Crypto World

What is a bonding curve? Memecoin pricing explained

Before a memecoin reaches a normal exchange, its price is not set by buyers and sellers meeting in a market. It is set by a formula. That formula is the bonding curve, and it is the engine behind nearly every Solana memecoin launch. Here is how a bonding curve works, why launchpads use it, and why understanding it is the difference between trading and reacting late.

Summary

- A bonding curve is a mathematical formula that sets a token’s price automatically based on how much of its supply has been bought, so the price rises as people buy and falls as they sell.

- It lets a token launch with instant liquidity and no pre-funded pool, because buyers trade against the curve’s contract rather than against other traders.

- On the leading Solana launchpad, a token sells along its curve until it “graduates,” at which point its accumulated liquidity moves to a normal exchange and the curve is left behind.

- Curves come in shapes, mainly linear and exponential, that determine how violently the price moves and how brutally late buyers are punished.

- A bonding curve is a pricing mechanism, not a safety mechanism, and the large majority of tokens launched on curves lose most of their value within days.

A bonding curve is a mathematical pricing formula that sets a token’s price automatically based on how much of its supply has already been bought, so that the price rises as people buy and falls as people sell, without needing the traditional matching of buyers and sellers in an order book or a pre-funded pool of liquidity. That definition contains the whole idea, but its consequences are profound, because the bonding curve is what made the modern memecoin explosion possible. In an ordinary market, a token’s price emerges from buyers and sellers placing orders that meet at an agreed price, which requires liquidity to exist before trading can happen. A bonding curve removes that requirement.

It lets a brand-new token trade from the very first moment, with its price determined by a formula rather than by a market, and with liquidity created automatically as people buy. This is why a person with no technical skill and a small amount of money can launch a coin that is instantly tradable, and it is why tens of thousands of new tokens can appear every day. The bonding curve is the mechanism underneath all of it. Because the bonding curve governs how a memecoin behaves in its earliest and most volatile phase, understanding it is the single most useful piece of technical knowledge for anyone trying to make sense of memecoin launches, even from a safe distance.

This guide explains what a bonding curve is and how trading against one works, why launchpads adopted the model, how it operates in practice on the dominant Solana launchpad including the all-important moment of graduation, the different curve shapes and why they matter, a worked example that traces a buy through the curve, the uses of bonding curves beyond memecoins, and the risks the curve does and does not protect against. The point is not to encourage trading these tokens, most of which lose nearly all their value, but to make the mechanism legible, because a person who understands the curve can at least see what is happening when a fresh token rockets and collapses, instead of reacting late to forces they cannot name. The curve is the rule of the game, and knowing the rule is the beginning of not being its victim.

What a bonding curve actually is

Start with how trading against a bonding curve differs from trading in a normal market, because the distinction is the key to everything. In a conventional exchange, when you buy a token, you are buying it from another person who is selling, and the price is whatever buyers and sellers agree on through their orders. With a bonding curve, there is no counterparty on the other side; you are trading against a smart contract that follows a formula. When you buy, you send the network’s currency, on Solana that is SOL, to the bonding curve contract, and the contract issues you tokens at a price determined by the formula, then moves the price up the curve.

When you sell, you send your tokens back to the contract, which removes them from circulation and returns SOL to you at the formula’s current price, then moves the price down the curve. The price is purely a function of how far along the curve the supply has been bought; more buying pushes it up, more selling pulls it down, automatically and without any human market-maker. The reason this is called a bonding curve is that the price follows a curve plotted against the supply sold. As more of the token’s supply is purchased and moves out along the curve, each successive token costs more than the last, so the price climbs as the coin sells.

Crucially, the currency that buyers send in does not go to a seller; it stays locked in the contract, where it serves as the token’s liquidity, the pool of value that backs the ability to sell tokens back later. This is how a bonding curve creates liquidity automatically: every purchase adds to the locked pool, so the token is tradable from its first moment without anyone having to fund a liquidity pool in advance. That self-contained quality, a contract that prices the token, holds the liquidity, and handles both buying and selling by formula, is what makes the bonding curve such a powerful launch mechanism. It collapses everything a normal token launch requires, smart-contract deployment, liquidity provision, market-making, into a single automated curve that anyone can use.

Why launchpads use bonding curves

The appeal of the bonding curve to a launchpad, and to the people launching coins, comes down to removing barriers, and seeing why clarifies the model’s role. Traditionally, issuing a token that people could actually trade was involved: a developer had to write and deploy a smart contract, then pre-fund a liquidity pool with a meaningful amount of capital so the token had something to trade against, since without liquidity a token cannot be bought or sold at a stable price. This required both technical skill and money up front, which kept token creation in the hands of relatively few. The bonding curve demolishes both barriers.

Because the curve provides liquidity automatically as people buy, no one has to pre-fund a pool, and because the launchpad handles the contract, no one has to write code. A creator needs only a name, an image, a ticker, and a tiny amount of the network’s currency to cover a creation fee. This is why bonding-curve launchpads turned token creation into a one-click activity and unleashed the flood of memecoins now defining parts of Solana. The model also delivers what the platforms call a fair launch, in the sense that every buyer enters through the same curve from the same starting point, with no presale or insider allocation funded in advance, so the earliest public buyer and the latest both interact with the same automated pricing.

One launchpad even folds in a measure against the oldest memecoin scam by having creators buy their own tokens through the same curve as everyone else at launch, rather than secretly hoarding a huge allocation to dump later, which levels the starting field somewhat even though it does not remove all risk. The bonding curve, then, is the technology that made memecoin creation cheap, instant, and open to anyone, which is simultaneously the source of its creative energy and the reason the space is flooded with low-quality and predatory tokens. The same mechanism that empowers a hobbyist empowers a scammer, because the curve does not care who is using it. The fees around that system also matter, which is why the fees layered on each curve trade became a central debate for memecoin launchpads.

How it works on the leading launchpad

To see the bonding curve in action, it helps to follow how it operates on the dominant Solana launchpad, where the mechanics are well defined. When a coin is created there, it is issued with a large fixed supply, commonly 1 billion tokens, and a major portion of that supply, around 800 million tokens, is placed on the bonding curve to be sold. As buyers send the network’s currency to the curve, they receive tokens and the price rises along the curve, climbing as more of those 800 million are purchased. In the early phase, the coin exists only on the curve, not on any normal exchange, so all of its trading happens against the formula.

