Crypto World

Could the IPO wave drain crypto’s liquidity?

A record run of mega-listings is pulling hundreds of billions in fresh equity supply into the market. The fear is that the money to buy it comes partly out of crypto. The truth is more tangled than the timeline suggests.

Summary

- SpaceX completed the largest IPO in history in June 2026, and anticipated listings from OpenAI and Anthropic could bring the wave of new equity supply above $240 billion by year-end.

- The core worry is mechanical: an IPO does not create new money, so investors sell existing holdings to fund allocations, and crypto is among the easiest assets to liquidate quickly.

- The evidence for a drain is real: Bitcoin fell hard around the SpaceX listing, spot Bitcoin ETFs posted a record $4.5 billion of outflows in June, and higher-beta altcoins took the most damage.

- The evidence against a simple story is just as real: the same weeks brought a sharp equity selloff, geopolitical shocks, and a hawkish Fed, so macro, not the IPOs alone, drove much of Bitcoin’s drop.

- The likely answer is that the wave is a genuine short-term headwind that competes with macro forces, and whether it becomes a lasting drain depends on flows reversing once the deals are digested.

There is an obvious villain in crypto’s rough summer. SpaceX carried out the biggest IPO ever, OpenAI and Anthropic are lining up behind it, and Bitcoin fell through the same window. The story writes itself: the mega-IPO wave is a giant vacuum, sucking capital out of digital assets to fund the hottest listings in a generation. The mechanism is plausible, the timeline lines up, and the fear is widespread.

But correlation this clean often hides a messier truth, and the question deserves more than a chart with two lines pointing opposite directions. This piece lays out the scale of the wave, the mechanism behind the drain thesis, the evidence for it, the macro confound that complicates it, and what would tell us which force is really in control. It also looks at the strange counterpoint that the same IPO wave pulling liquidity from crypto is also pushing equity-like speculation onto crypto rails. The result is not a clean bullish or bearish answer, but a liquidity map.

The scale of the wave

Start with the numbers, because they are genuinely large. SpaceX went public around June 12, 2026, targeting roughly $75 billion at a valuation near $1.75 trillion, the largest listing in history, with reported demand exceeding $250 billion. Behind it sit two of the most anticipated technology debuts in years, OpenAI and Anthropic, whose listings and fundraising are expected to pull in tens of billions more. One estimate puts the combined new equity supply from this cluster above $240 billion by year-end.

That figure is what makes the drain thesis credible. Markets absorb new supply by finding buyers, and buyers need cash. When the supply arriving is measured in hundreds of billions and concentrated in a short window, the question of where the money comes from stops being academic. The wave is not one event but a sequence, which is why the concern is less about any single listing and more about the cumulative pull of several mega-deals stacking up across the same months.

For crypto readers, SpaceX’s Bitcoin position on public markets matters because it complicates the simple drain story. SpaceX did not only pull money from risk assets; it also brought 18,712 BTC onto the balance sheet of a public-market giant. That makes the listing both a competitor for crypto liquidity and a legitimizing event for Bitcoin as a corporate asset. The tension between those two effects is the core of the debate.

The mechanism: an IPO does not create new money

The heart of the drain argument is a simple truth that is easy to forget in a rally. An IPO does not print new money into the system. It transfers existing capital from investors into a newly public company and its early backers. To buy into a hot offering, investors free up cash, and they free up cash by selling something they already own.

Crypto is a prime candidate for that selling, because it trades around the clock and can be liquidated fast when someone needs capital in a hurry. The mechanism has several strands. Retail overlap is one: a large share of the SpaceX allocation targeted retail investors, a group that overlaps heavily with active crypto participants, so some of the money chasing shares comes straight out of crypto positions. Index-fund mechanics are another: once a giant company enters the indices, funds tracking those benchmarks are forced to buy billions of its shares, and because they hold little spare cash, they raise it by selling existing positions.

Institutional rebalancing is the third: funds holding Bitcoin through ETFs face a choice about trimming crypto to fund IPO allocations. Each strand points the same way, toward selling pressure on liquid risk assets, with crypto near the front of the line. That is why how ETF flows move the market matters in this context. When crypto ETF shares are sold to raise cash, the effect is not abstract; it removes a real bid from the market.

The evidence for a drain

The tape offers real support for the thesis. Around the SpaceX filing and listing, Bitcoin fell roughly 20% and slipped under $60,000, and the broader crypto market bled with it. The clearest institutional signal came from the funds: U.S. spot Bitcoin ETFs recorded about $4.5 billion of net outflows in June 2026, the worst month since the products launched, removing the steady bid that had cushioned earlier drops. Crypto ETFs had already seen billions in outflows the month before.

Analysts explicitly cited capital rotation and the SpaceX IPO among the drivers of the redemptions. The pattern extended beyond Bitcoin. Space and hard-tech stocks rallied in the same weeks that crypto slid, a visual rotation from digital assets into aerospace and AI exposure. And altcoins fared worse than Bitcoin, consistent with the idea that investors raising cash sell their highest-beta positions first.

Taken together, the outflows, the rotation into listing-adjacent equities, and the outsized altcoin damage form a coherent picture of capital leaving crypto as the IPO wave built. It does not prove the IPO wave caused all of the selloff, but it proves the drain thesis has more than vibes behind it. The timing, the flow data, and the asset-performance pattern all point in the same direction. The next question is whether they point only to the IPO wave or to a broader risk-off event that happened to arrive at the same time.

The evidence against a simple story

Here is where the clean narrative frays. The same weeks that saw Bitcoin fall also delivered a broad risk-off shock that had nothing to do with any IPO. Equity markets sold off sharply, with the Nasdaq posting one of its worst single days of the year and AI bellwethers dropping as bubble fears flared. Geopolitics piled on, with missile exchanges in the Middle East pushing oil higher and stoking the inflation fears that keep the Fed hawkish.

Under a hawkish Fed, with markets pricing a strong chance of a December rate hike as inflation drifts back up, risk assets were under pressure across the board. Bitcoin, which trades far more like a high-beta risk asset than like digital gold, did what every speculative position did in that environment: it got sold. When it recovered, it recovered on macro news, not on IPO mechanics. That sequence exposes the flaw in blaming the listings alone.

The IPO wave competed with genuine global risk-off conditions, and it is close to impossible to cleanly separate how much of Bitcoin’s drop came from capital rotating into SpaceX versus capital fleeing risk in general. Correlation with the IPO timeline is not proof of causation when a dozen other bearish forces arrived at once. That is why the Bitcoin market backdrop still matters more than any single listing. If macro remains hostile, even a completed IPO wave will not automatically restore crypto liquidity.

The rotation-back case

The drain thesis also has a time limit that its loudest versions ignore. An IPO is a one-time reallocation, not a permanent siphon. Once allocations are funded and the deals are digested, the selling pressure fades, and the capital that rotated out can rotate back. If the listings price well and risk sentiment improves, the same investors who sold crypto to fund IPO positions may redeploy into digital assets, turning a short-term headwind into a medium-term tailwind.

There is a structural sweetener too. SpaceX carried a multibillion-dollar Bitcoin position onto public markets, so every new shareholder gained indirect exposure to the asset, and a successful debut could encourage other pre-IPO companies to hold and disclose Bitcoin to court crypto-friendly investors. In that scenario, the IPO wave ends up expanding the base of Bitcoin holders rather than shrinking crypto’s capital. The drain, if it is one, may be the front end of a cycle that feeds back into the asset it briefly pulled from.

This is why the rotation-back case should not be dismissed, even if it is slower than the drain. Liquidity can leave quickly and return gradually. The first leg shows up as selling pressure, ETF outflows, and weaker altcoins. The second leg would show up later, through renewed ETF inflows, higher risk appetite, and capital moving back down the crypto risk curve once the IPO allocations have settled.

