Crypto World

Bitcoin’s July Outlook Depends on These Key Factors

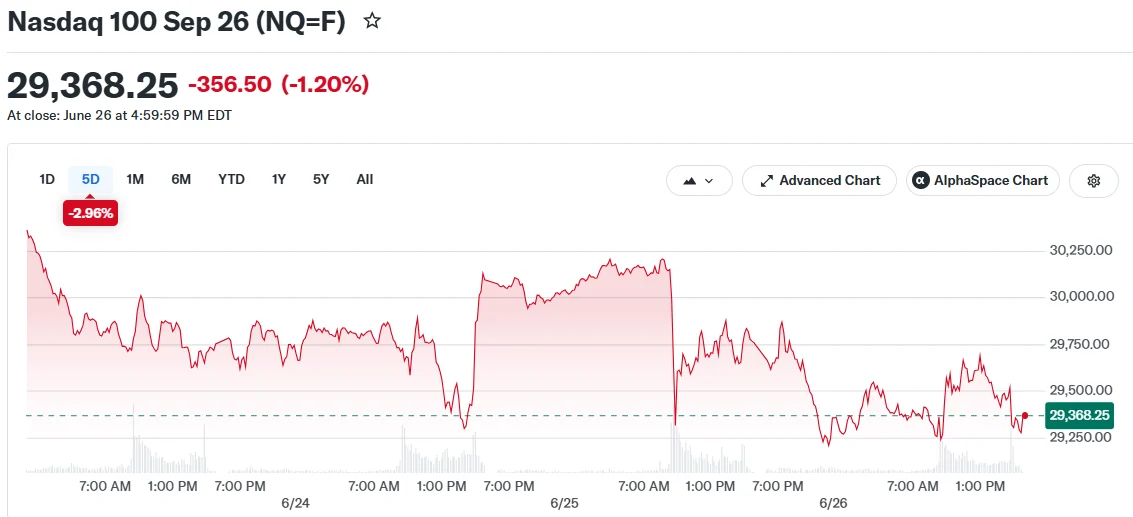

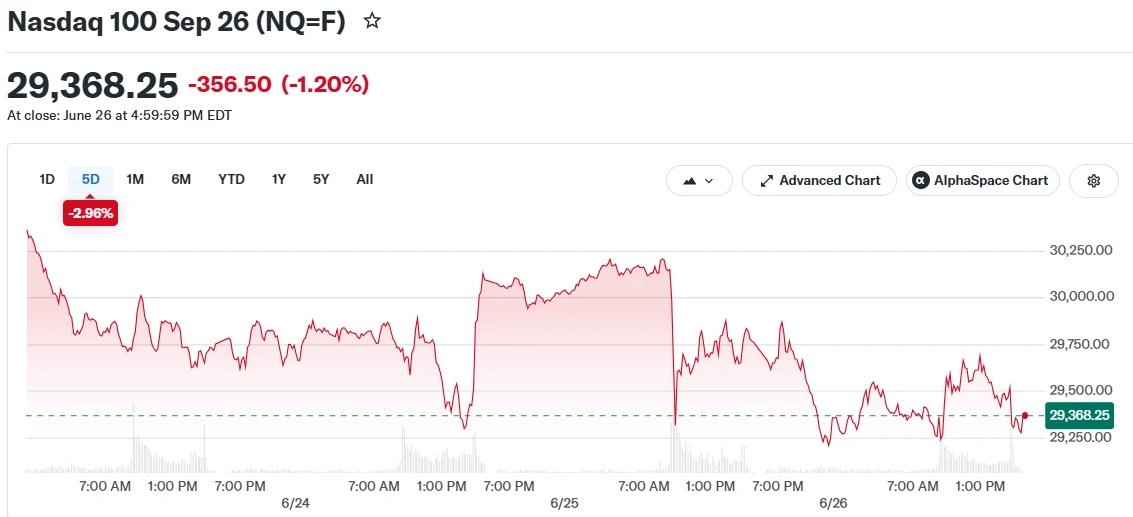

With just a few days left in June, it’s safe to say that bitcoin would require nothing short of a miracle to end the month in the green, as current data show a substantial 18% decline.

On-chain data depicts a few key factors behind BTC’s latest nosedive and what has to change for a stronger July.

Demand Lacks

In a recent post on X, popular analyst Ali Martinez explained that bitcoin accumulation levels have stalled for the past seven months.

“Bitcoin apparent demand has remained negative for 208 consecutive days, recently dropping to a new low of -273,000 BTC.”

The evident decline in this metric indicates that real spot market demand has fallen, as it compares new BTC creation to the movement of existing inventory. The trend change came after the massive liquidation event in early October, when over $19 billion was wiped out in a single day.

From November 9, 2025, to May 31, 2026, this demand “hovered quietly in negative territory between 0 and -150,000 BTC, indicating a mild but steady distribution of supply,” Martinez added. However, the metric plummeted to -273,000 BTC following the early and late June crashes and has “flatlined around this level.”

The metric remaining in negative territory for so long means a significant amount of old supply is entering circulation faster than the spot market can absorb it. This substantial divergence suggests that selling pressure continues to outpace new capital inflows, which is the first crucial factor that has to change for BTC to have a more robust and favorable July.

Just a few days ago, Martinez pointed to another metric showing no real demand for BTC but primarily from US investors. The Coinbase Premium remains deep in the red for nearly two months. More specifically, it went into negative territory after BTC peaked at over $82,000 in mid-May and has remained there ever since.

