Crypto World

Ethereum Whales Offload Almost $900M Worth of ETH: Is Another Crash Looming?

Ethereum continues to trade under severe pressure, although it managed to recover around around 5% from its recent multi-year low at just over $1,500.

The threat remains since many of the major investors in its ecosystem continue to offload. The only positive change in the past few weeks has been the return of SharpLink.

Whales Dump

Data shared by popular analyst Ali Martinez shows that these large market participants have disposed of $880 million worth of the largest altcoin in the span of just one week. From an Ethereum perspective, this means a massive dump of 550,000 ETH, which, according to him, means a substantial $880 million injection in “sell-side supply into the market.”

He added that this heavy selling volume is among the reasons behind the asset’s drop below its first immediate support at $1,633. The other could be the behavior of ETF investors. As reported earlier this weekend, those gaining exposure to Ethereum through the exchange-traded funds sold over $270 million during the week, as ETH dropped toward $1,500 for the first time in over a year.

Citing URPD data, Martinez outlined the significance of the $1,583 level as a critical volume support. If ETH breaks below it, it would open a “clear path for extended liquidations.” He doubled down that Ethereum’s asset risks falling to a new cycle low of somewhere between $1,237 and $1,089.

ETH WHALES SELL $880 MILLION IN ONE WEEK

Large-scale holders have offloaded roughly 550,000 ETH over the past week, injecting $880 million in sell-side supply into the market.

This heavy selling volume has successfully pushed Ethereum below its immediate $1,633 support floor.… https://t.co/2n4rVK4oTK pic.twitter.com/7g1zSPepez

— Ali Charts (@alicharts) June 28, 2026

Fellow analyst Ted Pillows commented that ETH remains stuck between key support (at $1,500) and resistance (at $1,700). A breakout above the latter would be “what bulls need,” while a potential decisive drop below $1,500 is “what bears are pushing for a new cycle low.”

Who Is Buying

On the flipside, the two largest corporate holders of Ethereum are accumulating. While this is not really a surprise for Bitmine, which has been buying consistently even through the bear market, the return of SharpLink made the headlines over the week.

The Joe Lubin-chaired firm made its first ETH buy in eight months on Friday and has only doubled down since then. Lookonchain noted earlier today that the company accumulated another 29,196 ETH for $46.7 million. Thus, it has acquired over $62 million worth of ETH in the past three days alone.

The post Ethereum Whales Offload Almost $900M Worth of ETH: Is Another Crash Looming? appeared first on CryptoPotato.

