rate you saw when you clicked.

Third, the back-run: immediately after your trade pushes the price up further, the bot sells the tokens it bought a moment earlier, cashing out at the elevated price your own swap helped produce. The bot is the bread on both sides, your trade is the filling, and the profit it skimmed came directly out of your execution. You still got your tokens, the transaction succeeded, and you may never realize anything was taken, which is precisely why it is called an invisible tax.

Now notice how the defenses described earlier would have stopped it. Had you routed the swap through a private transaction service like Flashbots Protect or MEV Blocker, your trade would never have entered the public mempool, so the bot would never have seen it coming, and the sandwich would have been impossible.

Had you traded on a batch-auction venue like CoW Swap, everyone in your batch would have settled at one uniform price, removing the ordering advantage the bot relied on. One swap shows both the attack and the cure, and it explains why the simple habit of keeping important trades out of the public mempool is the single most effective thing an ordinary user can do.

Why MEV is permanent, and why that is not the end of the story

The honest conclusion is that MEV will never be fully eliminated, because the underlying source, the value of controlling transaction ordering, is woven into how blockchains reach agreement. Any system where transactions are ordered, and where that order affects who profits, will have MEV. Pretending otherwise is a fantasy, and the most serious people working on the problem say so plainly.

But permanence is not defeat, because the real question was never whether MEV exists. It is who captures it, how transparently, and at whose expense. On that question, the progress has been substantial. A destructive free-for-all of gas wars became an orderly, mostly private auction. Predatory sandwich extraction has fallen as protection spread. Solo validators can earn a fair share of MEV without being extraction experts. Ordinary users can shield their trades with a single setting, and new designs are starting to rebate MEV back to the people who generate it.

The trajectory is from opaque and extractive toward transparent and redistributive, and the protocols are working to pull the whole auction into the base layer where it can be made fairer still. MEV is the hidden machinery beneath every on-chain trade, and understanding it changes how you transact, because once you can see the dark forest, you can choose to walk around it.

Frequently Asked Questions

What is MEV in simple terms?

MEV, or maximal extractable value, is the profit that can be made by whoever decides the order of transactions in a block on a blockchain. Because a block producer can choose which transactions to include and in what order, that power can be turned into money, for example by placing a profitable trade ahead of yours or squeezing a transaction between two others. It used to stand for “miner extractable value” but became “maximal extractable value” after Ethereum switched from miners to validators. MEV is often called crypto’s invisible tax because users pay for it without seeing it.

Why does MEV exist?

MEV exists because transactions do not settle instantly. After you send a transaction, it waits in a public pool called the mempool before a block producer orders it into a block, and during that window your intended trade is visible. Bots scan the mempool for opportunities and compete to have their own transactions placed in profitable positions relative to yours. As long as there is a gap between sending and finalizing a transaction, and someone controls the ordering, the chance to extract value from that ordering will exist, which is why MEV is intrinsic to public blockchains.

What is a sandwich attack?

A sandwich attack is a predatory form of MEV. A bot spots your large pending swap, buys the asset just before you to push the price up, lets your trade execute at that worse price, then sells right after for a profit. Your transaction is the filling squeezed between the bot’s buy and sell, and you end up with a worse rate than you should have gotten. It is one of the main reasons MEV is called an invisible tax, because the trade still goes through and most users never notice the value taken from them.

What are Flashbots and MEV-Boost?

Flashbots is a research organization that reshaped how MEV works by moving the competition for transaction ordering off the public chain into an orderly auction, ending the destructive gas wars of the early days. Its key software, MEV-Boost, implements proposer-builder separation, which splits the job of proposing a block from building it. A validator running MEV-Boost simply chooses the most valuable block offered by competing builders, so even small validators earn a fair share of MEV. Well over ninety percent of Ethereum validators run it.

How can I protect myself from MEV?

The simplest defense is to keep your transaction out of the public mempool by using a private transaction service, or private RPC, such as Flashbots Protect or MEV Blocker, which send your trade directly to builders so predatory bots never see it. Switching is usually a one-line change in your wallet, and MEV Blocker even rebates recovered value to you. You can also trade large swaps on MEV-aware venues like CoW Swap, which settles trades in batches at a uniform price that removes the front-running advantage by design.

Can MEV be eliminated?

No, not fully. MEV comes from the value of controlling transaction ordering, which is built into how blockchains reach agreement, so any system that orders transactions will have some MEV. The realistic goal is not elimination but control: making the extraction transparent, reducing the predatory kind that harms users, and redistributing the value more fairly. Progress has been real, with sandwich attacks falling, protection tools spreading, and new designs that rebate MEV back to the users who create it, and the networks are working to make the underlying auction fairer still.

This article is educational and does not constitute financial or investment advice. The MEV landscape, including infrastructure, protective tools, and extracted-value figures, changes quickly and varies by data source. As of June 22, 2026, verify current details with official sources before relying on anything described here.

