Crypto World

Pi Network’s pivot to AI and identity infrastructure

On Pi2Day, Pi Network stopped talking about mobile mining and started talking about infrastructure, launching tools to sell its compute, identity, and verification to the outside world. It is a real strategic pivot toward the AI era. Whether it fixes Pi’s actual problem, a token down 96% with no demand, is the harder question.

Summary

- On June 28, 2026, Pi Network used its annual Pi2Day event to launch three products, SoloHost, Pi Sign-in, and PiVerify, reframing the project from a mobile-mining app into infrastructure for compute, identity, and AI.

- SoloHost turns Pi Desktop into a platform for local, privacy-first AI apps and, in time, distributed computing across Pi’s hundreds of thousands of user-run nodes, with node operators paid in Pi.

- Pi Sign-in offers a “sign in with Pi” identity login for third-party apps, and PiVerify opens Pi’s human-verification system, which has checked over 18 million users, to outside businesses that pay in Pi.

- The pivot is a credible attempt to monetize Pi’s genuine assets, a large verified user base and a node network, by targeting real demand for private AI, decentralized compute, and trusted digital identity.

- The harder problem is that none of it directly addresses Pi’s core issue: a token down roughly 96% from its peak, weighed down by daily unlocks and migration supply, with no tier-one exchange listing, and the price fell after the announcement.

On June 28, 2026, Pi Network used its annual Pi2Day celebration to make a statement about what it wants to become, and for once the statement was not about mining. The project that grew famous as a mobile app letting tens of millions of people tap a button each day to earn tokens launched three products, SoloHost, Pi Sign-in, and PiVerify, and framed them as a deliberate pivot: from a mining-centric community toward an infrastructure provider for the artificial-intelligence era, offering compute, identity, and verification services to the outside world. The pitch was explicit. Rather than relying only on growth inside its own walled ecosystem, Pi would begin selling its genuine assets, a verified user base of more than 18 million people, a network of hundreds of thousands of user-run nodes, and a hybrid human-verification system, to external developers and businesses.

It was, by the standards of a project often dismissed as a mobile mining curiosity, a substantive strategic statement, and several observers called it the most concrete attempt yet to give Pi real utility beyond its internal apps. The reception was telling, and it frames the question this article examines. The new products were widely covered and broadly seen as more serious than Pi’s usual announcements, yet the token’s price fell after the news, extending a long decline, and the community split between those who welcomed a focus on real infrastructure and those frustrated that, once again, there was no major price catalyst and no tier-one exchange listing. That split is the heart of the matter.

This piece works through what Pi actually announced and what each product does, the logic behind the pivot and why it could matter, the harder reasons it may not move the needle, the community’s divided reaction, the identity angle that may be Pi’s most distinctive asset, and what would have to happen for the pivot to become real. The analysis is information, not advice. The honest framing throughout is that Pi has made a genuine strategic turn toward a credible thesis, and that a strategic turn is not the same as a solution to the supply-and-demand problem that has defined the token’s brutal 2026.

What Pi actually launched

Begin with the products, because the substance matters more than the framing. The headline release is SoloHost, an open, permissionless framework built into Pi Desktop that lets developers build and list applications which users run locally on their own computers, rather than on remote servers. Its emphasis is privacy-focused local AI: the flagship example shipped alongside it, an open-source AI agent, runs and stores its data entirely on the user’s own device, so a person can use AI assistance while keeping their data off third-party servers. SoloHost effectively turns a Pioneer’s computer into their own server, accessible from their phone through the Pi Browser, which lowers the technical barrier to running self-hosted software.

Looking further ahead, SoloHost is positioned to support distributed computing: the network plans to let its node operators contribute computing power to AI tasks, turning the hundreds of thousands of user-run Pi nodes into a practical computing layer for AI workloads, with participating nodes compensated in Pi by the third-party clients that use them. That last detail matters, because it is a direct attempt to create external demand for the token. The other two products target identity and authentication. Pi Sign-in is an authentication service that lets people log into supported third-party websites and apps using their existing Pi account, much like the familiar option to sign in with a major technology provider’s account.

It gives outside developers access to Pi’s large, verified user base while offering users a password-free login, and it extends Pi’s reach beyond its own browser into the wider web. PiVerify is arguably the most strategically interesting of the three: it opens Pi’s identity-verification system to external businesses, letting them use Pi’s know-your-customer and human-verification infrastructure, with those businesses paying in Pi. This is built on a verification base of real scale, a hybrid system combining automated and human checks that has reportedly verified over 18 million users across more than 200 countries and regions. Taken together, the three products share a single thesis: compute through SoloHost and the node network, identity through PiVerify and Pi Sign-in, and privacy-preserving AI running through all of it.

Each is designed to let outside parties use Pi’s existing resources and, in several cases, to pay for that use in Pi. The substance is real, and it is a meaningful departure from the mobile-mining identity that has defined the project. For readers who need the older model first, Pi’s mining and consensus basics explain why the daily tap was never computational mining in the Bitcoin sense. Pi2Day’s message was that the project now wants the conversation to move from how people earned PI to what the network can sell.

The logic of the pivot

The strategy behind these launches is more coherent than Pi’s critics often allow, and it rests on a clear-eyed assessment of what Pi actually has. After years of operation, Pi’s genuine assets are not a sophisticated technology stack or a thriving decentralized-finance ecosystem; they are scale and identity. The project has tens of millions of registered users, more than 18 million of them verified through identity checks, and a network of hundreds of thousands of nodes run by ordinary people on their own computers. Those are unusual assets.

Few crypto projects have a verified human user base of that size, and few have a distributed network of that many participant-operated nodes. The pivot is an attempt to monetize precisely those assets by turning them into services the outside world might actually pay for: the node network becomes a compute layer, the verified user base becomes an identity and authentication resource, and the whole thing is pointed at the demand wave around artificial intelligence. The timing aligns with real trends, which is what gives the thesis its credibility. Three of the most sought-after capabilities in technology right now are privacy-focused local AI, in which computation happens on a user’s device rather than in a corporate cloud; decentralized compute, in which distributed networks provide processing power outside the big data centers; and trusted digital identity, which has become acutely valuable as AI-generated content and bots make it harder to know whether an online actor is human.

Pi’s three releases map directly onto those trends: SoloHost addresses local AI and decentralized compute, while PiVerify and Pi Sign-in address trusted identity. The deeper narrative Pi has leaned into is “human infrastructure for AI,” the idea that its validator network, which has processed enormous volumes of human-verification tasks, makes it a provider of proof-of-human services in an age when distinguishing people from machines is increasingly difficult and increasingly valuable. The founders made this case publicly at a major industry conference, signaling that the pivot is a considered repositioning instead of a one-off product drop. As a strategy, monetizing real scale against genuine demand trends is a reasonable plan, and a more credible one than waiting for an internal app ecosystem to spontaneously produce value.

Why it could matter

Give the bull case its full weight, because parts of it are sound. The first point is that Pi is, for the first time, attempting to create external demand for the token instead of relying solely on internal ecosystem growth. The mechanisms are concrete: businesses using PiVerify pay in Pi, third-party clients using node compute through SoloHost pay node operators in Pi, and external developers tapping Pi Sign-in bring their users into contact with the network. If any of these gains real traction, it would represent something Pi has never had, namely outside parties paying to use Pi’s resources, which is a far healthier source of token demand than speculation or mining rewards.

Genuine utility demand, money flowing in from external use, is exactly what a token needs to escape a purely speculative valuation, and the pivot is at least pointed at creating it. The second point is that Pi’s scale is real and hard to replicate. A verified user base in the tens of millions and a node network in the hundreds of thousands are assets that most projects pursuing identity or decentralized compute would envy, and if Pi can convert even a fraction of that scale into paying external usage, the numbers could be meaningful. The third point is that the trends Pi is targeting are not hype cycles likely to fade quickly; privacy-preserving AI, decentralized compute, and trusted identity are durable, structural demands that are growing as AI adoption accelerates, so Pi is aiming at expanding instead of shrinking markets.

The fourth point is signaling: the launch represents Pi’s most serious attempt yet to position its existing resources for real external use, and a project that ships substantive infrastructure and pitches it at conferences is behaving more like a builder than a promotional scheme, which has value for credibility even before adoption arrives. None of this guarantees success, but it confirms that the pivot is a real strategy aimed at real demand using real assets, which is more than the project’s harshest critics concede. The bull case is not empty. The key is that the bull case depends on usage showing up outside Pi’s own community, not simply on another announcement cycle.

That is also why the SoloHost compute model matters beyond Pi itself. In crypto terms, Pi is trying to move closer to a DePIN-style thesis, where users contribute hardware resources and receive token incentives when external demand pays for those resources. If Pi can turn its node network into a usable compute market, the token gains a clearer reason to circulate. If it cannot, SoloHost remains a credible feature without becoming a meaningful demand engine.