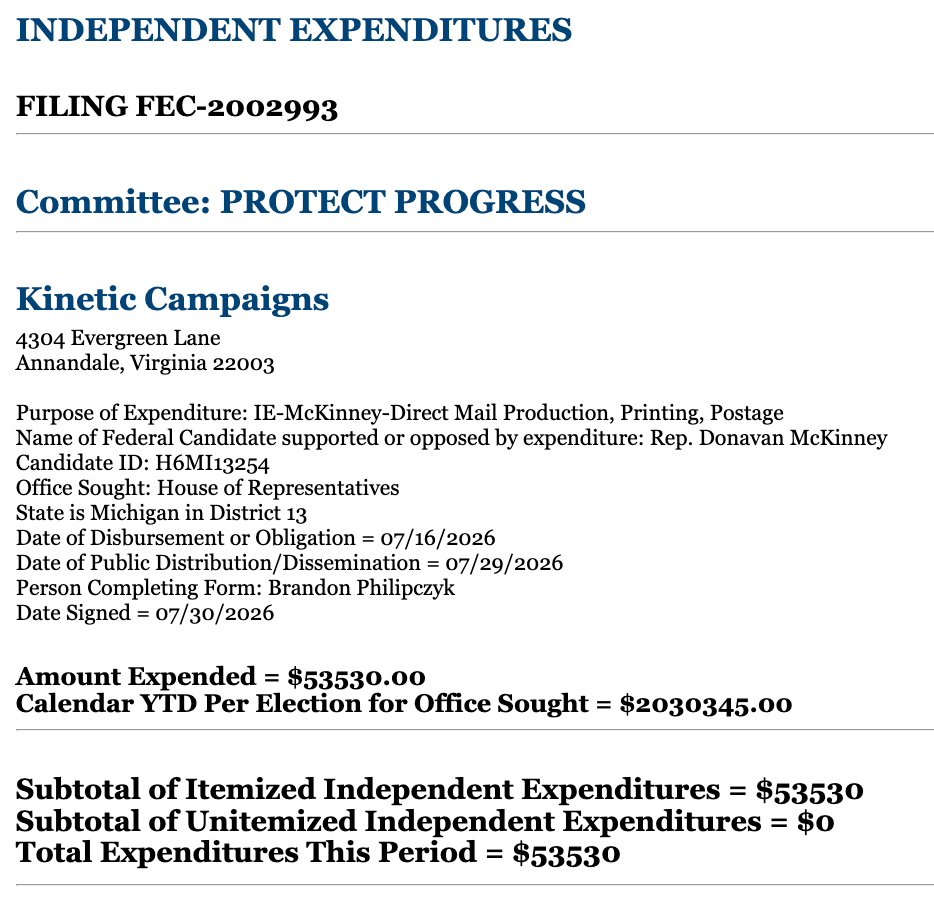

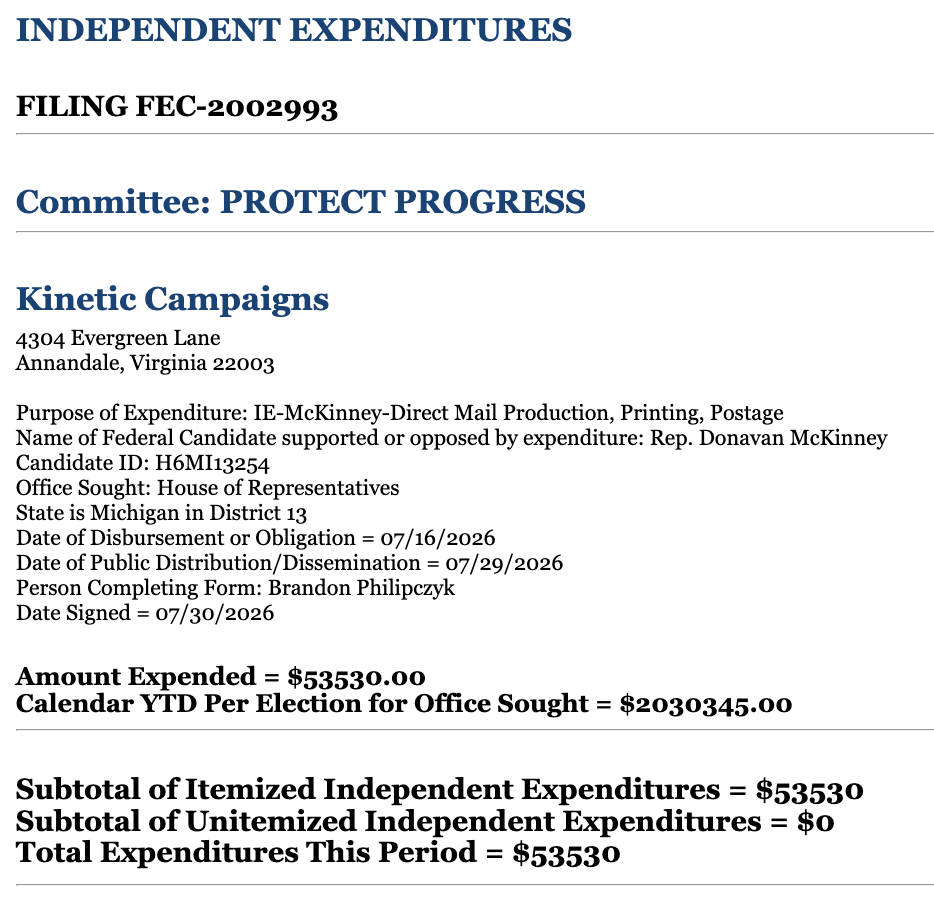

A crypto-industry-backed political action committee affiliate has intensified its advertising push ahead of next week’s Michigan Republican primary, according to the latest Federal Election Commission (FEC) filings. Protect Progress PAC, which the filings indicate is funded largely by contributions from cryptocurrency companies Ripple Labs and Coinbase, has spent more than $2 million on media to influence the contest in Michigan’s 13th Congressional District.

The most recent updates, filed as of Thursday, show the committee ramping up spending in support of U.S. Representative Shri Thanedar while also funding opposition to his Democratic challenger, Donavan McKinney. The renewed disclosures come shortly after earlier reporting showed the PAC had already ramped up its buy—effectively doubling its reported ad spending from the prior week.

Key takeaways

- FEC filings show Protect Progress PAC has spent over $2 million on media for Michigan’s 13th district primary race.

- New disclosures add $884,240 to advertisements supporting Shri Thanedar and more than $150,000 to ads opposing Donavan McKinney.

- The PAC’s funding is described in the filings as being largely backed by cryptocurrency companies Ripple Labs and Coinbase.

- Thanedar’s legislative record includes support for crypto-related bills such as the GENIUS Act and the CLARITY Act.

- Protect Progress is an affiliate of Fairshake, a major outside spender in U.S. elections tied to crypto industry policy goals.

Michigan’s 13th district: Protect Progress increases ad buys

According to FEC disclosures accessed via the commission’s docquery system, Protect Progress PAC reported spending more than a combined $2 million on media in connection with Michigan Representative Shri Thanedar and his Democratic primary contest against Donavan McKinney.

As of Thursday, the filings reflect a further escalation: compared with what the PAC had already reported spending a week earlier, the committee’s latest report effectively doubled its media spending. The additional outlay includes $884,240 dedicated to ads supporting Thanedar and more than $150,000 aimed at opposing McKinney.

