Crypto World

Base says same sequencer bug caused June 25 and 26 outages

Base has explained why its mainnet stopped producing blocks twice in two days.

Summary

- Base’s latest postmortem shows one sequencer bug caused two mainnet halts within two straight days.

- Funds stayed safe, but transaction queues overflowed as Base stopped producing new L2 blocks temporarily.

- The team plans stronger fuzz tests, load tests, monitoring, and recovery tools after the outage.

The Coinbase-backed Ethereum layer-2 network said both outages came from the same bug in its sequencer block-building logic.

The first outage began on June 25 and lasted about 116 minutes. The second began on June 26 and lasted about 20 minutes. Base said funds stayed safe during both incidents.

Sequencer bug stopped block production

In its official postmortem, Base said an invalid transaction failed during execution, as expected. The issue came after that failure, when stale journal state remained inside the block builder.

That stale state included accounts and storage slots touched by the failed transaction. When a valid transaction came next, the system used the wrong journal state and charged gas incorrectly.

This created a block with an invalid state transition. Other nodes could not accept the block, so the chain stopped producing new L2 blocks.

“The integrity of the chain was not compromised and all funds on Base were safe,” Base said.

The team added that block production resumed safely after mitigation.

Transactions queued during the halt

During the outages, users could not get new transactions included onchain. Base said transactions queued in the mempool while the chain waited for block production to recover.

The transaction pool later grew beyond what it could store. As a result, new eth_sendRawTransaction requests returned errors during the outage window.

The halt also affected sequencer and validator progress. Base said these nodes could not move beyond the invalid block until sequencing returned.

As previously reported, Base first flagged unhealthy block production on June 25 before engineers isolated a consensus problem tied to an invalid block.

Patch fixed stale state issue

Base said it fixed the main bug by applying a sequencer patch. The patch ensures journal state updates properly during execution after a failed transaction.

The team also found a second issue during recovery. Base said mitigation took longer because a race condition in the engine reset feature stopped sequencers from catching up after restart.

That second issue helped explain why the incident returned the next day. Base said the problem affected sequencers, not validator nodes, but it still slowed recovery.

The Base status page showed sequencing resumed on June 25. It also told ecosystem node operators to restart Base nodes if they were still stuck.

Testing and recovery changes planned

Base said it will strengthen protocol fuzz testing and load testing. These methods help teams find strange transaction patterns that may expose hidden bugs.

The team also plans better monitoring and operational checks. It said these changes should help engineers detect similar problems earlier and respond faster.

Base also wants to add graceful recovery to base-consensus. That change would make it easier for validator nodes to continue syncing after similar failures.

The outage came during a busy week for the network. Base also moved forward with its Beryl upgrade, which adds the B20 token standard and cuts the standard Base-to-Ethereum withdrawal period from seven days to five days.

The incident gives developers and users a clearer view of the weak point. Base has now named the bug, released a patch, and listed the tests it plans to improve.

Ethereum is trading near the $1,570 to $1,580 area after a calm weekend that failed to ease the pressure on the second-largest cryptocurrency.

Summary

- Ethereum trades near $1,570 as ETF outflows and whale selling pressure keep buyers cautious.

- Analysts see $1,583 as a key support level after whales sold 550,000 ETH this week.

- A clean move above $1,800 could ease pressure, while losing $1,583 may deepen losses.

The price has stayed mostly range-bound, even as new tension in the Middle East tested risk appetite across global markets.

The calm move does not mean the market has turned strong. ETH remains below the $1,800 level that many traders see as a key recovery zone. The asset is also under pressure from ETF outflows, whale selling, and weak spot demand.

ETF outflows weigh on Ethereum sentiment

U.S. spot Bitcoin and Ethereum ETFs recorded their seventh straight day of outflows on June 26, according to SoSoValue data. Spot Bitcoin ETFs saw about $445 million in net outflows, while spot Ethereum ETFs posted $12.848 million in net outflows.

The Ethereum outflow was smaller than Bitcoin’s, but the streak matters because ETFs can act as a source of steady spot demand. When flows stay negative for several days, that support weakens. This can make it harder for ETH to recover when traders are already cautious.

Earlier Ethereum ETF coverage showed that ETH had already been testing major support as fund withdrawals mounted. That pressure has continued into late June, keeping the market focused on whether institutional demand can return.

Another price analysis noted that ETH traded near $1,600 even after BitMine reportedly bought another 75,000 ETH. That showed that large purchases have not been enough to reverse the wider downtrend.

Whales sell into weak support

Analyst Ali Martinez said large holders sold about 550,000 ETH over the past week. At current prices, that sale equals roughly $880 million in fresh supply hitting the market.

The analyst said this selling helped push Ethereum below its immediate $1,633 support level. ETH is now testing volume support near $1,583, a level traders are watching closely because a clean break could open the way for deeper losses.

Ali said if selling continues into next week, the next high-volume demand areas could sit near $1,237 and $1,089. These levels are not guaranteed targets, but they show where past trading activity may attract buyers if ETH breaks lower.

This pressure matches the current chart structure. ETH continues to print lower highs, and buyers have not yet shown enough strength to reclaim the $1,800 area.

Analysts split on ETH’s next move

Money Ape warned that Ethereum could post three straight red quarters for the first time. The analyst said ETH may fall below $1,000 if market confidence keeps weakening.

That view reflects the bearish side of the current setup. Ethereum has failed to recover quickly from its slide, and traders remain worried about ETF outflows, whale activity, and weak momentum.

Michaël van de Poppe offered a different view. He said anything below $1,800 is not attractive for day trading but may be a strong opportunity for longer-term accumulation.

He also said ETH may be forming a bullish divergence across several timeframes. In his view, a clear break above $1,800 would be more useful than trying to catch every small move inside the current downtrend.

Van de Poppe also pointed to lower levels near $1,505 and $1,385 as possible buying zones if ETH sweeps liquidity. He said he doubts the market is eager to move much lower, but he still wants to see a clean recovery above $1,800.

Derivatives data shows sellers still in control

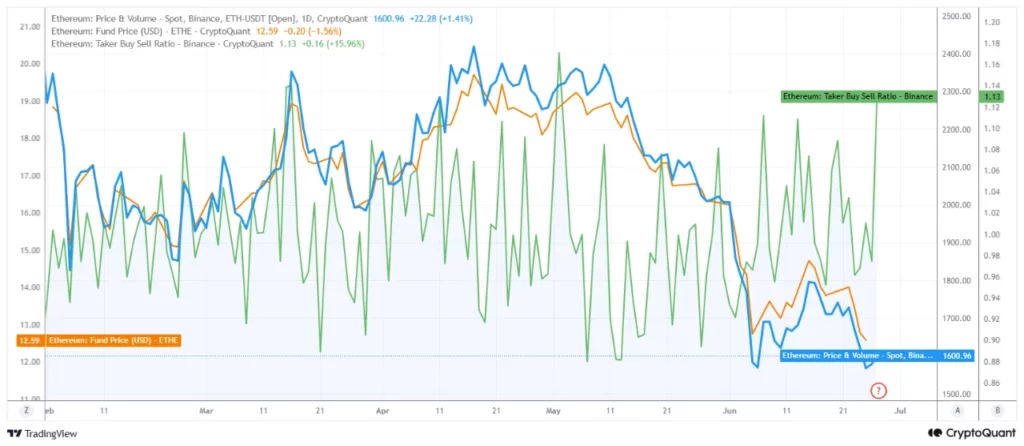

CryptoQuant analyst PelinayPA said Ethereum’s taker buy/sell ratio on Binance remains above 1. That usually points to stronger buying activity, but ETH has not reacted with a strong recovery.

The analyst said this muted response suggests larger sellers may be absorbing buy orders. In simple terms, buyers are active, but they are not strong enough to push the price higher.

The same report said Ethereum’s fund price has been falling since April. That suggests traders are reducing long exposure in derivatives markets and taking less risk.

This creates a weak setup for ETH. Even when buying activity rises, price action remains soft. That can happen when whales use short rallies to sell into demand.

The analyst said ETH still forms lower highs while fresh lows keep developing. That confirms the broader bearish structure remains in place until Ethereum breaks its current downtrend.

Ethereum price outlook

Ethereum’s near-term outlook now depends on the $1,583 support area. If buyers defend this zone, ETH could attempt another move toward $1,633 and then $1,800.

A clean break above $1,800 would be the first stronger sign that bulls are regaining control. It could also shift attention back toward higher resistance zones after weeks of weak trading.

If ETH loses $1,583, traders may look toward $1,505 and $1,385. A deeper sell-off could bring the $1,237 and $1,089 demand zones into focus if whale selling continues.