US institutional demand is key to bitcoin’s price moves and ranks as the second factor that has to change in July.

ETF Outflows

Aligned with the aforementioned developments, the spot Bitcoin ETFs have been on a massive withdrawal streak for weeks. The past week was no exception, as red dominated all days. On Thursday, the day BTC plummeted to $58,000 for the first time in almost two years, investors pulled out nearly $700 million from the funds.

Bitget Wallet’s Research Analyst Lacie Zhang told CryptoPotato that ETF outflows have to stabilize, and volatility will normalize after the massive options expiry event of $11 billion that took place on June 26.

“If redemptions resume and post-expiry positioning remains defensive, the market may stay choppy around current levels. The key point is that Bitcoin’s July direction may be shaped less by last week’s PCE print and more by how flows, leverage, and on-chain accumulation behave in the 72 hours after expiry settles,” she concluded.

The post Bitcoin’s July Outlook Depends on These Key Factors appeared first on CryptoPotato.

Key Takeaways

- Oracle shares plummeted 19% over the past week — the most severe weekly decline since August 2001

- The company’s market valuation has dropped approximately 55% from its September peak near $900 billion

- Capital spending exploded 162% to almost $56 billion during fiscal 2026

- The company’s debt load reached approximately $130 billion by late May, accompanied by nearly $24 billion in negative free cash flow

- Despite the selloff, 71% of Wall Street analysts maintain Buy ratings — a 15-year high

Oracle has just endured its most punishing week on the stock market in a quarter century. Shares tumbled 19% over five straight trading sessions, with daily losses exceeding 2.6% each day. The last time the enterprise software giant experienced such a devastating stretch was during August 2001, amid the dot-com bubble collapse.

The recent downturn represents more than just a bad week. Oracle’s market capitalization has contracted by roughly 55% since reaching approximately $900 billion last September.

Both the extended decline and this week’s brutal selloff share a common culprit: the escalating expenses tied to Oracle’s artificial intelligence strategy.

Oracle has committed heavily to AI infrastructure development, particularly through its involvement with OpenAI as part of the Stargate initiative. Constructing this infrastructure demands massive capital investment — and currently, shareholders are paying a hefty price.

Financial Metrics Paint a Concerning Picture

As of May’s conclusion, Oracle’s outstanding debt stood at roughly $130 billion. The company’s capital expenditure soared 162% during fiscal year 2026, hitting close to $56 billion.

Free cash flow registered at nearly negative $24 billion for the fiscal year.

To continue financing its infrastructure expansion, Oracle intends to secure an additional $40 billion in fiscal 2027 through combined debt and equity offerings. This follows the previous year’s $43 billion in debt issuance plus $5 billion raised through equity sales.

The fundamental challenge is clear: Oracle finds itself competing against Amazon, Microsoft, and Google in the race to construct AI data center capabilities — yet unlike these rivals, it cannot offer a comprehensive technology ecosystem. This constraint puts pressure on margins for what amounts to an extraordinarily expensive gamble.

Analyst Community Remains Largely Optimistic

Remarkably, analyst confidence hasn’t wavered despite the sharp decline. FactSet data shows 71% of ORCL analysts maintain Buy ratings — representing the strongest bullish sentiment in 15 years. The overall consensus stands at Strong Buy, reflecting 28 Buy recommendations, five Hold ratings, and zero Sell calls over the most recent three-month period.

The mean price target stands at $263.86, suggesting potential upside exceeding 77% from present levels.

Evercore, which holds a Buy rating on the stock, explained the situation in Wednesday’s research note: “We expect financing/leverage and the pace of equity issuance to remain the central investor debate near term, even as demand signals stay strong.”

This disconnect between professional analyst optimism and actual market performance represents the key narrative entering the following week.

As a footnote, Oracle co-founder Larry Ellison has also dropped several spots on global wealth rankings this week, falling behind Google’s co-founders, Jeff Bezos, and Michael Dell.

Key Highlights

- Starting July 1, AWS will implement a 20% price increase on reserved GPU compute resources, affecting Nvidia B200, B300, H100, and H200 processors.

- H200 pricing has now increased for three consecutive quarters — AWS GPU reservation costs have surged 20–50% since the start of the year.

- Wells Fargo reaffirmed its Buy recommendation on AMZN with a $312 price objective, viewing the increase as confirmation of cloud infrastructure pricing strength.

- Analyst consensus shows 57 Buy ratings on AMZN, with an average price objective of $312.78 — suggesting approximately 38.5% potential appreciation from current prices.

- Institutional shareholders control 72.2% of AMZN shares, with several major funds expanding their holdings during Q1 2026.

Amazon (AMZN) shares climbed 2.5% Thursday following Wells Fargo’s positive commentary on AWS’s latest 20% reserved GPU compute price adjustment, interpreting the move as evidence of robust pricing dynamics and sustained AI infrastructure appetite.

AMZN began Friday’s session at $232.69. The shares currently trade beneath their 50-day moving average of $255.53 while maintaining a position above the 200-day moving average of $234.13. The stock’s 52-week trading band extends from $196.00 to $278.56.

The pricing adjustments become effective July 1 and apply to multiple Nvidia processor architectures — including the B200, B300, H100, and H200 models.