The Michigan primary is scheduled for Tuesday, but the filings underscore that the committee and its network have been willing to deploy substantial resources well before Election Day. Similar patterns have been visible across multiple congressional races during the 2026 cycle, according to the article’s referenced coverage and FEC-based reporting.

Why the race is drawing crypto-linked political money

Thanedar’s congressional record is at the center of the narrative around why outside groups see his candidacy as important for crypto policy. During his time in the House, he voted in favor of the stablecoin-focused GENIUS Act and supported the legislative push for clearer digital asset market structure—the Digital Asset Market Clarity (CLARITY) Act, which has been discussed in the Senate.

He also cosponsored the Promoting Innovation in Blockchain Development Act, an effort aimed at protecting developers. Supporters of crypto policy reform often point to such measures as steps toward a more predictable regulatory environment, while critics argue the industry has too much influence over the political process.

For voters watching the contest, the spending escalation suggests the primary is being treated as more than a local political test—it is being framed by donors and advocacy networks as part of a broader strategy to influence which lawmakers back specific digital asset legislation.

McKinney’s response and the broader allegations over crypto influence

McKinney has publicly characterized the ad push as a payoff for political favors. In a July 21 statement related to the PAC spending, he said “the crypto lobby is paying my opponent back for helping Trump make over $1 billion since taking office,” according to a video shared on his campaign’s Facebook page.

That comment appears to reference the U.S. President’s disclosures about crypto-related earnings, including a figure cited in earlier reporting referenced by the article—more than $1.4 billion from crypto investments in 2025—along with concerns raised by Democrats that Trump could be using his role to profit through policies such as GENIUS.

While those claims are rooted in political argument rather than direct proof of intent tied to the specific Michigan ads, they highlight a recurring tension in U.S. crypto politics: outside spending may be framed by industry-aligned PACs as policy support, while opponents often describe it as evidence of undue influence.

Cointelegraph reports that it reached out to both Thanedar’s and McKinney’s campaigns for comment on the PAC expenditures but did not receive an immediate response.

Fairshake’s affiliates: national momentum in multiple primaries

Protect Progress PAC is an affiliate of Fairshake, a political network that has become one of the most prominent outside spenders linked to crypto industry policy goals. Fairshake was responsible for spending more than $170 million across the 2024 election cycle through media buys supporting candidates it viewed as aligned with crypto-friendly regulation, as summarized in the article.

The article also notes that affiliates have already deployed millions of dollars in 2026 races beyond Michigan, pointing to activity in states including Texas and Illinois. In addition, it cites Public Citizen reporting from June that Fairshake and its affiliates accounted for more than $82 million out of roughly $189 million deployed by crypto companies during the 2026 election cycle.

Fairshake itself reportedly listed holding a $193 million “war chest” as of January, according to figures referenced in the piece. Taken together with the Michigan disclosures, the pattern suggests a sustained approach: deploy substantial resources early enough to shape narrative and voter attention around specific legislative priorities.

The article further describes similar affiliate activity in other congressional primaries. It says Defend American Jobs PAC spent more than $65,000 on media in Washington’s 4th congressional district to support a Republican candidate, with Washington holding primaries on the same day as Michigan.

In Alabama, scheduled primaries on Aug. 11 are also described as a focus for Fairshake-linked spending. FEC filings cited in the article indicate Defend American Jobs PAC spent more than $511,000 on media supporting Jerry Carl Jr., a Republican who represented Alabama’s 1st congressional district from 2021 to 2025.

For readers tracking the cycle, these parallel contests illustrate how crypto-aligned PAC affiliates appear to treat primary elections as strategic targets—places where candidate positioning on digital asset policy could be determined before general election dynamics begin.

What to watch as Michigan’s primary approaches

With Michigan’s 13th district primary scheduled for Tuesday, the key question is whether Protect Progress’s latest ad surge will further alter voter perceptions or turnout in the remaining days. More broadly, the filings reinforce that crypto-linked political spending is not limited to high-profile general election races—affiliates are actively contesting primaries with resources intended to influence policy direction well after election season announcements fade.

Binance founder Changpeng Zhao (CZ) says this bear market has no shortage of money. Plenty of it is hunting for somewhere to go.

Elsewhere, Social Capital founder Chamath Palihapitiya said where he thinks it should land. Not in artificial intelligence (AI) chips.

The Bear Market Has Money. It Is Not Buying Crypto

CZ did not say where the money should go, but acknowledged that there was a lot of liquidity floating despite the bear market.

The numbers show why it is not going into crypto. Bitcoin (BTC) trades near $63,037. It is down 45% in a year. That is almost exactly half its October 6 record.

Chamath Is Buying Land, Not Chips

Meanwhile, the Social Capital founder Chamath Palihapitiya, a venture capitalist, entrepreneur, and investor, buys three things at once. Land, a power connection, and an empty building to hold the computers.