Why it might not move the needle

Now the hard part, because the bull case runs into a problem the new products do not directly solve. Pi’s central issue is not a lack of strategy; it is a brutal supply-and-demand imbalance that the pivot does not address head-on. The token trades near $0.12, down roughly 96% from its peak near $3 in early 2025, weighed down by a structural overhang: large daily unlocks add millions of new tokens to the sellable supply, and the ongoing migration of users from the app to the mainnet steadily converts previously locked balances into liquid, sellable tokens, all against demand that has so far been thin and unproven. On top of that, Pi still lacks a listing on a top-tier exchange, which limits the buying power and liquidity available to absorb the supply.

The new products, however credible as a long-term strategy, do nothing immediate about the daily unlocks, the migration overhang, or the absence of a major listing, which are the forces actually pressing on the price. That is why the supply overhang in detail matters more for the chart than the branding of the pivot. The timing problem compounds this. SoloHost, Pi Sign-in, and PiVerify are early, with the flagship compute framework in beta and the distributed-computing vision still ahead, so any external demand they generate will build slowly, if it builds at all, while the supply pressure is immediate and continuous.

Infrastructure adoption is a multiyear process measured in developers onboarded and businesses signed, not a catalyst that lifts a price in weeks, and the gap between a strategy being announced and that strategy producing measurable token demand can be very long. The market reflected exactly this skepticism: the price fell after the Pi2Day announcement instead of rising, because traders recognized that a credible long-term plan does not change the near-term arithmetic of supply exceeding demand. The sober reading is that the pivot, even if it eventually succeeds, is unlikely to reverse the token’s trajectory soon, because the thing weighing on Pi is a supply overhang that infrastructure announcements do not lift. A good strategy and a falling price can coexist for a long time when the supply side is the problem, and for Pi, the supply side is the problem.

The community split

The divided reaction to Pi2Day captures the project’s central tension, and it is worth understanding because it reflects two legitimate but incompatible expectations. On one side are community members who welcomed the announcements as exactly the kind of substantive, building-focused progress Pi needs, evidence that the team is constructing real infrastructure and pursuing genuine utility instead of chasing speculative attention. To this group, the pivot toward compute, identity, and AI is encouraging precisely because it is unglamorous and long-term, the unflashy work of turning a large community into a useful network. They read SoloHost and PiVerify as signs that Pi is maturing into something with a reason to exist beyond mining rewards, and they value that even though it does not immediately move the price.

On the other side are community members frustrated by the same announcement, for the same reason it pleased the first group: it shipped services instead of a price catalyst, and in particular it did not bring the tier-one exchange listing that much of the community has long anticipated. The days before Pi2Day were thick with speculation, including rumors of a major listing, and when the actual announcement delivered infrastructure instead, the disappointment showed up immediately in the price. This group experiences Pi’s slow, conditions-based pace as a recurring letdown, a pattern of significant events that produce features but not the liquidity and demand that would let holders realize value. The split between these camps is not really a disagreement about facts; it is a disagreement about what Pi should be optimizing for, long-term infrastructure or near-term price and liquidity, and Pi2Day satisfied the first while frustrating the second.

That tension, between the builders and the price-watchers, is structural to a project that has an enormous community sitting on tokens it mostly cannot yet sell at a price it likes, and it will persist until the pivot either produces real demand or it does not. The same tension appears in smaller ecosystem updates, including tools meant to improve app visibility and activity inside Pi’s own directory. Builders can see those as pieces of a broader utility stack, while traders see them as too indirect to absorb the supply hitting the market. Both reactions make sense because they are measuring different things.

The identity angle

Of everything Pi announced, the identity thesis may be its most distinctive and defensible asset, and it deserves a closer look because it is where the pivot is strongest. The problem PiVerify and Pi Sign-in address, verifying that an online actor is a real, unique human, has become one of the most pressing in technology as AI systems generate convincing text, images, and behavior at scale, making bots and fake accounts harder to detect. A network that can reliably attest to human identity has genuine value in that environment, and Pi has built exactly that: a hybrid automated-and-human verification system that has checked over 18 million users across more than 200 countries, producing a large base of verified human identities. Opening that system to external businesses through PiVerify, and offering identity-based login through Pi Sign-in, points Pi at a real and growing market, proof-of-human services for an age of AI bots, where its scale is a genuine competitive asset instead of a liability.

The honest caveats keep this from being a slam dunk. Pi is not alone in pursuing decentralized identity and proof-of-personhood; other projects have built reputations and technology in the same space, and some have more sophisticated cryptographic approaches, so Pi’s advantage is its scale instead of its novelty. Questions also remain about the robustness of Pi’s verification against determined fraud, the privacy implications of a large identity database, and whether external businesses will actually choose Pi’s system over established identity providers. But even with those caveats, the identity angle is the part of the pivot where Pi’s existing assets line up most cleanly with real, growing demand, and where its scale is most clearly an advantage.

If any piece of the AI-infrastructure thesis becomes a meaningful business for Pi, the identity layer is the most likely candidate, because it is the one where Pi already has something large and hard to replicate that the market increasingly needs. For an observer judging whether the pivot has substance, the identity angle is the most credible reason to take it seriously. It is also where the identity thesis Pi is chasing connects most directly to a wider crypto problem, not just a Pi-specific one. In an internet crowded with AI agents and synthetic users, verified human identity is not a niche use case; it is becoming basic infrastructure.

What would make the pivot real

In the end, the pivot will be judged not by its announcement but by whether it produces the one thing Pi has always lacked: real, external demand large enough to matter against the token’s supply. That requires a recognizable set of developments, and naming them is more useful than guessing at a price. The first and most direct is external businesses actually paying in Pi at scale, real companies using PiVerify for identity checks, real clients paying node operators for compute through SoloHost, real developers integrating Pi Sign-in, with the resulting token demand visible and growing instead of nominal. Adoption metrics, not announcements, are the proof.

The second is that this demand grows fast enough to outpace the supply pressure, the daily unlocks and the migration overhang, so that real usage absorbs the new tokens entering the market instead of being swamped by them. That is where why migration adds sell pressure becomes central to the investment case. The third is liquidity, which for Pi means a tier-one exchange listing that would bring the deep markets and buying power needed to support a higher valuation, the catalyst much of the community has awaited and that the infrastructure pivot does not by itself provide. The honest reading is that the bull case requires these together, real external demand, demand outpacing supply, and the liquidity to express it, not any one alone, and that none of them is presently in hand.

What Pi2Day delivered is a credible strategy and a set of early products pointed at genuine demand trends, which is necessary but not sufficient. A token cannot pay its bills with potential, and the supply weighing on Pi is immediate while the demand the pivot might create is prospective and slow. The realistic conclusion is that Pi has made a serious and arguably overdue strategic turn, that the identity and compute thesis is more credible than the project’s reputation suggests, and that whether it rescues the token depends entirely on execution that has not yet happened. The pivot is real; whether it works is the question the coming months, not the announcement, will answer.

Frequently asked questions

What did Pi Network announce on Pi2Day 2026?

On June 28, 2026, Pi Network launched three products framed as a pivot toward infrastructure for compute, identity, and AI. SoloHost is an open framework in Pi Desktop for running local, privacy-first AI apps and, in time, distributed computing across Pi’s node network, with node operators paid in Pi. Pi Sign-in is a “sign in with Pi” authentication service letting people log into third-party apps with their Pi account. PiVerify opens Pi’s identity-verification system, which has checked over 18 million users across more than 200 countries, to external businesses that pay in Pi. Together they reframe Pi from a mobile-mining app into a provider of compute, identity, and AI-related services to the outside world. The important point is that these products try to monetize resources Pi already has: a large verified user base and a large network of user-run nodes. That makes the pivot more substantive than a branding change, even if adoption remains unproven.

Is Pi Network pivoting away from mining?

In emphasis, yes. The Pi2Day launches mark a deliberate shift from a mobile-mining-centric identity toward positioning Pi as an infrastructure provider for the AI era, monetizing its genuine assets, a large verified user base and a node network, as external services. Mining and the broader migration process continue, but the strategic narrative has moved toward compute, identity, and AI. The logic is that Pi’s real assets are its scale and its verified human identities, not a sophisticated technology stack, so the path to value is turning that scale into services outside parties will pay for. Whether the pivot succeeds depends on actual external adoption, which has not yet been proven. The daily tap may still define how millions of users think about Pi, but it is no longer the most important part of the project’s pitch. The new pitch is that Pi can sell identity, verification, and compute to third parties.

Will the Pi2Day pivot raise Pi’s price?

