Crypto World

What is a bridge asset? How XRP and XLM are meant to move value

A bridge asset is a cryptocurrency used as a neutral middle step to move value between two different currencies without pre-funding accounts in each one. XRP and XLM were both built for this job. Here is how a bridge asset works, the problem it solves, and the hard question of whether being a bridge makes a token valuable.

Summary

- A bridge asset is a cryptocurrency used as a neutral intermediary to convert one currency into another, source currency into bridge asset into destination currency, without holding pre-funded accounts in every currency.

- The problem it solves is the cost of traditional cross-border payments, where banks must lock up capital in pre-funded accounts around the world; a bridge asset frees that capital by settling in seconds.

- XRP and XLM are the two most prominent bridge assets, designed respectively for Ripple’s payment network and the Stellar network, both aiming to move value between currencies quickly and cheaply.

- The hard question is whether serving as a bridge creates lasting demand for the token, because a bridge asset is held only momentarily during a transfer, a tension known as the velocity problem.

- Stablecoins increasingly compete as bridge instruments, offering price stability that a volatile bridge token cannot, which complicates the long-term value case for bridge assets.

A bridge asset is a cryptocurrency that serves as a neutral intermediary for moving value between two different currencies, allowing a sender to convert from one currency into the bridge asset and then out into another currency, without needing to hold pre-funded balances in each currency along the way. The idea sits at the heart of one of crypto’s oldest and most practical use cases, cross-border payments, and it is the design purpose behind two of the largest cryptocurrencies by market value, XRP and XLM.

In a world where moving money across borders is slow, expensive, and capital-intensive, a bridge asset promises a faster and cheaper path: instead of a bank needing accounts pre-funded with local currency in every country it pays into, it can convert the source currency into a bridge asset, send that asset across a blockchain in seconds, and convert it into the destination currency on the other side. The bridge asset is the universal middle step, the common denominator that connects any currency to any other without requiring a direct relationship between them.

Understanding the bridge-asset concept is the key to understanding what XRP and XLM were actually built to do, and also to understanding the central debate about whether that role makes them valuable. This guide explains what a bridge asset is and the specific problem it solves, how the mechanics work step by step, how XRP and XLM each implement the idea, a worked example of a cross-border payment, the crucial difference between a bridge asset and a cross-chain bridge, and then the hard part: the unresolved question of whether being a bridge asset creates sustained demand for a token, including the velocity problem and the growing competition from stablecoins.

The aim is to give you both the clear mechanical picture and the honest analytical debate, because the bridge-asset story is genuinely useful technology wrapped around a genuinely contested investment thesis, and you cannot understand one without the other. This is educational material, not investment advice.

The problem a bridge asset solves

To see why a bridge asset is useful, you have to understand the problem with how cross-border payments traditionally work, because the bridge asset is an answer to a specific and expensive inefficiency. When money moves across borders through the conventional banking system, it travels through a network of correspondent banks, each holding accounts with the others. To pay out in a foreign currency, a bank typically needs a pre-funded account in that currency, sitting in a bank in the destination country, a setup known in the industry as nostro and vostro accounts.

The bank fills these accounts in advance with the local currency so that when a payment needs to be made, the money is already there to send. Multiply this across every currency and every corridor a large bank operates in, and the result is enormous amounts of capital locked up around the world, sitting idle in pre-funded accounts purely so that payments can be made when needed. That trapped capital has a cost, and it is one of the reasons cross-border payments are expensive, slow, and inaccessible to smaller players.

A bridge asset attacks this problem directly by eliminating the need for pre-funding. Instead of holding local currency in an account in the destination country, an institution can convert the source currency into the bridge asset at the moment of payment, send the bridge asset across a blockchain to the destination in a matter of seconds, and convert it into the local currency there, where it is paid out. Because the whole round trip happens almost instantly, there is no need to keep capital parked in advance; the liquidity is sourced and settled on demand. This is the core promise of a bridge asset: it replaces pre-funded, idle capital with just-in-time conversion, freeing up the money that would otherwise be locked in nostro accounts and making cross-border settlement faster and cheaper.

A neutral bridge asset is especially powerful because it does not belong to any one country or currency, so it can connect any pair of currencies without requiring a direct trading relationship between them. Rather than maintaining liquidity between every possible pair of currencies, which grows impossibly complex as you add currencies, institutions only need liquidity between each currency and the single common bridge. The bridge asset becomes the hub that every spoke connects to.

How the mechanics work

The mechanics of a bridge-asset payment follow a consistent pattern regardless of which asset is used, and walking through the steps shows why speed is everything. The process begins when a sender wants to move value from a source currency to a destination currency.

First, the source currency is converted into the bridge asset, typically on an exchange or liquidity venue in the source market, turning, say, dollars into the bridge token at the current market rate.

Second, the bridge asset is transferred across its blockchain from the source side to the destination side, a step that takes seconds on the networks designed for this purpose.

Third, on the destination side, the bridge asset is converted into the local currency at a liquidity venue in that market, turning the token into, say, pesos or euros, which are then paid out to the recipient.

The entire sequence, convert in, transfer, convert out, completes in seconds rather than the days a traditional cross-border transfer can take. The reason speed matters so much is that it is what makes pre-funding unnecessary, and it also limits the risk of holding the bridge asset. Because the bridge token is only held for the few seconds between conversion in and conversion out, the parties are exposed to its price for only a moment, which limits the risk that the token’s volatility moves against them during the transfer. This is essential, because bridge assets like XRP and XLM are themselves volatile cryptocurrencies, and no institution would want to hold a volatile asset for long simply to make a payment.

The design solves this by minimizing the holding time to near zero. It also depends on deep liquidity at both ends: there must be enough of a market to convert the source currency into the bridge asset, and the bridge asset into the destination currency, without large price slippage, which is why bridge-asset systems concentrate on building liquidity in the corridors they serve. When liquidity is deep and the transfer is fast, the bridge-asset path can be cheaper and faster than the correspondent-banking alternative. When liquidity is thin, the conversions become expensive and the advantage erodes, which is one of the practical limits of the model and one reason adoption has concentrated in specific corridors rather than spreading evenly everywhere.

How XRP and XLM implement the idea

XRP and XLM are the two most prominent bridge assets, and although they share the core concept, they come from related but distinct lineages. XRP is the native asset of the XRP Ledger and is the bridge asset used by Ripple’s cross-border payment offering, where it functions as the intermediary for sourcing liquidity on demand instead of pre-funding destination accounts. Ripple’s branded implementation of this, its on-demand liquidity service, is the productized version of using XRP as a bridge between currencies for institutional payments, and it is the clearest real-world deployment of the bridge-asset concept at scale.

The XRP Ledger settles transactions in a few seconds with very low fees, which are the properties a bridge asset needs, and XRP’s entire original design rationale was to serve as this neutral settlement intermediary between currencies. When people describe XRP as a “bridge currency,” this is what they mean: an asset meant to sit in the middle of cross-border value transfers, converted in and out within seconds.

XLM, the native asset of the Stellar network, was designed with a closely related purpose, and Stellar’s architecture makes the bridge role especially explicit. Stellar was built to move money between currencies cheaply, with a particular focus on payments, remittances, and financial inclusion. On Stellar, institutions called anchors issue tokens that represent fiat currencies, backed by reserves, and the network includes a built-in decentralized exchange and a feature called path payments that automatically finds the cheapest route to convert one asset into another. XLM serves as a bridge in this system, a neutral asset that can connect currency pairs that lack a direct market, and it is also used to pay the network’s small transaction fees.

So both assets are built around the same fundamental idea, a fast, cheap, neutral intermediary for moving value between currencies, but XRP is most associated with institutional, bank-facing cross-border payments through Ripple, while XLM is most associated with a more open, anchor-based network oriented toward payments and financial inclusion. Both illustrate the bridge-asset concept in production, and both face the same hard question about whether the role translates into lasting token value.