For now, Ethereum is stable but not strong. The price is calm near $1,570, yet ETF outflows, whale distribution, and weak derivatives demand keep the risk tilted toward another test of lower support.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

California’s Digital Financial Assets Law will take effect on July 1. It requires any firm conducting digital asset business activity with state residents to hold a DFAL license, and have a completed application on file with the DFPI, or cease covered operations. Right now, as of public records, no Ripple entity appears among applicants. XRP price has fallen below the $1.10 level at this moment of uncertainty.

DFAL covers the exchange of digital assets for fiat or other digital assets, their transfer between persons, custody, and the issuance of reserve-backed instruments. It maps directly onto Ripple’s California-facing operations: payments infrastructure, custody services, and the issuance and redemption of RLUSD, Ripple’s dollar-pegged stablecoin.

— SMQKE (@SMQKEDQG) June 26, 2026

BEGINNING JULY 1 2026 ONLY LICENSED CRYPTO COMPANIES WILL BE ALLOWED TO OPERATE IN CALIFORNIA

BEGINNING JULY 1 2026 ONLY LICENSED CRYPTO COMPANIES WILL BE ALLOWED TO OPERATE IN CALIFORNIA

Documented below.

https://t.co/0KRRRyDe1u pic.twitter.com/T1VIzh8AVR

https://t.co/0KRRRyDe1u pic.twitter.com/T1VIzh8AVR

Ripple’s existing portfolio of 40-plus U.S. money transmitter licenses does not automatically satisfy DFAL; the law is a separate regime administered by the DFPI through the Nationwide Multistate Licensing System.

However, there are three paths to legal compliance by July 1: hold a DFAL license, have a completed application pending with the DFPI, or qualify under a narrow statutory exemption, primarily available to banks, certain trust companies, and SEC- or CFTC-registered entities operating within already-regulated activity.

— WrathofKahneman (@WKahneman) June 19, 2026

Key date for @Ripple – July 1.

Key date for @Ripple – July 1.

Ripple previously engaged CA's DFPI for a DFAL license noting firms can keep operating if submit by 7/1/26. Public docs through March '26 don't list any Ripple entities, though likely filed. Necessary for all CA offerings, issue/redeem/custody. pic.twitter.com/xfQK4Z3IBc

Ripple has engaged with the process as the company submitted a formal comment letter to the DFPI, pushing to eliminate redundant money transmitter license requirements for DFAL-licensed firms. However, engagement is not the same as a filed application.

Law firms, including Chambers-ranked practices, have described DFAL as one of the most expansive state-level digital asset licensing regimes in the country.

Discover: The Best Crypto to Diversify Your Portfolio

Can XRP Price Hold $1 If Ripple Misses the DFAL Deadline?

XRP is trading near $1.10, far below the expected $2.50 many predicted. Recent price action reflects weak momentum, with sellers repeatedly capping rallies around the $1.15 to $1.20 area. Despite ongoing attention on Ripple’s regulatory developments, the market has yet to price in a decisive positive outcome.

Meanwhile, investors remain focused on several legal and regulatory milestones involving Ripple. The court’s earlier finding that XRP itself is not inherently a security removed a major uncertainty. However, the remaining penalty and injunction issues still matter because they could influence Ripple’s future business operations and market sentiment.

From a technical perspective, XRP must first reclaim the $1.15 to $1.20 zone before traders can discuss a stronger trend reversal. If buyers regain control and regulatory developments remain favorable, the next resistance area could emerge around $1.30 to $1.50. A sustained move above those levels would likely require a meaningful catalyst.

On the downside, support remains clustered around $1.05 and $1.00. If regulatory expectations weaken or broader crypto markets turn lower, those levels could come under pressure. The $1.00 mark remains an important psychological threshold, as a decisive break could invite additional selling.

For now, the market appears to be waiting for confirmation rather than trading on assumptions. Regulatory progress could improve sentiment, yet XRP’s longer-term trajectory will likely depend on both legal clarity and stronger demand returning to the market.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post California’s DFAL Clock Is Ticking: XRP Price Hanging in the Balance appeared first on Cryptonews.

For most of 2026, the CLARITY Act has been XRP’s one great catalyst, the bill that would write its commodity status into federal law. Now prediction markets put its 2026 passage at 42%, down from the low seventies, as a human-trafficking backlash, a banking-lobby fight, and a closing legislative window collide. Here is what the falling odds actually mean for XRP.

Summary

- Prediction markets now price the CLARITY Act’s chances of becoming law in 2026 at around 42%, down sharply from highs near 73% earlier in the year.

- The bill would codify XRP’s classification as a digital commodity into federal statute, the catalyst analysts say could unlock billions in institutional ETF demand.

- The odds fell as an anti-trafficking coalition attacked a decentralized-finance provision, the banking lobby fought stablecoin rules, and the path to 60 Senate votes narrowed.

- The legislative window is closing fast: the White House targeted a July finish, the Senate Banking and Agriculture versions still need reconciling, and the August recess effectively ends the year’s chances.

- For XRP, passage could open a path toward analyst targets of several dollars, while failure or delay removes its one Ripple-specific catalyst and leaves it moving with Bitcoin.

For most of 2026, XRP has had one great catalyst hanging over it, a single piece of legislation that holders have treated as the event capable of finally breaking the token out of its year-long range: the CLARITY Act, the crypto market-structure bill that would write XRP’s status as a digital commodity into federal law. For months the bill advanced, clearing the House, then a key Senate committee, and prediction markets priced its passage as increasingly likely, with odds climbing into the low seventies. That optimism has now reversed. As of late June, prediction-market data assigns roughly a 42% probability that the CLARITY Act becomes law in 2026, a sharp decline that reflects mounting trouble on several fronts at once.

A bill that looked, for a while, like it was on a glide path to the president’s desk now sits on a knife edge, and because XRP’s near-term thesis has been so tightly bound to it, the falling odds are a genuinely important development for anyone holding the token. The reason the odds matter so much is that the CLARITY Act is not just another crypto bill for XRP; it is the specific catalyst the market has been waiting on, the one event that could turn today’s favorable but fragile regulatory interpretation into durable statutory certainty. Spot XRP exchange-traded funds have launched and gathered over $1 billion, the token won legal clarity when its long battle with the securities regulator ended, and a later joint classification treated it as a digital commodity, but all of that rests on interpretive ground that a future administration could in principle reverse. The CLARITY Act would put XRP’s commodity status into actual law, removing the last layer of uncertainty that keeps large institutions on the sidelines, and analysts have projected that passage could unlock several billion dollars in additional ETF inflows.

This piece explains why the odds have fallen, the specific obstacles now in the bill’s path, the closing legislative window, and, most importantly, what each outcome, passage or failure, would actually mean for XRP’s price and prospects. The aim is to give holders a clear, grounded read on a catalyst that has become harder to handicap.

Why the odds fell

The decline from the low seventies to the low forties did not come from a single event but from a convergence of problems that have collectively made passage look less certain. The most striking new obstacle is a backlash centered on a specific provision of the bill. According to a letter obtained by a Washington publication, the Alliance to End Human Trafficking, a Catholic-backed anti-trafficking organization, urged Senate leaders to revisit a decentralized-finance provision in the CLARITY Act, warning that it could weaken safeguards against illicit finance. The concern centers on Section 604 of the bill, which would codify the Blockchain Regulatory Certainty Act.

Under that provision, software developers who build decentralized blockchain applications would not be held responsible for crimes committed by users of those platforms and would not be treated as money transmitters. The anti-trafficking group warned that this language could open regulatory gaps that make it harder for authorities to detect and track financial activity tied to crimes such as human trafficking. This kind of opposition is politically potent in a way that technical crypto disputes are not, because it reframes the bill from a question of market structure into a question of whether Congress is weakening tools used to fight trafficking. That framing gives wavering lawmakers a powerful reason for caution.

It is not the only pressure. The banking lobby has been fighting provisions related to stablecoin yield and what it characterizes as insufficient bank-equivalent regulation for stablecoin issuers, with prominent banking figures vowing to challenge the bill on the floor, because the CLARITY Act’s framework directly threatens traditional finance’s competitive position in payments. Layered on top is the simple arithmetic of the Senate, where advancing major legislation requires 60 votes to overcome a filibuster. With the governing party holding 53 seats, the bill needs at least seven crossover votes from the opposition, a structurally harder problem than the committee votes it has already cleared.

Each of these pressures, the trafficking backlash, the banking fight, and the vote math, has chipped away at the perceived likelihood of passage, and together they explain why the market has repriced the odds so sharply downward. That is also why the politics around the bill now matter as much as the market-structure text itself. The policy framework may be close, but the votes still have to survive a crowded field of objections before the bill reaches the president’s desk.

