Crypto World

Securitize Tokenizes Secz Stock On Nyse Debut As Shares Jump 10%

Securitize entered the public market with an onchain push that ties its NYSE debut to tokenized equity. The BlackRock-backed platform tokenized its common stock, SECZ, on Solana and Avalanche as trading began. The move also came as crypto-linked stocks rallied, while Bitcoin recovered to the $62,000 level.

Securitize Brings SECZ Shares Onchain

Securitize launched its tokenized common stock on the same day it listed on the New York Stock Exchange. The company trades under the ticker SECZ after completing its merger process with Cantor Equity Partners II. Therefore, the listing gives the tokenization firm a public-market platform and an onchain equity structure together.

The company made tokenized SECZ available to eligible U.S. users through its regulated platform. It selected Solana and Avalanche for the initial rollout, giving the stock exposure across two major blockchain networks. However, the company said the tokenized version represents the same common stock listed on the NYSE.

Securitize has long built its business around regulated tokenized assets and issuer-led market infrastructure. The company has supported tokenized funds and real-world asset products across public blockchains. As a result, its own stock tokenization marks a direct test of the model it promotes.

Tokenized Stock Keeps The Same Share Rights

Securitize said the tokenized SECZ does not create a separate share class or change the underlying stock. Instead, tokenization changes the form of ownership while the traditional share remains the same. Therefore, legal limits, transfer rules, and contractual restrictions still apply to the equity.

The company expects the launch to create an onchain shareholder base from its first day as a public firm. It also expects future market tools and utility to develop around the tokenized shares. However, the current rollout focuses on regulated access and direct representation of listed common stock.

The launch adds fresh context to the wider tokenization market, which has gained stronger institutional interest. Asset managers and blockchain firms have moved more bonds, funds, and securities onto digital rails. Consequently, Securitize’s public listing places tokenized equity closer to mainstream market infrastructure.

SECZ Stock Rises As Crypto Market Rebounds

SECZ gained more than 10% during its first trading session, according to TradingView data cited in the report. The stock traded near $12 as broader crypto-linked equities also advanced. Meanwhile, Bitcoin’s rebound to around $62,000 helped improve sentiment across the digital asset sector.

The rally followed a stronger session for several companies connected to crypto markets and blockchain infrastructure. Securitize benefited from its public debut and its tokenization announcement on the same day. Moreover, the BlackRock connection added further attention to the company’s market entrance.

The debut also arrived after Cantor Equity Partners II shareholders approved the merger that allowed the listing. That approval cleared the path for Securitize to enter public markets through the transaction. Now, the company has positioned SECZ as both an NYSE-listed stock and a regulated onchain equity product.

Public miners have dumped Bitcoin at a record pace, hashprice has collapsed to post-halving lows, and older machines are switching off. That is the textbook definition of capitulation. The harder question is whether it marks a bottom or the start of a deeper shakeout.

Summary

- Publicly traded Bitcoin miners sold more than 32,000 BTC in the first quarter of 2026, a single-quarter record that exceeded their combined sales for all of 2025 and topped the roughly 20,000 BTC sold during the Terra-Luna collapse in 2022.

- The pressure is economic: hashprice, the revenue a miner earns per unit of computing power, fell to post-halving lows in the high-$20s per petahash per day by mid-2026, well below the roughly $35 breakeven for older machines, putting a large share of the industry underwater.

- Network hashrate has started to fall as older hardware powers down, the classic signature of a miner capitulation, in which the least efficient operators stop mining at a loss.

- The bull reading is that capitulation has historically marked bottoms, because it clears weak capacity, lowers difficulty, and rewards the survivors. The bear reading is that this squeeze is structural, with heavy debt, record ETF outflows, and even Strategy turning seller removing the usual counterweight.

- Whether this is a bottom or a way station depends on whether Bitcoin can reclaim miner production cost, estimated by some near $80,000, against a price sitting closer to $58,000.

Bitcoin miners are supposed to be the market’s most committed holders, the operators who spend real money to produce coins and who have every incentive to keep them. So when miners start dumping Bitcoin at a record pace and switching off machines, the market pays attention, because it usually means something has broken in the economics of production. That is exactly what has happened through the first half of 2026. Public miners have sold more Bitcoin than in any prior quarter on record, hashprice has fallen to lows not seen since the last halving, and network hashrate has begun to slip as older rigs go dark.

This piece works through what is driving the selling, what capitulation actually means, and the real disagreement underneath it: whether a miner capitulation at these levels marks the bottom, as it often has, or whether this cycle is different. The signal matters because miners sit at the production edge of Bitcoin, where price, power costs, difficulty, debt, and treasury strategy meet. It also lands at a moment when Bitcoin sentiment is already washed out, making every capitulation signal easier to overread.

The record selling

The headline number is stark. Publicly traded mining companies, including MARA, CleanSpark, Riot Platforms, Cango, Core Scientific, and Bitdeer, collectively sold more than 32,000 Bitcoin in the first quarter of 2026, according to industry trackers. That figure set a single-quarter record. It exceeded what those same companies sold across all four quarters of 2025 combined, and it surpassed the roughly 20,000 Bitcoin they offloaded during the second quarter of 2022, the depths of the bear market that followed the Terra-Luna collapse.

When miners sell more in three months than they did in a full prior year, and more than during one of the worst crises in crypto history, the signal is hard to ignore. The individual disclosures fill in the picture. Riot Platforms sold 3,778 Bitcoin in the first quarter at an average price near $76,626, generating about $289.5 million, while producing only 1,473 coins in the same period, meaning it sold far more than it mined. Core Scientific liquidated roughly 1,900 Bitcoin worth about $175 million in January alone. Cango sold 2,000 Bitcoin in March for approximately $143 million, using the proceeds to retire Bitcoin-backed loans.

In a single week, MARA, Genius Group, and Nakamoto Holdings revealed combined sales of more than 15,000 coins, with the largest share from MARA. These were not routine sales of freshly mined coins to cover the power bill; they were drawdowns of treasury reserves the companies had previously chosen to hold. The trend shows up in the aggregate data too. The total Bitcoin held by miners, a metric some analysts call the miner reserve, has been declining since 2023, falling from more than 1.86 million coins at the end of that year toward roughly 1.8 million by mid-2026.

Selling that once looked like occasional balance-sheet management has become a sustained drawdown, and the pace accelerated as prices fell. The question is what forced it. The answer begins with mining economics, but it does not end there.

Why miners are selling

The answer is a profit squeeze that has been building since the last halving. The central metric is hashprice, which measures the daily revenue a miner earns per unit of computing power. Hashprice has been sliding since mid-2025, and by the first half of 2026 it had fallen to record post-halving lows, dropping into the high-$20s per petahash per day on some trackers, down roughly two-thirds from the October 2025 peak. The breakeven level for many miners running older equipment sits near $35 per petahash per day.

With hashprice well below that line, a large share of the industry, estimated at around a fifth at points earlier in the year, has been operating at a loss. Several forces compounded to produce that squeeze. The April 2024 halving cut the block reward in half, instantly halving the Bitcoin miners earn for the same work. Network difficulty has climbed relentlessly since, sitting roughly 10 times higher than in 2021, which means far more computing power now competes for that smaller reward.

Energy costs rose as Middle East conflict pushed oil higher and pressured power prices. Bitcoin itself fell, dropping toward a 21-month low near $58,000, so the coins miners produce are worth less at the moment they most need the cash. Taken together, mining profitability has compressed by close to an order of magnitude from its peak. Debt turned the squeeze into forced selling.

Aggregate miner debt surged over the past year, rising from around $2.1 billion to roughly $12.7 billion as companies borrowed to fund expansion, buy more efficient rigs, and diversify. Debt has to be serviced regardless of price, so when revenue collapses, miners with loan obligations have little choice but to sell coins or, in some cases, sell coins specifically to repay Bitcoin-backed loans. Some estimates put the all-in cost to produce a single Bitcoin near $80,000, well above the current price, which means the least efficient operators are now mining at a loss on every coin. That is the condition that forces capitulation.

What capitulation actually means

Capitulation is a loaded word, so it helps to define it precisely. In mining, capitulation is the point in a cycle where revenue falls below what a meaningful share of the network costs to run, and those operators power down their machines rather than keep mining at a loss. It is not a crash or a malfunction. It is the market clearing, the mechanism by which the least efficient capacity leaves the network when it can no longer pay for itself.

The signature of capitulation is a falling hashrate, and that is now visible. As unprofitable machines switch off, the total computing power securing the network declines. By mid-2026, a meaningful slice of older hardware had gone offline, and the 30-day average network hashrate had fallen by several % from its highs, after earlier swings in which difficulty dropped sharply and then rebounded as miners reconnected. When hashrate falls and stays down, Bitcoin’s built-in difficulty adjustment eventually lowers the bar, making it cheaper and more profitable to mine for the operators who remain.

That self-correcting loop is what distinguishes a mining capitulation from a permanent decline. Analysts track this through indicators built on hashrate momentum, which flag when short-term hashrate falls below its longer-term trend, historically a marker of miner stress and, often, of a market bottom forming. The pattern moves through recognizable stages: revenue falls below cost, weak operators power down, hashrate and difficulty drop, and the survivors, who sit on cheaper power and more efficient machines, absorb the share the leavers gave up and become more profitable. The shakeout is loud and it photographs like a collapse, but the underlying mechanism is orderly.

