Crypto World

Aave Confirms Aavenomics 3.0 Is Live With Buybacks and DAO Spending Cut

Aave’s governance framework confirms that Aavenomics 3.0 is now active, with automated AAVE token buybacks running and DAO operational spending reduced, completing a governance roadmap the protocol has built toward since mid-2024. The activation follows passage of the Aavenomics Part One ARFC and… Read the full story at The Defiant

Sony Interactive Entertainment is removing 551 purchased films from UK PlayStation Store accounts on September 1, 2026, citing content licensing agreements with StudioCanal.

The affected library spans decades of cinema, from Terminator 2: Judgment Day and Rambo: First Blood to Bridget Jones’ Diary, Pan’s Labyrinth, and Paddington. Customers who paid for those titles will lose access regardless of their purchase history.

When a Purchase is Not Ownership

Sony published a formal legal notice confirming the removal, attributing it to the expiration of its licensing agreement with StudioCanal. The notice offered no refunds or alternative compensation for affected buyers.

The situation exposes a structural reality most consumers overlook at checkout. A digital “purchase” on any platform-controlled storefront functions more like a temporary license than outright ownership.

Therefore, Sony and StudioCanal can modify or terminate that license, and the buyer absorbs the loss.

With 551 titles set for deletion, this is one of the largest single-event disappearances of purchased digital content in recent memory.

PlayStation Digital Ownership and the Gaming Parallel

The concern is not limited to films. When GTA 6 pre-orders opened this week, Rockstar confirmed that physical retail editions would include only a digital download code, with no disc.

For buyers who assumed a boxed copy meant a physical artifact they owned outright, that detail reinforced a growing unease. The GTA launch also sent shockwaves through crypto markets that same day, highlighting how far the digital ownership question now extends across gaming and finance.

Together, the two events make the same point. Across entertainment and gaming, consumers are paying for access, not ownership.

The Web3 Argument Gets Louder

Non-fungible tokens (NFTs) were built to address exactly this problem by creating on-chain, portable title deeds that no single platform can revoke. If StudioCanal had issued film rights as NFTs, Sony could not have overridden them.

Those tokens would remain in the buyer’s wallet, transferable and verifiable, independent of any licensing dispute between corporations.

That argument is gaining fresh credibility. Earlier this year, market observers noted a shift in the NFT sector away from speculation toward tangible utility, with digital ownership emerging as the strongest long-term use case.

Meanwhile, Worldcoin’s biometric identity push brought parallel questions about who controls proof-of-ownership in digital spaces into mainstream debate. Across the broader GameFi sector, 2026 has already seen renewed investor appetite for blockchain-backed digital economies.

The PlayStation film deletions may appear to be a routine licensing dispute on paper.

However, they crystallize a question that streaming, gaming, and digital media platforms have not resolved: when a platform changes its terms, what does a consumer actually own?

For blockchain advocates, Sony just provided the most mainstream illustration yet.

The post Sony Deletes 500+ Purchased Movies From PlayStation, Reigniting Blockchain Debate appeared first on BeInCrypto.

Jeremy Grantham, the GMO co-founder who called both the 2000 dot-com crash and the 2008 housing collapse, branded Bitcoin (BTC) “a useless, speculative mechanism” and predicted it would dwindle over the next few decades.

The veteran strategist built his critique around three failures he sees in crypto. Bitcoin pays no yield, holds no stable value, and fails as a usable currency in daily life, he argued.

Proof of Work, Proof of Nothing

Grantham singled out Bitcoin’s proof-of-work design for particular scorn. The energy burned to validate transactions, he argued, generates no economic benefit for society.

“Proof of unnecessary work shouldn’t be worth a bucket of warm spit, and it will not be.”

Bitcoin Falls Short as Money and Store of Value

Beyond the mining critique, he said Bitcoin does not work as a practical currency. Regular users do not accept it at the supermarket, and serious investors do not settle large transactions with it. Without a functioning transaction layer, the asset cannot claim monetary legitimacy, he added.

He also dismissed Bitcoin as a store of value. Unlike equities, it pays no dividend and generates no cash flow. In his view, that leaves speculators with nothing to anchor a fair price.

A Skeptic With a Record

Grantham’s warnings carry weight because of his track record. He flagged the dot-com bubble before 2000 and warned of the US housing collapse before 2008. His more recent AI bubble stock warning extended that thesis to US equities, where he now sees downside of up to 70%.

However, his timing is not always precise. His 2021 epic-bubble call on US stocks arrived early, as markets climbed before their 2022 correction.

The Bitcoin remarks land as BTC trades near $60,500, down sharply from its late-2025 peak above $126,000. US spot Bitcoin ETF records outflows of $6.35 billion over 30 days through mid-June, reflecting cooling institutional demand.

Earlier, Coinbase CEO’s Bitcoin outlook has also flagged AI infrastructure costs as a variable reshaping crypto capital flows.

Grantham is not alone in his skepticism. Peter Schiff has made similar bearish arguments, contending that Bitcoin holds no intrinsic value.

Whether Bitcoin’s current price holds key support in Q3 2026 will test both camps. Grantham predicted the decline would come gradually, over years or even decades, not all at once.

The post Billionaire Grantham Uses Extreme Words to Describe Bitcoin appeared first on BeInCrypto.

