Crypto World

Pi Network’s pivot to AI and identity infrastructure

On Pi2Day, Pi Network stopped talking about mobile mining and started talking about infrastructure, launching tools to sell its compute, identity, and verification to the outside world. It is a real strategic pivot toward the AI era. Whether it fixes Pi’s actual problem, a token down 96% with no demand, is the harder question.

Summary

- On June 28, 2026, Pi Network used its annual Pi2Day event to launch three products, SoloHost, Pi Sign-in, and PiVerify, reframing the project from a mobile-mining app into infrastructure for compute, identity, and AI.

- SoloHost turns Pi Desktop into a platform for local, privacy-first AI apps and, in time, distributed computing across Pi’s hundreds of thousands of user-run nodes, with node operators paid in Pi.

- Pi Sign-in offers a “sign in with Pi” identity login for third-party apps, and PiVerify opens Pi’s human-verification system, which has checked over 18 million users, to outside businesses that pay in Pi.

- The pivot is a credible attempt to monetize Pi’s genuine assets, a large verified user base and a node network, by targeting real demand for private AI, decentralized compute, and trusted digital identity.

- The harder problem is that none of it directly addresses Pi’s core issue: a token down roughly 96% from its peak, weighed down by daily unlocks and migration supply, with no tier-one exchange listing, and the price fell after the announcement.

On June 28, 2026, Pi Network used its annual Pi2Day celebration to make a statement about what it wants to become, and for once the statement was not about mining. The project that grew famous as a mobile app letting tens of millions of people tap a button each day to earn tokens launched three products, SoloHost, Pi Sign-in, and PiVerify, and framed them as a deliberate pivot: from a mining-centric community toward an infrastructure provider for the artificial-intelligence era, offering compute, identity, and verification services to the outside world. The pitch was explicit. Rather than relying only on growth inside its own walled ecosystem, Pi would begin selling its genuine assets, a verified user base of more than 18 million people, a network of hundreds of thousands of user-run nodes, and a hybrid human-verification system, to external developers and businesses.

It was, by the standards of a project often dismissed as a mobile mining curiosity, a substantive strategic statement, and several observers called it the most concrete attempt yet to give Pi real utility beyond its internal apps. The reception was telling, and it frames the question this article examines. The new products were widely covered and broadly seen as more serious than Pi’s usual announcements, yet the token’s price fell after the news, extending a long decline, and the community split between those who welcomed a focus on real infrastructure and those frustrated that, once again, there was no major price catalyst and no tier-one exchange listing. That split is the heart of the matter.

This piece works through what Pi actually announced and what each product does, the logic behind the pivot and why it could matter, the harder reasons it may not move the needle, the community’s divided reaction, the identity angle that may be Pi’s most distinctive asset, and what would have to happen for the pivot to become real. The analysis is information, not advice. The honest framing throughout is that Pi has made a genuine strategic turn toward a credible thesis, and that a strategic turn is not the same as a solution to the supply-and-demand problem that has defined the token’s brutal 2026.

What Pi actually launched

Begin with the products, because the substance matters more than the framing. The headline release is SoloHost, an open, permissionless framework built into Pi Desktop that lets developers build and list applications which users run locally on their own computers, rather than on remote servers. Its emphasis is privacy-focused local AI: the flagship example shipped alongside it, an open-source AI agent, runs and stores its data entirely on the user’s own device, so a person can use AI assistance while keeping their data off third-party servers. SoloHost effectively turns a Pioneer’s computer into their own server, accessible from their phone through the Pi Browser, which lowers the technical barrier to running self-hosted software.

Looking further ahead, SoloHost is positioned to support distributed computing: the network plans to let its node operators contribute computing power to AI tasks, turning the hundreds of thousands of user-run Pi nodes into a practical computing layer for AI workloads, with participating nodes compensated in Pi by the third-party clients that use them. That last detail matters, because it is a direct attempt to create external demand for the token. The other two products target identity and authentication. Pi Sign-in is an authentication service that lets people log into supported third-party websites and apps using their existing Pi account, much like the familiar option to sign in with a major technology provider’s account.

It gives outside developers access to Pi’s large, verified user base while offering users a password-free login, and it extends Pi’s reach beyond its own browser into the wider web. PiVerify is arguably the most strategically interesting of the three: it opens Pi’s identity-verification system to external businesses, letting them use Pi’s know-your-customer and human-verification infrastructure, with those businesses paying in Pi. This is built on a verification base of real scale, a hybrid system combining automated and human checks that has reportedly verified over 18 million users across more than 200 countries and regions. Taken together, the three products share a single thesis: compute through SoloHost and the node network, identity through PiVerify and Pi Sign-in, and privacy-preserving AI running through all of it.

Each is designed to let outside parties use Pi’s existing resources and, in several cases, to pay for that use in Pi. The substance is real, and it is a meaningful departure from the mobile-mining identity that has defined the project. For readers who need the older model first, Pi’s mining and consensus basics explain why the daily tap was never computational mining in the Bitcoin sense. Pi2Day’s message was that the project now wants the conversation to move from how people earned PI to what the network can sell.

The logic of the pivot

The strategy behind these launches is more coherent than Pi’s critics often allow, and it rests on a clear-eyed assessment of what Pi actually has. After years of operation, Pi’s genuine assets are not a sophisticated technology stack or a thriving decentralized-finance ecosystem; they are scale and identity. The project has tens of millions of registered users, more than 18 million of them verified through identity checks, and a network of hundreds of thousands of nodes run by ordinary people on their own computers. Those are unusual assets.

Few crypto projects have a verified human user base of that size, and few have a distributed network of that many participant-operated nodes. The pivot is an attempt to monetize precisely those assets by turning them into services the outside world might actually pay for: the node network becomes a compute layer, the verified user base becomes an identity and authentication resource, and the whole thing is pointed at the demand wave around artificial intelligence. The timing aligns with real trends, which is what gives the thesis its credibility. Three of the most sought-after capabilities in technology right now are privacy-focused local AI, in which computation happens on a user’s device rather than in a corporate cloud; decentralized compute, in which distributed networks provide processing power outside the big data centers; and trusted digital identity, which has become acutely valuable as AI-generated content and bots make it harder to know whether an online actor is human.

Pi’s three releases map directly onto those trends: SoloHost addresses local AI and decentralized compute, while PiVerify and Pi Sign-in address trusted identity. The deeper narrative Pi has leaned into is “human infrastructure for AI,” the idea that its validator network, which has processed enormous volumes of human-verification tasks, makes it a provider of proof-of-human services in an age when distinguishing people from machines is increasingly difficult and increasingly valuable. The founders made this case publicly at a major industry conference, signaling that the pivot is a considered repositioning instead of a one-off product drop. As a strategy, monetizing real scale against genuine demand trends is a reasonable plan, and a more credible one than waiting for an internal app ecosystem to spontaneously produce value.

Why it could matter

Give the bull case its full weight, because parts of it are sound. The first point is that Pi is, for the first time, attempting to create external demand for the token instead of relying solely on internal ecosystem growth. The mechanisms are concrete: businesses using PiVerify pay in Pi, third-party clients using node compute through SoloHost pay node operators in Pi, and external developers tapping Pi Sign-in bring their users into contact with the network. If any of these gains real traction, it would represent something Pi has never had, namely outside parties paying to use Pi’s resources, which is a far healthier source of token demand than speculation or mining rewards.