Whether that orderly clearing is bullish or bearish for the Bitcoin price is where the disagreement begins. For miners, capitulation is an industry sorting event. For traders, it is a possible bottom signal. Those are related, but not identical.

The bull case: capitulation marks bottoms

The optimistic reading rests on history. Miner capitulations have consistently preceded recoveries rather than endings. The logic is mechanical, not hopeful. When high-cost operators power down, network difficulty falls, which lowers the cost to mine for everyone still online.

The efficient survivors, running new machines on cheap power, then capture a larger share of a reward that has become cheaper to earn, so their margins expand even if the price does not move. The capitulation sorts the industry on a single variable, cost per hash, and consolidates it around its lowest-cost producers. For the price, the argument is that miner capitulation tends to coincide with peak seller exhaustion. Miners are a persistent source of supply, selling coins into the market to fund operations.

When the highest-cost miners give up and switch off, that stream of forced selling thins out, removing pressure that had been weighing on the price. Historically, the crossover in hashrate momentum indicators that signals capitulation has aligned with attractive long-term entry points, because it marks the moment the weakest hands, on the production side, have been washed out. The recovery mechanism has proven fast in the modern, industrialized mining sector. Earlier in 2026, a difficulty drop of around 11% was followed within two weeks by a record upward adjustment near 15% as miners reconnected the moment conditions eased.

That speed is the point: surviving operators are committed and well-capitalized enough to scale back up quickly when hashprice recovers. In this reading, the record selling and the falling hashrate are not a warning but a washout, the part of the cycle where the field clears before the next leg up. The bull case does not deny the pain. It argues that the pain is how the reset finishes.

The bear case: this squeeze may be structural

The skeptical reading argues that the usual capitulation-marks-a-bottom pattern assumes a market backdrop that no longer holds. The first difference is debt. The mining sector carries far more leverage than in past cycles, with aggregate debt having climbed toward $12.7 billion, which means capitulation now involves not just idle machines but the risk of defaults, forced liquidations, and distressed asset sales that can overhang the market longer than a simple hashrate reset would. The second and larger difference is who is buying.

In past capitulations, miner selling was absorbed by a mix of retail and, more recently, institutional demand. In 2026, the marginal buyer has turned into a seller. U.S. spot Bitcoin ETFs recorded their worst month on record in June, with roughly $4.5 billion in net outflows, removing the very demand channel that had absorbed supply on the way up. Even Bitcoin treasury companies, long the reliable counterweight to miner selling, have wobbled: the largest corporate holder made its first Bitcoin sale in years to fund a dividend and has come under pressure over its financing structure.

When miners sell into a market where ETFs are bleeding and the corporate bid is faltering, the supply has fewer places to go, and the price can keep falling even as capitulation runs its course. The third concern is duration. Capitulation clears quickly only if price recovers to pull survivors back and thin the selling. If Bitcoin remains stuck well below the estimated production cost for an extended period, held down by a hawkish Fed and tight liquidity, the squeeze can grind on, pushing even mid-cost operators toward the exit and turning a healthy shakeout into a prolonged contraction.

In this view, the capitulation signal is real, but the conditions that historically turned it into a bottom, rebounding demand and easing macro, are absent, so the pattern may not repeat on its usual schedule. This is also where Strategy’s balance sheet matters, because the market’s biggest corporate Bitcoin buyer is no longer treated as an unconditional bid. The bear case is not that miner capitulation does not exist. It is that capitulation may not be enough when the buyers are missing.

The AI pivot: capitulation or reinvention

There is a third storyline that complicates the simple capitulation frame, and it is specific to this cycle. Many miners are not simply powering down; they are repurposing. The same data centers, power contracts, and cooling infrastructure that mine Bitcoin can, with investment, host the computing demand of artificial intelligence and high-performance workloads, which command far higher and more stable revenue than mining at current hashprice. Several operators have pivoted hard in that direction, converting capacity or striking deals to serve AI customers instead of mining coins.

That pivot muddies the read on hashrate and selling. Some of the machines going dark are not distressed operators giving up but companies reallocating capacity to a more profitable use, and some of the Bitcoin being sold is funding that transition instead of covering losses. For those firms, selling coins and reducing mining is a strategic reallocation, not a capitulation in the traditional sense. It is a rational response to a world where a unit of power and compute is worth more pointed at AI than at a halved block reward.

The implication cuts both ways for Bitcoin. On one hand, the AI pivot means some hashrate decline reflects opportunity rather than distress, which is less bearish for the price and could permanently shrink the pool of forced sellers. On the other hand, it means the mining industry’s most valuable operators may increasingly treat Bitcoin as a secondary business, weakening the reflexive commitment that made miners such steadfast long-term holders. A sector that once mined and held because it believed in the asset is becoming a sector that mines, or computes, wherever the margin is best.

That shift also connects miners to the broader class of Bitcoin treasury companies, where balance-sheet Bitcoin is no longer always sacred. Coins can be collateral, reserves, working capital, or transition funding. In a tight market, that difference matters. It means miner selling is not always panic, but it is still supply.

The divergence that matters

Underneath all of it sits one divergence worth watching more than any single figure. On the supply side, miners are selling into weakness while their reserves shrink and their hashrate falls. On the demand side, the buyers who absorbed that supply on the way up have stepped back, with ETFs posting record outflows and the flagship corporate holder turning seller. In prior cycles, miner capitulation coincided with new demand stepping in at low prices, which is what turned the washout into a floor.

This time, the demand side is thinner precisely when the supply side is capitulating. That is why the capitulation signal, on its own, is not enough to call a bottom in 2026. The historical pattern is real, and the mechanics that clear weak capacity and reward survivors still function. But the pattern completed into a recovery in past cycles because demand returned to meet the reduced supply.

The open question now is whether a new source of demand, renewed ETF inflows, a macro shift toward easier policy, or a return of the corporate bid, arrives to meet the capitulating miners. Until it does, the cleaner read is that miners are doing exactly what they do at cycle lows, while the buyers who usually meet them there have not yet shown up. That makes this capitulation signal important, but incomplete. It is a setup, not a confirmation.

The same distinction applies to corporate Bitcoin holders. A company can hold Bitcoin and still create supply pressure if it sells, or demand if it accumulates. The market does not care which category a holder belongs to; it cares whether they are adding or removing coins from available supply. Right now, the supply-side pressure is visible, and the demand-side recovery has not yet proven itself.

What to watch

For anyone trying to judge whether this capitulation marks a turn, a handful of signals matter more than the daily price. The first is hashprice: a sustained recovery back above the roughly $35 per petahash breakeven would ease the forced selling at its source, while a further slide would deepen it. The second is hashrate and difficulty: a stabilization in network hashrate, followed by a downward difficulty adjustment, would confirm the clearing is working and would improve economics for the survivors. Momentum indicators built on hashrate crossing back above their longer-term trend have historically flagged the completion of a capitulation.

The third is the demand side, which this cycle makes decisive. A return of net inflows to spot Bitcoin ETFs would signal that the marginal buyer is back, and a resumption of corporate treasury accumulation would restore the counterweight to miner selling. The fourth is the price relative to production cost: Bitcoin reclaiming and holding above the estimated all-in cost to mine a coin would pull the economics back into profitability and remove the pressure driving the sales. Until those turn, the record miner selling and the falling hashrate tell a consistent story of an industry clearing its weakest capacity, with the crucial question, whether fresh demand arrives to complete the pattern, still unanswered.

That is the disciplined read. Miner capitulation can mark a bottom, but it does not create one by itself. It needs confirmation from price, hashprice, ETF flows, and corporate demand. Without that, capitulation remains evidence of stress, not proof of recovery.

Frequently asked questions

Why are Bitcoin miners selling so much Bitcoin?

Miners are selling because their economics have collapsed. Hashprice, the revenue earned per unit of computing power, fell to post-halving lows in the high-$20s per petahash per day by mid-2026, below the roughly $35 breakeven for older machines. The 2024 halving cut rewards, difficulty rose about 10 times from 2021, energy costs climbed, and Bitcoin fell toward a 21-month low, forcing miners with heavy debt to sell coins to cover costs.

How much Bitcoin did miners sell in 2026?

Publicly traded miners including MARA, CleanSpark, Riot, Cango, Core Scientific, and Bitdeer collectively sold more than 32,000 Bitcoin in the first quarter of 2026. That set a single-quarter record, exceeding their combined sales for all of 2025 and topping the roughly 20,000 Bitcoin sold during the 2022 Terra-Luna bear market. The total Bitcoin held by miners has fallen from about 1.86 million at the end of 2023 toward 1.8 million. The pace of selling shows miners treating reserves as working capital in a stressed market.

What is miner capitulation?

Miner capitulation is the point in a cycle where mining revenue falls below what a meaningful share of the network costs to run, so those operators power down instead of mining at a loss. Its signature is a falling network hashrate as unprofitable machines switch off. It is a market-clearing mechanism: weak capacity leaves, Bitcoin’s difficulty adjustment lowers the bar, and the efficient survivors become more profitable. It is painful for the sector but can improve economics for the miners that remain.