Regarding the H200 particularly, this marks the third straight quarter of upward pricing pressure. AWS implemented a 15% H200 price increase in Q1, followed by 10% in Q2, and now an additional 20% entering Q3. Cumulatively this year, AWS GPU reservation pricing has escalated between 20% and 50% across different chip configurations.

Wells Fargo analyst Ken Gawrelski maintained his Buy recommendation while establishing a $312 price objective. His interpretation: the sustained pricing increases demonstrate that AI compute demand continues exceeding available supply, enabling hyperscale providers like AWS to transfer elevated infrastructure expenses to end customers.

Understanding AWS Reservation Pricing Dynamics

AWS reservation blocks enable clients to secure GPU capacity for periods extending up to six months. The willingness of customers to accept escalating prices for guaranteed access reveals the persistent tightness in available supply.

Wells Fargo recognized that these price adjustments may not translate immediately into revenue gains, given that certain clients operate under existing contractual arrangements. Nevertheless, the firm views this development as reinforcing AWS’s extended growth trajectory.

AMZN maintains a Strong Buy consensus rating throughout Wall Street. Among analysts providing coverage within the last three months, 44 assign Buy ratings while one assigns a Hold rating. The consensus price objective stands at $319.24, implying roughly 38.5% upside potential.

Recent price objective adjustments include: JPMorgan elevating its target to $330, Truist increasing to $320, Wolfe Research establishing a $320 target, and Deutsche Bank moving to $315.

Institutional Holdings and Additional Growth Drivers

Institutional ownership represents 72.2% of outstanding shares. Clark Asset Management acquired 4,879 additional shares during Q1, expanding its complete AMZN holdings to 38,238 shares valued at approximately $7.96 million. Arrowstreet Capital expanded its position by 21% in Q4, currently maintaining over 24.6 million shares worth roughly $5.7 billion.

Beyond GPU pricing developments, Amazon has several additional strategic initiatives underway. The company revealed a $13 billion commitment to India extending through 2030 for AI and cloud infrastructure expansion. Prime Day performance also appears promising, with industry observers anticipating record-breaking sales figures.

Regarding potential headwinds, EU regulatory authorities have suggested AWS could encounter more stringent competitive oversight — representing a possible concern for investors. Certain analysts have additionally expressed reservations regarding the company’s substantial capital investment requirements.

Amazon’s latest quarterly performance delivered $2.78 EPS, exceeding the $1.63 consensus estimate by $1.15. Revenue reached $181.52 billion, representing 16.6% year-over-year expansion.

CEO Andrew Jassy divested 20,000 shares on May 21 at $263.42 through a previously established 10b5-1 trading arrangement.

Ripple CTO emeritus David Schwartz has pushed back on a fresh social media debate over whether XRP existed before Bitcoin.

Summary

- Schwartz said Fugger’s 2004 idea was a payment network, not XRP or decentralized assets.

- XRPL history places XRP’s creation in 2012, years after Bitcoin launched in 2009 officially.

- The debate shows how older RipplePay ideas still drive confusion around XRP’s real origin.

The exchange began after Crypto Dyl News claimed on X that “Bitcoin was NOT the 1st” and that XRP was created in 1988.

That claim drew a question from XRP community user MitchRob, who asked Schwartz whether Ryan Fugger had conceptualized XRP and the XRP Ledger before or after Bitcoin. Schwartz replied that Fugger had conceptualized a decentralized payment and settlement network around 2004, well before Bitcoin.

Schwartz added one key limit to that answer. He said Fugger’s idea did not include decentralized assets. That distinction separates RipplePay, Fugger’s early payment concept, from XRP and the XRP Ledger, which arrived later.

Ryan Fugger built RipplePay, not XRP

Fugger’s RipplePay concept dates back to 2004. It focused on payments, IOUs and trust lines between users. It did not operate as a blockchain in the modern crypto sense, and it did not include XRP as a native asset.

Schwartz’s answer makes that point clear. He wrote that Fugger conceptualized a decentralized payment and settlement network “but without decentralized assets” around 2004. That means the idea came before Bitcoin, but XRP itself did not.

The official XRP Ledger history page places XRP’s launch in 2012. It says Schwartz, Jed McCaleb and Arthur Britto built a distributed ledger that aimed to improve on Bitcoin’s limits. The ledger included a native asset that became XRP.

The XRPL learning portal also says the three developers joined forces in 2011 to create a faster and more scalable digital asset. That timeline puts XRP after Bitcoin, not before it.

XRP origin debate continues online

MitchRob later asked whether Satoshi Nakamoto may have drawn any inspiration from Fugger’s earlier concepts. He also asked which network was built with a better framework for payments and settlement.

Schwartz had not answered that follow-up in the provided thread at the time of writing. The question remains speculative because no public evidence in the thread shows that Satoshi used Fugger’s work when designing Bitcoin.

The confusion comes from the Ripple name. Fugger’s RipplePay project came before Bitcoin, while the XRP Ledger came after Bitcoin. Ripple Labs later used the Ripple name, but the technical system behind XRP was built separately.

As previously reported, David Schwartz recently explained his XRP Ledger role after stepping back from daily leadership. The report noted that he remains CTO emeritus and one of XRPL’s co-creators.

XRPL history still matters

The debate comes as XRP Ledger development continues. In a previous article, crypto.news discussed Schwartz backing the XRP Ledger 3.2.0 upgrade, which renamed the core server software from rippled to xrpld.