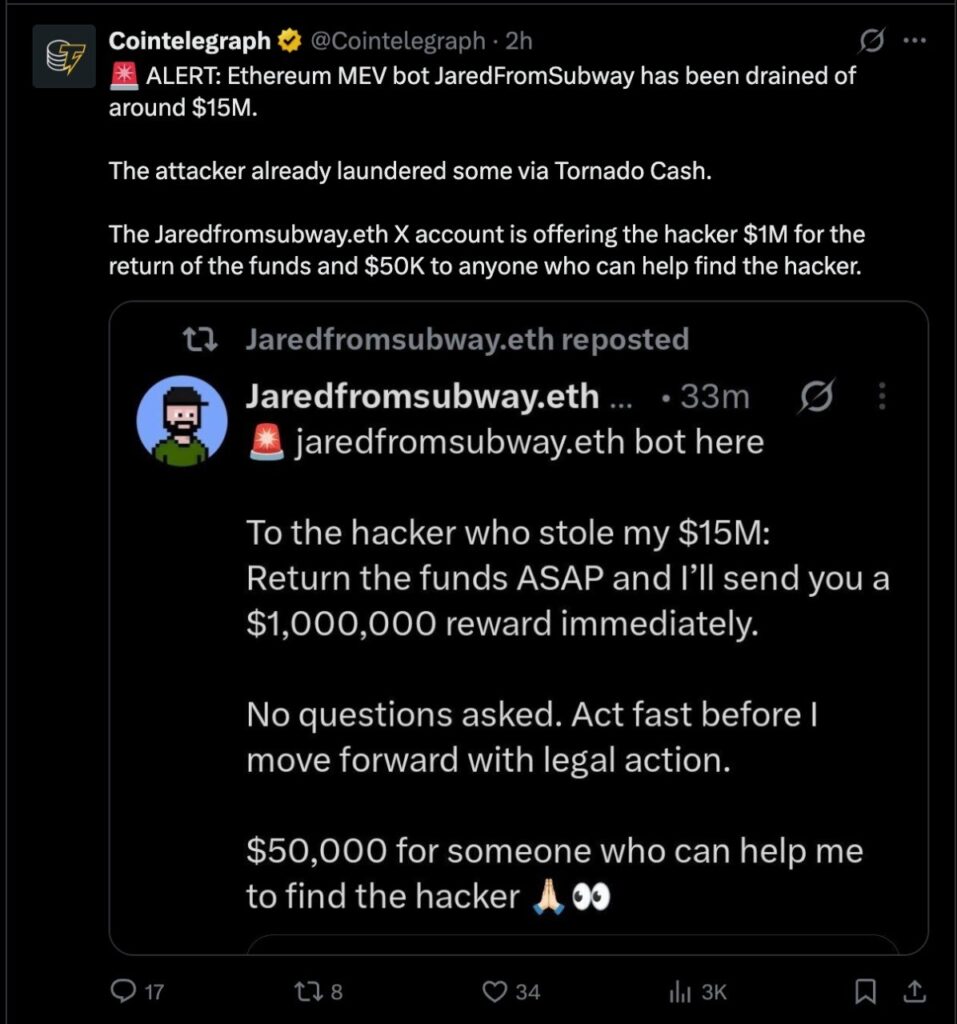

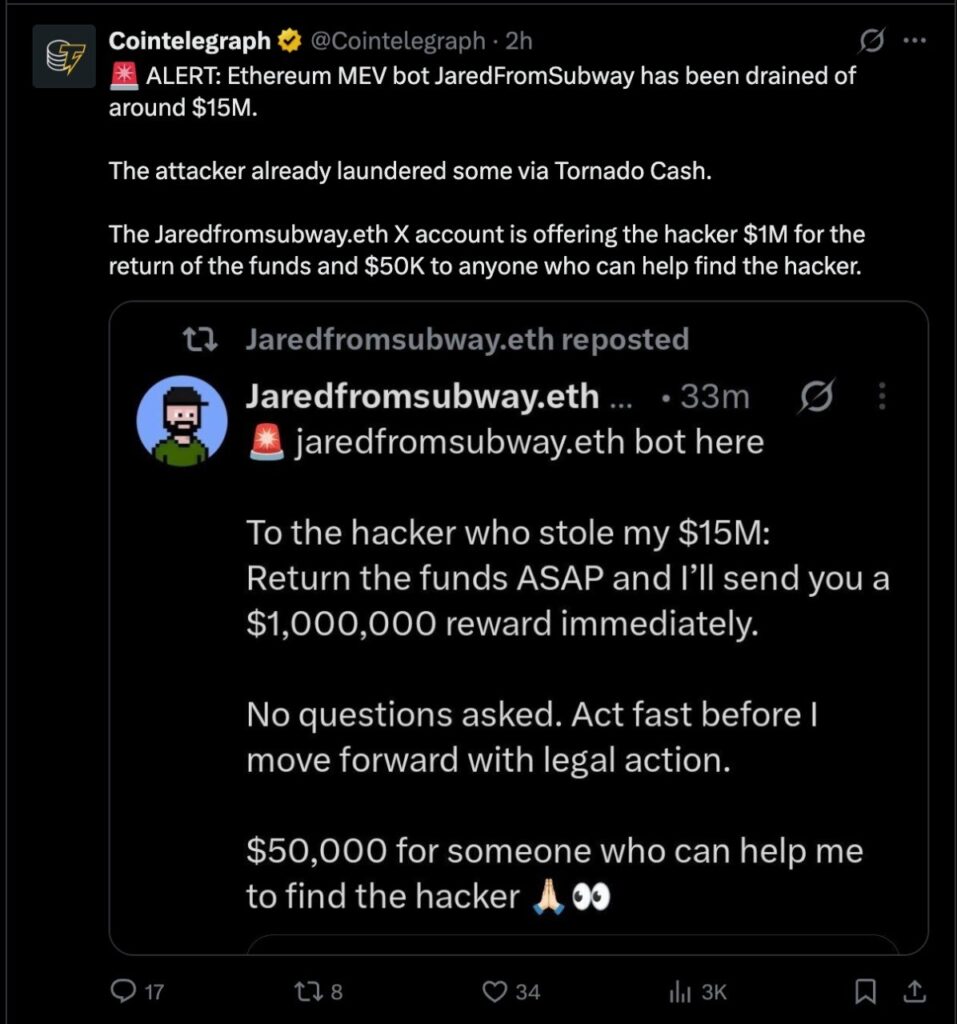

Prolific MEV “sandwich” bot JaredFromSubway.eth lost a total of $7.5 million worth of crypto over the weekend after being lured into a trap over almost one hundred blocks.

In a dramatic case of on-chain karma, the plot to relieve the bot of what many see as its ill-gotten gains involved fake tokens, small wins and an equally dramatic sting.

Blockchain investigator Specter flagged the suspicious transaction, which saw approximately 1,475 WETH ($2.6 million), $2.9 million USDC, and $2 million USDT drained from JaredFromSubway.eth’s bot.

Read more: JaredFromSubway.eth sandwich attacked Vitalik Buterin

The ‘victim’

The victim address, labelled “jaredfromsubway: MEV Bot 2” on block explorer Etherscan, has been active since August 2024 and is the operator’s second iteration.

Between the two bots, and 6.4 million transactions, the operator has made millions of dollars by “sandwiching” on-chain trades.

This process involves scanning the network’s mempool of pending transactions before front-running and back-running user trades. The front-run manipulates swap prices, while the back-run makes a profit off the difference, paying block builders a tip to be included at the right position in the block.

As transaction fees on Ethereum have dropped, sandwichers often target increasingly small wins, such as JaredFromSubway’s attack on Ethereum co-founder Vitalik Buterin last month.

The bot operator’s choice of name is a dark nod to the popular sandwich shop’s erstwhile mascot Jared Fogle, who was later discovered to be a sex offender.

Read more: Explained: How JaredFromSubway.eth still sandwich attacks victims

The campaign

The attacker specifically targeted JaredFromSubway’s bot, luring it in with small, profitable sandwich attacks on fake attacker-created token pairs.

A report from Yearn developer Banteg describes how, over the course of 97 blocks, the bot was offered “small real-token profits,” on “profitable fake-DEX arbitrage” opportunities.

However, during the transactions, the bot contract inadvertently “approved attacker-controlled child contracts to spend real WETH, USDC, and USDT,” which were not consumed during the sandwiches, nor revoked afterwards.

The attacker was then able to harvest the pre-approved tokens in the final drain transaction.

Read more: Aztec Network hit by second hack this week as escapeHatch drained of $2M

The aftermath

Taking advantage of the news, recently-renamed X handle “jaredsmev” made various scam bounty offers of $1 million to $7.5 million, citing the erroneous, but widely reported total loss of $15 million.

Cointelegraph even reposted one of the scammer’s offers to its 2.9 million X followers, before deleting.

Read more: Cointelegraph says Bitcoin ETF approved despite no proof

In an on-chain transaction from JaredFromSubway.eth, the bot’s real operator sent an input data message to the attacker, with a seemingly genuine bounty offer.

“Well played,” begins the message, before requesting the return of 2150 ETH, equivalent to approximately 50% of the stolen funds, in the next 48 hours.

“Otherwise we will pursue all available legal and law-enforcement remedies,” it threatens.

Other users have reached out to the attacker on-chain, claiming to be victims of JaredFromSubway’s MEV operations, and requesting reimbursement of their supposed losses.

One called the attacker “our Robin Hood in a White Hat.” Others were less subtle.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Perpetual futures, or perps, are the most traded instrument in crypto. They let you bet on price with leverage and never expire, held in line with the spot market by a clever fee called the funding rate. They are powerful, they are dangerous, and in 2026 they are finally arriving onshore in the United States.

Summary

- Perpetual futures let traders take leveraged long or short positions without an expiry date, using funding rates to keep prices aligned with the spot market.

- Funding payments flow between longs and shorts, while leverage and margin determine how quickly a position can be liquidated during adverse price moves.

- Crypto perps have begun entering regulated U.S. markets in 2026, bringing the industry’s most traded derivative product into a new regulatory framework.

A perpetual future, usually shortened to perp, is a derivative contract that lets a trader bet on the price of an asset with leverage and hold that bet open indefinitely, because unlike a traditional futures contract it has no expiration date. The price of a perp is kept tethered to the real spot price of the underlying asset by a recurring payment between traders called the funding rate, which nudges the contract back toward the market whenever it drifts.

Perps let you go long if you think the price will rise or short if you think it will fall, control a position far larger than the cash you put down, and never worry about a contract expiring out from under you. That combination has made perpetual futures the single most heavily traded product in all of crypto, and also one of the fastest ways to lose money in it.