Not directly or quickly, on the evidence so far. The price fell after the announcement, because the new products, however credible as long-term strategy, do not address Pi’s immediate problem: a supply overhang from large daily unlocks and ongoing migration converting locked tokens into sellable ones, against thin demand and no tier-one exchange listing. Infrastructure adoption builds slowly, over years of onboarding developers and businesses, while the supply pressure is continuous. The pivot could eventually create real token demand if external businesses pay to use Pi’s compute and identity services at scale, but that is prospective and gradual. The forces weighing on the price are present and ongoing. A good strategy and a falling price can coexist when supply is the problem. For Pi, the market is asking for proof that demand can absorb unlocks, not only proof that the team can ship products.

What is the “human infrastructure for AI” narrative?

It is Pi’s framing of its core thesis: that its network of verified human users and the validators who process identity checks make it a provider of proof-of-human services in an age when AI makes distinguishing people from bots increasingly difficult. Pi’s verification system has processed enormous volumes of human-verification tasks across a base of more than 18 million verified users in over 200 countries. The pivot leans on this, positioning Pi’s identity and verification resources, through PiVerify and Pi Sign-in, as infrastructure that businesses need as AI-generated content and bots proliferate. It is the most distinctive part of Pi’s strategy, because trusted digital identity is a real and growing demand, and Pi’s scale of verified humans is genuinely hard to replicate. The challenge is turning that verified base into a product outside businesses actually choose to use. Scale alone is not enough if the verification layer is not trusted, easy to integrate, and privacy-conscious. That is why PiVerify is strategically important: it is the bridge between Pi’s internal verification work and an external identity market.

Why is Pi’s price so low despite a large community?

Because supply has overwhelmed demand. Pi trades near $0.12, down roughly 96% from its early-2025 peak near $3, because large daily token unlocks and the ongoing migration of users to the mainnet keep converting locked tokens into sellable supply, while demand has been thin and there is no tier-one exchange listing to bring deep liquidity and buying power. Many users treat mined Pi as tokens to sell once they become transferable, and weak app adoption has meant little organic usage to absorb the supply. The community’s goals, faster migration and bigger listings, ironically increase the sellable supply. The result is a structural imbalance that ecosystem announcements, including the Pi2Day pivot, do not by themselves resolve. For the price to stabilize, usage demand has to become large enough to meet the supply entering the market. Until then, even good news can fail to move the token if holders use liquidity as an exit.

What would make Pi’s pivot succeed?

Real, external demand large enough to matter against the supply. Concretely, that means external businesses actually paying in Pi at scale: companies using PiVerify for identity checks, clients paying node operators for compute through SoloHost, developers integrating Pi Sign-in, with visible, growing token demand instead of nominal usage. It also means that demand growing fast enough to outpace the daily unlocks and migration overhang, so real usage absorbs the new supply. And it likely means a tier-one exchange listing to provide the liquidity and buying power a higher valuation requires. The bull case needs these together, not any one alone, and none is presently in hand. Adoption metrics, not announcements, will determine whether the pivot becomes real. Pi has made the strategic argument; now it has to prove that outside customers want what the network is selling.

This article is information, not financial or investment advice. Details of Pi Network’s Pi2Day releases, user and node figures, price levels, and supply dynamics reflect reporting available as of June 30, 2026, are point-in-time, and can change. Cryptocurrency is highly volatile and you can lose money. Nothing here is a recommendation about Pi or any asset. Do your own research and consult a qualified professional before making any decision.

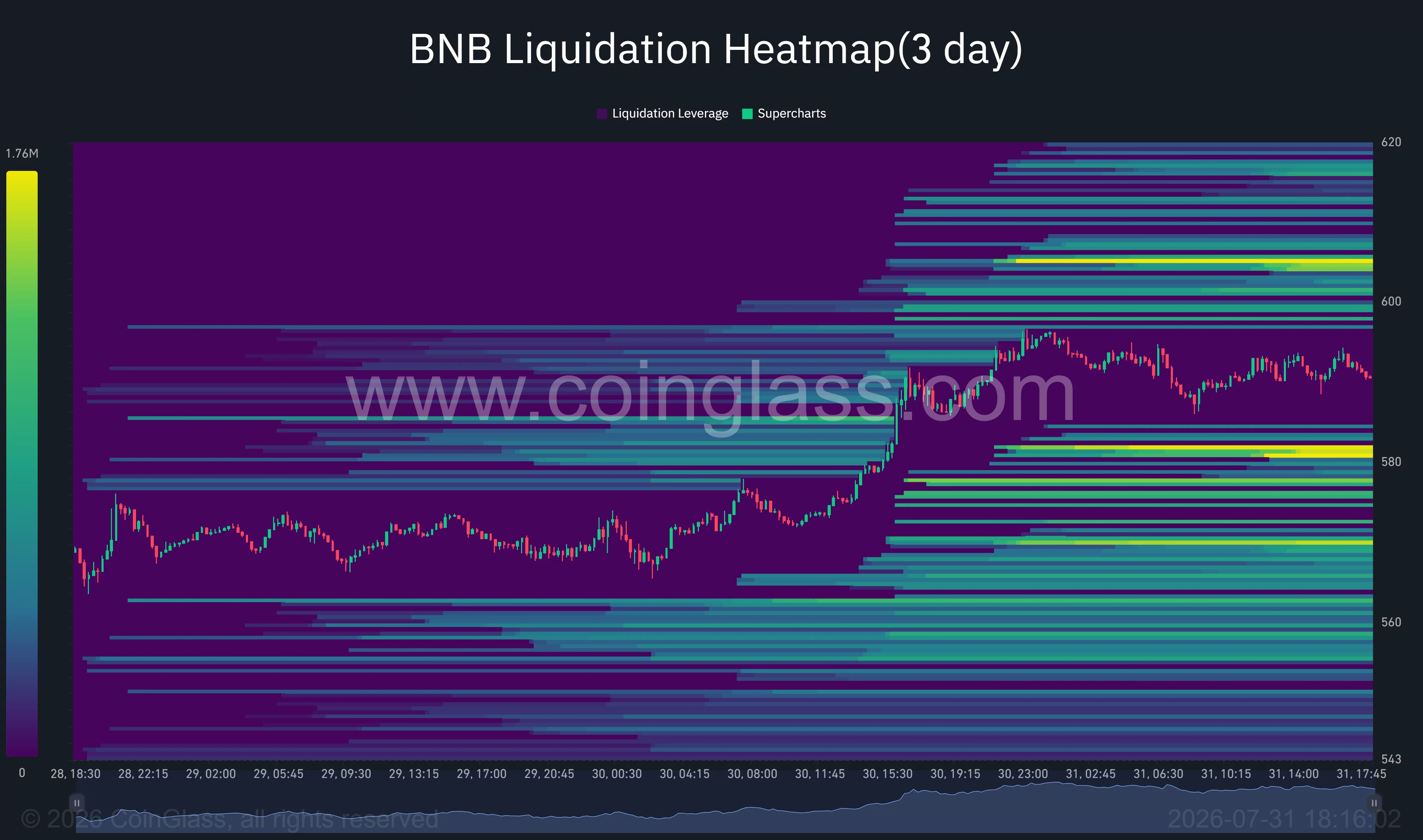

BNB price rallied more than 5% before sellers halted the advance near $600, leaving the token at about $590 on July 31 as traders assessed whether its breakout can hold.

Summary

- BNB price climbed above $590 after breaking a descending trendline that had capped price for about 45 days.

- The daily price moved above the Bollinger Band’s $587.85 upper boundary, signaling strong but stretched momentum.

- A 3-day liquidation heatmap shows major liquidity clusters near $580 and $605–$610.

- 4-hour RSI remains bullish at 65.14, while the MACD continues to favor buyers.

BNB price action today

According to data from crypto.news, BNB (BNB) price surged from the $570 area and reached an intraday high near $595 before easing to approximately $590 at the time shown on the charts. The move carried the token out of the narrow range that had controlled trading during the second half of July.

The 4-hour chart shows a sharp breakout candle above $575, followed by an extension toward $595. Buyers have since defended the $586–$590 region, although several upper wicks near $595 show that sellers remain active below the psychological $600 level.

BNB has tested this broader resistance area several times since June. Price reached nearly $598 on June 22 and approached $594 in early July, but neither attempt produced a sustained move above $600.

The latest breakout is stronger than the previous tests because it followed a period of higher lows around $560–$570. However, BNB must still close above $600 to confirm that the wider consolidation has ended.

What is driving the BNB move?

Technical positioning appears to be the immediate driver. BNB broke above a descending resistance line that had connected lower highs since the token traded near $632 in mid-June.

Analyst Hanah described the move as a possible change in short-term momentum after 45 days of downward pressure.

“If BNB can hold above the breakout level, it could pave the way for a stronger bullish continuation.”

Network activity has also provided a fundamental backdrop for the recovery. BNB Chain reportedly processed about $19 billion in weekly decentralized exchange volume, placing it ahead of Ethereum and Solana during the measured period. Network utilization also rose from roughly 17% to nearly 30%.