Some launchpads add gamified milestones to this phase; one highlights a coin prominently on its homepage once the coin reaches a certain threshold of buying, which functions as free visibility that can attract more buyers and accelerate the climb. The pivotal event in a curve’s life is graduation, and understanding it is essential. A coin graduates when enough of its curve supply has been bought to reach a set threshold, often described as around a particular market-cap level. At graduation, the liquidity that has accumulated in the curve, the pool of currency buyers sent in, migrates out of the curve and into a normal liquidity pool on a decentralized exchange, where the token then trades like a conventional market with buyers and sellers instead of against the curve.

On the leading launchpad, the accumulated liquidity moves to its associated exchange and the liquidity-pool tokens are burned, which is meant to assure traders that no one controls and can withdraw that liquidity. Reaching graduation typically requires the curve to fill with a meaningful amount of the network’s currency, and migrating costs a small additional amount in fees, so a coin whose creator cannot or will not push it over the line can stall on the curve indefinitely, a state traders sometimes call limbo. Graduation is a meaningful milestone because it signals a coin attracted enough buying to reach a normal market, but as the risk section stresses, it is emphatically not a guarantee of safety. Once graduation happens, the next question is where liquidity goes after graduation, because the token leaves the formula-driven phase and enters a pool-based market.

Curve shapes and why they matter

Not all bonding curves are the same shape, and the shape determines how the price behaves, which has direct consequences for anyone trading on it. The two broad types are linear and exponential curves, and the difference is intuitive once you picture it. A linear curve raises the price by a steady increment for each unit of supply sold, so the price climbs in a straight, predictable line. To use a simple illustration that explainer sources cite, with a linear formula where the price starts at $1 and rises by a fixed step, the first token might cost $1 and the hundredth token $11, a smooth and modelable progression.

Because the increase is steady, a linear curve is easier to reason about: a trader can estimate how much the price will move as they buy, and can scale into a position with some idea of their average entry and the slippage they will incur. An exponential curve behaves very differently and more dangerously for latecomers. On an exponential curve, the price does not just rise; it accelerates, so each additional unit of supply pushes the price up by a larger amount than the last. This creates powerful incentives to buy early, because the earliest buyers get in before the acceleration, and it punishes late buyers brutally, because by the time social attention arrives and a crowd rushes in, the price may already have moved far up the steepening curve.

Latecomers pay dramatically more and have far less room for the price to rise further before they are underwater. The practical lesson is that the curve’s shape is itself information a trader should read: a linear curve allows methodical, sized entries, while an exponential curve rewards speed and savagely penalizes the momentum traders who arrive after the supply has already climbed. Notably, on the leading launchpad, linear-style curves have been associated with higher survival rates than fixed-price launches, because the automated, progressive pricing resists the instant dumps that plague other launch formats. The shape of the curve, in short, is not a technicality; it is a map of where the danger lies, including why curve entries move against you when the formula changes the price as demand arrives.

A worked example: tracing a buy through the curve

To make the mechanics concrete, follow a single buyer through a bonding curve, using simplified numbers for clarity. Imagine a fresh coin on a launchpad with a linear curve, early in its life, where only a small fraction of the 800 million curve tokens have been bought, so the price per token is still very low. A buyer, call her the early entrant, sends a modest amount of SOL to the curve contract. The contract issues her a large number of tokens at the current low price and nudges the price up the curve as her purchase moves the supply further along.

Because she bought early on a curve that has barely moved, her tokens are cheap and her average entry price is low. The currency she sent stays locked in the contract as liquidity. Now imagine the coin starts trending. A wave of new buyers sends SOL to the same curve, each purchase moving the supply further along and ratcheting the price higher.

A later buyer, the latecomer, arrives after the coin has been featured and hyped, when much of the curve supply has already been bought. He sends the same amount of SOL the early entrant did, but because the price has climbed far up the curve, he receives far fewer tokens at a much higher average price. If the curve is exponential, the gap is even more extreme, because the price accelerated as the crowd bought in. Should the hype fade and buyers start selling back to the curve, the price slides back down it, and the latecomer, who paid the high price, is underwater long before the early entrant is.

This is the core dynamic of bonding-curve trading laid bare: the curve mechanically rewards those who buy when the supply is low and punishes those who buy after attention has already pushed the price up. The early entrant’s advantage is not skill but position on the curve, and the latecomer’s disadvantage is structural. The example shows why, in this arena, timing relative to the curve matters more than the quality of the coin, and why so many people who chase a trending token arrive precisely when the curve has already made the trade dangerous. For a cultural view of that behavior, trading the curve in practice is what traders call life in the trenches.

Bonding curves beyond memecoins

Although memecoins are where most people encounter bonding curves, the mechanism is a general tool with legitimate uses, and recognizing that gives a fuller picture. The core idea, pricing a token by formula against its supply and providing liquidity automatically, is useful anywhere a project wants continuous, demand-driven issuance instead of a single fixed launch event. Some projects use bonding curves so that demand determines access and pricing over time, letting a token be issued gradually as people buy in, instead of forcing everything through one launch moment. This continuous-issuance model has appeared in corners of crypto beyond memecoins, including in social applications where the curve priced access to a creator or community, with one well-known social-token experiment matching the curve mechanism to its product in a way many later copycats did not.

The honest framing is that the bonding curve is a neutral piece of financial engineering whose character depends entirely on what it is attached to. On its constructive side, it solves a real problem: it lets a project bootstrap liquidity and discover price without a pre-funded pool or a centralized market-maker, which is genuinely useful for certain launch and issuance designs. On its speculative side, the same mechanism can price anything, including tokens with no purpose, and it works mechanically even when it works economically against the people buying. As one analysis put it, a bonding curve can price anything, but it cannot create lasting demand for something nobody wants to hold once the launch excitement fades.

That is the crux. The curve is excellent at manufacturing a price and a tradable market out of nothing, which is exactly why it powers both legitimate continuous-issuance designs and the endless churn of disposable memecoins. The technology is the same; the outcomes diverge based on whether there is any real reason to hold the token after the novelty wears off. Most of the time, in the memecoin context, there is not, even when a curve launch that went parabolic briefly makes the mechanism look like a wealth machine.

Risks: the curve is a mechanism, not a safety net

The most important thing to understand about a bonding curve is what it does not do, because misreading its protections is how people get hurt. A bonding curve sets a price and provides liquidity; it does not make a token safe, valuable, or likely to succeed. The hard data on this is sobering. Analyses of Solana memecoin launches have found that the large majority of tokens launched on bonding curves, on the order of 80% or more, lose more than 90% of their value within about a week, often tied to creators or insiders dumping once the curve phase ends and conditions change.

