Crypto World

Solana firm to support Kazakhstan’s $6B crypto megacity plan

Solana Company has entered a formal partnership aimed at building the blockchain and crypto infrastructure for Alatau City, Kazakhstan’s planned digital-first megacity. The Nasdaq-listed firm signed a memorandum of understanding (MOU) during the Alatau City Roadshow in Shenzhen and Hong Kong in June, according to the report that said the event yielded 30 cooperation agreements with a combined investment potential of more than $6 billion.

Solana Company chairman and CEO Joseph Chee said the parties plan to deepen their relationship and expand Solana’s ecosystem presence across the region. The agreement also adds to Kazakhstan’s growing exposure to Solana-related initiatives, including a Solana Economic Zone launched in Astana last year in cooperation with the Solana Foundation.

Key takeaways

- Solana Company signed an MOU to advise on Alatau City’s blockchain and crypto infrastructure during the June roadshow in Shenzhen and Hong Kong.

- The collaboration is framed around institutional adoption, infrastructure buildout, and Solana-aligned digital asset treasury capabilities.

- Kazakhstan’s earlier Solana Economic Zone in Astana and KASE’s Solana ETF launch help position the country as a recurring focus for Solana-related products and pilots.

- Alatau City remains in early planning, while reported constitutional and on-the-ground infrastructure hurdles raise questions about how quickly the crypto-focused vision can become real.

What Solana Company’s MOU covers

The MOU outlines four areas of cooperation between Solana Company and Alatau City’s authorities: digital asset treasury, blockchain infrastructure, accelerating institutional blockchain adoption, and platform development.

In addition, Alisher Abdykadyrov, CEO of the Alatau City Authority, said Solana Company will take part in creating an Alatau Crypto Cluster—a dedicated pilot zone and special economic area within the future city where crypto is intended to be used for everyday transactions.

Kazakhstan’s expanding Solana footprint

This is not Solana’s first attempt to formalize a presence in Kazakhstan. Last year, Kazakhstan reportedly launched Central Asia’s first Solana Economic Zone in Astana with the Solana Foundation. More recently, the Kazakhstan Stock Exchange (KASE) launched what was described as its first Solana ETF, providing a regulated channel for investors to gain exposure to Solana (SOL) through one of the region’s major exchanges.

Separately, the Solana Foundation also signed an MOU connected to Alatau City—this time specifically to develop blockchain capabilities—during the China roadshow. Taken together, the Solana-linked agreements suggest a multi-layer strategy: create policy and pilot environments, support infrastructure development, and wrap it in investment products that meet local regulatory expectations.

Why Alatau City matters to crypto markets

Megacity pilots have often been positioned as “real-world” testing grounds for blockchain infrastructure—especially where digital identity, payments, and regulated tokenization could be integrated into public services. In Alatau City’s case, the project is being marketed as a comprehensive smart-city build, including AI, digital identity, and blockchain technology from the outset, as noted by the Alatau City Authority during the Solana Summit Kazakhstan 2026, where a deputy CEO discussed the digital-economy concept.

For investors and builders, the question is less about whether a city plan sounds futuristic and more about whether it produces measurable adoption: working infrastructure, enforceable rules for crypto usage, and a path from pilots to scale. The emphasis on a crypto cluster and institutional adoption is particularly relevant because institutional participation tends to require clearer custody, compliance frameworks, and standards for how on-chain assets interact with the traditional financial system.

The project faces regulatory and practical constraints

While Alatau City is still largely in the early development and planning stage, multiple reports point to hurdles that could slow a crypto-forward rollout. In March, The Diplomat reported that Kazakhstan’s National Bank and the Financial Monitoring Agency had raised concerns about constitutional changes needed to support a crypto-based economy.

Other independent coverage has also suggested that day-to-day realities in the area may be lagging behind the megacity vision. Reports indicated residents were dealing with shortages including gas, water, electricity, and internet connectivity, implying the current state of infrastructure may be far from the “fully integrated” smart-city picture.

Cointelegraph reported reaching out to Alatau City for comment, but the underlying uncertainty remains: the next steps will likely depend on regulatory progress, infrastructure buildout, and how the crypto cluster is structured in practice.

Investors and builders watching this story should monitor how the MOU translates into concrete deliverables—such as the rollout timeline for the crypto cluster, regulatory outcomes tied to constitutional or compliance requirements, and whether Kazakhstan’s existing Solana pilots (including the economic zone and KASE ETF access) deepen into broader institutional infrastructure rather than staying limited to announcements.

NEAR Protocol has launched a staking-based payment system for its AI platform, allowing users to access confidential inference and autonomous AI agents by locking NEAR tokens instead of paying with a credit card.

Summary

- NEAR Protocol has launched staking based AI payments that convert locked NEAR into monthly compute credits for AI services.

- Users can access all 43 AI models on NEAR AI without a credit card, while retaining ownership of their staked tokens until they choose to unstake.

- NEAR said the system supports confidential AI inference and always on agents through an onchain staking mechanism.

- The launch adds a new utility for NEAR staking after earlier initiatives including an institutional staking fund and a network upgrade that reduced token inflation.

According to an announcement published by NEAR Protocol on X, the new feature converts staked NEAR into monthly compute credits that can be used across the platform’s artificial intelligence services.

The protocol said users can adjust the amount they stake based on their computing needs, while the underlying tokens remain locked rather than spent and become available again after unstaking.

The rollout covers all 43 AI models currently available through NEAR AI, including models from Anthropic, OpenAI and Google. NEAR Protocol said the mechanism removes the need for a cloud billing account, stored payment credentials or a credit card to access those services.

The protocol described the launch as one of the first production systems to let users pay for confidential AI inference and always-on agents through onchain staking. In its announcement, NEAR said the feature brings together “the NEAR you hold and the AI you run, joined without a card in between.”

NEAR staking converts locked tokens into AI compute credits

Under the new system, users stake NEAR before using AI services, with the amount locked determining how many monthly compute credits they receive. According to NEAR Protocol, larger staking positions generate more compute points, allowing users to scale usage without moving to a different payment model.

Unlike a traditional subscription where funds are spent each billing cycle, the protocol said the staked tokens themselves are not consumed while the service is being used. Users can increase their stake to obtain additional one-time credits, reduce it when usage declines or withdraw their tokens completely by unstaking.

NEAR Protocol said every supported AI model on NEAR AI is available through the staking mechanism, allowing developers and users to switch between providers without changing how they pay for inference or agent hosting.

Describing the design, the protocol said users can “stake the token and it converts into monthly compute credits that scale with the size of your stake,” while the capital “is not spent but staked, and it returns to your wallet when you unstake.”

The company also framed the feature as part of its effort to let users keep control of their assets and credentials while interacting with AI services. According to the announcement, confidential inference and hosted agents can run without requiring users to hand over payment information to third-party platforms.

NEAR ties AI usage to token staking

Alongside the product launch, NEAR Protocol connected the payment model to its long-term view of an AI-driven onchain economy. The protocol argued that if software agents become primary participants in digital markets, the assets securing blockchain networks could also become the assets used to pay for machine-generated work.

According to NEAR Protocol, staking for AI turns the token into a recoverable payment instrument instead of a consumable expense. Rather than purchasing credits that disappear after use, users temporarily lock tokens while accessing computing resources and receive them back after the staking period ends.

The protocol wrote that “staking NEAR equates to AI usage, prepaid in a form you can recover,” adding that the payment process, staking and unstaking all remain onchain throughout the lifecycle.

NEAR also argued that the same token supports two functions at once by helping secure the blockchain while simultaneously paying for AI computation. The company presented that approach as part of what it calls the “agent economy,” where digital assets secure network infrastructure while also facilitating automated economic activity.

AI payments add another use case for NEAR token

Beyond user payments, NEAR Protocol said staking AI fees could influence the network’s token economics because the locked assets remain out of circulation while supporting AI workloads.

According to the protocol, a single AI subscription would have little effect on overall supply, but repeated usage across developers and applications could result in more tokens being committed to active computing instead of remaining freely tradable.

The company said every AI inference request or autonomous agent paid through staking contributes to the same cycle by locking tokens against real network activity rather than speculative trading. NEAR added that the value created through that activity can return to participants securing the network instead of accumulating with centralized service providers.

The announcement stopped short of estimating how much supply could eventually become locked through AI payments and did not provide adoption forecasts.

The latest AI payment feature introduces another role for staking within the NEAR ecosystem by linking token deposits directly to AI computing instead of relying only on validator participation or investment products.

Closing its announcement, NEAR Protocol described the system as an example of “AI sovereignty,” where users can stake tokens, allow private AI agents to run without exposing credentials, and later recover the same tokens after unstaking.

Previous staking initiatives laid groundwork for the launch

The new payment model builds on earlier efforts by NEAR to expand staking beyond conventional validator rewards.