Why altcoins bear the brunt

If there is a drain, its incidence is uneven, and that unevenness is itself informative. Bitcoin is the deepest, most liquid crypto asset and the one institutions hold through ETFs, so it absorbs pressure but also attracts the first capital back. Altcoins are higher-beta and thinner, which means investors raising cash tend to liquidate them first and rebuild them last. That dynamic delays any altcoin season and concentrates the pain in the long tail of the market, even when Bitcoin itself is only mildly affected.

For readers trying to gauge the wave’s impact, the altcoin-versus-Bitcoin spread is a useful tell. If the drain is real and ongoing, altcoins keep underperforming as capital stays parked in equities. If the pressure is easing, the higher-beta names are where the recovery shows up first once risk appetite returns. The brunt falling on altcoins is both a symptom of the drain and an early indicator of its reversal.

The reason is behavioral as much as mechanical. In a cash-raising event, investors usually sell what is liquid, volatile, and easiest to replace later. That puts altcoins near the front of the liquidation queue. It also means a later altcoin rebound would be meaningful, because it would suggest the market has moved from forced cash-raising back into risk-taking.

What to watch

The debate does not resolve with a single number, but a few signals will show which force is winning. ETF flow direction is the clearest: a return to sustained net inflows would signal the drain is over and capital is coming back, while continued outflows would confirm the pressure persists. The timing of the OpenAI and Anthropic listings is the second: if they cluster into the same window, the cumulative supply shock intensifies, whereas spacing them out softens it. The third is whether post-deal capital actually rotates back after SpaceX is digested, the test of the rotation-back thesis.

The fourth is Bitcoin’s behavior around its support in the high $50,000s to $60,000 range, since holding there through the wave would suggest the selling is absorbable, while breaking down would suggest the drain is compounding other bearish forces. And the fifth is the macro backdrop, because as long as the Fed stays hawkish and risk-off conditions dominate, it will be hard to blame crypto weakness on the IPOs alone. Watched together, these signals separate a temporary reallocation from a structural outflow, which is the distinction that actually matters. One rough rule: if ETF flows turn positive while altcoins stop underperforming, the IPO drain is probably fading.

The harder signal is whether the IPO wave changes investor preference, not just investor positioning. A temporary drain means investors sold crypto to fund new listings and later returned. A structural drain would mean they now prefer listed AI and hard-tech exposure over crypto as their main risk-on trade. The first is a headwind; the second would be a deeper challenge.

The pre-IPO perps signal

One of the most revealing threads in this story has nothing to do with the drain itself and everything to do with where financial infrastructure is heading. Before SpaceX shares ever reached Wall Street, crypto exchanges rolled out pre-IPO perpetual futures tied to the expected listing, letting traders bet on the valuation through crypto rails. The activity was substantial, and the price action was wild: one pre-IPO SPCX perpetual fell sharply from its listing high as speculation swung, showing both the demand for the exposure and its volatility. Crypto venues, in other words, became the first place retail could trade SpaceX at all.

That detail reframes the whole liquidity question. The same infrastructure that the drain thesis says is losing capital to equities is simultaneously absorbing equity-style trading onto crypto rails. If pre-IPO perps on tokens and stocks become a durable product, then crypto exchanges are not just donors of liquidity to the IPO wave; they are also venues capturing a slice of the speculative interest the wave generates. The relationship between crypto and the mega-listings is more two-way than a one-directional siphon, which complicates the simple picture of capital flowing out and not coming back.

It also hints at a longer arc. As tokenized and pre-IPO markets mature, the line between trading a stock and trading a token blurs, and the platforms that started in crypto are positioned to sit in the middle of that convergence. The IPO wave may pull spot capital out of Bitcoin in the near term while pushing trading volume and relevance toward crypto-native infrastructure at the same time, a nuance the drain narrative misses entirely. For readers new to the product, the pre-IPO perps market sits inside the broader world of perpetual futures, where traders can take synthetic exposure without owning the underlying asset.

Lessons from past capital events

History offers a rough template for how these episodes resolve, even if no two are identical. Large capital events that pull attention and money toward a specific opportunity tend to produce a front-loaded effect: the pressure is heaviest in the run-up and immediate aftermath, when investors are raising cash and reallocating, and it eases once the event is digested and positions settle. The reallocation is a one-time transfer, not a permanent change in how much capital exists, so the assets that gave up liquidity often see some of it return once the opportunity is fully priced. The variable that decides whether the return happens quickly is the macro environment.

In a risk-on backdrop with ample liquidity, a big IPO gets absorbed with little lasting damage to other assets, because there is enough capital to fund the new supply without deep selling elsewhere. In a tight, risk-off backdrop like mid-2026, the same IPO bites harder, because investors are already defensive and more willing to sell liquid positions to raise cash. The current wave is landing in the harder version of that setup, which is part of why its effect on crypto feels sharp. The same deal that might have been absorbed cleanly in a looser market becomes a visible drain when liquidity is already scarce.

The practical lesson is to separate the temporary from the structural. A front-loaded drain that reverses once the deals clear is a headwind to trade around, not a reason to abandon the asset class. A structural shift, where capital permanently prefers listed innovation stocks over crypto, would be a bigger deal, but it requires evidence beyond a few months of correlated moves. So far, the pattern looks more like a large, concentrated reallocation arriving into an already-weak market than proof of a lasting migration, which is why the flows in the months after the listings matter more than the drawdown during them.

Who actually gets drained, and who does not

A subtlety the blunt drain thesis misses is that not all crypto capital is equally at risk of being pulled into an IPO. The money most likely to rotate out is the marginal, liquid, opportunistic kind: leveraged traders, short-term speculators, and investors who hold crypto as one line in a broader risk portfolio and will happily sell it to chase a hot listing. That is exactly the capital that flows through the venues showing the most stress, and its exit shows up fast in falling open interest and higher volatility.

The capital least likely to leave is the opposite: long-term holders, self-custody accumulators, and conviction buyers who treat Bitcoin as a multi-year position instead of a source of dry powder for equities. The exchange-outflow data discussed above suggests this cohort has been buying weakness even as the speculative money leaves, which means the drain is concentrated in the flighty end of the market and cushioned at the sticky end. That split matters for how deep and how lasting any drain can be, because a market losing its weak hands while its strong hands accumulate is behaving very differently from one where everyone is heading for the exits.

There is a geographic and structural layer too. The retail overlap that funds IPO allocations is heaviest in the markets and platforms where the same investors trade both stocks and crypto, so the drain is not uniform across the world or across venues. Institutions holding Bitcoin through ETFs face a cleaner rebalancing decision than a self-custody holder in a jurisdiction with limited access to the SpaceX offering, who may have no easy way to swap one for the other even if they wanted to. The result is that the drain is real but uneven, biting hardest where crypto and equity trading overlap and barely at all where they do not. For anyone trying to size the effect, the question is not whether capital is leaving, but which capital, and the answer, that it is mostly the liquid and opportunistic kind, is part of why the impact may prove more temporary than the headline drop suggests.

Frequently asked questions

How big is the IPO wave?

SpaceX completed the largest IPO in history in June 2026, targeting roughly $75 billion at a valuation near $1.75 trillion, with reported demand above $250 billion. Anticipated listings and fundraising from OpenAI and Anthropic could push the combined new equity supply from this cluster above $240 billion by year-end, concentrated into a relatively short window. That is why the drain thesis is being taken seriously: the scale is too large to ignore. The issue is whether the money comes mainly from crypto, from broader equities, or from cash and other liquid holdings.

