Crypto World

Is XRP complementing the banking network or replacing it?

For years the XRP community has promised that XRP would flip SWIFT, the messaging network behind global banking. In 2026 the reality is stranger than the slogan. SWIFT is building its own blockchain ledger that pointedly leaves XRP out, even as XRP gets wired into SWIFT through a side door.

Summary

- The long-running claim that XRP will replace SWIFT has given way to a more complicated 2026 reality in which the two systems both compete and connect.

- SWIFT is a messaging network used by more than 11,000 institutions to move trillions of dollars a day, and it completed its migration to the ISO 20022 data standard in late 2025 and is now building its own blockchain shared ledger.

- That SWIFT ledger deliberately excludes public-network assets like XRP, keeping settlement in tokenized bank deposits, which undercuts the idea that XRP becomes the settlement rail.

- At the same time, a SWIFT integration with the payments firm Thunes gives banks optional access to Ripple’s liquidity products, including XRP as a bridge asset, so XRP is wired in as an option rather than a requirement.

- Ripple itself has hedged by pushing its RLUSD stablecoin as speed without volatility, pointing toward a future where XRP is one optional liquidity leg in a fragmented, interoperable system rather than the network that replaces SWIFT.

The single most durable promise in the XRP community is that XRP will one day replace SWIFT, the messaging network that sits behind nearly every international bank transfer on earth. It is a powerful story, the idea that a fast, cheap digital asset will sweep away a slow, decades-old system and capture the enormous value flowing through global payments, and it has motivated XRP holders for years. The trouble is that the story has always blurred two very different things: SWIFT, which is a messaging system that tells banks how to move money, and XRP, which is an asset that can actually move value.

In 2026, the relationship between the two has become more interesting and more complicated than the slogan suggests. SWIFT is not standing still, having finished a major data-standard overhaul and begun building its own blockchain ledger. Ripple, for its part, has quietly softened its rhetoric from replacing SWIFT to complementing it, and has hedged its own bets by leaning into a dollar stablecoin alongside XRP. The blunt replacement narrative no longer fits the facts.

What makes the question genuinely worth examining now is that both systems are making concrete moves that reveal how they actually see each other. SWIFT has built a blockchain ledger that deliberately leaves XRP out, a telling choice. Yet through a separate integration, XRP has been wired into SWIFT as an optional liquidity tool, an equally telling choice in the other direction.

The result is neither the clean replacement the bulls predicted nor the irrelevance the skeptics expected, but something messier: a fragmented, interoperable landscape in which XRP is one option among several, available but not required. This piece works through what SWIFT actually is and what Ripple actually built, the reality behind the ISO 20022 hype, SWIFT’s own blockchain project and why it excludes XRP, the side door through which XRP gets connected anyway, Ripple’s pivot toward its stablecoin, and an honest verdict on whether XRP is complementing the banking network or replacing it. The answer matters because so much of the XRP investment case rests on which of those two things is true.

What SWIFT actually is, and is not

To judge the rivalry clearly, you have to be precise about what SWIFT does, because the replacement narrative often gets this wrong. SWIFT is not a payment system that moves money; it is a messaging network that moves instructions about money. When a bank in one country needs to send funds to a bank in another, SWIFT carries the standardized message that says, in effect, pay this amount to this account.

The actual money moves separately, through the banks’ own accounts and the correspondent banking system. More than eleven thousand financial institutions use SWIFT, and the value of payments it helps coordinate runs into trillions of dollars every day, which makes it the central nervous system of cross-border finance. It is, above all, a trusted standard and a network, deeply embedded in how banks talk to one another.

The weaknesses the replacement narrative points to are real, but they live in the settlement layer beneath SWIFT, not strictly in SWIFT itself. Because a cross-border payment often hops through a chain of correspondent banks, each holding pre-funded accounts in various currencies and each taking a fee and adding delay, the traditional process can take one to three business days and is closed on weekends and holidays. A payment from Japan to Brazil might pass through three or four intermediaries before arriving.

SWIFT has worked to improve this. Its gpi service, launched in 2017, sped things up so that a large share of payments now credit within thirty minutes and effectively all within a day, with tracking along the way. But gpi modernized the messaging and tracking without changing the underlying correspondent-banking architecture, which still relies on pre-funded accounts and intermediaries. So SWIFT is best understood as the messaging and standards layer of a settlement system whose plumbing is slow, and the question is whether a blockchain alternative can replace that plumbing, the messaging layer, or both.

What Ripple actually built

Ripple’s pitch is aimed squarely at the settlement plumbing, and understanding its core product clarifies where XRP fits. Ripple is a blockchain financial-technology company built around the XRP Ledger, and its enterprise network, historically called RippleNet, lets financial institutions send payments to one another more directly than the correspondent system allows.

The mechanism that actually involves XRP is called On-Demand Liquidity, or ODL, and it is the heart of the XRP value proposition. Instead of a bank pre-funding accounts in every destination country, ODL converts the sending currency into XRP on a crypto exchange, moves that XRP across the XRP Ledger in three to five seconds, and converts it into the destination currency on the other side. The XRP acts as a bridge asset, a momentary carrier of value between two currencies, which removes the need for the expensive pre-funded accounts that slow the traditional system.

The advantages are concrete. An XRP Ledger transaction settles in seconds rather than days, costs a fraction of a cent, and runs around the clock, including weekends, with the network having processed billions of transactions cumulatively and supported tens of billions of dollars in liquidity volume. For a bank or payment provider, ODL promises to free up the capital that would otherwise sit idle in pre-funded foreign accounts, while settling far faster.

This is the genuine innovation behind the XRP thesis: not a new messaging standard, but a new way to handle the settlement leg, using a digital asset as a bridge so value can move without the correspondent-banking overhead. Whether this complements SWIFT or replaces it depends on whether banks adopt the bridge for the settlement leg while keeping SWIFT for messaging, or whether something more wholesale occurs. And as the rest of this piece shows, the 2026 evidence points firmly toward the former.

The ISO 20022 reality check

No discussion of Ripple versus SWIFT is complete without addressing ISO 20022, because few topics generate more confusion and hype in the XRP community. ISO 20022 is a global standard for the format of financial messages, replacing older, less structured message types with a richer format that carries far more data, such as detailed remittance information, compliance data, and structured identifiers.

It improves automation, transparency, and anti-money-laundering monitoring, and it has become the common language toward which the world’s major payment systems are migrating. SWIFT completed its full migration to ISO 20022 in November 2025, ending the long coexistence with legacy message types, a genuine milestone for global finance.

Here is where the confusion sets in. A persistent claim in XRP circles holds that XRP is ISO 20022 compliant in a way that guarantees it a central role once banks adopt the standard. The reality is more limited. Ripple did join the ISO 20022 standards body, becoming one of the first blockchain firms to do so, and RippleNet is built to send and receive ISO 20022 messages, which lets it interoperate cleanly with banks using the standard.