That update moved XRPL further away from older Ripple-branded software names. It also added cleanup fixes for features tied to DeFi tools, vaults, lending, permissioned domains and token functions.

Previously, crypto.news explored XRPL’s growing tokenized finance use cases. Schwartz said XRPL use is expanding from payments into tokenized assets, stablecoins and other financial tools.

The latest exchange does not change XRP’s history. Fugger helped shape an early payment idea before Bitcoin. XRP and XRPL, however, began later as separate code written by Schwartz, McCaleb and Britto.

Cathie Wood has said that rising global instability has created the conditions for another Bitcoin rally as investors increasingly look for assets that can protect wealth across borders.

Summary

- Cathie Wood says capital leaving unstable countries could drive Bitcoin’s next major rally.

- Wood argues AI cannot replace Bitcoin’s role as a tool for protecting wealth during uncertainty.

- ARK Invest added $25.54 million in Coinbase, SpaceX, Circle, Bullish, and Robinhood shares.

According to a June 27 X post by ARK Invest founder Cathie Wood, capital leaving economically and politically unstable countries is likely to provide fresh momentum for Bitcoin and other digital assets.

She argued that while artificial intelligence has captured investor attention and a large share of market liquidity, it cannot replace the role digital assets play during periods of uncertainty.

Bitcoin remains a hedge against global instability

In her post, Wood said AI has launched a technological revolution and is attracting substantial investment, but described digital assets as a form of “insurance policy” for protecting wealth when confidence in traditional financial systems weakens.

She linked this view to growing capital outflows from less stable nations, saying those flows could “light another fire” under Bitcoin and the broader digital asset market.

Rather than competing directly, Wood suggested AI and crypto serve different purposes in today’s investment landscape. While AI companies continue drawing fresh capital because of their growth prospects, she argued that Bitcoin addresses a separate need by offering an alternative store of value that can move across borders more easily than many traditional assets.

Her comments come as investors continue weighing geopolitical tensions, inflation concerns, currency weakness in several regions, and uncertainty surrounding monetary policy. According to Wood, these conditions are increasing demand for assets that can preserve purchasing power while remaining accessible outside domestic financial systems.

The remarks also follow a post by ARK analyst Lorenzo Valente, who argued that many investors are overlooking crypto’s original purpose. Valente wrote that although the market has become increasingly institutional, digital assets should not be viewed only as risk-on investments because they continue to serve as financial protection in uncertain environments.

ARK continues adding crypto-related investments

Wood’s latest comments coincide with continued buying activity across ARK Invest’s exchange-traded funds.

According to ARK Invest’s latest daily trade disclosure, the firm purchased about $25.54 million worth of shares in Coinbase, SpaceX, Circle, Bullish, and Robinhood.

Coinbase represented the largest purchase by value. ARK acquired 68,366 shares through the ARK Innovation ETF, ARK Next Generation Internet ETF, and ARK Fintech Innovation ETF. Based on Friday’s closing price of $149.06, the transaction was worth about $10.19 million.

SpaceX ranked second after ARK bought 45,728 shares through four of its ETFs, including ARKQ and ARKX, for roughly $7.01 million using the company’s closing price of $153.23.

The investment manager also added 78,756 Circle shares valued at approximately $5.79 million, alongside smaller purchases of Bullish and Robinhood shares worth around $1.34 million and $1.21 million, respectively.

The latest buying activity is consistent with Wood’s positive view on financial markets despite ongoing concerns about inflation and interest rates.

As crypto.news previously reported, she said discussions with investors across Asia and Europe indicated many expect inflation to remain persistent and believe the Federal Reserve could tighten monetary policy further. Even so, Wood argued that incoming economic data points toward a different outcome.

Hong Kong has confirmed that its first regulated stablecoins are expected to enter circulation between the middle and second half of 2026 after two bank-backed institutions secured issuer licenses earlier this year.

Summary

- Hong Kong expects its first regulated stablecoins to launch between mid and late 2026 after licensing two bank-backed issuers.

- The HKMA says licensed issuers must hold eligible reserve assets and will remain under ongoing regulatory supervision.

- Hong Kong plans to expand crypto oversight with new rules for trading, custody, advisory, and management service providers.

According to a written reply by Secretary for Financial Services and the Treasury Christopher Hui to Hong Kong’s Legislative Council, the Hong Kong Monetary Authority (HKMA) granted stablecoin issuer licenses to two institutions with banking backgrounds in April 2026. Hui said the expected launch timeline is based on the institutions’ existing business plans.

The response also outlined how regulators intend to supervise the market after the rollout, saying the licensing framework is designed to support financial innovation while protecting users and maintaining monetary and financial stability.

Licensed issuers face reserve and supervision requirements

While confirming the launch window, the government said the HKMA had already considered the effect that regulated stablecoins could have on Hong Kong’s banking system before creating the licensing framework.

Under the Stablecoins Ordinance, which took effect in August 2025, licensed issuers must back their tokens with eligible reserve assets, including bank deposits and high-quality liquid debt securities. The government said those reserves must be placed with banks in Hong Kong, while the HKMA retains the authority to impose additional requirements if market conditions warrant.

Beyond the reserve rules, the central bank said it will carry out ongoing supervision once regulated stablecoins begin circulating and will continue assessing whether issuance affects bank deposits, lending activity, or overall financial stability.