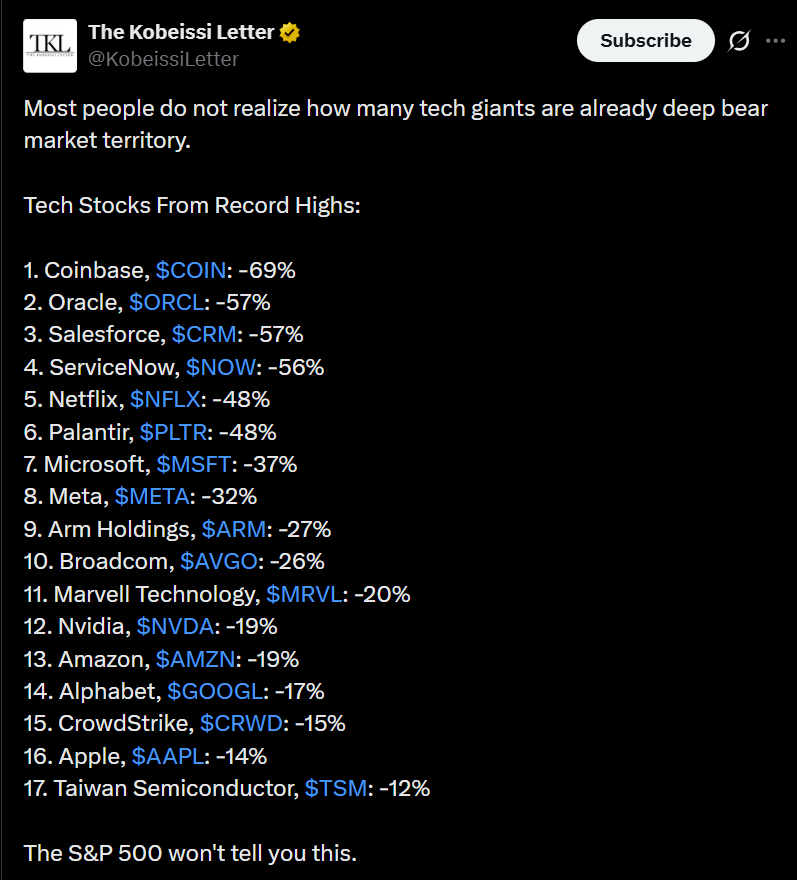

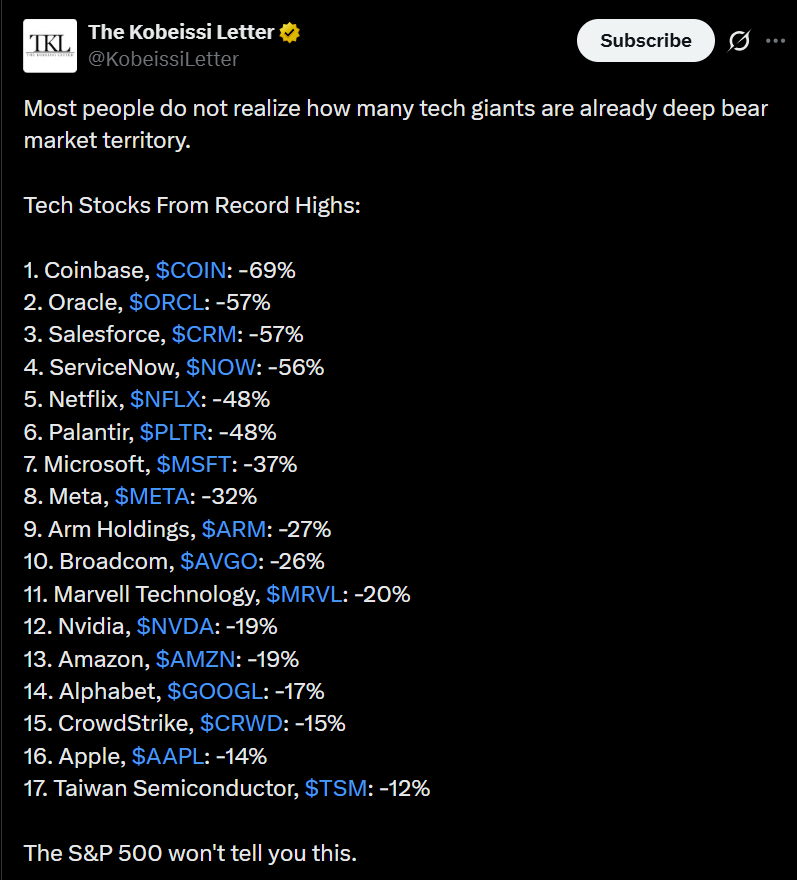

Stocks tied to digital assets are sliding faster than the broader US market, reinforcing an increasingly visible split between crypto-focused equities and the S&P 500. The latest comparison comes from The Kobeissi Letter, which points to steep drawdowns at major crypto businesses as technology selloffs ripple through risk assets.

According to The Kobeissi Letter, Coinbase and Circle shares are down 69% and 72%, respectively, from their all-time highs. Those declines outpace drops seen in several large technology names—such as Oracle, Salesforce, Netflix and Palantir—each down between 48% and 57% from peak levels, while the S&P 500 has retreated about 3.5% from its recent high.

Key takeaways

- Crypto-related equities are falling much more sharply than the S&P 500, according to The Kobeissi Letter.

- Investor pressure is tied not only to broader risk-off moves, but also to weaker digital asset markets and policy uncertainty in the US.

- Bitcoin’s drop below $60,000 and Ether sliding toward $1,500 have intensified selling across the sector.

- Corporate earnings stress is compounding the downturn, with Coinbase missing Wall Street expectations in its latest quarterly report.

- Despite continued institutional activity, 21Shares says crypto’s four-year market cycle remains a key driver of prices into 2026.

Crypto equities break away from the broader market

The widening gap between crypto-adjacent stocks and the S&P 500 appears tied to a combination of macro pressure and sector-specific risk. The pullback in technology equities reflects growing concerns that rapid advances in artificial intelligence could disrupt existing business models across parts of the sector. Within that environment, crypto businesses face additional headwinds.

Even as semiconductor stocks have managed to hold up better through periods of volatility, crypto-related shares have remained under pressure. The Kobeissi Letter’s comparison suggests the underperformance is not just a beta story tied to general market weakness—it also reflects how quickly public equities react to sentiment around digital asset performance.

Digital asset selling feeds equity declines

Market conditions in crypto have worsened alongside equities. The article notes that Bitcoin fell below $60,000 this week and extended its decline to more than 54% from its October peak. Ether has likewise faced heavy selling, recently dropping to around $1,500—about 69% below last year’s high.

When crypto prices slide, revenue expectations for exchanges, custody providers, and payments platforms can come under pressure, and investors often reprice the sector more aggressively than the general market. That dynamic helps explain why Coinbase and Circle have experienced drawdowns that exceed those of several major technology companies.

Broader digital asset policy is also part of the backdrop. The report points to uneven progress on comprehensive crypto market structure legislation in the United States, a factor that continues to influence how investors value the long-term prospects of crypto businesses.

Earnings disappointment adds another layer

Financial results have not helped. The coverage highlights that Coinbase reported first-quarter results that missed Wall Street expectations. As described in earlier reporting from Cointelegraph, the company’s revenue fell 21% from the prior quarter and it posted a loss of $1.49 per share, compared with analysts’ expectations for earnings of $0.27 per share.

For investors, earnings misses during a period of declining crypto market activity can have outsized impact: they reinforce concerns about transaction-driven revenues and trading volume sensitivity. In short, equity investors appear to be dealing with both the market-level hit from weaker coin prices and company-level pressure from the latest quarterly numbers.

21Shares trims 2026 expectations, but sees institutional progress

While public equities are under strain, institutional participation remains a key part of the crypto narrative. In a midyear outlook, 21Shares lowered its expectations for 2026, arguing that digital asset prices have underperformed relative to underlying fundamentals.