In February 2025, Nomura-backed Laser Digital introduced the Laser Digital NEAR Adoption Fund for institutional investors seeking long-term exposure to the blockchain’s native token. The fund uses TruStake, an institutional staking solution developed by TruFin, allowing participants to earn staking rewards while supporting network consensus.

At the time, Laser Digital Chief Executive Officer Jez Mohideen said the fund combined exposure to artificial intelligence and digital assets with staking income. The product was made available to eligible institutional and professional investors in selected jurisdictions outside the United States.

NEAR also changed its monetary policy later that year. On Oct. 30, 2025, the protocol activated a network upgrade reducing annual token inflation from about 5% to roughly 2.4%, cutting yearly token issuance by nearly 60 million NEAR. The update also lowered expected staking yields from around 9% to approximately 4.5%, assuming roughly half of the circulating supply remained staked.

Quantum Solutions and Hyperscale Data each redirected part of their crypto treasuries toward AI data centers on July 30.

Summary

- 1,000 ETH sale raised $1.9 million for Quantum Solutions’ Japanese AI data center expansion plans.

- 100 BTC were monetized as Hyperscale Data established a Bitcoin-backed credit facility for Michigan construction.

- 4,375 ETH sale ceiling leaves Quantum authorized to dispose of another 2,471 tokens by October.

Tokyo-listed Quantum sold 1,000 ETH for $1.903 million, while U.S.-listed Hyperscale monetized about 100 BTC and established a Bitcoin-backed credit facility.

The transactions show two approaches to using digital assets as operating capital. Quantum converted Ethereum directly into cash. Hyperscale combined a Bitcoin sale with collateralized borrowing to finance its Michigan AI data center.

Quantum Solutions converts ETH into AIDC funding

Quantum’s subsidiary GPT Pals Studio sold 1,000 ETH at $1,903 per token, generating $1.903 million after transaction fees. The company expects to record a $100,970 loss, equal to about ¥17 million, because the sale price was below its May 31 carrying value of $2,003.97 per ETH. The accounting loss is not measured against the original purchase price.

The July transaction followed a June 16 sale of 904 ETH for about $1.61 million. Together, the two disposals raised roughly $3.51 million and reduced Quantum’s balance from 6,668.8 ETH to 4,764.8 ETH, a decline of about 28.6%.

Quantum increased its cumulative sale limit from 1,875 ETH to 4,375 ETH through October 30. The company may therefore sell another 2,471 ETH. However, its filing states that the higher ceiling “does not constitute a decision to immediately sell” the full amount. Future transactions will depend on ETH prices, funding requirements and progress in the AI Infrastructure Data Center business.

Most of Quantum’s remaining ETH is pledged

Of Quantum’s remaining 4,764.8 ETH, 3,050 ETH is pledged as collateral to a Singapore-based financial services company. Another 1,714.8 ETH remains in GPT Pals’ crypto trading account. The company has not identified the lender publicly.

The unused sale authorization exceeds Quantum’s freely held trading-account balance by 756.2 ETH. Selling the full authorized amount would therefore appear to require the release or replacement of some collateral, additional ETH purchases or another arrangement. Quantum has not announced plans to take any of those steps.

The sale also changed Quantum’s position among Japanese corporate Ethereum holders. Def Consulting reported 4,976 ETH on June 30, which is 211.2 ETH more than Quantum’s post-sale balance. Based on the companies’ latest disclosed figures, Quantum no longer appears to be Japan’s largest listed ETH holder, although the balances were reported on different dates.

Ascrypto.news previously reported, Quantum had become the largest Ethereum treasury company outside the U.S. after rapidly accumulating ETH in October 2025. Its latest disposals mark a shift from treasury expansion toward business funding.

In addition, Quantum said the proceeds would support data center contracts, GPU equipment and preparations for its AIDC business. In June, it signed a memorandum of understanding with Hong Kong-based Integrated Capital to examine financing and resource cooperation for a Japanese AI data center.

The proposed infrastructure would focus on systems using NVIDIA B300 and GB300 GPUs. However, the memorandum is nonbinding. Quantum said “specific investment amounts, financing conditions and implementation timing remain undecided.” The ETH sales therefore provide capital flexibility but do not confirm that a completed data center investment has been agreed.

Hyperscale Data monetizes 100 BTC for Michigan

Hyperscale Data separately said it monetized approximately 100 BTC and invested the proceeds into its Michigan AI data center campus. The company also created a Bitcoin-backed facility with an expected variable interest rate of 4.5% to 5%.

The release did not identify the lender, borrowing limit, maturity, collateral ratio or amount of Bitcoin pledged. Hyperscale had reported 1,106.0467 BTC on July 27, valued at about $71.7 million. Subtracting the stated sale would leave roughly 1,006 BTC, but that figure is an estimate because the company has not disclosed a precise post-transaction balance.

Hyperscale is building capacity for a neocloud provider under a definitive master services agreement. The initial deployment covers about 20 megawatts and has a ten-year term with two optional five-year extensions. The company estimates that the maximum term could produce more than $1.2 billion in revenue.

The customer also has an option for another 32 MW. Hyperscale said the expanded arrangement “would be expected” to raise total contract revenue above $3 billion if the capacity and extension options are exercised. Those amounts are conditional forecasts, not revenue already earned.

Crypto treasuries become operating finance tools

The announcements show digital-asset treasuries moving beyond passive holding. Quantum is selling ETH to fund a project that remains at an early stage. Hyperscale is selling and borrowing against Bitcoin to support a data center tied to a signed customer agreement.

The model is spreading across crypto-linked infrastructure companies. In related coverage, Core Scientific sold 2,385 BTC during the first quarter to fund AI capital expenditure. Crypto.news also found that listed miners had secured more than $70 billion in announced AI and high-performance computing contracts while selling Bitcoin to cover development costs.

Quantum’s next deadline is October 30, when its expanded ETH sale authorization expires. The company has promised disclosures if it makes additional sales and expects to recognize the ¥17 million loss in its fiscal second quarter.

Hyperscale said it will issue further construction, financing and operational updates. Investors will be watching for the credit facility’s full terms, an updated Bitcoin balance and evidence that planned Michigan capacity is delivered according to schedule.

Bitcoin Archive renewed a long-running dispute over Bitcoin self-custody on July 31, arguing that poor wallet usability is sometimes defended as cultural gatekeeping rather than treated as a barrier to adoption.

Summary

- Bitcoin Archive criticized self-custody culture, arguing wallet experiences can exclude less technical users from adoption.

- Only 43% of surveyed participants correctly recognized a seed phrase in Carnegie Mellon research findings.

- Bitkey, Ledger and Proton offer different recovery designs aimed at reducing permanent self-custody losses.

The account said a “large contingent” of Bitcoin maximalists “do NOT care about mainstream adoption” and described difficult self-custody experiences as “elitism dressed up as virtue.” Its July 31 post named no individuals, products or organizations and provided no data supporting its claims. It should therefore be read as commentary, not a verified finding about the wider Bitcoin community.

Bitcoin self-custody UX remains the core dispute

Self-custody lets a Bitcoin holder control the private keys needed to move funds. That removes dependence on an exchange or custodian, but it also shifts recovery, backup and transaction-verification duties to the user. A lost backup or exposed recovery phrase can result in permanent loss.

Bitcoin Core’s wallet documentation warns that forgotten passphrases cannot be recovered and that backup files must remain reliable and free from malware. Those instructions show that the usability and responsibility trade-off predates the latest culture debate.

Bitcoin Archive’s criticism focuses on how that responsibility is communicated. Its claim that technical difficulty is intentionally preserved as gatekeeping is disputed and cannot be established from the post alone.

Research supports usability concerns, not motive claims

Academic evidence supports the narrower point that wallet concepts remain difficult for many users. Carnegie Mellon researchers said only 43% of participants correctly identified an image of a seed phrase, while some believed a lost phrase could be reset. The findings pointed to weak mental models that can increase exposure to scams and accidental loss.

A separate CHI study of 24 crypto users found that wallet choices varied by use case, experience and perceived risk. Participants often preferred hardware or smart-contract wallets for larger sums, showing that users balance convenience, phishing exposure, physical risk and dependence on third parties.

A 2026 Scientific Reports paper also described self-custody users as a potential single point of failure and called inadequate recovery a continuing wallet problem.

Separately, the Bitcoin Design guide recommends clear explanations, backup confirmation and recovery testing rather than assuming users already understand key management.

Wallet makers are testing different recovery models

Several products now try to reduce seed-phrase dependence without returning full control to a custodian. Bitkey’s updated recovery documentation describes a two-of-three key design using an app key, hardware key and server key. Any two keys can authorize actions, while the company says its server key cannot move funds alone. Recovery Contacts can also help restore access without receiving the wallet’s keys.