Why would an IPO drain crypto liquidity?

Because an IPO does not create new money. Investors fund allocations by selling assets they already own, and crypto is easy to liquidate quickly. Retail buyers overlap with crypto holders, index funds are forced to buy the new shares by selling other positions, and institutions may trim Bitcoin ETF holdings to raise cash. Each channel points to selling pressure on liquid risk assets. Crypto sits near the front of that line because it trades 24/7, has deep venues, and is often held by investors who also chase high-growth tech listings. That does not mean every dollar funding the IPO wave comes from crypto. It means crypto is one obvious source of dry powder when investors need cash quickly.

Is there proof the drain is happening?

There is supporting evidence, not proof. Bitcoin fell around the SpaceX listing, spot Bitcoin ETFs saw a record $4.5 billion of outflows in June 2026, space stocks rallied as crypto slid, and altcoins underperformed. Analysts cited capital rotation and the IPO among the drivers. But the same period brought a broad risk-off shock, so the IPO cannot be cleanly isolated as the cause. The cleaner way to frame it is that the IPO wave was one headwind among several. It likely added pressure at the margin, especially through ETF outflows and altcoin selling. But macro conditions, Fed expectations, equity weakness, and geopolitical stress were also moving risk assets at the same time.

What else could explain Bitcoin’s drop?

Macro forces that arrived at the same time. Equity markets sold off sharply, AI stocks fell on bubble fears, geopolitical tension pushed oil higher, and a hawkish Fed pricing a likely December rate hike pressured risk assets broadly. Bitcoin trades like a high-beta risk asset, so it got sold in that environment regardless of the IPO wave. Macro and the listings are hard to separate. This matters because blaming only the IPO wave can lead to the wrong read. If the drop was mainly macro, then even after the listings clear, crypto can stay weak until risk appetite improves. If the drop was mainly IPO funding pressure, flows should recover once the deals are digested. The market’s next move depends on which force dominates.

Could the IPO wave actually help crypto later?

Yes, potentially. An IPO is a one-time reallocation, not a permanent siphon. Once deals are funded and digested, capital that rotated out can rotate back, especially if listings price well and risk sentiment improves. SpaceX also carried Bitcoin onto public markets, giving new shareholders indirect exposure and possibly encouraging other pre-IPO firms to hold and disclose Bitcoin. That is where the corporate-Bitcoin angle becomes relevant. If large public companies normalize holding BTC, the long-term adoption signal can offset some of the near-term liquidity drain. The question is whether that normalization is strong enough to matter for flows, not merely for narrative.

Why do altcoins get hit harder than Bitcoin?

Altcoins are higher-beta and less liquid, so investors raising cash tend to sell them first and rebuild them last. Bitcoin is deeper and held through ETFs, so it absorbs pressure but also draws capital back first. That dynamic concentrates the pain in altcoins and delays any altcoin season, which is why the altcoin-versus-Bitcoin spread is a useful gauge of the drain. If altcoins keep underperforming after the IPO allocations settle, the pressure is probably not over.

What signals show whether the drain is easing?

The clearest is ETF flow direction: a return to sustained inflows would signal capital coming back, while continued outflows would confirm ongoing pressure. Also watch the timing of the OpenAI and Anthropic listings, whether capital rotates back after SpaceX is digested, Bitcoin’s behavior around its support, and the macro backdrop, since a hawkish Fed keeps risk assets pressured independently. The altcoin-versus-Bitcoin spread is another useful tell. If higher-beta crypto starts recovering first, the forced cash-raising phase may be ending.

Does an IPO wave always pull money from crypto?

Not necessarily. The effect depends on overlap between IPO buyers and crypto holders, the size and timing of the deals, and the macro environment. In a risk-on market with ample liquidity, large IPOs can be absorbed without much crypto selling. In a tight, risk-off market like mid-2026, the overlap and the cash needs make crypto a more likely source of funding, amplifying the effect. The SpaceX, OpenAI, and Anthropic wave is unusual because the listings are large, concentrated, and aimed at the same risk-seeking investor base that often owns crypto. That makes the drain plausible. It still does not make it the only driver of crypto weakness.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and market analysis is speculative and can change quickly. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of July 1, 2026, and will change.

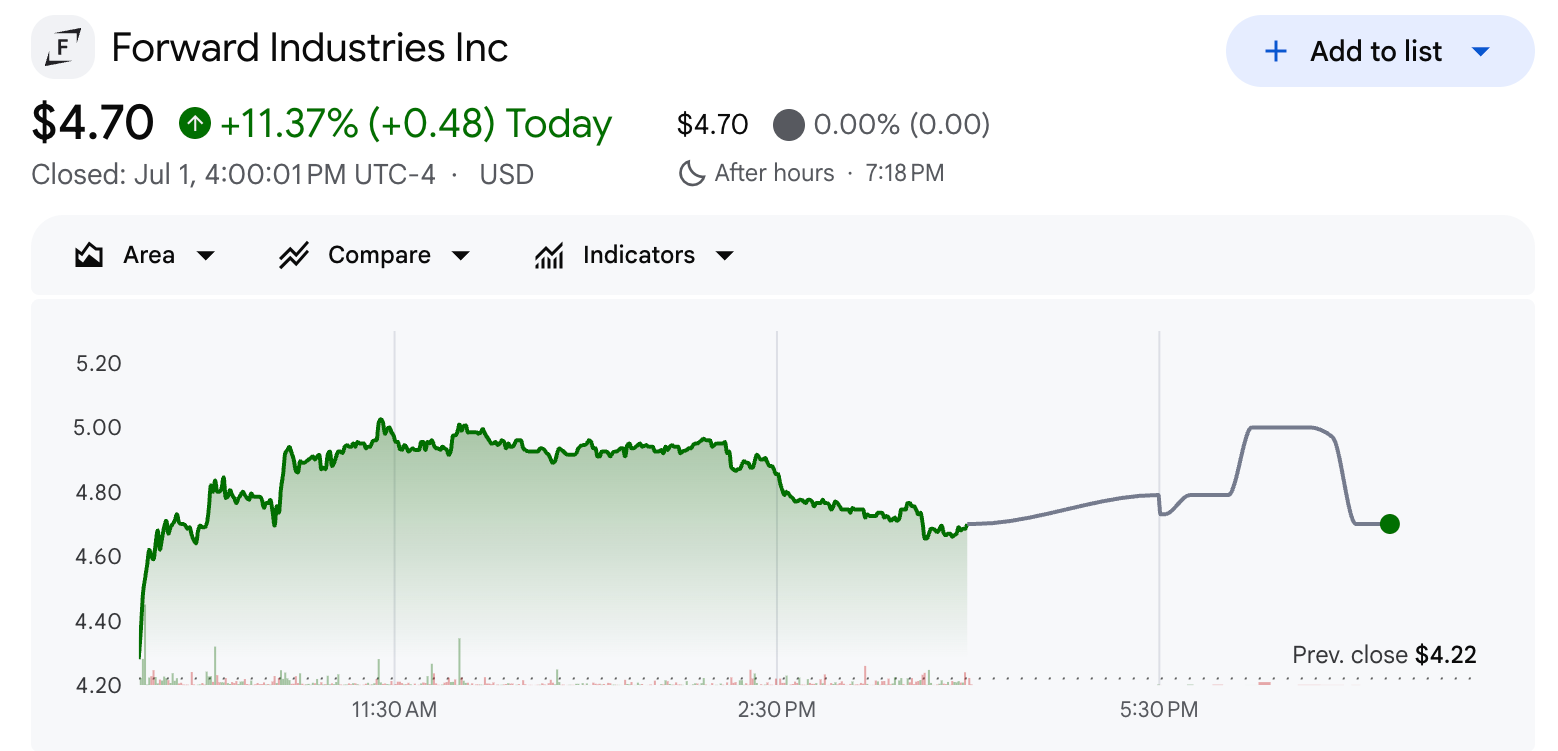

Forward Industries, the largest corporate Solana (SOL) holder, saw its share price rise by double-digits on Wednesday.