So the default expectation for a fresh curve launch should be a temporary opportunity at best and a near-certain loss at worst, not a durable asset. The curve’s automated pricing does nothing to change the fact that most of these tokens have no purpose and no reason for anyone to hold them once the initial excitement fades. Several specific risks deserve naming. Creator and insider dumping is common: once a curve completes or conditions shift, those holding large early positions may sell into the buyers who arrived later, collapsing the price.

Whale-driven distortion is another: a large buyer can push the price quickly up the curve to create the appearance of demand, then unwind into the crowd that follows. Graduation, despite feeling like a milestone, is not safety; a graduated coin trading on a normal exchange can still collapse if hype fades, whales sell, or new buyers stop arriving, and post-graduation liquidity can be thin. The curve’s shape compounds these dangers, with exponential curves punishing latecomers especially hard. And the broader environment is one in which, by some estimates, the overwhelming majority of launchpad tokens are scams, pump-and-dumps, or jokes with no lasting viability.

The clear-eyed conclusion is that a bonding curve is a clever pricing and liquidity mechanism, not a protective one, and that understanding the curve should make a person more cautious, not more confident. Knowing how the curve works lets you see the trap; it does not disarm it. The only reliable protection is to treat curve-launched tokens as high-risk speculation, to check holder concentration, liquidity, and curve shape before doing anything, and to never commit money you cannot afford to lose entirely.

Frequently asked questions

What is a bonding curve in simple terms?

A bonding curve is a formula that sets a token’s price based on how much of its supply has been bought, so the price rises as people buy and falls as they sell. Instead of trading against other people in a market, you trade against a smart contract that follows the formula: you send currency and receive tokens at the curve’s current price, which then moves up. The currency you send stays locked in the contract as the token’s liquidity. This lets a brand-new token be tradable instantly, with no pre-funded liquidity pool and no order book, which is why bonding curves power the one-click memecoin launches common on Solana

How does a token graduate from a bonding curve?

A token graduates when enough of its curve supply has been bought to reach a set threshold, often described around a particular market-cap level. At that point, the liquidity accumulated in the curve, the currency buyers sent in, migrates out of the curve into a normal liquidity pool on a decentralized exchange, where the token then trades like a conventional market between buyers and sellers instead of against the curve. On the leading Solana launchpad, the liquidity-pool tokens are burned at graduation so no one can withdraw that liquidity. Reaching graduation requires the curve to fill with a meaningful amount of currency, and a coin that never gets there can stall on the curve indefinitely.

What is the difference between linear and exponential curves?

The difference is how fast the price rises. A linear curve raises the price by a steady, fixed increment for each unit of supply sold, so the price climbs in a predictable straight line, which makes it easier to estimate slippage and scale into a position. An exponential curve accelerates, raising the price by a larger amount with each unit sold, so the price rises faster and faster. Exponential curves strongly reward early buyers and brutally punish late ones, because by the time a crowd arrives, the price may have already climbed steeply, leaving latecomers paying far more with much less upside.

Does a bonding curve make a token safe?

No. A bonding curve is a pricing and liquidity mechanism, not a safety mechanism. It sets a price and provides liquidity, but it does nothing to make a token valuable or likely to succeed. Analyses of Solana launches found that the large majority of bonding-curve tokens, around 80% or more, lose over 90% of their value within about a week, often when creators or insiders dump after the curve phase. Graduation is not safety either, since a graduated coin can still collapse.

Why do launchpads use bonding curves?

Because they remove the two big barriers to launching a tradable token: technical skill and upfront capital. Normally a creator would have to deploy a smart contract and pre-fund a liquidity pool so the token had something to trade against. A bonding curve eliminates both, because it provides liquidity automatically as people buy and the launchpad handles the contract, so a creator needs only a name, image, ticker, and a tiny fee. This turned token creation into a one-click activity and unleashed the flood of memecoins on Solana.

Can bonding curves be used for things other than memecoins?

Yes. The bonding curve is a general tool for any project that wants continuous, demand-driven token issuance instead of a single fixed launch, because it lets demand determine pricing and access over time while providing liquidity automatically. It has been used beyond memecoins, including in social applications where a curve priced access to a creator or community. The mechanism itself is neutral financial engineering; its character depends on what it is attached to. It can support legitimate continuous-issuance designs, and it can equally price tokens with no purpose.

This article is educational information, not financial advice. Descriptions of bonding-curve mechanics, launchpad behavior, and failure statistics reflect reporting available as of June 29, 2026, and can change. Tokens launched on bonding curves are extremely high-risk and the large majority lose most or all of their value. Nothing here encourages trading such tokens. Verify any specific platform’s mechanics independently and consult a qualified professional before making any decision.

ARK Invest’s biggest crypto stock purchases over the past three trading days were Coinbase and Circle, whose shares have fallen 17% and 27.6%, respectively, over the past month.

Tech-focused asset manager ARK Invest has capitalized on the recent crypto market downturn, buying a combined $43.5 million worth of shares in crypto firms such as Coinbase and Circle over the past three trading days.

Data from ARK Invest shows the asset manager bought another 122,544 shares in Coinbase (COIN) worth about $18.6 million since Thursday, while adding another 169,777 shares in Circle (CRCL) worth roughly $12.9 million over the same time frame.

The firm also purchased nearly $5.2 million worth of shares in crypto exchange Bullish (BLSH) and added another $5.12 million in brokerage firm Robinhood (HOOD), which has pushed aggressively into the crypto tokenization space in recent months. It also bought $1.69 million worth of shares in crypto-friendly bank SoFi Technologies (SOFI) on Monday.

ARK’s purchases come as investors have turned bearish on these crypto-related stocks. CRCL, COIN and BLSH have fallen 27.6%, 16.9% and 26.3%, respectively, over the past month. During that time, Bitcoin (BTC) slipped to a near two-year low of $58,190, while confidence that the CLARITY Act will pass before the US midterm elections in November has faded.

Changes made to ARK’s ARK Innovation ETF (ARKK) on Monday. Source: ARK Invest

Most of the newly purchased shares were added to the ARK Innovation ETF (ARKK), the firm’s flagship fund, followed by the ARK Next Generation Internet ETF (ARKW).

Related: Kiwoom eyes Bithumb stake as Korean brokerages push into crypto: Report

The ARK Blockchain & Fintech Innovation ETF (ARKF) was also topped up with crypto-related stocks.

ARK also added to its positions in Elon Musk’s SpaceX (SPCX) and software intelligence platform Palantir (PLTR) over the past three trading days.