Genuine utility demand, money flowing in from external use, is exactly what a token needs to escape a purely speculative valuation, and the pivot is at least pointed at creating it. The second point is that Pi’s scale is real and hard to replicate. A verified user base in the tens of millions and a node network in the hundreds of thousands are assets that most projects pursuing identity or decentralized compute would envy, and if Pi can convert even a fraction of that scale into paying external usage, the numbers could be meaningful. The third point is that the trends Pi is targeting are not hype cycles likely to fade quickly; privacy-preserving AI, decentralized compute, and trusted identity are durable, structural demands that are growing as AI adoption accelerates, so Pi is aiming at expanding instead of shrinking markets.

The fourth point is signaling: the launch represents Pi’s most serious attempt yet to position its existing resources for real external use, and a project that ships substantive infrastructure and pitches it at conferences is behaving more like a builder than a promotional scheme, which has value for credibility even before adoption arrives. None of this guarantees success, but it confirms that the pivot is a real strategy aimed at real demand using real assets, which is more than the project’s harshest critics concede. The bull case is not empty. The key is that the bull case depends on usage showing up outside Pi’s own community, not simply on another announcement cycle.

That is also why the SoloHost compute model matters beyond Pi itself. In crypto terms, Pi is trying to move closer to a DePIN-style thesis, where users contribute hardware resources and receive token incentives when external demand pays for those resources. If Pi can turn its node network into a usable compute market, the token gains a clearer reason to circulate. If it cannot, SoloHost remains a credible feature without becoming a meaningful demand engine.

Why it might not move the needle

Now the hard part, because the bull case runs into a problem the new products do not directly solve. Pi’s central issue is not a lack of strategy; it is a brutal supply-and-demand imbalance that the pivot does not address head-on. The token trades near $0.12, down roughly 96% from its peak near $3 in early 2025, weighed down by a structural overhang: large daily unlocks add millions of new tokens to the sellable supply, and the ongoing migration of users from the app to the mainnet steadily converts previously locked balances into liquid, sellable tokens, all against demand that has so far been thin and unproven. On top of that, Pi still lacks a listing on a top-tier exchange, which limits the buying power and liquidity available to absorb the supply.

The new products, however credible as a long-term strategy, do nothing immediate about the daily unlocks, the migration overhang, or the absence of a major listing, which are the forces actually pressing on the price. That is why the supply overhang in detail matters more for the chart than the branding of the pivot. The timing problem compounds this. SoloHost, Pi Sign-in, and PiVerify are early, with the flagship compute framework in beta and the distributed-computing vision still ahead, so any external demand they generate will build slowly, if it builds at all, while the supply pressure is immediate and continuous.

Infrastructure adoption is a multiyear process measured in developers onboarded and businesses signed, not a catalyst that lifts a price in weeks, and the gap between a strategy being announced and that strategy producing measurable token demand can be very long. The market reflected exactly this skepticism: the price fell after the Pi2Day announcement instead of rising, because traders recognized that a credible long-term plan does not change the near-term arithmetic of supply exceeding demand. The sober reading is that the pivot, even if it eventually succeeds, is unlikely to reverse the token’s trajectory soon, because the thing weighing on Pi is a supply overhang that infrastructure announcements do not lift. A good strategy and a falling price can coexist for a long time when the supply side is the problem, and for Pi, the supply side is the problem.

The community split

The divided reaction to Pi2Day captures the project’s central tension, and it is worth understanding because it reflects two legitimate but incompatible expectations. On one side are community members who welcomed the announcements as exactly the kind of substantive, building-focused progress Pi needs, evidence that the team is constructing real infrastructure and pursuing genuine utility instead of chasing speculative attention. To this group, the pivot toward compute, identity, and AI is encouraging precisely because it is unglamorous and long-term, the unflashy work of turning a large community into a useful network. They read SoloHost and PiVerify as signs that Pi is maturing into something with a reason to exist beyond mining rewards, and they value that even though it does not immediately move the price.

On the other side are community members frustrated by the same announcement, for the same reason it pleased the first group: it shipped services instead of a price catalyst, and in particular it did not bring the tier-one exchange listing that much of the community has long anticipated. The days before Pi2Day were thick with speculation, including rumors of a major listing, and when the actual announcement delivered infrastructure instead, the disappointment showed up immediately in the price. This group experiences Pi’s slow, conditions-based pace as a recurring letdown, a pattern of significant events that produce features but not the liquidity and demand that would let holders realize value. The split between these camps is not really a disagreement about facts; it is a disagreement about what Pi should be optimizing for, long-term infrastructure or near-term price and liquidity, and Pi2Day satisfied the first while frustrating the second.

That tension, between the builders and the price-watchers, is structural to a project that has an enormous community sitting on tokens it mostly cannot yet sell at a price it likes, and it will persist until the pivot either produces real demand or it does not. The same tension appears in smaller ecosystem updates, including tools meant to improve app visibility and activity inside Pi’s own directory. Builders can see those as pieces of a broader utility stack, while traders see them as too indirect to absorb the supply hitting the market. Both reactions make sense because they are measuring different things.

The identity angle

Of everything Pi announced, the identity thesis may be its most distinctive and defensible asset, and it deserves a closer look because it is where the pivot is strongest. The problem PiVerify and Pi Sign-in address, verifying that an online actor is a real, unique human, has become one of the most pressing in technology as AI systems generate convincing text, images, and behavior at scale, making bots and fake accounts harder to detect. A network that can reliably attest to human identity has genuine value in that environment, and Pi has built exactly that: a hybrid automated-and-human verification system that has checked over 18 million users across more than 200 countries, producing a large base of verified human identities. Opening that system to external businesses through PiVerify, and offering identity-based login through Pi Sign-in, points Pi at a real and growing market, proof-of-human services for an age of AI bots, where its scale is a genuine competitive asset instead of a liability.

The honest caveats keep this from being a slam dunk. Pi is not alone in pursuing decentralized identity and proof-of-personhood; other projects have built reputations and technology in the same space, and some have more sophisticated cryptographic approaches, so Pi’s advantage is its scale instead of its novelty. Questions also remain about the robustness of Pi’s verification against determined fraud, the privacy implications of a large identity database, and whether external businesses will actually choose Pi’s system over established identity providers. But even with those caveats, the identity angle is the part of the pivot where Pi’s existing assets line up most cleanly with real, growing demand, and where its scale is most clearly an advantage.

If any piece of the AI-infrastructure thesis becomes a meaningful business for Pi, the identity layer is the most likely candidate, because it is the one where Pi already has something large and hard to replicate that the market increasingly needs. For an observer judging whether the pivot has substance, the identity angle is the most credible reason to take it seriously. It is also where the identity thesis Pi is chasing connects most directly to a wider crypto problem, not just a Pi-specific one. In an internet crowded with AI agents and synthetic users, verified human identity is not a niche use case; it is becoming basic infrastructure.

What would make the pivot real

In the end, the pivot will be judged not by its announcement but by whether it produces the one thing Pi has always lacked: real, external demand large enough to matter against the token’s supply. That requires a recognizable set of developments, and naming them is more useful than guessing at a price. The first and most direct is external businesses actually paying in Pi at scale, real companies using PiVerify for identity checks, real clients paying node operators for compute through SoloHost, real developers integrating Pi Sign-in, with the resulting token demand visible and growing instead of nominal. Adoption metrics, not announcements, are the proof.