The uptick came after the company revealed it bought over 500,000 Solana (SOL) in fiscal Q3 2026.

Forward Industries SOL Treasury Tops 7.5M

FWDI closed at $4.70 on July 1, up 11.37%. The gain extended a rally that began in late June, when SOL started to recover. That rebound has offered relief to a stock weighed down by a broader 2026 downturn.

Follow us on X to get the latest news as it happens

According to the announcement, the firm acquired the tokens at an average price of about $79 each. Forward held 7.55 million SOL as of June 30, 2026.

SOL-per-fully diluted share rose to 0.0729 from 0.0669 in the prior quarter, a 36% annualized growth rate. Furthermore, shares outstanding fell to 73.85 million from 76.31 million.

Meanwhile, the company sold 93,642 shares through its at-the-market program during the quarter. Forward also cited its recent inclusion in the Russell 2000 and Russell 3000 indexes.

“By repurchasing shares when Forward trades at a discount to NAV and issuing equity when our shares trade at a premium, we dynamically allocate capital in a way that compounds SOL per share and enhances long-term intrinsic value,” CIO Ryan Navi said.

Losses Still Weigh on the Largest SOL Holder

The buying spree came after a painful stretch. Forward recorded a $283.1 million net loss for the quarter ended March 31, 2026, driven by fair-value markdowns on its SOL stack. Revenue still quadrupled year over year on staking rewards.

Market conditions have since turned more favorable. SOL gained over 15% over the past week on strong network activity, outperforming large-cap cryptocurrencies, BeInCrypto Markets data shows.

The coming months will test whether SOL’s recovery can hold, a swing that flows directly to Forward’s balance sheet as the largest SOL holder.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Forward Industries Shares Rise 11% as Solana Bet Grows to 7.5 Million appeared first on BeInCrypto.

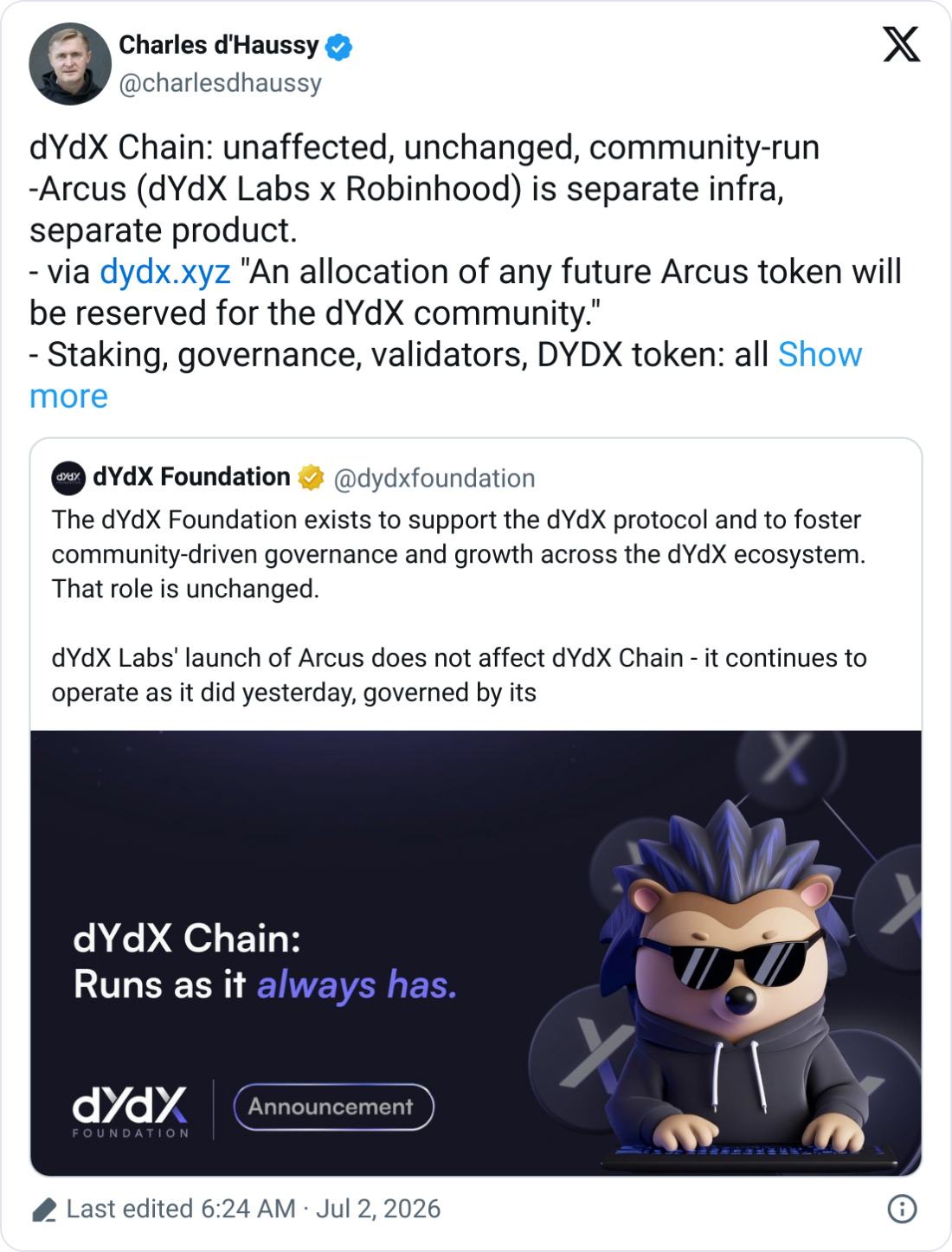

The company behind the dYdX decentralized exchange (DEX) has partnered with Robinhood to rebrand and launch the protocol as Arcus on the Robinhood Chain.

An X account for Arcus posted on Wednesday that “dYdX is now Arcus” and would launch on the Robinhood Chain, Robinhood’s Arbitrum-based layer 2 blockchain that went live the same day.

The dYdX Foundation said that dYdX Labs created Arcus “in partnership with Robinhood” and that the dYdX blockchain “is not affected by it in any way.” The platform is set to be blockchain’s “leading DEX” and will give users access to perpetual products and fee-free trading of 95 tokenized stocks.

Source: Charles d’Haussy

The DEX is part of Robinhood’s expanded push into tokenized assets and perpetual trading, two areas of crypto that have recently exploded in popularity as US regulators have shown interest in allowing the products to more easily come to market.

Robinhood’s embrace of perpetual trading comes as it looks to entice traders who have flocked to the crypto perpetual futures platform Hyperliquid, whose token has climbed nearly 150% so far this year as it has captured market share.

Arcus to offer tokenized stock, perps trading

“Until now, traders have been shut out of the most valuable markets on earth — US equities, commodities, and indices — because of where they live, market hours, and institutions restricting access,” Arcus said in a blog post. “We built Arcus to reduce these barriers.”

The protocol said that it will offer perpetuals and tokenized stock trading that will go live this month, allowing tokenized stocks to be used as collateral for perpetuals and providing access to pre-IPO markets.

Related: CFTC chair says perp trading not suitable for all assets it regulates

It added that Robinhood Crypto, the company’s crypto technology arm, made an investment in Arcus but did not disclose further details.