A worked example

Trace a single payment to make the concept concrete. Imagine a business in the United States needs to pay a supplier in Mexico the equivalent of $10,000, and consider how this works with and without a bridge asset. In the traditional model, the US business’s bank would rely on having a pre-funded account holding Mexican pesos at a bank in Mexico, or on a chain of correspondent banks that do. The payment instruction passes through this chain, the pesos are paid out from the pre-funded account, and the whole process can take one to several business days, with fees taken at multiple points and a large amount of peso liquidity sitting idle in that account at all times to make such payments possible. The cost of that idle capital, plus the intermediary fees, is what makes the traditional transfer expensive.

In the bridge-asset model, the same payment takes a different path. The $10,000 is converted into a bridge asset, say XRP or XLM, on a liquidity venue in the United States, turning dollars into the token at the current rate. The bridge asset is then sent across its blockchain to Mexico in a matter of seconds. On the Mexican side, the bridge asset is immediately converted into pesos on a local liquidity venue, and the pesos are paid out to the supplier.

The entire round trip completes in seconds, and at no point did anyone need to keep pesos pre-funded in advance, because the liquidity was sourced on demand at the moment of payment. The business’s bank did not need idle peso capital sitting in Mexico; it converted exactly what it needed, exactly when it needed it. If the liquidity on both ends is deep, the total cost of the two conversions plus the tiny network fee can be lower than the traditional route, and the settlement is far faster. This is the bridge asset doing its job: replacing days and pre-funded capital with seconds and just-in-time conversion. The token was held for only the few seconds of the transfer, which is the whole point of the design, and also, as the next sections explain, the source of the central debate about its value.

Bridge asset versus cross-chain bridge

A crucial point of confusion deserves its own section, because the word “bridge” is used in two very different ways in crypto and conflating them leads to real misunderstanding. The bridge asset described in this guide is about moving value between currencies, an asset used as a neutral intermediary to convert one currency into another in a payment. A cross-chain bridge, by contrast, is about moving tokens between blockchains, a piece of infrastructure that lets you take a token on one blockchain and represent or transfer it onto a different blockchain, for example moving an asset from Ethereum to another network. These are entirely different concepts that happen to share a word. A bridge asset is a currency playing a role in a payment; a cross-chain bridge is software connecting two blockchains, often by locking a token on one chain and minting a wrapped version on another.

The distinction matters for several reasons. First, the risks are completely different. Cross-chain bridges have been among the most exploited pieces of infrastructure in crypto, with several large hacks resulting from vulnerabilities in the smart contracts that lock and mint tokens across chains, so “bridge risk” in that context refers to the security of that connecting infrastructure. A bridge asset used in a payment carries different risks, mainly the price volatility of the token during the brief moment it is held and the depth of liquidity on each side, not smart-contract exploit risk of a chain-connecting bridge.

Second, the purpose is different: a bridge asset answers “how do I move value from one currency to another,” while a cross-chain bridge answers “how do I move a token from one blockchain to another.” When you read about XRP or XLM as bridge assets, the meaning is the currency-to-currency payments sense, not the chain-to-chain infrastructure sense. Keeping the two ideas separate is essential to understanding both the technology and the risks, because a discussion that mixes them will mislead on both. The shared word is an unfortunate accident of terminology, and the careful reader learns to ask which kind of bridge is meant.

Does being a bridge asset make a token valuable?

Now the hard question, the one that turns a clean technical story into a truly contested investment debate: does serving as a bridge asset actually create lasting demand for the token, and therefore support its value? The intuitive answer is yes, surely a token used to move large volumes of cross-border payments must capture value from that usage. But the reality is more complicated, and the complication has a name: the velocity problem.

A bridge asset, by design, is held for only the few seconds of a transfer. It is bought, used, and sold almost instantly, never accumulated. High transaction volume through a bridge asset therefore does not necessarily translate into sustained holding demand, because the same units of the token can be reused over and over for many transfers without anyone needing to hold a growing stockpile. A token can process enormous payment volume while generating little persistent demand to own it, because payments require the token to flow through, not to be held. This is the core tension in the bridge-asset value thesis, and it is why critics argue that network usage and token price can diverge: the network can be busy while the token is weak.

There is a serious counterargument, and the honest treatment gives it weight. Proponents contend that very large and growing payment volume does require deeper liquidity pools at every conversion point, and that maintaining those pools effectively takes a meaningful float of the token out of circulation, creating a baseline of demand that scales with usage. They argue that if a bridge asset became the settlement layer for a significant share of global cross-border value, the liquidity required to support that volume without slippage would be substantial and persistent, supporting the token’s value even if no individual holder keeps it for long.

The debate, then, is between the velocity critique, which says payments flow through without creating holding demand, and the liquidity-depth argument, which says sufficient scale forces a persistent float. Layered on top is a growing competitive threat: stablecoins. A stablecoin pegged to a currency can serve as a bridge instrument too, moving value between parties quickly, and it offers something a volatile bridge token cannot, price stability, so neither sender nor receiver bears volatility risk during the transfer.

As regulated stablecoins proliferate, including ones issued by the very companies behind bridge-asset networks, some of the cross-border settlement role that bridge tokens were meant to fill may flow to stablecoins instead, which would weaken the demand case for the volatile bridge asset. None of this is settled, and a careful reader should hold all of it at once: the bridge-asset technology is real and useful, the velocity problem is a genuine challenge to the token-value thesis, the liquidity-depth rebuttal is a legitimate counter, and stablecoin competition is a real and growing complication. The mechanism works; whether it makes the token valuable is the open question.

Frequently Asked Questions

What is a bridge asset in crypto?

A bridge asset is a cryptocurrency used as a neutral intermediary to move value between two different currencies. Instead of converting one currency directly into another, or keeping pre-funded accounts in every currency, a sender converts the source currency into the bridge asset, sends that asset across a blockchain in seconds, and converts it into the destination currency on the other side. The bridge asset is the common middle step that can connect any currency to any other without a direct relationship between them. XRP and XLM are the two most prominent examples, both designed to make cross-border payments faster and cheaper by replacing idle pre-funded capital with just-in-time conversion through the bridge token.

How is XRP used as a bridge asset?

XRP is the native asset of the XRP Ledger and serves as the bridge in Ripple’s cross-border payment system. Instead of a bank pre-funding accounts with local currency in every destination country, it can convert the source currency into XRP, send the XRP across the ledger in a few seconds at very low cost, and convert it into the destination currency on arrival. Ripple’s branded version of this is its on-demand liquidity service, the productized use of XRP as a settlement bridge for institutional payments. XRP’s original design purpose was exactly this neutral-intermediary role, which is why it is described as a bridge currency: an asset meant to sit briefly in the middle of cross-border value transfers.

Is XLM the same as XRP?

They share the same core idea but are distinct assets on distinct networks. XLM is the native asset of the Stellar network, which was built to move money between currencies cheaply with a focus on payments, remittances, and financial inclusion. On Stellar, institutions called anchors issue fiat-backed tokens, and the network’s built-in exchange and path-payment feature find the cheapest route to convert one asset into another, with XLM serving as a bridge between pairs that lack a direct market and paying the network’s small fees. XRP, by contrast, is most associated with institutional, bank-facing cross-border payments through Ripple. Both are bridge assets built around fast, cheap, neutral settlement, but they come from different networks with different emphases.

What problem does a bridge asset solve?

It solves the cost and slowness of traditional cross-border payments, specifically the need to pre-fund accounts. In the conventional system, a bank must keep accounts filled in advance with local currency in every country it pays into, known as nostro and vostro accounts, which locks up enormous amounts of capital sitting idle around the world. A bridge asset removes this need by sourcing liquidity on demand: the institution converts into the bridge asset and out into the destination currency at the moment of payment, in seconds, so no capital has to sit pre-funded. This frees up trapped liquidity and can make cross-border settlement faster and cheaper, which is the central promise of the bridge-asset model.

Does high payment volume make a bridge asset valuable?