“LPS (Land Power Shell) is still the most obvious and fastest path to cash on cash returns,” Palihapitiya wrote.

Palihapitiya is a former senior executive at Facebook (now Meta), a renowned SPAC sponsor, and former minority owner of the Golden State Warriors.

His reason is simple. Towns keep blocking data centers. Every site that already has power gets rarer.

The numbers back him. Data Center Watch counted at least 75 US projects blocked or delayed in early 2026, worth about $130 billion.It was the worst quarter on record. Opposition groups doubled and now operate in 49 states.

Politicians joined in. More than 300 state data center bills were filed in six weeks. Maine missed becoming the first state to ban them outright by one House vote.

Why He Quit the Chip Business

He says he helped start Groq in 2016. Nvidia licensed Groq’s technology last December. The deal was not exclusive. Groq founder Jonathan Ross moved to Nvidia.

Neither company gave a price, but Palihapitiya says $20 billion. Still, he would not do it again as chips have to run too fast, factories have to be too exact, and a startup cannot get enough memory.

How Much Power He Has Bought

Palihapitiya says he and his partner Anita Vlallian have acquired almost six gigawatts (GW). It arrives in stages through 2029.

One deal shows the going rate. Nasdaq-listed TeraWulf used to mine Bitcoin. In July it leased a 401-megawatt site in Hawesville, Kentucky, to Anthropic. The lease runs 20 years and should bring in about $19 billion.

Here is the part that proves his point. That site is not built yet. Power starts flowing in late 2027 and reaches full load in early 2028.

The money is committed anyway. Palihapitiya holds roughly 15 times that much capacity. His is not leased out yet, so the figure shows the size of his bet, not its value.

However, miners got there first, and already own cheap power, land with grid hookups, and empty sheds. Coinbase chief executive Brian Armstrong disputed the mining warning in July.

What Could Go Wrong

Jordi Visser of 22V Research says easy money is over in AI. He expects about 30% a year now.

The land bet also needs the protests to keep coming. If towns start approving data centers again, the scarcity goes away.

TeraWulf’s $19 billion is a forecast too. Its own filing calls it expected revenue.

CZ is right. The money is out there. The question is whether it buys power lines or comes back to Bitcoin and crypto markets.

The post CZ Says Bear Market Money is Hunting, Social Capital Founder Says Skip AI Chips appeared first on BeInCrypto.

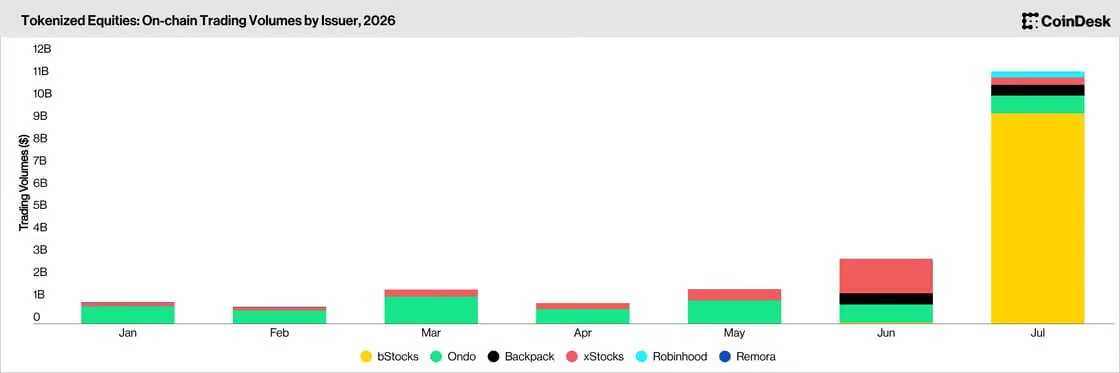

Trading volume for tokenized stocks and ETFs surged 288% to a record $11.3 billion in July, though most of the increase came from a single Binance-linked token.

Binance bStocks accounted for $9.41 billion, or 83.3% of the total, according to CoinDesk Data’s latest Stablecoins & Tokenized Assets report. A bStocks token, QQQB, tracking Invesco’s QQQ ETF, generated $9.27 billion alone, equivalent to roughly 82% of all tokenized-equity volume.

Excluding QQQB, July volume was roughly $2.03 billion, about 30% below the market’s implied June total of $2.91 billion. xStocks volume dropped to $335 million from $1.55 billion, while Ondo recorded $792 million and Backpack $479 million, the report details.

QQQB began trading on Binance on June 30 with zero maker fees through Aug. 31. Binance also began counting stocks and bStocks volume at three times its traded value for some users seeking higher VIP tiers on July 23, though the multiplier does not alter actual trading volume.

An affiliate committee of the crypto-focused Fairshake political operation has increased its ad spending ahead of next week’s primary election in Michigan’s 13th Congressional District, according to Federal Election Commission filings. The spending highlights how cryptocurrency companies continue to shape campaign activity through super PAC and affiliate structures as lawmakers consider major digital-asset policy.