Ledger offers several options, including a PIN-protected physical Recovery Key and the optional Ledger Recover subscription. Ledger says Recover encrypts and splits backup material among three providers, with identity checks used during restoration.

Proton Wallet takes another approach by simplifying transfers through email addresses while retaining a standard wallet seed phrase. These are company-described models, and each introduces different privacy, availability and trust considerations.

Security failures keep the trade-off unresolved

Easier recovery does not remove the need for secure wallet generation and user education. In related coverage, crypto.news reported that the Ill Bloom weakness exposed wallets created with poor randomness across several blockchains.

Crypto.news also reported on physical phishing letters designed to trick Ledger and Trezor users into revealing recovery phrases. These cases show that improving the interface cannot fully remove weak randomness, social engineering or backup exposure.

Self-custody removes the risk that an exchange freezes withdrawals, fails or mismanages customer assets. It does not remove phishing, device compromise, backup loss or inheritance problems. As crypto.news explained in its self-custody guide, control and responsibility arrive together.

What happens next will depend on measurable product work rather than social-media arguments. Wallet developers can publish audits, test recovery flows with nontechnical users, support interoperable backups and report failure rates. Bitcoin Archive’s broader allegation about maximalist culture remains opinion, but the underlying usability challenge is documented and actively being addressed.

KSNet has partnered with the Solana Foundation to test blockchain payments and AI-driven transaction systems for South Korea’s financial market.

Summary

- KSNet and the Solana Foundation signed an agreement to test blockchain based payment infrastructure in South Korea.

- The companies will begin proof of concept projects covering Solana Pay integration and AI payments using the x402 protocol.

- KSNet plans to connect Solana Pay with its merchant network while incorporating AML controls and won settlement support.

- The partnership adds to Solana’s recent enterprise payment initiatives across stablecoins, AI services, and regulated financial infrastructure.

KSNet announced on July 30 that it has signed a memorandum of understanding (MOU) with the Solana Foundation to jointly develop a next-generation digital asset payment infrastructure, with the partnership beginning through proof-of-concept projects focused on Solana Pay and AI-powered payment technology.

The agreement brings together KSNet’s domestic payment network and Solana’s blockchain infrastructure as both companies evaluate digital asset payments that can work alongside South Korea’s existing financial system. The first phase centers on technical verification rather than a commercial rollout.

Solana Pay will be tested on KSNet’s merchant network

As part of the first proof-of-concept, KSNet said it will test the integration of Solana Pay with the online and offline merchant payment network the company has built over the past 26 years. The demonstration will examine whether Solana Pay’s payment standard can operate within South Korea’s existing payment environment while remaining compatible with local merchant infrastructure.

The companies also said compliance requirements will form part of the testing process. KSNet plans to incorporate anti-money laundering (AML) controls into the payment system to prevent abnormal fund flows before any commercial deployment is considered.

In addition, the proof-of-concept will connect blockchain-based settlements with KSNet’s existing won settlement network. According to the company, the structure is intended to comply with domestic financial guidelines while reducing exchange-rate fluctuations and liquidity risks that can arise during digital asset settlements.

Rather than replacing traditional payment rails, the companies are testing how blockchain payments can operate alongside existing financial infrastructure under domestic regulatory requirements.

AI payment model will use the x402 protocol

A second proof-of-concept under the agreement focuses on artificial intelligence payments using the x402 protocol.

KSNet said it will evaluate the protocol by integrating it into an AI-based payment system that is already undergoing internal testing. The review will determine whether the technology is suitable for future payment services that rely on autonomous software agents.

The x402 protocol uses the HTTP 402 “Payment Required” status code, allowing AI agents to make small payments automatically when accessing APIs or paid online services without relying on conventional logins or credit card authentication.

According to the companies, machine-to-machine payment models require transactions to settle quickly while keeping processing costs low. Existing card payment systems have long faced cost challenges when handling very small payments because multiple intermediaries contribute to the overall fee structure.

The proof-of-concept will therefore examine whether blockchain infrastructure can support those payment models more efficiently while remaining compatible with existing financial systems.

Park Han-han, chief executive officer of KSNet, said the company plans to build on its payment and settlement experience to provide what it described as a secure payment infrastructure for users.

Following the technical validation, KSNet and the Solana Foundation said they intend to gradually explore commercialization models suitable for South Korea’s financial market.

Solana has continued expanding payment partnerships

The KSNet partnership adds another enterprise payments initiative to the Solana Foundation’s recent activities across financial services.

Earlier this month, the Solana Foundation partnered with SBI Holdings to establish SBI Solana Global, a venture focused on regulated on-chain financial infrastructure in Japan. According to the companies, the initiative includes work on yen-backed stablecoins, tokenized financial products, institutional settlement services, cross-border payments, and AI-related payment applications.

South Korea has also become part of Solana’s payment strategy. In April, Shinhan Card announced a proof-of-concept with the Solana Foundation to test stablecoin payments on Solana’s testnet. According to Shinhan Card, the pilot evaluates transaction performance, non-custodial wallet security, and blockchain payment infrastructure while examining hybrid financial services that combine conventional payment systems with decentralized finance.

Artificial intelligence has become another area of development for the blockchain network. Earlier this month, the Solana Foundation and Google Cloud introduced Pay.sh, a payment gateway that allows AI agents to purchase API access using stablecoins on Solana. According to the companies, the platform enables per-request payments for Google Cloud services, including Gemini, BigQuery, and Vertex AI, without requiring traditional API subscriptions.

Enterprise adoption has also extended into corporate finance. On July 22, Ramp launched Solana-powered stablecoin accounts that allow businesses to hold USDC and USDT, manage treasury balances, and make cross-border payments through a single financial workflow. Ramp said more than 70% of stablecoin payment volume on its platform occurs outside traditional banking hours, indicating continued demand for around-the-clock settlement.

Consumer payment products have also incorporated Solana’s infrastructure. Last year, Gemini introduced a Solana Edition credit card that automatically stakes SOL rewards earned from purchases, allowing users to participate in network validation while earning staking rewards through Gemini’s platform.

The launch followed the exchange’s addition of USDC and USDT transfers on Solana, which Gemini said benefited from the network’s low fees and fast settlement times.