Not necessarily, and this is the central debate. A bridge asset is held for only the few seconds of a transfer, so it is bought, used, and sold almost instantly instead of accumulated. This means high payment volume does not automatically create sustained demand to hold the token, because the same units can be reused for many transfers, a tension known as the velocity problem. Proponents counter that very large volume requires deeper liquidity pools, which take a meaningful float out of circulation and create demand that scales with usage. The question is unresolved, and it is complicated further by stablecoins, which can serve as bridge instruments too while offering price stability a volatile token cannot.

Is a bridge asset the same as a cross-chain bridge?

No, and confusing them is a common error. A bridge asset is a currency used to move value between two different currencies in a payment. A cross-chain bridge is infrastructure that moves tokens between two different blockchains, often by locking a token on one chain and minting a wrapped version on another. They share the word “bridge” but are entirely different concepts with different risks. Cross-chain bridges have been frequently exploited through smart-contract vulnerabilities, so their risk is about infrastructure security, while a bridge asset’s risks are mainly the token’s price volatility during the brief holding period and the depth of liquidity on each side. When XRP or XLM are called bridge assets, the meaning is the currency-to-currency payments sense.

This article is educational information, not financial or investment advice. Descriptions of XRP, XLM, and their networks reflect their design and general operation as understood in mid-2026 and can change. Nothing here is a recommendation about any asset, and the question of whether bridge assets accrue value is truly contested. Cryptocurrency is volatile, and you can lose money. Do your own research and consult a qualified professional before making any decision.