This guide explains perpetual futures in plain English, with no derivatives background assumed. It covers what a perp actually is, the traditional futures contract it evolved from, the funding-rate mechanism that makes the whole thing work, how leverage and margin lead to liquidation, the difference between mark price and index price that decides when you get liquidated, where perps are traded and the major shift happening in the United States in 2026, the real risks that blow up accounts, and why this instrument came to dominate crypto trading.

By the end, you will understand not just how to read a perp but why it behaves the way it does, and why even regulators who now permit it call it a product to treat with respect.

What a perpetual future actually is

The name packs two ideas together. “Future” means it is a contract whose value is derived from the price of something else, a derivative, where you agree to gain or lose money based on how that price moves without necessarily owning the asset. “Perpetual” means the contract never expires, so you can hold the position open for as long as you like and your margin allows.

That second word is the whole innovation. A perp lets you take a leveraged bet on, say, Bitcoin, and simply keep it open, adjusting or closing whenever you choose, with no expiry forcing your hand. You can go long, profiting if the price rises, or short, profiting if it falls, and because the contract is leveraged, you can put down a fraction of the position’s value as collateral, called margin, and control the full size.

If you post one thousand dollars at ten times leverage, you control a ten-thousand-dollar position, so a ten percent move in your favor doubles your collateral, and a ten percent move against you wipes it out. The perp itself is settled in cash or a stablecoin, so you never have to take delivery of the underlying asset; you are trading the price, not the coin.

The product was invented by the crypto exchange BitMEX in 2016, and it spread because it fit crypto perfectly: traders wanted leverage, they wanted to bet in both directions, and they did not want the friction of contracts that expire and have to be rolled over. The perp gave them a single instrument that did all of that, and the rest of the market followed.

Futures first: the contract perps evolved from

To see what makes a perp special, it helps to understand the ordinary futures contract it grew out of, because the perp is essentially a futures contract with its biggest inconvenience removed.

A traditional futures contract is an agreement to buy or sell an asset at a set price on a specific future date. If you buy a Bitcoin futures contract expiring in three months, you are locking in a price now for settlement then, and when that date arrives, the contract expires and settles.

This is useful, and it is how commodities and financial futures have worked for a very long time, but it has an awkward feature for someone who simply wants ongoing leveraged exposure: the contract ends. If you want to keep your position past the expiry, you have to “roll” it, closing the expiring contract and opening a new one further out, paying costs and friction each time. Traditional futures also have a “basis,” a gap between the futures price and the spot price that opens and closes as expiry approaches, which adds complexity.

The perpetual future strips out the expiry entirely. There is no settlement date, so there is nothing to roll and no countdown forcing you to act. But removing the expiry creates a new problem. In a normal future, the looming settlement date is what drags the contract price toward the real spot price, because at expiry they must converge.

Take away the expiry, and you remove the very thing that keeps the contract honest. So the designers of the perp had to invent a replacement, a mechanism that would keep a never-expiring contract anchored to the spot price using market forces instead of a deadline. That mechanism is the funding rate, and it is the beating heart of every perp.

The funding rate: the mechanism that keeps perps honest

The funding rate is the single most important concept in perpetual trading, and it is the part beginners most often miss until it quietly costs them money.

Because a perp never expires, nothing automatically forces its price to match the spot price of the underlying asset. Left alone, a perp could drift well above or below the real market. The funding rate fixes this by creating a recurring payment, typically every eight hours, between the two sides of the market.

When the perp trades above the spot price, meaning demand to be long is too strong, the funding rate is positive, and longs pay shorts. When the perp trades below the spot price, meaning shorts are crowded, the funding rate is negative, and shorts pay longs. The payment is a small percentage of position value, and it flows directly between traders, not to the exchange.

The effect is elegant. If too many people are long and the perp price runs above spot, longs must keep paying a fee to shorts, which makes holding a long more expensive and encourages traders to close longs or open shorts, pushing the price back down toward spot. The mechanism is self-correcting: whichever side is crowded pays the other, and that cost pulls the contract back in line with the real market.

This is why a perp tracks spot closely without ever expiring. It also turns the funding rate into a live sentiment gauge, because a strongly positive rate tells you the market is aggressively long and paying for the privilege, while a negative rate tells you shorts dominate. Traders watch funding both as a cost they must pay or earn and as a signal of how the crowd is positioned. Even regulators who have studied perps note that funding rates, far from being a trick, perform roughly the same economic job as the costs of repeatedly rolling expiring futures, just packaged differently.

Leverage, margin, and the liquidation that follows

Leverage is what makes perps thrilling and what makes them lethal, so it is worth being precise about how it actually works and where it ends.

When you open a perp position, you post collateral, called margin, and the exchange lets you control a position several times larger. The multiple is your leverage. At five times leverage, a thousand dollars of margin controls five thousand dollars of exposure; at twenty times, it controls twenty thousand. Leverage magnifies both directions equally. A favorable move multiplies your gains against your small margin, and an unfavorable move multiplies your losses just as fast. The crucial consequence is that with leverage you do not need the price to go to zero to lose everything. You only need it to move against you by a fraction equal to your margin.

That is where liquidation comes in. Every leveraged position has a liquidation price, the level at which your losses have eaten through your posted margin. If the market reaches that price, the exchange automatically closes your position to prevent your losses from exceeding your collateral, and your margin is gone. At ten times leverage, a roughly ten percent move against you is enough to trigger liquidation; at twenty-five times, about four percent will do it; at one hundred times, a one percent flicker can end the trade.

Offshore venues have historically offered enormous leverage, and the extreme figures sometimes quoted, fifty, one hundred, even more, are a hallmark of those unregulated platforms. Regulated perpetual products in the United States are subject to the same leverage limits as other regulated futures, which are far lower. High leverage does not make you more likely to be right; it only makes you more likely to be liquidated before you are proven right, and that distinction has emptied more accounts than any single price crash.

Mark price versus index price: why you actually get liquidated

A detail that confuses many new perp traders, and burns some of them, is that the price used to decide your liquidation is not always the last traded price on the exchange. Understanding this can be the difference between a survivable trade and an avoidable wipeout.

Exchanges track two prices. The index price is an average of the spot price across several major markets, a clean reading of what the asset is really worth right now. The mark price is a smoothed, fair value derived largely from that index, and it is the price the exchange uses to calculate your unrealized profit, your losses, and your liquidation.

Why not just use the last traded price on the perp itself? Because the last traded price on a single venue can spike or crash briefly during a moment of thin liquidity or a manipulation attempt, and if liquidations were based on that, a momentary wick could liquidate thousands of traders unfairly. By marking positions to a broad index-based fair value instead, the exchange protects traders from being liquidated by a fleeting, unrepresentative blip on one order book.

The practical lesson is that you are liquidated when the mark price, not necessarily the screaming candle on the chart, reaches your liquidation level. Most of the time, mark and last price are nearly identical, but in violent moments they can diverge, and knowing which one governs your position is part of trading perps without nasty surprises. It is also why checking your exact liquidation price before entering a trade, and giving yourself a wide margin of safety, matters far more than guessing where the price “should” go.

Where perps are traded, and the 2026 shift onshore

For most of their history, perps lived offshore, outside the reach of United States regulators, and that map is being redrawn right now in a way every trader should understand.

On centralized exchanges, perps are a flagship product, with venues such as Binance, Bybit, OKX, Deribit, and the original inventor BitMEX offering deep perpetual markets in hundreds of assets. A newer wave runs perps fully on-chain through decentralized exchanges, where trades settle on a blockchain, and users keep custody of their funds.

Hyperliquid has risen to dominate on-chain perpetual trading, alongside established names like dYdX and GMX, proving that a decentralized venue can match the speed and depth traders once thought only centralized platforms could provide. For years, United States traders were largely walled off from regulated crypto perps, pushing demand offshore.

That wall is now coming down. In May 2026, the Commodity Futures Trading Commission approved a Bitcoin perpetual futures contract from the prediction-market exchange Kalshi, the first regulated crypto perp cleared for United States traders, and Kalshi quickly expanded into perps tied to Ethereum, XRP, and others, reporting more than five billion dollars in trading volume within weeks. Coinbase secured its own regulated route to offer perpetual products domestically.