That is a real advantage for Ripple’s network. But the XRP token itself is not ISO 20022 certified, because ISO 20022 standardizes messaging formats and does not certify cryptocurrencies or blockchains at all. The standard governs how payment information is structured, not which asset settles a payment. So while RippleNet’s compliance gives Ripple a seat at the table and makes integration easier, the idea that ISO 20022 anoints XRP as the chosen settlement asset is a misreading.

The standard raises the bar for every payment solution, traditional or crypto, and SWIFT, as the established messaging hub that helped shape the standard, arguably benefits at least as much as Ripple does. ISO 20022 is a prerequisite for interoperability, not a victory for any single token.

SWIFT is not standing still

The replacement narrative tends to picture SWIFT as a static, aging incumbent waiting to be disrupted, but the 2026 reality is that SWIFT is actively building its own path into the blockchain era. After completing the ISO 20022 migration, SWIFT moved on to a more ambitious project: a blockchain-based shared ledger designed to enable round-the-clock cross-border settlement. Having run trials since 2025 with a group of more than forty banks, SWIFT completed the design phase of this ledger in early 2026 and began building its first working version, with the aim of processing real transactions before the end of the year.

The ledger is permissioned and compatible with common smart-contract tooling, and it is tied closely to the ISO 20022 messaging SWIFT already runs, so banks can plug into it through SWIFT’s trusted infrastructure instead of adopting an entirely new public blockchain.

Crucially, SWIFT has been explicit that this is about extending its existing role, not handing the rails to a competitor or issuing new money. Its chief innovation officer framed the effort as preserving settlement in central-bank money, commercial-bank money, or tokenized deposits, while adding the ability to lock in commitments, execute complex cross-border transactions atomically, and share a single auditable record across networks. In other words, SWIFT wants to keep value inside the regulated banking system while gaining the speed and programmability of a blockchain.

To get there, it has been stress-testing nearly every digital-asset rail available, running trials with major banks on tokenized deposits, tokenized bonds, and stablecoins, including a March 2026 interoperability trial that tested several stablecoins. The picture this paints is not of an incumbent asleep at the wheel, but of a network methodically absorbing blockchain technology into its own infrastructure, on its own terms, while keeping its central position as the orchestrator of global banking. That ambition sets up the most consequential detail for XRP holders.

The detail XRP holders cannot ignore

If SWIFT is building its own blockchain ledger, the obvious question for the XRP thesis is whether XRP is part of it, and the answer, pointedly, is no. SWIFT’s shared-ledger project is designed around tokenized bank deposits in currencies such as dollars, euros, and Canadian dollars, transferred between banks under the same regulations that govern wires, and it deliberately avoids public-network assets like XRP.

The design principle is that no value should escape regulated accounts, so reaching a public-ledger asset would require an additional step outside the system’s perimeter, a step the project intentionally does not take. SWIFT’s ledger is permissioned and built for the control and auditability that central banks and supervisors demand, which is precisely the opposite of XRP’s open, public network.

This is a genuinely important development that much of the bullish commentary glosses over. If banks get the round-the-clock, blockchain-based settlement they want from SWIFT’s own ledger, using tokenized deposits they already trust and within the regulated perimeter they are comfortable with, then a significant part of the problem ODL was meant to solve gets solved without XRP. SWIFT is, in effect, building a competitor to the settlement innovation that underpins the XRP thesis, and building it in a way that keeps XRP out by design.

For an XRP holder, this should temper any expectation that banks will inevitably route settlement through XRP simply because blockchain is faster. The institutions have a path to blockchain settlement that does not touch XRP at all, offered by the network they already use and trust. That does not mean XRP is shut out of the banking system entirely, because there is a side door, but it does mean the headline rail SWIFT is building is, by deliberate choice, an XRP-free one.

The side door: how XRP gets wired in anyway

The story has another turn, because even as SWIFT’s own ledger excludes XRP, XRP has been connected to SWIFT through a separate channel, and understanding this optionality is essential to an honest verdict. Through an integration involving the payments firm Thunes, the more than eleven thousand banks on the SWIFT network gain optional access to Ripple’s liquidity products, including XRP as a bridge asset.

The routing works in sequence: a company sends a payment via SWIFT, SWIFT can route it through Thunes, Thunes offers access to Ripple’s ODL infrastructure, and XRP settles that leg. The critical word in that sequence is optional. No step forces a bank to use XRP; the connection makes XRP available as one liquidity choice among others, not a mandated part of the flow.

This optionality is structurally meaningful, but it is a double-edged thing for XRP holders, and the distinction matters enormously for how to read the narrative. On one hand, being wired into SWIFT, even optionally, gives XRP distribution at a scale it could never reach through Ripple’s direct partnerships alone, putting an XRP settlement option in front of thousands of institutions. On the other hand, optional access creates demand optionality, not guaranteed volume.

The banks can use the XRP rail, but nothing compels them to, and many will default to the rails and assets they already know. So the SWIFT connection is real and potentially valuable, but it is a long way from the mandatory, network-wide adoption the replacement narrative imagined. The accurate way to hold it is that XRP now has a foot in the door of the world’s dominant banking network, as one option a bank can choose, while SWIFT simultaneously builds its own settlement ledger that bypasses XRP. Both things are true at once, which is exactly why the simple replace-or-die framing fails.

Ripple’s own pivot tells the story

Perhaps the clearest signal about whether XRP is replacing SWIFT comes from Ripple itself, which has been quietly repositioning in a way that speaks volumes. Alongside its push for XRP-based settlement, Ripple has been aggressively advancing its dollar-pegged stablecoin, RLUSD, and the rationale reveals how Ripple now sees the landscape.

RLUSD is fully reserved with cash and short-term government securities, audited regularly, and positioned as enterprise-grade infrastructure that offers the speed of blockchain rails without the price volatility of XRP. In effect, Ripple is offering banks and payment firms stablecoin-as-a-service: a way to get fast, programmable settlement while holding a stable dollar value instead of a fluctuating token. This directly complements SWIFT’s own tokenized-deposit strategy instead of trying to overthrow it.

The significance of this pivot is hard to overstate for the replacement debate. A company that truly believed XRP was on the verge of replacing SWIFT and capturing all that settlement value would have little reason to build a competing stablecoin product that settles without XRP. Ripple is hedging, building rails that work whether or not banks choose XRP, because it understands that enterprises often want stability over a bridge asset and that the future is more likely to be a fragmented mix of instruments than a single winner.

This is the same complementary posture Garlinghouse has signaled in softening from earlier replace-SWIFT rhetoric toward language about Ripple complementing existing systems. Ripple, in other words, has read the room. It is positioning itself as a provider of modern settlement infrastructure, of which XRP is one component and RLUSD is another, instead of betting everything on XRP displacing the incumbent network. When the company most invested in XRP’s success diversifies away from pure-XRP settlement, holders should take note of what that says about the realistic ceiling of the replacement thesis.

Complement or replace: the honest verdict

So where does this leave the question at the heart of the matter? The honest verdict is that XRP is complementing the banking network far more than replacing it, and that the 2026 evidence has largely retired the clean replacement narrative. The landscape that is actually forming is not winner-takes-all but fragmented and interoperable, a world in which several systems coexist and connect instead of one sweeping the others away.