Over the same period, ARK reduced positions in Alibaba (BABA), Roku (ROKU), Strata Critical Medical (SRTA) and several other companies.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Bitcoin is down over 1% on Tuesday as the Japanese yen slipped to four-decade lows against the U.S. dollar, triggering volatility in currency markets.

The leading cryptocurrency by market value traded below $60,000, holding below the pivotal 200-week simple moving average.

On Monday, Strategy, the world’s largest publicly listed BTC holder, authorized plans to buy back as much as $1 billion each of its preferred and Class A common shares, and is launching a $1.25 billion “monetization program” to raise capital with bitcoin sales. Essentially, it may sell BTC worth over a billion dollars in an already weak market — a sharp pivot from founder Michael Saylor’s longtime mantra of “never sell your bitcoin.”

This pivot, however, may offer little long-term solace, according to some observers. Strategy’s preferred stock STRC, a yield-generating play, has cratered in recent weeks, weakening the company’s major funding channel for BTC purchases.

“The can has been kicked down the road for a year or two,” Jeff Dorman, CIO of Arca, said on X.

Prediction-market platforms are increasingly trying to control more of their own trading stack—an “operational consolidation” trend that analysts at Bernstein say could accelerate mergers and acquisitions across crypto exchanges, brokerages, sportsbooks, and consumer trading apps.

In a research report released on Monday, Bernstein argued that major players are consolidating both distribution and execution functions, tightening links between what used to be separate parts of the market. The shift matters for investors and operators because it can change fee structures, reduce dependence on external infrastructure providers, and potentially reshape how regulators view these products.

Key takeaways

- Bernstein characterizes the sector’s shift as “operational consolidation,” with platforms merging distribution, brokerage, exchange, and clearing functions.

- Several mainstream consumer and prediction platforms have moved toward tighter in-house routing and infrastructure control, according to Bernstein’s examples.

- Owning more of the stack can preserve fees that previously went to outside partners, making acquisitions an efficient way to fill gaps or gain licenses.

- Greater vertical integration may also increase legal and regulatory pressure as the line between financial trading and gambling becomes harder to define.

- State-by-state approaches—alongside ongoing legal challenges—could limit how quickly consolidation proceeds.

Platforms move from partnerships to vertical control

Historically, prediction markets often relied on third-party infrastructure for routing, exchange operations, or clearing—arrangements that made it easier to launch products without building everything internally. Bernstein says that model is weakening as leading consumer platforms consolidate functions across the prediction-market workflow.

In its report, Bernstein pointed to examples spanning different parts of the ecosystem. Robinhood has routed major World Cup contracts through Rothera, the exchange it jointly owns with Susquehanna, according to Bernstein’s account. DraftKings is also cited by Bernstein for launching DKeX and shifting volume away from venues that previously handled some execution, including CME and Crypto.com infrastructure.

The report also highlights consolidation efforts at the crypto-operations layer. Bernstein cited Coinbase’s acquisition of The Clearing Company—framed in related coverage as a move tied to expanding prediction-market capabilities—and Coinbase’s launch of event contracts, adding to the pattern of larger consumer crypto firms seeking greater control over the prediction-market stack.

Why “owning the stack” can change deal economics

Bernstein’s central argument is straightforward: integration can be a direct business advantage. By controlling more of distribution, brokerage, execution, and clearing, platforms can keep revenue streams that would otherwise be shared with specialized partners.

That matters because acquisitions can become a faster path to operational control than building from scratch. Bernstein suggested that deal-making may accelerate as companies pursue missing components—whether that means distribution reach, exchange capabilities, or clearing infrastructure—using purchases to close gaps and strengthen end-to-end product delivery.

However, vertical integration doesn’t only affect profitability. It also reshapes the competitive landscape: businesses that historically operated in different industries—consumer finance apps, sportsbooks, exchanges, and crypto trading infrastructure providers—can end up competing under a single set of product and customer expectations.

Regulatory conflict is the largest constraint

Bernstein singled out regulation as the principal friction point for larger integrations. As prediction markets blend with brokerages, sportsbooks, and exchanges, regulators may scrutinize whether specific products should be treated as financial derivatives or as gambling.

The report suggests that these classifications are not merely academic. They drive enforcement priorities, licensing requirements, and how courts determine jurisdiction. Bernstein warned that such questions could feed antitrust disputes as firms attempt to merge capabilities across multiple market segments.

The regulatory tension has already played out in the U.S. Minnesota enacted what the CFTC described as the first outright ban on prediction markets, while Illinois adopted legislation requiring platforms to obtain a state license before offering sports event contracts—developments Bernstein cited through earlier coverage.

Kalshi challenged restrictions in both states, arguing that federally regulated exchanges fall under the CFTC’s exclusive authority. Bernstein’s framing implies that these legal fights create a practical uncertainty: consolidation may make commercial sense, but execution could remain constrained until regulators and courts clarify where federal derivatives oversight ends and state gambling authority begins.

What to watch as consolidation accelerates

With platforms continuing to move routing, exchange functions, and clearing in-house, the next phase of the sector may hinge less on product launches and more on legal outcomes—particularly whether courts establish a clearer boundary between federal trading regulation and state gambling rules. Until that boundary hardens, consolidation could keep happening, but with deal structures and operating decisions likely shaped by ongoing jurisdictional risk.

Onchain demand stayed soft through the slide, according to Glassnode data. The number of active addresses, a rough gauge of how many users are actually transacting, sat around 618,000, in the middle of its recent range rather than breaking higher.

The value of coins moving across the network held near $4.2 billion, just above the bottom of its range around $3.6 billion, pointing to subdued rather than surging activity, the firm said in a Monday report.

Total transaction fees, or what users pay to move funds and a read on competition for space in each block, kept contracting. Together, the three say demand has not picked up even with prices lower.

Adding to the caution, Strategy, the largest corporate holder of bitcoin, said Monday it may sell more than a billion dollars of the token under a new program to shore up its finances, a reversal of founder Michael Saylor’s long-standing refusal to sell.

The prospect of those sales hangs over an already thin market. That leaves crypto where it has traded for weeks, pinned by a strong dollar and a lack of fresh demand rather than any single shock.

The next tests are whether the dollar’s climb stalls and whether the yen’s slide forces Japan to step in, a move some warn could unwind the cheap-yen borrowing long used to fund risk trades worldwide.