Key Takeaways

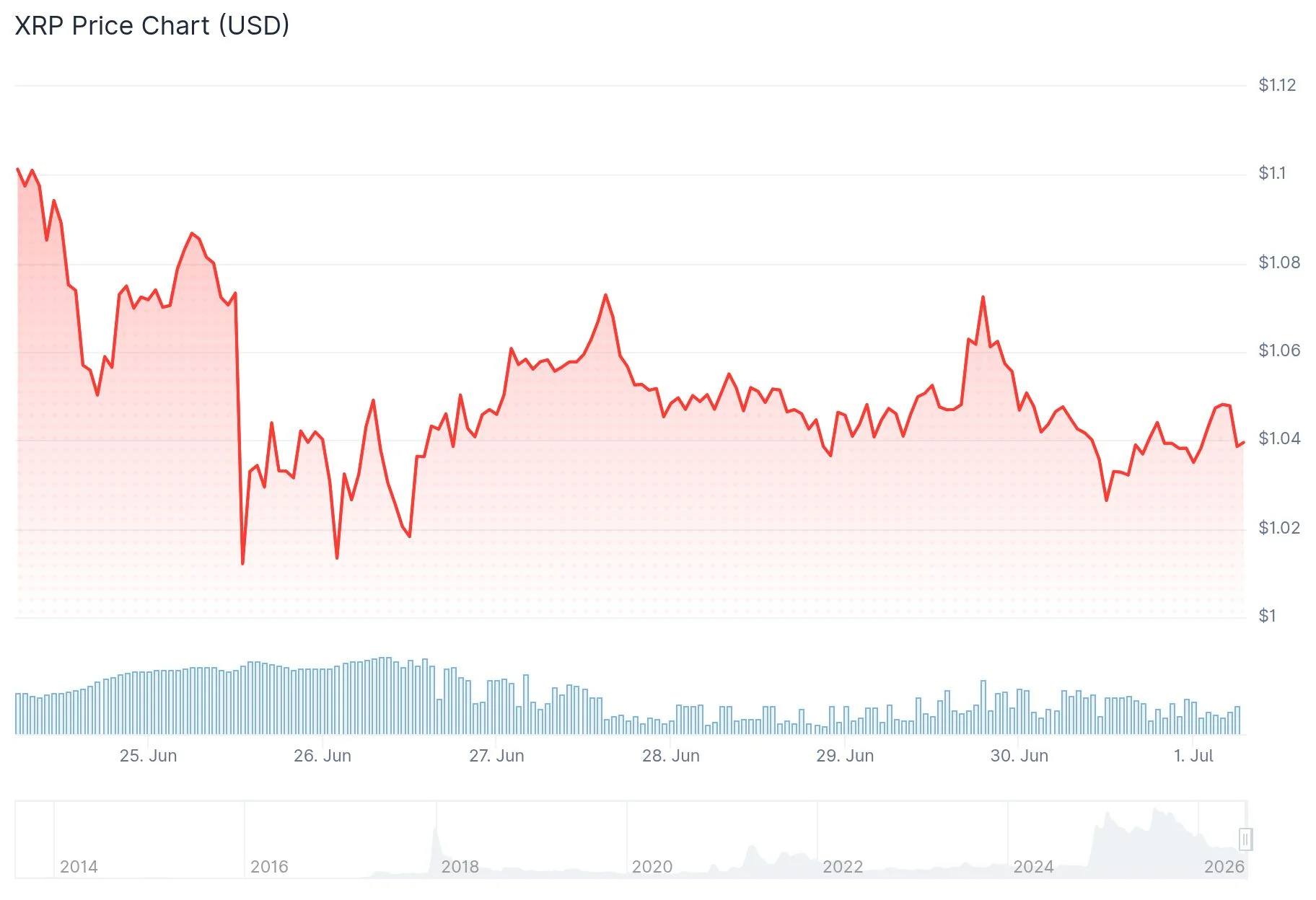

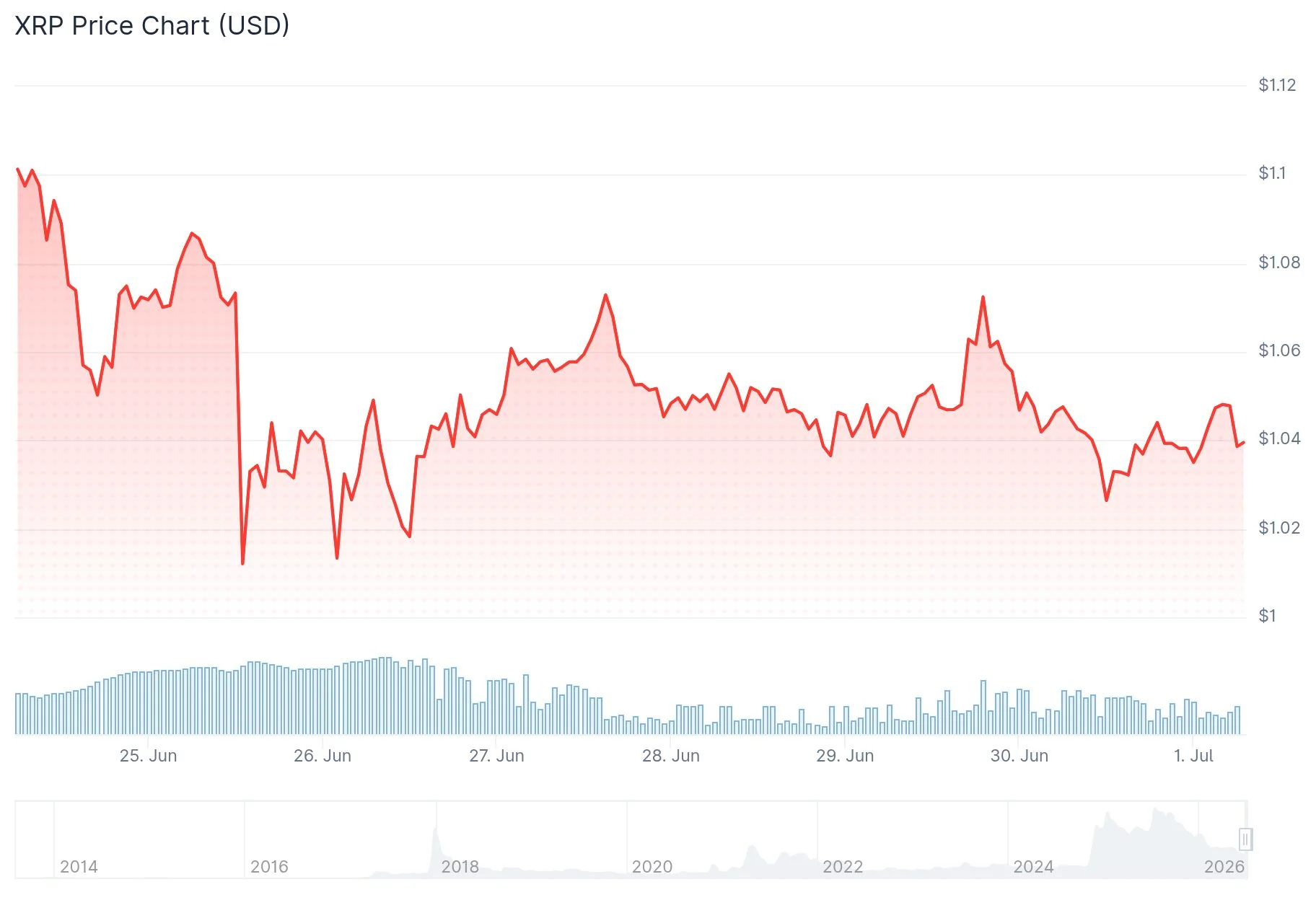

- On June 26, XRP touched $1.009, marking its lowest level since November 2024

- Despite the price decline, XRP spot ETF inflows remained in positive territory

- Technical analysis reveals a sustained downtrend originating from July 2025

- Open Interest has found equilibrium around 400 million XRP, indicating reduced speculative fervor

- Bullish divergence patterns on daily timeframes hint at potentially weakening bearish momentum near the $1 threshold

On June 26, 2026, XRP declined to $1.009, representing the token’s lowest point since it last visited these levels in November 2024.

The decline occurred against a backdrop of continuing positive flows into XRP spot exchange-traded funds. Market participants continued accumulating through these investment vehicles despite downward price momentum.

While ETF accumulation reduces circulating supply available for trading, this dynamic has yet to catalyze upward price movement given prevailing market sentiment.

Overall market appetite for XRP has diminished considerably over recent months, accompanied by a notable contraction in speculative trading activity.

Technical Analysis Overview

The daily timeframe reveals XRP locked in a downward trajectory that originated in July 2025. The decisive break beneath the April 2025 swing low at $1.61, which occurred in February, validated the bearish market structure.

Following this breakdown, XRP consolidated within a defined range for multiple months. Late May witnessed an aggressive selling wave that shattered this consolidation pattern and accelerated the downside move.

A temporary recovery pushed prices toward $1.30 before momentum faded, leaving XRP hovering around $1.05.

Futures market data indicates Open Interest has stabilized at approximately 400 million XRP. The corresponding Open Interest Turnover Ratio has maintained levels near 0.71.

According to analyst Arab Chain, market participants should monitor these indicators for sudden increases. Rapid expansion in either Open Interest or turnover ratio typically precedes elevated volatility periods.

Examining the 4-hour chart, XRP rallied to $1.2935 during mid-June. This advance reached the 78.6% Fibonacci retracement zone around $1.2985 before encountering renewed selling pressure.

Should the bearish trajectory persist, potential downside objectives emerge at $0.975 and $0.854. Market probabilities favored a breach below $1 during July.

Potential Support Dynamics

An alternative technical interpretation presents a more constructive outlook. XRP has consistently rebounded from the $0.90-$1.00 zone, establishing this region as durable support through multiple challenges.

The $1.13 level has transitioned from support into resistance. A successful reclaim of this threshold would indicate emerging bullish momentum.

A bullish divergence pattern on daily charts has persisted for approximately one week. Such formations typically suggest diminishing selling intensity rather than imminent capitulation.

On social platforms, trader Celal Kucuker stated XRP should maintain current support levels and projected a potential climb to $10 within the next twelve months, acknowledging significant volatility along that path.

Technical analyst ChartNerd identified a repeating accumulation structure observed during previous bear cycles, highlighting historical drawdowns ranging from 85% to 96% spanning 14 to 37 months, contrasting with the current 72% retracement over 11 months.

The immediate focus centers on the $1.00 threshold. Maintaining this level preserves the possibility of retesting $1.13 resistance, while a breakdown would expose the $0.87-$0.90 support zone.

Crypto World

What is OpenUSD (OUSD)? Visa, BlackRock, Coinbase, and 140+ Firms Fuel Buzz Around New Stablecoin

Open USD (OUSD) stablecoin has emerged as one of the crypto market’s biggest trending topics after the project drew attention with the announcement of a consortium-backed stablecoin initiative involving more than 140 companies.

Developed by Open Standard, the stablecoin is expected to go live later this year.

Open USD Frenzy

According to the latest findings by Santiment, the scale of participation from major financial and crypto firms has fueled massive discussion across the market. The initiative has attracted some of the biggest names in the industry, making it one of the most talked-about developments in addition to discussions surrounding ANSEM whale activity and Markets in Crypto-Assets (MiCA) licensing.

“The crowd is also debating custody, transparency, liquidity, and whether another major stablecoin can truly compete with USDC and USDT. Either way, the spike in attention shows the market is taking this launch seriously.”

The growing interest follows the official unveiling of OUSD by Open Standard, an independent organization that will oversee the stablecoin. According to the official blog post, Open USD is designed to support global money movement while addressing several issues businesses face when using existing stablecoins.

While stablecoins have become increasingly important because they offer faster, lower-cost, and programmable digital payments, Open Standard said that many businesses still face high minting and redemption fees, limited access to revenue generated by reserve assets, and dependence on third-party issuers for future development.

To address these concerns, OUSD has been built around three core principles. First, businesses will be able to mint and redeem the stablecoin without paying fees or facing volume restrictions. Second, participating partners will receive the earnings generated from the stablecoin’s reserves after a small management fee is deducted to cover operational costs. Third, governance will be handled collectively through Open Standard, whose board will consist of partner organizations rather than a single controlling issuer.

Open Standard said this structure is intended to ensure decisions are made in the interests of the broader ecosystem. The organization also confirmed that more than 140 businesses have already signed up to support or use Open USD, including companies such as Visa, Stripe, Mastercard, American Express, Coinbase, BlackRock, BNY, Standard Chartered, Intercontinental Exchange, Bybit, Solana, Base, OKX, and Ripple.

Commenting on the development, BlackRock’s Global Head of Market Development, Samara Cohen, said,

“We believe stablecoins can play an important role in the evolution of digital markets when supported by trusted infrastructure and practical utility. Open USD is a constructive step toward giving businesses more choice in how they access tokenized value and participate in internet native digital rail.”

Bearish For Circle?

The announcement of OUSD also appeared to weigh on investor sentiment surrounding the USDC issuer, Circle. On Tuesday, CRCL shares fell 17.55% and closed at $62.63.

Former Enterprise Research Analyst at Messari, Sam Ruskin, tweeted that the new stablecoin’s model could pose a competitive challenge to USDC because of its three core design principles. He believes that OUSD’s new model could pressure Circle to expand revenue-sharing agreements, find new distribution partners, or focus on other parts of its stablecoin business.

The post What is OpenUSD (OUSD)? Visa, BlackRock, Coinbase, and 140+ Firms Fuel Buzz Around New Stablecoin appeared first on CryptoPotato.

Taiwanese lawmakers on Tuesday passed a law to establish a regulatory framework for crypto, which includes licensing and rules for stablecoins.

The country’s financial watchdog, the Financial Supervisory Commission (FSC), said that the Legislative Yuan passed the law requiring all virtual asset service providers, or VASPs, to get approval from the regulator to operate.

The law also says stablecoins issued in the country must get approval from the central bank and the FSC, and issuers must maintain sufficient reserves with a trustee and undergo regular audits.

The law is the first to regulate crypto and stablecoins in Taiwan, bringing it in line with other nations in the region, such as Japan, Singapore and Hong Kong, that have long passed laws to regulate the sector in a bid to attract the industry.