SilentSwap’s integration added another use case by bringing private cross-chain swaps to the ecosystem. Rising transactions and gas usage may support demand for BNB, which users need to pay fees across BNB Chain.

Still, those developments do not guarantee that price will clear $600. The immediate rally remains heavily influenced by technical positioning and liquidity concentrated around nearby resistance.

BNB indicators favor buyers but show stretched conditions

BNB closed near $590.15 on the daily chart, above the Bollinger Band’s upper boundary at $587.85. The middle band sits at $573.53, while the lower band is near $559.21.

A move above the upper band reflects strong buying pressure, but it can also precede a short-term pullback when price rises too quickly. A daily close back inside the band would put $573.53 in focus as the first mean-reversion target.

The Average Directional Index stands at 22.27. That reading suggests the developing trend has moderate strength but has not yet reached the levels normally associated with a powerful directional move.

Momentum is clearer on the 4-hour timeframe. The relative strength index is at 65.14, above its moving average of 61.84 but below the overbought threshold of 70. This leaves room for another advance while warning that buyers are approaching stretched territory.

The 4-hour MACD line stands at 5.79, above the 4.33 signal line, with a positive histogram reading of 1.46. The configuration remains bullish, although the shrinking histogram bars suggest that the initial burst of momentum is beginning to cool.

Key BNB levels to watch

The 3-day liquidation heatmap identifies a dense pool of leveraged positions around $605–$610. That cluster could attract price if BNB clears $600, but it may also increase volatility as short liquidations and profit-taking occur in the same region.

A decisive close above $610 would strengthen the breakout and open a route toward the former $620–$632 supply zone. The latter marks the high from which the descending trendline began.

Immediate support sits between $587 and $580. The heatmap shows the brightest nearby liquidity concentration around $580–$582, making that area a possible downside target if the rally loses momentum.

Below $580, the Bollinger midline near $573.53 becomes the next technical support. Losing that level would weaken the breakout and expose $559–$560, where the daily lower band aligns with July’s established demand zone.

US market context could limit the breakout

US investors are also watching broader risk appetite as geopolitical tensions and elevated energy prices keep inflation concerns in focus. Higher oil prices can complicate the Federal Reserve’s policy outlook by raising the risk that inflation remains above target.

A more restrictive interest-rate environment generally reduces liquidity available for speculative assets, including altcoins. BNB may therefore struggle to sustain an independent rally if Bitcoin and US technology stocks weaken as investors reduce risk.

The near-term setup remains constructive while BNB holds above $580. A confirmed break through $600–$610 would favor continuation, while a retreat below $573 would suggest the latest move was another failed breakout within the wider range.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Crypto World

Strategy Posts $8.33 Billion Operating Loss As Downturn Pushes Bitcoin Below Acquisition Cost

Bitcoin treasury company Strategy has reported a second-quarter operating loss of $8.33 billion, largely due to an unrealized loss of $8.32 billion on its Bitcoin (BTC) holdings. The company currently holds 843,775 BTC, worth $54.77 billion, significantly lower than the $63.69 billion acquisition cost.

Strategy has created a $3.75 billion cash reserve as part of its BTC monetization program to support interest and dividend obligations.

Strategy Losses Deepen

Strategy has reported an operating loss of $8.33 billion in Q2 as unrealized losses on its Bitcoin holdings climbed to $8.32 billion after Bitcoin prices declined substantially. The flagship cryptocurrency traded around $88,400 at the end of 2025 and was near $64,700 when Strategy announced its quarterly earnings. The decline pushed the value of Strategy’s Bitcoin holdings below their aggregate purchase cost of $63.69 billion.

The company recorded an operating loss of $8.33 billion, and a net loss of $8.22 billion, working out to $24.45 per diluted common share. In comparison, Strategy’s net income stood at $10.00 billion during Q2 2025. The quarterly earnings report did not have much impact on Strategy (MSTR) shares. MSTR rose 4.7% during regular trading hours before registering a marginal decline following the report.

Meanwhile, Strategy’s core software business reported quarterly revenue of $122.4 million, a 6.9% increase from a year earlier, and gross profit stood at $81.6 million.

Bitcoin Bet Weighs Heavy

Strategy’s Bitcoin holdings stood at 843,775 BTC as of July 26, with an acquisition cost of $63.69 billion. The company’s Bitcoin holdings are currently valued at $54.77 billion, putting them $8.92 billion underwater. However, this loss is unrealized and reflects the change in BTC’s market value rather than an actual loss from selling the position. Strategy has also sold a small portion of its Bitcoin holdings to fund its dividend obligations, as the company continues to monetize its portfolio when necessary.

Strategy Building Dollar Reserve

Strategy’s capital markets programs have helped raise $17.06 billion this year while reporting a Bitcoin yield of 4.5%. The company also repurchased $1.5 billion of its senior convertible notes at an 8% discount, cutting its convertible debt to $6.71 billion. The move reduces Strategy’s debt burden after declining Bitcoin prices put substantial pressure on its balance sheet. Strategy also expanded its US Dollar Reserve by $525 million to $3.75 billion. The company stated that the reserve can cover dividend obligations for 2.1 years under its current policy. However, it conceded that it cannot guarantee payments under changing or adverse market conditions.

Strategy has also initiated repurchase programs for its common shares and digital credit securities, giving the company the option to buy back securities without using the entire authorized amount.

Strategy Must Maintain Liquidity Phong Le

Strategy CEO Phong Le stressed the importance of maintaining liquid US Dollars to fund dividend obligations during the company’s earnings call. Le stated:

“We thought that liquid Bitcoin would be important, but what Mike [Michael Saylor] mentioned earlier is that the people who are holding these preferreds don’t look at Bitcoin the way they look at U.S. dollars.”

Le stressed that ensuring a Dollar reserve to cover two to three years of dividend obligations is a prudent strategy.

Market Impact

Strategy is the largest publicly traded holder of Bitcoin, giving US investors indirect exposure to the flagship cryptocurrency. The company’s shares reflect fluctuations in Bitcoin’s price and also respond to equity issuance, debt costs, preferred dividends, and any change to its capital structure.

Strategy’s cash reserve and lower convertible debt give the company some financial flexibility. However, the value of its Bitcoin holdings must recover above the acquisition cost. A further decline in Bitcoin prices could deepen unrealized losses and increase pressure on the company.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

New York has filed a lawsuit against prediction market platform Kalshi, accusing the company of running an illegal, unlicensed gambling operation in the state. The case centers on Kalshi’s event contracts tied to outcomes such as sports results and elections.

In its filing, New York seeks an order stopping Kalshi’s alleged gambling activity, along with forfeiture of “illegal gains,” restitution to users, and civil penalties reportedly set at three times the amount of those gains. Attorney General Letitia James said prediction markets like Kalshi are gambling “plain and simple,” adding that the state is acting to enforce its laws and protect residents.

Key takeaways

- New York is pursuing injunctive relief and financial remedies against Kalshi, framing event contracts as unlicensed gambling.

- The lawsuit follows a cease-and-desist order from the New York State Gaming Commission issued in October 2025.

- Kalshi has challenged the regulator in federal court, but a judge denied its bid for a preliminary injunction in July 2026.

- The dispute escalates a wider fight over whether federally regulated prediction markets can be blocked under state gambling laws.

- Regulators have been increasingly scrutinizing the prediction market sector as it expands—both in mainstream visibility and blockchain-based infrastructure.

New York challenges Kalshi’s business model

The lawsuit targets Kalshi’s offering of contracts whose settlement depends on real-world outcomes, including sports and election-related events. New York’s position is that these products function as gambling and therefore require appropriate state licensing and compliance.

While Kalshi operates as a prediction market platform, New York’s complaint does not treat the platform as merely financial speculation. Instead, it argues that calling the contracts “prediction” does not change their practical nature as wagers on future results.

This action arrives after the New York State Gaming Commission issued a cease-and-desist order in October 2025. Kalshi responded by suing the regulator in federal court, and the immediate conflict has moved through multiple procedural steps.

Earlier this year, a judge denied Kalshi’s request for a preliminary injunction in July. An appeals court later rejected Kalshi’s attempt to halt enforcement while the appeal continues, meaning New York’s efforts can proceed even as the legal battle plays out.

Kalshi’s legal fight intersects with CFTC’s federal oversight

The New York case is part of a broader jurisdictional tug-of-war over prediction markets—specifically whether state gambling laws can restrict products that a federal regulator treats as within its own regulatory scope.

Just before New York filed, the U.S. Commodity Futures Trading Commission (CFTC) submitted an emergency motion in court seeking to block New York’s enforcement efforts. The CFTC argued that the state’s action interferes with the agency’s “exclusive authority” under the Commodity Exchange Act to regulate designated contract markets such as Kalshi.

The CFTC’s approach has been consistent in similar disputes involving other states. In those arguments, the commission has warned that if states can independently ban event contracts listed by federally regulated exchanges, it would create conflicting rules—undermining a uniform federal commodities framework.