The dYdX Foundation said that Arcus “is a distinct, independent product built on separate infrastructure” and that the dYdX blockchain would continue to operate and be owned by its community.

Major retail-focused trading platforms have been moving to expand their offerings to remain competitive. Crypto exchange Coinbase has looked to rival Robinhood and become a full-service trading platform, having added access to thousands of stocks earlier this year.

Robinhood’s blockchain also follows a similar move from Coinbase in 2023, when the latter launched its Ethereum layer-2 blockchain Base that has grown to be the fifth-largest by value locked, according to DeFiLlama.

Meanwhile, Bitget Wallet, the self-custodial wallet from the Bitget crypto exchange, said on Wednesday that it partnered with Robinhood Crypto to integrate the company’s blockchain to allow its users to trade tokenized stocks.

The decentralized exchange 1inch also said on Wednesday that it would be among the first major swap platforms to support Robinhood Chain.

Big Questions: Do we really only need 2–5 cryptocurrencies?

Bitcoin traded above $60,700 on Thursday after a quick overnight reversal after Federal Reserve Chair Kevin Warsh said inflation risks had eased, giving a market that spent most of June grinding lower its first clear lift in weeks.

Speaking at the European Central Bank’s annual forum in Sintra, Portugal, on Wednesday, Warsh said “inflation risks have come down” while reaffirming the Fed’s commitment to returning inflation to 2%.

He declined to signal what the central bank will do at its meeting later this month, saying policymakers would weigh incoming data first. Bitcoin pared earlier losses and pushed back above $60,000 after the remarks, according to CoinDesk reporting.

Solana led the majors. The token rose about 4% on the day to around $78 and is up roughly 16% over the past week, per CoinDesk data, the only large token with a meaningful weekly gain. Ether traded near $1,630, up about 3% on the day, while XRP held at about $1.06. BNB, dogecoin and Tron were softer over the week.

Forward Industries has expanded its Solana treasury after buying more than 500,000 SOL during fiscal Q3 2026.

Summary

- Forward Industries bought over 500,000 SOL, raising its treasury to 7.55M SOL by June 30.

- The company reported 36% annualized SOL-per-share growth while selling 93,642 shares during fiscal Q3 2026.

- Earlier losses show Solana treasury firms remain exposed to price swings and U.S. accounting rules.

The Nasdaq-listed company said its total holdings reached 7.55 million SOL as of June 30.

The company bought the tokens at an average price of about $79 per SOL. It also said SOL per fully diluted share rose to 0.0729 from 0.0669 at the end of the prior quarter.

Forward Industries stock recently traded at $4.70 on Nasdaq, up more than 10% in the past day, with an intraday high of $5.04 and volume above 3 million shares (per Google Finance data).

Forward Industries said the increase represented 36% annualized SOL-per-share growth. The update comes as the company continues to build its Solana treasury while earlier filings show how crypto price moves have shaped its reported results.

Forward Industries expands Solana holdings

In a July 1 company release, Forward Industries said it sold 93,642 common shares through its At The Market offering during fiscal Q3. The company said it used public market capital in a way that raised SOL per share for existing shareholders.

Forward described itself as the largest Solana treasury company. It said its recent inclusion in the Russell 2000 and Russell 3000 indexes gives it wider access to institutional investors when its shares trade above net asset value.

The company also said it can borrow against fwdSOL collateral through institutional partners. Forward said this lets it seek liquidity at a lower cost than its staking yield, which it placed between 6.4% and 7.3%.

Forward links strategy to SOL per share

“Our mandate is simple: maximize SOL per share and create long-term shareholder value,” said Chief Investment Officer Ryan Navi. He said the company uses several capital formation methods to add SOL in a way it views as accretive.

Navi added that Forward can repurchase shares when they trade below net asset value and issue equity when they trade above it. He said the Russell index additions could also widen the company’s investor base and help fund more SOL purchases.

Forward also pointed to Solana network activity in a separate X post. The post quoted SolanaFloor data saying daily, weekly, and monthly Solana transaction counts had reached record levels across measured timeframes.

Earlier losses remain part of the story

The latest purchase follows a period of reported losses tied to SOL price changes. As previously reported, Forward Industries neared a $1 billion Solana paper loss after the company reported a $585.6 million net loss for the quarter ended Dec. 31, 2025.

That earlier result included a $560.2 million loss on digital assets and a $33 million impairment under U.S. GAAP treatment. The company said the loss reflected fair-value accounting for its SOL holdings, not a direct cash outflow.

In addition, Forward also transferred 455,784 SOL to Coinbase Prime in June. That move drew attention because deposits to prime brokerage platforms can serve several purposes, including custody, liquidity management, collateral use, or asset sales.

Solana treasury model faces market test

Forward launched its Solana treasury strategy in September 2025 with backing from investors and partners including Galaxy Digital, Jump Crypto, and Multicoin Capital. The company says its strategy includes buying, holding, staking, trading, and investing in SOL-related assets and projects.

The broader digital asset treasury sector has faced pressure during crypto market declines. As crypto.news reported, treasury companies tied to Bitcoin, Ethereum, and Solana have carried large unrealized losses as token prices fell.

Forward’s Q3 update shows that the company is still adding SOL despite earlier losses. The central measure it is asking investors to watch is SOL per fully diluted share. That metric now sits higher than the prior quarter, while the value of the treasury still depends on SOL market prices, staking revenue, borrowing costs, and shareholder dilution.

Binance said its Direct Stocks product crossed $1 billion in U.S. equities acquired within 30 days of launch.

Summary

- Binance’s Direct Stocks crossed $1B in user-held U.S. equities within 30 days of launch globally.

- Emerging markets made up 73% of users, showing demand for app-based access to U.S. stocks.

- Stablecoins helped users buy fractional equities beside crypto without traditional brokerage and bank transfer barriers.

The product went live on June 1 and gives eligible users access to more than 7,000 U.S. stocks and ETFs in the same app they use for crypto.

The exchange said the product also processed close to $3 billion in trading volume during the same period. The 30-day window included 22 trading days, according to a Binance blog post.

Binance said about 73% of Direct Stocks users came from emerging markets. The company framed the data around demand from regions where brokerage accounts, bank wires, minimum balances, and foreign market access have often limited retail participation.

Binance stock access gains early demand

Direct Stocks lets users buy fractional U.S. stocks and ETFs with stablecoins and selected crypto balances. As previously reported, Binance opened U.S. stock trading access for eligible non-U.S. users in June, offering more than 7,000 equities and ETFs with purchases starting from $5.

The product places equities beside crypto balances in one interface. Binance said the setup removes some steps tied to traditional brokerage access, including separate bank transfers and new account flows. The company said users acquired more than $150 million in U.S. equities per day during the first 30 days.

Emerging markets drive the user base

Binance said emerging markets accounted for most Direct Stocks users. The company also said about one in seven visitors to its stock trading page registered an account, and nearly 90% of those new sign-ups placed a trade.

The data follows earlier Binance Research claims about broader demand for equity access through crypto exchanges. As reported by crypto.news, Binance Research projected that crypto exchanges could bring 300 million new equity investors and $2 trillion in new capital into global stock markets by 2031. The report linked that growth to stablecoins, crypto exchange reach, and users in underbanked regions.

Shunyet Jan, Binance’s Head of Spot and Derivatives Business, said, “A billion dollars in 30 days is a sign of the demand that’s been waiting decades for a door to walk through.” He added that Binance built the product for users who “never had a way in.”

Stock trading uses broker-linked rails

Binance does not custody the securities traded through Direct Stocks. Binance disclosed an Alpaca stake as its stock trading service expanded. Nest Trading acts as introducing broker, while Alpaca handles execution, clearing, settlement, custody, dividends, and corporate actions.