The second is that this demand grows fast enough to outpace the supply pressure, the daily unlocks and the migration overhang, so that real usage absorbs the new tokens entering the market instead of being swamped by them. That is where why migration adds sell pressure becomes central to the investment case. The third is liquidity, which for Pi means a tier-one exchange listing that would bring the deep markets and buying power needed to support a higher valuation, the catalyst much of the community has awaited and that the infrastructure pivot does not by itself provide. The honest reading is that the bull case requires these together, real external demand, demand outpacing supply, and the liquidity to express it, not any one alone, and that none of them is presently in hand.

What Pi2Day delivered is a credible strategy and a set of early products pointed at genuine demand trends, which is necessary but not sufficient. A token cannot pay its bills with potential, and the supply weighing on Pi is immediate while the demand the pivot might create is prospective and slow. The realistic conclusion is that Pi has made a serious and arguably overdue strategic turn, that the identity and compute thesis is more credible than the project’s reputation suggests, and that whether it rescues the token depends entirely on execution that has not yet happened. The pivot is real; whether it works is the question the coming months, not the announcement, will answer.

Frequently asked questions

What did Pi Network announce on Pi2Day 2026?

On June 28, 2026, Pi Network launched three products framed as a pivot toward infrastructure for compute, identity, and AI. SoloHost is an open framework in Pi Desktop for running local, privacy-first AI apps and, in time, distributed computing across Pi’s node network, with node operators paid in Pi. Pi Sign-in is a “sign in with Pi” authentication service letting people log into third-party apps with their Pi account. PiVerify opens Pi’s identity-verification system, which has checked over 18 million users across more than 200 countries, to external businesses that pay in Pi. Together they reframe Pi from a mobile-mining app into a provider of compute, identity, and AI-related services to the outside world. The important point is that these products try to monetize resources Pi already has: a large verified user base and a large network of user-run nodes. That makes the pivot more substantive than a branding change, even if adoption remains unproven.

Is Pi Network pivoting away from mining?

In emphasis, yes. The Pi2Day launches mark a deliberate shift from a mobile-mining-centric identity toward positioning Pi as an infrastructure provider for the AI era, monetizing its genuine assets, a large verified user base and a node network, as external services. Mining and the broader migration process continue, but the strategic narrative has moved toward compute, identity, and AI. The logic is that Pi’s real assets are its scale and its verified human identities, not a sophisticated technology stack, so the path to value is turning that scale into services outside parties will pay for. Whether the pivot succeeds depends on actual external adoption, which has not yet been proven. The daily tap may still define how millions of users think about Pi, but it is no longer the most important part of the project’s pitch. The new pitch is that Pi can sell identity, verification, and compute to third parties.

Will the Pi2Day pivot raise Pi’s price?

Not directly or quickly, on the evidence so far. The price fell after the announcement, because the new products, however credible as long-term strategy, do not address Pi’s immediate problem: a supply overhang from large daily unlocks and ongoing migration converting locked tokens into sellable ones, against thin demand and no tier-one exchange listing. Infrastructure adoption builds slowly, over years of onboarding developers and businesses, while the supply pressure is continuous. The pivot could eventually create real token demand if external businesses pay to use Pi’s compute and identity services at scale, but that is prospective and gradual. The forces weighing on the price are present and ongoing. A good strategy and a falling price can coexist when supply is the problem. For Pi, the market is asking for proof that demand can absorb unlocks, not only proof that the team can ship products.

What is the “human infrastructure for AI” narrative?

It is Pi’s framing of its core thesis: that its network of verified human users and the validators who process identity checks make it a provider of proof-of-human services in an age when AI makes distinguishing people from bots increasingly difficult. Pi’s verification system has processed enormous volumes of human-verification tasks across a base of more than 18 million verified users in over 200 countries. The pivot leans on this, positioning Pi’s identity and verification resources, through PiVerify and Pi Sign-in, as infrastructure that businesses need as AI-generated content and bots proliferate. It is the most distinctive part of Pi’s strategy, because trusted digital identity is a real and growing demand, and Pi’s scale of verified humans is genuinely hard to replicate. The challenge is turning that verified base into a product outside businesses actually choose to use. Scale alone is not enough if the verification layer is not trusted, easy to integrate, and privacy-conscious. That is why PiVerify is strategically important: it is the bridge between Pi’s internal verification work and an external identity market.

Why is Pi’s price so low despite a large community?

Because supply has overwhelmed demand. Pi trades near $0.12, down roughly 96% from its early-2025 peak near $3, because large daily token unlocks and the ongoing migration of users to the mainnet keep converting locked tokens into sellable supply, while demand has been thin and there is no tier-one exchange listing to bring deep liquidity and buying power. Many users treat mined Pi as tokens to sell once they become transferable, and weak app adoption has meant little organic usage to absorb the supply. The community’s goals, faster migration and bigger listings, ironically increase the sellable supply. The result is a structural imbalance that ecosystem announcements, including the Pi2Day pivot, do not by themselves resolve. For the price to stabilize, usage demand has to become large enough to meet the supply entering the market. Until then, even good news can fail to move the token if holders use liquidity as an exit.

What would make Pi’s pivot succeed?

Real, external demand large enough to matter against the supply. Concretely, that means external businesses actually paying in Pi at scale: companies using PiVerify for identity checks, clients paying node operators for compute through SoloHost, developers integrating Pi Sign-in, with visible, growing token demand instead of nominal usage. It also means that demand growing fast enough to outpace the daily unlocks and migration overhang, so real usage absorbs the new supply. And it likely means a tier-one exchange listing to provide the liquidity and buying power a higher valuation requires. The bull case needs these together, not any one alone, and none is presently in hand. Adoption metrics, not announcements, will determine whether the pivot becomes real. Pi has made the strategic argument; now it has to prove that outside customers want what the network is selling.

This article is information, not financial or investment advice. Details of Pi Network’s Pi2Day releases, user and node figures, price levels, and supply dynamics reflect reporting available as of June 30, 2026, are point-in-time, and can change. Cryptocurrency is highly volatile and you can lose money. Nothing here is a recommendation about Pi or any asset. Do your own research and consult a qualified professional before making any decision.