The FSC said the bill further strengthens the protection of traders’ rights and that issuing stablecoins will help Taiwan integrate with the international market and secure a place in the global crypto market.

Source: Cointelegraph

Taiwan’s rules outline seven types of VASPs, including exchanges, trading platforms, custodians and lenders, which will all be subject to rules for internal control and audits, cybersecurity systems, crypto listing and delisting rules, customer asset segregation and financial reporting.

The rules outlaw crypto-based fraud and price manipulation, with violators facing between three and 10 years in prison and fines ranging from about 10 million New Taiwan dollars ($300,000) to 200 million New Taiwan dollars ($6.3 million).

Those caught operating a VASP or issuing a stablecoin without a license face up to seven years in prison and fines of up to 100 million New Taiwan dollars ($3.1 million), Taiwan’s national news agency, CNA, reported on Tuesday.

Related: US ban on stablecoin yield could see others fill the void: Ledger exec

The implementation date of the bill is still to be determined, and the law will take effect only after it is published by the government’s executive branch.

The FSC said VASPs that complete anti-money laundering registration before the bill is implemented, and institutions that provide related services under the agency, should apply for a license within 12 months after the bill is implemented.

CNA reported that lawmakers also passed a resolution asking the FSC to propose a plan within a year outlining how the crypto industry can provide derivative crypto commodity services, with the aim of providing diversified investments and improving the sector’s health.

Asia Express: Japanese pension fund tips 1% in crypto, G7 urges action on NK hackers

Anthropic is restoring access to its two most advanced AI models after the U.S. government lifted the export controls that forced it to pull them last month.

The controls on Claude Fable 5 and Claude Mythos 5 were removed on June 30, the company said. Fable 5 returns globally on July 1 across Anthropic’s platforms, while Mythos 5, which shares the same underlying model but carries fewer safety restrictions, is being restored to a set of U.S. organizations after government approval on June 26.

The freeze dated to June 12, when the government applied export controls, rules that limit which foreign nationals can access a technology, to both models.

Because the order took effect immediately and Anthropic could not verify users’ nationality in real time, it suspended access for everyone rather than risk breaching the rule.

The trigger was a cybersecurity finding after Amazon researchers reported a way to bypass Fable 5’s safeguards, a technique known as a jailbreak, prompting the model to identify software vulnerabilities and, in one case, produce code showing how one could be exploited.

The EU’s Markets in Crypto-Assets regulation hits its final deadline today, July 1. Licensed exchanges are pulling Tether’s USDT from their platforms. Circle is stepping into the gap.

The split falls cleanly along regulatory lines. One issuer spent years building toward this deadline. The other bet Europe wasn’t worth the compliance cost.

Why Circle Is Walking Away With Europe

Circle prepared for this moment years in advance. The company secured MiCA compliance for both USDC and its euro-denominated EURC. Among the top ten stablecoins by market cap, Circle is the only issuer that cleared that bar.

Tether never applied for the e-money-token authorization MiCA requires. That decision now locks its roughly $185 billion USDT out of licensed European exchanges.

Tether’s decision wasn’t an oversight. CEO Paolo Ardoino has publicly defended the company’s stance, arguing that MiCA’s requirement to hold 60% of e-money token reserves in European bank deposits introduces its own risk. Rather than restructure its reserve model to meet that bar, Tether’s leadership has chosen to prioritize markets outside the EU.

The timing sharpens Circle’s advantage. A day before the deadline, BNY (Bank of New York Mellon) confirmed it made USDC the first stablecoin on its Digital Asset Custody platform.

Institutional clients can now store, transfer, mint, and burn USDC there. Together with the EU exchange shift, the move gives Circle regulatory validation on two continents in the same week.

A Business Story, Not Just a Compliance One

The shakeout extends well beyond stablecoins. Of the roughly 1,200 virtual-asset firms that held pre-MiCA national registrations across the EU, only around 210 converted to full CASP authorization, a conversion rate near 17%.

The more durable story is what Circle built toward for years. Regulated venues can no longer route liquidity through USDT, and Circle stands ready to absorb it. Tether may still seek authorization someday, but nothing signals that shift is coming.

The real test arrives over the next few weeks: how much EU trading volume actually migrates to USDC.

The post Circle Emerges as MiCA’s Quiet Winner While USDT Exits Europe appeared first on BeInCrypto.

For years, Bitcoin has been viewed primarily as a store of value—a digital asset designed to preserve wealth rather than actively generate it. While decentralized finance (DeFi) has transformed blockchains like Ethereum by enabling lending, borrowing, staking, and yield generation, Bitcoin has largely remained on the sidelines.

That narrative is rapidly changing.

Bitcoin Finance, commonly known as BTCFi, is emerging as one of the fastest-growing sectors in decentralized finance. By unlocking Bitcoin’s liquidity and allowing BTC holders to participate in financial applications without selling their assets, BTCFi has the potential to become the next multi-billion-dollar market.

What Is BTCFi?

BTCFi refers to the ecosystem of decentralized financial services built around Bitcoin. Rather than simply holding BTC in a wallet, users can now:

- Earn yield on idle Bitcoin

- Borrow stablecoins using BTC as collateral

- Provide liquidity to decentralized exchanges

- Participate in decentralized lending markets

- Trade Bitcoin-based assets

- Access structured financial products

- Use Bitcoin in cross-chain DeFi ecosystems

The goal is simple: transform Bitcoin from passive capital into productive capital.

Why the Timing Is Right

Several major developments have aligned to make BTCFi more viable than ever.

Bitcoin Holds Massive Untapped Liquidity

Bitcoin remains the largest cryptocurrency by market capitalization, representing hundreds of billions of dollars in value. Yet only a small fraction of this capital is actively used in DeFi.

Even modest participation from long-term Bitcoin holders could inject enormous liquidity into decentralized financial markets.

Institutional Interest Is Growing

The approval of Bitcoin exchange-traded funds (ETFs), increasing corporate treasury adoption, and rising institutional investment have strengthened Bitcoin’s position as a mainstream financial asset.

As institutions seek additional yield opportunities, BTCFi offers ways to generate returns while maintaining Bitcoin exposure.

Better Infrastructure Is Finally Here

Early attempts to bring DeFi to Bitcoin struggled due to limited programmability.

Today, new technologies are changing the landscape:

- Bitcoin Layer-2 networks

- Sidechains

- Cross-chain bridges

- Smart contract platforms secured by Bitcoin

- Native Bitcoin lending protocols

These innovations make sophisticated financial applications possible without compromising Bitcoin’s core security model.

The Rise of Bitcoin Layer-2 Networks

Scaling solutions are becoming the backbone of BTCFi.

Modern Layer-2 ecosystems enable:

- Faster transactions

- Lower transaction fees

- Smart contract execution

- Better user experiences

- Expanded developer ecosystems

These improvements create the foundation necessary for a thriving Bitcoin financial ecosystem.

New Yield Opportunities

One of BTCFi’s biggest attractions is allowing Bitcoin holders to earn passive income.

Instead of letting BTC sit idle in cold storage, users can:

- Supply liquidity

- Lend assets

- Participate in decentralized money markets

- Stake wrapped or tokenized Bitcoin in supported ecosystems

- Earn protocol incentives

This represents a significant shift from Bitcoin’s traditional “buy and hold” strategy.

Expanding Use Cases

BTCFi is moving beyond basic lending.

Emerging applications include:

- Decentralized exchanges

- Stablecoin collateralization

- Prediction markets

- Tokenized real-world assets

- On-chain derivatives

- Cross-chain liquidity protocols

- Automated yield strategies

- AI-powered financial management

As these applications mature, Bitcoin becomes increasingly integrated into the broader decentralized economy.

Why Developers Are Paying Attention

Developers are increasingly building products around Bitcoin because of its unmatched security, liquidity, and global recognition.