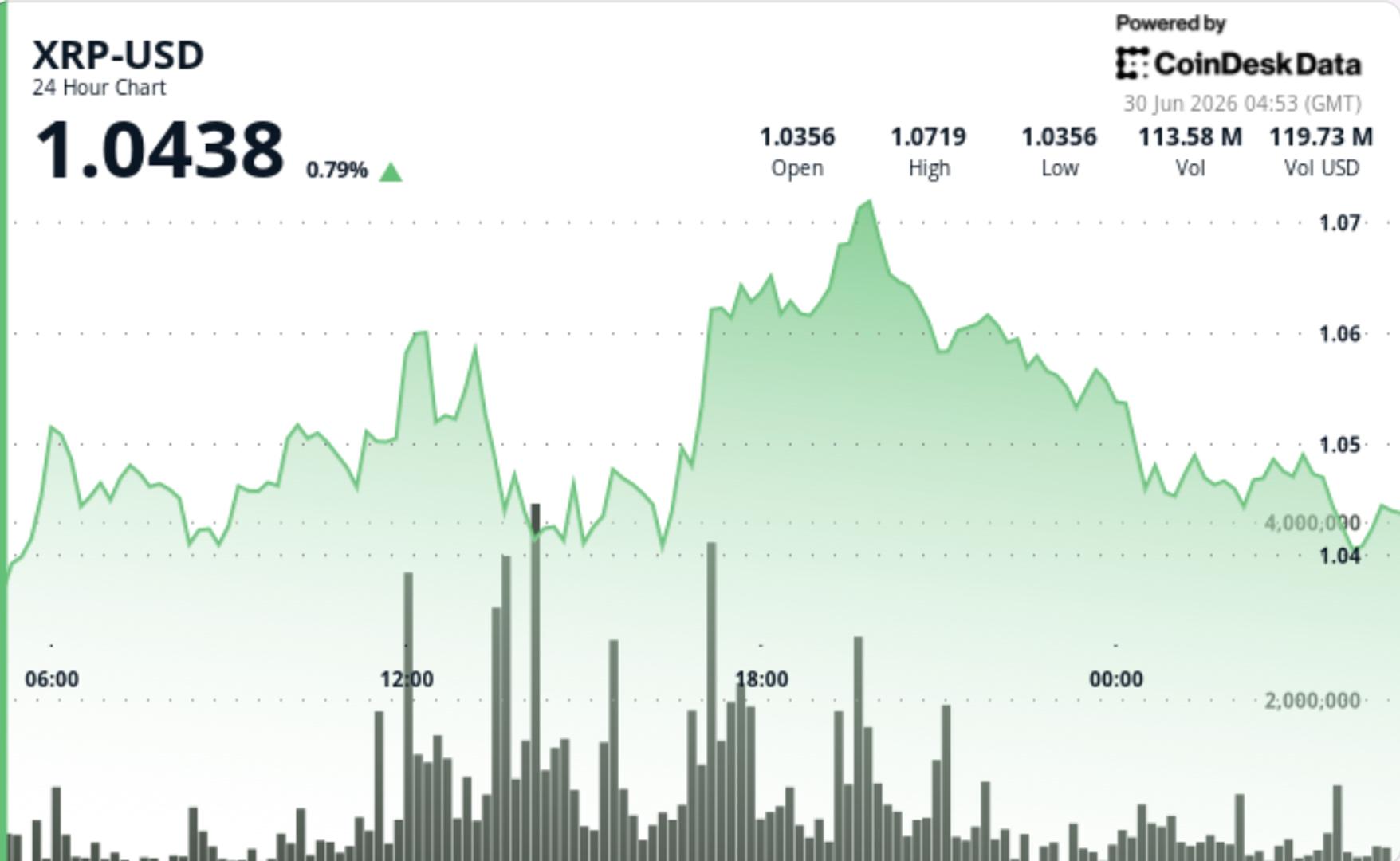

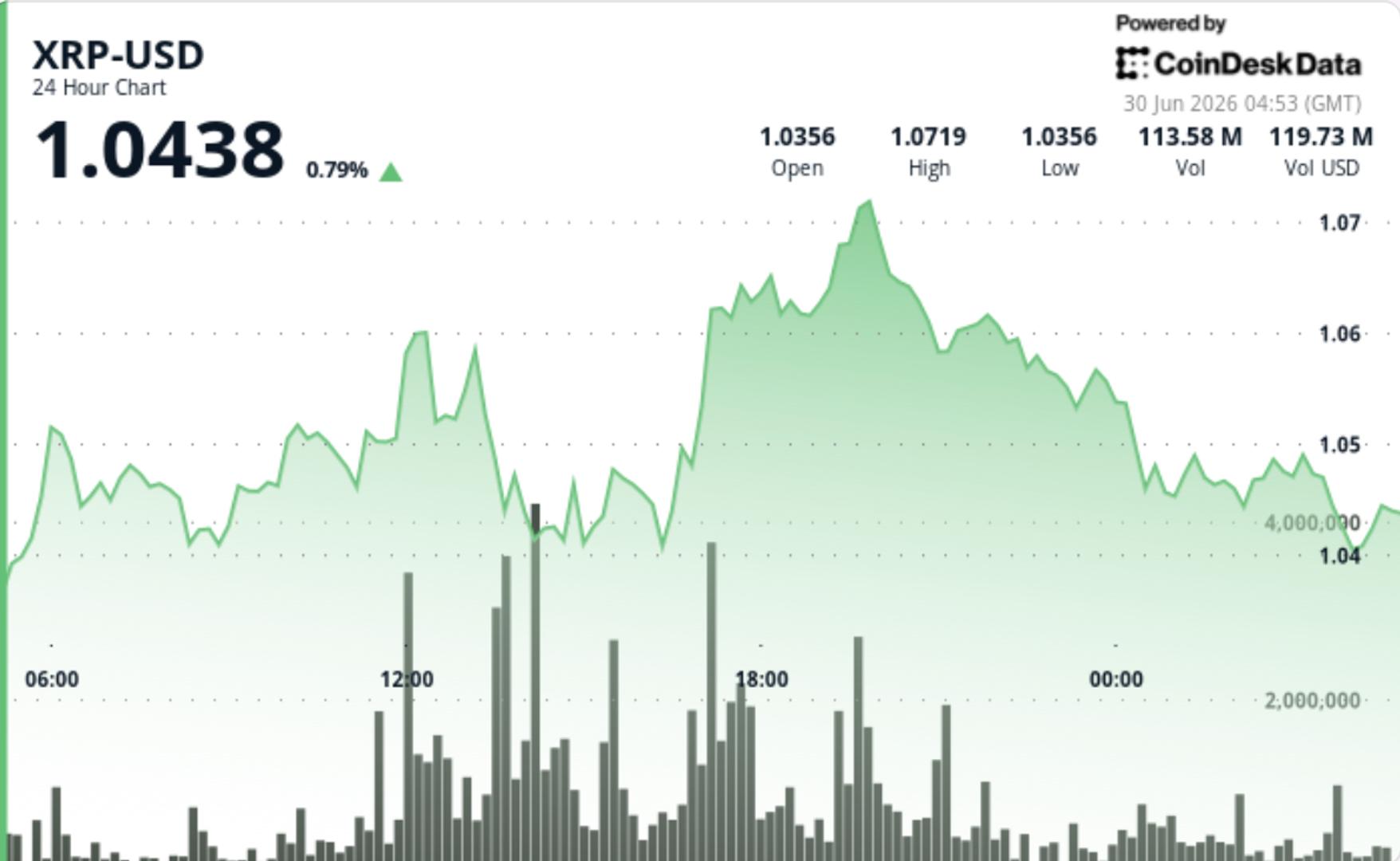

• The token traded in a $0.0435 range and continued to hold above the $1.00 psychological support level.

• The main burst of activity came on June 29 at 17:00, when volume reached 86.5 million XRP, about 67% above the 24-hour average.

• Price later consolidated between $1.03 and $1.06, leaving the market range-bound rather than in a confirmed recovery.

Technical Analysis

• The key development is that XRP continues to defend $1.00 even after a 19% monthly decline.

• The leverage reset improves the setup. Open interest has fallen sharply, funding has turned negative and forced long liquidations have cleared out crowded positioning.

• The on-chain picture is stronger than the chart. Active addresses are rising, ETF inflows are continuing and exchange reserves remain stable, but price is still below major moving averages.

• XRP remains capped by resistance near $1.10, with larger barriers near the 50-day EMA around $1.20 and the 100-day EMA around $1.31.

• The 4-hour RSI has recovered from oversold territory to 46, but momentum remains below the neutral 50 level.

What traders should watch

• $1.00 remains the key support level. A break below it would put $0.90-$0.87 back in focus.

• $1.06 is the first short-term resistance level, followed by $1.09-$1.10, where recent rallies have stalled.

Bitcoin (BTC) steadied itself over the weekend after a volatile week that saw its value drop to its lowest level since September 2024.

The flagship cryptocurrency fell to a low of $58,000 on Thursday, struggling against sustained ETF outflows, a hawkish Federal Reserve, concerns around Strategy, and a stronger US Dollar.

Bitcoin Stabilizes After Sharp Selloff

BTC experienced a substantial downturn last week, falling from a high of $65,553 on Monday to a low of $58,000 on Thursday. ETF outflows, a stronger US Dollar, a hawkish Federal Reserve, and the ongoing geopolitical situation continue to pressure Bitcoin and the broader market. However, price action steadied over the weekend and has reclaimed the $60,000 level after falling to a low of $58,800 earlier today.

Bulls have defended $58,000, a key support level, despite substantial selling pressure. BTC maintained its position above $58,000 over the weekend despite fresh US-Iran tensions over a volatile ceasefire. Markets had registered a substantial recovery earlier this month after tensions in the Middle East thawed, easing oil prices and inflation concerns. However, the rally soon fizzled out, pushing the price to sub-$60,000 levels.

BTC’s price action could go one of two ways. If the flagship cryptocurrency fails to regain momentum and slips below $58,000, a drop toward $55,000 or lower can be expected. However, a clean recovery above $60,000 would suggest buying pressure returning.

Strategy Under Pressure

Concerns around Strategy’s capital structure have also impacted market sentiment. STRC, the company’s preferred stock product, is currently trading around $74.57, significantly lower than its intended $100 mark. Annual dividend obligations have risen to $1.2 billion, while dividend coverage dropped to 14 months thanks to declining cash reserves. Strategy used its stock premium to raise capital for more BTC acquisitions. However, weak pricing has made it substantially harder for the Michael Saylor-led firm to depend on this model to raise additional capital.