Does miner capitulation mean the price has bottomed?

Historically, miner capitulation has often preceded recoveries, because it clears weak capacity, lowers difficulty, and thins the forced selling that weighs on price. But that pattern completed into a bottom in past cycles because new demand stepped in at low prices. In 2026, ETFs have posted record outflows and even the largest corporate holder turned seller, so the usual demand counterweight is thinner, making the signal less reliable on its own. Capitulation is a bottoming condition, not a guaranteed bottom.

What is hashprice and why does it matter?

Hashprice is the daily revenue a miner earns per unit of computing power, typically quoted per petahash per second per day. It combines the Bitcoin price, network difficulty, and transaction fees into a single profitability measure. When hashprice falls below a miner’s cost to operate, roughly $35 per petahash for older machines, that operator loses money on every coin, which is what drives capitulation and forced selling. A recovery in hashprice would be one of the clearest signs the pressure is easing.

Are miners capitulating or pivoting to AI?

Both are happening, which complicates the read. Some miners are genuinely distressed and powering down, while others are repurposing their data centers, power contracts, and cooling infrastructure to serve artificial intelligence and high-performance computing, which pays more than mining at current hashprice. That means some hashrate decline reflects strategic reallocation instead of distress, and some coin sales fund the transition instead of covering losses. The result is a sector that is both stressed and reinventing itself.

How does this capitulation compare to past cycles?

The mechanics are familiar, but the backdrop differs in two ways. Miner debt is far higher, having climbed toward $12.7 billion, so capitulation now carries default and forced-liquidation risk. The demand side is weaker too, with spot ETFs recording their worst month on record in June and the flagship corporate buyer turning seller. Past capitulations resolved into bottoms partly because fresh demand met the reduced supply, which is less certain now.

What signals would show the capitulation is ending?

Watch four things: hashprice recovering back above the roughly $35 breakeven, network hashrate stabilizing followed by a downward difficulty adjustment, a return of net inflows to spot Bitcoin ETFs and corporate treasury buying, and Bitcoin reclaiming the estimated production cost near $80,000. Hashrate momentum indicators crossing back above their longer-term trend have historically marked the completion of a miner capitulation. In this cycle, ETF inflows may be the most important confirmation because they show the marginal buyer has returned.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices and mining economics are highly volatile, and historical patterns do not guarantee future outcomes. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed professional before making financial decisions. Figures are accurate as of July 2, 2026, and will change.

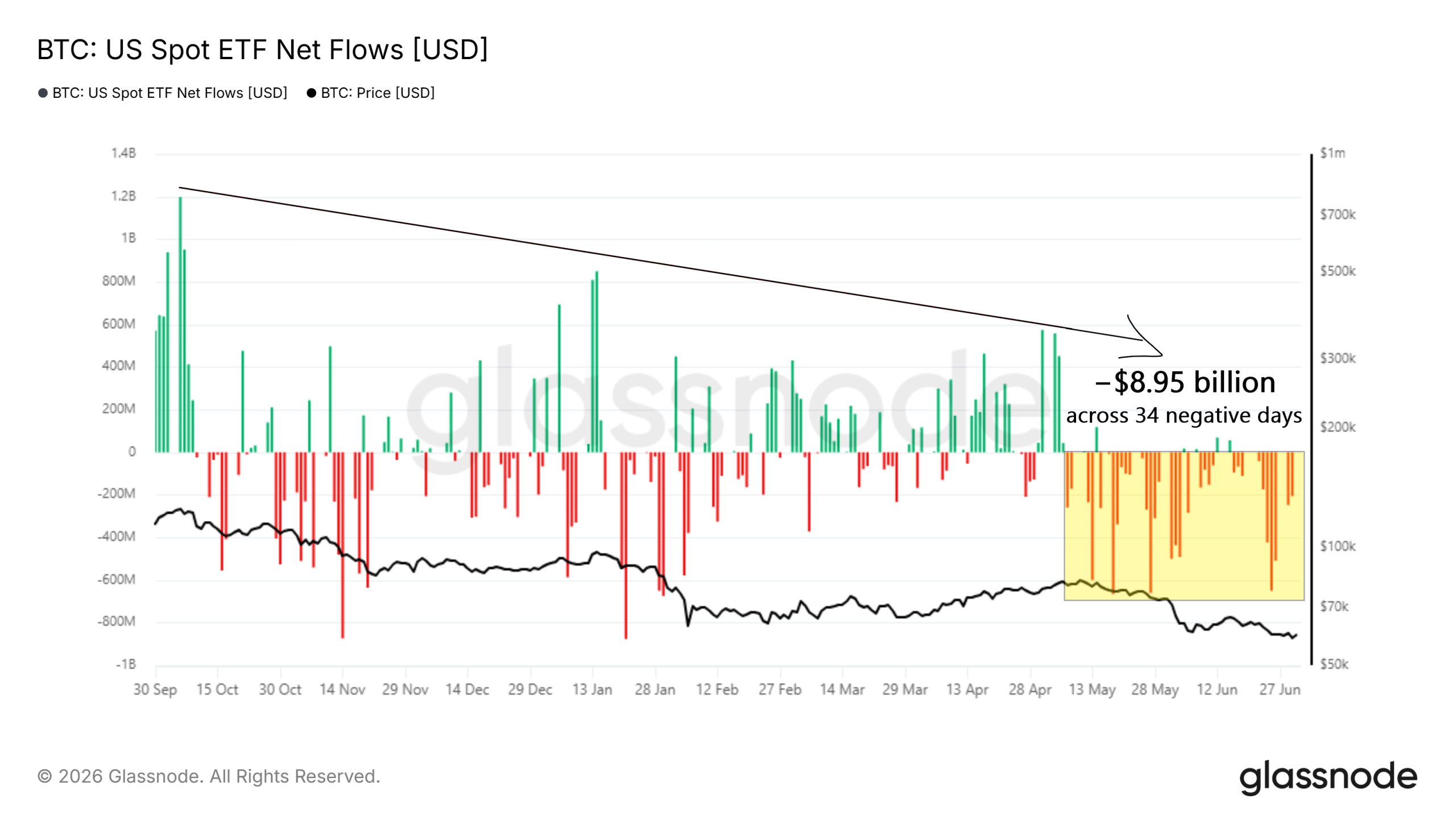

US spot Bitcoin (BTC) exchange-traded funds (ETFs) recorded another $296 million in net outflows over the past 24 hours, equal to roughly 5,050 BTC. BlackRock led the redemptions, with Grayscale, Fidelity, and ARK Invest also posting losses.

Glassnode data shows the sell-off has now reached $8.95 billion since May 7. Bitcoin trades near $61,600, up 2.4% in 24 hours, but flow data suggests the bounce rests on fragile ground.

ETF Outflows Total $8.95 Billion Across 34 Negative Days

Glassnode’s US spot ETF net flow data shows demand weakening since late September 2025. Daily inflows peaked above $1.2 billion back then. Since then, positive days have grown smaller and less frequent.

The decisive shift arrived on May 7. Since that date, the funds have posted only five positive sessions. The remaining 34 trading days were negative, draining $8.95 billion in total.

June alone accounted for $4.5 billion, the worst monthly outflow since the products launched in January 2024. Meanwhile, bitcoin fell 20.48% over the month, its steepest drop since June 2022.

In an X post, analyst That Martini Guy argued that the latest rebound changes little.

“Everyone got excited by yesterday’s bounce. But ETF selling hasn’t stopped. Funding is starting to shift, sentiment still looks fragile, and I don’t think the market structure has changed just yet.”

For the pressure to ease, the ETFs would need a sustained run of net inflows rather than isolated green days. So far, no such streak has appeared.

Coins Leave Exchanges, Yet Bitcoin Keeps Falling

Exchange balance data complicates the bearish picture. Glassnode’s net position change metric shows coins flowing out of exchanges since late May. Traders usually read such withdrawals as accumulation, because coins move into long-term storage.

However, history offers a warning. The current move is the third deep negative stretch since bitcoin’s all-time high in late 2025. The first ran from late October through December 2025. The second lasted from late January to early March 2026, when the metric dipped near minus $100 billion.

Each episode coincided with a continuation of the downtrend rather than a reversal (blue boxes). In contrast to the usual bullish reading, apparent accumulation has repeatedly failed to stop the decline. Deepening capitulation signals elsewhere on-chain tell a similar story.

Moreover, part of the withdrawal may reflect mechanics rather than fresh buying. Coins redeemed from ETFs can move between custody wallets and cold storage without touching order books. Weak US demand readings support that interpretation.

BTC Price Outlook Hinges on Slowing ETF Redemptions

The two datasets point to one conclusion. ETF flows, not exchange balances, currently set the marginal price of Bitcoin. Until redemptions slow, on-chain accumulation looks unable to absorb the selling.

BTC trades near $61,600 after a 2.4% daily gain. Nevertheless, the price has hovered just above $60,000 since mid-June. A decisive close below that area would confirm that redemption pressure still dominates the market.

Conversely, a sustained flip to net inflows could mark the first structural change since early May. Historically, flow reversals of that kind have preceded durable bottoms rather than followed them.