Innovative startups are creating:

- Native Bitcoin lending markets

- Bitcoin-backed stablecoins

- Cross-chain liquidity hubs

- Decentralized trading infrastructure

- Institutional-grade custody solutions

- Advanced financial automation tools

A growing developer ecosystem typically leads to stronger network effects and increased adoption.

Challenges Still Remain

Despite its promise, BTCFi is still in its early stages.

Some of the biggest challenges include:

- Cross-chain security risks

- Smart contract vulnerabilities

- Limited user education

- Liquidity fragmentation

- Regulatory uncertainty

- User experience complexity

Addressing these issues will be essential for sustainable long-term growth.

Why BTCFi Could Become a Multi-Billion-Dollar Industry

Several factors support BTCFi’s long-term growth potential:

- Bitcoin possesses the largest liquidity base in crypto.

- Infrastructure has matured significantly over the past few years.

- Institutional demand for Bitcoin-based financial products continues to increase.

- Developers are launching innovative protocols at a rapid pace.

- More users are seeking passive income opportunities without selling their BTC.

- Cross-chain technology continues to improve accessibility and capital efficiency.

If only a small percentage of Bitcoin’s total market value becomes actively utilized within decentralized finance, the BTCFi ecosystem could expand into one of the largest sectors in the blockchain industry.

Looking Ahead

BTCFi represents the next phase in Bitcoin’s evolution.

Instead of serving solely as digital gold, Bitcoin is increasingly becoming a productive financial asset capable of powering lending markets, liquidity pools, payments, and decentralized financial infrastructure.

While the sector remains young, its momentum is accelerating. Continued innovation in Layer-2 solutions, interoperability, security, and institutional adoption could transform BTCFi from a promising niche into a foundational pillar of decentralized finance.

For investors, developers, and long-term Bitcoin holders alike, BTCFi is more than just another trend—it is a growing movement aimed at unlocking the full economic potential of the world’s most valuable digital asset.

REQUEST AN ARTICLE

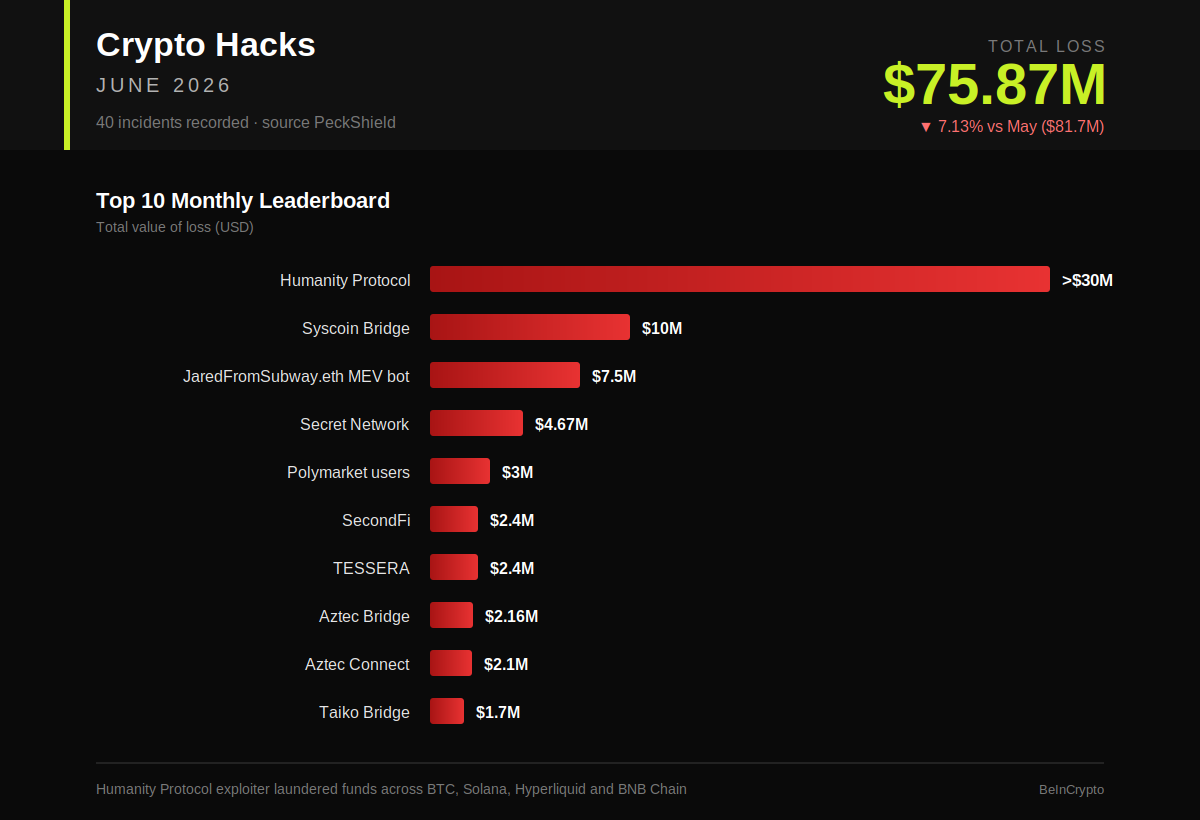

Crypto platforms lost roughly $75.87 million to 40 hacks in June 2026, according to security firm PeckShield.

The monthly total reinforces a familiar pattern for the sector, where bridges, smart contracts, and compromised keys remain the most common failure points.

Humanity Protocol Exploit Tops June Crypto Hacks

According to PeckShield, June’s figure marks a 7.13% decline from May’s $81.7 million. The Humanity Protocol breach headlined June with over $30 million in losses. Attackers compromised private keys that had been backed up to a malware-infected developer machine.

According to Quantstamp, the attacker relied on tooling and techniques commonly associated with North Korean hacking groups.

The exploiter has since laundered proceeds across multiple networks, including Bitcoin (BTC), Solana (SOL), Hyperliquid (HYPE), and BNB Chain.

These funds have also been commingled with proceeds linked to the KelpDAO exploiter, suggesting a potential overlap between the threat actors behind both incidents,” the security firm said.

Follow us on X to get the latest news as it happens

Syscoin Bridge followed with a $10 million loss after an attacker minted unauthorized SYS tokens. The JaredFromSubway.eth Maximal Extractable Value (MEV) bot lost $7.5 million, while Secret Network was drained for $4.67 million.

Aztec Products Hit Despite Years of Dormancy

Two separate attacks targeted Aztec-linked products within the month. Aztec Payments Product lost $2.16 million, and Aztec Connect lost $2.1 million, for a combined total near $4 million.

Both products had been deprecated years earlier, and Aztec Labs said it held no control over the affected systems.

Other June incidents included Polymarket users losing $3 million after reportedly being targeted in a phishing campaign, along with $2.4 million in losses for SecondFi and TESSERA. The Taiko Bridge exploit closed out the top 10 at $1.7 million.

With both deprecated code and cross-chain laundering in play, June showed that old contracts remain in attackers’ crosshairs long after teams walk away.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Hackers Steal $75.87 Million From Crypto Platforms in June 2026 appeared first on BeInCrypto.