The provision at the center of the fight

It is worth dwelling on Section 604, because it has become the lightning rod, and understanding it clarifies why the bill suddenly looks more vulnerable. The provision would codify into law a principle that the crypto industry considers foundational: that developers who write the code for decentralized applications should not be treated as money transmitters and should not be held criminally liable for what users do with their software, in the same way that the makers of a web browser or an email protocol are not liable for crimes committed using those tools. To the industry, this is a basic protection for open-source software development, without which building decentralized systems in the U.S. becomes legally perilous. It is one of the reasons crypto firms have pushed so hard for the bill.

To critics, the same provision looks like a loophole. The anti-trafficking coalition’s argument is that by shielding decentralized-finance developers from money-transmitter obligations, the language could remove a layer of monitoring and accountability that helps authorities trace illicit funds, including money tied to human trafficking and other serious crimes. The dispute is, at its core, a genuine and difficult policy tension between two legitimate goals: protecting software developers and open innovation on one side, and preserving law-enforcement tools against financial crime on the other. That tension is precisely what makes the provision such an effective pressure point, because it cannot be dismissed as mere industry lobbying or partisan obstruction; it pits real concerns against each other.

For the bill’s prospects, the significance is that Section 604 gives opponents a substantive, morally weighted objection to rally around, and gives undecided senators a defensible reason to demand changes or withhold support. That is exactly the kind of friction that can stall legislation when the calendar is tight and the vote margin is thin. The bill does not only need supporters who like digital-asset clarity; it needs senators who are comfortable defending the developer-shield language under pressure from law-enforcement and anti-trafficking groups. That is a harder political task than simply explaining why tokens need a market-structure framework.

The legislative window is closing

Even setting aside the substantive fights, the CLARITY Act faces a brutal constraint that may matter more than any single objection: time. The legislative calendar for passing a controversial bill in 2026 is narrow and closing. The White House pushed for a finish around the July 4 holiday, a target that officials themselves conceded was tight, and the harder deadline is the August recess, after which campaigning for the autumn elections begins in earnest and the Senate’s floor schedule effectively closes to contested votes. Any realistic path to passage this year therefore runs through a small number of remaining legislative days, and every additional dispute consumes some of that dwindling supply.

Compounding the time pressure is a procedural step that the headline timeline often obscures: reconciliation between two Senate committees. The CLARITY Act’s framework splits jurisdiction over digital assets between the securities regulator and the commodities regulator, and because both the Senate Banking Committee and the Senate Agriculture Committee have claimed a stake, the Banking Committee’s version of the bill must be merged with the Agriculture Committee’s companion legislation before any floor vote can happen. That merger is not complete. The bill cleared the Banking Committee on a bipartisan vote in May and was placed on the Senate’s legislative calendar in early June, making it formally eligible for floor consideration, which is the closest it has ever been to becoming law.

But floor eligibility is not passage. To actually become law, the bill must still be reconciled across the two committees, survive a 60-vote floor vote, be reconciled again with the version the House passed, and then be signed by the president. Each of those steps takes time the calendar may not provide, and if the vote does not come before the recess, the political window that opened this opportunity may not reopen on the same terms. One senator who has championed the bill captured the stakes bluntly, saying they did not come this far to quit at the five-yard line, but the five-yard line in a closing window is exactly where bills die.

What passage would mean for XRP

For XRP holders, the entire point of tracking the CLARITY Act is what its outcome would do to the token, so it is worth being specific about both scenarios, beginning with passage. If the bill becomes law and codifies XRP’s digital-commodity status into federal statute, the most important effect would be the removal of the last meaningful layer of regulatory uncertainty, which is the gatekeeper that has kept large institutions cautious. XRP already enjoys more regulatory clarity than almost any major token after its legal battle ended and the joint classification treated it as a commodity, but that clarity rests on interpretive releases rather than statute, and a statute is far more durable. With permanent legal footing, the institutional capital that has waited on the sidelines, pension funds, asset managers, and the like, would have the certainty it needs to allocate.

The clearest channel for that capital is the spot ETF complex. Analysts at a major bank have projected that passage and the resulting clarity could drive several billion dollars of additional inflows into XRP exchange-traded funds, on the order of three to six times what those funds have gathered since launching. Flows of that magnitude would represent a demand shock large enough to push XRP through the resistance levels that have capped it and toward higher targets, with mainstream analyst forecasts in a passage scenario clustering in the several-dollar range by year-end. The more bullish projections reach higher still if a second catalyst, such as Ripple securing a Federal Reserve master account, were to follow.

The important caveat is that some of this may already be partly priced in, because the market has watched the bill advance for months, so the real question is not whether clarity helps XRP but how much of the waiting money actually moves once passage is law versus how much already has. Still, the directional case is clear: passage would be a powerful, fundamentally positive catalyst for XRP, the event that could finally connect the token’s long-promised institutional thesis to actual demand. It would also sit alongside another XRP catalyst in the spotlight, where holders have been trying to separate company-level events from token-level value. In this case, unlike many Ripple corporate developments, the statutory classification would apply directly to the token.

What failure or delay would mean

The other side of the ledger is just as consequential, and with the odds now below even, it deserves equal weight. If the CLARITY Act fails or stalls, whether by missing the legislative window, dying in the reconciliation process, or falling short of 60 votes on the floor, XRP would lose its one Ripple-specific catalyst, the single event distinguishing it from the rest of the market. In that scenario, XRP would likely revert to moving with Bitcoin rather than leading on its own regulatory story, surrendering the independent upside that the bill represented. The institutional flows that have supported XRP could reverse, the way weekly ETF inflows did earlier in the year when momentum faded, falling from over $200 million to a trickle within a month.

Without the statutory catalyst, Ripple’s institutional infrastructure would keep growing through stablecoins and fiat rails, but in a way that does not necessarily drive XRP token demand, leaving the familiar gap between corporate progress and token price intact. That is XRP’s other open question: whether Ripple’s wins translate into XRP demand, or whether stablecoins and company-level infrastructure capture most of the value. If the CLARITY Act fails, that question becomes even more important because the regulatory unlock would no longer be there to carry the near-term thesis. XRP would then need ETF flows, ledger usage, and broader crypto risk appetite to do the work instead.

The price implications of failure are meaningful. Analysts have suggested that in a no-bill scenario, XRP could slip back toward the lower end of its range, with some pointing to support around the $1.20 to $1.30 area and warning that a break of the key technical floor on a broader market sell-off could open a path toward materially lower levels with little support in between. A bank that projected large inflows on passage had already trimmed its XRP target on the assumption of a delayed bill rather than a failed one, illustrating how much of the token’s valuation has been riding on this single legislative outcome. That is why the price levels at stake matter: the legal catalyst and the technical chart are now feeding into each other.

The sharpest risk is not merely that the bill fails this year but that failure pushes it out of reach entirely, since a missed 2026 window could shelve the effort for years if the political configuration that enabled it does not recur. For XRP, that would mean losing not just a near-term catalyst but the central pillar of its independent investment case, throwing the token back onto Bitcoin’s coattails and onto the slow, uncertain process of turning network usage into token demand without the regulatory unlock.

The priced-in problem

A subtler issue complicates both scenarios and deserves its own attention, because it shapes how XRP might actually react to news: the question of how much of the CLARITY Act’s effect is already in the price. Markets are forward-looking, and the bill’s advance has been the most-watched regulatory story in crypto for the better part of a year, which means XRP’s current price already embeds some probability of passage. This creates a genuine puzzle for holders. If passage is partly priced in, then the actual event, should it come, might produce a smaller pop than the headline suggests, as the market has already bought the rumor and could sell the news.

Conversely, if the market has grown skeptical and priced the bill closer to the current 42% odds, then a clear passage could still surprise to the upside by forcing a repricing toward certainty. This is why XRP has traded in a range even as the bill progressed: each catalyst has been priced as a possibility instead of a fact, because a proof-of-concept settlement is priced as a proof of concept until it becomes recurring volume, an ETF is priced on the flows it actually attracts instead of the flows it might, and a legislative catalyst is priced on the probability of passage, which for the CLARITY Act has stayed well short of certainty. A token sitting on a stack of maybes trades like a token sitting on a stack of maybes: range-bound, reactive, and quick to sell the news. That is the practical problem facing XRP now.

The practical implication for holders is that the falling odds are informative in two directions. They lower the probability the market assigns to the positive catalyst, which is bearish, but they also mean that less of the good news is now priced in, which paradoxically increases the potential upside surprise if the bill does pass against the odds. The cleanest way to read XRP right now is as a token whose price reflects a market that has grown genuinely uncertain about its central catalyst. That makes both the downside of failure and the upside of surprise passage larger than they would be if the outcome were close to settled.