That position has been cited in enforcement disputes the CFTC has taken against at least nine states, according to reporting that highlights how the agency frames state restrictions as a threat to federal oversight of commodities markets.

Prediction markets keep attracting mainstream attention

Prediction markets are built on a simple premise: users trade contracts tied to the outcome of future events, and the price of those contracts is intended to reflect market-implied probabilities. In theory, that mechanism helps participants aggregate information about what is likely to happen.

But as the sector grows, regulators across jurisdictions have increasingly treated certain prediction market products as gambling—especially when settlement depends on outcomes and participation mirrors typical wager-based behavior. The resulting legal uncertainty has encouraged closer scrutiny of how platforms structure their offerings and what regulatory category they fall under.

Kalshi is not the only high-profile operator to face regulatory pressure. Its competitor, Polymarket, has also encountered scrutiny from regulators abroad, with some authorities restricting or investigating operations over licensing and gambling-related concerns.

Beyond the regulatory front, prediction markets have also expanded technologically. Kalshi began broadening into blockchain-based infrastructure in December 2025, launching tokenized prediction markets on Solana and later adding support for multiple blockchain networks. That shift mirrors a wider trend in crypto markets, where trading venues seek faster settlement, greater programmability, and broader distribution.

Crypto analytics point to rapid growth in on-chain prediction activity

While the legal battles unfold, on-chain prediction markets have shown signs of growing participation. According to analytics firm Chainalysis, blockchain-based prediction markets processed about $20 billion in trading volume tied to the 2026 FIFA World Cup, with more than 400,000 wallets participating.

The implication for investors and builders is that even as regulators debate classification—commodities regulation versus gambling law—the user demand for outcome-trading continues to show up in measurable on-chain activity. That activity can raise the stakes for platforms that want to operate at scale without running afoul of differing legal interpretations.

For market participants, the tension is straightforward: platforms may market prediction markets as probability markets or informational tools, but regulators may focus on the wager-like economic structure and licensing requirements. The New York lawsuit against Kalshi is a direct test of how far state enforcement can go when a federal agency argues for exclusive jurisdiction under the Commodity Exchange Act.

What to watch next is whether the CFTC’s federal arguments continue to constrain or defeat New York’s enforcement, and whether Kalshi’s appeal of the preliminary-injunction denial changes the immediate timeline. The outcome could shape how other states pursue enforcement against prediction markets—and how platforms design their products to manage regulatory risk.

Japan’s central bank kept interest rates unchanged at 1.0% on Friday, according to a Bank of Japan (BoJ) statement issued after its policy decision. The meeting outcome landed in line with market expectations, even as the yen had just swung sharply following reports of intervention.

The BoJ’s decision came shortly after the Japanese currency strengthened quickly against the US dollar—moving up as much as 3.5% overnight, based on TradingView data—an advance many traders linked to coordinated or related foreign-exchange actions involving the yen. With Japan also flagging inflation pressures later in the year, investors are now watching how currency policy, yields, and global risk appetite intersect for crypto markets.

Key takeaways

- The BoJ held the uncollateralized overnight call rate at around 1.0% after an outcome supported by eight of nine Policy Board members.

- Recent yen volatility reportedly coincided with currency intervention activity involving Japan and South Korea, as the JPY briefly jumped versus the USD.

- The BoJ warned that CPI inflation may accelerate to clearly above 2% from the second half of fiscal 2026.

- Since the yen carry trade unwind in 2024, JPY moves have continued to influence Bitcoin and altcoin risk sentiment.

BoJ holds rates steady after yen turbulence

In its latest statement, the BoJ said it would “encourage the uncollateralized overnight call rate to remain at around 1.0 percent,” confirming a broadly shared view among officials for keeping policy unchanged. The decision was passed by eight of nine members of the Policy Board, with Hajime Takata the only dissenting vote, proposing a 0.25% rate hike.

Markets had largely expected this result ahead of the meeting, according to earlier coverage referenced by Cointelegraph. The policy decision also arrived just hours after the yen’s brief surge—an FX move that coincided with speculation about official action. While the BoJ did not comment directly on the reported intervention, the timing is likely to keep FX traders attentive to any future shifts in the currency’s direction.

Reported Japan–Korea involvement raises the stakes

Several reports tied the yen’s sharp move to intervention efforts. The BoJ did not confirm the details, but commentary in regional media pointed to alignment between Japan and South Korea’s policy priorities. At the time, the South Korean won was reportedly rising as well, suggesting traders were reacting to developments across both currencies.

Analyst Lee Min-hyuk of KB Kookmin Bank, as quoted by Straits Times, argued that cooperation could amplify the impact because the won and yen are closely linked. Separate reporting also noted that the US had conducted “rate checks”—a softer form of intervention that can precede stronger operations—during Thursday’s session, fueling speculation about a wider, multi-country FX response.

Traders typically treat intervention expectations as a constraint on how far a currency can move in either direction. If intervention remains a credible backstop, it can affect not only FX markets but also broader capital flows—an important link for assets like Bitcoin that have repeatedly shown sensitivity to liquidity conditions and global risk changes.

BoJ turns to inflation headwinds for fiscal 2026

Beyond the rate decision, the BoJ’s outlook for prices may carry longer-term significance. In its quarterly Outlook for Economic Activity and Prices, the central bank said the year-on-year rate of increase in the consumer price index (CPI) “is likely to accelerate to a level clearly above 2 percent from the second half of fiscal 2026.”

In the same report, the BoJ pointed to additional drivers of inflation such as durable goods prices. It also referenced the “waning of the effects of high crude oil prices,” tying this shift to factors including the ongoing US–Iran war and the closure of the Strait of Hormuz oil-transit route—elements that can influence energy costs and therefore the inflation trajectory.

For investors, this matters because inflation expectations can eventually pressure policymakers toward tighter conditions, or at minimum change the path of interest-rate expectations. Even though Friday’s decision was unchanged, the direction of the BoJ’s CPI outlook can affect longer-dated yields and, by extension, currency dynamics and carry-trade behavior.

Why yen moves still matter for crypto

FX volatility has remained a meaningful input for crypto traders since the “unwinding” of the yen carry trade in August 2024, when yen funding pressures and related liquidity shifts coincided with significant downside across Bitcoin and other major tokens. Since then, Japan-related rates and the yen’s direction have continued to serve as a proxy for risk conditions—especially when changes in JPY funding costs trigger broader adjustments in global portfolios.

Earlier this year, Arthur Hayes, former CEO of crypto exchange BitMEX, suggested that a weak yen combined with rising Japanese bond yields could encourage some investors to rotate away from low-yielding US bond exposures. In his framing, central bank liquidity interventions and related yield dynamics can flow through to crypto demand by shifting broader risk and liquidity availability.

Hayes also previously argued that USD/JPY could rise significantly—he predicted in December 2025 that the pair might reach as high as 200. While Friday’s BoJ decision does not validate that forecast on its own, the ongoing interplay between FX moves, yields, and policy signals remains central to how traders map macro conditions onto digital-asset positioning.

With the BoJ holding rates steady, the immediate question for markets is whether recent yen strength proves durable or fades—particularly given reports of intervention-linked volatility and the central bank’s warning that inflation pressures could strengthen later in fiscal 2026. Crypto traders will likely watch for follow-through in JPY/USD and Japanese yield expectations, because those variables continue to shape liquidity assumptions that underpin risk appetite.