As of Thursday, Protect Progress PAC reported spending more than $2 million on broadcast and digital media related to the Michigan Democratic primary between Rep. Shri Thanedar and challenger Donavan McKinney. The latest filing reflected a rapid acceleration from the amount the PAC reported just a week earlier, including nearly $884,240 in additional ad buys supporting Thanedar and more than $150,000 aimed at opposing McKinney.

Key takeaways

- Protect Progress PAC reported over $2 million in media spending tied to Michigan’s 13th District Democratic primary, based on FEC filings as of Thursday.

- New filings nearly doubled prior reported spend, adding $884,240 for Thanedar and more than $150,000 to oppose McKinney.

- The spending is connected to crypto-aligned political groups, with Protect Progress described as an affiliate of Fairshake.

- Thanedar’s record includes crypto-related legislative actions, including support for stablecoin and digital asset market structure proposals.

- Fairshake affiliates are active in multiple primaries, including races in Washington and Alabama ahead of their own election dates.

Michigan primary: Protect Progress ramps up ad buys

FEC documents show Protect Progress PAC has concentrated its spending on one of the most closely watched parts of this election cycle for crypto industry-aligned political efforts: candidate positioning around digital-asset legislation. In Michigan’s 13th district, the committee’s ad spending is designed to back incumbent Rep. Shri Thanedar while targeting his Democratic primary opponent, Donavan McKinney.

The latest filing effectively widened the committee’s footprint compared with what it had reported in an earlier submission. It added $884,240 in media expenditures supporting Thanedar and more than $150,000 opposing McKinney, bringing total reported media spend to over $2 million.

FEC filings are available through the committee’s FEC record: FEC document inquiry.

Why Thanedar’s crypto record mattered to the PAC

Protect Progress’s focus on Thanedar aligns with the incumbent’s legislative record on digital-asset issues. During his time in the U.S. House, Thanedar voted in favor of stablecoin-focused legislation known as the GENIUS Act. He also voted in favor of a crypto market structure proposal currently under consideration in the Senate, the Digital Asset Market Clarity (CLARITY) Act.

In addition, Thanedar cosponsored the Promoting Innovation in Blockchain Development Act, an effort aimed at protecting blockchain developers. For PAC-affiliated political spending, these votes and sponsorships are often treated as concrete signals of candidate alignment—especially as CLARITY work advances through Congress.

McKinney’s campaign challenged the premise that the race is driven solely by local issues. In a July 21 statement related to the PAC’s spending, McKinney argued that “the crypto lobby is paying my opponent back” for his support of policy decisions tied to the Trump administration.

McKinney also referenced President Donald Trump’s disclosures that he earned more than $1.4 billion from crypto investments in 2025, including through his memecoin, Official Trump (TRUMP), and via his family’s business, World Liberty Financial. Democrats have frequently accused the Trump administration of profiting from its position through laws affecting the crypto sector, including proposals like GENIUS. (Those claims are linked in the original reporting to Trump’s disclosed earnings and related coverage.)

Fairshake affiliates keep spending across the election map

Protect Progress is described as an affiliate of the Fairshake PAC. Fairshake and related committees have been a major force in U.S. federal elections in recent cycles, channeling large sums toward candidates seen as supportive of crypto-industry aligned policy.

Earlier reporting cited that Fairshake was responsible for more than $170 million in spending during the 2024 election cycle through media supporting candidates it viewed as favorable to crypto policy. The same reporting framework also noted that Protect Progress and other affiliates had already directed millions of dollars into 2026 races in multiple states.

More broadly, the consumer advocacy group Public Citizen reported in June that Fairshake and its affiliates accounted for spending of more than $82 million out of roughly $189 million that crypto companies used across the 2026 election cycle. Public Citizen also reported Fairshake’s claimed war chest of $193 million as of January, underscoring the scale of activity behind affiliate PAC machinery.

More primaries: Washington and Alabama spotlight additional spending

While Michigan remains a focal point, other Fairshake affiliates have also targeted races as primaries approach. In Washington’s 4th congressional district, the Fairshake affiliate Defend American Jobs PAC spent more than $65,000 on media to support a Republican candidate. Washington’s primary is scheduled for the same day as Michigan’s.

Alabama’s primary, set for Aug. 11, has similarly attracted attention from Fairshake affiliates. FEC filings indicate Defend American Jobs spent more than $511,000 on media supporting Jerry Carl Jr., a Republican who served in Alabama’s 1st congressional district from 2021 to 2025.

One additional datapoint in the reporting around the Alabama race is the scale of the candidate’s personal wealth. The original article referenced a reported net worth figure of up to $15 million in 2023, citing a separate local report.

What to watch next in crypto-linked elections

As PAC affiliate spending continues to surge in primary contests, voters and market participants will likely watch whether crypto-aligned policy commitments translate into measurable legislative momentum—particularly on stablecoin and market-structure proposals such as GENIUS and CLARITY. The next FEC disclosures may clarify how much more media time these committees add as voting dates approach.