What holders should watch

For an XRP holder trying to navigate a catalyst that has become harder to handicap, the analysis points to a focused set of signals worth tracking over the coming weeks. The first and most important is simply whether a floor vote gets scheduled before the August recess, because the closing window is the binding constraint, and the absence of a scheduled vote as the recess approaches would be a strong signal that 2026 passage is slipping away. The progress of the committee reconciliation between the Banking and Agriculture versions is a related early indicator, since the floor vote cannot happen until that merger is done. The second signal is the trajectory of the opposition, particularly whether the Section 604 trafficking objection gains traction with undecided senators or whether sponsors find a way to address it, because that fight has the potential to either stall the bill or, if resolved, clear a path.

The third thing to watch is the prediction-market odds themselves, which have proven to be a useful real-time gauge of the bill’s perceived chances and which will move as developments unfold; a recovery back toward the sixties or seventies would signal renewed momentum, while a further slide would confirm the pessimism. Alongside the legislative signals, holders should keep an eye on the observable market data that will register the outcome regardless of the politics: ETF flows, which would surge on passage and stall on failure, and XRP’s behavior around its key technical levels, particularly whether it holds the support that the bear case threatens. The stablecoin fight also matters because it is one of the pressure points inside the bill, and the stablecoin rules in the bill are part of why banks and crypto firms are fighting so hard over the final text.

The honest synthesis is that the CLARITY Act has gone from a likely catalyst to a genuine coin flip, and with it XRP’s near-term path has become a binary bet on a contested vote in a closing window. Passage would be a powerful positive catalyst capable of unlocking institutional demand; failure would strip XRP of its defining catalyst and throw it back onto Bitcoin’s movements. At 42% and falling, the market is telling holders that the outcome it once treated as probable is now anything but. The next few weeks of the legislative calendar are likely to decide which way XRP breaks.

Frequently asked questions

What is the CLARITY Act and why does it matter for XRP?

The CLARITY Act is a crypto market-structure bill that would codify the classification of tokens like XRP as digital commodities into federal law. For XRP, this matters enormously because the token’s current commodity status rests on interpretive regulatory releases instead of statute, which a future administration could in principle reverse. Writing that status into actual law would remove the last major source of regulatory uncertainty that keeps large institutions cautious, and analysts have projected that passage could unlock several billion dollars in additional XRP ETF inflows. It has been XRP’s single most important catalyst throughout 2026, which is why its odds of passing move the token.

Why did the CLARITY Act’s odds fall to 42%?

The odds fell from highs near 73% because of several problems converging at once. An anti-trafficking coalition attacked Section 604 of the bill, a provision shielding decentralized-finance developers from money-transmitter obligations, warning it could weaken tools against illicit finance. The banking lobby has fought provisions on stablecoin yield and regulation, while the Senate math is hard because advancing the bill requires 60 votes, meaning at least seven crossover votes from the opposition. Combined with a closing legislative calendar, these pressures made passage look far less certain, and prediction markets repriced the probability sharply downward to around 42%.

What happens to XRP if the CLARITY Act passes?

Passage would remove the last layer of regulatory uncertainty by writing XRP’s commodity status into durable federal law, giving cautious institutions the certainty they need to allocate. The clearest effect would flow through spot ETFs, with analysts projecting several billion dollars of additional inflows, three to six times what the funds have gathered so far. That demand could push XRP through its resistance levels toward analyst targets in the several-dollar range by year-end, with higher projections if a second catalyst like a Federal Reserve master account followed. The main caveat is that some of this may already be priced in, so the size of the reaction depends on how much waiting money actually moves.

What happens to XRP if the bill fails?

Failure or delay would strip XRP of its one Ripple-specific catalyst, likely sending it back to moving with Bitcoin instead of leading on its own regulatory story. Institutional ETF flows could reverse, as they did earlier in the year when momentum faded, and analysts have suggested XRP could slip toward support around $1.20 to $1.30, with a break of its key floor on a broader sell-off opening a path to materially lower levels. The sharpest risk is that a missed 2026 window could shelve the effort for years. That would cost XRP not just a near-term catalyst but the central pillar of its independent investment case.

When is the deadline for the CLARITY Act?

The practical deadline is the Senate’s August recess, after which election-year campaigning effectively closes the floor schedule to contested votes. The White House had pushed for a finish around the July 4 holiday, a target officials conceded was tight. Before any floor vote, the Senate Banking Committee’s version must be reconciled with the Senate Agriculture Committee’s companion bill, a merger that is not yet complete, and after a floor vote the bill would still need to be reconciled with the House-passed version and signed by the president. If the vote does not happen before the recess, 2026 passage becomes very unlikely.

Is the CLARITY Act’s effect already priced into XRP?

Partly, which complicates how the token may react. The bill’s advance has been the most-watched regulatory story in crypto for nearly a year, so XRP’s price already embeds some probability of passage, which is part of why the token has stayed range-bound: each catalyst gets priced as a possibility instead of a fact. If passage is partly priced in, the actual event could produce a smaller move than expected. But with odds now down at 42%, less of the good news is currently priced in, which paradoxically increases the potential upside surprise if the bill passes against the odds, while also reflecting greater downside risk if it fails.

This article is information, not investment advice. Legislative timelines, prediction-market odds, prices, and analyst projections reflect reporting available as of June 28, 2026, and can change quickly. The status and prospects of the CLARITY Act are uncertain and contested. Nothing here is a recommendation to buy or sell XRP or any security. Verify current developments from primary sources and consider your own circumstances before making any decision.

Crypto World

NFTs Battle Crypto Arena (NCA) Launches June 30, Turning Any Polygon NFT Into a USDT-Earning Fighter

A new permissionless GameFi arena on Polygon lets any NFT — even a long-dead JPEG — earn fair, randomized combat stats and battle for stablecoin rewards. No pay-to-win, no walled gardens.

SINGAPORE, June 2026 — NFTs Battle Crypto Arena (NCA), a fully open, permissionless Web3 GameFi battle platform built on the Polygon network, will officially launch on June 30, 2026, at 9:00 AM EDT (1:00 PM UTC). NCA’s thesis takes direct aim at one of crypto’s most visible failures: the millions of “dead JPEGs” sitting idle in wallets across the ecosystem. Any NFT on Polygon — regardless of collection, origin, or floor price — can be brought into the arena, assigned algorithmically generated combat attributes, and sent into battle for rewards paid in USDT.

The Dead-NFT Problem NCA Attacks

Successive market cycles left holders with the same outcome: an expensive image, a thin promise of “utility,” and nothing to actually do with the asset. GameFi was supposed to fix this, but most projects rebuilt the same trap — closed economies, assets locked to a single game, and tokens whose value evaporated faster than players could earn them.

NCA argues this is a design failure, not a technology failure, and rebuilds the model around three principles:

- No walled gardens. NCA does not sell its own NFTs as a gate. Any Polygon NFT can become a fighter, so the asset already in a user’s wallet becomes the entry point — not a fresh purchase.

- No pay-to-win. On entry, every NFT is assigned algorithmically generated stats across a transparent rarity structure — Normal (60%), Rare (25%), Super Rare (12%), and Super Super Rare (3%). Outcomes are decided by strategy, not by how much a player spent.

- Stablecoin rewards. The play-to-earn economy settles in USDT rather than a volatile native token, so rewards hold a clear, real unit of value.

Where the Idea Came From

NCA did not start in a boardroom. It started with two unrelated moments, years apart.

The first was childhood. Growing up with few toys, the founder would stand simple monster trading cards upright and imagine them coming alive to fight. The card was just paper; all the value lived in the imagination. The question that stuck: if a child’s mind can assign power and stats to a piece of cardboard, why couldn’t a smart contract do the same for a JPEG?

The second came years later, inside an underground, encryption-gated crypto forum. Entry was not bought with a password — it was granted only to wallets holding a specific NFT. The system ignored the art entirely. It verified one thing: the token’s unforgeable existence on-chain, and used that existence as a key. It was quiet proof that an NFT’s deepest utility is not the picture — it is the verifiable, tamper-proof credential underneath.

The synthesis became NCA: fuse the imaginative, open battle mechanics of childhood with the unforgeable on-chain authentication that defines Web3 — a global arena where the cards are real, ownership is verifiable, and the rewards are tangible.

How It Works

- Battle modes. NCA launches with 1v1 PvP duels and PvE Boss raids, with the architecture already in place for upcoming 3v3 squad battles and deeper strategic modes.

- A living universe. Every fight unfolds inside Wasteland Survivor, NCA’s cyberpunk, post-apocalyptic world, with a Genesis Collection available now on OpenSea.

- Built on Polygon. Low fees and open-by-default composability make Polygon-wide NFT compatibility the standard, not a premium feature — keeping the barrier to entry low for frequent players.

A Word From the Founder

“Crypto sold millions of people a JPEG and then gave them nothing to do with it,” said 0xGuda, Founder of NCA. “NCA gives that JPEG a reason to exist. Bring the dead asset in your wallet into the arena, and watch it fight, earn, and finally mean something. The card on my childhood floor was worthless paper until imagination gave it a fight to win. We just rewrote that imagination as code.”