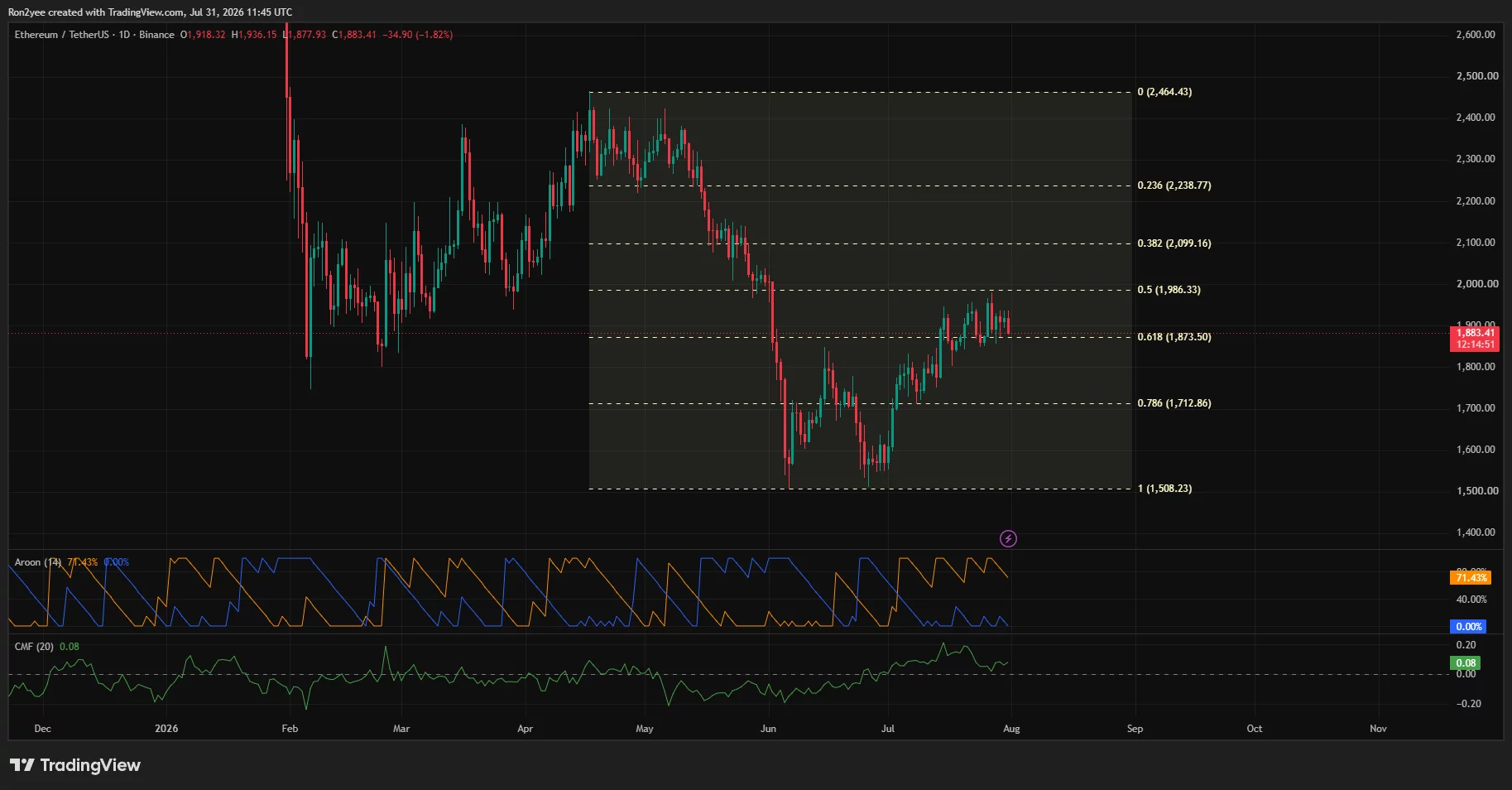

Ethereum price fell nearly 2% to about $1,883 on July 31 after another rejection below $2,000 weakened momentum and pushed the token toward a key technical support zone.

Summary

- Ethereum price traded near $1,883, down 1.8% on the daily chart.

- The 4-hour RSI dropped to 43.02, showing weakening short-term momentum.

- Support sits near $1,873–$1,875, with deeper liquidity around $1,850.

- Liquidation clusters near $1,935–$1,940 could attract price during a recovery.

Ethereum price action today

According to data from crypto.news, Ethereum (ETH) price extended its retreat on Thursday after buyers failed to sustain a move toward the $2,000 psychological level.

The token traded at approximately $1,883 at the time of the charts, down 1.82% on the day. ETH reached an intraday high of $1,936 before falling to a low near $1,878, showing that sellers remained active above $1,900.

Price action on the 4-hour chart shows Ethereum breaking below the middle Bollinger Band at $1,906. The move placed ETH close to the lower band at $1,875, where buyers may attempt to stabilize the decline.

Short-term momentum has also deteriorated. The 4-hour Relative Strength Index fell to 43.02, below its moving average of 50.13. An RSI below 50 generally indicates that sellers have gained control, although the reading remains above the oversold threshold of 30.

Ethereum’s retreat follows several failed attempts to establish support above $1,930. Each rebound produced renewed selling, leaving the token inside a broader consolidation range instead of confirming a breakout.

What is driving the ETH decline?

Profit-taking near $1,950 and the continued defense of $2,000 appear to be the immediate technical drivers behind the decline.

The $2,000 level also sits close to the 50% Fibonacci retracement at $1,986.33 on the daily chart. That overlap has created a wider resistance zone where short-term traders may be closing positions rather than adding exposure.

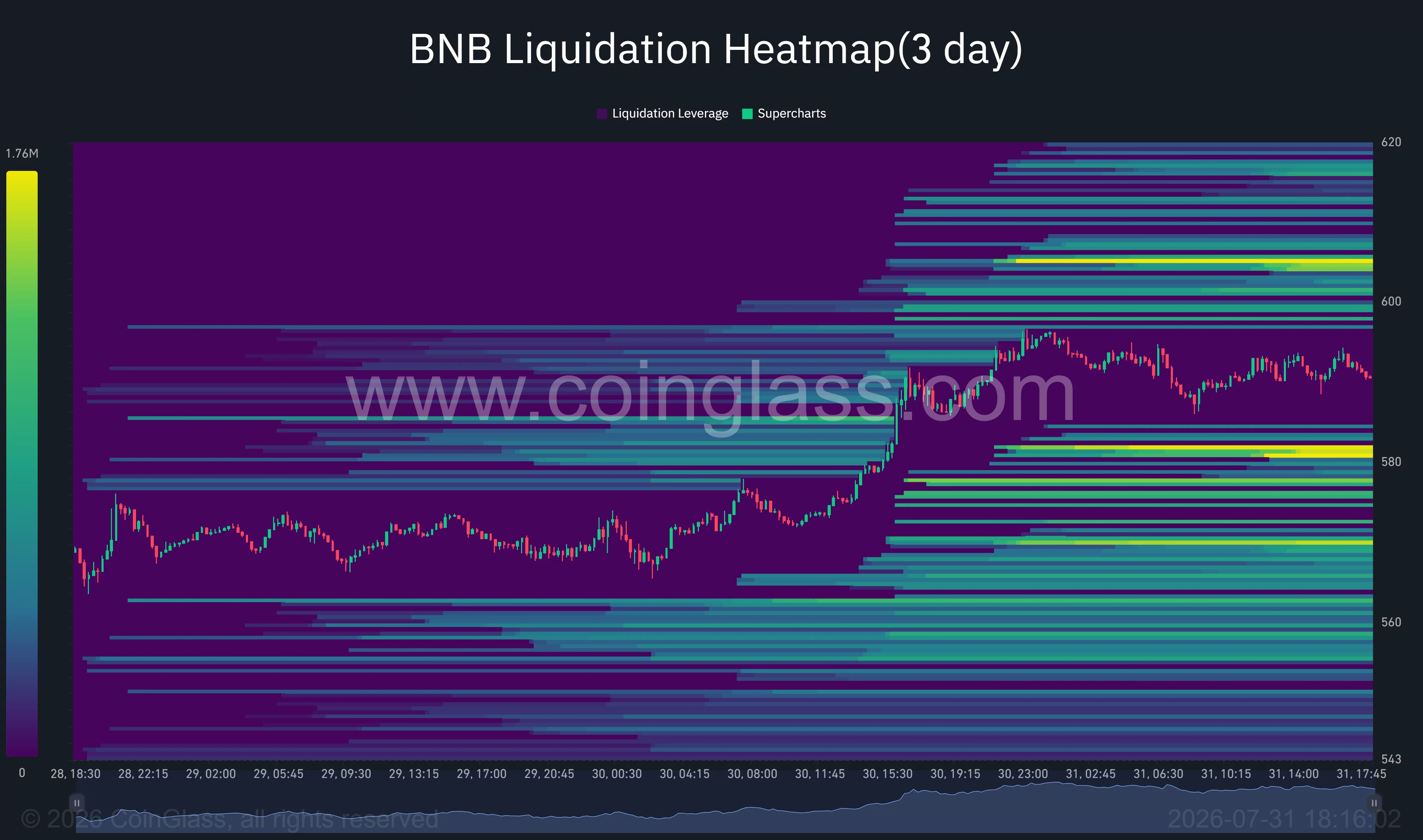

Derivatives positioning likely amplified the pullback. The 3-day CoinGlass liquidation heatmap shows that ETH dropped sharply after trading around $1,920, passing through liquidity near $1,900 before reaching the upper $1,880s.

Leveraged traders who positioned for an immediate breakout above $2,000 faced pressure as the price moved in the opposite direction. Forced long closures can accelerate a decline because exchanges sell the underlying position when margin requirements are no longer met.

Broader conditions remain challenging for risk assets. The Federal Reserve’s decision to maintain elevated interest rates has kept financing conditions restrictive for US investors, while geopolitical uncertainty in the Middle East has supported a more defensive market posture.

Ethereum has also lacked the sustained spot demand needed to separate from those macro pressures. Weak on-chain activity and redemptions from spot Ethereum exchange-traded products have reduced two potential sources of buying support.

Ethereum support at $1,873 faces a test

Ethereum is now testing an important technical area between $1,873 and $1,875.

The daily chart places the 0.618 Fibonacci retracement at $1,873.50, while the 4-hour lower Bollinger Band stands at $1,875.19. The convergence makes this range the first level bulls need to defend.

A daily close below $1,873 would weaken the recovery structure that developed from the late-June low. The liquidation heatmap points to additional liquidity between approximately $1,850 and $1,870, making that area the next potential downside target.

Below $1,850, attention would shift toward $1,800. Losing that psychological support could expose the 0.786 Fibonacci retracement at $1,712.86, although ETH would need a much deeper correction to test that level.

Some longer-term indicators remain constructive. Chaikin Money Flow stood at 0.08 on the daily chart, suggesting capital flows were still marginally positive despite the price decline. The Aroon readings also showed Aroon Up at 71.43 and Aroon Down at zero, indicating that the broader July recovery had not been fully invalidated.

Those signals contrast with the weaker 4-hour RSI, showing a market in which the medium-term recovery remains intact but near-term momentum favors sellers.

Liquidation heatmap points to $1,940 resistance

The largest nearby concentration of liquidation leverage sits around $1,935–$1,940, according to the 3-day heatmap.