The arrival has not been smooth. The CME Group, the giant traditional derivatives exchange, sued the CFTC, arguing that perpetual futures should be regulated as swaps under the Dodd-Frank Act rather than as ordinary futures, and that the regulator bypassed proper procedure.

The CFTC’s chair has pushed back publicly, arguing that nothing in the law requires a futures contract to have a fixed expiration date, that regulated perps face the same leverage limits as other United States futures rather than the extreme offshore multiples, and that funding rates are a legitimate pricing mechanism. However that legal fight resolves, the direction is clear: the most popular instrument in crypto trading is moving from the offshore shadows into regulated American markets, and the rules for it are being written in real time.

The risks: why perps blow up accounts

Perps deserve their fearsome reputation, and an honest guide has to be blunt about why so many traders lose, because the dangers are structural, not just a matter of bad luck.

The first and largest risk is leverage itself. The same multiplication that makes a winning perp trade so satisfying makes a losing one fatal, and at high leverage a small, ordinary price move is enough to liquidate you entirely, which is why most accounts that chase big leverage do not last. The second is liquidation cascades.

When prices move sharply, waves of leveraged positions hit their liquidation prices at once, and the forced selling or buying pushes the price further in the same direction, triggering still more liquidations, a self-reinforcing spiral that can turn a modest move into a violent one and catch even careful traders. The third is funding cost. Holding a position on the crowded side of the market means paying funding every few hours, and over time that steady drain can quietly erode or erase a position that the price action alone would have left profitable.

The fourth is the psychological trap: perps are available around the clock, they encourage constant action, and the leverage makes every move feel urgent, which pushes traders toward overtrading, revenge trading after a loss, and holding losers too long. The fifth, on offshore venues especially, is platform and counterparty risk, because you are trusting the exchange’s solvency, its liquidation engine, and its honesty with your collateral.

The uncomfortable summary is that perps are a professional’s instrument that retail traders can access with one tap, and the gap between those two facts is where the damage happens. The product is not a scam, and the mechanics are sound, but the combination of high leverage, constant availability, and human emotion is genuinely hazardous, and that is true no matter how confident any individual trade feels.

A worked example: one long trade, from open to liquidation

Numbers make the danger concrete in a way definitions cannot, so walk through a single leveraged trade step by step, because every concept in this guide shows up in the life of one position.

You have one thousand dollars, and you are convinced Bitcoin is about to rise. You open a long perp at ten times leverage, so your one thousand dollars of margin now controls a ten thousand dollar position.

The exchange shows you a liquidation price roughly ten percent below where you entered, because a ten percent move against a ten-times position consumes your entire margin. You are also told the funding rate is positive, meaning longs are crowded, and you will pay a small fee to shorts every eight hours for as long as you hold. The trade is on.

Suppose Bitcoin rises five percent. Your position gained five percent of ten thousand dollars, or five hundred dollars, which is a fifty percent return on your one thousand dollar margin. This is the seduction of leverage: a modest move produced an outsized gain. Now suppose instead that Bitcoin falls.

At a four percent drop, you are down four hundred dollars and nervous. At a move near ten percent against you, the mark price reaches your liquidation level, the exchange automatically closes the position, and your one thousand dollars is gone. Notice what did not happen: Bitcoin did not crash, it did not go to zero, it simply moved ten percent, an ordinary day in crypto, and your account was wiped out.

Had you used two times leverage instead of ten, the same ten percent drop would have cost you two hundred dollars, painful but survivable. Had you used one hundred times leverage, a one percent flicker would have ended you.

Layer in the funding cost and the picture sharpens further. If you held that crowded long for several days, you paid funding every eight hours the whole time, a steady drain that eats into gains and deepens losses. And if the market dropped sharply, your liquidation might have been one of thousands firing at once, the forced selling pushing the price down faster and triggering still more liquidations around you. One trade, and you have lived through leverage, margin, the liquidation price, the mark price, funding cost, and a liquidation cascade. That is why experienced traders obsess over position size and liquidation distance before they ever think about where the price is going.

Why perps took over crypto trading

For all the danger, perps did not come to dominate by accident, and understanding why explains a great deal about how crypto markets actually function. A perp gives a trader almost everything they could want in a single instrument: leverage to amplify a view, the ability to profit in both rising and falling markets, no expiry to manage, a price kept honest by funding, and deep liquidity that makes entering and exiting easy. For speculators, it is the sharpest tool available. For sophisticated participants it is also a hedging instrument, a way to offset the risk of a spot holding or to manage exposure without buying or selling the underlying coin. That versatility is why perpetual futures now account for the large majority of all crypto trading volume, dwarfing the spot market most newcomers assume is the main event.

The instrument that BitMEX dreamed up in 2016 has become the center of gravity of crypto markets, and in 2026 it is crossing from the unregulated fringe into the regulated mainstream, with traditional exchanges fighting over how it should be classified. That trajectory tells you something important: perps are not a passing fad but a durable financial innovation that traditional finance is now scrambling to adopt and contain. The right way to approach them is with respect. Understand the funding rate, know your liquidation price, treat leverage as the dangerous tool it is, and never confuse the thrill of a leveraged win with skill. The traders who survive perps are the ones who understand the machinery before they ever pull the lever.

Frequently Asked Questions

What is a perpetual future in simple terms?

A perpetual future, or perp, is a contract that lets you bet on the price of an asset with leverage and hold the bet open with no expiration date. You can go long if you think the price will rise or short if you think it will fall, and you post a fraction of the position’s value as collateral, called margin, to control a much larger position. The perp’s price is kept close to the real spot price by a recurring payment between traders called the funding rate. It settles in cash, so you never own the underlying asset.

How does the funding rate work?

Because a perp never expires, nothing automatically keeps its price matched to the spot market, so the funding rate does that job. Roughly every eight hours, a payment flows between longs and shorts. When the perp trades above spot, longs pay shorts, which makes being long costlier and pushes the price back down. When it trades below spot, shorts pay longs. The payment goes between traders, not to the exchange, and it both keeps the perp anchored to spot and signals which side of the market is crowded.

What is liquidation in perpetual trading?

Liquidation is when the exchange automatically closes your leveraged position because your losses have consumed your posted margin. Every leveraged position has a liquidation price, and if the market reaches it, your collateral is gone. The higher your leverage, the smaller the move needed to liquidate you: at ten times leverage about a ten percent move against you is enough, and at one hundred times around one percent will do it. Liquidations are usually triggered by the mark price, a fair value based on a broad index, not the last traded price on a single venue.

Why are perps so risky?

The core risk is leverage, which multiplies losses as fast as gains, so a small price move can wipe out a highly leveraged account. Liquidation cascades can make sharp moves worse, as forced closures push the price further and trigger more liquidations. Funding costs can quietly erode a position held on the crowded side of the market. Perps are also available around the clock and encourage emotional overtrading, and on offshore venues you take on the platform’s solvency and honesty as additional risks.

Where can you trade perpetual futures?

Perps trade on centralized exchanges such as Binance, Bybit, OKX, Deribit, and BitMEX, and increasingly on decentralized exchanges that settle on-chain, where Hyperliquid, dYdX, and GMX are leading venues. For years, United States traders were largely excluded from regulated crypto perps, but that changed in 2026 when the CFTC approved a Bitcoin perpetual contract from Kalshi, and Coinbase gained a regulated route, bringing perps onshore even as exchanges like CME dispute how they should be classified.

Who invented perpetual futures?

The perpetual swap was created by the crypto exchange BitMEX in 2016. It caught on quickly because it suited crypto traders perfectly: it offered leverage, allowed betting in both directions, and removed the expiry and rollover hassle of traditional futures, all in a single instrument anchored to spot by the funding rate. The design spread across the industry, and perpetual futures now account for the majority of all crypto trading volume.