Availability

NFTs Battle Crypto Arena goes live on June 30, 2026, at 9:00 AM EDT (1:00 PM UTC) on the Polygon network. Players connect a wallet, bring any existing Polygon NFT into the arena, and begin competing for USDT rewards. The Genesis Collection is available now on OpenSea.

About NFTs Battle Crypto Arena (NCA)

NFTs Battle Crypto Arena is a fully open, permissionless Web3 GameFi platform on the Polygon network that turns any Polygon NFT into a combat-ready fighter. Through algorithmically generated stats, transparent on-chain logic, and a USDT-settled play-to-earn economy, NCA aims to redefine GameFi as borderless, fair, and player-first — reviving the “dead JPEGs” sitting idle across the ecosystem.

Media Contact: 0xGuda, Founder — NFTs Battle Crypto Arena — nftsbattlecrypto@gmail.com

Disclaimer: This press release is for informational purposes only and does not constitute financial, investment, legal, or tax advice. Digital assets and play-to-earn participation carry significant risk, including the potential loss of capital. Readers should conduct their own research (DYOR) before making any decisions.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

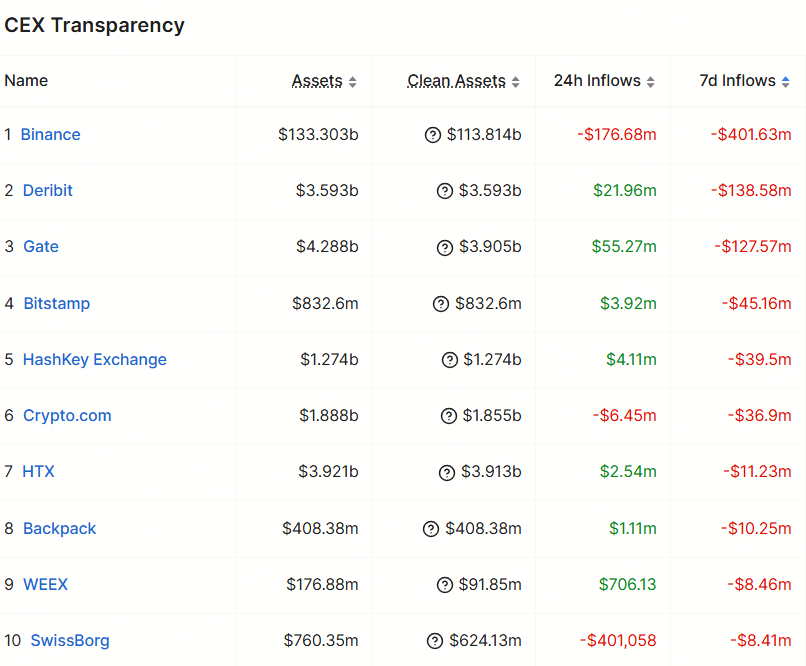

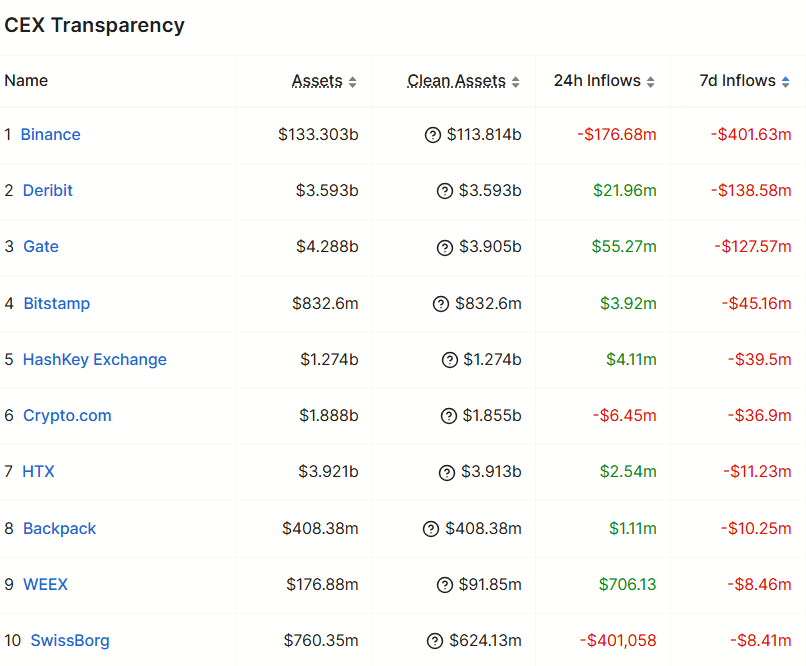

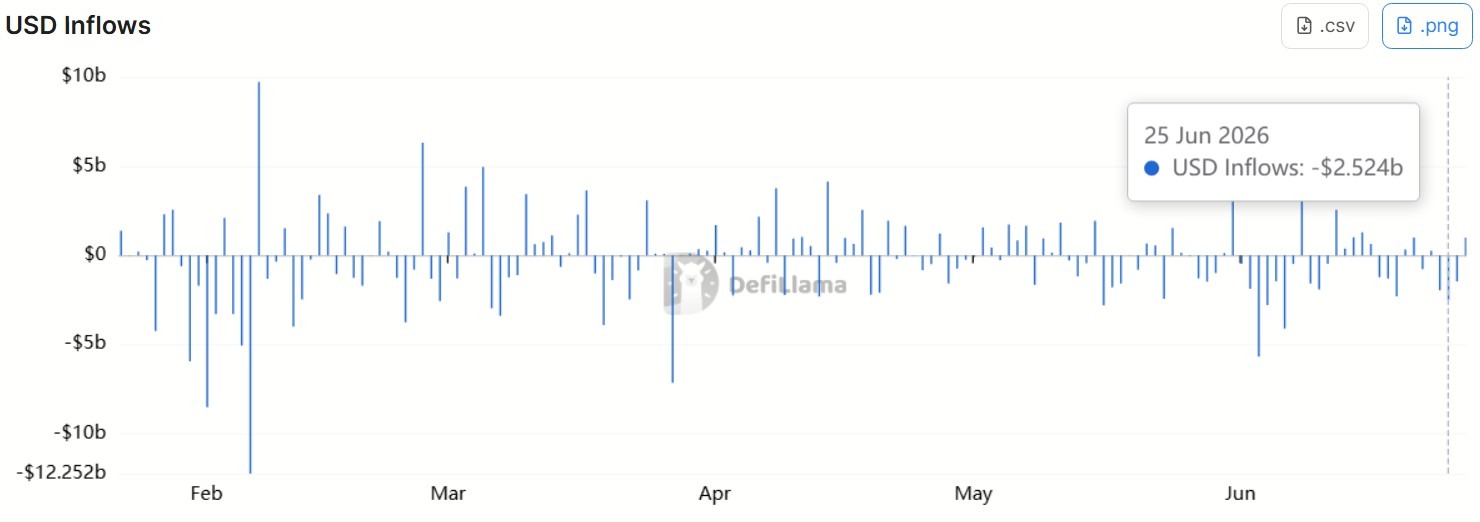

Binance saw a sharp pullback in customer funds in the run-up to the EU’s Markets in Crypto-Assets Regulation (MiCA) transition deadline, after the exchange withdrew its MiCA license application in Greece. DefiLlama data reviewed by Cointelegraph shows the withdrawal coincided with the week beginning June 22 becoming the latest period of heavy net outflows for the platform.

During that seven-day window, Binance recorded more than $400 million in net outflows, equivalent to 0.3% of its $133.3 billion in tracked assets. When excluding BNB, the figures rise slightly: outflows amounted to 0.35% of Binance’s $113.8 billion in tracked crypto assets, according to DefiLlama’s exchange datasets.

Key takeaways

- Binance reported net outflows of over $400 million in the week starting June 22, following its decision to withdraw a MiCA license application in Greece.

- The outflow burst intensified on Wednesday, when Binance recorded $1.96 billion in net outflows—followed by two more high-outflow days.

- Exchanges have tried to capture Binance liquidity ahead of July 1, but clear “winners” are not obvious from the net inflow rankings.

- Binance says it remains committed to the EU market and is still pursuing MiCA authorization, even as it prepares some restrictions for affected users.

- ESMA guidance indicates that crypto service providers not authorized by July 1 must wind down EU activities and limit what they can do.

Outflows spike as Greece MiCA setback hits

Binance’s move to pull its Greece MiCA license application marked a fresh regulatory complication as the EU approaches July 1. According to DefiLlama, net outflows accelerated on Wednesday—when Binance announced the withdrawal from Greece’s securities regulator—jumping to $1.96 billion. The following two days saw additional net outflows of $2.52 billion and $1.46 billion, before the week’s total rose to more than $400 million.