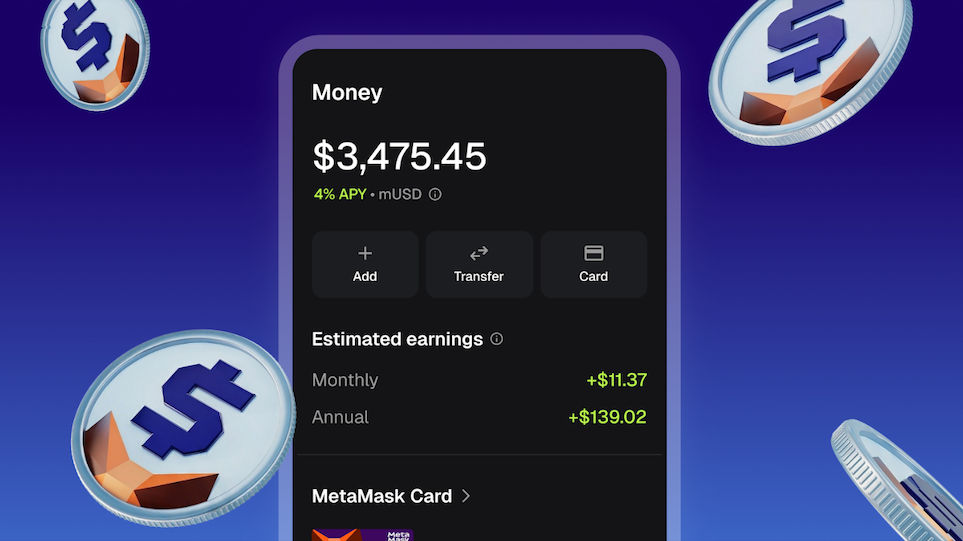

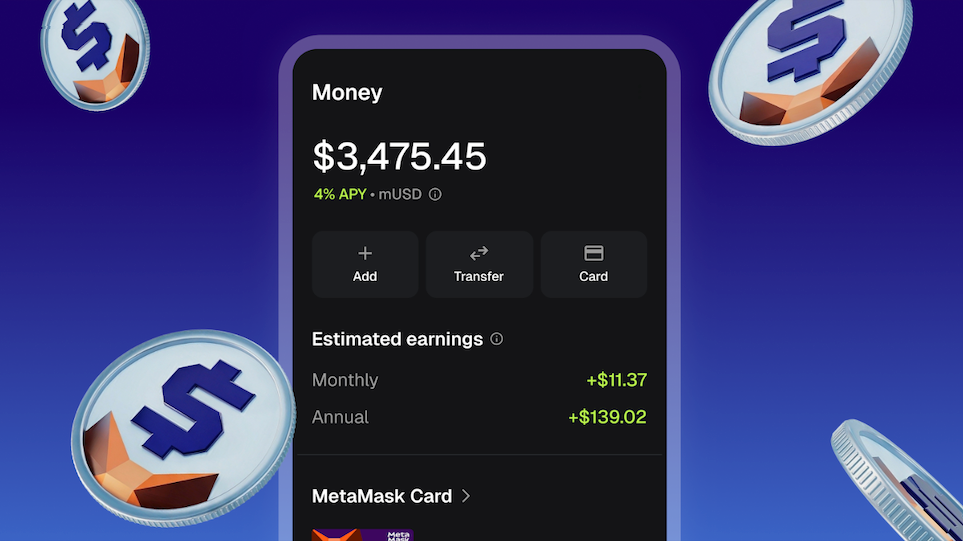

MetaMask is rolling out a new way for users to earn yield on its wallet-native MetaMask USD (mUSD) stablecoin—while keeping the wallet self-custodial. The Consensys-backed team says its newly launched Money Account can provide up to 4% variable APY on eligible deposits, with funds intended to be spent via a card on the Monad blockchain.

The launch lands at a moment when US regulators and lawmakers have been closely debating whether yield-bearing stablecoins—especially those that pay interest to token holders—should be treated like traditional financial products. MetaMask’s approach attempts to separate the stablecoin’s reserve backing from the mechanics of how returns are generated.

Key takeaways

- MetaMask Money Account targets up to 4% variable APY on eligible mUSD deposits in supported jurisdictions.

- Yield is described as coming from DeFi lending activity, not issuer-paid interest.

- mUSD reserves are said to be backed 1:1 by US dollar assets held by Bridge, a Stripe company.

- Availability is limited: the product excludes the UK, EU member states, and sanctioned jurisdictions.

- Because MetaMask is self-custodial, KYC is not performed by MetaMask itself, but is required for regulated features like fiat on-ramps and the MetaMask Card.

A yield product that MetaMask says is “structurally separate”

Consensys positions Money Account as a two-layer system that distinguishes how mUSD is backed from how users’ yield is produced. In an explanation provided to Cointelegraph, Johann Bornman, MetaMask senior director of product, said the design deliberately separates the stablecoin’s reserve backing from the yield layer.

According to Bornman, the first layer concerns reserve backing. He said Bridge, described as holding US dollar reserves and short-term Treasury bills, backs mUSD on a 1:1 basis. In this model, the issuer is not portrayed as paying yield to holders.

The second layer is the onchain yield engine. When users open a Money Account and deposit mUSD, the stablecoin is routed into a DeFi system managed through a vault provider called Veda. Veda then allocates capital into lending protocols including Aave and Morpho.

Bornman summarized the intent behind the product’s architecture by stating that reserve backing and yield generation are “structurally separate,” adding that the yield “doesn’t come from the issuer” but from DeFi protocol activity.

How users can earn—and where the spend flow fits

MetaMask says Money Account allows users to earn yield and spend without waiting to redeem. In remarks attributed to Consensys CEO Joe Lubin, the company characterized the product as enabling users to earn the moment funds are added and spend the moment they need to.

While MetaMask frames the yield mechanism as DeFi-driven, the company’s spending functionality is tied to a specific environment: yield-bearing funds are intended to be spent via a card exclusively on Monad. The product’s rollout therefore appears to combine an earnings layer built on DeFi lending with an application layer for spending within a particular blockchain ecosystem.

Investors and traders watching stablecoin yield mechanics will likely focus on whether this “separation” of backing versus yield impacts regulatory exposure. That question has been central in the broader US debate over whether certain stablecoin designs resemble interest-bearing investment products.

Regulatory friction in the US, and the CLARITY Act backdrop

MetaMask’s launch comes amid continued discussion in the United States around yield-bearing stablecoins. The article notes that the CLARITY Act contains provisions related to restricting payment of interest or yield on payment stablecoins when tied to holding.

MetaMask’s product design—using reserve backing by Bridge and generating yield via DeFi protocols—can be read as an attempt to fit into a narrower interpretation of how returns are created. Still, the practical regulatory classification will depend on how authorities interpret the overall arrangement, including how users experience “yield” and how control and economics are distributed.

For readers, the key takeaway is that Money Account may offer a clearer explanation of its mechanics, but it does not automatically resolve regulatory risk. What matters next is how regulators treat yield features in practice, especially where stablecoins are used with spending rails like cards.

Self-custody, KYC boundaries, and restricted access

Money Account is rolling out globally starting Tuesday, but excluding the United Kingdom, EU member states, and sanctioned jurisdictions, Bornman said.

MetaMask’s self-custodial model affects how compliance is implemented. The wallet itself, as described, does not require KYC because it does not custody user funds. However, Bornman emphasized that KYC is required for features that interact with regulated services—explicitly including fiat on-ramps and the MetaMask Card.

Bornman further said Money Account does not require KYC and that users can hold mUSD and earn yield with the “click of a button.” In cases where KYC is needed, he attributed the responsibility to third-party providers that operate regulated services, rather than MetaMask.

For users in eligible jurisdictions, this could reduce friction compared with yield products that require full identity verification before deposit. For builders and compliance teams, the model suggests a split between self-custody interfaces and regulated rails—something the market increasingly looks for as stablecoin products scale.

mUSD is still small—so the rollout is about distribution

The broader story here is not only the yield feature, but MetaMask’s push to expand the utility of mUSD. The launch follows MetaMask’s wallet-native stablecoin debut in September 2025. CoinGecko data cited in the article shows mUSD’s market capitalization briefly peaked above $100 million shortly after launch, then fell below $30 million. At the time of writing, mUSD’s market cap was around $32 million, placing it among smaller US dollar-pegged stablecoins by market size.