SWIFT retains its position as the standards-setter and messaging hub of global finance, and it is extending that position into blockchain on its own terms, with a settlement ledger that keeps value inside the regulated banking system and deliberately excludes XRP. Ripple, meanwhile, controls a suite of modern settlement tools, including the XRP Ledger, the optional XRP bridge liquidity now reachable through SWIFT, and the RLUSD stablecoin, and it is selling all of them into a market that increasingly wants choice instead of a single rail.

Within that landscape, XRP’s realistic role is as one optional liquidity leg among many, valuable where it is chosen but never mandated, available to thousands of institutions through the SWIFT connection yet competing against tokenized deposits, stablecoins, and SWIFT’s own XRP-free ledger for each transaction. That is a meaningful role, and it is not nothing: a foot in the door of global banking, with genuine speed and cost advantages, is a real asset. But it is a long way from the world the slogan promised, in which XRP becomes the settlement rail of international finance and captures the value flowing across it.

For holders, the practical takeaway is to replace the binary replace-or-die framing with a more accurate one. XRP’s banking future is about optionality and adoption rates: how often institutions actually choose the XRP rail when given the option, and whether ODL volume grows enough to matter against the token’s large supply. The replacement dream made XRP a bet on inevitability. The complementary reality makes it a bet on competition, in which XRP must win each transaction against capable rivals, including the incumbent it was supposed to replace. That is a more sober thesis, but it is the one the facts now support.

Frequently Asked Questions

Is XRP going to replace SWIFT?

The 2026 evidence strongly suggests no, at least not in the wholesale way the community long predicted. SWIFT is a messaging network used by over eleven thousand institutions, and instead of being swept away, it has modernized, completing its ISO 20022 data-standard migration and building its own blockchain settlement ledger. That ledger deliberately excludes XRP, keeping value in tokenized bank deposits. XRP has been connected to SWIFT optionally through a Thunes integration, giving banks access to XRP as one liquidity choice, but participation is not required. The realistic picture is XRP complementing the banking network as one optional settlement tool, not replacing the network that coordinates global payments.

What is the difference between SWIFT and Ripple?

SWIFT is a messaging network that carries standardized instructions about payments between banks; it does not move the money itself, which travels separately through correspondent banking. Ripple is a blockchain company whose On-Demand Liquidity product actually moves value, converting a sending currency into XRP, moving it across the XRP Ledger in seconds, and converting it to the destination currency, which removes the need for pre-funded accounts. So SWIFT is primarily the messaging and standards layer, while Ripple targets the settlement layer beneath it. They operate at different points in the payment process, which is part of why they can complement each other instead of being pure substitutes.

Is XRP ISO 20022 compliant?

This is widely misunderstood. RippleNet, Ripple’s payment network, is built to handle ISO 20022 messages and Ripple joined the standards body, which helps its network interoperate with banks adopting the standard. But the XRP token itself is not ISO 20022 certified, because ISO 20022 is a messaging-format standard that does not certify cryptocurrencies or blockchains at all. It governs how payment data is structured, not which asset settles a payment. So the popular claim that ISO 20022 guarantees XRP a central role is a misreading. The standard raises the bar for all payment solutions and arguably benefits SWIFT, the established messaging hub, at least as much as it benefits Ripple.

Does SWIFT’s blockchain ledger use XRP?

No, and this is one of the most important developments for XRP holders. SWIFT’s blockchain shared ledger, which moved into its building phase in 2026, is designed around tokenized bank deposits and deliberately avoids public-network assets like XRP. It is permissioned, keeps value inside regulated accounts, and is built for the control and auditability central banks require. This means SWIFT is creating a path to round-the-clock blockchain settlement that does not involve XRP, solving much of the problem ODL was meant to address without the token. Banks wanting blockchain settlement have an XRP-free option from the network they already trust, which meaningfully tempers the case for inevitable XRP adoption.

How does XRP connect to SWIFT then?

Through a separate integration involving the payments firm Thunes. The arrangement gives the more than eleven thousand banks on SWIFT optional access to Ripple’s liquidity products, including XRP as a bridge asset. A payment can route from SWIFT through Thunes to Ripple’s ODL infrastructure, where XRP settles the leg. The key point is that this access is optional, not mandated. It gives XRP exposure to a vast network of institutions, which is truly valuable for distribution, but it creates demand optionality instead of guaranteed volume, since banks can choose the XRP rail but are never forced to use it over the alternatives available to them.

What does this mean for XRP’s value?

It reframes the XRP thesis from inevitability to competition. The replacement narrative implied XRP would automatically capture global settlement value; the complementary reality means XRP is one optional liquidity tool that must win each transaction against tokenized deposits, stablecoins, including Ripple’s own RLUSD, and SWIFT’s XRP-free ledger. XRP retains real advantages in speed, cost, and round-the-clock settlement, and its optional presence on SWIFT gives it broad distribution. But its value will depend on how often institutions actually choose the XRP rail and whether that volume grows enough to matter against XRP’s large supply, instead of on a wholesale replacement of SWIFT that the current evidence does not support.

This article is information, not investment advice. Details of SWIFT’s and Ripple’s products, integrations, and strategies reflect reporting available as of June 27, 2026, and can change. The competitive landscape in cross-border payments is evolving quickly. Nothing here is a recommendation to buy or sell XRP or any asset. Verify current details from primary sources and consider your own circumstances before making any decision.

Prediction-market platforms are increasingly trying to control more of their own trading stack—an “operational consolidation” trend that analysts at Bernstein say could accelerate mergers and acquisitions across crypto exchanges, brokerages, sportsbooks, and consumer trading apps.

In a research report released on Monday, Bernstein argued that major players are consolidating both distribution and execution functions, tightening links between what used to be separate parts of the market. The shift matters for investors and operators because it can change fee structures, reduce dependence on external infrastructure providers, and potentially reshape how regulators view these products.

Key takeaways

- Bernstein characterizes the sector’s shift as “operational consolidation,” with platforms merging distribution, brokerage, exchange, and clearing functions.

- Several mainstream consumer and prediction platforms have moved toward tighter in-house routing and infrastructure control, according to Bernstein’s examples.

- Owning more of the stack can preserve fees that previously went to outside partners, making acquisitions an efficient way to fill gaps or gain licenses.

- Greater vertical integration may also increase legal and regulatory pressure as the line between financial trading and gambling becomes harder to define.

- State-by-state approaches—alongside ongoing legal challenges—could limit how quickly consolidation proceeds.

Platforms move from partnerships to vertical control

Historically, prediction markets often relied on third-party infrastructure for routing, exchange operations, or clearing—arrangements that made it easier to launch products without building everything internally. Bernstein says that model is weakening as leading consumer platforms consolidate functions across the prediction-market workflow.

In its report, Bernstein pointed to examples spanning different parts of the ecosystem. Robinhood has routed major World Cup contracts through Rothera, the exchange it jointly owns with Susquehanna, according to Bernstein’s account. DraftKings is also cited by Bernstein for launching DKeX and shifting volume away from venues that previously handled some execution, including CME and Crypto.com infrastructure.