Meanwhile, CryptoQuant has urged Strategy to pause its acquisitions and rebuild its cash reserves. However, the plea looks to have fallen on deaf ears, with Michael Saylor teasing another buy, posting the company’s Bitcoin tracker with the caption “We’re going to need more charts.”

Analysts Divided

Meanwhile, analysts remain divided on Bitcoin’s price action. Analyst Market Watcher highlighted a downtrend from July and August highs of around $70,000 and $67,000, adding that a break of the line would make investors more willing to deploy capital. The analyst described the current price range as an “indecisive summer chop.” However, he added that a break of the main trend around $58,000 could change the entire setup.

Another analyst, EGRAG CRYPTO, highlighted Bitcoin’s 12-month cycle, adding that the current cycle may be different from the usual “three years up one year down” cycle. Meanwhile, CryptoQuant analyst Crazzyblockk stated that Bitcoin is currently in an undervalued zone after its short-term holder realized dominance fell to 27.6%. Previous cycles have witnessed market tops when short-term holders controlled the realized capital. Bear markets witness the opposite, as short-term holders realize their losses and realized capital drops.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

The US Securities and Exchange Commission has won its fraud suit against crypto platform NanoBit Limited, nearly two years after the agency accused it of stealing hundreds of thousands of dollars from at least 18 investors between 2023 and 2024.

The announcement by the SEC on Monday came nearly two weeks after the US District Court for the Eastern District of New York entered a final judgment against four entities and two individuals tied to the NanoBit fraud case on June 16.

The SEC alleged that NanoBit’s operators impersonated financial professionals in WhatsApp groups to trick investors into depositing funds on the fake platform. Instead, the funds were allegedly diverted to scheme participants, the SEC said.

The case is another example of the SEC’s continued crackdown on crypto-themed fraud under the Trump administration, even as the agency has softened its regulatory approach to crypto companies and revised what it considers to be a securities offering.

On May 29, the SEC charged a Texas man with allegedly running a fraud scheme that raised more than $12 million from roughly 150 investors by falsely claiming to use AI-powered trading bots to generate guaranteed returns.

In April, the SEC also charged crypto executive Donald Basile and two companies he controlled for raising roughly $16 million from hundreds of investors through false claims tied to a crypto token called Bitcoin Latinum.

NanoBit perpetrators ordered to pay $5.4 million

The New York court found that the defendants violated US securities laws and issued permanent injunctions against them, prohibiting them from engaging in the issuance, purchase or sale of securities.