This article is educational and does not constitute financial or investment advice. Perpetual futures are high-risk leveraged products, and the rules governing them, especially in the United States, are changing quickly. As of June 22, 2026, verify current product details, leverage limits, and regulatory status with official sources, and never trade with money you cannot afford to lose.

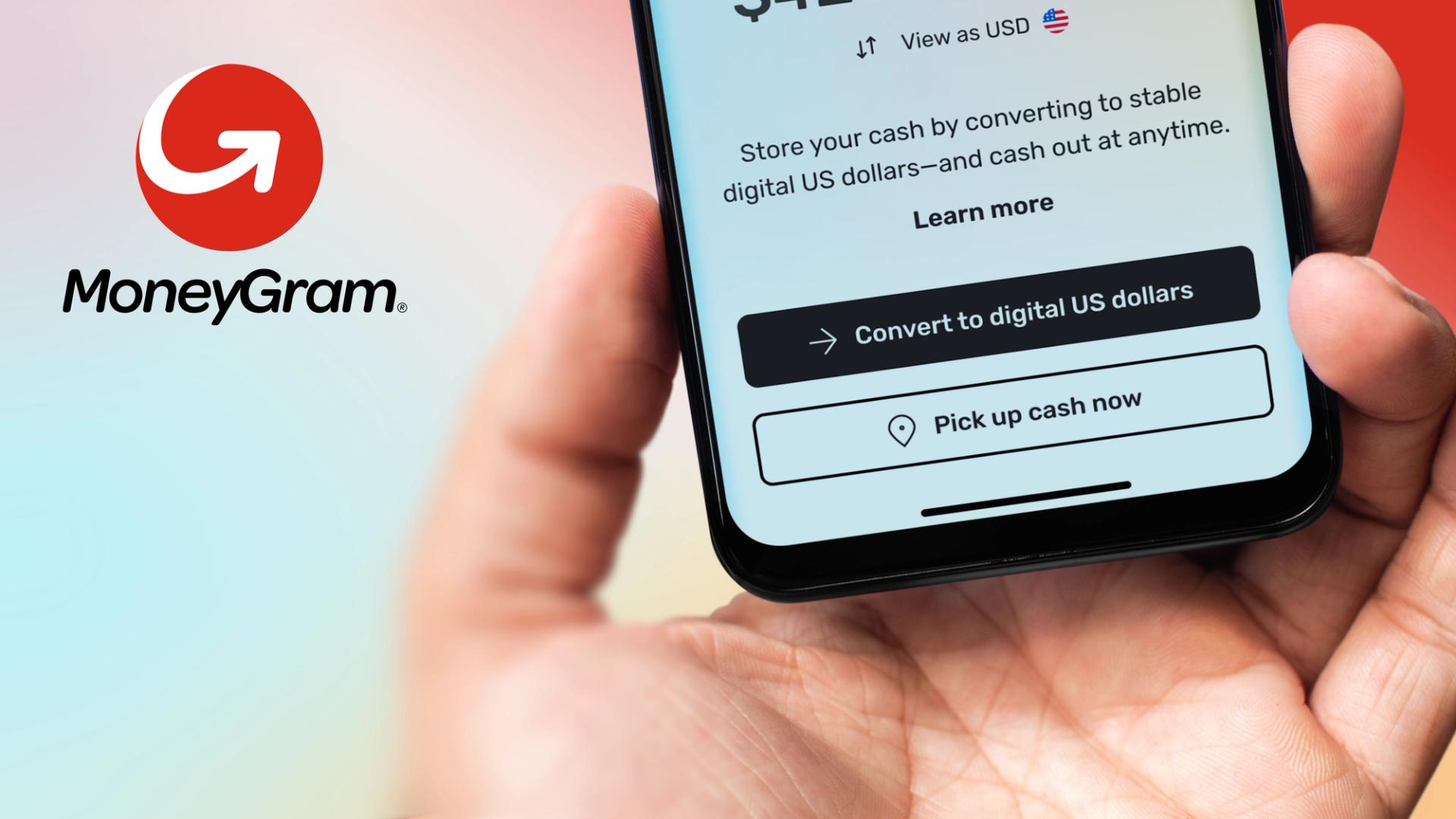

MoneyGram has joined the Solana ecosystem as a network validator and participant in the Solana Developer Platform, expanding the payments company’s blockchain infrastructure strategy beyond stablecoins and payment services.

Summary

- MoneyGram has become a validator on the Solana blockchain and joined the Solana Developer Platform as it expands its blockchain payments strategy.

- The company now operates official validator nodes on Solana, Tempo and Midnight while continuing to build stablecoin based payment services.

- The move follows MoneyGram’s recent launch of its MGUSD stablecoin and broader efforts to integrate blockchain infrastructure into global money transfers.

According to a June 22 announcement from MoneyGram, it now operates an active validator on the Solana blockchain, where it stakes SOL, processes transaction blocks, and contributes to network security and performance. The company also joined the Solana Developer Platform, a development environment designed for institutions building financial products on Solana.

The company described the move as the next stage of a blockchain strategy that has become part of its treasury, product development and payments operations over the past five years.

MoneyGram expands blockchain infrastructure role

Luke Tuttle, Chief Product and Technology Officer at MoneyGram, said operating a validator places the company directly within Solana’s consensus process and allows it to help secure the network at the protocol level.

“We help run the rails we move money on,” Tuttle said, adding that MoneyGram is also developing products intended to support money movement across different forms of value.

Sheraz Shere, General Manager of Payments and Commerce at the Solana Foundation, said MoneyGram’s participation demonstrates how organizations involved in global payments are becoming active members of blockchain networks as more payment activity moves onchain.

MoneyGram said it joined the Solana Developer Platform alongside institutions that include Mastercard. The company said the platform provides tools to build and scale compliant financial products on Solana.

Anthony Soohoo, Chairman and CEO of MoneyGram, said blockchain infrastructure has become a core component of the company’s payment systems and that future development efforts will build on that foundation.

“We believe the future of global money movement will be built on open, interoperable stablecoin rails that anyone, anywhere can access,” Soohoo said.

The company did not announce any new payment products tied to Solana but said its participation in the network forms part of a long-term effort to support open blockchain infrastructure for global money transfers.

Follows stablecoin and validator expansion

The Solana announcement comes weeks after MoneyGram launched MGUSD, its own U.S. dollar stablecoin, on the Stellar blockchain.

MoneyGram introduced the stablecoin on June 2 through a partnership with Bridge, a Stripe-owned company that serves as the issuer. M0 provides the infrastructure used to mint and burn the token, while Fireblocks supplies custody services.

MGUSD became the latest addition to a blockchain payments strategy that has expanded through partnerships with Stellar, Crossmint, Fireblocks and Kraken. MoneyGram has also introduced stablecoin-based remittance services, crypto-to-cash withdrawals and digital dollar products across multiple markets.

The company previously became an anchor remittance validator on the Tempo blockchain and was named a validator for Midnight, Cardano’s privacy-focused sidechain. Solana now becomes the third blockchain network where MoneyGram operates an official validator.

MoneyGram also worked with Ripple between 2019 and 2021, using RippleNet and XRP-based On-Demand Liquidity products before the partnership ended following the U.S. Securities and Exchange Commission’s lawsuit against Ripple.