The report also highlights consolidation efforts at the crypto-operations layer. Bernstein cited Coinbase’s acquisition of The Clearing Company—framed in related coverage as a move tied to expanding prediction-market capabilities—and Coinbase’s launch of event contracts, adding to the pattern of larger consumer crypto firms seeking greater control over the prediction-market stack.

Why “owning the stack” can change deal economics

Bernstein’s central argument is straightforward: integration can be a direct business advantage. By controlling more of distribution, brokerage, execution, and clearing, platforms can keep revenue streams that would otherwise be shared with specialized partners.

That matters because acquisitions can become a faster path to operational control than building from scratch. Bernstein suggested that deal-making may accelerate as companies pursue missing components—whether that means distribution reach, exchange capabilities, or clearing infrastructure—using purchases to close gaps and strengthen end-to-end product delivery.

However, vertical integration doesn’t only affect profitability. It also reshapes the competitive landscape: businesses that historically operated in different industries—consumer finance apps, sportsbooks, exchanges, and crypto trading infrastructure providers—can end up competing under a single set of product and customer expectations.

Regulatory conflict is the largest constraint

Bernstein singled out regulation as the principal friction point for larger integrations. As prediction markets blend with brokerages, sportsbooks, and exchanges, regulators may scrutinize whether specific products should be treated as financial derivatives or as gambling.

The report suggests that these classifications are not merely academic. They drive enforcement priorities, licensing requirements, and how courts determine jurisdiction. Bernstein warned that such questions could feed antitrust disputes as firms attempt to merge capabilities across multiple market segments.

The regulatory tension has already played out in the U.S. Minnesota enacted what the CFTC described as the first outright ban on prediction markets, while Illinois adopted legislation requiring platforms to obtain a state license before offering sports event contracts—developments Bernstein cited through earlier coverage.

Kalshi challenged restrictions in both states, arguing that federally regulated exchanges fall under the CFTC’s exclusive authority. Bernstein’s framing implies that these legal fights create a practical uncertainty: consolidation may make commercial sense, but execution could remain constrained until regulators and courts clarify where federal derivatives oversight ends and state gambling authority begins.

What to watch as consolidation accelerates

With platforms continuing to move routing, exchange functions, and clearing in-house, the next phase of the sector may hinge less on product launches and more on legal outcomes—particularly whether courts establish a clearer boundary between federal trading regulation and state gambling rules. Until that boundary hardens, consolidation could keep happening, but with deal structures and operating decisions likely shaped by ongoing jurisdictional risk.

Onchain demand stayed soft through the slide, according to Glassnode data. The number of active addresses, a rough gauge of how many users are actually transacting, sat around 618,000, in the middle of its recent range rather than breaking higher.

The value of coins moving across the network held near $4.2 billion, just above the bottom of its range around $3.6 billion, pointing to subdued rather than surging activity, the firm said in a Monday report.

Total transaction fees, or what users pay to move funds and a read on competition for space in each block, kept contracting. Together, the three say demand has not picked up even with prices lower.

Adding to the caution, Strategy, the largest corporate holder of bitcoin, said Monday it may sell more than a billion dollars of the token under a new program to shore up its finances, a reversal of founder Michael Saylor’s long-standing refusal to sell.

The prospect of those sales hangs over an already thin market. That leaves crypto where it has traded for weeks, pinned by a strong dollar and a lack of fresh demand rather than any single shock.

The next tests are whether the dollar’s climb stalls and whether the yen’s slide forces Japan to step in, a move some warn could unwind the cheap-yen borrowing long used to fund risk trades worldwide.