Related: Crypto scammers exploit World Cup ticket demand, TRM warns

NanoBit was ordered to pay a $1.18 million fine, disgorgement of more than $532,000 for the ill-gotten gains and prejudgment interest of nearly $81,200, totaling nearly $1.8 million.

NanoBit’s affiliates — Radiant Horizons, Sweet Karma and Zhao Deli — were each ordered to pay a $1.18 million fine, while one of the scheme’s main orchestrators, Jiajie Liu, was ordered to pay about $120,000 in penalties, disgorgement and prejudgment interest.

In the September 2024 complaint, the SEC alleged that NanoBit investors were solicited on social media, such as Instagram, before being added to the WhatsApp groups.

Investors were allegedly shown a fake dashboard depicting rising returns, creating the illusion that their funds were growing.

It allegedly persuaded investors by falsely claiming that its affiliate, NanobitUS Securities, was an SEC-registered broker, while also promoting fake initial coin offerings (ICOs) promising substantial returns.

However, “no transactions took place on the NanoBit platform and investors’ funds in fact went to scheme participants who wired more than $2 million to bank accounts in Hong Kong and misappropriated hundreds of thousands of dollars’ worth of investors’ crypto assets,” the securities regulator alleged.

The SEC alleged that investors who sought to withdraw funds were met with excuses and asked to pay large fees, while others were removed from the WhatsApp groups for questioning the platform’s legitimacy.

Magazine: The end of anonymity? AI could unmask crypto’s hidden identities

Ethereum co-founder Vitalik Buterin has laid out a longer-term cryptography blueprint for private, onchain voting that aims to avoid the need for a trusted group to handle ballots. In a technical essay published Monday, Buterin argues that a cryptographic technique known as indistinguishability obfuscation (iO) could let blockchain systems compute voting results while keeping individual votes hidden and limiting opportunities for collusion.

The proposal centers on replacing traditional threshold-style committees—groups that collectively decrypt encrypted votes—with protected programs designed to reveal only the final outcome. Buterin cautions, however, that the approach is not yet practical, with the most conservative versions requiring extremely heavy computation and faster variants depending on less-tested security assumptions.

Key takeaways

- Buterin’s proposal uses indistinguishability obfuscation (iO) to create “protected programs” that can compute vote tallies without exposing ballot contents.

- The design is intended to reduce reliance on threshold committees that jointly decrypt results, potentially lowering the trust needed for private onchain voting.

- Even with iO, blockchains remain essential because protected programs can’t stop being copied or support state updates on their own.

- Buterin describes current constructions as computationally impractical, positioning the idea as research direction rather than a near-term deployment plan.

From encrypted ballots to protected programs

Buterin frames iO as a method for hiding software logic. In his explanation, iO transforms a piece of code into a protected program such that others can run it to obtain the intended output, but cannot inspect the internal code or retrieve embedded sensitive data. He emphasizes that this approach focuses on concealing the program itself, rather than solely masking the data it processes.

In the context of voting, the idea would be to package the tallying and eligibility logic into an obfuscated program. Voters could submit encrypted ballots, and the system would execute the protected program to produce a final tally without exposing how individual participants voted. In effect, this would remove a key requirement of many private voting schemes: coordinating a set of operators (a threshold committee) that holds decryption capabilities and must behave honestly.

Buterin also notes that blockchains still have to do the heavy lifting for public coordination and evolving state. While iO can hide computation details, it cannot prevent copying or manage changing information by itself, so a blockchain—or similar distributed infrastructure—would remain necessary for the system to function over time.

Why dropping threshold committees matters

Private onchain voting typically involves operational trust assumptions, even when votes remain cryptographically protected. In many designs, groups of operators must safeguard information and follow the protocol correctly—particularly during decryption or tallying. Buterin argues that eliminating (or sharply reducing) the need for threshold committees could make decentralized governance more resistant to manipulation.

In his view, reducing this dependency could also lower the risk of insider interference and enable voters to participate without exposing voting behavior. However, the core promise is not only privacy for individuals; it is also a shift in who has meaningful control over the outcome. Instead of multiple parties jointly controlling decryption, the tally would be derived from running a protected program intended to reveal only what the system needs to disclose.

That said, the essay’s emphasis on security assumptions and computational feasibility underlines that the practical challenge is formidable. The approach is designed to minimize trust—but it still must be engineered so that security holds under realistic operating constraints.

Security trade-offs and why deployment is still out of reach

Buterin’s assessment is explicit: the idea, while conceptually aligned with “almost no trust assumptions,” is not ready for real-world use. He describes the most conservative constructions as requiring what he calls “galactic” amounts of computation—suggesting that the computational overhead would overwhelm any system intended for everyday participation.

He also points to a tension faced by cryptographic research more broadly: faster constructions tend to rely on weaker or less-tested security assumptions. In other words, an implementation that is technically feasible may not yet offer the same level of assurance as the most conservative theoretical design. This leads Buterin to characterize iO-based private voting less as a deployment-ready system and more as a long-term research direction.

For investors and builders watching Ethereum’s roadmap, the takeaway is that privacy research is moving toward more rigorous “how it’s computed” privacy—yet the path from cryptographic theory to production-grade systems will require major advances in efficiency and confidence in assumptions.

How this fits into Buterin’s broader privacy agenda

This iO voting essay builds on earlier work by Buterin linking advanced cryptography to stronger privacy and reduced coercion risk. In October 2024, he connected iO with private voting in an Ethereum roadmap he published, arguing that the technique could improve privacy guarantees.

He has also pushed for practical privacy steps within Ethereum’s ecosystem. In April 2025, Buterin proposed a more immediate privacy roadmap that called for integrating privacy tools into existing wallets. That proposal also advocated for stronger protections against data collection by infrastructure providers used by wallets to access Ethereum, reflecting an emphasis on privacy not just at the cryptographic layer but in the surrounding network services.

Buterin has additionally directed personal funds toward privacy-preserving projects. According to earlier coverage by Cointelegraph, on Jan. 30 he earmarked 16,384 Ether (ETH) (about $45 million at the time) to support initiatives focused on privacy, open infrastructure, and self-sovereign tools.

Read together, these threads show a consistent direction: privacy improvements are being pursued both through long-horizon cryptographic designs like iO and through nearer-term engineering changes that could reduce exposure to tracking and data collection.

For now, the most important question is what—if anything—can be improved to make iO-based voting computationally viable without sacrificing security confidence. Readers should watch for follow-up research that narrows the performance gap and clarifies which security assumptions would be acceptable for real deployments.

Bitmine Immersion Technologies said it added more than 27,000 Ether to its treasury last week after completing a $43 million purchase. The update comes as the company prepares for greater visibility with its inclusion in the Russell 1000, an index that many funds use as a benchmark for passive investing.