Until either signal appears, caution remains the sober reading of the data. The next leg depends on whether ETF holders stop selling before spot buyers give up.

The post Bitcoin ETFs Bleed $8.95 Billion in Two Months, and the Selling Isn’t Over appeared first on BeInCrypto.

Strategy’s era as the dominant Bitcoin buyer may have come to an end following last week’s STRC turmoil, which cast doubt on the company’s Bitcoin-buying strategy and sent the cryptocurrency to a nearly two-year low, according to Bitwise chief investment officer Matt Hougan.

“For years, Strategy has been the most dominant Bitcoin buyer in the world and a one-way source of Bitcoin demand. Those days are likely over,” Hougan said Thursday.

“I just expect it to be a less important figure in Bitcoin in the next cycle than it was in the last,” Hougan said, adding that investment banks, asset managers, pensions, endowments and sovereign wealth funds will likely replace Strategy as Bitcoin’s primary demand driver.

Confidence in Strategy’s Bitcoin-buying model weakened late last month when its main perpetual preferred stock offering — Stretch (STRC) — broke sharply from its $100 par value to below $75, raising fears that its dividend model was unsustainable.

The STRC incident coincided with Bitcoin (BTC) falling to a 21-month low of $58,190 on June 25, further rattling confidence across the crypto market.

Strategy responded by committing to sell Bitcoin where necessary to fund dividends and by expanding its US dollar reserve to $2.55 billion — easing immediate concerns but weakening its position as the industry’s most aggressive Bitcoin buyer, Hougan said.

Hougan said he still expects Strategy to be a “net buyer” in the next bull run, however.

Bitwise portfolio manager Gordon Grant (left) speaks with Hougan (right) about Strategy’s future outlook with STRC. Source: Bitwise

STRC example of “financial engineering” gone wrong

Hougan described the STRC incident as “classic end-of-cycle dynamics” and likened its collapse to a similar case of “financial engineering” in 2021, when Grayscale’s GBTC premium imploded.

“Money searching for high yields and low volatility was used to buy Bitcoin, which offers neither,” Hougan said. “This money never really fit Bitcoin. And so, it needs to be cleared out before we can find a bottom. That’s what’s happening today.”

Strategy’s issue with STRC overblown: Strive CEO

Strive CEO Matt Cole, however, said Strategy’s incident with STRC has drawn too much media attention and pushed down Bitcoin’s price more than it should have.

Related: Bitcoin doesn’t need Ethereum-style yield, says Strategy’s Michael Saylor

Speaking with NovaDius Wealth Management president Nate Geraci on Thursday, Cole noted that Strategy’s 847,363 Bitcoin represents just 4% of the total supply, and while Bitcoin isn’t a public company, by the US Securities and Exchange Commission’s standards, a 4% stake wouldn’t be considered material.

“If one person owned 4%, you don’t even have to report that publicly to the SEC because the SEC deems 4% to be immaterial. They start to view a position to be material at 5%.”

Strategy isn’t facing liquidity risk: Hougan

Despite concern over STRC, Hougan said Strategy has $52 billion worth of liquid assets marked against $7 billion of debt, and that Bitcoin would need to drop another 70% (about $18,500) for the company to be put at risk.

Hougan also noted that if Strategy were to start selling its Bitcoin today, it could cover dividends from STRC and its other perpetual preferred stock offerings for the next 28 years.

Magazine: Bitcoin decouples from tech stocks, Ether eyes ‘selling wave’: Market Moves

Tokenization platform Securitize rallied on its New York Stock Exchange debut on Thursday, as it brought tokenized versions of its shares to two blockchains.

The company, which is backed by BlackRock and Morgan Stanley, began trading on the NYSE under the ticker SECZ on Thursday after merging with a Cantor Fitzgerald-backed special-purpose acquisition company to take it public.

Securitize said Thursday that it simultaneously launched tokenized versions of its shares on the Avalanche and Solana blockchains, which will be available to eligible US investors on its platform.

It marks the first time a newly public company has also offered tokenized stocks, an area of crypto technology that has quickly gained attention among major institutions drawn to the idea that it can bring deeper liquidity and longer trading hours.

Securitize has carved out a lead in the tokenization space for institutions. It partnered with the NYSE in March to create tokenized assets for the exchange’s upcoming tokenized securities platform.

US laws allow for tokenized stocks, Securitize says

Securitize said that tokenizing its stock demonstrates that tokenized securities “can be issued and accessed in the US under existing securities laws and market structure,” adding that access will be subject to onboarding, eligibility, and customer ID and money-laundering checks.

“We have long said that public equities are moving on-chain, and there is no stronger validation of that belief than tokenizing our own public stock on Day 1,” said Securitize co-founder and CEO Carlos Domingo.

“SECZ is not a synthetic token or offshore wrapper. It is issuer-sponsored tokenization of the same common stock trading on the NYSE, made available through regulated infrastructure,” he added. “This is how tokenization should scale: with real ownership, regulatory clarity and the issuer at the center.”

The US Securities and Exchange Commission clarified in January that issuer-sponsored tokenized securities are still subject to US securities laws.

In mid-May, the SEC was reportedly ready to announce an exemption for the trading of tokenized stocks, but delayed the plan later that month after stock exchange officials raised concerns over how it would be implemented.

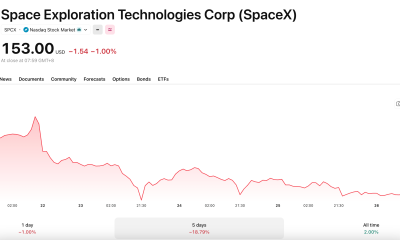

Securitize shares rise on debut

Shares in Securitize (SECZ) hit a high of $13.70 in trading Thursday but retracted slightly and ended the day at $12.30, a gain of 4.4%. The share price continued to climb 2.4% after-hours to $12.60.

Securitize ended its debut trading day on Thursday at a gain of nearly 4.5%. Source: Google Finance

Securitize raised $400 million from its public offering at a valuation of more than $1 billion.

The market for tokenized real-world assets currently exceeds $43 billion, the majority of which is tokenized money market funds, while tokenized commodities account for nearly $7 billion and tokenized stocks account for $1.6 billion, according to Token Terminal.

Analysts expect the tokenization market to grow quickly in the coming years, with Citigroup predicting last month that it could grow to between $5.5 trillion and $8.2 trillion by 2030.

Big Questions: Do we really only need 2–5 cryptocurrencies?

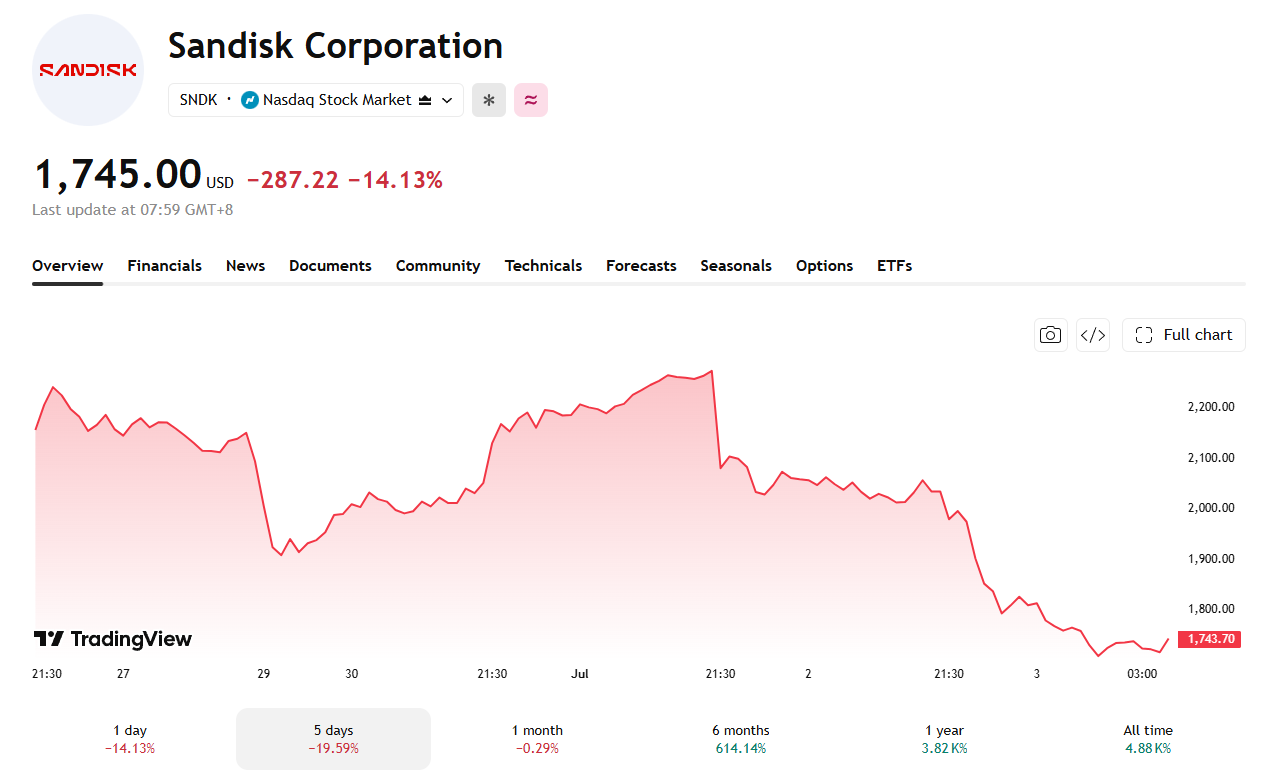

Over the last 24 hours, SanDisk shares sank 14.13%, Seagate dropped 10.38%, and Micron fell 5.49% as investors priced in a looming memory supply glut.