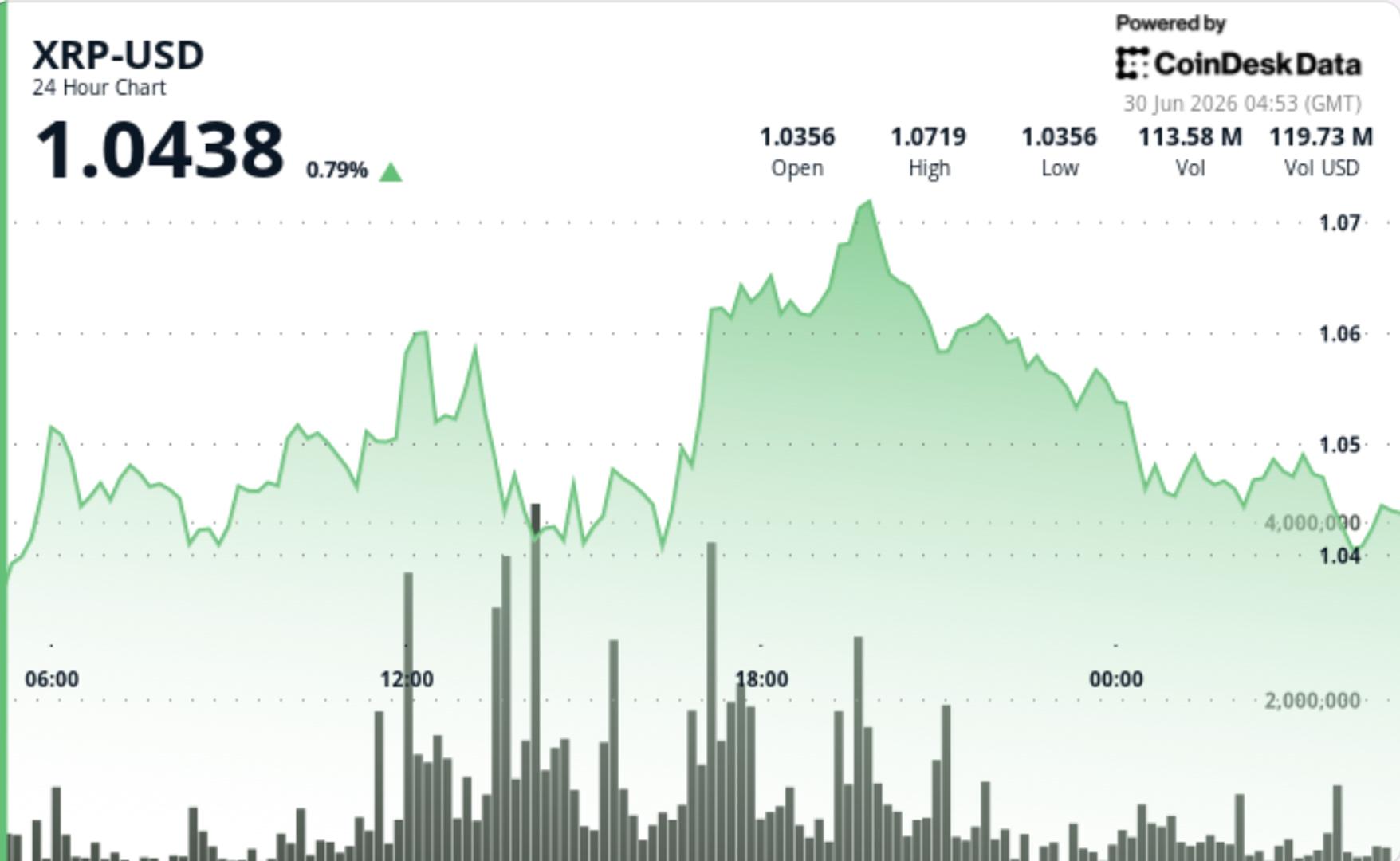

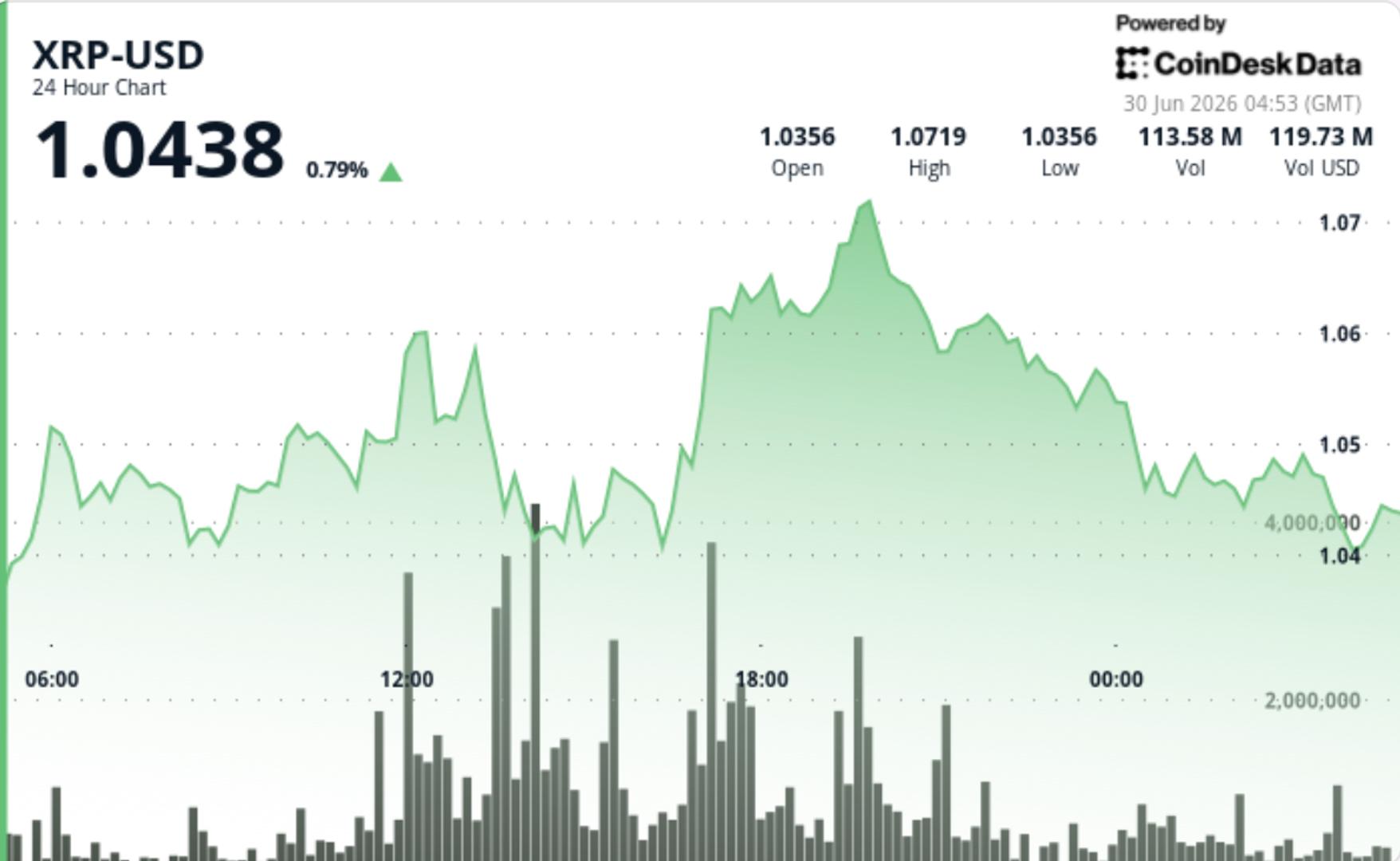

• The token traded in a $0.0435 range and continued to hold above the $1.00 psychological support level.

• The main burst of activity came on June 29 at 17:00, when volume reached 86.5 million XRP, about 67% above the 24-hour average.

• Price later consolidated between $1.03 and $1.06, leaving the market range-bound rather than in a confirmed recovery.

Technical Analysis

• The key development is that XRP continues to defend $1.00 even after a 19% monthly decline.

• The leverage reset improves the setup. Open interest has fallen sharply, funding has turned negative and forced long liquidations have cleared out crowded positioning.

• The on-chain picture is stronger than the chart. Active addresses are rising, ETF inflows are continuing and exchange reserves remain stable, but price is still below major moving averages.

• XRP remains capped by resistance near $1.10, with larger barriers near the 50-day EMA around $1.20 and the 100-day EMA around $1.31.

• The 4-hour RSI has recovered from oversold territory to 46, but momentum remains below the neutral 50 level.

What traders should watch

• $1.00 remains the key support level. A break below it would put $0.90-$0.87 back in focus.

• $1.06 is the first short-term resistance level, followed by $1.09-$1.10, where recent rallies have stalled.

Bitcoin (BTC) steadied itself over the weekend after a volatile week that saw its value drop to its lowest level since September 2024.

The flagship cryptocurrency fell to a low of $58,000 on Thursday, struggling against sustained ETF outflows, a hawkish Federal Reserve, concerns around Strategy, and a stronger US Dollar.

Bitcoin Stabilizes After Sharp Selloff

BTC experienced a substantial downturn last week, falling from a high of $65,553 on Monday to a low of $58,000 on Thursday. ETF outflows, a stronger US Dollar, a hawkish Federal Reserve, and the ongoing geopolitical situation continue to pressure Bitcoin and the broader market. However, price action steadied over the weekend and has reclaimed the $60,000 level after falling to a low of $58,800 earlier today.

Bulls have defended $58,000, a key support level, despite substantial selling pressure. BTC maintained its position above $58,000 over the weekend despite fresh US-Iran tensions over a volatile ceasefire. Markets had registered a substantial recovery earlier this month after tensions in the Middle East thawed, easing oil prices and inflation concerns. However, the rally soon fizzled out, pushing the price to sub-$60,000 levels.

BTC’s price action could go one of two ways. If the flagship cryptocurrency fails to regain momentum and slips below $58,000, a drop toward $55,000 or lower can be expected. However, a clean recovery above $60,000 would suggest buying pressure returning.

Strategy Under Pressure

Concerns around Strategy’s capital structure have also impacted market sentiment. STRC, the company’s preferred stock product, is currently trading around $74.57, significantly lower than its intended $100 mark. Annual dividend obligations have risen to $1.2 billion, while dividend coverage dropped to 14 months thanks to declining cash reserves. Strategy used its stock premium to raise capital for more BTC acquisitions. However, weak pricing has made it substantially harder for the Michael Saylor-led firm to depend on this model to raise additional capital.