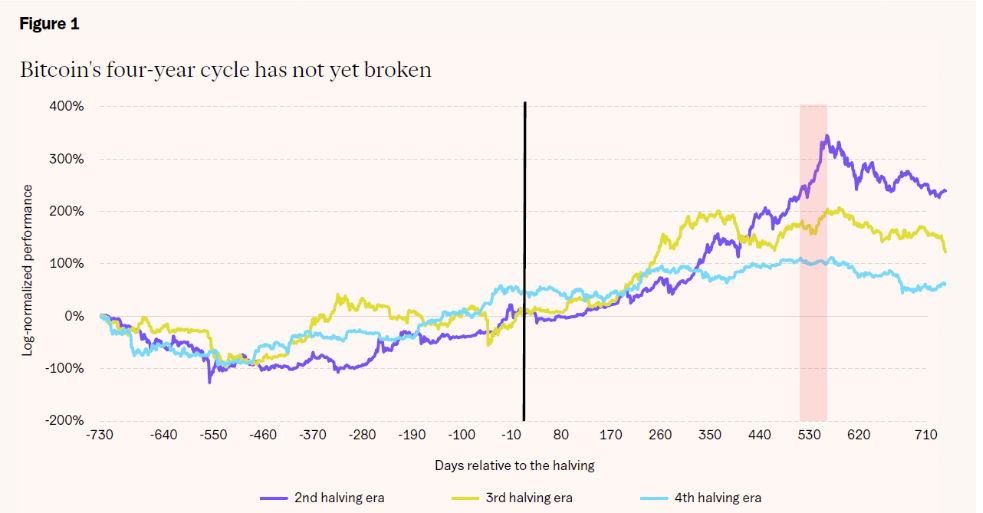

According to the report, institutional adoption is still strengthening—particularly in stablecoins, tokenization, and prediction markets. However, 21Shares emphasizes that the dominant force behind crypto prices continues to be Bitcoin’s four-year cycle.

In the same outlook, 21Shares states that increasing institutional ownership may have moderated Bitcoin’s drawdowns but has not fundamentally changed the asset’s cyclical behavior. The firm also indicated it previously forecast the four-year cycle could become obsolete, but has since walked back that view, saying the cycle is “evolving, but it has not broken yet.”

The argument matters for investors because it frames market volatility as more structural than purely sentiment-driven. If Bitcoin’s cycle remains intact, rallies could be more dependent on timing and macro liquidity than on incremental improvements in on-chain or institutional usage metrics—an outlook that can influence positioning across both crypto assets and crypto equities.

What to watch next

Investors will likely focus on whether crypto price action stabilizes—especially around the $60,000 level for Bitcoin and the $1,500 area for Ether—as well as whether upcoming corporate reports from major crypto platforms show earnings pressure easing or continuing. At the same time, market participants will watch how US legislative progress advances, since regulatory clarity (or its absence) continues to shape valuation assumptions for the sector.

Crypto World

AMLBot Puts Polymarket Phishing Toll at $3.1M Across 11 Wallets, Funds Traced to Ethereum

Blockchain intelligence firm AMLBot has fixed the total stolen in Thursday's Polymarket supply-chain attack at approximately $3.1 million in PUSD, providing the first forensically confirmed on-chain dollar figure and tracing the stolen assets from Polygon to Ethereum. On-chain investigator Specter,… Read the full story at The Defiant

The world’s largest altcoin felt the pain of the overall market weakness over the past week, dropping to just over $1,500 for the first time in well over a year.

The asset remains below key support levels, including $1,800, which holds a particular significance in its long-term potential, according to popular analyst Michaël van de Poppe.

ETH Below $1.8K Means…

The market observer believes ETH sliding below $1,800 is a “massive opportunity” and that day traders should avoid it, as it’s “not really attractive” here. The chart below paints a clear picture, showing that the asset has been in a clear downtrend for months. It peaked at almost $5,000 last summer, but it has plunged by nearly 70% since then to the current $1,600.

However, there’s finally light at the end of the tunnel as the asset is “making a potential strong bullish divergence on many levels that would indicate that ETH is going to follow Bitcoin.”

Perhaps the biggest catalyst for future price gains in the crypto market, especially for tokens like ETH, which some analysts believe would benefit more than BTC, is the CLARITY Act. The bill, expected to be signed into law in the US this year, should increase regulatory clarity on the entire market in the US.

Van de Poppe says ETH is currently following a classic “sell the rumor, buy the news” type of price action. He also named $1,505 and $1,385 as the next levels at which ETH would present a “tremendous buying opportunity” if it gets there. Overall, though, he believes markets are not eager to go down more, and he doubts ETH will drop to those levels.

“I much rather see a clear breakthrough at $1,800 and see these levels as strong opportunities to be accumulating more positions.”