The three names have now lost 19.59%, 17.54%, and 14.36% over the past five sessions, respectively. That drop erases a chunk of 2026’s extraordinary rally.

A Glut Narrative Takes Hold

Morningstar’s director of research, Lorraine Tan, told Bloomberg TV that AI-linked stocks could fall 20% to 30% before becoming buyable again. She pointed to new supply coming from Samsung and SK Hynix and a potential plateau in AI capital spending.

Traders have turned that warning into this week’s working thesis. They are now questioning whether the pricing power behind the sector’s margin expansion can survive once fresh capacity lands.

A separate catalyst sharpened that realization. It was announced that Meta Platforms is building a cloud service to sell its own excess AI computing power. Investors took the plan as evidence that hyperscaler capex, and the chip demand tied to it, may be nearing a ceiling.

The news triggered a broad AI stock selloff that dragged memory and storage names down alongside chip equipment suppliers. A separate antitrust suit accusing Samsung, SK Hynix, and Micron of inflating DRAM prices has added to the scrutiny.

Bulls Push Back

Not every desk agrees with the glut thesis. Bank of America raised its SanDisk price target to $2,500 with a Buy rating. Citi made a similar call days earlier, lifting its own SanDisk target to the same level. Micron’s market capitalization surpassed Meta’s last month.

Micron reported fiscal third-quarter revenue of $41.46 billion, up 346% year over year, and guided fourth-quarter revenue to $50 billion. Micron stock still trades near seven times forward earnings even after the pullback.

Meta’s cloud ambitions could signal a genuine capex slowdown. They could also mark a new revenue stream layered onto continued AI spending. Either way, that question will likely shape the memory trade into next week.

The post AI Memory Supply Glut Fears Loom as SanDisk, Micron, Seagate All Plunge appeared first on BeInCrypto.

Bitcoin was sold as digital gold, an uncorrelated hedge that would hold up when markets broke. In 2026 it fell roughly 50% alongside the Nasdaq while gold hit record highs. So what is Bitcoin now, and did the hedge thesis ever survive contact with Wall Street?

Summary

- Bitcoin has spent 2026 moving with the Nasdaq rather than against it, with rolling correlations to U.S. tech indices reaching as high as 0.80 early in the year while its link to gold fell toward zero.

- The change traces to the spot ETF era: once institutions could hold Bitcoin inside the same portfolios as tech stocks, the same capital flows began driving both, tying Bitcoin to equity risk appetite.

- Analysts describe the current setup as the worst of both worlds, with Bitcoin taking the downside when stocks fall but not the full upside when they rally, behaving as a high-beta tail of macro risk instead of a standalone store of value.

- The counter-case is that Bitcoin is not a clean tech proxy either, since it fell on crypto-specific shocks even when tech rose, and that long-term holders kept accumulating, pointing toward an independent asset class instead of a tech clone.

- Whether the correlation is structural or a feature of the current tight-liquidity regime is the open question, and it decides whether the digital gold thesis is dead or merely dormant.

Bitcoin was supposed to be the asset that zigged when everything else zagged. For years it was sold as digital gold, an uncorrelated hedge that would protect a portfolio when stocks fell and uncertainty rose. In 2026, it has done close to the opposite. Bitcoin is down roughly 50% from its October 2025 record near $126,200, and it fell in near lockstep with technology stocks while gold climbed to record highs above $5,000 an ounce.

The asset marketed as a crisis hedge behaved like a leveraged bet on the same risk appetite that drives the Nasdaq. This piece works through the evidence that Bitcoin now trades like a tech stock, why that happened, and the serious counter-argument that the story is more complicated than a simple correlation chart suggests. The answer matters because it changes how investors should size Bitcoin, how they should compare it with gold, and whether the ETF era strengthened the asset or quietly rewired it into the same macro trade it was supposed to diversify away from.

The evidence: Bitcoin moves with the Nasdaq now

The correlation data is the starting point, and it is stark. Rolling 30-day correlations between Bitcoin and the Nasdaq 100 reached about 0.80 early in 2026, the highest level in close to four years, and Bitcoin’s longer-run five-year correlation with the tech-heavy index sits near 0.54. Standard Chartered analysts have pegged the Bitcoin-Nasdaq correlation around 0.5 with peaks near 0.8, while short-term readings against U.S. tech indices have ranged between roughly 0.55 and 0.68 through the year. However you measure it, Bitcoin and the Nasdaq have been moving together.

The relationship with gold has gone the other way. As Bitcoin’s tie to tech strengthened, its correlation with gold fell toward zero, at points reaching just 0.2. And the price paths made the divergence impossible to ignore. While Bitcoin dropped through 2026, gold surged to record highs above $5,000 and briefly toward $5,600 an ounce, outperforming Bitcoin by a wide margin over the same stretch.

The clearest test came under real stress. When conflict in the Middle East pushed oil higher and rattled markets, gold did what a safe haven does and climbed, while Bitcoin fell alongside risk assets. A hedge is supposed to prove itself precisely in those moments, and Bitcoin did not. The pattern that defined 2026 is simple to state: when the tech trade got hit, Bitcoin got hit, and when investors fled to safety, they chose gold.

Why the digital gold thesis mattered

To understand what has been lost, it helps to recall what the digital gold pitch actually claimed. Bitcoin’s founding appeal to institutions was not only its potential for gains but its supposed independence from everything else. It had a fixed supply capped at 21 million coins, no central issuer, and no cash flows tied to the economy, which in theory made it a store of value that would not move with stocks, bonds, or the business cycle. In its early years, Bitcoin was not just uncorrelated with equities; it was uncorrelated with nearly every major asset class, which made it look like the ultimate portfolio diversifier.

That property was the entire institutional case. A diversifier that zigs when the rest of a portfolio zags reduces overall risk, and that is worth paying for. Wall Street bought into the idea that Bitcoin could serve as a hedge against monetary debasement, market volatility, and economic uncertainty, a role gold has played for centuries. The digital gold narrative underpinned much of the adoption story, from corporate treasuries to the campaign for spot ETFs, because it promised something distinct from a simple speculative growth bet.

The trouble is that an asset’s identity depends not only on its design but on who owns it and how it is traded. Bitcoin’s code did not change in 2026. What changed is the profile of the people holding it and the machinery through which they buy and sell. That shift, more than anything about the protocol, is what turned the hedge into a high-beta risk asset.

What changed: the ETF made Bitcoin a portfolio asset

The pivotal event was the arrival of spot Bitcoin ETFs in January 2024, and the irony is sharp. The ETFs were celebrated as the moment Bitcoin was legitimized, folded into the regulated financial system at last. That same integration is what tied it to the equity market. Research published in late 2025 found robust evidence that ETF approval structurally altered Bitcoin’s role, marking a shift from an independent, idiosyncratic asset toward a conventional risk asset whose correlation with the S&P 500 rose sharply after the launch.

The mechanism is straightforward once you follow the money. Before ETFs, much of Bitcoin sat with crypto-native holders who traded it on its own logic. After ETFs, large institutions could hold Bitcoin exposure inside the same portfolios as their technology stocks, managed by the same risk desks using the same tools. When those desks adjust risk, they buy or sell Bitcoin and tech at the same time, for the same reasons, which welds the two together.

The marginal dollar in Bitcoin became, increasingly, the same dollar chasing artificial intelligence and growth equities, so when that dollar turned cautious, it sold both at once. This is the deeper story behind capital rotating into AI stocks that has drained crypto momentum all year. It is not only that money left Bitcoin for semiconductors; it is that the money still in Bitcoin now behaves like the money in tech, responding to the same Federal Reserve signals, the same liquidity conditions, and the same growth expectations. Bitcoin did not choose to become a tech stock. Its new owners made it one.

The worst of both worlds: downside without the upside

If Bitcoin simply tracked the Nasdaq one for one, that would be a clean story. The reality analysts have flagged is worse for holders. Trading firm Wintermute has argued that while Bitcoin’s directional correlation with the Nasdaq stayed high, the quality of that correlation deteriorated into what it called a bearish skew. In plain terms, Bitcoin has kept the downside beta, falling hard when equities fall, while losing much of the upside participation, failing to rally proportionally when equities recover.

Wintermute’s Jasper De Maere tied this to a shift in investor attention. As mindshare and risk-on capital crowded into mega-cap tech, Bitcoin remained correlated when global sentiment turned negative but stopped benefiting fully when optimism returned. He described Bitcoin as reacting like a high-beta tail of macro risk rather than a standalone narrative, keeping the downside beta while shedding the upside premium. The Kobeissi Letter put the same idea more bluntly, noting that Bitcoin was increasingly behaving like a leveraged technology stock.