Meanwhile, CryptoQuant has urged Strategy to pause its acquisitions and rebuild its cash reserves. However, the plea looks to have fallen on deaf ears, with Michael Saylor teasing another buy, posting the company’s Bitcoin tracker with the caption “We’re going to need more charts.”

Analysts Divided

Meanwhile, analysts remain divided on Bitcoin’s price action. Analyst Market Watcher highlighted a downtrend from July and August highs of around $70,000 and $67,000, adding that a break of the line would make investors more willing to deploy capital. The analyst described the current price range as an “indecisive summer chop.” However, he added that a break of the main trend around $58,000 could change the entire setup.

Another analyst, EGRAG CRYPTO, highlighted Bitcoin’s 12-month cycle, adding that the current cycle may be different from the usual “three years up one year down” cycle. Meanwhile, CryptoQuant analyst Crazzyblockk stated that Bitcoin is currently in an undervalued zone after its short-term holder realized dominance fell to 27.6%. Previous cycles have witnessed market tops when short-term holders controlled the realized capital. Bear markets witness the opposite, as short-term holders realize their losses and realized capital drops.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

The US Securities and Exchange Commission has won its fraud suit against crypto platform NanoBit Limited, nearly two years after the agency accused it of stealing hundreds of thousands of dollars from at least 18 investors between 2023 and 2024.

The announcement by the SEC on Monday came nearly two weeks after the US District Court for the Eastern District of New York entered a final judgment against four entities and two individuals tied to the NanoBit fraud case on June 16.

The SEC alleged that NanoBit’s operators impersonated financial professionals in WhatsApp groups to trick investors into depositing funds on the fake platform. Instead, the funds were allegedly diverted to scheme participants, the SEC said.

The case is another example of the SEC’s continued crackdown on crypto-themed fraud under the Trump administration, even as the agency has softened its regulatory approach to crypto companies and revised what it considers to be a securities offering.

On May 29, the SEC charged a Texas man with allegedly running a fraud scheme that raised more than $12 million from roughly 150 investors by falsely claiming to use AI-powered trading bots to generate guaranteed returns.

In April, the SEC also charged crypto executive Donald Basile and two companies he controlled for raising roughly $16 million from hundreds of investors through false claims tied to a crypto token called Bitcoin Latinum.

NanoBit perpetrators ordered to pay $5.4 million

The New York court found that the defendants violated US securities laws and issued permanent injunctions against them, prohibiting them from engaging in the issuance, purchase or sale of securities.

Related: Crypto scammers exploit World Cup ticket demand, TRM warns

NanoBit was ordered to pay a $1.18 million fine, disgorgement of more than $532,000 for the ill-gotten gains and prejudgment interest of nearly $81,200, totaling nearly $1.8 million.

NanoBit’s affiliates — Radiant Horizons, Sweet Karma and Zhao Deli — were each ordered to pay a $1.18 million fine, while one of the scheme’s main orchestrators, Jiajie Liu, was ordered to pay about $120,000 in penalties, disgorgement and prejudgment interest.

In the September 2024 complaint, the SEC alleged that NanoBit investors were solicited on social media, such as Instagram, before being added to the WhatsApp groups.

Investors were allegedly shown a fake dashboard depicting rising returns, creating the illusion that their funds were growing.

It allegedly persuaded investors by falsely claiming that its affiliate, NanobitUS Securities, was an SEC-registered broker, while also promoting fake initial coin offerings (ICOs) promising substantial returns.

However, “no transactions took place on the NanoBit platform and investors’ funds in fact went to scheme participants who wired more than $2 million to bank accounts in Hong Kong and misappropriated hundreds of thousands of dollars’ worth of investors’ crypto assets,” the securities regulator alleged.

The SEC alleged that investors who sought to withdraw funds were met with excuses and asked to pay large fees, while others were removed from the WhatsApp groups for questioning the platform’s legitimacy.

Magazine: The end of anonymity? AI could unmask crypto’s hidden identities

Ethereum co-founder Vitalik Buterin has laid out a longer-term cryptography blueprint for private, onchain voting that aims to avoid the need for a trusted group to handle ballots. In a technical essay published Monday, Buterin argues that a cryptographic technique known as indistinguishability obfuscation (iO) could let blockchain systems compute voting results while keeping individual votes hidden and limiting opportunities for collusion.

The proposal centers on replacing traditional threshold-style committees—groups that collectively decrypt encrypted votes—with protected programs designed to reveal only the final outcome. Buterin cautions, however, that the approach is not yet practical, with the most conservative versions requiring extremely heavy computation and faster variants depending on less-tested security assumptions.

Key takeaways

- Buterin’s proposal uses indistinguishability obfuscation (iO) to create “protected programs” that can compute vote tallies without exposing ballot contents.

- The design is intended to reduce reliance on threshold committees that jointly decrypt results, potentially lowering the trust needed for private onchain voting.

- Even with iO, blockchains remain essential because protected programs can’t stop being copied or support state updates on their own.

- Buterin describes current constructions as computationally impractical, positioning the idea as research direction rather than a near-term deployment plan.

From encrypted ballots to protected programs

Buterin frames iO as a method for hiding software logic. In his explanation, iO transforms a piece of code into a protected program such that others can run it to obtain the intended output, but cannot inspect the internal code or retrieve embedded sensitive data. He emphasizes that this approach focuses on concealing the program itself, rather than solely masking the data it processes.

In the context of voting, the idea would be to package the tallying and eligibility logic into an obfuscated program. Voters could submit encrypted ballots, and the system would execute the protected program to produce a final tally without exposing how individual participants voted. In effect, this would remove a key requirement of many private voting schemes: coordinating a set of operators (a threshold committee) that holds decryption capabilities and must behave honestly.

Buterin also notes that blockchains still have to do the heavy lifting for public coordination and evolving state. While iO can hide computation details, it cannot prevent copying or manage changing information by itself, so a blockchain—or similar distributed infrastructure—would remain necessary for the system to function over time.

Why dropping threshold committees matters

Private onchain voting typically involves operational trust assumptions, even when votes remain cryptographically protected. In many designs, groups of operators must safeguard information and follow the protocol correctly—particularly during decryption or tallying. Buterin argues that eliminating (or sharply reducing) the need for threshold committees could make decentralized governance more resistant to manipulation.

In his view, reducing this dependency could also lower the risk of insider interference and enable voters to participate without exposing voting behavior. However, the core promise is not only privacy for individuals; it is also a shift in who has meaningful control over the outcome. Instead of multiple parties jointly controlling decryption, the tally would be derived from running a protected program intended to reveal only what the system needs to disclose.

That said, the essay’s emphasis on security assumptions and computational feasibility underlines that the practical challenge is formidable. The approach is designed to minimize trust—but it still must be engineered so that security holds under realistic operating constraints.