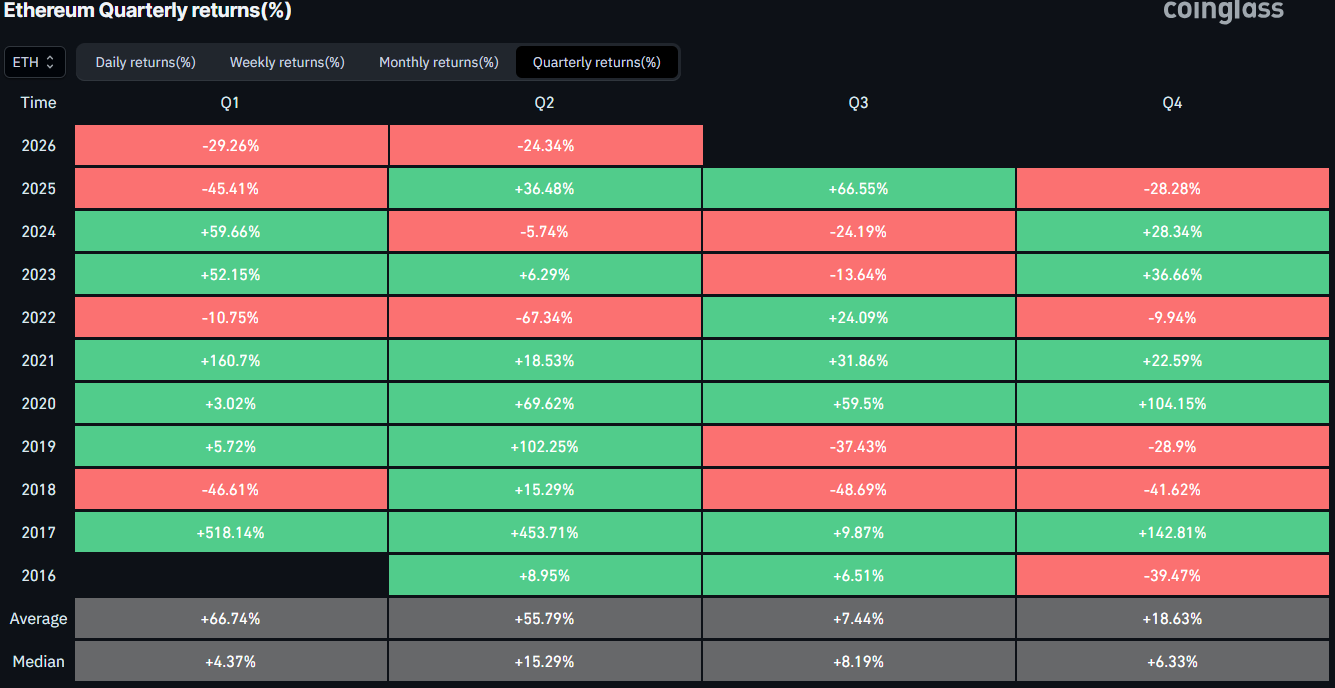

3 in a Row

Ethereum’s native token is just days away from creating history but in a negative manner by ending a third consecutive quarter in the red. Despite its previous bear cycles, it has never done this but it would require nothing short of a miracle to avoid it now. It closed with a 28.28% drop in Q4 2025, another 29.26% decline in Q1 2026, and is down by more than 24% in Q2 as of press time.

With June almost gone, investors have focused on July now. Ted Pillows brought some hope for the bulls, indicating that ETH has historically seen a bounce back in July. This has been particularly true in 2020, 2021, 2022, and 2025. ETH has posted notable gains in those July, all of which followed a red June.

The post Ethereum (ETH) Below $1.8K: What Does It Mean for Investors appeared first on CryptoPotato.

A pullback across US technology stocks is spilling into the crypto sector, and the market reaction is revealing a wider split between digital-asset equities and the broader S&P 500. Shares of Coinbase and Circle have fallen far more sharply from their peak levels than many large-cap technology names, underscoring how investors are treating crypto stocks as a higher-beta exposure to both risk sentiment and digital-asset fundamentals.

According to data cited from The Kobeissi Letter, Coinbase shares are down 69% from their all-time high, while Circle is down 72%. Those declines outpace drawdowns in several major technology companies—Oracle, Salesforce, Netflix and Palantir—each down roughly 48% to 57% from their peaks. By comparison, the S&P 500 has retreated about 3.5% from its recent high, suggesting crypto-linked equities are absorbing additional pressure beyond the general market rotation.

Key takeaways

- Crypto-focused stocks are declining much more than the S&P 500, pointing to company- and sector-specific risk on top of broad tech weakness.

- Sentiment has deteriorated alongside digital asset prices, with Bitcoin slipping below $60,000 and Ether falling to around $1,500.

- Operational stress is showing up in earnings: Coinbase reported results that missed expectations, including a quarterly revenue drop and a per-share loss.

- 21Shares says institutional adoption is improving some aspects of the market (notably stablecoins and tokenization), but the firm still sees Bitcoin’s four-year cycle as the key driver of price behavior.

Why crypto equities are moving differently from traditional tech

The immediate backdrop is a broad selloff in technology shares, but the crypto space appears to be reacting with additional intensity. The pressure is being linked to rising uncertainty that advances in artificial intelligence could disrupt existing business models within parts of the technology sector. While semiconductor stocks have generally held up better—despite volatility—crypto-related equities have remained under pressure amid weakness in digital asset markets.

Investors also appear to be weighing the pace of US policy progress on crypto market structure. The article notes uneven advancement toward comprehensive legislation in the United States, which can matter to publicly traded crypto firms that depend on clearer regulatory frameworks and more predictable market access conditions.

Digital asset price weakness adds fuel to equity declines

Market sentiment toward crypto has turned more cautious as Bitcoin and Ether extended their downturns. The report states that Bitcoin fell below $60,000 this week, widening its decline to more than 54% from its October peak. Ether, meanwhile, has faced heavy selling pressure, trading around $1,500—about 69% below last year’s high.

When crypto prices drop, equity investors often reprice more than just revenue expectations. They may also adjust assumptions about liquidity, trading activity, custody demand, and the overall risk appetite for crypto-exposed businesses. In that sense, the equity selloff can be interpreted as a compounding effect: traditional market weakness lowers risk tolerance, while falling token prices directly compress fundamentals for crypto-linked companies.

Coinbase results highlight how financial performance is getting tested

Beyond price action, corporate fundamentals are contributing to the negative tone. The article points to Coinbase’s first-quarter performance, stating that the exchange operator reported results that missed Wall Street expectations. According to the referenced coverage from Cointelegraph, Coinbase’s revenue fell 21% from the previous quarter, and the company posted a loss of $1.49 per share compared with analysts’ expectations for a profit of $0.27 per share.

Those numbers help explain why the stock reaction has been so pronounced during periods of weaker market conditions. In downturns, revenue for crypto platforms can be particularly sensitive to reduced trading volumes and tighter liquidity. Even when institutional participation grows, quarterly results can remain under pressure if broader market activity declines faster than new demand offsets it.

CoinShares data and other industry metrics often emphasize institutional adoption, but equity markets tend to react quickly to near-term earnings signals. In this case, the report suggests Coinbase’s fundamentals are worsening at the same time that the wider digital asset market is selling off.

21Shares trims its 2026 outlook while still tracking the four-year Bitcoin cycle

While crypto equities have been under pressure, at least one prominent asset manager is offering a more structured view of what to watch next. The article highlights a midyear outlook from 21Shares in which the firm reduced its expectations for 2026, arguing that digital asset prices have underperformed relative to the industry’s underlying fundamentals.

In the report, 21Shares says institutional adoption is still strengthening—particularly in areas such as stablecoins, tokenization and prediction markets. However, the firm’s central framework remains unchanged: Bitcoin’s four-year market cycle continues to exert the dominant influence on crypto prices.

21Shares notes that growth in institutional ownership has helped moderate Bitcoin’s drawdowns, but it has not fundamentally altered the cyclical behavior of the asset. The firm explicitly walks back an earlier position that the four-year cycle had become obsolete, stating that “Bitcoin’s cycle is evolving, but it has not broken yet,” as reported in the article.