It was precisely six years ago when a rather unknown company in the cryptocurrency industry at the time made a revolutionary change to its asset reserve strategy and adopted Bitcoin. The entity in question, called MicroStrategy back then, started to accumulate BTC en masse and only accelerated its purchases after the 2024 presidential elections in the US.

The community became accustomed to hearing about new acquisitions made by the company, some of which were worth billions of dollars. Its total stash grew exponentially and currently sits at 843,775 units. Within this timeframe, BTC bulls consistently heard that the company (and its former CEO) would never sell… until they did. And then everything changed.

During the most recent earnings call, the company hinted that it has plans to sell up to $5 billion in bitcoin, which is significantly higher than the previously claimed $1.25 billion.

The Latest Shift

Strategy (as it is called now) has gone five consecutive weeks without purchasing BTC, marking its longest acquisition pause in years. Instead of deploying capital into BTC, the firm has steadily increased its cash reserve through recent fundraising activities. As we previously reported, Strategy has been rebuilding its USD position while continuing to explore financial options tied to its expanding portfolio of preferred stock offerings.

In the most recent official change, CEO Phong Le took to X to announce the company’s new primary corporate objective, which reads:

“Our corporate objective is for STRC to trade at $99-$100 over time.”

In the earnings call, he was more specific:

“Our intent is to sell bitcoin for three reasons when we think it’s appropriate for the company. One, fund the U.S. dollar reserve up to $1.25 billion. Additional reasons include funding dividend and interest payments of $1.76 billion a year and funding up to $2 billion in common and preferred stock repurchases,” Le said, according to a FactSet transcript.

The tweet and comments garnered immediate reactions from some well-known industry commentators as well as constant critic Peter Schiff, who was quick to determine that: “In other words, common shareholders are screwed.”

Crypto Kaleo, though, a popular analyst who recently argued that Strategy would have to sell at least 50,000 BTC in the next couple of years to fund dividend payments, wasn’t so kind. In one tweet, he ironically asked whether the CEO remembers when the company’s primary corporate objective was to increase Bitcoin per share before adding: “It was only two months ago, so shouldn’t be difficult!”

In another post, though, he brought the bashing to a higher level, claiming that Strategy is no longer a BTC company. Instead, it operates as a credit company, and its credit rating is “atrocious.”

Strategy went from having a primary objective of increasing Bitcoin per share to trying to make sure their preferred shares trade back to $100… in just two months.

They’re no longer a BTC company.

They’re a credit company.

And their credit rating is atrocious. https://t.co/fHoXr376QY

— K A L E O (@CryptoKaleo) July 31, 2026

The comments below his post were split. Some agreed that Strategy is increasingly resembling a leveraged financial organization rather than a straightforward BTC holding company. Others defended the firm’s approach, noting that maintaining confidence in STRC is essential if Strategy wants to continue raising capital efficiently and safely for future crypto purchases.

STRC Matters

The Saylor-co-founded company launched STRC as part of its growing suite of preferred stock offerings designed to finance its long-term BTC accumulation strategy. However, it needs to trade at its par price of $100 to function properly, and it hasn’t been able to for months. It dumped below $75 at one point, before the company shifted its focus to rebuilding its USD reserve. It has since recovered to almost $90.

As such, some investors view Le’s comments as a tactical, short-term objective rather than believing Strategy has abandoned its Bitcoin-focused vision. Still, the timing has fueled questions about the firm’s evolving identity and strategy, especially given the ongoing market uncertainty.

The post Analyst Blasts Strategy After CEO Signals New Priority Beyond Bitcoin appeared first on CryptoPotato.

The U.S. Securities and Exchange Commission (SEC) has paused Nasdaq’s approval of cash-settled bitcoin index options and will reconsider the decision following a legal challenge from CME Group, the agency said in an order released for public inspection on July 31.

Back in May, the SEC granted Nasdaq PHLX conditional approval to list cash-settled bitcoin index options under the ticker QBTC. The product still required exemptions from the Commodity Futures Trading Commission (CFTC) before it could launch.

CME Group challenged the approval in June, arguing that bitcoin is a commodity and, as such, options tied directly to its value fall under the CFTC’s exclusive jurisdiction rather than the SEC’s.

If the CME is right, the SEC would have no authority to approve QBTC, and Nasdaq would need to register as a CFTC-regulated futures or swaps venue, or redesign the contracts to track a security such as a spot bitcoin exchange-traded fund.

The CME already operates regulated bitcoin futures and options markets, while Nasdaq’s QBTC would compete for the same trading activity without Nasdaq registering under the CFTC framework that governs the CME.

Crypto World

Bitcoin mining difficulty shrinks 14% from this year’s high as plunging revenues force operators to pivot

Bitcoin’s mining difficulty has fallen below its year-earlier level for only the second time in the network’s history as weak mining economics and the shift toward artificial intelligence weigh on capacity growth.