In a disclosure shared on Monday via PR Newswire, Bitmine said its Ether holdings reached just over 5.7 million ETH. The company reported buying the tokens at an average price of $1,569 per Ether and said it now holds about 4.7% of Ethereum’s 120.7 million token supply—moving it closer to its stated objective of owning 5% of the asset.

Key takeaways

- Bitmine reported a $43 million Ether purchase that increased holdings to just over 5.7 million ETH at an average $1,569 per token.

- The firm said its stake is now roughly 4.7% of Ethereum’s circulating supply, edging toward a 5% target.

- Bitmine’s Russell 1000 inclusion is expected to bring additional institutional demand through funds that track the index.

- Despite broader Ethereum developments, Bitmine’s chairman described the prior week as difficult for crypto investors after Ether fell about 8%.

- Other crypto-linked firms were also added to the Russell 3000 Index recently, expanding how traditional investors encounter crypto treasury businesses.

A growing Ether treasury amid a volatile week

Bitmine’s announcement frames the latest acquisition as part of a continued push to build a larger corporate Ether position. After its recent buy, the company said it holds slightly above 5.7 million Ether and has reduced the gap to its 5% supply goal.

The filing also highlights how market price swings can complicate treasury strategies even when the broader Ethereum ecosystem is active. Bitmine chairman Tom Lee characterized the preceding week as challenging for crypto investors, saying Ether fell by 8%. In his remarks, he noted Ethereum-related positives—including the creation of Ethlabs—and pointed to a softer tone from the Bank of England regarding stablecoins.

Even with those developments, Lee said the selloff played out in ways that can influence investor behavior. He later attributed some of the pullback to what he described as “window dressing,” where investors reduce exposure to assets that have declined over recent months.

Why Russell 1000 inclusion could change Bitmine’s investor base

Beyond the treasury update, the more market-facing development is Bitmine’s addition to the Russell 1000, which tracks the largest 1,000 US companies. Bitmine said this step may increase investor demand for its shares because many mutual funds, ETFs, and pension funds follow Russell indices and must buy constituents once they are added.

Lee previously discussed this mechanism when Bitmine was first under consideration for the Russell index in May. He said passive index funds can account for up to 25% of the market capitalization of stocks included in the index.

In Monday’s comments, Lee said Russell 1000 membership is expected to add “hundreds and possibly thousands” of additional institutional investors as equity owners of Bitmine. For a company whose business model is closely tied to holding and managing Ether exposure, a shift in the shareholder base can matter: institutional ownership patterns can influence liquidity, trading volume, and the range of investors willing to hold crypto-treasury equities over the long run.

Stock movement follows Ether, despite new corporate catalysts

Bitmine’s share performance on Monday reflected both the company’s corporate update and the broader pressure on Ether. The stock rose 1.7% to close at $13.80, according to the article, but it has fallen roughly 9% over the past week in tandem with Ether’s decline.

That pattern underscores an important tension for investors watching crypto treasury businesses: even when the company executes meaningful purchases or secures index inclusion, the underlying price of Ether can still dominate near-term equity performance. In other words, Bitmine’s catalysts may improve access to new capital sources, but the valuation of its holdings remains directly linked to market conditions for ETH.

Broader index adoption for crypto-related firms

The Russell inclusion story is not unique to Bitmine. The article noted that rival crypto treasury firms Sharplink and Forward Industries—along with Gemini and Galaxy Digital—were also added to the Russell 3000 Index on Friday. The Russell 3000 tracks the largest 3,000 US companies, which can create additional pathways for traditional market participants to build exposure to crypto-linked public equities.

For investors, this trend signals a gradual normalization of crypto-related businesses inside mainstream index ecosystems. However, it also raises a watchpoint: as more crypto treasury firms enter large-cap indices, their stock demand may become more mechanically tied to index-tracking flows, potentially increasing short-term trading activity around reconstitution dates.

At the same time, it does not remove the central risk for equity holders—Ether’s market volatility. Bitmine’s chairman’s remarks about window dressing and short-term reductions in exposure illustrate how quickly sentiment can shift even when broader Ethereum developments continue.

Investors should watch whether Bitmine’s Russell 1000 entry translates into sustained institutional ownership or whether near-term trading remains dominated by ETH price movements. The next key question is how the company continues to balance incremental Ether acquisitions with the equity volatility created by shifting crypto market sentiment.

In recent days, USDT has traded at a premium across several Indian exchanges, with premiums generally ranging between 7% and 10%, depending on liquidity and market activity. On CoinSwitch, USDT has traded at around a 9% premium over the past few days.

“At CoinSwitch, users always see the live buy and sell price before placing an order. We do not charge any hidden fees beyond our disclosed brokerage. The premium reflects prevailing market conditions rather than any platform-imposed markup,” Singhal said.

Both CoinDCX and CoinSwitch attribute the premium entirely to organic supply-and-demand dynamics: more buyers than sellers, thinner liquidity near the global reference price, and a market mechanism — not platform pricing decisions — setting the rate. Neither executive directly addressed the ED’s enforcement action or its effect on token supply in their statements.

Nevertheless, the supply squeeze that drove the premium unusually higher could be linked to the enforcement action.

Market makers and liquidity provides could have scaled back from sourcing USDT overseas after the ED’s action, which would show up exactly as a supply-side liquidity shortage, the same mechanism both Thakur and Singhal describe in general terms.

Operating on Indian exchanges has been relatively tougher for market makers because of a flat 30% tax on gains, no allowance to offset losses, and a restrictive 1% tax deducted at source (TDS). These rules have long contributed to market dislocations.

Opinion: Pitch decks as a business pointer

ARK Invests Buys $43.5 Million in Crypto-Related Stocks

Angelina Jolie Makes Rare Admission About Her Love Life

-

Sports6 days ago

Sports6 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics4 days ago

Politics4 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics4 days ago

Politics4 days agoPotential 2028er World Cup attendee leaderboard

-

News Videos1 day ago

News Videos1 day agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Business4 days ago

Business4 days agoAsia stock markets slide as tech shares slump

-

Tech4 days ago

Tech4 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World6 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business6 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World3 days ago

Crypto World3 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports3 days ago

Sports3 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech2 days ago

Tech2 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World4 days ago

Crypto World4 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World4 days ago

Crypto World4 days agoRTX holders must register wallets before token distribution begins

-

Crypto World5 days ago

Crypto World5 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

You must be logged in to post a comment Login