That context matters: Money Account could help drive additional demand for mUSD by turning a wallet-native token into an yield-bearing balance with a spending pathway. But market participants will likely watch whether the yield feature increases sustained usage—or whether deposits remain limited given the restricted geography and the narrower user flow to Monad-based card spending.

With Money Account now live, the next signals to monitor are user uptake in supported regions, any changes in APY as DeFi strategies and conditions evolve, and how the product’s “issuer vs DeFi yield” structure is received by regulators amid US debates over yield-bearing stablecoins.

The Clarity Act is widely viewed as the crypto industry’s most important market structure bill because it would establish clear rules for when digital assets are regulated as securities by the Securities and Exchange Commission (SEC) or commodities by the Commodity Futures Trading Commission (CFTC), replacing years of regulatory uncertainty.

Supporters say that legal clarity would make it easier for banks, asset managers and other institutions to launch tokenized products, custody services and blockchain-based financial offerings, potentially unlocking broader institutional adoption and investment in the sector.

According to Jefferies, passage would provide the durable regulatory framework banks, asset managers and exchanges need to expand tokenization, custody, staking, lending and other blockchain-based services. The bank also expects it to accelerate tokenized securities, broaden crypto exchange-traded fund (ETF) offerings beyond bitcoin and ether (ETH), and revive the pipeline for crypto infrastructure IPOs.

A delay, however, would extend regulatory uncertainty. While recent SEC, CFTC and OCC guidance has improved the outlook, the report said agency actions can be reversed by future administrations, potentially prompting regulated financial institutions to slow blockchain initiatives while reassessing legal and compliance risks.

The bank’s analysts expect the legislative process to drive volatility in crypto-linked equities including Circle (CRCL), Coinbase (COIN) and CoinDesk’s owner Bullish (BLSH), as well as select crypto tokens.

Key Takeaways

- Dish DBS, EchoStar’s satellite television division, is expected to enter chapter 11 bankruptcy protection this week, potentially by Tuesday.

- A pre-negotiated restructuring agreement has secured support from bondholders representing over 82% of approximately $10 billion in Dish DBS obligations.

- The parent company shoulders approximately $25 billion in aggregate debt while hemorrhaging subscribers—losing about 177,000 pay TV customers in the latest quarter.

- Awaited spectrum transactions with AT&T (valued at $22.65 billion) and SpaceX (valued at $17 billion) remain incomplete, preventing debt reduction.

- On Monday, SATS stock started trading at $103.80, carrying a consensus Hold recommendation with analysts projecting an average target of $137.71.

Shares of EchoStar (SATS) began Monday’s session at $103.80, slipping 0.1% as the company moves forward with plans to file chapter 11 bankruptcy for its Dish DBS satellite television division, the Wall Street Journal reports.

The bankruptcy petition could be submitted as early as this Tuesday. The move addresses close to $10 billion in Dish DBS liabilities that have burdened EchoStar’s balance sheet.

Underpinning the bankruptcy strategy is a restructuring framework negotiated earlier this year. Bondholders controlling more than 82% of Dish DBS debt have already committed to the arrangement.

The proposal seeks to reduce outstanding obligations, resolve bondholder litigation, and provide EchoStar with increased financial flexibility for future strategic transactions. White & Case has been retained for legal representation, while FTI Consulting serves as financial advisor for Dish DBS.

Financial Deterioration Drives Restructuring

EchoStar’s traditional pay television operations continue to deteriorate. The segment generated $2.26 billion in revenue during the most recent quarter, representing a year-over-year decline exceeding $260 million.

Customer attrition compounds the revenue challenge. Approximately 177,000 net pay TV subscribers departed during the quarter, reducing the total customer base to slightly above 6.6 million.

The company’s consolidated debt burden stands at roughly $25 billion. This substantial leverage poses increasing challenges for an enterprise confronting what EchoStar characterized as “intense and increasing competition” across video, broadband, and wireless markets.

This restructuring represents EchoStar’s latest attempt to stabilize its financial position. A proposed 2024 merger between Dish Network and DIRECTV ultimately failed after bondholders rejected a mandatory debt exchange.

Those creditors contended the transaction would improperly transfer billions in assets to entities controlled by EchoStar founder Charlie Ergen. That contentious episode clearly influenced the negotiation approach for the current restructuring plan.

Spectrum Asset Sales Remain Incomplete

Regulatory pressure from the FCC regarding 5G network deployment commitments has also complicated EchoStar’s situation. To resolve compliance issues, the company arranged spectrum asset sales to AT&T for $22.65 billion and to SpaceX for $17 billion.

Both transactions remain unconsummated. The combined proceeds are intended to substantially reduce EchoStar’s debt burden once the sales finalize.

The extended timeline has already created operational disruptions. EchoStar defaulted on interest obligations for multiple bonds scheduled for June 1 payment, attributing the missed payments to delayed AT&T transaction proceeds.

By mid-June, EchoStar announced that Dish DBS would satisfy those delinquent interest payments. This temporary solution maintained operational continuity while the comprehensive restructuring advanced.

Regarding operational performance, EchoStar reported a quarterly loss of $0.51 per share, underperforming analyst projections by three cents. Quarterly revenue reached $3.67 billion, marginally exceeding the $3.65 billion consensus estimate and representing improvement from the $0.71 per-share loss recorded one year prior.

Analyst sentiment toward SATS stock remains divided but generally cautious. The consensus recommendation stands at Hold, with price objectives spanning from Weiss Ratings’ sell recommendation to TD Cowen’s $155 buy-rated target.

CEO Hamid Akhavan executed a sale of 52,586 shares on June 5 at an average price of $121.00 per share, generating proceeds exceeding $6.36 million. The transaction occurred pursuant to a predetermined trading arrangement and reduced his holdings by 5.73%, though company insiders collectively maintain 55.90% ownership.

Crypto World

Ethereum Price Analysis: ETH Defends $1.5K Support, But Weak Demand Puts Recovery in Question

Ethereum continues to trade within a firmly bearish market structure despite showing signs of stabilization around a major support zone. While buyers have managed to defend the recent lows, both the daily and 4-hour charts suggest that any recovery attempt still faces significant overhead resistance. Meanwhile, exchange price data indicates that institutional demand through Coinbase remains weak, reinforcing the cautious outlook.

Ethereum Price Analysis: The Daily Chart

The daily chart shows ETH extending its broader downtrend inside a well-defined descending channel. Price remains below the major moving averages, with the 100-day and 200-day averages both sloping lower overhead.

Following the sharp breakdown below the $1.85K support and a decisive retest and rejection, ETH is trading range-bound around the $1.5K support zone, which currently spans roughly $1.45K to $1.55K. This area has once again attracted buying interest and prevented further downside, making it the most important support for the buyers in the near term.

On the upside, the first notable resistance sits around $1.85K, which previously acted as support before turning into resistance after the breakdown. Above that, sellers are likely to defend the $2K to $2.2K supply zone, which also aligns with the declining moving averages and the upper boundary of the descending channel.

ETH/USDT 4-Hour Chart

On the 4-hour timeframe, Ethereum has finally broken above the descending trendline that had capped price action throughout last week’s decline. This is the first meaningful improvement in its short-term market structure. The price is now retracing for a potential retest, and if buyers successfully defend, it will increase the credibility of an upward move.