While the scale of outflows can look alarming in absolute terms, the data underscores that the magnitude aligns with Binance’s typical flow pattern. The source material notes that Binance often records billions of dollars in both daily inflows and outflows, and the DefiLlama figures do not disclose where the withdrawn capital originates geographically.

Still, the timing is notable: these outflows took place during the final week before the MiCA transition deadline. Starting July 1, Binance will restrict onboarding and some services for EU users covered by the affected scope, turning the final days into a practical test of how traders and institutions reposition.

Liquidity chase: rivals court Binance users, but ranking gaps remain

With MiCA deadlines approaching, multiple exchanges have attempted to attract users shifting away from Binance ahead of regulatory constraints. In DefiLlama’s proof-of-reserves-based rankings, OKX—one of the most vocal exchanges courting Binance users—logged $285.5 million in net inflows over the same week.

OKX also disclosed MiCA authorization in Malta in January 2025, which could make it an appealing alternative for compliant EU-facing operations. However, the weekly net inflow picture suggests that the “Binance exodus” narrative does not cleanly map onto a single beneficiary.

DefiLlama rankings show OKX finishing third in weekly net inflows behind Bitget, which recorded $710 million, and Bitfinex, which logged $400 million. The source material adds that neither Bitget nor Bitfinex appears on ESMA’s interim MiCA register, which was last updated on Friday and is used to track authorized and in-scope entities.

This creates a tension between user migration expectations and the compliance optics implied by MiCA-related registers. Investors watching for liquidity flows into “MiCA-ready” venues may need to account for other factors—such as routing, custody preferences, and how traders interpret which platforms will remain accessible after July 1—rather than assuming net inflows will map directly to ESMA-listed authorization status.

Binance’s stance: Europe still “important,” restrictions vary

Binance’s messages indicate the firm views Europe as strategically significant, even if it may miss the July 1 authorization “buzzer.” Earlier coverage cited by the source notes that a CryptoQuant analyst, Maartunn, argued euro trading accounts for about 1% of Binance’s spot volume—an assertion that, if accurate, would suggest the business impact could be limited in relative terms.

Nevertheless, Binance’s public posture remains that the company intends to keep pursuing a MiCA license. In the source material, Binance co-founder Yi He is quoted via social media saying the company takes the EU seriously, describing it as a small but important portion of its business and reaffirming commitment to the EU and its customers.

Alongside messaging, Binance has begun advising some EU users to move funds either to self-custodial wallets or to other exchanges. A Binance representative told Cointelegraph that restrictions vary depending on users’ jurisdictions. The representative also stated that no action is required for users not served through a local registered entity.

Those distinctions matter because MiCA compliance is not uniform across all product categories and customer onboarding paths. For traders, the difference between “restricted onboarding” and “restricted services” can shape execution choices—particularly around order types, funding routes, and whether counterparties can be accessed after July 1.

What ESMA requires from unlicensed providers

Regulatory expectations are a key driver of user behavior as July 1 nears. The source highlights an ESMA statement from June 23 stating that crypto service providers not authorized by July 1 must take “immediate steps” to wind down EU activities.

ESMA’s guidance, as reflected in the source, also specifies that unlicensed providers should limit services to actions such as selling, transferring, relocating assets, or closing positions. For market participants, this is often read as a shift from growth-oriented service delivery to exit mechanics—meaning liquidity providers and active traders may pull ahead of restrictions to avoid interruptions.

In that context, the combination of Binance’s Greece application withdrawal, visible multi-day net outflow pressure, and the July 1 operational transition creates a clearer cause-and-effect chain than the raw percentage figures alone.

Going forward, traders and institutions should watch how Binance’s EU user restrictions roll out across jurisdictions and whether outflows stabilize after July 1 or continue to re-route toward specific venues. The open question remains which exchanges will be able to convert regulatory certainty into sustained customer retention, especially when net flows do not neatly align with ESMA interim register visibility.

Ethereum continues to trade under severe pressure, although it managed to recover around around 5% from its recent multi-year low at just over $1,500.

The threat remains since many of the major investors in its ecosystem continue to offload. The only positive change in the past few weeks has been the return of SharpLink.

Whales Dump

Data shared by popular analyst Ali Martinez shows that these large market participants have disposed of $880 million worth of the largest altcoin in the span of just one week. From an Ethereum perspective, this means a massive dump of 550,000 ETH, which, according to him, means a substantial $880 million injection in “sell-side supply into the market.”

He added that this heavy selling volume is among the reasons behind the asset’s drop below its first immediate support at $1,633. The other could be the behavior of ETF investors. As reported earlier this weekend, those gaining exposure to Ethereum through the exchange-traded funds sold over $270 million during the week, as ETH dropped toward $1,500 for the first time in over a year.

Citing URPD data, Martinez outlined the significance of the $1,583 level as a critical volume support. If ETH breaks below it, it would open a “clear path for extended liquidations.” He doubled down that Ethereum’s asset risks falling to a new cycle low of somewhere between $1,237 and $1,089.

ETH WHALES SELL $880 MILLION IN ONE WEEK

Large-scale holders have offloaded roughly 550,000 ETH over the past week, injecting $880 million in sell-side supply into the market.

This heavy selling volume has successfully pushed Ethereum below its immediate $1,633 support floor.… https://t.co/2n4rVK4oTK pic.twitter.com/7g1zSPepez

— Ali Charts (@alicharts) June 28, 2026

Fellow analyst Ted Pillows commented that ETH remains stuck between key support (at $1,500) and resistance (at $1,700). A breakout above the latter would be “what bulls need,” while a potential decisive drop below $1,500 is “what bears are pushing for a new cycle low.”

Who Is Buying

On the flipside, the two largest corporate holders of Ethereum are accumulating. While this is not really a surprise for Bitmine, which has been buying consistently even through the bear market, the return of SharpLink made the headlines over the week.

The Joe Lubin-chaired firm made its first ETH buy in eight months on Friday and has only doubled down since then. Lookonchain noted earlier today that the company accumulated another 29,196 ETH for $46.7 million. Thus, it has acquired over $62 million worth of ETH in the past three days alone.

The post Ethereum Whales Offload Almost $900M Worth of ETH: Is Another Crash Looming? appeared first on CryptoPotato.

Coinbase CEO Brian Armstrong responded to criticism over the company’s promotion of high-risk products to young and financially vulnerable users. He called for responsible product design that does not restrict adult choice.

Zcash founder Zooko publicly criticized Coinbase for promoting sports betting and Bitcoin (BTC) price prediction to inexperienced users. Armstrong acknowledged the tension, noting that companies must balance user freedom against platform responsibility.

The CEO Draws a Line on Aggressive Promotion

The CEO argued on X that companies should not aggressively promote high-risk products to unsophisticated users. A clear distinction exists between making products available and actively pushing them on people least equipped to handle the risks.

Three practical measures followed from that position. Platforms should offer clearer risk disclosures, built-in financial literacy tools, and user preference settings to control which products appear. Together, these options could create a more personalized experience without removing adult access.

Additionally, Zooko’s criticism targeted how Coinbase surfaces Bitcoin price prediction and sports betting to inexperienced users. That kind of aggressive in-app promotion crosses a line, Armstrong said, even if the products themselves remain available.

Criticism Arrives as Coinbase Expands Its Reach

The Coinbase chief recently commented on Coinbase’s Bitcoin market view, noting AI cost reductions alongside broader product expansion. Responsible design, he suggested, needs to accompany that growth rather than trail it. However, those ambitions now face questions about whether user safety has kept pace.

Meanwhile, scrutiny of Coinbase’s 2026 product direction reflects the broader sentiment around the company’s trajectory. Critics have argued that feature expansion has outpaced user protections. That tension sharpened further with Zooko’s public call-out this week.

Beyond the exchange, Coinbase’s Base chain B20 push and Coinbase Luxembourg MiCA hub show a widening footprint. That scope makes it harder to enforce product design standards uniformly across user segments.

The CEO also addressed whether sports prediction markets should exist at all. Private companies should not decide that question on their own. Instead, democratic processes are better suited to establish those limits.

The position separates two types of responsibility. How a platform promotes products differs from whether those products should exist.

The Coinbase CEO supports tighter design standards, including opt-in controls and personalized risk settings. Nevertheless, the case for regulatory rather than corporate limits remains central to that position.

The post Coinbase CEO Armstrong Comments on Betting Promotion Concerns in the Base App appeared first on BeInCrypto.

Bitcoin is trading near $60,000 after a volatile week that pushed the largest cryptocurrency to its lowest level since late 2024.

Summary

- Bitcoin is holding near $60,000 despite Middle East tension and renewed pressure from Strategy concerns.

- Analysts say a break above $66,000 could revive momentum, while $58,000 remains key support.