That cluster could act as a price magnet if Ethereum rebounds from current support. A recovery above $1,906, the middle Bollinger Band, would be the first indication that short-term momentum is improving.

ETH would then face resistance at $1,938, which marks the upper Bollinger Band and overlaps with the main liquidation pocket. Clearing that area could open another test of $1,986 and $2,000.

Additional liquidity appears near $1,950–$1,965 and immediately below $2,000. These clusters could fuel a short squeeze if buyers reclaim $1,940, but they may also attract fresh selling as traders defend the wider resistance zone.

Failure to recover $1,900 would keep the downside scenario active. In that case, leveraged positions accumulated around $1,875 and $1,850 could become vulnerable.

What analysts are saying about Ethereum

Crypto analyst Michaël van de Poppe described the current decline as a lower-timeframe correction while maintaining a positive longer-term view.

“ETH is holding above $1,800 and as long as that’s the case, there’s not much to worry,” van de Poppe said. He added that he still expects Ethereum to reach $2,500 in the coming months.

Analyst Ted Pillows identified a narrower support range. He said momentum was weakening after ETH fell below $1,900 but noted that the token remained above its $1,850 support zone.

“As long as it holds, I think ETH is more likely to rally towards $2,000.”

The charts therefore place Ethereum at a decision point. Holding $1,873–$1,850 would preserve the possibility of another move toward $1,940 and $2,000. A sustained breakdown below that range would instead reinforce the rejection and raise the risk of a deeper pullback toward $1,800.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

The state is seeking at least $36 billion in damages from the prediction market platform it calls an unlicensed gambling operation, and has filed for a temporary restraining order to halt its contracts immediately.

Summary

- New York Attorney General Letitia James and Governor Kathy Hochul sued KalshiEX on July 31, 2026, in New York Supreme Court, Manhattan, seeking at least $36 billion in compensatory damages, triple-gains penalties, and $100,000 per unauthorized sports wagering offer.

- The state simultaneously filed a motion for a temporary restraining order to halt Kalshi’s event contracts in New York immediately, citing ongoing harm to consumers including users under the legal gambling age of 21.

- Kalshi users bet over $1 billion monthly on the platform in 2025, with 90% of that volume on sports, according to figures cited in the AG’s own release, a concentration that makes the bipartisan Senate proposal to ban sports event contracts existential for the business.

- Kalshi, valued at roughly $22 billion with annualized volume of approximately $178 billion, calls the suit “political theater” and argues its CFTC registration as a designated contract market means exclusive federal oversight.

- A bipartisan coalition of 38 state attorneys general has already filed an amicus brief supporting Massachusetts in a parallel case, signaling that the enforcement wave extends far beyond the 13 states with active litigation.

The lawsuit that prediction markets knew was coming

Two days after the Second Circuit denied Kalshi emergency relief on July 29, New York filed the most aggressive state action yet against the prediction market industry. The suit arrived with a coordinated announcement from AG James and Governor Hochul, counts spanning multiple bodies of state law, a $36 billion damages demand, and a motion for an immediate restraining order.

The $36 billion figure, reported by The Block based on the court filings, is roughly 1.6 times Kalshi’s reported valuation. It is the number every major outlet is leading with, and it signals that New York is treating this as a revenue-extraction case, not merely a cease-and-desist.

This piece examines the filing, the legal arguments on both sides, the federal regulator caught between them, and what the case means for an industry now fighting a war on two fronts: in courtrooms and in Congress.

What the complaint actually alleges

The core claim is straightforward: Kalshi is running an unlicensed gambling business in New York.

The AG’s office says the platform lets users place wagers on uncertain future events, from Super Bowl outcomes to reality TV winners to election results, without a Gaming Commission license and without paying state gaming taxes. New York treats these as bets, not derivatives, regardless of Kalshi’s CFTC registration.

The complaint goes further. It alleges Kalshi allows users aged 18 to 20 to place bets, violating New York’s 21-and-older minimum for mobile sports betting. It alleges the platform offered wagers on games involving New York college teams, a separate violation under state law.

The AG’s investigators placed test wagers from New York accounts as evidence: four “Yes” contracts on a UConn-Michigan basketball game at $1.14 in April 2026, and ten contracts on the winner of “Big Brother” in July 2026. Both transactions completed without obstruction.

The filing also introduces a count under the federal Interstate Wire Act, alleging Kalshi used wire communications to transmit bets across state lines. This is significant because it widens the legal exposure beyond state gambling statutes into federal criminal law, giving the state an argument that operates independently of the preemption question. Even if Kalshi’s CFTC registration were found to preempt state gambling law, the Wire Act is a federal statute, and the state is arguing that Kalshi violates it.

The complaint details the investigative methods in unusual specificity. Rather than relying on industry reports or third-party data, the OAG built its case from the inside. Investigators created accounts, placed real wagers, and documented each step. This matters for the TRO motion: the state can present firsthand evidence that illegal gambling is actively occurring in New York, not merely that it could occur.

“Prediction markets like Kalshi are gambling platforms, plain and simple,” James said in a statement accompanying the filing.

Governor Hochul framed the action around consumer protection, saying Kalshi “has chosen to ignore New York’s gaming laws, which exist to protect consumers, prevent problematic gambling, deliver funding for critical public services, and ensure that every company plays by the same rules.” The coordinated announcement from both the AG and the Governor signals that this is not a routine regulatory action. It is a political priority.

The $36 billion in damages and the TRO

New York is not seeking a slap on the wrist. The headline number is at least $36 billion in compensatory damages, pending a full accounting of Kalshi’s operations. The remedies demand:

- A permanent injunction barring Kalshi from operating unlicensed gambling in the state

- A temporary restraining order halting Kalshi’s event contracts in New York immediately

- A full accounting of every customer bet and loss processed through the platform

- Forfeiture and disgorgement of all gains the state deems illegal

- Restitution to affected consumers

- Penalties of three times Kalshi’s gains under Penal Law Section 80.10

- A fine of $100,000 per unauthorized sports wagering offer under the Racing Law

The TRO is the near-term threat. If granted, Kalshi would need to suspend operations in New York while the case proceeds, potentially for years. The triple-damages provision is the long-term one. At $36 billion, New York is claiming a figure that exceeds the platform’s reported valuation of $22 billion by more than 60%.

The per-offer fine structure adds another layer. The AG’s release notes that Kalshi users bet over $1 billion monthly in 2025, with 90% of that volume on sports. Each unauthorized sports offering carries a $100,000 fine under the Racing Law. At that volume, the per-offer penalties alone could produce a figure in the hundreds of millions.

The damages calculation itself reveals the state’s theory of the case. New York is not treating Kalshi as a minor regulatory violator that failed to file paperwork. It is treating Kalshi as a gambling operation that processed billions in unlicensed wagers over multiple years, and it wants the full economic benefit of that activity returned. The $36 billion figure presumably reflects the total volume of wagers placed by New York users, or a substantial fraction of it, multiplied by the treble-damages provision. The final number will depend on the full accounting the state is requesting, but the opening demand is meant to establish the scale of the alleged violation.

The TRO motion deserves separate attention because it operates on a different timeline from the main case. A TRO hearing can happen within days or weeks, while the underlying lawsuit could take years. If New York secures the restraining order, Kalshi faces an immediate operational decision: comply and lose the New York market, or challenge the order and risk contempt proceedings. Either outcome sets a precedent that other states can follow. Michigan and Nevada secured their own TROs through similar procedural mechanisms, and each one reduced Kalshi’s geographic footprint.

The $1 billion monthly number and why it matters

The AG’s release includes a figure that has received less attention than the $36 billion headline: Kalshi users bet over $1 billion every month on the platform in 2025, and 90% of that money went to sports betting.

This is the number that makes the bipartisan Senate proposal to ban CFTC-licensed platforms from offering sports event contracts existential. Sports are not a side product for Kalshi. They are the product. If sports contracts are removed, whether by state enforcement or federal legislation, the platform loses nine-tenths of its recorded consumer activity.

The figure also undercuts Kalshi’s framing of its offerings as sophisticated financial derivatives. A billion dollars a month on the Super Bowl, the NBA, and college basketball looks like a sportsbook by any name. New York is making exactly that argument, and the AG’s investigators have the receipts.

The concentration matters for investors and market participants as well. Kalshi’s $22 billion valuation implies a diversified event-contract platform serving a range of use cases: elections, weather, economics, entertainment. The AG’s data shows something closer to a sports gambling platform with a derivatives label. If the valuation was underwritten on the assumption of product diversity, the 90% sports concentration represents a disclosure risk independent of the legal outcome.

Kalshi’s federal preemption defense

Kalshi’s position rests on a single legal premise: that its 2020 registration with the CFTC as a designated contract market means its event contracts are regulated derivatives under the Commodity Exchange Act, subject to exclusive federal oversight.