The model gives Binance exposure to traditional equities while keeping securities activity linked to regulated brokerage partners. Users fund stock purchases with stablecoins and supported crypto assets. Binance said the product targets eligible users outside the U.S.

Tokenized equity race widens

The direct stock rollout comes as exchanges add more equity-linked products. Crypto.news reported that Binance launched bStocks, letting eligible users convert supported U.S. stock holdings into tokenized assets that can trade around the clock.

Moreover, other exchanges are also moving into stock access. Bitget launched Stock+, allowing eligible users to buy real U.S. stocks with crypto converted into USDC through regulated brokers.

Binance said technology stocks made up the largest share of Direct Stocks holdings. It said the technology sector accounted for about 71% of holdings, while semiconductor names made up around 48%. The company also projected that Direct Stocks could exceed $10 billion by the end of 2026 if current growth continues, though it said the projection was illustrative and not a guarantee.

Crypto World

FBI Director Kash Patel caught sleeping on required disclosure of six-figure MSTR investment

FBI Director Kash Patel failed to timely disclose a six-figure purchase of stock in Strategy (MSTR), the world’s largest publicly-listed bitcoin holder, according to a report by nonpartisan news outlet NOTUS.

Patel supposedly purchased between $100,001 and $250,000 worth of MSTR on Nov. 21, but did not report the trade to regulators until May 26.

The reason for the delay? miscommunication. Patel informed the Office of Government Ethics that he “inadvertently omitted” the transaction due to an unspecified “miscommunication.”

According to the Stop Trading on Congressional Knowledge (STOCK) Act, high-ranking executive branch officials need to publicly disclose individual stock trades over $1,000 within 45 days from the transaction.

The trade has drawn intense scrutiny from government watchdogs due to Strategy’s BTC accumulation business and its previous business with federal agencies.

The company, which according to NOTUS has done millions of dollars in business over the years with the Justice Department, calls itself as a “Bitcoin Treasury Company,” and aggressively accumulates BTC as its primary reserve asset. Since 2020, the company has built a coin stash of 847,363 BTC, worth over $50 billion as of this writing.

French Interior Minister Laurent Nuñez has promised a “more ambitious” approach to tackling crypto ransom attacks after confirming there were 77 kidnapping, extortion or attempted extortion incidents linked to crypto in the first half of 2026.

Nuñez said Tuesday that the 77 incidents recorded so far this year are up sharply from the 45 recorded in all of 2025, according to local outlet BFM Business.

“These are serious matters, and your concern is legitimate,” he told the Association for the Development of Digital Assets (ADAN) as he promised more government support.

France has become one of the biggest hot spots for crypto wrench attacks, where criminals use physical violence to coerce victims into handing over crypto. Approximately 11% of French people own cryptocurrencies, according to ADAN, which equates to about 7.3 million people.

France’s rapid alert and protection system

Earlier this year, French authorities launched a dedicated prevention platform and a rapid-alert and protection system for crypto holders and professionals, which has attracted 724 sign-ups so far, Nuñez said.

Nuñez said that emergency measures have resulted in 200 arrests, with one recent attacker being arrested within eight hours on Friday, thanks in part to the victim using an emergency identification hotline.

Related: StarkWare introduces ‘Private KYC’ to address personal data breaches

Nuñez promised a “more ambitious” three-part plan to reinforce security measures for the crypto sector. This includes stronger intelligence-sharing, since criminal networks are often based abroad, a deeper partnership with ADAN and better operational coordination between security services.

French wrench attacks on the rise

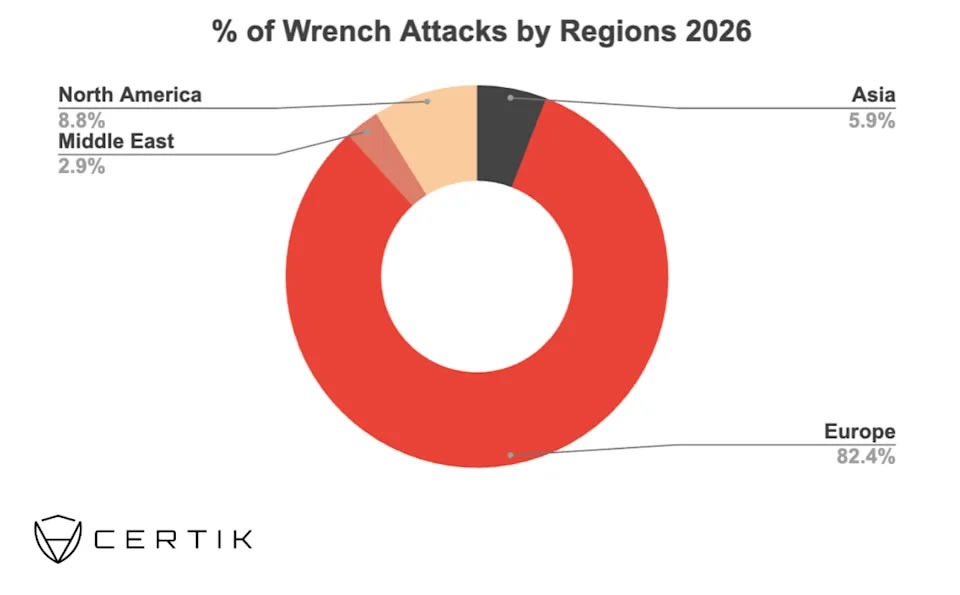

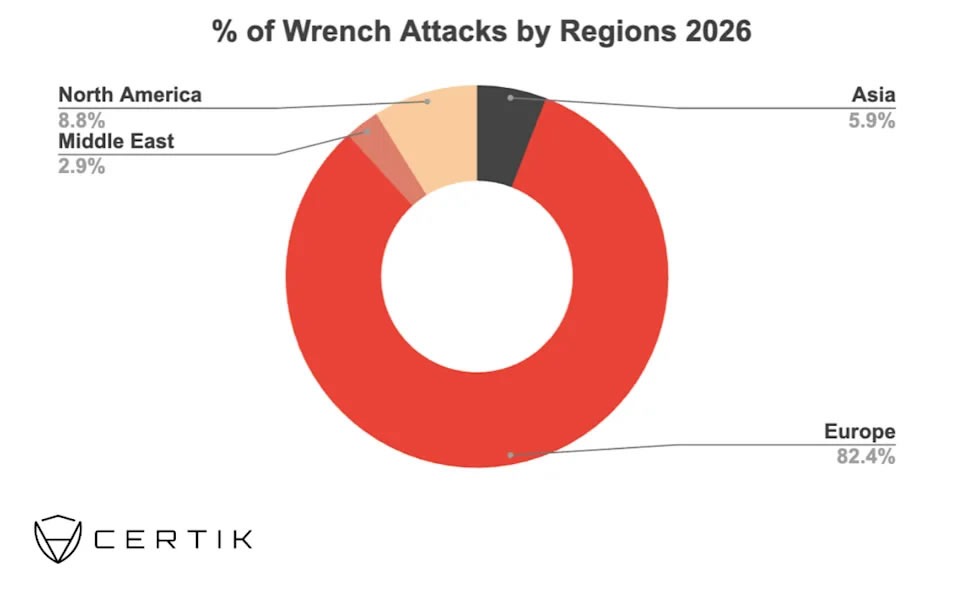

Blockchain security firm CertiK reported in May that wrench attacks globally were up 41% in the first four months of 2026, compared with the same period last year, with most attacks in Europe.