At the international level, the government added that the HKMA is participating in studies led by organizations such as the Bank for International Settlements to examine how wider stablecoin adoption could affect traditional banking systems and to keep Hong Kong’s framework aligned with evolving global standards.

Separately, the government said the two licensed issuers are already participating in pilot projects involving central bank digital currency networks, tokenized deposits, and cross-border payment infrastructure. According to the reply, future adoption of these payment technologies will depend on demand across different use cases.

The announcement follows another digital payments initiative in Hong Kong. As previously reported by crypto.news, HKEX, and the HKMA recently began testing a wholesale e-HKD for derivatives trading, allowing clearing participants to use central bank digital currency for after-hours margin payments. The pilot is intended to improve settlement outside normal banking hours, although any commercial rollout remains subject to regulatory approval and operational readiness.

Enforcement expands as Hong Kong prepares more crypto rules

Alongside the rollout plans, the government said regulators have begun taking action against businesses that continue offering stablecoins without authorization.

According to the Legislative Council reply, the HKMA has issued letters to unregulated stablecoin providers explaining the legal requirements under the Stablecoins Ordinance and has continued monitoring whether those businesses comply. Depending on the circumstances, cases may be referred to the Police or the Department of Justice.

The Securities and Futures Commission (SFC) also shares information with the HKMA when it identifies suspected marketing of unregulated stablecoins to Hong Kong residents through its monitoring under the Anti-Money Laundering and Counter-Terrorist Financing Ordinance.

Looking beyond stablecoin issuance, the government said it will introduce legislation later this year covering virtual asset trading, custody, advisory, and management service providers to create a more comprehensive regulatory framework.

Officials also reiterated that regulated stablecoins are intended to function as blockchain-based payment instruments rather than speculative investments. The government warned that people who acquire unregulated stablecoins through unregulated channels do so at their own risk, while adding that financial regulators will continue public education campaigns and maintain updated lists of licensed entities.

Key Takeaways

- Shares of Moderna surged approximately 13% to $67.50, marking the highest closing price since September 2024, driven by announcements at its investor day presentation.

- The biotech firm introduced mRNA-6007, its inaugural in vivo CAR-T therapy program, aimed at autoimmune conditions such as lupus, with clinical trials scheduled to start in 2027.

- A unanimous 9-0 vote from an FDA advisory committee supported approval of Moderna’s influenza vaccine for individuals aged 50 and above, with a final FDA ruling expected on August 5, 2026.

- Jefferies analyst Andrew Tsai increased his price target to $53 from $45, while Piper Sandler’s Edward Tenthoff boosted his to $77, reaffirming an Overweight stance.

- Overall Street sentiment remains neutral with a Hold consensus rating and an average price target of $45.42 — suggesting potential downside from current price levels.

Shares of Moderna (MRNA) experienced a substantial rally on Friday, climbing roughly 13% to reach $67.50, positioning the biotech stock for its strongest close since September of last year. The impressive gain made MRNA the standout performer within the S&P 500 during the trading session. Intraday, shares briefly spiked nearly 15%, approaching the $69 level.

The surge was triggered by Moderna’s investor day presentation, during which the company unveiled an extensive expansion of its drug development pipeline that reaches far beyond its COVID-19 vaccine foundation.

MRNA has now advanced approximately 42% over the past 30 days, indicating a notable shift in market sentiment toward the stock.

The marquee reveal was mRNA-6007, Moderna’s inaugural in vivo CAR-T therapy program. The company intends to initiate clinical development by 2027, with an initial focus on B-cell-driven autoimmune disorders, particularly systemic lupus erythematosus.

Unlike conventional ex vivo CAR-T treatments that require removing patient T-cells, engineering them in laboratory settings, and reinfusing them, in vivo CAR-T therapy reprograms T-cells directly within the patient’s body. This approach offers greater efficiency and reduced costs.

Moderna isn’t the only pharmaceutical company pursuing this cutting-edge technology. Earlier this year, Eli Lilly acquired Orna Therapeutics primarily to gain access to its in vivo CAR-T platform. Notably, Lilly shares also rose 6% on Friday, boosted by favorable feedback from European regulators regarding its oral cancer treatment.

Strategic Roadmap Divided Into Three Phases

Moderna presented its strategic vision organized into three separate “horizons.” The initial phase emphasizes advanced, near-commercial assets, including current marketed products and late-stage pipeline candidates.

Jefferies analyst Andrew Tsai projects the company could launch more than seven new products spanning respiratory, oncology, and rare disease categories within the next two years. This would represent a significant expansion from its current portfolio of three approved vaccines.

Tsai highlighted Phase III melanoma trial results, anticipated in the latter half of 2026, as a critical upcoming milestone, describing it as “a major event” for shareholder value. He maintains a Hold rating while elevating his price target to $53 from the previous $45.

Another program drawing considerable attention is mRNA-4194, Moderna’s pioneering cancer prevention therapy designed for Lynch syndrome patients. Additionally, the company is progressing with mRNA-1195, its multiple sclerosis candidate, which should generate preliminary data later in 2026.

Influenza Vaccine Provides Additional Momentum

Beyond oncology and autoimmune therapeutics, Moderna received encouraging news regarding its flu vaccine candidate mRNA-1010 when an FDA advisory committee delivered a unanimous 9-0 vote recommending approval for adults 50 years and older.