Security trade-offs and why deployment is still out of reach

Buterin’s assessment is explicit: the idea, while conceptually aligned with “almost no trust assumptions,” is not ready for real-world use. He describes the most conservative constructions as requiring what he calls “galactic” amounts of computation—suggesting that the computational overhead would overwhelm any system intended for everyday participation.

He also points to a tension faced by cryptographic research more broadly: faster constructions tend to rely on weaker or less-tested security assumptions. In other words, an implementation that is technically feasible may not yet offer the same level of assurance as the most conservative theoretical design. This leads Buterin to characterize iO-based private voting less as a deployment-ready system and more as a long-term research direction.

For investors and builders watching Ethereum’s roadmap, the takeaway is that privacy research is moving toward more rigorous “how it’s computed” privacy—yet the path from cryptographic theory to production-grade systems will require major advances in efficiency and confidence in assumptions.

How this fits into Buterin’s broader privacy agenda

This iO voting essay builds on earlier work by Buterin linking advanced cryptography to stronger privacy and reduced coercion risk. In October 2024, he connected iO with private voting in an Ethereum roadmap he published, arguing that the technique could improve privacy guarantees.

He has also pushed for practical privacy steps within Ethereum’s ecosystem. In April 2025, Buterin proposed a more immediate privacy roadmap that called for integrating privacy tools into existing wallets. That proposal also advocated for stronger protections against data collection by infrastructure providers used by wallets to access Ethereum, reflecting an emphasis on privacy not just at the cryptographic layer but in the surrounding network services.

Buterin has additionally directed personal funds toward privacy-preserving projects. According to earlier coverage by Cointelegraph, on Jan. 30 he earmarked 16,384 Ether (ETH) (about $45 million at the time) to support initiatives focused on privacy, open infrastructure, and self-sovereign tools.

Read together, these threads show a consistent direction: privacy improvements are being pursued both through long-horizon cryptographic designs like iO and through nearer-term engineering changes that could reduce exposure to tracking and data collection.

For now, the most important question is what—if anything—can be improved to make iO-based voting computationally viable without sacrificing security confidence. Readers should watch for follow-up research that narrows the performance gap and clarifies which security assumptions would be acceptable for real deployments.

Bitmine Immersion Technologies said it added more than 27,000 Ether to its treasury last week after completing a $43 million purchase. The update comes as the company prepares for greater visibility with its inclusion in the Russell 1000, an index that many funds use as a benchmark for passive investing.

In a disclosure shared on Monday via PR Newswire, Bitmine said its Ether holdings reached just over 5.7 million ETH. The company reported buying the tokens at an average price of $1,569 per Ether and said it now holds about 4.7% of Ethereum’s 120.7 million token supply—moving it closer to its stated objective of owning 5% of the asset.

Key takeaways

- Bitmine reported a $43 million Ether purchase that increased holdings to just over 5.7 million ETH at an average $1,569 per token.

- The firm said its stake is now roughly 4.7% of Ethereum’s circulating supply, edging toward a 5% target.

- Bitmine’s Russell 1000 inclusion is expected to bring additional institutional demand through funds that track the index.

- Despite broader Ethereum developments, Bitmine’s chairman described the prior week as difficult for crypto investors after Ether fell about 8%.

- Other crypto-linked firms were also added to the Russell 3000 Index recently, expanding how traditional investors encounter crypto treasury businesses.

A growing Ether treasury amid a volatile week

Bitmine’s announcement frames the latest acquisition as part of a continued push to build a larger corporate Ether position. After its recent buy, the company said it holds slightly above 5.7 million Ether and has reduced the gap to its 5% supply goal.

The filing also highlights how market price swings can complicate treasury strategies even when the broader Ethereum ecosystem is active. Bitmine chairman Tom Lee characterized the preceding week as challenging for crypto investors, saying Ether fell by 8%. In his remarks, he noted Ethereum-related positives—including the creation of Ethlabs—and pointed to a softer tone from the Bank of England regarding stablecoins.

Even with those developments, Lee said the selloff played out in ways that can influence investor behavior. He later attributed some of the pullback to what he described as “window dressing,” where investors reduce exposure to assets that have declined over recent months.

Why Russell 1000 inclusion could change Bitmine’s investor base

Beyond the treasury update, the more market-facing development is Bitmine’s addition to the Russell 1000, which tracks the largest 1,000 US companies. Bitmine said this step may increase investor demand for its shares because many mutual funds, ETFs, and pension funds follow Russell indices and must buy constituents once they are added.

Lee previously discussed this mechanism when Bitmine was first under consideration for the Russell index in May. He said passive index funds can account for up to 25% of the market capitalization of stocks included in the index.

In Monday’s comments, Lee said Russell 1000 membership is expected to add “hundreds and possibly thousands” of additional institutional investors as equity owners of Bitmine. For a company whose business model is closely tied to holding and managing Ether exposure, a shift in the shareholder base can matter: institutional ownership patterns can influence liquidity, trading volume, and the range of investors willing to hold crypto-treasury equities over the long run.

Stock movement follows Ether, despite new corporate catalysts

Bitmine’s share performance on Monday reflected both the company’s corporate update and the broader pressure on Ether. The stock rose 1.7% to close at $13.80, according to the article, but it has fallen roughly 9% over the past week in tandem with Ether’s decline.

That pattern underscores an important tension for investors watching crypto treasury businesses: even when the company executes meaningful purchases or secures index inclusion, the underlying price of Ether can still dominate near-term equity performance. In other words, Bitmine’s catalysts may improve access to new capital sources, but the valuation of its holdings remains directly linked to market conditions for ETH.

Broader index adoption for crypto-related firms

The Russell inclusion story is not unique to Bitmine. The article noted that rival crypto treasury firms Sharplink and Forward Industries—along with Gemini and Galaxy Digital—were also added to the Russell 3000 Index on Friday. The Russell 3000 tracks the largest 3,000 US companies, which can create additional pathways for traditional market participants to build exposure to crypto-linked public equities.

For investors, this trend signals a gradual normalization of crypto-related businesses inside mainstream index ecosystems. However, it also raises a watchpoint: as more crypto treasury firms enter large-cap indices, their stock demand may become more mechanically tied to index-tracking flows, potentially increasing short-term trading activity around reconstitution dates.

At the same time, it does not remove the central risk for equity holders—Ether’s market volatility. Bitmine’s chairman’s remarks about window dressing and short-term reductions in exposure illustrate how quickly sentiment can shift even when broader Ethereum developments continue.

Investors should watch whether Bitmine’s Russell 1000 entry translates into sustained institutional ownership or whether near-term trading remains dominated by ETH price movements. The next key question is how the company continues to balance incremental Ether acquisitions with the equity volatility created by shifting crypto market sentiment.

In recent days, USDT has traded at a premium across several Indian exchanges, with premiums generally ranging between 7% and 10%, depending on liquidity and market activity. On CoinSwitch, USDT has traded at around a 9% premium over the past few days.

“At CoinSwitch, users always see the live buy and sell price before placing an order. We do not charge any hidden fees beyond our disclosed brokerage. The premium reflects prevailing market conditions rather than any platform-imposed markup,” Singhal said.