The firm said France is the “epicenter” of attacks because of the presence of several flagship industry companies and their executives, a “culture of flexing and voluntary doxxing that remains deeply embedded in the community,” and proven exposure from numerous sensitive data leaks.

David Balland, co-founder of French hardware wallet maker Ledger, was kidnapped and held for ransom along with his partner in January 2025 before being rescued by police.

Ledger suffered one of the industry’s most damaging data breaches when its customer database was hacked in 2020, resulting in the leak of more than 270,000 personal records and a wave of phishing and wrench attacks that continue to this day.

“France ranks among the most targeted countries in the world for this type of breach,” CertiK said.

Europe is becoming a hotbed for wrench attacks in 2026. Source: CertiK

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

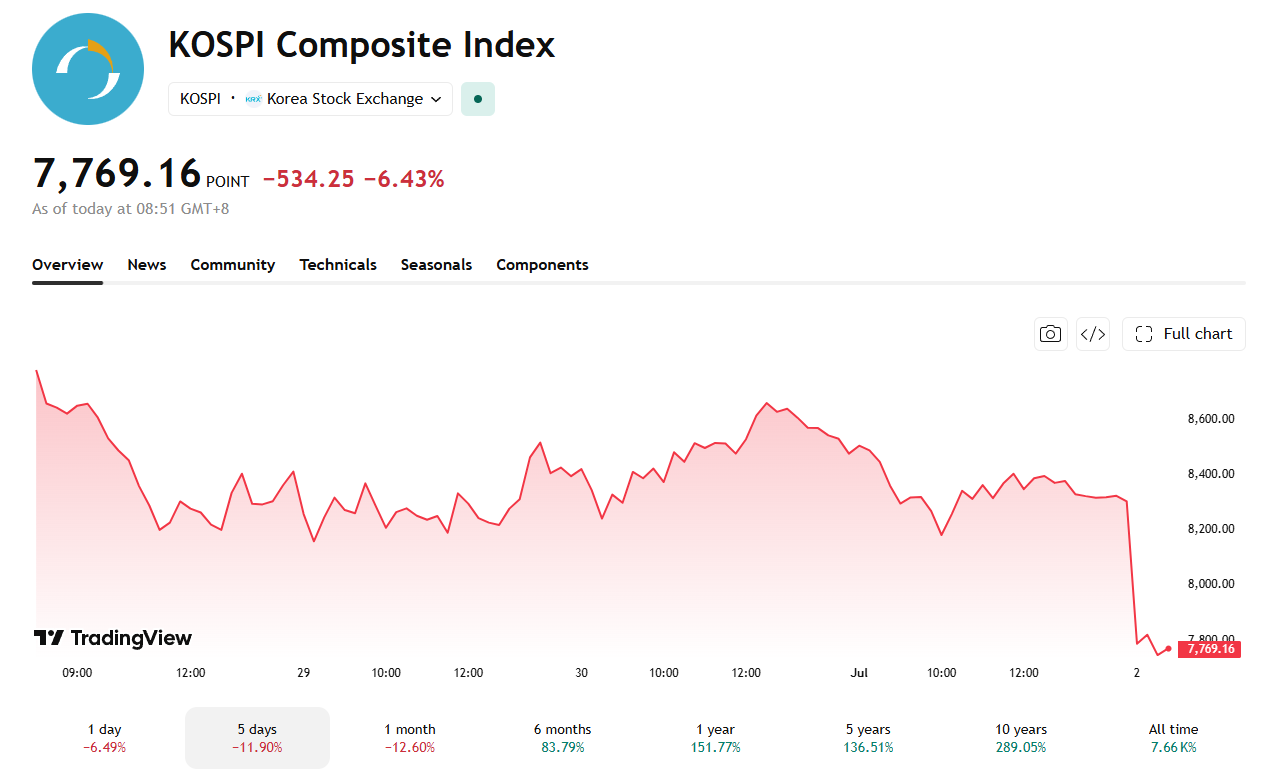

The KOSPI sank below 8,000 on July 2. The drop pushed the Korea Exchange (KRX) to activate a sell-side sidecar within minutes of the opening bell.

The Korea Exchange suspended program trading on KOSPI-listed shares for five minutes. Heavy selling in semiconductor stocks drove the move. The benchmark opened 4.46% lower and kept falling from there.

Another Halt in a Record-Breaking Year

The index had dropped 534.25 points, or 6.43%, to 7,769.16 by 9:51 a.m. local time. A sell-side sidecar triggers automatically once KOSPI 200 futures fall 5% or more for at least one minute.

Thursday’s pause is far from an isolated event. The exchange has repeatedly triggered sidecars and circuit breakers throughout 2026. Volatility this year has already topped the 2008 financial crisis, when the KOSPI set its prior annual sidecar record of 26 halts.

By late June, the KRX had logged close to 30 sidecar activations and five circuit breakers this year alone. Both figures already beat that 2008 tally.

Chipmakers Bear the Brunt

Samsung Electronics and SK Hynix together make up roughly half of the KOSPI’s market capitalization. The two chipmakers have repeatedly driven these swings. Their shares extended losses again Thursday, tracking a global chip stock selloff that started on Wall Street overnight.

The Nasdaq Composite slid 0.66% Wednesday. The VanEck Semiconductor ETF lost 5.4%. Micron Technology and Sandisk each dropped more than 10%. The rout followed weeks of sharp reversals in the KOSPI’s chip-driven rally, a rally that had pushed the index to record highs earlier this year.

Semiconductor stocks still dominate the index. Traders now face a familiar question: will Thursday’s selloff deepen further, or fade as quickly as prior swings have this year.

The post KOSPI Drops Below 8,000, Triggers Yet Another 2026 Trading Halt appeared first on BeInCrypto.

Senator Cynthia Lummis defended the Clarity Act against Senator Elizabeth Warren, rejecting claims that the digital-asset bill creates illicit finance loopholes and pointing to more than 16 safeguards written into the legislation.

The Wyoming Republican responded after Warren argued that adversaries exploit crypto to move billions and that the bill would weaken standards. Their clash comes as the Senate races against a narrow legislative calendar.

Follow us on X to get the latest news as it happens

Lummis Points to Built-In Safeguards

Lummis countered that the Clarity Act strengthens illicit finance rules rather than weakening them. She listed specific provisions in a public rebuttal.

Lummis noted that Section 201 applies the Bank Secrecy Act and anti-money laundering (BSA/AML) rules to crypto. Section 303 adds new sanctions aimed at Iran. Section 305 lets exchanges freeze dirty money.

“If you don’t like crypto, then say it, but stop these baseless attacks,” she said.

Illicit finance concerns have become a central sticking point for the legislation. Law enforcement groups and Catholic coalitions pushed back in separate letters last month.

Their objections targeted Section 604, the bill’s developer safe harbor. Critics say broad exemptions could weaken oversight of criminal fund flows.