That distinction matters for investors because it reframes “adoption” as a stabilizing force rather than an immediate cycle-breaker. Stablecoin usage, tokenization activity, and other institutional channels can support the ecosystem even when price trends lag, but if Bitcoin continues to follow its historical rhythm, broader market valuations may still face pressure until the cycle shifts.

What investors should monitor next

With crypto equities currently reflecting both a risk-off tech backdrop and renewed weakness in Bitcoin and Ether, the near-term signal investors will likely seek is whether fundamentals stabilize—particularly around trading volumes and quarterly reporting for major listed platforms. At the same time, 21Shares’ view suggests market participants should keep focusing on Bitcoin’s cycle dynamics even as institutional adoption expands; the question now is whether improved adoption can translate into clearer price recovery during the next phase of the cycle.

Robinhood says layoffs aren’t being driven by AI integration

According to a Forbes report published on June 4, 2026, AI has been the top reason cited for tech layoffs during 2026. Robinhood, however, seems to be taking a different tack.

Unlike BitGo, attributing its cuts to AI, Robinhood hasn’t indicated these layoffs were driven by AI adoption. The company’s stated reason is that it’s reducing management layers and streamlining operations to improve efficiency. And at this point, there is no clear evidence that Robinhood is replacing laid-off employees with AI.

That said, AI is likely part of the broader trend affecting how companies think about staffing. Rather than completely replacing employees, AI is often used to make existing teams more productive. Tasks involving research, customer support, coding, analysis and administrative work can frequently be handled faster and with fewer people than in the past.

As for service quality, users should probably expect the core user experience to remain largely unchanged. Functions such as trade execution, portfolio tracking, market data and charting are already highly automated.

The areas to watch are customer support and specialized assistance. AI can handle many routine questions effectively, but more complex issues, such as account restrictions, tax-related questions or crypto transfer problems, still benefit from human expertise.

Key Highlights

- Anthropic may receive clearance to reactivate its Fable 5 AI system following a 15-day suspension

- Final authorization from the Pentagon and NSA remains outstanding before full deployment

- Limited Mythos 5 access was reinstated on Friday by the Commerce Department for select users

- Commerce Secretary Howard Lutnick and Treasury Secretary Scott Bessent facilitated resolution discussions

- Anthropic and OpenAI are advocating for standardized government evaluation protocols for cutting-edge AI systems

According to a recent Axios report, Anthropic’s Fable 5 AI system may return to operation as soon as next week. The Trump administration is reportedly approaching a final determination to remove restrictions that have disabled the model since June 12.

The system went offline following a U.S. government export control directive that raised national security questions. The interruption disrupted access for numerous developers and enterprises who had integrated the technology into their workflows.

According to Axios sources with knowledge of the deliberations, the restrictions may be removed within the upcoming week. Dialogue between Anthropic representatives and government officials is anticipated to continue throughout the weekend.

However, universal approval hasn’t been achieved yet. Both the Pentagon and the National Security Agency must provide their authorization before the model can be reactivated. Several other government entities have already determined that the system poses no significant security risks for public deployment.

Commerce Secretary Howard Lutnick and Treasury Secretary Scott Bessent were instrumental in advancing negotiations. In correspondence to Anthropic, Lutnick acknowledged that the company “has worked with the US government to address risks” connected to both AI systems.

Partial Access Restored for Mythos 5

The Commerce Department granted Anthropic permission on Friday to reinstate Mythos 5 access for a select cohort of vetted users. Mythos 5 represents the more sophisticated version of the two systems and has never been released for widespread public consumption.

Both the Fable 5 and Mythos 5 platforms share the same foundational AI architecture. The primary distinction lies in their deployment strategy: Fable 5 targets general public accessibility, whereas Mythos 5 incorporates enhanced protective measures designed to minimize risks such as cyberattacks or biological weapons development.

The Significance of Fable 5 for Development Teams

Prior to its June 12 suspension, Fable 5 had gained substantial traction among software developers due to its superior coding and analytical functions. Payment processing firm Stripe allegedly utilized it to restructure a 50 million-line codebase within a single day—a task that would have required manual engineering efforts exceeding two months.

Following the suspension, automated development processes were interrupted, and certain organizations migrated their operations to alternative AI platforms, including more affordable Chinese-developed models.

The shutdown also occurred amid broader tensions between Anthropic and the Trump administration. Defense Secretary Pete Hegseth had previously characterized Anthropic as a “Supply-Chain Risk to National Security.” The anticipated reinstatement of Fable 5 signals a transformation in that dynamic.

An administration representative informed Axios that Anthropic “has worked positively with the government.”

Advocacy for Standardized Evaluation Framework

Both Anthropic and OpenAI are urging the Trump administration to establish a formalized assessment framework for advanced AI models prior to their public release. This initiative follows President Trump’s June 2 executive order that introduced voluntary government screening for powerful AI technologies.

OpenAI secured approval on Friday for a restricted preview of GPT-5.6. In an official statement, the organization expressed that it doesn’t believe government access mechanisms “should become the long-term default.”

Anthropic has similarly advocated for an evaluation process that is “transparent, fair, clear, and grounded in technical facts.”

A broad selloff in technology stocks has weighed even more heavily on crypto-focused companies, highlighting a growing divergence between digital asset equities and the broader US stock market.

Shares of Coinbase (COIN) and Circle (CRCL) have fallen 69% and 72%, respectively, from their all-time highs. Those declines exceed the drawdowns seen in several major technology companies, including Oracle (ORCL), Salesforce (CRM), Netflix (NFLX) and Palantir (PLTR), which are down between 48% and 57% from their peaks, according to data from The Kobeissi Letter

By comparison, the large-cap S&P 500 Index has retreated just 3.5% from its recent high.

Source: The Kobeissi Letter

The pullback in technology stocks reflects mounting concerns that advances in artificial intelligence could disrupt existing business models across parts of the sector. Semiconductor stocks have generally held up better despite bouts of volatility, while crypto-related equities have remained under pressure amid broader weakness in digital asset markets and uneven progress on comprehensive crypto market structure legislation in the United States.

Negative sentiment toward the sector has intensified after Bitcoin fell below $60,000 this week, extending its decline to more than 54% from its October peak. Ether has also come under heavy selling pressure, recently falling to around $1,500, roughly 69% below last year’s high.

Bear market conditions have also weighed on corporate earnings, with Coinbase reporting first-quarter results that missed Wall Street expectations. Revenue fell 21% from the previous quarter, while the company posted a loss of $1.49 per share, versus analysts’ expectations for a profit of $0.27 per share.

Related: Crypto Biz: The cost of stacking sats

Analysts downgrade crypto market’s 2026 outlook despite strong institutional adoption

The crypto market’s prolonged downturn has prompted analysts at 21Shares to lower their expectations for 2026, arguing that digital asset prices have significantly underperformed the industry’s underlying fundamentals.