That combination, all of the downside and only part of the upside, is the least attractive profile an asset can have. It means Bitcoin has been amplifying the pain of equity selloffs without delivering the diversification that justified holding it, and without matching the gains of the tech names it now mirrors. For a portfolio manager, an asset that adds volatility without adding either diversification or reliable upside is hard to defend, which is part of why some funds have re-labeled Bitcoin from a long-term hedge to a tactical growth position sized like any other speculative bet.

The counter-case: Bitcoin is decoupling, just not how bulls hoped

Here the story turns, because the simple tech-proxy narrative has a serious flaw. If Bitcoin were purely a leveraged Nasdaq, it would have risen when tech rose. Instead, for stretches since the October 2025 peak, Bitcoin fell while the Nasdaq strengthened, a divergence that some analysts said had rarely been so wide. Tech stocks climbed on strong earnings while Bitcoin dropped more than 30% from its high, driven by forces that had nothing to do with corporate profits.

Those forces were crypto-specific. The October 10 flash crash triggered a cascade of leveraged liquidations that hit Bitcoin while barely touching equities. Spot ETF outflows accelerated, pulling out the marginal buyer. The reflexive feedback loop around Bitcoin treasury companies like Strategy, most visibly Strategy, threatened to reverse from a buyer of last resort into a source of supply. And post-halving mining economics added their own pressure through miner selling pressure. None of that is in a Nasdaq chart.

So the honest reading is that Bitcoin is not a clean tech proxy: it takes the downside when tech falls, but it also falls on its own crypto-native shocks when tech rises. That is a worse outcome than pure correlation, but it also means Bitcoin is not simply a technology stock in disguise. The distinction matters for anyone trying to model the asset. A pure tech proxy would at least be predictable, rising and falling with the Nasdaq. What Bitcoin actually did in 2026 was absorb equity-market downside through the ETF-era ownership channel while simultaneously generating its own downside through leverage unwinds, ETF redemptions, treasury-company stress, and miner selling. It behaved less like gold, less like a clean tech stock, and more like a uniquely fragile hybrid during a bad year.

The maturation argument: a third asset class

There is a more optimistic frame that some analysts and long-term holders favor, which is that Bitcoin is becoming its own asset class instead of a copy of gold or tech. On this view, the correlation to equities is a phase driven by who happens to hold the marginal coin today, not a permanent identity. Bitcoin still has properties neither gold nor a tech stock shares: a hard-capped supply that cannot be expanded by decision, no cash flows or earnings to miss, and no management team or governance structure that can fail. Those features do not disappear because a correlation chart spikes.

The behavior of long-term holders supports the maturation read. During the same 2026 window when the ETF complex bled, the supply held by long-term holders moved in the opposite direction, with those flows running far larger in magnitude than ETF flows and skewing toward net accumulation. In other words, the traders treating Bitcoin as a high-beta risk asset were selling through ETFs, while conviction holders who treat it as a long-term store of value were buying. Two different populations, two different theses, playing out in the same asset at the same time.

Which group defines Bitcoin’s identity depends on which one is setting the marginal price, and that can change. Standard Chartered, for its part, has kept multiyear price targets well above current levels even while acknowledging the rotation into AI, framing the moment as a question of timing and competition for capital rather than a verdict on what Bitcoin fundamentally is. The maturation argument does not deny that Bitcoin trades like a risk asset right now. It argues that the current correlation is a snapshot of a particular ownership mix and liquidity regime, not the final word on an asset that is still only in its second decade.

Is this structural or cyclical?

The whole debate reduces to one question: is Bitcoin’s correlation with tech a permanent feature of the ETF era, or a temporary product of the current environment? The case for structural is that the ownership change is not reversing. ETFs are here to stay, institutions will keep managing Bitcoin alongside equities, and as long as they do, the flows that link the two assets will persist. If that is right, the digital gold thesis is effectively dead for as long as this ownership base dominates, and Bitcoin is a growth allocation that happens to be more volatile than most.

The case for cyclical rests on how correlations behave over time. Cross-asset correlations tend to spike during tight-liquidity, risk-off regimes and to loosen when liquidity returns and assets trade more on their own fundamentals. Bitcoin’s correlation with the Nasdaq has swung dramatically before, from deeply negative to strongly positive within weeks, which is not the signature of a fixed relationship. A shift in Federal Reserve policy, a change in the liquidity backdrop, or a rotation of capital away from the crowded AI trade could all loosen the tie and give Bitcoin room to trade on its own narrative again.

Some analysts even argue the correlation has already begun to break, though so far in the unhelpful direction of falling while tech rose. What would restore the digital gold thesis is a period where Bitcoin holds up while equities fall, proving the hedge in the only way that counts. That has not happened in 2026, which is why the thesis is on the ropes. But a single bad year in which a leverage-driven crypto drawdown collided with an AI-fueled equity rally is not a controlled experiment, and reading a permanent identity change off it may be as premature as the original digital gold claim was.

What it means for how to hold Bitcoin

For anyone actually holding Bitcoin, the practical takeaway is to match the thesis to the timeframe. Over the horizon that matters in 2026, Bitcoin has behaved as a high-beta risk asset, so treating it as a crisis hedge or a portfolio insulator has not worked and is not supported by the data. An allocation sized as if Bitcoin will hold up when stocks crash is mis-sized, because this year it fell harder than the stocks it was meant to hedge. The more defensible approach in the current regime is to treat Bitcoin as a volatile growth position, size it to risk tolerance, and watch the Nasdaq and AI-stock sentiment as closely as the crypto charts, because that is where much of the near-term direction is being set.

Over a longer horizon, the store-of-value case does not depend on short-term correlation. The fixed supply, the absence of governance and cash-flow risk, and the accumulation behavior of long-term holders are the pillars of that argument, and they survive a year of trading like a tech stock. The honest conclusion is that Bitcoin is currently being priced as a leveraged expression of risk appetite, not as digital gold, and that this reflects who owns it in the ETF era more than any change in what it is. Whether it grows into the independent, hedge-like asset its supporters imagine, or stays a high-beta satellite of the tech trade, will be settled by the next regime, not this one.

For now, the market has given its answer, and it is not gold. The strongest near-term read is not ideological; it is practical. In a world of a hawkish Fed and tight liquidity, Bitcoin behaves like a risk asset, and risk-off market sentiment matters as much as on-chain conviction. The digital gold thesis is not dead by definition, but in 2026 it has not been the trade.

Frequently asked questions

Is Bitcoin still considered digital gold?

Less and less in practice. Through 2026, Bitcoin behaved like a high-beta risk asset instead of a safe haven, falling alongside technology stocks while gold climbed to record highs. Its correlation with the Nasdaq reached as high as 0.80 while its link to gold fell toward zero. The digital gold label describes Bitcoin’s design and long-term thesis, but its 2026 trading behavior did not match it.

Why does Bitcoin move with tech stocks now?

The main driver is the spot ETF era that began in January 2024. Once institutions could hold Bitcoin inside the same portfolios as technology stocks, managed by the same risk desks, the same capital flows started moving both. When those desks adjust risk exposure, they buy or sell Bitcoin and tech together, which ties Bitcoin to equity market sentiment and Federal Reserve policy the same way growth stocks are.

How correlated is Bitcoin with the Nasdaq?

Correlation varies with the time window, but it has been high in 2026. Rolling 30-day correlations with the Nasdaq 100 reached about 0.80 early in the year, the highest in nearly four years, and the five-year correlation sits near 0.54. Short-term readings against U.S. tech indices have ranged roughly between 0.55 and 0.68. Correlations shift over time and have swung from negative to strongly positive within weeks.

Did the Bitcoin ETFs cause this?

They appear to be the central cause. Research from late 2025 found that spot ETF approval structurally raised Bitcoin’s correlation with the S&P 500, marking a shift from an independent asset to a conventional risk asset. The ETFs legitimized Bitcoin by integrating it into traditional finance, and that same integration tied its price to equity flows and institutional risk management.

What is the bearish skew analysts mention?

It refers to Bitcoin keeping the downside of its tech correlation while losing much of the upside. Trading firm Wintermute described Bitcoin as falling hard when equities fall but failing to rally proportionally when they recover, behaving as a high-beta tail of macro risk. That combination, full downside and partial upside, is a poor profile because it adds volatility without reliable gains or diversification.

Is Bitcoin just a leveraged tech stock then?

Not cleanly. If Bitcoin were purely a leveraged Nasdaq, it would have risen when tech rose, but for stretches in 2026 it fell while tech strengthened, driven by crypto-specific shocks: the October flash crash, ETF outflows, treasury-company stress, and miner selling. So Bitcoin took equity downside while also generating its own downside, which is a fragile hybrid instead of a simple tech proxy.

Could Bitcoin become a hedge again?

It is possible, and it hinges on whether the correlation is structural or cyclical. Cross-asset correlations tend to spike in tight-liquidity, risk-off regimes and loosen when liquidity returns. A shift in Federal Reserve policy or a rotation away from the crowded AI trade could let Bitcoin trade on its own narrative again. Restoring the hedge thesis would require Bitcoin to hold up while equities fall, which has not happened in 2026.