The company calls the suit “political theater” and argues states cannot simply shut down a federally licensed exchange. The framing is deliberate. Kalshi wants this treated as a jurisdictional question, not a gambling question.

It is the strongest version of their argument, and it carries legal weight. The CFTC itself has backed the position, filing lawsuits against multiple states and claiming exclusive regulatory authority over prediction markets. On the same day New York filed its suit, the CFTC filed an emergency counter-motion in Manhattan federal court less than one hour before the state complaint dropped, attempting to reassert federal jurisdiction preemptively.

The federal regulator has now challenged state enforcement in at least nine states, including filing suit against Arizona, Connecticut, and Illinois in April 2026. The CFTC is not a passive bystander in this dispute. It is an active combatant on Kalshi’s side.

Why the federal shield is cracking

On July 7, U.S. District Judge Analisa Torres denied Kalshi’s preliminary injunction against New York’s Gaming Commission enforcement. Her reasoning cut directly at the preemption argument.

Torres cited Section 2 of the Commodity Exchange Act, which states the law “shall not supersede or limit the jurisdiction conferred on other regulatory authorities under the laws of the United States or of any state.” She wrote that “Congress did not intend to regulate so broadly as to exclude all state gambling laws from regulating transactions involving swaps.”

Her conclusion was blunt: “There is nothing preventing Kalshi from obtaining a license pursuant to New York law.”

The Second Circuit denied Kalshi emergency relief on July 29. With the appellate safety net gone, the state had a clear path to file.

The Torres ruling matters beyond New York because it provides a template. Other states facing Kalshi’s preemption argument can cite it directly. The decision rejects the premise that CFTC registration creates a blanket exemption from state gambling law, and it does so by citing the Commodity Exchange Act’s own text. Before Torres, Kalshi could argue that no court had squarely addressed the question. That argument is gone.

The legal logic is worth following in detail. Kalshi’s preemption claim rests on the idea that CFTC registration means its products are regulated derivatives, full stop. Torres responded that the Commodity Exchange Act explicitly preserves state jurisdiction, that the products in question resemble gambling under New York law, and that nothing in federal statute prevents Kalshi from obtaining a state gaming license if it wants to operate in New York. The decision does not say Kalshi cannot exist. It says Kalshi cannot avoid state gambling law by pointing to a federal license that, by its own statute’s terms, was never meant to override it.

The Second Circuit’s refusal to grant emergency relief on July 29 reinforced this reasoning. It did not issue a full opinion, but the denial means Kalshi failed to show a likelihood of success on the merits, which is the standard for emergency relief. Two levels of federal courts have now declined to protect the company from state enforcement.

The result is a genuine constitutional question about the boundary between federal commodity regulation and state gambling law. Kalshi needs either a circuit court reversal or Congressional action to restore the shield it thought it had.

The 38-state coalition

The count that matters is not 13 states with active litigation. It is 38.

In April 2026, James joined a bipartisan coalition of 38 state attorneys general filing an amicus brief supporting Massachusetts in its parallel case against Kalshi. The coalition spans from Alabama to Wisconsin, including red states, blue states, and the District of Columbia. The full list: Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware, Hawaii, Idaho, Illinois, Iowa, Kansas, Louisiana, Maine, Maryland, Michigan, Minnesota, Mississippi, Nebraska, Nevada, New Jersey, New Mexico, New York, North Carolina, Ohio, Oklahoma, Oregon, Pennsylvania, Rhode Island, South Carolina, South Dakota, Tennessee, Utah, Vermont, Virginia, Wisconsin, and DC.

On the same day the AGs filed, the CFTC filed its own amicus brief at the Massachusetts Supreme Judicial Court asserting exclusive federal jurisdiction, creating a direct confrontation between the federal regulator and a supermajority of state enforcement agencies.

New York is not operating in isolation. The suit fits into a pattern of escalating state enforcement that has accelerated through 2026:

Massachusetts has a court order restricting Kalshi. Polymarket has countersued the state, opening a second front.

Michigan secured a temporary restraining order against the platform under AG Dana Nessel, making it the third state to obtain a court order.

Nevada issued a TRO covering sports, election, and entertainment contracts. Kalshi responded by removing those categories for Nevada users, effectively conceding the state’s authority in practice while contesting it in court.

Washington holds its own court order restricting the platform. The state’s Gambling Commission issued a cease-and-desist, and Kalshi did not challenge it in court.

Wisconsin handed down an adverse ruling the week of July 28, adding another state to the enforcement column in a decision that received less coverage than the New York and Massachusetts actions but follows the same legal reasoning.

New York itself previously sued Coinbase and Gemini in April 2026 on similar prediction-market allegations. That suit broadened the target set beyond pure-play prediction platforms, signaling that New York views any company offering prediction-style products to state residents as subject to gaming law, regardless of whether the company’s primary business is elsewhere.

In Congress, a bipartisan Senate proposal has emerged that would ban CFTC-licensed prediction market platforms from offering sports event contracts, which would remove the category that accounts for 90% of Kalshi’s recorded volume.

The arithmetic that matters

Kalshi’s reported valuation of $22 billion rests on the assumption that its CFTC registration provides a durable regulatory moat. The annualized transaction volume of $178 billion flows through that assumption. If the federal preemption argument fails at the circuit level, the business model does not downgrade gracefully.

The platform cannot operate as a state-licensed gambling business without fundamental changes to its product, its economics, and its user base. State gaming licenses come with specific requirements: age floors (21 in New York for mobile betting), tax obligations, product restrictions, and compliance infrastructure that a CFTC-registered exchange was never built to support.

Nevada’s example is instructive. When the state issued its TRO, Kalshi did not fight to keep sports, election, and entertainment contracts available to Nevada users. It removed them. If that pattern repeats across additional states, the platform’s addressable market contracts with each new enforcement action.

The numbers tell the story in three layers. First, $36 billion in damages sought in New York alone, exceeding the company’s valuation by 60%. Second, 38 state attorneys general aligned against the federal preemption argument, representing a supermajority of American enforcement capacity. Third, 90% of Kalshi’s monthly volume concentrated in sports, the single category most vulnerable to both state enforcement and the pending Senate ban.

The counter-argument deserves its strongest form. Kalshi’s $178 billion in annualized volume proves genuine consumer demand for event contracts. The CFTC registration is not a legal fiction, and federal regulators are actively fighting to preserve federal jurisdiction. The Commodity Exchange Act does grant the CFTC authority over designated contract markets, and a reasonable reading of federal preemption could conclude that state gambling law should not apply to products traded on a federally licensed exchange. If the CFTC prevails at the appellate level, or if Congress acts to clarify federal preemption, the state cases collapse. Kalshi’s appeal of the Torres ruling remains live, and the Second Circuit has not yet ruled on the merits.

There is also a policy argument that Kalshi rarely makes explicitly but that supports its position. Prediction markets have informational value. Research from academic institutions and the CFTC’s own prior statements have recognized that event contracts can produce useful price signals about future events. A state-by-state licensing regime could effectively kill a market structure that regulators, academics, and the public have found valuable for forecasting elections, economic indicators, and policy outcomes.

But the burden has shifted. Two federal courts have declined to protect Kalshi from state enforcement. Thirty-eight attorneys general have aligned against the federal preemption argument. And 90% of Kalshi’s volume is concentrated in sports, the single category most politically vulnerable. The question is no longer whether states can regulate prediction markets. The question is whether Kalshi can find a court that says they cannot.

What to watch

- The TRO hearing in New York Supreme Court. If granted, Kalshi must suspend operations in the state while the case proceeds. The timeline and conditions of this hearing will set the pace for the entire case.

- The Second Circuit appeal of Judge Torres’s July 7 ruling. If the court reverses on federal preemption, the state enforcement wave stalls. If it affirms, expect additional state filings within weeks.

- The CFTC’s emergency motion filed hours before New York’s suit. The federal court’s handling of this motion will signal whether the judiciary treats CFTC registration as a meaningful shield or a regulatory label.

- Congressional action on the bipartisan Senate proposal to ban sports event contracts. At 90% of Kalshi’s volume, this would be a structural blow regardless of court outcomes.

- Kalshi’s operational response in states with active enforcement. Nevada’s pattern, removal of categories rather than legal confrontation, is the leading indicator of how the business adapts under pressure.

Frequently asked questions

What did New York sue Kalshi for?

New York filed a lawsuit alleging Kalshi operates an unlicensed gambling business by offering wagers on sports, entertainment, and election outcomes without a Gaming Commission license and without paying state gaming taxes. The suit includes counts under the state constitution, Penal Law gambling provisions, the Racing Law, and the federal Interstate Wire Act.

How much is New York seeking in damages?

The state is seeking at least $36 billion in compensatory damages, pending a full accounting of Kalshi’s operations. Additional penalties include three times the company’s gains under Penal Law and $100,000 per unauthorized sports wagering offer under the Racing Law.