In its midyear outlook, 21shares said institutional adoption continues to strengthen, particularly in stablecoins, tokenization and prediction markets. However, the asset manager argued that Bitcoin’s four-year market cycle remains the dominant force driving crypto prices.

According to the report, growing institutional ownership has helped moderate Bitcoin’s drawdowns but has not fundamentally altered its cyclical behavior.

Bitcoin’s price action this year suggests the four-year cycle remains intact. Source: 21shares

“Bitcoin’s cycle is evolving, but it has not broken yet,” 21Shares said, walking back its earlier forecast that the four-year cycle had become obsolete.

Related: Ethereum Foundation leadership exodus continues with director’s departure

Tokenized real-world assets crossed $30 billion on-chain in 2026, with BlackRock, JPMorgan, and Franklin Templeton leading the charge. This guide explains what RWA tokenization actually is, how it works, why the biggest names in finance are betting on it, and the risks the hype tends to skip.

Summary

- Real-world asset tokenization is the process of creating a blockchain token that represents legal or economic rights to an asset that exists off-chain, such as a Treasury bill, a property, or a bar of gold.

- The token is not the asset itself; it is an on-chain record of a claim on an off-chain asset, and that claim is enforced by legal structures, custodians, and jurisdictions outside the blockchain.

- The on-chain RWA market grew from roughly $5.5 billion in early 2025 to around $30 billion by mid-2026, led by tokenized US Treasuries near $12.9 billion and private credit around $19 billion.

- The momentum comes from traditional finance, not retail traders, with BlackRock, JPMorgan, Franklin Templeton, and others building tokenized funds and settlement systems.

- The promise is fractional ownership, 24/7 settlement, and programmability, but the risks are real: the token is only as strong as the legal structure, the custodian, and the regulatory wrapper behind it.

Real-world asset tokenization is the process of creating a blockchain-based token that represents legal or economic rights to an asset that exists in the traditional, off-chain world, such as a US Treasury bill, a share in a building, a unit of a money market fund, or a gram of gold held in a vault.

The single most important thing to understand at the outset is that the token is not the asset. When you hold a tokenized Treasury, you do not hold the Treasury bill itself on the blockchain; you hold a digital record of a claim on an underlying bill that a custodian or legal entity holds on your behalf. The token is a convenient way to track and transfer ownership, but the actual legal and economic substance lives off-chain, in contracts, custody arrangements, and the laws of whatever jurisdiction governs the asset.

This distinction is the key to understanding everything else about real-world assets, often shortened to RWAs, because it explains both why tokenization is powerful and where its risks come from.

The reason RWA tokenization has become one of the most discussed topics in crypto in 2026 is that it represents a bridge between two worlds that have mostly stayed separate: the enormous, established markets of traditional finance, and the always-on, programmable infrastructure of blockchains.

The on-chain value of tokenized real-world assets grew from roughly $5.5 billion at the start of 2025 to around $30 billion by the middle of 2026, and the forces driving that growth are not retail speculators chasing the next memecoin but the largest financial institutions on earth.

This guide explains what RWA tokenization actually is, how the process works step by step, the main categories of assets being tokenized, why institutions are moving so fast, how RWAs differ from other crypto assets, a concrete worked example, and, crucially, the risks that the enthusiastic coverage often skips over. By the end, you should be able to tell the difference between the genuine innovation and the hype.

What a tokenized real-world asset actually is

Begin with a precise definition, because the term gets used loosely. A real-world asset, in the crypto sense, is any asset that exists outside the blockchain and has been given an on-chain representation through tokenization. The underlying asset can be tangible, such as real estate, gold, or commodities, or it can be a traditional financial instrument, such as a government bond, a corporate bond, a share of a fund, or a slice of private credit.

Tokenization is the process of issuing a token that stands in for defined rights related to that asset, so those rights can be tracked, held, and transferred on a blockchain. A useful working definition is this: an RWA token is an on-chain record of rights to an off-chain asset, enforced by legal and operational structures that exist outside the blockchain.

The phrase rights to an asset is doing important work in that definition, because what the token represents varies. In some cases, the token reflects fractional ownership of the asset itself. In others, it represents an entitlement to the cash flows the asset produces, such as the interest on a bond. In still others, it is a redemption right, a promise that the holder can exchange the token for the underlying asset or its cash value, or a claim secured by collateral.

What the token means in any specific case depends entirely on the legal structure behind it, which is why two tokens that both call themselves tokenized Treasuries can carry very different rights and protections. The blockchain provides a shared, transparent ledger for recording who holds what and for moving those holdings quickly, but it does not, by itself, create or enforce the underlying rights. That enforcement comes from the contracts, the custodians who hold the real asset, and the courts and regulators of the relevant jurisdiction. Tokenization, in short, changes the wrapper around the asset, not the asset itself.

How tokenization actually works

The lifecycle of a tokenized real-world asset connects the physical or financial world to the blockchain through a chain of legal, operational, and technical steps, and each link matters. It begins with asset selection and valuation, where an issuer identifies an asset suitable for tokenization and gets it properly valued, which, for real estate, means appraisals and, for private credit, means underwriting.

Next comes the legal structure, typically the creation of a special purpose vehicle, a separate legal entity that holds the underlying asset on behalf of token holders and defines their rights. This legal layer is the foundation of the whole arrangement, because it determines what holders actually own and what happens if the issuer fails. A well-designed structure with bankruptcy-remoteness, meaning the asset is insulated from the issuer’s other obligations, offers far stronger protection than a simple contractual promise.

With the legal structure in place, the token itself is issued, usually following an established standard such as ERC-20 for fungible tokens or specialized security-token standards built to carry compliance rules. Smart contracts, the self-executing programs on the blockchain, then handle much of the assets’ on-chain lifecycle, automating the minting of new tokens, transfer restrictions, distribution of yield such as interest or dividends, and the redemption process.

Because most tokenized RWAs fall under existing securities rules, compliance is woven throughout: many require identity verification, and once a holder is verified, their wallet address is often whitelisted, meaning the token can only be transferred to other approved addresses.

Custody arrangements guarantee that the real asset backing the token is held securely, and a redemption process defines how a holder converts the token back into the underlying asset or its value. Services such as proof-of-reserve attestations, which cryptographically confirm that the on-chain tokens are fully backed by real assets held with a custodian, and cross-chain interoperability standards that let tokens move between blockchains, are increasingly layered on top to build trust and avoid fragmented liquidity. The result is an asset that behaves like its traditional counterpart legally but moves with the speed and programmability of crypto.