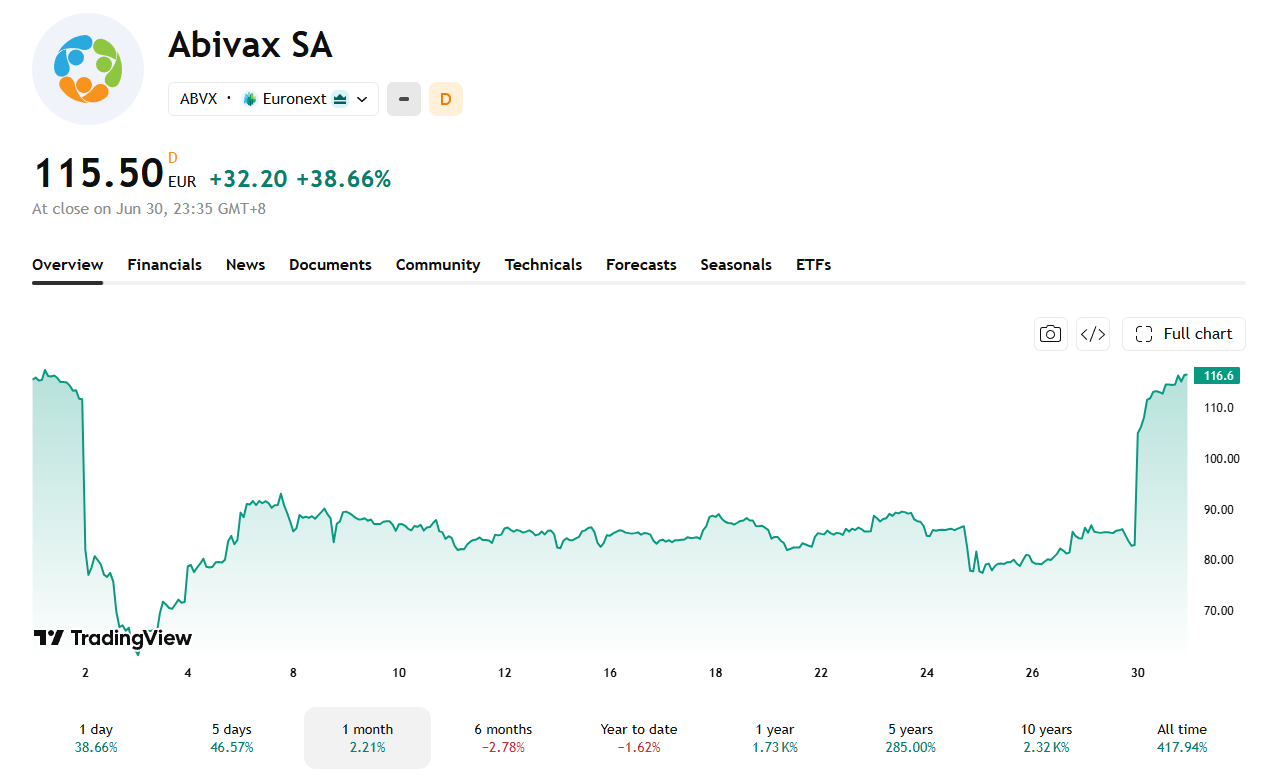

Abivax shares surged over 38% on June 30, 2026, after new Phase 3 data eased cancer-safety fears that had erased 43% of the French biotech’s value earlier in June.

The rally follows fresh results for obefazimod, Abivax’s lead ulcerative colitis drug. The data showed durable remission with no new safety signals.

A Reversed Safety Signal

Abivax’s stock crashed 43% on June 2. Early trial data had shown a rise in malignancies among patients taking obefazimod.

The company released new Phase 3 data on Sunday, June 28, covering patients who failed initial treatment. Researchers found malignancy rates within the range doctors typically see in ulcerative colitis patients. The update calmed the safety concern that triggered the June 2 sell-off.

Among patients who failed initial treatment, 37.2% reached clinical remission and 34.5% reached endoscopic remission at week 44. Those results reinforced the drug’s efficacy case in harder-to-treat patients.

Abivax shares have now climbed more than 1,730% over the past year.

Wall Street Splits on the Risk

Analysts did not agree on how much risk remains. Citizens raised its Abivax price target to $187 and kept its Outperform rating, pointing to the drug’s placebo-adjusted remission benefit.

Wedbush took a more cautious view. The firm upgraded Abivax from Underperform to Neutral but cut its price target to $90. Wedbush cited lingering malignancy questions at the 50 mg dose as a regulatory risk.

Abivax still plans to file a new drug application with the FDA in the fourth quarter of 2026. That filing will keep the stock sensitive to any additional safety data before then.

The post From Cancer Scare to Comeback, Abivax Shares Erase a Month of Losses in a Day appeared first on BeInCrypto.

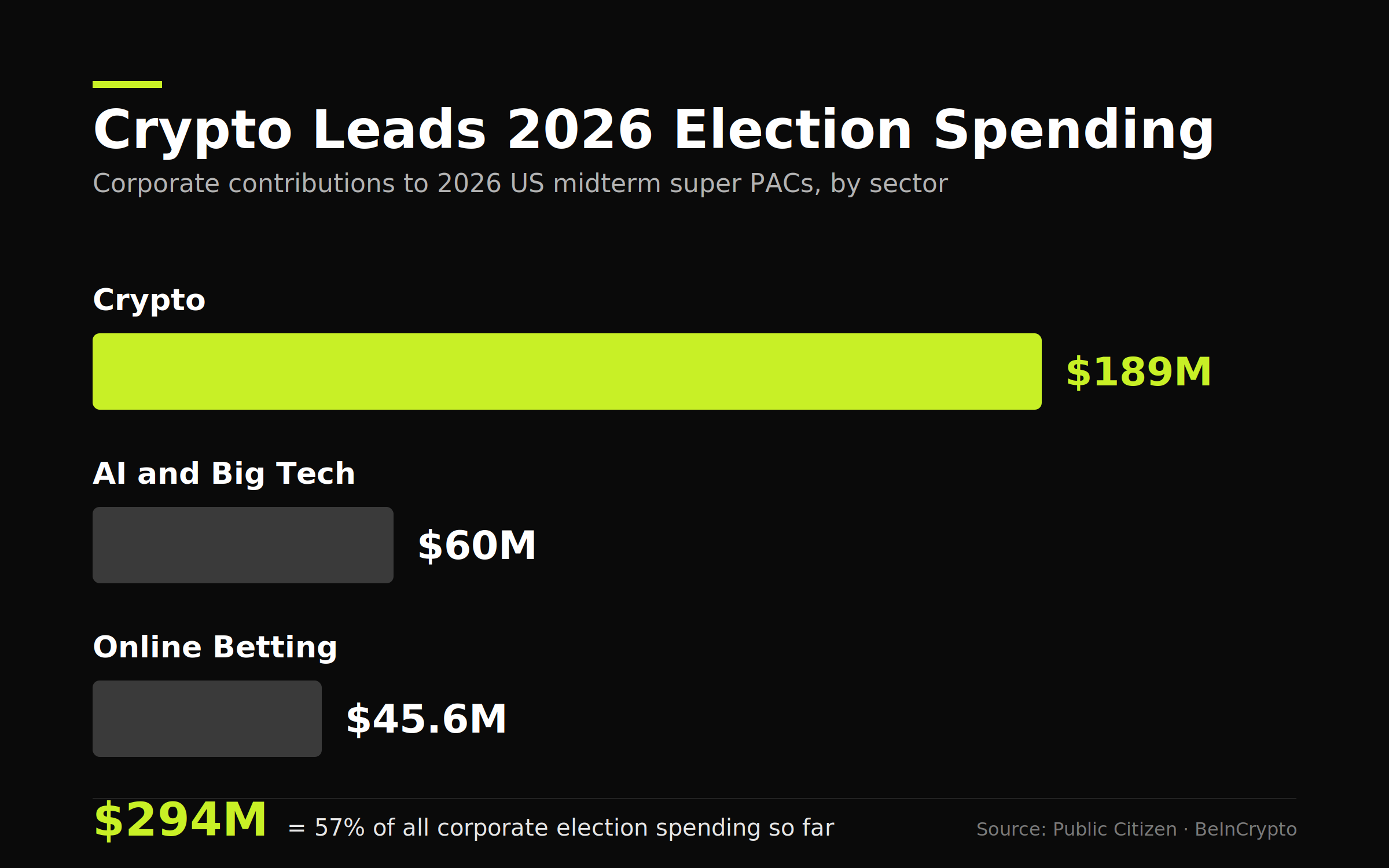

Cryptocurrency corporations have spent $189 million on the 2026 US midterm elections, roughly 37% of all reported corporate election spending, according to a Public Citizen report.

The figure keeps crypto ahead of every other industry in funding federal races this cycle. It reflects a strategy the sector introduced in 2024 that other industries now imitate.