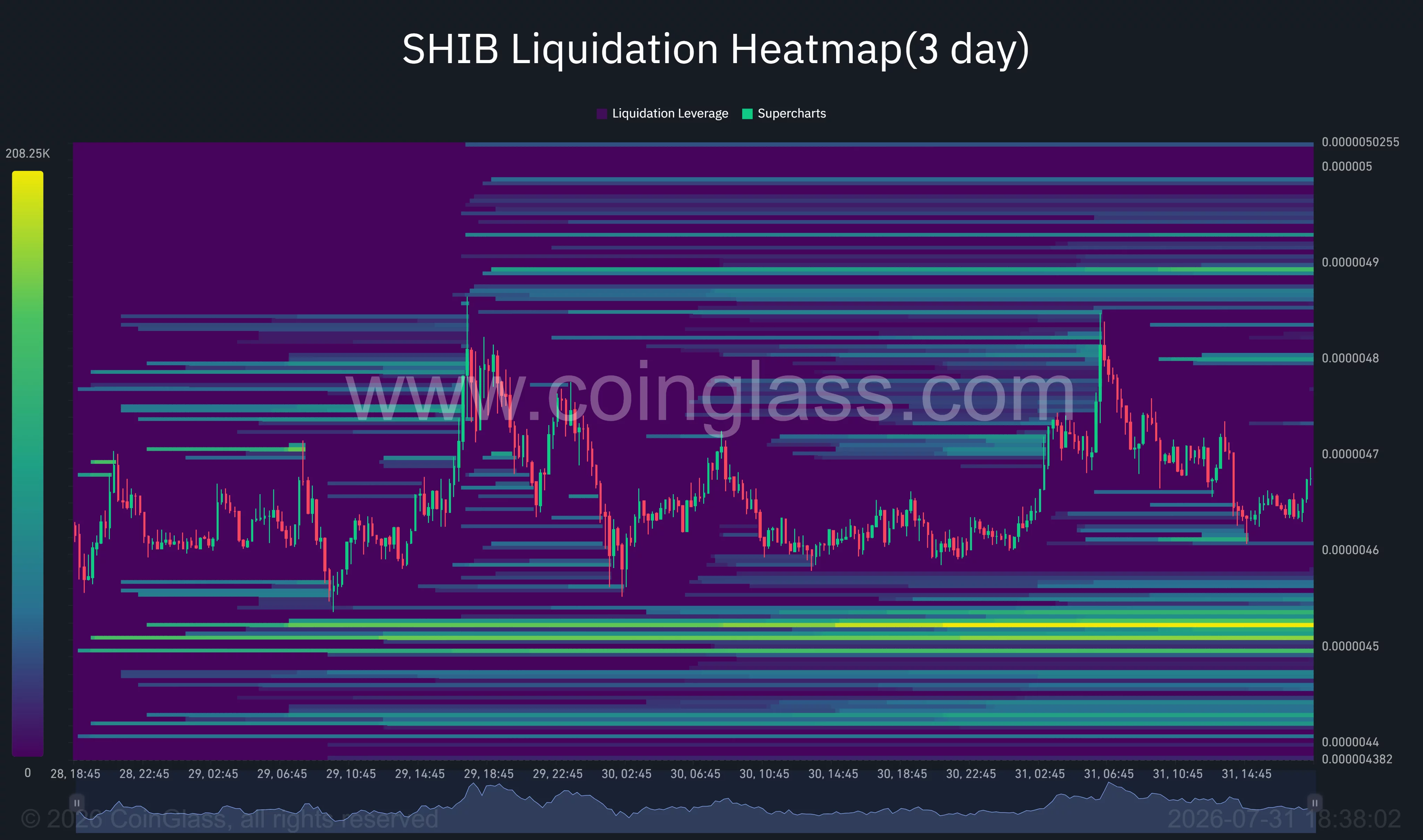

Shiba Inu price surrendered much of its 40% breakout after sellers rejected the meme coin near $0.0000058, leaving bulls to defend a newly established support zone around $0.0000045.

Summary

- SHIB price surged nearly 40% before retreating to approximately $0.0000047.

- Daily ADX climbed to 31.03, confirming that volatility has developed into a stronger directional trend.

- The 4-hour chart places immediate support between $0.00000444 and $0.00000466.

- Liquidation data shows dense leverage near $0.0000045, raising the risk of another volatility spike.

SHIB price rally loses momentum

According to data from crypto.news, SHIB price traded near $0.00000468 on July 31 after its vertical rally encountered heavy selling above $0.0000054. The token briefly reached approximately $0.0000058 during the breakout, marking a gain of nearly 40% from its pre-rally base around $0.0000041.

However, the long upper wick on the 4-hour chart showed that sellers quickly absorbed demand near the peak. SHIB subsequently formed a series of lower highs before stabilizing between $0.0000046 and $0.0000048.

The pullback leaves SHIB roughly 20% below its intraday peak, although the token remains above the range that contained its price through most of July. That distinction matters because the move has not yet completed a full round trip to its breakout point.

South Korean retail activity, a sharp increase in token burns and renewed whale participation reportedly accompanied the rally. However, the rapid reversal suggests that some traders used the sudden liquidity expansion to take profits rather than build longer-term positions.

Four-hour chart shows bulls defending support

SHIB’s 4-hour structure has shifted from a vertical advance into tight consolidation.

The token is trading around its 20-period and 50-period simple moving averages, located near $0.00000466 and $0.00000468, respectively. Holding this area would allow buyers to establish a higher base after the breakout.

Stronger support sits at the 100-period SMA near $0.00000444 and the 200-period SMA around $0.00000437. Both averages are rising, and SHIB continues to trade above them, preserving the short-term recovery structure.

The moving average convergence divergence indicator is less decisive. Its MACD and signal lines have converged near zero after the earlier bullish impulse faded. This shows that selling momentum has slowed, but buyers have not yet regained enough strength to start another sustained advance.

A 4-hour close above $0.0000048 would be an early bullish signal. SHIB would then face resistance at $0.0000050, followed by the post-breakout supply zone between $0.0000052 and $0.0000054.

SHIB liquidation map warns of a sweep toward $0.0000045

The 3-day liquidation heatmap shows that SHIB is trading between two notable leverage clusters.

The largest nearby concentration sits below the market around $0.00000450 to $0.00000452. This bright liquidity band could attract price if SHIB loses the $0.0000046 floor, potentially triggering leveraged long liquidations.

Below that area, additional liquidity appears around $0.0000044. A drop through both zones would erase most of the breakout and expose the July base near $0.0000041.

Upside liquidity is comparatively scattered. The first meaningful bands appear near $0.0000048 and $0.0000049, with another cluster around $0.0000050. Clearing these positions could produce a short squeeze, but SHIB must first overcome the moving-average congestion on its 4-hour chart.

The liquidation structure therefore favors continued volatility. A sweep toward $0.0000045 could occur before either side establishes control.

Daily indicators preserve SHIB’s recovery attempt

Despite the rejection, SHIB’s daily chart contains one constructive development that is price remains above the Supertrend support at approximately $0.00000444.

The indicator recently flipped from bearish to bullish following the breakout. Losing that level on a daily closing basis would reverse the improvement and increase the chance of a decline toward $0.0000042.

Average Directional Index, or ADX, has risen to 31.03 from below 20. An ADX reading above 25 generally points to a strengthening trend, although the indicator does not determine whether that trend will remain bullish or turn bearish.

For bulls, the next confirmation would require a move above $0.0000049, followed by a successful recovery of $0.0000052. Breaking the rally peak near $0.0000058 would reopen the path toward $0.0000060 and the May resistance zone around $0.0000064.

Commenting on SHIB’s broader structure, pseudonymous analyst SHIBMortal said:

“The floor seems to be holding (so far). We are not out of the woods yet.”

The analyst described the bounce as promising but said SHIB was still testing resistance through weekly price action and relative strength.

What the setup means for US traders

SHIB’s next move may also depend on wider risk appetite during US trading hours. Meme coins generally carry higher volatility than Bitcoin and large-cap altcoins, making them more sensitive to changes in interest-rate expectations and geopolitical risk.

The immediate setup remains neutral above $0.00000444 and turns more constructive if SHIB reclaims $0.0000049. A daily close below $0.00000444 would invalidate the short-term bullish structure and place the July lows back in focus.

Bulls have preserved part of the breakout, but the failed move above $0.0000054 shows that another rally will require stronger and more persistent demand.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Circle has secured a New York trust charter to expand its state regulatory footprint.

Summary

- Circle has received a New York trust charter from the NYDFS for Circle New York Trust.

- The approval follows Circle’s recent federal trust bank authorization from the U.S. OCC under a separate regulatory framework.

- Circle said the charter strengthens oversight for its USDC business and extends its decade long relationship with the NYDFS.

According to an announcement from Circle on Friday, the stablecoin issuer has received a limited-purpose trust charter from the New York Department of Financial Services for Circle Internet Trust Company LLC, doing business as Circle New York Trust.

The approval gives Circle another regulatory authorization in New York, where the company says its global headquarters is located. Circle said the charter reinforces its compliance framework and builds on a relationship with the state regulator that began in 2015, when it became the first company to receive a BitLicense from the NYDFS.

The new authorization comes less than a month after Circle secured final approval from the U.S. Office of the Comptroller of the Currency to establish a federally supervised trust bank. While both approvals involve trust entities, they serve different regulatory roles within the U.S. financial system.

New York approval complements Circle’s federal trust bank

Earlier this month, the OCC approved the formation of First National Digital Currency Bank, N.A., which will operate as Circle National Trust under federal supervision for fiduciary digital asset custody. At the time, Circle said management of USDC reserves would remain outside the bank during its initial phase, with reserve activities expected to move later as the institution develops.

The New York charter follows a separate path. Circle had previously indicated that issuance of USDC would continue through a New York limited-purpose trust company rather than its federally chartered bank, making the latest approval an important part of its existing stablecoin structure.

In the official announcement, Circle co-founder, chairman and chief executive Jeremy Allaire said obtaining a New York trust charter had been a long-term objective because of the regulatory clarity associated with the state’s framework.