The FDA’s final determination is scheduled for August 5, 2026. Approval would provide the company with another revenue-generating product independent of its COVID franchise.

Piper Sandler analyst Edward Tenthoff elevated his price target to $77 from $69 and maintained an Overweight rating, citing the substantial progress showcased during the investor day event.

However, despite positive reactions from select analysts, the broader Wall Street consensus remains at Hold, comprising two Buy ratings, 19 Hold ratings, and three Sell ratings across the past three months. The consensus price target of $45.42 suggests more than 31% potential downside from current trading levels.

Crypto World

Qualcomm (QCOM) Stock Rockets 15% After Meta Partnership and Aggressive Data Center Goals

Key Takeaways

- Qualcomm increased its fiscal 2029 non-smartphone revenue forecast to approximately $40 billion from $22 billion

- The chip manufacturer established a data center revenue objective exceeding $15 billion by fiscal 2029

- Meta Platforms committed to a multi-year partnership utilizing Qualcomm’s Dragonfly C1000 server chip

- Automotive segment generated record $1.3 billion in Q2 FY2026, representing 38% growth year-over-year

- QCOM shares surged up to 15% following the announcement before moderating

During Wednesday’s investor presentation, Qualcomm unveiled an aggressive expansion strategy that sent Wall Street into a frenzy. The semiconductor company nearly doubled its fiscal 2029 revenue projection for non-smartphone segments, elevating the target to approximately $40 billion from the previous $22 billion goal announced in 2024. The stock rallied as much as 15% during trading.

The previous $22 billion projection was already considered ambitious for a corporation still predominantly associated with mobile phone processors. The revised figure signals that Qualcomm is making a substantial wager on markets outside traditional handsets.

The cornerstone of this transformation is the data center sector. Qualcomm introduced the Dragonfly C1000, a server chip featuring over 250 proprietary cores. Additionally, the company launched a portfolio of AI acceleration products specifically engineered for inference workloads rather than training applications. Leadership is pursuing more than $15 billion in data center revenue by fiscal 2029, starting from essentially zero currently.

To put this in perspective, Qualcomm generated $10.6 billion in total revenue during fiscal Q2 2026. Mobile chip sales accounted for approximately $6 billion of that figure. Data center contributions remain negligible at present.

The most significant announcement wasn’t technical specifications — it was customer validation. Meta Platforms committed to a multi-year, multi-generation agreement to deploy Qualcomm’s new processor across its data center infrastructure, with production scheduled to commence in the second half of 2028. Securing Meta as a launch partner lends substantial credibility to the data center initiative.

Meta Agreement Validates Data Center Strategy

Qualcomm’s innovative High Bandwidth Compute (HBC) architecture employs vertical chip stacking instead of traditional horizontal layouts, positioning memory and processing units in closer proximity. The manufacturer claims this configuration enhances data transfer rates and power efficiency.

The initial generation of this architecture is slated to debut in data center deployments next year, with widespread commercial availability anticipated in 2028. Qualcomm is simultaneously engaging with mobile device, personal computer, and automotive manufacturers about future integration of this technology into their products.

Executive Vice President Durga Malladi stated directly: “What starts in data centers is not going to end there.”

The AI250 accelerator, built on the HBC framework, won’t enter commercial sampling until mid-2027. Meta’s CPU manufacturing doesn’t begin until late 2028. These remain forward-looking milestones rather than realized revenue.

Automotive Segment Delivers Current Results

While the data center narrative focuses on 2028 and beyond, the automotive division is generating results today. Qualcomm reported record automotive revenue of $1.3 billion in fiscal Q2 2026, reflecting 38% year-over-year expansion. The company projects $10 billion in annual automotive revenue by fiscal 2029, supported by a design-win backlog the company estimates at approximately $65 billion.

This trajectory provides tangible evidence for the broader diversification thesis. The automotive business demonstrates the strategy can succeed beyond smartphones in at least one significant market.

From a valuation perspective, the stock trades at roughly 17 times non-GAAP earnings. That multiple sits well below broader market averages and significantly trails valuations assigned to leading AI semiconductor companies — indicating the market continues to view Qualcomm primarily through the lens of its smartphone chip business.

QCOM finished Thursday at $189.39, declining 7.57% for the session, retreating from Wednesday’s investor day-driven rally.

TLDR

- Brent crude plunged more than 4% to approximately $72 per barrel Friday; WTI declined 3% to roughly $69

- Commercial traffic through the Strait of Hormuz climbed to the highest volume since conflict escalated in late February

- An Iranian attack drone targeted a Singapore-flagged container vessel on Thursday

- US forces retaliated Friday with strikes against Iranian drone storage facilities, missile depots, and radar installations

- Crude prices staged a partial comeback in late Friday trading following confirmation of American military action

Crude oil markets experienced dramatic volatility on Friday, plunging in early trading before staging a recovery after the United States conducted military operations against Iranian targets in response to a drone assault on a commercial ship navigating the Strait of Hormuz.

Brent crude tumbled over 4% during regular trading hours, settling near the $72 per barrel level. West Texas Intermediate experienced a roughly 3% decline to approximately $69 — marking its first closing price beneath $70 since the Iran conflict intensified in late February. Both benchmark grades have now surrendered approximately 25–27% of their value during the past month.