- On-chain data shows weaker short-term holder dominance, a structure often seen near accumulation zones.

The price has stayed calm through the weekend, even as new tension in the Middle East tested risk appetite across global markets.

BTC had opened the previous business week with strength, rising to about $65,500 after reclaiming support near $64,000. That move failed to hold. Sellers later pushed the asset below $62,400, then toward $59,000, before another drop sent Bitcoin near $58,000.

Bitcoin steadies after sharp weekly sell-off

Bitcoin’s latest price action shows a market trying to hold a base after a fast decline. BTC now trades around the $60,000 area, with bulls defending the zone after repeated tests below that mark.

The weekend calm stands out because the U.S. and Iran exchanged fresh blame over the broken ceasefire. Earlier this month, Bitcoin had climbed above $65,500 after a U.S.-Iran deal eased oil and inflation fears across markets.

That relief rally did not last. Bitcoin soon lost strength as traders returned to concerns around liquidity, ETF flows, and Strategy-related risk.

The current setup leaves BTC stuck between two near-term levels. A move below $58,000 could invite more selling, while a clean recovery above $64,000 to $66,000 may show that buyers are regaining control.

Strategy fears remain a market pressure point

One of the main pressure points remains Strategy, the company formerly known as MicroStrategy. Growing concern around its capital structure has affected Bitcoin sentiment because the firm remains the largest corporate holder of BTC.

As previously reported, Bitcoin fell below $60,000 for the second time in June as liquidations topped $850 million. Strategy shares also dropped sharply as traders watched the company’s stock, preferred shares, and Bitcoin treasury.

Another report said Strategy’s Bitcoin flywheel has started to work in reverse. The company once used a stock premium to raise capital and buy more BTC, but weaker market pricing now makes that model harder to sustain.

CryptoQuant has also urged Strategy to pause Bitcoin purchases and rebuild cash reserves. The firm said dividend coverage tied to STRC had fallen to about 14 months as cash reserves declined.

This pressure does not mean Strategy must sell Bitcoin now. Still, the market is watching whether further stress in STRC or MSTR could create more fear around BTC.

Analysts split on breakout or deeper chop

Crypto analyst Market Watcher said Bitcoin’s weekly structure remains clear. The analyst pointed to a downtrend from the July and August highs near $70,000 and $67,000 and said a break of that line would make them more willing to deploy capital.

The same analyst described the current zone as “indecisive summer chop” between about $59,000 and $66,000. That range matches the current market, where BTC has not broken down fully but has also failed to reclaim lost momentum.

Market Watcher said a break of the main trend near $58,000 would change the setup. The analyst also compared the current downtrend to the December 2022 and January 2023 breakout, which later started a major BTC uptrend.

EGRAG CRYPTO took a longer view and focused on Bitcoin’s 12-month cycle. The analyst said the usual rhythm has been three years up and one year down, but this cycle may be different if 2026 closes as a red yearly candle.

EGRAG said the four-year cycle remains intact for now, but added that structure matters more than hope. That view keeps attention on the yearly close and whether Bitcoin can regain a stronger long-term pattern.

On-chain data points to possible reset

CryptoQuant analyst Crazzyblockk said Bitcoin’s short-term holder realized dominance has fallen to 27.6%. The analyst said that places BTC inside a historical undervaluation zone where long-term holders control most realized capital.

In past cycles, market tops formed when short-term holders held most realized capital. That often showed heavy speculation and late-cycle buying.

Bear markets have shown the opposite setup. Short-term holders realize losses, their share of realized capital falls, and long-term holders regain control.

The analyst said current data looks closer to past accumulation phases than cycle tops. However, they also warned that bottoms often form through a process, and another capitulation phase remains possible.

Another CryptoQuant analyst, Facundo Fama, pointed to long-term holder SOPR. The analyst said when LTH-SOPR moves near or below 1, long-term holders are selling coins at or near a loss.

The last time LTH-SOPR stayed below 1 on the monthly timeframe for more than three months was in October 2022, when BTC traded near $20,000. That data does not guarantee a bottom, but it shows that long-term holder stress has returned to a rare zone.

Bitcoin price outlook

Bitcoin’s short-term outlook now depends on whether bulls can defend $58,000 and recover the $64,000 to $66,000 range. A close above that upper band could support a stronger recovery attempt.

A loss of $58,000 would weaken the current base and could expose lower areas as traders reduce risk. In that case, Bitcoin may revisit deeper support before building a new range.

For now, BTC is neither breaking down nor confirming a strong reversal. The market remains calm near $60,000, but that calm depends on support holding, Middle East risk staying contained, and Strategy-related fear easing.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Binance recorded over $400 million in net outflows during the week beginning June 22, as the cryptocurrency exchange announced the withdrawal of its Markets in Crypto-Assets Regulation (MiCA) license application in Greece.

According to DefiLlama data viewed by Cointelegraph on Sunday, Binance’s seven-day net outflows amount to 0.3% of its $133.3 billion in tracked assets. Excluding BNB, Binance’s native token, the outflows equal 0.35% of the exchange’s $113.8 billion in crypto assets.

Binance led tracked exchanges in weekly net outflows. Source: DefiLlama

Net outflows accelerated on Wednesday, when Binance announced its withdrawal from Greece’s securities regulator, recording $1.96 billion in net outflows, followed by two more days of $2.52 billion and $1.46 billion.

The scale of outflows is not unusual for Binance, which regularly records billions of dollars in daily inflows and outflows. The data also does not identify the geographic origin of the fund movements.

The outflows came during the final week before the European Union’s MiCA transition deadline. Starting July 1, Binance will restrict onboarding and some services for affected EU users.

Daily net flows in the billions of dollars are not unusual for Binance. Source: DefiLlama

MiCA winners are less clear than expected

Several rival exchanges have sought to attract Binance users ahead of the bloc’s deadline.

OKX, one of the most vocal exchanges courting Binance users, recorded $285.5 million in net inflows over the same period, according to DefiLlama’s rankings based on exchanges’ proof of reserves. The exchange received MiCA authorization in Malta in January 2025.

However, OKX was third in weekly net inflows, behind Bitget’s $710 million and Bitfinex’s $400 million. Neither exchange appears on the European Securities and Markets Authority’s (ESMA) interim MiCA register, which was last updated on Friday.

Related: Spain regulator rules out extension for non-MiCA compliant crypto companies

Binance says Europe still matters

CryptoQuant analyst Maartunn recently told Cointelegraph that euro trading accounts for just 1% of Binance’s spot volume, which may limit potential MiCA-related setbacks for the exchange.

However, Binance’s public messaging is that the company intends to continue pursuing a MiCA license, despite being on pace to miss the July 1 buzzer.

“As for Binance and Europe, we take this market seriously. It’s a small part of our business, but an important one, and we’re committed to the EU and our customers there,” Yi He, a co-founder of the exchange, said on Friday.

Meanwhile, Binance has started telling some EU users to move funds to self-custodial wallets or other exchanges.

A Binance representative told Cointelegraph that the restrictions vary depending on users’ jurisdictions and that no action is required for users not served through a local registered entity.

ESMA said in a June 23 statement that crypto service providers unlicensed by July 1 must take “immediate steps” to wind down EU activities, and limit services to actions to sell, transfer, relocate assets or close positions.

Magazine: AI is banking the unbanked in Africa… faster than crypto

Ripple settled a tokenized Treasury with JPMorgan in five seconds, expanded a stablecoin deal across Latin America, and powered remittances to 170 million people. The catch for XRP holders: the cash leg in deal after deal is RLUSD, Ripple’s dollar stablecoin, not XRP. Here is whether the token they hold is being quietly sidelined by the company built around it.

Summary

- Ripple’s biggest recent wins, a five-second tokenized Treasury settlement with JPMorgan and Mastercard, a stablecoin expansion across Latin America, and a major remittance deal, increasingly use RLUSD, Ripple’s dollar stablecoin, as the cash leg rather than XRP.

- RLUSD crossed $1 billion in market value quickly and is becoming the settlement asset enterprises actually want, raising the question of whether it is taking the role XRP was built to play.

- The pattern reflects a real tension: Ripple the company keeps winning institutional deals, while XRP the token stays pinned near a dollar, beneath every major moving average.

- The bullish counterargument is that Ripple is the largest XRP holder with aligned incentives, that RLUSD and XRP serve different functions, and that ledger activity can still benefit XRP indirectly.

- For holders, the question is whether XRP’s value will accrue from network usage and catalysts like the CLARITY Act and ETF flows, or whether RLUSD will capture the settlement demand XRP was meant to capture.

In June 2026, Ripple completed something that should have been a milestone for XRP. Working with JPMorgan, Mastercard, and the tokenization firm Ondo Finance, it settled the cross-border redemption of a tokenized U.S. Treasury fund across banks on the XRP Ledger, and the blockchain leg finalized in under five seconds, against the one to three business days the same transaction can take on traditional rails. It was a genuine showcase of what Ripple’s technology can do, the kind of institutional validation the XRP community has predicted for years.