Allaire also described the NYDFS as an international standard setter for digital asset regulation and said the approval places USDC within what he called a strong and respected regulatory framework as digital dollars become more important in global finance.

Circle deepens decade-long relationship with NYDFS

Circle’s latest approval extends a regulatory relationship with the NYDFS that spans more than a decade.

The company noted that it became the first recipient of a BitLicense in 2015, making New York one of the earliest jurisdictions to supervise its digital asset business. The newly granted trust charter adds another license under the same regulator as Circle continues operating regulated stablecoin services.

Unlike the federal OCC approval, which established a national trust bank, the New York authorization is issued at the state level and governs Circle New York Trust under NYDFS oversight.

The two approvals together expand Circle’s regulatory footprint without replacing one another, as each operates under a different legal framework.

Circle continues expanding infrastructure around USDC

The trust charter arrives during a period of continued expansion across Circle’s payments and blockchain infrastructure.

As crypto.news previously reported, Circle announced on July 27 that it had acquired more than 680 IBM patent families covering nearly 1,000 issued patents worldwide. According to the company, the portfolio spans blockchain infrastructure, banking, payments, enterprise systems, insurance, supply-chain verification and secure cloud operations, with intended support for products including USDC, Circle Payments Network and Arc.

Circle did not disclose financial terms for the patent acquisition or identify which patents directly relate to stablecoin issuance or payment infrastructure.

Earlier in July, Circle also signed separate memorandums of understanding with South Korea’s Kakao Group and fintech operator Toss to explore blockchain payments, cross-border settlement and stablecoin infrastructure. According to the companies, the discussions include possible connections between future KRW-denominated digital assets, USDC and existing financial networks, although no commercial launch has been announced.

Circle has also said it does not plan to issue its own won-denominated stablecoin, instead positioning USDC as infrastructure that could connect local digital currencies with international payment networks.

The latest New York approval adds another regulatory milestone as Circle continues building its stablecoin and payments business across both U.S. regulatory frameworks and overseas partnerships.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

QuantPilot aims to simplify crypto market research by combining fragmented on-chain, market, and DeFi data into AI-assisted analysis workflows.

Summary

- QuantPilot brings AI research agents to crypto markets, combining live data, code execution, and automated analysis.

- Th platform uses AI agents and live data integrations to automate crypto market research and recurring analysis.

- QuantPilot expands AI-powered crypto research with live data connectors and scheduled analytics for traders.

Ask a crypto trader what they lack, and almost nobody says data. They have CoinGecko open in one tab, a Dune dashboard in another, DefiLlama for TVL, a Telegram channel for flow, Glassnode or CryptoQuant for on-chain, and a news feed they mostly skim. The raw material is abundant, and much of it is free.

Say someone wants to answer a fairly ordinary question: over the past two years, did stablecoin balances moving onto exchanges tend to precede rallies in mid-cap DeFi tokens, and did that relationship hold during the drawdowns? Every input needed to answer that exists publicly. Getting to an answer still means pulling exchange stablecoin flows from one API, TVL and token price history from another, aligning timestamps across sources that disagree on what a day is, deciding what counts as a mid-cap, running a correlation, and then checking whether the result survives outside the window you happened to pick.

QuantPilot, the platform 3Commas launched in April 2026 has built its crypto market research layer specifically around it. Whether the approach holds up is worth examining closely, because “AI for crypto research” is a phrase that has covered a lot of nonsense over the past two years.

Agents are not chatbots, and the difference is the whole point

A chatbot receives a question and produces text. Ask a general-purpose model about stablecoin flows, and it will write something fluent from training data that may be eighteen months stale, and it will do so with complete confidence. That is the failure mode that has made experienced traders rightly skeptical of AI research claims.

An agent works differently. It takes a goal, breaks it into steps, executes those steps against live tools, looks at what came back, and adjusts. QuantPilot’s research agents plan a task, create their own to-do lists, write and run code, work with files, and build charts. Applied to the stablecoin question above, that means the agent is not recalling anything. It is fetching current data, writing the analysis code, running it, and showing you the chart it produced.

The output is checkable. That matters more than any capability claim, because a research process you cannot audit is worthless in a market where being confidently wrong costs money.

The data layer is the part that determines quality

An agent with no data access is a chatbot with extra steps. What makes the research layer usable is what it can reach, and QuantPilot connects to its sources through MCP servers, an open standard for giving models structured access to external tools and data.

The current connectors cover CoinMarketCap for price and coin-level information, DefiLlama for DeFi metrics, CryptoQuant for on-chain Bitcoin and stablecoin data, CryptoNews API for current and historical news, and Tavily for agent-driven web search. The team has said more are being added.

The choice of MCP over bespoke integrations is a quiet but meaningful detail. It means adding a new data source is a connector, not a rebuild, which is the difference between a platform whose coverage grows and one that ships with a fixed list and stays there. If you have watched analytics tools in this space launch with impressive integrations and then stagnate, you will recognize why the architecture matters more than the launch-day feature list.

The practical effect is cross-source questions. Not “what is Bitcoin’s price”, which any tool answers, but questions that span data types. Did protocol revenue on a given chain track its token price, or diverge? Do news sentiment spikes lead or lag on-chain accumulation? Which DeFi protocols grew TVL while their token underperformed? These are the questions where an edge might actually live, precisely because they are annoying enough to compute that most people do not bother.

Scheduled research changes the shape of the work

One feature deserves more attention than it has received. QuantPilot supports scheduled automated research, so an agent can run a defined research task on a recurring basis and deliver findings without you being present.

Consider what that replaces. Most traders’ research is reactive. Something moves, they go look, they form a view, and by then the move is largely done. Scheduled research inverts that: a trader defines what they want monitored, and the analysis runs whether or not they are watching. The output arrives as a finding rather than a raw alert, which is the difference between “TVL on this protocol dropped 12%” and a note explaining that the drop tracks a single wallet’s exit rather than broad outflows.

Price alerts have existed forever and mostly train people to react to noise. A recurring analytical task is a different instrument. Whether traders actually use it well is another matter, since the discipline to define good monitoring questions is rarer than the tooling to answer them.

The line between research and a testable claim

Research that stops at “interesting” is entertainment. The reason QuantPilot’s research product sits alongside its strategy engine is that a finding can be handed to the backtesting side and turned into something with numbers attached.

That pipeline runs from an observation, to a hypothesis, to a strategy expressed in plain language, to a backtest with statistical metrics, to an optimization pass that checks whether the result holds across different market conditions, and finally to deployment. QuantPilot compiles strategies into QuantScript and deploys them to supported venues, with Hyperliquid as the first execution integration. Anyone tracking the growth of Hyperliquid and on-chain perpetuals generally will understand why that venue was chosen first.

It is worth separating this from the automated trading bots most traders already know. A DCA or grid bot is a template with parameters, and it executes a strategy someone else designed. The research pipeline is upstream of that. It is concerned with whether the trader’s particular idea has ever worked, not with running a standard pattern efficiently. Both have their place, and confusing them is how people end up running a grid bot into a trend and wondering why it bleeds.

The value of the pipeline is not automation. It is that it makes the honest step, testing the idea before risking money on it, the path of least resistance. Most retail losses come from skipping that step entirely.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

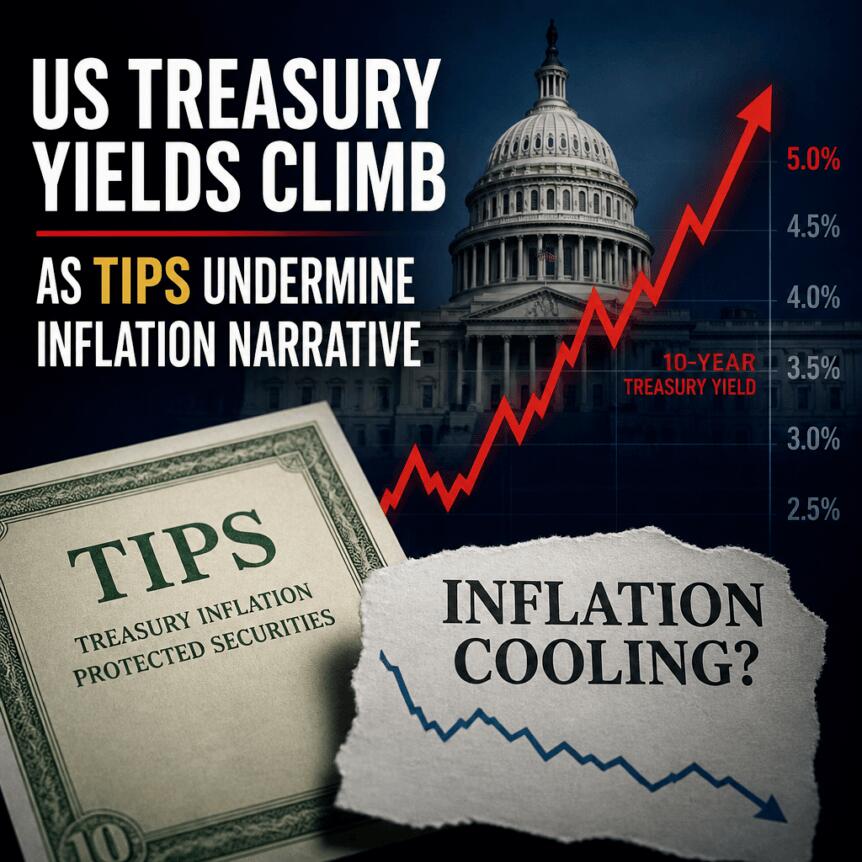

US Treasury yields have been rising for months, and the market’s latest move has pushed 30-year rates to their highest level since 2007. While mainstream coverage has largely pinned the sell-off on inflation concerns tied to higher energy prices, analysis of inflation-protected bonds suggests the more important driver is the climb in real yields—an outcome that can be especially challenging for assets that don’t pay investors along the way, including Bitcoin.