Both CoinDCX and CoinSwitch attribute the premium entirely to organic supply-and-demand dynamics: more buyers than sellers, thinner liquidity near the global reference price, and a market mechanism — not platform pricing decisions — setting the rate. Neither executive directly addressed the ED’s enforcement action or its effect on token supply in their statements.

Nevertheless, the supply squeeze that drove the premium unusually higher could be linked to the enforcement action.

Market makers and liquidity provides could have scaled back from sourcing USDT overseas after the ED’s action, which would show up exactly as a supply-side liquidity shortage, the same mechanism both Thakur and Singhal describe in general terms.

Operating on Indian exchanges has been relatively tougher for market makers because of a flat 30% tax on gains, no allowance to offset losses, and a restrictive 1% tax deducted at source (TDS). These rules have long contributed to market dislocations.

The U.S. Securities and Exchange Commission has secured a final default judgment in its case against NanoBit Limited and several linked defendants.

Summary

- SEC judgment orders NanoBit-linked defendants to pay over $5.5M after alleged WhatsApp investor fraud scheme.

- Regulators said the fake platform used group chats, false broker claims, and fake ICO pitches.

- The case shows fraud enforcement continues even as broader crypto rulemaking moves toward clearer standards.

According to the SEC litigation release, the U.S. District Court for the Eastern District of New York entered the judgment on June 16, nearly two years after the agency filed its complaint.

The court ordered NanoBit, Radiant Horizons Limited, Sweet Karma Fashion Inc., Zhao Tropical Deli Inc., Jiajie Liu and Hua Zhao to pay penalties, disgorgement and interest. The final judgment lists total payment obligations of about $5.52 million across the defendants.

SEC says NanoBit platform was fake

The case centered on claims that NanoBit operated as a fake crypto trading platform. The SEC said the defendants and other scheme participants used social media apps to reach investors before moving them into WhatsApp groups.

In its September 2024 complaint, the agency said the participants posed as financial industry professionals and built trust with investors. The SEC alleged that NanoBit falsely claimed an affiliate, NanobitUS Securities, was registered with the regulator.

WhatsApp groups and false broker claims

The SEC said the supposed financial professionals promoted fake initial coin offerings and presented NanoBit as a working trading venue. Investors allegedly saw platform screens that appeared to show crypto prices, account balances and trading activity.

“No transactions took place on the NanoBit platform” and that “investors’ funds in fact went to scheme participants,” the regulator said.

According to the SEC, more than $2 million was wired to bank accounts in Hong Kong, while hundreds of thousands of dollars in crypto assets were misused.

Fraud enforcement continues

The NanoBit judgment adds to a string of crypto fraud actions even as U.S. regulators change their wider approach to digital asset policy. As reported by crypto.news, the SEC had already named NanoBit and CoinW6 among relationship investment scam cases in its 2024 enforcement review.

As reported by crypto.news, the SEC also charged Texas resident Nathan Fuller in May over an alleged $12.3 million AI crypto arbitrage scheme. That case involved claims of guaranteed returns from a trading robot, according to the report.

The same fraud risks have spread beyond fake trading platforms. As reported by crypto.news, TRM Labs warned this month that scammers had created World Cup-related crypto fraud operations, including fake ticketing sites and a fixed-match betting scheme.

The SEC has also warned investors about group-chat scams. In a December 2025 investor alert, Investor.gov said people should “never rely solely on information from group chats” when making investment decisions. The agency also urged investors to check the background of anyone offering or selling investments.

Strategy opened a new funding chapter after authorizing Bitcoin monetization for credit support, preferred security buybacks, and dividends. The company also paused Bitcoin purchases while raising $1.15 billion through MSTR stock sales. The move shifts part of its treasury policy from pure accumulation to broader capital management.

Bitcoin Monetization Plan Takes Shape

Strategy adopted its Digital Credit Capital Framework on June 29 through a new regulatory filing with broader funding options. The framework targets stronger liquidity, preferred security support, and long-term exposure to Bitcoin. It also aims to protect shareholder value as the firm manages larger credit obligations and capital needs.

The central tool is a Bitcoin Monetization Program, which allows controlled BTC sales for defined purposes rather than simple accumulation. Strategy may generate up to $1.25 billion and place the cash in its USD Reserve for near-term needs. The reserve can fund dividends, interest payments, cash buffers, and approved repurchase programs without selling new shares.

However, the company said the program does not require any Bitcoin sales under current conditions or future obligations. Therefore, Strategy may keep its full Bitcoin position if management avoids monetization and protects its treasury. Still, the recent 32 BTC sale raised market questions among traders and analysts after the new plan became public.

MSTR Stock Sale Funds Balance Sheet

Strategy reported no Bitcoin purchases for the week ending June 28, ending a steady accumulation phase after active weeks. The pause ended its recent buying streak, although the company kept its total holdings unchanged for now. Its treasury still holds 847,363 BTC, bought for an aggregate cost of $64.10 billion.

At the same time, Strategy sold 12.67 million MSTR shares under its at-the-market program to raise fresh cash. The sale produced about $1.152 billion in net proceeds for the company during the same period after fees. That capital gives management more room to handle payouts, reserves, and credit security needs without immediate Bitcoin buying.

The stock sale also adds context to the new framework and its wider treasury shift after the weekly update. Strategy has long used equity issuance and preferred securities to support Bitcoin accumulation while protecting BTC exposure. Now, it has added Bitcoin monetization as another funding option for balance sheet management as markets change.

Digital Credit Securities Buyback Gets Approval

Strategy also authorized repurchases of up to $1 billion in Digital Credit Securities under the new framework. The approval covers STRC, STRF, STRD, and STRK, depending on management’s capital structure view and pricing. The company said buybacks could occur if they improve liquidity, security pricing, or capital efficiency.

If Strategy uses Bitcoin proceeds for repurchases, it must route them through the monetization program. This link gives the company a formal path from BTC sales to credit support and cash reserves. Even so, the framework leaves final action with management and market conditions, not automatic triggers.

The company also lifted the annual STRC dividend rate to 12% from July 1. Strategy designed to help pull STRC closer to its $100 par value over time. STRC rose 9.48% in premarket trading to $81.64 after the announcement, showing a sharp early response.

SCOTUS rules location data is protected by Fourth Amendment

Ripon Grammar School named Northern school of the year

Russell 2000 Slips 0.6% as Small-Cap Stocks Face Rotation Pressure Amid Mixed Economic Signals

-

Sports6 days ago

Sports6 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics4 days ago

Politics4 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics4 days ago

Politics4 days agoPotential 2028er World Cup attendee leaderboard

-

News Videos1 day ago

News Videos1 day agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Business4 days ago

Business4 days agoAsia stock markets slide as tech shares slump

-

Tech4 days ago

Tech4 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World6 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business6 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World3 days ago

Crypto World3 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports3 days ago

Sports3 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech2 days ago

Tech2 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World4 days ago

Crypto World4 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World4 days ago

Crypto World4 days agoRTX holders must register wallets before token distribution begins

-

Crypto World5 days ago

Crypto World5 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

You must be logged in to post a comment Login