What is the temporary restraining order?

Alongside the lawsuit, New York filed a motion for a TRO to halt Kalshi’s event contracts in the state immediately while the case proceeds. If granted, Kalshi would need to suspend operations in New York, potentially for years.

What is Kalshi’s defense?

Kalshi argues that its registration with the CFTC as a designated contract market since 2020 means its event contracts fall under exclusive federal oversight and that states cannot regulate them as gambling. The company calls the suit “political theater.”

How did the court rule on federal preemption?

U.S. District Judge Analisa Torres denied Kalshi’s preliminary injunction on July 7, ruling that the Commodity Exchange Act does not prevent states from applying their gambling laws to event contracts. The Second Circuit denied emergency relief on July 29.

How many states are aligned against Kalshi?

A bipartisan coalition of 38 state attorneys general filed an amicus brief supporting Massachusetts in a parallel case. At least five states, Massachusetts, Michigan, Nevada, Washington, and Wisconsin, have active court orders or adverse rulings restricting Kalshi’s operations.

What role is the CFTC playing?

The CFTC has positioned itself as the exclusive federal regulator of prediction markets, filing lawsuits against multiple states and an emergency motion less than one hour before New York’s suit. The agency has challenged state enforcement in at least nine states and filed an amicus brief directly opposing the 38-state attorney general coalition.

Could this lawsuit shut down prediction markets entirely?

The New York case alone would not end the industry, but it tests whether CFTC registration shields platforms from state gambling laws. With 38 attorneys general aligned against the federal preemption argument and 90% of Kalshi’s volume concentrated in sports betting, the combination of state enforcement and the pending Senate ban on sports event contracts could force a fundamental restructuring of the business model. This is educational analysis, not investment advice.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or investment advice. The information presented reflects the state of events as of July 31, 2026, and may change as legal proceedings develop. Readers should consult qualified professionals before making decisions based on this material.

Banca d’Italia has released a July 2026 study finding that stablecoin remittances do not consistently beat traditional transfer services on cost or speed.

Summary

- Ten USDC corridors produced total remittance costs ranging from 0.30% to nearly 9%, researchers found.

- Under 20 minutes was achievable where instant payment systems supported both fiat conversion endpoints efficiently.

- Three corridors beat Wise, while four cost more, showing stablecoin savings remained highly corridor-specific overall.

Researchers executed real transfers of 200 USDC across ten corridors linking Italy with Argentina, Brazil, South Africa, the United Arab Emirates and Japan.

The mystery-shopping study recorded total costs from 0.30% to almost 9%. The blockchain leg averaged only 0.4%, while exchange purchases, funding methods, withdrawals and foreign-exchange conversion produced most of the expense. The authors said stablecoins showed “no systematic cost advantage” over traditional channels.

Stablecoin remittance costs varied sharply by corridor

The Italy-to-Argentina transfer was the cheapest at 0.30%, while Argentina-to-Italy cost 8.96%. The study warned that the low outbound Argentina result partly reflected differences between the country’s official and market exchange rates, rather than blockchain efficiency alone.

Brazil-to-Italy cost 2.21%, compared with 2.70% in the opposite direction. South Africa-to-Italy cost 5.44%, while Italy-to-South Africa reached 4.58%. The two UAE routes were among the most expensive at 7.20% and 8.95%, partly because card funding and withdrawal charges increased the total.

USDC beat Wise in only three comparable routes

Banca d’Italia compared its transactions with Wise simulations for the same $200 amount. USDC was cheaper in three routes: Italy to Argentina, Italy to South Africa and Brazil to Italy. It was more expensive in four, including both UAE routes and Italy to Brazil.

The researchers cautioned that the transfers and Wise simulations occurred on different dates. They also described the World Bank comparison as an indicative benchmark rather than a like-for-like test. The paper covers one stablecoin and a limited number of transactions, so its findings “cannot be readily generalized” to every provider or corridor.

Fast domestic payments determined transfer speed

The onchain portion took less than 15 minutes in seven of eight directly comparable corridors. However, complete settlement depended on the banking systems used to fund exchanges and withdraw local currency.

Transfers involving Italy’s TIPS, Brazil’s Pix and Argentina’s Transferencias 3.0 finished in under 20 minutes. South African routes took one or two business days because standard bank transfers slowed the fiat endpoints. The study therefore found that stablecoin rails and domestic instant-payment systems worked as complements, not substitutes.

Japan presented a separate problem. The Japan-to-Italy transfer cost 1.6%, but regulatory limits required an unhosted wallet and fragmented transactions, making the process unsuitable for a direct timing comparison. The reverse route cost 1.3% without completing the final off-ramp.

Better on-ramps may matter more than cheaper blockchains

The findings support Banca d’Italia Governor Fabio Panetta’s May assessment that stablecoins may work in selected corridors but do not provide a universal answer to expensive remittances. He argued that regulators should improve domestic payment infrastructure and connect fast-payment systems across borders.

A March 2026 BIS paper reached a related conclusion, identifying weak interoperability, fragmented standards and institutional differences as the main barriers to cheaper cross-border payments. That suggests blockchain settlement alone cannot remove compliance, banking and local-currency bottlenecks.

Industry deployments continue to test the other side of the argument. As crypto.news reported, Borderless.xyz found competitive stablecoin pricing across 260 business-payment corridors during the second quarter. In related coverage, a Hyundai trial moved $20,000 between the U.S. and Mexico in about seven minutes, while SBI Remit partnered with Fasset to develop stablecoin remittance infrastructure.

Those cases do not directly contradict the central-bank experiment. They involve different transfer sizes, business models and endpoints. The next step is broader testing across more tokens, providers, dates and transaction amounts, with full disclosure of exchange spreads, withdrawal costs and local payout times.

The largest corporate bitcoin holder now sits $9 billion underwater on 843,775 coins, has sold bitcoin for the first time in four years, and is funding preferred dividends from the asset it promised never to sell.

Summary

- Strategy reported an $8.22 billion net loss for Q2 2026, driven almost entirely by an $8.32 billion unrealized markdown on its bitcoin holdings under fair-value accounting, swinging from a $10.02 billion profit in Q2 2025.

- The company holds 843,775 bitcoin purchased at an average of $75,476 per coin, now worth roughly $54.8 billion against a $63.7 billion acquisition cost, a gap of approximately $9 billion.

- Strategy sold bitcoin for the first time in four years, disposing of 3,588 coins for $218.4 million to fund preferred stock dividends, and has authorized a program allowing up to $1.25 billion in future sales.

- The capital structure has shifted toward preferred equity, with $14.4 billion in preferred stock outstanding, annual dividend obligations approaching $1.2 billion, and cash reserves of $3.75 billion covering roughly 2.1 years of payments.

- MSTR shares declined 0.67% in after-hours trading, a muted reaction that reflects how thoroughly the market has internalized Strategy as a leveraged bitcoin proxy rather than a software company.

The Q2 numbers in context

Strategy’s Q2 2026 earnings report arrived on July 30 with an $8.22 billion net loss, a $24.45 loss per diluted share, and the kind of headline that writes itself. The number missed analyst estimates of negative $7.52 per share by a margin wide enough to qualify as a different conversation.

Set it against Q2 2025 and the swing is $18.24 billion in a single year: from $10.02 billion in net income to $8.22 billion in net loss. The underlying software business generated $122.39 million in revenue, roughly in line with the $122.91 million estimate and up 6.9% year over year. Subscription revenue grew 54%. Gross margin held at 66.6%.

None of that mattered. The software business is not why anyone owns this stock, and it has not been for years. The $8.32 billion unrealized markdown on bitcoin holdings is what produced the operating loss, and the operating loss is what produced the headline. Everything else is a rounding error on a balance sheet dominated by 843,775 coins.

The accounting rule that swings billions

The loss is real in an accounting sense and meaningless in an operational one, and understanding why requires understanding a single rule change.

In 2025, Strategy adopted ASU 2023-08, the Financial Accounting Standards Board’s fair-value standard for digital assets. Under the previous impairment model, companies marked bitcoin down when prices fell but could not mark it back up when prices recovered. The new standard requires marking to market at the end of every quarter and running the change, up or down, straight through net income.

When bitcoin rises, Strategy books a gain. When bitcoin falls, Strategy books a loss. No coins need to change hands. The $8.32 billion markdown in Q2 2026 reflects the decline in bitcoin’s price during the quarter, from roughly $86,000 at the end of Q1 to $64,915 at the end of Q2. The $10.02 billion profit in Q2 2025 reflected a price increase over that quarter.