The initial selloff occurred as maritime traffic navigating through the Strait of Hormuz climbed to its most robust levels since hostilities commenced. This development alleviated concerns regarding potential oil supply interruptions and applied downward pressure on crude valuations.

Factors Behind the Crude Selloff

Washington and Tehran finalized a 60-day memorandum of understanding during the previous week, temporarily halting active conflict. The agreement incorporates provisions for restoring commercial shipping operations through the Strait of Hormuz, alongside nuclear negotiations contingent upon sanctions relief.

As maritime vessels resumed more normal transit patterns through the strategic waterway, market participants reduced the conflict-related risk premium that had accumulated in oil futures.

Dennis Kissler, senior vice president at BOK Financial, cautioned on Thursday that the price correction might be excessive. “While the Strait of Hormuz is moving oil, there still exists the possibility of mines in the area as well as rogue Iranian militia continuing to make threats on shipping lanes,” he said. “The latest sell-off in prices is likely overstating the true near-term fundamentals,” he added.

The Drone Attack That Shifted Market Sentiment

On Thursday, Iran launched an attack on the Singapore-flagged container vessel Ever Lovely using what American officials characterized as a one-way attack drone. The commercial ship suffered damage during its passage through the strait.

President Trump expressed dissatisfaction with the assault on Friday. “I don’t like the fact that they took a shot,” he told reporters. “They shouldn’t be doing that.”

US Central Command announced that American military aircraft targeted Iranian missile storage locations, drone facilities, and coastal radar systems on Friday. The command characterized the operation as a “powerful response to yesterday’s attack.”

Iran’s Islamic Revolutionary Guard Corps claimed its forces “successfully repelled the attack.”

The military exchange generated renewed uncertainty about the sustainability of the ceasefire arrangement. Trump had previously indicated he would authorize resumed military operations if Iran breached the agreement’s provisions.

Notwithstanding the strikes, commercial shipping maintained its movement through the strait on Friday. Central Command confirmed it would continue facilitating safe passage coordination for commercial maritime traffic.

An outstanding issue involves whether Iran will implement transit fees for vessels passing through Hormuz. Oman informed European officials that certain tolls might eventually be imposed — a matter of continuing dispute between Washington and Tehran.

Crude oil prices climbed back above session lows in late Friday trading after confirmation of the US military strikes.

TLDR

- The Nasdaq Composite declined 0.2% Friday, marking its fifth consecutive session of losses, while the S&P 500 also retreated, with both indices recording weekly declines of more than 4% and nearly 2% respectively.

- Reports from the New York Times indicating OpenAI could postpone its public offering to 2027 intensified selling pressure in technology shares.

- Chip stocks experienced significant weakness following concerns about escalating memory and storage expenses after Apple increased pricing on MacBook and iPad products.

- Expectations of potential Federal Reserve interest rate increases strengthened following robust May Personal Consumption Expenditures data that sustained prospects for tighter policy.

- The Dow Jones outperformed competing indices with a modest weekly advance below 1%, benefiting from reduced technology sector allocation.

American equity markets experienced turbulence throughout the week, with technology shares bearing the brunt of investor anxiety. The Nasdaq Composite extended its losing streak to five consecutive sessions on Friday, settling 0.2% lower. The S&P 500 also registered modest losses. Both benchmarks concluded the week with substantial declines.

The Dow Jones Industrial Average shed a modest 56 points, representing a 0.1% decline on Friday. Despite the daily loss, the blue-chip index managed to secure a weekly gain of less than 1%. The Dow’s limited technology sector representation provided insulation from the broader selloff.

Artificial Intelligence Skepticism Fuels Market Weakness

Market participants have adopted a more cautious stance toward artificial intelligence investments. The sector confronted multiple headwinds this week, including questions about token economics and free cash flow generation, alongside intensifying competition from budget-friendly AI alternatives and Chinese rivals.

A New York Times article amplified the negative sentiment. The publication reported that OpenAI might delay its much-anticipated initial public offering from 2026 to 2027. This development dampened enthusiasm across the broader technology landscape.

Mizuho’s Daniel O’Regan, an analyst covering the sector, captured the prevailing sentiment. “Feels like every time I open Bloomberg or the WSJ there’s another negative AI headline,” he noted. He suggested the relentless stream of unfavorable coverage would likely continue unsettling individual investors.

Semiconductor manufacturers faced particularly acute pressure. Apple’s recent decision to increase prices on MacBook and iPad devices highlighted rising memory and storage component costs. Micron, a leading chipmaker, delivered solid quarterly results but cautioned that cost pressures would persist.

Hot Inflation Reading Revives Rate Hike Speculation

The Federal Reserve’s favored inflation gauge, the Personal Consumption Expenditures index, registered an elevated reading for May. This data point reinforced the possibility that the central bank might implement a rate increase this year, creating additional headwinds for growth-oriented and technology stocks.

Elevated interest rates typically present challenges for technology companies, whose valuations depend heavily on discounted future earnings projections. Any indication of potential borrowing cost increases disproportionately affects these securities compared to other market segments.

Nevertheless, not all indicators painted a bearish picture. Market breadth metrics remained constructive. Approximately two-thirds of S&P 500 constituents continued trading above their 200-day moving averages at week’s end.

David Donabedian, a senior investment strategist at CIBC Private Wealth, characterized the week’s price action as a recalibration rather than a structural breakdown. He observed that defensive sectors including health care, real estate, and consumer staples demonstrated resilience, while industrials and technology absorbed the heaviest losses.