Despite this constructive development, ETH continues to trade below the key horizontal resistance at $1.75K, which remains the primary obstacle before a larger recovery can unfold. A decisive break above this supply zone could pave the way for a move toward the $1.85K resistance, where sellers are expected to become active once again.

Momentum has also improved following the breakout, with the RSI recovering toward the neutral 50 level after previously emerging from oversold conditions. While this suggests selling pressure has eased, buyers still need to reclaim the nearby resistance cluster to fully confirm a short-term bullish reversal.

As long as Ethereum holds above the broken trendline and the $1.5K support region, the probability of an extended relief rally remains elevated. However, losing these support levels would invalidate the breakout and shift momentum back in favor of the sellers.

Sentiment Analysis

The Coinbase Premium Index continues to paint a cautious picture for Ethereum. The metric has remained predominantly below the neutral line and recently dropped deeper into negative territory, indicating that ETH is trading at a discount on Coinbase relative to other exchanges.

This generally reflects weaker buying pressure from U.S.-based institutional and large-scale investors, a group that has historically played an important role during sustained recoveries. Although occasional rebounds in the premium have appeared throughout the past several months, they have failed to develop into persistent positive readings.

As long as the Coinbase Premium Index remains negative, institutional demand appears subdued, limiting the probability of a strong bullish reversal. A sustained recovery in the premium back above zero would be an early indication that larger buyers are returning to the market and could provide additional confirmation for any technical breakout.

The post Ethereum Price Analysis: ETH Defends $1.5K Support, But Weak Demand Puts Recovery in Question appeared first on CryptoPotato.

Strategy stock has remained under pressure after TD Cowen cut its price target despite backing Michael Saylor’s latest capital strategy and maintaining a bullish rating on the company.

Summary

- TD Cowen cut its Strategy price target to $260 while maintaining a buy rating on the stock.

- The brokerage cited a weaker long-term Bitcoin outlook, not concerns over Strategy’s new capital plan.

- Investors are closely watching whether Strategy will resume Bitcoin purchases as mNAV remains below 1.0.

According to a recent TD Cowen research note, the brokerage reduced its price target for Strategy (MSTR) from $400 to $260 while keeping a “buy” rating on the stock. The firm attributed the lower valuation to a more conservative long-term outlook for Bitcoin (BTC), rather than concerns over Strategy’s newly announced Digital Credit Capital Framework.

Despite the reduction, TD Cowen said the revised target still implies roughly 200% upside from current trading levels.

The revision came a day after Strategy shares rallied more than 12% as investors reacted to the company’s latest financing framework. Although the stock gave back part of those gains in the following session, TD Cowen described the new capital plan as a positive step that could improve the company’s financial flexibility over time.

Bitcoin outlook has driven the target reduction

TD Cowen’s report separates its Bitcoin expectations from its view on Strategy’s corporate actions. Instead of questioning the company’s latest financial decisions, the brokerage lowered its valuation because it expects a weaker long-term Bitcoin price than previously forecast.

The updated assessment arrives as Strategy continues adjusting how it manages its Bitcoin treasury. In a regulatory filing dated June 29, the company introduced its Digital Credit Capital Framework, giving it the ability to raise up to $1.25 billion through Bitcoin sales.

According to the filing, proceeds could be used to maintain U.S. dollar reserves, fund preferred dividend payments, meet interest obligations, increase cash holdings, and finance future share repurchases.

Alongside the new framework, Strategy authorized the repurchase of up to $1 billion of its Digital Credit Securities, including STRC, STRF, STRD, and STRK, if management determines that buybacks would strengthen the company’s capital structure.

The company also disclosed that it has paused additional Bitcoin purchases while selling about $1.15 billion worth of MSTR shares as part of its capital management strategy.

Strategy faces new questions over Bitcoin accumulation

Attention has also turned to whether Strategy can continue expanding its Bitcoin holdings under current market conditions.

On June 28, Michael Saylor posted Strategy’s Bitcoin tracker on social media alongside the message, “We’re gonna need more charts.” Similar tracker posts have preceded previous Bitcoin purchase announcements, leading some investors to speculate that another acquisition could be disclosed.

Strategy’s most recent reported purchase came on June 22, when it acquired 520 BTC for approximately $35 million at an average price of $67,068 per coin. The purchase increased the company’s total holdings to 847,363 BTC, according to its official Bitcoin purchase tracker.

Recent market conditions, however, have complicated the company’s long-running accumulation model. As previously reported, Strategy’s mNAV has fallen below 1.0 for the first time during this market cycle, dropping to around 0.80 after Bitcoin slipped below $60,000.

Trading below the value of its Bitcoin holdings makes it harder for the company to issue new shares at a premium and use those proceeds to buy additional BTC without diluting existing shareholders.

Management has previously indicated that issuing common equity below roughly 1.22 times mNAV can become value-destructive on a per-share basis. As a result, some investors have questioned whether restoring the valuation premium should take priority over further Bitcoin purchases.

Strategy’s updated framework has also sparked criticism from some market participants because it allows limited Bitcoin monetization. Critics argue that selling Bitcoin could weigh on market sentiment, while Ripple CEO Brad Garlinghouse has publicly criticized Strategy’s role during the recent crypto market decline.

The debate has gained additional attention because Saylor has consistently encouraged long-term Bitcoin holding even as the company evaluates new ways to manage its balance sheet.

MetaMask, a self-custodial wallet developed by Consensys, is launching a new product that it says lets users earn yield on its MetaMask USD (mUSD) stablecoin and spend it via a card exclusively on the Monad blockchain.

The company on Tuesday announced the launch of Money Account, a product it says offers up to 4% variable annual percentage yield (APY) on eligible stablecoin deposits in supported jurisdictions.

“Your balance earns the moment you add funds, and you can spend the moment you need to,” Consensys CEO Joe Lubin said in a statement seen by Cointelegraph.

The launch comes amid ongoing debate over yield-bearing stablecoin products in the US, where the CLARITY Act includes provisions restricting the payment of interest or yield on payment stablecoins when tied to holding.

Yield engine powered by DeFi vaults

Money Account generates yield through decentralized finance (DeFi) lending strategies rather than issuer-paid interest, MetaMask senior director of product Johann Bornman told Cointelegraph.

The system relies on two entirely separate mechanisms, separating how the stablecoin is backed from how yield is generated, Bornman said.

A preview of MetaMask’s Money Account. Source: ConsenSys

The first mechanism involves stablecoin backing. Bridge, a Stripe company, holds US dollar reserves and short-term Treasury bills that back mUSD on a 1:1 basis. Under this structure, the issuer does not pay any yield to holders.

The second mechanism is the DeFi yield layer. When users deposit into a Money Account, funds are routed through onchain vault provider Veda, which allocates capital into established lending protocols such as Aave and Morpho.

“Simply put, mUSD’s reserve backing and the yield users earn are structurally separate,” Bornman said, adding: “The yield doesn’t come from the issuer, it comes from DeFi protocol activity.”

KYC and availability: EU and UK among restricted geos

The Money Account is rolling out globally on Tuesday, except in the United Kingdom, European Union member states and sanctioned jurisdictions, Bornman said.

As MetaMask operates a self-custodial wallet, the platform itself does not require Know Your Customer checks, but KYC is required for any features that interact with regulated services, including fiat on-ramps and the MetaMask Card.