How should investors treat Bitcoin given this?

Match the thesis to the timeframe. In the current regime, Bitcoin trades as a volatile growth asset, so sizing it as a crisis hedge is not supported by the data, and investors may watch the Nasdaq and AI sentiment as closely as crypto charts. Over a longer horizon, the store-of-value case rests on fixed supply, no governance risk, and long-term holder accumulation, which do not depend on short-term correlation.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and correlations between assets change over time and may not persist. Nothing here is a recommendation to buy or sell any asset. Always do your own research and consider consulting a licensed financial professional before making investment decisions. Information is accurate as of July 2, 2026, and may change.

Cross-margining lets your whole account balance backstop every open trade, so a winning position can keep a losing one alive. It is more capital-efficient than isolated margin, and it can also wipe out your entire account in one bad move. Here is how it works.

Summary

- Cross-margining is a margin mode in which all the funds in your account act as shared collateral for all your open positions, so gains and spare equity in one position can support a losing one.

- It contrasts with isolated margin, where a fixed amount of collateral is locked to each position and losses are capped to that amount.

- Cross margin is more capital-efficient and can delay liquidation, but it puts your entire account at risk, because a large enough loss can be covered from the whole balance and trigger a portfolio-wide liquidation.

- Traders generally use cross margin for hedged, offsetting, or core positions, and isolated margin for speculative, high-risk, or single bets where they want a hard loss cap.

- The same principle scales to institutions, where prime brokers cross-margin positions across entire asset classes, using assets like stablecoins as shared collateral.

Cross-margining is a way of managing collateral in leveraged trading where your entire account balance backs all of your open positions at once, instead of each trade standing on its own. In practice, that means the profit or spare equity in one position can be used to support another that is losing, which can keep trades alive through volatility. The trade-off is that your whole account is exposed: a large enough loss draws on the entire balance and can liquidate everything. Cross margin is one of the two main margin modes offered on crypto trading platforms, the other being isolated margin, and understanding the difference is essential to managing risk. This explainer covers how margin trading works, how cross and isolated margin differ, a worked example, the pros and cons, and how the same idea operates at the institutional level.

Margin trading basics: leverage, collateral, liquidation

Cross-margining only makes sense once the basics of margin trading are clear. Margin trading means borrowing funds to open a position larger than your own cash balance would allow. The money you put up is the margin, and it serves as collateral for the borrowed funds. Leverage describes how much larger your position is than your own capital: at five-to-one leverage, a trader controls a position five times the size of their margin. Leverage amplifies everything, so both gains and losses grow in proportion to the position size instead of the smaller amount of capital actually committed.

Two thresholds govern a margin position. The initial margin is the collateral required to open the position. The maintenance margin is the minimum equity that must be kept to hold it open. As long as the position’s equity stays above the maintenance margin, the trade continues. If the market moves against the position enough that equity falls below the maintenance margin, the platform issues a margin call or, more commonly in crypto, moves straight to liquidation.

Liquidation is the forced closure of a position when its equity drops below the maintenance requirement. The platform’s liquidation engine closes the position at market prices, sometimes in partial steps, to prevent the account from going negative. Because leverage magnifies losses, liquidation can happen fast: at high leverage, a small adverse price move can wipe out the margin buffer entirely. This is the central risk of all margin trading, and the choice between cross and isolated margin is fundamentally a choice about how liquidation is calculated and how much of your account is exposed to it.

Cross margin versus isolated margin: the core difference

The two margin modes differ in one crucial respect: what pool of collateral backs each position. In cross margin, all the funds in your account form a single shared pool that backs every open position together. Unrealized profits and spare equity from one position can flow to support another that is drawing down, which can delay or prevent the liquidation of the losing trade. The account is managed as one book, and liquidation becomes a portfolio-level event that depends on the combined equity of everything you hold.

In isolated margin, collateral is ring-fenced to each position individually. You decide how much of your funds to assign to a specific trade, and that amount is the maximum you can lose on it. If the position is liquidated, only its allocated collateral is lost, and the rest of your account, including your other positions, is untouched. Isolated margin gives you a predictable, per-trade liquidation price and a hard cap on the damage any single idea can do, at the cost of not being able to draw on the rest of your balance to save a position.

The consequence is a clear trade-off between capital efficiency and risk containment. Cross margin uses your capital more efficiently, because idle equity and winning positions automatically backstop losing ones, and it tends to produce fewer forced liquidations on individual legs. But it places your entire account on the line, since a bad enough move can consume the whole balance. Isolated margin sacrifices efficiency for control: each position is walled off, so a single blow-up cannot spread, but you must actively manage collateral and accept more frequent single-position liquidations. Neither is inherently better; the right mode depends on the strategy.

A worked example

A concrete example makes the difference tangible. Imagine a trader with a $15,000 account who wants to open a leveraged long position on Bitcoin with an initial margin requirement of $5,000. Under cross margin, the entire $15,000 backs the position, giving a $10,000 buffer above the initial requirement. That large cushion makes liquidation far less likely on a normal pullback, because the whole account absorbs the drawdown. If the trader also holds other positions, profits on those can further support the Bitcoin trade. The catch is that if the combined account equity falls below the maintenance level, the liquidation engine can close positions and consume the full $15,000, not just a slice of it.

Now run the same trade under isolated margin. The trader allocates exactly $5,000 to the Bitcoin position and no more. If Bitcoin falls and the position is liquidated, the maximum loss is that $5,000, and the remaining $10,000 in the account is safe, available for other trades or simply preserved. The liquidation price is predictable and tied only to that position’s collateral. The downside is that the position has a much thinner buffer, so it will be liquidated sooner than the cross-margined version, since it cannot draw on the rest of the account to survive a dip.

The example shows the core tension. Cross margin gave the Bitcoin trade a bigger cushion and a better chance of surviving volatility, but it risked the entire $15,000. Isolated margin capped the loss at $5,000 but liquidated the position more readily. A trader who is confident and wants staying power, and who is comfortable risking the whole account, leans cross. A trader who wants a firm loss limit on a specific, uncertain bet leans isolated. The same $15,000 produces very different risk profiles depending on the mode chosen.

The pros and cons of cross-margining

Cross-margining has real advantages that explain its popularity among active and professional traders. Its main strength is capital efficiency: because all equity backs all positions, none of your capital sits idle behind a single trade, and winning positions automatically support losing ones. This produces a smoother equity curve and fewer forced exits on individual legs, which is especially valuable for hedged or offsetting strategies where one position is meant to counterbalance another. It is also simpler to monitor in one sense, since you watch a single account-level margin level instead of tracking collateral on many separate positions.

The disadvantages are equally real and more dangerous if ignored. The defining risk is that your entire account is exposed: once combined equity falls below the maintenance margin, liquidation can consume the whole balance, not a contained portion. This becomes acute when positions are correlated, which is common in crypto, where many assets move together. In a sharp, broad sell-off, several cross-margined positions can lose at once, draining account equity rapidly and triggering a cascade of liquidations across the book. A single violent move can therefore wipe out everything, where isolated margin would have contained the damage.

Cross margin also carries a psychological hazard. Because the shared pool makes positions feel more resilient, it can tempt traders to over-leverage, opening larger positions than they should because the buffer looks generous. That temptation, combined with the whole-account exposure, is how traders turn a manageable loss into a total one. The mode rewards discipline and punishes its absence. Used carefully within a hedged framework, cross margin is efficient and forgiving of ordinary volatility; used carelessly with correlated, over-leveraged bets, it is the fastest route to a blown-up account.

When to use cross versus isolated

The choice between the modes should follow the strategy rather than habit. Cross margin fits situations where positions offset or support one another. Hedging programs, basis trades, pairs trades, and market-making all benefit from a shared collateral pool, because a gain on one leg naturally cushions a loss on another, and pooling the collateral reduces the chance of an unnecessary single-leg liquidation. Core positions that a trader intends to hold through volatility also suit cross margin, since the deeper buffer provides staying power. In these cases, the whole-account exposure is an acceptable trade for the efficiency and resilience gained.

Isolated margin fits the opposite situations. Speculative, event-driven, or high-volatility bets, and single-ticket trades where the outcome is uncertain, are better ring-fenced, so that if the idea fails it cannot damage the rest of the account. A trader taking a focused shot on a volatile small-cap token, for instance, can cap the loss at a fixed amount and sleep easily knowing the rest of the balance is safe. Isolated margin also suits newer traders building discipline, because it enforces a hard maximum loss per trade and makes the risk of each position explicit.

Many experienced traders combine both in a core-satellite structure. They run cross margin on a core book of hedged or offsetting positions that benefit from pooled equity, while keeping speculative satellite trades in isolated buckets with fixed loss caps. This keeps the core capital-efficient without letting a single high-risk bet sink the whole account. The practical rule is to match the mode to the intent of each trade: shared exposure for positions designed to work together, walled-off exposure for standalone bets you want to contain. Some platforms even offer a smart cross margin that nets opposite-direction positions across products, further improving efficiency for hedged books.