And yet there was a detail in it that has become the defining unease for XRP holders: the cash leg of that settlement used RLUSD, Ripple’s dollar-pegged stablecoin, not XRP. The same pattern has repeated across Ripple’s other recent wins. A partnership expanding stablecoin settlement across Latin America runs on a regulated peso-backed stablecoin issued on the XRP Ledger and integrated with Ripple’s infrastructure, while a major remittance deal reaching 170 million people uses RLUSD as the primary settlement asset. Deal after deal, Ripple keeps winning, and deal after deal, the asset doing the actual settling is increasingly a stablecoin, while XRP trades near a dollar and change as though none of it is happening.

This is the question that has moved to the center of the XRP story, and it is a fair and uncomfortable one: if every Ripple win runs on RLUSD rather than XRP, is the token being quietly sidelined by the very company built around it? The concern is not baseless, because it touches the oldest puzzle in the XRP thesis, the gap between Ripple’s corporate success and XRP’s token price, and gives it a specific, mechanical explanation. But it is also not the whole story, because there are real counterarguments about why RLUSD and XRP are not simply competitors, why Ripple’s incentives remain aligned with holders, and how ledger activity can still benefit the token.

This piece works through both sides honestly. It lays out the pattern of RLUSD showing up where holders expected XRP, explains what RLUSD is and why enterprises prefer it for settlement, examines whether the stablecoin is cannibalizing XRP’s intended role, presents the bullish case that the two assets are complementary, and arrives at a grounded view of what holders should actually take from it. The goal is neither to stoke the fear nor to dismiss it, but to give holders an accurate read on whether their token is being left behind.

The pattern: RLUSD where holders expected XRP

Start with the pattern itself, because it is real and worth seeing clearly across the recent run of Ripple announcements. The flagship example is the tokenized Treasury settlement with JPMorgan, Mastercard, and Ondo Finance. For years, the XRP pitch held that cross-border institutional settlement was exactly what XRP was built for, the bridge asset that would let value move between currencies and institutions in seconds. When Ripple finally delivered a marquee demonstration of that capability, settling a tokenized Treasury redemption across borders and banks in under five seconds, the XRP Ledger provided the rails, but RLUSD provided the cash leg.

That detail matters because it changes what the event proved. It proved that the XRP Ledger can support serious institutional flows, with names that compliance departments recognize and a settlement speed legacy rails cannot match. But it did not prove that XRP the asset sits at the center of the payment, because the money leg moved through a stablecoin rather than the volatile token. As previously reported, Ripple’s tokenized Treasury settlement with JPMorgan showed that the ledger can win important business before the token captures meaningful demand.

The same shape recurs elsewhere. Ripple expanded a payments partnership in which a regulated peso-backed stablecoin is issued on the XRP Ledger and integrated into Ripple’s payment infrastructure to support enterprise stablecoin settlement across Latin America. Ripple also backed Flutterwave in a round that valued the African payments company at $3.2 billion, with RLUSD positioned for use across payment rails that reach a very large user base. In each case, the XRP Ledger and Ripple’s infrastructure become more relevant, but the settlement asset is a stablecoin.

Across these deals, the consistent feature is that the XRP Ledger, the blockchain Ripple built and that XRP is native to, is doing real and valuable work, but the asset moving through it as money is increasingly a stablecoin rather than XRP. This is what gives the holder concern its force: it is not a single anomalous deal but a repeated pattern in which Ripple’s institutional wins showcase the ledger and the company’s technology while routing the actual settlement value through RLUSD or another stablecoin. For holders who bought XRP on the thesis that institutional settlement demand would drive token demand, watching that settlement demand flow through a stablecoin instead is a legitimate cause for unease. The first honest step is simply to acknowledge that the pattern is real.

What RLUSD is and why enterprises prefer it

To judge whether this pattern is a problem, you have to understand what RLUSD is and why enterprises keep choosing it, because the answer explains the dynamic without requiring any conspiracy against XRP. RLUSD is Ripple’s dollar-pegged stablecoin, a token designed to hold a steady value of $1, backed by reserves, and issued on the XRP Ledger and other chains. It crossed $1 billion in market value quickly after launch, a sign of real demand, and it has become the asset Ripple increasingly puts forward as the cash leg in its enterprise settlements.

The reason enterprises prefer a stablecoin for the money side of a transaction is straightforward and has nothing to do with any view about XRP. Businesses settling real-world value need price stability. When a company moves money across borders, it wants the amount it sends to equal the amount that arrives, with no exposure to price swings in between. XRP, like any freely traded cryptocurrency, fluctuates in price, which makes it difficult to use as the unit in which an enterprise wants to denominate and hold a settlement, even if it can still work as a bridge for moving value quickly.

A stablecoin solves this by holding a fixed dollar value, so the enterprise can settle in something that behaves like the dollars it already thinks in. This is why, across the industry and not just at Ripple, stablecoins have become the dominant on-chain settlement instrument: they combine the speed and programmability of crypto with the price stability that commerce requires. RLUSD is Ripple’s entry into that category, and its growing use in Ripple’s deals reflects the same market logic that has made stablecoins central everywhere. For readers who want the basics, how RLUSD holds its dollar peg is the starting point for understanding why enterprises gravitate toward it.

The same logic explains why exchange and liquidity integrations matter. When RLUSD is listed with XRP pairs and broader access, the stablecoin becomes easier to move, price, and route through the infrastructure Ripple wants enterprises to use. That helps Ripple’s payments stack, and it can deepen activity on the XRP Ledger, but it still does not mean every dollar of settlement creates direct XRP demand. The holder question is what remains for XRP once the stablecoin has taken the stable cash role.

Understanding this matters because it reframes the concern. RLUSD is not showing up in Ripple’s settlements simply because Ripple is trying to sideline XRP; it is showing up because enterprises asked for a stable settlement asset and Ripple built one to give them. That is a rational business decision for Ripple and a useful product decision for institutions. The harder question is whether that useful product decision narrows the value-accrual path that XRP holders were counting on.

Is RLUSD cannibalizing XRP’s role?

This is the crux of the matter, and it deserves to be stated plainly: there is a real argument that RLUSD is taking the settlement role XRP was originally meant to play. The classic XRP thesis cast the token as the bridge asset for cross-border value transfer, the thing that would sit in the middle of international settlements, moving value between currencies in seconds and capturing demand as global payment volume flowed through it. Stablecoins complicate that thesis directly, because a dollar stablecoin can perform much of the cross-border settlement function that XRP was built for, moving value quickly and programmably while also offering the price stability XRP cannot. If enterprises can settle in RLUSD on the XRP Ledger, getting the speed of the ledger without the volatility of the token, then the specific demand driver that was supposed to accrue to XRP may instead accrue to the stablecoin.

This is the structural worry beneath the holder concern, and it is not easily waved away. The bull case for XRP has long depended on the idea that Ripple’s growing settlement business would translate into demand for the token, but if the settlement business increasingly runs on RLUSD, that translation weakens. Ripple’s institutional infrastructure could keep growing impressively, opening corridors and closing deals, while the value of that growth flows through stablecoins and fiat instead of driving XRP token demand. That would leave the familiar gap between corporate progress and token price not just intact but mechanically explained.

The token could end up as the rails, valuable to the system but not the asset that captures the economic value moving across it. This is the version of events that should genuinely concern holders, and it is why the RLUSD pattern is more than a cosmetic detail. It points to a possible future in which XRP’s network succeeds, Ripple thrives, RLUSD becomes a major settlement asset, and XRP the token still struggles to convert all of that activity into sustained demand because the demand has a stablecoin to flow into instead. That is also why the older question of XRP’s bridge-asset role needs to be revisited rather than repeated as if nothing has changed.

There is a broader parallel here with other infrastructure tokens. A network can be useful without its native token absorbing the full value of that usefulness, especially when users can interact with the network through stable assets, tokenized deposits, or application-level instruments. XRP holders have already seen this in miniature: the ledger gets institutional proof points, Ripple gets business wins, and XRP gets fees, reserves, or optional routing rather than obvious direct demand. Whether that is enough depends on scale, and that scale has not yet shown up in the price.

The bullish case: complementary, not competing

The other side of this debate is serious and deserves a full hearing, because the framing of RLUSD versus XRP as a zero-sum contest may be too simple. The first counterargument is that RLUSD and XRP serve different functions and can coexist productively. A stablecoin is the cash leg, the stable unit in which value is denominated and held. XRP, in the bridge role, can still serve as the connective asset that moves value between different currencies and stablecoins, the neutral intermediary in a world where many different fiat-backed stablecoins exist and need to be exchanged.