Related: Trezor adds native USDt, USDC yield via Morpho integration

“Money Account itself does not require KYC, users can hold mUSD and earn yield with the click of a button,” Bornman said. “Where KYC is required, those checks are carried out by third-party providers that operate those regulated services, not by MetaMask,” he added.

The launch comes less than a year after MetaMask officially launched its wallet-native mUSD stablecoin in September 2025.

MetaMask USD (mUSD) market capitalization since launch. Source: CoinGecko

The stablecoin’s market capitalization briefly peaked above $100 million shortly after launch before slipping below $30 million, according to CoinGecko data.

At the time of writing, mUSD’s market cap stood at $32 million, placing it among smaller US dollar-pegged stablecoins by market size.

Magazine: Bitcoin decouples from tech stocks, Ether eyes ‘selling wave’: Market Moves

Key Highlights

- Micron Technology (MU) has pledged $250 million toward Trump Accounts, officially designated as 530A Accounts.

- The initiative aims to benefit approximately one million young Americans and their families.

- Employees receive matching contributions of up to $1,000 annually for each child under age 18.

- Qualifying children across Idaho, New York, Virginia, California, Colorado, Minnesota, and Texas will receive initial $250 deposits.

- This move complements Micron’s previously announced $200 billion domestic manufacturing expansion.

Micron Technology (MU) has made a substantial financial commitment to a newly established federal children’s savings initiative. The semiconductor manufacturer revealed its $250 million pledge to Trump Accounts on Tuesday, marking the occasion alongside America’s 250th birthday celebration.

Trump Accounts—officially designated as 530A Accounts—represent a fresh approach to childhood savings programs. These accounts channel investments into low-cost U.S. index funds, providing minors with access to sustained equity market performance over time.

The company characterizes its financial pledge as the most significant corporate participation in the program to date. Micron anticipates extending benefits to nearly one million young people through this initiative.

Program Structure and Benefits

Employees of Micron will receive dollar-for-dollar contribution matching for deposits made into their children’s accounts. This matching program covers annual contributions reaching $1,000 per qualifying child under 18 years old.

Beyond employee benefits, the chipmaker has designated funds for broader community impact. Children residing in designated states will receive a one-time $250 initial deposit into newly established Trump Accounts.

The eligible states—Idaho, New York, Virginia, California, Colorado, Minnesota, and Texas—align with Micron’s current manufacturing and operational footprint.

The distribution strategy focuses resources on areas where Micron maintains active facilities. Consequently, workers and residents in proximity to company sites will receive primary access to these financial benefits.

Alignment with Domestic Expansion Plans

This financial commitment doesn’t exist in isolation. Micron previously announced plans to deploy over $200 billion toward domestic memory chip production and innovation facilities.

That capital allocation targets the creation of more than 90,000 American employment opportunities. The Trump Accounts participation represents a parallel investment in human capital development.

CEO Sanjay Mehrotra emphasized that Micron recognizes human investment as equally critical to technological advancement. He expressed appreciation to the Trump administration for establishing the account framework.

Treasury Secretary Scott Bessent responded positively to the announcement, characterizing the commitment as promising and positioning Micron as an example for other corporations. [[LINK_START_4]]Dell Technologies[[LINK_END_4]] CEO Michael Dell endorsed the initiative as well, referencing existing commercial relationships between the two companies.

Invest America founder Brad Gerstner distinguished the pledge as substantive rather than ceremonial. He emphasized that the commitment places tangible capital into private accounts benefiting close to one million children.

Micron’s investment portfolio extends beyond savings accounts into additional workforce development channels. The company supports K-12 STEM programming, semiconductor-focused educational materials, artificial intelligence learning initiatives, and collaborations with two-year and four-year educational institutions.

The semiconductor manufacturer also funds registered apprenticeship opportunities within the chip industry. While administered separately from the Trump Accounts program, these initiatives align with Micron’s comprehensive workforce cultivation strategy.

Families seeking to establish a Trump Account can access the platform at trumpaccounts.gov. Micron indicated that comprehensive eligibility criteria for community seed funding will become available through its dedicated portal at micron.com/communityinvestment.

Bitget, the world’s largest Universal Exchange (UEX), has launched TradFi 101, a long-term educational initiative designed to help crypto users understand traditional financial markets and navigate the growing intersection between digital assets and global finance. The program introduces structured learning resources covering financial foundations, asset classes, market mechanics, macroeconomics, risk management, and the evolution of multi-asset investing.

As tokenized assets become more accessible and investors increasingly participate across crypto, equities, commodities, ETFs, and real-world assets, financial literacy is becoming an essential skill for market participants. TradFi 101 is designed for a market environment where crypto-native investors can learn the drivers behind stocks, commodities, currencies, and capital flows.

Built with an education-first approach, TradFi 101 is designed as an open industry initiative that brings together exchanges, media platforms, researchers, educators, and creator communities to make financial education more accessible. Current participating and invited ecosystem contributors include Coin Bureau, CoinGecko, and TradingView among others.

“Financial markets are becoming increasingly connected, and traders are already navigating more than a single asset class,” said Gracy Chen, CEO of Bitget. “Crypto investors today pay attention to interest rates, inflation, equities, commodities, and global liquidity alongside digital assets. As tokenization expands access to financial markets, understanding how these systems work together becomes increasingly important. TradFi 101 was created to make that knowledge more accessible and help users prepare for a future where traditional and digital assets exist within the same investment landscape.”

TradFi 101 consists of six learning modules released through a structured curriculum and supported by weekly educational content, community participation, and assessments. The program will answer 100 essential financial questions through simplified lessons designed for crypto audiences. Modules include Financial Foundations: Rediscover TradFi, Asset Encyclopedia: Your Global Wealth Checklist, Market Mechanics: How Trading Happens, Macroeconomics: The Invisible Hand, Risk & Human Nature: The Trader’s Mindset, and Universal Exchange: The Final Form of Finance.

The final module explores the convergence of traditional and digital assets within a unified trading environment. As the world’s largest Universal Exchange, Bitget already provides access to more than 2 million crypto tokens alongside over 10,000 US stocks, 500+ tokenized stocks, ETFs, commodities, foreign exchange products, and precious metals. TradFi 101 examines how tokenization is expanding access to global markets and why a broader understanding of finance will become increasingly valuable in the years ahead.

TradFi 101 is designed as a long-term initiative that contributes to the industry’s broader effort to improve financial literacy for the multi-asset era. By bringing together educational contributors from across the ecosystem, the program aims to help the next generation of traders build the knowledge needed to participate more confidently in an increasingly connected financial system.

For more information, visit: https://www.bitget.com/activity-hub/tradfi-101

About Bitget

Bitget is the world’s largest Universal Exchange (UEX), serving over 125 million users and offering access to over 2M crypto tokens, 500+ tokenized stocks, ETFs, commodities, FX, and precious metals such as gold. The ecosystem is committed to helping users trade smarter with its AI agent, which co-pilots trade execution. Bitget is driving crypto adoption through strategic partnerships with LALIGA and MotoGP™. Aligned with its global impact strategy, Bitget has joined hands with UNICEF to support blockchain education for 1.1 million people by 2027. Bitget currently leads in the tokenized TradFi market, providing the industry’s lowest fees and highest liquidity across 150 regions worldwide.