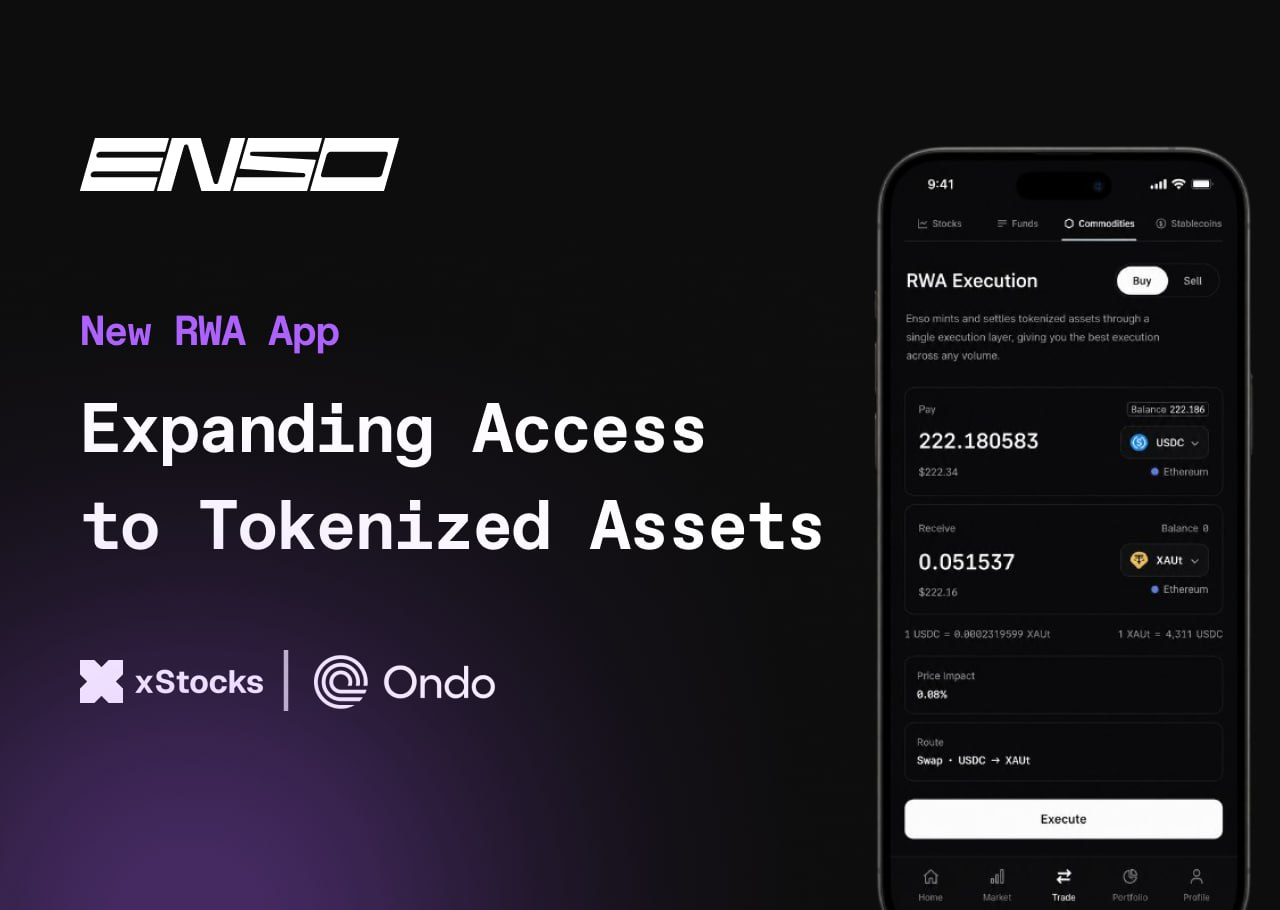

Switzerland-based Web3 development platform Enso has launched a real-world asset (RWA) application offering access to more than 500 tokenized assets through integrations with xStocks, Ondo Finance and Anchorage Digital’s Porto.

Through Enso’s execution layer, users can access tokenized stocks, ETFs, Treasurys, commodities and stablecoins. Ondo will provide tokenized equities, treasury products and capital markets infrastructure, while xStocks will enable access to tokenized equities and ETFs, according to a Monday announcement shared with Cointelegraph.

Available assets include major US companies such as Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, Tesla and SpaceX.

Enso said bringing these assets under a unified distribution and execution layer would simplify access to tokenized assets across multiple venues and improve the user experience.

The launch adds Enso to a growing field of European crypto firms expanding into tokenized traditional assets. Earlier this year, Austria-based Bitpanda expanded its offering to roughly 10,000 stocks and ETFs, while a number of European digital asset firms have moved to capitalize on growing demand for tokenized securities.

Enso expands access to tokenized assets. Source: Enso

Tokenized US equities have attracted significant demand from investors outside the US, particularly in Europe, Enso co-founder and CEO Connor Howe told Cointelegraph:

The demand concentrates in two places: tokenized access to US markets, with the around-the-clock trading traditional venues can’t match, and yield-bearing dollar assets.”

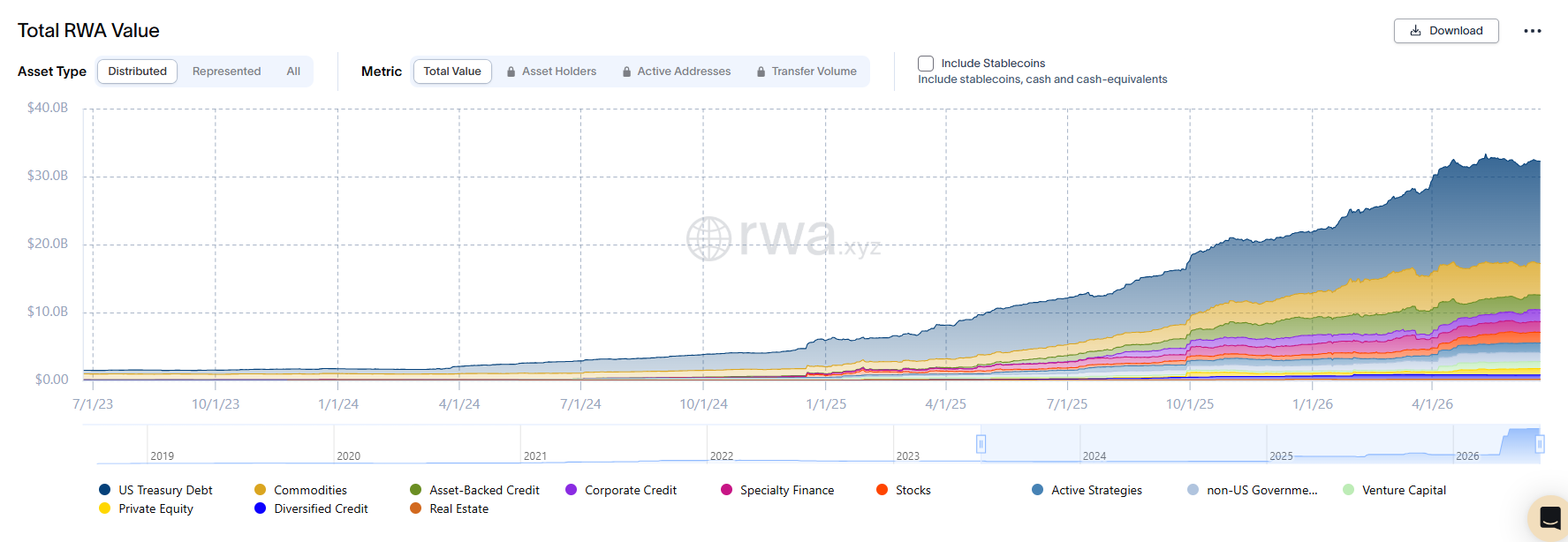

Tokenized asset holders rise 13% amid growing demand

The launch comes amid growing demand for tokenized assets. The number of tokenized asset holders rose 13.4% over the past 30 days to 930,612, according to data from RWA.xyz. The total value of tokenized assets, however, fell 0.9% during the same period.

Total RWA value onchain, all-time chart. Source: RWA.xyz

US Treasury debt was the largest tokenized asset category with $15 billion in onchain value, followed by tokenized commodities at $4.6 billion and asset-backed credit at $2.2 billion. Tokenized stocks accounted for $1.6 billion in total onchain value, ranking fifth among tokenized asset categories.