The shift is also changing the trade-offs between traditional fixed-income strategies and crypto exposure. According to Glassnode’s latest research, government bond investments have become more profitable than certain cash-and-carry style trades in crypto markets for the first time since 2019.

Key takeaways

- 30-year Treasury yields have surged to the highest levels since 2007 amid a multi-month sell-off in government debt.

- Market pricing for a September rate hike is elevated, with CME FedWatch placing the probability at 63%.

- Treasury Inflation-Protected Securities point to falling five-year inflation expectations (around 2.2% and trending down since May), even as nominal yields rise.

- Data indicates the nominal yield increase is driven more by rising real yields than by higher inflation expectations—typically a headwind for non-yielding assets.

- Multiple potential transmission channels to crypto exist, but the direction is generally bearish if higher real rates reflect weaker growth or tighter liquidity.

Why Treasuries are selling off again

After US government debt yields hit local lows in early March, Treasuries have entered a prolonged period of selling. Following the most recent FOMC meeting, 30-year Treasury yields made headlines by reaching levels not seen since 2007. Within the same window, the two-year yield climbed by 76 basis points, and markets increasingly price another Fed move: a September rate hike is currently weighted at 63% according to CME FedWatch.

The higher the yield environment becomes, the more investors compare alternatives across asset classes. Glassnode’s research—published in its “The Week Onchain” series—notes that, for the first time since 2019, returns from government bond investments have become more attractive than cash-and-carry style trades involving crypto futures.

Inflation fears are loud, but TIPS tell a different story

Many observers have connected the bond sell-off to rising commodity and energy prices. The timing overlaps with the start of the Iran war and the resulting closure of the Strait of Hormuz, and the daily moves in oil and interest rates have tracked each other since March. In that framing, stronger crude prices feed directly into inflation expectations, pushing yields higher.

However, inflation-protected securities complicate that narrative. Treasury Inflation-Protected Securities (TIPS) are designed so their principal—and therefore their coupon payments—are adjusted to reflect the Consumer Price Index. Because TIPS exist alongside regular Treasuries of similar maturity, comparing their yields allows investors to estimate the market’s implied inflation path through the breakeven rate.

According to data referenced from FRED, the five-year breakeven inflation rate has dropped sharply since May and is currently around 2.2%. That figure suggests the market expects the Fed to achieve its 2% inflation target over the medium term. More importantly, the breakeven rate has been moving in the opposite direction to nominal Treasury yields: while nominal yields rise, the inflation component implied by TIPS declines.

In the dataset cited, a 33-basis-point increase in the five-year nominal yield is paired with an 84-basis-point rise in the real yield, partially offset by a 51-basis-point decline in expected inflation. In other words, the market’s “real yield” story is changing—and it is the real rate that appears to be doing the heavy lifting.

What higher real yields can mean for Bitcoin and other non-yielding assets

In general, when real returns on traditional investments rise—after adjusting for CPI—investors may prefer assets that offer carry rather than those that do not. Bitcoin is typically treated as a non-yielding asset in this framework, so the direction of travel in real rates can matter.

Still, the impact on crypto depends on why real yields are moving higher. The analysis outlines several mechanisms that can coexist, with different implications for liquidity and demand.

1) FX or reserve liquidation pressures: unclear for crypto

One possible explanation involves global currency and funding dynamics. Higher oil prices can worsen trade balances for energy importers in Asia because oil is priced and settled in US dollars. That can lead to pressure in offshore US-dollar funding markets and force central banks to intervene to defend exchange rates.

The discussion cites Cointelegraph coverage of yen defense and Bloomberg reporting on interventions involving the Philippine peso and Indian rupee. It also notes that these interventions can be funded by selling US Treasury reserves, which can increase upward pressure on yields. In this scenario, the bond sell-off may reflect external funding strain rather than a direct verdict on the dollar or inflation.

As a result, the direct implications for crypto are not automatic: if the driver is more about FX mechanics than about deteriorating growth expectations, crypto’s reaction could be muted or different from the classic “rates up, risk assets down” story.

2) Demand destruction and recession risk: bearish setup

Another pathway is growth damage. If an oil shock persists long enough, the argument goes, it stops being merely inflationary and begins to suppress economic output. Neuberger Berman’s fixed-income outlook—referenced in the analysis—suggests investors may be underpricing how sustained energy costs could hit output.

That matters because a recessionary environment typically tightens liquidity. In such conditions, both equities and Bitcoin can face pressure as credit conditions worsen and risk appetite declines. The analysis also points to the expectation of widening credit spreads as a sign that credit could deteriorate.

It further references Cointelegraph reporting on early signals of stress, connected to rising costs to insure AI-linked debt amid an Asian semiconductor pullback. While that example is specific, it underscores the broader theme: if credit markets begin to price higher risk, non-yielding and speculative assets often struggle.

3) Capital competition from AI issuance: another headwind

A third channel is that higher real rates may be tied to expected growth and capital demand—especially from the AI sector. The analysis argues that as corporate bond issuance, including from major AI-related players, becomes unusually large, government issuance competes more directly for investor capital.

Goldman Sachs Research is cited projecting roughly $755 billion of AI capex in 2026 and about $920 billion in 2027. UBS is also cited as raising its 2026 investment-grade issuance forecast to $1.8 trillion, with technology supply lifted to $360 billion based on hyperscaler guidance. In that environment, investors’ willingness to allocate incremental capital to crypto could be constrained, not necessarily because crypto is “bad,” but because the fundraising pipeline elsewhere is intense.

What to watch next

For crypto investors, the critical question is whether TIPS-implied breakevens stabilize while real yields remain elevated—or whether the market reinterprets the move as a growth scare. Watching the evolution of TIPS breakevens and real-yield dynamics, alongside credit conditions such as spreads, may provide the clearest signal on whether this bond sell-off turns into a sustained liquidity headwind or fades as a temporary funding/energy-driven episode.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

XRP ETF inflows surpass $1.5 billion as investors explore alternative digital asset strategies, including cloud mining and DeFi yield platforms.

Summary

- Rising XRP ETF inflows are boosting interest in EX DeFi as investors explore cloud mining and yield opportunities.

- As XRP ETF inflows top $1.5 billion, EX DeFi highlights cloud mining as an alternative way to earn on XRP holdings.

- Institutional demand lifts XRP ETF inflows past $1.5 billion, while EX DeFi promotes long-term crypto yield solutions.

The XRP-backed ETF has just surpassed a significant milestone in inflows, further boosting institutional investor confidence. Simultaneously, a growing number of investors are turning their attention to ex-DeFi, hoping to explore more long-term yield opportunities beyond simply waiting for XRP prices to rise.

The continued inflows into the XRP ETF further demonstrate the growing demand for XRP from institutional investors. While retail investors remain cautious due to market volatility and price uncertainty, institutional funds continue to allocate XRP through regulated financial products, keeping it one of the most watched mainstream digital assets in the market.

As the regulatory environment and funding conditions continue to improve, many investors are beginning to consider a practical question: are there more efficient and sustainable ways to participate in the long-term returns of XRP besides waiting for prices to rise?

The milestone of XRP ETF inflows surpassing $1.5 billion is significant.

As of the closing on July 29, the XRP spot ETF market has reached a significant milestone. According to data released by the analytics platform uToday, driven by continuous net inflows, XRP-related exchange-traded funds (ETFs) have seen cumulative inflows exceeding $1.5 billion.

Meanwhile, the overall market liquidity has continued to improve. Although secondary market trading activity has slowed somewhat, and retail investor sentiment remains relatively cautious, institutional investor allocation demand has remained stable, resulting in net inflows on most trading days.

A new option for XRP investors: The yield growth path of EX DeFi

In light of this trend, more and more XRP investors are turning their attention to EX DeFi, exploring more stable and sustainable yield models through cloud mining and yield aggregation mechanisms.