The metric, which measures how difficult it is to mine a Bitcoin block, is now at 126.23 trillion after falling 0.74%, about 1.1% below the 127.62 trillion reached a year earlier and 19.1% from the 155.97 trillion all-time high seen in November 2025.

Difficulty adjusts every 2,016 blocks, or roughly every two weeks, to keep Bitcoin’s average block time near 10 minutes. Falling difficulty indicates that less computing power was competing during the previous adjustment period, while reducing competition for miners that remain online.

The metric has dropped about 14% from its January peak, reached this year, following declines of 10% in June and 5% earlier in July, according to network data.

The only previous year-over-year decline was after China’s 2021 mining ban, which temporarily removed roughly half of the network’s computing power. Difficulty recovered as miners relocated to other regions.

This time around, the plunge is more mining economics-based.

For years, stablecoins have been marketed as crypto’s breakthrough application for cross-border payments, promising near-instant transfers at a fraction of the cost charged by traditional remittance providers.

Sending USDC across a blockchain may indeed cost only a few cents but a new study from the Bank of Italy suggests that isn’t what most people actually pay when they send money home.

In a mystery-shopping exercise spanning 10 international remittance corridors, researchers found that stablecoin-based transfers were not systematically cheaper than conventional money transfer operators once the full journey, from bank account to crypto wallet and back into local currency, was taken into account.

The study, published as Markets, Infrastructures and Payment Systems Paper No. 86, tracked transfers of 200 USDC from Italy to destinations including Argentina, Brazil, South Africa, the UAE and Japan.

End-to-end costs varied dramatically, ranging from roughly 0.3% to almost 9% of the value transferred depending on the corridor and service providers used. Settlement times also differed widely, from around 20 minutes where domestic instant payment systems supported withdrawals to as long as two business days when recipients relied on conventional bank transfers.

Blind spots

A central bank highlighting shortcoming in the promises that stablecoins may make is in some ways to be expected. Traditional financial (TradFi) institutions may have a vested interest in undermining adoption of stablecoins – digital tokens pegged to fiat currencies. Digital currencies and blockchain were designed to remove much of the need for intermediaries, such as central banks, after all.

An affiliate of a political action committee (PAC) funded largely by contributions from cryptocurrency companies Ripple Labs and Coinbase has poured more cash into ads for next week’s primary race in Michigan’s 13th Congressional District.

According to Federal Election Commission (FEC) filings as of Thursday, the Protect Progress PAC had spent more than a combined $2 million on media to support Michigan Representative Shri Thanedar in the state’s 13th district and oppose his Democratic challenger, Donavan McKinney.

The most recent filings effectively doubled what the PAC had reported spending a week prior, with an additional $884,240 on ads to support Thanedar and more than $150,000 to oppose McKinney.

Source: FEC

During his time in the US House of Representatives, Thanedar voted in favor of the stablecoin-focused GENIUS Act legislation and the crypto market structure bill currently under consideration in the Senate, the Digital Asset Market Clarity (CLARITY) Act. He also cosponsored the Promoting Innovation in Blockchain Development Act in an effort to protect developers.

In a July 21 statement on the PAC spending supporting Thanedar, McKinney said “the crypto lobby is paying my opponent back for helping Trump make over $1 billion since taking office.” He was likely referring to the US President disclosing that he earned more than $1.4 billion from crypto investments in 2025, including from his memecoin, Official Trump (TRUMP) and through his family’s business, World Liberty Financial. Many Democrats have accused Trump of using his position to profit from the presidency through laws like GENIUS.

Cointelegraph reached out to Thanedar’s and McKinney’s campaigns for comment on the PAC expenditures but did not receive an immediate response.

Related: US senators sent revised ethics rules to White House for CLARITY Act: Report

Protect Progress is an affiliate of the Fairshake PAC, which was responsible for spending more than $170 million in the 2024 US election cycle through media supporting candidates it considered favoring crypto industry-aligned policies. The Michigan primary is scheduled for Tuesday, but the PAC and its affiliates have already poured millions of dollars into 2026 races in Texas, Illinois and other states.

The US consumer advocacy group Public Citizen reported in June that Fairshake and its affiliates were responsible for spending more than $82 million out of the roughly $189 million crypto companies had used in the 2026 election cycle. Fairshake reported holding a $193 million war chest as of January.

PAC spending in Washington and Alabama with primaries looming

In addition to Michigan’s primaries, the Fairshake affiliate Defend American Jobs PAC spent more than $65,000 on media to support a Republican running in Washington’s 4th congressional, according to FEC filings. Washington is scheduled to hold primaries the same day as Michigan.

Alabama, scheduled to hold primaries on Aug. 11, has also been a focus for Fairshake. FEC filings showed that Defend American Jobs spent more than $511,000 on media to support Jerry Carl Jr., a Republican who represented the state’s 1st congressional district from 2021 to 2025. Notably, the former Alabama lawmaker was one of the wealthiest in the state’s House delegation, with a reported net worth of up to $15 million in 2023.