The accounting treatment turns Strategy’s income statement into a bitcoin price chart with a six-digit multiplier. This is not a criticism of the standard; fair-value accounting is what the industry asked for, and it replaced a rule that was genuinely worse. Under the old impairment model, Strategy once carried its bitcoin at below $16,000 per coin on its balance sheet while the market price sat above $94,000. The new rule fixes that distortion. But it introduces a different one: every quarterly earnings report is now dominated by a number that tracks bitcoin’s spot price, and every headline leads with a figure that tells you nothing about whether the company can meet its obligations.

The swing between quarters illustrates how extreme this effect can be. In Q2 2025, bitcoin rose and Strategy booked $10.02 billion in net income, the largest quarterly profit in the company’s history. One year later, bitcoin fell and Strategy booked an $8.22 billion loss, the largest quarterly loss. The software business, the thing the company actually operates, generated roughly the same revenue in both quarters. The P&L swung $18 billion on the movement of an asset that was neither bought nor sold during the period.

For investors who understand the accounting, the earnings figure is noise. For headline readers, it is the story. And for analysts who must issue estimates, it requires predicting bitcoin’s end-of-quarter price, which is another way of saying it requires predicting the unpredictable. The $7.52 consensus estimate for the loss per share was off by more than three times, not because the analysts were wrong about Strategy’s business, but because they were wrong about where bitcoin would close on June 30.

843,775 coins and a $9 billion gap

The holdings are the thesis and the risk in a single number. Strategy holds 843,775 bitcoin purchased at an average price of $75,476 per coin, for a total acquisition cost of approximately $63.69 billion. At the reporting date price near $64,915, the portfolio was worth roughly $54.8 billion.

The gap is approximately $9 billion. Strategy is underwater on its aggregate position.

Year to date, the company acquired 29,997 additional bitcoin, growing holdings by 25% in 2026 and 11% quarter over quarter. The BTC Yield metric, which measures the growth in bitcoin per assumed diluted share, stood at 4.5% for the first half. Management frames this as the core performance indicator: not the price of bitcoin, but the rate at which the company accumulates more of it per share outstanding.

The framing is self-serving, but it is not without logic. If bitcoin’s price eventually exceeds the cost basis, the accumulation during the drawdown period represents buying at a discount. If it does not, the accumulation represents compounding a loss. The metric assumes an outcome and measures progress toward it. No traditional financial metric works this way, which is either the point or the problem, depending on your priors about bitcoin’s long-term trajectory.

The doctrine that broke

For four years, one rule anchored the most influential trade in crypto: Strategy buys bitcoin and never sells it. Michael Saylor said it in earnings calls, in interviews, in tweets that became doctrine. The promise was the spine of the thesis, the thing that made MSTR a leveraged bitcoin proxy rather than a fund that might trade around its position.

In late May, Strategy sold 32 bitcoin for $2.5 million. In late June and early July, it sold 3,588 bitcoin for $218.4 million. The proceeds funded preferred stock dividend payments. On June 29, the board formalized the shift with the Digital Credit Capital Framework, authorizing up to $1.25 billion in bitcoin sales to fund dividends, reserve maintenance, and debt service.

The never-sell era is over. Saylor has reframed his advice, saying “never sell your bitcoin” was directed at individual holders, not a corporate treasury commitment. Whether the distinction holds depends on whether you think the people who bought MSTR at $400 understood it that way.

The sales are small relative to the position. The 3,588 coins sold represent roughly 0.4% of holdings. But the doctrine was not about the size of the sales. It was about the certainty that there would be none. Once that certainty breaks, every future quarterly report invites the question: how much did they sell this time?

The Digital Credit Capital Framework formalized on June 29 makes the conditions explicit. The framework authorizes bitcoin sales for three purposes: funding preferred stock dividends, maintaining the USD reserve at target levels, and servicing debt obligations. It also established a $1 billion buyback program for common stock and a $1 billion buyback program for STRC preferred shares. The architecture is designed to give management flexibility in both directions, buying bitcoin when conditions are favorable and selling when obligations require it.

Saylor framed the shift on the Q1 earnings call, saying Strategy would “probably sell some bitcoin to pay a dividend just to inoculate the market and send the message that we did it.” The word “inoculate” is revealing. It treats the sale as a vaccine against future panic, a controlled exposure to the idea that Strategy can sell, so that when it sells again, the reaction is smaller. Whether the inoculation worked is testable: the stock declined less than 1% on earnings day, suggesting the market has absorbed the new regime.

The question that remains unanswered is scale. Selling 3,588 coins to cover a quarterly dividend is manageable. Selling bitcoin to cover a $1.5 billion annual dividend load, if issuance continues at the current pace, is a different proposition. The framework permits it. The thesis requires it not to happen.

The capital structure underneath

Strategy has built the most complex capital structure in crypto, and possibly the most unusual one on any major exchange.

On the debt side, $6.71 billion in convertible notes remain outstanding, down 18% after the company repurchased $1.5 billion at an 8% discount. On the equity side, $14.4 billion in preferred stock is outstanding, spread across multiple series. The company raised $8.41 billion in Q2 alone through at-the-market stock offerings: $2.95 billion from common shares and $5.47 billion from STRC preferred stock. Year-to-date capital raised: $17.06 billion.

The preferred stock is where the pressure lives. STRC, listed on Binance as the company expanded its funding channels, trades near par and pays an 11.5% annual dividend. Strategy calls it “Digital Credit” and frames it as a new asset class. In practice, it is a preferred share that funds bitcoin purchases and requires cash dividends that bitcoin appreciation alone cannot pay.

Preferred dividends paid to date total $1.06 billion. The annual obligation is projected to rise from $217 million in 2025 to $904 million in 2026. As the company issues more STRC to buy more bitcoin, the dividend load grows. This is the flywheel running in reverse: the mechanism that accelerated accumulation during the bull market now accelerates cash outflows during the bear market.

Cash reserves stand at $3.75 billion, which CFO Andrew Kang says covers existing dividend and interest obligations for “more than 2.1 years.” The target range is two to three years of coverage, a window the company has publicly committed to maintaining. That is adequate today. Whether it remains adequate depends on how much more STRC the company issues and what bitcoin does over those two years.

The company also authorized a $1 billion share repurchase program for common stock. No buybacks have been executed to date. The authorization exists as optionality, not as a signal of intent: buying back stock while simultaneously issuing new stock would be contradictory, and Strategy is still firmly in issuance mode.

The convertible debt reduction deserves separate attention. By repurchasing $1.5 billion of convertible notes at an 8% discount, Strategy reduced its fixed-income obligations while taking advantage of the notes trading below par. This shifts the capital structure from debt (with maturity dates and conversion triggers) toward preferred equity (with no maturity but perpetual dividend obligations). The trade-off is clear: less risk of a forced conversion event, more risk of a perpetual cash drain. Whether that exchange favors shareholders depends entirely on how long bitcoin stays below cost basis.

Why the stock did not move

MSTR shares declined 0.67% to $97.09 in after-hours trading. For a company reporting an $8.22 billion loss against a $2.15 billion estimate, a sub-1% decline is remarkably composed.

The reason is straightforward: MSTR does not trade on earnings. It trades on bitcoin, and bitcoin’s price was already known. The quarterly loss was baked into the share price the moment bitcoin fell below Strategy’s cost basis. The earnings report confirmed what the market had been pricing for months.

This is what the stock price prediction analysis identified as the core dynamic: MSTR is a bitcoin derivative with a management fee attached. The management fee is the dilution from continuous stock issuance and the dividend obligations on preferred shares. As long as bitcoin’s expected return exceeds that fee, the stock has a thesis. When it does not, the stock trades below the net asset value of the bitcoin it holds.

At recent prices, Strategy’s market capitalization has traded at or below the value of its bitcoin holdings for the first time. The premium that powered the accumulation flywheel, allowing the company to issue stock worth more than the bitcoin it could buy with the proceeds, has compressed to zero or turned negative. Without a premium, the flywheel does not work.

Software subscription revenue growing 54% year over year is a footnote in this context, but it matters for one reason: it provides roughly $500 million in annualized revenue that partially offsets the cash costs of the capital structure. Strategy is not purely a holding company. It has a business that generates cash, even if that business is now roughly 2% of the enterprise value conversation.

The VanEck analysis published before earnings noted that credit risk has fallen as preferred equity value now surpasses convertible debt, removing the forced-sale scenario that would occur if convertible notes matured without refinancing. That structural improvement is real, even if the headline number obscured it. The market, which lives in the details rather than the headlines, appears to have noticed.

The arithmetic that matters

The sustainability question reduces to a comparison between cash coming in and cash going out.

Cash in: $3.75 billion in reserves, plus software revenue of roughly $500 million annualized, plus the ability to raise more capital through stock issuance (though the premium compression limits how accretive this can be).

Cash out: preferred dividends projected at $904 million in 2026, plus convertible note interest, plus operating expenses. The bitcoin monetization program provides a release valve, but exercising it means selling the asset the company exists to accumulate.