The main categories of tokenized assets

The RWA label covers a wide and growing range of asset classes, and each behaves differently, so it helps to know the major categories. By distributed value on public blockchains, tokenized US Treasuries are the largest single category, at roughly $12.9 billion in 2026, prized because they bring the steady, low-risk yield of government debt on-chain in a form that settles 24/7 and can be used inside decentralized finance. Closely related are tokenized money market funds, which package short-duration government debt into a single yield-bearing token. Private credit is the other giant of the sector, with active on-chain private credit around $19 billion, representing loans to businesses that produce yield for token holders, and depending on how it is measured, private credit may be the largest category of all.

Beyond those two, tokenized equities and exchange-traded funds let investors hold on-chain exposure to stocks, though most such products provide economic exposure to a stock’s price and dividends rather than direct share ownership or voting rights, a distinction regulators have drawn sharply. Commodities, dominated by gold-backed tokens such as PAXG and XAUT, rose sharply to around $5.5 billion as gold itself climbed, each token backed 1-to-1 by physical metal in a vault.

Real estate tokenization lets people buy fractional stakes in properties and receive a share of rental income, lowering the entry cost of a market once reserved for the wealthy. Bonds, both government and corporate, round out the core categories.

It is worth noting that stablecoins, which are technically tokenized claims on real-world reserves like dollars, are usually tracked separately because of their enormous scale, around $300 billion, and their distinct role as payment instruments rather than investments. The breadth of these categories is part of why advocates describe tokenization as potentially touching nearly all of human economic activity, even if the reality today is concentrated in Treasuries, credit, and gold.

Why institutions are betting billions

The defining feature of the 2026 RWA boom, and what separates it from most crypto trends, is that the institutions driving it are the largest names in traditional finance rather than crypto-native startups. BlackRock, the world’s largest asset manager, has committed firmly to tokenization through its BUIDL fund, a tokenized money market fund that surpassed $2.5 billion in assets, and its chief executive Larry Fink has repeatedly described tokenization as the next generation for markets, comparing its current stage to where the internet was in 1996 and envisioning a future of one general ledger on which all assets are tokenized.

Alongside BlackRock sit Franklin Templeton with its BENJI token, Circle, Securitize, and the major banks: JPMorgan processes large volumes of tokenized transactions through its blockchain platform, while Goldman Sachs, HSBC, and UBS have explored or piloted tokenized issuances.

The reasoning behind these bets is a combination of efficiency and opportunity. Tokenization can consolidate the traditionally separate processes of distribution, trading, clearing, settlement, and safekeeping into a single layer, reducing the counterparty risk and operational cost that come from passing an asset through many intermediaries. It enables near-instant settlement instead of the days that traditional securities can take; it allows assets to trade around the clock, and it makes them programmable, so that compliance rules, yield distributions, and other functions can be automated in code.

For institutions managing vast portfolios, even modest efficiency gains translate into large savings, and the ability to offer clients 24/7 access and fractional products opens new markets. This is why the institutional move is best understood as a bet on the infrastructure of tomorrow’s financial system instead of a trade on today’s prices, and why forecasts from major consultancies, while varying widely, are strikingly large, with estimates of the tokenized market reaching figures from $2 trillion to $16 trillion by 2030. Whether those forecasts prove accurate or optimistic, the direction of institutional conviction is clear.

A worked example: tokenized gold

To make the abstract concrete, consider tokenized gold, one of the clearest illustrations of how RWA tokenization works in practice. A company that issues gold-backed tokens takes physical gold, held and audited in professional vaults, and issues tokens against it on a 1-to-1 basis, so that each token represents ownership of a specific quantity of gold, often one fine troy ounce. If the issuer holds a 400-ounce gold bar, it can issue 400 tokens, each backed by 1 ounce of that bar. A holder of 1 token owns the rights to 1 ounce of gold sitting in the vault, and can redeem the token for the physical metal or its cash value according to the issuer’s terms.

What tokenization adds to this otherwise ordinary gold ownership is the set of capabilities that come from the asset living on a blockchain. The token can be divided into very small fractions, in some cases as small as a millionth of a unit, so a person can own a tiny sliver of gold instead of a whole bar or coin. It can be transferred person to person in minutes, at any hour, without the logistics of moving physical metal. And because it is a programmable token, it can be used within decentralized finance, for example, as collateral to borrow against without selling the underlying gold.

The token’s value tracks the price of gold, because that is what backs it, so the holder gets the store-of-value characteristics of physical gold combined with the portability and programmability of crypto. This example captures the essence of the RWA thesis at the level of an individual asset: real-world value on one side, the flexibility of crypto infrastructure on the other, joined by a token whose worth depends entirely on the gold actually sitting in the vault and the legal right to claim it.

How RWAs differ from regular crypto

A common source of confusion is the difference between tokenized real-world assets and native crypto assets, and the distinction is fundamental to understanding what an RWA is and is not. Native crypto assets, such as Bitcoin or Ether, originate directly on a blockchain and have no claim on anything outside it. Their value comes from network activity, utility, governance roles, scarcity, and market demand, and they exist purely on-chain with no custodian or legal entity standing behind them holding a real-world counterpart. When you hold Ether, the asset itself is the on-chain token; there is no off-chain thing it represents.

A tokenized real-world asset is the opposite in this respect. Its value derives from an off-chain asset held by a custodian or structured through a legal entity, and the token is a representation of rights to that external asset instead of a self-contained on-chain asset. This difference shapes nearly everything about how the two are treated. RWA tokens typically fall within securities classifications because they reflect ownership, economic rights, or claims linked to a financial instrument, which means they usually require compliance, regulated custody, and clear legal documentation.

Native crypto tokens are often classified as utility tokens and regulated, where they are regulated at all, under different frameworks. A useful way to hold the distinction in mind is that tokenization does not change the regulatory nature of the underlying product: if an asset is treated as a security in the traditional world, it will generally be treated as a security once tokenized, because the token is just a new wrapper around the same legal substance. Crypto-native assets, having no such off-chain substance, sit in a different regulatory category entirely.

Risks and what can go wrong

For all the genuine promise of RWA tokenization, the risks are real and specific, and an honest understanding of them is essential before treating any token as a reliable claim on a real asset. The foundational risk is that the token is only as good as the legal structure behind it.

Because the enforceable rights live off-chain, a token’s value in a crisis depends on whether the legal arrangement actually holds up, and a well-designed special purpose vehicle with bankruptcy-remoteness offers far stronger protection than a loose contractual promise.