Magazine: Crypto lobby spending on Republicans far outpaces Democratic support

MicroStrategy endorsed the CLARITY Act on Friday, one day after reporting an $8.22 billion quarterly loss. The bill would rewrite how the United States regulates digital asset trading.

The endorsement hands MSTR shareholders a second variable to price. Regulatory momentum now sits beside the loss, a rising dividend bill, and a share price near 52-week lows.

Why the Timing Matters

Strategy, formerly MicroStrategy, reported second quarter results on July 30 and backed the market structure bill the next day. That sequence turned a policy statement into an earnings postscript.

The quarter was brutal. An $8.32 billion write-down produced an $8.22 billion net loss, or $24.45 per diluted share. A year earlier the same line delivered $32.60 of profit.

The market answered on Friday. MSTR closed at $93.28, down 4.56%, within 14% of its 52-week low of $81.81. Clear Street trimmed its price target to $201 from $240.

Management therefore needed a story the quarter could not supply. Backing clearer rules delivered one.

What Clearer Rules Would Change for MSTR

The bill’s central jurisdictional split is plain enough. Securities-like tokens would sit with the Securities and Exchange Commission (SEC).

Digital commodities would move to the Commodity Futures Trading Commission (CFTC).

For MicroStrategy, that is a funding question rather than a Bitcoin question. The company raised $17.06 billion through at-the-market equity programs this year.

STRC preferred issuance added $7.53 billion, a 254% jump. The catalyst runs through the price of that capital.

Strategy pays 12% on STRC because the shares keep clearing below their $100 stated amount. A wider institutional bid would let it pay less.

Cheaper credit lowers the 10.8% hurdle. If that hurdle ever drops beneath the Bitcoin yield, per-share accretion resumes. That spread is the whole argument for owning MSTR instead of Bitcoin.

Those buyers answer to compliance committees. Executive Chairman Michael Saylor has argued for years that regulation accelerates institutional acceptance rather than restraining it.

“I support advancing the CLARITY Act through bipartisan work to establish clear, durable rules, protect property rights, promote innovation, and strengthen American capital markets. Bitcoin will succeed with or without legislation, but America needs clarity for digital assets,” he articulated.

Follow us on X to get the latest news as it happens

The Spread Clarity Would Have to Close

Clarity would not close that spread quickly. Chief Financial Officer Andrew Kang put the effective cost of credit at 10.8%. Strategy’s Bitcoin yield for the year is 4.5%.

Preferred dividends consumed $400.7 million last quarter, against $49.1 million a year earlier. The STRC rate now stands at 12.00%.

Investors are not paying par for that paper. Strategy repurchased 288,930 STRC shares at an average $86.53, a 13.47% discount to the $100 stated amount.

Bitcoin traded near $63,016 on Saturday, down 1.3% over 24 hours. At that price the 843,775 coin position is worth about $53.2 billion, roughly $10.5 billion below cost.

MSTR carries a market value of $35.87 billion. That collapse in MSTR’s premium tracks the senior claims stacked ahead of common shareholders, not the legal status of Bitcoin.

Strategy also authorized $1.0 billion to repurchase MSTR and has bought nothing. Management will act only below intrinsic value, a threshold it has not declared reached.

The bill’s record is stronger than its calendar. The House passed it 294 to 134 in July 2025. Senate Banking then advanced it 15 to 9 on May 14 under Chairman Tim Scott.

No floor vote is scheduled, however, and the Senate’s state work period begins August 10. MSTR holders inherit a catalyst with no date, while the 10.8% hurdle keeps its own schedule.

The post MicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock appeared first on BeInCrypto.

Firefighters battle huge fire inside building at quarry in Peterhead

Crocs: My Target Was Hit– Downgrading To Hold After Taking The Win

Yorkshire Burrito opens in Coney Street, York city centre

-

Sports6 days ago

Sports6 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business3 days ago

Business3 days agoWhy Trees Belong on the Risk Register

-

Fashion1 day ago

Fashion1 day agoWeekend Open Thread: Wit & Wisdom

-

Tech6 days ago

Tech6 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Politics21 hours ago

Politics21 hours agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Crypto World7 days ago

Crypto World7 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics5 days ago

Politics5 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World3 hours ago

Crypto World3 hours agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics4 days ago

Politics4 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos6 days ago

News Videos6 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Entertainment4 days ago

Entertainment4 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Business4 days ago

Business4 days agoMajor shareholder moves on Canyon

-

Crypto World6 days ago

Crypto World6 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Politics6 days ago

Politics6 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

News Videos2 days ago

News Videos2 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World12 hours ago

XRP Ledger v3.3.0 brings five institutional features

-

Entertainment7 days ago

Entertainment7 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Crypto World4 days ago

Crypto World4 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech5 days ago

Tech5 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos4 days ago

News Videos4 days agoClaude: Build Financial Dashboards in Minutes (2026)

You must be logged in to post a comment Login