Related: Franklin Templeton, BNP Paribas see tokenization boosting EU’s capital efficiency

Tokenized stocks first crossed $1 billion in total onchain value on March 10, when Ondo accounted for about 58% of the market and xStocks about 24%.

Magazine: Can Robinhood or Kraken’s tokenized stocks ever be truly decentralized?

Crypto World

TradFi fund manager Baillie Gifford introduces Solana, Ethereum tokenized fund with BNY

Baillie Gifford, a 118-year-old investment firm based in the Scottish capital of Edinburgh, unveiled a fixed-income tokenized fund in association with global custody giant BNY, the companies said on Monday.

Baillie Gifford Enhanced Yield Fund (BAGEY) is denominated in dollars, and gives eligible investors access to an actively managed, short-duration portfolio of public corporate bonds using the Ethereum and Solana public blockchains, according to a press release.

The fund is operated through a U.K.-regulated Open-Ended Investment Company (OEIC), a type of collective investment fund structured as a limited liability company that spreads capital from multiple investors across equities or bonds.

The fund, which currently offers a yield of around 7%, will be available to eligible investors in the U.K., Switzerland and Cayman Islands, subject to applicable laws, regulations and distribution restrictions.

Tokenization of real-world assets (RWAs) has taken the traditional finance world by storm, but merely wrapping legacy infrastructure in a digital layer will not fundamentally improve finance, said Theo Golden, head of digital assets and tokenization at Baillie Gifford.

- Solana (SOL) is stuck between $72 support and $76 resistance.

- Solana’s price action shows a tight range with possible short-term rejection risk.

- $90 remains the key breakout level for a stronger bullish move.

Solana has moved back above the $74 level after a period of sideways trading, putting the asset close to a key technical zone that traders have been watching for several days.

The latest gains come after a gradual recovery from the lower $70 range, where price repeatedly found support before pushing higher.

Is this a correction within a larger bearish trend?

Recent price action shows Solana compressing inside a well-defined range between $62.08 and $76.00.

This range has become the main battleground for buyers and sellers, with repeated reactions near both ends.

On the lower side, support has been consistently observed around $69.50 and $62.08, where buying interest has prevented deeper declines.

On the upper side, resistance is clustered between $76.00 and $83.00, a zone that has rejected multiple upward attempts in recent sessions.

Some short-term technical analysis, however, suggests that the current upward move may still be part of a broader corrective phase within a larger bearish structure.

Market analysis highlights the possibility of a short squeeze toward the $76 region, followed by a rejection if bulls fail to maintain momentum above resistance.

If price is rejected from this zone, downside pressure could return quickly, with initial support at $69.50, followed by the lower boundary near $62.08.

The $76–$90 range is now the key decision area

While short-term resistance sits near $76, higher timeframe analysis places a more important threshold at the $90 level.

This zone has been highlighted as a structural breakout point that could determine whether Solana transitions into a stronger upward trend or remains in consolidation.

A move above $90 could open room toward the $100 to $114 range, which has been identified as the next liquidity zone on higher timeframes.

However, failure to break this level would likely keep price action trapped in a broader corrective environment.

At the same time, one technical interpretation suggests that the current movement is still part of a countertrend rally within a wider bearish cycle in the crypto market.

Under this scenario, upward moves into resistance zones are viewed as temporary expansions designed to capture liquidity before potential reversals.

This conflict between breakout potential and bearish continuation has created a split in analyst expectations.

The $90 level now acts as the line between the continuation of the recovery and renewed consolidation.

Morgan Stanley’s Solana ETF adds a layer of optimism

Beyond technical levels, institutional developments are also shaping sentiment around Solana.

Morgan Stanley has reportedly advanced filings for proposed spot Solana and Ethereum exchange-traded funds (ETFs, with a proposed management fee of 0.14%, which would place them among the lowest-cost crypto ETF proposals currently under consideration.

The structure of these proposed products includes staking mechanisms, in which a large portion of staking rewards would be returned to investors after operational costs are covered.

Although these ETFs are not yet approved, the filings signal increasing institutional interest in structured Solana exposure through regulated financial instruments.

MoneyGram said Monday it has become a validator on the Solana (SOL) blockchain, the latest step in the remittance firm’s ongoing push into crypto infrastructure as it builds payment services around stablecoins.

By operating a validator, MoneyGram will help process transactions and secure Solana’s proof-of-stake network, becoming a key part of the infrastructure that keeps the network running.

The company also joined Solana Developer Platform, an initiative aimed at helping institutions build financial products on the blockchain.

The move comes weeks after MoneyGram unveiled its MGUSD stablecoin on the Stellar blockchain, a sign of the company’s growing commitment to blockchain-based payments infrastructure. After spending several years integrating crypto into remittances and settlement, MoneyGram is now taking a more active role in the networks that support those services.

“MoneyGram has spent the past several years integrating blockchain into our payment infrastructure, and everything we are building now leverages this foundation,” CEO Anthony Soohoo said in a statement. “We believe the future of global money movement will be built on open, interoperable stablecoin rails that anyone, anywhere can access.”

TLDR

- Strive acquired 759 Bitcoin for approximately $50 million between June 15 and June 21.

- The company paid an average price of $65,850 per BTC for the latest purchase.

- Strive’s total Bitcoin holdings increased to about 19,000 BTC.

- The Bitcoin treasury is valued at more than $1.2 billion at current market prices.

- The purchase price was roughly 11% lower than Strive’s May acquisition cost.

Strive expanded its Bitcoin treasury after purchasing 759 BTC for about $50 million. The company disclosed the transaction in a June 22, 2026, filing, and the purchase increased its total holdings to nearly 19,000 BTC. Those holdings now carry a value exceeding $1.2 billion based on current market prices.

Strive Adds More Bitcoin at a Lower Average Cost

The company acquired 759 BTC between June 15 and June 21, 2026. According to the filing, Strive paid an average price of $65,850 per Bitcoin. As a result, the purchase cost was approximately $50 million.

The latest acquisition came at a lower price than Strive’s previous major Bitcoin purchase. In May 2026, the company bought more than 2,500 BTC for $185.2 million. That transaction carried an average purchase price of $74,092 per coin.

The difference in acquisition prices reflects changing market conditions during the quarter. While the company paid less per coin in June, it continued increasing its Bitcoin position. Consequently, Strive maintained its ongoing treasury accumulation strategy.

Since January 2026, the company has added more than 3,700 BTC to its balance sheet. That figure includes Bitcoin obtained through the Semler Scientific acquisition. It also includes coins acquired through direct market purchases.

Bitcoin Treasury Growth Reaches 19,000 BTC

The latest purchase lifted Strive’s Bitcoin reserves to approximately 19,000 BTC. Therefore, the company remains among the largest public corporate Bitcoin holders. The treasury has grown steadily throughout 2026 through several acquisitions.

Strive has funded part of its Bitcoin strategy through SATA perpetual preferred stock. The company describes the instrument as non-dilutive because it does not require issuing common shares. This structure allows the firm to raise capital while preserving existing shareholder ownership levels.

The company recently increased the dividend rate on SATA preferred stock to 13%. Strive has continued using the instrument to support treasury expansion. At the same time, the company has avoided common equity issuance for these purchases.

Corporate Bitcoin accumulation remains a central part of Strive’s capital allocation strategy. The company has repeatedly used structured financing tools to acquire additional Bitcoin. The June filing confirmed that the latest purchase added 759 BTC to the balance sheet.

The filing also confirmed the transaction period and average acquisition price. Strive reported that it purchased the Bitcoin between June 15 and June 21. The company paid an average of $65,850 per coin during that period.

Three altcoins enter the fourth week of June 2026 with bullish-to-neutral chart setups. All 3 altcoins to watch are ranked among last week’s biggest gainers.

Each token now sits near a pivotal Fibonacci or channel level. Their daily charts show how momentum, volume, and support could shape the next directional move.