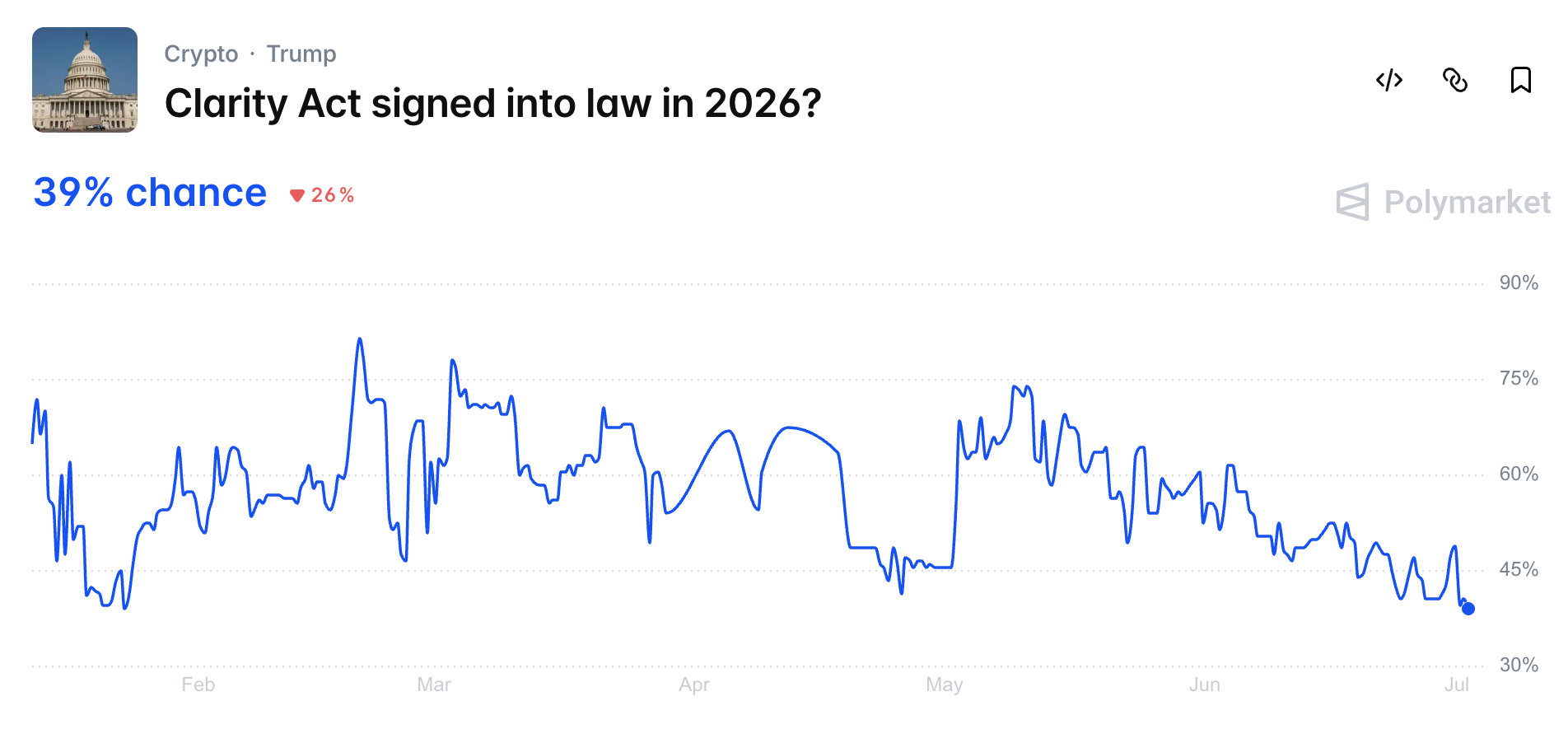

Clarity Act Passage Odds Slide on Polymarket as Deadline Nears

Meanwhile, the timing raises the stakes for the bill. The Senate returns from recess on July 13, leaving a narrow window before the August break.

The bill must clear the Senate by then to stand a chance of becoming law this year. That path requires 60 votes, including at least seven Democrats.

Prediction markets have turned cautious. On Polymarket, the odds of the Clarity Act becoming law in 2026 fell to 39%, down from 64% in early June.

Analysts have shifted, too. Galaxy Research now puts the odds of the CLARITY Act becoming law in 2026 at 50%, down from 60% on June 5, citing the shrinking Senate calendar.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Senator Lummis Calls to Stop ‘Baseless Attacks’ on the Clarity Act appeared first on BeInCrypto.

Tether has frozen USDT balances in 131 TRON wallets linked to ISIS-K after U.S. sanctions officials added more than 100 crypto identifiers tied to the group.

Summary

- Tether froze USDT balances across 131 ISIS-K-linked TRON wallets after OFAC updated its sanctions identifiers.

- Chainalysis said the TRON wallets received over $1.4 million and sent over $880,000 since 2023.

- The action adds pressure on VASPs to update sanctions screening for newly listed crypto addresses.

The move places stablecoin issuer controls at the center of a new terrorism-financing action involving TRON and Monero addresses.

Chainalysis said the U.S. Treasury’s Office of Foreign Assets Control updated its ISIS-K designation on July 1. The update added 134 crypto wallet identifiers, including 131 TRON addresses and three Monero addresses.

“Tether has frozen the balances on all 131 TRON addresses,” said Chainalysis.

The official OFAC update lists the wallets under ISIL Khorasan, also known as ISIS-K. The group is the Islamic State’s Afghanistan and Pakistan branch. OFAC had already designated ISIS-K as a terrorist group before adding the new crypto wallet identifiers.

Chainalysis tracks Tether flows across TRON wallets

Chainalysis said the 131 TRON addresses had received more than $1.4 million since 2023. The same wallets sent out more than $880,000 over that period. The blockchain analytics firm said several listed wallets had exposure to mainstream services and also sent funds to Syria-based crypto exchangers.

The report said ISIS-K’s media branch, al-Azaim Media Foundation, has used websites and messaging platforms to seek crypto donations. Chainalysis said it had collected past donation addresses on TRON, Monero, and Bitcoin. The firm also noted that earlier public terrorism-financing campaigns often used smaller donations, rather than a few large transfers.

Stablecoin freeze role keeps growing

The latest freeze follows a wider rise in issuer-level enforcement around USDT. As previously reported, Tether’s T3 Financial Crime Unit passed $450 million in frozen suspected illicit assets since its 2024 launch. The unit is backed by Tether, TRON, and TRM Labs, and focuses on USDT activity on the TRON network.

Moreover, Tether froze more than $514 million across 370 addresses during one 30-day period earlier this year. Most of the frozen funds were on TRON. BlockSec data cited in that report showed Tether blacklisted 4,163 addresses in 2025, freezing $1.26 billion across Ethereum and TRON.

Sanctions pressure reaches compliance teams

The ISIS-K action also comes after other terrorism-linked wallet freezes this year. Victims with U.S. terrorism judgments asked a New York court to order Tether to turn over 344,149,759 USDT held in two OFAC-blocked TRON wallets linked to Iran’s IRGC. That case centers on whether frozen stablecoins can be transferred to judgment creditors.

Chainalysis said the July 1 actions require virtual asset service providers and financial institutions to update sanctions screening and transaction monitoring. The firm also said it labeled the relevant addresses in its products. The step gives compliance teams a way to detect exposure to the newly listed ISIS-K wallets and related networks.

Lightning sign veteran defenceman John Carlson to two-year deal

Want to be an astronaut? Career routes that can take you to space

Putin’s revenge: Kyiv is hit by huge drone and missile attack in Russian retaliation for Ukraine’s long-range strikes

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics6 days ago

Politics6 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World2 days ago

Crypto World2 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics6 days ago

Politics6 days agoPotential 2028er World Cup attendee leaderboard

-

Business6 days ago

Business6 days agoAsia stock markets slide as tech shares slump

-

News Videos3 days ago

News Videos3 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech6 days ago

Tech6 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World7 days ago

Crypto World7 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World5 days ago

Crypto World5 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business2 days ago

Business2 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World5 days ago

Crypto World5 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports5 days ago

Sports5 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech4 days ago

Tech4 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech2 days ago

Tech2 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Tech5 days ago

Tech5 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World6 days ago

Crypto World6 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRTX holders must register wallets before token distribution begins

-

Sports17 hours ago

Sports17 hours agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business3 days ago

Business3 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

You must be logged in to post a comment Login