If the issuer becomes insolvent, the legal structure determines whether holders recover anything, which makes the quality of that structure the single most important thing to evaluate.

The other risks build on this foundation. Counterparty and custodial risk means that holding a tokenized Treasury requires trusting that the custodian actually holds the underlying bills and that the issuer will honor redemptions; if the custodian suffers a breach or the issuer fails, holders can face losses regardless of how sound the blockchain is.

Regulatory uncertainty is significant because the treatment of RWA tokens remains unsettled in many jurisdictions, and tokenization does not exempt an asset from securities laws. Smart contract and oracle risk means that bugs in the code, or manipulation of the price feeds some tokens rely on, can affect how the token functions.

Liquidity and redemption constraints are a practical danger: many RWA tokens restrict transfers to whitelisted, identity-verified addresses, and redemption may be limited to the issuer or approved purchasers, so a token that looks liquid can become hard to exit under stress, which is often the most underappreciated risk.

Issuers also typically hold administrative keys that let them pause transfers, blacklist addresses, or upgrade contracts, introducing a degree of central control. And it is worth remembering that only a small fraction of tokenized RWAs, around $2.5 billion of the roughly $30 billion on-chain, is actually active in decentralized finance, because compliance rails limit open-market use.

The blunt summary is that tokenization changes the wrapper, not the underlying exposure: an RWA token carries all the risks of the underlying asset plus a new set of technical, custodial, and legal risks layered on top.

Frequently Asked Questions

What is real-world asset tokenization in simple terms?

It is the process of creating a blockchain token that represents rights to an asset that exists in the traditional world, such as a Treasury bill, a property, or gold. The token is not the asset itself; it is an on-chain record of a claim on an off-chain asset, and that claim is enforced by legal structures, custodians, and jurisdictions outside the blockchain. Tokenization lets the asset be held, divided, and transferred on a blockchain with the speed and programmability of crypto, while the underlying legal and economic substance stays governed by traditional law.

What is the difference between an RWA token and a cryptocurrency like Bitcoin?

Bitcoin and Ether are native crypto assets that originate directly on a blockchain and have no claim on anything off-chain; their value comes from network activity, scarcity, and demand. An RWA token is the opposite: its value derives from an off-chain asset held by a custodian, and the token represents rights to that external asset. Because of this, RWA tokens usually fall under securities rules and require compliance and regulated custody, while native crypto tokens are typically treated differently. Tokenization does not change an asset’s legal nature, so a security stays a security once tokenized.

How big is the RWA tokenization market?

The on-chain value of tokenized real-world assets grew from roughly $5.5 billion in early 2025 to around $30 billion by mid-2026. Tokenized US Treasuries are the largest category by distributed on-chain value at approximately $12.9 billion, while private credit is around $19 billion and may be larger depending on the measurement. Tokenized gold rose to about $5.5 billion. Stablecoins, technically tokenized dollar claims, are tracked separately due to their roughly $300 billion scale. Forecasts for 2030 vary widely, from $2 trillion to $16 trillion.

Which companies are driving RWA tokenization?

The leaders are major traditional finance institutions instead of crypto startups. BlackRock’s BUIDL tokenized money market fund surpassed $2.5 billion, and its chief executive has called tokenization the next generation for markets. Franklin Templeton issues the BENJI token, JPMorgan processes large volumes of tokenized transactions through its blockchain platform, and Circle, Securitize, Goldman Sachs, HSBC, and UBS are all active. This institutional involvement is the defining feature of the 2026 RWA boom and the main reason it has continued to grow even while other parts of the crypto market struggled.

What can be tokenized?

In principle, almost anything of value, which is why advocates describe the potential market as enormous. In practice today, the activity is concentrated in US Treasuries and money market funds, private credit, commodities such as gold, equities, and exchange-traded funds, real estate, and bonds. Smaller emerging categories include non-US government debt, private equity, carbon credits, and art. Each category behaves differently in terms of risk, yield, and liquidity, and the legal structure varies by asset and jurisdiction, so the experience of holding a tokenized Treasury differs significantly from holding tokenized real estate or private credit.

Is RWA tokenization safe?

It carries real risks that should be understood before treating any token as a reliable claim. The token is only as good as the legal structure behind it, and in an issuer’s insolvency, recovery depends on how well that structure is designed. There is counterparty and custodial risk, regulatory uncertainty, smart contract and oracle risk, and liquidity constraints, since many RWA tokens restrict transfers to whitelisted addresses and limit redemption. Tokenization changes the wrapper, not the underlying exposure, so an RWA token carries all the risks of the underlying asset plus new technical, custodial, and legal risks. Careful due diligence on the issuer, custodian, and legal structure is essential.

This article is educational information, not financial, legal, or tax advice. Market sizes, products, and institutional activity reflect reporting available as of June 26, 2026, and the RWA sector is evolving quickly. Tokenized real-world assets carry significant risks and are not suitable for everyone. Verify current details and the specific legal structure of any product from primary sources, and consider your own circumstances before making any decision.

The hospital waived two-thirds of the fees for patients facing financial hardship.#thepitt #shorts

Quartets shine at the Ladies Association of British Barbershop Singers prelims!

Sony Deletes 500+ Purchased Movies From PlayStation, Reigniting Blockchain Debate

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Blockchain.com files with SEC for U.S. IPO

Renter of Home in Anne Heche Crash Denies Settlement With Son

The hospital waived two-thirds of the fees for patients facing financial hardship.#thepitt #shorts

XRP IS COLLAPSING!!! Here’s What They Aren’t Telling You!

BEHIND CLOSED DOORS: CLARITY Act SHOWDOWN puts crypto in Trump’s crosshairs

-

Entertainment7 days ago

Entertainment7 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports4 days ago

Sports4 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech5 days ago

Tech5 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread: Staud – Corporette.com

-

Business7 days ago

Business7 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics1 day ago

Politics1 day agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics2 days ago

Politics2 days agoPotential 2028er World Cup attendee leaderboard

-

Business1 day ago

Business1 day agoAsia stock markets slide as tech shares slump

-

Tech2 days ago

Tech2 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World4 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World2 days ago

Crypto World2 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business4 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World13 hours ago

Crypto World13 hours agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports21 hours ago

Sports21 hours agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World1 day ago

Crypto World1 day agoRTX holders must register wallets before token distribution begins

-

Crypto World1 day ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Sports2 days ago

Sports2 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Tech6 days ago

Tech6 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Crypto World1 day ago

The DATA Foundation Launches to Tackle AI’s Multi-Billion Dollar Training Data Bottleneck

You must be logged in to post a comment Login