Oil prices also retreated during the week. Brent crude declined to approximately $72 per barrel while West Texas Intermediate traded near $69. Shipping activity in the Strait of Hormuz persisted despite an incident involving a container vessel, alleviating some supply concerns. The United States and Iran reached agreement on a 60-day ceasefire, though regional tensions persist.

Investors now turn their attention to a holiday-shortened trading week ahead. The June employment situation report arrives Thursday and will receive close scrutiny for additional insights regarding economic momentum and monetary policy trajectory.

Key Takeaways

- SpaceX receives Nasdaq 100 inclusion effective July 7, carrying less than 1% index weighting and potentially generating $7.3 billion in passive investor demand

- The stock tumbled 17.2% during its inaugural trading week, reducing market capitalization from over $2.5 trillion to approximately $2 trillion

- Shares currently hover around the $135 initial public offering price after dipping beneath the $150 debut level

- The aerospace company completed a $25 billion bond offering that attracted $90 billion in demand, though the debt has accumulated roughly $305 million in unrealized losses

- Company insiders offloaded $1.2 million worth of shares during the previous three months without any recorded purchases

SpaceX (SPCX) concluded its inaugural trading week as a publicly traded entity at $153.23, representing a 17.2% decline from its market debut. This downturn compressed the company’s valuation from a zenith exceeding $2.5 trillion to roughly $2 trillion.

Space Exploration Technologies Corp., SPCX

Shares commenced trading at $150 and surged to $225.64 before experiencing a sharp reversal. The stock currently trades marginally above its $135 offering price — a critical threshold that market participants are monitoring intently.

Notwithstanding the challenging debut week, a significant market event looms. Nasdaq announced Friday that SPCX will enter the Nasdaq 100 index effective July 7. The aerospace manufacturer meets Nasdaq’s accelerated eligibility criteria, which permits recently public companies to qualify for index membership soon after listing.

Market analysts project the index inclusion may compel passive investment vehicles to acquire approximately $7.3 billion in SPCX shares. This purchasing pressure originates from both Nasdaq 100 and Russell index additions. The company’s allocation within the Nasdaq 100 will represent less than 1% of total index composition.

This wave of passive capital inflows might deliver short-term price stability. However, the company’s underlying financial metrics present a more nuanced picture.

Recent Debt Offering Raises Eyebrows

On Tuesday, SpaceX executed a $25 billion bond transaction. The offering generated approximately $90 billion in investor interest and was expanded from an original $20 billion target. Initial reception appeared robust.

Nevertheless, the bonds have underperformed since issuance. Bloomberg data indicates the debt has generated paper losses approaching $305 million when measured against comparable US Treasury securities.

Certain Wall Street observers are questioning the rationale behind a massive debt raise immediately following one of history’s largest initial public offerings. The consecutive capital-raising activities have sparked market skepticism.

Ludovic Subran, chief investment officer at Allianz, commented during the FT Global Insurance Summit that the SpaceX transaction demonstrates markets transitioning “from a stretched boom into bubble territory.”

Financial Metrics Raise Red Flags

SpaceX registers a GF Score of merely 12 out of 100, indicating subpar performance across profitability and balance sheet strength metrics. The enterprise reported a net margin of -26.44% alongside an operating margin of -11.05%.

The company’s price-to-sales ratio stands at 79.15 — an elevated valuation multiple that embeds expectations of substantial future expansion.

Corporate insiders divested $1.2 million in equity over the preceding three-month period. Zero insider acquisitions were documented during this timeframe.

In separate developments, the Financial Times disclosed SpaceX is evaluating a direct-to-consumer mobile service leveraging Starlink’s satellite-to-phone technology. This initiative would position the company as a retail wireless provider in direct competition with traditional telecommunications carriers.

OpenAI has reportedly postponed its own public listing plans, a decision market observers interpret as evidence of waning investor appetite for artificial intelligence-related equities.

SpaceX’s official Nasdaq 100 membership becomes effective July 7.

Hotter Chip Prices Are Just One of Many Summer Tests for Wall Street

Oracle (ORCL) Stock Plunges 19% in Worst Weekly Decline Since Dot-Com Era

Lukas Gage On Being ‘Fearful’ Of Coming Out As Gay

-

Entertainment7 days ago

Entertainment7 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports4 days ago

Sports4 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech5 days ago

Tech5 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion19 hours ago

Fashion19 hours agoWeekend Open Thread: Staud – Corporette.com

-

Business7 days ago

Business7 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics1 day ago

Politics1 day agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics1 day ago

Politics1 day agoPotential 2028er World Cup attendee leaderboard

-

Business1 day ago

Business1 day agoAsia stock markets slide as tech shares slump

-

Tech2 days ago

Tech2 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World3 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World2 days ago

Crypto World2 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business3 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Sports15 hours ago

Sports15 hours agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World7 hours ago

Crypto World7 hours agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World19 hours ago

Crypto World19 hours agoRTX holders must register wallets before token distribution begins

-

Crypto World22 hours ago

Crypto World22 hours agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Sports2 days ago

Sports2 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Tech6 days ago

Tech6 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Crypto World1 day ago

The DATA Foundation Launches to Tackle AI’s Multi-Billion Dollar Training Data Bottleneck

You must be logged in to post a comment Login