Crypto Leads The Corporate Spending Surge in 2026 Elections

Total corporate spending on the 2026 midterms reached $517 million, according to the watchdog group. That marks a 12% rise over the $461 million corporations spent across the entire 2024 cycle.

“In the 2026 midterm elections, corporate money is poised to play a bigger role than ever before in influencing how Americans vote,” the report read.

Crypto’s $189 million exceeded the combined totals from artificial intelligence and Big Tech firms at $60 million and online betting companies at $45.6 million. Together, these sectors contributed $294 million, or 57% of all corporate spending so far.

Follow us on X to get the latest news as it happens

The report frames the trend as a copycat effect. Crypto firms pioneered the model of routing large sums into sector-focused super PACs during the last presidential cycle. AI and gambling companies have since built their own versions.

Where the Crypto Money Went

Fairshake, the crypto-aligned super PAC, received $82 million in corporate contributions. That sum represents 60% of its total 2026 receipts of $135 million.

The Trump-backing MAGA Inc. super PAC drew a separate $56.2 million from crypto donors. Ripple Labs and Coinbase steered $81.5 million toward Fairshake, while Crypto.com, Gemini, and Blockchain.com directed funds to MAGA Inc.

Crypto.com operator Foris Dax alone gave $35 million to MAGA Inc., making it the largest single corporate backer of that committee across all industries. The Winklevoss twins funded a separate Republican-only vehicle, the Digital Freedom Fund, with $21.3 million.

Public Citizen notes that its total likely undercounts real spending, since dark-money groups and state-level contributions escape federal disclosure rules.

Voter Interest Tells a Different Story

The spending contrasts sharply with public sentiment. A Politico poll conducted with Public First found only 4% of Americans weigh a candidate’s crypto position when voting. Just 18% want Congress to prioritize crypto rules.

Another survey found that 41% of respondents said special interest groups hold too much political influence. Whether that skepticism converts into ballot-box pressure against heavily funded candidates remains an open question for November.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Crypto Corporations Fund 37% of All 2026 Corporate Election Spending appeared first on BeInCrypto.

Hollywood director Carl Rinsch has been sentenced to 30 months in federal prison after prosecutors said he defrauded Netflix out of $11 million intended to finance a science-fiction television production. According to U.S. authorities, Rinsch diverted the funds into speculative trading—including cryptocurrency—before spending large portions on personal expenses and luxury purchases.

The case, handled in Manhattan federal court, closes a 15-month legal saga that began with Rinsch’s arrest in March 2025. He was convicted in December on charges that included wire fraud and money laundering and then faced sentencing for additional counts related to financial transactions tied to alleged unlawful activity.

Key takeaways

- Rinsch received a 30-month prison sentence for a scheme prosecutors say involved $11 million wired by a streaming company for a TV project.

- Prosecutors said the money was used for speculative bets in crypto and stocks, rather than completing the show.

- The court ordered $11 million in forfeiture on top of the prison term and supervision.

- The sentence was far below the maximum penalty the government said he faced across all counts, which totaled up to 90 years.

Fraud scheme tied to a streaming production

Manhattan U.S. Attorney Jay Clayton said in a statement that Rinsch “orchestrated a scheme to steal millions” by seeking $11 million from a subscription streaming service, claiming the funds would be used to finance his television show. Prosecutors said that representation was false.

Instead, Clayton stated, Rinsch made what the government characterized as risky bets on speculative stock options and cryptocurrency and also spent millions on luxury goods. “Today’s sentence sends a deterrent message: fraud will not be tolerated,” Clayton added.

Rinsch, best known for directing the 2013 film “47 Ronin” starring Keanu Reeves, was convicted in December on counts including fraud and money laundering. At sentencing, the court also considered defense arguments that he had mental health issues, including support letters submitted by people close to him.

Prosecutors said the case began as a continuation of an earlier funding arrangement. Earlier reporting and court filings cited in the case describe that Rinsch initially received $44 million from the streaming service for a project later renamed “Conquest,” after a show initially titled “White Horse.” The additional $11 million was wired in March 2020, according to the indictment and accounts described in court materials.

Crypto trading and the Dogecoin liquidation

One of the central claims in the case involved how Rinsch allegedly used part of the new $11 million to attempt to multiply the money through market speculation. According to a March 2025 indictment and reporting connected to a confidential arbitration described by the New York Times, Rinsch used $10.5 million from the additional funding to gamble in the stock market and quickly lost about half within weeks, as described in the indictment.

Prosecutors also said Rinsch moved more than $4 million of remaining funds to the crypto exchange Kraken and then “went all in” on Dogecoin (DOGE). The indictment materials referenced by the article state that the DOGE trade generated about $27 million after he liquidated in May 2021, based on a statement described as seen by The Times.

For readers tracking how court cases interpret crypto activity, the case offers a clear example of prosecutors linking on-exchange transfers and concentrated positions to broader alleged intent. Here, the government framed crypto trading not as a detached investment decision but as part of an overall use of client funds that prosecutors argued was deceptive.

Spending that allegedly followed the trades

After the reported DOGE winnings, prosecutors alleged Rinsch spent about $10 million on personal expenses and luxury purchases instead of completing the show or returning the money. The indictment described expenditures including $1.8 million on credit card bills, $1 million for lawyers to sue Netflix, $3.8 million on furniture and antiques, and large purchases of luxury vehicles, including Rolls-Royces and a Ferrari.

The indictment also cited smaller but specific categories such as $652,000 for watches and clothes, alongside other personal spending. Prosecutors said Rinsch never finished the television project and did not return the funds that had been provided.

While the sentence itself is a criminal-law outcome, the underlying narrative—funds intended for production allegedly redirected into speculative markets and then into personal consumption—highlights how financial misuse allegations can draw on both traditional asset trading records and crypto exchange activity.

What prosecutors sought vs. what the court imposed

At trial, Rinsch was convicted of one count each of wire fraud and money laundering. Each of those counts carried a maximum of 20 years in prison, prosecutors said, while five additional counts involving monetary transactions tied to unlawful activity carried maximum penalties of up to 10 years each.

In a mid-June sentencing memo filed in court, prosecutors asked for a five-year prison term, after Rinsch argued for a sentence without incarceration. The court ultimately imposed a 30-month term—shorter than the government’s request.

Along with prison time, prosecutors said the judge ordered three years of supervised release, $11 million in forfeiture, and $700 in mandatory special assessments.

The defense argued Rinsch’s mental health played a role in his behavior around the time of the alleged offenses, and support letters included submissions from friends and family, as well as a letter from Keanu Reeves. Authorities, however, emphasized the deliberate nature of the scheme, including the alleged misrepresentations used to secure the $11 million.

For investors and crypto users, the practical takeaway is less about any single coin and more about how courts may interpret crypto trading activity when prosecutors tie it to alleged fraud, money laundering, and diversion of funds. Readers should watch how similar cases develop evidence standards—particularly how exchange withdrawals, concentrated token bets, and liquidation timing are presented as part of intent and purpose in fraud prosecutions.

XRP Price Analysis: Critical $1 Support Level Under Pressure as July 2026 Approaches

Politics Home | How consumer-led flexibility can benefit households and our future energy system

Chaotic street takeover breaks out in Pacoima after Mexico’s World Cup win

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics5 days ago

Politics5 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World1 day ago

Crypto World1 day agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics5 days ago

Politics5 days agoPotential 2028er World Cup attendee leaderboard

-

Business5 days ago

Business5 days agoAsia stock markets slide as tech shares slump

-

News Videos3 days ago

News Videos3 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech5 days ago

Tech5 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business1 day ago

Business1 day agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World4 days ago

Crypto World4 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports4 days ago

Sports4 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech4 days ago

Tech4 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World5 days ago

Crypto World5 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

-

Crypto World5 days ago

Crypto World5 days agoRTX holders must register wallets before token distribution begins

-

Tech1 day ago

Tech1 day agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Business2 days ago

Business2 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

You must be logged in to post a comment Login