Cross-margining at the institutional level

The same principle that governs a retail trader’s account scales all the way up to the largest institutions, and it is worth seeing the connection. When a hedge fund or trading firm operates through a prime broker, the broker cross-margins the firm’s positions across entire asset classes, netting exposures in digital assets, foreign exchange, derivatives, and fixed income so the firm posts collateral against the combined risk of its whole book rather than each position separately. This is cross-margining as a foundation of professional trading, and it is a major reason institutions value prime brokers: it frees up enormous amounts of capital that would otherwise sit idle.

Crypto has begun importing this institutional version. Prime brokers serving digital assets now let clients cross-margin crypto positions against traditional exposures, and stablecoins have started to play the role of shared collateral in that system. Ripple’s RLUSD, for example, has been positioned as a stablecoin that enables cross-margining between digital assets and traditional markets through institutional prime brokerage, letting a firm post the token as collateral recognized across both worlds. That is the same idea a retail trader meets in a cross-margin account, applied at the scale of institutional portfolios spanning many markets.

Seeing the two levels together clarifies what cross-margining really is: a method for treating a collection of positions as a single risk pool to use capital more efficiently. For a retail trader, the pool is the account balance backing a handful of trades. For an institution, it is a multi-asset book backed by cash and collateral like stablecoins across a prime broker. The mechanics and the stakes differ by orders of magnitude, but the core logic, and the core trade-off between efficiency and concentrated risk is identical.

The risks you must respect

Whatever the level, cross-margining demands respect for a specific set of risks, and ignoring them is how accounts are lost. The first is correlation risk. Crypto assets frequently move together, so a broad sell-off can push multiple cross-margined positions into loss simultaneously, draining shared equity far faster than a single position would. The very diversification that looks like safety can become a synchronized drawdown when markets turn risk-off together, and the shared pool that was meant to cushion individual losses instead absorbs many at once.

The second is liquidation and leverage risk. Because cross margin can make positions feel durable, it invites higher leverage, and higher leverage means a smaller adverse move can breach the maintenance margin. When that happens in cross mode, the liquidation is a portfolio-level event that can close multiple positions and consume the whole account. Flash crashes and liquidation cascades, where forced selling drives prices lower and triggers still more liquidations, are especially dangerous, and thin order books during such events can cause execution at prices far worse than expected. The market has seen sharp, leverage-driven cascades wipe out over-extended traders in minutes.

The disciplined response is to size positions conservatively, avoid over-leverage, and match the margin mode to the trade. Use cross margin for genuinely hedged or core positions where offsetting exposure justifies the shared pool, and isolate speculative or high-beta bets so a single failure cannot spread. Set alerts and plan collateral top-ups in advance instead of reacting during a crash. Cross-margining is a powerful tool for capital efficiency, but it concentrates risk at the account level, and the traders who use it well are the ones who never forget that the whole balance is on the line.

Frequently Asked Questions

What is cross-margining in simple terms?

Cross-margining is a margin mode where all the funds in your trading account act as shared collateral for all your open positions at once. Profits and spare equity from one position can support another that is losing, which can delay liquidation. The trade-off is that your entire account is exposed, so a large enough loss can be covered from the whole balance and liquidate everything.

How is cross margin different from isolated margin?

In cross margin, your whole account balance backs every position, so gains on one can cushion losses on another, but your entire account is at risk. In isolated margin, a fixed amount of collateral is locked to each position, capping the loss on that trade to the allocated amount and protecting the rest of your account. Cross is more efficient; isolated is more contained.

Which is better, cross or isolated margin?

Neither is universally better; it depends on the trade. Cross margin suits hedged, offsetting, or core positions that benefit from a shared collateral pool and staying power. Isolated margin suits speculative, event-driven, or single high-risk bets where you want a hard loss cap. Many traders use both, running cross margin on a core book and isolating speculative satellite trades.

What is the main risk of cross-margining?

The main risk is that your entire account is exposed. Once combined equity falls below the maintenance margin, liquidation can consume the whole balance rather than a contained amount. This is especially dangerous with correlated crypto assets, where a broad sell-off can push several positions into loss at once, draining shared equity quickly and triggering a portfolio-wide liquidation.

Can cross-margining cause bigger losses?

It can, because it puts the full account balance behind your positions. In a sharp, correlated downturn or a flash crash, multiple cross-margined positions can lose simultaneously and a portfolio-level liquidation can wipe out the entire account. Cross margin can also tempt traders to over-leverage because the shared buffer feels generous, which magnifies losses when the market turns.

What is a maintenance margin?

The maintenance margin is the minimum equity you must keep to hold a leveraged position open. As long as equity stays above it, the position continues. If the market moves against you and equity falls below the maintenance margin, the platform liquidates the position. In cross margin, this is calculated at the account level; in isolated margin, it is calculated for each position separately.

Do institutions use cross-margining?

Yes, at large scale. When institutions trade through a prime broker, the broker cross-margins their positions across entire asset classes, netting exposures in digital assets, foreign exchange, derivatives, and fixed income so the firm posts collateral against the combined risk of its whole book. Stablecoins such as RLUSD have started to serve as shared collateral in this institutional cross-margining system.

How can I use cross-margining safely?

Match the mode to the trade: use cross margin for hedged or core positions where offsetting exposure justifies the shared pool, and isolate speculative or high-volatility bets. Size positions conservatively, avoid over-leverage, set liquidation alerts, and plan collateral top-ups in advance. Always remember that in cross mode, your entire account is on the line, so discipline about leverage and position size is essential.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or trading advice. Margin trading involves a high risk of loss, including the potential loss of your entire account, and is not suitable for all investors. Nothing here is a recommendation to trade or use any strategy. Always do your own research and consider consulting a qualified professional before trading on margin. Information is accurate as of July 2, 2026, and may change.

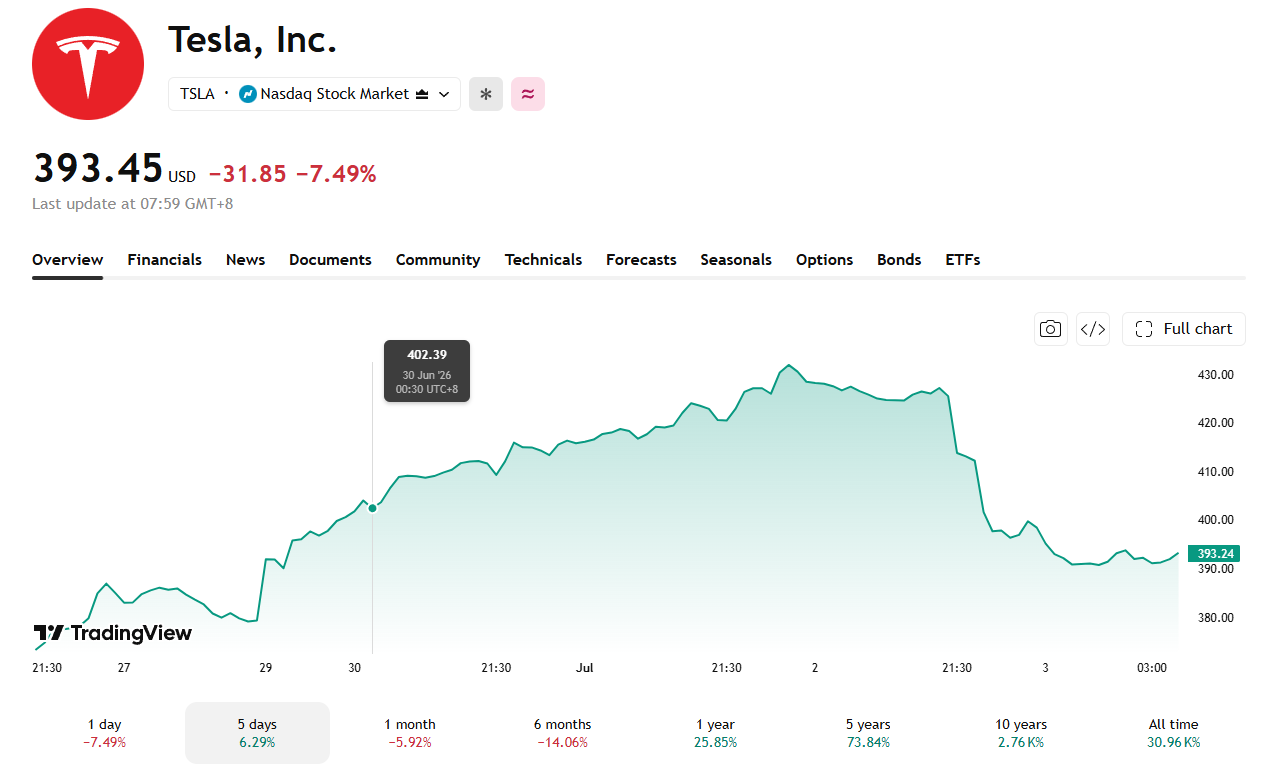

Tesla shares sank about 7.5% on July 2, their worst single-day decline in nearly a year. The drop came even after the company reported second-quarter deliveries far above Wall Street’s expectations.

The selloff came just three trading days after Tesla stock jumped more than 8% on optimism around a new self-driving software rollout.

Deliveries Crushed Estimates, But the Rally Came Early