LAB Defends the 0.618 Fibonacci Level Near $13

LAB (LAB) trades around $14.97, up about 1.7% on the day, with a market cap near $4.7 billion. The token has printed higher highs and higher lows since early May.

Price recently retested resistance at the 0.382 Fibonacci level near $19. It also confirmed support at the 0.618 Fibonacci level near $13. Earlier, the former $7 resistance flipped to support twice (blue circles), in early June and again on June 11.

The move follows a violent crash that wiped billions from its value in early June. The RSI now reads near 60 and rises slowly, yet it has not entered bullish territory. A daily close above $19 would open room toward higher Fibonacci bands.

Uniswap (UNI) Bounces at the 0.382 Fibonacci Near $3

Uniswap (UNI) changes hands around $3.01, up roughly 0.6% on the day. The token gained almost 16% over the past week, one of the strongest moves in the large-cap group.

The daily chart attempts a bounce and tries to confirm the 0.382 Fibonacci level near $3 as support. If that level holds, resistance sits at the 0.5 Fibonacci near $3.30 and the 0.618 Fibonacci near $3.50.

Volume spiked sharply in mid-June (blue ellipse), which signaled renewed momentum. However, the June 17 candle carried strong selling pressure.

The RSI tried to reach bullish territory, got rejected, and now reads a neutral 53. A recent $100 target from Standard Chartered for 2030 has kept attention on the token.

Stellar (XLM) Tests $0.20 Support After Channel Breakout

Stellar (XLM) trades around $0.21, down about 0.8% over 24 hours, yet still up close to 12% on the week. For most of 2026, XLM moved inside a horizontal channel.

The upper band rejected price four times before the breakout (red arrows). The token finally broke out on May 28 with a sharp volume spike, then reclaimed its long-term channel structure. Volume has since declined, which points to a compression phase.

The former channel resistance flipped to support between June 10 and June 15 (blue circle). Price then turned higher toward resistance near $0.23. It now tries to hold $0.20 as support and extend the upturn. The RSI reads a neutral 54.

Centrifuge brought real-world assets to Stellar on June 20, adding a fresh catalyst.

Altcoins to Watch for Week Ahead

All three altcoins share a similar message. Momentum has improved, yet none of the RSI readings confirm a strong trend.

LAB looks the most extended after its sharp rebound, UNI the most reactive around its Fibonacci pivot, and XLM the most structurally clean after the channel breakout.

Holding their respective support levels could decide whether the rallies continue or stall into the new week. Traders may also watch broader market conditions, since altcoin moves often track Bitcoin closely during fast trend shifts.

The post 3 Altcoins to Watch in the Fourth Week of June 2026 appeared first on BeInCrypto.

Key Takeaways

- JPMorgan boosted its WDC price target to $650 from $530, keeping an Overweight rating on improved HDD pricing trends

- Wells Fargo increased its target to $575 from $500, also maintaining an Overweight rating

- Fiscal Q3 2026 results showed 45% year-over-year revenue expansion, with sequential growth of 11%

- The company projects Q4 fiscal 2026 revenue of $3.65 billion, representing 9.4% quarter-over-quarter growth

- WDC shares have climbed 333% year-to-date, currently trading near $746.93

Western Digital (WDC) is delivering the kind of performance that turns heads across Wall Street. With shares climbing 333% year-to-date and hovering around $746.93, the storage giant has emerged as one of the most compelling beneficiaries of AI infrastructure expansion — even as Sandisk (SNDK) captures attention with its staggering 820% rally.

Western Digital Corporation, WDC

Major financial institutions are responding with upgraded expectations. On June 12, JPMorgan elevated its price target for WDC to $650 from $530, maintaining its Overweight recommendation. The investment bank cited improved earnings projections for hard disk drive manufacturers, pointing to strengthening pricing power and expanding profit margins.

According to JPMorgan, year-over-year pricing momentum across the HDD sector is expected to accelerate in upcoming quarters, with sequential price improvements staying within the low- to mid-single digit range. These incremental gains compound into significant margin expansion.

Wells Fargo followed suit, raising its price objective to $575 from $500 on June 1, while confirming its Overweight stance on the stock.

Financial Performance Validates Bullish Sentiment

The wave of analyst optimism isn’t unfounded speculation — Western Digital‘s recent financial results provide solid justification. The company delivered 45% year-over-year revenue growth during fiscal Q3 2026. Quarter-over-quarter, revenue expanded by 11%, a growth rate typically associated with companies riding major technology shifts.

Looking ahead to Q4 fiscal 2026, management has guided for $3.65 billion in revenue, implying 9.4% sequential expansion. This kind of consistent growth trajectory tends to attract long-term institutional capital.

CEO Irving Tan articulated the fundamental driver in the Q3 earnings release: “Virtually every AI workload, from training, inference, agentic AI to physical AI, creates data that is stored persistently and cost-efficiently on HDDs.”

This statement captures Western Digital’s strategic positioning. As AI applications multiply, data generation accelerates exponentially. That data requires storage infrastructure. Western Digital manufactures the high-capacity drives that provide it.

AI Infrastructure Buildout Fuels HDD Demand

Cloud hyperscalers continue deploying AI accelerators at unprecedented scale, and those computing resources generate massive data volumes requiring persistent storage. Western Digital’s enterprise HDD portfolio addresses precisely this need.

Grand View Research projects a 30.6% compound annual growth rate for the storage market through 2033. Currently, 809 data centers are in various planning and construction phases globally. Each facility will require extensive storage capacity.

Western Digital shares reached a 52-week peak of $799.87, with current levels around $746.93. The company’s market capitalization now stands at $257 billion.

Micron Technology recently achieved a $1 trillion valuation milestone, while Sandisk maintains its remarkable upward trajectory. Western Digital, with its 333% year-to-date appreciation, ranks among the top-performing stocks across the entire market this year.

Toyota and pedestrian involved in Easingwold crash

Investor support for Target chairman Brian Cornell hits record low

MEV bot JaredFromSubway.eth loses $7.5M to approvals honeypot

![Finance Case Study Example | SaaS Startup Financial Model [Template Included]](https://wordupnews.com/wp-content/uploads/2026/06/1782137607_maxresdefault-80x80.jpg)

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Miami – Corporette.com

-

Tech6 days ago

Tech6 days agoThe Adder At The Heart Of Intel’s 8087 FPU

-

Entertainment2 days ago

Entertainment2 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Business2 days ago

Business2 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Business2 days ago

Business2 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Politics4 days ago

Politics4 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Crypto World3 days ago

Crypto World3 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World2 days ago

Crypto World2 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Sports4 days ago

Sports4 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

-

Crypto World2 days ago

Crypto World2 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Business2 days ago

Business2 days agoMHP SE 2026 Q1 – Results – Earnings Call Presentation (OTCMKTS:MHPSY) 2026-06-20

-

Business4 days ago

Business4 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

-

Crypto World4 days ago

Crypto World4 days agoAnthropic’s Dario Amodei Urged AI Unity at G7, Even as US Banned His Models

-

Tech2 hours ago

Tech2 hours agoMicrosoft accidentally kills epic Outlook email threads

-

Crypto World7 days ago

Crypto World7 days agoRobinhood opens AI-powered trading to all users, sending HOOD stock past $100

-

Tech5 days ago

Tech5 days agoWeeks Of In-The-Field Testing And A Verdict

-

Politics2 days ago

Politics2 days agoAndy Burnham and the meaning of Makerfield

-

Tech4 days ago

Tech4 days agoAdobe adds its AI assistant to Premiere, Illustrator and InDesign

-

Crypto World4 days ago

Crypto World4 days agoIren (IREN) Stock Surges on Jefferies Buy Rating: AI Infrastructure Play Gains Momentum

-

News Videos4 days ago

News Videos4 days agoIMPACT ON BITCOIN IF NO GOLD IS FOUND IN FORT KNOX

You must be logged in to post a comment Login