For more information, visit: Website | Twitter | Telegram | LinkedIn | Discord

Risk Warning: Digital asset prices are subject to fluctuation and may experience significant volatility. Investors are advised to only allocate funds they can afford to lose. The value of any investment may be impacted, and there is a possibility that financial objectives may not be met, nor the principal investment recovered. Independent financial advice should always be sought, and personal financial experience and standing carefully considered. Past performance is not a reliable indicator of future results. Bitget accepts no liability for any potential losses incurred. Nothing contained herein should be construed as financial advice. For further information, please refer to our Terms of Use.

The post Bitget Launches TradFi 101 to Prepare Users for the Universal Exchange Era appeared first on BeInCrypto.

OKX has launched a beta marketplace for artificial intelligence (AI) agents, positioning the platform as “economic infrastructure” for agentic commerce. The initiative lets developers list their own AI agents to earn revenue, while other agents and users can post tasks, find suitable agents, and complete work with onchain settlement and a shared reputation layer.

OKX says the marketplace will connect an agent marketplace—where builders monetize agent services—with a separate task marketplace that matches incoming work to agents. The beta will run until OKX sees “consistent, repeat usage patterns” across users, with trading, onchain activity, and research tasks expected to be the first major categories.

Key takeaways

- OKX’s AI agent marketplace connects a service-listing agent market with a task market for matching agent-to-agent work.

- Builders can get paid in stablecoins initially including USDT and USDG, with escrow for complex tasks and instant pay-per-call for standardized services.

- All agent tasks feed into a single onchain reputation system designed to reduce hiring risk from agents with poor or disputed histories.

- The beta is expected to emphasize trading, onchain tasks, and research, and remains in testing until usage patterns stabilize.

How OKX’s AI agent marketplace works

According to OKX’s announcement shared with Cointelegraph, the OKX AI platform is built around two marketplaces. In the agent marketplace, AI developers can list agents that offer services, and earn income when those agents are selected. In the task marketplace, tasks are posted and agents can locate other agents capable of completing them.

OKX also describes the platform as a combined stack for identity, reputation, payments, and a skills marketplace. Its spokesperson told Cointelegraph that it is not just another catalog of AI tools, but a framework meant to let agent-driven transactions proceed with verifiable histories.

Stablecoin payments and escrow-based settlement

For compensation, OKX says AI agent builders will be paid in stablecoins. The beta is scheduled to start with Tether’s USDT (USDT) and Paxos’ Global Dollar (USDG), with settlement handled through smart-contract mechanisms depending on task type.

For more complex work, OKX says payments will use escrow-based contracts until deliverables are completed and verified. For standardized services, the platform will support instant “pay-per-call” transactions, aiming to reduce friction where outcomes are less subjective.

The practical implication for participants is that payout logic is designed to map to how tasks are executed: escrow is intended to slow down releases when verification is needed, while pay-per-call is intended for repeatable operations that can be confirmed quickly.

Onchain reputation as an anti-malicious layer

A central feature of the beta is an onchain reputation system managed through the OKX Agentic Wallet. OKX says the reputation tracks an agent’s work history onchain, so agents without track records—or those with failed or disputed work—should become less attractive to other agents during selection.

OKX’s spokesperson also tied the system to reducing the damage a bad actor can do in a single transaction. For larger projects, escrow held under contract terms is intended to limit the cost of a dispute relative to a scenario where payment occurs upfront and cannot be recovered.

OKX further says it is building additional defense layers beyond reputation, including more sophisticated dispute resolution and an anomaly detection system aimed at coordinated bad-actor behavior. The goal, per OKX, is to strengthen protection as more transaction history accumulates and reputation signals become statistically meaningful.

Who is onboard and what comes next for the beta

OKX says the marketplace launch includes support from companies and ecosystem participants including Amazon Web Services (AWS), AltLayer, CertiK, the Ethereum Foundation, the Solana Foundation, Opentensor Foundation, and StraitsX.

The rollout is explicitly framed as a beta rather than a fully mature network. OKX told Cointelegraph it will remain in beta until it observes “consistent, repeat usage patterns” among users. Early priority categories are expected to include trading, onchain activity, and research tasks, suggesting OKX wants to focus on workflows where agent behavior can be evaluated and where onchain reputation will build quickly.

There is also a wider industry tailwind behind the launch. OKX is entering a space where crypto-native platforms are increasingly experimenting with agentic payments and automation. In earlier Cointelegraph coverage, Coinbase launched a tool on June 12 that allows AI agents to make payments and trade crypto on behalf of users, while MetaMask introduced a self-custodial wallet for AI-powered DeFi trading within user-defined spending and security limits. In January, Nansen launched autonomous crypto trading tools that execute trades via natural language prompts rather than traditional charts or order books.

Cointelegraph also reported that agentic payment activity on Coinbase’s Base network passed 100 million transactions as of June 3, according to Chainalysis—an indicator that machine-to-machine transfers have progressed beyond early prototypes.

As OKX’s marketplace moves through beta, the key question for investors and builders will be whether onchain reputation and escrow-based settlement meaningfully reduce disputes and malicious hiring at scale—especially across the first task categories OKX expects to dominate. Readers should watch for whether “repeat usage patterns” appear as expected, and how OKX evolves its dispute resolution and anomaly detection as more agents and tasks join the network.

A federal judge in New York entered a $5.5 million default judgment against NanoBit Limited and five related defendants over an alleged relationship-investment scam built on a fake crypto trading platform.

The U.S. District Court for the Eastern District of New York ordered $5,518,902 in combined disgorgement, prejudgment interest, and civil penalties on June 16, the U.S. Securities and Exchange Commission (SEC) announced.

The agency alleged that from September 2023 to June 2024, scheme participants posed as financial-industry professionals in WhatsApp groups, built trust with investors, and then directed them to deposit funds into NanoBit.

Although users’ dashboards displayed what appeared to be profitable trades, the SEC alleged the platform never executed any crypto transactions. At least 18 investors lost nearly $1 million in crypto and fiat currency, according to the SEC’s complaint.

Investor funds weren’t used to trade, but rather went to bank accounts in Hong Kong, the SEC said. Participants wired more than $2 million offshore and misappropriated hundreds of thousands of dollars in investors’ crypto assets.

NanoBit also falsely claimed an affiliate, NanobitUS Securities, was SEC-registered and tied to reputable financial firms.

‘I heard my spine and body split’: Pedestrian hospitalised for month with serious injuries after smash with child e-bike rider calls on London Mayor to clamp down on Lime bikes

Builders’ merchants James Burrell weathers construction slump

MetaMask Adds Stablecoin Yield Account With Card Spending

-

Sports7 days ago

Sports7 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics4 days ago

Politics4 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics5 days ago

Politics5 days agoPotential 2028er World Cup attendee leaderboard

-

News Videos2 days ago

News Videos2 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Business4 days ago

Business4 days agoAsia stock markets slide as tech shares slump

-

Tech5 days ago

Tech5 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World13 hours ago

Crypto World13 hours agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Crypto World6 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business7 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World3 days ago

Crypto World3 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports4 days ago

Sports4 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech3 days ago

Tech3 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World4 days ago

Crypto World4 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World4 days ago

Crypto World4 days agoRTX holders must register wallets before token distribution begins

You must be logged in to post a comment Login